Embed Size (px)

Citation preview

1

Global Trends & Forecasts, 2016Forging new connections

January 2016

2

• Retail is going through an unprecedented period of rapid dynamism - and this is primarily due to a changing shopper.

• The past decade has seen a number of long-standing socio-demographic changes combining with technological advances to create a more powerful consumer.

• This is leading to consumers being drawn towards convenience, value, health & wellness and personalisation.

• In contrast, they have turned away from big-box stores -the core channel for most of the leading global grocers.

• The rise of new personal technologies (primarily smartphones) is now giving consumers the ability to engage with retailers in new ways, often on their own terms.

• Understanding these shifts in consumer behaviour will be vital, especially as the rate of change is likely to accelerate further in the future.

Retailers are having to navigate and reposition themselves in an increasingly complex world.

The only constant is change

Global Trends & Forecasts, 2016: Forging new connections

Key Trends of the Future

Constantly connected consumers

The store reinvented

Evolution of marketing & loyalty

Personalised & contextualised

experiencesThe on-demand

economyHealth & Wellness

authorities

Safety in numbers

Demise of discount?

Search for simplification

3

1. The Global Retail Landscape in 2016

2. A Changing Shopper

3. Retailer Impact

4. Future Trends

Contents

Global Trends & Forecasts, 2016: Forging new connections

Robert GregoryGlobal Research Director

[email protected]@RobGregOnRetail

All images ©Planet Retail Ltd unless otherwise stated.

Malcolm PinkertonResearch Director

[email protected]@MGQPinkerton

4

What interested you in 2015

1. The Global Retail Landscape in 2016

Based on Planet Retail’s most read news stories during the year.

5

Our Top 5 developments of 2015

1. The Global Retail Landscape in 2016

Stories we predict will have a lasting impact:

JANUARY

The year started with the news that Tesco was looking to shore up its balance sheet amid falling sales and disappearing profits.

This included the closure of unprofitable stores and a reduction in capex, while peripheral operations which had been acquired or built up in recent years, such as movie service blinkbox and Tesco Mobile, were also sold as the company moved to refocus on its core food unit. Later in the year, its South Korean operation was divested and further operations are likely to be under review. All of this was underpinned by the announcement of one of the biggest losses in UK corporate history, totalling GBP6.4 billion (USD10 billion), in April.

APRIL

Alibaba forms partnership with China Telecom to leverage the national mobile network and target rural locations.

The move will help Alibaba gain a presence with those who have so far escaped from the smartphone revolution sweeping China. Importantly, with the phone coming pre-loaded with Alibaba apps, the move will keep consumers within the retailer’s burgeoning ecosystem. Planet Retail’s Shopology data shows that 20% of Chinese shoppers use their mobiles for shopping, compared to 9% in the US, so gaining early stickiness now will be crucial to long-term loyalty and success.

JULY

Walmart takes full ownership of online grocery service Yihaodianin China.

This clearly signals that Walmart is not waiting to be left behind in the digital arms race and that online will play a big part in its future, even in China. This coincides with ongoing investment in creating a seamless digital experience in markets as varied as India (all stores to offer online services this year) to the US (grocery collection service expanded). In fact, accelerated investment in online was cited as a major reason behind Walmart’s October warning on profits in the years to come.

AUGUST

Several leading European retailers (including Edeka, ITM, Eroski, Colruyt, Conad and Coop CH) join forces to form the Agecore buying group.

This was just one high-profile example of a spate of buying alliances which arose across Europe in 2015. Others included Metro Group/Auchan and Leclerc/Rewe Group. With the creation of so many strong buying alliances of late, most notably in France, manufacturers will be challenged as regards striking a balance between realising new sales opportunities and maintaining relatively stable selling prices.

OCTOBER

Walgreens Boots Alliance acquires Rite Aid, combining the second and third-largest drugstore chains in the US.

Aside from leaving rival CVS Health trailing behind in the US, the mega-merger has global implications. The combined entity has potential annual sales in excess of USD130 billion, enough to make it the world’s second-largest retailer behind Walmart. Further acquisitions in Asia and Latin America could follow as the retailer looks to develop global scale.

6

Regional Overview

1. The Global Retail Landscape in 2016

NORTH AMERICA

ASIA & OCEANIA

RetailerSales, 2015

(USD bn)Sales, 2020

(USD bn)

1 Walmart 398 455

2 Kroger 116 140

3 Costco 105 132

94%

6%

95%

5%

Modern vs Traditional Split

Modern Traditional

Growth ChannelCAGR, 2015-

2020 (%)Major Players

Discount stores +7.7% Dollar General, Dollar Tree, Aldi

2015 2020

RetailerSales, 2015

(USD bn)Sales, 2020

(USD bn)

1 Seven & I 77 97

2 AEON 62 67

3 Woolworths (AUS) 51 62

30%

70%

29%

71%

Modern vs Traditional Split

Modern Traditional

Growth ChannelCAGR, 2015-

2020 (%)Major Players

Convenience stores

+6.6% Seven & I, FamilyMart,LAWSON

2015 2020

7

Regional Overview

1. The Global Retail Landscape in 2016

RetailerSales, 2015

(USD bn)Sales, 2020

(USD bn)

1 Walmart 50 61

2 Casino 25 38

3 Cencosud 19 25

Growth ChannelCAGR, 2015-

2020 (%)Major Players

Discount stores +8.6% Walmart, Dia, Casino

RetailerSales, 2015

(USD bn)Sales, 2020

(USD bn)

1 Schwarz Group 22 34

2 Magnit 17 39

3 Metro Group 15 23

Growth ChannelCAGR, 2015-

2020 (%)Major Players

Hypermarkets & superstores

+9.3% Auchan, Schwarz Group, Lenta

LATIN AMERICA

CENTRAL & EASTERN EUROPE

50%50% 51%49%

Modern vs Traditional Split

Modern Traditional

2015 2020

54%46%

58%

42%

Modern vs Traditional Split

Modern Traditional

2015 2020

8

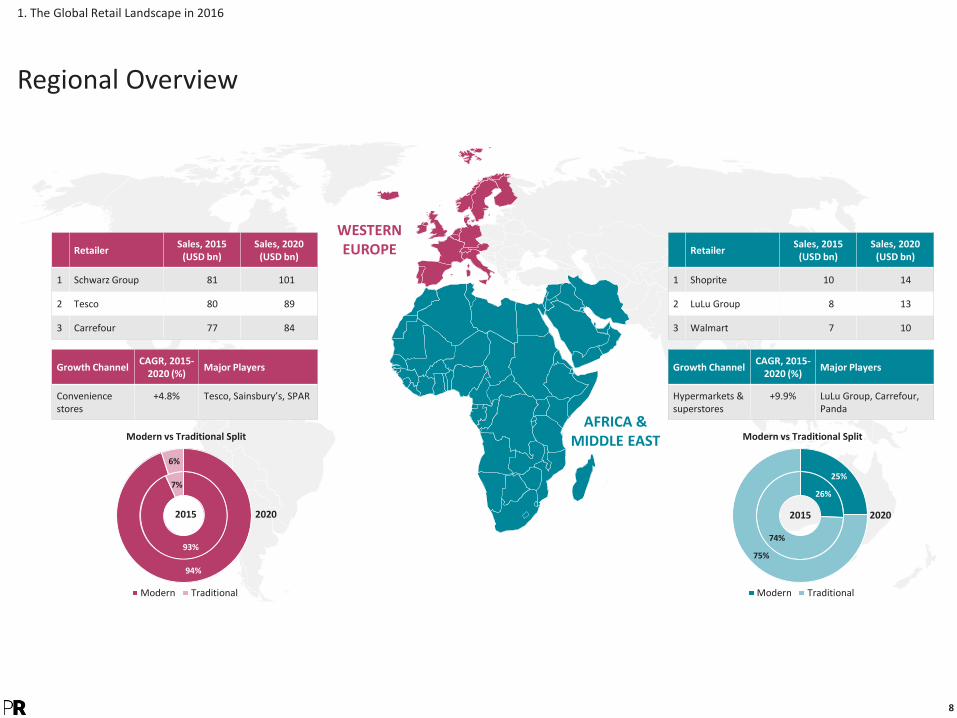

Regional Overview

1. The Global Retail Landscape in 2016

RetailerSales, 2015

(USD bn)Sales, 2020

(USD bn)

1 Schwarz Group 81 101

2 Tesco 80 89

3 Carrefour 77 84

Growth ChannelCAGR, 2015-

2020 (%)Major Players

Conveniencestores

+4.8% Tesco, Sainsbury’s, SPAR

RetailerSales, 2015

(USD bn)Sales, 2020

(USD bn)

1 Shoprite 10 14

2 LuLu Group 8 13

3 Walmart 7 10

Growth ChannelCAGR, 2015-

2020 (%)Major Players

Hypermarkets & superstores

+9.9% LuLu Group, Carrefour,Panda

WESTERN EUROPE

93%

7%

94%

6%

Modern vs Traditional Split

Modern Traditional

2015 2020

26%

74%

25%

75%

Modern vs Traditional Split

Modern Traditional

2015 2020

AFRICA & MIDDLE EAST

9

Rapid development in emerging markets is set to disrupt the evolution of traditional retailing.

Global online sales are set to grow by 108% over the next five years

1. The Global Retail Landscape in 2016

31% of US retailers currently accept payment via a mobile device.

+77%Tech-savvy consumers seeking value. Demand facilitated by sophisticated infrastructure making for advanced logistical capabilities. Seamless shopping experiences expected as the norm.

+84%

Online: Sales Growth by Country, 2015e-2020f (%)

Established but will develop further

Markets set to explode

+128%

+263%

+153%

+74%

+126%

+198%

+407%

Planet Retail expects retail sales in Brazil to grow by c.28% (in real terms) overall in the decade to 2020.

+269%

+176%

A strong AUS dollar has encouraged Australians to spend overseas through online retailer sites.

+113%

+153%

Note: e - estimate; f - forecast.Source: Planet Retail

10

Traditional retail will still dominate, especially in emerging markets.

In 2020, online share of total retail spend in emerging markets will still be low

1. The Global Retail Landscape in 2016

Online: Percentage of Total Retail Sales, 2020f (%)

Established but will develop further

Markets set to explode

Success dependent on innovation across all touchpoints. The US is warming to the concept of collaborative and personalised business models that provide more engaging experiences. Providing sophisticated messaging based on shopping habits across all channels will yield great results.

10.7%Online population reaching saturation point; further growth will come from getting the existing population to spend more. As disposable income of the next generation, who see online shopping as the norm, increases, more spend is likely to be transferred online.

19.3%

10.2%

1.9%7.9%

0.9%

12.2%

17.4%

5.9%

2.3%

7.2%Europe's largest internet population, which is set to grow as its rural populace gains access, driving up online sales. Very fragmented online market with no overall leader. Price and assortment are key influencers of online spend.

14.4%

10.8%Infrastructure improvements, increased internet access in rural areas, rising wealth and appetite for spending. World’s largest internet population and highest internet usage.

Note: f - forecast.Source: Planet Retail

11

The stage of market lifecycle dictates the strategy.

Adopting the right strategy to maximise market potential

1. The Global Retail Landscape in 2016

Emerging markets

• Taking a shortcut to traditional online retail maturity - as online retail grows in parallel to physical retail becoming more organised.

• Consumers are fast adopting the same behavioursas in established retail economies - mobile ownership, embracing internet penetration and shopping online, along with using mobile for shopping and engaging with social media when making purchasing decisions.

• In emerging markets, it is more about providing solutions that help remove barriers to online shopping - such as enhanced payment and logistics systems and overcoming trust/confidence issues. Established but will develop further

Markets set to explode

In emerging markets, leverage domain expertise gained in mature areas of tech development to help implement systems facilitating speedier adoption of sophisticated customer services. These may be click & collect or same-day delivery in Eastern Europe, or developing solutions to better manage the peaks and troughs of internet traffic in fast-growing regions like South-East Asia.

Established markets

• Growth rates vary within these markets and are dependent on the active online buying population.

• A greater focus on linking the store and online experience through omni-channel solutions.

• Success in established markets will rely on innovation across all touchpoints, better insights to provide understanding of the shopper in terms of how, why and when they use different touchpoints, and their expectations of using them.

12

Our Analysts have scoured the globe to highlight the greatest stores over the past 12 months.

Key Stores of 2015 - Whole Foods Market, Georgia, USA

1. The Global Retail Landscape in 2016

The store leverages digital technology to enhance the shopping experience with product demos, recipe how-to’s and product information. Interactive digital displays allow shoppers to engage directly with local suppliers and the community.

Alpharetta, Georgia

USA

While appealing to customers who prioritise freshness and support local producers, the

focus on in-season produce also enables Whole Foods to take cost out of the supply

chain, which has become increasingly important as it invests in price cuts.

13

Key Stores of 2015 - Waitrose, King’s Cross, London, UK

1. The Global Retail Landscape in 2016

Kings Cross, London

UK

Located in a historic Grade 2-listed former train shed and opened in September 2015, the new store juxtaposes Victorian-era charm with a modern, premium, best-in-class supermarket. Key features include a cookery school, and an impressive foodservice offering, including Waitrose’s latest wine bar, as well as personalised loyalty card promotions and customer 5-star rated product displays.

14

Key Stores of 2015 - Carrefour, El Pinar, Madrid, Spain

1. The Global Retail Landscape in 2016

El Pinar, Madrid

Spain

Carrefour El Pinar is often referred to as Carrefour Spain’s ‘connected hypermarket’, incorporating digital terminals and mirrors, as well as the Mi Carrefour mobile phone app. Terminals (such as shown at left) allow shoppers to give the thumbs-up to their favourite private label product, while cardholders are also able to shop instore, then leave their cart at a dedicated corner (right) where their basket will be delivered direct to their home for a fee.

15

Key Stores of 2015 - Amazon Books, Seattle, USA

1. The Global Retail Landscape in 2016

University Village, Seattle

USA

In late 2015, Amazon opened its first physical bookstore called Amazon Books. The store showcases how a pure-play retailer approaches the store with some interesting results. Mimicking the online experience, books are displayed with the covers facing the customer, accompanied with a tag quoting an Amazon review. The range of 5,000-6,000 titles is curated through the power of data, with Amazon basing the range on customer ratings and pre-orders on Amazon.com.

The reasoning behind Amazon’s latest venture is down to the fact consumers see and shop the brand, not the channel. A physical presence for any online player is about customer acquisition, brand building and catering for how consumers engage, interact and shop their favourite brands.

All images © Amazon

16

Shoppers driving global change

An interconnected world means multiple touchpoints of engagement for retailers and brands.

2. A Changing Shopper

TECHNOLOGICAL

POLITICAL ECONOMIC

SOCIAL

Regulations

Wearabletech

Urbanisation

Risingsmartphoneownership

Local

Multi-channel

Ageingpopulation

Slow realGDP in core

markets

Personalhealth

tracking

Growth ofdiscounters

Rising costof primaryhealthcare

Strongdollar

Fluctuatingenergy / fuel

costs

Singleperson

households

Social media peer

recommendations

Range

Connected experiences

Convenience Trust

Health &Wellness

Value

Personalisation

17

Snapshot of the global consumer

2. A Changing Shopper

Shopper trends being accelerated by the greater availability and advances in technology.

Globally, by 2014 more than half (54%) of the world’s population lived in urban areas. In 1950, 30% was urban and, by 2050, 66% of the world’s population is projected to be urban. By 2015, 33 million lived in Chongqing in China - equivalent to the combined populations of the Netherlands, Belgium and Ireland.

Source: UN; Planet Retail City Data

According to the UN, the proportion of persons aged 60 and over will double between 2007 and 2050, while their actual number will more than triple, reaching 2 billion by 2050.

Source: UN

In 2015, more than a quarter of the world's population used a smartphone. By 2018, over half the world’s population will do so. China alone now accounts for over 28% of all smartphone users in the world.

Source: eMarketer

On 24 August 2015, 1 billion people used Facebook in a single day -1 in 7 of the world’s entire population

Source: Facebook

On Singles Day in 2015, Alibaba clocked up sales of USD14.3 billion in a single 24-hour period - more than the annual sales of retailers such as Dia and Toys ‘R’ Us - and enough sales to break into the Top 100 retailer ranking globally in 2015.

Source: Facebook

18

Shoppers are encouraged to choose a retailer if it…

The basic principles of retailing still influence the choice of retailer

2. A Changing Shopper

Is conveniently located

Offers broad range and assortment of products

Offers brands I like

Is a trusted reputable retailer/brand

Allows return of unwanted items purchased online to the store

Rewards me for my spend and loyalty

Appealing promotions instore/online

Offers a loyalty scheme

Has flexible delivery times and options for online purchases

Has convenient collection points to pick up online purchases

Offers an own-branded product that I like

Makes experience relevant to my needs

Accepts alternative payments for purchases

Offers online customer service

63%

62%

61%

59%

58%

58%

57%

55%

52%

49%

46%

45%

41%

39%

Planet Retail’s View

• Shoppers continue to value convenience, choice, big brands and trust above all else. In fact, convenience remains the biggest influencer for consumers in both developed and emerging markets.

• In the excitement of a new shopping era, it is essential that retail fundamentals are not forgotten.

• That said, even the basics are getting complicated, with the name of the game in some - such as loyalty - changing fast. The value equation is continuously evolving, where consumers want the shortest, easiest, most enjoyable route to their purchase.

• This means retailers are striving to satisfy the instant-gratification generation with the provision of speed and convenience.

66%Emerging Markets

55%Developed

Markets

54%Emerging Markets

33%Developed

Markets

61%Emerging Markets

46%Developed

Markets

49%Emerging Markets

33%Developed

Markets

66%Emerging Markets

55%Developed

Markets

69%of consumers prefer

shopping with retailers they

know well

Base: 90,000. Period covered: Aug 2014 to Nov 2015Source: Planet Retail Shopology

19

Mobile is the ultimate shopping companion, binding all touchpoints

2. A Changing Shopper

Planet Retail’s View

• For now, mobile can be defined as a complimentary channel to bricks and mortar, with shoppers predominantly utilising it to enhance the shopping experience and seamlessly blend the best of the physical and digital worlds. It is evident that these devices are now a key part in assisting and guiding shoppers in making purchasing decisions.

• With shoppers seeing and shopping the brand, not the channel or format, mobile is the glue binding the digital and physical experience. Understanding how consumers are using - and want to be using - their mobile on the path-to-purchase is now imperative.

• This will require greater collaboration between retailers, manufacturers and intermediaries to ensure the seamless experience being demanded by shoppers is delivered.

Base: 90,000. Period covered: Aug 2014 to Nov 2015Source: Planet Retail Shopology

• The rise of the smartphone has been a gamechanger, enabling a constantly-connected consumer that can be hyper-targeted at any stage of their purchasing journey with messages relevant to their shopping occasion and mission.

• Being able to engage, interact and influence at any stage of the path-to-purchase is essential - and now possible, thanks to mobile and other connected devices such as tablets.

Top 5 ways shoppers areusing MOBILE for shopping

30% Get more information about a product when out shopping

31% Find the nearest store of a particular retailer

40% Compare prices when out shopping

29% Log into a store’s Wi-Fi

24% Download a retailer’s app

20%found that the

price on the retailer's website didn't match the

price instore.

The impact of technology on customers is significant. Increasingly, they are walking around stores with smartphones, checking the best prices available. Historically, behaviour was driven by reputation that you would build over a period of time. Nowadays, it's driven by truth.

David CheesewrightPresident & CEO, Walmart International

16%had a good

experience using a retailer's free

Wi-Fi when in-store

33%of shoppers’ retailer choice

is influenced by having a website designed specifically for use on mobile phone and

tablet computers

20

Impact on the channel landscape

2. A Changing Shopper

Shopper TrendHypermarkets& superstores

Supermarkets & neighbourhood

stores

Discount stores

Convenience & forecourt

stores

Drugstores & pharmacies

Warehouse clubs and cash

& carriesE-commerce

Health & wellness

Ageing populations

Internet/smartphonepenetration

Localisation andprovenance

Personalisation

Promiscuity

Urbanisation

Negative Medium Positive

Impact

21

Online

Global: Channel Sizes by Banner Sales, 2010e-2020f

Hypermarkets& Superstores

Supermarkets & Neighbourhood

Stores

Discount Stores

Drugstores, Pharmacies & Perfumeries

Convenience& Forecourt

Stores

Cash & carries, Warehouse

Clubs

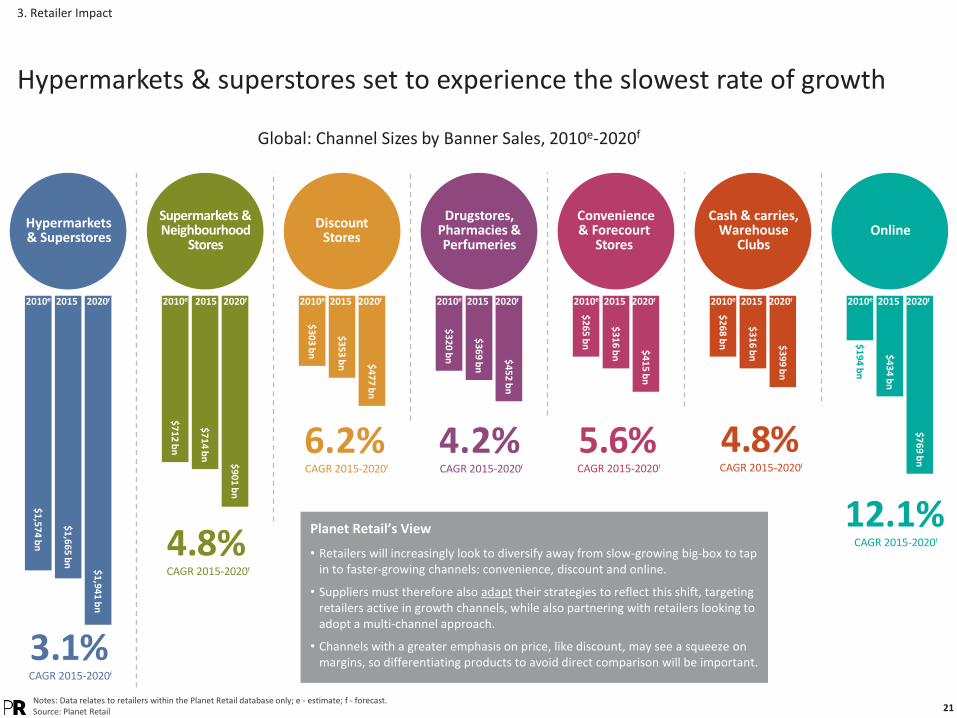

3. Retailer Impact

Hypermarkets & superstores set to experience the slowest rate of growth

$3

20

bn

$3

69

bn

$4

52

bn

$2

68

bn

$3

16

bn

$3

99

bn

$1

94

bn

$4

34

bn

$7

69

bn

2010e 2015 2020f

$1

,94

1b

n

$1

,66

5b

n

$1

,57

4b

n

2010e 2015 2020f

$7

12

bn

$7

14

bn

$9

01

bn

2010e 2015 2020f

$3

03

bn

$3

53

bn $4

77

bn

2010e 2015 2020f 2010e 2015 2020f

$2

65

bn

$3

16

bn

$4

15

bn

2010e 2015 2020f 2010e 2015 2020f

Planet Retail’s View

• Retailers will increasingly look to diversify away from slow-growing big-box to tap in to faster-growing channels: convenience, discount and online.

• Suppliers must therefore also adapt their strategies to reflect this shift, targeting retailers active in growth channels, while also partnering with retailers looking to adopt a multi-channel approach.

• Channels with a greater emphasis on price, like discount, may see a squeeze on margins, so differentiating products to avoid direct comparison will be important.

Notes: Data relates to retailers within the Planet Retail database only; e - estimate; f - forecast.Source: Planet Retail

3.1%CAGR 2015-2020f

4.8%CAGR 2015-2020f

6.2%CAGR 2015-2020f

4.2%CAGR 2015-2020f

5.6%CAGR 2015-2020f

4.8%CAGR 2015-2020f

12.1%CAGR 2015-2020f

22

Global grocers are investing in smaller store formats, while scaling back big-box opening plans.

Global retailers decreasing dependence on hypermarkets

3. Retailer Impact

Channel Evolution of Leading Grocers, 2010e-2020f (%)

75.8

82.62010e

2020f

53.5

55.92010e

2020f

63.8

77.62010e

2020f

Hypermarkets & Superstores

Convenience & Forecourt

stores

Discount stores

Cash & Carries & Wholesale

Clubs

Supermarkets & Neighbourhood

stores

E-commerce Other

Notes: e - estimate; f - forecast.Source: Planet Retail

I see it as a shift in what customers want or need, and it’s our job to respond. What I do see as a challenge is that whilst the customer was heading in one direction the industry was heading in the other.

Dave LewisCEO, Tesco

Retail history is very clear. Those that are unwilling or unable to change go away.

Doug McMillonCEO, Walmart

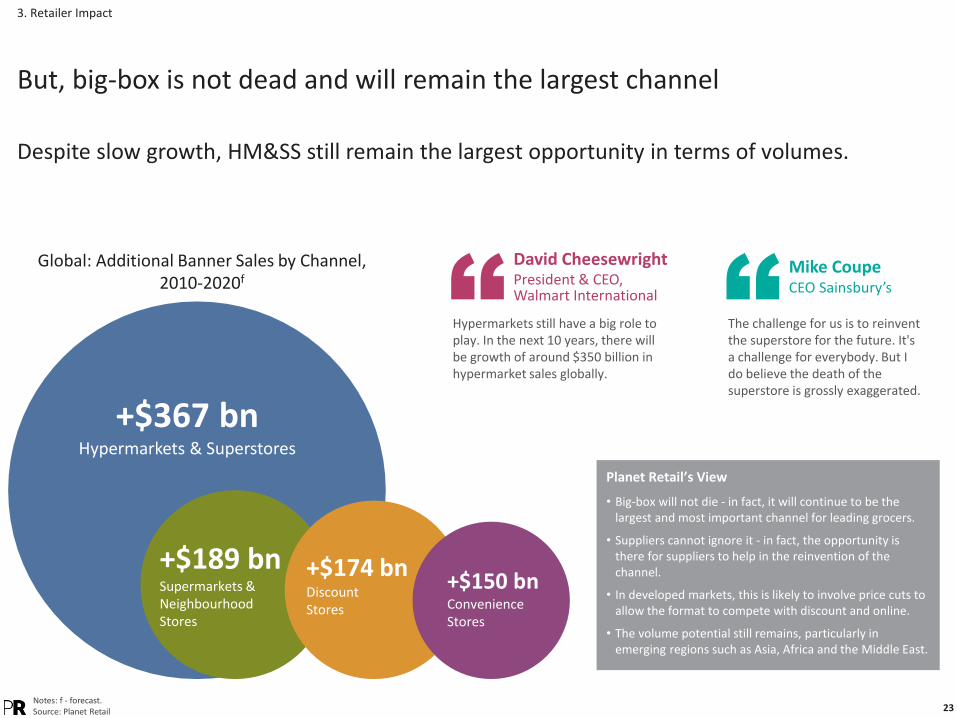

23

But, big-box is not dead and will remain the largest channel

Global: Additional Banner Sales by Channel,2010-2020f

Despite slow growth, HM&SS still remain the largest opportunity in terms of volumes.

3. Retailer Impact

Planet Retail’s View

• Big-box will not die - in fact, it will continue to be the largest and most important channel for leading grocers.

• Suppliers cannot ignore it - in fact, the opportunity is there for suppliers to help in the reinvention of the channel.

• In developed markets, this is likely to involve price cuts to allow the format to compete with discount and online.

• The volume potential still remains, particularly in emerging regions such as Asia, Africa and the Middle East.

Hypermarkets still have a big role to play. In the next 10 years, there will be growth of around $350 billion in hypermarket sales globally.

David CheesewrightPresident & CEO, Walmart International

The challenge for us is to reinvent the superstore for the future. It's a challenge for everybody. But I do believe the death of the superstore is grossly exaggerated.

Mike CoupeCEO Sainsbury’s

+$367 bnHypermarkets & Superstores

+$189 bnSupermarkets &Neighbourhood Stores

+$174 bnDiscount Stores

+$150 bnConvenienceStores

Notes: f - forecast.Source: Planet Retail

24

Global: Top 10 Retailer Ranking, 2015 Global: Top 10 Retailer Ranking, 2020f

Notes: f - forecast; * = assumes Walgreens Boots Alliance plus Rite Aid acquisition.Source: Planet Retail

Global ranking: two new players set to break into the Top 3 by 2020

Discounters Schwarz Group and Aldi are also gaining ground, while those players reliant on their hypermarket & superstore networks are set to slip down the ranking.

3. Retailer Impact

WBA acquisition of Rite Aid unites the first and third-largest drugstore players in the US and creates a new #3 globally.

Schwarz Group becomes seventh-largest global player by 2020, boosted by existing store growth and expansion in existing markets as well as new market entries (e.g. USA).

Tesco is set to be major loser, falling from sixth to 10th place following disposals and stagnant growth in the UK.

Ranking, 2015Banner Sales,

(USD bn)No. of

Outlets

1 Walmart 517 11,713

2 Costco 121 687

3 Carrefour 119 13,222

4 Kroger 116 3,750

5 Amazon 114 --

6 Tesco 105 7,980

7 Seven & I 105 38,647

8 Walgreens Boots Alliance 105 13,565

9 Schwarz Group 103 11,555

10 Aldi 90 10,655

Change Ranking, 2020f Banner Sales,(USD bn)

No. of Outlets

-- 1 Walmart 602 13,345

▲ 2 Amazon 211 ?

▲ 3 Walgreens Boots Alliance* 156 18,750

▼ 4 Costco 153 782

▼ 5 Carrefour 146 16,547

▼ 6 Kroger 140 3,755

▲ 7 Schwarz Group 135 13,216

▼ 8 Seven & I 133 47,652

▲ 9 Aldi 115 12,083

▼ 10 Tesco 108 7,335

25

Leading players continue to push internationalisation

3. Retailer Impact

Retailers looking to reduce dependence on home markets, while limiting risk and investment.

Planet Retail’s View

• Despite a renewed focus on solving problems at home, international markets are becoming increasingly important contributors to leading retailers’ sales.

• This will increasingly mean they look to expand into new markets over the next five years, with particular focus on regions such as the Middle East and Africa.

• Increasing flexibility to overseas expansion will see retailers look to shift away from big-box stores towards smaller store concepts, online partnerships and joint ventures with local players.

• FMCG suppliers are well-advised not to be idle and not to rely on Western hypermarket giants to lead them into emerging markets. Opportunities are present with fast-growing local players as well as in traditional trade.

Major global players, such as Costco, Woolworths (above) and Sainsbury's, have attempted to tap into the enthusiasm for foreign - particularly premium - brands among Chinese shoppers by offering private labels on Alibaba’s Tmall platform. Such an approach is an effective and inexpensive way to test the Chinese waters.

Top 10 Global Grocers: Average Number of Markets, 2010-2020f

15.0

2010e

16.4

2012e

16.5

2014e

17.2

2020f

Top 10 Global Grocers: Share of Banner Sales from International Operations, 2010e-2020f (%)

33.0%

2010e

34.0%

2012e

35.3%

2014e

38.5%

2020f

Notes: e - estimate; f - forecast.Source: Planet Retail

26

The fastest-growing players are regional and local players in emerging markets

3. Retailer Impact

USD9 billion additional sales by 2020 (doubling in size).

Store expansion: planning over 500 new stores annually.

Focus on growth channel: Discount.

International: presence in Morocco and Egypt.

BIM (Turkey)

Magnit (Russia)

USD22 billion additional sales by 2020 (doubling in size).

Set to be Central & Eastern Europe’s largest grocery retailer by 2019, overtaking Metro Group.

Store expansion: planning over 2,000 new stores annually.

Diversifying: Into new regions and channels, such as drugstores.

Planet Retail’s View

• Identifying and partnering with local growth champions represents significant opportunity for next 5 years and beyond.

• Often, these are small-box specialists, putting them in a strong position to serve a burgeoning consumer base in expanding urban and provincial regions.

• Ten years from now, the global grocery Top 10 might well include names from Russia, China or India.

Notes: f - forecast; Calculated in local currency.Source: Planet Retail

19.118.2

17.6

13.3

7.8

0

5

10

15

20

BIM Magnit Indomaret Saigon Co-op OXXO

5 Players to Watch: Sales Growth Forecast (CAGR), 2015-2020f (%)

27

What makes a growth winner?

3. Retailer Impact

Global/Regional Players

• Strong, or growing focus, on growth channelsSmall stores (Convenience, drugstores)E-commerce

• Growing international presenceSupported by strong/stable domestic operations

• Focus on small number of formats/bannersSimpler operations, clear management focus, clear customer proposition

Local Players

• Situated in growth market

• Focus on small store operationsConvenience, discount, supermarkets & neighbourhood stores

• Rapid expansion.

• Clear focus on core operations/banner, but desire and ability to diversify into new channels.

Some common characteristics:

28

Constantly-connected consumers

The store reinvented

Evolution of marketing & loyalty

Personalised & contextualised

experiencesThe on-demand

economyHealth & Wellness

authorities

Safety in numbers

Demise of discount?

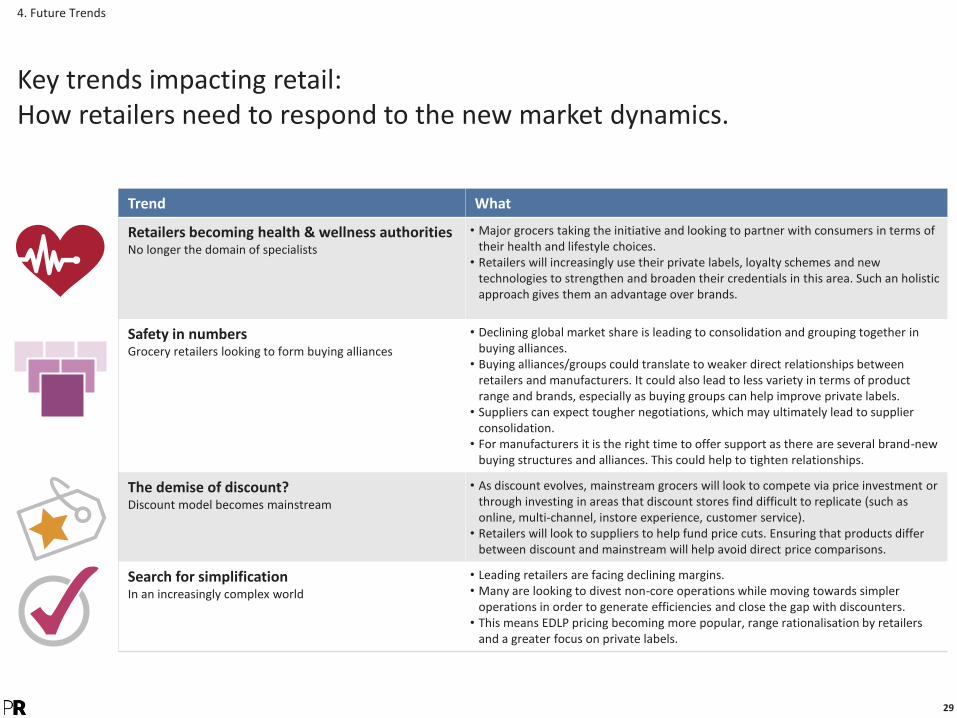

Search for simplification

29

Key trends impacting retail: How retailers need to respond to the new market dynamics.

4. Future Trends

Trend What

Retailers becoming health & wellness authoritiesNo longer the domain of specialists

• Major grocers taking the initiative and looking to partner with consumers in terms of their health and lifestyle choices.• Retailers will increasingly use their private labels, loyalty schemes and new

technologies to strengthen and broaden their credentials in this area. Such an holistic approach gives them an advantage over brands.

Safety in numbersGrocery retailers looking to form buying alliances

• Declining global market share is leading to consolidation and grouping together in buying alliances.• Buying alliances/groups could translate to weaker direct relationships between

retailers and manufacturers. It could also lead to less variety in terms of product range and brands, especially as buying groups can help improve private labels.• Suppliers can expect tougher negotiations, which may ultimately lead to supplier

consolidation. • For manufacturers it is the right time to offer support as there are several brand-new

buying structures and alliances. This could help to tighten relationships.

The demise of discount?Discount model becomes mainstream

• As discount evolves, mainstream grocers will look to compete via price investment or through investing in areas that discount stores find difficult to replicate (such as online, multi-channel, instore experience, customer service).• Retailers will look to suppliers to help fund price cuts. Ensuring that products differ

between discount and mainstream will help avoid direct price comparisons.

Search for simplificationIn an increasingly complex world

• Leading retailers are facing declining margins. • Many are looking to divest non-core operations while moving towards simpler

operations in order to generate efficiencies and close the gap with discounters. • This means EDLP pricing becoming more popular, range rationalisation by retailers

and a greater focus on private labels.

30

Key trends impacting retail: How retailers need to respond to the new market dynamics.

4. Future Trends

Trend What

Constantly-connected consumersRetailing is no longer about a location or a channel

• Consumers are always on their mobiles, and increasingly willing and able to use these during the path-to-purchase. • They demand constant connectivity with retailers. Smart operators are those finding

ways to accommodate these valuable shoppers. • By implementing solutions around how consumers use technology they already have,

retailers will be able to create brand advocates and drive sales across all channels.

The store reinventedCreating engaging experiences

• The future of stores hinges on their ability to serve customers across all channels. However, simply filling them with technology like interactive kiosks isn’t necessarily the right solution. • Retailers need to understand what technology will work best for customers and

where it needs to be placed.

Evolution of marketing & loyaltyLoyalty has to be personalised and engaging

• There has been a fundamental shift in retailer-consumer interaction. Retailers need to engage in two-way conversations across multiple channels, while earning, not acquiring, the loyalty and respect of the consumer.

Personalised & contextualised experiencesUsing digital marketing to delight shoppers

• The demand for more relevant, tailored shopping experiences is on the rise and is influential in choosing a retailer. • Contextual interaction will enable retailers to hyper-target customers when they’re

most likely to buy, and gather relevant data so the retailer can continuously improve the instore experience. • Retailers will need excellent customer data management to achieve this.

The on-demand economyCatering for instant gratification

• Convenience and speed are differentiators. Fulfilment speed and reliability is no longer enough. • Providing choice and flexibility will be hugely influential in consumer retailer choice. • Convenience is being redefined and simplified thanks to auto-replenishment.

31

• Health & wellness is no longer solely the domain of the specialists:

Channel blurring is accelerating as supermarkets, drugstores, discounters, warehouse clubs and even convenience stores all chase the fast-growing category.

Warehouse club operator Costco was able to deliver sales of organic lines of USD4 billion in FY2015, up from USD3 billion in FY2014.

In the US, supermarkets and mass retailers are opening instore clinics to meet consumer demand for quick-service and low-cost diagnosis and treatment of common ailments amid a shortage of primary-care physicians and rising healthcare premiums.

• Increased scrutiny from governments in areas like sugar and ‘obesity taxes’ could result in accelerated pre-emptive responses from retailers.

Retailers like Tesco and Lidl in the UK have already removed confectionery from their checkouts, to be replaced by healthy impulse items.

Retailers are becoming health & wellness authorities

4. Future Trends

This Delhaize-owned Mega-Image store in Romania recently launched a new instore concept, Equilibrium Health & Wellness, where its healthy living assortment is merchandised across categories. © Delhaize.

Retailers, such as Tesco in the UK, have taken pre-emptive action and removed confectionery from their checkouts.

32

Going forward, expect to see more:

• Co-ordinated private label ranges - retailers looking to differentiate against rivals, build trust and loyalty and widen appeal through more affordable ranges.

• Dedicated areas set aside within stores - dedicated health areas can be used to utilise excess space in larger stores and act as destinations in their own right.

• New, health-focused store concepts - retailers may even look to launch their own niche formats, such as LAWSON’s Natural LAWSON in Japan or AEON’s G.G. outlets, that focus on senior customers aged 55+.

• Partnering with consumers - consumers are willing to be assisted in their healthier lifestyles and choices. Retailers, with their holistic customer-facing operations and loyalty card data are much better placed to do this than brands.

Taking health & wellness to the next level

4. Future Trends

Planet Retail’s View

• Retailers will actively look to promote themselves as health & wellness authorities in order to build trust and loyalty - this will be a new battleground of the future.

• Expect growing focus on bringing health & wellness into new physical channels (like convenience stores) and online as well as retailers developing their own apps and schemes to influence and reward healthy behaviour.

• Opportunity for manufacturers to support retailers through combined promotional activity and new products.

Last October, Walmart launched ‘America’s Biggest Health Fair’ at 4,400 stores nationwide. Offering free blood pressure, blood glucose and vision screenings, the move was as part of a larger effort to brand itself as a health & wellness destination.

Making health affordable is key to growing its accessibility. Retailers are looking to do this through expanding their standard and economy private label ranges. In Japan in late 2014, AEON added a budget-friendly version of its Gurinai organic and eco-friendly private label. Marketed as TopvaluGurinai, the label features 140 items and is available across 4,000 stores in Japan.

Auchan has a dedicated Mieux Vivre (Better Living) online shop for organic and natural products, specifically targeting shoppers with food allergies and intolerances. It allows users to filter products according to their allergies and provides detailed ingredient lists.

33

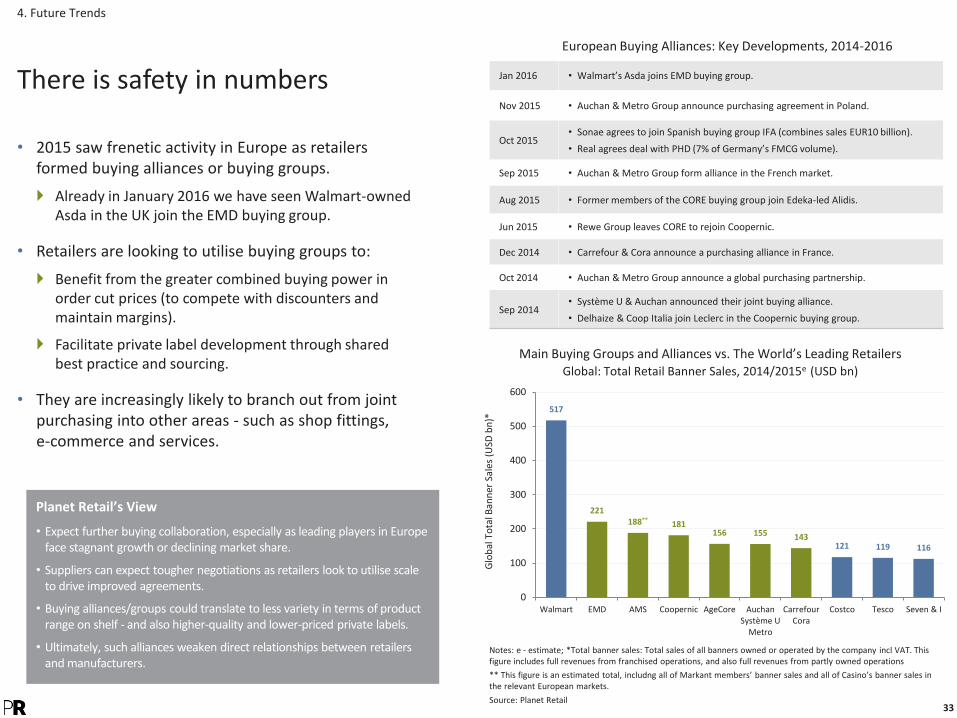

• 2015 saw frenetic activity in Europe as retailers formed buying alliances or buying groups.

Already in January 2016 we have seen Walmart-owned Asda in the UK join the EMD buying group.

• Retailers are looking to utilise buying groups to:

Benefit from the greater combined buying power in order cut prices (to compete with discounters and maintain margins).

Facilitate private label development through shared best practice and sourcing.

• They are increasingly likely to branch out from joint purchasing into other areas - such as shop fittings, e-commerce and services.

4. Future Trends

There is safety in numbers

517

221188**

181156 155 143

121 119 116

0

100

200

300

400

500

600

Walmart EMD AMS Coopernic AgeCore AuchanSystème U

Metro

CarrefourCora

Costco Tesco Seven & I

Glo

bal

To

tal B

ann

er S

ales

(U

SD b

n)*

Main Buying Groups and Alliances vs. The World’s Leading RetailersGlobal: Total Retail Banner Sales, 2014/2015e (USD bn)

Planet Retail’s View

• Expect further buying collaboration, especially as leading players in Europe face stagnant growth or declining market share.

• Suppliers can expect tougher negotiations as retailers look to utilise scale to drive improved agreements.

• Buying alliances/groups could translate to less variety in terms of product range on shelf - and also higher-quality and lower-priced private labels.

• Ultimately, such alliances weaken direct relationships between retailers and manufacturers.

Jan 2016 • Walmart’s Asda joins EMD buying group.

Nov 2015 • Auchan & Metro Group announce purchasing agreement in Poland.

Oct 2015• Sonae agrees to join Spanish buying group IFA (combines sales EUR10 billion).

• Real agrees deal with PHD (7% of Germany’s FMCG volume).

Sep 2015 • Auchan & Metro Group form alliance in the French market.

Aug 2015 • Former members of the CORE buying group join Edeka-led Alidis.

Jun 2015 • Rewe Group leaves CORE to rejoin Coopernic.

Dec 2014 • Carrefour & Cora announce a purchasing alliance in France.

Oct 2014 • Auchan & Metro Group announce a global purchasing partnership.

Sep 2014• Système U & Auchan announced their joint buying alliance.

• Delhaize & Coop Italia join Leclerc in the Coopernic buying group.

European Buying Alliances: Key Developments, 2014-2016

Notes: e - estimate; *Total banner sales: Total sales of all banners owned or operated by the company incl VAT. This figure includes full revenues from franchised operations, and also full revenues from partly owned operations

** This figure is an estimated total, includng all of Markant members’ banner sales and all of Casino’s banner sales in the relevant European markets.

Source: Planet Retail

34

• The discount model has become increasingly mainstream, with upscaling of store concepts, product ranges and services.

Aldi and Lidl are both experimenting with e-commerce operations in markets such as the Netherlands, UK and Germany.

• This will increasingly mean discounters are looking to bigger stores and larger product ranges.

The average size of a Lidl in Europe has increased from less than 700 sq m in 2000 to over 950 sq m in 2015 - an increase of 40%.

Increasing complexity of discount operations might be a challenge, and potentially open the door to rivals.

4. Future Trends

The demise of discount?

In November 2015, Lidl acquired Kochzauber, a grocery delivery service, in Germany (pictured above). This follows the announcement in September that Aldi is to offer wine and non-food in the UK market in 2016 (it already sells wine online in Australia).

The ‘Lidl of the Future’ store concept (above & below), which features customer toilets, higher staff levels, self-checkouts, an expanded product range and more upmarket feel, is to be rolled out across a number of markets from 2016 after its launch in 2015.

Planet Retail’s View

• It will become increasingly difficult to distinguish between discount operators and mainstream grocers as both sides introduce elements taken from the other.

• Larger product ranges (and tentative steps online) will lead to greater opportunities for brands and manufacturers to partner with discount players, especially in premium, local, ethical and health categories.

• There is a risk that rising complexity of discounters could open up room for new ‘no frills’ discounters to enter the market below them -effectively beating them at their own game.

We have to leave hard discounting behind… Lidl needs to become the supermarket of the middle classes and the affluent.

Friedrich FuchsMD, Lidl France

Those (hard discount) times are over. We are now a supermarket.

Ronny GottschlichMD, Lidl UK

35

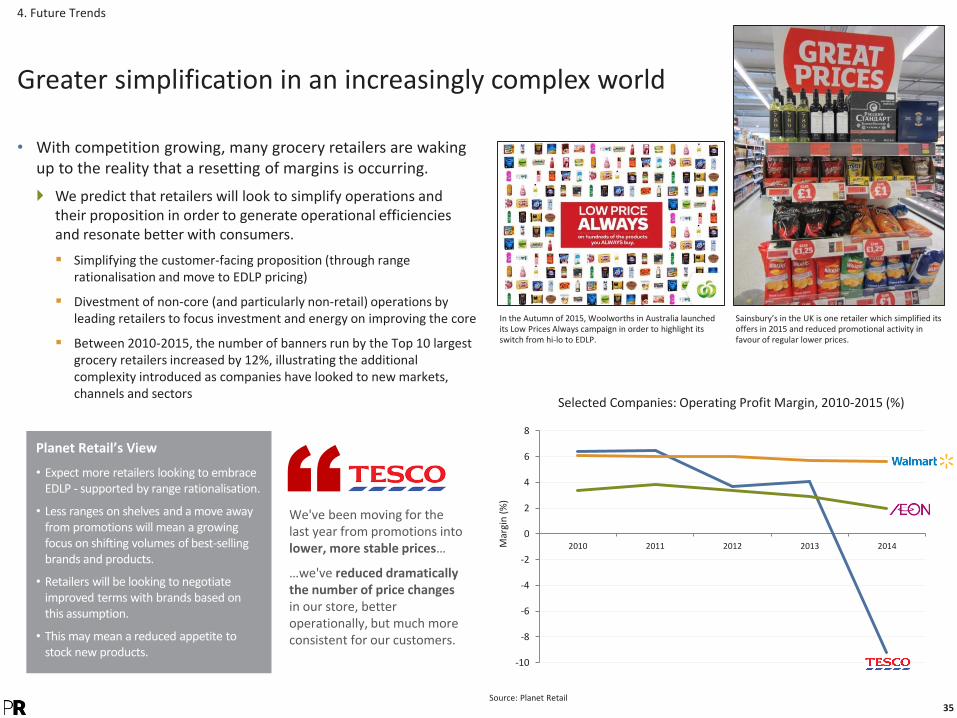

• With competition growing, many grocery retailers are waking up to the reality that a resetting of margins is occurring.

We predict that retailers will look to simplify operations and their proposition in order to generate operational efficiencies and resonate better with consumers.

Simplifying the customer-facing proposition (through range rationalisation and move to EDLP pricing)

Divestment of non-core (and particularly non-retail) operations by leading retailers to focus investment and energy on improving the core

Between 2010-2015, the number of banners run by the Top 10 largest grocery retailers increased by 12%, illustrating the additional complexity introduced as companies have looked to new markets, channels and sectors

4. Future Trends

Greater simplification in an increasingly complex world

Sainsbury’s in the UK is one retailer which simplified its offers in 2015 and reduced promotional activity in favour of regular lower prices.

In the Autumn of 2015, Woolworths in Australia launched its Low Prices Always campaign in order to highlight its switch from hi-lo to EDLP.

Planet Retail’s View

• Expect more retailers looking to embrace EDLP - supported by range rationalisation.

• Less ranges on shelves and a move away from promotions will mean a growing focus on shifting volumes of best-selling brands and products.

• Retailers will be looking to negotiate improved terms with brands based on this assumption.

• This may mean a reduced appetite to stock new products.

-10

-8

-6

-4

-2

0

2

4

6

8

2010 2011 2012 2013 2014Mar

gin

(%

)

Selected Companies: Operating Profit Margin, 2010-2015 (%)

Source: Planet Retail

We've been moving for the last year from promotions into lower, more stable prices…

…we've reduced dramatically the number of price changesin our store, better operationally, but much more consistent for our customers.

36

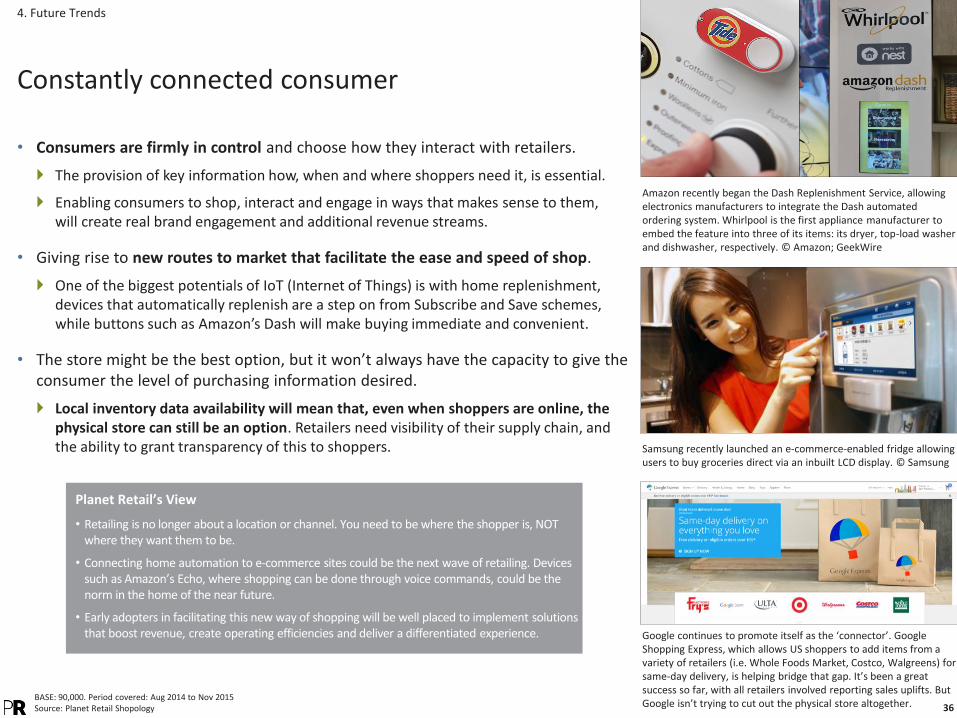

• Consumers are firmly in control and choose how they interact with retailers.

The provision of key information how, when and where shoppers need it, is essential.

Enabling consumers to shop, interact and engage in ways that makes sense to them, will create real brand engagement and additional revenue streams.

• Giving rise to new routes to market that facilitate the ease and speed of shop.

One of the biggest potentials of IoT (Internet of Things) is with home replenishment, devices that automatically replenish are a step on from Subscribe and Save schemes, while buttons such as Amazon’s Dash will make buying immediate and convenient.

• The store might be the best option, but it won’t always have the capacity to give the consumer the level of purchasing information desired.

Local inventory data availability will mean that, even when shoppers are online, the physical store can still be an option. Retailers need visibility of their supply chain, and the ability to grant transparency of this to shoppers.

Constantly connected consumer

4. Future Trends

Planet Retail’s View

• Retailing is no longer about a location or channel. You need to be where the shopper is, NOT where they want them to be.

• Connecting home automation to e-commerce sites could be the next wave of retailing. Devices such as Amazon’s Echo, where shopping can be done through voice commands, could be the norm in the home of the near future.

• Early adopters in facilitating this new way of shopping will be well placed to implement solutions that boost revenue, create operating efficiencies and deliver a differentiated experience.

Amazon recently began the Dash Replenishment Service, allowing electronics manufacturers to integrate the Dash automated ordering system. Whirlpool is the first appliance manufacturer to embed the feature into three of its items: its dryer, top-load washer and dishwasher, respectively. © Amazon; GeekWire

Samsung recently launched an e-commerce-enabled fridge allowing users to buy groceries direct via an inbuilt LCD display. © Samsung

Google continues to promote itself as the ‘connector’. Google Shopping Express, which allows US shoppers to add items from a variety of retailers (i.e. Whole Foods Market, Costco, Walgreens) for same-day delivery, is helping bridge that gap. It’s been a great success so far, with all retailers involved reporting sales uplifts. But Google isn’t trying to cut out the physical store altogether.

BASE: 90,000. Period covered: Aug 2014 to Nov 2015Source: Planet Retail Shopology

37

The store reinvented

4. Future Trends

• Store sales are increasingly influenced by digital.

Deploying technology that meets a need or solves a pain point is the answer.

• As their role changes, retailers are looking to make stores more relevant.

Enabling shoppers to commence their journey in one channel and complete it in another through seamless, convenient and fast facilities will become essential.

• Consumers are bringing the digital world into stores.

Building solutions that accommodate this will be a cost-effective way of future-proofing the store.

Developing solutions that link shoppers’ devices to instore technology will provide information-rich content tailored to their needs, while digitising the store.

• Instore solutions that increase the speed and ease of shop will be well received by shoppers.

Converging existing platforms and systems with mobile app and digital wallets has the potential to create an entirely self-service instore shopping experience.

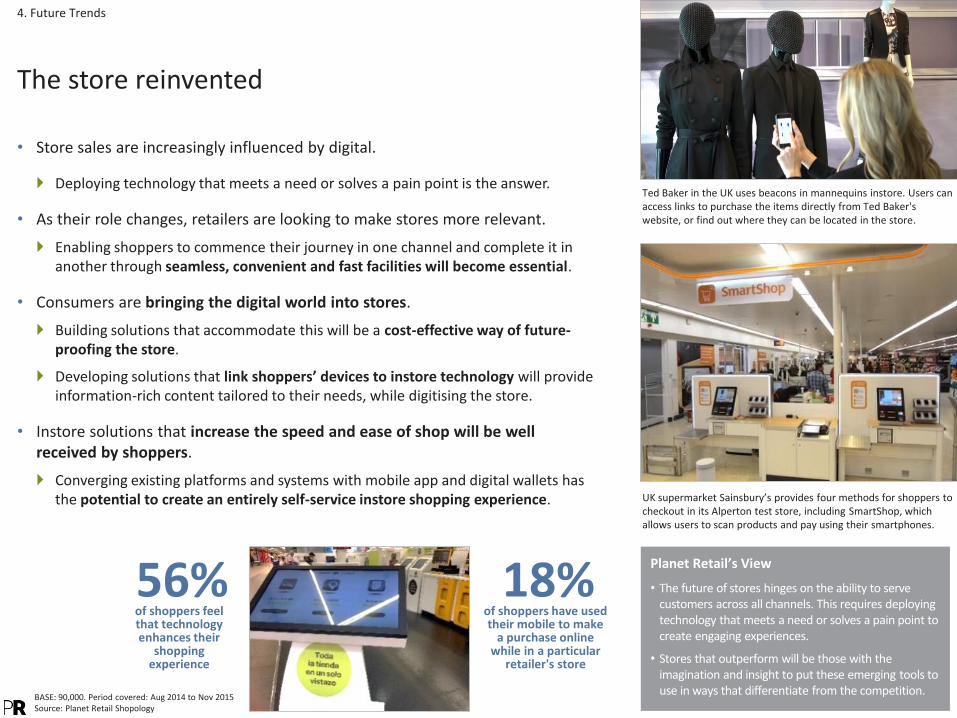

Ted Baker in the UK uses beacons in mannequins instore. Users can access links to purchase the items directly from Ted Baker's website, or find out where they can be located in the store.

UK supermarket Sainsbury’s provides four methods for shoppers to checkout in its Alperton test store, including SmartShop, which allows users to scan products and pay using their smartphones.

Planet Retail’s View

• The future of stores hinges on the ability to serve customers across all channels. This requires deploying technology that meets a need or solves a pain point to create engaging experiences.

• Stores that outperform will be those with the imagination and insight to put these emerging tools to use in ways that differentiate from the competition.

56%of shoppers feel that technology enhances their

shopping experience

18%of shoppers have used their mobile to make

a purchase online while in a particular

retailer's store

BASE: 90,000. Period covered: Aug 2014 to Nov 2015Source: Planet Retail Shopology

38

Creating engaging experiences

4. Future Trends

• Creating retail experiences is becoming essential.

More experiential stores and retailer partnerships with focus on experiences.

• To establish true destination stores, retailers are creating omni-channel experiences.

Often based around key seasonal events, these initiatives are set to increase, given that shoppers’ spending decisions are influenced by a variety of media and touchpoints.

• Hospitality and entertainment is fundamental to re-energising the store.

Equipping staff with the tools of their digital age, so they are able to effectively deal with the digital shopper, will resonate.

• As channels blur, we’re likely to see greater collaboration between retailers as they look to maximise store revenues and profitability.

With consumers now shopping the brand not the channel, we’re likely to see more collaboration between pure-play and traditional retailers.

Enables customer acquisition and a physical presence for the pure-play, while boosting destination appeal for traditional retailer.

Specialist tea retailer T2tea, with stores in Australia, New Zealand, the UK and US, focuses on creating exceptional instore experiences.

Partnerships such as Argos and Sainsbury’s are likelyto be replicated.

Others are set to follow the likes of online beauty retailer BirchBox - which has concessions in Selfridges in the UK and Nordstrom in the US.

43%of shoppers agree

that store associates are useful in helping them decide what

to buy

34%of shoppers’ retailer of choice is influenced by

a compelling instore environment

(e.g. inspirational displays, technology linking to

retailer’s website)

Planet Retail’s View

• Stores providing a compelling environment, with excellent customer service and linkages to the digital world, will outperform.

• The store will evolve from a hub of products into a distinctive experience that helps the consumer be more connected to the brand and its values.

BASE: 90,000. Period covered: Aug 2014 to Nov 2015Source: Planet Retail Shopology

39

Evolution of marketing & loyalty

4. Future Trends

• Selling the experience. Making customers feel valued, special and integral to the brand’s success is all-important.

• Shoppers are paying more attention to their peers when making purchasing decisions.

It is critical to encourage spend and nurture advocacy through engaging in honest, relevant and personalised conversations at every touchpoint.

Social messaging apps are set to become a way to engage customers with targeted products and offers.

Social media will evolve into a purchase channel. Facebook, Twitter and Pinterest all now have a buy button. With brands needing to be where the customer is looking to buy, investment in social commerce and partnerships with social selling tools - such as LiketoBuy and Soldsie - are set to rise.

• The rules of the loyalty game have changed.

Schemes have evolved from generic notices to highly targeted, relevant and personalised messaging.

• Moving forward, rewards-based loyalty schemes are likely to have far greater impact.

Blending content and commerce makes customers feel valued and integral to the brand’s success.

Apps help blend the brand with the customer’s technology to make their life easier.

BASE: 90,000. Period covered: Aug 2014 to Nov 2015Source: Planet Retail Shopology

Walgreens Balance Rewards programme is now integrating fitness activity information from devices like Fitbit and feeds into its programme enabling Walgreen’s to analyse buying patterns and offer better promotions.

With Like2Buy, Instagram isn’t just a feed of images, it’s a gallery of products, available for purchase.

Planet Retail’s View

• This is now possible thanks to better use of Big Data, social media, instore technology and the ability to track consumers as they progress through their purchasing journey. Retailers will need to gain greater expertise in converging technology, marketing and merchandising. Ensuring seamless experiences while deriving meaningful insight from all the various intersection methods - stores, e-commerce, mobile, social, instore technology, even wearables - is a key challenge moving forward.

Marks & Spencer’s Sparks ‘member’ scheme continues a trend for loyalty schemes to offer real instant benefits rather than accumulated points. Members benefit from priority access to sales, events and are rewarded for charitable donations.

39%of shoppers feel that

social media is important in helping decide what to buy

58%of shoppers’ retailer of choice is influenced by

being rewarded for their spend and loyalty

40

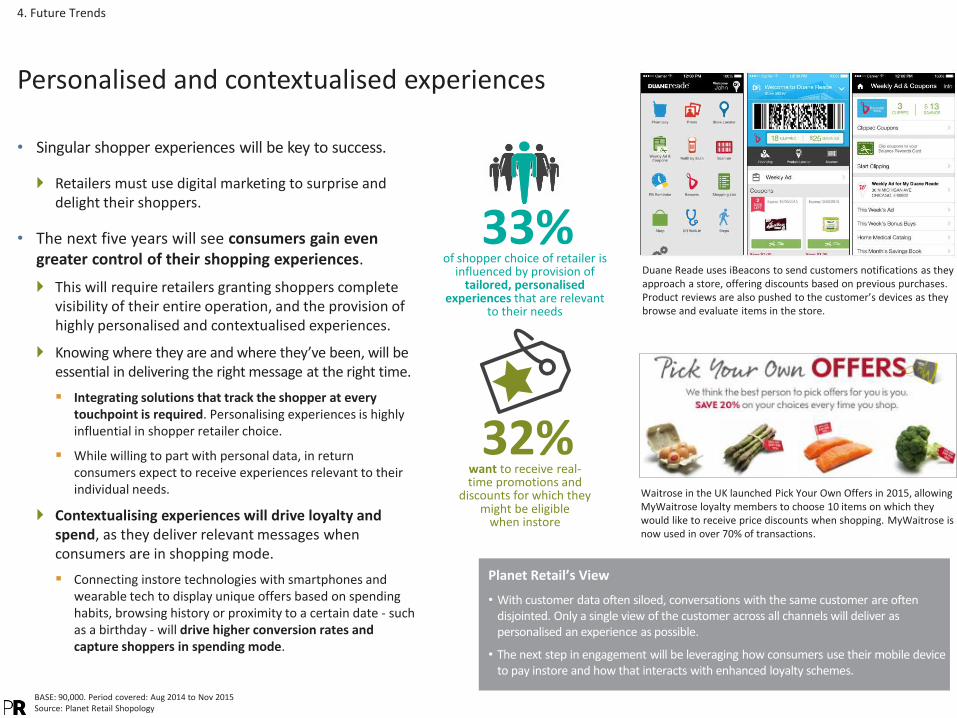

Duane Reade uses iBeacons to send customers notifications as they approach a store, offering discounts based on previous purchases. Product reviews are also pushed to the customer’s devices as they browse and evaluate items in the store.

Personalised and contextualised experiences

4. Future Trends

• Singular shopper experiences will be key to success.

Retailers must use digital marketing to surprise and delight their shoppers.

• The next five years will see consumers gain even greater control of their shopping experiences.

This will require retailers granting shoppers complete visibility of their entire operation, and the provision of highly personalised and contextualised experiences.

Knowing where they are and where they’ve been, will be essential in delivering the right message at the right time.

Integrating solutions that track the shopper at every touchpoint is required. Personalising experiences is highly influential in shopper retailer choice.

While willing to part with personal data, in return consumers expect to receive experiences relevant to their individual needs.

Contextualising experiences will drive loyalty and spend, as they deliver relevant messages when consumers are in shopping mode.

Connecting instore technologies with smartphones and wearable tech to display unique offers based on spending habits, browsing history or proximity to a certain date - such as a birthday - will drive higher conversion rates and capture shoppers in spending mode.

Planet Retail’s View

• With customer data often siloed, conversations with the same customer are often disjointed. Only a single view of the customer across all channels will deliver as personalised an experience as possible.

• The next step in engagement will be leveraging how consumers use their mobile device to pay instore and how that interacts with enhanced loyalty schemes.

BASE: 90,000. Period covered: Aug 2014 to Nov 2015Source: Planet Retail Shopology

Waitrose in the UK launched Pick Your Own Offers in 2015, allowing MyWaitrose loyalty members to choose 10 items on which they would like to receive price discounts when shopping. MyWaitrose is now used in over 70% of transactions.

33%of shopper choice of retailer is

influenced by provision of tailored, personalised

experiences that are relevant to their needs

32%want to receive real-time promotions and

discounts for which they might be eligible

when instore

41

The on-demand economy

4. Future Trends

• Catering for the instant-gratification generation.

Consumers are demanding the shortest, easiest and most enjoyable route to their purchase.

• Retailers need to find ways to make everything simple, frictionless and fast.

Subscribe and save schemes are appealing. Retailers like Target, seeing the potential to gain a loyal customer base, have followed Amazon’s lead in providing such services.

Many will attempt to mimic Amazon Prime.

Retailers and third party platforms like the Alibaba-backed ShopRunner already offer subscription-based shopping as they look to lock in loyalty.

Desire for convenience has made product-specific box schemes popular, especially in highly-standardised categories like beauty.

Jet.com trades off convenience and speed with saving money. This generates new customer streams and a more profitable way to sell online.

More retailer partnerships with likes of Instacart, Curbside, and Shutl are likely in meeting fulfilment expectations without the logistical hassles or cost.

Fulfilment is a differentiator. Speed, flexibility and choice are imperatives. Creating desirable delivery options that don’t erode margin will be a priority.

Planet Retail’s View

• Auto-replenishment, tied with fast, efficient, cost effective fulfilment, will go a long way in winning consumer spend and loyalty.

• These services have the potential to disrupt online and instore purchasing behaviour, especially in household care, petcare and beauty. They have implications for pricing, promotions, packaging sizes and assortment. E-commerce-ready packaging of products will also be needed to avoid damage and high returns rates.

Through Prime, Pantry and Subscribe and Save, Amazon is able to retain the shopper within its ecosystem, creating exceptionally loyal customers whose habits will be hard to alter or influence.

ShopRunner is one of a number of start-ups nibbling away at Amazon. Backed by Alibaba, it is working with the e-commerce giant and its affiliate Alipay to help US retailers access China.

Jet’s customer-centric approach and provision of complete transparency is sure to appeal to value-conscious consumers looking for players that grant them power to control their experience.

59%of shoppers’ retailer

choice is influenced by the ability to return

unwanted items bought online to their

nearest store

52%of shoppers’ retailer

choice is influenced by more flexible delivery

times and options

BASE: 90,000. Period covered: Aug 2014 to Nov 2015Source: Planet Retail Shopology

42

UK

AirW120 Air StreetLondonW1B 5ANUK

T: +44 (0)20 7715 6000E: [email protected]

Germany

Weserstr. 460329 Frankfurt am MainGermany

T: +49 (0) 69 96 21 75-6E: [email protected]

USA

1000 Winter StSuite 3100WalthamMA 02451USA

T: +1 (781) 957-1226E: [email protected]

India

ICC Chambers4th floorSaki Vihar RoadAndheri (E)-Mumbai - 400072 India

T: +852 2996 3157E: [email protected]

Researched and published by Planet Retail Limited

Company No: 3994702 (England & Wales) - Registered Office: c/o Top Right Group Limited, The Prow, 1 Wilder Walk, London W1B 5AP

Terms of use and copyright conditions

Content provided within this documentation which is the Intellectual Property (IP) of Planet Retail is copyrighted. All rights reserved and no part of this publication as it relates to Planet Retail’s IP may be reproduced, stored in a retrieval system or transmitted in any form without the prior permission of the publishers. We have taken every precaution to ensure that details provided in this document are accurate. The publishers are not liable for any omissions, errors or incorrect insertions, nor for any interpretations made from the document.

planetretail.net