Embed Size (px)

Citation preview

Global Banking &Capital MarketsKey themes from the 2Q 2017 earnings callsAugust 2017

Table of contents

Revenues grow in the US, reflecting the benefit of higher short-term interest rates.

Differentiated investments in innovation continue amid an ongoing focus on expense discipline.

Lending is not growing at robust rates, but banks are not willing to sacrifice credit quality in exchange for growth.

Management is cautiously optimistic about the outlook, as legacy head winds ease and capital levels improve.

2

5

7

9

Main topics from 2Q 2017 earnings calls

• Financial performance trends in 2Q 2017 were mixed when compared to 2Q 2016. Americas-based banks generally enjoyed revenue growth and improved profitability, as the tailwinds from higher short-term interest rates offset a weak trading environment. In Europe, however, rates remained low, providing no relief for market challenges.

• Only 10 of the 32 banks included in this analysis reported lower expenses from 2Q 2016. Management at a number of banks, primarily in North America, attributed cost growth to higher business volumes. However, investments in business initiatives and innovation also contributed to the increase.

• Return on average equity (ROAE) dropped from 2Q 2016 levels at 13 banks. While outsized provisions for legacy conduct issues have generally receded for the industry, it is notable that three of the four banks with the biggest declines in net income were dogged by legal issues. Profits were also driven lower as a result of reshaping activities, such as stake sales, portfolio divestments and acquisitions.

2Q17 2Q16

-8.9 -6

.7

2.7

2.9

6.1

6.4 6.7

6.8

7.4

7.5

7.8

8.1

8.3

8.39

8.4

8.8

9.0

9.0

9.5

9.8

10.4

11.0

11.4

11.4

11.7

12.4

13.4

15.6

16.7

19.9

25.5

Return on average equity (ROAE), 2Q 2017

Revenues grow in the US, reflecting the benefit of higher short-term interest rates.

Source: SNL Financial *ING data is from company reports

2Key themes from the 2Q 2017 earnings calls |

Percentage change in FICC trading revenue from 2Q 2016 in reported currency, selected banks

Source: Company reports

Revenue trends in 2Q 2017 were disappointing for many banks, particularly in Europe, as market conditions for fixed income trading deteriorated from 1Q 2017 and the low interest rate environment persisted outside of the US. Notably, only two banks in the Americas — Itaú Unibanco and Goldman Sachs — reported lower revenues than in 2Q 2016, while 12 European banks saw their revenues fall. Three of these banks — Barclays, Deutsche Bank and Société Générale — reported a double-digit revenue plunge.

In terms of profitability, 13 of the banks included in this analysis reported a decline in return on average equity (ROAE) in 2Q 2017 when compared with the year-ago quarter. While multiple factors contributed to reduced profitability, the two most notable were increased conduct provisions at a select few banks and the impact of reshaping activities.

• Société Générale increased legal provisions by €300 million following its settlement of a long-running legal battle with the Libyan Investment Authority, while Barclays and Lloyds Banking Group both added to their provisions for payment protection insurance (PPI) claims. Barclays faced a further profit impact from the sell-down of its Africa business.

• Lower returns at several banks, including BBVA, BNP Paribas, Société Générale and U.S. Bancorp, reflected the non-recurrence of gains related to their sales of stakes in Visa Europe in 2Q 2016.

• At American Express, 2Q 2016 ROAE was boosted by one-time gains from the sale of the Costco portfolio, while Citigroup, which acquired that portfolio, incurred higher credit costs associated with its integration in 2Q 2017.

-40%

-19%

-19%

-16%

-15%

-14%

-12%

-11%

-9%

-7%

-6%

-4%

-3%

1%

GS

UBS

JPM

BNP

BARC

BAC

DB

NOM

HSBC

SG

C

MS

RBC

CS

3 | Key themes from the 2Q 2017 earnings calls

Notable and quotable “The revenue environment for us was more challenging. Client activity across many of our businesses remained muted. Extremely low levels of price volatility, notwithstanding the geopolitical backdrop, drove low volumes of trading. … Persistently low interest rates in the Euro area and the sea change in inflation expectations in the US both acted as brakes on our revenue in the quarter.”

John Cryan, CEO Deutsche Bank

“We didn’t navigate the market as well as we aspire to or as well as we have in the past.”

Marty Chavez, CFO Goldman Sachs

-25.

6%-1

5.3%

-10.

4%-9.1

%-7.7

%-7

.7%

-4.1

%-3

.4%

-2.6

%-1

.8%

-1.7

%-0

.9%

-0.6

%-0

.3%

0.0%0.

7%0.

9%1.8%

1.9%

2.0%2.

6%4.

3%4.

5%4.8%

6.6%

6.7%7.

2%8.2%

8.3%9.

2%9.

0%

23.6

%

SGHSBCDB BARC

CBKUCG

BNPCAUBS

INT

ITAUBBVA

ING

GS

WFCAXPUSB

CSC CIBCTDJPM

STANNOM

BKBACLLD

RBCMSSTT

SANTRBS

Percentage change in revenues from 2Q 2016

Source: Company reports, EY analysis

For more information on banks’ strategic priorities, please see EY Global Banking Outlook 2017: uncertainty is no excuse for inaction.

4Key themes from the 2Q 2017 earnings calls |

5 | Key themes from the 2Q 2017 earnings calls

Differentiated investments in innovation continue amid an ongoing focus on expense discipline.

Expense performance in 2Q 2017 was also mixed. Management at a number of banks highlighted their progress in achieving cost targets, however, cost-income ratios deteriorated at 18 banks and only half of the banks included in this analysis saw revenues grow faster than expenses. Nevertheless, management across regions discussed plans for reinvesting in their businesses, noting that upfront costs will eventually translate into higher revenues and improved efficiency.

The innovation agenda continued to be a primary reinvestment priority. While digital banking capabilities are well-developed across the industry, management comments indicated that banks are continuously looking for opportunities to improve upon existing apps. Examples of this included the launch of a “voice-enabled search feature” on CIBC’s mobile banking app, “the ability to open accounts through mobile” at Wells Fargo and RBS’s “mobile Get Cash functionality, [which] allows customers to withdraw cash from a cash machine without the need of a debit card.” In addition, and perhaps more interesting, however, were the details they provided on more mature and differentiated investments in innovation. Such initiatives included partnerships with FinTech firms, improved payments capabilities, deployments of artificial intelligence and the development of digital applications for commercial and wholesale customers.

For more information on how to develop a FinTech strategy, please see Unleashing the potential of FinTech in banking and for more information on emerging trends in payments, please see EY quarterly newsletter, #payments.

Notable and quotable “We’re investing in the wider Canadian digital ecosystem to drive the future prosperity of the country as shown by our recently announced partnerships with OneEleven and C100.”

David McKay, CEO Royal Bank of Canada

“In May, we released Lyf Pay in France, in partnership with leading retail groups. Lyf Pay is a new high value-added application, which provides a universal mobile payment solution, combining payments with loyalty programs, coupons and discount offers.”

Lars Machenil, CFO BNP Paribas

“We keep developing our education app, Yolt, in the UK. We clearly see Yolt as a step towards [the future of] banking and improving the customer experience through what we call open platforms, which basically means that what you offer to your clients is not necessarily limited to your own product or your own service, but you open yourself up to third-party providers as well. And as you know, we just don’t develop these things ourselves. We also partner with external FinTechs on these kinds of things.”

Ralph Hamers, CEO ING Group

2Q17 2Q16

47.5

51.0

52.7

53.1

54.3

54.4

54.6

57.7

58.9

59.2

59.5

59.7

60.0

60.8

61.6

63.0

64.6

64.9

65.5

66.2

68.2

68.7

69.5

72.2

75.0

78.5

80.0

80.2

80.6

84.9

86.3

122.1

Source: SNL Financial *Data is from company reports

Efficiency ratios, 2Q 2017

6Key themes from the 2Q 2017 earnings calls |

7 | Key themes from the 2Q 2017 earnings calls

Lending is not growing at robust rates, but banks are not willing to sacrifice credit quality in exchange for growth.

As of 30 June 2017, almost two-thirds of the banks covered in this report reported increased net loan balances from the end of 2Q 2016. However, growth rates were weak, exceeding 5% at only five banks. Banco Santander was the only European bank to break the 5% threshold, due to its acquisition of Banco Popular. Excluding the acquisition, net customer loans at Banco Santander actually fell 0.6%. During the 2Q 2017 season, management acknowledged the weak lending trends, but also indicated that they would rather focus on customers that could meet strict underwriting criteria than chase potentially higher-risk volume growth.

Notable and quotable “We have a selective approach towards the segment of clients for housing loans. … We decided to focus the new mortgage provision on affluent clients. 80% of the new production is coming from affluent clients. We assume [that we will] lose — for a short period of time — market share on mass market clients.”

Laurent Goutard, Head of French Retail Banking Société Générale Group

“Driven primarily by the expected decline in auto loans, which were down US$2.5 billion from the first quarter, total loans declined US$982 million from the prior quarter. As we’ve discussed previously, we’ve tightened credit underwriting standards in auto, which has reduced our origination volume.”

John Shrewsberry, CFO Wells Fargo

Year-over-year growth in end-of-period net loans, 30 June 2017

8Key themes from the 2Q 2017 earnings calls |

-8%

-8%

-4%

-4%

-4%

-3%

-2%

-2%

0%

0%

1%

1%

1%

1%

2%

2%

2%

3%

3%

4%

4%

4%

5%

5%

8%

10%

10%

11%

23%

Source: SNL Financial *Data is from company reports

Key themes from the 2Q 2017 earnings calls |

9 | Key themes from the 2Q 2017 earnings calls

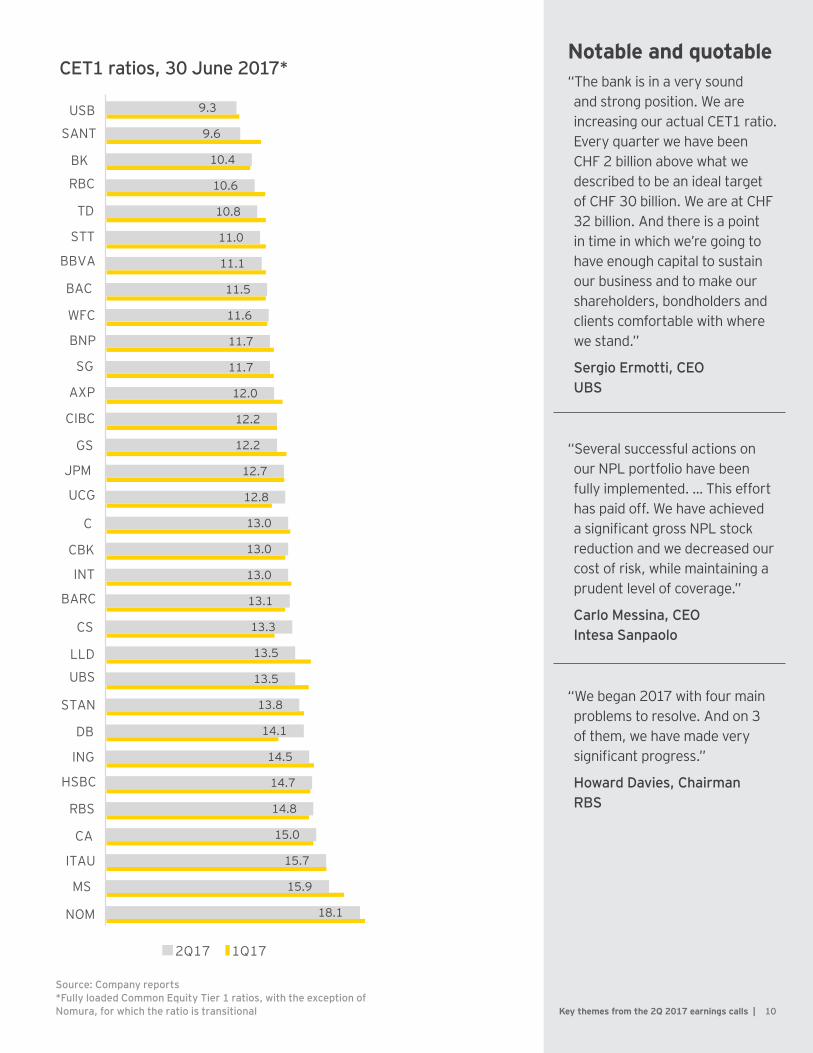

Management is cautiously optimistic about the outlook, as legacy head winds ease and capital levels improve.

While financial performance did not universally improve in 2Q 2017 and the sustainability of improved revenue performance in future quarters remains dependent on market conditions and monetary policy decisions, management at global banks appeared to be cautiously optimistic on the outlook. During the 2Q 2017 earnings season, banks pointed to progress in shoring up their balance sheets and resolving crisis-related weaknesses.

• Capital levels are strong. For the first time, the US Federal Reserve did not object to the capital plans of any of the banks subject to the US Comprehensive Capital Analysis and Review (CCAR) exercise, clearing the way for higher dividends, more share buybacks and greater flexibility in investing in growth opportunities. In Europe, most banks added to their capital ratios, and while dividends have not been restored across the board, management offered assurances that they were well-positioned to meet upcoming hurdles such as the implementation of IFRS-9 standards and potential further risk-weighted asset inflation under the so-called “Basel IV” reforms.

• A June 2017 report from the US Treasury Department outlining 100 recommendations for reforming the current regulatory landscape appeared to reignite US banks’ optimism about prospects for regulatory relief. European banks, meanwhile, commented on the continuing uncertainty about the shape and timing of the final Basel rules but seemed confident that they could generate sufficient capital to meet additional requirements.

• Credit quality continued to improve, as evidenced by lower cost of credit and reduced levels of non-performing loans (NPL).

• Finally, legacy issues related to financial crisis misconduct are receding, as banks made progress in resolving claims and needed to set aside fewer litigation provisions.

For more information on the role of regulation in shaping banks’ structures, please see Should structure shape strategy? from the Global EY Regulatory Network.

Notable and quotable “The bank is in a very sound and strong position. We are increasing our actual CET1 ratio. Every quarter we have been CHF 2 billion above what we described to be an ideal target of CHF 30 billion. We are at CHF 32 billion. And there is a point in time in which we’re going to have enough capital to sustain our business and to make our shareholders, bondholders and clients comfortable with where we stand.”

Sergio Ermotti, CEO UBS

“Several successful actions on our NPL portfolio have been fully implemented. … This effort has paid off. We have achieved a significant gross NPL stock reduction and we decreased our cost of risk, while maintaining a prudent level of coverage.”

Carlo Messina, CEO Intesa Sanpaolo

“We began 2017 with four main problems to resolve. And on 3 of them, we have made very significant progress.”

Howard Davies, Chairman RBS

10Key themes from the 2Q 2017 earnings calls |

CET1 ratios, 30 June 2017*

2Q17 1Q17

9.3

9.6

10.4

10.6

10.8

11.0

11.1

11.5

11.6

11.7

11.7

12.0

12.2

12.2

12.7

12.8

13.0

13.0

13.0

13.1

13.3

13.5

13.5

13.8

14.1

14.5

14.7

14.8

15.0

15.7

15.9

18.1

Source: Company reports *Fully loaded Common Equity Tier 1 ratios, with the exception of Nomura, for which the ratio is transitional

Further reading

Unleashing the potential of FinTech in banking

EY quarterly newsletter, #payments

EY regulatory perspectives

Download the complete report

Download the complete report

Download the complete report

EY | Assurance | Tax | Transactions | AdvisoryContact

Laura J. Tayman

Banking and Capital

Markets Analyst

Ernst & Young LLP

+1 720 931 4450

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

About EY’s Global Banking & Capital Markets SectorIn today’s globally competitive and highly regulated environment, managing risk effectively while satisfying an array of divergent stakeholders is a Sector key goal of banks and securities firms. EY’s Global Banking & Capital Markets network brings together a worldwide team of professionals to help you succeed — a team with deep technical experience in providing assurance, tax, transaction and advisory services. The Sector team works to anticipate market trends, identify their implications and develop points of view on relevant sector issues. Ultimately, it enables us to help you meet your goals and compete more effectively.

© 2017 EYGM Limited.All Rights Reserved.

EYG no. 04905-174GblED None

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax or other professional advice. Please refer to your advisors for specific advice.

ey.com