Embed Size (px)

Citation preview

Global Market Trends & Traps

Produced by: Robert Parker, Senior Advisor, Credit Suisse March 2010

Slide 2

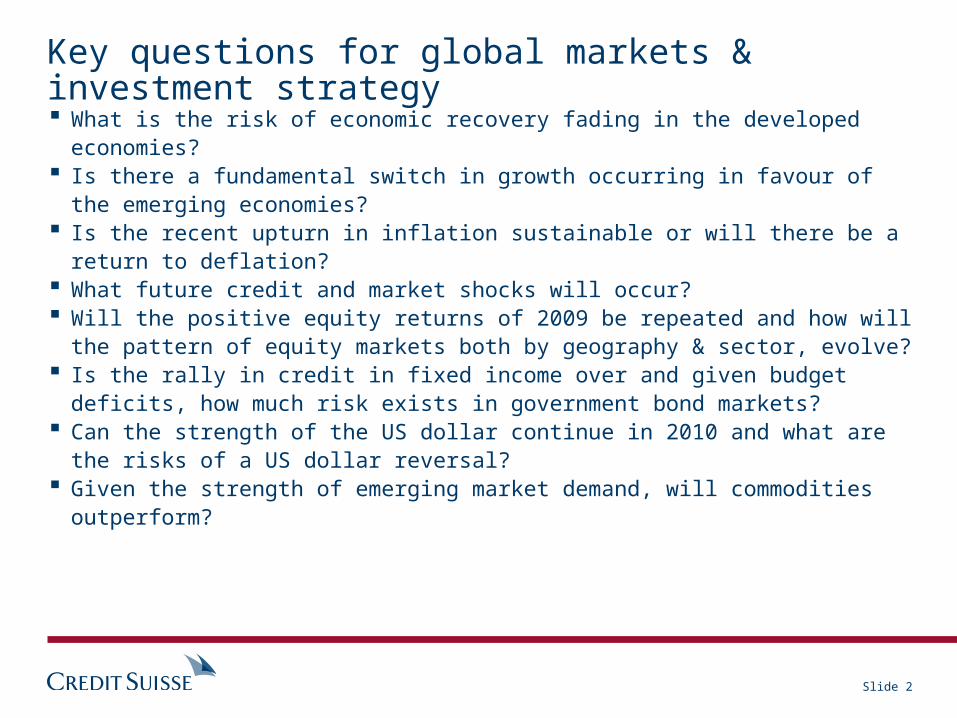

Key questions for global markets & investment strategy What is the risk of economic recovery fading in the developed

economies? Is there a fundamental switch in growth occurring in favour of the

emerging economies? Is the recent upturn in inflation sustainable or will there be a return to

deflation? What future credit and market shocks will occur? Will the positive equity returns of 2009 be repeated and how will the

pattern of equity markets both by geography & sector, evolve? Is the rally in credit in fixed income over and given budget deficits, how

much risk exists in government bond markets? Can the strength of the US dollar continue in 2010 and what are the

risks of a US dollar reversal? Given the strength of emerging market demand, will commodities

outperform?

Slide 3

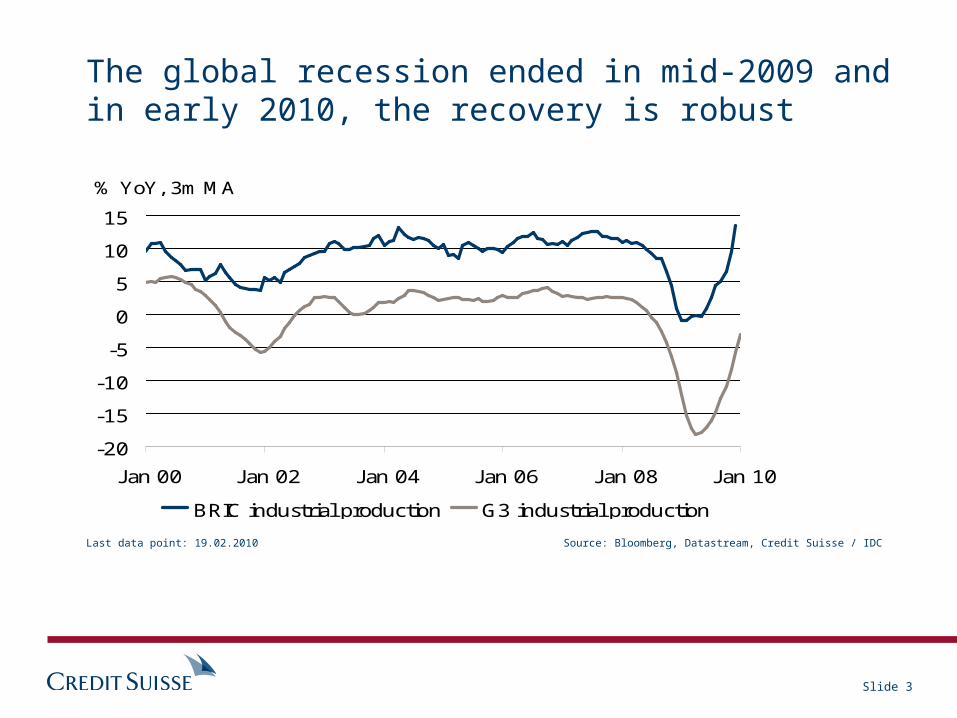

The global recession ended in mid-2009 and in early 2010, the recovery is robust

-20

-15

-10

-5

0

5

10

15

J an 00 J an 02 J an 04 J an 06 J an 08 J an 10

BRIC industrial production G3 industrial production

% YoY, 3m MA

Source: Bloomberg, Datastream, Credit Suisse / IDCLast data point: 19.02.2010

Slide 4

-4.0

-3.0

-2.0

-1.0

0

1.0

2.0

3.0

4.0

5.0

6.0

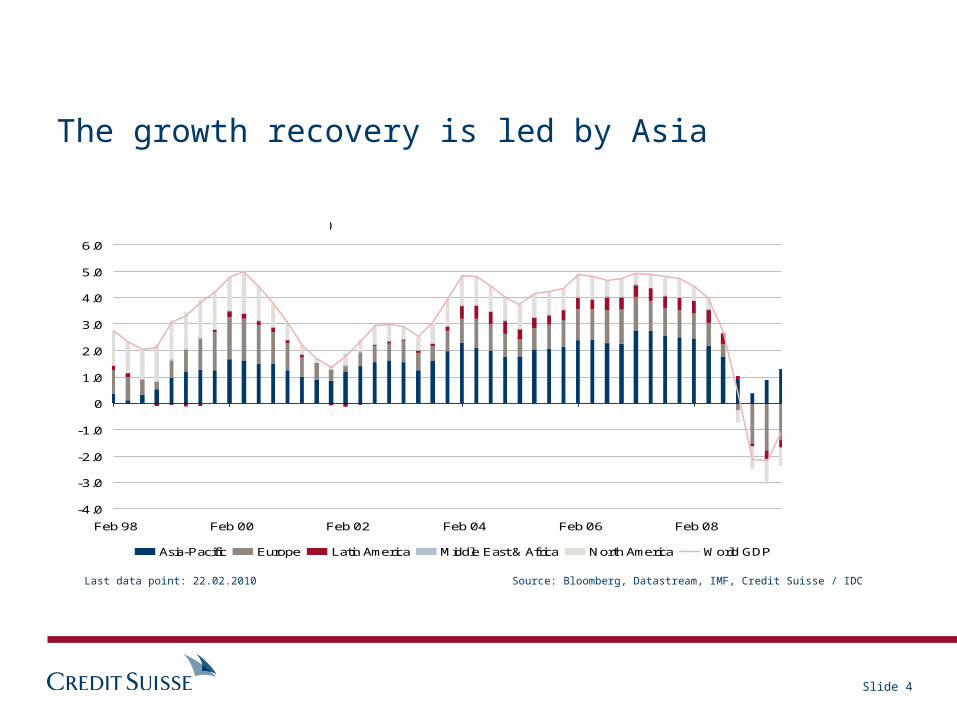

Feb 98 Feb 00 Feb 02 Feb 04 Feb 06 Feb 08

Asia-Pacific Europe Latin America Middle East & Africa North America World GDP

Contribution to YoY World GDP Growth (%)

The growth recovery is led by Asia

Last data point: 22.02.2010 Source: Bloomberg, Datastream, IMF, Credit Suisse / IDC

Slide 5

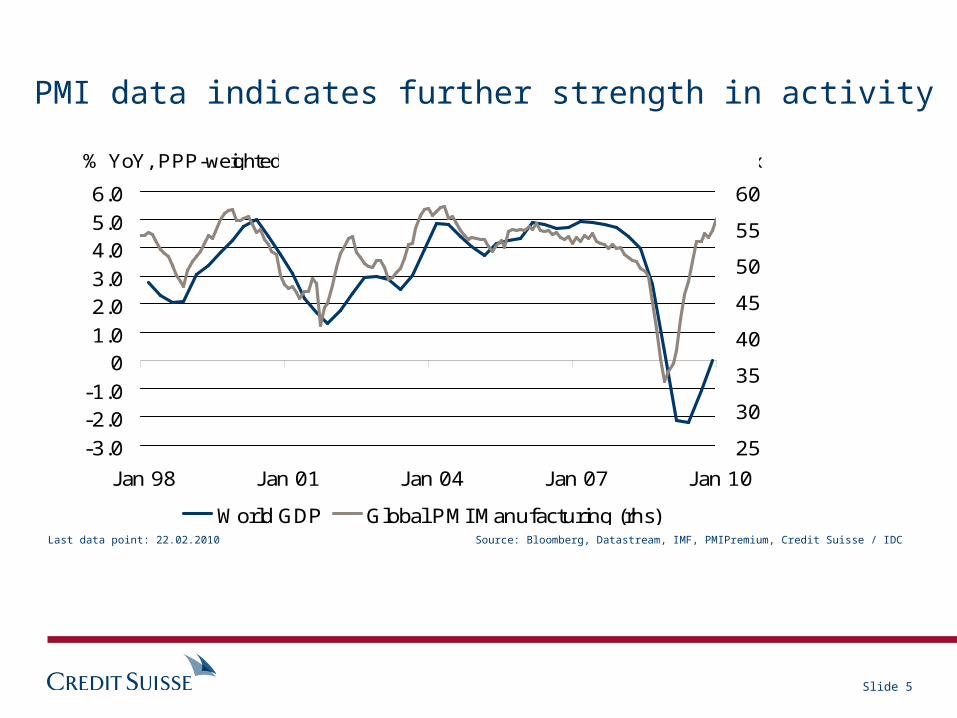

-3.0-2.0-1.0

01.02.03.04.05.06.0

J an 98 J an 01 J an 04 J an 07 J an 10

25

30

35

40

45

50

55

60

World GDP Global PMI Manufacturing (rhs)

% YoY, PPP-weighted Index

PMI data indicates further strength in activity

Last data point: 22.02.2010 Source: Bloomberg, Datastream, IMF, PMIPremium, Credit Suisse / IDC

Slide 6

25

30

35

40

45

50

55

60

J an 07 J ul 07 J an 08 J ul 08 J an 09 J ul 09 J an 10

China PMI Eurozone PMI UK PMI J apan PMI US PMI

In the next six months, the UK and the Eurozone PMI’s should lag the US & Asia

Last data point: 22.02.2010 Source: Bloomberg, Credit Suisse / IDC

Slide 7

-3-2-10123456

J an 00 J an 02 J an 04 J an 06 J an 08

EMU CPI J P CPI US CPI CH CPI

% YoY

Japan still has deflation, while inflation in the US & Europe is peaking

Source: Bloomberg, Credit Suisse / IDCLast data point: 31.01.2010

Slide 8

0

20

40

60

80

100

120

140

160

FED ECB BOJ BOE BOC RBA RBNZ SNB

Cumulative interest rate expectations over 12 months, current

in bp

Cumulative interest rate expectations over 12 months

Source: Bloomberg, Credit Suisse / IDCLast data point: 19.02.2010

In the US and Europe, interest rate tightening will be slow. Japan will not raise rates

Slide 9

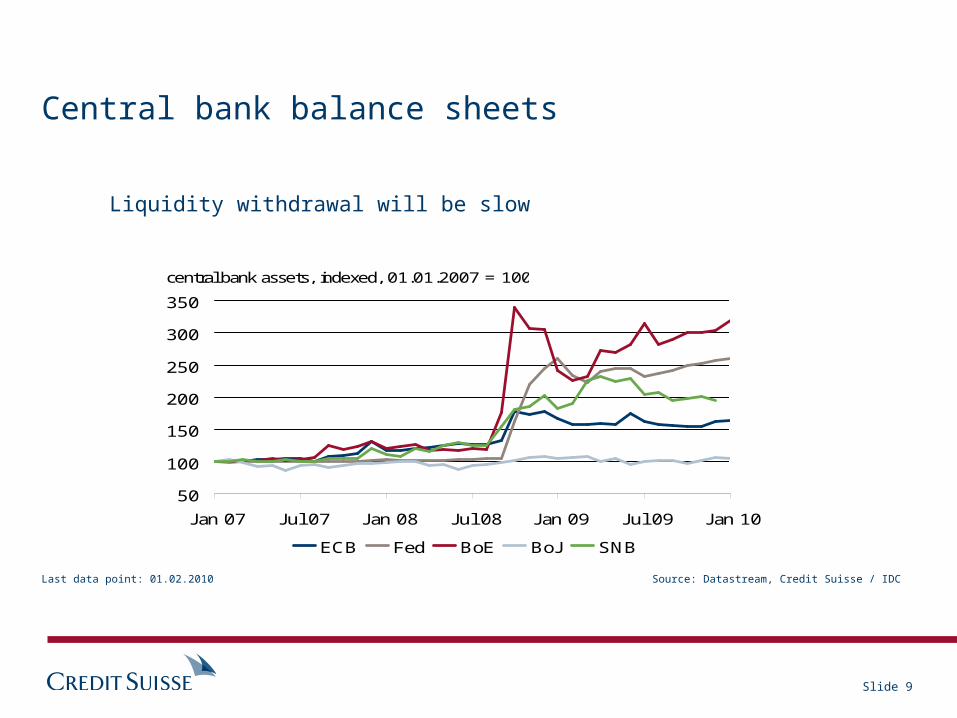

50

100

150

200

250

300

350

J an 07 J ul 07 J an 08 J ul 08 J an 09 J ul 09 J an 10

ECB Fed BoE BoJ SNB

central bank assets, indexed, 01.01.2007 = 100

Central bank balance sheets

Liquidity withdrawal will be slow

Source: Datastream, Credit Suisse / IDCLast data point: 01.02.2010

Slide 10

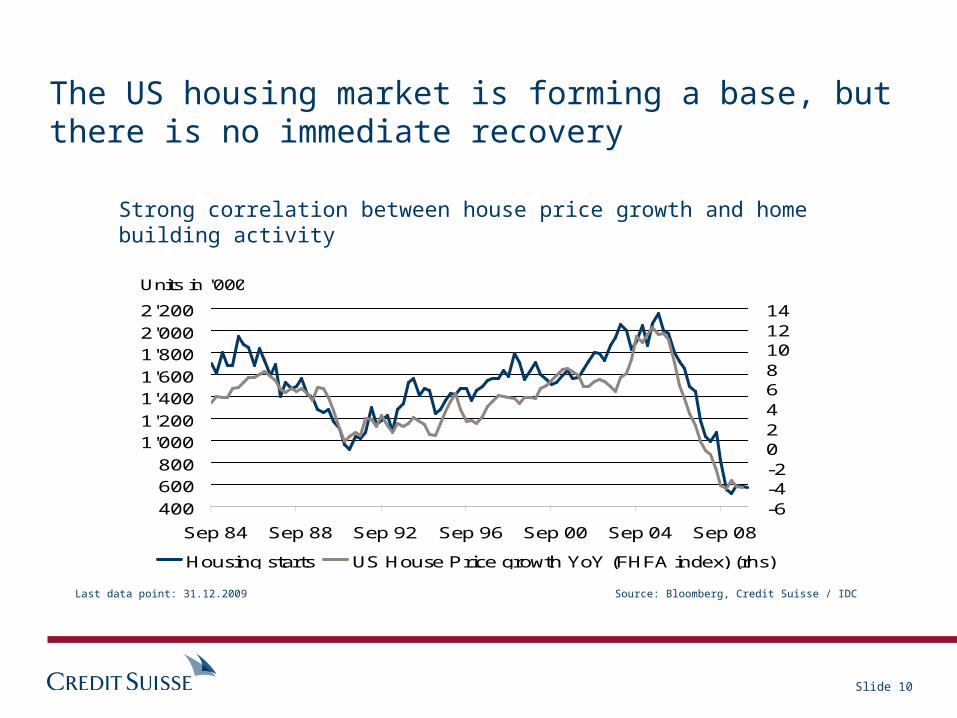

400600800

1'0001'2001'4001'6001'8002'0002'200

Sep 84 Sep 88 Sep 92 Sep 96 Sep 00 Sep 04 Sep 08

-6-4-202468101214

Housing starts US House Price growth YoY (FHFA index) (rhs)

Units in '000 % YoY

The US housing market is forming a base, but there is no immediate recovery

Strong correlation between house price growth and home building activity

Source: Bloomberg, Credit Suisse / IDCLast data point: 31.12.2009

Slide 11

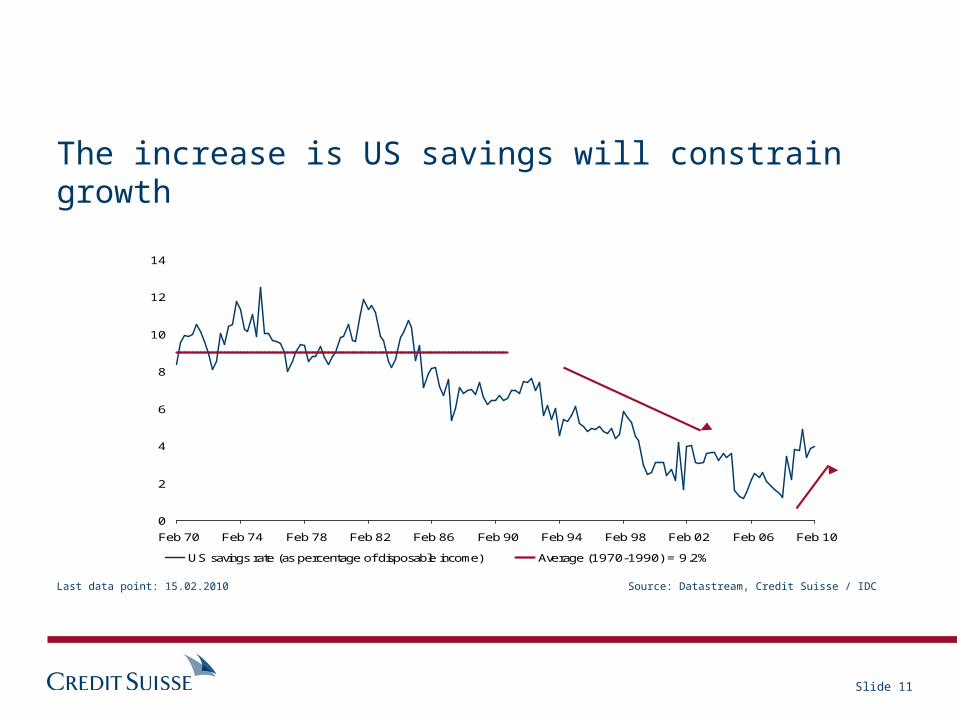

0

2

4

6

8

10

12

14

Feb 70 Feb 74 Feb 78 Feb 82 Feb 86 Feb 90 Feb 94 Feb 98 Feb 02 Feb 06 Feb 10

US savings rate (as percentage of disposable income) Average (1970-1990) = 9.2%

%

The increase is US savings will constrain growth

Source: Datastream, Credit Suisse / IDCLast data point: 15.02.2010

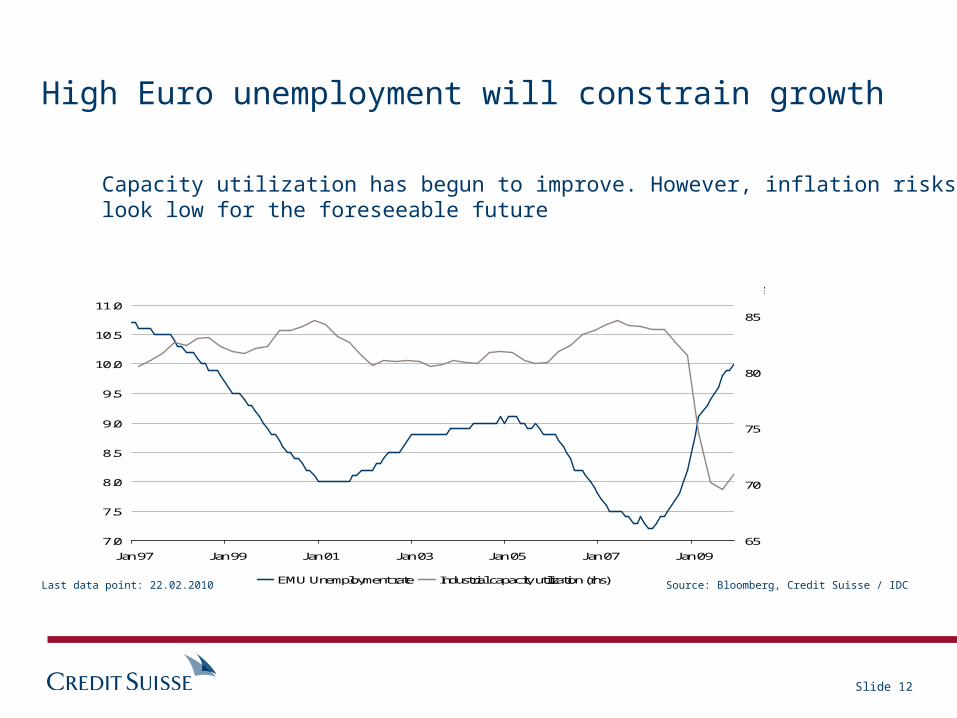

Slide 12

7.0

7.5

8.0

8.5

9.0

9.5

10.0

10.5

11.0

Jan 97 Jan 99 Jan 01 Jan 03 Jan 05 Jan 07 Jan 09

65

70

75

80

85

EMU Unemployment rate Industrial capacity utilization (rhs)

in % in %

High Euro unemployment will constrain growth

Capacity utilization has begun to improve. However, inflation risks look low for the foreseeable future

Source: Bloomberg, Credit Suisse / IDCLast data point: 22.02.2010

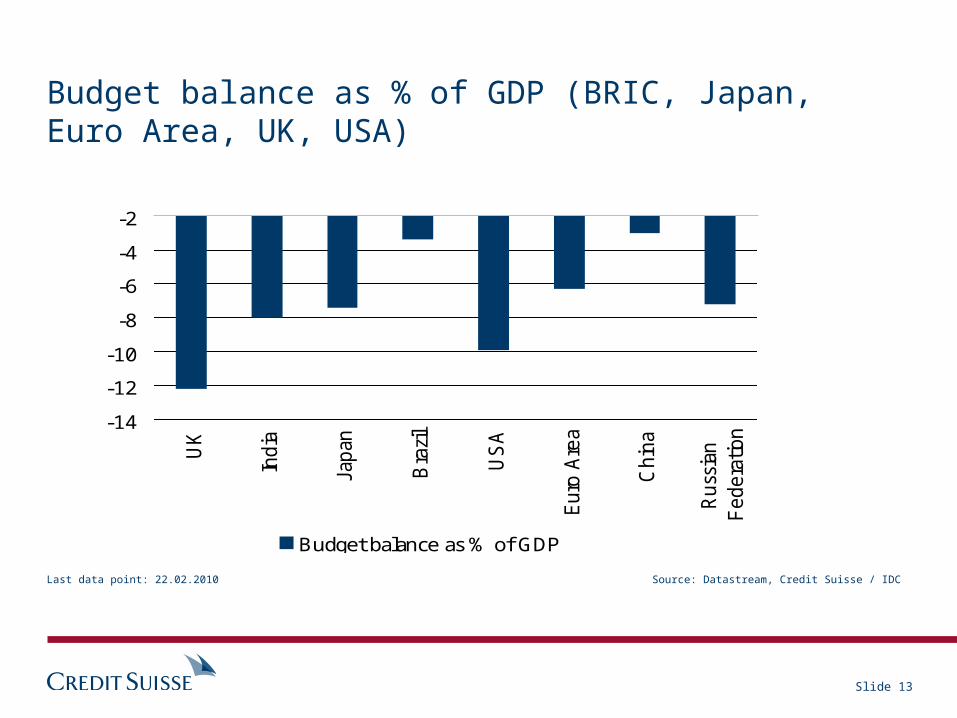

Slide 13

-14

-12

-10

-8

-6

-4

-2U

K

Indi

a

Japa

n

Bra

zil

USA

Eur

o Are

a

Chi

na

Rus

sian

Fed

erat

ion

Budget balance as % of GDP

Budget balance as % of GDP (BRIC, Japan, Euro Area, UK, USA)

Source: Datastream, Credit Suisse / IDCLast data point: 22.02.2010

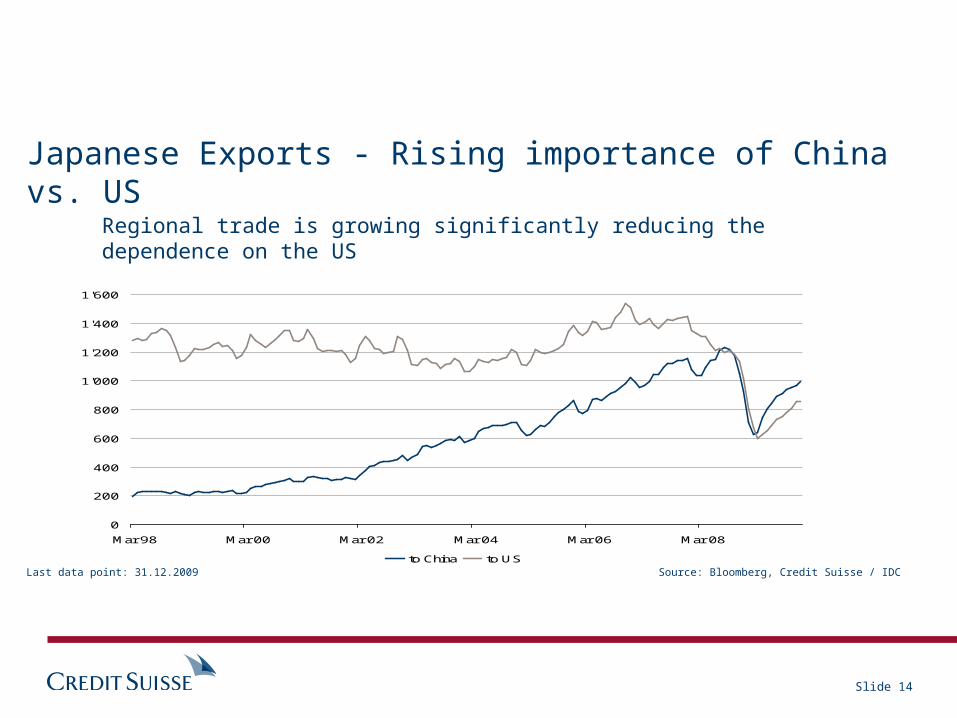

Slide 14

0

200

400

600

800

1'000

1'200

1'400

1'600

Mar 98 Mar 00 Mar 02 Mar 04 Mar 06 Mar 08

to China to US

bn J PY

Japanese Exports - Rising importance of China vs. US

Regional trade is growing significantly reducing the dependence on the US

Source: Bloomberg, Credit Suisse / IDCLast data point: 31.12.2009

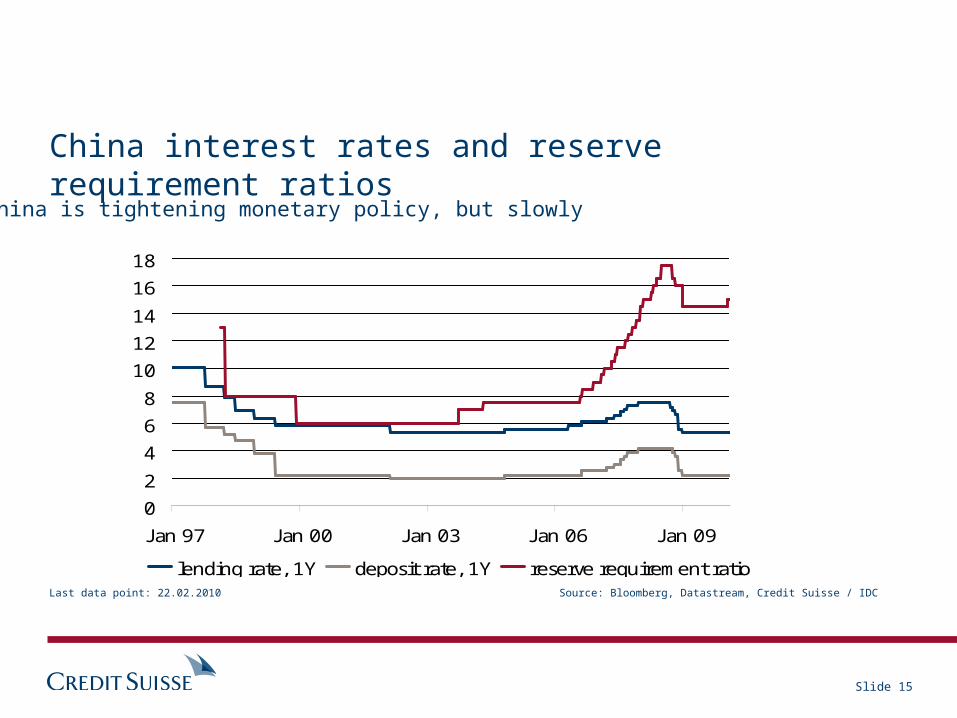

Slide 15

0

2

4

6

8

10

12

14

16

18

J an 97 J an 00 J an 03 J an 06 J an 09

lending rate, 1Y deposit rate, 1Y reserve requirement ratio

China interest rates and reserve requirement ratios

Source: Bloomberg, Datastream, Credit Suisse / IDCLast data point: 22.02.2010

China is tightening monetary policy, but slowly

Slide 16

500

600

700

800

900

1'000

1'100

1'200

1'300

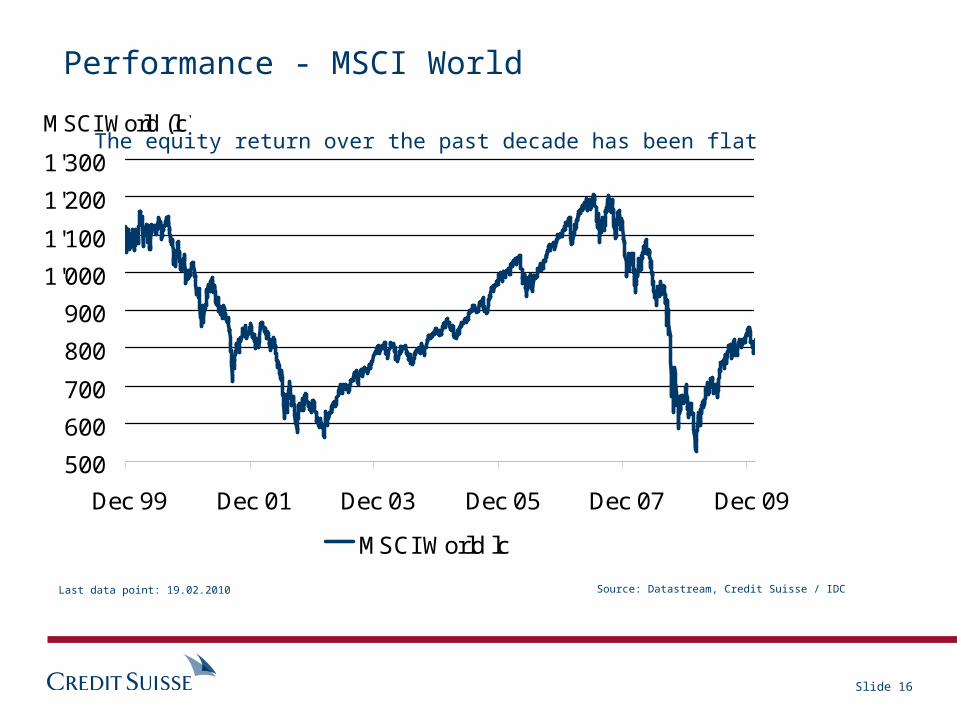

Dec 99 Dec 01 Dec 03 Dec 05 Dec 07 Dec 09

MSCI World lc

MSCI World (lc)

Performance - MSCI World

Source: Datastream, Credit Suisse / IDCLast data point: 19.02.2010

The equity return over the past decade has been flat

Slide 17

-6

-4

-2

0

2

4

6

8

J un 03 J un 04 J un 05 J un 06 J un 07 J un 08 J un 09

Euphoria

Panic

CS risk appetite

Last data point: 19.02.2010 Source: Credit Suisse / IDC

Slide 18

1.00

1.10

1.20

1.30

1.40

1.50

1.60

1.70

1.80

J an 97 J an 99 J an 01 J an 03 J an 05 J an 07 J an 09

Defensive to Cyclical ratio

Defensives Outperforming

Global defensives to cyclicals ratio

Increase equity exposure to high quality defensive sectors

Source: Datastream, Credit Suisse / IDCLast data point: 19.02.2010

Slide 19

5

10

15

20

25

30

J an 90 J an 92 J an 94 J an 96 J an 98 J an 00 J an 02 J an 04 J an 06 J an 08 J an 10

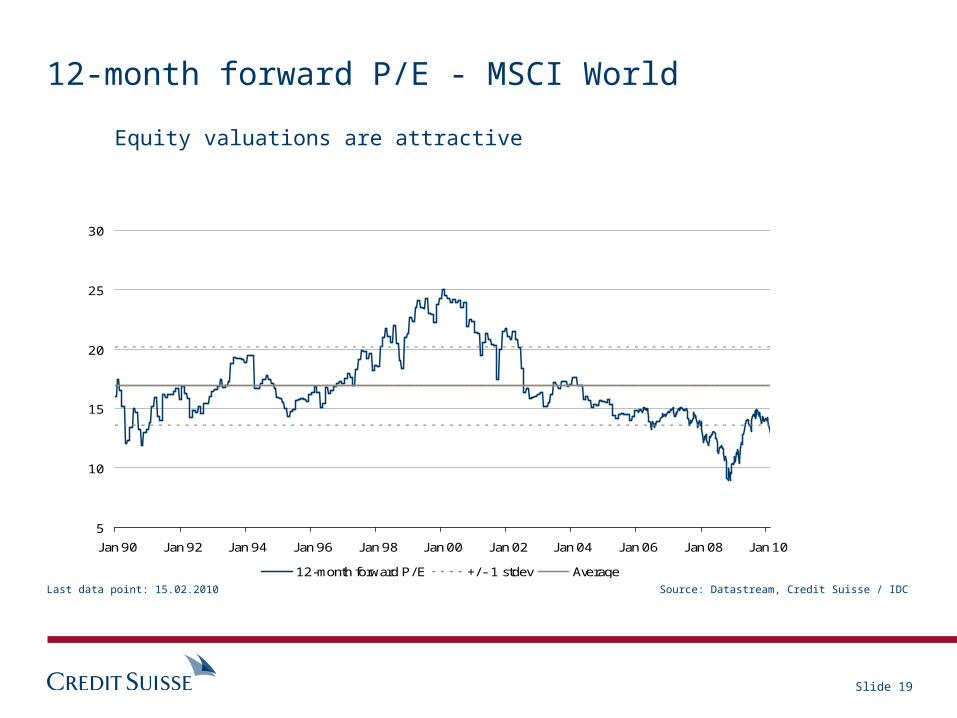

12-month forward P/E +/ - 1 stdev Average

12-month forward P/E

12-month forward P/E - MSCI World

Equity valuations are attractive

Source: Datastream, Credit Suisse / IDCLast data point: 15.02.2010

Slide 20

-6-4-202468

10

J an 91 J an 95 J an 99 J an 03 J an 07

-40

-30

-20

-10

0

10

20

30

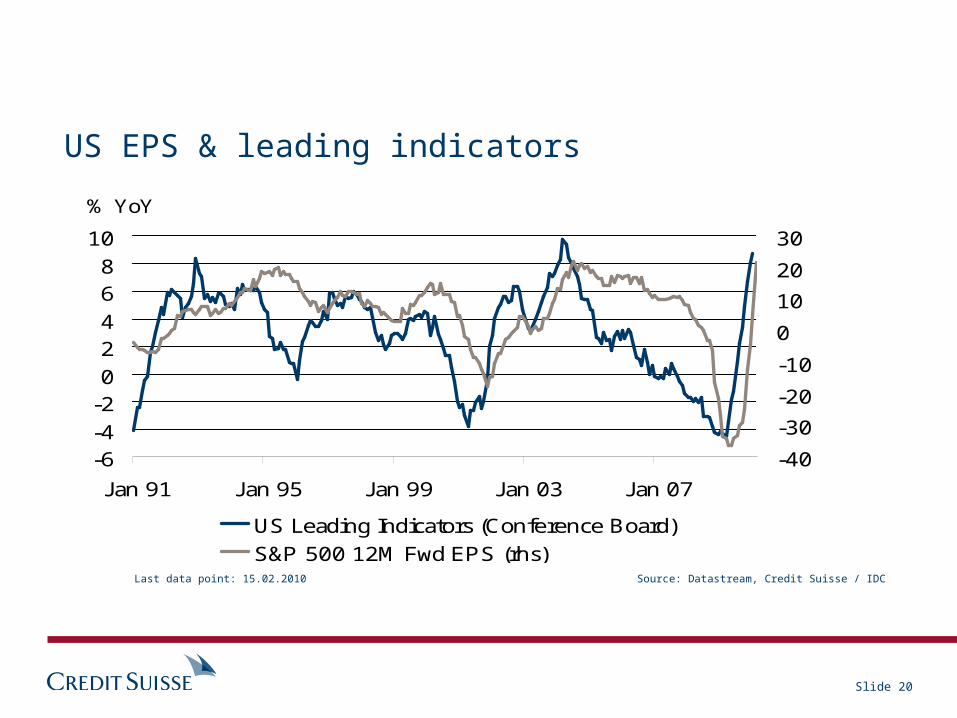

US Leading Indicators (Conference Board) S&P 500 12M Fwd EPS (rhs)

% YoY % YoY

US EPS & leading indicators

Last data point: 15.02.2010 Source: Datastream, Credit Suisse / IDC

Slide 21

50

100

150

200

250

300

350

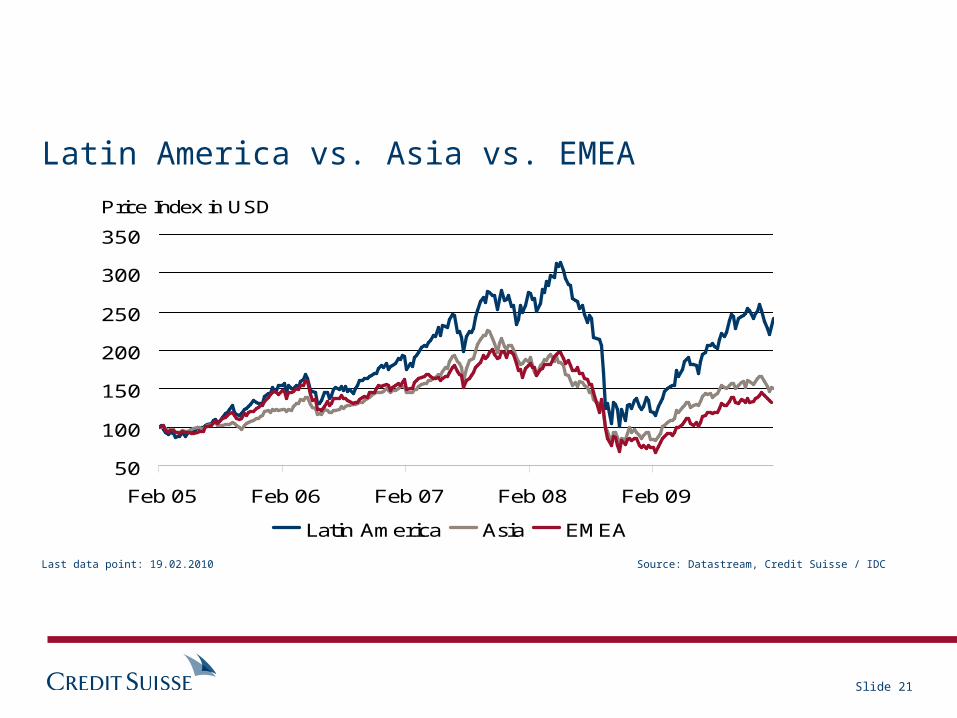

Feb 05 Feb 06 Feb 07 Feb 08 Feb 09

Latin America Asia EMEA

Price Index in USD

Latin America vs. Asia vs. EMEA

Source: Datastream, Credit Suisse / IDCLast data point: 19.02.2010

Slide 22

0

5

10

15

20

25

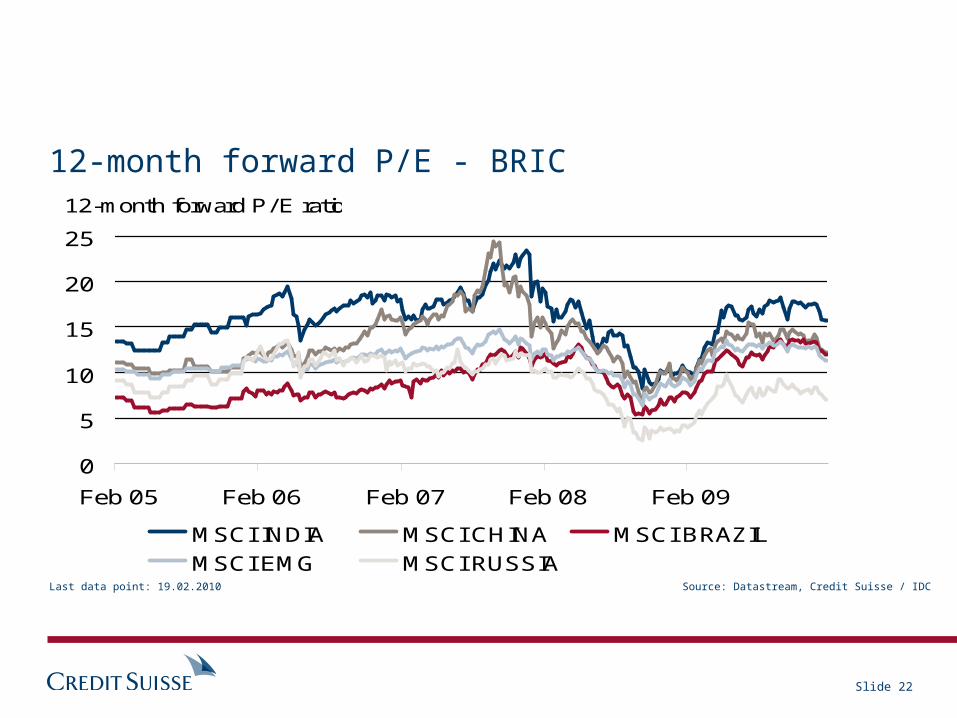

Feb 05 Feb 06 Feb 07 Feb 08 Feb 09

MSCI INDIA MSCI CHINA MSCI BRAZILMSCI EMG MSCI RUSSIA

12-month forward P/E ratio

12-month forward P/E - BRIC

Source: Datastream, Credit Suisse / IDCLast data point: 19.02.2010

Slide 23

1.5

2.0

2.5

3.0

3.5

4.0

4.5

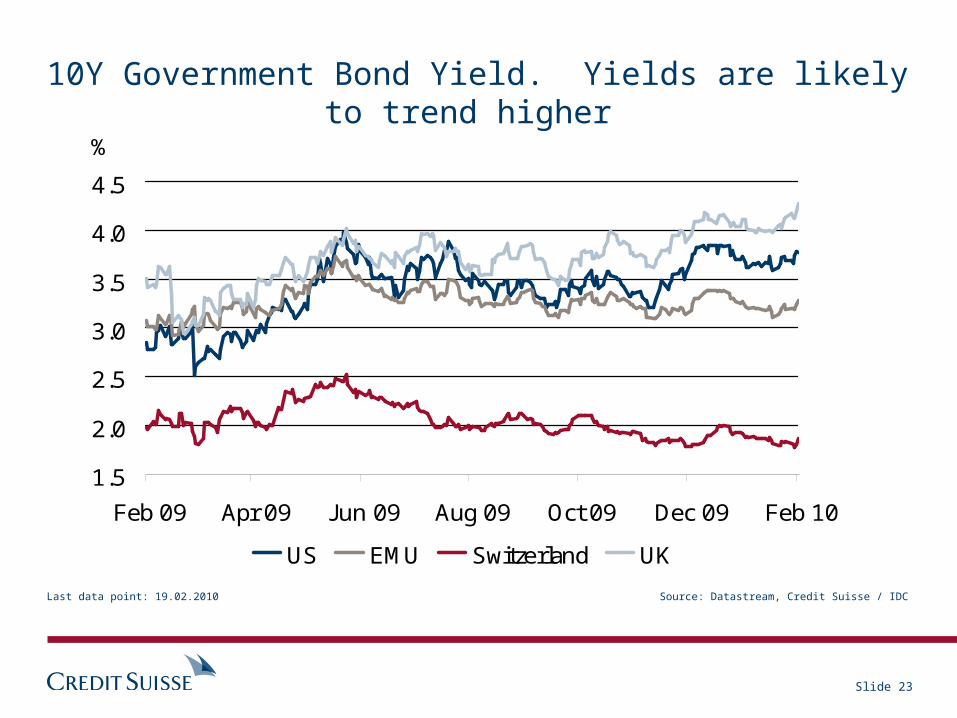

Feb 09 Apr 09 J un 09 Aug 09 Oct 09 Dec 09 Feb 10

US EMU Switzerland UK

%

10Y Government Bond Yield. Yields are likely to trend higher

Source: Datastream, Credit Suisse / IDCLast data point: 19.02.2010

Slide 24

0

100

200

300

400

500

600

700

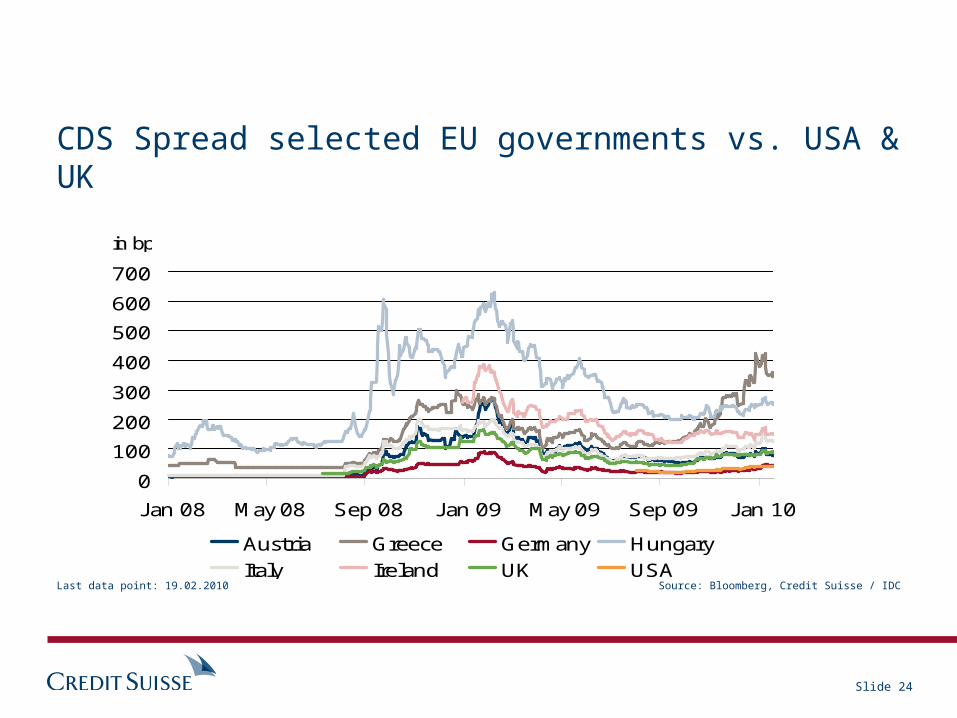

J an 08 May 08 Sep 08 J an 09 May 09 Sep 09 J an 10

Austria Greece Germany HungaryItaly Ireland UK USA

in bp

CDS Spread selected EU governments vs. USA & UK

Source: Bloomberg, Credit Suisse / IDCLast data point: 19.02.2010

Slide 25

0

100

200

300

400

500

600

700

800

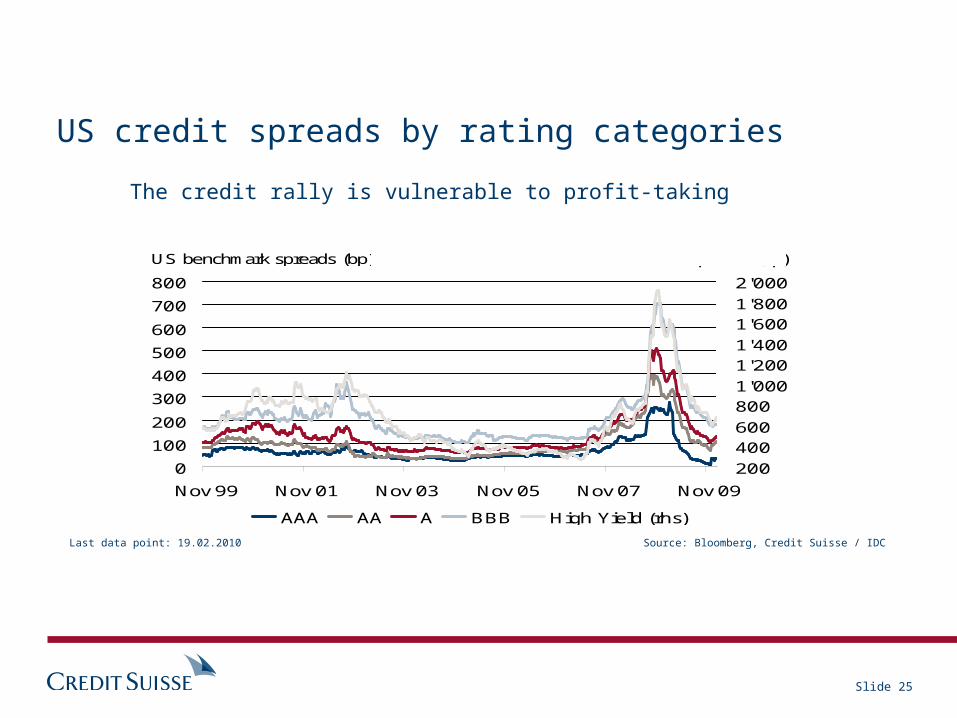

Nov 99 Nov 01 Nov 03 Nov 05 Nov 07 Nov 09

2004006008001'0001'2001'4001'6001'8002'000

AAA AA A BBB High Yield (rhs)

US benchmark spreads (bp) US benchmark spreads (bp)

US credit spreads by rating categories

Source: Bloomberg, Credit Suisse / IDCLast data point: 19.02.2010

The credit rally is vulnerable to profit-taking

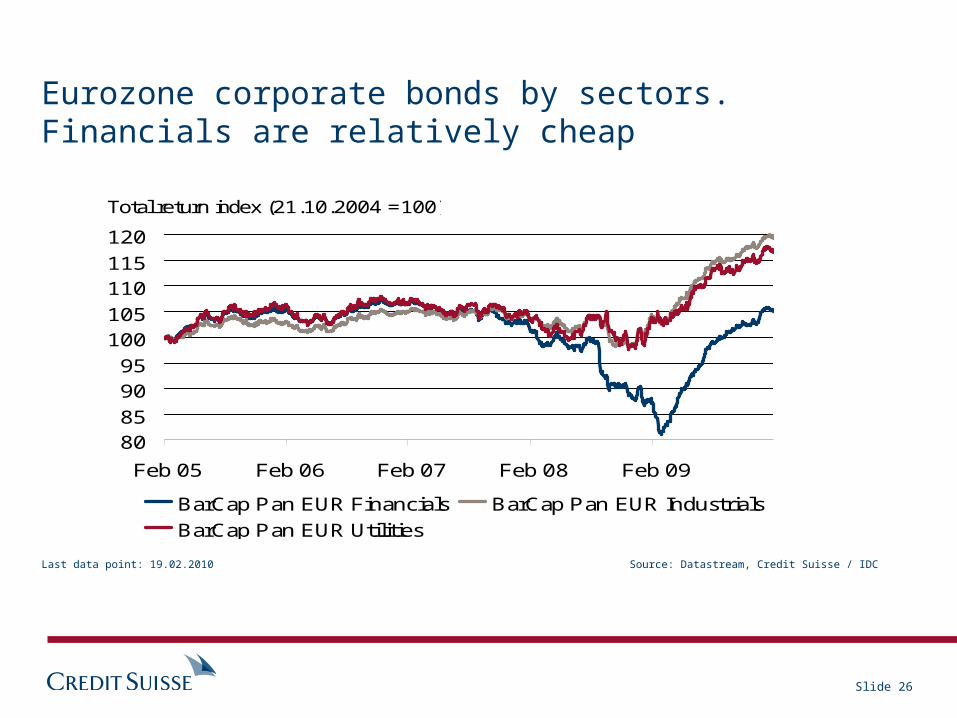

Slide 26

80859095

100105110115120

Feb 05 Feb 06 Feb 07 Feb 08 Feb 09

BarCap Pan EUR Financials BarCap Pan EUR IndustrialsBarCap Pan EUR Utilities

Total return index (21.10.2004 =100)

Eurozone corporate bonds by sectors. Financials are relatively cheap

Source: Datastream, Credit Suisse / IDCLast data point: 19.02.2010

Slide 27

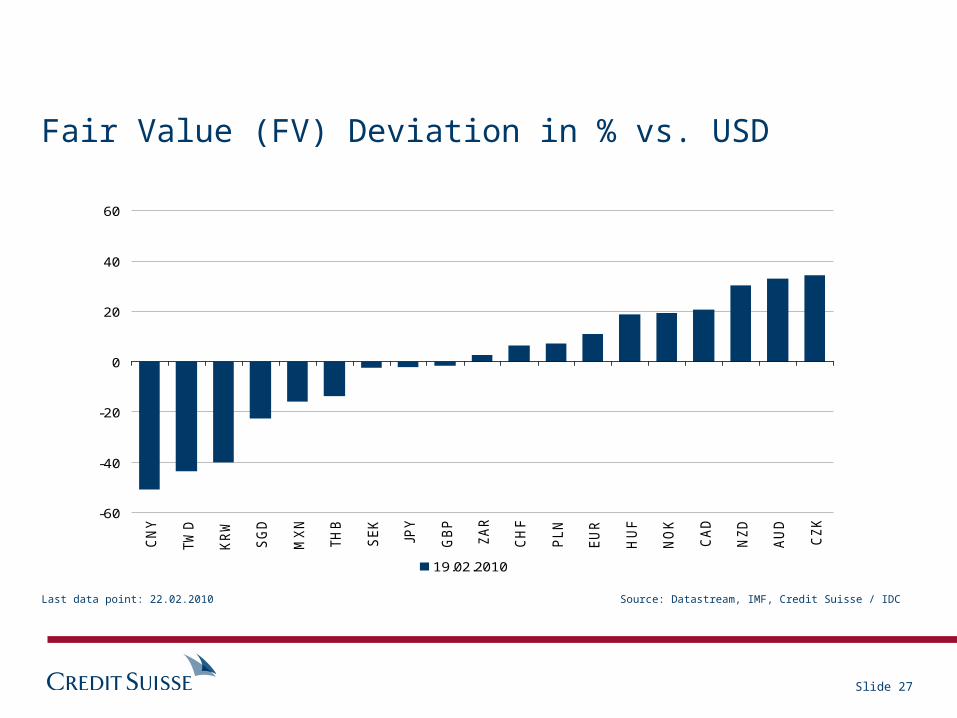

-60

-40

-20

0

20

40

60

CN

Y

TW

D

KRW

SG

D

MXN

TH

B

SEK

JPY

GBP

ZAR

CH

F

PLN

EU

R

HU

F

NO

K

CAD

NZD

AU

D

CZK

19.02.2010

Overvaluation vs. USD

Undervaluation vs. USD

Deviation in %

Fair Value (FV) Deviation in % vs. USD

Source: Datastream, IMF, Credit Suisse / IDCLast data point: 22.02.2010

Slide 28

70

80

90

100

110

120

130

J an 99 J an 01 J an 03 J an 05 J an 07 J an 09

-2

-1

0

1

2

3

DXY Dollar Index2Y Swap Spread USD minus weighted G6 yields (r.h.s)

Index in %

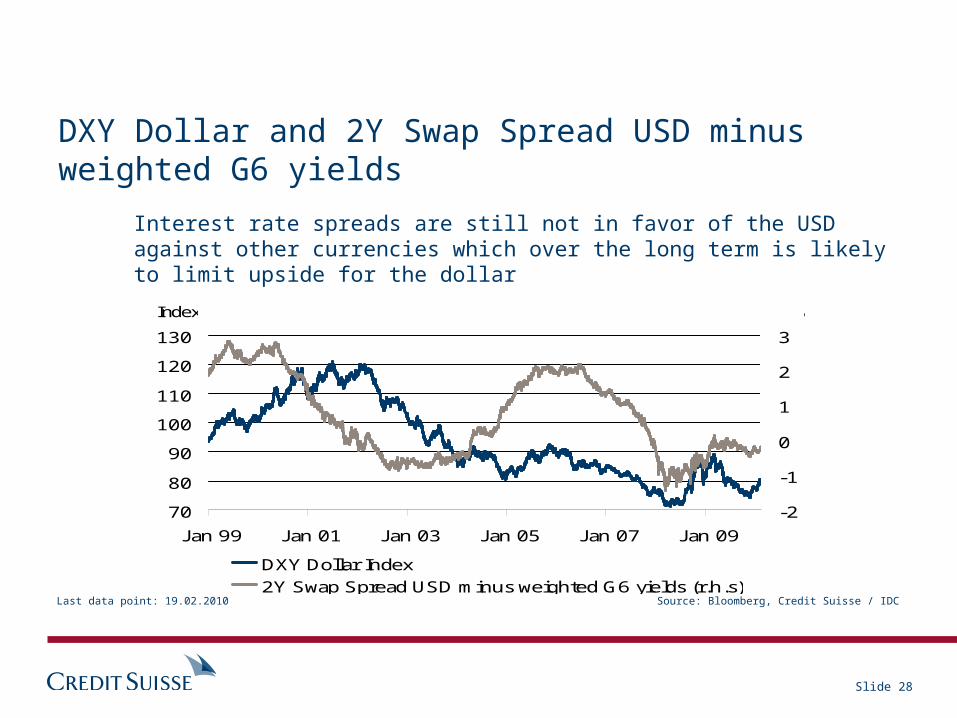

DXY Dollar and 2Y Swap Spread USD minus weighted G6 yields

Interest rate spreads are still not in favor of the USD against other currencies which over the long term is likely to limit upside for the dollar

Source: Bloomberg, Credit Suisse / IDCLast data point: 19.02.2010

Slide 29

1.301.401.501.601.701.801.902.002.102.20

J an 04 J an 05 J an 06 J an 07 J an 08 J an 09 J an 10

-1.0

-0.5

0

0.5

1.0

1.5

2.0

2.5

3.0

GBP/USD exchange rate 2-Year Swap GBP minus USD (r.h.s)

GBP/USD in %

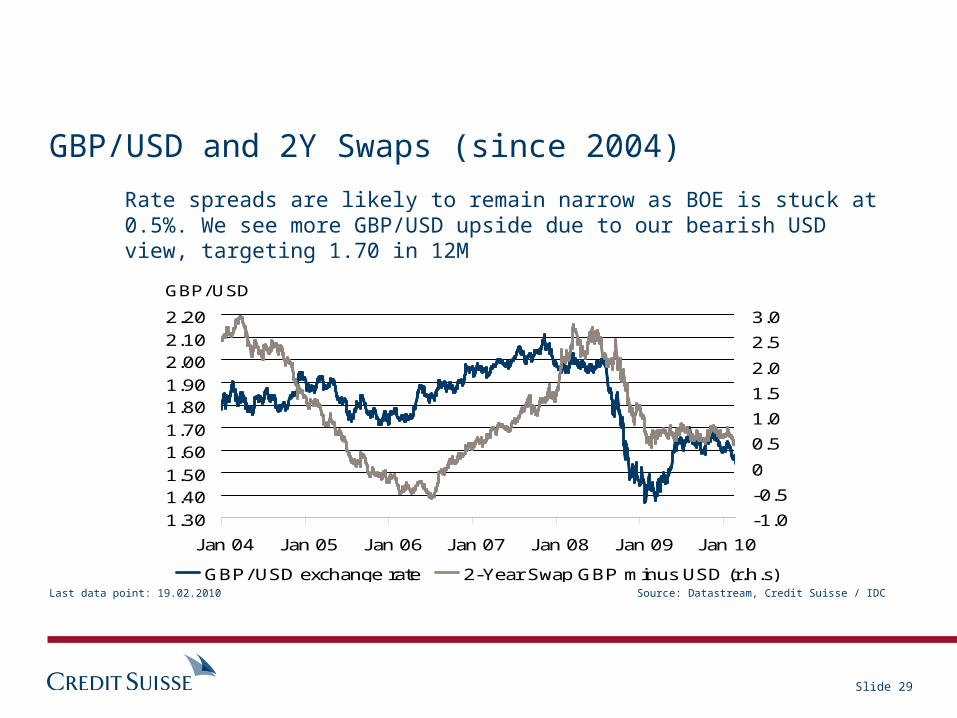

GBP/USD and 2Y Swaps (since 2004)

Rate spreads are likely to remain narrow as BOE is stuck at 0.5%. We see more GBP/USD upside due to our bearish USD view, targeting 1.70 in 12M

Source: Datastream, Credit Suisse / IDCLast data point: 19.02.2010

Slide 30

85

90

95

100

105

110

115

120

125

J an 04 J an 05 J an 06 J an 07 J an 08 J an 09 J an 10

00.51.01.52.02.53.03.54.04.55.0

USD/ J PY exchange rate 2 Year Swap USD minus J PY (r.h.s)

USD/J PY in %

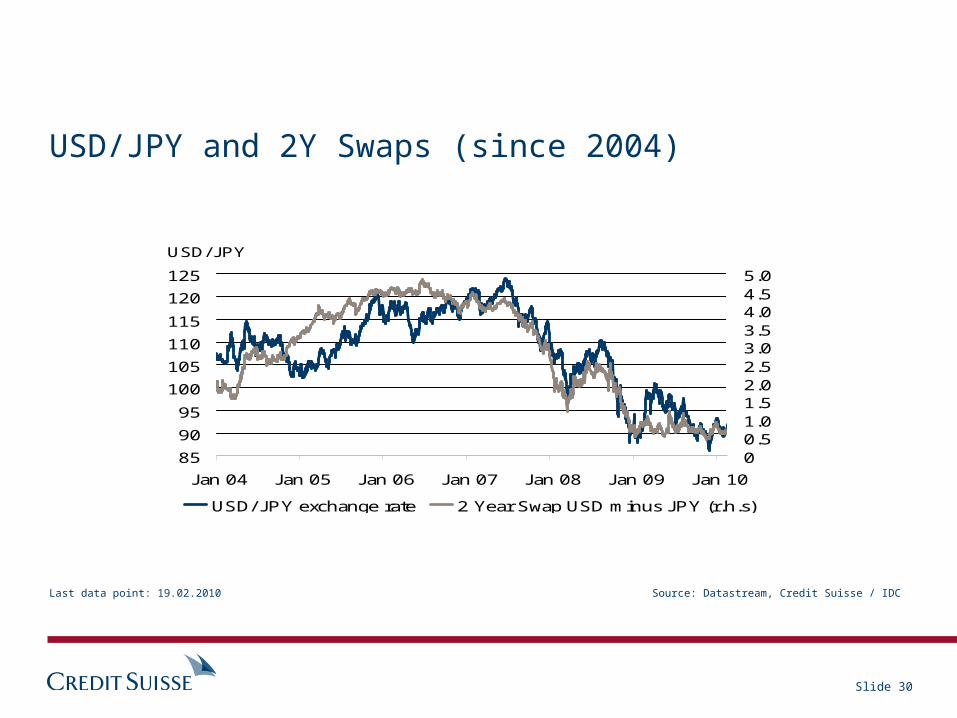

USD/JPY and 2Y Swaps (since 2004)

Source: Datastream, Credit Suisse / IDCLast data point: 19.02.2010

Slide 31

0.60

0.65

0.70

0.75

0.80

0.85

0.90

0.95

1.00

J an 06 J an 07 J an 08 J an 09 J an 10

0

1

2

3

4

5

6

AUD/USD 2-Year Swap AUD minus USD (r.h.s)

AUD/USD in %

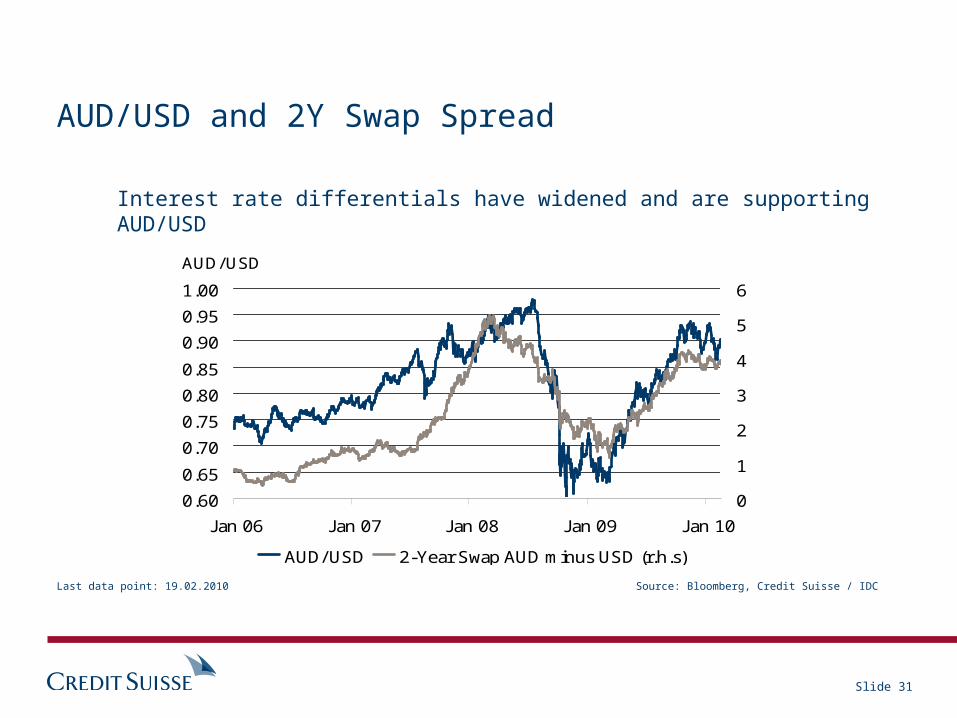

AUD/USD and 2Y Swap Spread

Interest rate differentials have widened and are supporting AUD/USD

Source: Bloomberg, Credit Suisse / IDCLast data point: 19.02.2010

Slide 32

20

40

60

80

100

120

140

160

J an 08 May 08 Sep 08 J an 09 May 09 Sep 09 J an 10

CSCB Energy Index CSCB Precious Metals IndexCSCB Agriculture Index CSCB Industrial Metals Index

Index, J anuary 2008 = 100

Credit Suisse commodity indices

Source: Bloomberg, Credit Suisse / IDCLast data point: 19.02.2010

Slide 33

4.0

4.5

5.0

5.5

6.0

6.5

56 64 72 80 88 96 04

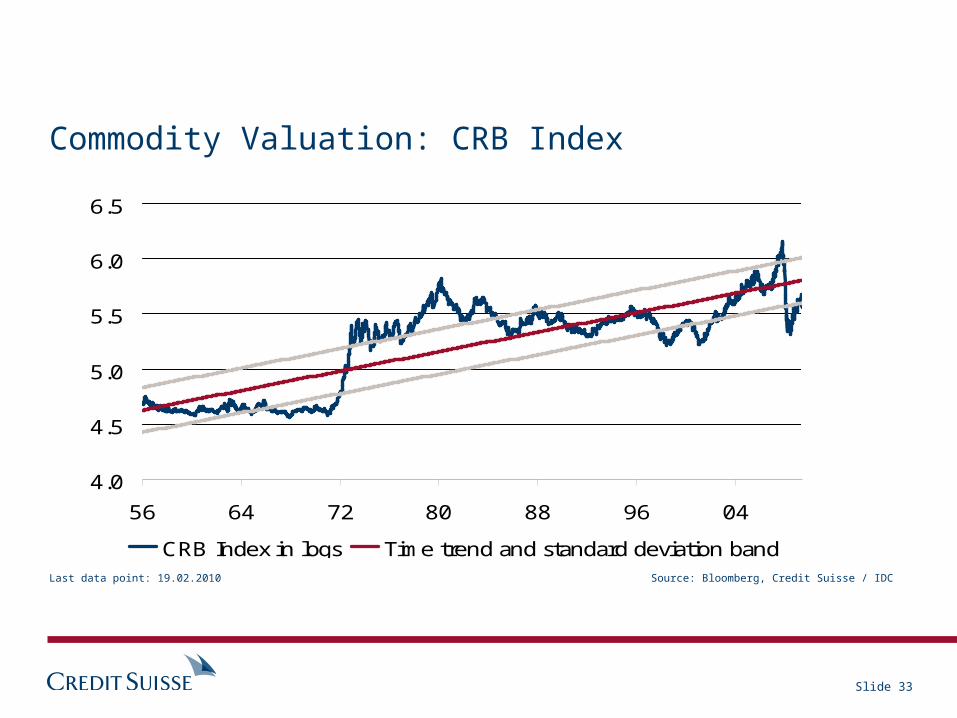

CRB Index in logs Time trend and standard deviation band

Commodity Valuation: CRB Index

Source: Bloomberg, Credit Suisse / IDCLast data point: 19.02.2010

Slide 34

-5-4-3-2-101234

Mar 05 Mar 06 Mar 07 Mar 08 Mar 09

Global oil demand growth Global oil supply growth

% YoY (3M rolling average)

Source: EIA, Credit Suisse / IDCLast data point: 22.02.2010

Global crude oil demand and supply growth

Global oil demand continues to recover and supply has started to grow as well. We think the oil market has started a new cycle and expect moderately higher prices in 2010

Slide 35

0

100

200

300

400

500

600

Feb 08 J un 08 Oct 08 Feb 09 J un 09 Oct 09 Feb 10

2'000

3'000

4'000

5'000

6'000

7'000

8'000

9'000

LME copper inventories LME 3M copper forward price (rhs)

in kt USD/t

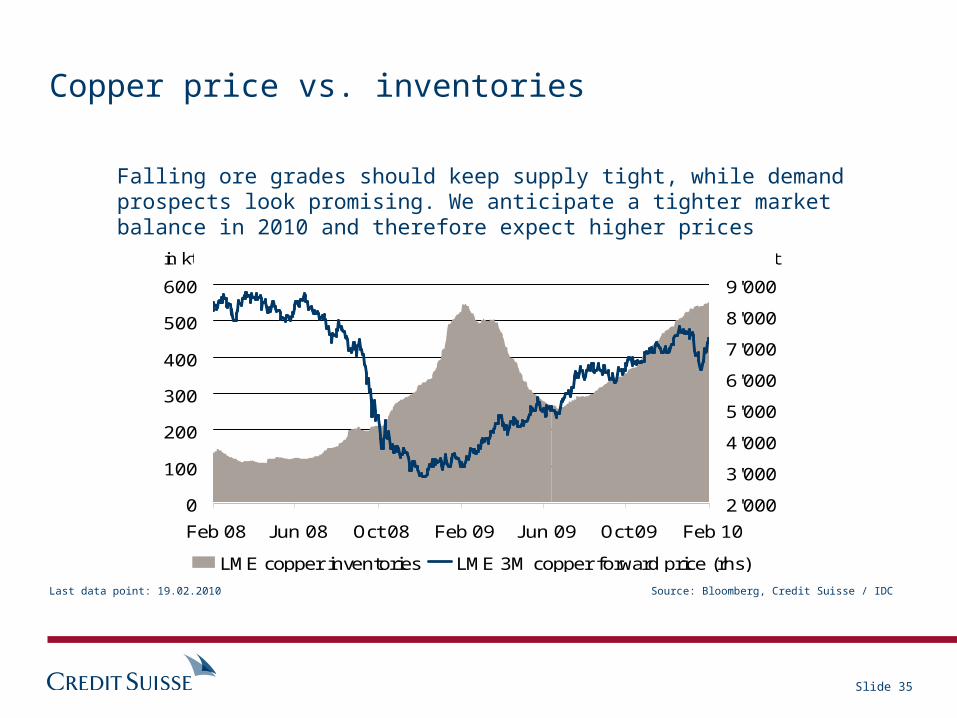

Copper price vs. inventories

Falling ore grades should keep supply tight, while demand prospects look promising. We anticipate a tighter market balance in 2010 and therefore expect higher prices

Source: Bloomberg, Credit Suisse / IDCLast data point: 19.02.2010

Slide 36

850

900

950

1'000

1'050

1'100

1'150

1'200

1'250

Feb 09 Apr 09 J un 09 Aug 09 Oct 09 Dec 09 Feb 10

120

140

160

180

200

220

240

260

280

Net speculative positions (rhs) Gold price

in USD / oz. in ,000 contracts

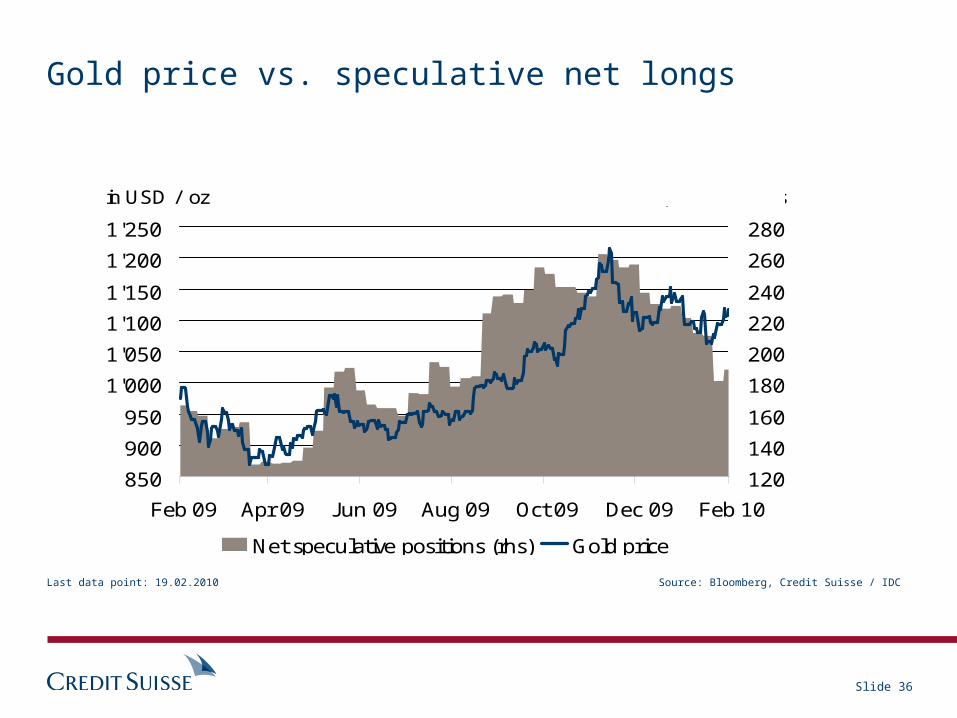

Gold price vs. speculative net longs

Source: Bloomberg, Credit Suisse / IDCLast data point: 19.02.2010

Slide 37

600800

1'0001'2001'4001'6001'8002'0002'2002'400

Feb 08 J un 08 Oct 08 Feb 09 J un 09 Oct 09 Feb 10

0

5

10

15

20

25

Net speculative long positions (rhs) Platinum price

in USD / oz. In '000 contracts

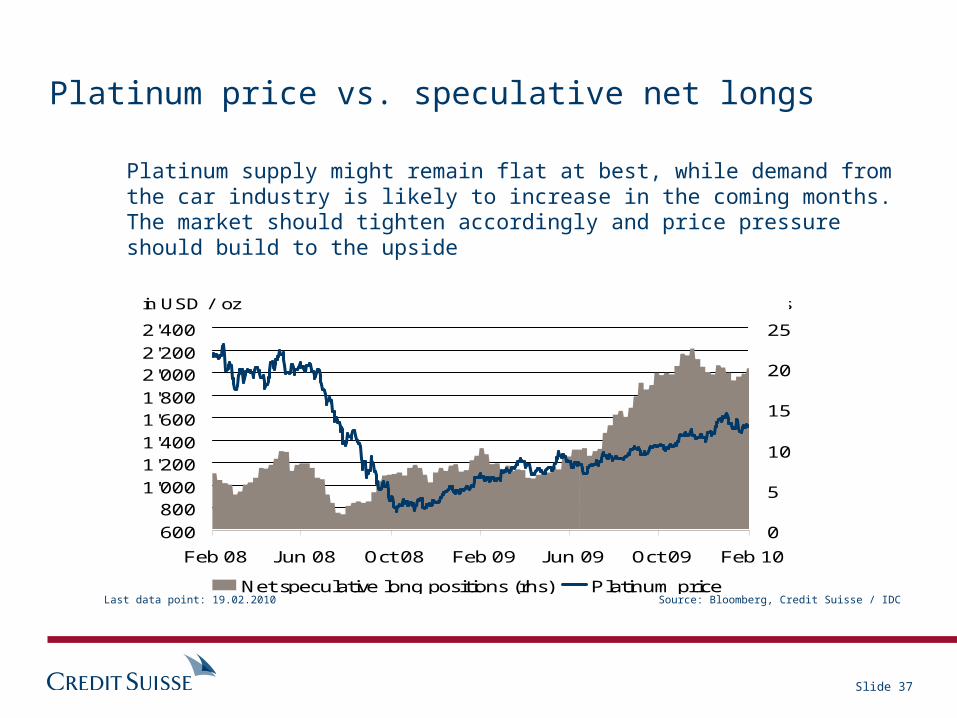

Platinum price vs. speculative net longs

Platinum supply might remain flat at best, while demand from the car industry is likely to increase in the coming months. The market should tighten accordingly and price pressure should build to the upside

Source: Bloomberg, Credit Suisse / IDCLast data point: 19.02.2010

Slide 38

200

400

600

800

1'000

1'200

1'400

J an 06 J an 07 J an 08 J an 09 J an 10

-80

-60

-40

-20

0

20

40

Net speculative long positions (rhs) CBOT wheat price

US cents / bushel in '000 contracts

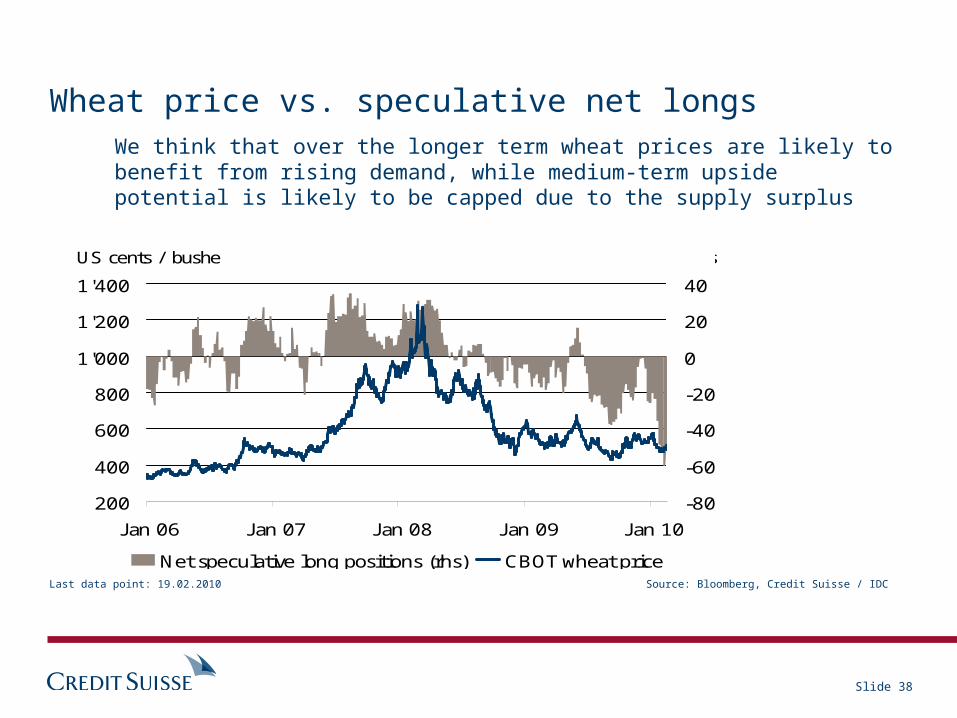

Wheat price vs. speculative net longsWe think that over the longer term wheat prices are likely to benefit from rising demand, while medium-term upside potential is likely to be capped due to the supply surplus

Source: Bloomberg, Credit Suisse / IDCLast data point: 19.02.2010

Slide 39

Conclusions and strategy

US and Japanese growth should surprise positively in 1H10, but fade thereafter

UK and European growth will be mediocre with the weaker Euroland economies and Eastern Europe struggling to emerge from recession

Growth leadership will come from Asia and Latin America Japan remains in deflation, inflation in Europe is slowing and

the upturn in inflation in the US and the UK will reverse The upturn in inflation in emerging markets is being met by

tighter monetary policies After the set-back in equity markets in early 2010, equity

markets should now advance for the rest of the year Defensive high quality sectors will outperform

Slide 40

Conclusions and strategy

During 2H10, emerging markets should start to outperform again

Dollar strength against the Euro and the pound should reverse during 2H10 as the US economy fades

Asian and Latin American currencies will continue to be subject to upward pressure

The credit rally will now consolidate, bank debt and emerging debt are attractive

Government bonds will see moderate selling pressure

Slide 41

General disclaimer / Important information

This document was produced by and the opinions expressed are those of Credit Suisse as of the date of writing and are subject to change. It has been prepared solely for information purposes and for the use of the recipient. It does not constitute an offer or an invitation by or on behalf of Credit Suisse to any person to buy or sell any security. Nothing in this material constitutes investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate to your individual circumstances, or otherwise constitutes a personal recommendation to you. The price and value of investments mentioned and any income that might accrue may fluctuate and may fall or rise. Any reference to past performance is not a guide to the future.

The information and analysis contained in this publication have been compiled or arrived at from sources believed to be reliable but Credit Suisse does not make any representation as to their accuracy or completeness and does not accept liability for any loss arising from the use hereof. Credit Suisse may have acted upon the information and analysis contained in this publication before being made available to clients of Credit Suisse. Investments in emerging markets are speculative and considerably more volatile than investments in established markets. Some of the main risks are political risks, economic risks, credit risks, currency risks and market risks. Furthermore, investments in foreign currencies are subject to exchange rate fluctuations. Before entering into any transaction, you should consider the suitability of the transaction to your particular circumstances and independently review (with your professional advisers as necessary) the specific financial risks as well as legal, regulatory, credit, tax and accounting consequences.

Neither this document nor any copy thereof may be sent to or taken into the United States or distributed in the United States or to a US person, in certain other jurisdictions the distribution may be restricted by local law or regulation. Neither this report nor any copy thereof may be sent, taken or distributed in Japan.

Credit Suisse, a Swiss bank, is authorized and regulated by the Swiss Financial Market Supervisory Authority. Credit Suisse disseminates research to its clients, which has been prepared by either itself or any of its affiliates.

This document has been issued in Hong Kong by Credit Suisse Hong Kong branch, which is an Authorized Institution licensed by the Hong Kong Monetary Authority and a Registered Institution under the Securities and Futures Ordinance (Chapter 571 of the Laws of Hong Kong).

Credit Suisse (Deutschland) AG, authorized and regulated by the Bundesanstalt für Finanzdienstleistungsaufsicht, disseminates research to its clients that has been prepared by one of its affiliates.

This document has been issued in the UK by Credit Suisse (UK) Limited and Credit Suisse Securities (Europe) Limited, London. Credit Suisse Securities (Europe) Limited and Credit Suisse (UK) Limited are associated but independent legal and regulated entities within the Credit Suisse Group. Both are authorized and regulated by the Financial Services Authority. The protections made available by the UK’s Financial Services Authority for private customers do not apply to investments or services provided by a person outside the UK, nor will the Financial Services Compensation Scheme be available if the issuer of the investment fails to meet its obligations.

This report may not be reproduced either in whole or in part, without the written permission of Credit Suisse.

Copyright © 2010 Credit Suisse Group AG and/or its affiliates. All rights reserved.