Embed Size (px)

Citation preview

Global Transfer Pricing Controversy: Trends and ManagementThomas Borstell

Global Director – Transfer Pricing Services

Global Transfer Pricing Controversy: Trends and ManagementPage 2

IRS Circular 230 disclosure

Any US tax advice contained herein was not intended or written to be used, and cannot be used, for the purpose of avoiding penalties that may be imposed under the Internal Revenue Code or applicable state or local tax law provisions

These slides are for educational purposes only and are not intended, and should not be relied upon, as accounting advice

Global Transfer Pricing Controversy: Trends and ManagementPage 3

► Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young LLP is a client-serving member firm of Ernst & Young Global Limited located in the U.S.

► This presentation is © 2012 Ernst & Young LLP. All rights reserved. No part of this document may be reproduced, transmitted or otherwise distributed in any form or by any means, electronic or mechanical, including by photocopying, facsimile transmission, recording, rekeying, or using any information storage and retrieval system, without written permission from Ernst & Young LLP. Any reproduction, transmission or distribution of this form or any of the material herein is prohibited and is in violation of U.S. and international law. Ernst & Young LLP expressly disclaims any liability in connection with use of this presentation or its contents by any third party.

► Views expressed in this presentation are not necessarily those of Ernst & Young LLP.

Disclaimer

Global Transfer Pricing Controversy: Trends and ManagementPage 4

Agenda

►Transfer pricing controversy trends► Global► Latin America

►Managing controversy risk► 1. Global documentation► 2. Advance Pricing Agreements (APAs)► 3. Operational TP► 4. I/C services

Global Transfer Pricing Controversy: Trends and ManagementPage 5

Transfer pricing controversy trends -Global

Global Transfer Pricing Controversy: Trends and ManagementPage 6

1. Transfer pricing still dominates taxpayers’ agendasEY’s Global 2010 Transfer Pricing Survey: Key findings

► Importance of transfer pricing for MNCs strongly confirmed► Increased enforcement and regulatory activity

►Transfer pricing documentation more important than ever► More globally consistent documentation undertaken► Increase of documentations with audit defense focus

►Controversy focus► Emphasis on intercompany financing and service transactions► Alternative dispute resolution options

►Key areas of audit activity► U.S. and other mature TP jurisdictions head the list► But significant increase in audit activity in China and India

Global Transfer Pricing Controversy: Trends and ManagementPage 7

2. Governments increasing regulatory and audit/enforcement activity►Pressure on budgets leads to increased regulatory and

audit/enforcement activity► Various countries have announced hire of substantial numbers of

new transfer pricing auditors

► Reports of rigorous approaches in transfer pricing audits

► More government-to-government cooperation foreseen

► Increased information sharing based on Art. 26 OECD-Model and capitalizing on the success of the Joint International Tax Shelter Information Center

► Joint/simultaneous transfer pricing audits

►New players enter the scene► Emerging countries learn fast

Global Transfer Pricing Controversy: Trends and ManagementPage 8

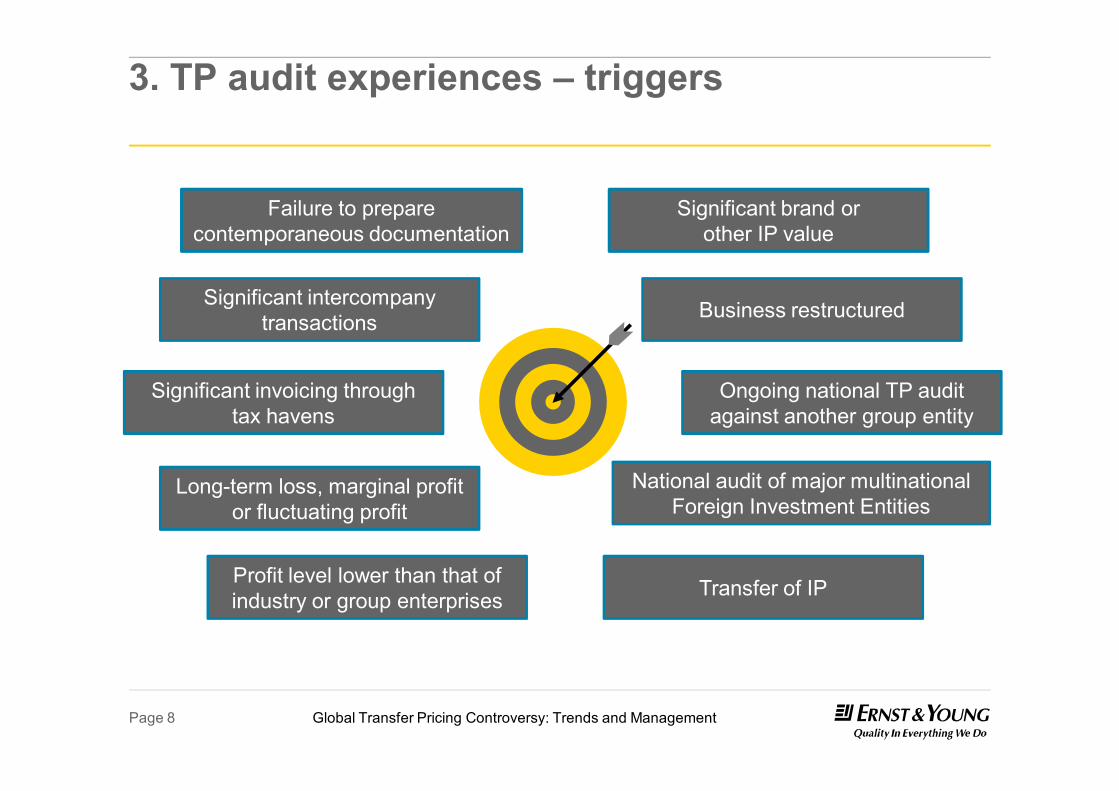

3. TP audit experiences – triggers

Failure to prepare contemporaneous documentation

Significant intercompany transactions

Significant invoicing through tax havens

Long-term loss, marginal profit or fluctuating profit

Profit level lower than that of industry or group enterprises

Significant brand or other IP value

Business restructured

Ongoing national TP audit against another group entity

National audit of major multinational Foreign Investment Entities

Transfer of IP

Global Transfer Pricing Controversy: Trends and ManagementPage 9

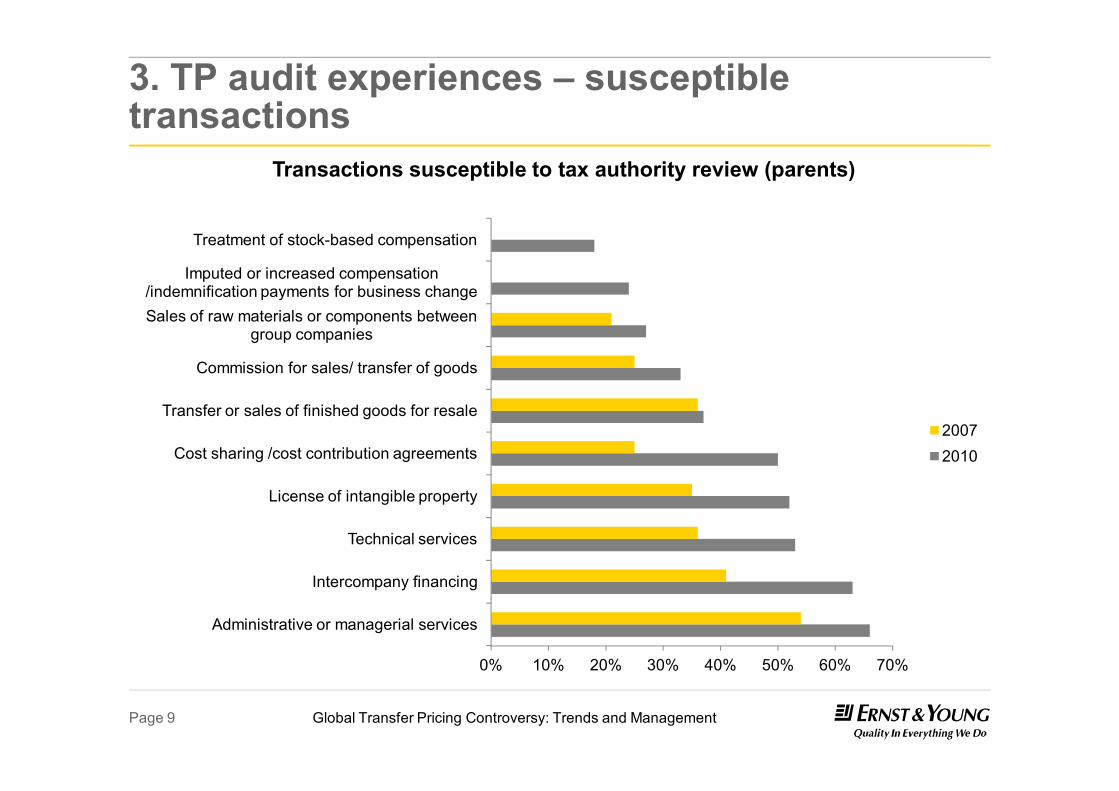

3. TP audit experiences – susceptible transactions

Transactions susceptible to tax authority review (parents)

0% 10% 20% 30% 40% 50% 60% 70%

Administrative or managerial services

Intercompany financing

Technical services

License of intangible property

Cost sharing /cost contribution agreements

Transfer or sales of finished goods for resale

Commission for sales/ transfer of goods

Sales of raw materials or components between group companies

Imputed or increased compensation /indemnification payments for business change

Treatment of stock-based compensation

20072010

Global Transfer Pricing Controversy: Trends and ManagementPage 10

Transfer pricing controversy trends –Latin America

Global Transfer Pricing Controversy: Trends and ManagementPage 11

1. Regional overview

►Majority of Latin America countries have TP rules in force

►OECD TP guidelines► considered as binding source of interpretation in case of local legal

loopholes or lack of regulations► Used in countries that acknowledge this status in local regulations

and others in frequent use of tax authorities in TP audits and TP assessments

►Burdensome requirements and expensive penalty regimes ► e.g., Columbia, Venezuela, Argentina, Ecuador, Peru

►According to Ernst & Young’s 2010 Global Transfer Pricing Survey, over 74% of respondents in Latin America considered TP documentation more important than it had been two years prior

Global Transfer Pricing Controversy: Trends and ManagementPage 12

1. Regional overview (cont.)

► Tax administrations have their own TP departments and are active in TP audits► Audits center on compliance with legal requirements and technical

analysis of the transactions

►Most active tax authorities are Colombia, Ecuador, Mexico, Brazil and Venezuela► Customs authorities are leveraging their customs value audits on

TP audits and TP returns (more focus on royalty payments, technical assistant and TP adjustments that may reveal the relationship has impacted price paid or payable of imported good)

Global Transfer Pricing Controversy: Trends and ManagementPage 13

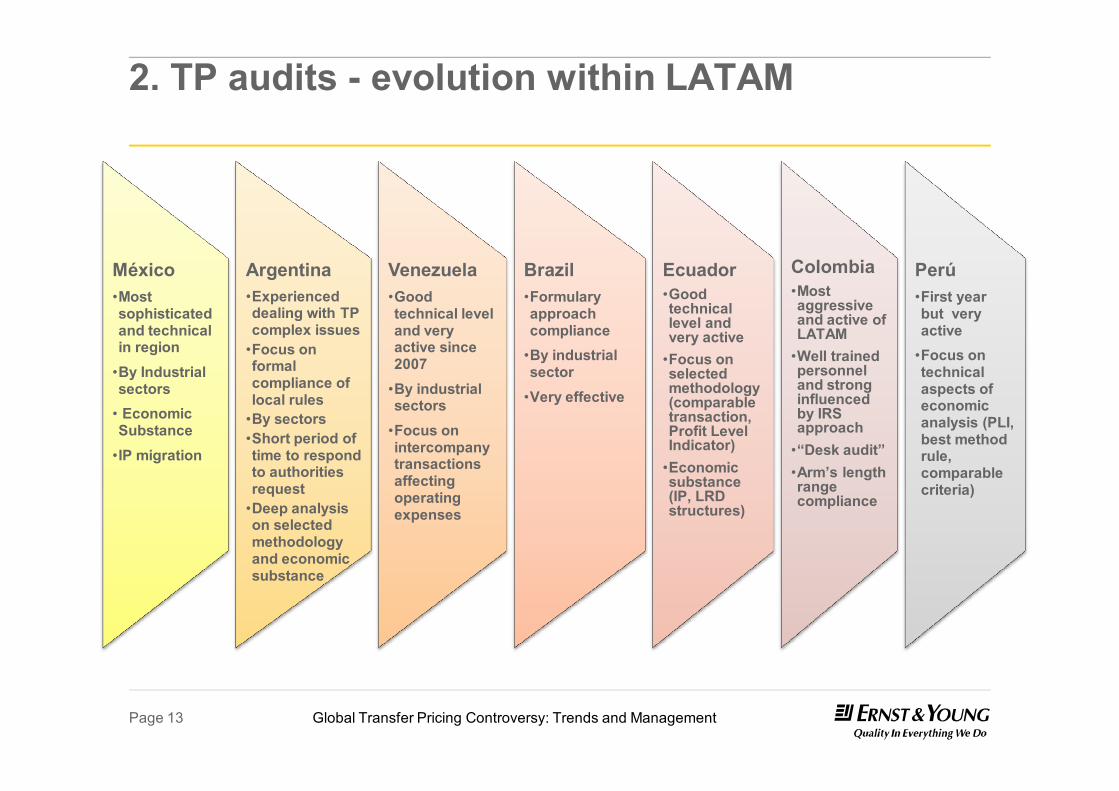

2. TP audits - evolution within LATAM

México•Most sophisticated and technical in region

•By Industrial sectors

• Economic Substance

•IP migration

Argentina•Experienced dealing with TP complex issues

•Focus on formal compliance of local rules

•By sectors•Short period of time to respond to authorities request

•Deep analysis on selected methodology and economic substance

Venezuela•Good technical level and very active since 2007

•By industrial sectors

•Focus on intercompany transactions affecting operating expenses

Brazil•Formulary approach compliance

•By industrial sector

•Very effective

Ecuador•Good technical level and very active

•Focus on selected methodology (comparable transaction, Profit Level Indicator)

•Economic substance (IP, LRD structures)

Colombia •Most aggressive and active of LATAM

•Well trained personnel and strong influenced by IRS approach

•“Desk audit”•Arm’s length range compliance

Perú •First year but very active

•Focus on technical aspects of economic analysis (PLI, best method rule, comparable criteria)

Global Transfer Pricing Controversy: Trends and ManagementPage 14

2. TP audits – trends

► Industries under scrutiny► Oil and gas, and related service providers► Mining► Pharmaceuticals ► Consumer products

►High risk intercompany transactions► Commodities related transactions► Technical assistance-CCA► Guarantee fees, loans► Royalties► Conversions

► Likelihood of being audited► High

Global Transfer Pricing Controversy: Trends and ManagementPage 15

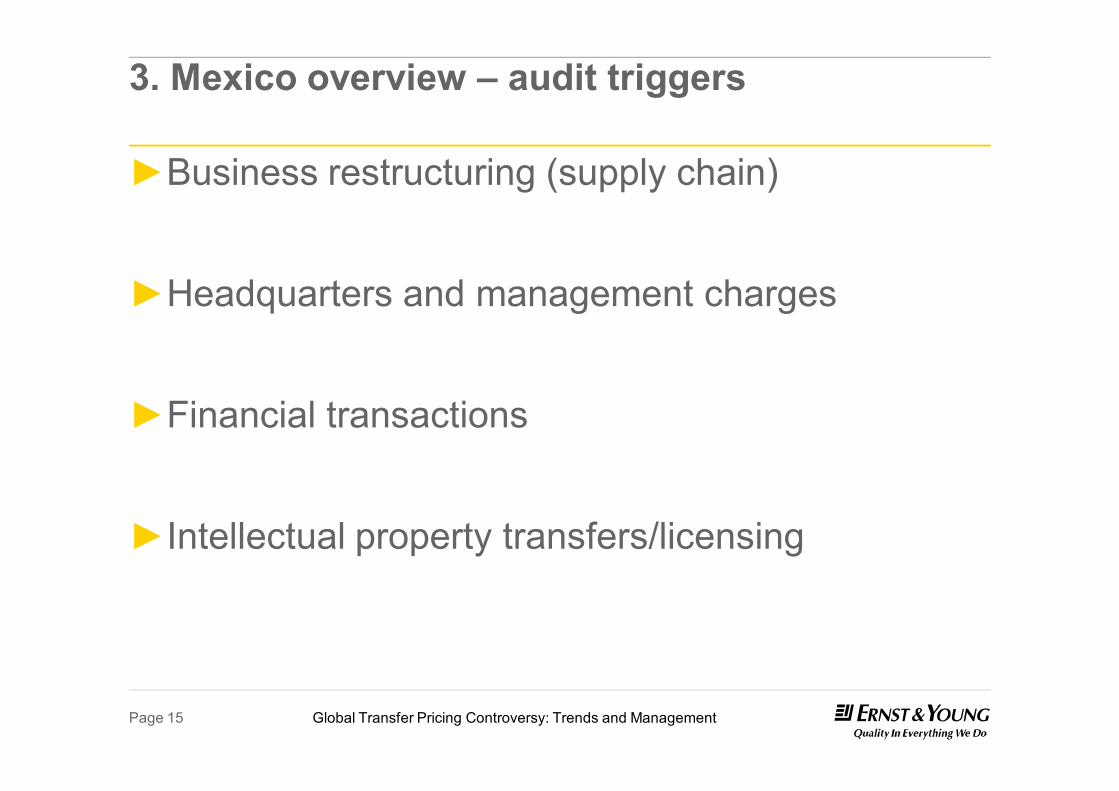

3. Mexico overview – audit triggers

►Business restructuring (supply chain)

►Headquarters and management charges

►Financial transactions

►Intellectual property transfers/licensing

Global Transfer Pricing Controversy: Trends and ManagementPage 16

Managing controversy risk

Global Transfer Pricing Controversy: Trends and ManagementPage 17

1. Global documentation – reasons to undertake

► When TP documentation is done as part of a global approach, it can be consistent across countries. This is a key advantage as tax authorities share more and more data under tax information exchange agreements, a key finding of our 2010 Global Transfer Pricing Survey, which highlights that:► There is an increased focus on bilateral and multilateral

coordination of transfer pricing administrations via the OECD Forum on Tax Administration and other international organizations

► Growing possibility for simultaneous and joint multi-jurisdictional audits

► Potential for synergized tax audit approaches and methodologies to mitigate controversy and double taxation

Global Transfer Pricing Controversy: Trends and ManagementPage 18

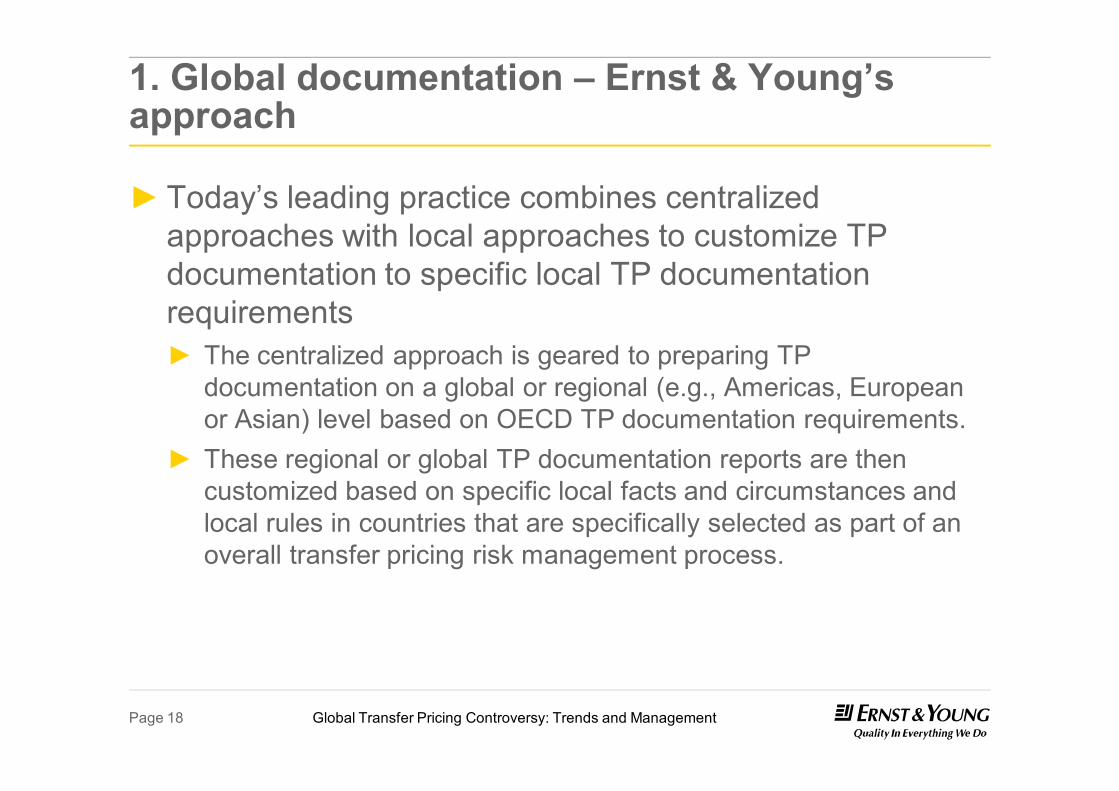

1. Global documentation – Ernst & Young’s approach

► Today’s leading practice combines centralized approaches with local approaches to customize TP documentation to specific local TP documentation requirements► The centralized approach is geared to preparing TP

documentation on a global or regional (e.g., Americas, European or Asian) level based on OECD TP documentation requirements.

► These regional or global TP documentation reports are then customized based on specific local facts and circumstances and local rules in countries that are specifically selected as part of an overall transfer pricing risk management process.

Global Transfer Pricing Controversy: Trends and ManagementPage 19

1. Global documentation – Ernst & Young’s approach

Centrally collectible information with relevance for the entire group

► Company overview► Business description► Ownership structure► Operations

Centrally collectible information with relevance at Business Unit level

► “Blueprint” of typical intercompany transaction flows

► Industry information► Analysis of key value

drivers► Function and risk profiles► Comparables searches

within economic analysis

Locally relevant information

► Local adaption of function and risk profiles

► Local adaption of economic analysis

► Local intercompany transaction

Global Transfer Pricing Controversy: Trends and ManagementPage 20

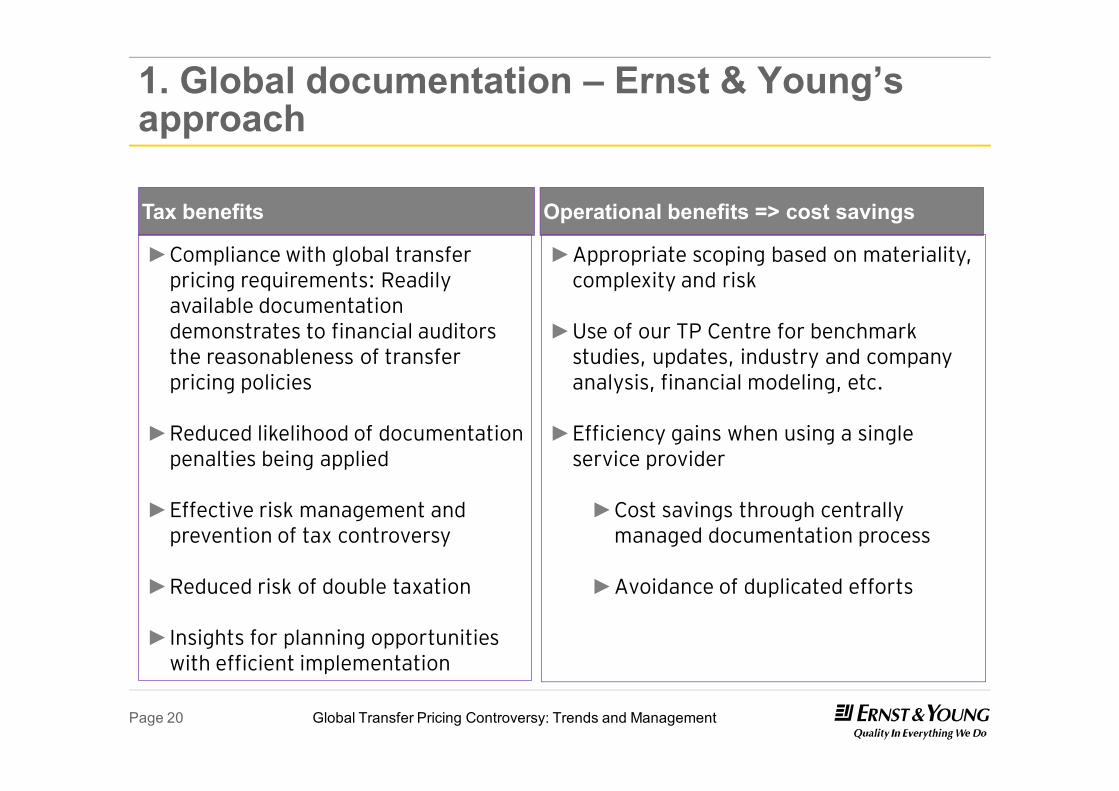

1. Global documentation – Ernst & Young’s approach

Tax benefits Operational benefits => cost savings

►Compliance with global transfer pricing requirements: Readily available documentation demonstrates to financial auditors the reasonableness of transfer pricing policies

►Reduced likelihood of documentation penalties being applied

►Effective risk management and prevention of tax controversy

►Reduced risk of double taxation

►Insights for planning opportunities with efficient implementation

►Appropriate scoping based on materiality, complexity and risk

►Use of our TP Centre for benchmark studies, updates, industry and company analysis, financial modeling, etc.

►Efficiency gains when using a single service provider

►Cost savings through centrally managed documentation process

►Avoidance of duplicated efforts

Global Transfer Pricing Controversy: Trends and ManagementPage 21

2. Advance pricing agreements – conditions

► Double Tax Treaty and/or APA Program required

► Unilateral vs. bi-/multilateral APAs:► Unilateral approaches (“rulings”) bind only one tax authority

► Unilateral APAs might raise concerns in other country

► Double-sided unilateral approaches

► “Right” transactions:► Possibility of rollback

► Volume aspects

► Complexity thresholds

Global Transfer Pricing Controversy: Trends and ManagementPage 22

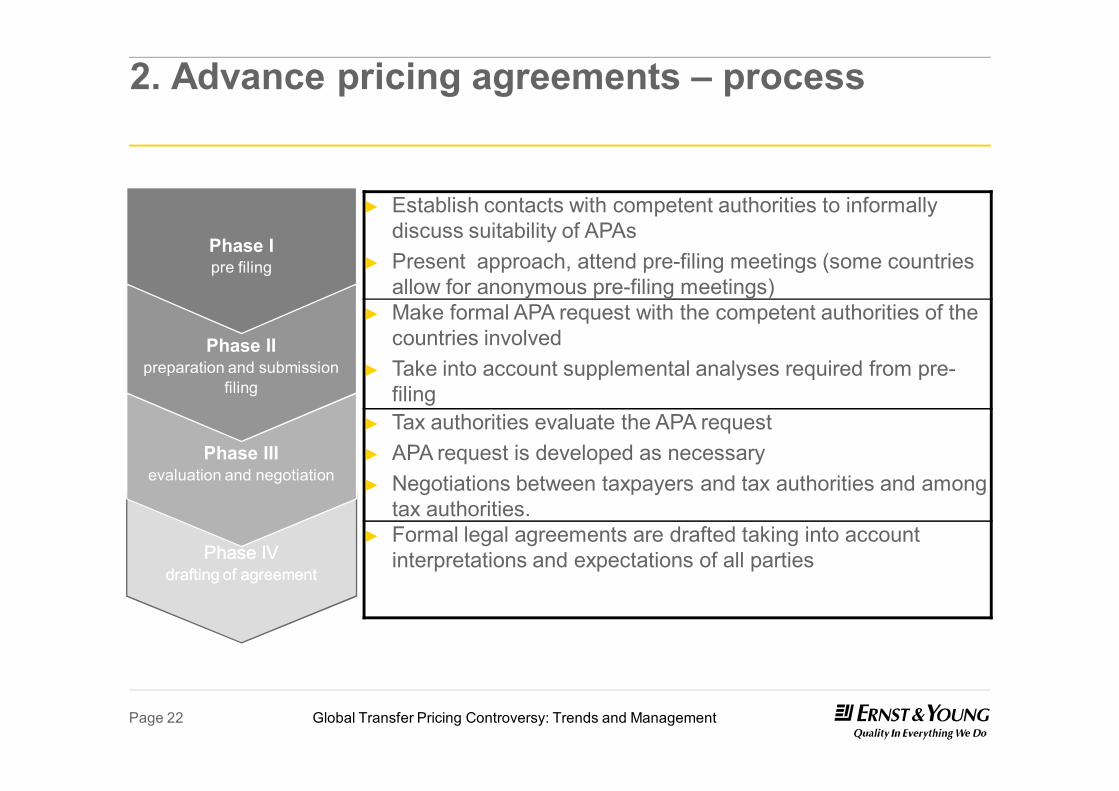

2. Advance pricing agreements – process

► Establish contacts with competent authorities to informally discuss suitability of APAs

► Present approach, attend pre-filing meetings (some countries allow for anonymous pre-filing meetings)

► Make formal APA request with the competent authorities of the countries involved

► Take into account supplemental analyses required from pre-filing

► Tax authorities evaluate the APA request ► APA request is developed as necessary► Negotiations between taxpayers and tax authorities and among

tax authorities.► Formal legal agreements are drafted taking into account

interpretations and expectations of all partiesPhase IVPhase IVdrafting of agreementdrafting of agreement

Phase IIIevaluation and negotiation

Phase IIpreparation and submission

filing

Phase I pre filing

Global Transfer Pricing Controversy: Trends and ManagementPage 23

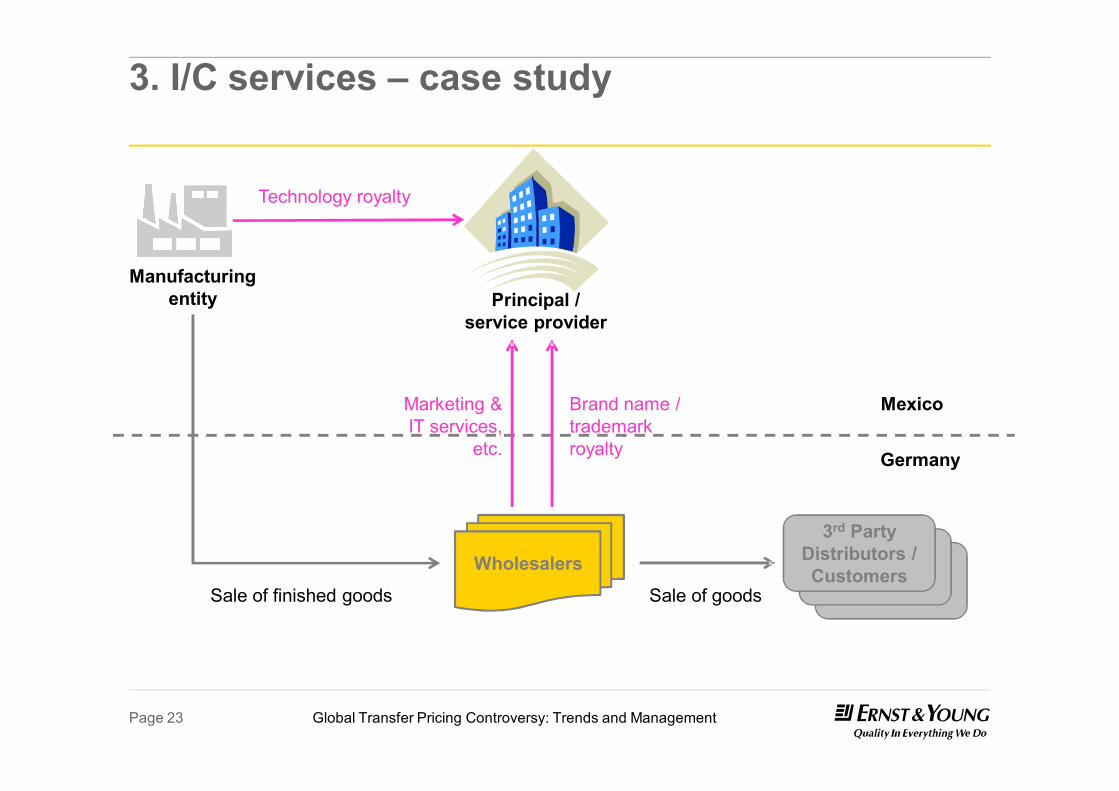

3. I/C services – case study

Principal / service provider

Wholesalers

Marketing & IT services,

etc.

Brand name / trademark royalty Germany

Mexico

Technology royalty

Sale of finished goods Sale of goods

Manufacturing entity

3rd Party Distributors / Customers

Global Transfer Pricing Controversy: Trends and ManagementPage 24

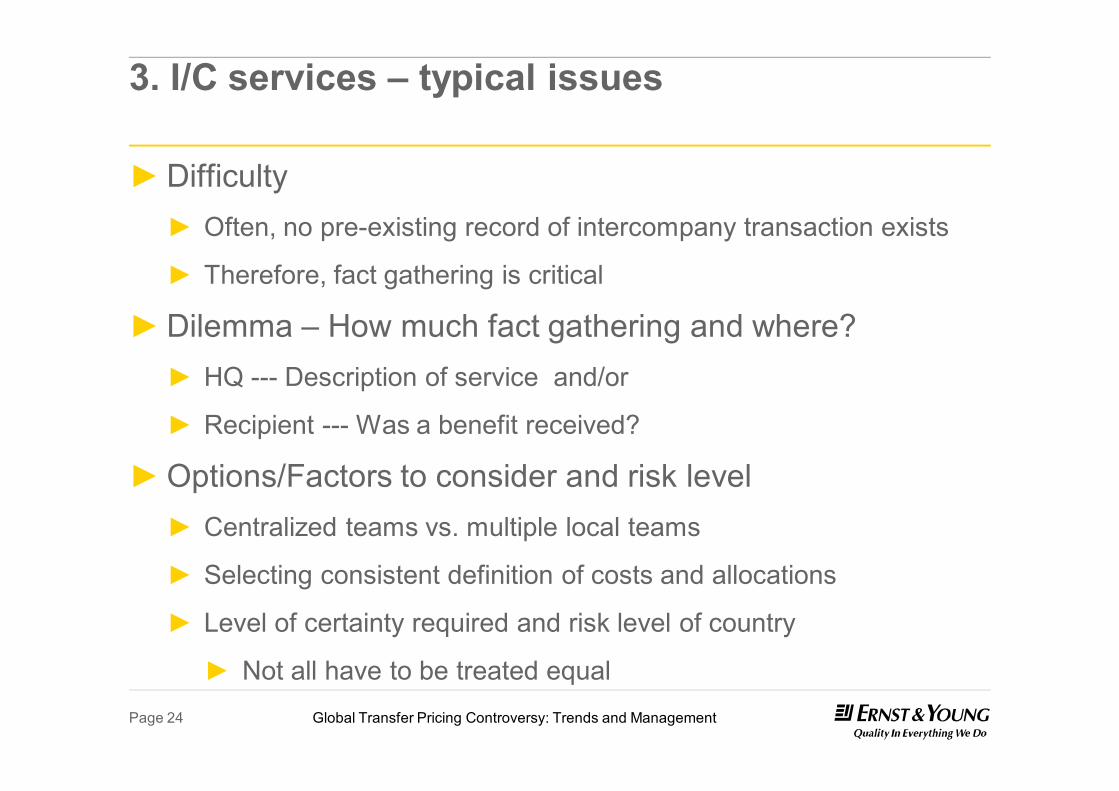

3. I/C services – typical issues

►Difficulty► Often, no pre-existing record of intercompany transaction exists

► Therefore, fact gathering is critical

►Dilemma – How much fact gathering and where?► HQ --- Description of service and/or

► Recipient --- Was a benefit received?

►Options/Factors to consider and risk level► Centralized teams vs. multiple local teams

► Selecting consistent definition of costs and allocations

► Level of certainty required and risk level of country

► Not all have to be treated equal

Global Transfer Pricing Controversy: Trends and ManagementPage 25

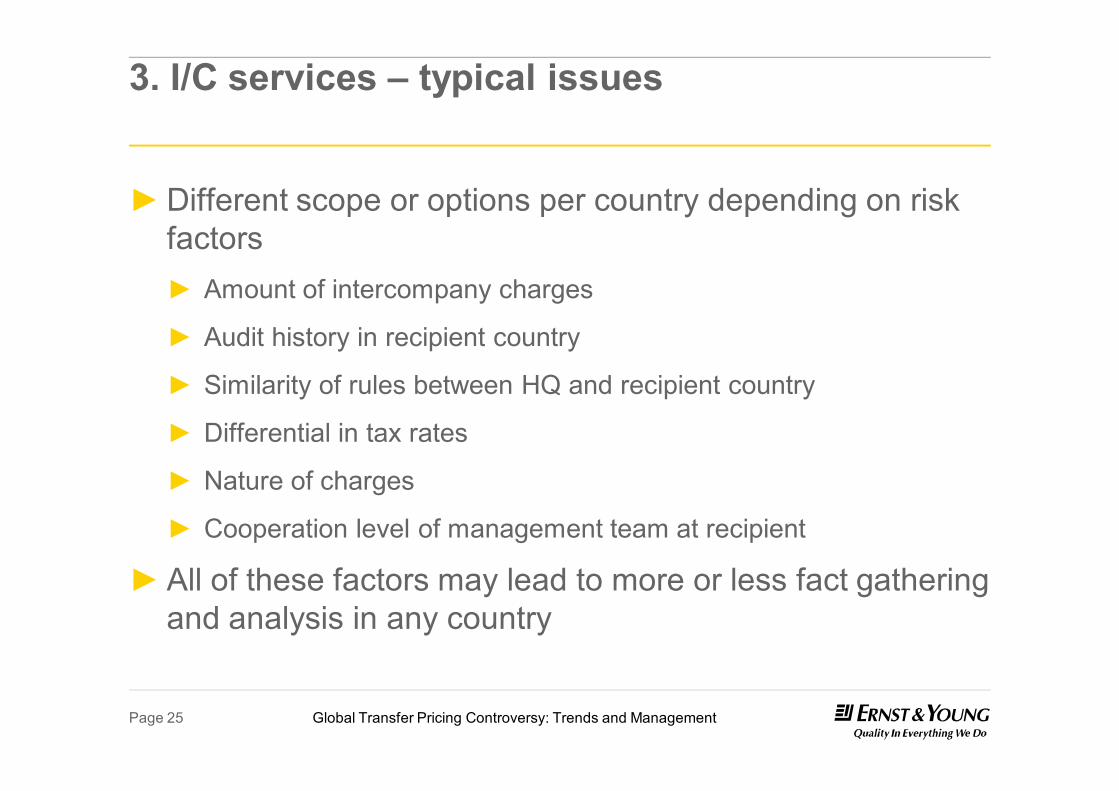

3. I/C services – typical issues

►Different scope or options per country depending on risk factors► Amount of intercompany charges

► Audit history in recipient country

► Similarity of rules between HQ and recipient country

► Differential in tax rates

► Nature of charges

► Cooperation level of management team at recipient

►All of these factors may lead to more or less fact gathering and analysis in any country

Global Transfer Pricing Controversy: Trends and ManagementPage 26

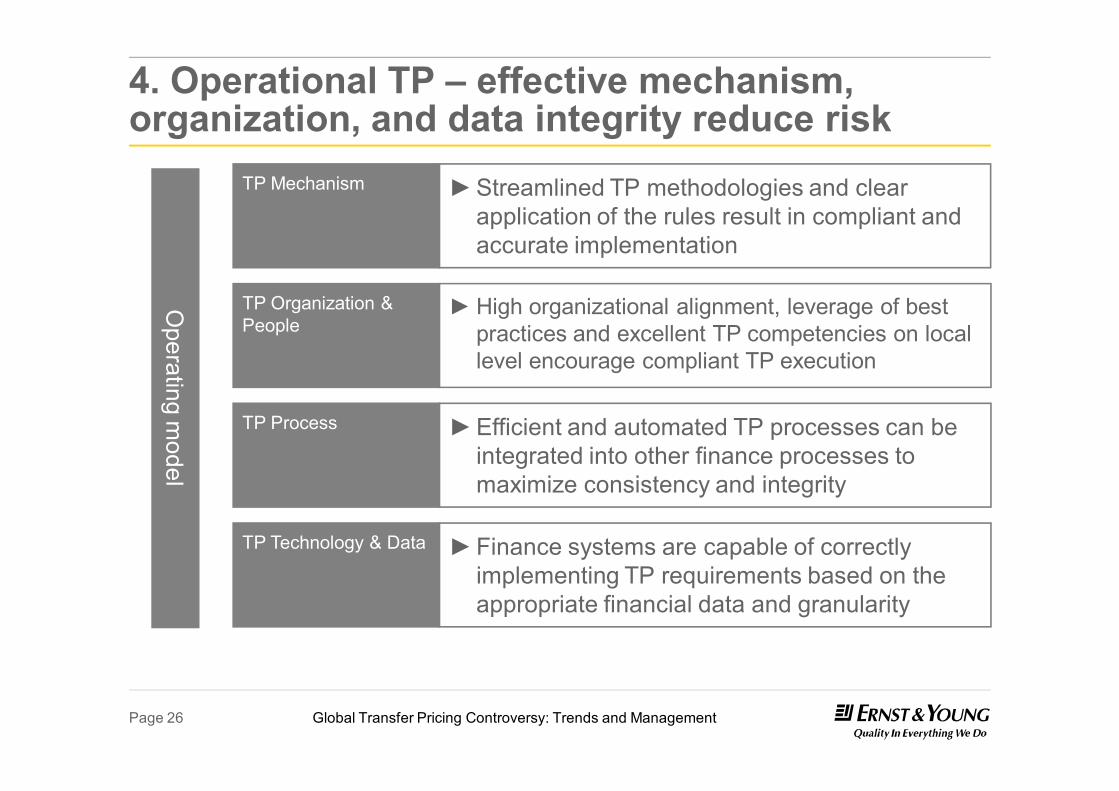

4. Operational TP – effective mechanism, organization, and data integrity reduce risk

TP Mechanism ►Streamlined TP methodologies and clear application of the rules result in compliant and accurate implementation

TP Organization & People

► High organizational alignment, leverage of best practices and excellent TP competencies on local level encourage compliant TP execution

TP Process ►Efficient and automated TP processes can be integrated into other finance processes to maximize consistency and integrity

TP Technology & Data ►Finance systems are capable of correctly implementing TP requirements based on the appropriate financial data and granularity

Operating m

odel

Global Transfer Pricing Controversy: Trends and ManagementPage 27

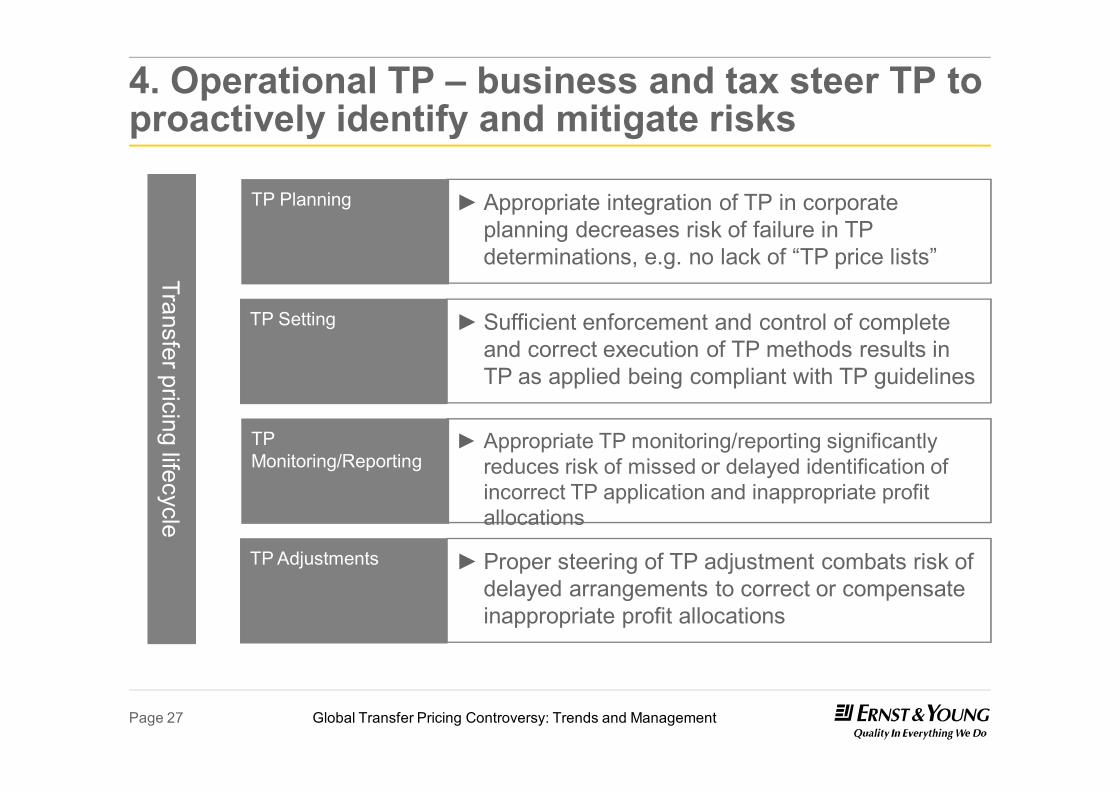

4. Operational TP – business and tax steer TP to proactively identify and mitigate risks

TP Planning ► Appropriate integration of TP in corporate planning decreases risk of failure in TP determinations, e.g. no lack of “TP price lists”

TP Setting ► Sufficient enforcement and control of complete and correct execution of TP methods results in TP as applied being compliant with TP guidelines

TP Monitoring/Reporting

► Appropriate TP monitoring/reporting significantly reduces risk of missed or delayed identification of incorrect TP application and inappropriate profit allocations

TP Adjustments ► Proper steering of TP adjustment combats risk of delayed arrangements to correct or compensate inappropriate profit allocations

Transfer pricing lifecycle

Global Transfer Pricing Controversy: Trends and ManagementPage 28

4. Operational TP – Intercompany Effectiveness Survey (IES)EY conducted a survey of 23 mostly Fortune 100 multinationals as a means of helping them understand how their peers across several other industries manage and monitor their transfer pricing function.

The study enables companies to answer the following questions:►How does the effectiveness of your company’s transfer pricing TP

operations benchmark against the participant group?

►What are the most significant TP operational issues facing other companies?

The study covers the operating model (organization, process, and technology) and the common challenges related to meeting transfer pricing requirements.

Global Transfer Pricing Controversy: Trends and ManagementPage 29

4. Operational TP – IES results: process and controls

►59% of the respondents monitor transfer pricing on a real time, monthly or quarterly basis

►Timely monitoring minimizes the need for year-end transfer pricing true-ups, which also helps avoid customs and other indirect tax issues

Key observations:

9%

48%17%

26%

Extent transfer pricing processes are standardized across company

and documented (QC 25)

2 - nonstandard

3

4

5 - standardized and documented

22%

22%

8%

35%

13%

Extent true-ups significant from financial reporting perspective and

impacting tax results (QC 26)

1 - insignificant

2

3

4

5 - highly significant

27%

20%17%

12% 11%8%

5%

% o

f Res

pond

ents

Transfer pricing methods

Transfer pricing methods supporting process (QC 23)

40%37%

11% 11%

Annually Quarterly Real-time Monthly

% o

f Res

pond

ents

Frequency of monitoring

Frequency of monitoring financial results to ensure transfer pricing policy compliance (QC 24)

Global Transfer Pricing Controversy: Trends and ManagementPage 30

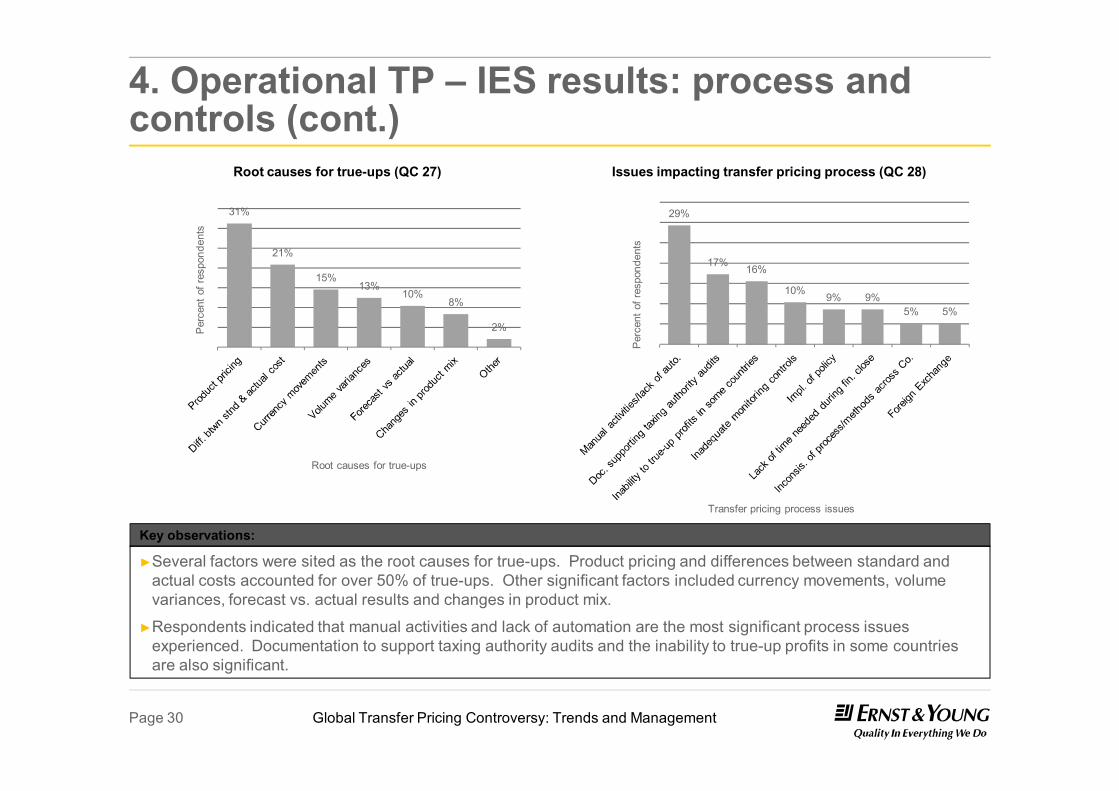

4. Operational TP – IES results: process and controls (cont.)

►Several factors were sited as the root causes for true-ups. Product pricing and differences between standard and actual costs accounted for over 50% of true-ups. Other significant factors included currency movements, volume variances, forecast vs. actual results and changes in product mix.

►Respondents indicated that manual activities and lack of automation are the most significant process issues experienced. Documentation to support taxing authority audits and the inability to true-up profits in some countries are also significant.

Key observations:

31%

21%

15%13%

10%8%

2%Per

cent

of r

espo

nden

ts

Root causes for true-ups

Root causes for true-ups (QC 27)

29%

17%16%

10%9% 9%

5% 5%

Per

cent

of r

espo

nden

ts

Transfer pricing process issues

Issues impacting transfer pricing process (QC 28)

Global Transfer Pricing Controversy: Trends and ManagementPage 31

4. Operational TP – IES results: improvement expectations

Key observations:

91%

9%

Planning improvements

Not planning improvements

Percent of companies planning improvements

3%

5%

23%

23%

46%

Other

None

People

Technology

Process

Percent of respondents planning improvements next year

Type

of T

P im

prov

emen

ts p

lann

ed

Improvements being made in next year to address transfer pricing issues (QE 43)

► More than 90% of companies surveyed indicated that they plan to make improvements to the transfer pricing process within the next year.

► Of the improvements sited, nearly half indicated that they plan process improvements. Nearly a quarter also indicated technology- and/or people-related improvements.

Avances y Perspectivas de la Fiscalización en México

Global Transfer Pricing Controversy: Trends and ManagementPage 33

Introducción

►Facultades de comprobación formales► Revisión de gabinete

► Visita domiciliaria

► Revisión de dictámen

► Visita específica en materia de ► Comprobantes fiscales

► RFC

► Obligaciones Aduaneras

► Marbetes y precinto

► Datos proporcionados a fedatarios

►Realización de avaluos

Global Transfer Pricing Controversy: Trends and ManagementPage 34

Introducción►Facultades de comprobación “informales”►Devolución►Compensaciones►Compulsas►Análisis de información proporcionada: ► Bancos

► Clientes y proveedores

► Dictámenes locales, IMSS

► Operaciones con partes relacionadas

►Carta invitación: Programa “Seguimiento Profundo”

Global Transfer Pricing Controversy: Trends and ManagementPage 35

Instrumentos de fiscalización más usados

a) Devolucionesb) Dictámen§ Revisión de “posiciones fiscales agresivas

c) Fiscalización tradicional§ Revisión de empresas; básicamente formal vía visita

domiciliaria o§ revisión de gabinete

d) Fiscalización especializada § Revisión de operaciones para PT, E.P. y RE con apoyo en compulsas y

solicitudes de información al extranjero

Global Transfer Pricing Controversy: Trends and ManagementPage 36

¿Cómo estar preparado para una auditoría?Proceso de Revisión

Revisión al Auditor Externo (SAT)

Orden de visita o Requerimiento a Empresa

(SAT)

Compulsa e

intercambio de

información

VAP, Oficio de observac

iones (SAT)

Escrito de

Inconformidad

(Empresa)

AF o Acta de

Auditoría (SAT)

Inicia Auditoria Resolución

Global Transfer Pricing Controversy: Trends and ManagementPage 37

Resultado del Ejercicio de Facultades

a) Resolución sin crédito fiscal b) Resolución determinante de crédito fiscal =

liquidación c) Responsabilidad profesional del auditord) Querella, denuncia o declaratoria de perjuicioLas resoluciones b y c requieren formalidades legales

Global Transfer Pricing Controversy: Trends and ManagementPage 38

Auditorías redituables

0

20,000

40,000

60,000

80,000

100,000

120,000

4 5 6 7 8 9 10 11

48,56142,181

64,79452,289

62,98074,413

97,966 102,622

A través de las auditorías, el SAT se ha hecho llegar una importante cantidad de recursos. (Recaudación por

auditorías/ Millones de pesos)

Fuente: SAT

Global Transfer Pricing Controversy: Trends and ManagementPage 39

Liquidaciones Atipicas

►Devoluciones o compensaciones improcedentes

►No retención IDE

Global Transfer Pricing Controversy: Trends and ManagementPage 40

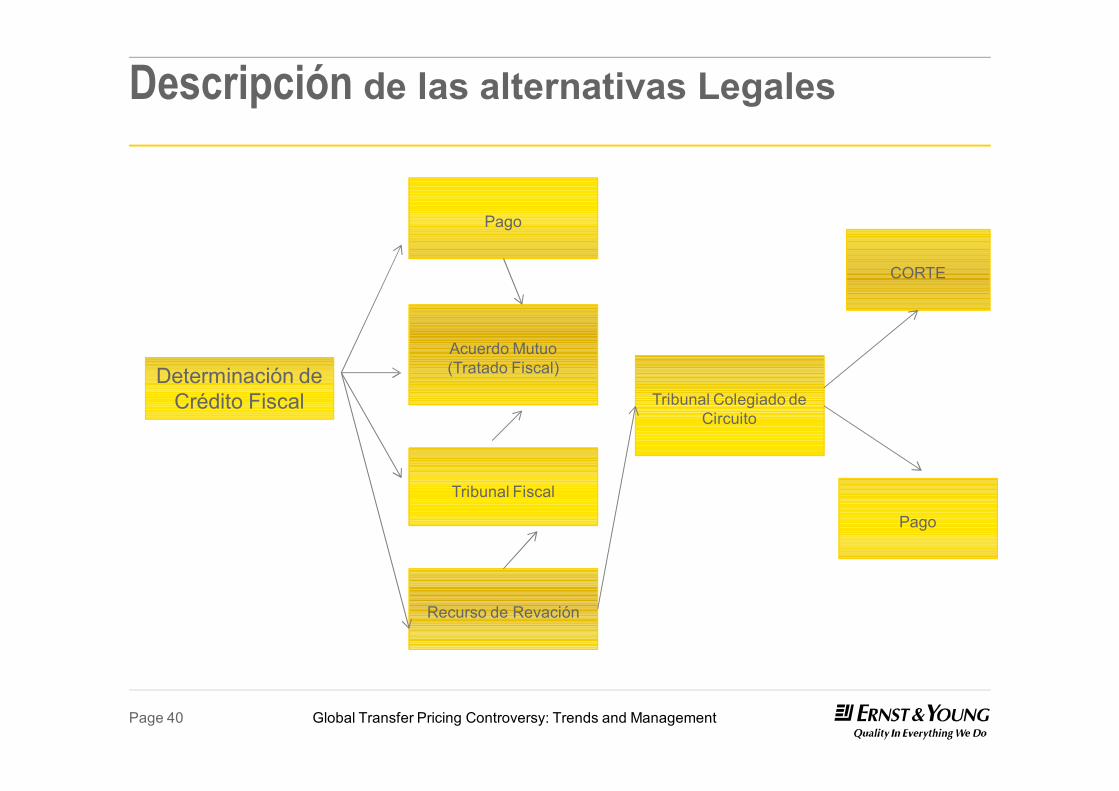

Descripción de las alternativas Legales

Determinación de Crédito Fiscal

Pago

Acuerdo Mutuo (Tratado Fiscal)

Tribunal Fiscal

Recurso de Revación

Tribunal Colegiado de Circuito

Pago

CORTE

Global Transfer Pricing Controversy: Trends and ManagementPage 41

Tribunal Federal de Justicia Fiscal y Administrativo

Tradicional

En línea

Sumario

Global Transfer Pricing Controversy: Trends and ManagementPage 42

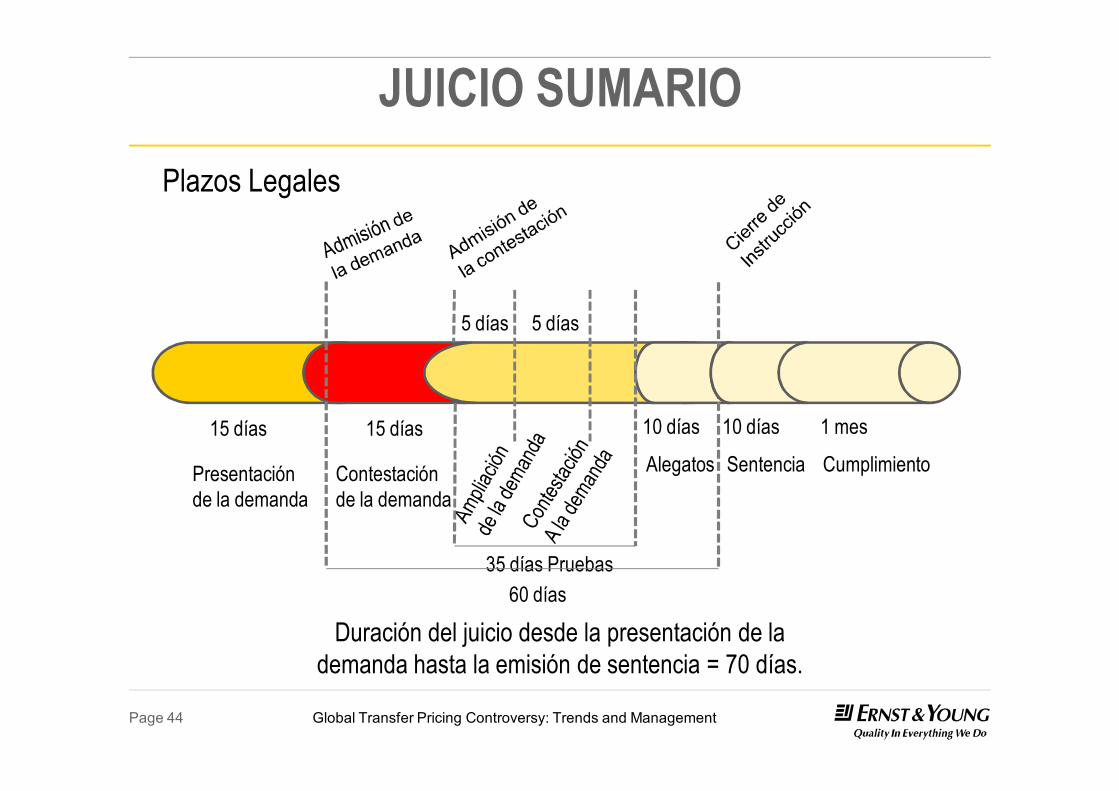

JUICIO SUMARIO

Procede:► Por cuantía menor. Contra resoluciones que no excedan de 5 veces el

SMGV en el DF elevado al año.

► En materia fiscal que no exceda esa cuantía. Créditos fiscales, multas,sanciones a las normas administrativas, que requieran el pago de unafianza o garantía y las que se dicten en los recursos administrativospromovidos en su contra.

► Que contravengan jurisprudencia. De la SCJN en materia deinconstitucionalidad de leyes, o del Pleno de la Sala Superior delTFJFA.

Global Transfer Pricing Controversy: Trends and ManagementPage 43

JUICIO SUMARIO

Será improcedente cuando:► No se reúnan los anteriores requisitos.► Se controvierta una regla administrativa de carácter general.► Se trate de responsabilidades administrativas de servidores

públicos:sanción económica o responsabilidad resarcitoria.

► Se impugnen multas en materia de propiedad intelectual.► Se controviertan sanciones que incluyan además otra carga u

obligación.► Las partes no puedan presentar a sus testigos.

Global Transfer Pricing Controversy: Trends and ManagementPage 44

JUICIO SUMARIO

5 días 5 días

10 días 10 días 1 mes

Alegatos Sentencia Cumplimiento15 días15 días

Contestación de la demanda

Presentación de la demanda

35 días Pruebas60 días

Plazos Legales

Duración del juicio desde la presentación de la demanda hasta la emisión de sentencia = 70 días.

Global Transfer Pricing Controversy: Trends and ManagementPage 45

JUICIO SUMARIO

►Reducción de los plazos para el ejercicio de los derechos de las partes.

►La capacidad del Tribunal se potenciará en tres veces. En vez de 44 Salas Regionales, tendremos 132 Juzgadores para resolver los juicios.

Global Transfer Pricing Controversy: Trends and ManagementPage 46

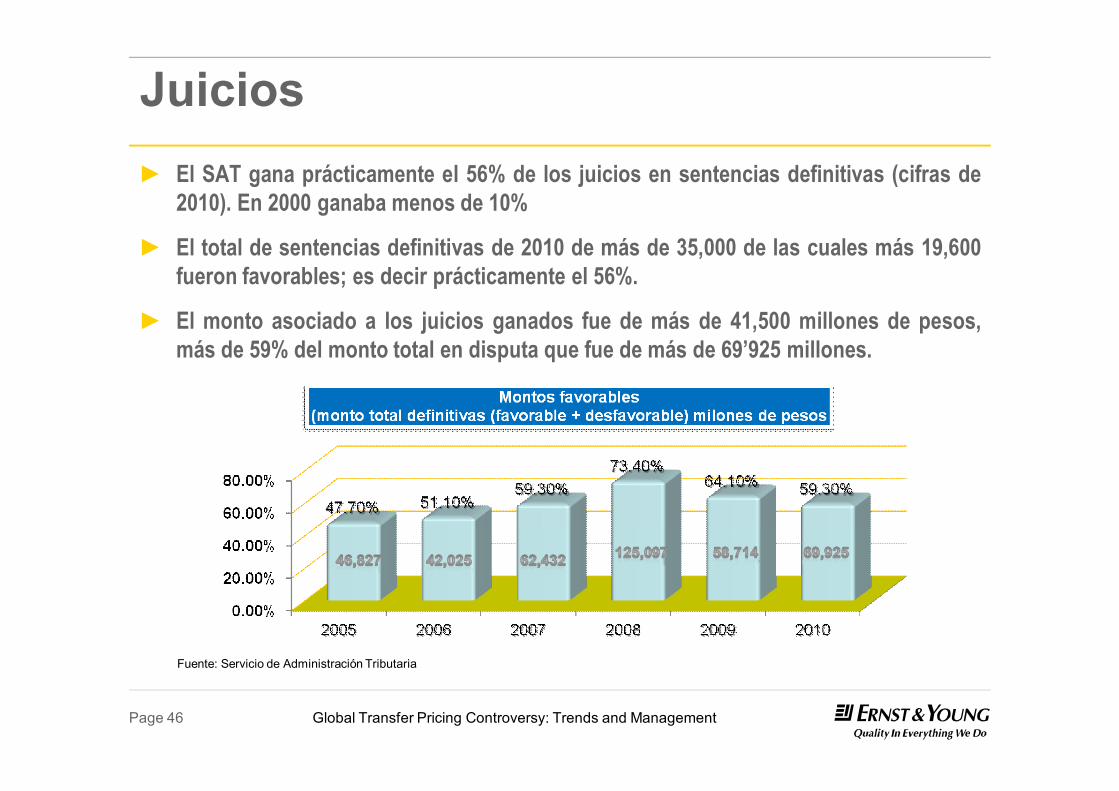

Juicios► El SAT gana prácticamente el 56% de los juicios en sentencias definitivas (cifras de

2010). En 2000 ganaba menos de 10%

► El total de sentencias definitivas de 2010 de más de 35,000 de las cuales más 19,600fueron favorables; es decir prácticamente el 56%.

► El monto asociado a los juicios ganados fue de más de 41,500 millones de pesos,más de 59% del monto total en disputa que fue de más de 69’925 millones.

Fuente: Servicio de Administración Tributaria

Global Transfer Pricing Controversy: Trends and ManagementPage 47

Questions?

Global Transfer Pricing Controversy: Trends and ManagementPage 48

Thank you!