Embed Size (px)

Citation preview

Global Credit Cards Report 2020: Everything with a single swipe –understanding global credit card trends

For questions and enquiries, please contact:Michael Le Lion: [email protected]

September 2020

2www.rfigroup.com Copyright Retail Finance Intelligence Limited Commercial in Confidence

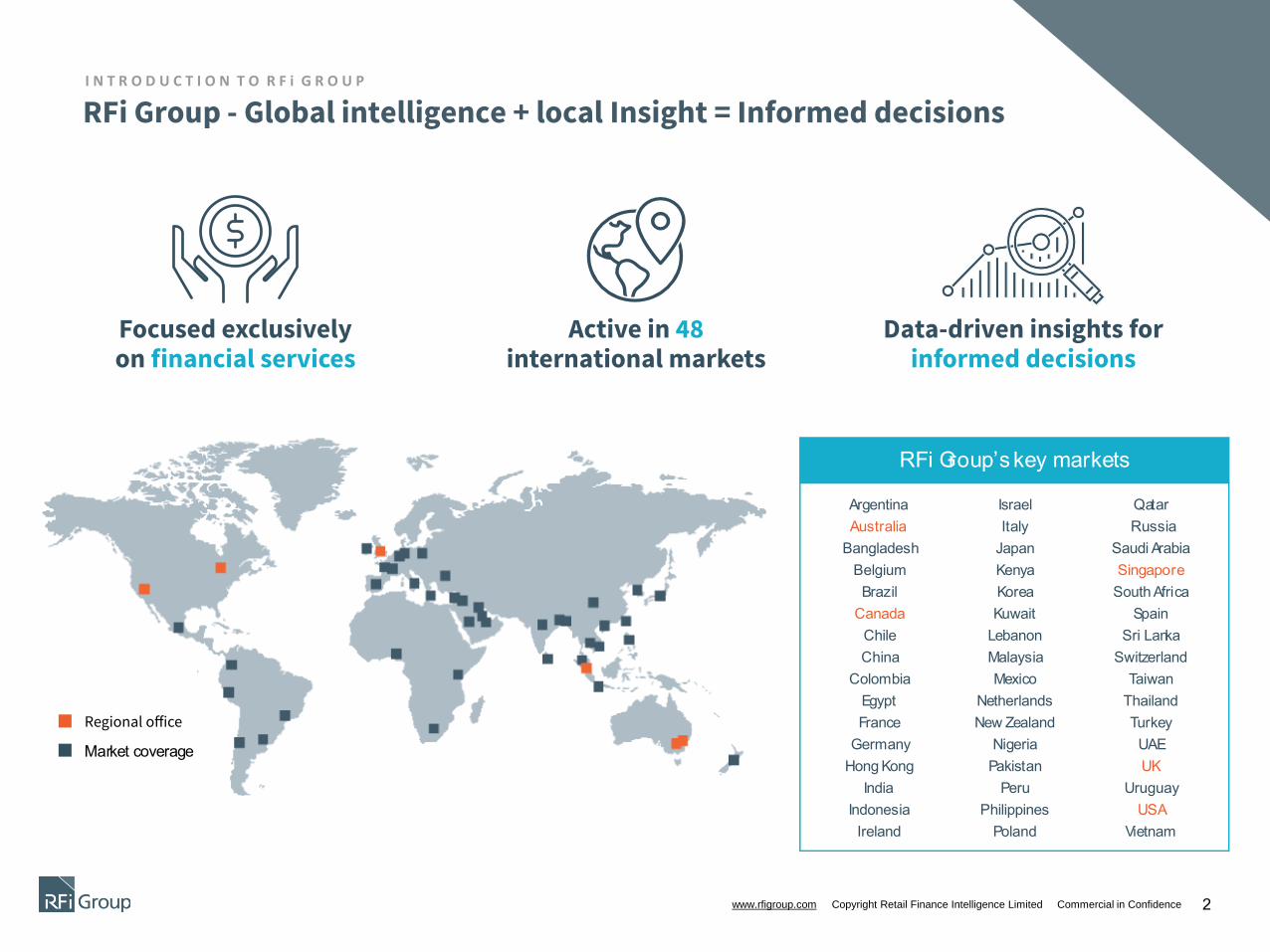

I N T R O D U C T I O N T O R F i G R O U P

RFi Group - Global intelligence + local Insight = Informed decisions

3www.rfigroup.com Copyright Retail Finance Intelligence Limited Commercial in Confidence

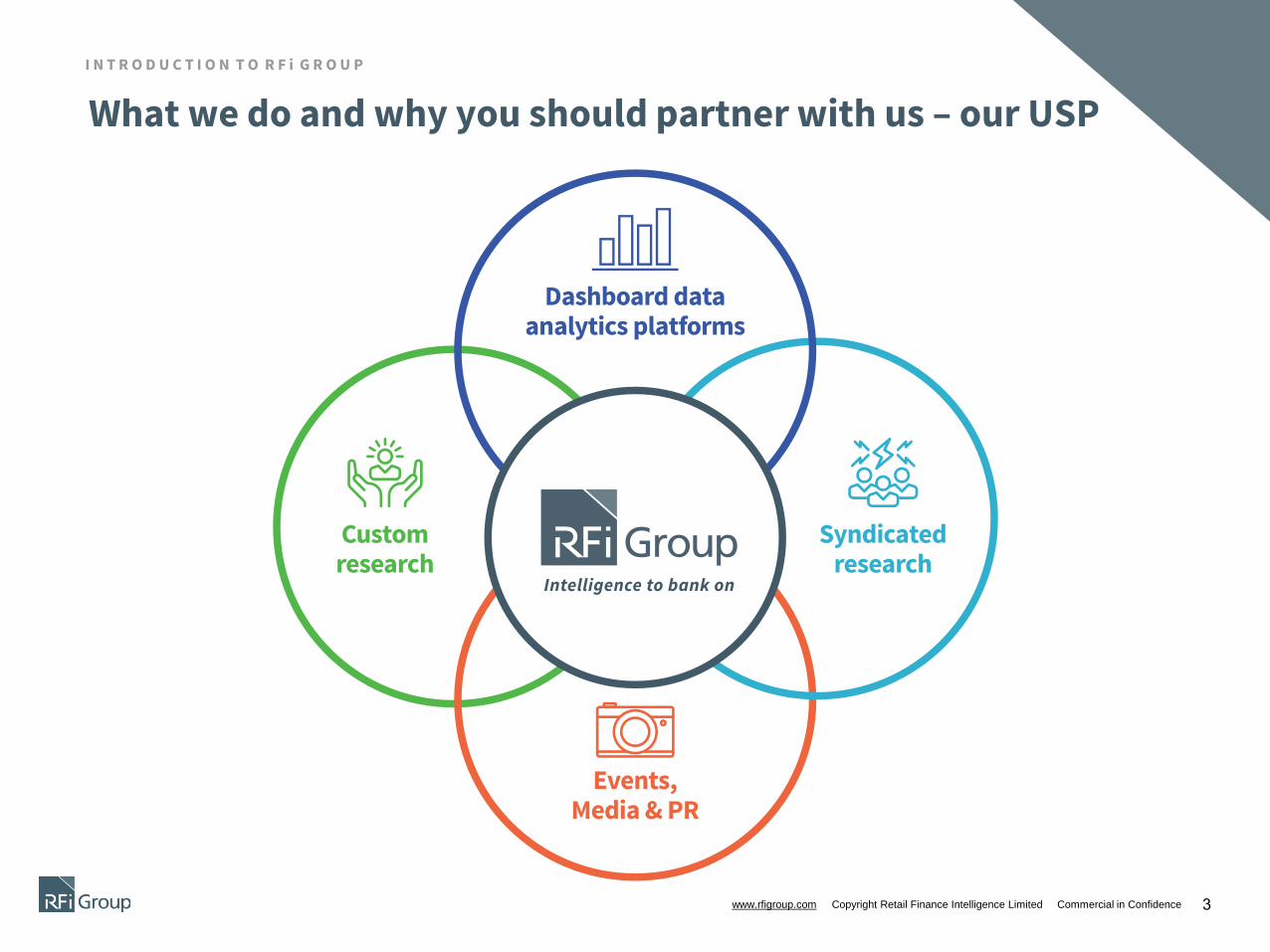

I N T R O D U C T I O N T O R F i G R O U P

What we do and why you should partner with us – our USP

4www.rfigroup.com Copyright Retail Finance Intelligence Pty Limited Commercial in Confidence

Selected RFi Group clients

I N T R O D U C T I O N T O R F i G R O U P

R F I G R O U P – G L O B A L C R E D I T C A R D S P R O G R A M M E

5

www.rfigroup.com Copyright Retail Finance Intelligence Pty Limited Commercial in Confidence

R F I G R O U P – G L O B A L C R E D I T C A R D S R E P O R T

1. Research Methodology

2. Focus area one: Credit cards

▪ Usage of credit cards

▪ Barriers to credit cards

▪ Driving frequent card usage

▪ Future intentions

3. Focus area two: Contactless cards and mobile wallets

▪ Usage of contactless cards

▪ Appeal of mobile wallets

▪ Mobile wallet preferences

4. Conclusion

▪ Key Insights

▪ Opportunities

Contents

R F I G R O U P – G L O B A L C R E D I T C A R D S P R O G R A M M E

6

www.rfigroup.com Copyright Retail Finance Intelligence Pty Limited Commercial in Confidence

R F I G R O U P – G L O B A L C R E D I T C A R D S R E P O R T

• The data used in this presentation is sourced from surveys conducted by RFi Group across 15 markets

during 2019.

• In all markets, except for Egypt and the UAE, over 2,000 consumers were interviewed online. In Egypt and

the UAE, 1,000 respondents were interviewed face-to-face.

• RFi Group market surveys interview the banked population in each market. To qualify as ‘banked’

respondents must hold a minimum of one banking product with a financial institution in their local market.

• The survey is nationally representative of each market, and quotas were applied to ensure respondents

representative of each market’s population by age, gender, region and income.

Methodology

7

Credit Cards

• Usage of credit cards

• Barriers to credit cards

• Driving frequent card usage

• Future intentions

R F I G R O U P – G L O B A L C R E D I T C A R D S P R O G R A M M E

8

www.rfigroup.com Copyright Retail Finance Intelligence Pty Limited Commercial in Confidence

R F I G R O U P – G L O B A L C R E D I T C A R D S R E P O R T

Which of the following financial products do you hold?Credit cards

62%

83%

64% 65%67%

83%

52%

44%

50%

72%75%

81%

71%

61%

71%67%

Australia Canada China Egypt France Hong

Kong

India Indonesia Malaysia Mexico Singapore Taiwan UAE UK US Global

Average

18H1 18H2 19H1

Source: RFi Group survey of 17,000 consumers across 15 different markets

Credit cards are most popular in Canada, Hong Kong and Taiwan.

Where are credit cards seeing the greatest popularity?

R F I G R O U P – G L O B A L C R E D I T C A R D S P R O G R A M M E

9

www.rfigroup.com Copyright Retail Finance Intelligence Pty Limited Commercial in Confidence

R F I G R O U P – G L O B A L C R E D I T C A R D S R E P O R T

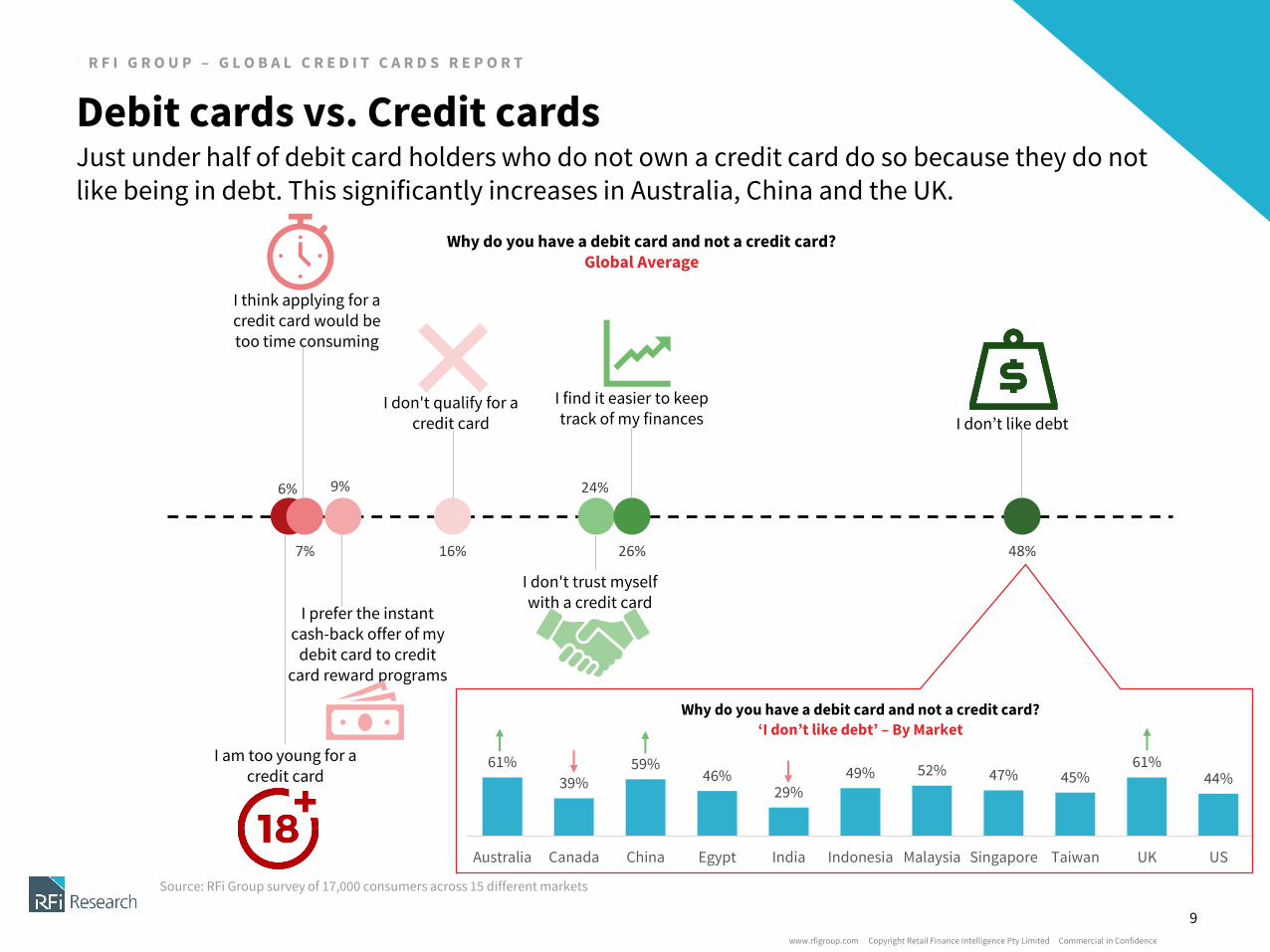

48%

9%

16%

6% 24%

26%7%

I don't trust myself with a credit card

I don’t like debt

I find it easier to keep track of my finances

I don't qualify for a credit card

I prefer the instant cash-back offer of my

debit card to credit card reward programs

I think applying for a credit card would be too time consuming

I am too young for a credit card

Why do you have a debit card and not a credit card?Global Average

61%

39%59%

46%29%

49% 52% 47% 45%61%

44%

Australia Canada China Egypt India Indonesia Malaysia Singapore Taiwan UK US

Why do you have a debit card and not a credit card?

‘I don’t like debt’ – By Market

Source: RFi Group survey of 17,000 consumers across 15 different markets

Just under half of debit card holders who do not own a credit card do so because they do not like being in debt. This significantly increases in Australia, China and the UK.

Debit cards vs. Credit cards

10

Contactless cards and mobile wallets

• Usage of contactless cards

• Appeal of mobile wallets

• Mobile wallet preferences

R F I G R O U P – G L O B A L C R E D I T C A R D S P R O G R A M M E

11

www.rfigroup.com Copyright Retail Finance Intelligence Pty Limited Commercial in Confidence

R F I G R O U P – G L O B A L C R E D I T C A R D S R E P O R T

19% 20%

61%

15%

24%

62% 63%

24%21%

26%

33%

Australia Canada China France Hong Kong India Mexico Singapore UK US Global Average

2016 2017 2018 2019

% of consumers who consider mobile wallets highly appealing (8+/10)

Source: RFi Group survey of 17,000 consumers across 15 different markets

Appeal of mobile wallets has picked up after a decrease in 2018, although their popularity remains strongest in emerging markets, where contactless is less prevalent.

Appeal of mobile wallets

12

Intelligence to bank on

R F I G R O U P – G L O B A L C R E D I T C A R D S P R O G R A M M E

13

www.rfigroup.com Copyright Retail Finance Intelligence Pty Limited Commercial in Confidence

Legal notice and disclaimer

- This presentation has been prepared by Retail Finance Intelligence Pty Limited ACN 121 015 192 and its associated entities worldwide (“RFi Group”) and is provided to you for the purposes set out in the agreement signed by you relating to this presentation.- All information contained in this presentation (including this notice) (“Information”) is confidential. By receiving the Information you are deemed to agree that you will hold the Information in strict confidence and keep it secret, and not reproduce, disclose or distribute the Information to any third party or publish the Information for any purpose. The obligations imposed upon you by this document are in addition to the obligations imposed upon you under any non-disclosure agreement or other agreement signed by you relating to the Information. You agree not to modify or alter the information in any way. If you are not the intended recipient you must not use or disclose the information in this research in any way. If you received it in error, please tell us immediately by return e-mail and delete the document. We do not guarantee the integrity of any e-mails or attached files and are not responsible for any changes made to them by any other person.- This Information shall not form the basis of any contract or commitment. No action should be taken on the basis of, or in reliance on, this presentation.- Except as required by law, no representation or warranty, express or implied, is made as to the fairness, accuracy, completeness or correctness of the Information, opinions and conclusions, or as to the reasonableness of any assumption contained in this presentation. By receiving this presentation and to the extent permitted by law, you release RFi Group and its officers, employees, agents and associates from any liability (including, without limitation, in respect of direct, indirect or consequential loss or damage or loss or damage arising by negligence) arising as a result of the reliance by you or any other person on anything contained in or omitted from this presentation.- Any forward looking statements included in this presentation involve subjective judgment and analysis and are subject to significant uncertainties, risks and contingencies, many of which are outside the control of, and are unknown to, RFi Group or its officers, employees, agents or associates. Actual future events may vary materially from any forward looking statements and the assumptions on which those statements are based. Given these uncertainties, you are cautioned to not place undue reliance on any such forward looking statements.- Unless otherwise specified in any agreement to which this presentation relates, no responsibility is accepted by RFi Group or any of its officers, employees, agents or associates, nor any other person, for any of the information or for any action taken by you on the basis of the Information.- RFi Group is not licenced to, has not and does not provide any financial advice or deal with any financial products or securities in the process of assisting in the compilation of this Information. This Information does not constitute investment, legal, taxation, financial product or other advice and the presentation does not take into account your investment objectives, financial situation or particular needs. You are responsible for forming your own opinions and conclusions on such matters and should make your own independent assessment of the information and seek independent professional advice in relation to the Information and any action taken on the basis of the Information. RFi Group does not make, adopt or endorse any recommendation in this document.- Unless otherwise specified in any agreement to which this presentation relates, The “Intellectual Property Rights” (meaning any and all patents, rights in inventions, trade marks, service marks, copyrights and related rights, database rights, moral rights, rights in designs, know-how and all or any other intellectual or industrial property rights whether or not registered or capable of registration in any part of the world together with all or any goodwill relating to them) in this presentation and those created by the creation of this presentation and any services to which this presentation relates, shall belong to RFi Group.

14

Contact Us

Global Intelligence, Local Insight

RFi ASIA109 North Bridge Rd,#05-21,Singapore 179097

Telephone +65 6597 [email protected]

RFi AUSTRALIA & NEW ZEALANDLevel 16175 Pitt StreetSydney NSW 2000Australia

Telephone +61 2 9159 [email protected]

RFi CANADA145 King Street WestSuite 1710Toronto, OntarioM5H 1J8

Telephone +1 416 644 [email protected]

RFi EMEAMinster Building,7th Floor, 21 Mincing Lane,London, EC3R 7AGUnited Kingdom

Telephone +44 203 862 [email protected]

![Credit cards[1]](https://img.pdfslide.us/doc/110x75/5551b7f1b4c905ca7f8b4b8d/credit-cards1.jpg)