Embed Size (px)

Citation preview

Global Webinar:Inverted & Negative Yield Curves, Trade Tensions & More

Jim O’Sullivan & Carl WeinbergHigh Frequency Economics www.hifreqecon.com/WebinarSep2019

U.S. Expansion Don’t Die Of Old Age ...Or From Trade Tensions?

Jim O’SullivanChief Economist www.hifreqecon.com/WebinarSep2019

High Frequency Economics® — Jim O’Sullivan, Chief Economist September 11, 2019 Page 3

© 2019 High Frequency Economics, Ltd. 445 Hamilton Avenue, White Plains, NY 10601. All rights reserved. No secondary distribution without express permission. www.hifreqecon.com/WebinarSep2019

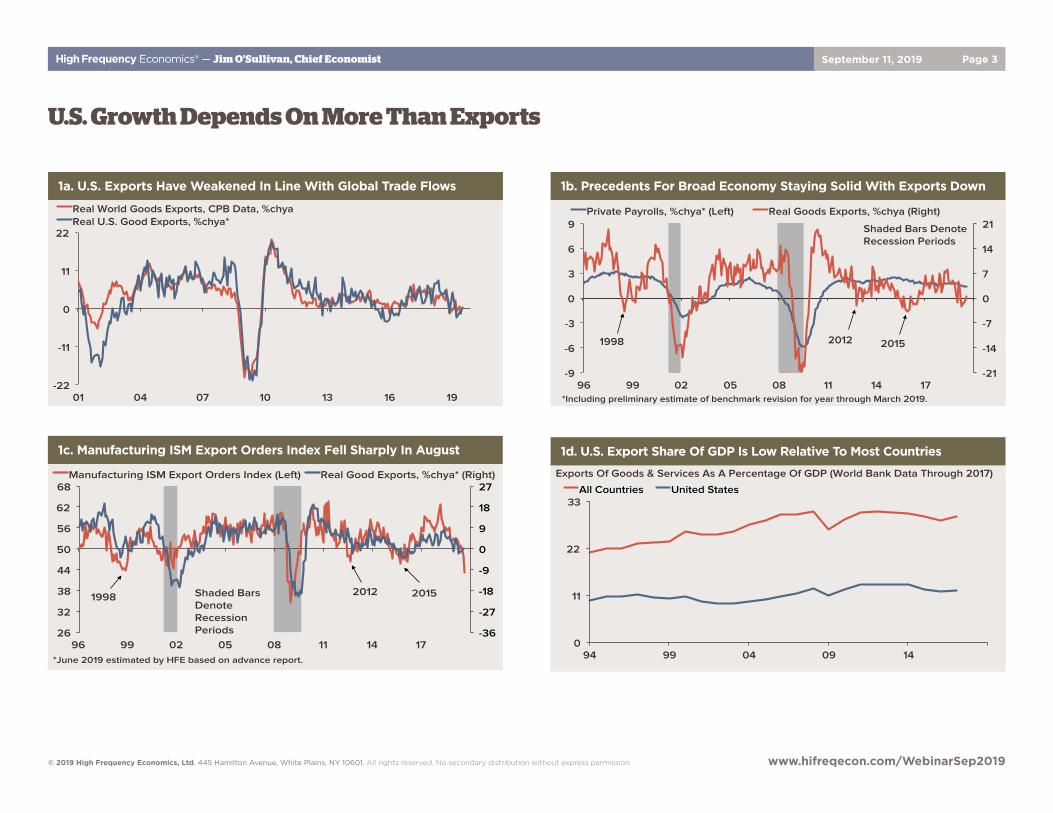

U.S. Growth Depends On More Than Exports

0

11

22

33

94 99 04 09 14

All Countries United States

Exports Of Goods & Services As A Percentage Of GDP (World Bank Data Through 2017)

1d. U.S. Export Share Of GDP Is Low Relative To Most Countries

-22

-11

0

11

22

01 04 07 10 13 16 19

Real World Goods Exports, CPB Data, %chya Real U.S. Good Exports, %chya*

1a. U.S. Exports Have Weakened In Line With Global Trade Flows

-36

-27

-18

-9

0

9

18

27

26

32

38

44

50

56

62

68

96 99 02 05 08 11 14 17

Manufacturing ISM Export Orders Index (Left) Real Good Exports, %chya* (Right)

Shaded Bars Denote Recession Periods

2015 2012 1998

*June 2019 estimated by HFE based on advance report.

1c. Manufacturing ISM Export Orders Index Fell Sharply In August

-21

-14

-7

0

7

14

21

-9

-6

-3

0

3

6

9

96 99 02 05 08 11 14 17

Private Payrolls, %chya* (Left) Real Goods Exports, %chya (Right)

Shaded Bars Denote Recession Periods

1998 2015 2012

*Including preliminary estimate of benchmark revision for year through March 2019.

1b. Precedents For Broad Economy Staying Solid With Exports Down

High Frequency Economics® — Jim O’Sullivan, Chief Economist September 11, 2019 Page 4

© 2019 High Frequency Economics, Ltd. 445 Hamilton Avenue, White Plains, NY 10601. All rights reserved. No secondary distribution without express permission. www.hifreqecon.com/WebinarSep2019

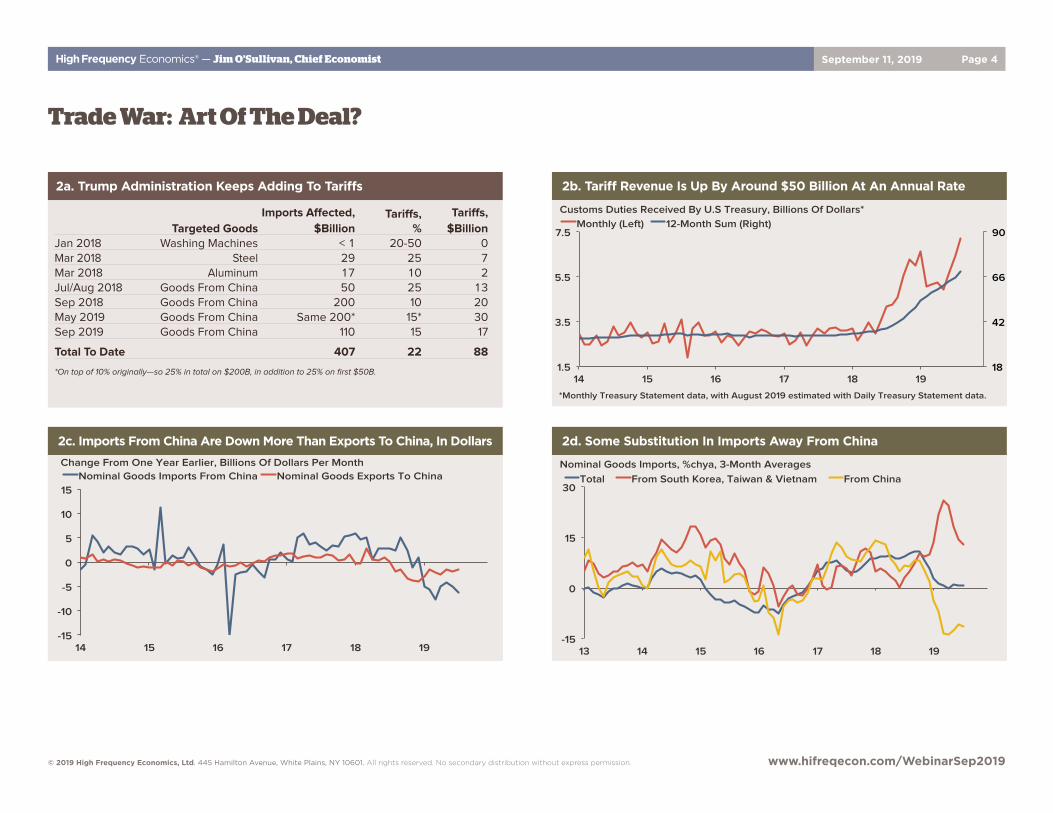

Trade War: Art Of The Deal?

-15

0

15

30

13 14 15 16 17 18 19

Total From South Korea, Taiwan & Vietnam From China Nominal Goods Imports, %chya, 3-Month Averages

2d. Some Substitution In Imports Away From China

-15

-10

-5

0

5

10

15

14 15 16 17 18 19

Nominal Goods Imports From China Nominal Goods Exports To China Change From One Year Earlier, Billions Of Dollars Per Month

2c. Imports From China Are Down More Than Exports To China, In Dollars

2a. Trump Administration Keeps Adding To Tariffs

Targeted GoodsImports Affected,

$BillionTariffs,

%Tariffs,

$BillionJan 2018 Washing Machines < 1 20-50 0Mar 2018 Steel 29 25 7Mar 2018 Aluminum 17 10 2Jul/Aug 2018 Goods From China 50 25 13Sep 2018 Goods From China 200 10 20May 2019 Goods From China Same 200* 15* 30Sep 2019 Goods From China 110 15 17

Total To Date 407 22 88

*On top of 10% originally—so 25% in total on $200B, in addition to 25% on first $50B. 18

42

66

90

1.5

3.5

5.5

7.5

14 15 16 17 18 19

Monthly (Left) 12-Month Sum (Right) Customs Duties Received By U.S Treasury, Billions Of Dollars*

*Monthly Treasury Statement data, with August 2019 estimated with Daily Treasury Statement data.

2b. Tariff Revenue Is Up By Around $50 Billion At An Annual Rate

High Frequency Economics® — Jim O’Sullivan, Chief Economist September 11, 2019 Page 5

© 2019 High Frequency Economics, Ltd. 445 Hamilton Avenue, White Plains, NY 10601. All rights reserved. No secondary distribution without express permission. www.hifreqecon.com/WebinarSep2019

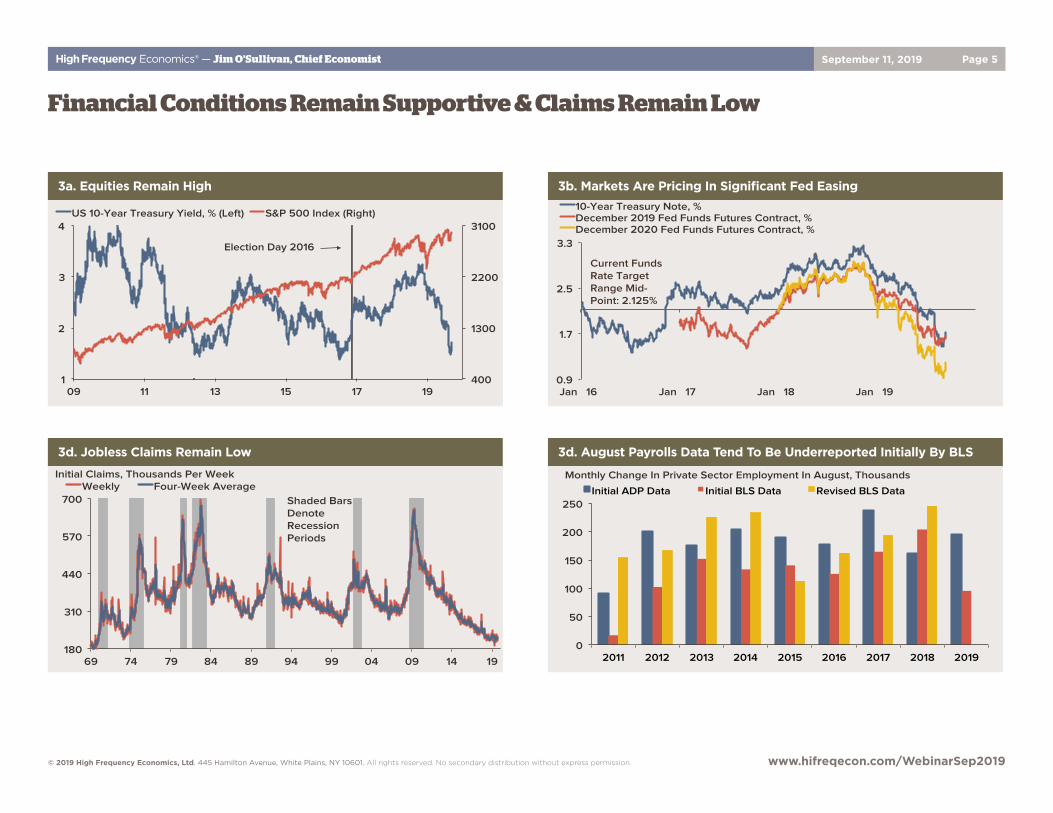

Financial Conditions Remain Supportive & Claims Remain Low

400

1300

2200

3100

1

2

3

4

09 11 13 15 17 19

US 10-Year Treasury Yield, % (Left) S&P 500 Index (Right)

Election Day 2016

3a. Equities Remain High

0.9

1.7

2.5

3.3

Jan 16 Jan 17 Jan 18 Jan 19

10-Year Treasury Note, % December 2019 Fed Funds Futures Contract, % December 2020 Fed Funds Futures Contract, %

Current Funds Rate Target Range Mid-Point: 2.125%

3b. Markets Are Pricing In Significant Fed Easing

180

310

440

570

700

69 74 79 84 89 94 99 04 09 14 19

Weekly Four-Week Average Shaded Bars Denote Recession Periods

Initial Claims, Thousands Per Week

3d. Jobless Claims Remain Low

2011 2012 2013 2014 2015 2016 2017 2018 2019 0

50

100

150

200

250 Initial ADP Data Initial BLS Data Revised BLS Data

Monthly Change In Private Sector Employment In August, Thousands

3d. August Payrolls Data Tend To Be Underreported Initially By BLS

High Frequency Economics® — Jim O’Sullivan, Chief Economist September 11, 2019 Page 6

© 2019 High Frequency Economics, Ltd. 445 Hamilton Avenue, White Plains, NY 10601. All rights reserved. No secondary distribution without express permission. www.hifreqecon.com/WebinarSep2019

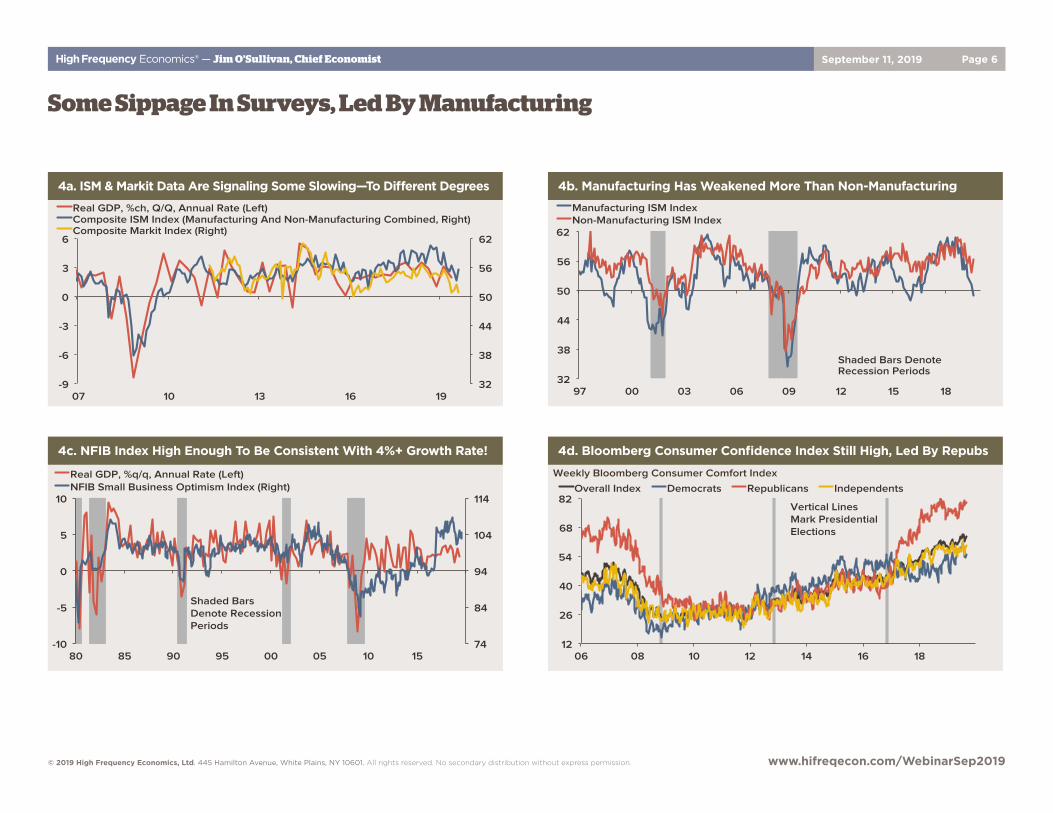

Some Sippage In Surveys, Led By Manufacturing

74

84

94

104

114

-10

-5

0

5

10

80 85 90 95 00 05 10 15

Real GDP, %q/q, Annual Rate (Left) NFIB Small Business Optimism Index (Right)

Shaded Bars Denote Recession Periods

4c. NFIB Index High Enough To Be Consistent With 4%+ Growth Rate!

32

38

44

50

56

62

-9

-6

-3

0

3

6

07 10 13 16 19

Real GDP, %ch, Q/Q, Annual Rate (Left) Composite ISM Index (Manufacturing And Non-Manufacturing Combined, Right) Composite Markit Index (Right)

4a. ISM & Markit Data Are Signaling Some Slowing—To Different Degrees

32

38

44

50

56

62

97 00 03 06 09 12 15 18

Manufacturing ISM Index Non-Manufacturing ISM Index

Shaded Bars Denote Recession Periods

4b. Manufacturing Has Weakened More Than Non-Manufacturing

12

26

40

54

68

82

06 08 10 12 14 16 18

Overall Index Democrats Republicans Independents

Vertical Lines Mark Presidential Elections

Weekly Bloomberg Consumer Comfort Index

4d. Bloomberg Consumer Confidence Index Still High, Led By Repubs

High Frequency Economics® — Jim O’Sullivan, Chief Economist September 11, 2019 Page 7

© 2019 High Frequency Economics, Ltd. 445 Hamilton Avenue, White Plains, NY 10601. All rights reserved. No secondary distribution without express permission. www.hifreqecon.com/WebinarSep2019

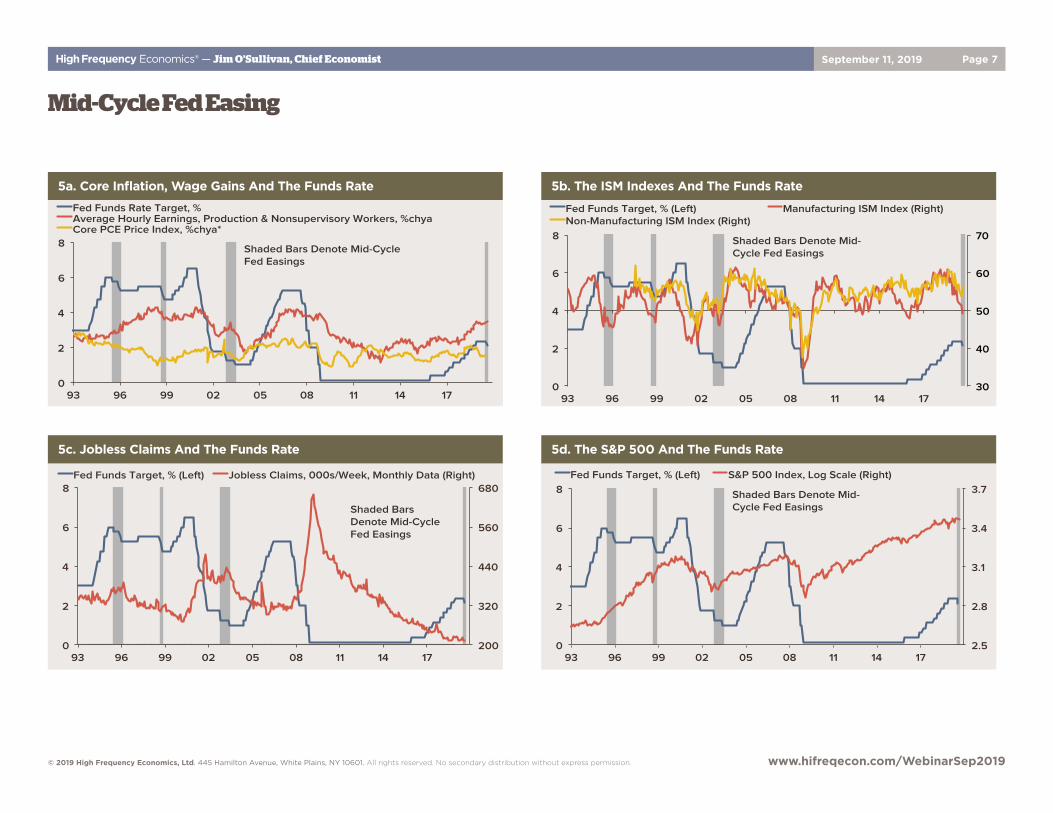

Mid-Cycle Fed Easing

2.5

2.8

3.1

3.4

3.7

0

2

4

6

8

93 96 99 02 05 08 11 14 17

Fed Funds Target, % (Left) S&P 500 Index, Log Scale (Right)

Shaded Bars Denote Mid-Cycle Fed Easings

5d. The S&P 500 And The Funds Rate

200

320

440

560

680

0

2

4

6

8

93 96 99 02 05 08 11 14 17

Fed Funds Target, % (Left) Jobless Claims, 000s/Week, Monthly Data (Right)

Shaded Bars Denote Mid-Cycle Fed Easings

5c. Jobless Claims And The Funds Rate

30

40

50

60

70

0

2

4

6

8

93 96 99 02 05 08 11 14 17

Fed Funds Target, % (Left) Manufacturing ISM Index (Right) Non-Manufacturing ISM Index (Right)

Shaded Bars Denote Mid-Cycle Fed Easings

5b. The ISM Indexes And The Funds Rate

0

2

4

6

8

93 96 99 02 05 08 11 14 17

Fed Funds Rate Target, % Average Hourly Earnings, Production & Nonsupervisory Workers, %chya Core PCE Price Index, %chya*

Shaded Bars Denote Mid-Cycle Fed Easings

5a. Core Inflation, Wage Gains And The Funds Rate

High Frequency Economics® — Jim O’Sullivan, Chief Economist September 11, 2019 Page 8

© 2019 High Frequency Economics, Ltd. 445 Hamilton Avenue, White Plains, NY 10601. All rights reserved. No secondary distribution without express permission. www.hifreqecon.com/WebinarSep2019

-12

-9

-6

-3

0

3

6

9

-8

-6

-4

-2

0

2

4

6

60 65 70 75 80 85 90 95 00 05 10 15 20

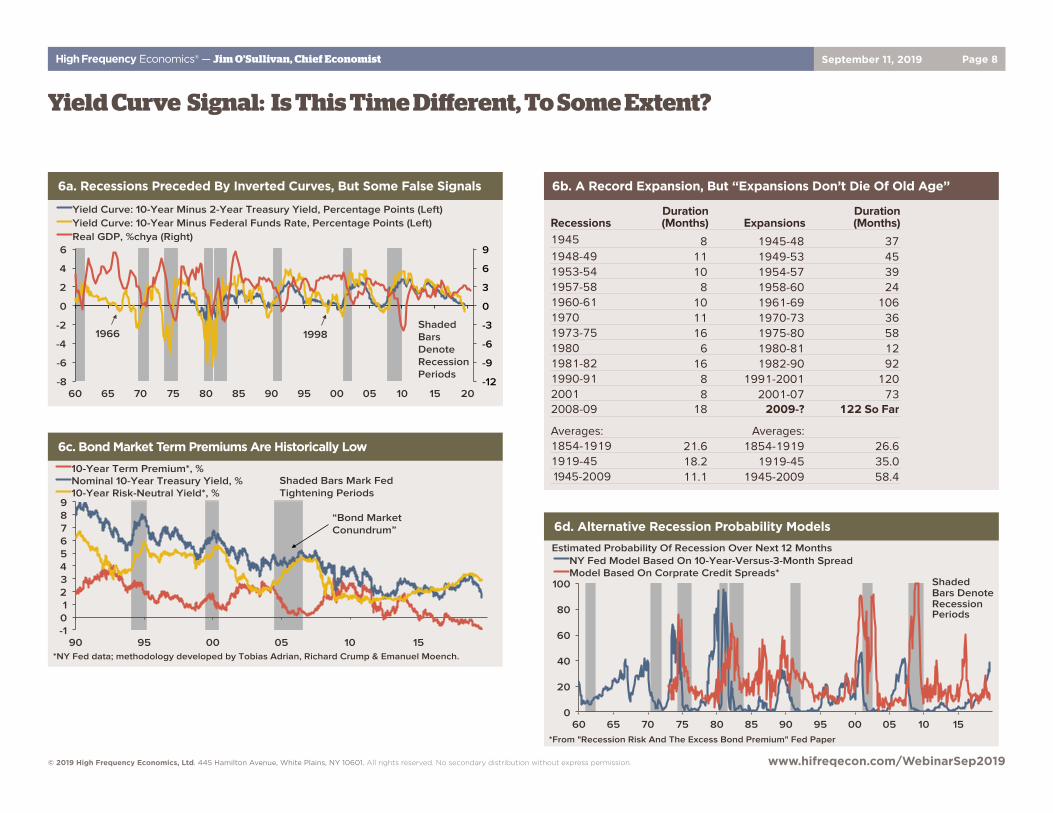

Yield Curve: 10-Year Minus 2-Year Treasury Yield, Percentage Points (Left) Yield Curve: 10-Year Minus Federal Funds Rate, Percentage Points (Left) Real GDP, %chya (Right)

Shaded Bars Denote Recession Periods

1966 1998

6a. Recessions Preceded By Inverted Curves, But Some False Signals

0

20

40

60

80

100

60 65 70 75 80 85 90 95 00 05 10 15

NY Fed Model Based On 10-Year-Versus-3-Month Spread Model Based On Corprate Credit Spreads*

Shaded Bars Denote Recession Periods

*From "Recession Risk And The Excess Bond Premium" Fed Paper

Estimated Probability Of Recession Over Next 12 Months

6d. Alternative Recession Probability Models

Yield Curve Signal: Is This Time Different, To Some Extent?

6b. A Record Expansion, But “Expansions Don’t Die Of Old Age”

RecessionsDuration (Months) Expansions

Duration (Months)

1945 8 1945-48 371948-49 11 1949-53 451953-54 10 1954-57 391957-58 8 1958-60 241960-61 10 1961-69 1061970 11 1970-73 361973-75 16 1975-80 581980 6 1980-81 121981-82 16 1982-90 921990-91 8 1991-2001 1202001 8 2001-07 732008-09 18 2009-? 122 So Far

Averages: Averages:1854-1919 21.6 1854-1919 26.61919-45 18.2 1919-45 35.0 1945-2009 11.1 1945-2009 58.4

-1 0 1 2 3 4 5 6 7 8 9

90 95 00 05 10 15

10-Year Term Premium*, % Nominal 10-Year Treasury Yield, % 10-Year Risk-Neutral Yield*, %

*NY Fed data; methodology developed by Tobias Adrian, Richard Crump & Emanuel Moench.

“Bond Market Conundrum”

Shaded Bars Mark Fed Tightening Periods

6c. Bond Market Term Premiums Are Historically Low

High Frequency Economics® — Jim O’Sullivan, Chief Economist September 11, 2019 Page 9

© 2019 High Frequency Economics, Ltd. 445 Hamilton Avenue, White Plains, NY 10601. All rights reserved. No secondary distribution without express permission. www.hifreqecon.com/WebinarSep2019

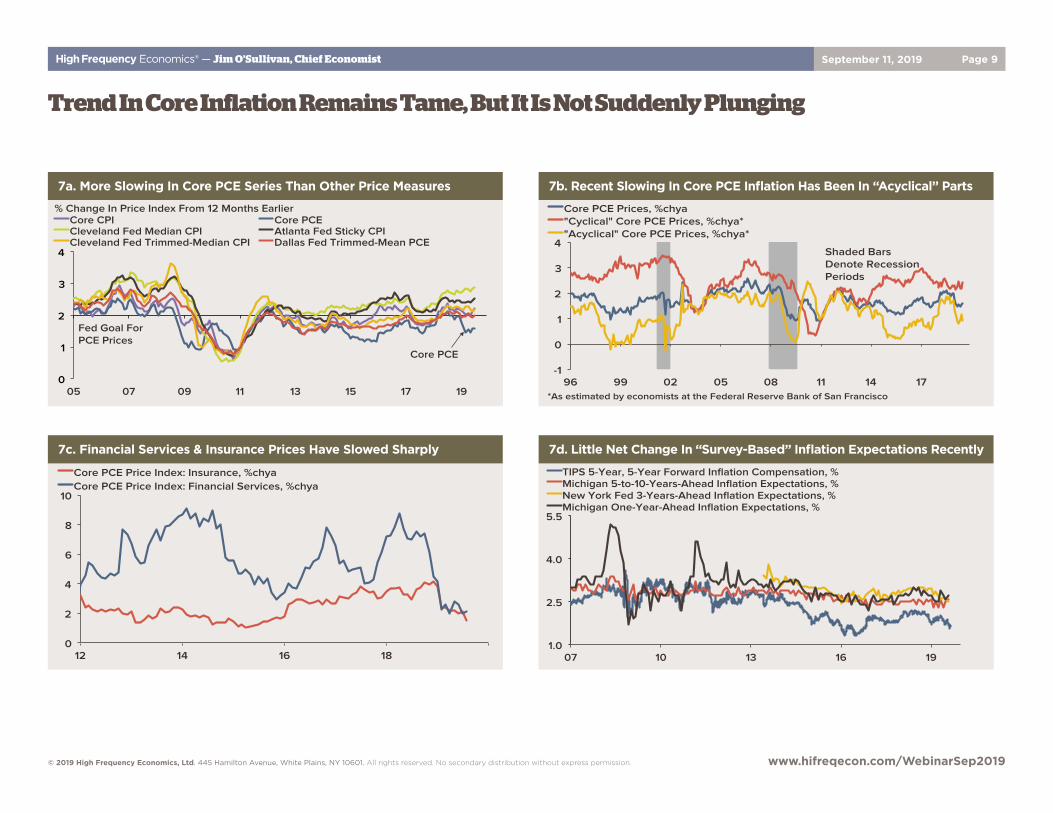

Trend In Core Inflation Remains Tame, But It Is Not Suddenly Plunging

0

2

4

6

8

10

12 14 16 18

Core PCE Price Index: Insurance, %chya Core PCE Price Index: Financial Services, %chya

7c. Financial Services & Insurance Prices Have Slowed Sharply

1.0

2.5

4.0

5.5

07 10 13 16 19

TIPS 5-Year, 5-Year Forward Inflation Compensation, % Michigan 5-to-10-Years-Ahead Inflation Expectations, % New York Fed 3-Years-Ahead Inflation Expectations, % Michigan One-Year-Ahead Inflation Expectations, %

7d. Little Net Change In “Survey-Based” Inflation Expectations Recently

0

1

2

3

4

05 07 09 11 13 15 17 19

Core CPI Core PCE Cleveland Fed Median CPI Atlanta Fed Sticky CPI Cleveland Fed Trimmed-Median CPI Dallas Fed Trimmed-Mean PCE

% Change In Price Index From 12 Months Earlier

Fed Goal For PCE Prices

Core PCE

7a. More Slowing In Core PCE Series Than Other Price Measures

-1

0

1

2

3

4

96 99 02 05 08 11 14 17

Core PCE Prices, %chya "Cyclical" Core PCE Prices, %chya* "Acyclical" Core PCE Prices, %chya*

Shaded Bars Denote Recession Periods

*As estimated by economists at the Federal Reserve Bank of San Francisco

7b. Recent Slowing In Core PCE Inflation Has Been In “Acyclical” Parts

High Frequency Economics® — Jim O’Sullivan, Chief Economist September 11, 2019 Page 10

© 2019 High Frequency Economics, Ltd. 445 Hamilton Avenue, White Plains, NY 10601. All rights reserved. No secondary distribution without express permission. www.hifreqecon.com/WebinarSep2019

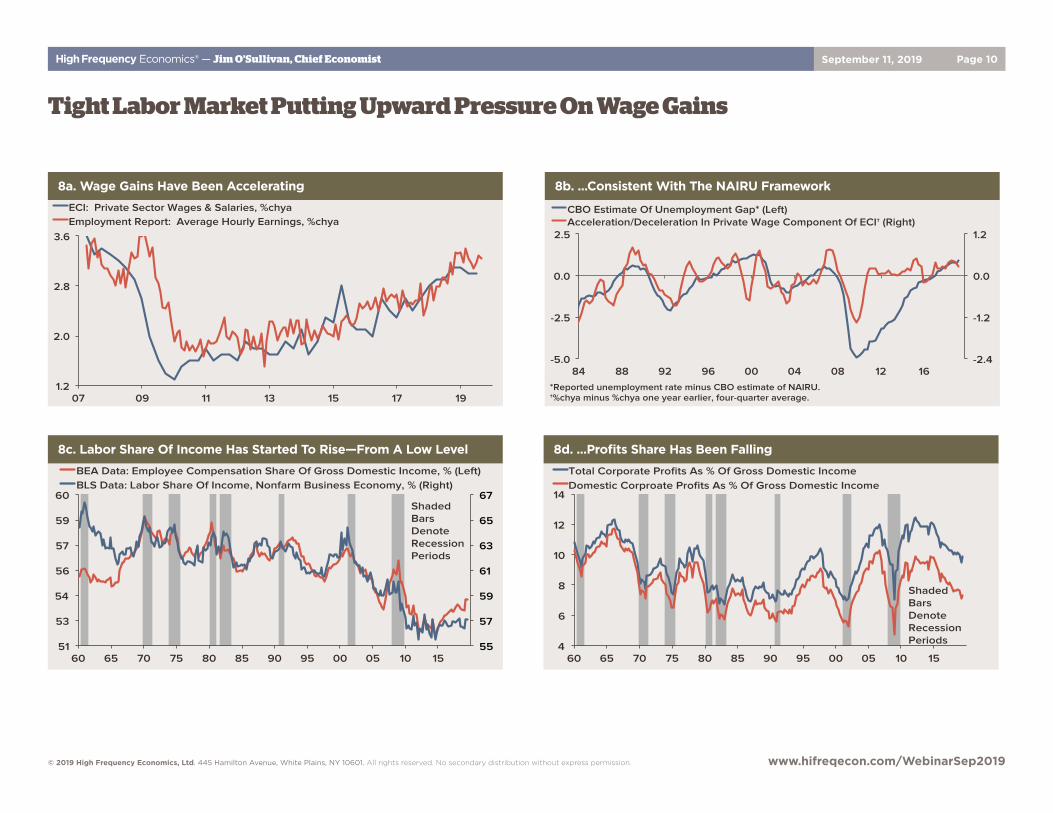

Tight Labor Market Putting Upward Pressure On Wage Gains

55

57

59

61

63

65

67

51

53

54

56

57

59

60

60 65 70 75 80 85 90 95 00 05 10 15

BEA Data: Employee Compensation Share Of Gross Domestic Income, % (Left) BLS Data: Labor Share Of Income, Nonfarm Business Economy, % (Right)

Shaded Bars Denote Recession Periods

8c. Labor Share Of Income Has Started To Rise—From A Low Level

4

6

8

10

12

14

60 65 70 75 80 85 90 95 00 05 10 15

Total Corporate Profits As % Of Gross Domestic Income Domestic Corproate Profits As % Of Gross Domestic Income

Shaded Bars Denote Recession Periods

8d. ...Profits Share Has Been Falling

-2.4

-1.2

0.0

1.2

-5.0

-2.5

0.0

2.5

84 88 92 96 00 04 08 12 16

CBO Estimate Of Unemployment Gap* (Left) Acceleration/Deceleration In Private Wage Component Of ECI† (Right)

*Reported unemployment rate minus CBO estimate of NAIRU. †%chya minus %chya one year earlier, four-quarter average.

8b. ...Consistent With The NAIRU Framework

1.2

2.0

2.8

3.6

07 09 11 13 15 17 19

ECI: Private Sector Wages & Salaries, %chya Employment Report: Average Hourly Earnings, %chya

8a. Wage Gains Have Been Accelerating

High Frequency Economics® — Jim O’Sullivan, Chief Economist September 11, 2019 Page 11

© 2019 High Frequency Economics, Ltd. 445 Hamilton Avenue, White Plains, NY 10601. All rights reserved. No secondary distribution without express permission. www.hifreqecon.com/WebinarSep2019

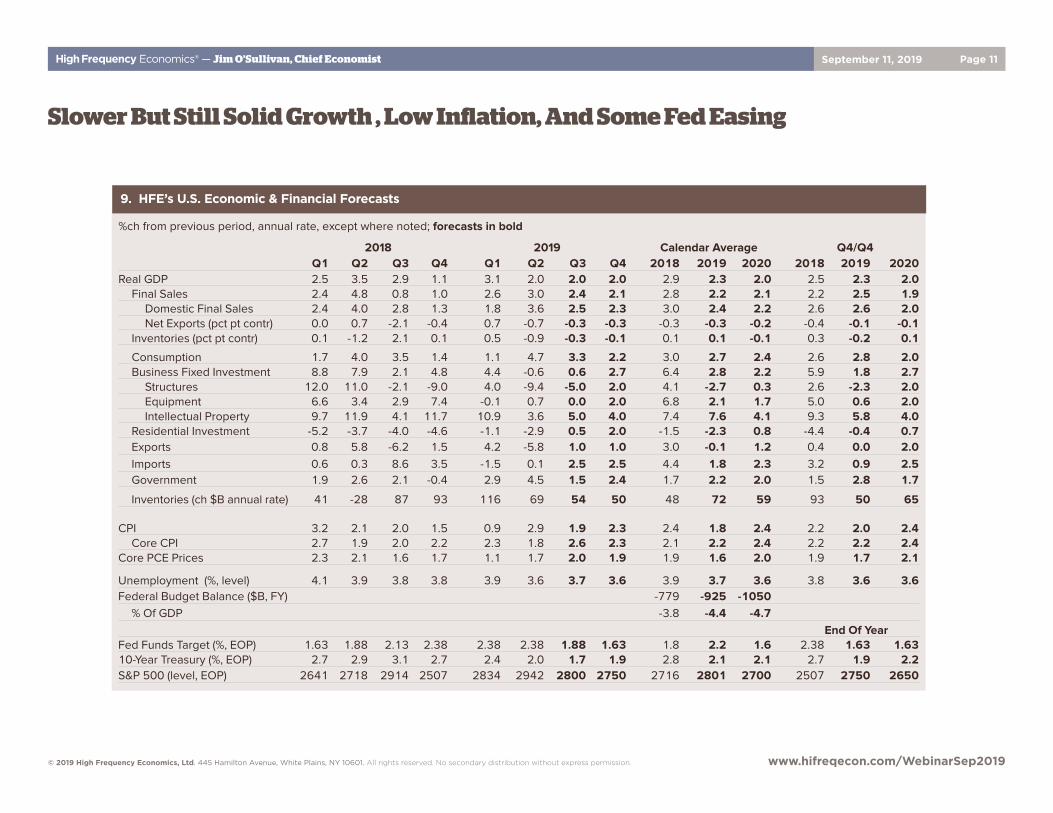

%ch from previous period, annual rate, except where noted; forecasts in bold

2018 2019 Calendar Average Q4/Q4Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 2018 2019 2020 2018 2019 2020

Real GDP 2.5 3.5 2.9 1.1 3.1 2.0 2.0 2.0 2.9 2.3 2.0 2.5 2.3 2.0Final Sales 2.4 4.8 0.8 1.0 2.6 3.0 2.4 2.1 2.8 2.2 2.1 2.2 2.5 1.9

Domestic Final Sales 2.4 4.0 2.8 1.3 1.8 3.6 2.5 2.3 3.0 2.4 2.2 2.6 2.6 2.0Net Exports (pct pt contr) 0.0 0.7 -2.1 -0.4 0.7 -0.7 -0.3 -0.3 -0.3 -0.3 -0.2 -0.4 -0.1 -0.1

Inventories (pct pt contr) 0.1 -1.2 2.1 0.1 0.5 -0.9 -0.3 -0.1 0.1 0.1 -0.1 0.3 -0.2 0.1

Consumption 1.7 4.0 3.5 1.4 1.1 4.7 3.3 2.2 3.0 2.7 2.4 2.6 2.8 2.0Business Fixed Investment 8.8 7.9 2.1 4.8 4.4 -0.6 0.6 2.7 6.4 2.8 2.2 5.9 1.8 2.7

Structures 12.0 11.0 -2.1 -9.0 4.0 -9.4 -5.0 2.0 4.1 -2.7 0.3 2.6 -2.3 2.0Equipment 6.6 3.4 2.9 7.4 -0.1 0.7 0.0 2.0 6.8 2.1 1.7 5.0 0.6 2.0Intellectual Property 9.7 11.9 4.1 11.7 10.9 3.6 5.0 4.0 7.4 7.6 4.1 9.3 5.8 4.0

Residential Investment -5.2 -3.7 -4.0 -4.6 -1.1 -2.9 0.5 2.0 -1.5 -2.3 0.8 -4.4 -0.4 0.7Exports 0.8 5.8 -6.2 1.5 4.2 -5.8 1.0 1.0 3.0 -0.1 1.2 0.4 0.0 2.0Imports 0.6 0.3 8.6 3.5 -1.5 0.1 2.5 2.5 4.4 1.8 2.3 3.2 0.9 2.5Government 1.9 2.6 2.1 -0.4 2.9 4.5 1.5 2.4 1.7 2.2 2.0 1.5 2.8 1.7

Inventories (ch $B annual rate) 41 -28 87 93 116 69 54 50 48 72 59 93 50 65

CPI 3.2 2.1 2.0 1.5 0.9 2.9 1.9 2.3 2.4 1.8 2.4 2.2 2.0 2.4Core CPI 2.7 1.9 2.0 2.2 2.3 1.8 2.6 2.3 2.1 2.2 2.4 2.2 2.2 2.4

Core PCE Prices 2.3 2.1 1.6 1.7 1.1 1.7 2.0 1.9 1.9 1.6 2.0 1.9 1.7 2.1

Unemployment (%, level) 4.1 3.9 3.8 3.8 3.9 3.6 3.7 3.6 3.9 3.7 3.6 3.8 3.6 3.6Federal Budget Balance ($B, FY) -779 -925 -1050

% Of GDP -3.8 -4.4 -4.7End Of Year

Fed Funds Target (%, EOP) 1.63 1.88 2.13 2.38 2.38 2.38 1.88 1.63 1.8 2.2 1.6 2.38 1.63 1.6310-Year Treasury (%, EOP) 2.7 2.9 3.1 2.7 2.4 2.0 1.7 1.9 2.8 2.1 2.1 2.7 1.9 2.2S&P 500 (level, EOP) 2641 2718 2914 2507 2834 2942 2800 2750 2716 2801 2700 2507 2750 2650

9. HFE’s U.S. Economic & Financial Forecasts

Slower But Still Solid Growth , Low Inflation, And Some Fed Easing

When Dirt Pays More Than Bonds: Negative & Inverted Yield Curves, Inflation Risks & Industrial Recessions

Carl B. WeinbergChief International Economist www.hifreqecon.com/WebinarSep2019

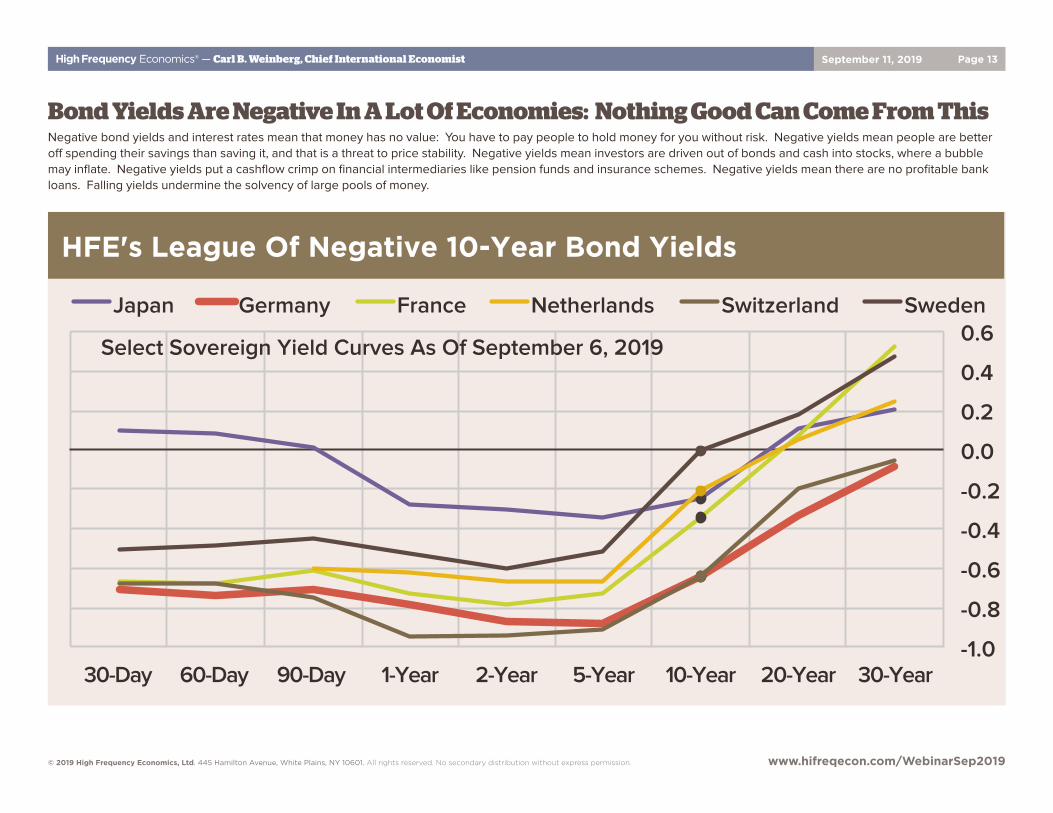

High Frequency Economics® — Carl B. Weinberg, Chief International Economist September 11, 2019 Page 13

© 2019 High Frequency Economics, Ltd. 445 Hamilton Avenue, White Plains, NY 10601. All rights reserved. No secondary distribution without express permission. www.hifreqecon.com/WebinarSep2019

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

30-Day 60-Day 90-Day 1-Year 2-Year 5-Year 10-Year 20-Year 30-Year

Japan Germany France Netherlands Switzerland Sweden

HFE's League Of Negative 10-Year Bond Yields

Select Sovereign Yield Curves As Of September 6, 2019

Bond Yields Are Negative In A Lot Of Economies: Nothing Good Can Come From ThisNegative bond yields and interest rates mean that money has no value: You have to pay people to hold money for you without risk. Negative yields mean people are better off spending their savings than saving it, and that is a threat to price stability. Negative yields mean investors are driven out of bonds and cash into stocks, where a bubble may inflate. Negative yields put a cashflow crimp on financial intermediaries like pension funds and insurance schemes. Negative yields mean there are no profitable bank loans. Falling yields undermine the solvency of large pools of money.

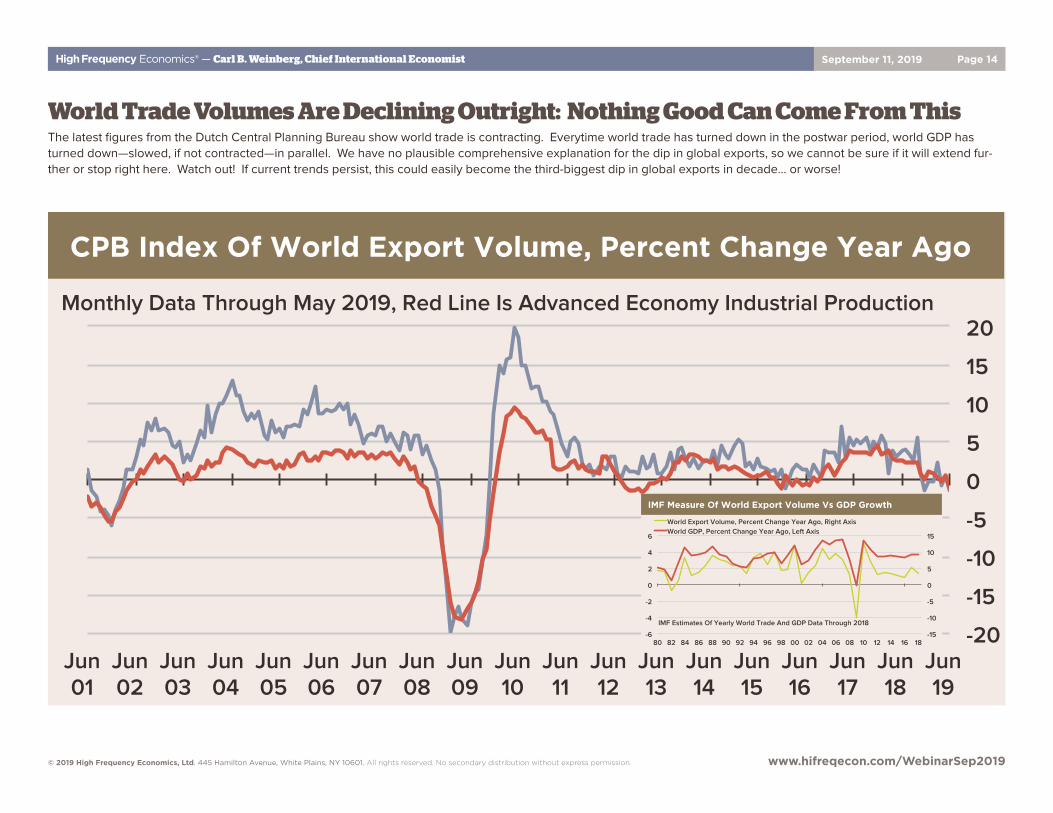

High Frequency Economics® — Carl B. Weinberg, Chief International Economist September 11, 2019 Page 14

© 2019 High Frequency Economics, Ltd. 445 Hamilton Avenue, White Plains, NY 10601. All rights reserved. No secondary distribution without express permission. www.hifreqecon.com/WebinarSep2019

World Trade Volumes Are Declining Outright: Nothing Good Can Come From ThisThe latest figures from the Dutch Central Planning Bureau show world trade is contracting. Everytime world trade has turned down in the postwar period, world GDP has turned down—slowed, if not contracted—in parallel. We have no plausible comprehensive explanation for the dip in global exports, so we cannot be sure if it will extend fur-ther or stop right here. Watch out! If current trends persist, this could easily become the third-biggest dip in global exports in decade… or worse!

-20

-15

-10

-5

0

5

10

15

20

Jun 01

Jun 02

Jun 03

Jun 04

Jun 05

Jun 06

Jun 07

Jun 08

Jun 09

Jun 10

Jun 11

Jun 12

Jun 13

Jun 14

Jun 15

Jun 16

Jun 17

Jun 18

Jun 19

Monthly Data Through May 2019, Red Line Is Advanced Economy Industrial Production

CPB Index Of World Export Volume, Percent Change Year Ago

-6

-4

-2

0

2

4

6

-15

-10

-5

0

5

10

15

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14 16 18

World Export Volume, Percent Change Year Ago, Right Axis World GDP, Percent Change Year Ago, Left Axis

IMF Estimates Of Yearly World Trade And GDP Data Through 2018

IMF Measure Of World Export Volume Vs GDP Growth

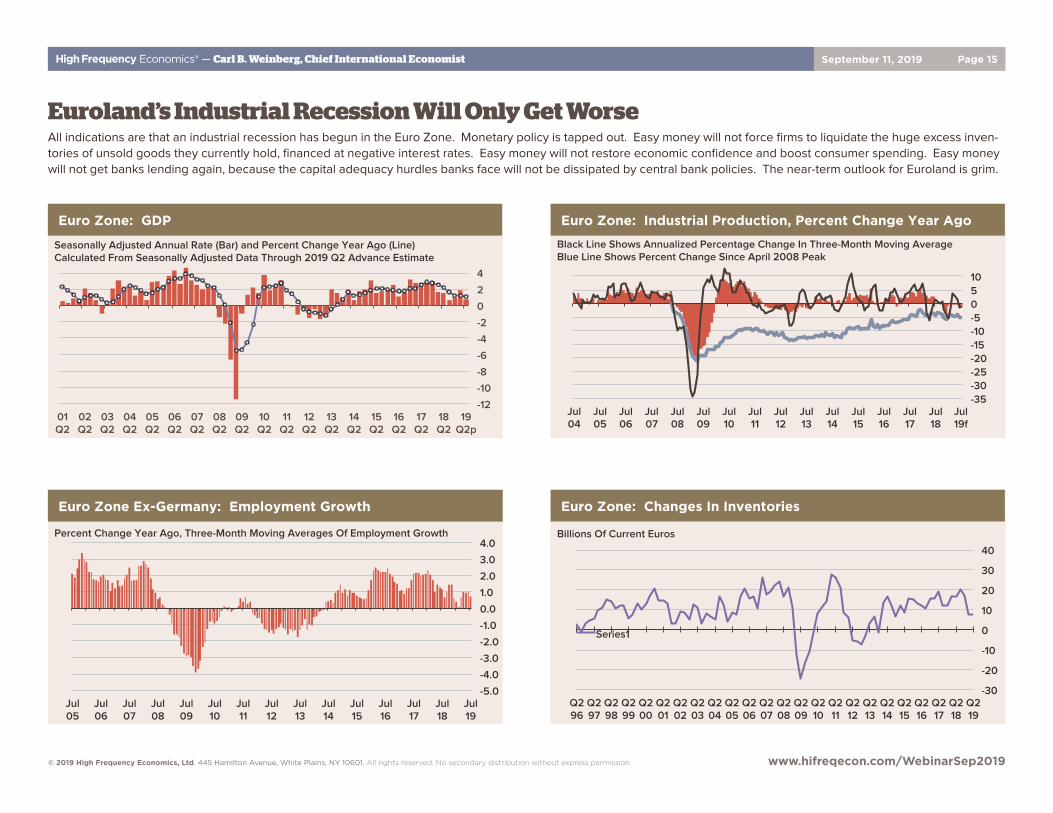

High Frequency Economics® — Carl B. Weinberg, Chief International Economist September 11, 2019 Page 15

© 2019 High Frequency Economics, Ltd. 445 Hamilton Avenue, White Plains, NY 10601. All rights reserved. No secondary distribution without express permission. www.hifreqecon.com/WebinarSep2019

-12

-10

-8

-6

-4

-2

0

2

4

01 Q2

02 Q2

03 Q2

04 Q2

05 Q2

06 Q2

07 Q2

08 Q2

09 Q2

10 Q2

11 Q2

12 Q2

13 Q2

14 Q2

15 Q2

16 Q2

17 Q2

18 Q2

19 Q2p

Euro Zone: GDP

Seasonally Adjusted Annual Rate (Bar) and Percent Change Year Ago (Line) Calculated From Seasonally Adjusted Data Through 2019 Q2 Advance Estimate

-35 -30 -25 -20 -15 -10 -5 0 5 10

Jul 04

Jul 05

Jul 06

Jul 07

Jul 08

Jul 09

Jul 10

Jul 11

Jul 12

Jul 13

Jul 14

Jul 15

Jul 16

Jul 17

Jul 18

Jul 19f

Black Line Shows Annualized Percentage Change In Three-Month Moving Average Blue Line Shows Percent Change Since April 2008 Peak

Euro Zone: Industrial Production, Percent Change Year Ago

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

Jul 05

Jul 06

Jul 07

Jul 08

Jul 09

Jul 10

Jul 11

Jul 12

Jul 13

Jul 14

Jul 15

Jul 16

Jul 17

Jul 18

Jul 19

Euro Zone Ex-Germany: Employment Growth

Percent Change Year Ago, Three-Month Moving Averages Of Employment Growth

-30

-20

-10

0

10

20

30

40

Q2 96

Q2 97

Q2 98

Q2 99

Q2 00

Q2 01

Q2 02

Q2 03

Q2 04

Q2 05

Q2 06

Q2 07

Q2 08

Q2 09

Q2 10

Q2 11

Q2 12

Q2 13

Q2 14

Q2 15

Q2 16

Q2 17

Q2 18

Q2 19

Series1

Billions Of Current Euros

Euro Zone: Changes In Inventories

Euroland’s Industrial Recession Will Only Get WorseAll indications are that an industrial recession has begun in the Euro Zone. Monetary policy is tapped out. Easy money will not force firms to liquidate the huge excess inven-tories of unsold goods they currently hold, financed at negative interest rates. Easy money will not restore economic confidence and boost consumer spending. Easy money will not get banks lending again, because the capital adequacy hurdles banks face will not be dissipated by central bank policies. The near-term outlook for Euroland is grim.

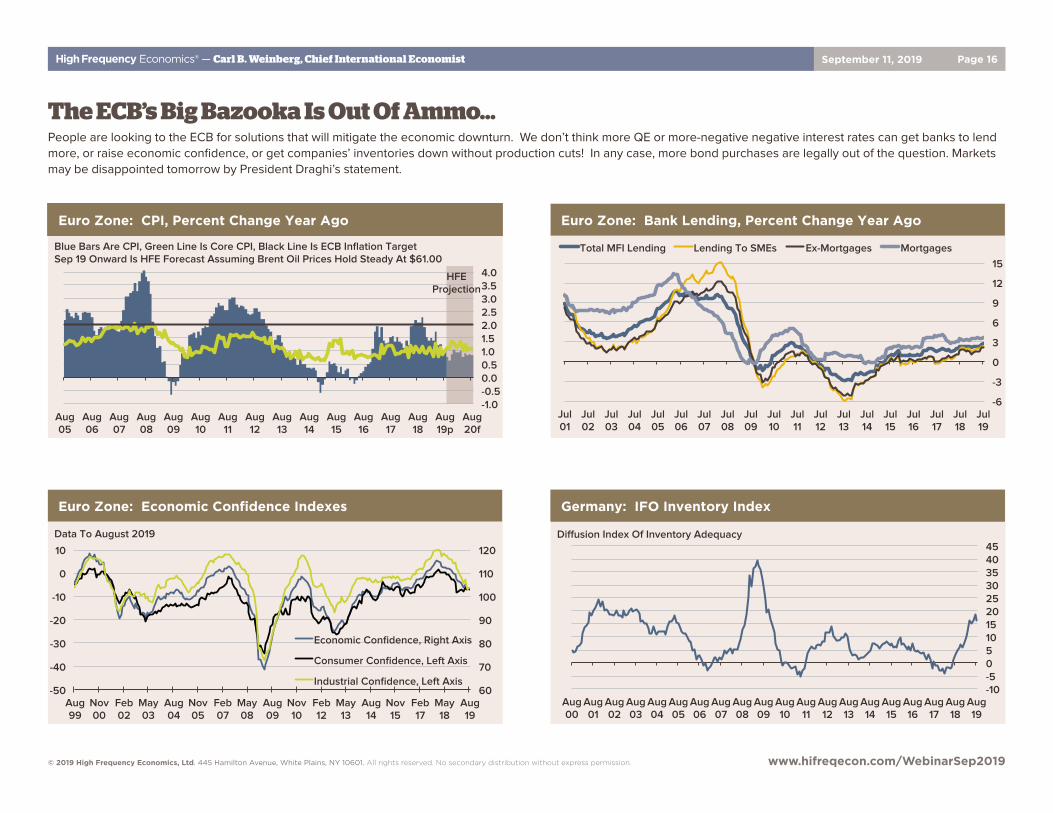

High Frequency Economics® — Carl B. Weinberg, Chief International Economist September 11, 2019 Page 16

© 2019 High Frequency Economics, Ltd. 445 Hamilton Avenue, White Plains, NY 10601. All rights reserved. No secondary distribution without express permission. www.hifreqecon.com/WebinarSep2019

-1.0 -0.5 0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0

Aug 05

Aug 06

Aug 07

Aug 08

Aug 09

Aug 10

Aug 11

Aug 12

Aug 13

Aug 14

Aug 15

Aug 16

Aug 17

Aug 18

Aug 19p

Aug 20f

Euro Zone: CPI, Percent Change Year Ago

Blue Bars Are CPI, Green Line Is Core CPI, Black Line Is ECB Inflation Target Sep 19 Onward Is HFE Forecast Assuming Brent Oil Prices Hold Steady At $61.00

HFE Projection

-6

-3

0

3

6

9

12

15

Jul 01

Jul 02

Jul 03

Jul 04

Jul 05

Jul 06

Jul 07

Jul 08

Jul 09

Jul 10

Jul 11

Jul 12

Jul 13

Jul 14

Jul 15

Jul 16

Jul 17

Jul 18

Jul 19

Total MFI Lending Lending To SMEs Ex-Mortgages Mortgages

Euro Zone: Bank Lending, Percent Change Year Ago

-50

-40

-30

-20

-10

0

10

60

70

80

90

100

110

120

Aug 99

Nov 00

Feb 02

May 03

Aug 04

Nov 05

Feb 07

May 08

Aug 09

Nov 10

Feb 12

May 13

Aug 14

Nov 15

Feb 17

May 18

Aug 19

Economic Confidence, Right Axis

Consumer Confidence, Left Axis

Industrial Confidence, Left Axis

Data To August 2019

Euro Zone: Economic Confidence Indexes

-10 -5 0 5 10 15 20 25 30 35 40 45

Aug 00

Aug 01

Aug 02

Aug 03

Aug 04

Aug 05

Aug 06

Aug 07

Aug 08

Aug 09

Aug 10

Aug 11

Aug 12

Aug 13

Aug 14

Aug 15

Aug 16

Aug 17

Aug 18

Aug 19

Germany: IFO Inventory Index Germany: IFO Inventory Index

Diffusion Index Of Inventory Adequacy

The ECB’s Big Bazooka Is Out Of Ammo…People are looking to the ECB for solutions that will mitigate the economic downturn. We don’t think more QE or more-negative negative interest rates can get banks to lend more, or raise economic confidence, or get companies’ inventories down without production cuts! In any case, more bond purchases are legally out of the question. Markets may be disappointed tomorrow by President Draghi’s statement.

High Frequency Economics® — Carl B. Weinberg, Chief International Economist September 11, 2019 Page 17

© 2019 High Frequency Economics, Ltd. 445 Hamilton Avenue, White Plains, NY 10601. All rights reserved. No secondary distribution without express permission. www.hifreqecon.com/WebinarSep2019

80

90

100

110

120

130

Sep 97

Sep 98

Sep 99

Sep 00

Sep 01

Sep 02

Sep 03

Sep 04

Sep 05

Sep 06

Sep 07

Sep 08

Sep 09

Sep 10

Sep 11

Sep 12

Sep 13

Sep 14

Sep 15

Sep 16

Sep 17

Sep 18

Sep 19

Westpac Trade-Weighted Yuan Index, 2000=100

Monthly Data, Final Datapoint Is September 6, 2019 Trend-Based Trading Channel Since 2015 Reform Shown

Westpac Trade-Weighted Yuan Index

0

50

100

150

200

250

300

350

400

450

Aug 03

Aug 04

Aug 05

Aug 06

Aug 07

Aug 08

Aug 09

Aug 10

Aug 11

Aug 12

Aug 13

Aug 14

Aug 15

Aug 16

Aug 17

Aug 18

Aug 19

Trade With The World

Trade With The United States

Exports Plus Imports Per Month, Billion Of U.S. Dollars, 12-Month Moving Averages Shown

China: Gross Trade China: Gross Trade (Exports + Imports)

-50 -40 -30 -20 -10 0 10 20 30 40 50 60 70 80 90 100

Aug 02

Aug 03

Aug 04

Aug 05

Aug 06

Aug 07

Aug 08

Aug 09

Aug 10

Aug 11

Aug 12

Aug 13

Aug 14

Aug 15

Aug 16

Aug 17

Aug 18

Aug 19

China: Monthly Imports From The United States

Percent Change Year Ago, Yellow Line Shows 5-Month Moving Average, In U.S. Dollars

China: Monthly Imports From The United States

-30

-20

-10

0

10

20

30

40

50

Aug 02

Aug 03

Aug 04

Aug 05

Aug 06

Aug 07

Aug 08

Aug 09

Aug 10

Aug 11

Aug 12

Aug 13

Aug 14

Aug 15

Aug 16

Aug 17

Aug 18

Aug 19

Percent Change Year Ago, Yellow Line Shows 5-Month Moving Average, In U.S. Dollars

China: Monthly Exports To The United States China: Monthly Exports To The United States

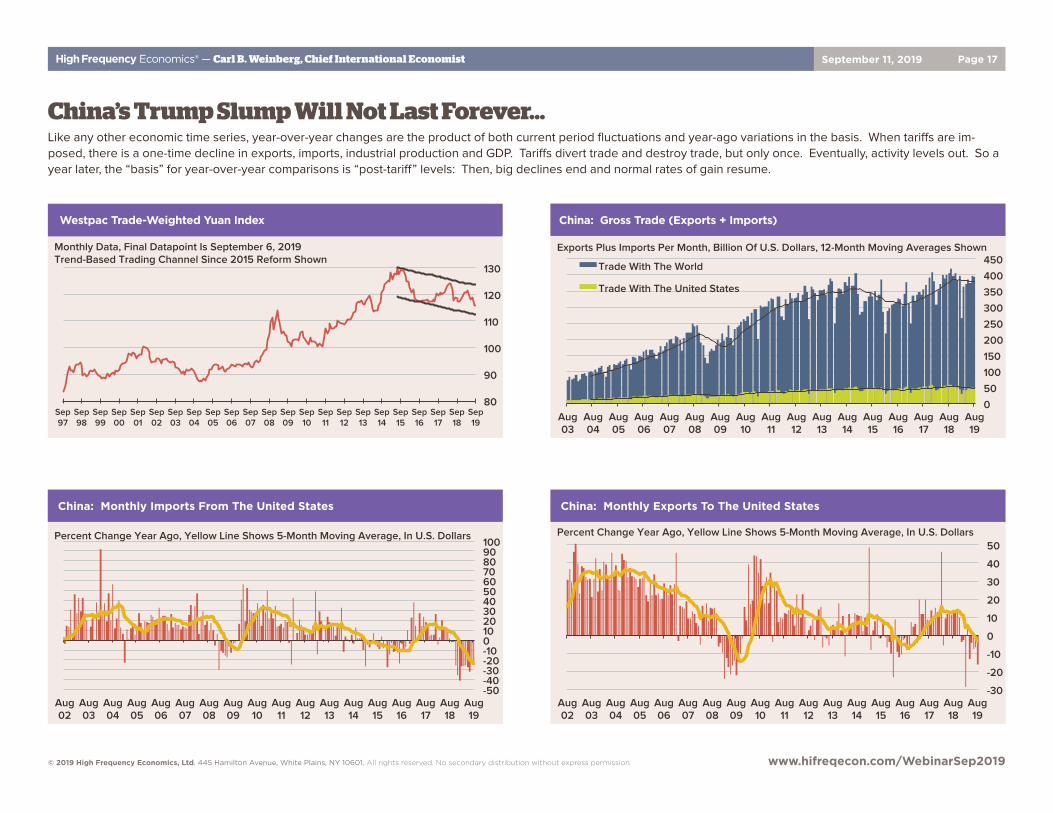

China’s Trump Slump Will Not Last Forever…Like any other economic time series, year-over-year changes are the product of both current period fluctuations and year-ago variations in the basis. When tariffs are im-posed, there is a one-time decline in exports, imports, industrial production and GDP. Tariffs divert trade and destroy trade, but only once. Eventually, activity levels out. So a year later, the “basis” for year-over-year comparisons is “post-tariff” levels: Then, big declines end and normal rates of gain resume.

High Frequency Economics® — Carl B. Weinberg, Chief International Economist September 11, 2019 Page 18

© 2019 High Frequency Economics, Ltd. 445 Hamilton Avenue, White Plains, NY 10601. All rights reserved. No secondary distribution without express permission. www.hifreqecon.com/WebinarSep2019

0

5

10

15

20

Sep 99

Sep 00

Sep 01

Sep 02

Sep 03

Sep 04

Sep 05

Sep 06

Sep 07

Sep 08

Sep 09

Sep 10

Sep 11

Sep 12

Sep 13

Sep 14

Sep 15

Sep 16

Sep 17

Sep 18

Sep 19

China: Required Reserve Ratio At Major Banks, Percent China: Required Reserve Ratio At Major Banks, Percent

0

5

10

15

20

25

30

Aug 03

Aug 04

Aug 05

Aug 06

Aug 07

Aug 08

Aug 09

Aug 10

Aug 11

Aug 12

Aug 13

Aug 14

Aug 15

Aug 16

Aug 17

Aug 18

Aug 19f

Stock Of Quasi-Money

Stock Of Quasi-Money

China: Growth Of Domestic Credit, Percent Change Year Ago China: Growth Of Domestic Credit, Percent Change Year Ago

0

5

10

15

20

Aug 04

Aug 05

Aug 06

Aug 07

Aug 08

Aug 09

Aug 10

Aug 11

Aug 12

Aug 13

Aug 14

Aug 15

Aug 16

Aug 17

Aug 18

Aug 19f

China: Industrial Production, Percent Change Year Ago

Yellow Line Is Three-Month Production Trend

China: Industrial Production, Percent Change Year Ago

-25

0

25

50

75

100

Aug 03

Aug 04

Aug 05

Aug 06

Aug 07

Aug 08

Aug 09

Aug 10

Aug 11

Aug 12

Aug 13

Aug 14

Aug 15

Aug 16

Aug 17

Aug 18

Aug 19f

M2 M1 Aggregate Financing

China: Money And Credit, Percent Change Year Ago China: Money And Credit, Percent Change Year Ago

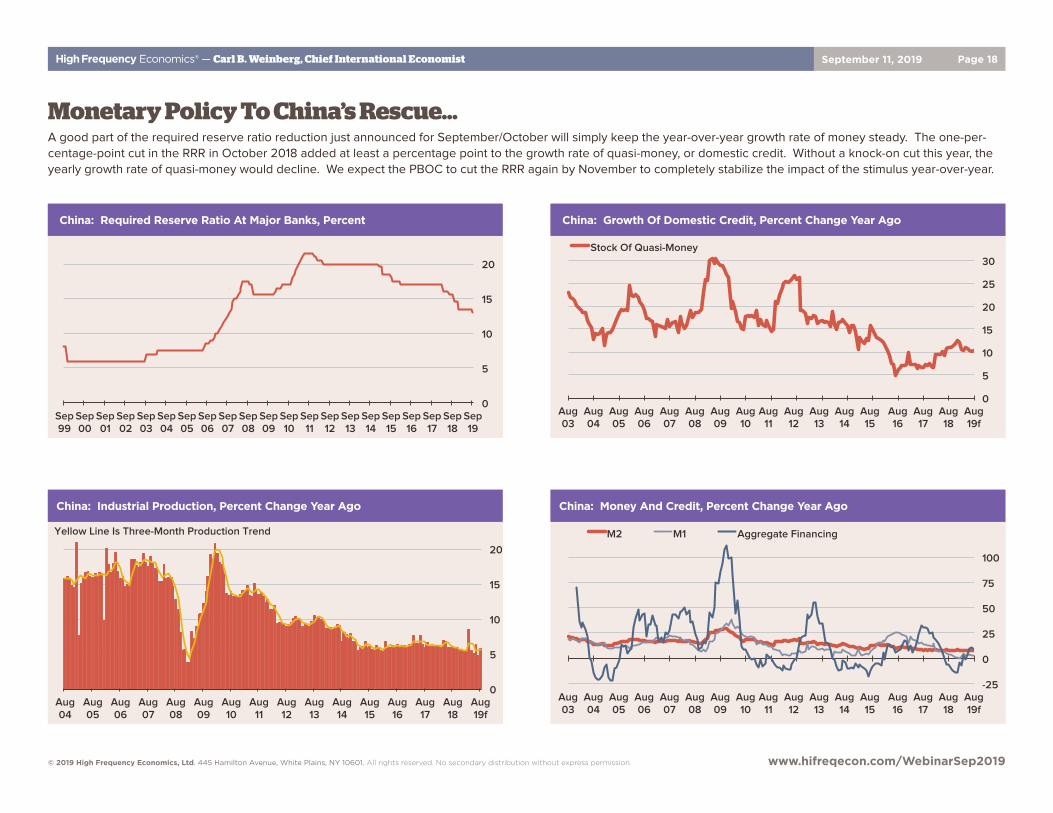

Monetary Policy To China’s Rescue…A good part of the required reserve ratio reduction just announced for September/October will simply keep the year-over-year growth rate of money steady. The one-per-centage-point cut in the RRR in October 2018 added at least a percentage point to the growth rate of quasi-money, or domestic credit. Without a knock-on cut this year, the yearly growth rate of quasi-money would decline. We expect the PBOC to cut the RRR again by November to completely stabilize the impact of the stimulus year-over-year.

High Frequency Economics® — Carl B. Weinberg, Chief International Economist September 11, 2019 Page 19

© 2019 High Frequency Economics, Ltd. 445 Hamilton Avenue, White Plains, NY 10601. All rights reserved. No secondary distribution without express permission. www.hifreqecon.com/WebinarSep2019

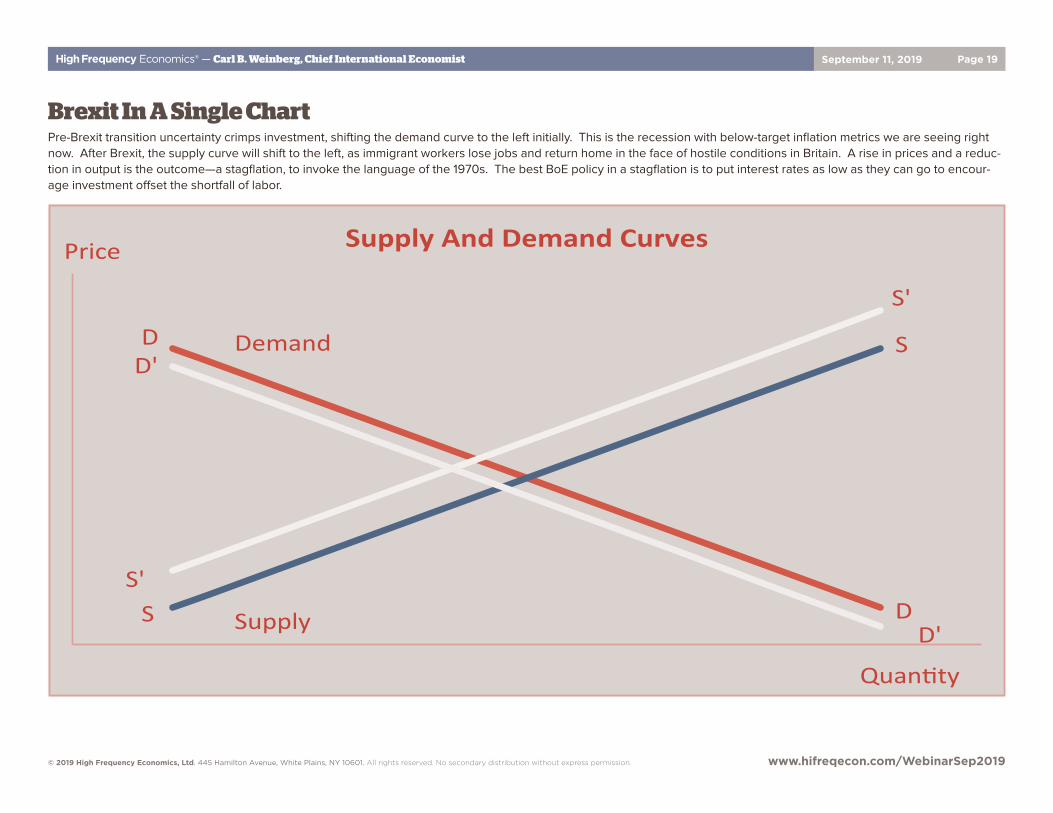

Brexit In A Single ChartPre-Brexit transition uncertainty crimps investment, shifting the demand curve to the left initially. This is the recession with below-target inflation metrics we are seeing right now. After Brexit, the supply curve will shift to the left, as immigrant workers lose jobs and return home in the face of hostile conditions in Britain. A rise in prices and a reduc-tion in output is the outcome—a stagflation, to invoke the language of the 1970s. The best BoE policy in a stagflation is to put interest rates as low as they can go to encour-age investment offset the shortfall of labor.

SupplyAndDemandCurves

Demand

Price

Quan.ty

D

D

D'

D'Supply

S'

S'

S

S

Global Webinar:Inverted & Negative Yield Curves, Trade Tensions & More

Jim O’Sullivan & Carl WeinbergHigh Frequency Economics www.hifreqecon.com/WebinarSep2019

![NFIB 2-2015 Committee Presentation [Compatibility Mode]](https://img.pdfslide.us/doc/110x75/55cf9264550346f57b9603a0/nfib-2-2015-committee-presentation-compatibility-mode.jpg)