Embed Size (px)

Citation preview

www.beyondphilosophy.com

Global Customer Experience Management Survey 2011

Beyond Philosophy

Steven Walden, Senior Head of Research

Colin Shaw, Founder & CEO

www.beyondphilosophy.com

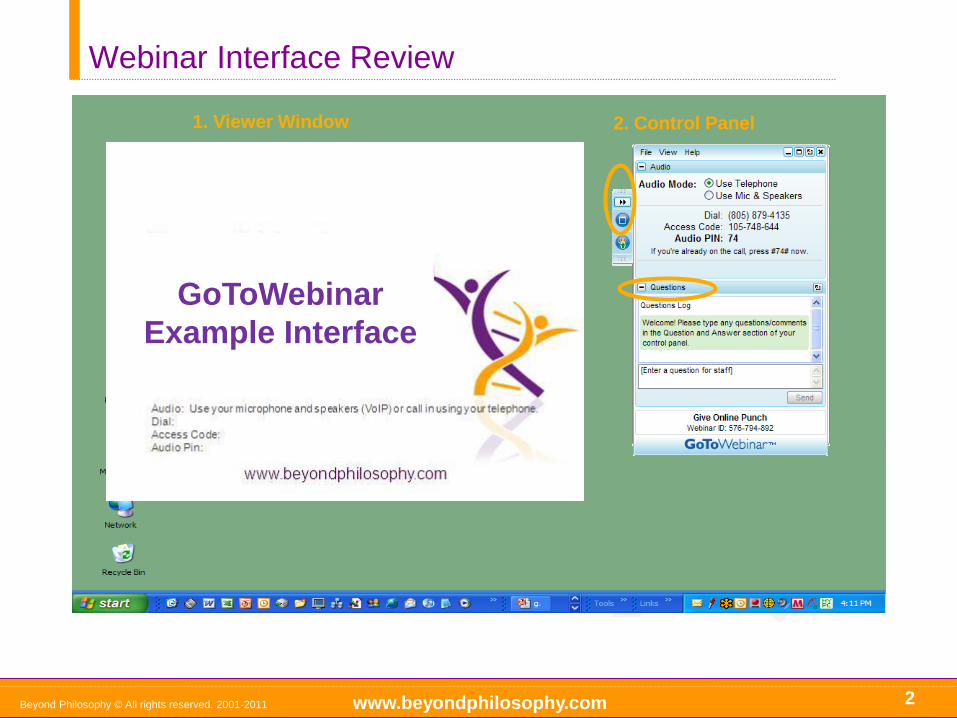

Webinar Interface Review

2

Beyond Philosophy © All rights reserved. 2001-2011

1. Viewer Window 2. Control Panel

GoToWebinar

Example Interface

www.beyondphilosophy.com

The Beyond Philosophy Perspective

3 Beyond Philosophy © All rights reserved. 2001-2011

Customer Experience

is all we do!

Thought leadership is

our differentiator

Offices in London,

Atlanta with partners in

Europe & Asia

New fourth book

Is now available

Links with academia Focus on the emotional side

of Customer Experience

www.beyondphilosophy.com

We are Proud to Have Helped Some Great Organizations

4 Beyond Philosophy © All rights reserved. 2001-2011

www.beyondphilosophy.com

Themes

5

How can we model the state of the market in Customer

Experience globally? 2

4 The risks, challenges and drivers to Customer

Experience programmes

Beyond Philosophy © All rights reserved. 2001-2011

5 Best Practice: what you need to do!

Methodology 1

How are global resources allocated to Customer

Experience?

3

www.beyondphilosophy.com

Questions

1. Learn about our 7-stage Customer Experience Maturity

model. Also, gain insight into how customer experience is

understood or misunderstood, and learn about the

implications and risks as it continues to evolve.

2. Where is customer experience management most needed?

What industry? What country? What companies?

3. Which industries spend the most on customer experience?

4. Which regions spend the most on customer experience?

5. What companies have seen the biggest customer

experience growth, by industry?

6. What industries will see the greatest growth in customer

experience over the next several years?

7. What are the drivers and challenges the customer

experience industry faces as it further develops?

8. What is the valuable element of a company’s customer

experience program? How does it differ by industry or

region?

9. How will social media affect the way companies approach

customer experience?

10. What will be the next great customer experience

advancement?: Best Practice and Innovations

6 Beyond Philosophy © All rights reserved. 2001-2011

How are global resources

allocated to Customer

Experience?

How can we model the

state of growth in

Customer Experience

Globally?

The risks, challenges and

drivers to Customer

Experience programmes

Best Practice: what you

need to do!

www.beyondphilosophy.com

Section 1

7 Beyond Philosophy © All rights reserved. 2001-2011

Methodology 1

www.beyondphilosophy.com

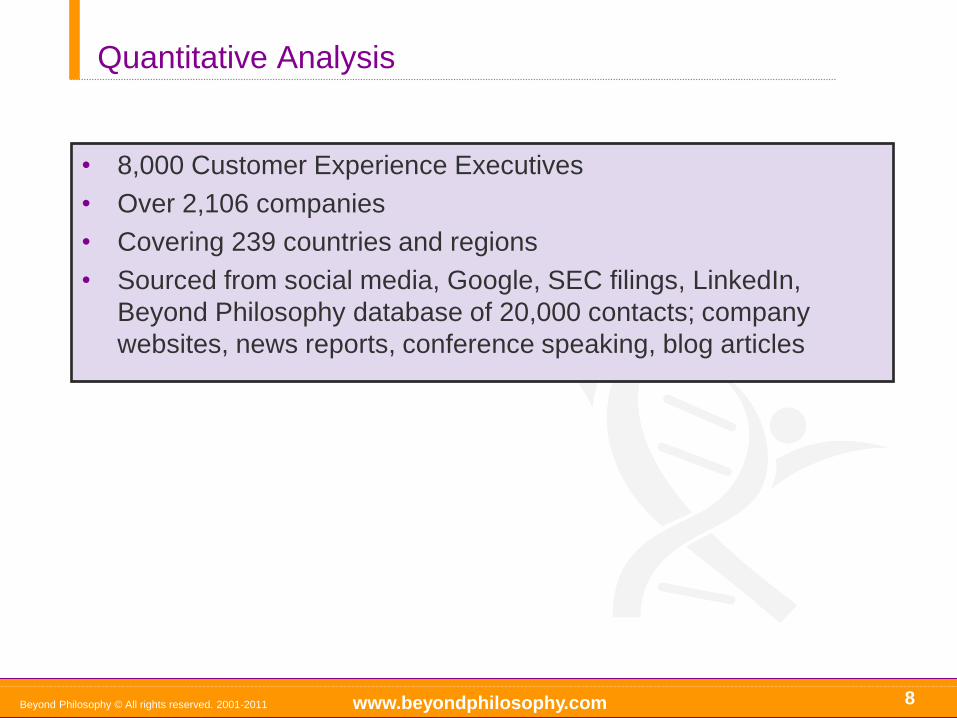

Quantitative Analysis

• 8,000 Customer Experience Executives

• Over 2,106 companies

• Covering 239 countries and regions

• Sourced from social media, Google, SEC filings, LinkedIn,

Beyond Philosophy database of 20,000 contacts; company

websites, news reports, conference speaking, blog articles

8 Beyond Philosophy © All rights reserved. 2001-2011

www.beyondphilosophy.com

A High Bar to Minimize the Inclusion of Weakly Active Firms or Those Not Really Doing CE

9

We selected CE ‘active’ companies e.g., those with a CE presence on

an in-country Google site ‘in the last year’ and/ or a presence of

executives with a LinkedIn CE title.

Beyond Philosophy © All rights reserved. 2001-2011

www.beyondphilosophy.com

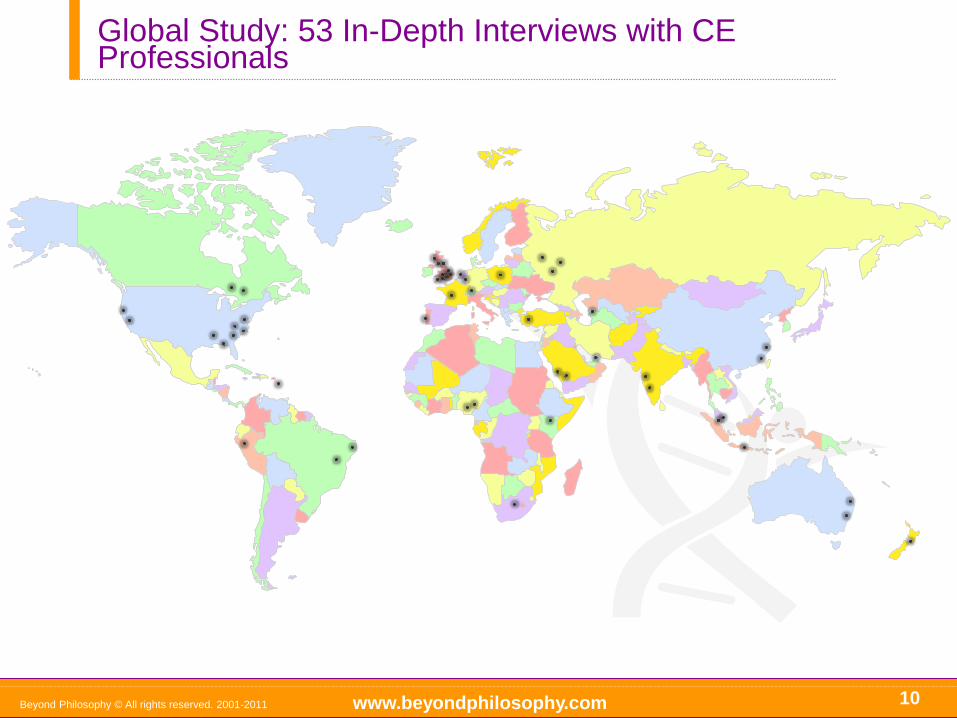

Global Study: 53 In-Depth Interviews with CE Professionals

Beyond Philosophy © All rights reserved. 2001-2011 10

www.beyondphilosophy.com

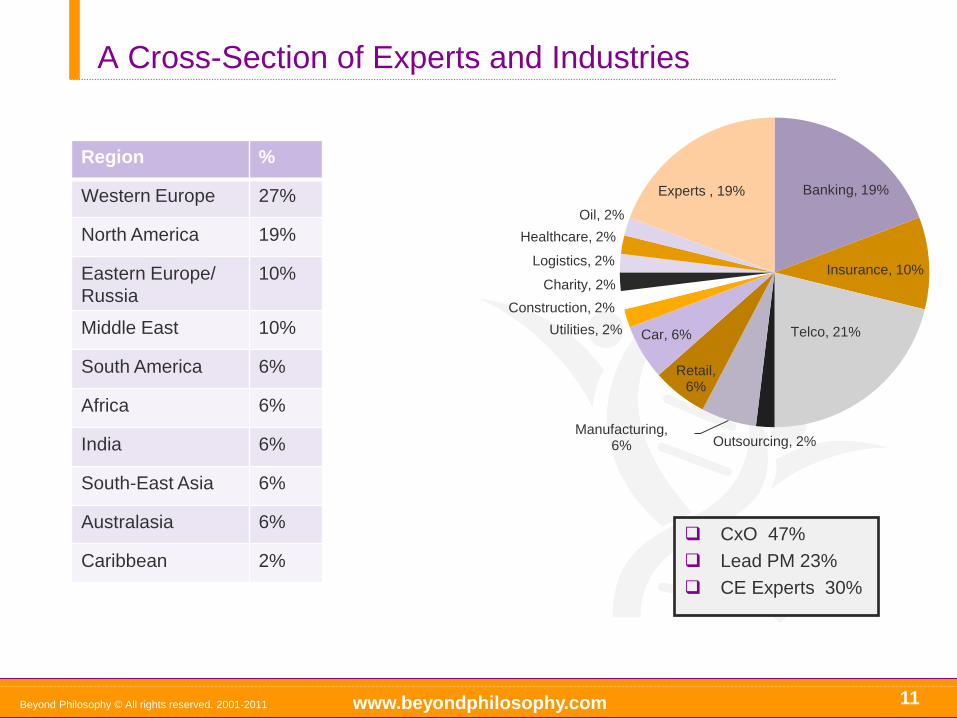

A Cross-Section of Experts and Industries

CxO 47%

Lead PM 23%

CE Experts 30%

11 Beyond Philosophy © All rights reserved. 2001-2011

Banking, 19%

Insurance, 10%

Telco, 21%

Outsourcing, 2% Manufacturing,

6%

Retail, 6%

Car, 6% Utilities, 2%

Construction, 2%

Charity, 2%

Logistics, 2%

Healthcare, 2%

Oil, 2%

Experts , 19%

Region %

Western Europe 27%

North America 19%

Eastern Europe/

Russia

10%

Middle East 10%

South America 6%

Africa 6%

India 6%

South-East Asia 6%

Australasia 6%

Caribbean 2%

www.beyondphilosophy.com

Section 2

12

How can we model the state of the market in Customer

Experience globally? 2

Beyond Philosophy © All rights reserved. 2001-2011

www.beyondphilosophy.com

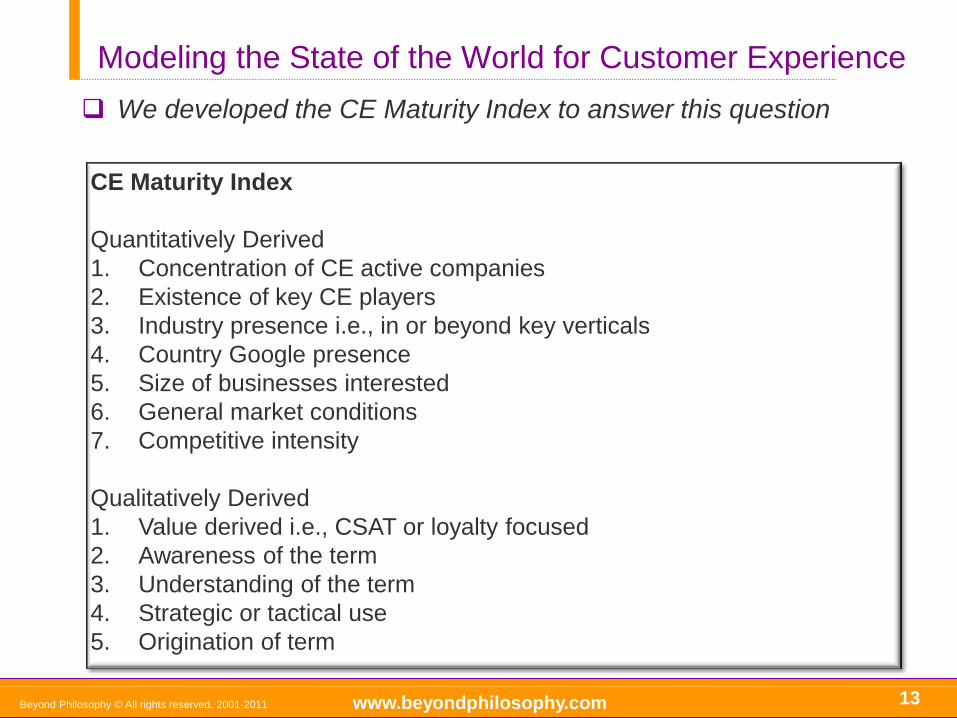

Modeling the State of the World for Customer Experience

CE Maturity Index

Quantitatively Derived

1. Concentration of CE active companies

2. Existence of key CE players

3. Industry presence i.e., in or beyond key verticals

4. Country Google presence

5. Size of businesses interested

6. General market conditions

7. Competitive intensity

Qualitatively Derived

1. Value derived i.e., CSAT or loyalty focused

2. Awareness of the term

3. Understanding of the term

4. Strategic or tactical use

5. Origination of term

13

We developed the CE Maturity Index to answer this question

Beyond Philosophy © All rights reserved. 2001-2011

www.beyondphilosophy.com

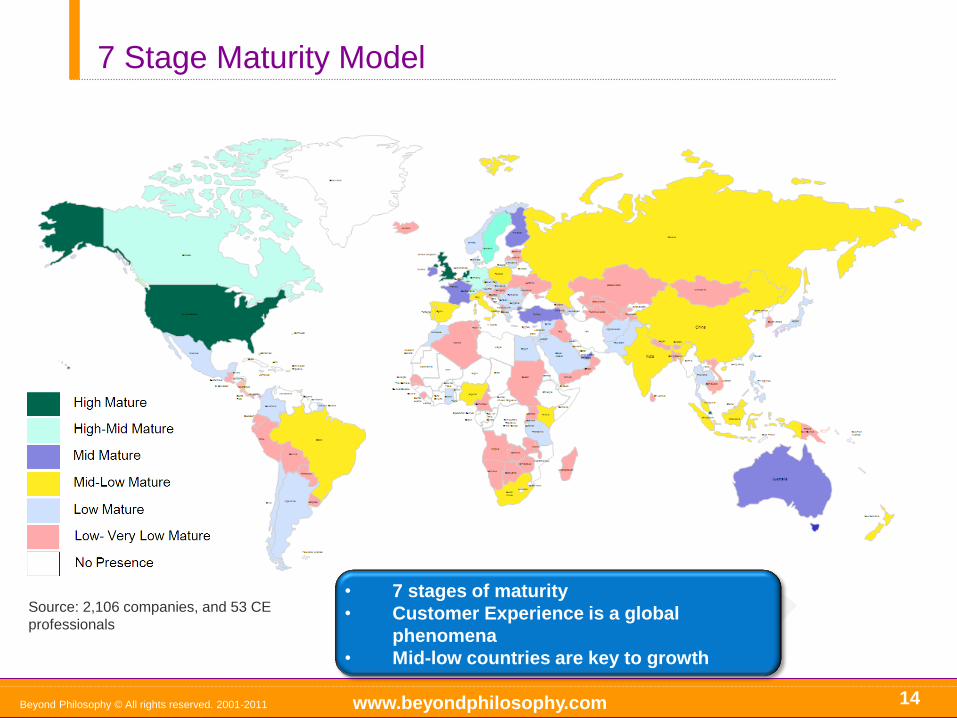

7 Stage Maturity Model

14 Beyond Philosophy © All rights reserved. 2001-2011

Source: 2,106 companies, and 53 CE

professionals

• 7 stages of maturity

• Customer Experience is a global

phenomena

• Mid-low countries are key to growth

www.beyondphilosophy.com

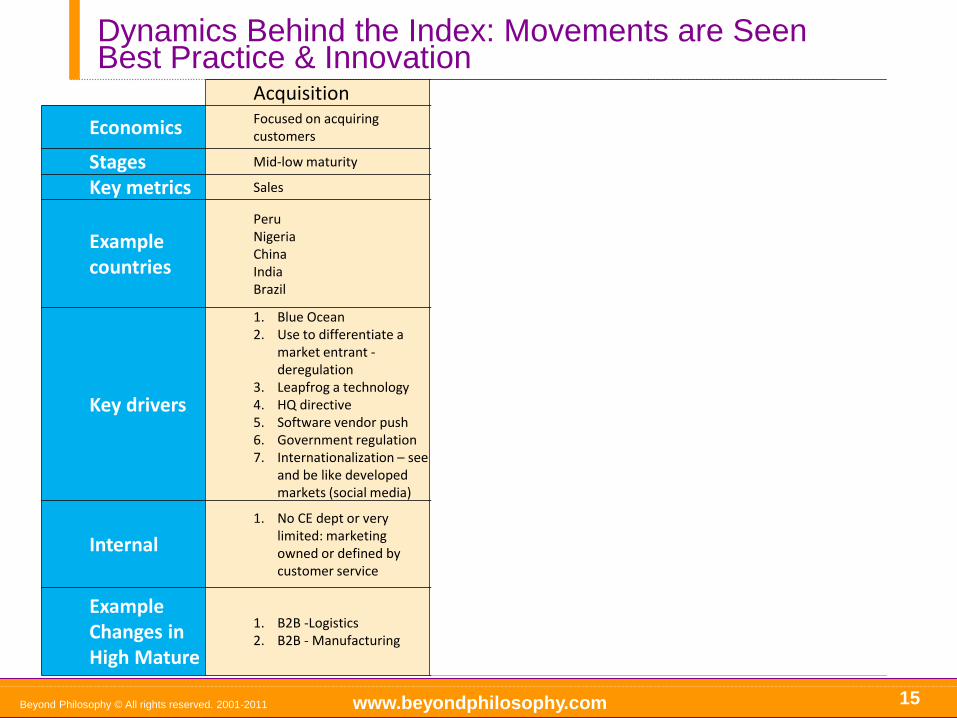

Acquisition Relationship Retention

Economics Focused on acquiring customers

Focused on relationship building with customers

Focused on retaining customers and preventing churn

Stages Mid-low maturity Mid-high maturity High maturity

Key metrics Sales Satisfaction and Sales Loyalty

Example countries

Peru Nigeria China India Brazil

Turkey UAE South Africa Russia

USA UK Singapore Canada

Key drivers

1. Blue Ocean 2. Use to differentiate a

market entrant - deregulation

3. Leapfrog a technology 4. HQ directive 5. Software vendor push 6. Government regulation 7. Internationalization – see

and be like developed markets (social media)

1. Target high margin segments

2. Manage a changed expectations set

3. HQ directive 4. Technology

programmes rebranded

1. Optimise channels 2. Manage retention

programmes 3. Launch branded

programmes 4. Regulation

Internal

1. No CE dept or very limited: marketing owned or defined by customer service

1. Start up CE dept. in certain verticals

1. Established key CE players 2. Start up CE going beyond

Telco, Banking and Retail

Example Changes in High Mature

1. B2B -Logistics 2. B2B - Manufacturing

1. Motor 2. Aviation 3. Utilities

1. Banking 2. Telecommunications 3. Retail 4. IT 5. Insurance

Dynamics Behind the Index: Movements are Seen Best Practice & Innovation

Beyond Philosophy © All rights reserved. 2001-2011 15

www.beyondphilosophy.com

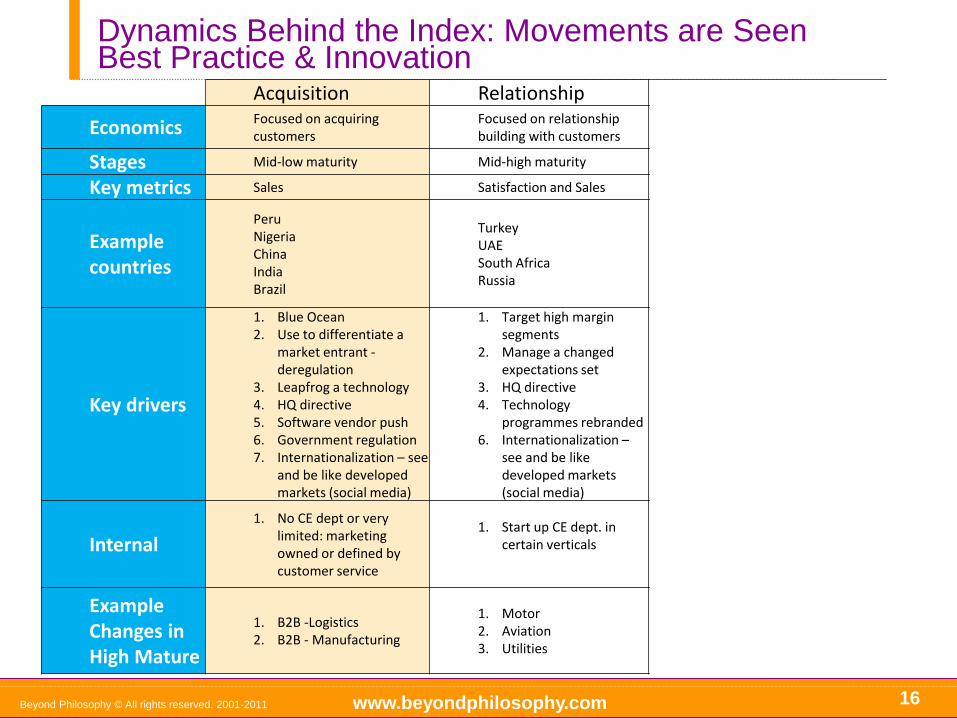

Acquisition Relationship Retention

Economics Focused on acquiring customers

Focused on relationship building with customers

Focused on retaining customers and preventing churn

Stages Mid-low maturity Mid-high maturity High maturity

Key metrics Sales Satisfaction and Sales Loyalty

Example countries

Peru Nigeria China India Brazil

Turkey UAE South Africa Russia

USA UK Singapore Canada

Key drivers

1. Blue Ocean 2. Use to differentiate a

market entrant - deregulation

3. Leapfrog a technology 4. HQ directive 5. Software vendor push 6. Government regulation 7. Internationalization – see

and be like developed markets (social media)

1. Target high margin segments

2. Manage a changed expectations set

3. HQ directive 4. Technology

programmes rebranded 6. Internationalization –

see and be like developed markets (social media)

1. Optimise channels 2. Manage retention

programmes 3. Launch branded

programmes 4. Regulation

Internal

1. No CE dept or very limited: marketing owned or defined by customer service

1. Start up CE dept. in certain verticals

1. Established key CE players 2. Start up CE going beyond

Telco, Banking and Retail

Example Changes in High Mature

1. B2B -Logistics 2. B2B - Manufacturing

1. Motor 2. Aviation 3. Utilities

1. Banking 2. Telecommunications 3. Retail

Dynamics Behind the Index: Movements are Seen Best Practice & Innovation

Beyond Philosophy © All rights reserved. 2001-2011 16

www.beyondphilosophy.com

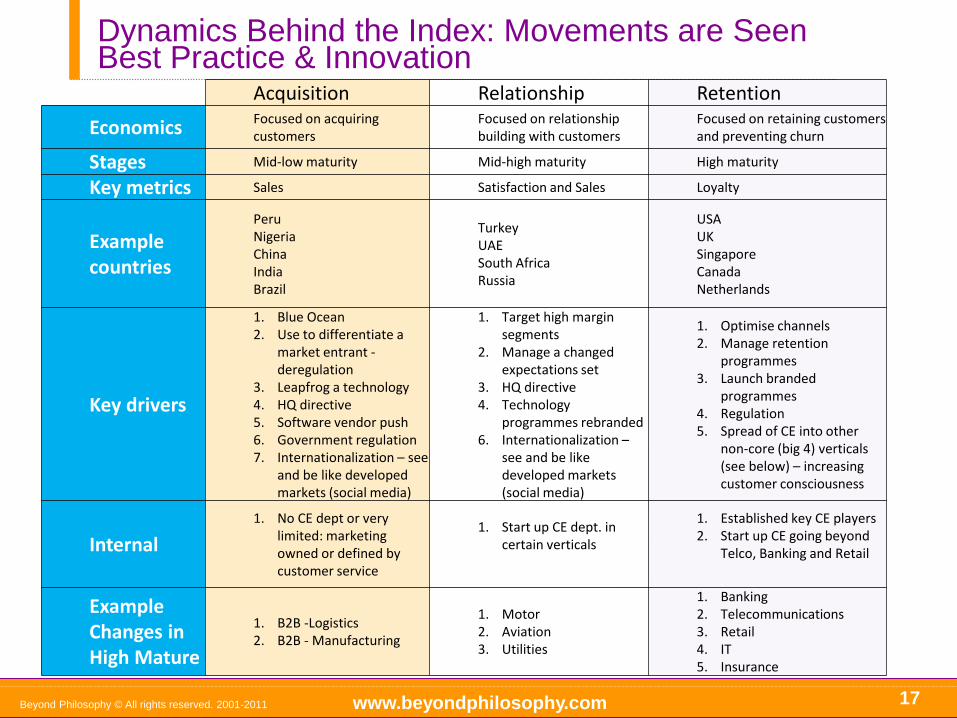

Acquisition Relationship Retention

Economics Focused on acquiring customers

Focused on relationship building with customers

Focused on retaining customers and preventing churn

Stages Mid-low maturity Mid-high maturity High maturity

Key metrics Sales Satisfaction and Sales Loyalty

Example countries

Peru Nigeria China India Brazil

Turkey UAE South Africa Russia

USA UK Singapore Canada Netherlands

Key drivers

1. Blue Ocean 2. Use to differentiate a

market entrant - deregulation

3. Leapfrog a technology 4. HQ directive 5. Software vendor push 6. Government regulation 7. Internationalization – see

and be like developed markets (social media)

1. Target high margin segments

2. Manage a changed expectations set

3. HQ directive 4. Technology

programmes rebranded 6. Internationalization –

see and be like developed markets (social media)

1. Optimise channels 2. Manage retention

programmes 3. Launch branded

programmes 4. Regulation 5. Spread of CE into other

non-core (big 4) verticals (see below) – increasing customer consciousness

Internal

1. No CE dept or very limited: marketing owned or defined by customer service

1. Start up CE dept. in certain verticals

1. Established key CE players 2. Start up CE going beyond

Telco, Banking and Retail

Example Changes in High Mature

1. B2B -Logistics 2. B2B - Manufacturing

1. Motor 2. Aviation 3. Utilities

1. Banking 2. Telecommunications 3. Retail 4. IT 5. Insurance

Dynamics Behind the Index: Movements are Seen Best Practice & Innovation

Beyond Philosophy © All rights reserved. 2001-2011 17

www.beyondphilosophy.com

Acquisition Relationship Retention

Economics Focused on acquiring customers

Focused on relationship building with customers

Focused on retaining customers and preventing churn

Stages Mid-low maturity Mid-high maturity High maturity

Key metrics Sales Satisfaction and Sales Loyalty

Example countries

Peru Nigeria China India Brazil

Turkey UAE South Africa Russia

USA UK Singapore Canada Netherlands

Key drivers

1. Blue Ocean 2. Use to differentiate a

market entrant - deregulation

3. Leapfrog a technology 4. HQ directive 5. Software vendor push 6. Government regulation 7. Internationalization – see

and be like developed markets (social media)

1. Target high margin segments

2. Manage a changed expectations set

3. HQ directive 4. Technology

programmes rebranded 6. Internationalization –

see and be like developed markets (social media)

1. Optimise channels 2. Manage retention

programmes 3. Launch branded

programmes 4. Regulation 5. Spread of CE into other

non-core (big 4) verticals (see below) – increasing customer consciousness

Internal

1. No CE dept or very limited: marketing owned or defined by customer service

1. Start up CE dept. in certain verticals

1. Established key CE players 2. Start up CE going beyond

Telco, Banking and Retail

Example Changes in High Mature

1. B2B -Logistics 2. B2B - Manufacturing

1. Motor 2. Aviation 3. Utilities

1. Banking 2. Telecommunications 3. Retail 4. IT 5. Insurance

Moving

Moving

Dynamics Behind the Index: Movements are Seen Best Practice & Innovation

Beyond Philosophy © All rights reserved. 2001-2011 18

www.beyondphilosophy.com

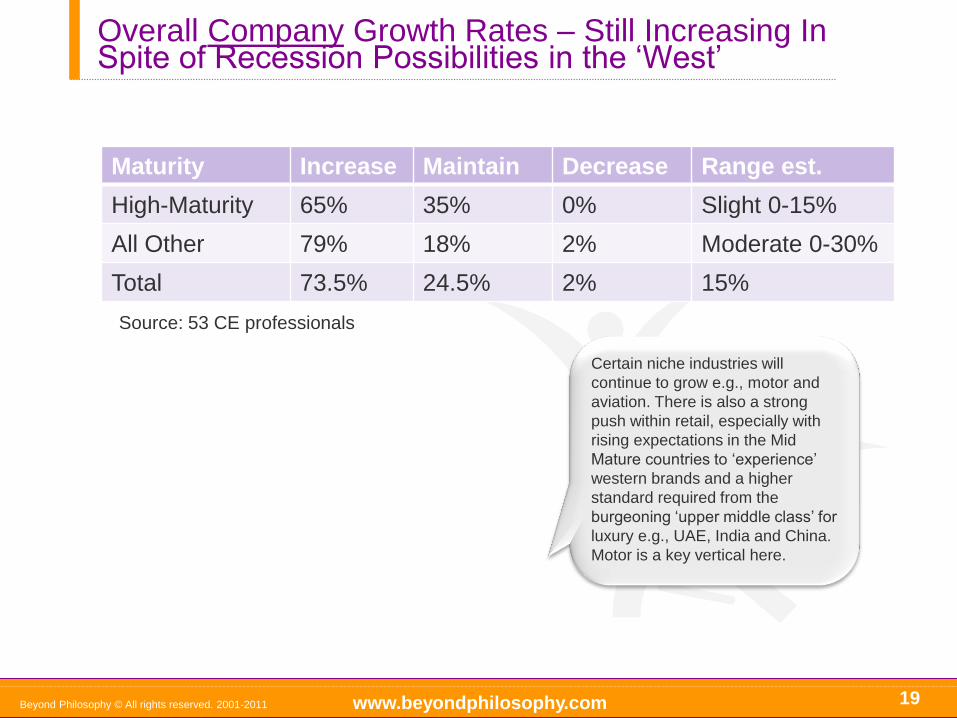

Overall Company Growth Rates – Still Increasing In Spite of Recession Possibilities in the ‘West’

19 Beyond Philosophy © All rights reserved. 2001-2011

Maturity Increase Maintain Decrease Range est.

High-Maturity 65% 35% 0% Slight 0-15%

All Other 79% 18% 2% Moderate 0-30%

Total 73.5% 24.5% 2% 15%

Source: 53 CE professionals

Certain niche industries will

continue to grow e.g., motor and

aviation. There is also a strong

push within retail, especially with

rising expectations in the Mid

Mature countries to ‘experience’

western brands and a higher

standard required from the

burgeoning ‘upper middle class’ for

luxury e.g., UAE, India and China.

Motor is a key vertical here.

www.beyondphilosophy.com

The Themes

20 Beyond Philosophy © All rights reserved. 2001-2011

How are global resources allocated to Customer

Experience?

3

www.beyondphilosophy.com

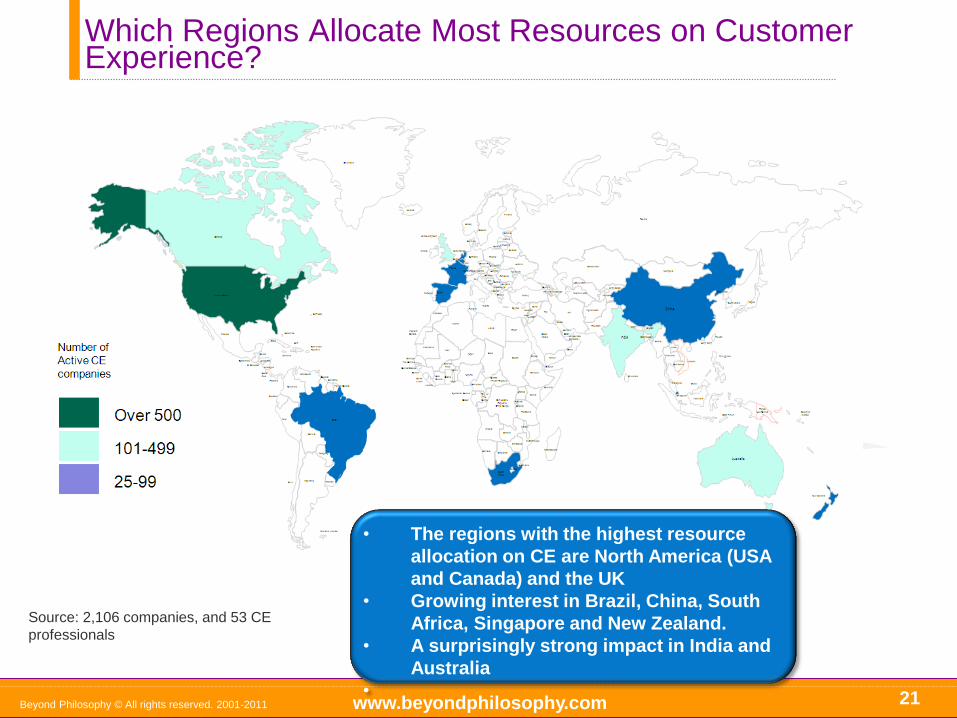

Which Regions Allocate Most Resources on Customer Experience?

Beyond Philosophy © All rights reserved. 2001-2011

Source: 2,106 companies, and 53 CE

professionals

• The regions with the highest resource

allocation on CE are North America (USA

and Canada) and the UK

• Growing interest in Brazil, China, South

Africa, Singapore and New Zealand.

• A surprisingly strong impact in India and

Australia

•

21

www.beyondphilosophy.com

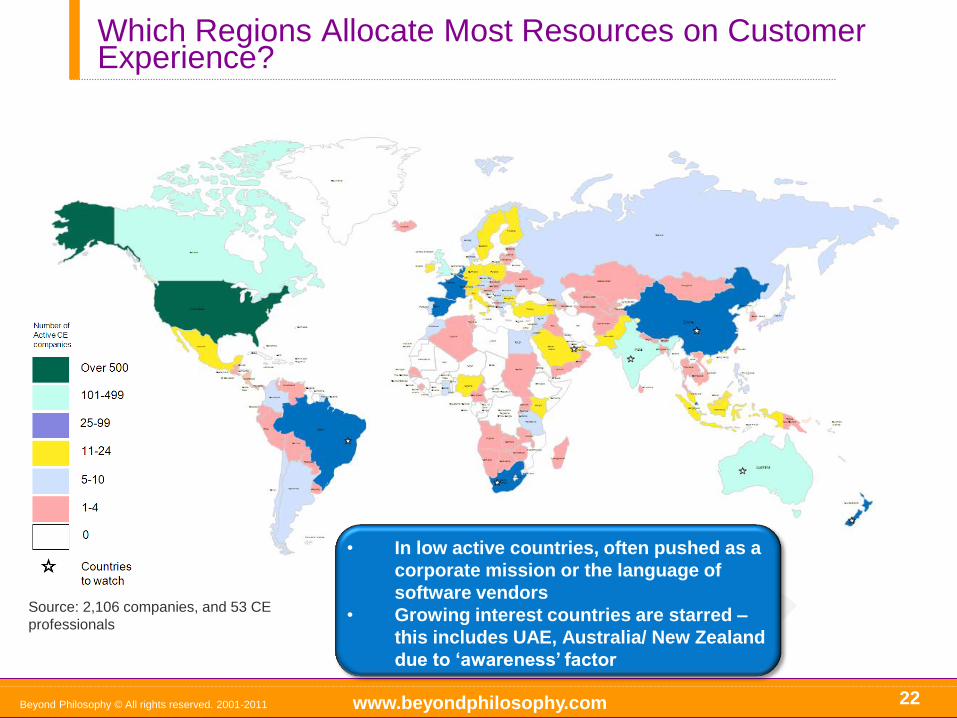

Which Regions Allocate Most Resources on Customer Experience?

22

Source: 2,106 companies, and 53 CE

professionals

Beyond Philosophy © All rights reserved. 2001-2011

• In low active countries, often pushed as a

corporate mission or the language of

software vendors

• Growing interest countries are starred –

this includes UAE, Australia/ New Zealand

due to ‘awareness’ factor

www.beyondphilosophy.com

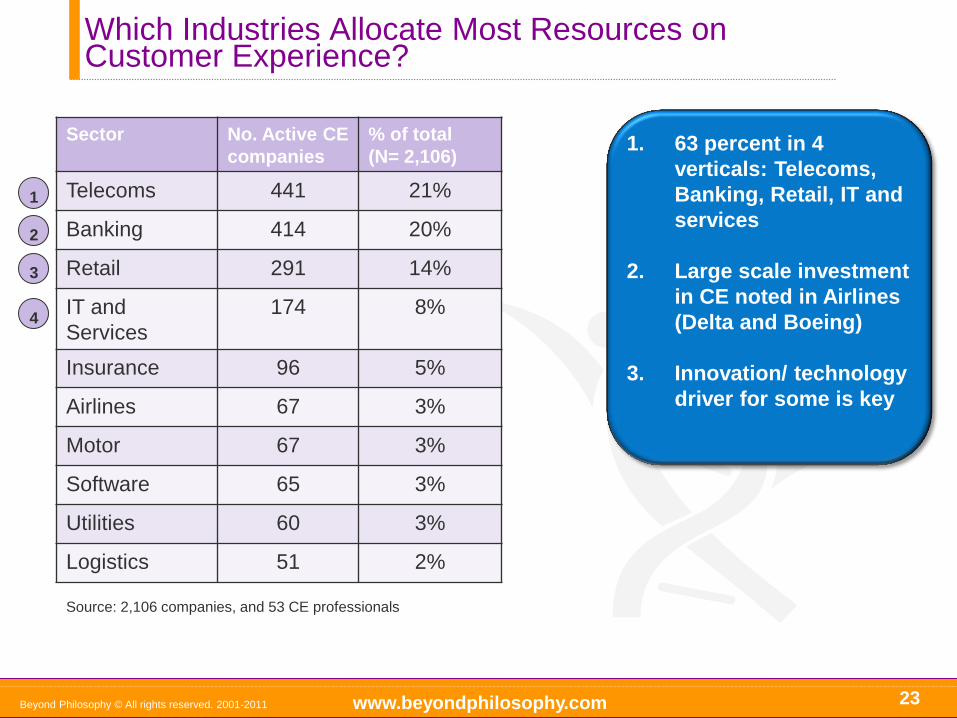

Which Industries Allocate Most Resources on Customer Experience?

23

1. 63 percent in 4

verticals: Telecoms,

Banking, Retail, IT and

services

2. Large scale investment

in CE noted in Airlines

(Delta and Boeing)

3. Innovation/ technology

driver for some is key

Beyond Philosophy © All rights reserved. 2001-2011

Sector No. Active CE

companies

% of total

(N= 2,106)

Telecoms 441 21%

Banking 414 20%

Retail 291 14%

IT and

Services

174 8%

Insurance 96 5%

Airlines 67 3%

Motor 67 3%

Software 65 3%

Utilities 60 3%

Logistics 51 2%

Source: 2,106 companies, and 53 CE professionals

1

2

3

4

www.beyondphilosophy.com 24

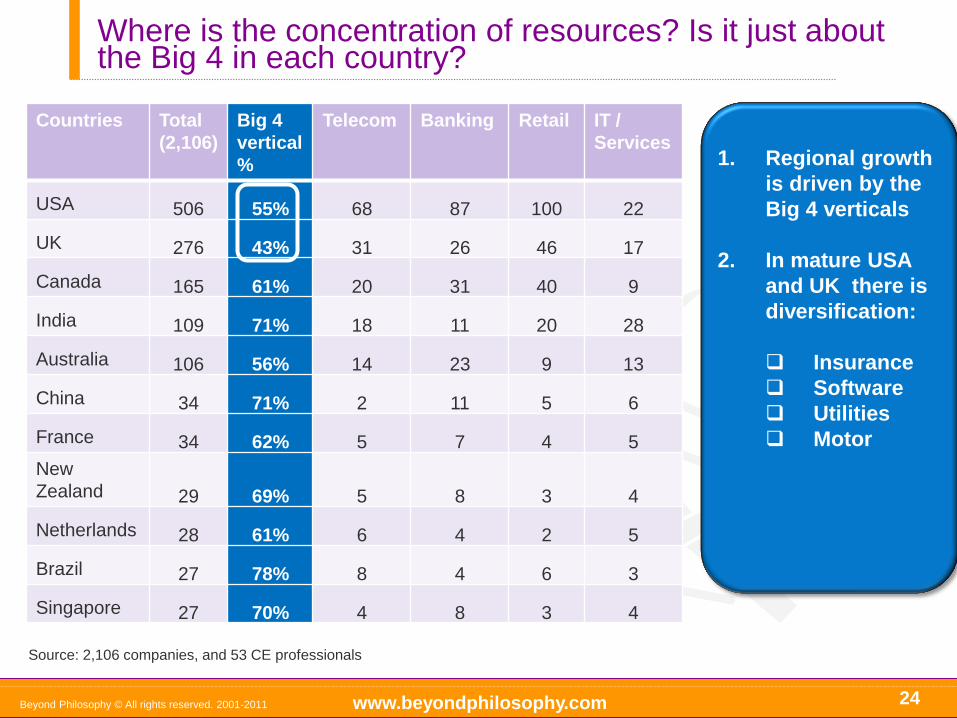

Countries Total

(2,106)

Big 4

vertical

%

Telecom Banking Retail IT /

Services

USA 506 55% 68 87 100 22

UK 276 43% 31 26 46 17

Canada 165 61% 20 31 40 9

India 109 71% 18 11 20 28

Australia 106 56% 14 23 9 13

China 34 71% 2 11 5 6

France 34 62% 5 7 4 5

New

Zealand 29 69% 5 8 3 4

Netherlands 28 61% 6 4 2 5

Brazil 27 78% 8 4 6 3

Singapore 27 70% 4 8 3 4

1. Regional growth

is driven by the

Big 4 verticals

2. In mature USA

and UK there is

diversification:

Insurance

Software

Utilities

Motor

Source: 2,106 companies, and 53 CE professionals

Beyond Philosophy © All rights reserved. 2001-2011

Where is the concentration of resources? Is it just about the Big 4 in each country?

www.beyondphilosophy.com

What Companies Have Seen the Biggest Customer Experience Resource Allocation, by Industry?

25

Source: 2,106 companies, and CE experts

Beyond Philosophy © All rights reserved. 2001-2011

Executives are by disclosure- the identified

executives give direction of focus and are for cross-

comparison purposes

Top 20

1. HP

2. HSBC

3. Vodafone

4. GAP

5. AMEX

6. Dell

7. Citibank

8. Best Buy

9. Sprint Nextel

10. AT&T

11. TD Bank

12. Bank of America

13. All State Insurance 14. Wells Fargo

15. BT

16. BSkyB

17. Lloyds Bank

18. Telstra

19. Verizon

20. T-Mobile

IT

Bank

Telecom

Retail

These companies are not

necessarily the best, they

claim most activity in CE

Criteria: location, spread

and number of country

locations, number of CE

executives

www.beyondphilosophy.com

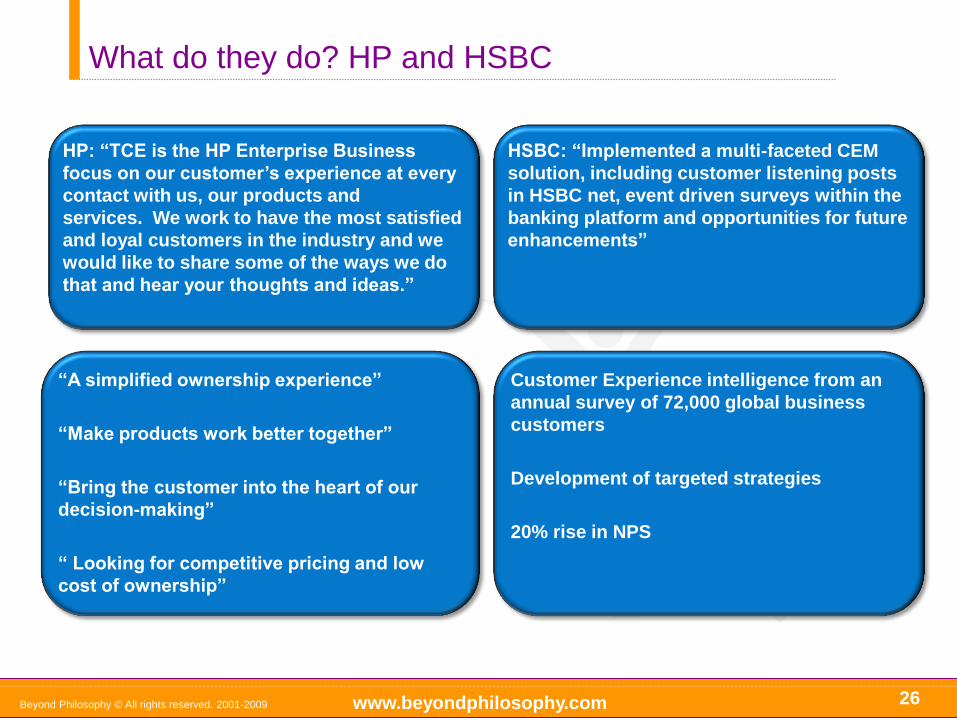

What do they do? HP and HSBC

26 Beyond Philosophy © All rights reserved. 2001-2009

“A simplified ownership experience”

“Make products work better together”

“Bring the customer into the heart of our

decision-making”

“ Looking for competitive pricing and low

cost of ownership”

HP: “TCE is the HP Enterprise Business

focus on our customer’s experience at every

contact with us, our products and

services. We work to have the most satisfied

and loyal customers in the industry and we

would like to share some of the ways we do

that and hear your thoughts and ideas.”

HSBC: “Implemented a multi-faceted CEM

solution, including customer listening posts

in HSBC net, event driven surveys within the

banking platform and opportunities for future

enhancements”

Customer Experience intelligence from an

annual survey of 72,000 global business

customers

Development of targeted strategies

20% rise in NPS

www.beyondphilosophy.com

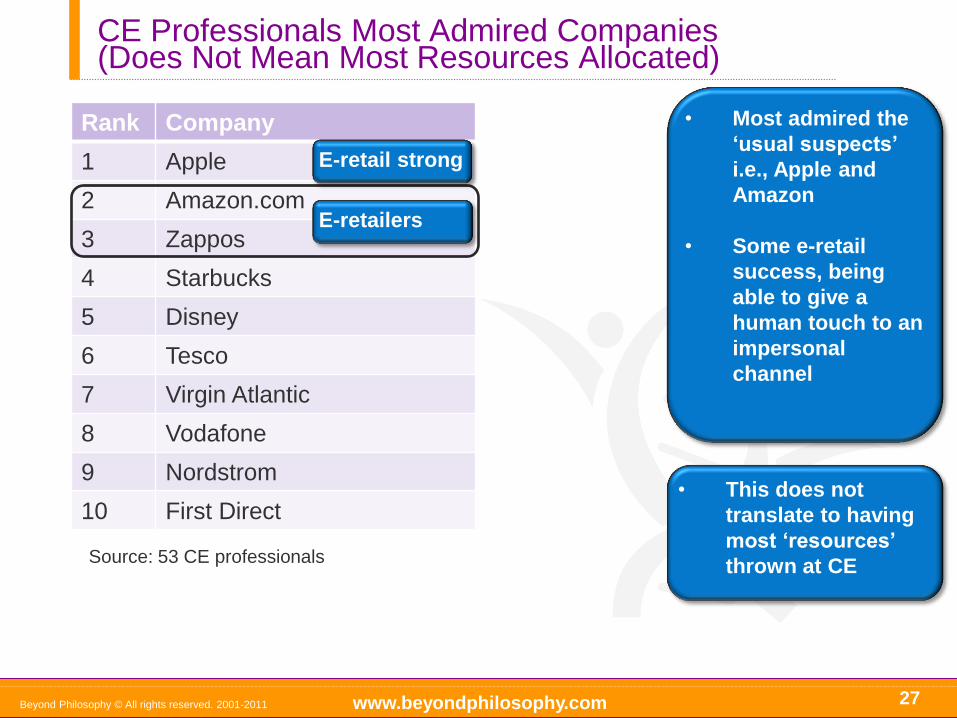

CE Professionals Most Admired Companies (Does Not Mean Most Resources Allocated)

27

• Most admired the

‘usual suspects’

i.e., Apple and

Amazon

• Some e-retail

success, being

able to give a

human touch to an

impersonal

channel

Rank Company

1 Apple

2 Amazon.com

3 Zappos

4 Starbucks

5 Disney

6 Tesco

7 Virgin Atlantic

8 Vodafone

9 Nordstrom

10 First Direct

E-retail strong

E-retailers

Source: 53 CE professionals

Beyond Philosophy © All rights reserved. 2001-2011

• This does not

translate to having

most ‘resources’

thrown at CE

www.beyondphilosophy.com

The Themes

28

4 The risks, challenges and drivers to Customer

Experience programmes

Beyond Philosophy © All rights reserved. 2001-2011

www.beyondphilosophy.com

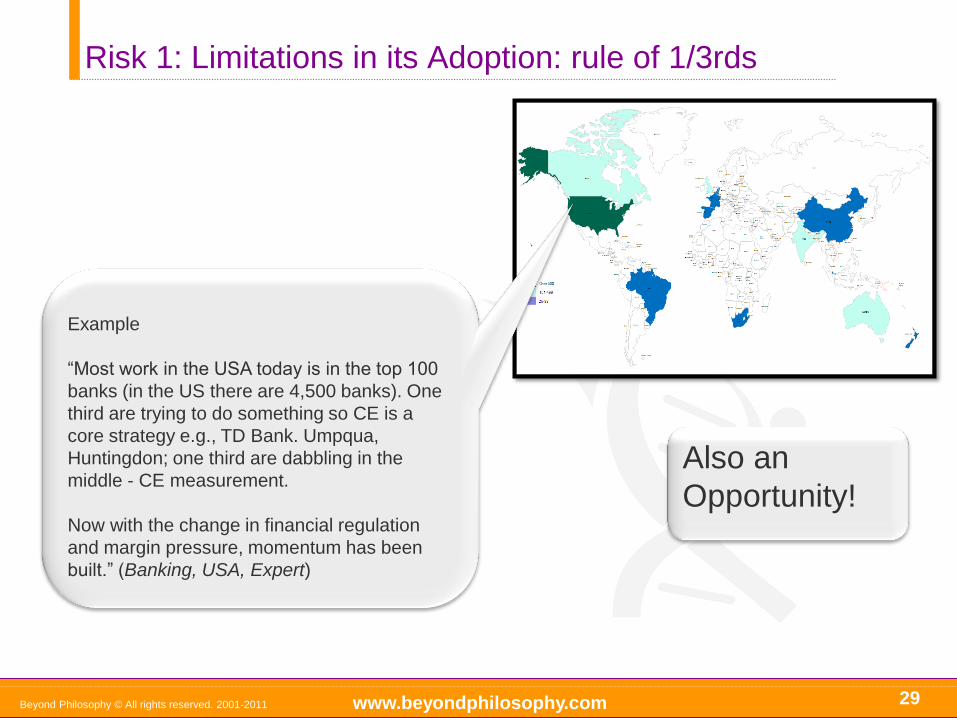

Risk 1: Limitations in its Adoption: rule of 1/3rds

29

Example

“Most work in the USA today is in the top 100

banks (in the US there are 4,500 banks). One

third are trying to do something so CE is a

core strategy e.g., TD Bank. Umpqua,

Huntingdon; one third are dabbling in the

middle - CE measurement.

Now with the change in financial regulation

and margin pressure, momentum has been

built.” (Banking, USA, Expert)

Beyond Philosophy © All rights reserved. 2001-2011

Also an

Opportunity!

www.beyondphilosophy.com

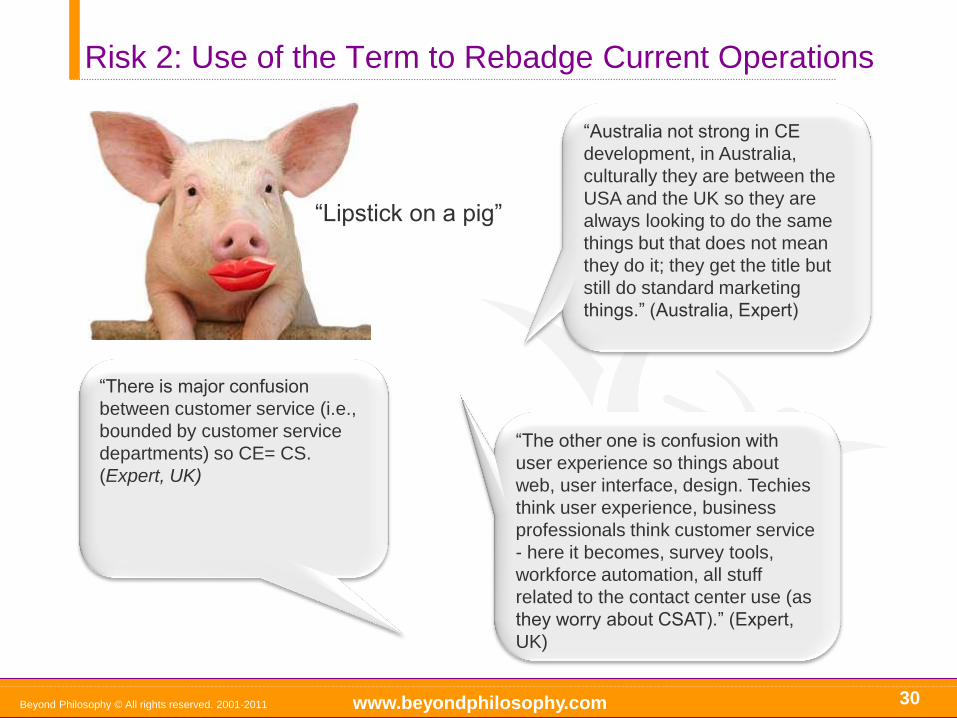

Risk 2: Use of the Term to Rebadge Current Operations

30

“There is major confusion

between customer service (i.e.,

bounded by customer service

departments) so CE= CS.

(Expert, UK)

“Australia not strong in CE

development, in Australia,

culturally they are between the

USA and the UK so they are

always looking to do the same

things but that does not mean

they do it; they get the title but

still do standard marketing

things.” (Australia, Expert)

“The other one is confusion with

user experience so things about

web, user interface, design. Techies

think user experience, business

professionals think customer service

- here it becomes, survey tools,

workforce automation, all stuff

related to the contact center use (as

they worry about CSAT).” (Expert,

UK)

Beyond Philosophy © All rights reserved. 2001-2011

“Lipstick on a pig”

www.beyondphilosophy.com

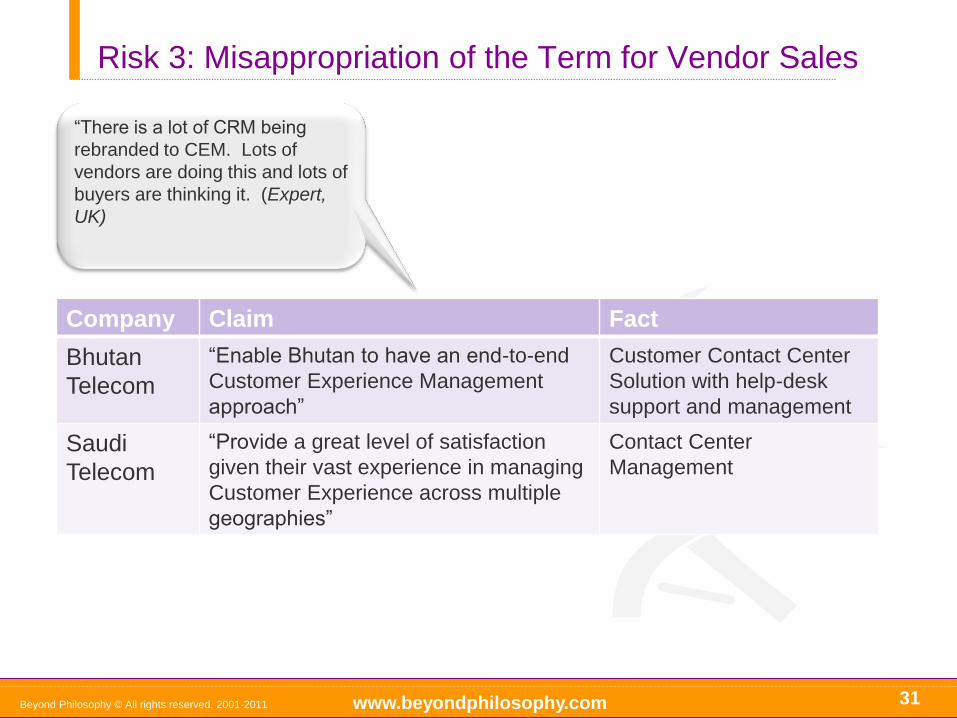

Risk 3: Misappropriation of the Term for Vendor Sales

31

“There is a lot of CRM being

rebranded to CEM. Lots of

vendors are doing this and lots of

buyers are thinking it. (Expert,

UK)

Beyond Philosophy © All rights reserved. 2001-2011

Company Claim Fact

Bhutan

Telecom

“Enable Bhutan to have an end-to-end

Customer Experience Management

approach”

Customer Contact Center

Solution with help-desk

support and management

Saudi

Telecom

“Provide a great level of satisfaction

given their vast experience in managing

Customer Experience across multiple

geographies”

Contact Center

Management

www.beyondphilosophy.com

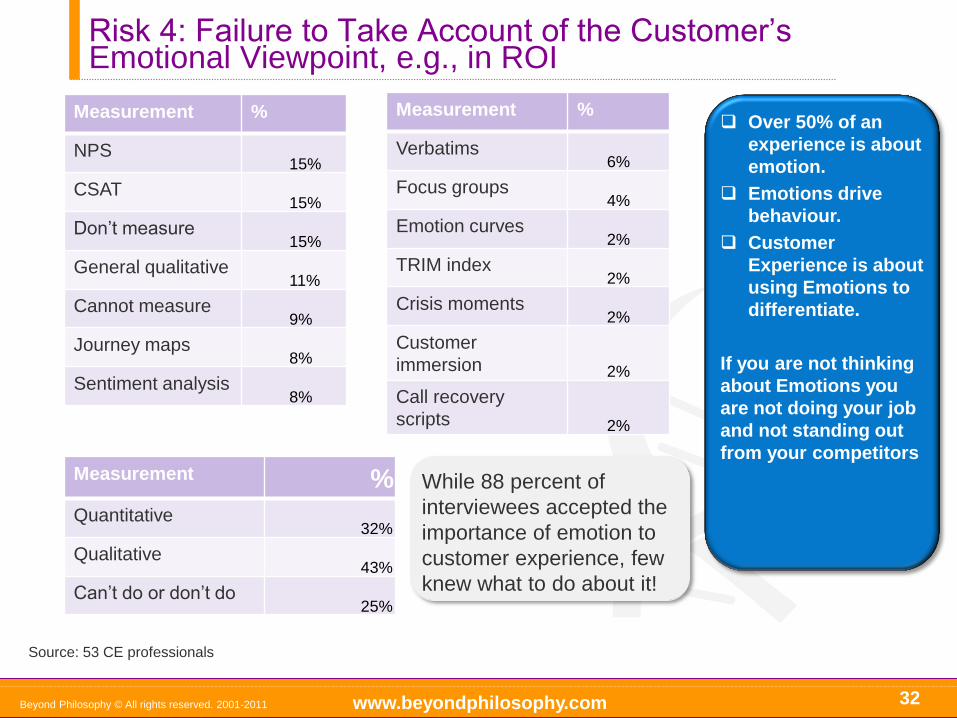

Risk 4: Failure to Take Account of the Customer’s Emotional Viewpoint, e.g., in ROI

32 Beyond Philosophy © All rights reserved. 2001-2011

While 88 percent of

interviewees accepted the

importance of emotion to

customer experience, few

knew what to do about it!

Measurement %

NPS 15%

CSAT 15%

Don’t measure 15%

General qualitative 11%

Cannot measure 9%

Journey maps 8%

Sentiment analysis 8%

Measurement %

Quantitative 32%

Qualitative 43%

Can’t do or don’t do 25%

Measurement %

Verbatims 6%

Focus groups 4%

Emotion curves 2%

TRIM index 2%

Crisis moments 2%

Customer

immersion 2%

Call recovery

scripts 2%

Source: 53 CE professionals

Over 50% of an

experience is about

emotion.

Emotions drive

behaviour.

Customer

Experience is about

using Emotions to

differentiate.

If you are not thinking

about Emotions you

are not doing your job

and not standing out

from your competitors

www.beyondphilosophy.com

Risk 5: Length of Time Required to Execute

33

“The change occurred over a 6-7

year time period. Driven by the

Chairman” (Motor, UK, CxO)

“Sprint is currently in a 3-4 year

turnaround period. It takes 5 years

to go from awful to ok then another

5 years from good to great – the

problem is companies are usually hit

by a recession in that time and

scrap it, short-termism does them

in.” (Expert, UK)

Beyond Philosophy © All rights reserved. 2001-2011

Are you fit for purpose over the

long run or just adding more

functionality?

www.beyondphilosophy.com

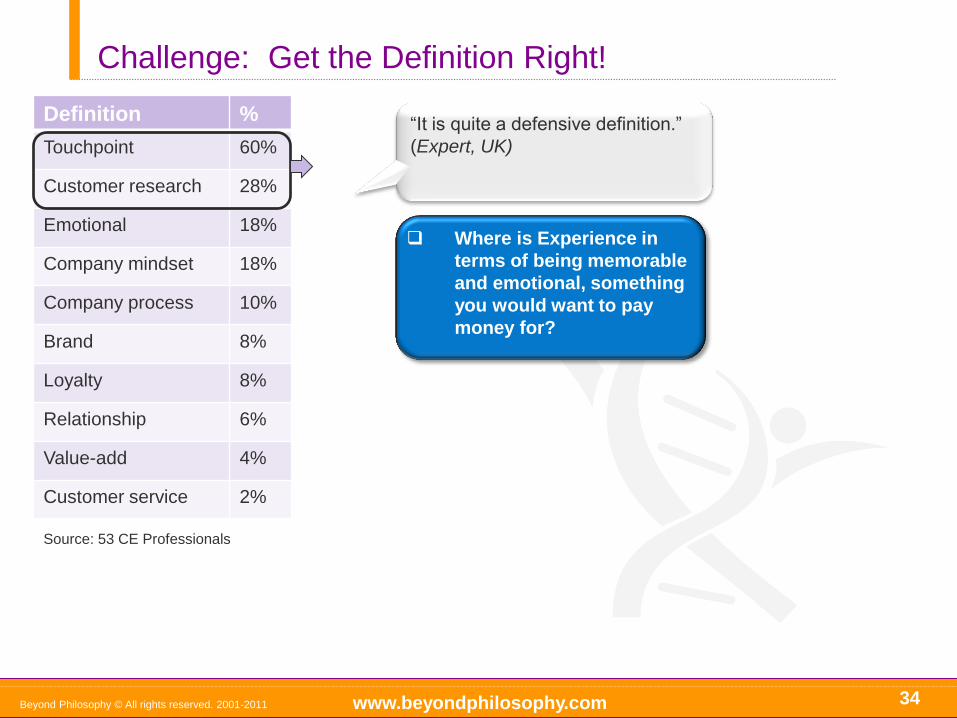

Challenge: Get the Definition Right!

34 Beyond Philosophy © All rights reserved. 2001-2011

Definition %

Touchpoint 60%

Customer research 28%

Emotional 18%

Company mindset 18%

Company process 10%

Brand 8%

Loyalty 8%

Relationship 6%

Value-add 4%

Customer service 2%

Source: 53 CE Professionals

“It is quite a defensive definition.”

(Expert, UK)

Where is Experience in

terms of being memorable

and emotional, something

you would want to pay

money for?

www.beyondphilosophy.com

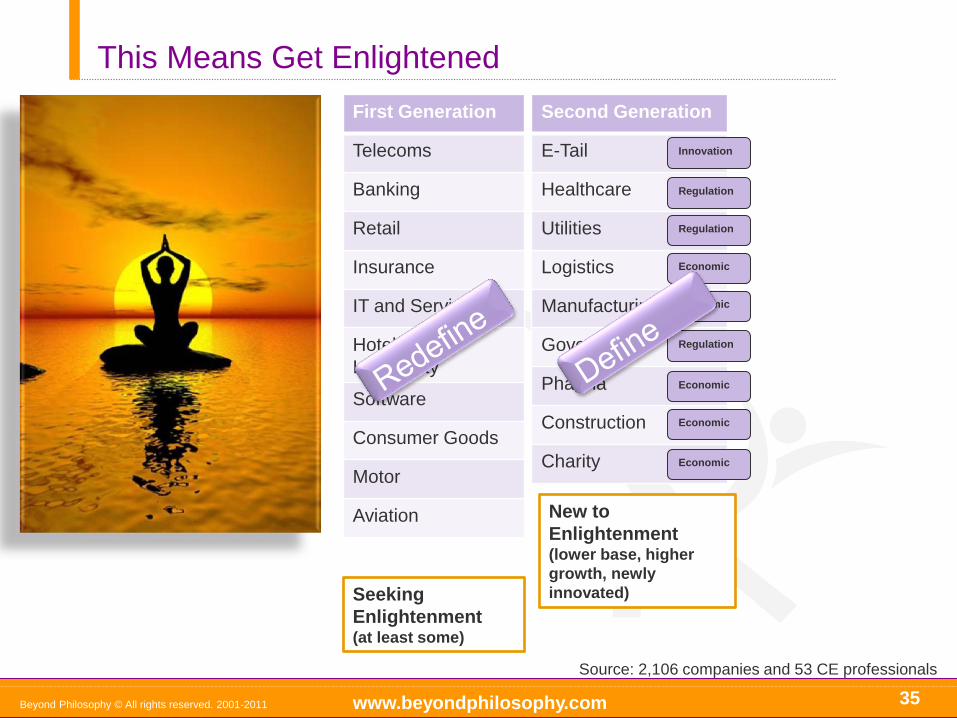

This Means Get Enlightened

35 Beyond Philosophy © All rights reserved. 2001-2011

First Generation

Telecoms

Banking

Retail

Insurance

IT and Services

Hotel and

Hospitality

Software

Consumer Goods

Motor

Aviation

Second Generation

E-Tail

Healthcare

Utilities

Logistics

Manufacturing

Government

Pharma

Construction

Charity

Seeking

Enlightenment (at least some)

New to

Enlightenment (lower base, higher

growth, newly

innovated)

Innovation

Regulation

Regulation

Economic

Economic

Regulation

Economic

Economic

Economic

Source: 2,106 companies and 53 CE professionals

www.beyondphilosophy.com

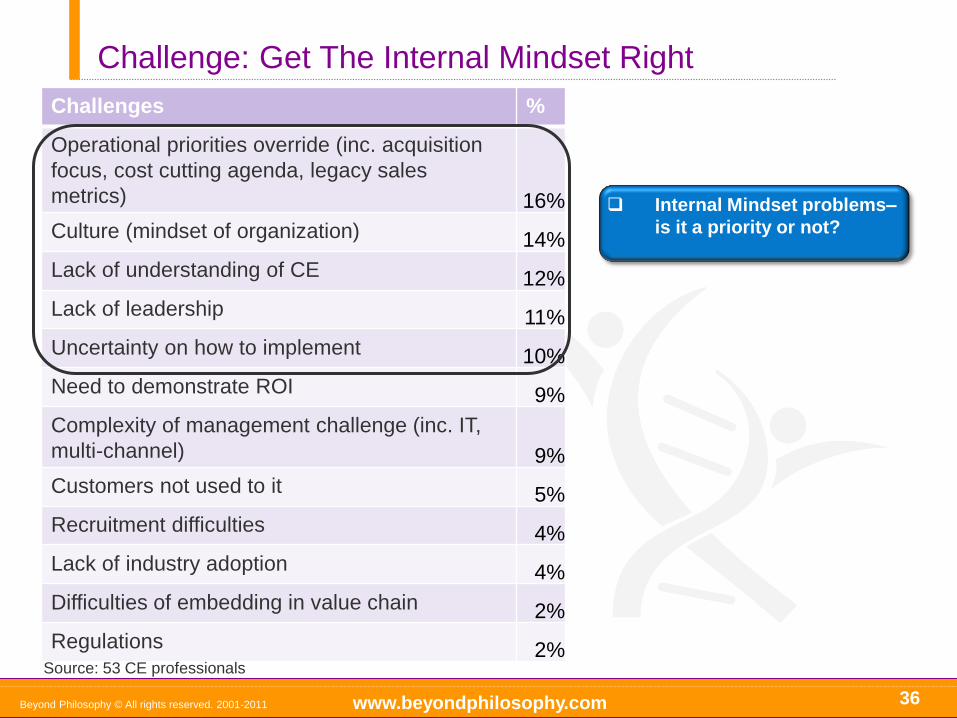

Challenge: Get The Internal Mindset Right

36 Beyond Philosophy © All rights reserved. 2001-2011

Challenges %

Operational priorities override (inc. acquisition

focus, cost cutting agenda, legacy sales

metrics) 16%

Culture (mindset of organization) 14%

Lack of understanding of CE 12%

Lack of leadership 11%

Uncertainty on how to implement 10%

Need to demonstrate ROI 9%

Complexity of management challenge (inc. IT,

multi-channel) 9%

Customers not used to it 5%

Recruitment difficulties 4%

Lack of industry adoption 4%

Difficulties of embedding in value chain 2%

Regulations 2% Source: 53 CE professionals

Internal Mindset problems–

is it a priority or not?

www.beyondphilosophy.com

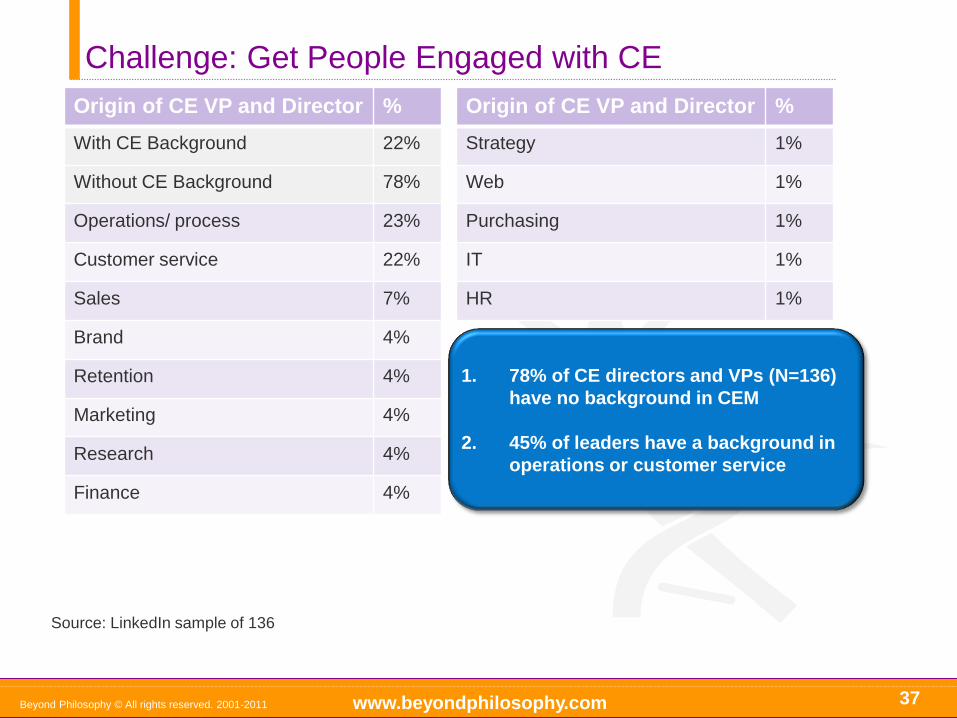

Challenge: Get People Engaged with CE

37

1. 78% of CE directors and VPs (N=136)

have no background in CEM

2. 45% of leaders have a background in

operations or customer service

Beyond Philosophy © All rights reserved. 2001-2011

Origin of CE VP and Director %

With CE Background 22%

Without CE Background 78%

Operations/ process 23%

Customer service 22%

Sales 7%

Brand 4%

Retention 4%

Marketing 4%

Research 4%

Finance 4%

Origin of CE VP and Director %

Strategy 1%

Web 1%

Purchasing 1%

IT 1%

HR 1%

Source: LinkedIn sample of 136

www.beyondphilosophy.com 38 Beyond Philosophy © All rights reserved. 2001-2011

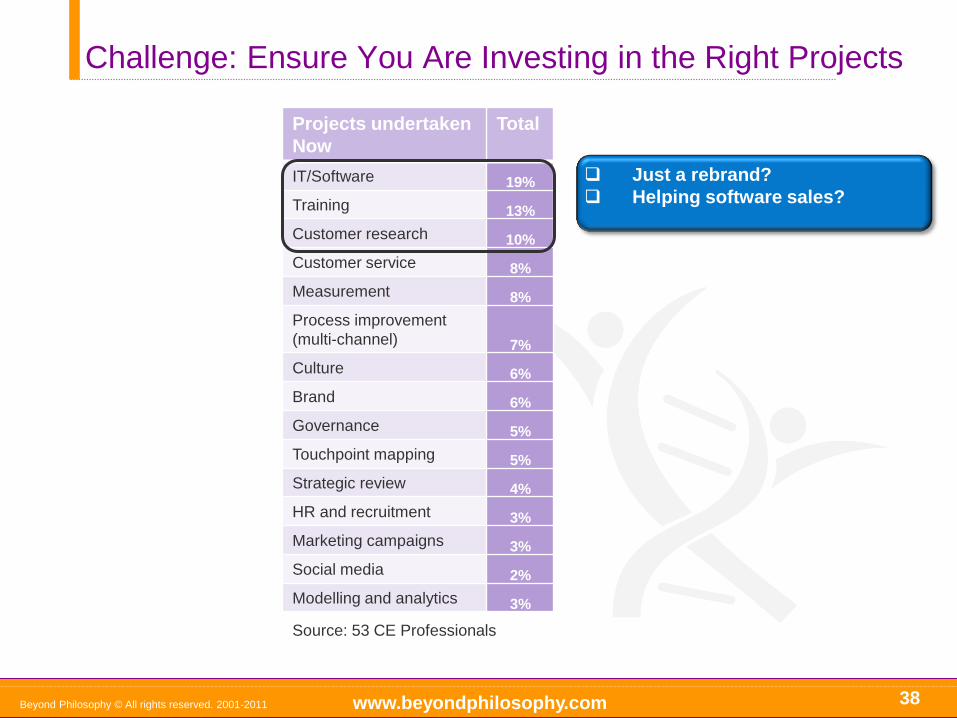

Projects undertaken

Now

Total

IT/Software 19%

Training 13%

Customer research 10%

Customer service 8%

Measurement 8%

Process improvement

(multi-channel) 7%

Culture 6%

Brand 6%

Governance 5%

Touchpoint mapping 5%

Strategic review 4%

HR and recruitment 3%

Marketing campaigns 3%

Social media 2%

Modelling and analytics 3%

Source: 53 CE Professionals

Challenge: Ensure You Are Investing in the Right Projects

Just a rebrand?

Helping software sales?

www.beyondphilosophy.com

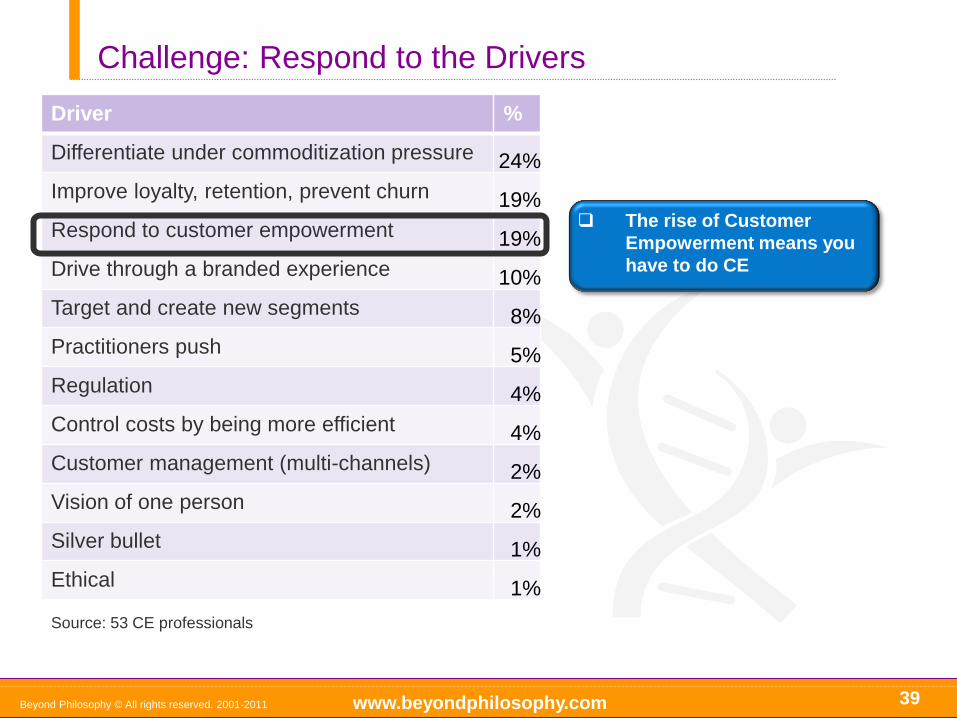

Challenge: Respond to the Drivers

39 Beyond Philosophy © All rights reserved. 2001-2011

Driver %

Differentiate under commoditization pressure 24%

Improve loyalty, retention, prevent churn 19%

Respond to customer empowerment 19%

Drive through a branded experience 10%

Target and create new segments 8%

Practitioners push 5%

Regulation 4%

Control costs by being more efficient 4%

Customer management (multi-channels) 2%

Vision of one person 2%

Silver bullet 1%

Ethical 1%

Source: 53 CE professionals

The rise of Customer

Empowerment means you

have to do CE

www.beyondphilosophy.com

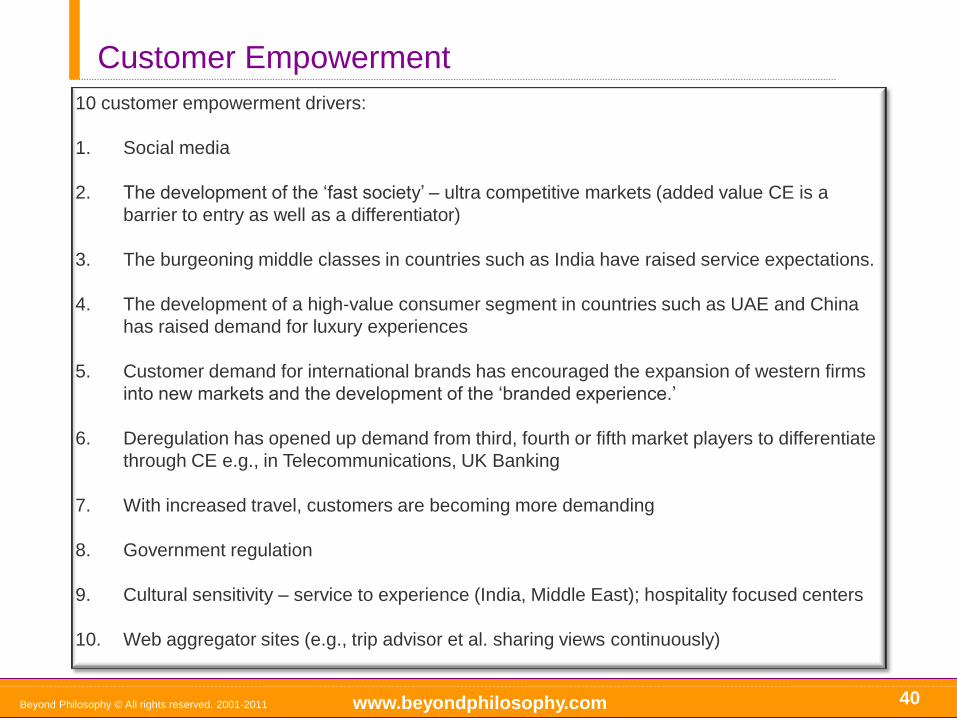

40

10 customer empowerment drivers:

1. Social media

2. The development of the ‘fast society’ – ultra competitive markets (added value CE is a

barrier to entry as well as a differentiator)

3. The burgeoning middle classes in countries such as India have raised service expectations.

4. The development of a high-value consumer segment in countries such as UAE and China

has raised demand for luxury experiences

5. Customer demand for international brands has encouraged the expansion of western firms

into new markets and the development of the ‘branded experience.’

6. Deregulation has opened up demand from third, fourth or fifth market players to differentiate

through CE e.g., in Telecommunications, UK Banking

7. With increased travel, customers are becoming more demanding

8. Government regulation

9. Cultural sensitivity – service to experience (India, Middle East); hospitality focused centers

10. Web aggregator sites (e.g., trip advisor et al. sharing views continuously)

Customer Empowerment

Beyond Philosophy © All rights reserved. 2001-2011

www.beyondphilosophy.com

Internationalization of Leadership and Customers Through Contact

41 Beyond Philosophy © All rights reserved. 2001-2011

www.beyondphilosophy.com

WHAT YOU NEED TO DO What Will be the Next Great Customer Experience Advancement?

42 Beyond Philosophy © All rights reserved. 2001-2011

www.beyondphilosophy.com

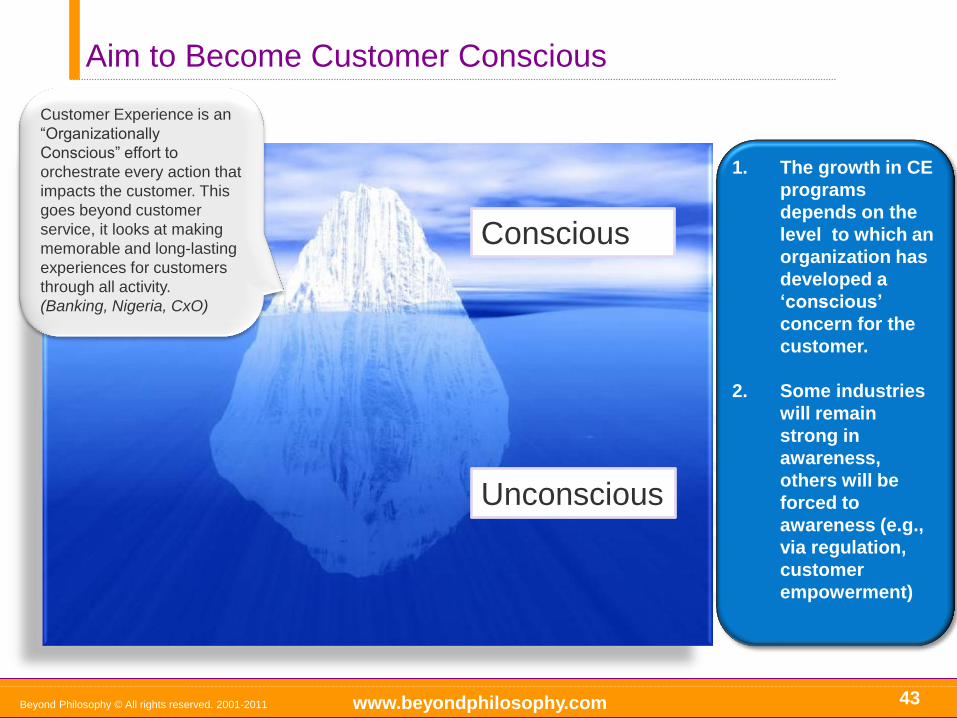

Aim to Become Customer Conscious

43

Unconscious

Conscious

1. The growth in CE

programs

depends on the

level to which an

organization has

developed a

‘conscious’

concern for the

customer.

2. Some industries

will remain

strong in

awareness,

others will be

forced to

awareness (e.g.,

via regulation,

customer

empowerment)

Customer Experience is an

“Organizationally

Conscious” effort to

orchestrate every action that

impacts the customer. This

goes beyond customer

service, it looks at making

memorable and long-lasting

experiences for customers

through all activity.

(Banking, Nigeria, CxO)

Beyond Philosophy © All rights reserved. 2001-2011

www.beyondphilosophy.com

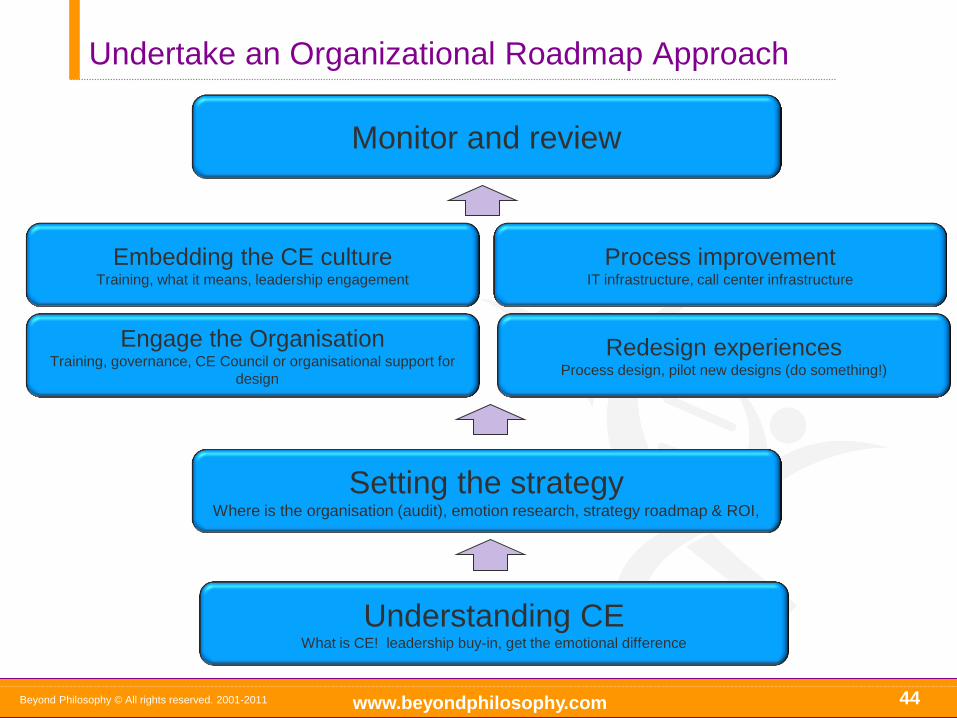

Undertake an Organizational Roadmap Approach

44

Beyond Philosophy © All rights reserved. 2001-2011

Setting the strategy Where is the organisation (audit), emotion research, strategy roadmap & ROI,

Embedding the CE culture Training, what it means, leadership engagement

Process improvement IT infrastructure, call center infrastructure

Engage the Organisation Training, governance, CE Council or organisational support for

design

Understanding CE What is CE! leadership buy-in, get the emotional difference

Redesign experiences Process design, pilot new designs (do something!)

Monitor and review

44

www.beyondphilosophy.com

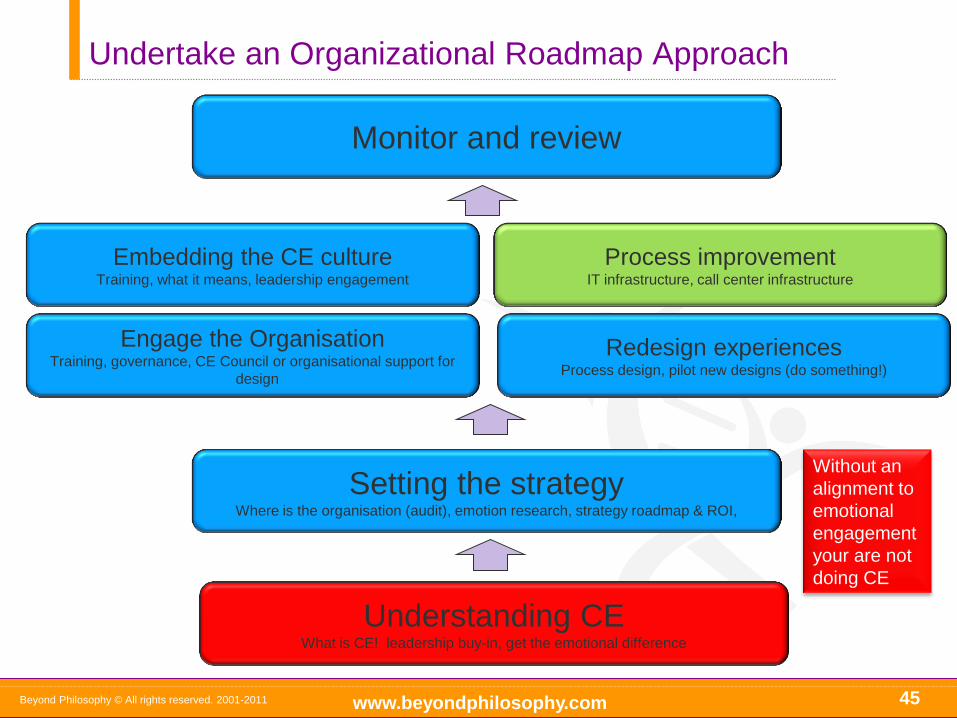

Undertake an Organizational Roadmap Approach

45

Beyond Philosophy © All rights reserved. 2001-2011

Setting the strategy Where is the organisation (audit), emotion research, strategy roadmap & ROI,

Embedding the CE culture Training, what it means, leadership engagement

Process improvement IT infrastructure, call center infrastructure

Engage the Organisation Training, governance, CE Council or organisational support for

design

Understanding CE What is CE! leadership buy-in, get the emotional difference

Redesign experiences Process design, pilot new designs (do something!)

Monitor and review

Without an

alignment to

emotional

engagement

your are not

doing CE

45

www.beyondphilosophy.com

Undertake an Organizational Roadmap Approach

46

Beyond Philosophy © All rights reserved. 2001-2011

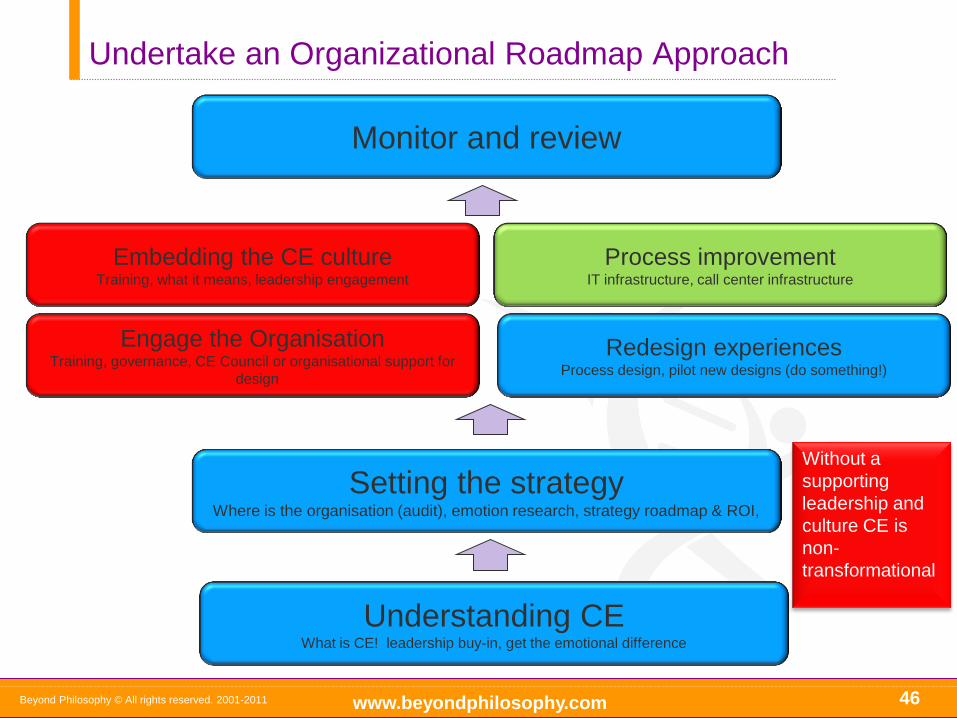

Setting the strategy Where is the organisation (audit), emotion research, strategy roadmap & ROI,

Embedding the CE culture Training, what it means, leadership engagement

Process improvement IT infrastructure, call center infrastructure

Engage the Organisation Training, governance, CE Council or organisational support for

design

Understanding CE What is CE! leadership buy-in, get the emotional difference

Redesign experiences Process design, pilot new designs (do something!)

Monitor and review

Without a

supporting

leadership and

culture CE is

non-

transformational

46

www.beyondphilosophy.com

Undertake an Organizational Roadmap Approach

47

Beyond Philosophy © All rights reserved. 2001-2011

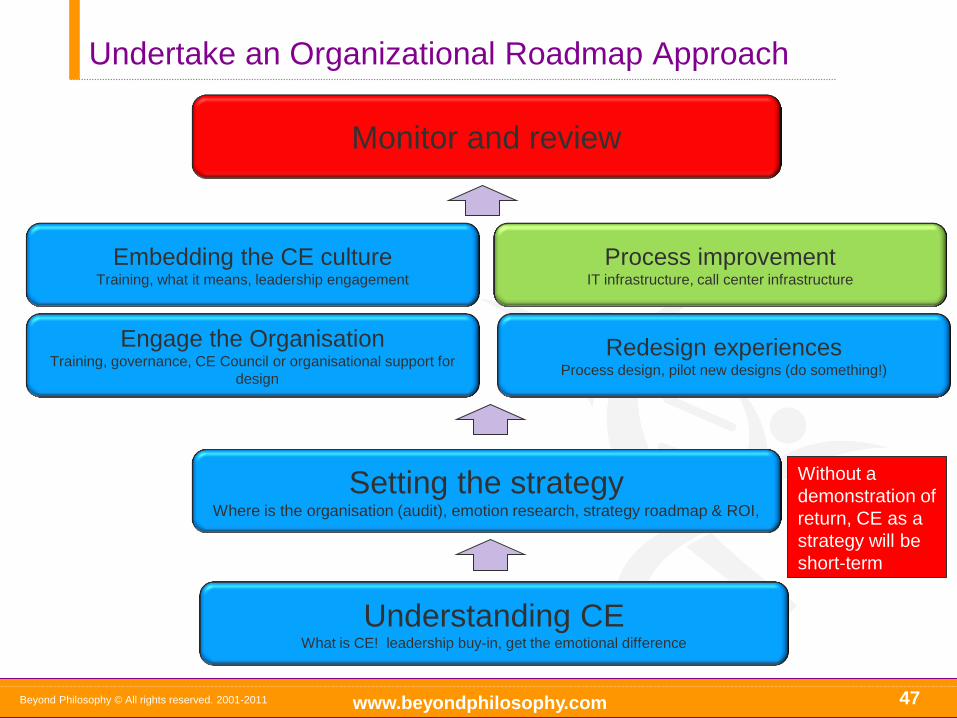

Setting the strategy Where is the organisation (audit), emotion research, strategy roadmap & ROI,

Embedding the CE culture Training, what it means, leadership engagement

Process improvement IT infrastructure, call center infrastructure

Engage the Organisation Training, governance, CE Council or organisational support for

design

Understanding CE What is CE! leadership buy-in, get the emotional difference

Redesign experiences Process design, pilot new designs (do something!)

Monitor and review

Without a

demonstration of

return, CE as a

strategy will be

short-term

47

www.beyondphilosophy.com 48 Beyond Philosophy © All rights reserved. 2001-2011

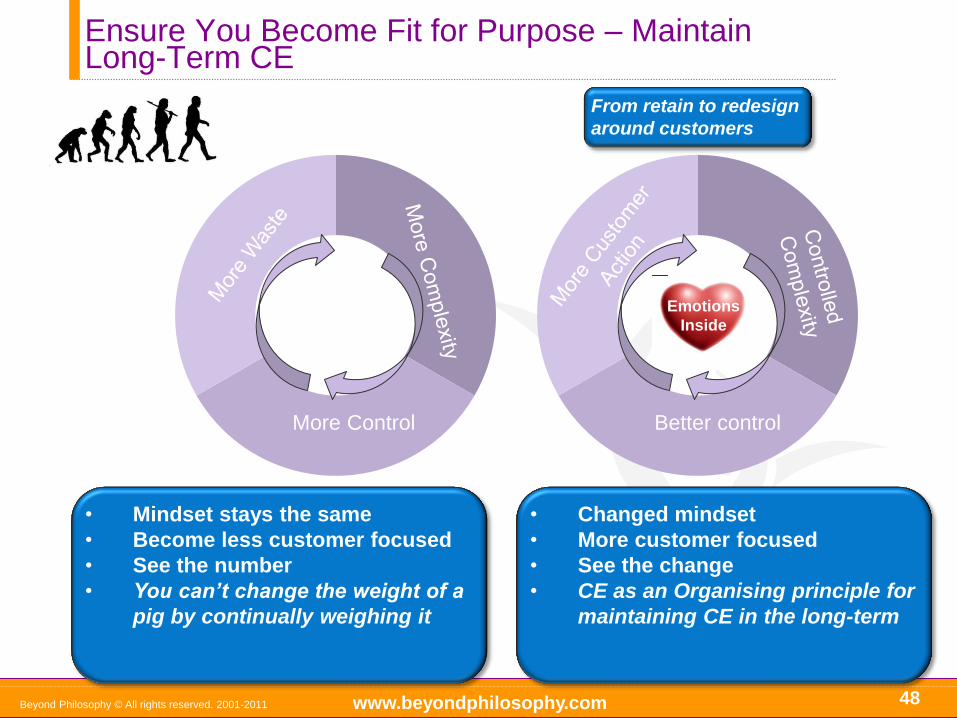

Ensure You Become Fit for Purpose – Maintain Long-Term CE

More Control

• Mindset stays the same

• Become less customer focused

• See the number

• You can’t change the weight of a

pig by continually weighing it

• Changed mindset

• More customer focused

• See the change

• CE as an Organising principle for

maintaining CE in the long-term

Better control

From retain to redesign

around customers

Emotions

Inside

www.beyondphilosophy.com

7 Strategic Questions

49

1. What is the Customer Experience

you are trying to deliver?

2. What are the emotions you are trying

to evoke?

3. What is your subconscious

experience telling Customers?

4. Is your Customer Experience

deliberate?

5. What do your Customers really want?

6. What provides you with the most

value?

7. How Customer centric is your

organisation?

Beyond Philosophy © All rights reserved. 2001-2011

www.beyondphilosophy.com

Thank You

Steven Walden

Senior Head of Research and Consulting

Beyond Philosophy

Email: [email protected]

Colin Shaw

CEO and Founder

Beyond Philosophy

Email: [email protected]

50 Beyond Philosophy © All rights reserved. 2001-2011

@Steven_Walden

We invite you to continue the conversation.

http://www.linkedin.com/pub/steven-walden/2/ba5/1ba

@ColinShaw_CX

http://www.linkedin.com/in/colinrjshaw

US Office: +1 770 206 5280

UK Office: +44 (0) 207 917 1717