Embed Size (px)

Citation preview

A UNIQUE PERSPECTIVE ON THE ISSUES AND OPPORTUNITIESFACING INVESTORS IN AUSTRALIAN PRIVATE EQUITY

Global Private Equity BarometerAustrAliA snApshot

A u s t r A l i A s n A p s h o t2

Coller Capital’s Global Private Equity Barometer

Coller Capital’s Global Private Equity Barometer is a unique

snapshot of worldwide trends in private equity – a twice-yearly

overview of the plans and opinions of institutional investors in

private equity (Limited Partners, or LPs, as they are known) based

in North America, Europe and Asia-Pacific.

Australia snapshot

This special edition of the Global Private Equity Barometer

on the Australian private equity market captured the views

of 35 private equity investors from around the world. The

Barometer’s findings are representative of the LP population

investing in Australia by:

Investor location

Type of investing organisation

Total assets under management

Length of experience of private equity investing

Contents

Key topics in this edition of the Barometer include:

LPs’ returns and appetite for PE in Australia

Prospects for PE dealflow

Attractive sectors for GP investment

Strengths of the Australian PE market

Risks facing Australian PE

Obstacles facing Australian venture capital

Risk/return profiles of key Asia-Pacific countries

A u s t r A l i A s n A p s h o t 3

LPs have done well from Australian buyouts

Half of investors have achieved net returns of 16%+ from their

investments in Australian buyouts.

Australian venture – like venture in Japan & Europe – has not

performed as strongly as buyouts. Just one in five LPs report

returns of 16%+ from Australian venture investments.

The apparently less robust performance of Australian venture

has not harmed LPs’ overall returns because the weight of

their exposure to Australian private equity is heavily biased

towards buyouts. Overseas investors in Australian PE tend to

have negligible allocations to venture, and even for Australian

investors venture is a relatively small part of their overall

commitments.

LPs expect strong Australian PE returns in the medium term

Three quarters of investors (77%) expect Australian buyouts

to yield net returns of 16%+ over the next 3-5 years. This

compares favourably with expected returns from buyouts in

other areas of the world.

LPs also have high expectations for Australian venture – over

half (55%) expect returns of 16%+.

lps achieving net returns of 16%+ from their portfolios since they began investing

(Figure 1)

Australianbuyouts

Australianventure

Japanesebuyouts

Japaneseventure

Asia-Pacific

buyoutsoverall

Asia-Pacific

ventureoverall

Europeanbuyouts

Europeanventure

NorthAmericanbuyouts

NorthAmericanventure

lps expecting net returns of 16%+ from their portfolios over the next 3-5 years

(Figure 2)

Australianbuyouts

Australianventure

Japanesebuyouts

Japaneseventure

Asia-Pacific

buyoutsoverall

Asia-Pacific

ventureoverall

Europeanbuyouts

Europeanventure

NorthAmericanbuyouts

NorthAmericanventure

A u s t r A l i A s n A p s h o t4

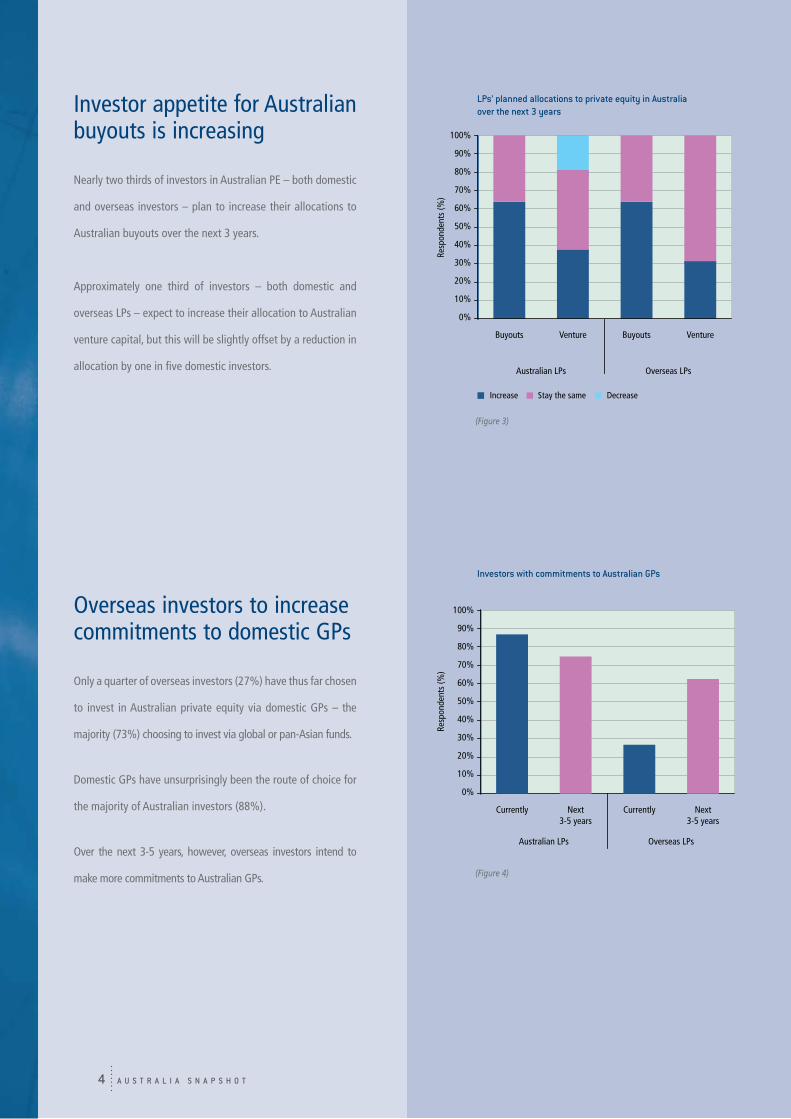

Investor appetite for Australian buyouts is increasing

Nearly two thirds of investors in Australian PE – both domestic

and overseas investors – plan to increase their allocations to

Australian buyouts over the next 3 years.

Approximately one third of investors – both domestic and

overseas LPs – expect to increase their allocation to Australian

venture capital, but this will be slightly offset by a reduction in

allocation by one in five domestic investors.

Overseas investors to increase commitments to domestic GPs

Only a quarter of overseas investors (27%) have thus far chosen

to invest in Australian private equity via domestic GPs – the

majority (73%) choosing to invest via global or pan-Asian funds.

Domestic GPs have unsurprisingly been the route of choice for

the majority of Australian investors (88%).

Over the next 3-5 years, however, overseas investors intend to

make more commitments to Australian GPs.

lps’ planned allocations to private equity in Australia over the next 3 years

(Figure 3)

investors with commitments to Australian Gps

(Figure 4)

Venture VentureBuyouts

Australian LPs Overseas LPs

Buyouts

Increase Stay the same Decrease

Next3-5 years

Next3-5 years

Currently

Australian LPs Overseas LPs

Currently

A u s t r A l i A s n A p s h o t 5

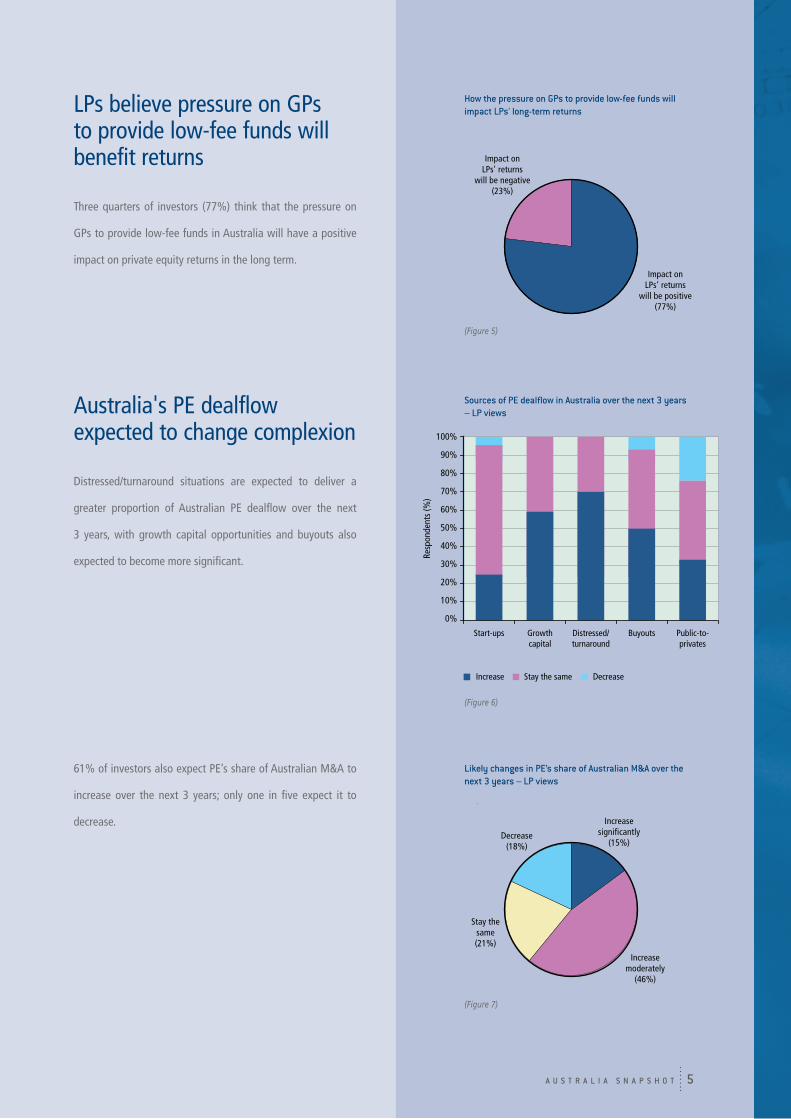

LPs believe pressure on GPs to provide low-fee funds will benefit returns

Three quarters of investors (77%) think that the pressure on

GPs to provide low-fee funds in Australia will have a positive

impact on private equity returns in the long term.

Australia's PE dealflow expected to change complexion

Distressed/turnaround situations are expected to deliver a

greater proportion of Australian PE dealflow over the next

3 years, with growth capital opportunities and buyouts also

expected to become more significant.

61% of investors also expect PE’s share of Australian M&A to

increase over the next 3 years; only one in five expect it to

decrease.

how the pressure on Gps to provide low-fee funds will impact lps' long-term returns

sources of pE dealflow in Australia over the next 3 years – lp views

likely changes in pE’s share of Australian M&A over the next 3 years – lp views

(Figure 5)

(Figure 6)

(Figure 7)

Impact onLPs’ returns

will be positive(77%)

Impact onLPs’ returns

will be negative(23%)

Growthcapital

Distressed/turnaround

Buyouts Public-to-privates

Start-ups

Increase Stay the same Decrease

Increasesignificantly

(15%)

Stay thesame(21%)

Decrease(18%)

Increasemoderately

(46%)

A u s t r A l i A s n A p s h o t6

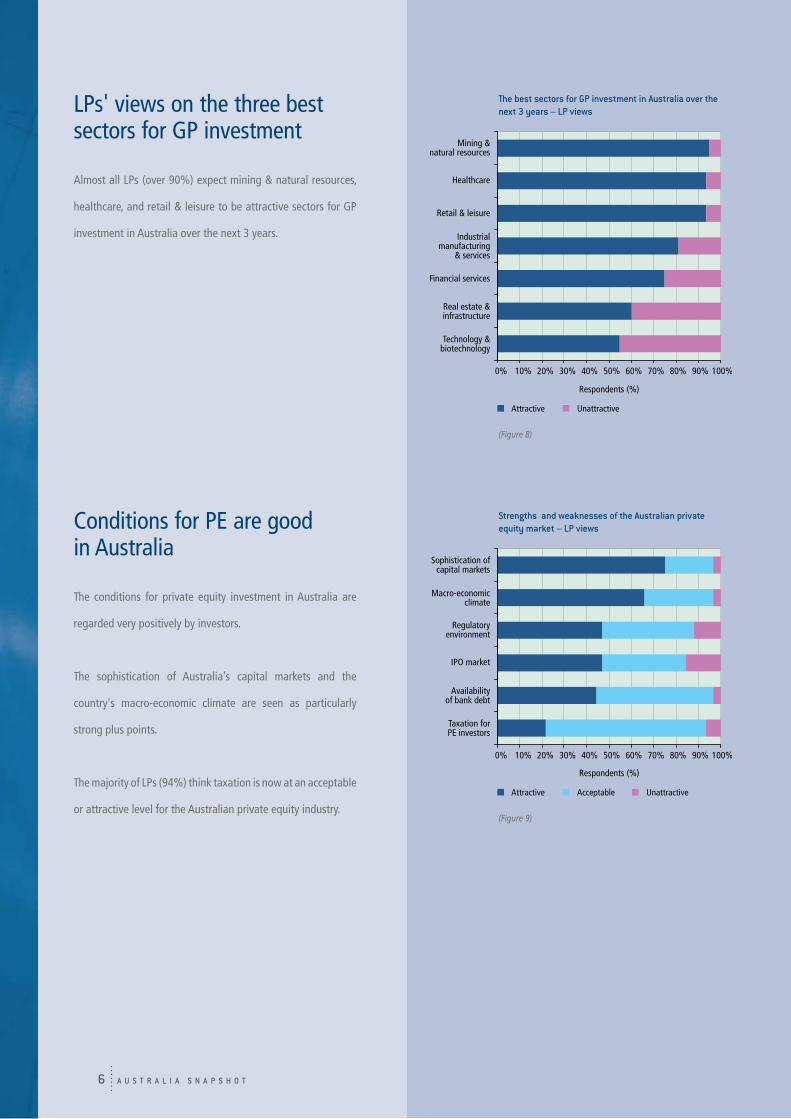

LPs' views on the three best sectors for GP investment

Almost all LPs (over 90%) expect mining & natural resources,

healthcare, and retail & leisure to be attractive sectors for GP

investment in Australia over the next 3 years.

Conditions for PE are good in Australia

The conditions for private equity investment in Australia are

regarded very positively by investors.

The sophistication of Australia’s capital markets and the

country's macro-economic climate are seen as particularly

strong plus points.

The majority of LPs (94%) think taxation is now at an acceptable

or attractive level for the Australian private equity industry.

the best sectors for Gp investment in Australia over the next 3 years – lp views

strengths and weaknesses of the Australian private equity market – lp views

(Figure 8)

(Figure 9)

Attractive Unattractive

Technology &biotechnology

Mining &natural resources

Healthcare

Retail & leisure

Financial services

Industrialmanufacturing

& services

Real estate &infrastructure

Attractive Acceptable Unattractive

Taxation forPE investors

Sophistication ofcapital markets

Macro-economicclimate

IPO market

Regulatoryenvironment

Availabilityof bank debt

A u s t r A l i A s n A p s h o t 7

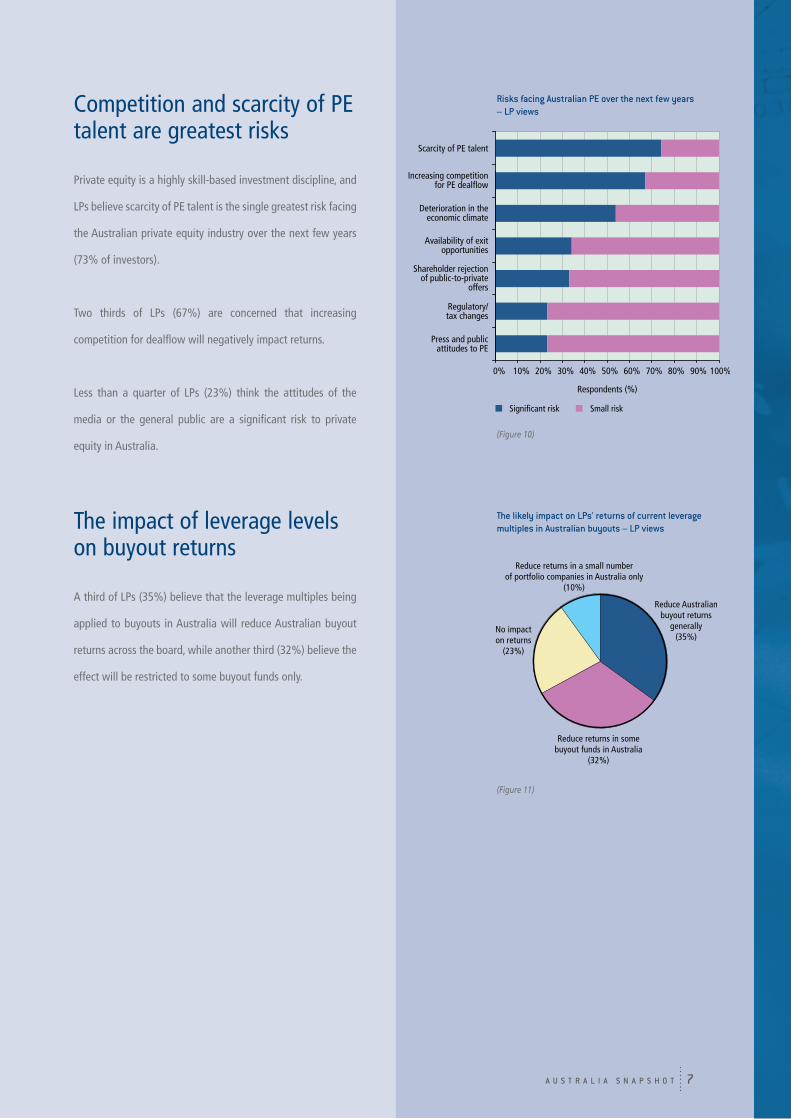

Competition and scarcity of PE talent are greatest risks

Private equity is a highly skill-based investment discipline, and

LPs believe scarcity of PE talent is the single greatest risk facing

the Australian private equity industry over the next few years

(73% of investors).

Two thirds of LPs (67%) are concerned that increasing

competition for dealflow will negatively impact returns.

Less than a quarter of LPs (23%) think the attitudes of the

media or the general public are a significant risk to private

equity in Australia.

risks facing Australian pE over the next few years – lp views

(Figure 10)

Significant risk Small risk

Press and publicattitudes to PE

Scarcity of PE talent

Availability of exitopportunities

Shareholder rejectionof public-to-private

offers

Deterioration in theeconomic climate

Increasing competitionfor PE dealflow

Regulatory/tax changes

The impact of leverage levels on buyout returns

A third of LPs (35%) believe that the leverage multiples being

applied to buyouts in Australia will reduce Australian buyout

returns across the board, while another third (32%) believe the

effect will be restricted to some buyout funds only.

the likely impact on lps' returns of current leverage multiples in Australian buyouts – lp views

(Figure 11)

Reduce Australianbuyout returns

generally(35%)

Reduce returns in somebuyout funds in Australia

(32%)

No impacton returns

(23%)

Reduce returns in a small numberof portfolio companies in Australia only

(10%)

A u s t r A l i A s n A p s h o t8

Skills and track records are in short supply in Australian venture capital

Two thirds of investors (62%) cite a lack of GPs with the

necessary skills and track record as a key factor reducing the

attractiveness of venture capital in Australia.

Another limiting factor is seen to be the relative under-

development of exit routes for Australian venture capital –

48% of LPs think exit routes are too few or too weak.

Overseas LPs believe it is too easy for ‘weak’ GPs to raise funds in Australia

Over half of overseas LPs (54%) say it is too easy for weak

GPs to raise funds in Australia. One third of Australian LPs

(31%) are of the same opinion.

Factors impacting the attractiveness of Australian venture capital – lp views

Ease with which weak Gps can raise funds in Australia – lp views

(Figure 12)

(Figure 13)

Significantly reduces attractiveness Not really a factor

Insufficient access tointernational commercial/

capital markets

Too few GPs withthe necessary skills

& track record

Exit routes are toofew/too weak

Unfavourable regulatory/tax environment

Entrepreneursreluctant to share ownership

of businesses

Australian marketplaceis too fragmented

Overseas investorsAustralian investors

No – it’s not easy forweak GPs to raise fundsin Australia

Yes – it’s too easy forweak GPs to raise fundsin Australia

A u s t r A l i A s n A p s h o t 9

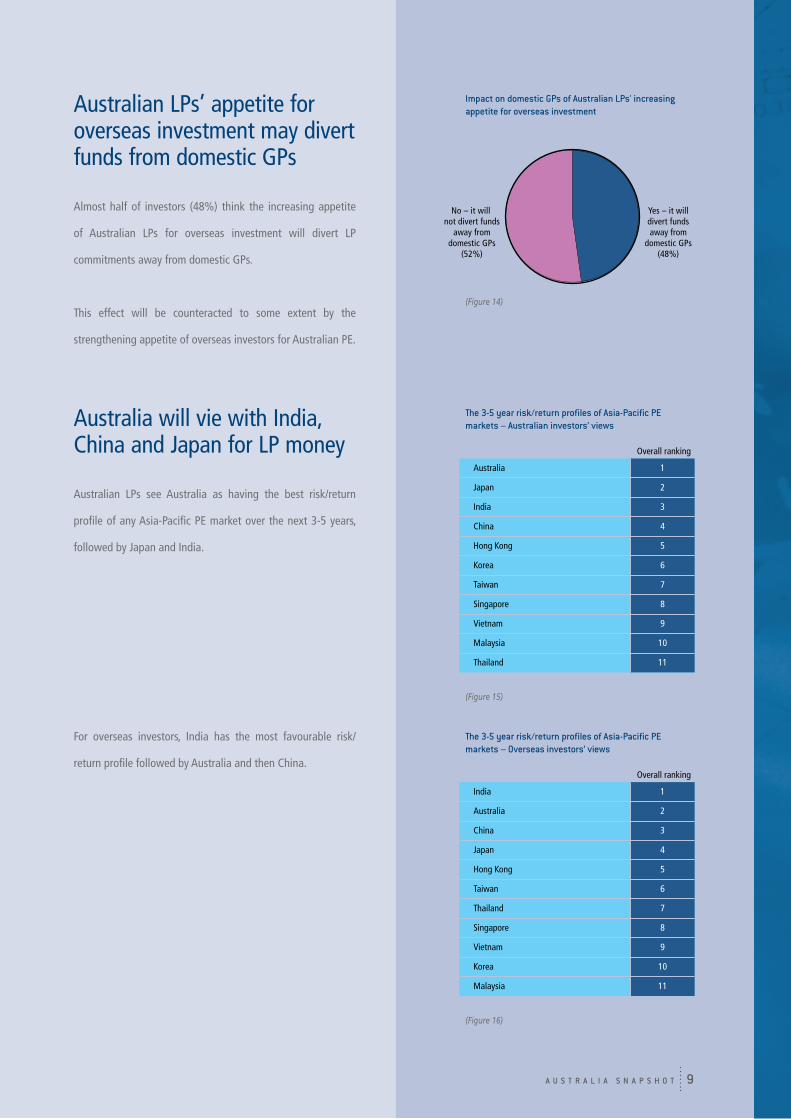

Australian LPs’ appetite for overseas investment may divert funds from domestic GPs

Almost half of investors (48%) think the increasing appetite

of Australian LPs for overseas investment will divert LP

commitments away from domestic GPs.

This effect will be counteracted to some extent by the

strengthening appetite of overseas investors for Australian PE.

Australia will vie with India, China and Japan for LP money

Australian LPs see Australia as having the best risk/return

profile of any Asia-Pacific PE market over the next 3-5 years,

followed by Japan and India.

For overseas investors, India has the most favourable risk/

return profile followed by Australia and then China.

impact on domestic Gps of Australian lps' increasing appetite for overseas investment

the 3-5 year risk/return profiles of Asia-pacific pE markets – Australian investors’ views

the 3-5 year risk/return profiles of Asia-pacific pE markets – overseas investors’ views

(Figure 14)

(Figure 15)

(Figure 16)

Yes – it willdivert fundsaway from

domestic GPs(48%)

No – it will not divert funds

away fromdomestic GPs

(52%)

Japan

India

China

Hong Kong

Korea

Taiwan

Singapore

Vietnam

Malaysia

Thailand

Australia 1

2

3

4

5

6

7

8

9

10

11

Australia

China

Japan

Hong Kong

Taiwan

Thailand

Singapore

Vietnam

Korea

Malaysia

India 1

2

3

4

5

6

7

8

9

10

11

A u s t r A l i A s n A p s h o t10

Respondents by region

(Figure 17)

Respondents by total assets under management

(Figure 18)

Respondents by type of organisation

(Figure 19)

Respondents by year in which they started to invest in Australian PE

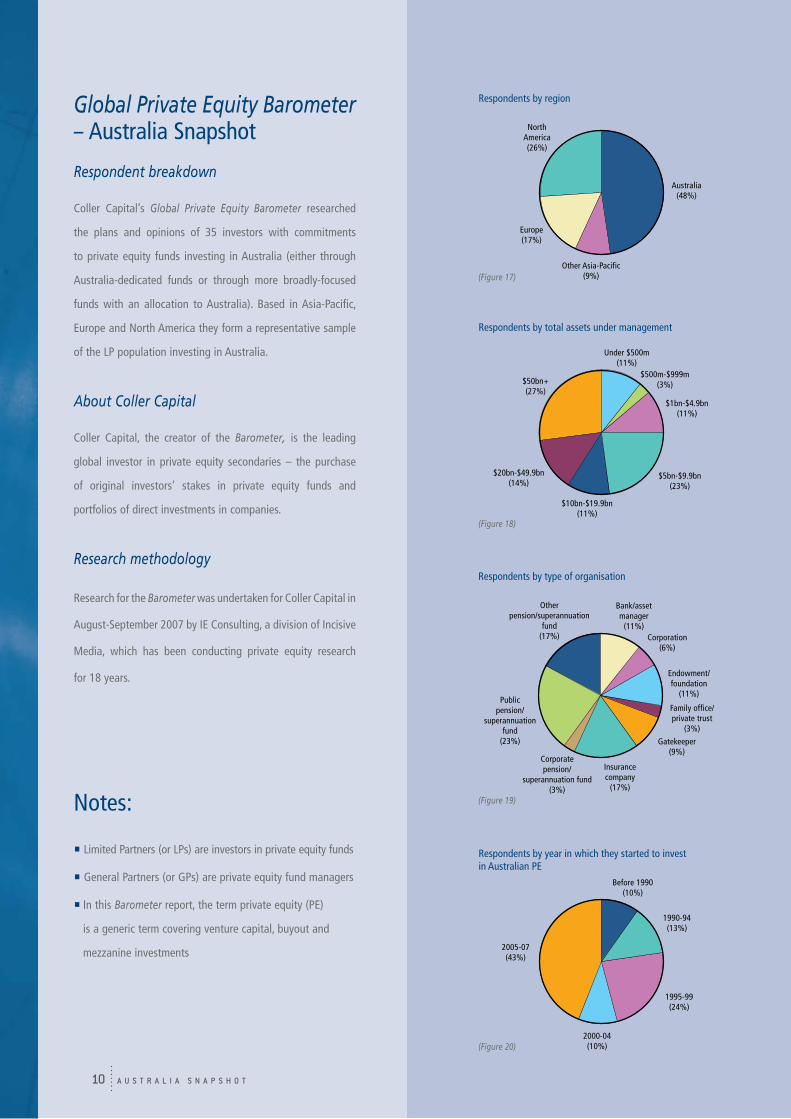

Global Private Equity Barometer – Australia Snapshot

Respondent breakdown

Coller Capital’s Global Private Equity Barometer researched

the plans and opinions of 35 investors with commitments

to private equity funds investing in Australia (either through

Australia-dedicated funds or through more broadly-focused

funds with an allocation to Australia). Based in Asia-Pacific,

Europe and North America they form a representative sample

of the LP population investing in Australia.

About Coller Capital

Coller Capital, the creator of the Barometer, is the leading

global investor in private equity secondaries – the purchase

of original investors’ stakes in private equity funds and

portfolios of direct investments in companies.

Research methodology

Research for the Barometer was undertaken for Coller Capital in

August-September 2007 by IE Consulting, a division of Incisive

Media, which has been conducting private equity research

for 18 years.

Notes:

Limited Partners (or LPs) are investors in private equity funds

General Partners (or GPs) are private equity fund managers

In this Barometer report, the term private equity (PE)

is a generic term covering venture capital, buyout and

mezzanine investments

Australia(48%)

Europe(17%)

NorthAmerica(26%)

Other Asia-Pacific(9%)

$1bn-$4.9bn(11%)

$5bn-$9.9bn(23%)

$10bn-$19.9bn(11%)

$20bn-$49.9bn(14%)

$50bn+(27%)

Under $500m(11%)

$500m-$999m(3%)

Bank/assetmanager

(11%)Corporation

(6%)

Endowment/foundation

(11%)

Family office/private trust

(3%)

Gatekeeper(9%)

Insurancecompany

(17%)

Corporatepension/

superannuation fund(3%)

Publicpension/

superannuationfund

(23%)

Otherpension/superannuation

fund(17%)

Before 1990(10%)

1990-94(13%)

1995-99(24%)

2000-04(10%)

2005-07(43%)

(Figure 20)

www.collercapital.com