Embed Size (px)

Citation preview

Global Snap Shot Gaseous Fuels

Warring Neilsen

Corporate Affairs Manager

Elgas – Linde Group

Autogas Shifting Global demand in last 5 years

A significant increase in Autogas consumption

Source: WLPGA

9.8%

23.1%

8.3%

11.3%

0%

10%

20%

30%

2006 2007 2008 2009 2010 2011 2012

Autogas Domestic

87.3%

42.8%

23.1%

0%

20%

40%

60%

80%

100%

2006200720082009201020112012

Fleet Stations Autogas

23.119.770 67.927 23.843.000

Global LPG Supply

Autogas – 25.8 Million Tonnes

Shale Gas: Key European Reserves

Source: EIA The chart above shows some of the locations of key European shale deposits

Country

Amount of

Shale

estimated (in trillion cubic

feet)

1 Russia 287

2 Ukraine 128

3 Romania 51

4 Poland 148

5 Germany 17

6 Denmark 32

7 Netherlands 26

8 France 137

9 UK 26

• In order to reduce its dependence on Russian natural gas resources, local governments step up efforts to tap their region's shale gas deposits.

• While other alternative fuels like LPG continue to be high cost to import, shale continues be a more near term solution. As accessing nearby shale gas resources would be cheaper than other option

LNG Forecast

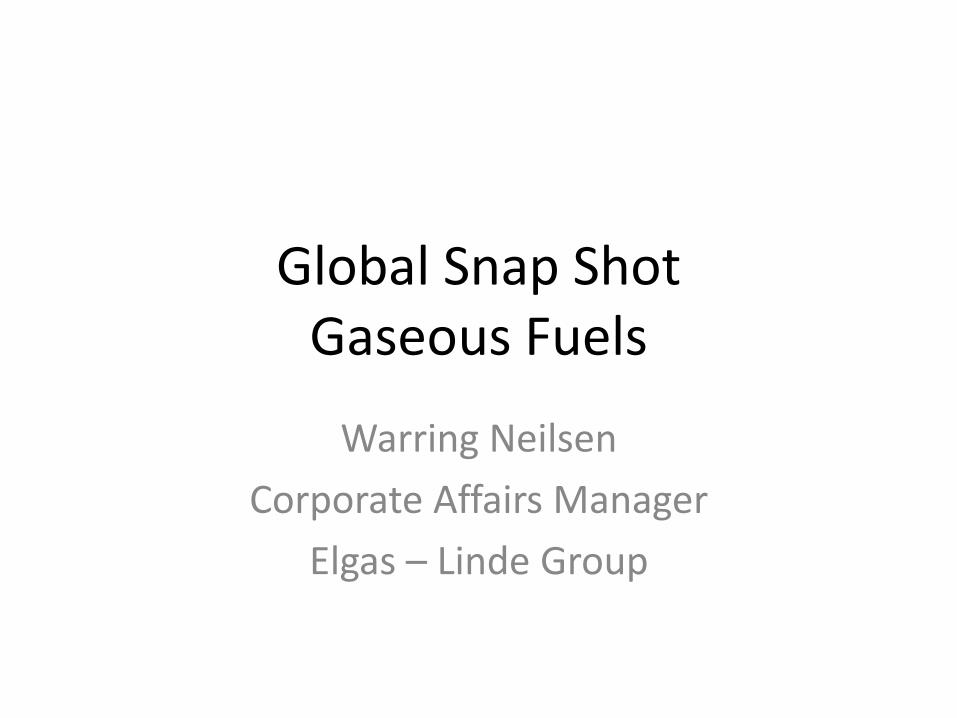

Global Mega Trends Impacting Powertrain

Car Sharing/Car Pooling

New Micro Mobility products

Integrated Mobility Solutions

E-Mobility

Connected and Wireless Planet

Sustainable Public Transportation and BRT

Urbanization

New Energy Sources (Shale gas) Power to the Middle Class and Gen

Y

Impact of Mega Trends on Powertrain technologies

Emergence of Tier

0.5 suppliers as

engine and

powertrain

aggregate

suppliers with

OEMs looking to

shift focus towards

“Mobility” solutions

The 2020 ACEA

Agreement target

of 95 gm/km of CO2

prompting

Hybridisation and

Electrification of

not only engines

but also

Transmissions

Cross-border

alliances and joint

ventures extending

beyond 4 wheelers

and into 2 wheelers

[Audi buying

Ducati]

Concept of

Powertrain

“rightsizing”

gradually replacing

downsizing trends

– fuel efficiency

and drivability key

drivers

Shale Gas

reserves

expected to shift

focus towards

LPG / CNG

powered

passenger

vehicles;

European and NA

OEMs keen on

offering gas

powered variants

European Energy Mix and Trends

Key Influencing factors: regional policies, oil price etc.

European

Energy

Fuel Mix

National / Supranational energy

policies

Gas price indexation to Oil price

Country specific incentives,

especially towards renewables EU Emission Targets

Reducing dependence on imports

by increasing share of renewable

and unconventional sources

Company Lobbies

LPG and CNG - Market Drivers and Restraints Government incentives play a key role in the success of alternative fuels in countries like Germany , Italy and the

Netherlands.

Driv

ers

R

estra

ints

Driv

ers

R

estra

ints

Total LPG and CNG Market: Key Market Drivers and Restraints, Europe, 2014–2020

Denotes long-term impact

Denotes current impact

Source: Frost & Sullivan

Existing

infrastructure Availability and

proximity of reserves

and plants

Structured

government

incentives for

Private and

Fleet

OEMs’ need to

reduce Carbon

Emission

vehicles

Dominance of diesel

and gasoline Poor utilization of

infrastructure

Lack of organized

NGV policy by

government

officials

Limited

Refueling

network

Trend towards

blends and

hybrids

Total cost of

ownership

Future opportunities for gaseous fuels in Europe by 2020 Market Impact of Top Growth Trends for gaseous fuels - Transportation

Projected Impact on the

Transportation Industry

(fuel market)

High Impact

Low Impact

Certainty

Low High

LPG vehicles

Shale gas within transportation

Gas 2 Liquid

CNG vehicles

Hydrogen Gas

Bio Fuel Blends

High Growth Impact

Low Growth Impact

Medium Growth Impact

Source: Frost & Sullivan.

24% 25% 26% 30% 33% 36% 37% 38% 39% 76% 75% 74% 70%

67%

64% 63%

62% 61%

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

2012 2013 2014 2015 2016 2017 2018 2019 2020

CNG LPG

Total LPG and CNG Unit Shipment Snapshot - 2020 vision in Europe The growth of alternative fuel vehicle in Europe can be attributed to the introduction of new models and revamped

infrastructure in several regions.

2014

74%

26%

52%

48%

350-375 Thousand

units

CNG and LPG Market: Unit Shipment Forecast, Europe, 2012–2020

CAGR = 13.8%

• The overall market scenario in Europe is much better than the rest of the world with close to 5% more alternative fuel vehicles than other regions.

• The high growth rate among the various EU countries can be attributed to the stringent Euro norms and individual government interest in the fuel as a means to reduce dependency on oil fuels.

2020

61%

39%

*Range used due to the fluctuating nature of the number.

Year

Un

its

Note: All figures are rounded. The base year is 2013. Source: Frost & Sullivan

800-850 Thousand

units

2020

100% 45%

24%

34%

21%

23% 15%

72%

55%

76%

63% 79%

77% 85%

28%

0

50

100

150

200

250

300

350

BMW Daimler Fiat-Chrysler Ford General Motors Hyundai PSA Renault-Nissan Volkswagen

Un

its

(‘0

00

)

CNG LPG

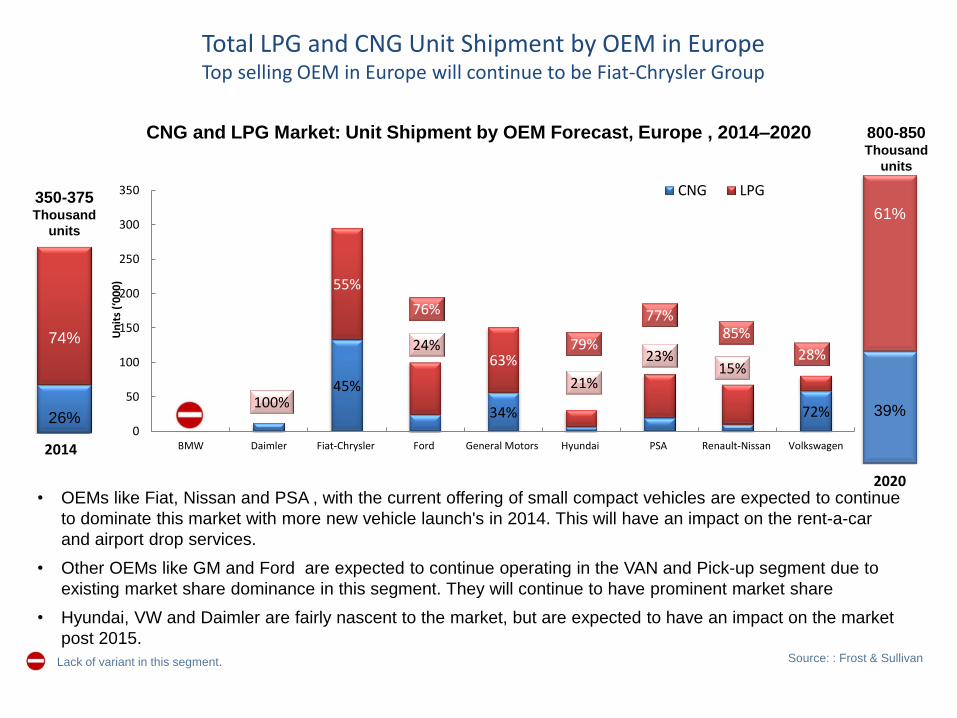

Total LPG and CNG Unit Shipment by OEM in Europe Top selling OEM in Europe will continue to be Fiat-Chrysler Group

• OEMs like Fiat, Nissan and PSA , with the current offering of small compact vehicles are expected to continue

to dominate this market with more new vehicle launch's in 2014. This will have an impact on the rent-a-car

and airport drop services.

• Other OEMs like GM and Ford are expected to continue operating in the VAN and Pick-up segment due to

existing market share dominance in this segment. They will continue to have prominent market share

• Hyundai, VW and Daimler are fairly nascent to the market, but are expected to have an impact on the market

post 2015.

CNG and LPG Market: Unit Shipment by OEM Forecast, Europe , 2014–2020

Lack of variant in this segment. Source: : Frost & Sullivan

2014

74%

26%

350-375 Thousand

units

61%

39%

800-850 Thousand

units

European LPG Conversion Centres

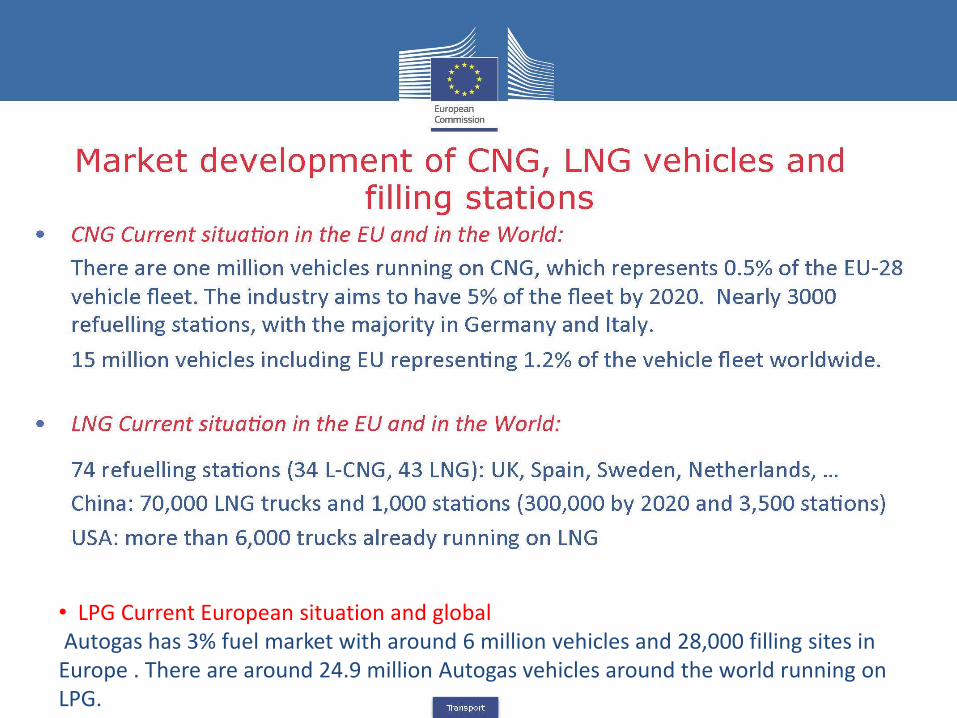

• LPG Current European situation and global Autogas has 3% fuel market with around 6 million vehicles and 28,000 filling sites in Europe . There are around 24.9 million Autogas vehicles around the world running on LPG.

Europe Infrastructure

Canada

USA

LNG –CNG- LPG Options Dedicated or Dual fuel

DAF Mitsubishi

Iveco Isuzu

MAN Hino

Mercedes Toyota

Renault Nissan

Volvo International Cummins Detroit Diesel

Sinotruk Scania

Hyundai

LNG – CNG -

Number of converted trucks: 22

Annual running expenses: € 350,- per truck

Annual machinery breakdown insurance: € 500,- per truck

Breakeven point reached in 15 months

No conspicuous repairs in the 27 months of this case study

Additional savings with on-site FLAGA LPG filling station

Diesel Blending LPG –

McDonald‘s HAVI Logistics – Austria

Thank You

Questions ?