Embed Size (px)

Citation preview

World Economic and Financial Surveys

Global Financial Stability ReportMarket Developments and Issues

March 2002

International Monetary FundWashington DC

© 2002 International Monetary Fund

Production: IMF Graphics SectionCover: Massoud Etemadi

Figures: Lai Oy LouieTypesetting: Choon Lee

ISBN 1-58906-105-5ISSN 0258-7440

Price: US$42.00(US$35.00 to full-time faculty members and

students at universities and colleges)

Please send orders to:International Monetary Fund, Publication Services

700 19th Street, N.W., Washington, D.C. 20431, U.S.A.Tel.: (202) 623-7430 Telefax: (202) 623-7201

E-mail: [email protected]:http://www.imf.org

recycled paper

The experience of the past decade with the rapid expansion of financial markets has underlined theimportance of a constant evaluation of the private sector capital flows that are the engine of world eco-nomic growth, but sometimes at the core of crisis developments as well. This experience demonstratesthat the opportunities offered by the international capital markets for enhancing global prosperitymust be balanced by a commitment to prevent debilitating financial crises.

The challenge facing the international community is to deepen our understanding of the potentialsystemic weaknesses and fault lines that have the potential to lead to crises. The International MonetaryFund is working on a comprehensive strategy aimed at safeguarding the stability and integrity of the in-ternational financial system by better understanding how to cope with the dynamics of rapidly evolvingcapital markets.

The founding of the IMF’s International Capital Markets Department in 2001 was an important stepin this effort to deepen our understanding of international capital flows and to strengthen the IMF’ssurveillance of developments in financial markets. The inauguration of the Global Financial StabilityReport, which now will become a quarterly publication of the IMF under the direction of theInternational Capital Markets Department, is aimed at this same purpose. I believe that this report willmake an important contribution to the effort to better understand the trends and issues that influencethe capital markets—thereby contributing to global financial stability and the prosperity of all ourmember countries.

Horst KöhlerManaging Director

iii

FOREWORD

Foreword iii

Preface ix

Chapter I. Overview 1

Chapter II. Recent Developments in International Capital Markets 5

The Recovery Rally 5What Are Markets Anticipating About Recovery? 9Emerging Market Financing 14References 22

Chapter III. Stability Implications of Global Financial Market Conditions 23

Financial Market Implications of Financial Imbalances and a Subdued Recovery 23How Effectively Is the Market for Credit Risk Transfer Vehicles Functioning? 36References 47

Chapter IV. Early Warning System Models: The Next Steps Forward 48

Current EWS Models at the IMF 49EWS: A Way Forward 53Conclusion 62References 62

Chapter V. Alternative Financial Instruments and Access to Capital Markets 65

Alternative Financial Instruments: What Are They and How Do They Work? 66Policy Implications 74Concluding Remarks 76

Boxes

2.1 Anticipating Economic Turnarounds: The Record of the Stock Market 102.2 Argentina and the Asset Class 163.1 Financial Implications of Enron’s Bankruptcy 414.1 The IMF’s Core Early Warning System Models—A Primer 504.2 Alternative Measures of Contagion 605.1 Recent Bond Warrants 715.2 The Structure of Future-Flow Securitizations—Modalities and

the Case of PEMEX 74

v

CONTENTS

Tables

2.1 Total Return Performance of Mature Equity Markets 72.2 U.S. Corporate Bond Total Returns 72.3 Emerging Market Financing 142.4 Performance of Emerging Bond Markets 142.5 Currency of Issue 192.6 Total Dollar Return Performance of Emerging Equity Markets 203.1 U.S. Financial Conditions During the 1990–91 and 2001 Recessions 253.2 Performance of Large European Banks 283.3 Performance of Major Japanese City Banks 295.1 Emerging Market Sovereign Bond and Loan Issues by Type 665.2 Market Conditions and Alternative Financial Instruments 67

Figures

2.1 Global Risk Aversion 52.2 Global Equity Markets 52.3 Net Purchases by Foreigners from U.S. Residents 62.4 U.S. Treasury Yield Differentials 62.5 S&P 500 Earnings Growth Forecasts for 2002 82.6 U.S. Treasury Credit Curves 82.7 U.S. Domestic Bond Issuance 92.8 The U.S. Dollar 92.9 Twelve-Month Forward Price-Earnings Ratio for the S&P 500 12

2.10 Twelve-Month Forward Price-Earnings Ratio of the Group of Three 122.11 Expected Policy Rates: Federal Funds Futures 132.12 Expected Changes in Forward Rates in the Group of Seven 132.13 Emerging Market Spreads 152.14 Average Cross-Correlation of Emerging Debt Markets 152.15 Emerging Market Spread Correlations with Argentina 182.16 Monthly Bond Issuance 182.17 Loan Issuance 202.18 Cumulative Gross Annual Issuance of Hard Currency Loans 202.19 Loan-Weighted Interest Margin 212.20 Net Foreign Purchases and Monthly Returns on Emerging Equity Markets 212.21 Capital Flows to Emerging Economies 223.1 United States: Financial Conditions, 1987–2001 243.2 Probability Density Functions for Group of Three Exchange Rates Implied

by Option Prices 263.3 Household and Corporate Sector Balance Sheets in the Euro Area and Japan 273.4 Japan Premium 303.5 United States: Household and Corporate Sector Balance Sheets and

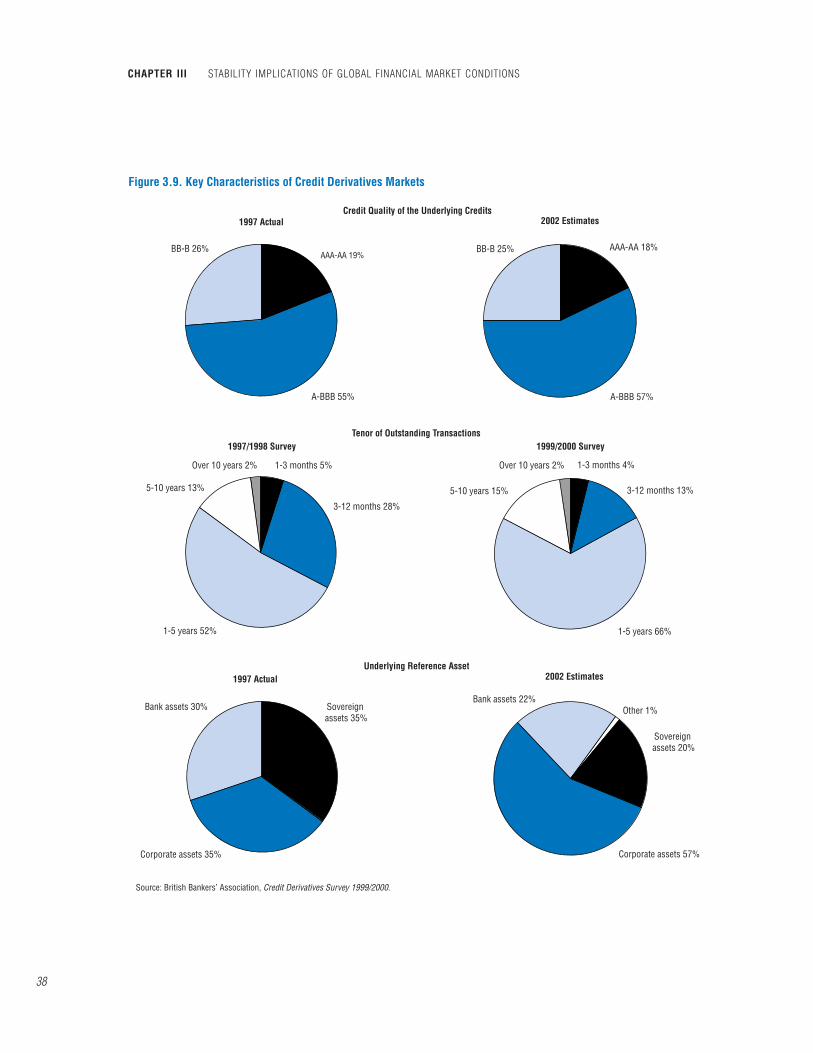

Debt Services Ratios 313.6 Performance of Bank Stock Indices 323.7 Implied Earnings Growth Rates 333.8 Global Credit Derivatives Market Size and Structure 373.9 Key Characteristics of Credit Derivatives Markets 38

CONTENTS

vi

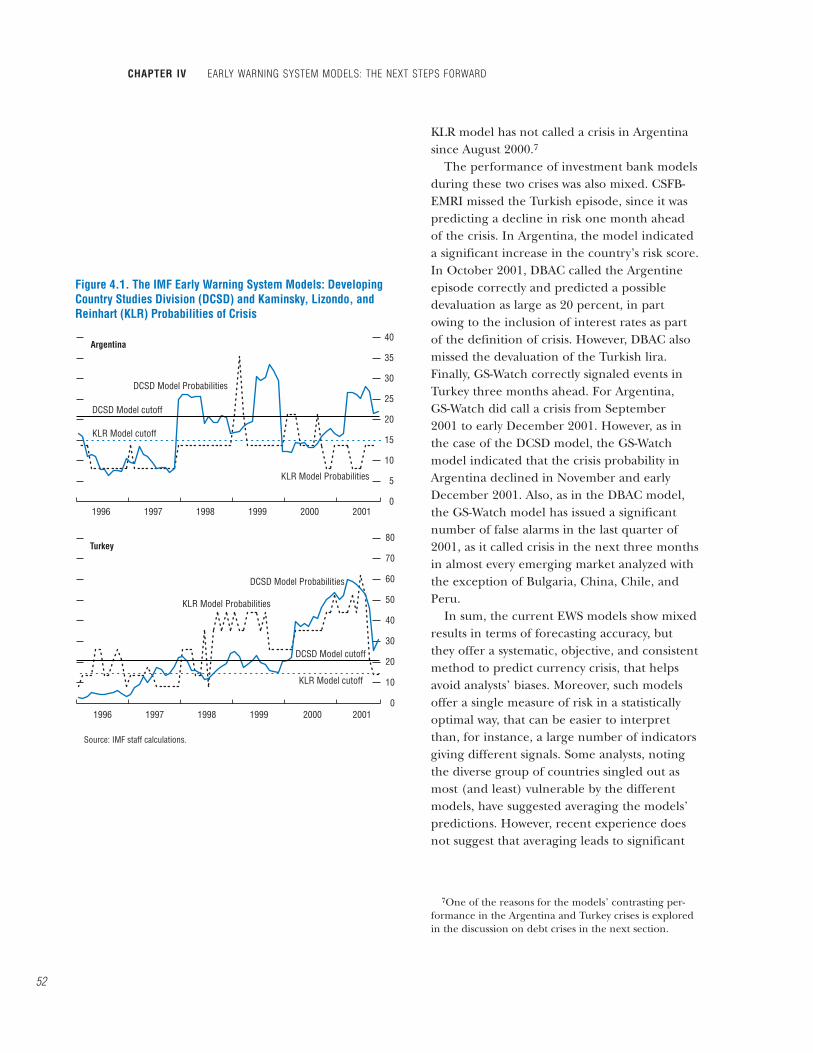

3.10 Spread Between Credit Derivatives Premium and Underlying Bond Spread 454.1 The IMF Early Warning System Models: Developing Country Studies Division

(DCSD) and Kaminsky, Lizondo, and Reinhart (KLR) Probabilities of Crisis 524.2 Forward Exchange Rates for Argentine Peso 544.3 Spot Price and Implied Probability Density Function for the Brazilian Real 554.4 Argentina and Turkey: External Liquidity and Debt Service Ratios 564.5 Slope of Default Swap Curve 574.6 Korea: Financial Institutions Index (1991–2001) 58

CONTENTS

vii

The following symbols have been used throughout this volume:

. . . to indicate that data are not available;

— to indicate that the figure is zero or less than half the final digit shown, or thatthe item does not exist;

– between years or months (for example, 1997–99 or January–June) to indicate theyears or months covered, including the beginning and ending years or months;

/ between years (for example, 1998/99) to indicate a fiscal or financial year.

“Billion” means a thousand million; “trillion” means a thousand billion.

“Basis points” refer to hundredths of 1 percentage point (for example, 25 basis pointsare equivalent to !/4 of 1 percentage point).

“n.a.” means not applicable.

Minor discrepancies between constituent figures and totals are due to rounding.

As used in this volume the term “country” does not in all cases refer to a territorial en-tity that is a state as understood by international law and practice. As used here, theterm also covers some territorial entities that are not states but for which statisticaldata are maintained on a separate and independent basis.

This is the first Global Financial Stability Report, a quarterly publication produced by the IMF’sInternational Capital Markets Department. It replaces two IMF publications: the annual InternationalCapital Markets Report (published since 1980) and the quarterly Emerging Market Financing (publishedsince 2000). The report was created to provide a more frequent assessment of global financial marketsand to address emerging market financing in a global context. The report focuses on current condi-tions in global financial markets, highlighting issues of financial imbalances, and of a structural nature,that could pose a risk to financial market stability and sustained market access by emerging market bor-rowers. As a quarterly, it will focus on relevant contemporary issues and not try to be a comprehensivesurvey of all potential risks, and on analyzing the financial ramifications of economic imbalances high-lighted by the IMF’s World Economic Outlook. It will regularly contain, as a special feature, articles onstructural or systemic issues relevant to international financial stability. Thus, the report is part of abroad effort by the IMF to strengthen bilateral and multilateral surveillance of international financialmarkets, with a view to promoting financial stability as a global public good. Other components of thisbroad effort include integrating financial market assessment with the World Economic Outlook, the WorldEconomic and Market Developments review, work on private sector involvement in the resolution of fi-nancial crises, work on standards and codes, the Financial Sector Assessment Program (FSAP), andSpecial Data Dissemination Standards (SDDS).

The Global Financial Stability Report was prepared in the International Capital Markets Department,under the direction of the Counsellor and Director, Gerd Häusler. The Global Financial Stability Reportproject is directed by an Editorial Committee comprised of Hung Q. Tran (Chairman), BankimChadha, Donald J. Mathieson, and Garry J. Schinasi, and benefits from comments and suggestions fromWilliam E. Alexander, Charles R. Blitzer, Matthew Fisher, Peter Dattels, Ronald Johannes, and L. EffiePsalida. Other contributors to the report from the International Capital Markets Department areTorbjorn Becker, Peter Breuer, Jorge Chan Lau, Anna Ilyina, Charles Kramer, Subir Lall, GabrielleLipworth, Jens Nystedt, Jorge Roldos, Srikant Seshadri, R. Todd Smith, Krishna Srinivasan, Amadou Sy,and James Yao. Martin Edmonds, Patricia Gillett, Silvia Iorgova, Anne Jansen, Oksana Khadarina, YoonSook Kim, Advin Pagtakhan, and Peter Tran provided research assistance. Maame Baiden, CarolineBagworth, Lucia Buono, Vera Jasenovec, Sheila Kinsella, Ramanjeet Singh, Adriana Vohden, and JoanWise provided expert word processing assistance. Jeff Hayden of the External Relations Department ed-ited the manuscript and coordinated production of the publication.

This particular quarterly issue of the report draws, in part, on a series of informal discussions withcommercial and investment banks, securities firms, asset management companies, insurance compa-nies, pension funds, stock and futures exchanges, and credit rating agencies in London, New York, andTokyo. The report contains data available up to February 8, 2002.

The study has benefited from comments and suggestions from staff in other IMF departments, aswell as from Executive Directors following their discussions of the Global Financial Stability Report onFebruary 27, 2002. However, the analysis and policy considerations are those of the contributing staffand should not be attributed to the Executive Directors, their national authorities, or the IMF.

ix

PREFACE

The year 2001 has yet again demon-strated how resilient the internationalfinancial system was in the face of anumber of serious challenges. In

chronological order, the past year saw the con-tinuing deflation of the telecom, media, andtechnology (TMT) bubble across global markets,the onset of a recession in the United Statesamid a synchronized global slowdown, a finan-cial crisis in Turkey, the terrorist attacks onSeptember 11, the record number of bankrupt-cies, and the default by Argentina after a longand drawn-out crisis. Throughout these events,several of which represented serious problemsrequiring prompt attention by the appropriateauthorities, the international financial systemhas shown remarkable resilience. This capacityto absorb shocks has been bolstered by the ro-bustness of the infrastructure of the financial sys-tem and the key players in it; the vigilance andready action of the financial and monetary au-thorities to ensure the smooth functioning ofthe system, including through the timely provi-sion of liquidity support; and the increasinglydiscriminating investment behavior of marketparticipants. Going forward, this resiliencewould again be tested if a global economic re-covery is subdued. However, the starting condi-tions this year would be weaker than those at thebeginning of 2001.

As analyzed in Chapter II, financial marketsended the year on a positive note. Equity mar-kets recovered and rallied noticeably from theirlows of late September. In bond markets, yieldspreads of corporates and high-yielding bonds,particularly emerging market bonds, narrowedagainst U.S. Treasuries. At the same time, theU.S. Treasury yield curve steepened, and theU.S. dollar has strengthened. Financial marketsthus anticipate, and have priced in, a recovery ineconomic activity and corporate earnings during2002. In the emerging market bond markets,

signs of financial contagion moderatedmarkedly. Fallout from the Argentina crisis anddefault has been quite limited, in contrast tomost previous experiences. The reasons for suchnoncontagion include more discriminating in-vestment behavior by market participants, thelack of any surprise element as the crisis slowlyproceeded to what the markets anticipatedwould be an inevitable default event, the gener-ally better economic policies, including the useof more flexible exchange rate regimes, adoptedby many emerging market countries, as well asvarious technical factors such as limited lever-aged positions and the significant reduction inArgentina’s weight in emerging market bond in-dexes, such as the EMBI+. New issuance byemerging market sovereign borrowers has re-vived since November and this rebound has con-tinued in the new year. For those emerging mar-ket countries, which have so far avoidedfinancial contagion from Argentina, it is impor-tant to reinforce the positive sovereign andcredit risk assessment currently held by investors.This can be most effectively achieved by bothstrengthening sustainable economic policieswhere necessary and consolidating the structuralreform achieved in recent years.

At present, the consensus view that the globaleconomy will recover during the course of 2002is being buttressed by recent economic statistics.In spite of this widespread expectation, as well asthe demonstrated resilience of the internationalfinancial system, there is no reason for compla-cency. In the view of many market participants,the risk of a subdued global economic recovery,subjecting the world to a second straight year ofslow growth, as well as opening a gap between fi-nancial market expectations and economic per-formance, is not insignificant. If that were to ma-terialize, it would exacerbate the financialimbalances and some of the underlying weak-ness in the financial sector. From a historical

1

CHAPTER I OVERVIEW

and cyclical perspective, it is important in themonths ahead to see whether the recovery ineconomic activity and corporate earnings willvalidate market expectations, especially for equi-ties. If not, the likely adjustment in asset pricesand deterioration in credit quality could erodethe still fragile business and consumer confi-dence. The implications of overleveraging andcredit quality deterioration, which would be ex-acerbated by a subdued recovery, for financialmarket stability are explored in Chapter III. First,downward asset price adjustment and further de-terioration in credit quality could weaken bal-ance sheets of corporates, households, and fi-nancial institutions in the major industrialcountries, all of which have increased their ex-posure to traded financial assets in recent years.Second, a subdued recovery would put furtherpressure on banks’ profitability. These develop-ments could be more worrisome in light of thefact that present levels of indebtedness in themajor industrial countries, both in the corporateand the household sectors, are high from a cycli-cal perspective. Their debt servicing burden isalso high relative to current income, despite thecyclically low interest rates. Consequently, ad-verse financial market developments could im-pair the incipient recovery and make a sustain-able recovery more difficult to achieve. Theappropriate policy response by the internationalcommunity to help sustain demand has been de-scribed in the IMF’s World Economic Outlook,December 2001. However, to the extent that theeventual recovery is accompanied by a furtherrise in the level of indebtedness, thereby increas-ing the sensitivity of these economies and finan-cial systems to financial asset price fluctuations,the situation warrants close monitoring in theperiod ahead.

Of some concern is the health of individualfinancial institutions in the major industrialcountries that have been weakened by the eventsof 2001. The resilience of the international fi-nancial system mentioned above has been duelargely to the strength of banking systems, and fi-nancial systems in general, in key countries, par-ticularly the United States. The banks in these

countries have built up their capital strengththrough improved profitability during the longexpansion of the 1990s, ongoing consolidation,and improvements in operational technologyand risk management practice. However,progress was not uniform or even among banksin the industrial countries; those lagging behindin the pace of consolidation and restructuringhave continued to cope with overcapacity, stiffcompetitive pressure, and sometimes poor prof-itability in their home markets even before thesynchronized growth slowdown. For some otherinstitutions, diversifying into overseas markets,including emerging markets, and pursuing newactivities, including lending to the telecom in-dustry and engaging in credit derivative busi-ness, have exposed them to the potential of ad-ditional losses. In particular, in Japan, the weightof nonperforming loans amid a prolonged pe-riod of deflation has seriously weakened manybanking institutions, leading to their downgrad-ing by the major rating agencies. Adverse finan-cial market developments would further squeezethe weak institutions between sharply reducedearnings expectations and a still rigid cost base,now burdened with the need for further loanloss provisioning. In the period ahead, such con-ditions would probably speed up the financialsector consolidation process, both in market andcross border.

Credit quality deterioration also provides animportant test of the performance and stabilityof the market for credit risk transfers that hasgrown rapidly in recent years. Overall, the prolif-eration of credit risk transfer instruments, in-cluding credit risk swaps, credit derivatives, andcollateralized debt obligations (CDOs), is a posi-tive step. It has enabled banks to remove creditexposures from their balance sheets and to dis-tribute them more widely among market partici-pants. In 2001, the market seemed to be able tocope with a series of credit events, with paymentsby and large being made by credit risk protec-tion sellers to protection buyers; even though insome cases only after arbitration (these caseshave led to improvements in the InternationalSwap and Derivatives Association documenta-

CHAPTER I OVERVIEW

2

tion, widely used in the market). Further deteri-oration in credit quality, which as a lagging indi-cator could persist for some time even if theglobal economy recovers, would continue to testthe market.

Independent of economic performance, sev-eral areas of risk are surfacing. First, to the ex-tent that regulatory arbitrage drives the growth ofthe market, banks may be encouraged to origi-nate more credit business than they would havedone otherwise, and then to transfer the creditrisks to non- or less-regulated entities, particu-larly with regard to capital adequacy require-ments, such as insurance companies and, to alesser degree, hedge funds. Banks, having signifi-cantly substituted traditional credit risks forcounterparty risks, now depend on their coun-terparties to perform when a credit event occursto keep their exposure within limits ex post. This,however, has been shown to be uncertain inmany cases. Second, the group of important non-traditional players has expanded to include indus-trial companies with an active financial arm. Dueto the lighter (or lack of) financial regulatoryregime, their disclosure has been less adequatethan from regulated financial institutions, lead-ing to a lack of information and transparencyabout the overall development of the marketand the pattern of risk distribution and concen-tration in the financial system. This makes it dif-ficult for market participants to gauge accuratelythe creditworthiness of companies and institu-tions in a timely fashion. Third, the complexity ofinstruments and transactions has grown overtime, and when a credit event occurs, it is notclear that all contracts can be expected to be au-tomatically executed in a way that protectionbuyers expect and with a high degree of cer-tainty. This is a risk even if one allows for thefact that new financial instruments will have“teething” problems initially as to solid legal doc-umentation. The collapse of Enron, and subse-quent events, illustrates the three areas of riskdescribed.

As a consequence, there seems to be the needto review and possibly improve regulatoryregimes in the industrial countries to keep pace

with the ongoing process of modernization andglobalization of finance. Specifically, there is theissue of regulatory arbitrage that might distortthe origination, distribution, and pricing ofcredit risks; and the need to identify and addressthe gaps in regulation that have allowed signifi-cant players in the financial markets, be theybanks or nonbanks, not to operate under a com-parable and consistent regulatory framework(“same business, same risk, same rule”). The na-tional authorities are already looking to developand enforce appropriate disclosure require-ments to enhance transparency in these com-plex markets. In addition, accounting rules andstandards are also in the process of being up-dated to address the increasing complexity of fi-nancial transactions. Of immediate interest isthe enhanced transparency of off-balance-sheetrisk management structures such as special pur-pose vehicles (SPVs)—particularly the extent towhich such vehicles genuinely remove risks fromthe balance sheet of the originating entity ratherthan merely disguise them. Such enhancedtransparency could strongly bolster the effective-ness of market discipline as the first line of de-fense against financial instability by enablingmarket participants to more clearly identify fi-nancial imbalances at an early stage. The result-ing repricing of credit to those institutions couldwork to limit the buildup of such vulnerabilitiesbefore they reach an unsustainable level and po-tentially pose risks to financial stability.

On the heels of slow global growth and ofcrises in Turkey and Argentina, the need to fur-ther develop and refine early warning systems(EWS) as a tool for crisis prevention has againbecome relevant to the international financialcommunity. Chapter IV analyzes the performanceof existing early warning system models that fo-cus mostly on foreign exchange markets. Theway forward includes building models for bank-ing and debt crises in addition to enhancing theexisting ones on foreign exchange crises, exam-ining the linkages among different types ofcrises and across countries (contagion), andmaking more efficient use of information em-bedded in financial asset prices. Chapter IV also

OVERVIEW

3

lays out a research program in this area for theIMF in the period ahead.

Chapter V addresses the role of alternativedebt instruments—other than new “plainvanilla” bonds and regular loan issues—in en-abling emerging market sovereigns to maintainaccess to global capital markets and better man-age their debt through risk diversification. Theneed for such instruments may increase at timesof financial stress, when investor appetite foremerging market debt could diminish and bor-rowing costs increase. In such circumstances,emerging market sovereigns often have adjusted

their debt management strategies, and havemade use of debt instruments embodying inno-vative features, including debt augmentations,time varying and state contingent instruments,structured notes, and collateralized borrowing.Chapter V evaluates these instruments and pres-ents a comparative analysis of the benefits andcosts of their use, including the risks of lockinginto high debt-service costs for prolongedperiod of time and creating inflexible debtstructures, as well as the implications of the dif-ficulty that markets often have in pricing theseinstruments.

CHAPTER I OVERVIEW

4

Changing perceptions of the economicslowdown and the prospects for recov-ery dominated global market develop-ments during the fourth quarter of last

year, and continue to do so in 2002. Marketshad reacted strongly to the events of September11, before staging a sharp rally from the begin-ning of the quarter as global risk aversion sub-sided (see Figure 2.1).1 The heightened marketuncertainty associated with the events surround-ing September 11 initially translated into highlevels of risk aversion at the beginning of thefourth quarter. Measures of risk aversionsteadily dissipated during October and Novem-ber, with a consensus emerging that, in hind-sight, financial markets overreacted to the po-tential impacts of the September 11 events. Thesubsequent rally, in conjunction with a strongrevision of views on economic recovery and itsstrength and scope, was also influenced by sev-eral technical factors and ample liquidity on thepart of investors.

The Recovery RallyDuring October and November, financial

markets rose markedly to price in an imminentrecovery in global activity, led by the UnitedStates, though opinion remained divided on thetiming and speed of the recovery (see Figure2.2). These expectations of economic recoverycombined with a decline in the “political” riskpremium, reflecting progress in the operationin Afghanistan, and led to a decline in measuresof global risk aversion to well below pre-

5

CHAPTER IIRECENT DEVELOPMENTS IN INTERNATIONAL CAPITAL MARKETS

Figure 2.1. Global Risk Aversion

Source: JP Morgan Chase.

0

10

20

30

40

50

60

70

80

90

100

022001200019991998

One standarddeviation

Mean

September 11

Figure 2.2. Global Equity Markets(January 2001 = 100)

Source: Bloomberg L.P.

50

60

70

80

90

100

110

120

Jan.2002

Oct.JulyApr.Jan.

September 11Recovery ExpectationsSlowdown Concerns

Dow

Emerging Market Free

All Country WorldIndex Free

Interest raterelief

Interest raterelief

Nasdaq

2001

1JP Morgan’s Liquidity and Credit Premia Index(LCPI). This index attempts to measure risk aversionmore broadly, and, therefore, captures not only risk ap-petite but also the liquidity premia demanded in U.S. fi-nancial markets. See the IMF’s Emerging Market Financing(November 14, 2001) for a detailed discussion.

September 11 levels and into markedly benignterritory. Oil prices remained low, supporting abenign outlook for inflation. Equity markets ral-lied first, followed by a sharp sell-off in U.S.bond markets, while spreads in high-yield(sub-investment grade) and emerging marketbonds (except Argentina) narrowed. Foreigninvestors in the United States reduced netpurchases of both stocks and bonds in Septem-ber as global risk aversion rose (see Figure 2.3).By October, however, they began participatingin both the U.S. equity and bond marketrallies, and by November, as risk aversion de-clined further, they reduced purchases ofbonds while adding to their purchases of U.S.stocks.

With the sharp movement in asset prices toprice in an imminent economic recovery raisingquestions about whether financial markets werebeing too optimistic, the dynamics of the turn-around in global market sentiment are of inter-est. While changes in market perceptions regard-ing the U.S. growth outlook and the budgetdeficit were the fundamental factors causing thesteepening of the U.S. yield curve, several techni-cal factors had triggered, and later reinforced,this trend (see Figure 2.4). One technical factorwas the rebalancing by asset allocation funds(mostly insurance company related) from theirgovernment bond portfolios, which had impres-sively overperformed in the aftermath ofSeptember 11, toward their equity portfolio. Thisrebalancing aimed at restoring funds’ preferredweightings between equity and fixed income thathad become skewed by up to 15 percentagepoints. Simultaneously, many investors over-weighted their portfolio holdings of U.S.Treasuries in the aftermath of September 11, ex-pecting an aggressive monetary policy responseby the U.S. Federal Reserve. These long positionsinitially proved highly profitable. However, fol-lowing the turnaround in the U.S. stock market,they became increasingly unattractive, and by thesecond week of November the liquidation ofthese long positions contributed to a surge in theyield on U.S. 10-year benchmark bonds (36 basispoints on November 15 alone). Furthermore,

CHAPTER II RECENT DEVELOPMENTS IN INTERNATIONAL CAPITAL MARKETS

6

Figure 2.3. Net Purchases by Foreigners from U.S. Residents(In billions of U.S. dollars; data through Novermber 2001)

Source: U.S. Department of the Treasury.

–20

–10

0

10

20

30

40

50

Oct.JulyApr.Jan.Oct.JulyApr.Jan.

Corporate bonds

Government bonds Stocks

2000 2001

Figure 2.4. U.S. Treasury Yield Differentials(In basis points)

–100

–50

0

50

100

150

200

250

300

350

Jan.02

Oct.JulyApr.Jan.

10-year Treasury minus 3-month Treasury

10-year Treasury minus 2-year Treasury

2001

Source: Bloomberg L.P.

portfolios including mortgage backed securities(MBS) faced a significant increase in the dura-tion of their holdings as a result of the decline ininterest rates (by as much as 40 percent). In or-der to bring the duration of their portfolios back,MBS holders sold longer maturity U.S. Treasurybonds, such as the benchmark 10-year, therebycontributing to the spike in yields.

During the fourth quarter, equity market per-formance also reflected perceptions of recovery.Morgan Stanley’s All Country World Index—Free (ACWIF) gained 9 percent, the S&P 500rose 10 percent, while the Nasdaq posted arecord quarterly return of 30 percent. An indi-cation of investor expectations driving the rallyis provided by the fact that cyclical sectors(mainly consumer durables, commercial serv-ices, and technology) significantly outper-formed defensive sectors during the rally, indi-cating investors were positioning for animminent recovery (see Table 2.1). A similarpattern was also in evidence in European mar-kets, whereas there is little evidence of Japaneseequities pricing in a strong economic recovery.The impact of the crisis in Argentina, however,sparked a sell-off in Spanish stocks, especiallybanks and telecom companies. The strong re-bound in emerging equity markets (see Figure 2.2),viewed as a “high beta” (that is, more than pro-

portional comovement) play on the state ofthe global economy, exactly on cue with globalequity markets, also suggests investor position-ing on expectations of a global recovery.Technology was by far the best performingsector, with returns for the sector exceeding theaverage for other sectors by more than twostandard deviations. This equity market rallyoccurred despite continuing downward revisionsto near term corporate earnings forecasts (seeFigure 2.5). The rally lost some steam in earlyDecember and January, coinciding with Enron’sbankruptcy filing, which raised, among otherthings, doubts about the reliability of corporateincome statements.

The increasing appetite for risk in the fourthquarter was clearly apparent in credit markets,where, for example, in the United States thepronounced flight to quality of the third quarterin the aftermath of September 11 was more thanreversed (see Table 2.2). In sharp contrast to thethird quarter, where returns were positively re-lated to credit ratings, returns in the fourthquarter were inversely related to credit ratings.European investment grade corporates per-formed similarly, with evidence of flight to qual-ity in the third quarter (while AAA corporatesposted a 3.3 percent return, BBB corporates hada –0.7 percent return) followed by a partial re-versal in the fourth quarter.

The post-September 11 steepening of the“credit quality curve” (average spreads measuredagainst average credit quality of issuers) was fullyreversed by early December (see Figure 2.6). By

THE RECOVERY RALLY

7

Table 2.1. Total Return Performance of MatureEquity Markets(In percent)

Jul. 1– Sep.10– Sep. 21– Sep.10–Sep. 10 Sep. 21 Dec. 31 Dec. 31

MSCI US$ index –10.7 –11.6 18.2 4.5Cyclical sectors –17.2 –16.1 27.5 7.0Defensive sectors –2.5 –6.7 8.6 1.3Banks and financials –11.8 –12.5 21.8 6.6

MSCI EU$ index –10.0 –13.9 23.8 6.7Cyclical sectors –11.3 –17.4 31.4 8.6Defensive sectors –9.4 –7.7 15.4 6.5Banks and financials –8.5 –20.7 29.8 2.9

MSCI Japan$ index –14.4 –4.1 –6.2 –10.1Cyclical sectors –17.9 –8.1 3.1 –5.3Defensive sectors –9.6 4.9 –12.7 –8.4Banks and financials –6.3 –1.9 –29.6 –30.9

Sources: Morgan Stanley Capital International; and IMF staffestimates.

Table 2.2. U.S. Corporate Bond Total Returns(In percent)

Sept. 10– Third Fourth Year-Sept. 26 Quarter Quarter 2001 to-Date1

AAA 0.9 4.8 0.5 9.4 1.2AA 0.8 4.6 0.9 10.7 1.3A 0.5 4.4 0.7 11.0 0.9BBB –0.1 3.7 0.8 10.5 0.4BB –4.9 –1.9 4.4 11.1 –0.3B –6.2 –4.9 6.5 2.6 0.9C –9.7 –8.3 7.0 4.3 –0.2

Source: Merrill Lynch.1February 8.

early January, reflecting expectations of eco-nomic recovery and a further move down thecredit spectrum, the credit quality curve had flat-tened relative to pre-September 11 levels.However, high-yield spreads remain high by his-torical standards, consistent with market expec-tations (reinforced by the bankruptcies ofEnron, Kmart, and Global Crossing) of contin-ued high rates of corporate defaults. For theyear as a whole, investment grade bonds postedtheir best year since 1995, while high-yield bondsturned in a modestly positive performance aftera dismal 2000.

In primary markets, U.S. high (investment)grade corporate bond issuance reached a recordweekly level of $27 billion by the end of October,reflecting pent up demand to issue as a result ofdisruptions in the aftermath of September 11,and an increased demand to issue debt in thelow interest rate environment (see Figure 2.7).With the rally in credit markets losing steam bylate November, and many issuers having pre-financed their needs, high-grade issuance fellwell below average levels by the end of the year,picking up again in early January. High-yield is-suance, in contrast, was slow to recover, notreaching weekly average levels over the previousyear until December and was slow to pick upagain in January.

The fourth quarter saw a pickup in syndicatedlending in the mature markets. Lenders, how-ever, remained discriminating regarding creditquality, with U.S. bank lending standardscontinuing to tighten. Refinancings continuedto dominate deal flows as borrowers sought totake advantage of lower interest rates, and theinterest rate cycle was perceived as reaching aturning point (see next subsection). Reflectingthe impact of the global slowdown and thesharp fall off in mergers and acquisitions andtelecom financing, however, 2001 volumes weresignificantly lower than in 2000, with Euroloanvolumes down roughly 30 percent. This declinein activity, and reliance on refinancings, is re-portedly placing pressure on banks, with (standalone) investment banks suffering dispropor-tionately, as commercial banks increasingly tie

CHAPTER II RECENT DEVELOPMENTS IN INTERNATIONAL CAPITAL MARKETS

8

Figure 2.5. S&P 500 Earnings Growth Forecasts for 2002(Percent change, year-on-year)

Source: Thomson Financial First Call.

Q1

Q2

Q3

–10

–5

0

5

10

15

20

25

30

35

Feb. 2001Oct. 2001Sept. 2001

Q1

Q2

Q3

Q1

Q2

Figure 2.6. U.S. Treasury Credit Curves(Spreads in basis points)

Source: Merrill Lynch.

0

200

400

600

800

1000

BBBBBBAAAAAA

October 1

September 1

Two-year average

February 8

the less lucrative extension of their balancesheets to the provision of more profitablefee-driven business. The move to a “one-stopshop” reflects not only the strengthened posi-tion of commercial banks with a large balancesheet in the context of the global slowdown, butalso the advances made by some of these banksin developing their mergers and acquisitionsand investment banking businesses in recentyears.

In foreign exchange markets, consistent with theview that global economic recovery was not onlyimminent but would be led by the UnitedStates, the U.S. dollar strengthened (see Figure2.8). At the same time, data confirmed furtherweakening in Japan, and the yen suffered asharp sell off to levels not seen since 1998. Theeuro, while weakening against the dollar,strengthened sharply against the yen duringthe quarter.

What Are Markets AnticipatingAbout Recovery?

The speed and magnitude of the turnaroundin global markets during the fourth quarter of2001 on expectations of a turnaround in theglobal economy, led by the United States, wereremarkable. Such a turnaround raised questionsabout whether the equity market rally, and inparticular the performance of telecom, media,and technology (TMT) stocks, was justified byfundamentals, and the extent to which it repre-sented a liquidity-driven “bear market rally” andeven a “new tech bubble.”

On the one hand, many view the run up inequity markets as appropriately pricing in therecovery, brought forward by the decisive mone-tary and fiscal policy responses, and view therecent positive economic data as ratifying theseexpectations. Box 2.1 examines the anticipationof economic recovery by equity markets in pastrecessions. Many argue that precisely becausethe cyclical downturn partly reflects the burst-ing of the tech bubble, recovery will be fastsince the half-life of technology investmentspending is estimated at only 18 months com-

WHAT ARE MARKETS ANTICIPATING ABOUT RECOVERY?

9

Figure 2.7. U.S. Domestic Bond Issuance(In billions of U.S. dollars)

Source: Bloomberg L.P.

September 11

Investment grade bond issuance

High-yield bond issuance

Averages

2001

0

5

10

15

20

25

30

Jan.02

Nov.Sept.JulyMayMar.Jan.

Figure 2.8. The U.S. Dollar

Source: Bloomberg L.P.

Yen/US$

95

100

105

110

115

120

Jan.02

Nov.Sept.JulyMayMar.Jan.

Euro/US$

Trade weighted

2001

CHAPTER II RECENT DEVELOPMENTS IN INTERNATIONAL CAPITAL MARKETS

10

How well have stock markets done in antici-pating recovery from past recessions?

The first four Figures document the historicalbehavior of stock markets during the six reces-sions since 1970, where the National Bureau ofEconomic Research’s (NBER) definitions of re-cessions are denoted by the shaded areas. Since1970, U.S. recessions have lasted between 7 to17 months and averaged about 12 months.

The data suggest that in the previous five re-cessions, equity markets have in fact had a rela-tively “good” record in anticipating the end of reces-sions. That is to say, historically, at least in theUnited States, equity markets began rising in an-ticipation of recovery, that is, before the end of

recessions, and, critically, these expectations ofrecovery were validated, that is, the recessionsended soon after.

By how much did the recoveries in stockmarkets precede the economic recoveries?Troughs in equity markets preceded the endof recessions as defined by the NBER on aver-age by 4.4 months, and turning points inindustrial production by a similar 4.2 months.The beginning of the equity market recoveryrallies generally occurred ahead of turn-arounds in corporate earnings, which occurredon average slightly more than a quarter later(based on quarterly data; see the Table). Ifthe recession of 1981–82, where earnings

Box 2.1. Anticipating Economic Turnarounds: The Record of the Stock Market

S&P 500 and Changes in Industrial Production1

Source: Primark Datastream. 1Shaded areas mark U.S. recessions.

Industrial production (right scale; year-on-year in percent)

60

80

100

120

140

160

180

848280787674721970–20

–15

–10

–5

0

5

10

15

20

S&P 500(left scale)

S&P 500 and Changes in Corporate Earnings1

Sources: I/B/E/S; Primark Datastream. 1Shaded areas mark U.S. recessions.

Corporate earnings (right scale; year-on-year in percent)

S&P 500(left scale)

848280787674721970–30

–20

–10

0

10

20

30

40

60

80

100

120

140

160

180

Comparing Troughs: Stock Market Troughs Versus Industrial Production and Corporate Earnings’ Troughs

Lags in Months_____________________________________U.S. Stock Industrial Lags in Quarters______________

Recession Dates1 Market Trough2 End of recession production trough Earnings trough

Dec. 1969 to Nov. 1970 June 1970 5 4 2Nov. 1973 to Mar. 1975 October 1974 5 7 1Jan. 1980 to Jul. 1980 April 1980 3 3 2Jul. 1981 to Nov. 1982 July 1982 4 2 –1Jul. 1990 to Mar. 1991 November 1990 5 5 2Mar. 2001 to present October 2001 . . . . . . . . .

Average Past Recessions 4.4 4.2 1.2

Sources: IMF staff estimates; and Thomson Financial First Call.1National Bureau of Economic Research.2S&P 500.

WHAT ARE MARKETS ANTICIPATING ABOUT RECOVERY?

11

actually began to rebound before the stockmarket trough, is excluded, the average was1.75 quarters. These averages can be viewedas the average time it took for the recoveriesin equity markets to be validated by actualdevelopments in the real economy. In reality,of course, these should be viewed as minimumtimes for the equity market rebound to bevalidated by data since it is only after theavailability of (several) post turning pointdata that the trough would clearly becomeapparent.

Turning to the current recession:• The equity market has already had one false

start in April–May 2001, in predicting an eco-nomic recovery.

• For the present rebound in equity markets tobe validated by developments in the real econ-omy in accordance with past historical experi-ence, industrial production would need to havereached a turning point (trough in year-on-yeargrowth) between November of last year andFebruary of this year.

• Similarly, corporate earnings would have to turnaround in the first quarter of this year. Histori-cally, corporate earnings (see the fifth Figure)have troughed four to seven quarters (meas-ured along the x-axis) following their pre-re-

cession peak (an index value of 100). Currentmarket expectations on earnings are for stableearnings in the first quarter of 2002 (sevenquarters into the downturn), and a recoveryduring the second quarter, which is in linewith earnings experience from past reces-sions. Based on historical trends, industrialproduction and earnings need to turn aroundthis quarter. If this turnaround does not mate-rialize, there is a risk of a market correction.

S&P 500 and Changes in Industrial Production1

Source: Primark Datastream. 1Shaded areas mark U.S. recessions.

S&P 500

Industrial production (right scale; year-on-year in percent)

–10

–8

–6

–4

–2

0

2

4

6

8

10

250

450

650

850

1050

1250

1450

2000989694921990 2000989694921990

S&P 500 and Changes in Corporate Earnings1

Sources: I/B/E/S; Primark Datastream. 1Shaded areas mark U.S. recessions.

S&P 500 (left scale)

Corporate earnings (right scale; year-on-year

in percent)

–30

–20

–10

0

10

20

30

250

450

650

850

1050

1250

1450

U.S. Corporate Earnings (Actual) Index

Source: I/B/E/S.

ConsensusForecasts

60

80

100

120

Peak Q2

Peak Q4 1981

Peak Q1 1980

Peak Q2 1974

121110987654321

Peak Q2 2000

110

90

70

Quarters

pared to several years for traditional physicalcapital. The optimists argue that the run up inTMT sector equity prices is justified by changesin fundamentals, with signs that excess capac-ity in the sector is being worked off, and the“winners being picked,” thereby creating thenecessary conditions for fast profit growth inthe sector. Others view the September 11 eventsas having created a (V-shaped) kink in anotherwise unaltered U-shaped recovery and,therefore, not representative of broader recov-ery. These market participants see the equitymarket rebound as pricing in a quick reboundin earnings growth that is faster than wasevident in previous business cycles. The pes-simists argue that the overcapacity built upduring the TMT bubble will in fact take longer(than previous business cycles) to work off, as it would only follow a recovery in othersectors.

With the expectations of imminent economicrecovery driving financial markets since thelast quarter, many policymakers are cautioningthat markets may be getting ahead of them-selves. While, as Box 2.1 notes, equity marketshave had a “good” record in anticipating thetiming of recovery, the combination of risingequity prices and falling earnings estimateshas pushed the 12-month forward price-earningsratio for the S&P 500, as well as for other coun-tries (e.g., Germany), to higher than averagelevels (see Figures 2.9 and 2.10). This has ledto concerns about the sustainability of growthassumptions priced into the stock marketvaluations.2

In other markets, many market participantsview the sell off in the U.S. bond market in the sec-ond week of November as having been consider-ably exaggerated by technical factors as notedabove. Similarly, there is a consensus that “capit-ulation” selling in the federal funds futures mar-ket resulted in a disconnect in the form of a verypronounced U shape for federal funds futures—

CHAPTER II RECENT DEVELOPMENTS IN INTERNATIONAL CAPITAL MARKETS

12

Figure 2.9. Twelve-Month Forward Price-Earnings Ratio for the S&P 500

Source: I/B/E/S.

5 year average=21.1

10 year average=17.3

average for entire period=15.2

5

10

15

20

25

021985 88 91 94 97 2000

Figure 2.10.Twelve-Month Forward Price-Earnings Ratio for theGroup of Three

Source: I/B/E/S.

German DAX

Japanese Topix (right scale)

S&P 500

0

5

10

15

20

25

30

0

10

20

30

40

50

60

70

80

1988 90 92 94 96 98 2000 02

2See, for example, IMF, International Capital Markets(various issues through 2001).

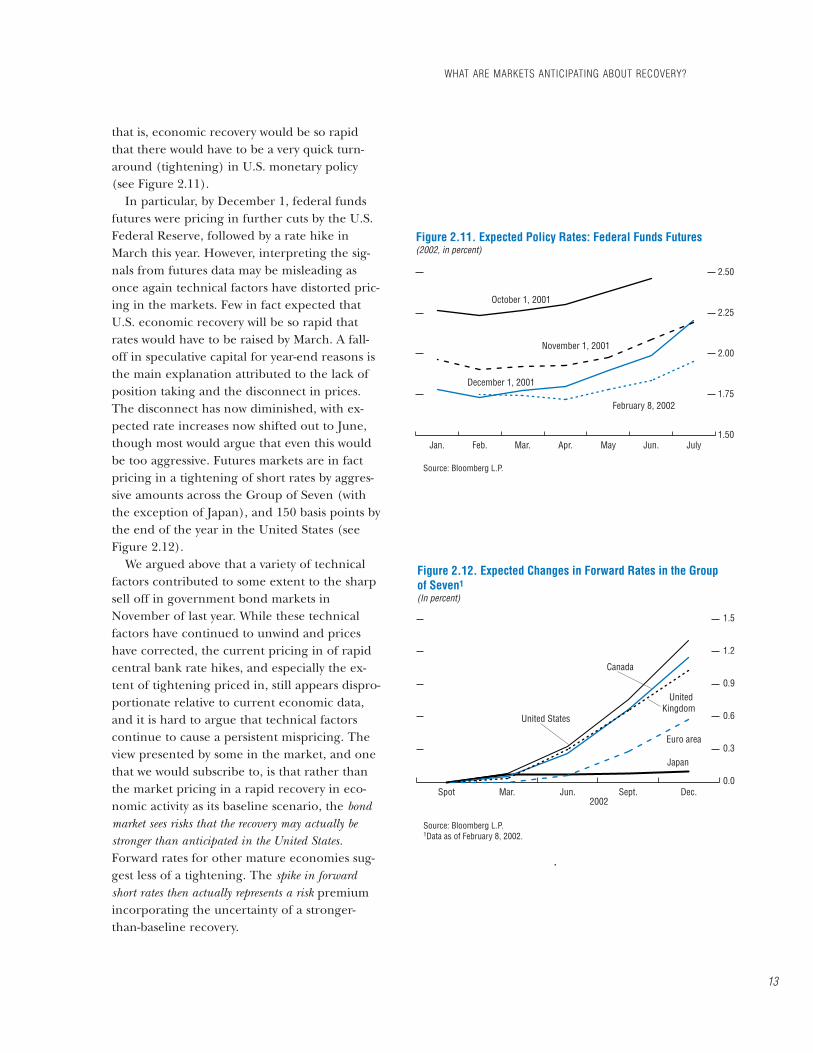

that is, economic recovery would be so rapidthat there would have to be a very quick turn-around (tightening) in U.S. monetary policy(see Figure 2.11).

In particular, by December 1, federal fundsfutures were pricing in further cuts by the U.S.Federal Reserve, followed by a rate hike inMarch this year. However, interpreting the sig-nals from futures data may be misleading asonce again technical factors have distorted pric-ing in the markets. Few in fact expected thatU.S. economic recovery will be so rapid thatrates would have to be raised by March. A fall-off in speculative capital for year-end reasons isthe main explanation attributed to the lack ofposition taking and the disconnect in prices.The disconnect has now diminished, with ex-pected rate increases now shifted out to June,though most would argue that even this wouldbe too aggressive. Futures markets are in factpricing in a tightening of short rates by aggres-sive amounts across the Group of Seven (withthe exception of Japan), and 150 basis points bythe end of the year in the United States (seeFigure 2.12).

We argued above that a variety of technicalfactors contributed to some extent to the sharpsell off in government bond markets inNovember of last year. While these technicalfactors have continued to unwind and priceshave corrected, the current pricing in of rapidcentral bank rate hikes, and especially the ex-tent of tightening priced in, still appears dispro-portionate relative to current economic data,and it is hard to argue that technical factorscontinue to cause a persistent mispricing. Theview presented by some in the market, and onethat we would subscribe to, is that rather thanthe market pricing in a rapid recovery in eco-nomic activity as its baseline scenario, the bondmarket sees risks that the recovery may actually bestronger than anticipated in the United States.Forward rates for other mature economies sug-gest less of a tightening. The spike in forwardshort rates then actually represents a risk premiumincorporating the uncertainty of a stronger-than-baseline recovery.

WHAT ARE MARKETS ANTICIPATING ABOUT RECOVERY?

13

Figure 2.11. Expected Policy Rates: Federal Funds Futures(2002, in percent)

Source: Bloomberg L.P.

October 1, 2001

1.50

1.75

2.00

2.25

2.50

JulyJun.MayApr.Mar.Feb.Jan.

November 1, 2001

December 1, 2001

February 8, 2002

Figure 2.12. Expected Changes in Forward Rates in the Group of Seven1

(In percent)

Source: Bloomberg L.P. 1Data as of February 8, 2002.

United States

0.0

0.3

0.6

0.9

1.2

1.5

Dec.Sept.Jun.Mar.Spot

Canada

United Kingdom

Euro area

Japan

2002

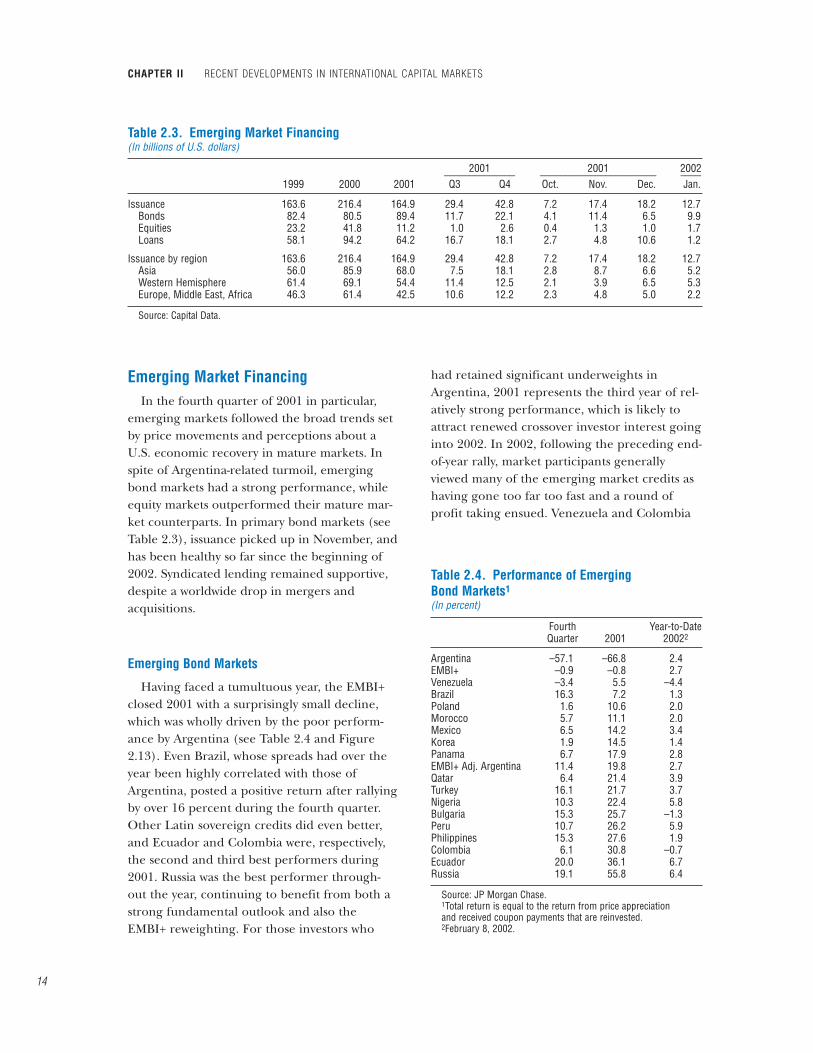

Emerging Market FinancingIn the fourth quarter of 2001 in particular,

emerging markets followed the broad trends setby price movements and perceptions about aU.S. economic recovery in mature markets. Inspite of Argentina-related turmoil, emergingbond markets had a strong performance, whileequity markets outperformed their mature mar-ket counterparts. In primary bond markets (seeTable 2.3), issuance picked up in November, andhas been healthy so far since the beginning of2002. Syndicated lending remained supportive,despite a worldwide drop in mergers andacquisitions.

Emerging Bond Markets

Having faced a tumultuous year, the EMBI+closed 2001 with a surprisingly small decline,which was wholly driven by the poor perform-ance by Argentina (see Table 2.4 and Figure2.13). Even Brazil, whose spreads had over theyear been highly correlated with those ofArgentina, posted a positive return after rallyingby over 16 percent during the fourth quarter.Other Latin sovereign credits did even better,and Ecuador and Colombia were, respectively,the second and third best performers during2001. Russia was the best performer through-out the year, continuing to benefit from both astrong fundamental outlook and also theEMBI+ reweighting. For those investors who

had retained significant underweights inArgentina, 2001 represents the third year of rel-atively strong performance, which is likely toattract renewed crossover investor interest goinginto 2002. In 2002, following the preceding end-of-year rally, market participants generallyviewed many of the emerging market credits ashaving gone too far too fast and a round ofprofit taking ensued. Venezuela and Colombia

CHAPTER II RECENT DEVELOPMENTS IN INTERNATIONAL CAPITAL MARKETS

14

Table 2.3. Emerging Market Financing (In billions of U.S. dollars)

2001 2001 2002______________ _______________________ ____1999 2000 2001 Q3 Q4 Oct. Nov. Dec. Jan.

Issuance 163.6 216.4 164.9 29.4 42.8 7.2 17.4 18.2 12.7Bonds 82.4 80.5 89.4 11.7 22.1 4.1 11.4 6.5 9.9Equities 23.2 41.8 11.2 1.0 2.6 0.4 1.3 1.0 1.7Loans 58.1 94.2 64.2 16.7 18.1 2.7 4.8 10.6 1.2

Issuance by region 163.6 216.4 164.9 29.4 42.8 7.2 17.4 18.2 12.7Asia 56.0 85.9 68.0 7.5 18.1 2.8 8.7 6.6 5.2Western Hemisphere 61.4 69.1 54.4 11.4 12.5 2.1 3.9 6.5 5.3Europe, Middle East, Africa 46.3 61.4 42.5 10.6 12.2 2.3 4.8 5.0 2.2

Source: Capital Data.

Table 2.4. Performance of EmergingBond Markets1

(In percent)

Fourth Year-to-DateQuarter 2001 20022

Argentina –57.1 –66.8 2.4EMBI+ –0.9 –0.8 2.7Venezuela –3.4 5.5 –4.4Brazil 16.3 7.2 1.3Poland 1.6 10.6 2.0Morocco 5.7 11.1 2.0Mexico 6.5 14.2 3.4Korea 1.9 14.5 1.4Panama 6.7 17.9 2.8EMBI+ Adj. Argentina 11.4 19.8 2.7Qatar 6.4 21.4 3.9Turkey 16.1 21.7 3.7Nigeria 10.3 22.4 5.8Bulgaria 15.3 25.7 –1.3Peru 10.7 26.2 5.9Philippines 15.3 27.6 1.9Colombia 6.1 30.8 –0.7Ecuador 20.0 36.1 6.7Russia 19.1 55.8 6.4

Source: JP Morgan Chase.1Total return is equal to the return from price appreciationand received coupon payments that are reinvested.2February 8, 2002.

were in particular focus during this latestsell-off.

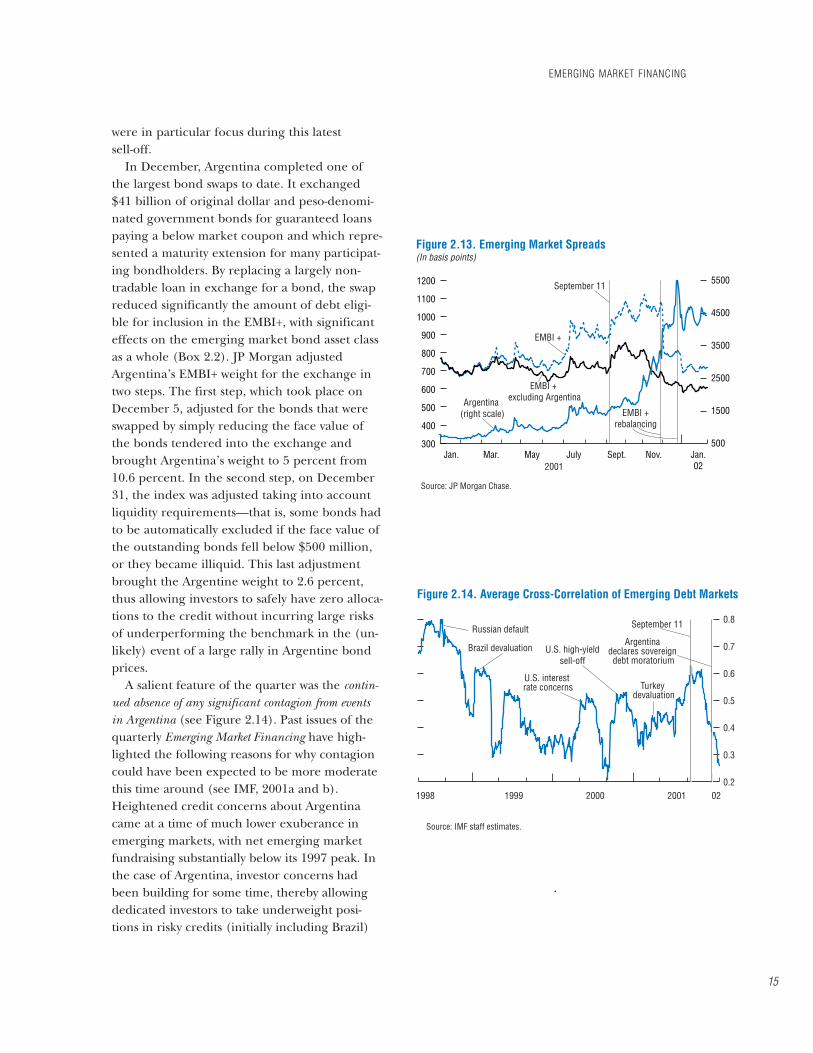

In December, Argentina completed one ofthe largest bond swaps to date. It exchanged$41 billion of original dollar and peso-denomi-nated government bonds for guaranteed loanspaying a below market coupon and which repre-sented a maturity extension for many participat-ing bondholders. By replacing a largely non-tradable loan in exchange for a bond, the swapreduced significantly the amount of debt eligi-ble for inclusion in the EMBI+, with significanteffects on the emerging market bond asset classas a whole (Box 2.2). JP Morgan adjustedArgentina’s EMBI+ weight for the exchange intwo steps. The first step, which took place onDecember 5, adjusted for the bonds that wereswapped by simply reducing the face value ofthe bonds tendered into the exchange andbrought Argentina’s weight to 5 percent from10.6 percent. In the second step, on December31, the index was adjusted taking into accountliquidity requirements—that is, some bonds hadto be automatically excluded if the face value ofthe outstanding bonds fell below $500 million,or they became illiquid. This last adjustmentbrought the Argentine weight to 2.6 percent,thus allowing investors to safely have zero alloca-tions to the credit without incurring large risksof underperforming the benchmark in the (un-likely) event of a large rally in Argentine bondprices.

A salient feature of the quarter was the contin-ued absence of any significant contagion from eventsin Argentina (see Figure 2.14). Past issues of thequarterly Emerging Market Financing have high-lighted the following reasons for why contagioncould have been expected to be more moderatethis time around (see IMF, 2001a and b).Heightened credit concerns about Argentinacame at a time of much lower exuberance inemerging markets, with net emerging marketfundraising substantially below its 1997 peak. Inthe case of Argentina, investor concerns hadbeen building for some time, thereby allowingdedicated investors to take underweight posi-tions in risky credits (initially including Brazil)

EMERGING MARKET FINANCING

15

Figure 2.13. Emerging Market Spreads(In basis points)

Source: JP Morgan Chase.

September 11

EMBI +

Argentina (right scale)

300

400

500

600

700

800

900

1000

1100

1200

Jan.02

Nov.Sept.JulyMayMar.Jan.500

1500

2500

3500

4500

5500

EMBI + excluding Argentina

EMBI +rebalancing

2001

Figure 2.14. Average Cross-Correlation of Emerging Debt Markets

Source: IMF staff estimates.

Russian default

Brazil devaluation U.S. high-yieldsell-off

0.2

0.3

0.4

0.5

0.6

0.7

0.8September 11

Argentina declares sovereign debt moratorium

Turkey devaluation

U.S. interest rate concerns

1998 1999 2000 2001 02

CHAPTER II RECENT DEVELOPMENTS IN INTERNATIONAL CAPITAL MARKETS

16

Argentina’s large stock of foreign currencydenominated bonds had been an importantsource of market concern about potential conta-gion in the run up to a default. Recently,Argentina had the highest or second highestweight in the EMBI+, and the sovereign was alsothe largest emerging market issuer in the euro-market. Even during non-crisis times, dedicatedinvestors benchmarked to the EMBI+ kept a“structural” underweight toward Argentina, inan attempt not to concentrate their portfoliosexcessively in one credit. Given Argentina’slarge weight, however, these investors could notreduce their portfolio allocations to zero inArgentina without running the risk of larger-than-tolerable index tracking error. Hence,there was a fear that losses in Argentina wouldforce dedicated investors to liquidate profitableoverweight positions elsewhere (Russia andBrazil). This “common ownership” motivationfor contagion was further exacerbated by con-cerns that a default on a quarter of the bench-mark index could frighten end-investors,thereby triggering a withdrawal of capital fromthe asset class. In the euro and yen markets,Argentine bonds were largely held by less so-phisticated “buy-and-hold” retail investors whowere not benchmarked to any index. The extentof contagion from the default hence differedacross the three segments:• In the case of dollar-denominated emerging market

bonds, investor discrimination was supportedby the falling weight of Argentina in the mar-ket cap weighted EMBI+. This allowed dedi-cated investors to automatically reduce theirexposure to Argentina further. The debt swapin early December created further support forthe decoupling of Argentina from the rest ofthe asset class. There had already at that timebeen signs of speculative investors and thestreet “front-running” the eventual change indedicated investors’ portfolio allocations. Inthe end, Argentina’s weight in the EMBI+ fellto 2.6 percent. The retrenchment by dedi-cated investors away from Argentina benefitedthose index constituents that stood to gainmost from the reweighting (notably Brazil,

Mexico, and Russia, see the figure) and hencenegated any contagion effects at that stage.

• The “common ownership” explanation forcontagion played a larger role for contagionacross Latin credits within the investor basefor euro-denominated emerging market bonds.When capitulation selling of Argentine bondsby mainly Italian, German, and Spanish retailinvestors occurred, these investors also largelyexited other Latin American sovereign bonds.Following the Argentine default, the euro-de-nominated market is currently in a state ofdisarray, as the large-scale exit of retail in-vestors has pushed the spreads of several euro-denominated emerging market bonds beyondthose of comparable dollar-denominatedbonds. As a result, the overall appetite forLatin American emerging market bonds hassubstantially declined, both in terms of supply(it is no longer price competitive relative todollar issuance) and demand. It remains anopen question whether the classic Europeanretail demand will again invest, in any size, inhigher risk emerging markets.

• In Japan, retail demand for any form ofhigher risk bond issue has suffered from boththe Enron and Argentine defaults. TheSamurai market remains firmly shut despite

Box 2.2. Argentina and the Asset Class

Historical EMBI Weights(In percent)

Source: JP Morgan Chase.

0

5

10

15

20

25

30

Mexico

Russia

Brazil

Argentina

0201200099989796951994

and to overweight those that were seen asrelatively immune. This increase in investor dis-crimination has been a positive developmentand shows maturation in at least the dollar-denominated segment of the asset class. We havein the past attributed the increase in investor dis-crimination to the rising relative importance ofdedicated and local investors, and to the declinein importance of leverage in the system. Ofcourse, in the past the major episodes of conta-gion in emerging markets have been a result ofsurprises, while Argentina’s default at the end ofDecember clearly was not.

Turning to the fourth quarter of 2001, we at-tribute the surprising lack of secondary marketspillovers from Argentina additionally to thesupportive global environment for fixed incomeproducts, the EMBI+ reweighting due to theArgentine bond swap, and market beliefsthroughout October and November that theexchange rate regime would either remain as

is or involve a stabilization, thereby supportingArgentine bond prices in the secondary market.

Our measure of contagion,3 the average cross-correlation of individual country returns in theEMBI+, continued to fall throughout Decemberand January, despite the increased turbulence inArgentina, and is currently around 0.3, beloweven the long-term average of 0.4. With respectto individual cross-country correlations,Argentine sovereign bonds continue to decouplefrom most other emerging market sovereigns(see Figure 2.15). However, the pair wise correla-tion with Venezuela has clearly been high, asVenezuela faces increasing investor concernsagainst a backdrop of political turmoil and oilprice weakness. Looking ahead, the risk of con-tagion has certainly not disappeared completelyand there remains a concern about contagion ei-ther though the foreign exchange markets, asseen during a few days in January, or through

EMERGING MARKET FINANCING

17

appearances to the contrary in the quarter. Inthe wake of Argentina–related credit concernsand then the actual default, the market is ex-pected to remain closed for some time toother low-rated credits. The Philippine shibo-sai (privately placed Samurai) went toEuropean investors who were comfortablewith the 97.5 percent credit enhancement bythe Japanese Export Import Agency NEXI(2.5 percent risk on the underlyingPhilippines risk was enough to deter Japaneseinvestors), while mid-December’s ThaiSamurai was taken up mainly by Japanesebanks operating in Thailand to fulfill local re-serve requirements. As a result, there has

been so far no issuance of any emerging mar-ket bond since mid-December.In conclusion, Argentina’s impact on the

emerging market bond class has been more sub-stantial in the euro and yen markets, where re-tail investors held on in the somewhat optimisticbelief that emerging market sovereigns wouldnot default. While these two markets will have togo through a transformation, it is indeed possi-ble that these necessary changes will in the endlead to a more developed and sophisticated in-stitutional investor base for emerging marketbonds with similar characteristics to that of thedollar segment, which has weathered theArgentine default quite well.

3The measure uses the average cross-correlation of spreads for a rolling 50-day window on the external debt of nineemerging markets (Argentina, Brazil, Ecuador, Mexico, Panama, Peru, Poland, Russia, and Venezuela). A criticism of simi-lar measures can be found by Forbes and Rigobon (2000), who point out that in measuring contagion, increases in volatil-ity during crisis periods can bias correlations upwards. However, Baig and Goldfajn (2000), argue that it is unclear theForbes and Rigobon correction should be made, as the same factors that result in increased volatility (thin markets, panic,margin calls) are precisely the factors responsible for contagion and controlling for one, causes a loss of power for theother.

primary markets (renewed closures) or a fall offin foreign direct investment (FDI) flows toemerging markets.

Turning to primary markets, following therecovery in global financial markets and declinein risk aversion, capital markets reopened inNovember to emerging market issuers followingthe longest bond market drought (11 weeks)since the Russian crisis (13 weeks). As expected,those issuers highest up the credit spectrumwere able to re-access markets first, using plain-vanilla structures in the case of sovereigns, andpolitical risk insurance in the case of non-investment-grade corporates. After near-recordbond issuance in November, issuance levels re-mained robust in December, allowing a substan-tial amount of pre-financing for emergingmarket borrowers. In the last quarter, bond is-suance reached $21.1 billion, which is abouthalfway between the healthy issuance level ofthe second quarter and the dismal third quarterof 2001 (Figure 2.16). As anticipated, invest-ment-grade issuers dominated the quarter andaccounted for 62 percent of total bond issuance(SingTel issued $2.3 billion), while, at leastinitially, non-investment-grade issuance wasdominated by credits that could be seen as di-versification plays (such as the DominicanRepublic, Guatemala, or Bulgaria) or were seenas enjoying the support of the internationalcommunity—for example, Turkey. The fourthquarter also marked the recovery of euro-de-nominated issuance, following both Turkey’sand the City of Moscow’s return to the market.Dollar-denominated issuance also took a largershare, while bond issuance denominated inJapanese yen fell back closer to its average his-torical quarterly level (see Table 2.5). For 2001as a whole, the recovery in issuance during thelast quarter brought total issuance to nearly $90billion (excluding exchanges) exceeding thelevels of 1998–2000, but was nonetheless stillbelow the $100 billion plus issuance of 1996and 1997.

Since the beginning of the year, emergingmarket bond issuance has remained at relativelyhealthy levels and $1 billion plus bond issues

CHAPTER II RECENT DEVELOPMENTS IN INTERNATIONAL CAPITAL MARKETS

18

Figure 2.15. Emerging Market Spread Correlations with Argentina1

Source: IMF staff estimates. 180-day rolling correlations.

September 11

Brazil

Non-Latin

–1.0

–0.8

–0.6

–0.4

–0.2

0

0.2

0.4

0.6

0.8

1.0

Jan.02

Nov.Sept.JulyMayMar.

Venezuela

Mexico

2001

Figure 2.16. Monthly Bond Issuance(In billions of U.S. dollars)

Source: Capital Data.

0

5

10

15

20

25Other Western HemisphereAsia

20012000199919981997

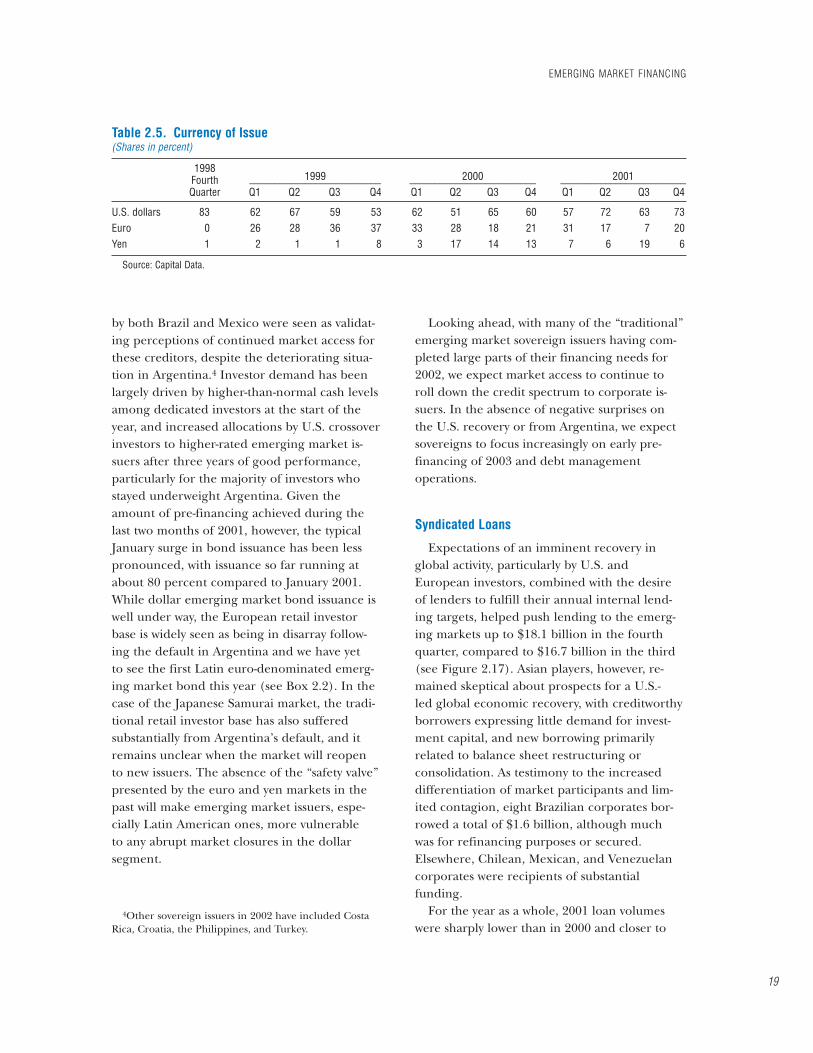

by both Brazil and Mexico were seen as validat-ing perceptions of continued market access forthese creditors, despite the deteriorating situa-tion in Argentina.4 Investor demand has beenlargely driven by higher-than-normal cash levelsamong dedicated investors at the start of theyear, and increased allocations by U.S. crossoverinvestors to higher-rated emerging market is-suers after three years of good performance,particularly for the majority of investors whostayed underweight Argentina. Given theamount of pre-financing achieved during thelast two months of 2001, however, the typicalJanuary surge in bond issuance has been lesspronounced, with issuance so far running atabout 80 percent compared to January 2001.While dollar emerging market bond issuance iswell under way, the European retail investorbase is widely seen as being in disarray follow-ing the default in Argentina and we have yetto see the first Latin euro-denominated emerg-ing market bond this year (see Box 2.2). In thecase of the Japanese Samurai market, the tradi-tional retail investor base has also sufferedsubstantially from Argentina’s default, and itremains unclear when the market will reopento new issuers. The absence of the “safety valve”presented by the euro and yen markets in thepast will make emerging market issuers, espe-cially Latin American ones, more vulnerableto any abrupt market closures in the dollarsegment.

Looking ahead, with many of the “traditional”emerging market sovereign issuers having com-pleted large parts of their financing needs for2002, we expect market access to continue toroll down the credit spectrum to corporate is-suers. In the absence of negative surprises onthe U.S. recovery or from Argentina, we expectsovereigns to focus increasingly on early pre-financing of 2003 and debt managementoperations.

Syndicated Loans

Expectations of an imminent recovery inglobal activity, particularly by U.S. andEuropean investors, combined with the desireof lenders to fulfill their annual internal lend-ing targets, helped push lending to the emerg-ing markets up to $18.1 billion in the fourthquarter, compared to $16.7 billion in the third(see Figure 2.17). Asian players, however, re-mained skeptical about prospects for a U.S.-led global economic recovery, with creditworthyborrowers expressing little demand for invest-ment capital, and new borrowing primarilyrelated to balance sheet restructuring orconsolidation. As testimony to the increaseddifferentiation of market participants and lim-ited contagion, eight Brazilian corporates bor-rowed a total of $1.6 billion, although muchwas for refinancing purposes or secured.Elsewhere, Chilean, Mexican, and Venezuelancorporates were recipients of substantialfunding.

For the year as a whole, 2001 loan volumeswere sharply lower than in 2000 and closer to

EMERGING MARKET FINANCING

19

Table 2.5. Currency of Issue(Shares in percent)

1998Fourth 1999 2000 2001__________________________ _________________________ _________________________Quarter Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

U.S. dollars 83 62 67 59 53 62 51 65 60 57 72 63 73Euro 0 26 28 36 37 33 28 18 21 31 17 7 20Yen 1 2 1 1 8 3 17 14 13 7 6 19 6

Source: Capital Data.

4Other sovereign issuers in 2002 have included CostaRica, Croatia, the Philippines, and Turkey.

trends in 1998–99. With demand for new moneylimited amid concern about the global slowdownand a dearth of mergers and acquisitions activity,the volume of lending reached $64.2 billion in2001 compared with $94.2 billion in 2000 (seeFigure 2.18).

On the pricing front, the syndicated lendingmarket in Asia remains characterized by ahigh degree of competition between banks tolend to the handful of top tier corporatesand financial institutions, while shutting outlower tier borrowers. With little demand fornew money, banks competed to lend to bor-rowers, making pricing very tight at the topend, while rationing out those entities thatmay be most in need of capital. As a result,syndicated loan spreads remained broadly flatin Asia at low levels, while spreads declined inLatin America, reflecting this quarter’s distri-bution of lending among Latin corporates (seeFigure 2.19).

Emerging Equity Markets

Emerging equity markets recovered on cuewith their mature market counterparts as a“high beta” play on global growth and reflectingtheir higher (than global markets) concentra-tion in TMT stocks (see Table 2.6). Emerging

CHAPTER II RECENT DEVELOPMENTS IN INTERNATIONAL CAPITAL MARKETS

20

Figure 2.17. Loan Issuance(In billions of U.S. dollars)

Source: Capital Data.

0

3

6

9

12

15OtherWestern HemisphereAsia

2000 2001

Figure 2.18. Cumulative Gross Annual Issuance of Hard Currency Loans(In billions of U.S. dollars)

Source: Capital Data.

0

30

60

90

120

150

2001 2000

1999

1998

1997

1996

Dec.Nov.Oct.Sept.Aug.JulyJuneMayApr.Mar.Feb.Jan.

Table 2.6. Total Dollar Return Performance ofEmerging Equity Markets(In percent)

Year-to-Date*

Q1 Q2 Q3 Q4 2001 2002

RegionsEM Free –6.2 3.1 –22.1 26.3 –4.9 2.3Asia –0.1 –1.6 –20.1 32.8 4.2 4.6LatAm –3.5 7.1 –24.0 21.8 –4.3 –2.8EMEA –22.0 4.5 –25.8 36.3 –17.7 –2.0

Mature market comparators

ACWI Free –12.8 2.3 –15.0 9.1 –17.3 –4.5S&P 500 –12.1 5.5 –15.0 10.3 –13.0 –2.8Dow –8.4 6.3 –15.8 13.3 –7.1 –6.7Nasdaq –25.5 17.4 –30.7 30.1 –21.1 –5.1

Sources: Bloomberg L.P.; and Morgan Stanley CapitalInternational.

*February 8.

equity markets comfortably outperformed theirmature market counterparts, with returns re-sembling those of the Nasdaq. Cyclical sectorsincluding technology led the rally. The initialrally, particularly in tech heavy markets such asKorea and Taiwan Province of China, was led byforeign investors increasing exposures to Asianequities in order not to underperform in theevent of a global rally. Local investors werenotably absent from the rally. Asian emergingmarkets received the bulk of substantial foreigninvestor flows into emerging equity marketsduring October and November (see Figure2.20). While having similar earnings growthforecasts as in mature markets, Asian equitiesare still seen as cheap, encouraging investors tomaintain neutral to overweight positions inAsia.

Primary market issuance in the fourthquarter (of $2.6 billion compared with $1 bil-lion in the third) was again dominated by Asiannames, but 2001 as a whole was only slightlyhigher than 1998 but lower than the succeedingtwo years. Issues were mainly privatization dealsfrom China, along with banking sector issuancefrom Singapore and the tobacco sector inKorea.

Foreign Direct Investment

In 2001, despite an estimated 42 percentdrop in global FDI to $760 billion, and anestimated 45 percent drop in cross-bordermergers and acquisitions activity, net FDI flowsto emerging market countries are estimated tohave held steady at $163 billion (see IMF,2001c) (see Figure 2.21). Reflecting an ongoingtrend, FDI flows to emerging market countriesremained highly concentrated, with 10 coun-tries accounting for nearly 70 percent of netFDI flows to emerging markets, and China,Brazil, and Mexico alone accounting for aboutone-half of net FDI flows. Looking ahead, netFDI flows to emerging markets are expected tofall further as mergers and acquisition activity isexpected to remain slow to recover, while thehigh cost of equity capital in emerging equity

EMERGING MARKET FINANCING

21

Figure 2.19. Loan-Weighted Interest Margin(In basis points, 1995–2001)

Source: Capital Data.

0

100

200

300

400

500

600

Western Hemisphere

Asia

2001200019991998199719961995

Figure 2.20. Net Foreign Purchases and Monthly Returns on Emerging Equity Markets1

Sources: IMF staff estimates; Central banks; and Bloomberg L.P. 1August data exclude $8.9 bn for Mexico the purchase of Banamex by Citigroup.

Russian CrisisAsian Crisis

US slowdownand tech rout

–4000

–3000

–2000

–1000

0

1000

2000

3000

4000

5000

6000Net purchases (left scale)

–20

–15

–10

–5

0

5

10

15

20

25

30MSCI Emerging Markets Free(monthly returns, right scale)

(In millions of U.S. dollars) (In percent)

1997 1998 1999 2000 2001

markets will hinder privatization-related FDIinflows.

ReferencesBaig, Taimur, and Ilan Goldfajn, 2000, “The Russian

Default and the Contagion to Brazil,” IMF WorkingPaper No. 00/160 (Washington: InternationalMonetary Fund).

Forbes, Kristin, and Roberto Rigobon, 2000, “Measur-ing Contagion: Conceptual and Empirical issues,”(unpublished).

International Monetary Fund, International CapitalMarkets: Developments, Prospects, and Key Policy Issues,World Economic and Financial Surveys(Washington), various issues.

———, 2001a, Emerging Market Financing, February 13,available on the Internet at http://www.imf.org/external/pubs/ft/emf/index.htm.

———, 2001b, Emerging Market Financing, August 8,available on the Internet at http://www.imf.org/external/pubs/ft/emf/index.htm.

———, 2001c, World Economic Outlook: December 2001,World Economic and Financial Surveys(Washington).

CHAPTER II RECENT DEVELOPMENTS IN INTERNATIONAL CAPITAL MARKETS

22

Figure 2.21. Capital Flows to Emerging Economies(In billions of U.S. dollars)

Source: IMF, World Ecomonic Outlook.

Total portfolio and banking flows, net

Direct investment, net

–150

–100

–50

0

50

100

150

200

20009896949290888684821980

Total private sector, net

Total official sector, net

As mentioned in Chapter I, during 2001the international financial system hasshown remarkable resilience in theface of sizable disruptions. Moreover,

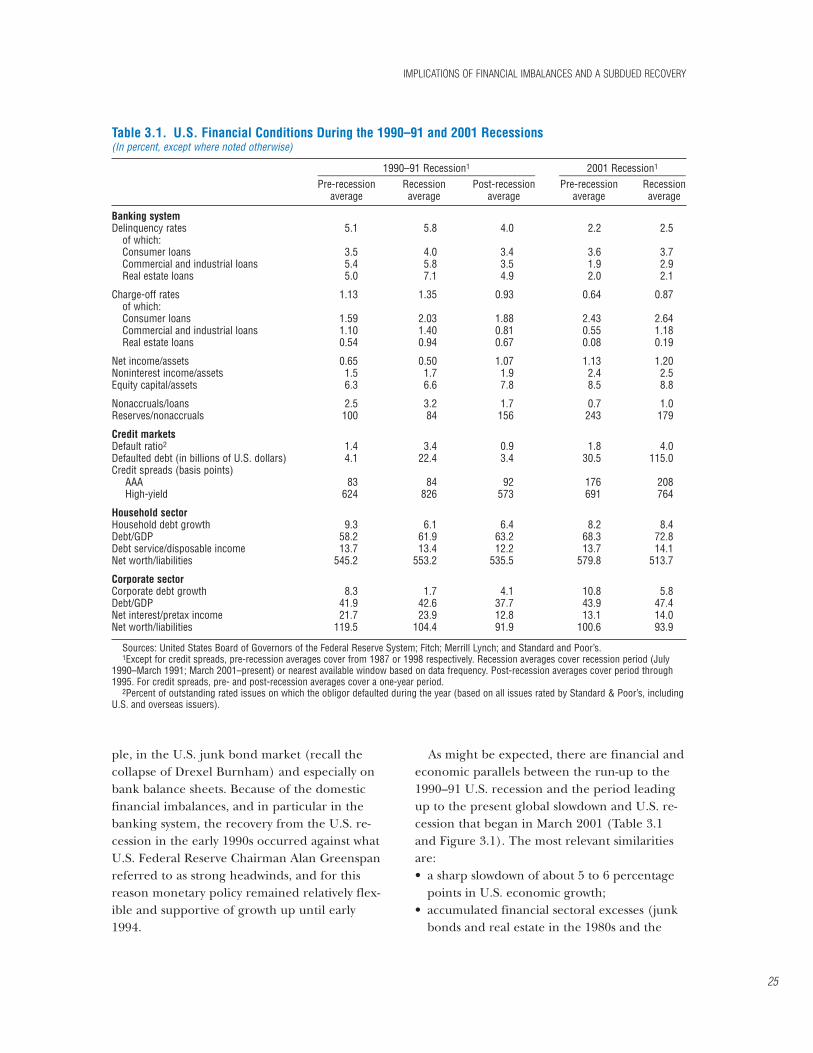

recent economic data seem to support marketexpectations that the global economy will re-cover soon. Nevertheless, for the purpose ofidentifying vulnerabilities in international finan-cial markets, this chapter considers the risks tointernational financial stability that could be as-sociated with the potential financial fallout ofseveral financial imbalances, which could be ex-acerbated by a subdued recovery. In light of ac-cumulated financial imbalances that have not yetbeen worked off, the main uncertainties wouldseem to be associated with the resilience ofhousehold, corporate, and bank (and nonbankfinancial institution) balance sheets in the pres-ence of the renewed declines in equity pricesand deterioration in credit quality that might oc-cur during a weaker-than-expected global recov-ery. If balance sheets are impaired and financialimbalances are aggravated as a result of such as-set price adjustments during the recession, thiscould itself lead to a subdued recovery andcould possibly delay it, which in turn could feedback to a further deterioration in financial con-ditions (and so on). This would lead to a lessfriendly operating environment for financial in-stitutions, especially for those already weakenedby the events of 2001, and to possible stresswithin the international financial system.

Another closely related source of risk derivesfrom the ongoing structural transformation inglobal finance. Many such sources can—and infuture issues of this report will—be identified.For the period immediately ahead, with creditdeterioration still unfolding, the increasing re-

liance on credit risk transfer mechanisms coulddevelop to be a source of financial market risk.The recent global rise in corporate debt defaultsto historically high levels, and the relatively lowdegree of financial disclosure and market trans-parency about these instruments and markets—and about who owns the credit risk—wouldseem to pose some risk that market participantsmight have difficulty in accurately gauging thenature and extent of the credit deterioration.Even though these instruments and marketshave coped fairly well with the events of 2001, itis still an open question how effectively they areworking in the presence of a global slowdownand record high default rates.

Financial Market Implications of FinancialImbalances and a Subdued Recovery