Embed Size (px)

Citation preview

2013ANNUAL REPORT

GENERAL GLICO GENERAL INSURANCE COMPANY LIMITED

GENERAL Annual Report & Financial Statements

stfor the year ended 31 December 2013

GLICO General 2013 Annual Report and Financial Statements

GLICO General 2013 Annual Report and Financial Statements

CONTENTS

0 1

02-09

10

11-14

15-17

18-19

20

22

23

24-25

26

27-62

Profile of Directors

Top Management

Chairman’s Report

Managing Director’s Review

Directors’ Report

Independent Auditors' Report

Statement of Comprehensive Income

Statement of Financial Position

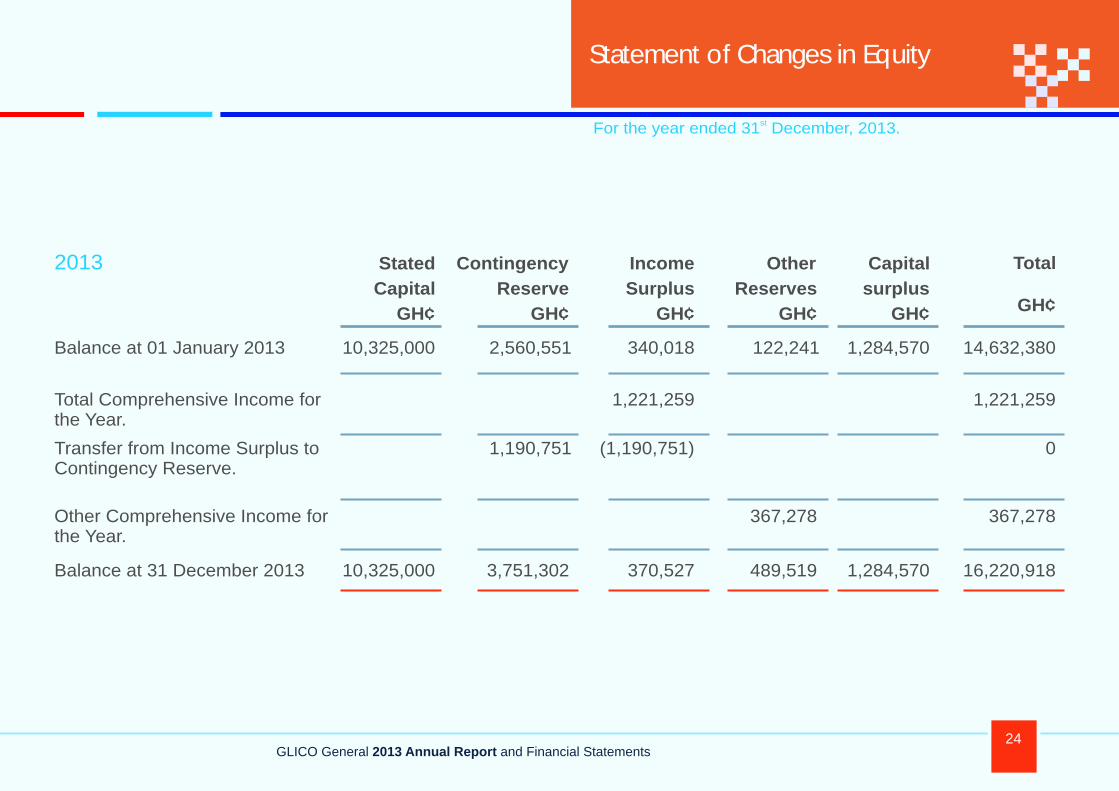

Statement of Changes in Equity

Statement of Cash Flow

Notes to the Financial Statements

Corporate information

FINANCIAL STATEMENTS:

To be a one-stop company and brand of choice providing insurance and financial services need in Ghana and the West African sub-region.

• To become an acknowledged leader in Ghana’s insurance and financial services industry.

• To provide innovative products, efficient and effective service delivery through optimal resource allocation.

• To continuously add value to the business so as to protect stakeholder’s interest.

Our Mission

Our Core Value Towards the attainment of our vision, we will be guided by these values:

Ethics – we abide by the rules and principles set by regulators of the industries we operate; as well as our own principles of business conduct that keeps us ahead of the competition.

Transparency – we operate and communicate in sincerity and promote the truth in all our business relationships.

Friendly and competitive services – we offer value to stakeholders through an efficient client relations system and prudent management practices.

Professionalism – we set high standards to remain competitive by providing quality service through a highly skilled and motivated staff.

Our Vision

GLICO General 2013 Annual Report and Financial Statements

CORPORATE INFORMATION

Andrew Acheampong-Kyei (Esq)P. O. Box 4251Accra

GLICO HouseNo. 47 Kwame Nkrumah AvenueAdabraka, Accra

Veritas AssociatesChartered AccountantsP. O. Box CT 6372Cantonments, Accra

Prudential Bank LimitedGhana Commercial Bank LimitedNational Investment Bank LimitedZenith Bank (Ghana) LimitedStanbic Bank Ghana LimitedBSIC Ghana LimitedBank of Baroda Ghana LimitedCAL Bank LimitedIntercontinental Bank Limited

Kwame Achampong-Kyei Alfred Y. Ofori Kuragu Edward Forkuo-Kyei Stephen Enchill (Dr) Joyce Aryee (Dr) Alex Quaynor (Esq) Eddie Safo Kwakye

Chairman Managing Director Member

Member Member

MemberMember

01

GLICO General 2013 Annual Report and Financial Statements

Profile of Director’s

Mr. Achampong-Kyei established

GLICO LIFE in 1987 as a specialist life insurance company at a time when life insurance in Ghana was dormant. Today, he has organically grown the component businesses: GLICO GENERAL, GLICO FINANCIAL, GLICO HEALTHCARE, GLICO PROPERTIES and GLICO PENSIONS which constitute the GLICO Group.

He is a visionary entrepreneur and a distinguished Insurance Executive and practitioner with over thirty-five years a c t i v e e x p e r i e n c e i n t h e insurance/financial industry gained through self development initiatives, commitment to application of modern insurance concepts and models both locally and internationally.

Mr. Achampong-Kyei has compounded academic and professional qualifications and is an accredited recipient of the International Quality Award as well as the Gold Award in Life Underwriting. He is also an esteemed member of the Chartered Insurance Institute and holds a B.Sc Degree in Business Studies, a Post Graduate Diploma in Management studies from the United Kingdom.

Mr. Achampong-Kyei serves as Chairman on the Executive Boards and Committees of the GROUP. For thirteen years (1993-2004), he assisted the National Insurance Commission-Ghana in establishing the foundations of the current Insurance Trade Association as a General Secretary.

Mr. Kwame Achampong - Kyei

Board Chairman

4702

GLICO General 2013 Annual Report and Financial Statements

Mr. Alfred Yaw Ofori-Kuragu is the

Managing Director of GLICO General Insurance Company (GLICO GENERAL).

Prior to joining GLICO GENERAL, he was the General Manager, Technical Operations, of SIC Insurance Company and he is an insurance professional with in-depth knowledge and experience in the business.

He is an Associate of the Chartered Insurance Institute (ACII) of London and holds an Executive MBA in finance from the University of Ghana Business School.

A product of the University of Ghana, he obtained the B.A Degree in Sociology combined with Political Science and further had legal education and training at the Ghana School of Law and was called to the Bar in October, 1997.

Mr. Ofori-Kuragu is skilled in underwriting Oil and Gas Insurance, having attended courses, Seminars and workshops on Oil and Gas held in Egypt, Nigeria, South Africa and Ghana.

Currently, he is a part-time Senior Lecturer at the Ghana Insurance College and delivers speeches at international conferences organized by the Ghana Reinsurance and Continental Re of Nigeria.

Mr. Alfred Yaw Ofori - Kuragu

Managing Director

Profile of Director’s - Contd.

03

47GLICO General 2013 Annual Report and Financial Statements

Mr. Edward Forkuo Kyei

Board Member

Profile of Director’s - Contd.

04

Mr. Forkuo Kyei joined GLICO in 1987 when he was still a student and fully in 1992 when he completed his first degree. He has and still plays a pivotal role in the growth and success of the organization since its inception in 1987.

His wealth of experience and expertise spans across two and half decades of working within the insurance and financial service industry.

He is an Associate member of the Chartered Insurance Institute (UK), a fellow of Ghana Insurance Institute and a member of the Life Council of the Ghana Insurers Association. He also holds an MBA in Finance & Advance Strategic Management from Cardiff Business School, Wales (UK). Further, he holds an MSc in Insurance & Risk Management from Cass Business School (UK).

He is also a graduate with a BSc in Development Planning from the Kwame Nkrumah University of Science and Technology (KNUST), Ghana.

Mr. Forkuo Kyei is currently the 2nd Vice President and the Chairman of the Life Insurance Council of the Ghana Insurers Association (GIA).

Mr. Kyei is passionate about insurance and has been instrumental in the quest to advancing life insurance in Ghana. He is indeed a valued resource for the Ghana Insurance industry.

Mr. Forkuo Kyei is the Chief Executive

officer and Managing Director of GLICO LIFE.

Hither to his appointments as Managing Director of GLICO LIFE, he held varied management position within GLICO including that of the Executive Director of GLICO LIFE.

GLICO General 2013 Annual Report and Financial Statements

Dr. Enchill is currently the Executive Vice- Chairman of the First Capital Plus Savings and Loan Limited. He also practices as a Chartered Accountant and a Senior Partner with Forbes Consult International (Chartered Accountants and Management Consultants).

Currently he holds the final part of ICA (Ghana) and is a member/fellow of the Institute of Chartered Accountants,Ghana. He is a member of the Association of MBAs (UK) after successfully graduating from IFM of Manchester University and University of Wales (UK) w i t h a n M B A i n F i n a n c e a n d Management.

He was recently awarded a Doctorate Degree in Business Administration with SMC University in Switzerland. Dr. Enchill has attended several seminars and courses both in Ghana and outside Ghana to enrich his knowledge base; that g i ves h im an edge in a l l h i s entrepreneurial business activities.

He is also a lecturer in Accounting & Financial Management (Stage 3) and an Examiner for the Institute of Chartered Accountants (Ghana) for the past 12 years.

Dr. Enchill serves on various Boards including GLICO Life Insurance Limited, GLICO General Insurance Limited, First Capital Plus, Action Aid Ghana and Ekumfiman Rural Bank.

Dr. Stephen Enchill

Board Member

Dr. Stephen Enchill is a Business

Executive and an Entrepreneur by practice. He is also a Chartered Accountant by profession. He has acquired many experiences in diverse business fields, both national and international.

His experience dates back from 1985, working with the Ghana Ports and Harbours Authority and subsequently working as a management personnel in UAC Ghana Limited (now Uniliver Ghana Limited), PKF (a firm of Chartered Accountants), Ghana National Petroleum Corporation, Ikam Limited and GLICO Life Insurance Company Limited.

Profile of Director’s - Contd.

05

47GLICO General 2013 Annual Report and Financial Statements

Profile of Director’s - Contd.

Dr. Joyce Rosalind Aryee

Board Member

She is a senior mentor for the African Leadership Initiative and the chair of the Moremi Init iat ive for Women in Leadership for African Development (MILEAD)both mentorship institutions for young Africans.

She serves on the boards of diverse organisations including Stanbic Bank Ghana Limited, Central University College, Finatrade Foundation, AEL Mining Services Limited, GLICO General, Engineers and Planners, Omatek Computers, The Ark Fund and MAN Ghana Limited to mention but a few.

She was given the Second Highest State Award, the Companion of the Order of the Volta in 2006 in recognition of her service to the nation. She is also the recipient of the Chartered Institute of Marketing, Ghana (CIMG) Marketing Woman of the Year award for 2007 and the African Leadership on Centre for Economic Development’s African Female Business Leader of the Year award for 2009.

She is an Honorary Fellow of the Ghana Institution of Engineers and received an Honorary Doctorate from the University of Mines and Technology in recognition of her immense contribution to the growth of the mining industry.

Dr. Aryee is the Founder and Executive Director of Salt & Light Ministries, a Christian para-church organisation and an avid promoter of Ghanaian classical and choral compositions.

Dr. Aryee is the former Chief Executive

Officer of the Ghana Chamber of Mines and the first woman to head an African Chamber of Mines.

An accomplished management and communication consultant and a professional counsellor Dr. Aryee has dedicated over forty years private and public sector service to Ghana. In particular, she served as Secretary (Minister) of Information and Education in government of the PNDC as well as a non-cabinet minister at the National Commission for Democracy.

06

GLICO General 2013 Annual Report and Financial Statements

Profile of Director’s - Contd.

Mr. Alex Quaynor

Board Member

Mr. Alex Quaynor is a lawyer, practicing

at Akufo-Addo Prempeh & Co; an Accra based legal firm. He graduated from the University of Ghana in 1986 with a Bachelor of Law (LLB Hons) Degree and was called to practice at the Ghana Bar in 1988.

He has been in active private legal practice since 1989 and his work has mainly been in the area of commercial law, corporate law, investment law, land law and general litigation. He is presently the Head of Akufo-Addo Prempeh & Co, one of the leading law firms in Ghana and has been providing legal services to various clients in his areas of law practice as well as managing the law firm.

Mr. Alex Quaynor was a Director of the Students Loan Trust Fund and also a Director of the Serious Fraud Office. He was a former Secretary of the Greater Accra Regional Bar and a member of the National Council of the Bar (Ghana).

He is currently a Director of Ernslex Ventures Limited, Ningo Salt Limited and Glico General Insurance Limited.

07

47GLICO General 2013 Annual Report and Financial Statements

Profile of Director’s - Contd.

Mr. Eddie Safo Kwakye

Board Member

He holds an MBA in Finance and Bachelor of Arts in Economics from the University of Ghana, Legon. He is, in addition, an aluminus of top academic and professional institutions with Certificates/Diplomas from several courses with these institutions including the World Bank; the IMF; Crown Agents (UK); University of Virginia, Darden Business School, USA; Executive Leadership Training Centre, York University, Toronto, Canada; and Boulders Institute of Microfinance, Turin, Italy.

His rich working experience spans across local and international f inancial institutions in senior and executive management positions with SG-SSB Bank and Ecobank Transnational Incorporated (ETI). In addition, he was Advisor and Coordinator for the Financial Sector as well as Manager of the Financial Sector Reform Programme (FINSSP/EMCB-FSR) implementation at the Ministry of Finance (2001-2008).

As Team Leader, Mr. Safo Kwakye worked with the World Bank/IMF/Donor Partners on the FINSSP / FSR implementation and also liaised with financial sector regulators and several financial institutions in Ghana and the outside world.

Mr. Safo Kwakye has deep and extensive corporate governance experiences from serving on Boards of top-notch and diversified numerous Corporate and Public Institutions. He presently serves on both GLICO Life and GLICO General Boards.

Mr. Safo Kwakye is an accomplished

Banker and Financial Analyst, with extensive knowledge and expertise in Finance and Management, Corporate and Financial Restructuring and Re-engineering, Investment Advisory Services, Merger and Acquisitions and P r o j e c t D e s i g n , S e t - u p a n d Management.

08

GLICO General 2013 Annual Report and Financial Statements

Profile of Director’s - Contd.

Mr. Andrew Achampong - Kyei Esq

Head of Legal/Company Secretary

Mr. Achampong-Kyei is a United

Kingdom qualified Solicitor and a Fellow of the Institute of Legal Executives. He has also been called to the Ghana Bar Association. He is thus, qualified to practice both in Ghana and the United Kingdom.He has extensive experience as a finance and project lawyer and has worked with leading law firms in the United Kingdom.

Andrew holds a Bachelor of Law Degree from the University of Kent (UK) and a Post-Graduate Diploma from the University of Westminster (UK).

Prior to his appointment, Andrew had been working intermittently with GLICO throughout schooling, whenever he was in Ghana. He rejoined GLICO in 2010 as the Head of Legal and Special Risks with unique skills in management, finance and insurance.

Andrew is currently the Company Secretary of GLICOLIFE and sits on the Executive Committees of the company.

09

Top Management

GLICO General 2013 Annual Report and Financial Statements4710

Mr. Alfred Yaw Ofori Kuragu Managing Director

Ms. Edwina Quayson Claims Manager

Mr. Charles Graham - Mensah General Manager, Marketing

Mr. Joshua Danso TwumGeneral Manager,

Finance & Administration

Mr. Ohenebeng Sarpong General Manager, Technical

CHAIRMAN’S REPORT

CHAIRMANKwame Achampong-Kyei

GLICO General 2013 Annual Report and Financial Statements11

GLICO GENERAL has

an exciting future.

We believe that the

major decisions taken

by your board will

ensure your company

achieves continued

long-term growth

and profitability.

4712GLICO General 2013 Annual Report and Financial Statements

CHAIRMAN’S REPORT - Contd.

Introduction

Economic Environment

Distinguished Ladies and Gentlemen, on behalf of the board of directors, I am pleased to report that 2013 was a year of advancement and progress with growth in premium income and profit for GLICO GENERAL.

It is my privilege to present to you the Annual Report and Financial Statements of the Company for the year ended December 31, 2013.

GLICO GENERAL achieved a gross premium growth of 24%. as our businesses continued to deliver growth and improved profitability. Indeed GLICO GENERAL has an exciting future.

There was also a significant improvement in our 2013 performance over 2012. Profit before tax amounted to GH¢ 1.6 million compared to GH¢ 1.3million of the previous year with net assets increasing from GHC 14.6million to 16.2 million in 2013.

With fast-growing emerging markets losing pace while developed nations gained strength, the 2013 performance reflected something of a role reversal among the players. In 2013, central banks in the U.S., Japan and Europe showered money on their economies, held interest rates low and promised to continue to do so in a bid to animate a recovery that remains tepid almost five years after the worst recession since the Great Depression.

In emerging markets such as Brazil and India, domestic demand softened and exports sagged as rates were boosted to stem inflation.

Despite the contrasting fortunes, the overall global economy appeared to be on a surer footing as the year ended. The International Monetary Fund forecasts that world output will grow 3.6% in 2014, compared with a 2.9% estimate for 2013.

The combination of fast-growing economies slowed slightly while the developed world picked up the pace setting the stage for synchronized growth in 2014.

Insurance IndustryGlobal

Ghana

Market performanceGlobal:

The global non-life industry generated around USD 2,100 billion of premium income in 2013 of which 18% came from emerging markets. Non-life insurance extends from standardized motor and household insurance to sophisticated tailor-made liability and property covers, including specialty commercial and industrial risk insurance.

The global non-life insurance sector was stable in 2013, with overall premium growth slightly up from 2012 to 3% in real terms. In the advanced markets, premium growth likewise remained steady at 1.4%. This mostly reflected moderate rate increases in some markets plus, to a lesser extent, growth in exposure weakened nevertheless by the slow-growing global economy. Southern Europe saw significant declines in premium income for the second year in a row.

The Ghanaian non- life insurance industry grew at a compound annual growth rate (CAGR) of 30.4% during the review period (2009?2013). Compared to other African countries, such as Cote d'Ivoire - 3.9% and Cameroon - 9.4% attesting to the fact that Ghana's non- life insurance industry is growing in terms of gross written premium in the West African sub region. The industry is also expected to grow at a forecast-period CAGR of 23.0% in 2018. The growth will be supported by the increase in oil and gas production, the implementation of compulsory fire insurance for commercial buildings and an increase in gold production.

Emerging market premiums grew by 7.8%, down from 8.0% in 2012: a reflection of the economic slowdown in many export-dependent countries in Southeast & Central Asia and Eastern Europe. That said, China's non-life premiums rose by about 13%, largely due to new car sales and infrastructure investments. Premium growth in Latin America, Africa and the Middle East was also estimated to be stronger in 2013 than it had been in 2012.

GLICO General 2013 Annual Report and Financial Statements13

CHAIRMAN’S REPORT - Contd.

Underwriting profitability improved marginally, thanks to a gradual strengthening of premium rates in the US, Europe and other selected markets, and also because claims growth remained benign. Canada and Germany among others, however, bucked this trend with an increase in natural catastrophe claims.

While 2013 underwriting results improved from the previous year, non-life earnings remained under pressure from weak investment returns. Six years after the financial crisis, the investment environment continues to challenge the insurance industry.

Overall non-life insurance profitability remains subdued by historical standards. The return on equity for the main non-life markets is estimated to have been about 7% in 2013, only slightly better than 2012 and well short of the industry's cost of capital.

The insurance industry continues to be competitive with the number of Non-Life Companies standing at 26. The industry continues to register new entrants and this is expected to further increase the level of competition already reaching cut-throat in the industry.

As a result of heightened competition, the industry continues to be plagued with high levels of outstanding premium owed insurers. In spite of the NIC credit guidelines to mitigate this situation, some insurance companies continue to flout the guidelines, accumulating very high debtors' levels on their balance sheets with the attendant challenge of writing off huge sum of money as bad debt.

The formulation and implementation of the "No Premium, No Cover" policy expected to commence in 2014, is expected to position insurers well to respond appropriately to claims when they fall due. Concomitantly, cash-strapped insurers will be once again made solvent by this policy.

Ghana:

In the wake of the high competition in the industry, GLICO GENERAL has continued with its unbending policy of not under cutting to secure businesses. The resultant effect has been GLICO GENERAL's ability to secure reinsurance covers for our businesses, which further strenthens our future survival in the event of claims demand.

Also, in the midst of these challenges, your Board provided excellent guiding principles that ensured that your Company leads the competition in quality and setting standards of performance whilst ensuring that your Company maintains a healthy financial position.

We continued to pursue our vision of creating value for all stakeholders and to this end, GLICO GENERAL rea l i zed an amoun t o f GH¢39,691,704 as Gross Earned Premium representing a 24% increase over last year's figure. Net Earned Premium Income after R e i n s u r a n c e s g r e w b y 3 8 % f r o m GH¢13,388,662 in year 2012 to GH¢18,589,408 in the year 2013.

Gross premium of GHC39,691,704 which is a 24% growth over 2012's performance of GH¢31,905,202 was realized. Premium earned increased from GHC13,388,662 to GH¢18,589,408 in 2013, showing an increase of 38%

On the other hand, claims payments increased b y 1 4 4 % f r o m G H ¢ 6 , 1 4 9 , 0 5 5 t o GH¢9,690,613 underscoring our commitment on prompt payment of legitimate claims

Management expenses increased from GH¢7, 765,761 to GH¢8, 892,713 for the year under review.

Profit before tax for the year under review was GH¢1,641,287 compared to last year of GH¢1,340,809. This shows an increase of 22%. Profit after tax also increased by 19% from GH¢1,019,899 to GH¢1,221,259 in 2013.

2013 Operating Results

•

•

•

•

4714GLICO General 2013 Annual Report and Financial Statements

CHAIRMAN’S REPORT - Contd.

•

•

Dividend

•

•

•

•

•

•

Corporate Social Responsibility

Net assets increased from GHC14,632,380 to GH¢16,220,918 as a result of prudent investment management.

i n c o m e w e n t u p f r o m I n v e s t m e n t GH¢1,088,405 to GH¢1,743,582 in 2013 representing a 60% growth.

Your Board is committed to delivering sustainable dividend growth. I am happy to announce that your Board declared a total interim dividend of GH¢100,000 for 2013. Major Development for 2013

Massive training of staff for both their personal and technical development.

An increase in the number of branches

Improved relationship with brokers with increased business placement following restructuring of the marketing department for efficiency.

The company also submitted to evaluation by the Global Credit Rating of South Africa and also invited Standard and Poors of USA to rate us. This has led to an "A-"and "B" rating respectively.

ndYour company also placed 52 position on the Ghana Club 100 ranking. By this feat, GLICO

ndGENERAL was the 2 highest ranked non-life insurer on the ranking.

GLICO GENERAL was also elevated to a “Premier Brand" status by The Centre for Brand Analysis Ghana.

As a corporate citizen, we take pride in our strong relationships with the communities where we live and work.

GLICO GENERAL continues to support a wide range of social services and educational organizations in our communities. Our CSR policy focuses on four key areas: sports, health, education and community relations.

In 2013, GLICO GENERAL took a distinct approach to community support in these areas through its philosophy to "Cushion you for life". The company spent GH¢73,909 in fulfilling this philosophy to "cushion" and invest in social activities that inures to the benefit of all.

Outlook for 2014

Acknowledgement

GLICO GENERAL has an exciting future. We believe that the major decisions taken by the board will ensure that your company achieves continued long-term growth and profitability.

Global growth forecasts for 2014 are more positive, which is expected to lead to increased demand for non-life insurance. Premium growth in the emerging markets will likely remain strong, at about the same levels as 2013.

GLICO GENERAL in 2014 is focusing on investing in the upgrade of robust ICT software to deliver value. Other areas of keen attention are on prudent and sound management practices, customer- centric approaches to services, good investment portfolio and prompt claim payment to yield maximum customer returns.

GLICO GENERAL relies on its dedicated and passionate staff both for past successes and to deliver the future expectations.

I wish to acknowledge the contribution of our Board, Management and Staff to our growth to date and look forward to their continued support in rolling our mission in the coming year and beyond.

2014 heralds significant changes in the nature and scope of our business and we know we can count on their creativity and commitment to deliver the growth on which the rewards for our shareholders depend.

We wish to finally express our gratitude to our most valued customers who have kept faith with us in these challenging times. We assure them we will continue to deliver excellent services that exceed their expectations.

Thank you and God bless us all.

CHAIRMANK. Achampong-Kyei

GLICO General 2013 Annual Report and Financial Statements15

Managing Director’s Review

Mr. Alfred Yaw Ofori - Kuragu

Managing Director

Introduction

Business Outlook

I am pleased to present our financial results for the full year 2013, which demonstrate strong underlying Profitability driven by our focus on pricing discipline and portfolio management.

GLICO GENERAL'S performance in 2013 gives us confidence in both our strategic direction and our ability to deliver shareholder value.

The Ghanaian insurance industry grew in terms of written premium value recording a Compound Annual Growth Rate (CAGR) of 27.0% between 2008 and 2012.

Competition in Ghana's non-life insurance industry deepened in the year gone by as companies with relatively lower business volumes continued to chip away at the market share of the biggest five.

The insurance industry in Ghana is undergoing rapid change and we face increasing competition from other companies. The rise in competition in the industry has been beneficial, as it has encouraged innovation among the companies. This has also induced higher productivity and efficiency.

The industry efficiency, measured by premium revenue per worker, has been improving and surged from less than GH¢200,000 in 2010 to GH¢301,000 last year.

In the same period, underwriting revenue more than doubled from GH¢271mil l ion to GH¢571million - even though as a share of GDP it registered 0.6 percent in both 2010 and 2013.

The other way competition benefits insurers is that as firms underwrite more business, they increase the scale of their operations, which enhances their ability to underwrite risks that previously were too large.

But competition has also produced a negative consequence for the industry: substantial premium debts due to companies selling insurance on credit in the scramble for business.This practice boosted premium debts owed by policyholders to a high of 39 percent of gross revenues in 2010.

As reported in the Chairman's statement, the 2 0 1 3 G r o s s E a r n e d P r e m i u m w a s GH¢39,691,704.00 which represents a 24% growth over the 2012 gross Earned Premium of GH¢31,905,202.00. This is a significant achievement by the company, especially in the face of competitive pressures.

The company has continued to provide protection and security to our numerous clients through the payment of claims.In 2013, the company paid a total of GH¢9,690,613.00 in claims to policyholders and third party claimants.

Claims Payment

4716GLICO General 2013 Annual Report and Financial Statements

Managing Director’s Review -Contd.

Speedy settlement of claims is a very vital aspect of service to the policyholders. Hence, the Company has laid great emphasis on expeditious settlement of claims. Average Claims Turn Around Time [CTAT] has consistently improved during the current financial year with overall claims Turn Around Time remaining well within 14 days.

GLICO GENERAL continues to generate strong underlying profitability. We have increased our revenues by defending our position in mature markets and diversifying into target emerging markets. Our investment performance was strong, delivering a total return of 13% growth in 2013. We were able to deliver these solid financial results in 2013 despite economic uncertainty around the world.

We are proud to have talented employees who work hard each and every day to help our customers understand and protect themselves from risk; we are thankful to our customers and recognize that we have to earn their trust by delivering excellent products and services that meet their needs; and we are grateful for the support of our shareholders, who recognize that GLICO GENERAL strives to provide stable and sustainable returns in a chal lenging environment.

We will continue to deliver quality service to our policyholders to ensure a sustained growth for GLICO GENERAL.

During the year, GLICO GENERAL was rated 'B' by Standard & Poor's (S&P), an International Rating Company based in USA, which we are naturally proud of.

In the Official Bulleting Update issued by Standard & Poor's, it stated "we are assigning our "B" counterparty credit and financial ratings to Ghana-based Glico Life Insurance Ltd and core subsidiary Glico General insurance company. Under our group rating methodology criteria, we classify GLICO GENERAL as core to its parent GLICO LIFE, which owns 100% of GLICO GENERAL.”

Business Development

Corporate Credit Rating

Glico General Insurance Company Limited has also retained its A- international credit rating, by Global Rating Company of South Africa, which relates to claims paying ability.

For GLICO GENERAL, corporate social responsibility (CSR) is a key ingredient of our strategy. It is about sustainable value creation, which is one of our values. We aim to create sustainable value for each of our main stakeholder groups by proactively addressing relevant environmental, social and governance issues.

GLICO GENERAL'S commitment to the United Nations Global Compact is also the foundation of our CSR strategy. We focus on areas related to our core business so that we can apply our insurance and risk management expertise to enhance our contributionto society. The company spent GH¢ 73,909.00 in creating sustainable value for each of our main stakeholder groups. CSR focused areas were among others, the sponsorship to Ghana Police, programs to combat child labour, stigma against aids patients, maternal and infant mortality and promotion of food security.Other areas include:

Environment, health and safety management in our office buildings.

Diversity and inclusion in our workforce

Responsible supply chain management

At GLICO GENERAL, we aim at becoming more Customer-driven. We operate for the sole purpose of delighting our customers and delivering value to its shareholders in the best professional manner. In order to reach this goal, we are upgrading our service infrastructure and adopting tools and techniques that will give us more insight into our customers' needs.

We have rolled out call centers with a singular objective to make sure that all clients enquiries and needs are met professionally and on time; offering solutions from operational to strategical.

Corporate Social Responsibility

•

•

•

Customer Service

GLICO General 2013 Annual Report and Financial Statements17

Managing Director’s Review

We continue to enhance our human resource skills set in this area of endeavor to ensure that clients needs are dealt with the highest levels of professionalism.

We also aim:

to create more value from our existing portfolio by expanding the opportunities for cross-selling and by increasing customer loyalty;

to win new business by improving our visibility and attractiveness to customers.

Persistency and efficiency-focused business will be the key to profitability. Renewal premiums have been pivotal in determining profitability and will continue to do so as the industry keeps on maturing.

Market resilience and improved penetration are important driving factors. A customer centric approach to business, well trained insurance advisors and an innovative product portfolio will be keys to generate business. As a commitment towards better sales support, GLICO GENERAL is in the process of opening 2 new branches in the coming year.

At GLICO GENERAL, we believe that employees are our prime competitive advantage that drives us ahead of our competition. For us, the Company's growth is simply the sum total of growth achieved by each one of our employees.

We do not underestimate the challenges ahead, but have confidence in our management and staff to manage both the risks and opportunities ahead as we work towards improving the results achieved in 2013.

On behalf of the Board of Directors, we wish to express our deep sense of appreciation to all employees and intermediaries, who continue to display outstanding professionalism and commitment, enabling the organization to retain market leadership in its business operations.

•

•

Future Outlook

Appreciation

The Directors would also like to take this opportunity to express their sincere thanks to the valued customers for their continued patronage.

The Directors also express their gratitude for the advice, guidance and support received from time to time, from the auditors.

I look forward to reporting on our continued progress next year.

Thank you.

Alfred Yaw Ofori-KuraguManaging Director

4718GLICO General 2013 Annual Report and Financial Statements

Directors’ Report

The Directors hereby present their report together with the audited financial statements of GLICO General Insurance Company Limited for the year ended 31 December 2013.

The Ghana Companies Code 1963 (Act 179) requires the Directors to prepare financial statements for each financial year, which gives a true and fair view of the state of affairs of the company and of the profit and loss for the period.

In preparing these financial statements, the Directors confirm that suitable accounting policies have been used and applied consistently reasonably and prudent judgments and estimates have been made in preparation of the financial statements for the year ended 31 December 2013. The directors confirm that the financial statements have been prepared on a going concern basis.

Statement of Directors' Responsibilities

The Directors are responsible for ensuring that the company keeps accounting that disclose, with reasonable accuracy at anytime, the financial position of the company. The directors are also responsible for safeguarding the assets of the company and taking reasonable steps for the prevention and detection of fraud and other irregularities. This responsibility includes: designing, implementing and maintaining internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error; selecting and applying appropriate accounting policies; and making estimates that are reasonable in the circumstances.

Financial ResultsThe financial results for the year ended 31 December, 2013 are set out below:

2013 2012 GH¢ GH¢

Profit Before Tax 1,641,287 1,340,809

To which is Charged: National Stabilization Levy of: (21,107) 0

Income Tax of (398,920) (320,910 ) Giving a Profit After Tax for the Year of: 1,221,259 1,019,899 From Which is Deducted: Dividend paid of 0 (60,000)

Transfer to Contingency Reserve of (1,190.751) (957, 156)

Leaving a Balance of: 30,508 2,743

When Added to the Opening Balance on the

Retained Earnings Account as of 1 January

340,108 3337,275

It leaves a Closing Balance on the Retained

Earnings Account of:

370,527 340,018

GLICO General 2013 Annual Report and Financial Statements19

Directors’ Report - Contd.

There was no change in the nature of the company's business during the year.

The directors recommend that a dividend of one hundred and twenty Ghana Cedis be paid to the shareholders. This has not been provided for in the accounts.

The auditors, Veritas Associates, will continue in office in accordance with Section 134 (5) of the Ghana Companies Code, 1963 (Act 179).

The directors confirm that no matter has arisen since 31 December 2013, which materially affect the financial statements of the company for the year ended on that date.

Approved by the Board on 28th April 2014 and signed by:

Director.......................................................

Director.......................................................

Dividends

Auditors

Other Matters

4720GLICO General 2013 Annual Report and Financial Statements

Auditor’s Report

We have audited the accompanying financial statements of GLICO General Insurance Company Limited which comprise the statement of financial position as at 31 December 2013 and the statement of comprehensive income, statement of changes in equity and cash flow for the year ended, and a summary of significant accounting policies and other explanatory notes and the directors report in this document.

The directors are responsible for the preparation and fair presentation of these financial statements in accordance with International Financial Reporting Standards and in the manner required by the Ghana Companies Code, 1963 (Act 179). This responsibility includes: designing, implementing and maintaining internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error; selecting and applying appropriate accounting policies; and making accounting estimates that are reasonable in the circumstances.

Our responsibility is to express an independent opinion on these financial statements based on our audit in accordance with International Standards on Auditing. Those standards require that we plan and perform the audit to obtain reasonable assurance that the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control.

Directors' Responsibility for the Financial Statements

Auditors' Responsibility

An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

In our opinion, the financial statements agree with the underlying records and present fairly, in all material respects, the financial position of GLICO General Insurance Company Limited at 31 December 2013 and its f inancial performance and its cash flows for the year then ended in accordance with the Ghana Companies Code, 1963 (Act 179), the Insurance Act 2007 (Act 724) and the International Financial Reporting Standards.

The Ghana Companies Code, 1963 (Act 179) requires that in carrying out our audit work we consider and report on the following matters.We confirm that:i. We have obtained all the information and

explanations which to the best of our knowledge and belief were necessary for the purpose of the audit;

ii. In our opinion proper books of account have been kept by the company so far as appears for our examination of those books; and

iii. The balance sheet and profit and loss account of the company are in agreement with the books of account.

Signed by Anthony Danquah (ICAG/P 1045)For and on behalf of Veritas Associates (ICAG/F/198)Chartered AccountantsAccra, Ghana

th29 April, 2014

Opinion

Report on Other Legal Requirements:

FINANCIAL STATEMENTS

GLICO General 2013 Annual Report and Financial Statements22

F stor the year ended 31 December, 2013.

Notes

Insurance Premium Revenue 3

Insurance Premium Ceded to Reinsurers 3

Net Insurance Premium Revenue

Investment Income 5

Other Operating Income 6

Net Income

Net commission Income / (Expense)

Insurance Claims and Loss Adjustment Expenses 7

Provision for unearned premium 8

Net Insurance Benefits and Claims

Operating and Other Expenses 9

Results of Operating Activities

Finance Cost

Net Profit Before Tax

National Stabilisation Levy

Taxation 10

Net Profit After Tax

Other Comprehensive Income

Changes in Available-for-Sale Assets, Net of Tax

Notes 1 to 26 Form an Integral Part of the Financial Statements.

2013

GH¢

39,691,704

(17,223,848)

22,467,856

1,743,582

561,738

24,773,175

(588,433)

(9,690,613)

(3,878,448)

10,615,682

(8,892,713)

1,722,969

(81,682)

1,641,287

(21,107)

(398,920)

1,221,259

367,278

1,588,537

Statement of ComprehensiveIncome.

2012

GH¢

31,905,202

(16,167,318)

15,737,884

1,088,405

89,408

16,915,697

748,125

(6,149,055)

(2,349,222)

9,165,545

(7,765,761)

1,399,784

(58,975)

1,340,809

0

(320,910)

1,019,899

105,247

1,125,146

4723GLICO General 2013 Annual Report and Financial Statements

Notes

Assets

Property Plant and Equipment 11

Investment Property 12

Available for Sales Equity Securities 13

Deferred Tax Assets 10(ii)

Insurance Receivable 14

Other Receivables 15

Cash and Cash Equivalents 16

Total Assets

Equity and Liabilities

Equity

Stated Capital 17

Contingency Reserve 18

Income Surplus 19

Other Reserves 20

Capital Surplus 21

Total Equity

Liabilities

Insurance Liabilities 22

Trade and Other Payables 23

National Stabilisation Levy

Income Tax 10

Total Liabilities

Total Equity and Liabilities

Approved by the Board on 28th April 2014 and Signed on its Behalf by:

......................................... Director ......................................... Director

2013

GH¢

2,296,556

6,569,397

1,401,629

51,641

14,705,146

792,339

15,440,265

41,256,974

10,325,000

3,751,302

370,527

489,519

1,284,570

16,220,918

21,805,399

2,961,376

21,107

248,174

25,036,056

41,256,974

F stor the year ended 31 December, 2013.

Statement of Financial Position

Notes 1 to 26 form an integral part of the financial statements.

2012

GH¢

1,712,690

6,569,397

1,034,352

4,752

10,846,152

596,337

12,406,044

33,169,724

10,325,000

2,560,551

340,018

122,241

1,284,570

14,632,380

14,876,988

3,155,091

0

505,265

18,537,344

33,169,724

2013

Balance at 01 January 2013

Total Comprehensive Income forthe Year.

Transfer from Income Surplus to Contingency Reserve.

Other Comprehensive Income forthe Year.

Balance at 31 December 2013

Stated

Capital

GH¢

10,325,000

10,325,000

Contingency

Reserve

GH¢

2,560,551

1,190,751

3,751,302

Income

Surplus

GH¢

340,018

1,221,259

(1,190,751)

370,527

Other

Reserves

GH¢

122,241

367,278

489,519

Capital

surplus

GH¢

1,284,570

1,284,570

Total

GH¢

14,632,380

1,221,259

0

367,278

16,220,918

GLICO General 2013 Annual Report and Financial Statements24

Fstor the year ended 31 December, 2013.

Statement of Changes in Equity

GLICO General 2013 Annual Report and Financial Statements25

Fstor the year ended 31 December, 2013.

Statement of Changes in Equity - Contd

2012

Stated

capital

GH¢

10,325,000

10,325,000

Contingency

reserve

GH¢

1,603,395

957,156

2,560,551

Income

surplus

GH¢

337,275

(957,156)

1,019,899

(60,000)

340,018

Other

reserves

GH¢

16,994

105,247

122,241

surplus

Capital

GH¢

0

1,284,570

1,284,570

Balance at 01 January 2012

Transfer from Income Surplus to Contingency Reserve.

Total Comprehensive Income for the Year

Other Comprehensive Income for the Year

Dividend Paid

Fair Value Gains/(Losses)

Balance at 31 December 2012

Notes 1 to 26 form an Integral Part of these Financial Statements.

Total

GH¢

12,228,816

0

1,019,899

105,247

(60,000)

1,284,570

14,578,533

4726GLICO General 2013 Annual Report and Financial Statements

Notes

Net Cash Flow from Operating Activities

Profit Before Taxation

Adjustment for:Depreciation Expense 12Interest Income

Interest Charged

Increase in Loans and Receivables

Increase in Insurance Receivables 15

Increase in Insurance Liabilities 22

Decrease in Deferred RevenueIncrease in Trade and Other Payables 23

Cash from Operating Activities

National Stabilization LevyTax Paid

Net Cash Inflow from Operating Activities

INVESTING ACTIVITIES

Payments to Acquire Property, Plant & Equipment 11

Purchase of Available for Sale Securities 13

Net Cash used in Investing Activities

FINANCING ACTIVITIES

Interest Paid

Interest Received

Dividend Paid

Increase in Cash and Cash Equivalents

Cash and Cash Equivalents at the Beginning of the Year.

Cash and Cash Equivalents at 31 December 16

Notes 1 to 26 form an Integral Part of the Financial Statements.

2013GH¢

1,641,287

187,560(1,894,352)

81,682(196,001)

(3,858,995)6,928,411

0(193,715)

2,695,879

0(702,901)

1,992,978

(771,426)0

(771,426)

1,221,551

(81,682)1,894,351

0

3,034,221

12,406,044

15,440,265

F stor the year ended 31 December, 2013.

Statement of Cash Flows

2012GH¢

1,340,809

143,666(1,088,405)

58,975(121,352)

(2,208,259)4,016,477(104,313)

875,590

2,913,189

0(200,000)

2,713,189

(314,752)(371,562)

(686,314)

2,026,875

(58,975)1,088,405(120,000)

2,936,305

9,469,739

12,406,044

GLICO General 2013 Annual Report and Financial Statements27

1. CORPORATE INFORMATION

The principal accounting policies adopted in the preparation of these financial statements are set out below. These policies have been consistently applied to all years presented, unless otherwise stated.

The financial statements are prepared in compliance with International Financial Reporting Standards (IFRS). Additional information required by the Companies Code, 1963, (Act 179) and the insurance Act 2006 (Act 724) are included where appropriate. The measurement basis applied is the historical cost basis, except as modified by the revaluation of land and buildings, investment property, available-for-sale financial assets, and financial assets and financial liabilities at fair value through income. The financial statements are presented in Ghana Cedis (GH¢).

The preparation of financial statements in conformity with IFRS requires the use of estimates and assumptions. It also requires management to exercise its judgement in the process of applying the Company’s accounting policies. The areas involving a higher degree of judgement or complexity, or where assumptions and estimates are significant to the financial statements, are disclosed in Note 2.15.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

2.1 Basis of Preparation

The Company is a limited liability company incorporated in Ghana under the Companies Code 1963, (Act 179) and domiciled in Ghana. The address of its registered office is GLICO House, 47 Kwame Nkrumah Avenue, Adabraka, P. O. Box 4251, Accra, Ghana. The Company underwrites non-life insurance risks such as those associated with property and liability.

During the year, there were certain amendments and revisions to some of the standards. The nature and the impact of each new standards and amendments are described below:

The amendment is effective for annual periods beginning on or after 1 January 2013 and requires thatitems of other comprehensive income be grouped into items that would be reclassified to profit or loss at a future point and items that will never be reclassified. This amendment only effects the presentation in the financial statements.

The amendment is effective for annual periods beginning on or after 1 January 2012 and introduces a rebuttable presumption that deferred tax on investment properties measured at fair value will be recognised on a sale basis, unless an entity has a business model that would indicate the investment property will be consumed in the business. If consumed a use basis should be adopted. This amendment will have no impact on the company after initial application.

IAS 1 Financial Statements Presentation (Amendment)

IAS 12 Income Taxes (Amendment)

2.2 Application of new and Revised International Financial Reporting Standards

F stor the year ended 31 December, 2013.

Notes to the Financial Statements

4728GLICO General 2013 Annual Report and Financial Statements

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

IAS 19 Post Employee Benefits (Amendment)

Recoverable Amount Disclosures for Non-Financial Assets – Amendments to IAS 36 Impairment of Assets

IAS 39 Novation of Derivatives and Continuation of Hedge Accounting — Amendments to IAS 39.

••

•

The amendments are effective for annual periods beginning on or after 1 January 2013. There are changes to post employee benefits in that pension surpluses and deficits are to be recognised in full (no more deferral mechanisms) and all actuarial gains and losses recognised in other comprehensive income as they occur with no recycling to profit or loss. Past service costs as a result of plan amendments are to be recognized immediately. Short and long-term benefits will now be distinguished based on the expected timing of settlement, rather than employee entitlement.

These amendments remove the unintended consequences of IFRS 13 on the disclosures required under IAS 36. In addition, these amendments require disclosure of the recoverable amounts for the assets or cash - generating units (CGUs) for which impairment loss has been recognised or reversed during the period. These amendments are effective retrospectively for annual periods beginning on or after 1 January 2014 with earlier application permitted, provided IFRS 13 is also applied. The company has not adopted earlier application of these amendments and hence had no impact on the company.

These amendments require an entity to disclose information about rights of set-off and related arrangements (e.g., collateral agreements). The disclosures will provide users with information that is useful in evaluating the effect of netting arrangements on an entity’s financial position. The new disclosures are required for all recognised financial instruments that are set off in accordance withIAS 32 Financial Instruments: Presentation. The disclosures also apply to recognised financialinstruments that are subjec t to an enforceable master netting arrangement or ‘similar agreement’, irrespective of whether they are set off in accordance with IAS 32. Effective for periods beginning o n o r a f t e r 1 J a n u a r y 2 0 1 3 T h e s e h a v e n o i m p a c t o n t h e c o m p a n y.

The amendments provide an exception to the requirement to discontinue hedge accounting in certain circumstances in which there is a change in counterparty to a hedging instrument in order to achieveclearing for that instrument. The amendment covers novations:

That arise as a consequence of laws or regulations, or the introduction of laws or regulations Where the parties to the hedging instrument agree that one or more clearing counterparties replace the original counterparty to become the new counterparty to each of the parties.That did not result in changes to the terms of the original derivative other than changes directlyattributable to the change in counterparty to achieve clearing All of the above criteria must be met to continue hedge accounting under this exception. The amendments cover novations to central counterparties, as well as to intermediaries such as clearing members, or clients of the latter that are themselves intermediaries. For novations that do not meet the criteria for the exception, entities have to assess the changes to the hedging instrument against the de-recognition criteria for financial instruments and the general conditions for continuation of hedge accounting. Effective for periods beginning on or after 1 January 2014 . These have no impact on the company.

IFRS 7 Disclosures - Offsetting Financial Assets and Financial Liabilities - Amendments to IFRS 7

F stor the year ended 31 December, 2013.

Notes to the Financial Statements - Contd.

GLICO General 2013 Annual Report and Financial Statements29

IFRS 9 Financial Instruments: Classification and Measurement

IFRS 10 Consolidated Financial Statements; IFRS 11 Joint Arrangements; IFRS 12 Disclosure of Interest in Other Entities.

IFRS 13 Fair Value Measurement

A revised version of IFRS 9 (supersedes IFRS 9 (2009)) incorporating revised requirements for theclassification and measurement of financial liabilities, and carrying requirements for the classification and measurement of financial liabilities, and carrying over the existing derecognition requirements from IAS 39 Financial Instruments:

The revised financial liability provisions maintain the existing amortised cost measurement basis for mostliabilities. New requirements apply where an entity chooses to measure a liability at fair value through profit or loss - in these cases, a portion of the change in fair value related to changes in the entity's own credit risk is presented in other comprehensive income rather than within profit or loss. However, for annual reporting periods beginning before 1 January 2015, an entity may early adopt IFRS 9 (2009)

instead of applying this Standard. The impact of adoption depends on the assets held by the Company at the date of adoption as it is not practicable to quantify the effect.

IFRS 10 replaces the portion of IAS 27 Consolidated and Separate Financial Statements that addresses the accounting for consolidated financial statements. It also includes the issues raised in SIC 12 Consolidation – Special Purpose Entities. IFRS 10 establishes a single control model with a new definition of control that applies to all entities. The changes will require management to make significant judgment to determine which entities are controlled and therefore required to be consolidated by the parent. Therefore, IFRS 10 may change which entities are within a Group.

IFRS 11 replaces IAS 31 Interest in Joint Ventures and SIC 13 Jointly Controlled Entities– Non-monetary Contributions by Ventures. IFRS 11 uses some of the terms that were used in IAS 31 but with different meanings which may create some confusion as to whether there are significant changes. IFRS 11 focuses on the nature of the rights and obligations arising from the arrangement compared to the legal form in IAS 31. IFRS 11 uses the principle of control in IFRS 10 to determine joint control which may change whether joint control exists. IFRS 11 addresses only two forms of joint arrangements; joint operations where the entity recognises its assets, liabilities, revenues and expenses and/or its relative share of those items and joint ventures which is accounted for on the equity method (no more proportional consolidation).

IFRS 12 includes all the disclosures that were previously required relating to an entity’s interests in subsidiaries, joint arrangements, associates and structured entities as well as a number of new disclosures. An entity is now required to disclose the judgments made to determine whether it controls another entity.

The company will need to consider the new definition of control to determine which entities are controlled or jointly controlled and then to account for them under the new standards. IFRS 10, 11 and 12 will be effective for the Group 1 July 2013.

IFRS 13 establishes a single framework for all fair value measurement (financial and non-financial assets and liabilities). When fair value is required or permitted by IFRS 13 does not change when an entity is required to use fair value but rather describes how to measure fair value under IFRS when it is permitted or required by IFRS. There are also consequential amendments to other standards to delete specific requirements for determining fair value. The Company will need to consider the new requirements to determine fair values going forward. IFRS 13 will be effective for the Group from 1 July, 2013.

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

F stor the year ended 31 December, 2013.

Notes to the Financial Statements -Contd.

4730GLICO General 2013 Annual Report and Financial Statements

IFRS 13 Fair Value Measurement

IFRIC 14 Prepayments of a Minimum Funding Requirement (Amendment)

IFRS 13 establishes a single framework for all fair value measurement (financial and non-financial assets and liabilities). When fair value is required or permitted by IFRS 13 does not change when an entity is required to use fair value but rather describes how to measure fair value under IFRS when it is permitted or required by IFRS. There are also consequential amendments to other standards to delete specific requirements for determining fair value. The Company will need to consider the new requirements to determine fair values going forward. IFRS 13 will be effective for the Group from 1 July 2013.

The amendment to IFRIC 14 is effective for annual periods beginning on or after 1 January 2011 with retrospective application. The amendment corrects an unintended consequence of IFRIC 14, ‘IAS 19–The limit on a defined benefit asset, minimum funding requirements and their interaction’. Without the amendments, entities are not permitted to recognise as an asset some voluntary prepayments for minimum funding contributions. The amendment provides guidance on assessing the recoverable amount of net pension asset. The amendment permits an entity to treat the prepayment of a minimum funding requirement as an asset. The amendment is deemed to have no impact on the financial statements of the Company.

I) Accounting policy changes in the year of adoption - The amendment clarifies that, if a first-time adopter changes its accounting policies or its use of the exemptions in IFRS 1 after it has publishedan interim financial report in accordance with IAS 34 Interim Financial Reporting, it has to explain those changes and update the reconciliations between previous GAAP and IFRS.

Improvements to IFRSs (Issued in 2010)

The following summarises the six amendments included that will be effective for June 2012 year ends:

• IFRS 1 First-time Adoption of International Financial Reporting Standards

ii) Revaluation basis as deemed cost - The amendment allows first-time adopters to use an event-driven fair value as deemed cost, even if the event occurs after the date of transition, but before the first IFRS financial statements are issued. When such re-measurement occurs after the date of transition to IFRS, but during the period covered by its first IFRS financial statements the adjustment is recognised directly in retained earnings (or if appropriate, another category of equity).

The amendment clarifies disclosures by emphasizing the interaction between quantitative and qualitative disclosures and nature and extent of risks associated with financial instruments.

• IFRS 7 Financial Instruments Disclosures

The amendment clarifies that an entity will present an analysis of other comprehensive income foreach component of equity, either in the statement of changes in equity or in the notes to the financialstatements. The amendment is applied retrospectively.

• IAS 1 Presentation of Financial Statements - Clarification of Statement of Changes in Equity

The amendment clarifies that when the fair value of award credits is measured based on the value of the awards for which they could be redeemed, the amount of discounts or incentives otherwise granted to customers not participating in the award credit scheme is to be taken into account. The amendment is applied retrospectively.

• IFRIC 13 Customer Loyalty Programmes - Fair Value of Award Credit

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

F stor the year ended 31 December, 2013.

Notes to the Financial Statements - Contd.

GLICO General 2013 Annual Report and Financial Statements31

IAS 34 Interim Financial Statements -Significant events and transactionsThe amendment provides guidance to illustrate how to apply disclosure principles in IAS 34 and add disclosure requirements around circumstances likely to affect fair values of financial instruments and their classification.

(a) Product classificationThe Company issues contracts that transfer insurance risk. Insurance contracts are those contracts that transfer significant insurance risk. Such contracts may also transfer financial risk. As a general guideline, the Company defines as significant insurance risk, the possibility of having to pay benefits on the occurrence of an insured event that are at least 10% more than the benefits payable if the insured event did not occur.

Once a contract has been classified as an insurance contract, it remains an insurance contract for the remainder of its lifetime, even if the insurance risk reduces significantly during this period, unless all rights and obligations are extinguished or expire.

2.2 Insurance Contract

Insurance contracts and investment contracts are classified into two main categories, depending on the duration of risk and in accordance with the provisions of the Insurance Act 2006 (Act 724)

Non-Life Insurance business means insurance business of any class or classes other than life insurance business.

Classes of general insurance business include Aviation, Engineering, Fire, Marine, Motor, Personal,Workmen's Compensation and Employer's Liability insurance.

Motor insurance business means the business of affecting and carrying out contracts of insurance against loss of, or damage to, or arising out of or in connection with the use of, motor vehicles, inclusive of third party risks but exclusive of transit risks.

Personal accident insurance business means the business of affecting and carrying out contracts ofinsurance against risks of the persons insured sustaining injury as the result of an accident or of an accident of a specified class or dying as the result of an accident or of an accident of a specified class or becoming incapacitated in consequence of disease or of disease of a specified class.

Fire insurance business means the business of affecting and carrying out contracts of insurance, otherwise than incidental to some other class of insurance business against loss or damage to property due to fire, explosion, storm and other occurrences customarily included among the risksinsured against in the fire insurance business.

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

F stor the year ended 31 December, 2013.

Notes to the Financial Statements -Contd.

4732GLICO General 2013 Annual Report and Financial Statements

Estimates of salvage recoveries are included as an allowance in the measurement of the insurance liability for claims, and salvage property is recognised in other assets when the liability is settled. The allowance is the amount that can reasonably be recovered from the disposal of the property. Subrogation reimbursements are also considered as an allowance in the measurement of the insurance liability for claims and are recognised in other assets when the liability is settled. The allowance is the assessment of the amount that can be recovered from the action against the liable third party.

(i) Insurance Premium Revenue

(ii) Commissions

(iii) Interest Income

(iv) Dividend Income

For all insurance contracts, premiums are recognised as revenue (earned premiums) proportionally over the period of coverage. The portion of premium received on in-force contracts that relates to unexpired risks at the balance sheet date is reported as the unearned premium liability. Premiums are shown before deduction of commission and are gross of any taxes or duties levied on premiums.

Commissions receivable are recognised as income in the period in which they are earned.

Interest income fo r all interest-bearing financial instruments, including financial instruments measured at fair value through income statement is recognised within ‘investment income’ (Note 4)in the income statement using the effective interest rate method. When a receivable is impaired, the the Company reduces the carrying amount to its recoverable amount, being the estimated future cash flow discounted at the original effective interest rate of the instrument, and continues unwinding the discount as interest income.

Dividend income for equities is recognised when the right to receive payment is established – this is the ex-dividend date for equity securities.

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

2.3 Revenue Recognition

The company recognises an item of property, plant and equipment as an asset when it is probable that future economic benefits will flow to it and the cost can be reliable measured by the company.

Property, plant and equipment are stated at cost less accumulated depreciation and any impairment in value. Depreciation is provided on the depreciable amount of each asset on a straight-line basis over the anticipated useful life of the asset. The depreciable amount related to each asset is determined as the difference between the cost and the residual value of the asset. The residual value is the estimated amount, net of disposal costs that the company would currently obtain from the disposal of an asset in similar age and condition as expected at the end of the useful life of the asset.

When significant parts of property, plant and equipment are required to be replaced in intervals, the company recognises such parts as individual assets with specific useful lives and depreciationrespectively. The present value of the expected cost for the decommissioning of the asset after its use is included in the cost of the respective asset if the recognition criteria for a provision are met.

2.4 P roperty, Plant and Equipment

F stor the year ended 31 December, 2013.

Notes to the Financial Statements -Contd.

GLICO General 2013 Annual Report and Financial Statements33

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

The current annual depreciation rates for each class of property, plant and equipment are as follows:

Costs associated with day-to-day servicing and maintenance of assets is expensed as incurred. Subsequent expenditure is capitalized if it is probable that future economic benefits associated with the item will flow to the company.

An item of property, plant and equipment is derecognized upon disposal or when no future economic benefits are expected to arise from the continued use of the asset. Any gain or loss arising on derecognition of the asset (calculated as the difference between the net disposal proceeds and the carrying amount of the item) is included in the statement of comprehensive income in the year item is derecognized.

Residual values, useful lives and methods of depreciation for property and equipment are reviewed, and adjusted if appropriate, at each financial year end.

Furniture and Fittings 10%Machinery and Equipment 20%Motor Vehicles 20%Computers 33?%Tools and Accessories 50%

The carrying values of property, plant and equipment are reviewed for indications of impairmentannually, or when events or changes in circumstances indicate the carrying value may not be recoverable. If any such indication exists and where the carrying values exceed the estimated recoverable amount, the assets or cash-generating units to which the asset belongs are written down to their recoverable amount. The recoverable amount of property, plant and equipment is the greater of net selling price and value in use. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset.

For assets, excluding goodwill, an assessment is made at each reporting date as to whether there is any indication that previously recognised impairment losses may no longer exist or may have decreased. A previously recognised impairment loss is reversed only if there has been a change in the assumptions used to determine the assets recoverable amount since the last impairment loss was recognised. The reversal is limited so that the carrying amount of the asset does not exceed its recoverable amount, nor exceed the carrying amount that would have been determined, net of depreciation, had no impairment loss been recognised for the asset in prior years. Such reversal is recognised in the income statement unless the asset is carried at revalue amount, in which case the reversal is treated as a revaluation increase.

Impairment of Non-Financial Assets

Buildings, or part of a building, (freehold or held under a finance lease) and land (freehold or held under an operating lease) held for long term rental yields and/or capital appreciation and are not occupied by the Company are classified as investment property. Investment property is carried at fair value, representing open market value determined annually by external valuers. Changes in fair values are included in other operating income in the income statement account.

2.5 Investment Properties

F stor the year ended 31 December, 2013.

Notes to the Financial Statements - Contd.

4734GLICO General 2013 Annual Report and Financial Statements

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Financial assets within the scope of IAS 39 are classified as financial assets at fair value through profit or loss, loans and receivables, held-to-maturity investments, available-for-sale financial assets, or as derivatives designated as hedging instruments in an effective hedge, as appropriate. The companydetermines the classification of its financial assets at initial recognition.

Financial assets are recognized initially at fair value plus, in the case of investments not at fair valuethrough profit or loss, directly attributable transaction costs.

Purchases or sales of financial assets that require delivery of assets within the time frame established by regulation or convention in the marketplace (regular way purchases) are recognized on the trade date, i.e., the date that the Company commits to purchase or sale of the asset.

2.6 F inancial AssetsInitial Recognition

The company’s assesses at each reporting date whether there is any objective evidence that a financial asset or a group of financial assets is impaired. A financial asset or group of financial assets is deemed to be impaired if, and only if, there is objective evidence of impairment as a result of one or more events that has occurred after the initial recognition of the asset (an incurred “loss event”) and that loss event has an impact on the estimated future cash flows of the financial asset or the group of financial assets that can be reliably estimated. Evidence of impairment may include indications that the debtors or a group of debtors is experiencing significant financial difficulty, default or delinquency in interest or principal payments, the probability that they will enter bankruptcy in the estimated future cash flows, such as change in arrears or economic conditions that correlate with defaults.

The company’s financial assets include cash, short term-term deposits, trade and other receivables and loan and other receivables.

Impairment of Financial Assets

•

•

The rights to receive cash flows from the asset have expired; or

The company has transferred its rights to receive cash flows from the asset or has assumedan obligation to pay the received cash flows in full without material delay to a third party under a “pass-through” arrangement; and either (a) the company has transferred substantially all risks and rewards of the asset, or (b) the company has neither transferred nor retained substantially all the risk and rewards of the asset but has transferred control of the asset.

When the company has transferred its rights to receive cash flows from an asset or has assumed an obligation to pay the received cash flows in full without material delay to a third party under the “pass-through” arrangement, and has neither transferred nor retained substantially all the risks and rewards of the asset nor transferred control of the asset, a new asset is recognized to the extent of the company’s continuing involvement in the asset.

Derecognition of Financial Assets

A financial asset (or where applicable a part of a financial asset or part of a group of similar financial assets) is derecognized when:

F stor the year ended 31 December, 2013.

Notes to the Financial Statements -Contd.

GLICO General 2013 Annual Report and Financial Statements35

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Continuing involvement that takes the form of a guarantee over the transferred asset is measured at the lower of the original carrying amount of the asset and the maximum amount of consideration that the company could be required to repay.

2.1 F inancial Liabilities

Initial Recognition

Financial liabilities within the scope of IAS 39 are classified as financial liabilities at fair value through profit and loss, loans and borrowings, or as derivatives designated as hedging instruments in an effective hedge, as appropriate. The company determines the classification of its financial liabilities at initial recognition. Financial liabilities are recognised initially at fair value and in the case of loans and borrowings, directly attributable to transaction costs.

The company’s financial liabilities include trade and other payables, bank overdraft and loans and borrowings.

Subsequent Measurement

The measurement of financial liabilities depends on their classifications as follows:

Financial liabilities at fair value through profit and loss

Financial liabilities at fair value through profit and loss includes financial liabilities held for trading andfinancial liabilities designated upon initial recognition as at fair value through profit and loss. Financialliabilities are classified as held for trading if they are acquired for the purposes of selling in the near term. Gains and losses on liabilities held for trading are recognized in the income statement. The company has not designated any financial liabilities as at fair value through profit or loss.

After initial recognition, interest bearing loans and borrowings are subsequently measured at amortised cost using the effective interest rate method.

Gains and losses are recognized in the income statement when the liabilities are derecognized as well as through the amortisation process.

Insurance payables are recognised when due and measured on initial recognition at the fair value of the consideration received less directly attributable transaction costs. Subsequent to initial recognition, they are measured at amortised cost using the effective interest rate method.

Insurance payables are derecognised when the obligation under the liability is settled, cancelled or expired.

Loans and Borrowings