Embed Size (px)

Citation preview

Global Poultry Sector Trends and External Drivers for Structural

Change

Presented by:

Clare NarrodCo-authors:

Marites Tiongco and Achilles Costales

Eugenia Saini

What is the future of smallholders?

Livestock Industrialization Process

Rapid changes happening; many smallholders moving out of livestock

production-poultry sector no exception

Talk covers

1. What are the external drivers of change promoting the industrialization process?

2. What has happened to poultry smallholders in the process of industrialization?

3. Will changing demands for food safety, food quality, and ensuring animal health disfavour smallholders?

4. Are there opportunities for smallholders to be competitive in the market given the changing structure of the poultry sector?

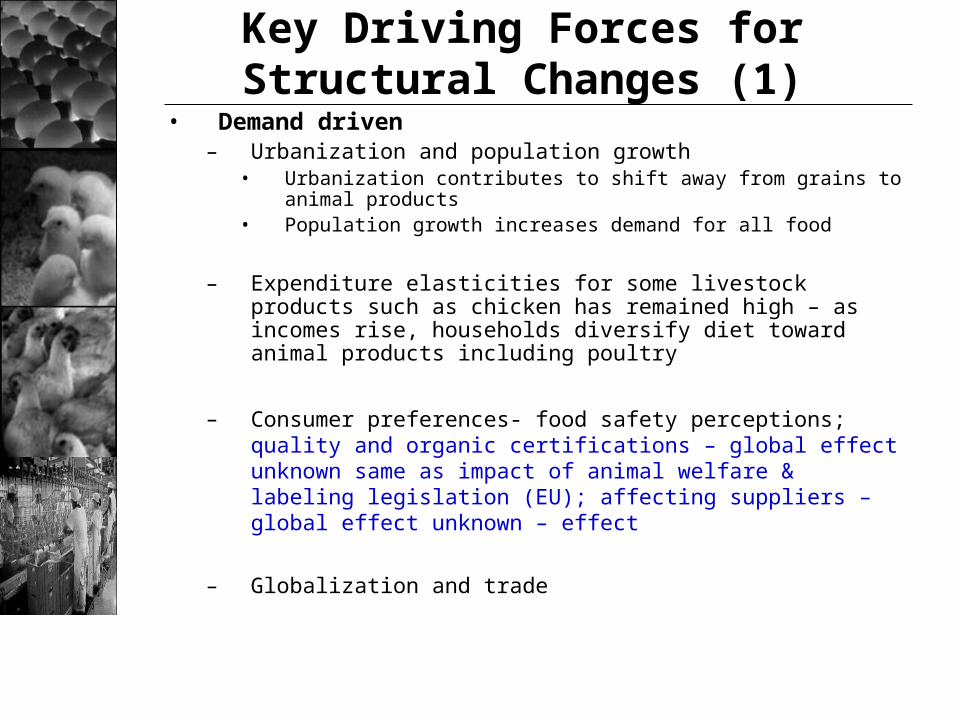

Key Driving Forces for Structural Changes (1)

• Demand driven– Urbanization and population growth

• Urbanization contributes to shift away from grains to animal products

• Population growth increases demand for all food

– Expenditure elasticities for some livestock products such as chicken has remained high – as incomes rise, households diversify diet toward animal products including poultry

– Consumer preferences- food safety perceptions; quality and organic certifications – global effect unknown same as impact of animal welfare & labeling legislation (EU); affecting suppliers – global effect unknown – effect

– Globalization and trade

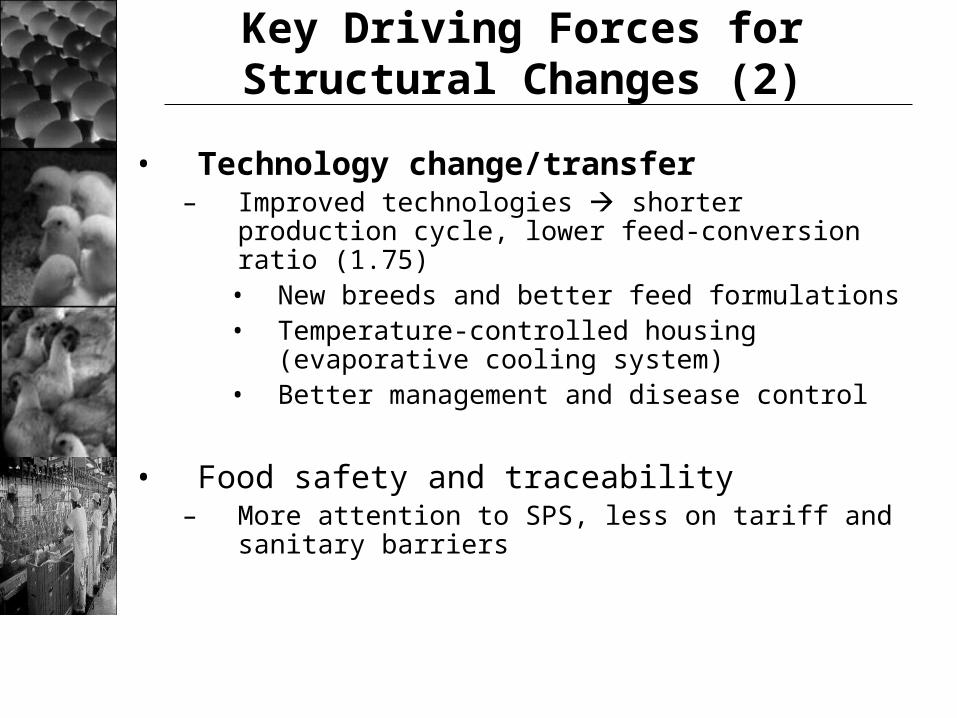

Key Driving Forces for Structural Changes (2)

• Technology change/transfer– Improved technologies shorter production cycle, lower

feed-conversion ratio (1.75) • New breeds and better feed formulations• Temperature-controlled housing (evaporative cooling

system) • Better management and disease control

• Food safety and traceability– More attention to SPS, less on tariff and sanitary barriers

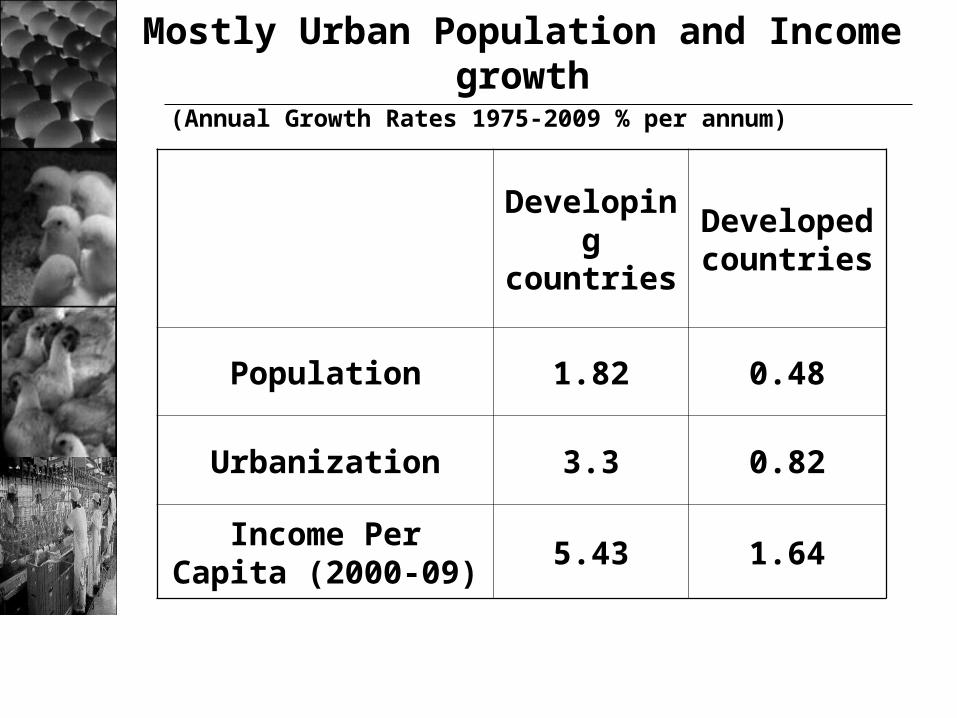

Mostly Urban Population and Income growth

(Annual Growth Rates 1975-2009 % per annum)

Developing countries

Developed countries

Population 1.82 0.48

Urbanization 3.3 0.82

Income Per Capita (2000-09)

5.43 1.64

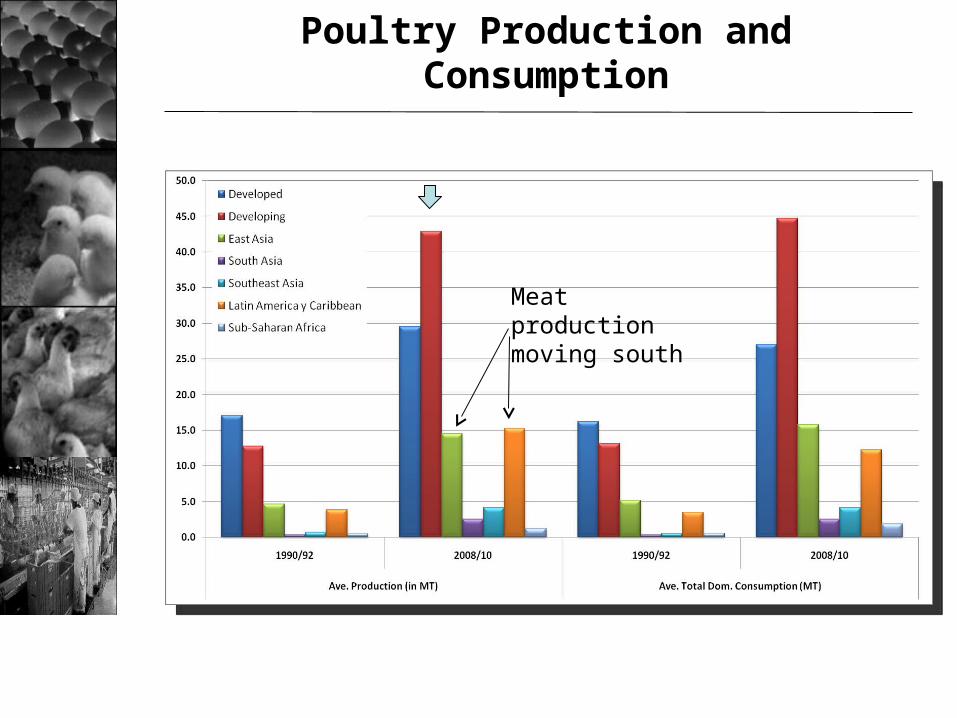

Poultry Production and Consumption

Meat production moving south

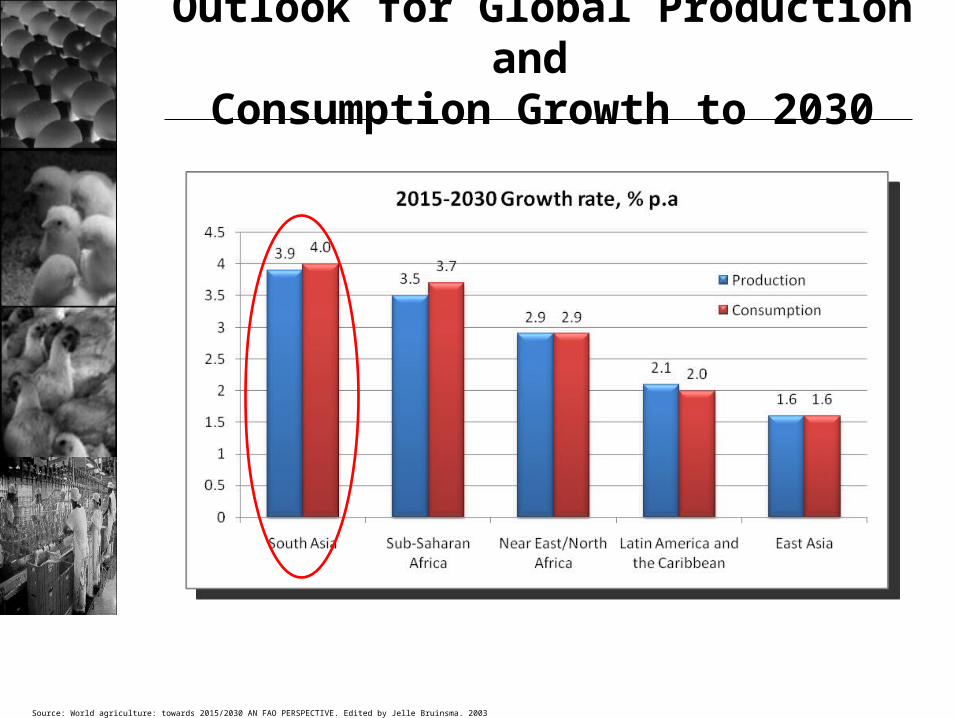

Outlook for Global Production and Consumption Growth to 2030

Source: World agriculture: towards 2015/2030 AN FAO PERSPECTIVE. Edited by Jelle Bruinsma. 2003

Major Trends Driving Growth

• Increasing per capita consumption of livestock products (worldwide)

• Moving toward more consolidated larger production system (Brazil, Thailand)

• Increasing “borderless movements” of commodities and inputs

Increases in productivity in LDC’s paralleled those in DC’s

Developing countries steadily transiting to more specialized enterprises using hired labour, borrowed capital, and purchased inputs so as to produce a more uniform quality livestock product under different modes of industrial organization so as to meet demand worldwide.

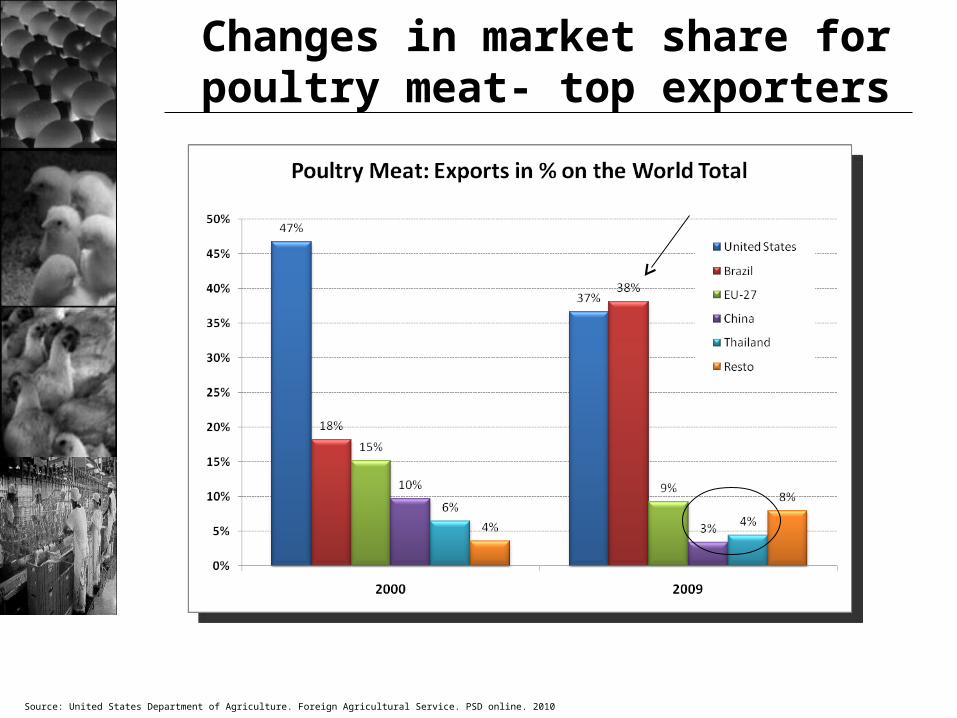

Changes in market share for poultry meat- top exporters

Source: United States Department of Agriculture. Foreign Agricultural Service. PSD online. 2010

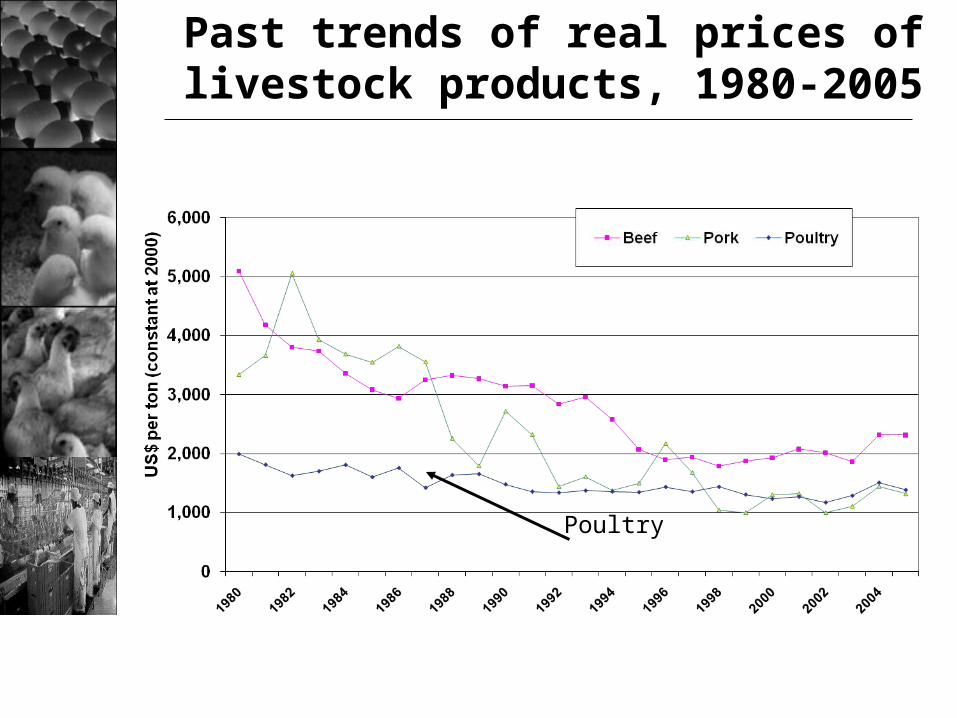

Past trends of real prices of livestock products, 1980-2005

Poultry

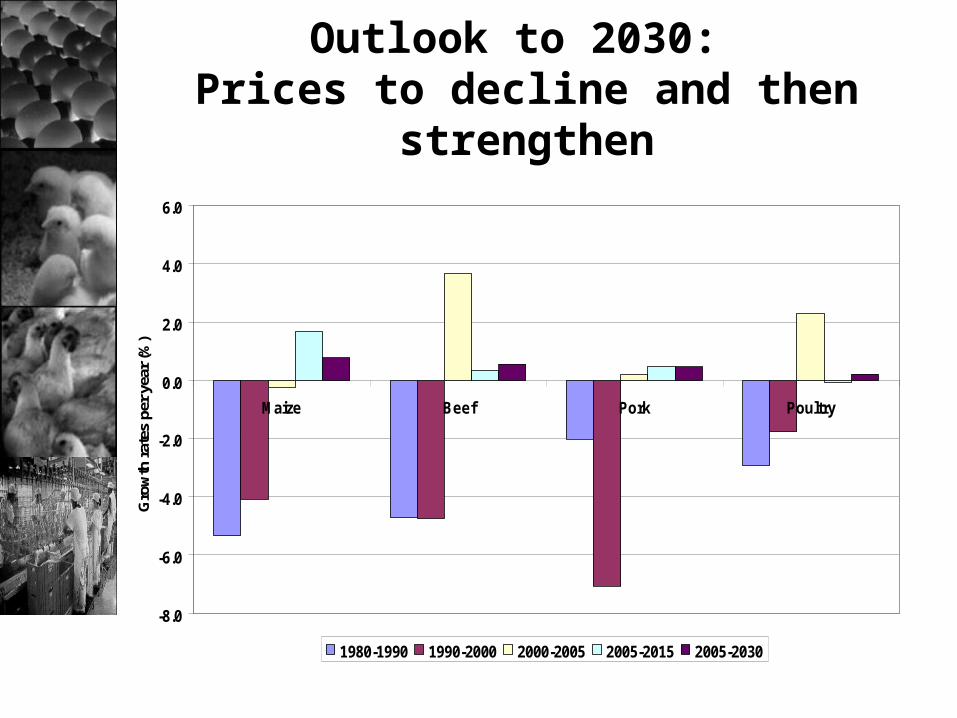

Outlook to 2030: Prices to decline and then strengthen

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

Maize Beef Pork Poultry

Gro

wth

rat

es p

er y

ear

(%)

1980-1990 1990-2000 2000-2005 2005-2015 2005-2030

What has happened to smallholders?

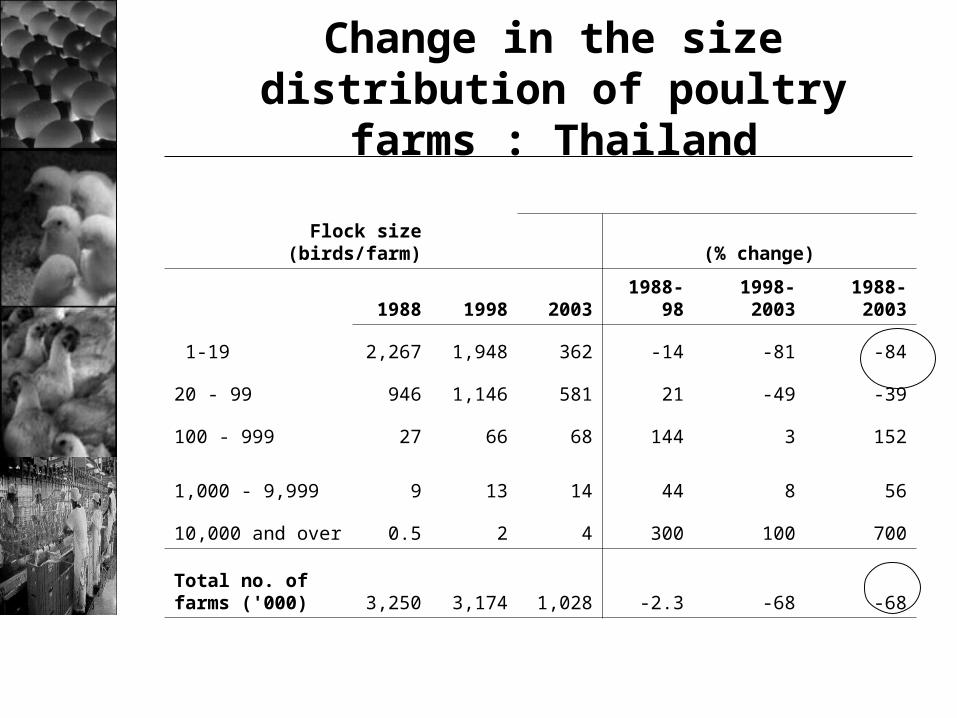

Change in the size distribution of poultry farms : Thailand

Flock size (birds/farm) (% change)

1988 1998 2003 1988-98 1998-2003 1988-2003

1-19 2,267 1,948 362 -14 -81 -84

20 - 99 946 1,146 581 21 -49 -39

100 - 999 27 66 68 144 3 152

1,000 - 9,999 9 13 14 44 8 56

10,000 and over 0.5 2 4 300 100 700

Total no. of farms ('000) 3,250 3,174 1,028 -2.3 -68 -68

What is happening to the smallholders? (cont.)

• Most work to date is descriptive, little systematic empirical analysis.

• (2002 – 2006) - number of colleagues set out to empirically capture various factors affecting profitability including transaction costs and efforts to mitigate against environmental externalities for different size producers in a number of countries involving HH surveys

• Case studies in Thailand, the Philippines, India, and Brazil

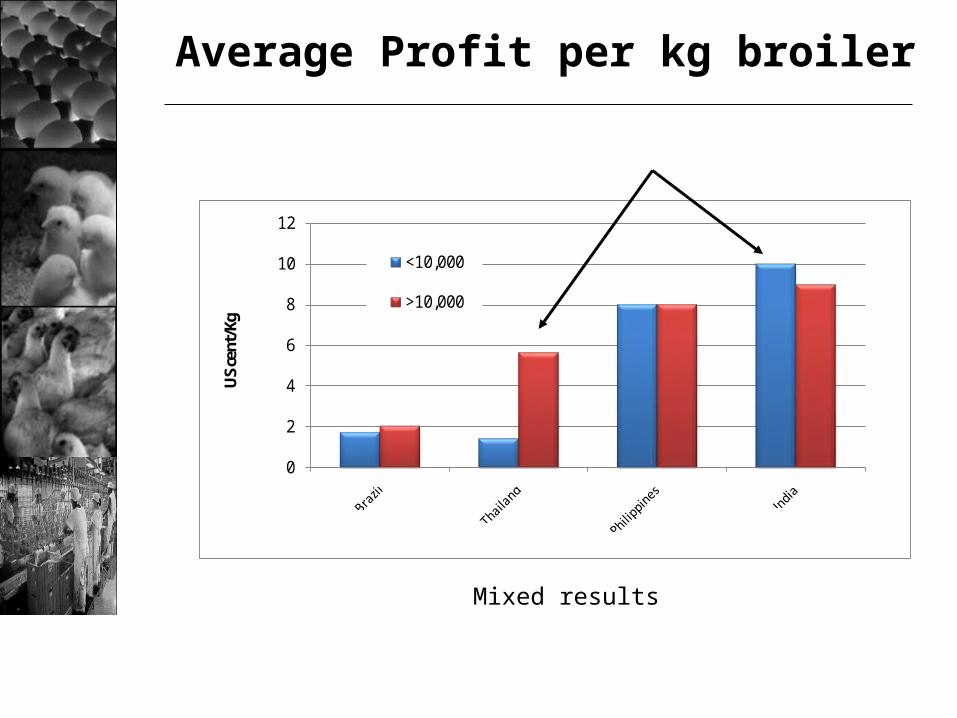

Average Profit per kg broiler

0

2

4

6

8

10

12US

cent

/Kg

<10,000

>10,000

Mixed results

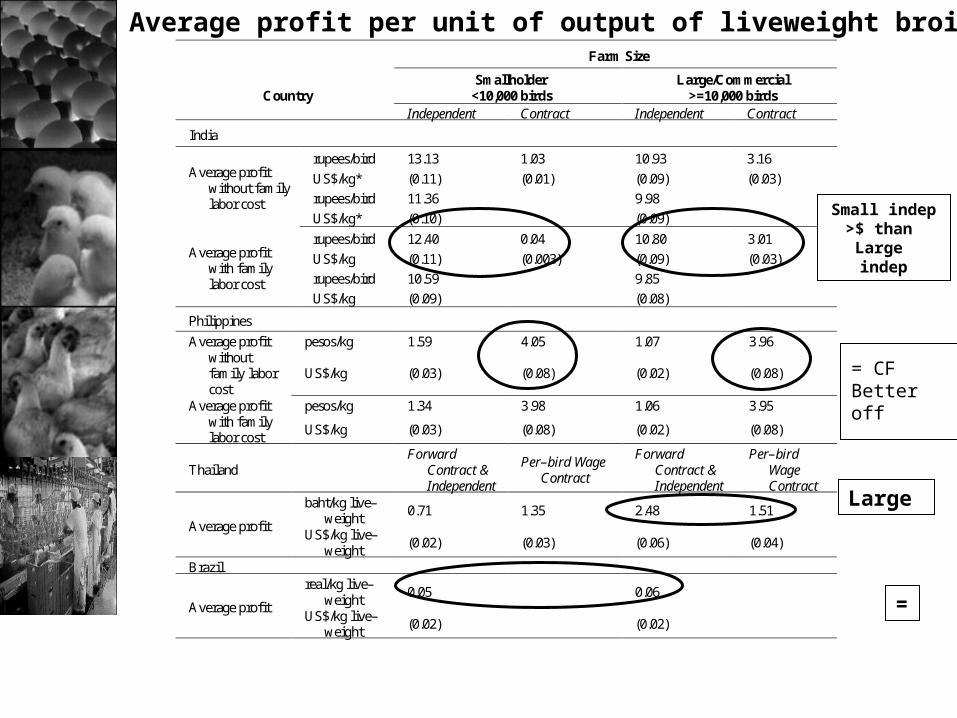

Farm Size

Smallholder <10,000 birds

Large/Commercial >=10,000 birds Country

Independent Contract Independent Contract

India

rupees/bird 13.13 1.03 10.93 3.16

US$/kg* (0.11) (0.01) (0.09) (0.03)

rupees/bird 11.36 9.98

Average profit without family labor cost

US$/kg* (0.10) (0.09)

rupees/bird 12.40 0.04 10.80 3.01

US$/kg (0.11) (0.003) (0.09) (0.03)

rupees/bird 10.59 9.85

Average profit with family labor cost

US$/kg (0.09) (0.08)

Philippines

pesos/kg 1.59 4.05 1.07 3.96 Average profit without family labor cost

US$/kg (0.03) (0.08) (0.02) (0.08)

pesos/kg 1.34 3.98 1.06 3.95 Average profit with family labor cost

US$/kg (0.03) (0.08) (0.02) (0.08)

Thailand Forward

Contract & Independent

Per–bird Wage Contract

Forward Contract & Independent

Per–bird Wage Contract

baht/kg live–weight

0.71 1.35 2.48 1.51 Average profit

US$/kg live–weight

(0.02) (0.03) (0.06) (0.04)

Brazil real/kg live–

weight 0.05 0.06

Average profit US$/kg live–

weight (0.02) (0.02)

Average profit per unit of output of liveweight broiler

Large

=

Small indep>$ than Large indep

= CF Better off

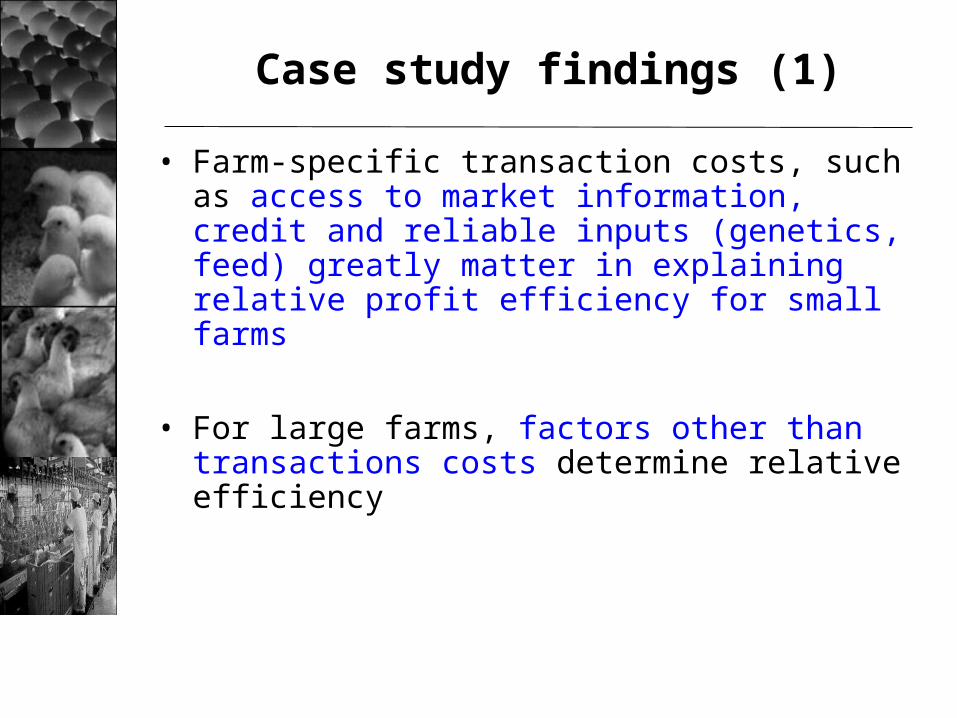

Case study findings (1)

• Farm-specific transaction costs, such as access to market information, credit and reliable inputs (genetics, feed) greatly matter in explaining relative profit efficiency for small farms

• For large farms, factors other than transactions costs determine relative efficiency

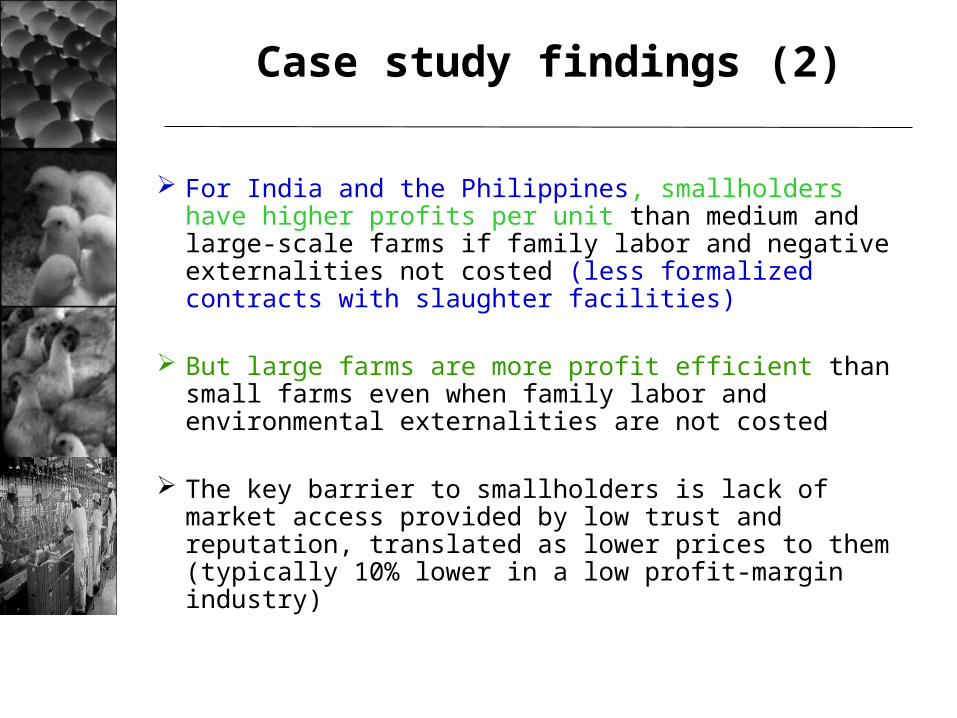

Case study findings (2)

For India and the Philippines, smallholders have higher profits per unit than medium and large-scale farms if family labor and negative externalities not costed (less formalized contracts with slaughter facilities)

But large farms are more profit efficient than small farms even when family labor and environmental externalities are not costed

The key barrier to smallholders is lack of market access provided by low trust and reputation, translated as lower prices to them (typically 10% lower in a low profit-margin industry)

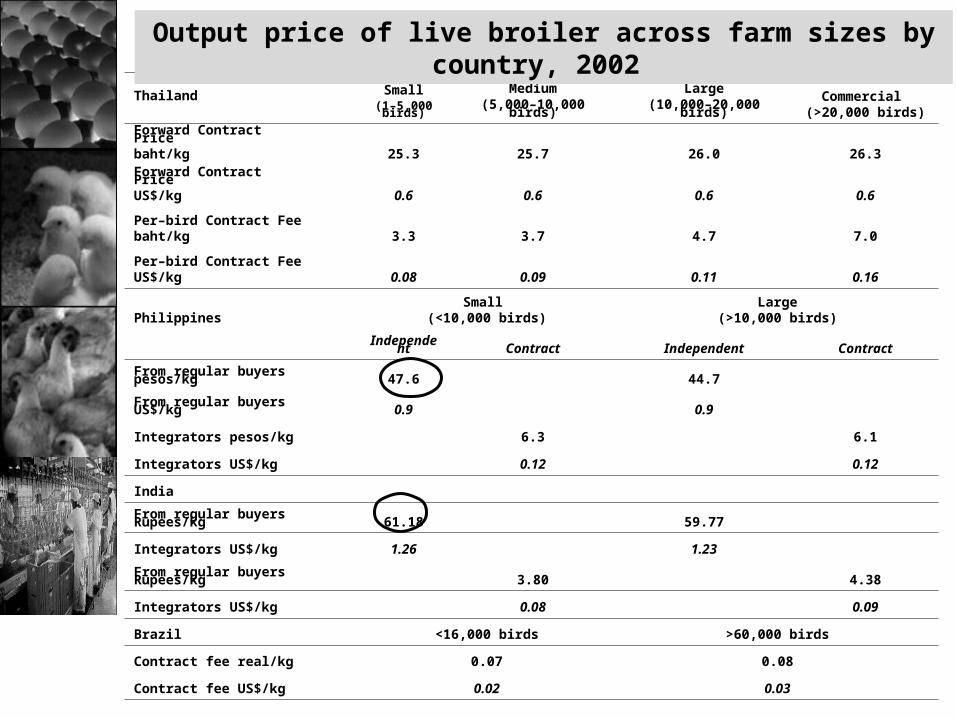

Thailand Small(1–5,000

birds)Medium

(5,000–10,000 birds)Large

(10,000–20,000 birds)Commercial

(>20,000 birds)

Forward Contract Price baht/kg 25.3 25.7 26.0 26.3

Forward Contract Price US$/kg 0.6 0.6 0.6 0.6

Per–bird Contract Fee baht/kg 3.3 3.7 4.7 7.0

Per–bird Contract Fee US$/kg 0.08 0.09 0.11 0.16

PhilippinesSmall

(<10,000 birds)Large

(>10,000 birds)

Independent Contract Independent Contract

From regular buyers pesos/kg 47.6 44.7

From regular buyers US$/kg 0.9 0.9

Integrators pesos/kg 6.3 6.1

Integrators US$/kg 0.12 0.12

India

From regular buyers Rupees/kg 61.18 59.77

Integrators US$/kg 1.26 1.23

From regular buyers Rupees/kg 3.80 4.38

Integrators US$/kg 0.08 0.09

Brazil <16,000 birds >60,000 birds

Contract fee real/kg 0.07 0.08

Contract fee US$/kg 0.02 0.03

Output price of live broiler across farm sizes by country, 2002

Overall implications

Small farms are not less efficient in all cases at securing profits per unit of output when family labour and environmental externalities are controlled for.

– For smallholders to survive livestock industrialization process, the key issue is the ability to use farm resources more efficiently than large-scale producers.

– If large–scale producers are more efficient on average, then they will be able to drive their costs down and survive on smaller unit profits and bigger volume of sales.

• Possible that smallholders will be driven out of the market because of their small volume of production.

– But smallholders have a chance; • Issue is access to output markets, since they face high

transaction costs in selling – Contract farming schemes in some cases enables

smallholders to remain as profitable as medium and large farmers

• if they are able to successfully link to the rest of the supply chain

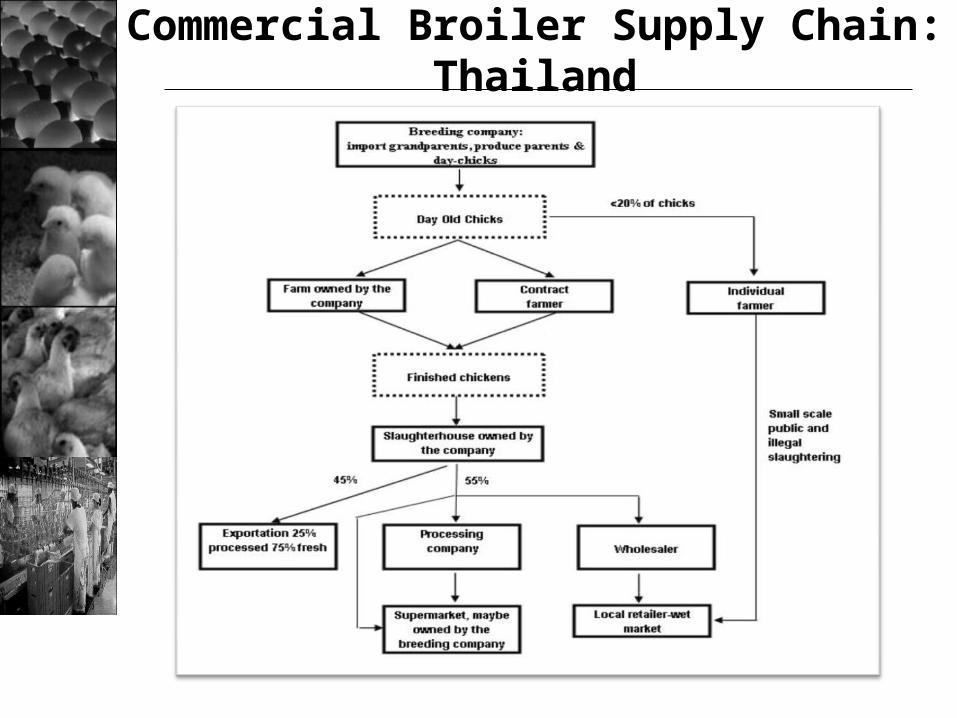

Commercial Broiler Supply Chain: Thailand

Types of markets and their characteristics

• Traditional local markets

• Dynamic urban domestic markets

• Export markets

• Food safety control• Standardization, grading,

supply• Supply chain organization• Price level for grower and

consumer• Value added• Participation of

smallholders

Increased demand for ensuring the delivery of animal sourced foods with

specific attributes

Emerging food systems are trying to meet the high demands of food safety, traceability and compliance and ensuring animal health often disfavour smallholders over larger operations for supplying specific supply chains due to: – high coordination costs– high transaction and marketing costs of

sourcing from smallholders

Events Beyond Farmers and Integrators

• There are large economies of scale in marketing chains, where transactions costs also abound

• Food safety concerns and demand for reliable timing and quality drives concentration of supermarkets

• Cheaper to monitor safety & quality from a few larger farms—even most reliable and safe small farmer may be unattractive

• Scaling-up of wholesaling probably leads to scaling-up of primary producers

Global Concerns Possibly Affecting the Viability of Smallholdings

• Disease-free certified export zones within developing countries increase pressures for monitored sanitary and traceability compliance by all, current technology or control measures are scale-neutral

• Need to understand how the rapidly changing food safety, animal disease control, and trade policy environment in developed countries will affect developing countries (directly/indirectly) and smallholders in particular

• Need to also understand how location of production, people, and zoonotic diseases might be intertwined and how this might affect developing countries current producers

Market failures effecting smallholder’s market access

Presence of market failures1. information asymmetry and transaction costs

2. organizational constraints

3. regulatory failure •

Information Problems-zoonotic diseases – food safety

• Lack of information due to poor surveillance – Agents do not know the state, hence a case of imperfect information.

• Incomplete information regarding strategies and payoffs about different players who determine the occurrence or transmission of the disease.

• Asymmetric information-lack of credibility of institutions to diagnose the problem in animals thus selling the idea to stakeholders along the value chain.

• Adverse selection problems relating to the information asymmetry where livestock keepers know the disease status and the public agencies do not.

Reality is that smallholders might disappear

Even if they have market access…they may be unable to meet

• High transaction costs for certain market outlets• Costs of compliance to meet standards:

– Import requirements...disease status, traceability, animal welfare, GAP, SPS, compulsory inspection

– Product requirement.....quality cuts, hygiene standards, packaging, labelling, traceability

• Changing marketing channels– concentration in export, processing, and retailing – changes in vertical coordination of supply chains (for

example, thought Thailand switched from contract farming to full vertical integration because of disease threat (AI)- not happening as expected)