Embed Size (px)

Citation preview

Economic Research & Consulting

Global insurance review 2012 and outlook 2013/14

December 2012

Published by:

Swiss Reinsurance Company LtdEconomic Research & ConsultingP.O. Box 8022 ZurichSwitzerland

Telephone +41 43 285 2551Fax +41 43 282 [email protected]

Armonk Office:175 King StreetArmonk, NY 10504

Telephone +1 914 828 8000

Hong Kong Office:18 Harbour Road, WanchaiCentral Plaza, 61st FloorHong Kong, SAR

Telephone + 852 25 82 5703Fax + 852 25 11 6603

Authors:Kurt KarlTelephone +41 43 285 3369

Thomas HolzheuTelephone +1 914 828 6502

Clarence WongTelephone +852 2582 5644

Co-editor:Jessica VillatTelephone +41 43 285 5189

Managing editor:Kurt Karl, Head of Swiss Re Economic Research & Consulting.

The editorial deadline for this study was 15 November 2012.

Graphic design and production:Swiss Re Logistics/Media Production

© 2012Swiss ReAll rights reserved.

The entire content of this report is subject to copyright with all rights reserved. The information may be used for private or internal purposes, provided that any copyright or other proprietary notices are not removed. Electronic reuse of the data published in this report is prohibited.

Reproduction in whole or in part or use for any public purpose is permitted only with the prior written approval of Swiss Re Economic Research & Consulting and if the source reference “Global insurance review 2012 and outlook 2013/214” is indicated. Courtesy copies are appreciated.

Although all the information used in this study was taken from reliable sources, Swiss Re does not accept any responsibility for the accuracy or comprehensiveness of the information given. The information provided is for informational purposes only and in no way constitutes Swiss Re’s position. In no event shall Swiss Re be liable for any loss or damage arising in connection with the use of this information.

Order no: 271_0512_en

1

Table of contents

Executive summary 2

The macroeconomic environment: Growth will be stronger next year 3

Non-life re/insurance: Premiums are growing, but profits remain weak 10

Life re/insurance: Navigating choppy waters 17

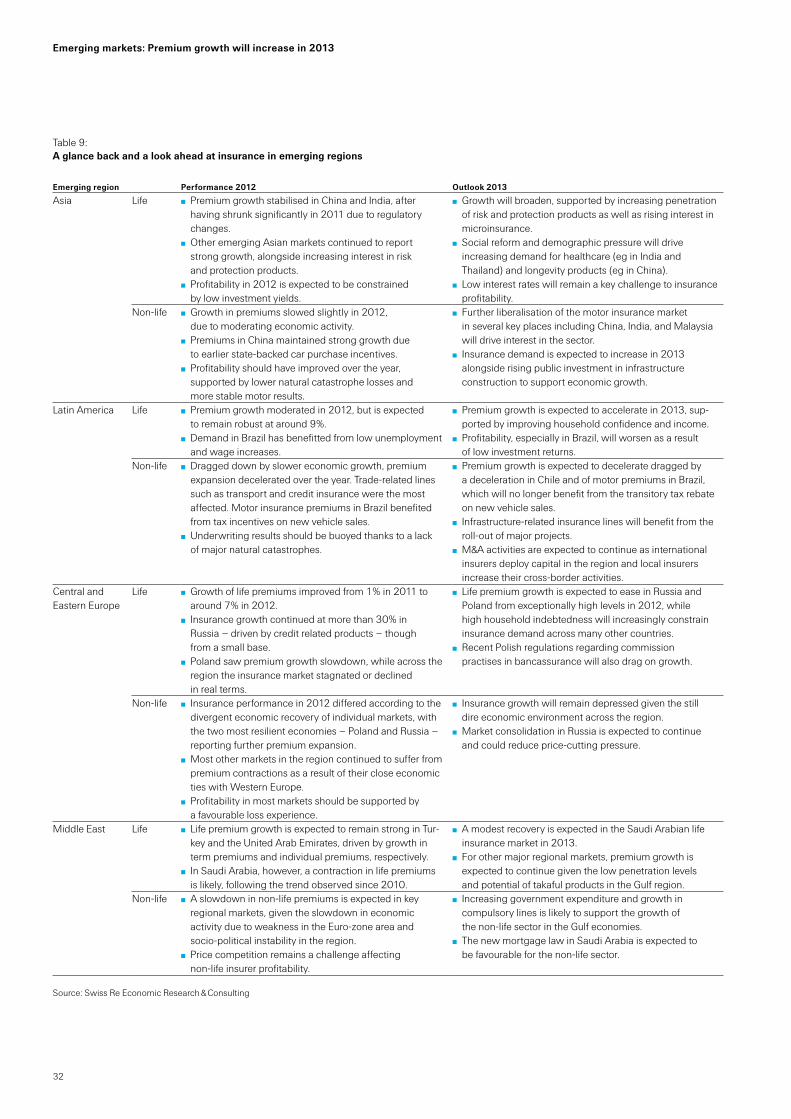

Emerging markets: Premium growth will increase in 2013 25

2

Executive summary

The global economy is currently fairly weak, but an improving housing market in the US, fiscal and monetary stimulus in China and a slow turnaround in the Euro area are expected to boost growth in 2013. Monetary policy will remain accommodative in the major economies well into 2015, providing the stimulus necessary to sustain growth, but with low interest rates reducing insurers’ investment returns. Inflation will stay tame since wage gains will be modest with unemployment rates declining only gradually.

Growth in non-life premiums accelerated a bit in 2012 and this will continue into next year as rates rise at a moderate pace. Underwriting results improved in 2012, compared to 2011 – a year with high catastrophe losses. Rates were stable to slightly up this year, but not by enough to compensate for decreasing investment yields. Next year, reserve releases are expected to turn to adverse reserve developments, supporting a bit stronger pace of price increases, particularly in the casualty lines. Currently, capacity is adequate, but appears robust under GAAP accounting due to low interest rates which boost the mark-to-market value of insurers’ bond portfolios.

Developments in reinsurance are following the primary sector closely, with the exception of the reinsurance industry’s higher exposure to natural catastrophe events. Thus, total cat losses, including Hurricane Sandy, are expected to produce a negative underwriting result and subdue overall profitability. This outlook assumes that the estimates for losses from Hurricane Sandy are consistent with recent forecasts from the major cat modellers.

Global primary life premium growth was close to zero this year, but is expected to be bet-ter next year. Emerging markets, in particular, are expected to have stronger premium growth as India and China more fully adjust to regulations passed in 2010/11. Advanced markets will also have positive real premium growth as many markets, including the US, Canada and Australia, rebound from declines in 2012. Stronger economic activity and rising interest rates will fuel the modest uptick in growth. Growth will improve in all prod-uct lines, including savings, term life and disability lines. Profitability will remain con-strained however because investment yields will continue to decline as bonds mature and must be replaced with lower yielding assets. Also, regulatory changes are expected to have a greater impact on life insurance business. Finally, life insurers with large books of savings products with interest rate guarantees will particularly struggle until interest rates rise.

The life reinsurance segment will continue to contract as regulatory challenges under-mine its value proposition. Reinsurers are seeking to grow premiums by expanding in emerging markets, taking on large transactions which provide capital relief and through new products, such as longevity reinsurance. Profitability of life reinsurers is challenged, as is the primary industry, by the low interest rate environment. However, reinsurers do not typically have large books of savings products with guarantees.

After struggling in 2011 and 2012, life insurance premium growth is expected to rebound in Emerging Asia next year, growing by about 5% in real terms. Growth in life insurance will increasingly focus on risk products because regulatory changes and low investment yields will continue to dampen savings product growth. Huge protection gaps, which exist in many key emerging markets including India and China, will help drive the shift to risk products. In the Middle East and Latin America, life insurance premium growth will continue to be robust. In Central and Eastern Europe premium growth will moderate a bit along with economic activity as the Euro debt crisis continues. Non-life premium growth moderated from about 9% growth in 2011 to 8% growth in 2012. Cat losses were fairly low in emerging markets so underwriting profitability improved. Premium growth will be driven by the growing wealth in emerging markets, which has been particularly beneficial to motor lines. Ongoing regulatory developments will strengthen the industry and enhance profitability in the long run.

The global economy is in a slump, but growth will improve next year.

Non-life premium growth and profitability will improve slowly.

Non-life reinsurance has again been significantly impacted by natural catastrophes.

Primary life premium growth will resume in 2013, but profitability will continue to be challenged by low interest rates.

Life reinsurance premium growth will continue to decline, but profitability will fare better than in the primary side due to a better product mix.

All emerging market regions are expected to have strong growth in life and non-life premiums next year.

3

The macroeconomic environment: Growth will be stronger next year

The major economies

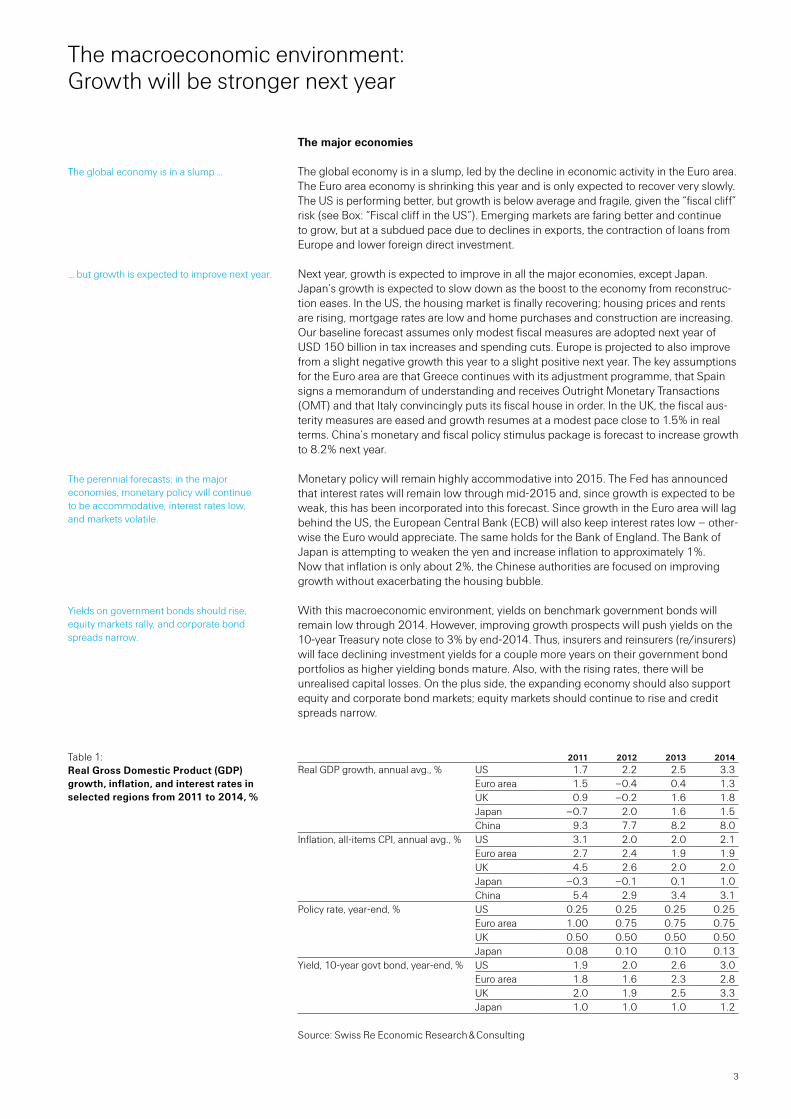

The global economy is in a slump, led by the decline in economic activity in the Euro area. The Euro area economy is shrinking this year and is only expected to recover very slowly. The US is performing better, but growth is below average and fragile, given the “fiscal cliff” risk (see Box: “Fiscal cliff in the US”). Emerging markets are faring better and continue to grow, but at a subdued pace due to declines in exports, the contraction of loans from Europe and lower foreign direct investment.

Next year, growth is expected to improve in all the major economies, except Japan. Japan’s growth is expected to slow down as the boost to the economy from reconstruc-tion eases. In the US, the housing market is finally recovering; housing prices and rents are rising, mortgage rates are low and home purchases and construction are increasing. Our baseline forecast assumes only modest fiscal measures are adopted next year of USD 150 billion in tax increases and spending cuts. Europe is projected to also improve from a slight negative growth this year to a slight positive next year. The key assumptions for the Euro area are that Greece continues with its adjustment programme, that Spain signs a memorandum of understanding and receives Outright Monetary Transactions (OMT) and that Italy convincingly puts its fiscal house in order. In the UK, the fiscal aus-terity measures are eased and growth resumes at a modest pace close to 1.5% in real terms. China’s monetary and fiscal policy stimulus package is forecast to increase growth to 8.2% next year.

Monetary policy will remain highly accommodative into 2015. The Fed has announced that interest rates will remain low through mid-2015 and, since growth is expected to be weak, this has been incorporated into this forecast. Since growth in the Euro area will lag behind the US, the European Central Bank (ECB) will also keep interest rates low – other-wise the Euro would appreciate. The same holds for the Bank of England. The Bank of Japan is attempting to weaken the yen and increase inflation to approximately 1%. Now that inflation is only about 2%, the Chinese authorities are focused on improving growth without exacerbating the housing bubble.

With this macroeconomic environment, yields on benchmark government bonds will remain low through 2014. However, improving growth prospects will push yields on the 10-year Treasury note close to 3% by end-2014. Thus, insurers and reinsurers (re/insurers) will face declining investment yields for a couple more years on their government bond portfolios as higher yielding bonds mature. Also, with the rising rates, there will be unrealised capital losses. On the plus side, the expanding economy should also support equity and corporate bond markets; equity markets should continue to rise and credit spreads narrow.

2011 2012 2013 2014Real GDP growth, annual avg., %

US 1.7 2.2 2.5 3.3Euro area 1.5 –0.4 0.4 1.3UK 0.9 –0.2 1.6 1.8Japan –0.7 2.0 1.6 1.5China 9.3 7.7 8.2 8.0

Inflation, all-items CPI, annual avg., %

US 3.1 2.0 2.0 2.1Euro area 2.7 2.4 1.9 1.9UK 4.5 2.6 2.0 2.0Japan –0.3 –0.1 0.1 1.0China 5.4 2.9 3.4 3.1

Policy rate, year-end, %

US 0.25 0.25 0.25 0.25Euro area 1.00 0.75 0.75 0.75UK 0.50 0.50 0.50 0.50Japan 0.08 0.10 0.10 0.13

Yield, 10-year govt bond, year-end, %

US 1.9 2.0 2.6 3.0Euro area 1.8 1.6 2.3 2.8UK 2.0 1.9 2.5 3.3Japan 1.0 1.0 1.0 1.2

Source: Swiss Re Economic Research & Consulting

The global economy is in a slump …

… but growth is expected to improve next year.

The perennial forecasts: in the major economies, monetary policy will continue to be accommodative, interest rates low, and markets volatile.

Yields on government bonds should rise, equity markets rally, and corporate bond spreads narrow.

Table 1: Real Gross Domestic Product (GDP) growth, inflation, and interest rates in selected regions from 2011 to 2014, %

4

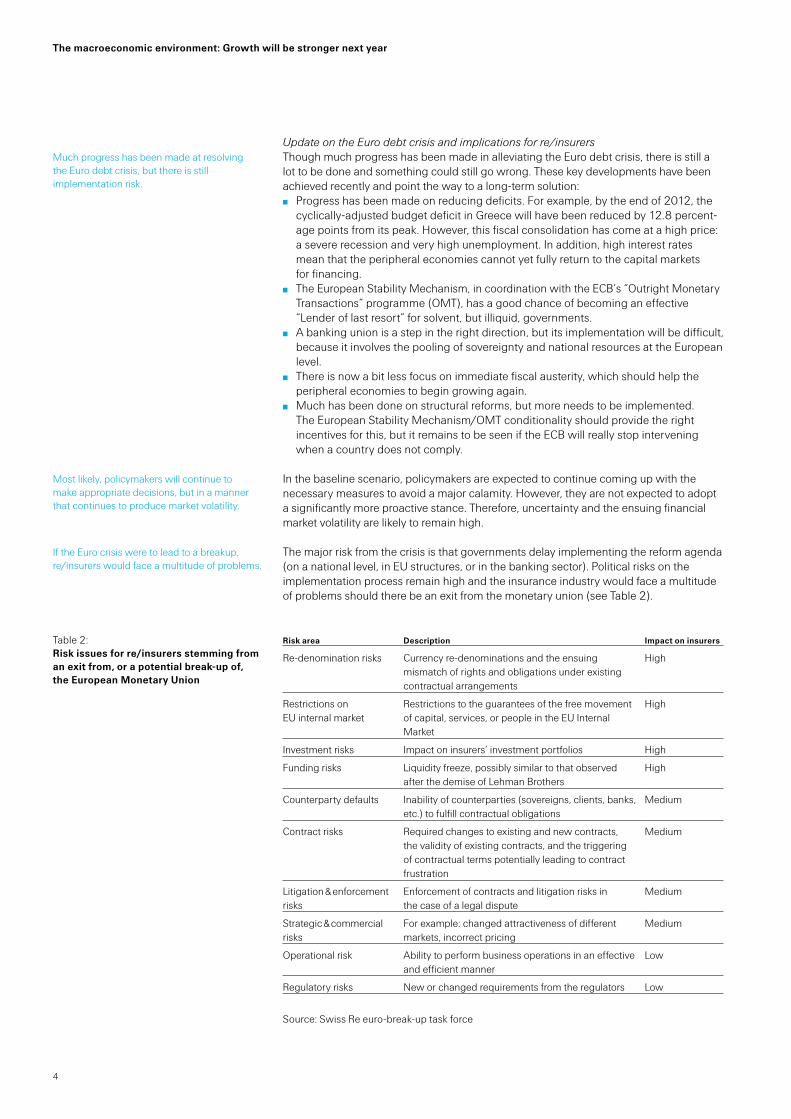

Update on the Euro debt crisis and implications for re/insurersThough much progress has been made in alleviating the Euro debt crisis, there is still a lot to be done and something could still go wrong. These key developments have been achieved recently and point the way to a long-term solution: Progress has been made on reducing deficits. For example, by the end of 2012, the

cyclically-adjusted budget deficit in Greece will have been reduced by 12.8 percent-age points from its peak. However, this fiscal consolidation has come at a high price: a severe recession and very high unemployment. In addition, high interest rates mean that the peripheral economies cannot yet fully return to the capital markets for financing.

The European Stability Mechanism, in coordination with the ECB’s “Outright Monetary Transactions” programme (OMT), has a good chance of becoming an effective “Lender of last resort” for solvent, but illiquid, governments.

A banking union is a step in the right direction, but its implementation will be difficult, because it involves the pooling of sovereignty and national resources at the European level.

There is now a bit less focus on immediate fiscal austerity, which should help the peripheral economies to begin growing again.

Much has been done on structural reforms, but more needs to be implemented. The European Stability Mechanism/OMT conditionality should provide the right incentives for this, but it remains to be seen if the ECB will really stop intervening when a country does not comply.

In the baseline scenario, policymakers are expected to continue coming up with the necessary measures to avoid a major calamity. However, they are not expected to adopt a significantly more proactive stance. Therefore, uncertainty and the ensuing financial market volatility are likely to remain high.

The major risk from the crisis is that governments delay implementing the reform agenda (on a national level, in EU structures, or in the banking sector). Political risks on the implementation process remain high and the insurance industry would face a multitude of problems should there be an exit from the monetary union (see Table 2).

Risk area Description Impact on insurers

Re-denomination risks

Currency re-denominations and the ensuing mismatch of rights and obligations under existing contractual arrangements

High

Restrictions on EU internal market

Restrictions to the guarantees of the free movement of capital, services, or people in the EU Internal Market

High

Investment risks Impact on insurers’ investment portfolios High

Funding risks Liquidity freeze, possibly similar to that observed after the demise of Lehman Brothers

High

Counterparty defaults Inability of counterparties (sovereigns, clients, banks, etc.) to fulfill contractual obligations

Medium

Contract risks

Required changes to existing and new contracts, the validity of existing contracts, and the triggering of contractual terms potentially leading to contract frustration

Medium

Litigation & enforcement risks

Enforcement of contracts and litigation risks in the case of a legal dispute

Medium

Strategic & commercial risks

For example: changed attractiveness of different markets, incorrect pricing

Medium

Operational risk Ability to perform business operations in an effective and efficient manner

Low

Regulatory risks New or changed requirements from the regulators Low

Source: Swiss Re euro-break-up task force

Much progress has been made at resolving the Euro debt crisis, but there is still implementation risk.

Most likely, policymakers will continue to make appropriate decisions, but in a manner that continues to produce market volatility.

If the Euro crisis were to lead to a breakup, re/insurers would face a multitude of problems.

Table 2: Risk issues for re/insurers stemming from an exit from, or a potential break-up of, the European Monetary Union

The macroeconomic environment: Growth will be stronger next year

5

Fiscal cliff in the US

In the US, there are a number of federal government tax increases and spending cuts scheduled to begin in January 2013. Congress could postpone these changes, which amount to a “fiscal cliff” of about USD 600 to 750 billion (4–5% of GDP), into 2013 by simply voting to delay the cliff. Thus, the new Congress would have sufficient time to address these budget issues early next year. The cliff consists of the end of the payroll tax cut (USD 120–125 bn1), the end of the Bush Administration tax cuts (USD 180–250 bn), delay the full roll-out of the Alternative Minimum Tax (USD 55–100 bn), the mandatory “sequester” budget cuts (USD 85–90 bn), the expiry of the extension of the unemploy-ment benefits (USD 30–35 bn), and a myriad of other tax changes and spending cuts (USD 130-200 bn). According to the Congressional Budget Office (CBO), the impact on the economy of allowing the cliff to transpire would be a mild recession, with real GDP declining 0.5% from Q4 of 2012 to Q4 2013.

In the baseline outlook, it is assumed that only about USD 150 billion of the full set of options is implemented and that the fiscal deficit falls about USD 300 billion to around USD 800 billion in fiscal year (FY) 2013 (ending in September 2013), or 5% of GDP. In FY 2012, the deficit declined by USD 200 billion with 2% real GDP growth. The spending cuts and tax increases will slow growth, but not derail the economy. Of course, there are many other likely outcomes, some of which include a recession. A temporary implemen-tation of all the policies, followed by Congress reversing them, would also probably result in a mild recession. The election results have not helped to reduce this risk’s uncertainty, which is likely causing the delay of investments. Commentators are split about what the new Congress will decide.

1 Estimates from the CBO, Barclay Research and Deutsche Bank.

The US faces a “fiscal cliff” which, if allowed to happen, would cause a recession.

Our baseline outlook assumes about USD 150 billion of deficit reduction measures, which keeps growth moderate while lowering the deficit by USD 300 billion, or 2% of GDP.

6

The macroeconomic environment: Growth will be stronger next year

Emerging markets

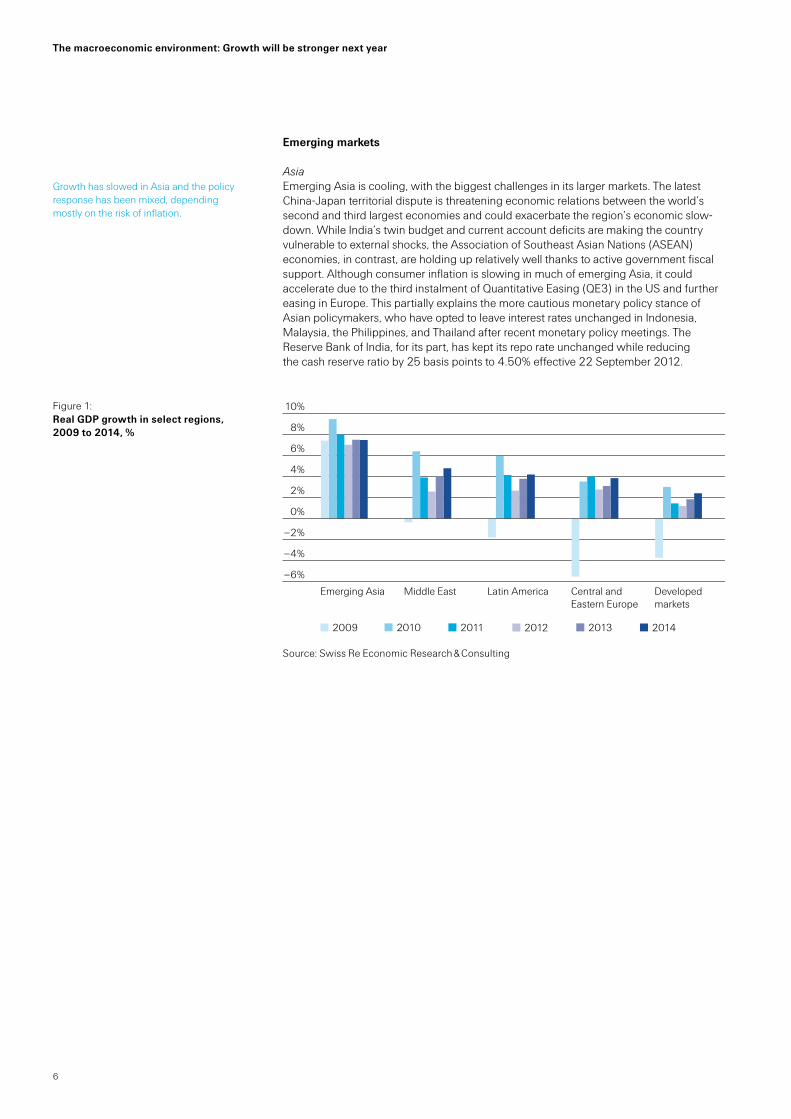

AsiaEmerging Asia is cooling, with the biggest challenges in its larger markets. The latest China-Japan territorial dispute is threatening economic relations between the world’s second and third largest economies and could exacerbate the region’s economic slow-down. While India’s twin budget and current account deficits are making the country vulnerable to external shocks, the Association of Southeast Asian Nations (ASEAN) economies, in contrast, are holding up relatively well thanks to active government fiscal support. Although consumer inflation is slowing in much of emerging Asia, it could accelerate due to the third instalment of Quantitative Easing (QE3) in the US and further easing in Europe. This partially explains the more cautious monetary policy stance of Asian policymakers, who have opted to leave interest rates unchanged in Indonesia, Malaysia, the Philippines, and Thailand after recent monetary policy meetings. The Reserve Bank of India, for its part, has kept its repo rate unchanged while reducing the cash reserve ratio by 25 basis points to 4.50% effective 22 September 2012.

–6%

–4%

–2%

0%

2%

4%

6%

8%

10%

201420132012201120102009

Developed markets

Central and Eastern Europe

Latin AmericaMiddle EastEmerging Asia

Source: Swiss Re Economic Research & Consulting

Growth has slowed in Asia and the policy response has been mixed, depending mostly on the risk of inflation.

Figure 1: Real GDP growth in select regions, 2009 to 2014, %

7

China’s hard landing

China’s economic growth slowed in 2012. The weakness in growth of exports, industrial production, and investment first observed in the second half of 2011 continued through to Q3 2012. Recent indicators suggest that the industrial sector is bottoming out, but not before some of the weaknesses have filtered through to the services sector. Moreover, the lingering territorial dispute with Japan is threatening bilateral economic relations. Although downside risk to growth dominates, China’s real GDP growth is still expected to remain close to 8% in 2012 and 2013. The risk of a hard landing remains unchanged at this stage (25%). Against the backdrop of low inflationary pressure, Chinese policy makers aim to provide further policy support which will likely be target-specific rather than broad-based.

The Gulf economiesGeopolitical tensions, tight credit markets, and increased global economic uncertainty pose a challenge to economic growth in the Gulf economies. A sustained drop in oil prices due to weakening global demand remains the key risk for the region’s oil-exporting economies and could negatively affect public spending plans. Barring this key risk, oil-exporting markets should profit from a pipeline of public sector projects and a strong services sector. Macroeconomic conditions have improved in the United Arab Emirates (UAE), despite the emergence of asset price risks due to geopolitical tensions. However, political unrest continues to be an issue and is leading to the deterioration of the region’s oil-importing markets, with the situation in Egypt still risky despite indications of a fresh start following the recent presidential election. Turkey’s economy picked up in the first quarter, but its current account deficit is likely to remain large and high inflation may be exacerbated by increasing agriculture prices.

Central and Eastern Europe (CEE)The leading economic indicators point to a continuing deterioration in economic growth across CEE in the third quarter of 2012. Poland, the region’s outperformer, has recently witnessed a considerable weakening in domestic demand which had been supporting growth. In contrast, Russian private consumption continues to be strong, increasing wage and price pressures and prompting the central bank to raise its policy rate. Weak demand for exports, particularly from Europe, will lead to a further slowdown in the region’s growth, with Hungary and the Czech Republic already in the throes of recession. The Czech national bank has lowered its policy rate to 0.05% in response, with other countries expected to follow suit if inflationary pressures (Poland) and investor risk perceptions (Hungary) permit. In light of Hungary’s unpredictable policy decisions over the past two years (nationalization of second pillar pensions; special taxes on banks, insurance companies, and financial transactions), the conclusion of an IMF/EU standby agreement would certainly help to restore confidence. To consolidate its sovereign debt, Hungary will clearly need to return to economic growth, given its economy’s stagnation since 2010.

Though growth in China is slowing, the risk of a hard-landing has not increased because China’s policy options have expanded as inflation has declined.

Despite political unrest, the Gulf region is growing, with major public sector projects underway.

The CEE countries are weakening, with growth slowing even in Poland.

8

The macroeconomic environment: Growth will be stronger next year

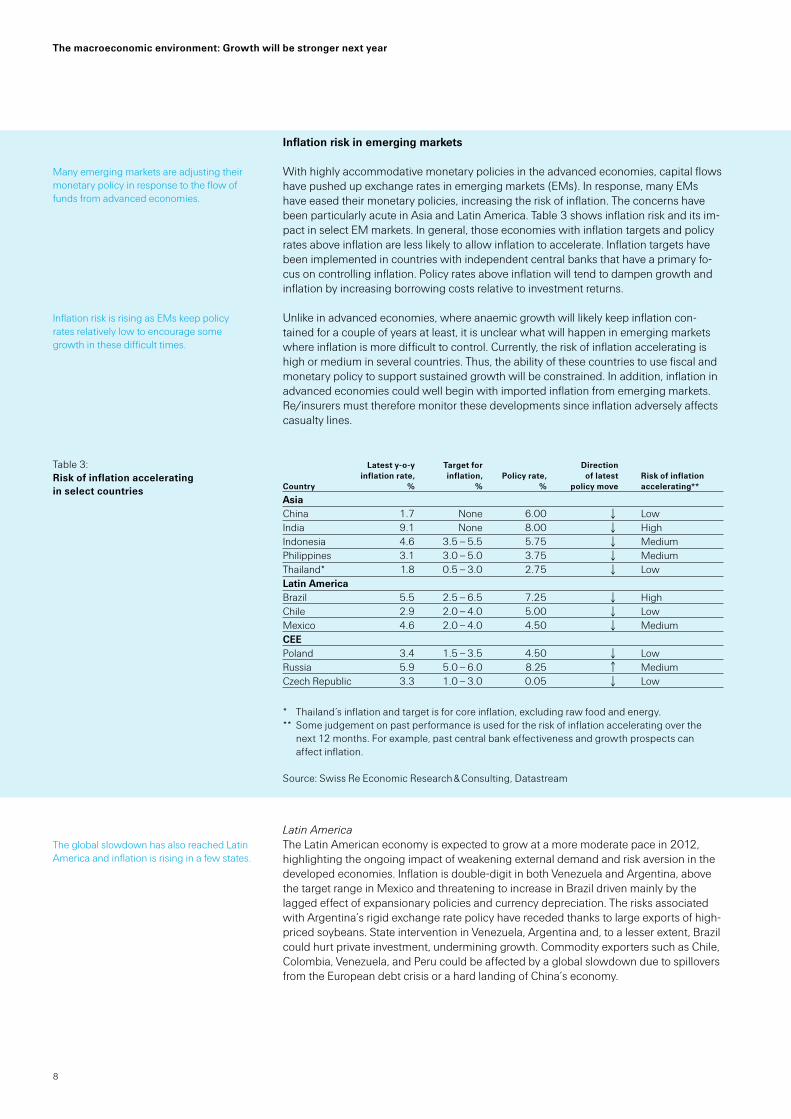

Inflation risk in emerging markets

With highly accommodative monetary policies in the advanced economies, capital flows have pushed up exchange rates in emerging markets (EMs). In response, many EMs have eased their monetary policies, increasing the risk of inflation. The concerns have been particularly acute in Asia and Latin America. Table 3 shows inflation risk and its im-pact in select EM markets. In general, those economies with inflation targets and policy rates above inflation are less likely to allow inflation to accelerate. Inflation targets have been implemented in countries with independent central banks that have a primary fo-cus on controlling inflation. Policy rates above inflation will tend to dampen growth and inflation by increasing borrowing costs relative to investment returns.

Unlike in advanced economies, where anaemic growth will likely keep inflation con-tained for a couple of years at least, it is unclear what will happen in emerging markets where inflation is more difficult to control. Currently, the risk of inflation accelerating is high or medium in several countries. Thus, the ability of these countries to use fiscal and monetary policy to support sustained growth will be constrained. In addition, inflation in advanced economies could well begin with imported inflation from emerging markets. Re/insurers must therefore monitor these developments since inflation adversely affects casualty lines.

Latest y-o-y Target for Direction inflation rate, inflation, Policy rate, of latest Risk of inflation Country % % % policy move accelerating**

Asia China 1.7 None 6.00 ↓ LowIndia 9.1 None 8.00 ↓ HighIndonesia 4.6 3.5 – 5.5 5.75 ↓ MediumPhilippines 3.1 3.0 – 5.0 3.75 ↓ MediumThailand* 1.8 0.5 – 3.0 2.75 ↓ LowLatin America Brazil 5.5 2.5 – 6.5 7.25 ↓ HighChile 2.9 2.0 – 4.0 5.00 ↓ LowMexico 4.6 2.0 – 4.0 4.50 ↓ MediumCEE Poland 3.4 1.5 – 3.5 4.50 ↓ LowRussia 5.9 5.0 – 6.0 8.25 ↑ MediumCzech Republic 3.3 1.0 – 3.0 0.05 ↓ Low

* Thailand’s inflation and target is for core inflation, excluding raw food and energy. ** Some judgement on past performance is used for the risk of inflation accelerating over the

next 12 months. For example, past central bank effectiveness and growth prospects can affect inflation.

Source: Swiss Re Economic Research & Consulting, Datastream

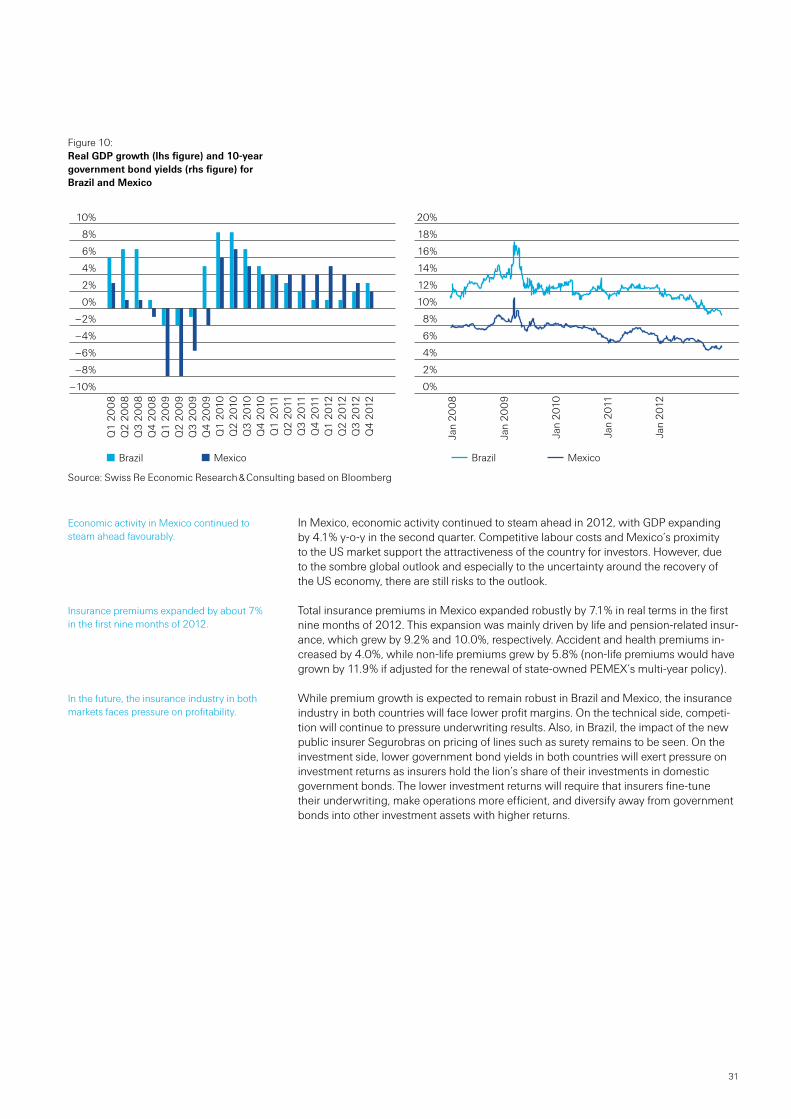

Latin America The Latin American economy is expected to grow at a more moderate pace in 2012, highlighting the ongoing impact of weakening external demand and risk aversion in the developed economies. Inflation is double-digit in both Venezuela and Argentina, above the target range in Mexico and threatening to increase in Brazil driven mainly by the lagged effect of expansionary policies and currency depreciation. The risks associated with Argentina’s rigid exchange rate policy have receded thanks to large exports of high-priced soybeans. State intervention in Venezuela, Argentina and, to a lesser extent, Brazil could hurt private investment, undermining growth. Commodity exporters such as Chile, Colombia, Venezuela, and Peru could be affected by a global slowdown due to spillovers from the European debt crisis or a hard landing of China’s economy.

Many emerging markets are adjusting their monetary policy in response to the flow of funds from advanced economies.

Inflation risk is rising as EMs keep policy rates relatively low to encourage some growth in these difficult times.

Table 3: Risk of inflation accelerating in select countries

The global slowdown has also reached Latin America and inflation is rising in a few states.

9

Risk scenarios

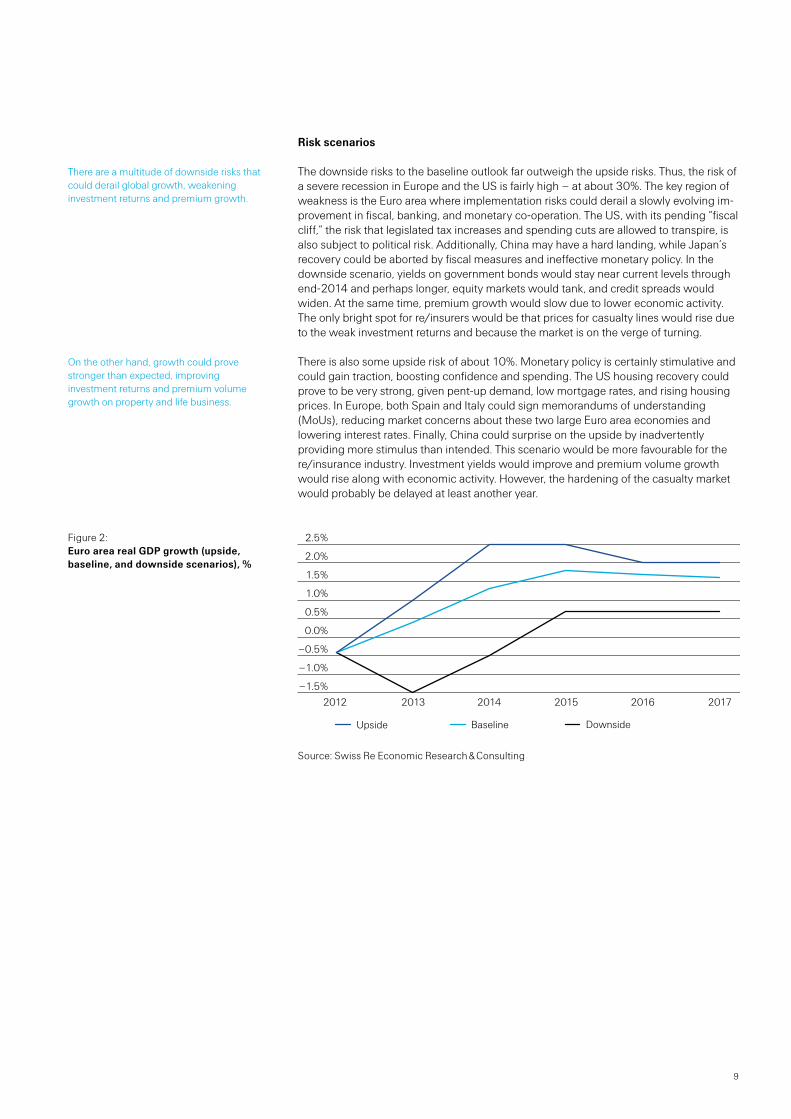

The downside risks to the baseline outlook far outweigh the upside risks. Thus, the risk of a severe recession in Europe and the US is fairly high – at about 30%. The key region of weakness is the Euro area where implementation risks could derail a slowly evolving im-provement in fiscal, banking, and monetary co-operation. The US, with its pending “fiscal cliff,” the risk that legislated tax increases and spending cuts are allowed to transpire, is also subject to political risk. Additionally, China may have a hard landing, while Japan’s recovery could be aborted by fiscal measures and ineffective monetary policy. In the downside scenario, yields on government bonds would stay near current levels through end-2014 and perhaps longer, equity markets would tank, and credit spreads would widen. At the same time, premium growth would slow due to lower economic activity. The only bright spot for re/insurers would be that prices for casualty lines would rise due to the weak investment returns and because the market is on the verge of turning.

There is also some upside risk of about 10%. Monetary policy is certainly stimulative and could gain traction, boosting confidence and spending. The US housing recovery could prove to be very strong, given pent-up demand, low mortgage rates, and rising housing prices. In Europe, both Spain and Italy could sign memorandums of understanding (MoUs), reducing market concerns about these two large Euro area economies and lowering interest rates. Finally, China could surprise on the upside by inadvertently providing more stimulus than intended. This scenario would be more favourable for the re/insurance industry. Investment yields would improve and premium volume growth would rise along with economic activity. However, the hardening of the casualty market would probably be delayed at least another year.

–1.5%

–1.0%

–0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

DownsideBaselineUpside

201720162015201420132012

Source: Swiss Re Economic Research & Consulting

There are a multitude of downside risks that could derail global growth, weakening investment returns and premium growth.

On the other hand, growth could prove stronger than expected, improving investment returns and premium volume growth on property and life business.

Figure 2: Euro area real GDP growth (upside, baseline, and downside scenarios), %

10

Non-life re/insurance: Premiums are growing, but profits remain weak

Non-life primary insurance

Growth in non-life insurance business further accelerated in 2012. The main driver of advanced market growth was no longer exposure growth – which weakened with the slowing global economy – but moderate rate increases in some markets. Meanwhile, non-life insurance growth in emerging markets moderated slightly, though at a much higher level than advanced markets.

Underwriting results recovered from record catastrophe losses in 2011. However, adjust-ing for catastrophe losses and positive reserve developments from earlier accident years, underlying underwriting profitability2 continued to erode due to rising claims and several years of softening rates. The gradual improvement in premium rates in some key markets has not yet been able to change the general soft market picture.

Additionally, the industry saw weak investment returns, partially due to record low inter-est rates, sluggish cash flows, and feeble capital gains or capital losses. The Euro debt crisis also lowered the mark-to-market valuations of some fixed income securities. Squeezed from all sides, the average profitability for the industry was low, with a return on equity (RoE) for 2012 of only 5%.3

Capital levels are strong, but balance sheet risks are also highThe solvency of the industry continues to be strong. With an average estimated solvency ratio of 118%, the industry is capitalized at pre-crisis levels. However, balance sheet risks have increased. Also, in the current macroeconomic environment, accounting rules tend to overstate non-life insurance assets and understate liabilities. Capital is sufficient to withstand the main catastrophe scenarios, but it is not excessive from an economic standpoint.4

Additionally, European non-life insurers are significantly exposed to the European sover-eign debt crisis. While the impairment of Greek bonds has had a limited direct impact on the non-life industry, mark-to-market write-downs on southern European government bonds are impacting asset values. Uncertainty around sovereign debt has multiplied via its effect on the banking sector. Insurance companies in southern European countries are especially impacted, with impairments and lending restrictions causing ripple effects in asset classes.

Apart from asset-related issues, the risks on the liability side are also rising. Due to higher precaution, insurers today are willing to back less capacity with the same dollar of capital than before the crisis. Insurers have begun to wonder how adequate their claims reserves are after years of soft market conditions and rising inflation risks. There are more frequent cases of reserve additions. Also the latest revisions to property catastrophe models show increasing exposures to natural catastrophes.

Another aspect is the impact of GAAP accounting on non-life insurers’ capital levels. Mark-to-market, or “fair market”, valuations of fixed income assets are inflated by low interest rates. Compared to 2010, the benchmark interest rates of AAA-rated government bond indices have further decreased by about 150 basis points, causing unrealized mark-to-market gains. These gains will disappear as the bonds mature5, even if interest rates remain, as expected, at low levels for the next two years.

2 The underwriting result is defined as the difference between premiums and the sum of expenses plus claims costs.

3 The calculation of the industry average is based on data for the following eight leading non-life insurance markets: Australia, Canada, France, Germany, Italy, Japan, the United Kingdom, and the US.

4 This phenomenon is the result of a discrepancy between accounting capital and economic capital. In a nutshell, under current accounting rules, the valuation of assets varies with changing interest rates, whereas liabilities remain stable. If liabilities, such as claims reserves, were discounted with the same interest rates, insurers’ capital would be far less volatile.

5 Realising these capital gains would not substantially change an insurer’s economic situation, since reinvesting the proceeds would result in lower yields.

In 2012, non-life growth accelerated slightly …

… while underlying underwriting profitability continued to deteriorate.

RoE remained at low levels.

Capitalisation, which now exceeds pre-crisis levels according to accounting figures, is overstated.

In addition, European non-life insurers are impaired by the European sovereign debt crisis and equity exposures.

Insurers are putting less capital at risk during this phase of high uncertainty.

Low interest rates inflate insurers’ assets.

11

Last but not least, current capital market conditions are still not favourable for raising capital, for example in case of a catastrophic event. Low price-to-book valuations make the option of raising capital unattractive. Many insurers, perhaps realising that their capital levels are not what they seem from an accounting perspective, have started hoarding capital. Many have scaled back their share buyback programmes.

Premium growth is making headway Compared to the long-term trend, global premium growth in 2012 continued to be weak, though it expanded at 3.0% in real terms (compared to 2.3% in 2011 and 1.4% in 2010). Expansion was driven by a slight acceleration in advanced market growth, which was more due to rate increases than to exposure growth in a slowing global economy.

In the emerging markets, growth slowed slightly, from 8.7% in 2011 to 7.9% in 2012, pri-marily as a result of macroeconomic cooling. Eastern Europe saw a strong and positive development: non-life insurance premiums expanded by 6.1% in 2012, compared to a meagre 2.8% in 2011. Expansion was broad based, meaning that all regions contributed. Emerging Asia was again the most robust region, with 9.7% non-life insurance premium growth.

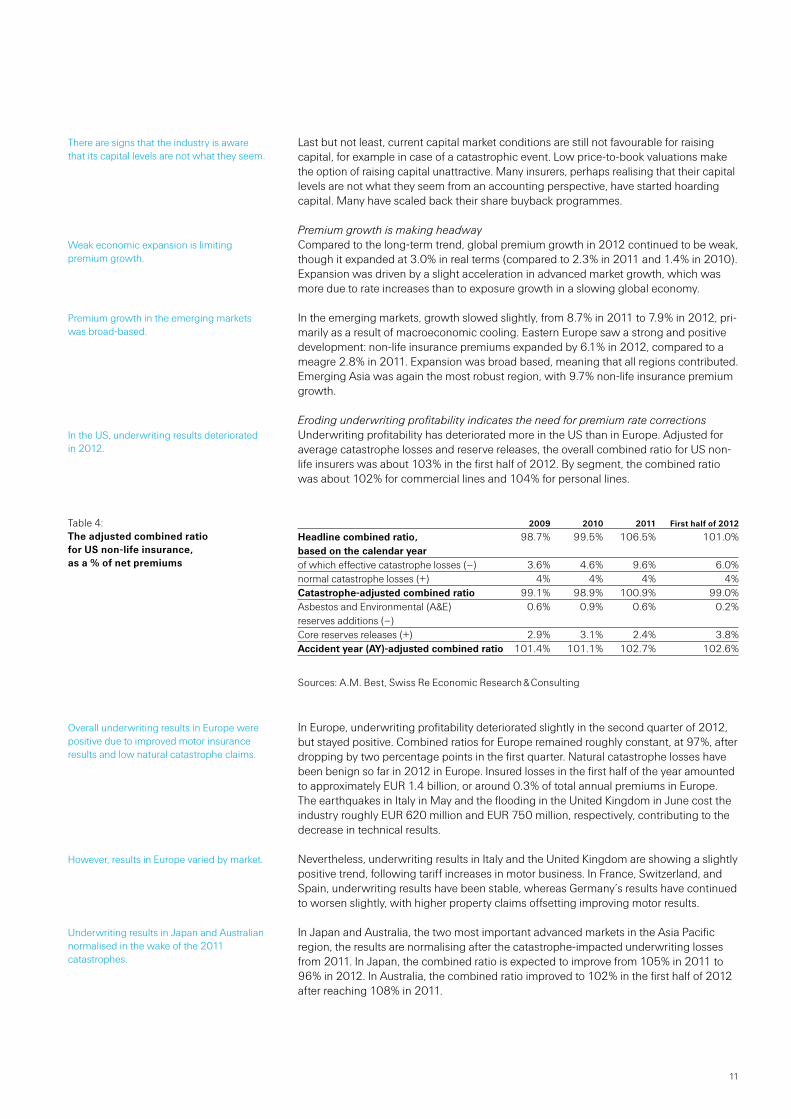

Eroding underwriting profitability indicates the need for premium rate corrections Underwriting profitability has deteriorated more in the US than in Europe. Adjusted for average catastrophe losses and reserve releases, the overall combined ratio for US non-life insurers was about 103% in the first half of 2012. By segment, the combined ratio was about 102% for commercial lines and 104% for personal lines.

2009 2010 2011 First half of 2012

Headline combined ratio, 98.7% 99.5% 106.5% 101.0% based on the calendar year of which effective catastrophe losses (–) 3.6% 4.6% 9.6% 6.0%normal catastrophe losses (+) 4% 4% 4% 4%Catastrophe-adjusted combined ratio 99.1% 98.9% 100.9% 99.0%Asbestos and Environmental (A&E) 0.6% 0.9% 0.6% 0.2% reserves additions (–) Core reserves releases (+) 2.9% 3.1% 2.4% 3.8%Accident year (AY)-adjusted combined ratio 101.4% 101.1% 102.7% 102.6%

Sources: A.M. Best, Swiss Re Economic Research & Consulting

In Europe, underwriting profitability deteriorated slightly in the second quarter of 2012, but stayed positive. Combined ratios for Europe remained roughly constant, at 97%, after dropping by two percentage points in the first quarter. Natural catastrophe losses have been benign so far in 2012 in Europe. Insured losses in the first half of the year amounted to approximately EUR 1.4 billion, or around 0.3% of total annual premiums in Europe. The earthquakes in Italy in May and the flooding in the United Kingdom in June cost the industry roughly EUR 620 million and EUR 750 million, respectively, contributing to the decrease in technical results.

Nevertheless, underwriting results in Italy and the United Kingdom are showing a slightly positive trend, following tariff increases in motor business. In France, Switzerland, and Spain, underwriting results have been stable, whereas Germany’s results have continued to worsen slightly, with higher property claims offsetting improving motor results.

In Japan and Australia, the two most important advanced markets in the Asia Pacific region, the results are normalising after the catastrophe-impacted underwriting losses from 2011. In Japan, the combined ratio is expected to improve from 105% in 2011 to 96% in 2012. In Australia, the combined ratio improved to 102% in the first half of 2012 after reaching 108% in 2011.

There are signs that the industry is aware that its capital levels are not what they seem.

Weak economic expansion is limiting premium growth.

Premium growth in the emerging markets was broad-based.

In the US, underwriting results deteriorated in 2012.

Table 4: The adjusted combined ratio for US non-life insurance, as a % of net premiums

Overall underwriting results in Europe were positive due to improved motor insurance results and low natural catastrophe claims.

However, results in Europe varied by market.

Underwriting results in Japan and Australian normalised in the wake of the 2011 catastrophes.

12

Investment returns continue to suffer from low interest rates and volatile capital markets While underwriting results improved compared to last year, earnings are under pressure from weak investment returns. In the fifth consecutive year of financial market turbulence, the investment environment for the insurance industry remained difficult. Investments in fixed income securities, by far the main asset class, provide only poor yields but are exposed to a multitude of risks. Other asset classes may offer better returns, but at the cost of elevated volatility.

The graph below shows that in Germany, non-life insurers’ running yields are following the general interest rate trend. Maturing bonds and new cash flows can only be invested at lower yields, driving down the average yield of a bond portfolio. Even if market rates bottom out at their current low levels, insurers’ running yields are predestined to decline further. The same will apply to other markets where interest rates are at historical lows.

0%

1%

2%

3%

4%

5%

6%

7%

8%

10-year government bond yileds, yearly average

Non-life insurers’ running yield

20142012201020082006200420022000

Sources: Bafin; GDV; Swiss Re Economic Research & Consulting

As a consequence of the low interest rate environment, contributions from investment returns to overall profitability are low and are expected to decline further. For 2012, investment returns are estimated at around 11% of net premiums earned, which is substantially below the 13.5% average achieved between 1999 and 2007.

Profitability is therefore under pressure from both the underwriting and the investment side, and the current moderate rate increases are not yet sufficient to offset past declines and low investment yields. The RoE from the main non-life insurance markets is expected to be about 5% in 2012, only slightly better than the low in 2011 and clearly falling short of the industry’s cost of capital.

The outlook for 2013 / 2014 shows more growth but persistently weak profitability For 2013, global economic forecasts are more positive and the demand for non-life insurance should increase. In the emerging markets, strong premium growth is set to continue, although expansion will decrease slightly next year due to weaker premium expansion in Latin America and Asia.

Pricing has started to improve in many non-life insurance segments, though it is still far away from a broader-based hardening. However, varying pricing signals have surfaced for different lines of business. In the US, according to recent surveys, commercial insur-ance rate increases are accelerating. In Europe, several market leaders have attempted to introduce modest rate improvements during the renewals of their commercial line books. Of all the personal lines, motor insurance is the largest and also the most cyclical. Motor insurance has registered some important improvements, even in markets with severe profitability issues, such as the UK and Italy.

Current investment yields are down ...

... and running yields are set to decline further.

Figure 3: Non-life insurers’ running yield in Germany versus 10-year German government bond yields

Investment returns are contributing less to net income.

The non-life insurance industry’s RoE is weak, at 5%.

Challenges will persist through 2013, but conditions should improve.

There are signs that pricing may be stabilising as rates improve in some markets and for some lines.

Non-life re/insurance: Premiums are growing, but profits remain weak

13

The current market situation is typical for a mature soft market cycle. Prices have stopped softening, but they are not yet hardening in all regions and market segments. A some-what broader and stronger turn in insurance pricing is expected in 2013, setting the stage for improving underwriting profitability. Exactly when a broader-scale hardening will occur is uncertain, but the following important factors point to an eventual strong turn in the market: Reserving may soon prove to be insufficient. It is difficult to estimate the timing of this

and there are big differences between individual companies. Reserves releases from previous years will eventually result in the need to strengthen reserves. When this sets in, it will no longer be possible to ignore insufficient pricing and the scene will be set for a hardening of rates.

Stricter solvency regulations and higher capital requirements will help turn the market. Solvency II is still expected to be implemented, though with a delay. A further tightening of rating agency models is also expected.

Volatile and significant capital market developments impacting insurers’ capital base may turn out to be another trigger for rate-hardening. Such developments could include significant impairment of invested assets or a quick and strong rise in interest rates.

Overall profitability is not expected to rebound quickly. Nevertheless, underwriting profit-ability is likely to improve slightly in most markets and segments in 2013 and 2014. Investment returns are expected to remain low next year. Profitability will rise slowly as prices and interest rates increase. Accounting profits will only rise gradually since some improvements accrue with a lag. Reserve releases may have adverse effects in 2013, reducing profits in the near term and accelerating the hardening of casualty rates.

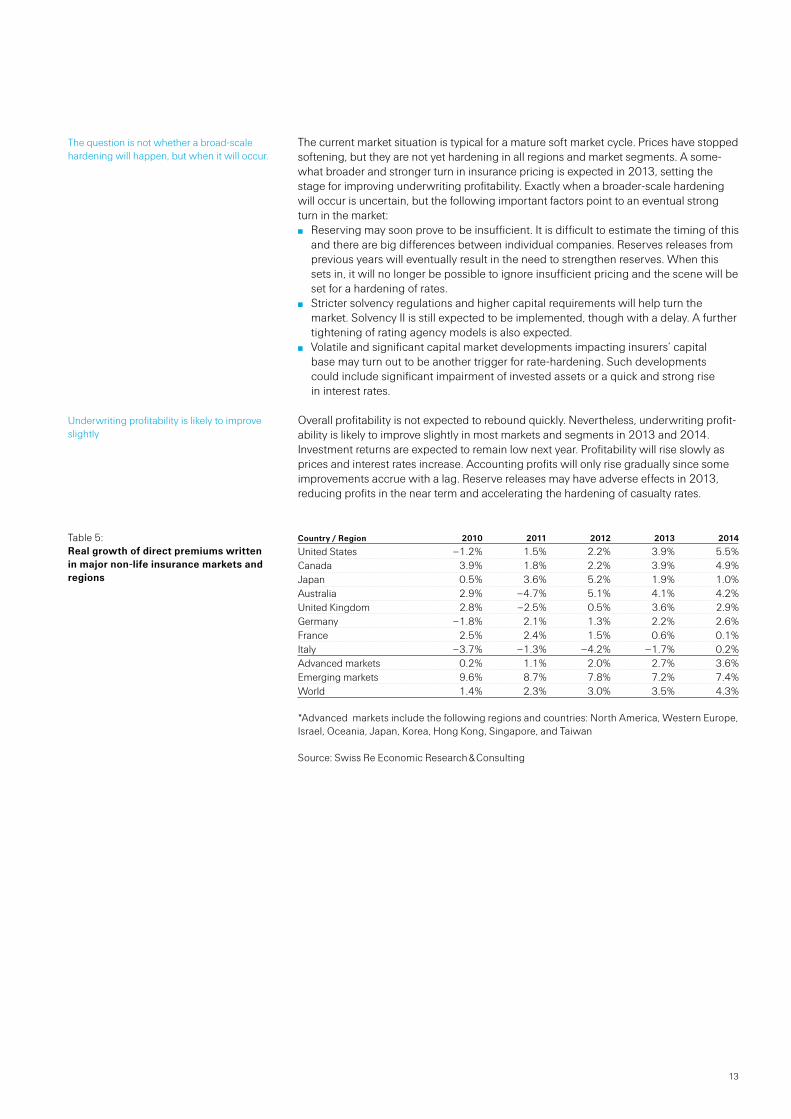

Country / Region 2010 2011 2012 2013 2014

United States –1.2% 1.5% 2.2% 3.9% 5.5%Canada 3.9% 1.8% 2.2% 3.9% 4.9%Japan 0.5% 3.6% 5.2% 1.9% 1.0%Australia 2.9% –4.7% 5.1% 4.1% 4.2%United Kingdom 2.8% –2.5% 0.5% 3.6% 2.9%Germany –1.8% 2.1% 1.3% 2.2% 2.6%France 2.5% 2.4% 1.5% 0.6% 0.1%Italy –3.7% –1.3% –4.2% –1.7% 0.2%Advanced markets 0.2% 1.1% 2.0% 2.7% 3.6%Emerging markets 9.6% 8.7% 7.8% 7.2% 7.4%World 1.4% 2.3% 3.0% 3.5% 4.3%

*Advanced markets include the following regions and countries: North America, Western Europe, Israel, Oceania, Japan, Korea, Hong Kong, Singapore, and Taiwan

Source: Swiss Re Economic Research & Consulting

The question is not whether a broad-scale hardening will happen, but when it will occur.

Underwriting profitability is likely to improve slightly

Table 5: Real growth of direct premiums written in major non-life insurance markets and regions

14

Non-life re/insurance: Premiums are growing, but profits remain weak

The non-life reinsurance market

Aside from the financial crisis and the soft underwriting cycle, natural catastrophes are leaving the most substantial mark on earnings for the reinsurance sector. In the first three quarters of 2012, the global reinsurance industry enjoyed a good, though not strong per-formance. However, the fourth quarter will be significantly impacted by the multi-billion-dollar Hurricane Sandy claim. It is too early to predict Hurricane Sandy’s exact impact on the reinsurance industry, but based on the assumption that there will not be another major catastrophe event in 2012, a combined ratio of between 103% and 105% and an RoE of 4% to 5% is expected for the reinsurance industry in 2012.

Non-life reinsurance capital is sufficient, but not as strong as it appearsRating agencies report of moderate excess capital globally. However, this capital is une-venly distributed across a few players and there is no trend of positive rating outlooks. Capital requirements have increased due to hikes in risk charges associated with re-serves, higher modelled exposures to natural catastrophes, and riskier assets. Additional uncertainties relating to Solvency II will also raise capital requirements on average. Furthermore, the risk of claims reserve deficiencies is increasing. On the one hand, much of the reserve redundancies accumulated during the last hard market has been released, on the other hand, the most recent accident years may develop negatively in the medium term.

Figure 4 depicts net premiums and GAAP shareholders’ equity for the global non-life reinsurance industry from 1999 until the first half 2012. It shows that: Capital levels recovered by the end of 2009 from the financial crisis-induced 2008

slump Throughout 2010 and 2011, capital remained constant and continued to increase

slightly until the first half of 2012 (light blue line). However, reinsurance capital is inflated by high assets valuations of fixed-income securities.

Unrealised capital gains on fixed income securities which were between 4% and 5% in 2009 and 2010, soared to 15% at the end of 2011. These unrealised gains are only temporary in nature und will disappear over time as interest rates rise or bonds mature.

Premium income has, after years of stagnation, started to increase again, reflecting the end of the soft market underwriting cycle and the moderate hardening of rates.

40

60

80

100

120

140

160

excl unrealised gains on fixed-income securities (from 2008 onwards)

CapitalNet premiums

2011200920072005200320011999

Index (2005 = 100)

Source: Swiss Re Economic Research & Consulting

Hurricane Sandy is turning underwriting results negative.

Global reinsurers maintained their strong capitalisation in 2012.

Figure 4: Global non-life reinsurance premiums and GAAP capital, Index 2005 = 100

15

Thus, the current capitalisation of the reinsurance industry provides an appropriate level of solvency to meet security needs of policyholders, regulators and rating agencies. But there is no substantial excess capital, given current balance sheet risks.

Non-life reinsurance rates are levelling out overall, and hardening in some segments The 2012 renewals in January, April, and July confirmed that reinsurance markets are improving. Reinsurance capacity was seen as adequate-to-abundant across all lines and regions, and rates have gradually started to harden. Even rates for long-tail lines of business have been firming after years of softening. However, adequate pricing must incorporate current risk exposures and the low interest rate environment.

Following the severe natural catastrophe losses in 2011, property catastrophe covers showed the most significant rate increases. Property catastrophe pricing improved be-tween 5% and 10% on a risk-adjusted basis. Areas that suffered the largest catastrophe losses showed the firmest upward rate pressure.

Underwriting profitability is becoming increasingly volatileReinsurer combined ratios benefited from below-average natural catastrophe claims in the first nine months of 2012. The industry’s average combined ratio through June was 90%, down from 125% in the first half of 2011. This is good news insofar as the 2012 combined ratio is roughly at the same level as in 2009. However, the volatility of the global reinsurance business is steadily increasing with the growing weight of the property catastrophe business. As evidence of this, Hurricane Sandy claims will dominate reinsur-ance underwriting results in the fourth quarter of 2012. The combined ratio for the year is expected to end at between 103% and 105%.

Nevertheless, underwriting profitability in reinsurance markets held up better than in many primary markets. The industry still benefits from the hard market years of 2002 and 2003, and from the more benign claims of the 2009 to 2010 recession years. Releases from loss reserves in prior years are currently helping to improve underwriting results by two-to-three percentage points.

Investment returns remain weak Like primary insurers, reinsurers have suffered from the European debt crisis, low interest rates, and weak equity markets, so their investment income will also remain weak in 2012. In the first half of the year, they showed a yield of 3.4% compared to 3.9% one year earlier. Non-life reinsurers leverage more assets, so declining investment returns affect their profitability more than primary non-life insurers’.

Due to below-average natural catastrophe losses, overall profitability was solid during the first half of the year. RoE for the first half of 2012 was 14%, compared to -1% in the first half of 2011. Year-to-date, the reinsurance industry’s average RoE level was higher than for primary insurers. For the full year 2012, an RoE of around 4% to 5% is expected, similar to the 4% RoE in 2011.

There is no substantial excess capital.

Property catastrophe rates are improving …

… while a broad market turn is still to come.

Catastrophe losses had again the biggest impact on earnings. The combined ratio for 2012 will be between 103% and 105%.

Reserves releases from the hard market years are still supporting profitability.

Capital gains and current yields are down.

RoE is expected to be only 4% to 5% in 2012, about the same as the 4% in 2011.

16

Non-life re/insurance: Premiums are growing, but profits remain weak

The outlook is subdued for 2012 but brighter for 2013, and growth is set to improve Premium income growth for 2013, which largely follows premium trends in the primary insurance sector, is expected to improve again, from 3.4% this year to 4.9% in 2013 and 5.7% in 2015. Of the additional expected volume of around USD 28 billion by 2014, around USD 18 billion will stem from advanced markets and USD 10 billion from emerg-ing markets. Pricing signals from this year’s re/insurance industry conventions in Monte Carlo and Baden-Baden indicate that the 2013 renewals will be stable to slightly firmer. Significant hardening will be limited to lines and segments that have recently experienced high losses. This could include higher rates for hurricane risks after Hurricane Sandy. Casualty rates, especially in the US, have moderately turned, but they are still far from their previ-ous levels; additional hardenings will only come with an expected increase in adverse claim developments.

Assuming average catastrophe losses, the combined ratio is expected to be around 97% in 2013. This estimate is based on a scenario that assumes a moderate rate increase, a less benign claims environment than the last three years, and declining reserve releases. Underwriting profitability is expected to remain below the average of recent years. Also, because of the low interest rate environment in advanced markets, which is expected to continue into 2014, investment returns are not expected to reach their pre-financial crisis levels. The overall profitability outlook for 2013 and 2014 is therefore moderate. For the reinsurance industry, an average RoE of 8% to 9% can be expected.

2010 2011 2012 2013 2014

Advanced markets –4.3% 5.9% 2.1% 3.8% 4.9%Emerging markets –0.2% 15.5% 7.7% 8.5% 7.8%World –3.5% 8.0% 3.4% 4.9% 5.7%

Source: Swiss Re Economic Research & Consulting

Premium growth will be subdued in advanced markets, but strong in emerging markets.

Prices will be stable to slightly firmer.

The average combined ratio is expected to be around 97% in 2013, and profitability in 2013 and 2014 is expected to be moderate.

Table 6: Real growth of non-life reinsurance premiums

17

Life re/insurance: Navigating choppy waters

The primary life insurance market

Global life insurance premium income stagnated in 2012 in real terms. Though companies reported respectable results, the situation and outlook remains challenging. Low interest rates, volatile financial markets, regulatory changes, and weak demand - especially for mainstay life insurance savings and accumulation products - will result in a demanding business environment over the next few years. However, there are business opportunities for life insurers that are able to turn the huge existing protection gap into sales

Capital further improved – but is overstated in financial accountingThe life insurance industry’s reported financial accounting capitalization has further improved in 2012, partially driven by declining interest rates. The decline in interest rates has resulted in temporary, mark-to-market fixed-income investment gains,6 which will revert once interest rates increase or these investments approach maturity. From an eco-nomic, risk-based framework perspective, however, the decline in interest rates in 2012 resulted in lower capital for life insurers. According to companies’ 2011 embedded value reports, a decrease in interest rates by one percentage point results in significant reduc-tions in embedded value whose magnitude depend on the life insurers’ product mix and the types of guarantees offered.7 The true picture is therefore likely not as favourable as might be concluded from an analysis of financial accounting statements.

0

20

40

60

80

100

120

140

Market cap weighted average

Q2

201

2

Q1

201

2

Q4

201

1

Q3

201

1

Q2

201

1

Q1

201

1

Q4

201

0

Q3

201

0

Q2

201

0

Q1

201

0

Q4

20

09

Q3

20

09

Q2

20

09

Q1

20

09

Q4

20

08

Q3

20

08

Q2

20

08

Q1

20

08

Q4

20

07

Sources: Company reports, Bloomberg, Swiss Re Economic Research & Consulting

Note: Based on IFRS/US GAAP data. Missing Q1/Q3 values are interpolated. Companies in the sample include: AFLAC; Allianz; Assurant inc; Aviva; AXA; China Life; CNP; Delphi Financial; Generali; Genworth Financial; Great-West Lifeco; Hartford; Legal & General; Lincoln National; Manulife; Metlife Group; Phoenix Companies; Ping An; Principal Financial Group; Protective Life; Prudential (UK); Prudential (US); St. James Place; Stan Corp Financial Group; Standard Life; Storebrand ASA; Sun Life; Swiss Life; Torchmark; Zurich.

6 In US GAAP and Japan GAAP, interest rates used to value liabilities are locked in. Under IFRS, valuation of insurance liability allows insurers to use either US or local GAAP. In the UK, Canada, Australia, Netherlands, Sweden, South Africa, and other countries, local GAAP do not lock in interest rates.

7 Source: Swiss Re Economic Research & Consulting, based on EEV/MCEV reports of 28 European and Asian companies. See sigma 4/2012.

Global premium income stagnated in 2012. The outlook remains challenging.

Capitalisation on an accounting basis has further improved in 2012; however, from an economic/risk-based view, capital has likely deteriorated.

Figure 5. The shareholder equity for 32 global composite and life insurance companies, Q4 2007=100

18

Life re/insurance: Navigating choppy waters

The biggest challenge in many markets is the ongoing low interest rate environment. The negative effect of low interest rates on investment yield is slow to fully play out because only current premium income, which is a fraction of total investments, is invested at market yields. Changes in insurers’ running yields therefore lag behind changes in interest rates. In many cases, the duration of liabilities is longer than the duration of investments and for this reason, insurers cannot fully offset the decline in investment yield by making adjustments to product guarantees and prices. Insurers increasingly must honour guar-antees close to, or even above, their average investment yield, resulting in lower profita-bility in recent years and perhaps negatively impacting capitalization and solvency if interest rates remain low. In view of these challenges, regulators in many countries have supported life insurance through various capital relief measures.

In-force premiums and new business developed poorly in 2012Global premium income stagnated in 2012. In advanced markets, premium income declined by 0.4% (after inflation). Premiums fell by about 1.9% in North America, 5% in Western Europe, and 4.4% in Oceania. The only advanced markets with strong growth were in Asia: Japan, Hong Kong, Singapore, Korea, and Taiwan.

In emerging markets, premium income increased by 2.3%. Growth was strongest in Latin America and Central and Eastern Europe (9.0% and 6.8%, respectively), followed by Africa with an increase in premium income of around 3.2%. In emerging Asian coun-tries, premium income declined by 0.3%, driven by a 2.0% contraction in both China and India. In China, the decline was driven by regulatory changes in 2011 that constrained bancassurance sales. These regulatory changes will continue to impact the industry in the future. In India, various regulatory changes are in motion to tackle existing issues in the sector, such as mis-selling and low transparency. While the short-term impact of these measures is negative, they will help to promote the further development of the Indian life insurance market in the long term.

Country 2010 2011 2012 2013 2014

US –0.6% 3.8% –2.1% 1.6% 3.1%Canada –1.0% –2.4% –0.8% 2.0% 3.0%UK –12.5% –8.8% –2.8% –1.0% 1.0%Japan 4.6% 8.5% 8.0% 2.0% 2.0%Australia –0.8% 5.9% –4.6% 4.5% 4.5%France 2.7% –15.1% –15.1% –0.3% 2.2%Germany 6.8% –7.1% –4.3% –0.7% 0.2%Italy 9.4% –20.2% –7.0% –0.9% 0.7%Spain –10.0% 8.6% –10.7% 0.8% 1.5%Netherlands –0.9% –0.5% –4.4% 2.4% 3.2%Advanced markets 1.6% –2.5% –0.4% 1.5% 2.5%Emerging markets 10.9% –5.0% 2.3% 6.2% 6.8%World 2.8% –2.9% 0.0% 2.2% 3.1%

Source: Swiss Re Economic Research & Consulting

Interest rates are the biggest challenge in life insurance.

With premium income in advanced markets declining slightly, global premium income stagnated in 2012.

Premium development in emerging market was hindered by weak premium development in India and China.

Table 7: In-force, real premium income growth for life insurance

19

Premium growth has been weak due to low macroeconomic growth, high uncertainty, and volatile financial markets. Most affected was the life insurance savings and retirement business, which becomes less attractive for customers when interest rates are low. With current record-low interest rates, customers tend to avoid unit-linked products and refrain from locking into long-term contracts. At the same time, such business also becomes less attractive for life insurance companies because low interest rates and volatile equity markets erode profit margins and risk-return patterns.

Unsurprisingly, new business in many countries deteriorated in 2012. In the US, new business dropped by more than 7%, reflecting a sharp sales decline in fixed and variable annuity products, the most important life insurance products by premium volume. Sales of these products were scaled back because of profitability challenges as well as con-sumer reluctance to buy due to less attractive guarantees and higher prices. In Italy and Germany, sales declined for a second year in a row, although at a slower pace than in 2011. In France, where most business is single-premium savings business, sales are estimated to have declined dramatically, in part because banks offered substitute prod-ucts at more attractive terms. In Australia, new business stagnated. The only exception among the major markets is Japan, where life insurance sales have continued their strong growth pattern.

Sales of insurance protection products (mortality and morbidity risk) are traditionally much less volatile than insurance savings products. Protection products held up relatively well during the crisis, but the picture in 2012 is rather mixed across markets. Insurance protection sales in the UK stabilised in the first half of 2012, following a number of years of contraction. The improvement was due to increased group business, which benefited from changes in state benefit entitlements as well as an improvement in employment. In contrast, individual policy sales continued to fall, with the sluggish housing market dragging down traditional term insurance business. Critical illness protection business remained broadly flat.

In the US, sales of term insurance products appear to have stabilized in 2012, after de-clining for three consecutive years. Disability insurance sales premiums have bounced back as well, especially in the group market, thanks to recently-implemented price in-creases and rising employment. In Canada, term sales rebounded strongly in the first half of the year, following a contraction in 2011. Term sales have slightly increased in Germany, while disability and long-term care insurance have continued to grow strongly. Also, in Australia and in many Asian markets (eg in Singapore, Taiwan, China, India, and Thailand), protection product sales have been relatively strong.

Going forward, there is ample potential to grow mortality protection products sales, given that a huge protection gap exists in many markets and consumer awareness of underinsurance is on the rise (see Box: “The US mortality protection gap”). At the same time, mortality protection business is attractive for life insurers in the current environment since its profitability performance is less sensitive to interest rates than savings and morbidity products.

Weak demand and reduced supply resulted in a strong decline in savings and retirement business.

New business volumes declined in most countries.

In the UK, sales of term, disability, and critical illness insurance products are flat-to-improving.

In the US, term insurance premium growth is stabilising, but other countries have strong growth in various products.

There is ample potential to increase protection product sales, both from the demand and supply side.

20

Life re/insurance: Navigating choppy waters

The US mortality protection gap

Over the past decade, the US mortality protection gap – or the extent to which families are insufficiently covered in the event of the death of the primary breadwinner – has reached staggering dimensions. In 2010, the gap reached USD 20 trillion, or 135% of GDP, up from USD 18 trillion in 2001 at constant 2010 prices. The average family headed by a breadwinner under the age of 55 had an estimated protection gap of USD 378 000.8

The gap represents the difference between the resources that surviving dependents need for income replacement, debt repayments, and other major expenses and the resources actually available from financial assets, Social Security payments, and pro-ceeds from existing life insurance coverage. In 2010, the protection gap for families whose primary breadwinner was between 35 and 44 years old was largest, at about USD 482 000 per family. The group headed by 45 to 54 year-olds had the second larg-est shortfall, at USD 355 000 per family. The youngest families (primary breadwinner under 35) had a slightly lower gap of USD 296 000 per family.

The economic environment has played an instrumental role in the protection gap’s in-crease since 2001. During the past decade, American families experienced a decline in real income, rising debt levels, lower investment returns, and eroded financial assets. In addition to these factors contributing to widening the gap, the portion of households with life insurance declined and the average amount of coverage shrank.

Life insurance can be a relatively low cost solution for many households. Nonetheless, and despite the acute financial vulnerabilities of the uninsured or underinsured, life insur-ance ownership is declining at an alarming rate and currently stands at a 50-year low, according to the Life Insurance Marketing and Research Association (LIMRA). Three out of ten households have no life insurance at all. At the same time, consumer awareness of underinsurance has improved. In 2010, half of US households believed they were not holding enough life insurance coverage, according to LIMRA.

Given the huge need for additional protection but little active demand, life insurers need to better understand consumers’ perceptions and behaviour around purchasing life in-surance. Budget issues are reported as the main impediment to buying more insurance, yet more than 80% of consumers across all demographic groups overestimate the cost of life insurance. Other common reasons consumers cite for not purchasing life insurance are other financial priorities, a need for advice in selecting the right products and cover-age, and the complexity of the purchase process.

To help households close the protection gap, life insurers need to more effectively com-municate the value and affordability of protection products. More action is needed to simplify underwriting processes and develop direct-to-consumer distribution to reach low- and middle-income families. Moreover, insurers need to abandon the industry jargon in their message to potential buyers among the younger generations, and align distribution methods to changing consumer preferences.

The huge and growing protection gap is not only a US issue, but also a global one. According to Swiss Re estimates, the protection gap has reached USD 41 trillion in Asia, close to USD 17 trillion in Europe, and nearly USD 1 trillion in Canada. Covering the gap presents a challenge, but also a sizeable business opportunity for life companies around the world. Mortality protection is the core of life insurance, and with no substitutes avail-able from outside the industry, life insurers are uniquely positioned to help societies close the protection gap by doing more to reach out to people.

8 For details see Swiss Re’s expertise publication ‘The mortality protection gap in the US,’ August 2012.

The US mortality protection gap has reached staggering dimensions in the last decade.

Families with a primary breadwinner aged 35 to 44 have the largest protection gap.

Economic factors played an instrumental role in the gap’s increase over the past decade.

Life insurance is available at a relatively low cost, yet life insurance purchases have declined at an alarming rate.

To help cover the gap, life insurers need to better understand consumer perceptions, behaviour, and needs.

Life insurers can pursue several avenues to help society close the mortality protection gap.

The huge and growing protection gap is a global issue and life insurers are uniquely positioned to help societies close the gap.

21

Profitability: towards a new equilibrium?After having recovered after the crisis, profitability has declined slowly but steadily since the end of 2009. Return on equity (RoE) is now close to 10% on average for a sample of global composite and large life insurers (see Figure 6). The development is similar for companies from all regions, despite some differences in the level of RoE. The reasons for the renewed weakening of profitability are declining interest rates, which have reduced investment margins (the difference between earned and guaranteed interest rate), and weak premium income.9

–10%

–5%

0%

5%

10%

15%

20%

25%

Full sample

14 US companies

2 Chinese companies

6 UK companies

7 European Globals

3 Canadian companies

Q2

201

2

Q1

201

2

Q4

201

1

Q3

201

1

Q2

201

1

Q1

201

1

Q4

201

0

Q3

201

0

Q2

201

0

Q1

201

0

Q4

20

09

Q3

20

09

Q2

20

09

Q1

20

09

Q4

20

08

Q3

20

08

Q2

20

08

Q1

20

08

Q4

20

07

RoE

Sources: Company reports, Bloomberg, Swiss Re Economic Research & Consulting

Note: Based on IFRS/US GAAP data. Missing Q1/Q3 values are interpolated. Companies in the sample include: AFLAC; Allianz; Assurant Inc; Aviva; AXA; China Life; CNP; Delphi Financial; Generali; Genworth Financial; Great-West Lifeco; Hartford; Legal & General; Lincoln National; Manulife; Metlife Group; Phoenix Companies; Ping An; Principal Financial Group; Protective Life; Prudential (UK); Prudential (US); St. James Place; StanCorp Financial Group; Standard Life; Storebrand ASA; Sun Life; Swiss Life; Tochmark; Zurich.

Prospects for 2013 and 2014: a challenging business environmentPivotal for the future of the life insurance industry will be the development of the macro-economic environment, financial markets, and interest rates. In the short term, the out-look is obviously challenging. Rating agencies have mostly remained neutral about the life insurance sector in most countries in the past two years, but are now beginning to take a worrisome stance. Standard & Poor’s has given the German life insurance industry, which has significant interest rate exposure, a negative outlook. Fitch has indicated that most Italian life insurers could be downgraded in the next 12 to 24 months. Moody’s has changed its outlook on the US life industry from stable to negative due to concerns about a gradual weakening of financial flexibility in the challenging macroeconomic environment.

Looking forward, premium income will recover only slowly. For 2013, it is estimated that global premium income will grow by 2.2% (after inflation) and then increase to slightly above 3% in 2014. In advanced markets, 1.5% and 2.5% growth is expected in 2013 and 2014, respectively. In emerging markets, growth is expected to quickly climb to 6% and then rise more slowly to 7%, well below the growth trend observed in the last two decades.

9 The decline in RoE was stronger than the decline in interest rates (ie the RoE above “risk free” also declined).

Profitability will stay below its pre-crisis level.

Figure 6: Return on equity of 32 global composite and life insurance companies, %

The development of the macroeconomic environment will be crucial.

Premium income will recover slowly in 2013.

22

Life re/insurance: Navigating choppy waters

Profitability is not expected to improve soon as there will be strong headwinds from low interest rates and weak sales. When interest rates fall, markets expect life insurers to see lower profits and therefore insurers’ stock prices decline, lowering the price-to-book ratio (see Figure 7). Markets expect life insurers’ profitability to remain constrained in the near future.

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

Average price-to-book ratio

Q2

201

2

Q1

201

2

Q4

201

1

Q3

201

1

Q2

201

1

Q1

201

1

Q4

201

0

Q3

201

0

Q2

201

0

Q1

201

0

Q4

20

09

Q3

20

09

Q2

20

09

Q1

20

09

Q4

20

08

Q3

20

08

Q2

20

08

Q1

20

08

Q4

20

07

Price-to-book ratio

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

UK USGerman

Long-term government bond yield

Sources: Company reports, Bloomberg, Swiss Re Economic Research & Consulting

Note: Based on IFRS/US GAAP data. Missing Q1/Q3 values are interpolated. Companies in the sample include. AFLAC; Allianz; Assurant inc; Aviva; AXA; China Life; CNP; Delphi Financial; Generali, Genworth Financial; Great-West Lifeco; Hartford; Legal & General; Lincoln National; manulife; Metlife Group; Phoenix Companies; Ping An; Principal Financial Group; Protective Life; Prudential (UK); Purdential (US); St. James Place; StanCorp Financial Group; Standard Life; Storebrand ASA; Sun Life; Swiss Life; Torchmark; Zurich.

The introduction of more stringent capital requirements will be another trial for the industry. As a result of the challenging business environment, regulators may require life companies to bolster their reserves to assure that liabilities can be met. In the US, for example, revised actuarial guidelines will require companies to hold more reserves for universal life policies with secondary (death benefit) guarantees as of January 2013. In Canada, upcoming actuarial and regulatory changes will increase reserve requirements for segregated fund and other guarantee products. In Germany, additional reserves in response to the low interest rate environment were introduced in 2011 (see Box: “Recent regulatory developments in Europe”). These higher regulatory capital requirements could also negatively impact the life insurance industry’s capitalization and profitability.

In addition, under Solvency II, whose introduction was postponed to 2014 at the earliest, capital requirements for long-term guarantees and asset risks will be more rigorous com-pared to the Solvency I regime, with material charges for risky assets. Higher expected investment results will need to be balanced against higher capital charges. This balancing is already posing a challenge to life insurance companies since returns on high quality debt securities are often too low to meet expected investment returns, and at the same time capitalization is insufficient to support more asset risk. It needs to go hand in hand with strategic decisions concerning the level and amount of guarantees life insurers sell. The product range, product features, and product mix will probably need to change in the coming years. Life insurers will likely try to move away from traditional guaranteed business, where margins have come under pressure and capital requirements have become increasingly onerous, and shift their product mix towards protection and unit-linked products.

Profitability will also likely stay at the current level; downside risks are looming.

Figure 7: Long-term government bond yields versus the average price-to-book ratio of 32 global composite and life insurance companies

Regulatory changes may negatively impact capitalization and profitability.

Solvency II, even if introduced with further delay, is already impacting life insurers’ strategies.

23

Life insurers have responded to the current challenges by improving investment and asset liability management, reducing operational costs, adjusting policyholder bonus and crediting rates, as well as improving technical profitability through improved under-writing. Some companies have also reassessed their business portfolios and undertaken structural changes.

Stressed companies will seek ways to improve their balance sheets, be it through further de-risking of the asset and liability side of their balance sheets, reinsurance, monetization of embedded future profits, or divestiture of some parts of their business. It cannot be ruled out, depending on how long interest rates stay low, that weak companies will be forced to stop writing new business or merge with stronger competitors. As a result, consolidation of the industry and mergers and acquisitions will likely accelerate.

The life reinsurance market

The top eight life reinsurers increased their net premiums by about 10% in the first half of 2012 (in USD). In part, this strong growth was driven by consolidation. Additionally, block transactions, longevity risk reinsurance, enhanced annuities, and accident & health business supported reinsurance growth and helped reinsurers diversify away from tradi-tional mortality business in the US and the UK.

Premiums from traditional life reinsurance, consisting of mortality and morbidity, are estimated to have decreased by 1.6% globally in 2012. In advanced markets, premiums fell 2.1%, while in emerging markets they increased by almost 5%, on the back of strong protection sales. The decline in advanced markets was driven by an ongoing contraction in the US and UK markets, which currently account for 55% of global cessions (while during the last decade these two markets had a share of 65% of the global free cession market). Reinsurance premiums in the US and UK fell by almost 4.5% in 2012, mainly due to declining cession rates as a result of receding regulatory arbitrage opportunities and regulatory changes.

Country 2010 2011 2012 2013 2014

Advanced markets 1.8% –0.4% –2.1% –1.3% –1.0%Emerging markets 7.0% 16.3% 4.8% 6.3% 6.3%World 2.1% 0.5% –1.6% –0.7% –0.4%

Source: Swiss Re Economic Research & Consulting

Prospects for 2013 and 2014Traditional life reinsurance is expected to further decrease in the next few years. In ad-vanced markets, life reinsurance premiums will decline by between 0.5% and 1% per year (after inflation). In the US and the UK, business opportunities will fade away with changes in regulation. In other advanced markets, where cession rates usually are much lower than in the US and the UK, traditional reinsurance will continue to record low, single-digit growth rates in line with the growth of protection business on the primary side. In emerging markets, life reinsurance is expected to increase by about 6% per year over the next few years. In these emerging markets, reinsurers’ main value proposition will be to support primary insurance in product development, underwriting, and claims management.