Embed Size (px)

DESCRIPTION

Citation preview

From wage suppression to

jobs crisis:Our alternatives

Özlem Onaran

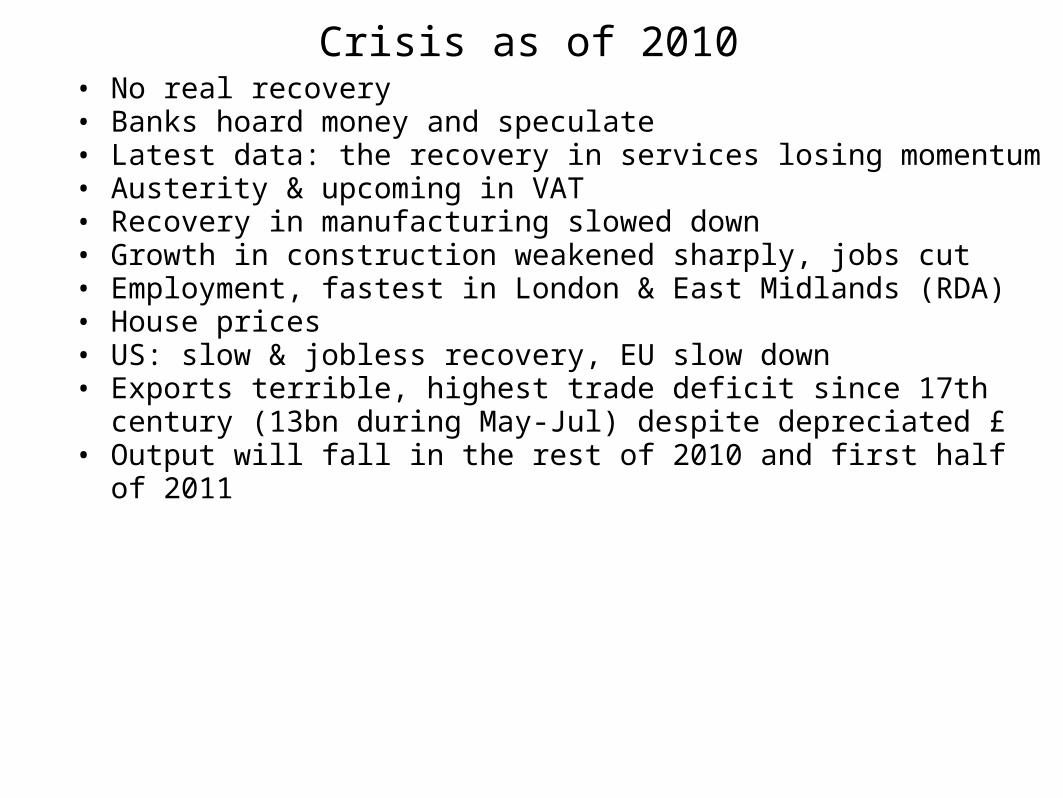

Crisis as of 2010• No real recovery• Banks hoard money and speculate • Latest data: the recovery in services losing momentum• Austerity & upcoming in VAT• Recovery in manufacturing slowed down• Growth in construction weakened sharply, jobs cut• Employment, fastest in London & East Midlands (RDA)• House prices • US: slow & jobless recovery, EU slow down• Exports terrible, highest trade deficit since 17th century (13bn during

May-Jul) despite depreciated £• Output will fall in the rest of 2010 and first half of 2011

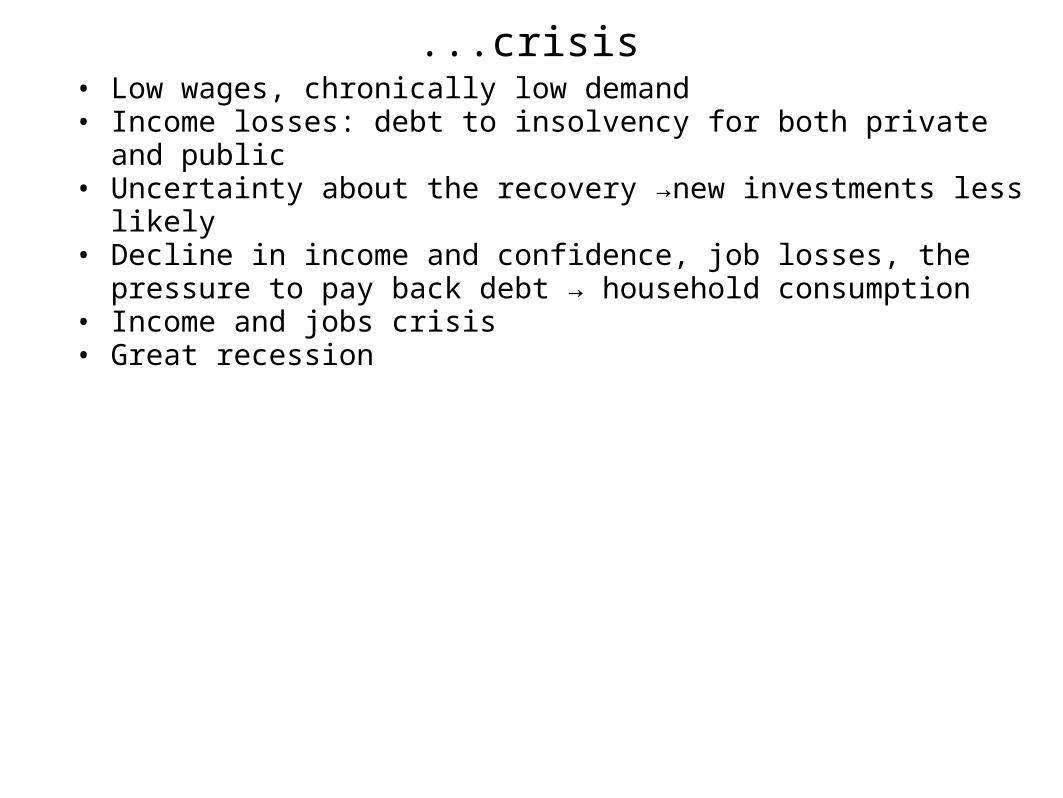

...crisis• Low wages, chronically low demand• Income losses: debt to insolvency for both private and public • Uncertainty about the recovery →new investments less likely • Decline in income and confidence, job losses, the pressure to pay back

debt → household consumption• Income and jobs crisis• Great recession

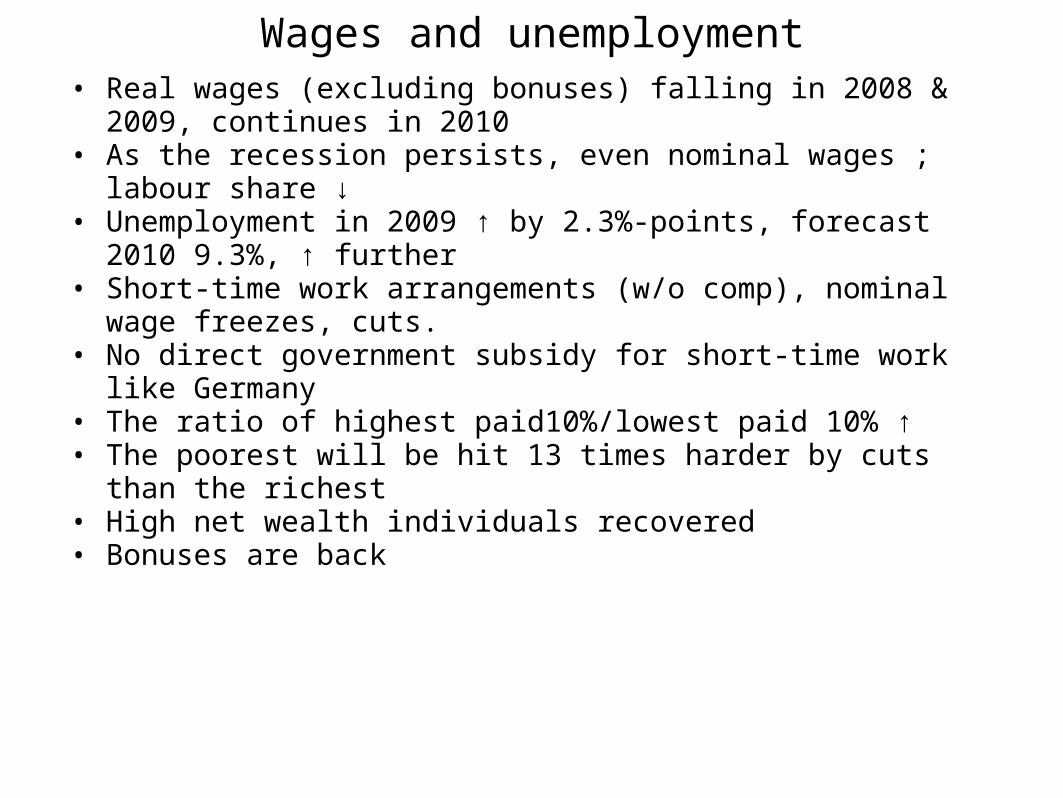

Wages and unemployment• Real wages (excluding bonuses) falling in 2008 & 2009, continues

in 2010• As the recession persists, even nominal wages ; labour share ↓ • Unemployment in 2009 ↑ by 2.3%-points, forecast 2010 9.3%, ↑

further• Short-time work arrangements (w/o comp), nominal wage freezes,

cuts. • No direct government subsidy for short-time work like Germany• The ratio of highest paid10%/lowest paid 10% ↑• The poorest will be hit 13 times harder by cuts than the richest• High net wealth individuals recovered• Bonuses are back

Company strategy

• Gender wage gap widening• Firms: a strategy of increasing productivity (work intensity,

exploitation), start a new wave of firing, engage in hiring freezes, increase the working hours

• Worse job chances of the unemployed and the first time job seekers. • an increase in long term unemployment & discouraged workers likely• structural problems in construction, finance; cuts in public sec jobs: • skill & regional mismatch

• Their crisis not ours

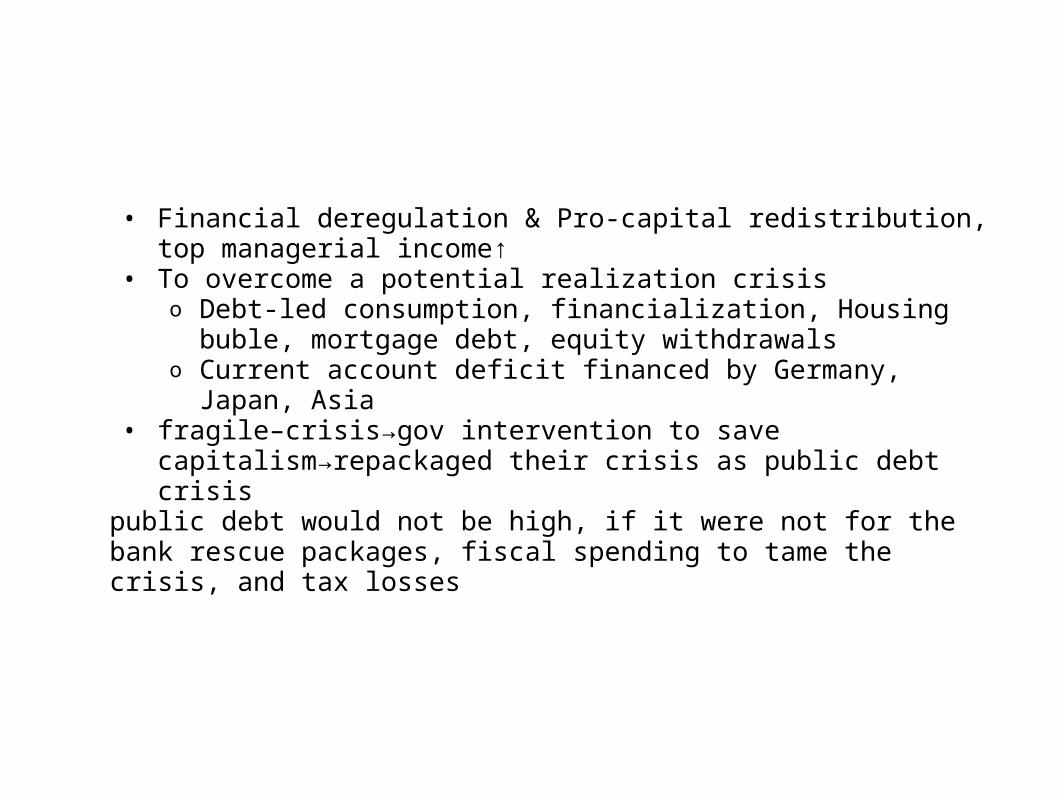

• Financial deregulation & Pro-capital redistribution, top managerial income↑

• To overcome a potential realization crisiso Debt-led consumption, financialization, Housing buble,

mortgage debt, equity withdrawalso Current account deficit financed by Germany, Japan,

Asia• fragile–crisis→gov intervention to save

capitalism→repackaged their crisis as public debt crisis• public debt would not be high, if it were not for the bank

rescue packages, fiscal spending to tame the crisis, and tax losses

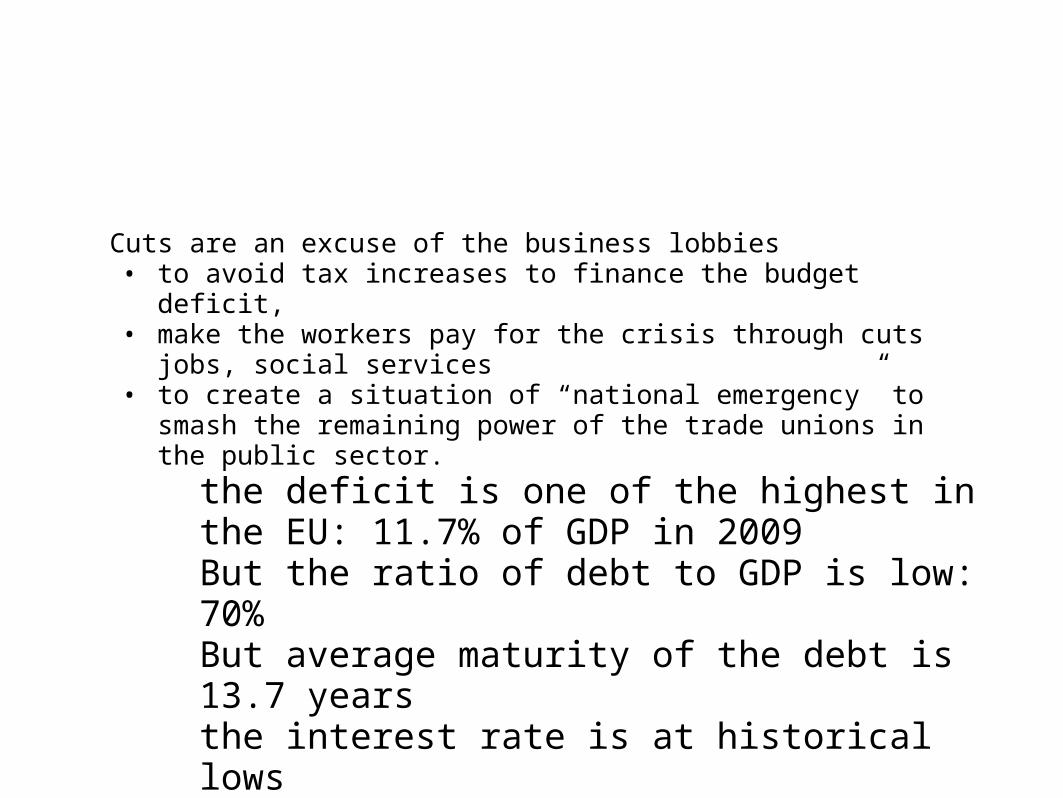

• Cuts are an excuse of the business lobbies too to avoid tax increases to finance the budget deficit, o make the workers pay for the crisis through cuts jobs,

social services, o to create a situation of “national emergency” to smash

the remaining power of the trade unions in the public sector. the deficit is one of the highest in the EU: 11.7% of

GDP in 2009 But the ratio of debt to GDP is low: 70% But average maturity of the debt is 13.7 years the interest rate is at historical lows Imf-ilo warnings, martin Wolf: gamble

• We won‘t pay for your crisis! make the responsible pay for the costs of crisis

• Financial deregulation & Pro-capital redistribution, top managerial income↑

• To overcome a potential realization crisiso Debt-led consumption, financialization, Housing buble, mortgage

debt, equity withdrawalso Current account deficit financed by Germany, Japan, Asia

• fragile–crisis→gov intervention to save capitalism→repackaged their crisis as public debt crisis

public debt would not be high, if it were not for the bank rescue packages, fiscal spending to tame the crisis, and tax losses

Cuts are an excuse of the business lobbies • to avoid tax increases to finance the budget deficit,• make the workers pay for the crisis through cuts jobs, social services• to create a situation of “national emergency” to smash the remaining

power of the trade unions in the public sector.

the deficit is one of the highest in the EU: 11.7% of GDP in 2009

But the ratio of debt to GDP is low: 70% But average maturity of the debt is 13.7 years the interest rate is at historical lows Imf-ilo warnings, martin Wolf: gamble

• We won‘t pay for your crisis! make the responsible pay for the costs of crisis

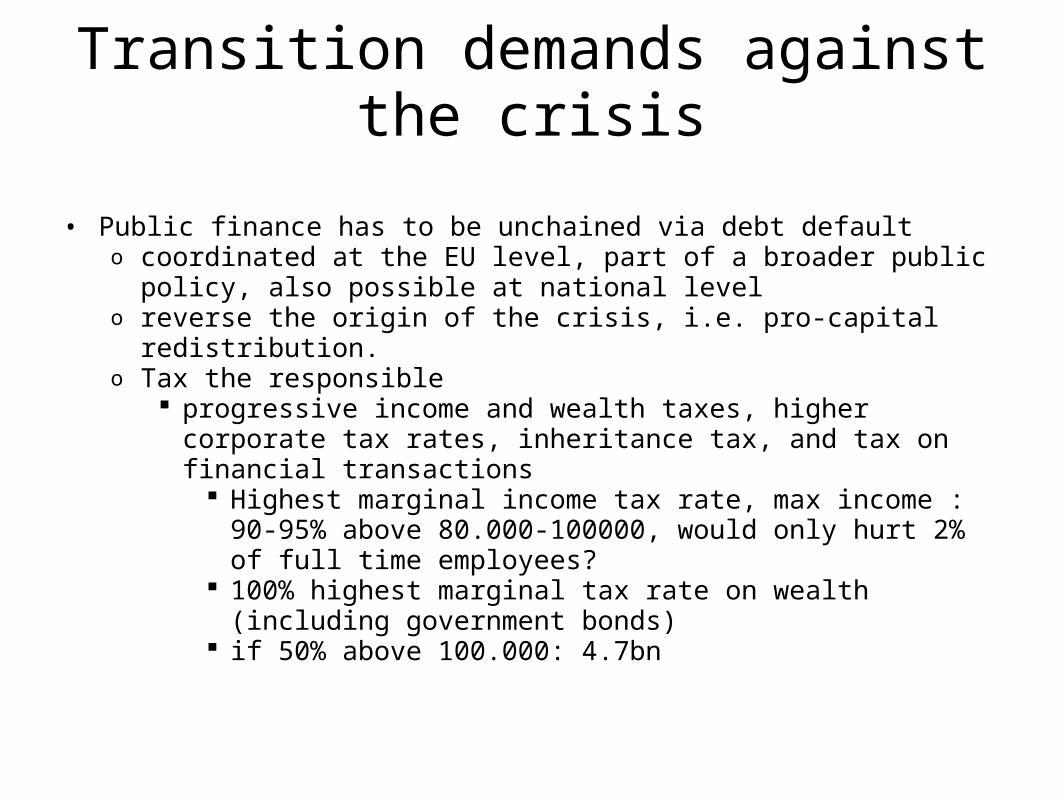

Transition demands against the crisis

• Public finance has to be unchained via debt default o coordinated at the EU level, part of a broader public policy, also possible

at national level o reverse the origin of the crisis, i.e. pro-capital redistribution.o Tax the responsible

progressive income and wealth taxes, higher corporate tax rates, inheritance tax, and tax on financial transactions

Highest marginal income tax rate, max income : 90-95% above 80.000-100000, would only hurt 2% of full time employees?

100% highest marginal tax rate on wealth (including government bonds)

if 50% above 100.000: 4.7bn

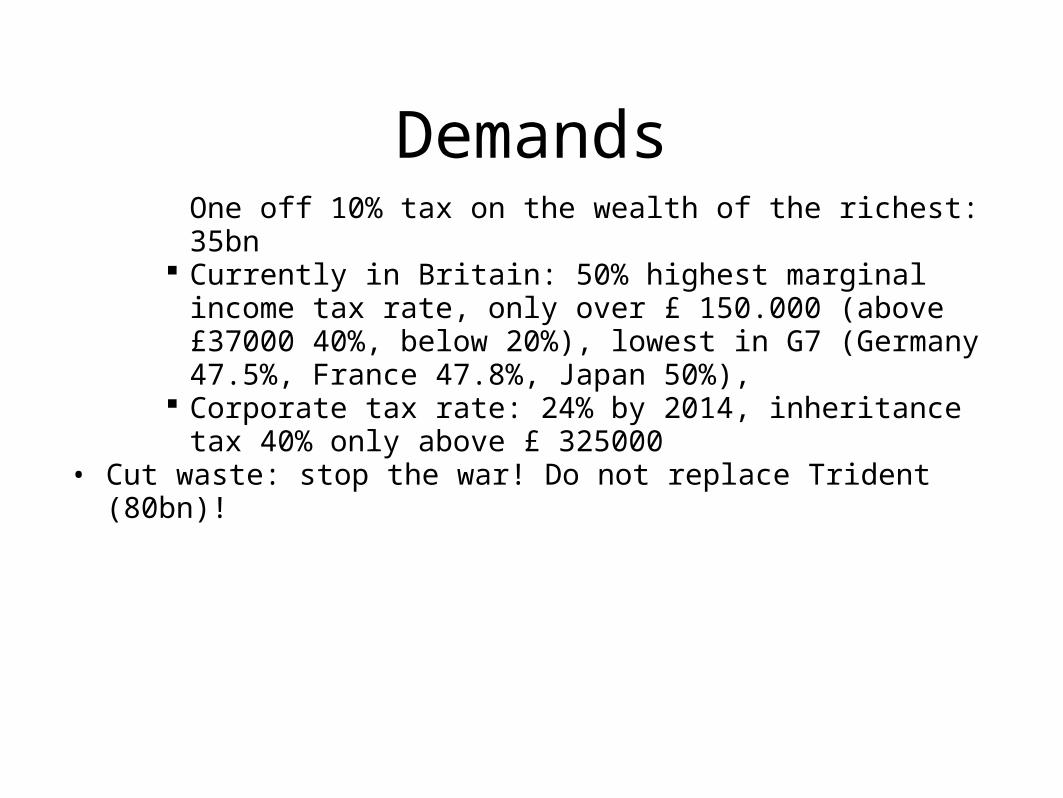

Demands One off 10% tax on the wealth of the richest: 35bn Currently in Britain: 50% highest marginal income tax rate,

only over £ 150.000 (above £37000 40%, below 20%), lowest in G7 (Germany 47.5%, France 47.8%, Japan 50%),

Corporate tax rate: 24% by 2014, inheritance tax 40% only above £ 325000

• Cut waste: stop the war! Do not replace Trident (80bn)!

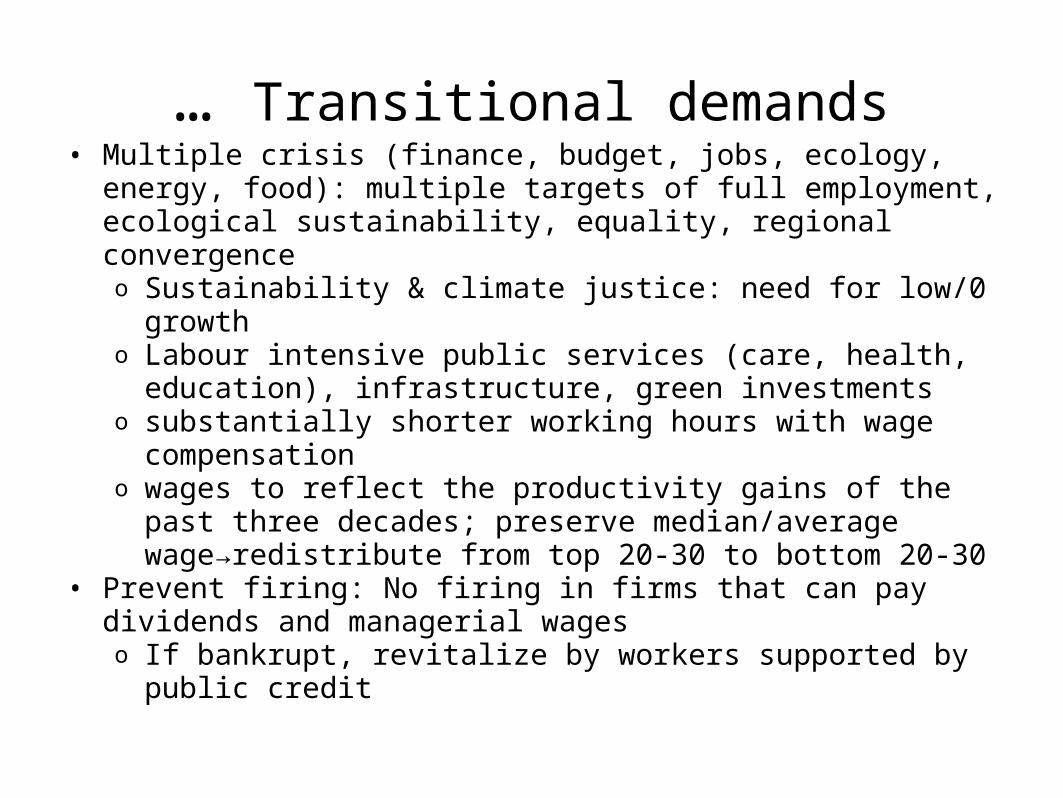

… Transitional demands• Multiple crisis (finance, budget, jobs, ecology, energy, food): multiple

targets of full employment, ecological sustainability, equality, regional convergenceo Sustainability & climate justice: need for low/0 growtho Labour intensive public services (care, health, education),

infrastructure, green investmentso substantially shorter working hours with wage compensation o wages to reflect the productivity gains of the past three decades;

preserve median/average wage→redistribute from top 20-30 to bottom 20-30

• Prevent firing: No firing in firms that can pay dividends and managerial wageso If bankrupt, revitalize by workers supported by public credit

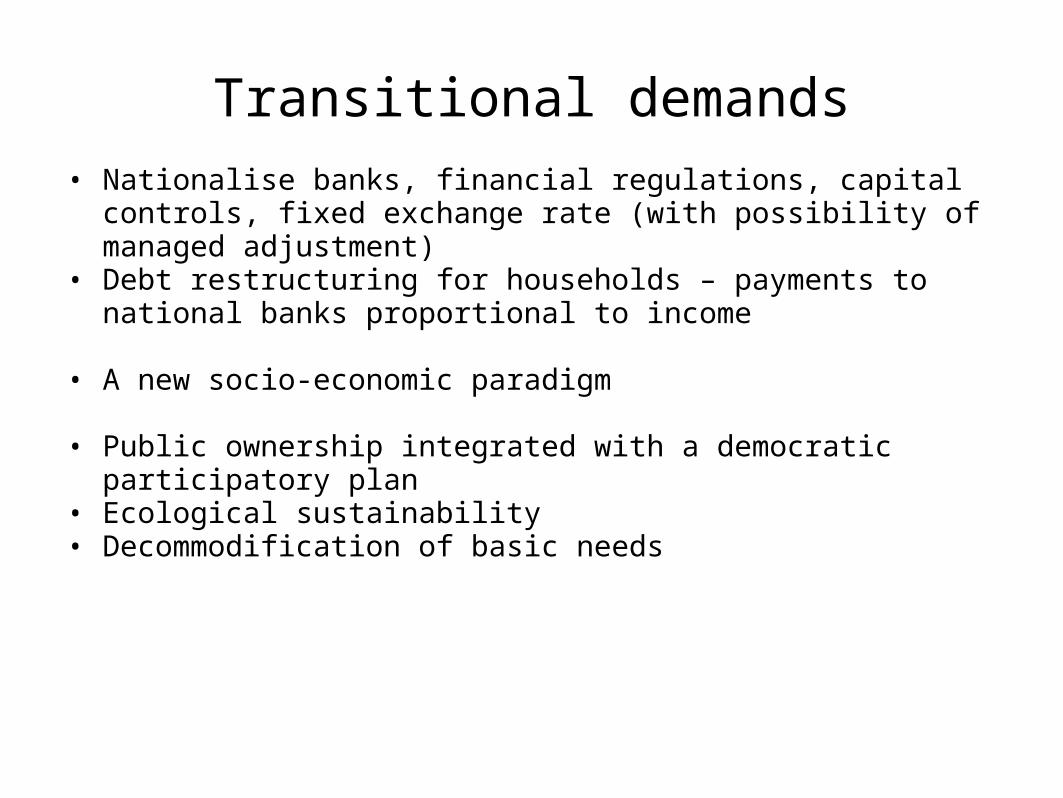

Transitional demands• Nationalise banks, financial regulations, capital controls, fixed

exchange rate (with possibility of managed adjustment)• Debt restructuring for households – payments to national banks

proportional to income

• A new socio-economic paradigm

• Public ownership integrated with a democratic participatory plan• Ecological sustainability• Decommodification of basic needs