Embed Size (px)

Citation preview

GLOBAL TRENDS IN ENTREPRENEURIAL FINANCE

COLLABORATE | INNOVATE 2017

1

2

SEEDLY IS AN EQUITY CROWDFUNDING PLATFORM… THE FIRST FOR ALL AUSTRALIANSWE WILL LAUNCH MORE BUSINESSES THAN ANY OTHER

WWW.SEEDLY.COM.AU

WHAT’S THE BIG PROBLEM?

3

USA, $75

AUS, $7.5

Israel, $150

VENTURE CAPITAL $PER CAPITA

FUNDING66%

OTHER34%

AUSTRALIANSMALL BUSINESS

SOURCES: Australia Bureau of Statistics, Australia Innovation Report

WHAT STOPS INNOVATION?

HOW DOES AUSTRALIA COMPARE?

WHERE’S THE MONEY?

DILUTIVE SOURCES

4

NON-DILUTIVE SOURCES

EQUITYCROWDFUNDING

ANGELINVESTORS

VENTURECAPITAL

STOCKMARKETIPO

CREDIT CARDBANK LOAN

PEER-PEERLENDING

DEBTCROWDFUNDING

MINIBONDS

CONVERTIBLENOTES

PARTNERS

SUPPLIER CREDIT

GRANTS

REWARD/DONATIONCROWDFUNDING

EQUITY DEBT OTHER

EMERGING TRENDS IN ENTREPRENEURIAL FINANCE

5

1. The VC industry is shifting at the biggest and smallest ends of the market.

2. Online platforms—for crowdfunding, angel syndication, and lending—are increasingly important options for seed-stage and early-stage startup needs.

3. Sources of capital are emerging outside of traditional geographical hubs.

4. Women are playing more decision-making roles in entrepreneurial capital.

5. There is robust experimentation with differentiated capital models.

GLOBAL MARKET DATA

6

$1.5TGLOBAL ENTREPRENEURIAL INVESTMENT FUNDS:

82% Personal (loans, lines of credit)16% Friends and Family2% Venture Capital and Crowdfunding

SOURCES OF FUNDS:

ALTERNATIVE FINANCE MARKET

• ness registrations (show that the demand is getting bigger

7

ASIA PACIFIC (EX CHINA)

SOURCES: The Asia-Pacific Alternative Finance Benchmarking Report, 2016, Cambridge University

CHINA ($USD)

VENTURE CAPITAL GLOBAL RANKINGS

• ness registrations (show that the demand is getting bigger

8

• Leading Venture Capital by region

• Venture Capital Investment often seen as a marker for innovation.

• Australia poorly ranked

• ness registrations (show that the demand is getting bigger

RESEARCH COMMERCIALISATION IN AUSTRALIA

9

$1.8B in successful exits from Australian university research projects

Irish Drug Group, Shire,acquired Melbourne based drug developer Fibrotech Therapeutics (scar tissue therapy) for $500M

Drug giant Novartis acquired Brisbane based pain relief company, Spinifex for $1B.

Hatchtech (head lice tech) $280M deal with Indian firm to commercialise product.

TRENDS: EQUITY CROWDFUNDING / CROWDCUBE

10

238Avg investors per

campaign (UK)

$762kAvg funds per campaign (UK)

Asia-Pacific Region (excluding China) Average Amount Raised in an Equity Crowdfunding campaign 2015 USD = $778,000 USDIn China, the average raised via ECF = $2.24m, Cambridge University

400kRegistered investors

525Successful raises

£1MIn 60 secondsFastest Raise

WHY EQUITY CROWDFUNDING

11

"I CAN'T TELL YOU HOW BAD THE WHOLE AUSTRALIAN VENTURE COMMUNITY IS, THE ANGEL COMMUNITY IS, THEY ARE JUST NASTY”

GORDON BELLINTERNET & COMPUTING INDUSTRY PIONEER

27 DAYSAvg days to fund (UK)

£600k +Avg funds per campaign (UK)

49% ROI*Across 375 deals at Seedrs (UK)

400,000Investors members on Crowdcube

TAX BREAKS ACCESSMore investors, more deals

A SHORT HISTORY OF EQUITY CROWDFUNDING

12

UKFirst ECF platform

launches 2011: Crowdcube

USA Opens broader ECF regulations

May 2016

NZ Opens ECF

regulations July 2014

AUSECF regulations

proposed in parliament 2015

£147million

UK ECF market 2015

AUSECF regulations go

live, Sept 2017

2011 2015 2017

WHERE NEXT?

13

CROSSOVER

SERVICE MODELS

SECONDARY ECF MARKET

RAPID SHORT TERM FUNDING

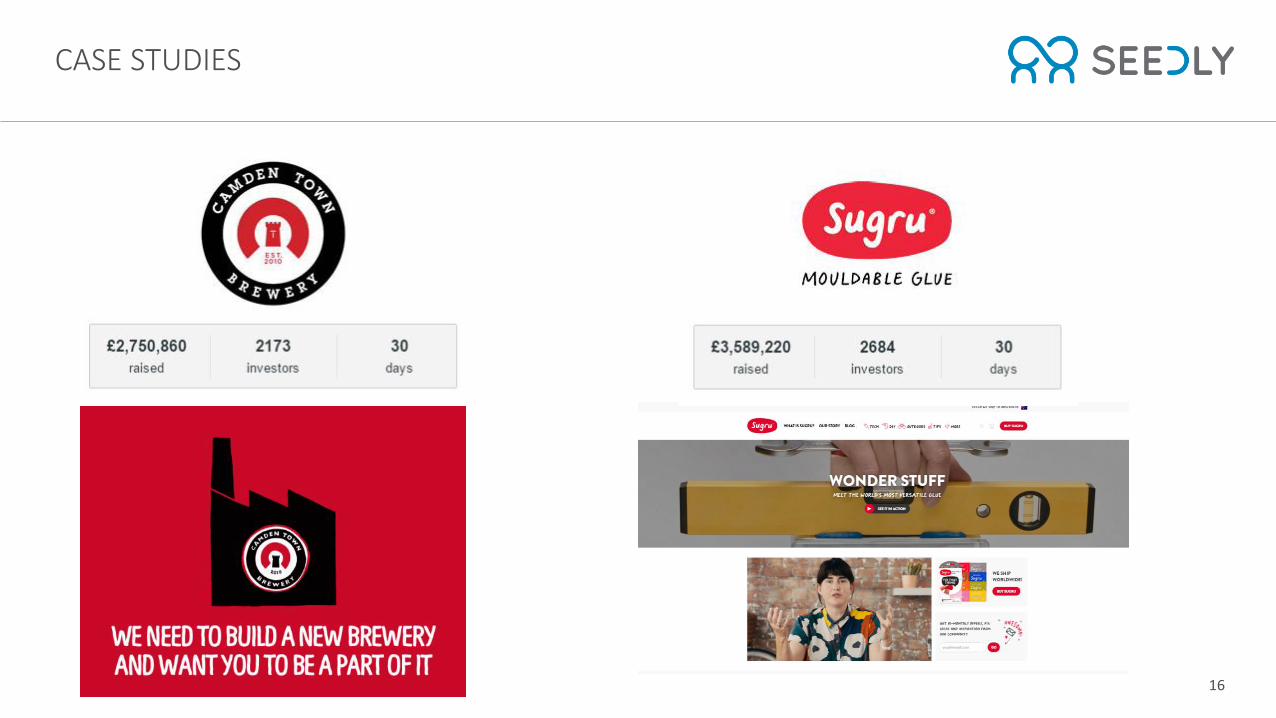

CASE STUDIES

14

BREWDOG - THE FIRST UNICORN EXIT

2,765%RETURN

$1.24BILLION VALUATION

(USD)

CASE STUDIES

15

CREATE A WINNING PITCH

• What problem do you solve? For who?

• How do you make money?

• What traction do you have?

• Why are you different?

• Who’s in the team?

• What are their roles?

• What skills, experience set you apart?

• What advisors & partnerships do you have?

• How big is it? What are the trends?

• What’s your go to market strategy?

• Competitors (Porters 5 forces)

• PESTEL analysis

17

THE IDEA

THE TEAM THE VIDEO

• Be direct & concise

• Be personable

• Be specific & give examples… eg ’46% faster than competitors processes’

• The first thing many investors look at

• Make it professional, make a connection

• You’ve got 30 seconds to win them over

• Don’t go longer than 3 minutes

• If you can’t afford motion graphics & animations, put a (good) person on camera

• First impressions count, be professional

• Strong logo and website

• An active Facebook and Twitter presence

LANGUAGE

YOUR BRANDTHE MARKET

THANK YOU

18

WWW.SEEDLY.COM.AU/CRC2017

An overview and comparison of new forms of entrepreneurial finance

New player Debt or equity Investment goal Investment approach Investment target

Active or passive Non-financial support

Accelerators (and incubators)

Depends on type of accelerator/ incubator

Financial, strategic, political (depends on type of accelerator/incubator)

Active Management support, training, network access

Early stage start-up

Angel networks Equity Financial Active Management support, network access

Early stage start-up

Crowd

- Debt-based Debt Financial Passive None Early stage start-up or project

- Donation-based – Social Passive None Social venture or project

- Reward-based – Product-related Passive, Sometimes active

Sometimes product testing

Early stage start-up or project

- Equity-based Equity Financial Passive, sometimes active

Advocacy, market & product testing

Dependant on legislative rules. Typically early stage start-up or Series A growth stage.

Corporate venture capital (CVC)

Equity Financial, technological, and strategic

Active Management support, technology support

Early and later stage start-up

New player Debt or equity Investment goal Investment approach Investment target

Active or passive Non-financial support

Family offices Equity Financial Mostly passive Little Later stage start-up

Governmental venture capital (GVC)

Debt or equity Financial and governmental Mostly passive Little Early and later stage start-up

IP-based investment funds

– Financial Passive None Patents

IP-backed debt funding

Debt Financial Passive IP-based start-ups and established mid-sized firms

Mini-bonds Debt Financial Passive Established mid-sized firms

Social venture funds or social venture capital

Debt and equity Financial and social Active Management support, network access

Social ventures

University-managed or university-based funds

Mostly equity Financial and university-related Active Management support, network access

Academic and student start-ups

Venture debt lenders or funds

Debt Financial Passive None Later stage start-up

Source: Block, J.H., Colombo, M.G., Cumming, D.J. et al. Small Bus Econ (2017)