Embed Size (px)

Citation preview

Glass Factories under the

Industrial Emissions Directive

Sites, competition and investment potentials in Europe

Cologne, June 2014

Picture credits: left: flat glass cladding of DuMont’s house in Cologne, Germany; lower right: container glass manufacturing; both by courtesy of Compagnie de Saint-Gobain. Upper right: © palomita0306 / Fotolia.com, container glass factory in Ernstthal, Germany.

Extract

ecoprogecoprog

ecoprog GmbH

Glass Factories under the Industrial Emissions Directive

The market for modernisation measures at European glass factories will increase considerably in the years

to come: By 2020, about 14 billion EUR will be invested in the European glass industry – an annual increase

of up to 45 per cent in comparison to the past years’ average.

The main reason for this growth is the coming into force of the Industrial Emissions Directive (IED), which

defines EU-wide limit values for air and water emissions for different industrial sectors, from 2016 on. The

specific limit values are determined in the BAT reference documents (BAT stands for Best Available

Techniques) and the BAT conclusions. The glass industry is one of the first industries BAT conclusions have

already been published for. The content of these conclusions and the way the affected glass factories will

handle them thus also give a signal to other industries.

More than 420 European glass factories have to comply with the limit values from 2016 on. The limit values

for nitrogen oxides and sulphur oxides will be particularly challenging for many glass factory operators, both

in technical and financial terms – and especially in countries with so far less strict legal frameworks, as is the

case in many Eastern European states. However, there are also many glass factories lacking state-of-the-art

technology in countries such as France and Spain.

This means that most glass manufacturers have to invest in modernising their factories. Funds will go to

optimising individual production processes or to new technical components for flue gas cleaning, furnace

technology or sealing the melter.

In the light of this development, ecoprog has collected information on the affected glass factories and

calculated the investment potentials by country.

The study “Glass Factories under the Industrial Emissions Directive” includes:

A detailed analysis of the IED, the BAT conclusions and other important legal frameworks as well as

the assessment of their importance for the glass industry.

Description and analysis (by country) of more than 420 European glass factories falling under the

IED criteria, including technical data, contact addresses and a geographical presentation of the

largest national markets in Europe.

A reliable estimation of future investment volumes by country.

A competitive analysis of the most important glass manufacturers in the European market.

An overview of the most important plant technology and cost structures in the glass industry.

The study is available in German and English from 2,900,- EUR plus VAT.

Contact:

Marcel Siebertz

ecoprog GmbH

Tel. +49 221 788 03 88 – 14

Content

Glass factories under the Industrial Emissions Directive

ecoprog GmbH, www.ecoprog.com

ecoprogecoprog

Preface 11

Management summary 13

1 Background 17

1.1 Introduction 17

1.2 Differentiation 17

1.3 Definitions 19

2 Plant technology 20

2.1 Glass batch preparation 21

2.2 Glass melting and refining 21

2.3 Cooling and forming 25

2.4 Flue gas cleaning 26

3 Costs 27

3.1 Investment costs 27

3.2 Current costs 28

3.3 Costs for reducing emissions 29

4 Current legal framework and market factors 31

4.1 Industrial Emissions Directive (IED) 31

4.2 BAT conclusions for the glass industry 33

4.3 European Union Emission Trading Scheme 36

4.4 Concentration processes in Europe 39

4.5 Transport and dependencies 40

5 Glass factories and market 43

5.1 Glass factories 43

5.2 Market 48

6 Competition 55

6.1 Glass manufacturers 55

6.2 Technology providers 59

7 National markets and sites 61

7.1 Belgium 61

7.2 Bulgaria 69

7.3 Denmark 75

7.4 Germany 79

7.5 Estonia 99

7.6 Finland 103

7.7 France 108

7.8 Greece 120

7.9 Italy 125

7.10 Croatia 139

7.11 Latvia 143

7.12 Lithuania 147

7.13 Luxembourg 151

7.14 Netherlands 153

7.15 Norway 160

7.16 Austria 165

7.17 Poland 171

7.18 Portugal 183

7.19 Romania 189

7.20 Sweden 195

7.21 Slovakia 199

7.22 Slovenia 205

7.23 Spain 209

7.24 Czech Republic 223

7.25 Hungary 232

7.26 United Kingdom 239

Data origin and methodology 248

Glossary 251

European glass factory register 252

Figures

Glass factories under the Industrial Emissions Directive

ecoprog GmbH, www.ecoprog.com

ecoprog

Figure 1: Analysed area 18

Figure 2: Schematic illustration of a glass factory 20

Figure 3: Types of glass furnaces in European glass factories 22

Figure 4: Model of a regenerative glass furnace, end-port 23

Figure 5: Model of a recuperative glass furnace, side-port 24

Figure 6: Melting capacities of different types of furnaces 25

Figure 7: Melting steps during glass production 26

Figure 8: Overview investment costs 27

Figure 9: Breakdown of investment costs in glass factories 28

Figure 10: Current costs of glass manufacturing 29

Figure 11: Investment costs for emission reduction measures 30

Figure 12: BAT emission ranges for air emissions 34

Figure 13: Upper BAT limit values for wastewater 35

Figure 14: Kyoto goals and status of implementation in Europe 36

Figure 15: European Union Emission Trading Scheme: price development 38

Figure 16: Development of glass production in Europe 2002-2012 39

Figure 17: Production and foreign trade balance of European glass industry 2012 41

Figure 18: Overview of other industries 41

Figure 19: IED glass factories in Europe 43

Figure 20: Production capacities in Europe 44

Figure 21: Production capacity by type of glass and region 44

Figure 22: Annual glass production in Europe 45

Figure 23: Glass factories in Europe 46

Figure 24: Glass industry country data 47

Figure 25: Market forecast Europe 48

Figure 26: Investment potential by industrial sector in Europe 2014-2020 49

Figure 27: Emission reduction measures 49

Figure 28: Estimated technology investments by region 50

Figure 29: Market volume Europe 2014-2020 51

Figure 30: Investments over course of time in Europe 2014-2020 52

Figure 31: Investment potentials by country 53

Figure 32: Market volume investments in glass factories 2014-2020 (million EUR) 54

Figure 33: Top 15 of European glass manufacturers 55

Figure 34: The ten largest glass factory operators in Europe 56

[…]

Figure 180: Structure of glass industry in the United Kingdom 239

Figure 181: Analysed sites by industrial sector in the United Kingdom 240

Figure 182: Glass production in the United Kingdom 241

Figure 183: Glass industry’s energy purchase in the United Kingdom 241

Figure 184: Glass factories in the United Kingdom 242

Figure 185: Investment potential by industrial sector in the United Kingdom 2014-2020 243

Figure 186: Market forecast United Kingdom 244

Figure 187: Differentiation of market regions 248

Extract, Chapter 4, Current legal framework and market factors

Glass factories under the Industrial Emissions Directive 33

ecoprog GmbH, www.ecoprog.com

ecoprog

4.2. BAT conclusions for the glass industry

The Industrial Emissions Directive says that the BAT reference documents (BAT stands for best

available techniques), also called BREFs, should define emission limit values (ELVs) for the

different industrial sectors.

The current BAT reference document for the glass industry was published in February 2012 as an

update of the first BREF from 2000. Furthermore, the legally binding conclusions were published in

all EU national languages for the first time within the framework of the IED. The conclusions

illustrate the summed up ELVs. The glass industry is one of the first industries BAT conclusions

have been completed for.

In practice, the EU-wide obliging limit values affect:

Glass manufacturing plants (including glass fibre) with a melting capacity of over 20 tons

per day and

plants melting mineral material (including mineral fibre production) with a melting capacity

of over 20 tons daily.

The BAT documents define upper emission limit values for these facilities. The specific values are

ranges from lower to upper limit values. The upper values reflect the maximum allowable limit

values, the lower the currently possible values that can be reached when applying BAT.

The upper limit values have only changed slightly in comparison to the 2000 BREF. Many lower

limit values, by contrast, have declined considerably due to technological advances. You will find

the differences when looking at the details. The limit values for hydrogen fluoride, for instance,

were tightened significantly.

Figure 12: BAT emission ranges for air emissions

Parameter

Container glass Flat glass Glass fibre/mineral wool

Mg/Nm³ kg/t glass Mg/Nm³ kg/t glass Mg/Nm³ kg/t glass

Dust 10-20 0.015-0.06 10-20 0.025-0.05 10-20 0.02-0.05

Carbon monoxide 100 - 100 - 100 -

Nitrogen oxides NO2 100-800 0.3-1.2 400-1.200 1-3 200-700 0.4-1.25

Sulphur oxides SO2

(natural gas furnace) 200-500 0.3-0.75 300-500 0.75-1.25

50-1,400 0.1-3.5 Sulphur oxides SO2

(heating oil furnace) 500-1,200 0.75-1.8 500-1,300 1.25-3.25

Emission ranges for the most important emission sources, simplified and grouped illustration. Source: Official Journal of the European Union 2012

The limit values for nitrogen oxides and sulphur oxides are the most decisive ones. Complying with

these values is the toughest challenge for most glass factory operators.

The most significant change, however, is not the tightening of individual values (as those were only

changed in specific cases). The fact that these values are now obliging throughout the EU and are

no longer only recommending, is much more important. […]

Extract, Chapter 7, National markets and sites, France

Glass factories under the Industrial Emissions Directive 108

ecoprog GmbH, www.ecoprog.com

ecoprog

7.7 France

Inhabitants [million] 66 Production sites under IED 46

EU ranking glass production [No./26] 2 Ø capacity of sites [estimated in 1,000 t/a] 93

EU ranking investments 2014-2020 [Nr./26] 4 Investments 2014-2020 [million EUR] 1,417

Management summary

France has the second largest glass manufacturing industry in Europe. Investments to modernise it

have been low in the past years. Many glass factories are out-of-date and some of them even lack

flue gas cleaning. There thus is a pressure to modernise this infrastructure, which is one again

intensified by the IED. This is why investments in modernising the French glass factories will

increase within the next two years especially.

Structure of the glass industry

France is one of the largest European glass manufacturers. About 1,300 companies are active in

this industry. The French industry is dominated by large enterprises: its 88 active large companies

employ 87 per cent of all staff and generate about 90 per cent of the overall industry’s turnover.

The IED affects 46 manufacturing sites, where approximately 20 per cent of the industry’s

employees work.

Figure 71: Structure of glass industry in France

< 50 employees 50+ employees Total EU ranking (No./26)

Companies 1,215 88 1,303 3

Staff 5,203 41,895 47,098 2

Turnover [m EUR] 764 6.901 7.665 2

[…]

6%

27%

55%

4%8%

Share of employees per sector

2%

35%

28%1%

34%

Share of enterprises per sector

13%

28%

45%

8%6%

Share of total revenue per sector

Source: Eurostat 2013

Flat glass

Processing of flat glass

Container glass

Glass fibre

Other

Share of turnover per sector

Extract, Chapter 7, National markets and sites, Italy

Glass factories under the Industrial Emissions Directive 128

ecoprog GmbH, www.ecoprog.com

ecoprog

Figure 41: Glass factories in Italy

Map for extract:

The map in the study will show all sites.

Extract, Chapter 7, National markets and sites, Poland

Glass factories under the Industrial Emissions Directive 172

ecoprog GmbH, www.ecoprog.com

ecoprog

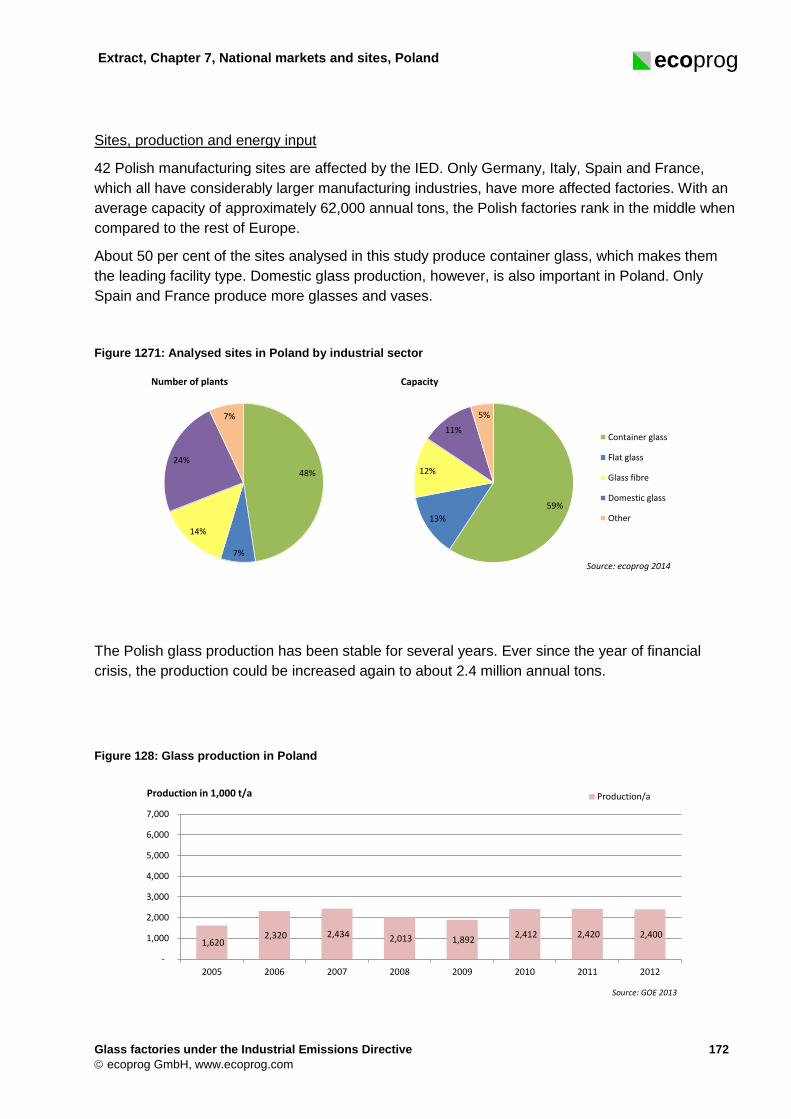

Sites, production and energy input

42 Polish manufacturing sites are affected by the IED. Only Germany, Italy, Spain and France,

which all have considerably larger manufacturing industries, have more affected factories. With an

average capacity of approximately 62,000 annual tons, the Polish factories rank in the middle when

compared to the rest of Europe.

About 50 per cent of the sites analysed in this study produce container glass, which makes them

the leading facility type. Domestic glass production, however, is also important in Poland. Only

Spain and France produce more glasses and vases.

Figure 1271: Analysed sites in Poland by industrial sector

The Polish glass production has been stable for several years. Ever since the year of financial

crisis, the production could be increased again to about 2.4 million annual tons.

Figure 128: Glass production in Poland

48%

7%

14%

24%

7%

Number of plants

59%

13%

12%

11%

5%

Capacity

Container glass

Flat glass

Glass fibre

Domestic glass

Other

Source: ecoprog 2014

1,620 2,320 2,434 2,013 1,892

2,412 2,420 2,400

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2005 2006 2007 2008 2009 2010 2011 2012

Production/aProduction in 1,000 t/a

Source: GOE 2013

Extract, Chapter 7, National markets and sites, Romania

Glass factories under the Industrial Emissions Directive 191

ecoprog GmbH, www.ecoprog.com

ecoprog

[…]

Sites, production and energy input

[…]

Most Romanian glass factories use natural gas. Heating oil also continues to play an important role

for generating energy, which is a sign for partly out-of-date factories, as natural gas is the

dominating fuel type of more recent glass furnaces.

Figure 141: Glass industry’s energy purchase in Romania

Adjustment and modernisation needs

About 24 million EUR have been invested annually in the Romanian glass industry over the past

years. This is circa 11 per cent of the overall industry’s turnover.

The nine affected glass factories will have to invest large amounts after the new limit values are put

into national law. The values are either significantly stricter than the ones in effect or they will be

introduced for the first time.

The best investment opportunities for modernisations and new constructions will develop in the flue

gas cleaning sector. Investments will especially increase in 2016 and 2017. In line with its large

production volume, the container glass industry will face the highest investment needs.

Figure 142: Investment potential by industrial sector in Romania 2014-2020

[…]

1020

0

100

200

300

400

500

600

Electricity Heat

million €

31%

68%

1%

Oil

Gas

District heat

Share of thermal energy per fuel type

21%

76%

3%Flat glass

Processing of flat glass

Container glass

Glass fibre

Other

Share of energy purchase by type of glass

Source: Estimation based on Eurostat

152 -

1,000

2,000

3,000

4,000

5,000

Investmentsum

million €

18%

56%

26% Flat glass

Container glass

Glass fibre

Other

Source: prognosis by ecoprog

Extract, Chapter 7, National markets and sites, Austria

Glass factories under the Industrial Emissions Directive 168

ecoprog GmbH, www.ecoprog.com

ecoprog

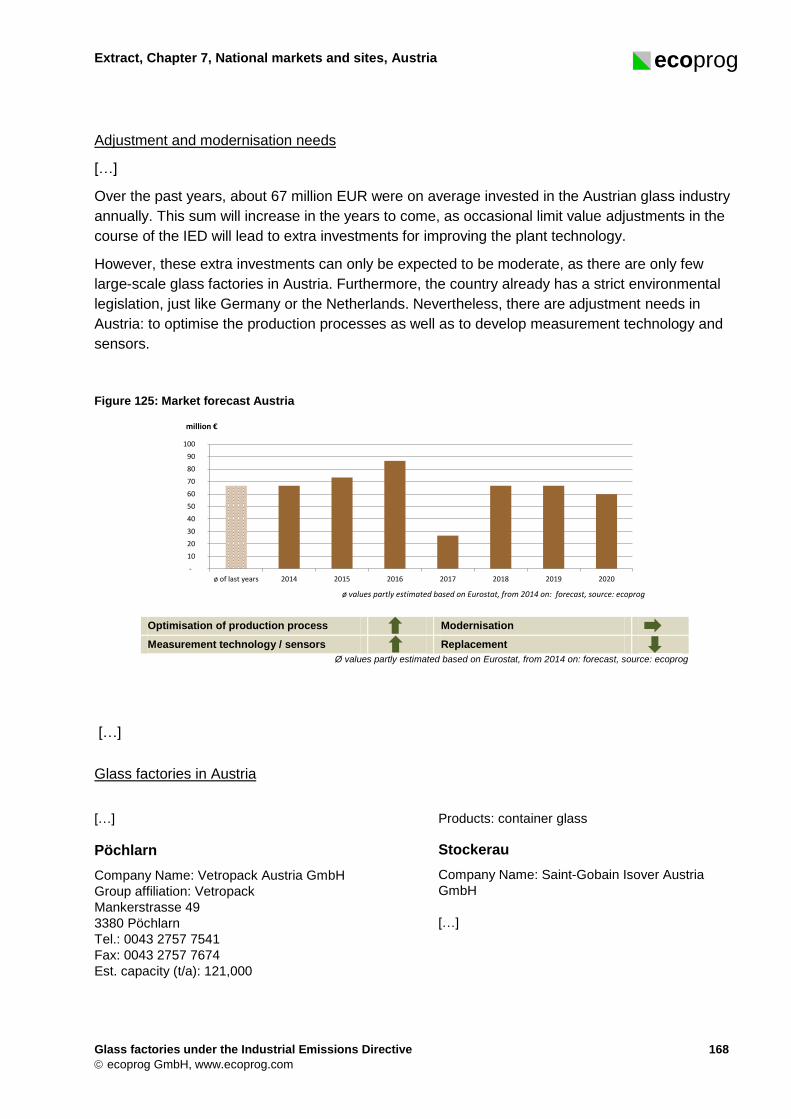

Adjustment and modernisation needs

[…]

Over the past years, about 67 million EUR were on average invested in the Austrian glass industry

annually. This sum will increase in the years to come, as occasional limit value adjustments in the

course of the IED will lead to extra investments for improving the plant technology.

However, these extra investments can only be expected to be moderate, as there are only few

large-scale glass factories in Austria. Furthermore, the country already has a strict environmental

legislation, just like Germany or the Netherlands. Nevertheless, there are adjustment needs in

Austria: to optimise the production processes as well as to develop measurement technology and

sensors.

Figure 125: Market forecast Austria

Optimisation of production process Modernisation

Measurement technology / sensors Replacement Ø values partly estimated based on Eurostat, from 2014 on: forecast, source: ecoprog

[…]

Glass factories in Austria

[…]

Pöchlarn

Company Name: Vetropack Austria GmbH

Group affiliation: Vetropack

Mankerstrasse 49

3380 Pöchlarn

Tel.: 0043 2757 7541

Fax: 0043 2757 7674

Est. capacity (t/a): 121,000

Products: container glass

Stockerau

Company Name: Saint-Gobain Isover Austria

GmbH

[…]

-

10

20

30

40

50

60

70

80

90

100

ø of last years 2014 2015 2016 2017 2018 2019 2020

million €

ø values partly estimated based on Eurostat, from 2014 on: forecast, source: ecoprog

Extract, Chapter 7, National markets and sites, United Kingdom

Glass factories under the Industrial Emissions Directive 246

ecoprog GmbH, www.ecoprog.com

ecoprog

Glass factories in the United Kingdom

[…]

UK-08

Wigan

Company Name: PPG Industries (UK) ltd

Group affiliation: PPG

Leigh Road Hindley Green

WN2 4XG Wigan

Tel.: 0044 1942 257161

Fax: 0044 1942 522385

Est. capacity (t/a): 54,000

Products: fiber glass

Remarks: The plant is using oxygen melting

technology.

UK-09

Runcorn

Company Name: BPB United Kingdom Limited

Group affiliation: Saint Gobain

Whitehouselnd Estate

WA7 3DP Runcorn

Est. capacity (t/a): 25,000

Products: insulation wool

UK-10

Leeds

Company Name: Allied Glass Containers Ltd

Group affiliation: AGC

South Accommodation Road

LS10 1NQ Leeds

Tel.: 0044 113 2451568

Fax: 0044 113 2449349

Est. capacity (t/a): 75,000

Products: glass bottles

UK-11

Barnsley

Company Name: Ardagh Glass Limited

Group affiliation: Ardagh

Bouron Road Monk Bretton

S71 SQG Barnsley

Tel.: 0044 1226710211

Fax: 0044 1226 716808

Est. capacity (t/a): 182,000

Products: packaging glass

UK-12

Pencoed

Company Name: Rockwool Limited

Group affiliation: Rockwool

CF35 6NY Pencoed

Tel.: 0044 1656 862621

Est. capacity (t/a): 197,000

Products: mineral wool, insulation

Employees: 350

UK-13

Knottingley 1

Company Name: Allied Glass Containers Ltd

Group affiliation: AGC

Fernley Green Road

WF11 8DH Knottingley 1

Tel.: 0044 1977 672661

Est. capacity (t/a): 65,000

Products: glass bottles

UK-14

Knottingley 2

Company Name: Ardagh Glass Limited

Group affiliation: Ardagh

Headlands Lane

W11 0HP Knottingley 2

Tel.: 0044 1977 674111

Fax: 0044 1977 635821

Est. capacity (t/a): 84,000

Products: packaging glass

[…]

ecoprog

Price and product information

Contact:

+49 (0) 221 788 03 88 14

You can order the market report here:

https://www.ecoprog.com/publikationen/energiewirtschaft/glaswerke-ier/order-glaswerke.htm

Price models:

Single user copy: 2,900,- EUR plus VAT

Company version: 5,800,- EUR plus VAT

Corporate version: POA

Explanation:

Single user copy: personal copy (personalised and password-protected PDF file, sent via e-mail)

Company version: company-wide copy (legal entity), sent via email

Corporate version: for different, legally connected companies (e.g. sister companies, subsidiaries abroad). Price depends on number of companies and employees

Additionally, you can order copies of the study on paper (hardcover book).

Price: 150,- EUR plus VAT per book.

![].pdf · Best Available Techniques (BAT) Reference Document for Common Waste Gas Management and Treatment Systems in the Chemical Sector . Industrial Emissions Directive 2010/75/EU](https://img.pdfslide.us/doc/110x75/5f40727f171ef02d0d32a4a8/1pdf-best-available-techniques-bat-reference-document-for-common-waste-gas.jpg)