Embed Size (px)

Citation preview

Ghent University, Department of Applied Mathematics, Computer Science and Statistics

Hedging and pricing of life insurance portfolios

Helene De Coninck

promotor: Prof. dr. M. Vanmaele

Thesis written to obtain a Master in Science in Mathematics:Applied Mathematics.

Academic Year: 2014-2015

Ghent University, Department of Applied Mathematics, Computer Science and Statistics

Hedging and pricing of life insurance portfolios

Helene De Coninck

promotor: Prof. dr. M. Vanmaele

Thesis written to obtain a Master in Science in Mathematics:Applied Mathematics.

Academic Year: 2014-2015

Preface

This thesis has been written with help from my promotor Prof. dr. M. Vanmaele. So specialthanks to her for all her tips and comments.Further I would like to thank her for first interesting me in the subject of financial mathematics.After attending her course “Financiele Wiskunde” in the second year of my education, I knewthe direction I wanted to go next. After achieving a Bachelor in Mathematics, the choice of aMaster in Applied Mathematics was easily made. To further deepen myself in the world of in-surance and financial mathematics I opted for the minor Economics and Insurance. Ultimately,all of it has led to writing this thesis.

I also would like to express my gratitude to my math teachers in high school, who first in-troduced me into the world of mathematics.Acknowledgment should go to all professors of Mathematics at Ghent University for givingtheir students such a broad knowledge about the matter as well as teaching us to be critical andindependent. We have not just learned definitions, theorems, lemmas and proofs by heart; wehave learned to work logically, structural and efficient, making fact-based conclusions, usingwhat already is at hand. As Gyorgy Polya1 once has said:

“Mathematics is being lazy. Mathematics is letting the principles do the work for you so thatyou do not have to do the work yourself”.

I also want to thank my parents for giving me the chance to develop myself as a person, forletting me choose my own directions in life and for supporting me through my years of study,both financially as mentally. They have done a wonderful job on raising my sister and me.

1Gyorgy Polya was a Hungarian mathematician born December 13, 1887 and died September 3, 1985 at theage of 97.

v

As author I give permission so that this thesis can be used for consultation and so that parts ofthis thesis may be copied for personal use only. Any other use falls directly under the limita-tions of the copyright, particularly one has the obligation to mention the source explicitly whenreferring to results in this thesis.

Date: Sunday 31st May, 2015 Signature: De Coninck, Helene

vi

Contents

1 Introduction 1

2 The basics of stochastic calculus 3

3 The risk-minimizing theory 153.1 The basics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 153.2 The discrete-time trading case . . . . . . . . . . . . . . . . . . . . . . . . . . 163.3 The continuous-time trading case . . . . . . . . . . . . . . . . . . . . . . . . . 193.4 The mixed continuous-discrete-time trading case . . . . . . . . . . . . . . . . 243.5 Comparison . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 303.6 Reconsideration of the GKW decomposition . . . . . . . . . . . . . . . . . . . 33

4 An affine stochastic mortality model 374.1 The setting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 374.2 The insurance contract . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 444.3 The survivor swap . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 574.4 The risk-minimization theory applied to survivor swaps . . . . . . . . . . . . . 604.5 Comparison of the risk . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 66

5 A Heath-Jarrow-Morton stochastic mortality model 695.1 The setting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 695.2 The insurance contract . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 735.3 The longevity bond . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 755.4 The risk-minimizing theory applied to longevity bonds . . . . . . . . . . . . . 845.5 The risk . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 91

6 Pricing theories 946.1 The pricing measure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 946.2 The indifference pricing theory . . . . . . . . . . . . . . . . . . . . . . . . . . 99

7 A mortality intensity model 1037.1 The setting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1037.2 The longevity risk price through the pricing measure . . . . . . . . . . . . . . 1127.3 The longevity risk price through indifference pricing . . . . . . . . . . . . . . 1147.4 Comparison . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 122

8 Conclusion 124

vii

CONTENTS

A Nederlandstalig samenvatting 127

B Proof second equality page 31-32 130

C Proof of Proposition 4.3.1 131

D Cramer’s method for Theorem 4.4.1 132

viii Pricing and hedging of life insurance portfolios H. De Coninck

List of Figures

2.1 A point process and its counting process, taken from Bremaud (1981). . . . . . 62.2 A three-variate point process and its counting process, taken from Bremaud

(1981). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

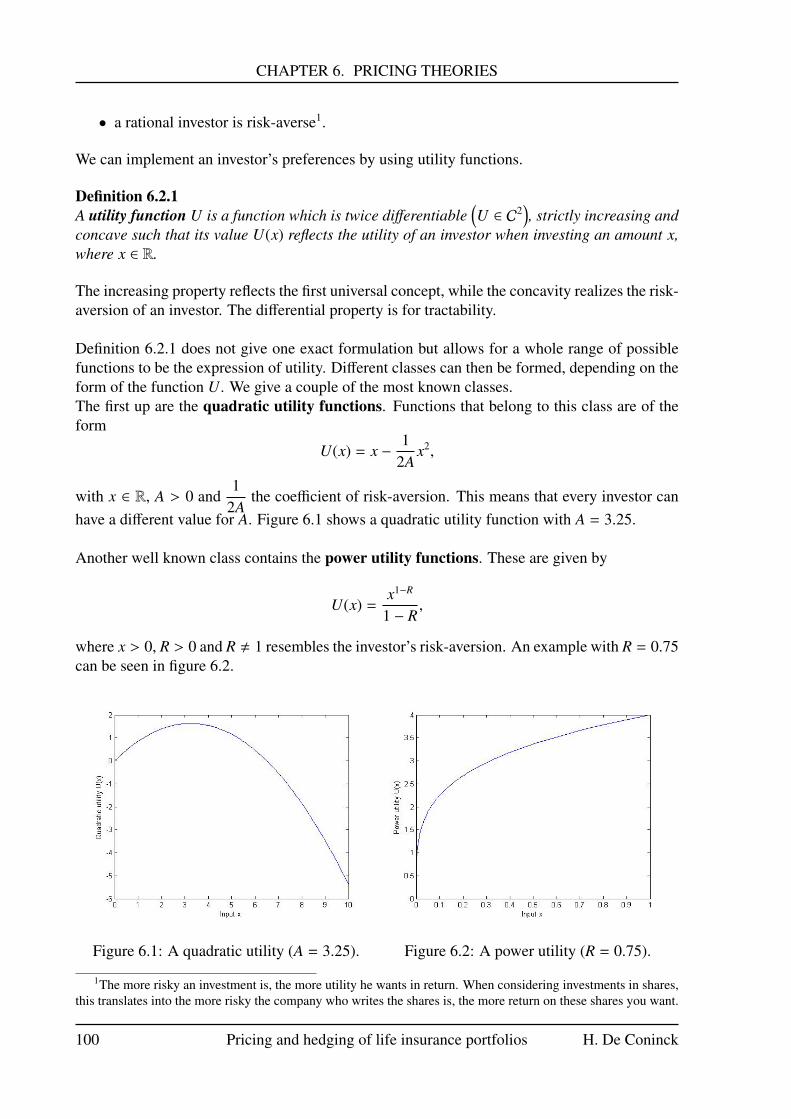

6.1 A quadratic utility (A = 3.25). . . . . . . . . . . . . . . . . . . . . . . . . . . 1006.2 A power utility (R = 0.75). . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1006.3 An exponential utility (γ = 5). . . . . . . . . . . . . . . . . . . . . . . . . . . 101

ix

Chapter 1

Introduction

In the world of today insurance is very important. They allow people to transfer their own riskin return for a price. This price can be a purchase price, which has to be paid only once, butone can also opt for periodical payments, called premiums. The price is paid by the insuredto either a person or company, called the insurer. In general one can choose freely to take onan insurance for a given price. In some cases however, insurance is compulsory. Think ofmotor insurance, employer’s liability (also known as occupational accident insurance effectedby employers) or insurance that is mandatory in the scope of the exercised activities, such ashunting policies, professional liability insurance et cetera1. We should note that despite thefact these insurance policies are compulsory, one is still allowed to choose the insurer. Othertypes of insurance are optional such as legal expenses insurance, life insurance, private healthinsurance, third party fire and theft car insurance, hail insurance and so on. Besides being nolonger responsible for the consequences of the risks you have insured, insurance can also haveother advantages. Life insurance, for example, can be an alternative manner of saving (insteadof depositing your money at a bank account, you could invest it in a life insurance). If one isalive when the contract terminates, you receive a capital. So this type of insurance can be seenas an investment of money, that at the end pays you back a certain amount. Some policies havefiscal advantages, which makes them more attractive than other investment options.

While the insured is disposed of his risk, the insurer has to be able to handle the prospect-ive risk. Since you can never tell for sure whether a risk will unfold or when it will happen,undertaking risk is relatively unpredictable. Throughout the years different methods, modelsand rules have been set up, trying to make realistic predictions about risk occurrences, abouthow much money they will cost the insurer, what kind of catastrophes may happen and whatthe impact will be on the insurer’s position,...One important feature of selling insurance contracts, is that the insurer has to be able to meet hisliabilities. In order to do so, the insurer will first have to determine correct prices for his con-tracts. This means that one needs to ask premiums or purchase prices which are high enough tocover the accepted risks. On the other hand the insurer must maintain sufficiently low prices sothat people will keep on buying those products and not the ones from the competition. Secondly,the money the insurer receives has to be invested properly in order to cover the (future) liab-ilities, as well as other costs that come with running an insurance business. This, in general,

1If you wish more information about this topic, you can always contact the FOD (Federal Government Service)or the FSMA (Financial Services and Markets Authority) or visit their websites.

1

CHAPTER 1. INTRODUCTION

is also referred to as hedging and can be done in many different ways. The most basic wayis to deposit money at a bank so that over time it accrues interest. Other options are to investin assets such as bonds, real estate, shares, commodities or derivatives. Depending on the typeof product, the investment can have a higher return but this will be at the expense of a higher risk.

In this thesis we will only consider life insurance contracts and focus on the two aspects men-tioned in the previous paragraph, namely the hedging and pricing. The first (and biggest) partwill cover the hedging. To begin with, we give an introduction to the risk-minimizing theorywhich will be used to derive the hedging formulas. We will discuss three trading settings: thediscrete-time trading case, the continuous-time trading case and the mixed continuous-discrete-time trading case. Chapters 4 and 5 start with describing a market setting, after which theexplanation of an insurance contract and a financial instrument follows. To the latter we thenapply the risk-minimizing theory. At the basis of chapters 3 to 5 are the papers of Dahl et al.(2011), Dahl et al. (2008), Follmer and Schweizer (1989) and Barbarin (2008).The contracts we will consider, are relatively simple. Nowadays, a lot of variations on suchcontracts can be made, allowing for different payments depending on the situation. Differencescan also arise in premiums and interest rates. They can be fixed, variable, (not) guaranteed orguaranteed until a certain level and so one. Some policies allow for profit sharing. Dependingon the profit, the insurer pays the contract holders an additional sum of money. On top of thatone can often include several options in the contract, making it more tailor made.

Chapter 6 gives again an introduction, but about pricing theories. We will highlight two differ-ent strategies in pricing: the equivalent martingale measure and the indifference pricing theory.The first method is widely known and frequently used in scientific literature. The second methodoriginates from a more economic perspective, but is also quite often used in papers. Many morecan be considered, though. For example, one could apply the well known Markowitz theory. Inthe work of Kahane (1979) one can find the application of this method along with advantagesand disadvantages. One can also use premium principles, where one derives a functional basedon a set of given axioms that premiums should follow. More details can be found in Tsanakasand Desli (2005). In chapter 7 we apply both theories to a simplified setting and we comparetheir outcomes. The pricing part is mainly based on Hainaut and Devolder (2008).The thesis will end with a conclusion about the methods used. In the appendix that follows, onecan find a brief summary of this thesis in Dutch.

2 Pricing and hedging of life insurance portfolios H. De Coninck

Chapter 2

The basics of stochastic calculus

Before we bring up the actual subject of this thesis, we give a more informative chapter. Theidea is to bring forward a couple of basics of stochastic calculus as well as introducing conceptsthat will be used throughout this work.

In general we work in a probability space (Ω,F ,P), where Ω is the space of all possible out-comes, F is a σ-algebra on Ω and P a probability measure. We call F the corresponding filtra-tion. The time interval that we will work on is defined by [0,T ] with T strictly positive.First we introduce some definitions and widely known concepts which can be found in Contand Tankov (2004), Dahl et al. (2011), Follmer and Sondermann (1986), Protter (2004), Jacodand Shiryaev (2003), Bremaud (1981) and Joshi (2008).

Definition 2.0.1A process X(t)t∈[0,T ] is called F-measurable if for all t ∈ [0,T ], X(t) is known conditional onF (t).

We also say that X(t)t∈[0,T ] is F-adapted or F-non-anticipating.

Definition 2.0.2A process X(t)t∈[0,T ] is called predictable if it isP-measurable whereP is a σ-algebra generatedby all F-measurable, left-continuous processes on [0,T ] ×Ω.

Definition 2.0.3A random variable τ is called an F (t)-stopping time if for every t ∈ [0,T ], you have thatτ ≤ t ∈ F (t).

The above definition means that F (t) contains enough information to determine whether a cer-tain event, characterized by the random variable τ, has occurred or not. Or thus for everyt ∈ [0,T ] we know whether τ ≤ t ∈ F (t) or not.

Definition 2.0.4A function f is called cadlag1 if it is right-continuous and has (a) left limit(s).

An analogue definition can be made for caglad.

1The word cadlag is an abbreviation of the French “continu a droite, limite a gauche”.

3

CHAPTER 2. THE BASICS OF STOCHASTIC CALCULUS

Consider an investment portfolio with value process X(t)t∈[0,T ] and with D(t)t∈[0,T ] the discount-ing process. We have that

d(DX)(t) = D(t)dX(t) + X(t)dD(t) + dD(t)dX(t),

because of the chain rule. In some cases this expression can be simplified.

Proposition 2.0.1Assume an investment portfolio with value process X(t)t∈[0,T ] generates a cash flow C(t)t∈[0,T ]

which is F-adapted, then the dynamics of the discounted value process (DX)(t)t∈[0,T ] are givenby

d(DX)(t) = D(t)dC(t),

for every t ∈ [0,T ].

Definition 2.0.5A process M(t)t∈[0,T ] is a local martingale if there exists an increasing sequence of stoppingtimes (Tn)n≥0 such that lim

n→+∞Tn = +∞ almost surely and each stopped process M(t∧ Tn)t∈[0,T ] is

again a martingale.

Note that every martingale is a local martingale but the inverse does not necessarily hold.

Definition 2.0.6A process M(t)t∈[0,T ] is called a semimartingale if, for every t ∈ [0,T ], M(t) can be written as

M(t) = M(t) + A(t),

with M(t)t∈[0,T ] a local martingale that has a finite starting value M(0) and A(t)t∈[0,T ] an adapted,real-valued cadlag process that satisfies A(0) = 0 and has a finite variation.

This decomposition is not necessarily unique, but if we can find a process A(t)t∈[0,T ] that fulfillsthe conditions in the previous definition and is F-predictable then we call

(M + A

)(t)t∈[0,T ] the

canonical decomposition of M(t)t∈[0,T ]. Since there is at most one process just described, thecanonical decomposition is unique if we can find such a process A(t)t∈[0,T ].

Definition 2.0.7Consider a process X(t)t∈[0,T ] with finite variation. There exists a unique, increasing, F-predictableprocess A(t)t∈[0,T ] such that (X − A)(t)t∈[0,T ] is a local martingale. This process A(t)t∈[0,T ] is thecompensator of X.

The quadratic variation process of a process X(t)t∈[0,T ] is denoted by the bracket process [X, X](t)t∈[0,T ]

and is widely used. But there also exists an angle-bracket process 〈X, X〉 (t)t∈[0,T ], which givesthe conditional quadratic variation of X. This process is defined as the compensator of [X, X].

Proposition 2.0.2Let X(t)t∈[0,T ] be a semimartingale, then

[X, X](t)t∈[0,T ] = [X, X]c (t)t∈[0,T ] +∑

0≤s≤t

(∆X)2(s)

= 〈Xc, Xc〉 (t)t∈[0,T ] +∑

0≤s≤t

(∆X)2(s),

where [X, X]c is the continuous part of [X, X], Xc is the continuous local martingale part of Xand the last term forms the discontinuous part, being the jumps.

4 Pricing and hedging of life insurance portfolios H. De Coninck

CHAPTER 2. THE BASICS OF STOCHASTIC CALCULUS

Note that if X(t)t∈[0,T ] is continuous and X(0) = 0, we get the following equality:

[X, X](t)t∈[0,t] = [X, X]c(t)t∈[0,T ] = 〈Xc, Xc〉 (t)t∈[0,T ] = 〈X, X〉 (t)t∈[0,T ].

One of the most used formulas in stochastic mathematics is the Ito formula:

f (t,W(t))

= f (0,W(0)) +

∫ t

0

∂

∂sf (s,W(s))ds +

∫ t

0

∂

∂xf (s,W(s))dW(s) +

12

∫ t

0

∂2

∂x2 f (s,W(s))d[W,W](s),

where f : [0,T ] × R → R is a sufficiently differentiable function and W(t)t∈[0,T ] is a Brownianmotion under P.If X(t)t∈[0,T ] is a semimartingale, we can still make use of the above expression, but in a slightlyaltered form.

Theorem 2.0.1 (Ito formula for semimartingales)Let X(t)t∈[0,T ] be a semimartingale and f : [0,T ]×R→ R a sufficiently differentiable, continuousfunction, then we have that

f (t, X(t)) = f (0, X(0)) +

∫ t

0

∂

∂sf (s, X(s))ds +

∫ t

0

∂

∂xf (s, X(s−))dX(s)

+12

∫ t

0

∂2

∂x2 f (s, X(s))d [X, X]c (s) +∑

0≤s≤t∆X(s),0

(∆ f (s, X(s)) − ∆X(s)

∂

∂xf (s, X(s−))

),

with [X, X]c the continuous part of [X, X] and ∆ f (s, X(s)) = f (s, X(s))− f (s, X(s−)) and ∆X(s) =

X(s) − X(s−).

Definition 2.0.8A point process on the interval [0,+∞[ is a process described by a sequence of random vari-ables (Tn)n≥0 in [0,+∞[ such thatT0 = 0

Tn < +∞ and Tn < Tn+1.

These random variables are often referred to as the realizations of the point process.

One can match a counting process N(t)t≥0 with any point process. For n ≥ 0, this process isdefined as follows:

N(t) =

+∞∑n=0

ITn ≤ t =

n if t ∈ [Tn,Tn+1[+∞ if t ≥ T∞.

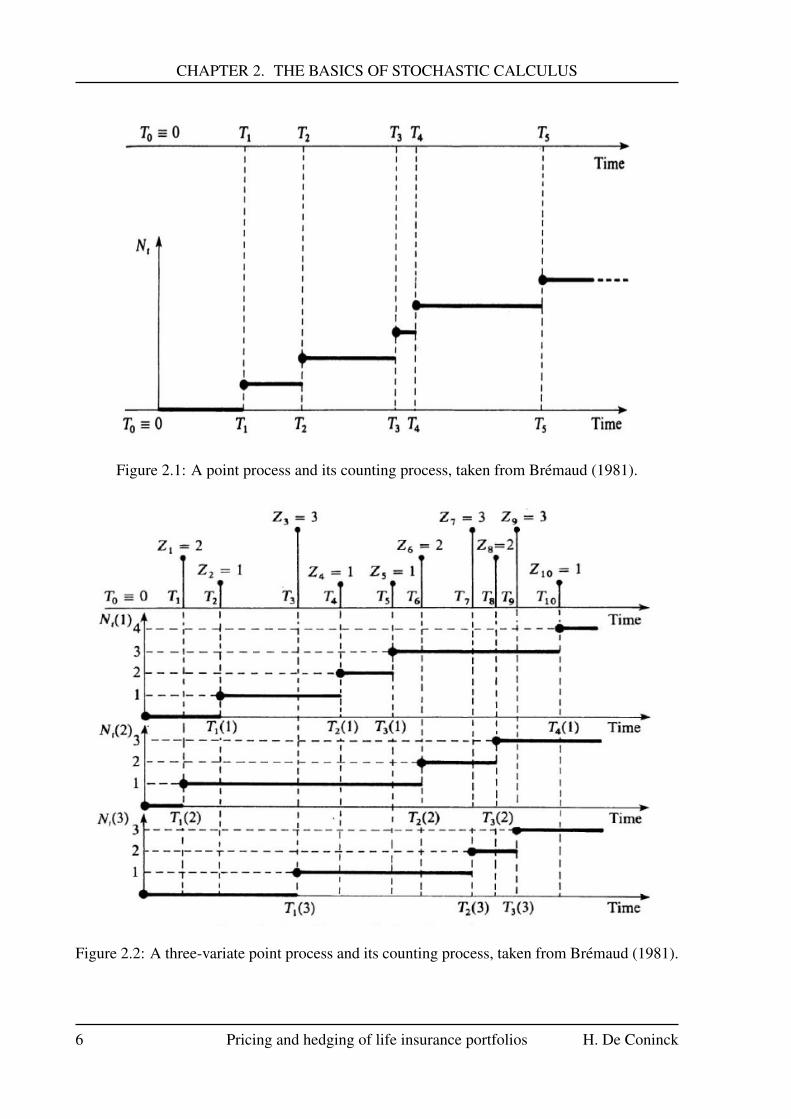

Note that by definition this counting process must be a right-continuous step function, that hasa starting value zero and exhibits jumps of magnitude one. Sometimes N(t)t≥0 is also called thepoint process.Figure 2.1, which can be found in Bremaud (1981), shows an example of a counting processmatched with the random variables (Tn)n≥0.

H. De Coninck Pricing and hedging of life insurance portfolios 5

CHAPTER 2. THE BASICS OF STOCHASTIC CALCULUS

Figure 2.1: A point process and its counting process, taken from Bremaud (1981).

Figure 2.2: A three-variate point process and its counting process, taken from Bremaud (1981).

6 Pricing and hedging of life insurance portfolios H. De Coninck

CHAPTER 2. THE BASICS OF STOCHASTIC CALCULUS

Definition 2.0.9A k-variate point process on a probability space (Ω,F ,P) is described by two sequences ofrandom variables (Tn,Zn)n≥0 such that:

• (Tn)n≥0 is a point process as in Definition 2.0.8,

• (Zn)n≥0 is a sequence that takes up values in the set 1, . . . , k.

For 1 ≤ x ≤ k and t ≥ 0, the corresponding counting process N(t, x)t≥0 is given by

N(t, x) =

+∞∑n=0

ITn ≤ tIZn = x.

Figure 2.2, which can be found in Bremaud (1981), shows a three-variate point process with itscorresponding counting process.

Definition 2.0.10An E-marked point process is a process described by a sequence of random variables (Tn,Zn)n≥0,with (Tn)n≥0 being a time-related random variable and (Zn)n≥0 being a magnitude-related ran-dom variable with values in the set E. This space E is called the mark space.If E = 1, . . . , k, we just have a k-variate point process (recall Definition 2.0.9).

The corresponding counting process is again

N(t, x) =

+∞∑n=0

ITn ≤ tIZn = x,

where now, x is an element in E.

Proposition 2.0.3A point process is P-non explosive if T∞ = lim

n→+∞Tn = +∞, which is equivalent with, for every

t ≥ 0, N(t) < +∞ P-almost surely.

Proposition 2.0.3 can be extended for k-variate point processes. We note that if the expectedvalue of the counting process is bounded, it is also integrable.

Definition 2.0.11A random variable X has a Poisson distribution with parameter λ if for all x in N (zero in-cluded) we have that

PX = x =e−λλx

x!.

If a random variable X is Poisson distributed with parameter λ, we write this as X ∼ P(λ).

Definition 2.0.12If a counting process N(t)t∈[0,T ] fulfills the following conditions:

1. for every t ∈ [0,T ] we have that N(t) is F (t)-adapted,

2. N(t)t∈[0,T ] has independent increments,

H. De Coninck Pricing and hedging of life insurance portfolios 7

CHAPTER 2. THE BASICS OF STOCHASTIC CALCULUS

3. N(t)t∈[0,T ] has stationary2 increments,

then N(t)t∈[0,T ] is called a Poisson process.

Proposition 2.0.4If N(t)t∈[0,T ] is a Poisson process, then there exists a λ ≥ 0 such that, for all t ∈ [0,T ], N(t) isPoisson distributed with parameter λt.This λ is called the intensity associated with the Poisson process N(t)t∈[0,T ].

Poisson processes have a couple of interesting properties. One that is often used, is that (N(t) −λt)t∈[0,T ], which is called the compensated Poisson process, is a martingale. Another propertyis given below.

Proposition 2.0.5If N(t)t∈[0,T ] is a Poisson process, then we have the next equalities for all t ∈ [0,T ]:

[N,N](t) = N(t) and 〈N,N〉 (t) = λt.

We also have that [N − λ,N − λ](t) = N(t). Note that the first equality in Proposition 2.0.5 isalso valid when N(t)t∈[0,T ] is just a counting process.

Definition 2.0.13Two random variables X and Y with finite variances are called orthogonal if E[XY] = 0.

In light of the previous definition we say that a random variable is orthogonal to a set if it isorthogonal to all random variables in this set.

Definition 2.0.14Two square-integrable (local) martingales are called orthogonal if their product is again a(local) martingale.

The definition of orthogonality of two martingales M1(t)t∈[0,T ] and M2(t)t∈[0,T ] is equivalent tothe following condition:

[M1,M2] = 0.

An important theorem that will be used frequently is the Galtchouk-Kunita-Watanabe decom-position. The theorem can by found in Cont and Tankov (2004). When referring to this theoremwe will use the abbreviation GKW instead of writing Galtchouk-Kunita-Watanabe.

Theorem 2.0.2 (Galtchouk-Kunita-Watanabe decomposition)Let M(t)t∈[0,T ] be a square-integrable martingale with respect to the equivalent martingale meas-ureQ. Any random variable H with finite variance depending on the history of M(t)t∈[0,T ] can berepresented as the sum of a stochastic integral with respect to M(t)t∈[0,T ] and a random variableNH, such that the martingale NH(t)t∈[0,T ] =

(EQ

[NH

∣∣∣F (t)])

t∈[0,T ]is orthogonal with respect to

M(t)t∈[0,T ].In other words, there exists a square-integrable, predictable process ϕ such that with probabilityone

H = EQ [H] +

∫ T

0ϕ(s)dM(s) + NH.

2We call increments stationary if the distribution of the increments is dependent on the length of the increments.Thus, if s ≤ t, k ≤ l and t − s = l − k then X(t) − X(s) should equal X(l) − X(k) in distribution.

8 Pricing and hedging of life insurance portfolios H. De Coninck

CHAPTER 2. THE BASICS OF STOCHASTIC CALCULUS

In particular, for any square-integrable, predictable process γ(t)t∈[0,T ],(NH(t)

∫ t

0γ(s)dM(s)

)t∈[0,T ]

is again a martingale.

Note that with “history” we mean all past values that the process has taken up since the startuntil the current moment, completed with all null sets.

We also state the next proposition, which will be frequently used.

Proposition 2.0.6Let X(t)t∈[0,T ] be a cadlag, square-integrable martingale and let ψ(t)t∈[0,T ] be a bounded, pre-

dictable process. Then∫ t

0ψ(s)dX(s) is also a square-integrable martingale.

Its local analogue is given by the next proposition.

Proposition 2.0.7Let X(t)t∈[0,T ] be a local martingale and ψ(t)t∈[0,T ] a locally bounded, predictable process. Then∫ t

0ψ(s)dX(s) is a local martingale.

Another important part of this thesis relies on Levy processes. We will give some importantdefinitions and features. For more details about these processes and their properties see Contand Tankov (2004), Applebaum (2004), Kuchler and Sørensen (1997) and Di Nunno et al.(2009).

Definition 2.0.15Let X be a random variable with distribution FX and u ∈ R. The moment generating functionof X is the function

φX(u) = E[euX

]=

∫ +∞

−∞

euxdFX(x).

In most literature mgf is used as the abbreviation for moment generating function. We will alsouse this notation.The mgf is of importance since taking the nth derivative with respect to u and then setting uzero, provides you with the nth moment. In particular, it is easy to find the mean and variance ifyou know the mgf.

Definition 2.0.16Let X be a random variable with distribution FX and u ∈ R, then

φX(iu) = E[eiuX

]=

∫ +∞

−∞

eiuxdFX(x)

is called the characteristic function of X.

One should note that the i in the previous definition is the irrational number i.

If a variable is Poisson distributed, then we have the following expression for the mgf (seeDefinitions 2.0.11 and 2.0.15). For the characteristic function an analogue expression can befound by using Definition 2.0.16.

φX(u) = E[euX

]H. De Coninck Pricing and hedging of life insurance portfolios 9

CHAPTER 2. THE BASICS OF STOCHASTIC CALCULUS

=

+∞∑x=0

eux fX(x) Poisson is a discrete distribution

=

+∞∑x=0

eux e−λλx

x!

= e−λ+∞∑x=0

(euλ)x

x!

= e−λeλeuseries expansion of e

= exp λ (eu − 1) .

Definition 2.0.17Let X(t)t∈[0,T ] be a stochastic process. If the following conditions are satisfied, we say thatX(t)t∈[0,T ] is a Levy process:

1. X(0) = 0 almost surely,

2. X(t)t∈[0,T ] has independent increments,

3. X(t)t∈[0,T ] has stationary increments,

4. X(t)t∈[0,T ] is stochastically continuous: (∀ε > 0) (∀s ≥ 0)(limt→sP |X(t) − X(s)| > ε = 0

).

A well known example of a Levy process is the Brownian motion. This is clear from its defini-tion, see for example Shreve (2004b).

Definition 2.0.18Let X(t)t∈[0,T ] be a Levy process and u ∈ R, then the characteristic function of X(t)t∈[0,T ] isdefined by

φX(t)(iu) = E[eiuX(t)

].

An analogue definition can be given for the mgf of X(t)t∈[0,T ].

The mgf and the characteristic function are related to one another:

φX(t)(u) = E[euX(t)

]by Definition 2.0.18

= E[e−i2uX(t)

]= φX(t)(i(−iu)).

By the previous relationship and because you can calculate the nth moment from the mgf, itis easy to see that by taking the nth derivative with respect to u of the characteristic function,dividing by in and then choosing u = 0, you also get the nth moment.

Definition 2.0.19For a Levy process X(t)t∈[0,T ] and u ∈ R we define the cumulant transform k as follows:

k(u) = ln E[exp uX(1)

]= ln φX(1)(u).

Before giving two of the most important theorems in connection with Levy processes: the Levy-Ito decomposition (Theorem 2.0.3) and the Levy-Khintchine representation (Theorem 2.0.4),we introduce some important measures and properties.

10 Pricing and hedging of life insurance portfolios H. De Coninck

CHAPTER 2. THE BASICS OF STOCHASTIC CALCULUS

Definition 2.0.20Let (A,A) be a measurable space. A random measure ν on (A,A) is a collection of randomvariables ν(B)B∈A such that:

1. ν(∅) = 0,

2. (σ-additive)

for every disjoint sequence of sets (Bn)n∈N inA, we have that ν

⋃n∈N

Bn

=∑n∈N

ν(Bn),

3. (independent scattered property)the measures ν(B1), . . . , ν(Bn) are independent for every disjoint family of sets (Bi)i=1,...,ninA.

Definition 2.0.21If ν is a random measure on a measurable space (A,A), then we say that ν is a Poisson randommeasure if for every B ∈ A with ν(B) < +∞, ν(B) has a Poisson distribution.

Lets consider a Levy process X(t)t∈[0,T ]. Its jumps are denoted by (∆X(t))t∈[0,T ]. We can thenassociate a Poisson random measure which counts the number of jumps that have given size.For A ∈ B

(Rd \ 0

)we get JX(t, A) =

∑0≤s≤t

I∆X(s) ∈ A, where B(Rd \ 0

)is the Borel set of

Rd \ 0.We can now define νX(A) as E [JX(1, A)], which is called the intensity of the Poisson randommeasure JX. The compensated Poisson random measure is then defined as JX(t, A) − tνX(A).

Definition 2.0.22Let A be a set, B(A) its Borel σ-algebra and ν a random measure on [0,+∞[×A. For everyB ∈ B(A) define the process ν(t, B)t∈[0,T ] = ν([0, t[×B)t∈[0,T ]. If there exists an element C ∈ B(A)such that ν(t,C)t∈[0,T ] is a martingale under the condition that the disjunction of the closure ofB and C is empty, or thus B ∩C = ∅, then ν is called a martingale-valued measure.

Proposition 2.0.8The compensated Poisson random measure JX(t, A) − tνX(A) for a Levy process X(t)t∈[0,T ] and aset A is a martingale-valued measure, or thus tνX is the compensator of JX.

The Levy-Ito decomposition allows one to “split” up the Levy process into different compon-ents: a time-related component, a Brownian motion part and the integral terms, which aredependent on the associated Poisson random measure.

Theorem 2.0.3 (Levy-Ito decomposition)Consider a Levy process X(t)t∈[0,T ]. There exists a vector γ in Rd, a d-dimensional Brownian mo-tion W(t)t∈[0,T ] with covariance matrix Σ, an independent Poisson random measure JX, definedon [0,+∞[×Rd \ 0, and its intensity νX such that for all t ∈ [0,T ] we have that

X(t) = γt + W(t) +

∫|x|<1

x (JX(t, dx) − tνX(dx)) +

∫|x|≥1

xJX(t, dx).

The intensity in this theorem is also called the Levy measure.The elements γ, νX and Σ characterize the Levy process so therefore (γ, νX,Σ) is called thecharacteristic triplet of X(t)t∈[0,T ].

H. De Coninck Pricing and hedging of life insurance portfolios 11

CHAPTER 2. THE BASICS OF STOCHASTIC CALCULUS

While the above theorem gives a decomposition of the Levy process itself, the Levy-Khintchinerepresentation gives a way to split up the characteristic function of the process.

Theorem 2.0.4 (Levy-Khintchine representation)Let X(t)t∈[0,T ] be a Levy process on Rd with characteristic triplet (γ, νX,Σ) and u ∈ Rd. Thecorresponding characteristic function is given by

φX(t)(iu) = exp(

iγtru −12

utrΣu +

∫Rd

(eiutr x − 1 − iutr xI|x| ≤ 1

)νX(dx)

)t.

Proposition 2.0.9A Levy process is a semimartingale.

Definition 2.0.23If a one-dimensional stochastic process X(t)t∈[0,T ] has a stochastic integral representation of thefollowing form:

X(t) = x +

∫ t

0α(s)ds +

∫ t

0β(s)dW(s) +

∫ t

0

∫R\0

γ(s, y)(J(ds, dy) − ν(dy)ds),

where α(t)t∈[0,T ], β(t)t∈[0,T ] and γ(t, y)t∈[0,T ] are predictable processes such that for all t ∈ [0,T ]and y ∈ R\0∫ t

0

(|α(s)| + β2(s) +

∫R\0

γ2(s, y)ν(dy))

ds < +∞,P-almost surely,

then we call X(t)t∈[0,T ] an Ito-Levy process.

Just as for semimartingales, we can find an adjusted form of the Ito formula for Ito-Levy pro-cess.

Theorem 2.0.5 (Ito formula for Ito-Levy process)Let X(t)t∈[0,T ] be an Ito-Levy process and f : [0,T ] × R → R a sufficiently differentiable,continuous function, then we have that

f (t, X(t))

= f (0, X(0)) +

∫ t

0

∂

∂sf (s, X(s))ds +

∫ t

0α(s)

∂

∂xf (s, X(s))ds +

∫ t

0β(s)

∂

∂xf (s, X(s))dX(s)

+12

∫ t

0β2(s)

∂2

∂x2 f (s, X(s))ds

+

∫ t

0

∫R\0

(f (s, X(s) + γ(s, y)) − f (s, X(s)) −

∂

∂xf (s, X(s))γ(s, y)

)ν(dy)ds

+

∫ t

0

∫R\0

( f (s, X(s−) + γ(s, y)) − f (s, X(s−))) (J(ds, dy) − ν(dy)ds) .

The differential form of the previous theorem is given by

d f (t, X(t))

=∂

∂tf (t, X(t))dt + α(t)

∂

∂xf (t, X(t))dt + β(t)

∂

∂xf (t, X(t))dX(t) +

12β2(t)

∂2

∂x2 f (t, X(t))dt

12 Pricing and hedging of life insurance portfolios H. De Coninck

CHAPTER 2. THE BASICS OF STOCHASTIC CALCULUS

+

∫R\0

(f (t, X(t) + γ(t, y)) − f (t, X(t)) −

∂

∂xf (t, X(t))γ(t, y)

)νX(dy)dt

+

∫R\0

( f (t, X(t−) + γ(t, y)) − f (t, X(t−))) (JX(dt, dy) − νX(dy)dt) .

Definition 2.0.24A subordinator is a one-dimensional, almost surely non decreasing Levy process.

Subordinators form a special class of Levy processes and are often used since they have goodproperties, such as tractability. Within the class of subordinators, you can find different sub-classes, depending on their properties. A more known subclass is the one formed by the α-stablesubordinators.In chapter 7 we will go deeper into this type of processes.

Proposition 2.0.10A process X(t)t∈[0,T ] is a subordinator if and only if its characteristic triplet is given by (γ, νX, 0),with:

1. νX(] −∞, 0]) = 0,

2.∫ 1

0xνX(dx) < +∞,

3. γ ≥ 0.

Proposition 2.0.11Every subordinator is of finite variation.

Proposition 2.0.11 gives an important feature of subordinators. Due to the finite variation prop-erty, the Levy-Ito decomposition from Theorem 2.0.3 and Levy-Khintchine representation fromTheorem 2.0.4 can be reduced. The next theorem gives the formulations.

Theorem 2.0.6 (Levy-Ito and Levy-Khintchine in the finite variation case)Let X(t)t∈[0,T ] be a Levy process with characteristic triplet (γ, νX, 0) and finite variation. Letu ∈ Rd. Then we get

X(t) = bt +

∫Rd

xJX(t, dx)

and

φX(t)(iu) = exp

ibtrut + t∫Rd

(eiutr x − 1

)νX(dx)

,

where b = γ −

∫|x|<1

xνX(dx) is the drift.

Last, the theorem of Fubini, which gives the conditions for swapping integrals in a doubleintegration, is introduced.

Theorem 2.0.7 (Fubini)Consider a measure space (X×Y,X⊗Y, p×q) with (X×Y) the product space of the sets X andY, (X ⊗ Y) the product σ-algebra of the minimal σ-algebras X and Y and (p × q) the product

H. De Coninck Pricing and hedging of life insurance portfolios 13

CHAPTER 2. THE BASICS OF STOCHASTIC CALCULUS

measure of the measures p and q on the spaces (X,X) and (Y,Y) respectively.Let f : X × Y → R be a function that is either integrable or non negative, then we have∫

X

(∫Y

f (x, y)dq(y))

dp(x) =

∫X×Y

f (x, y)d(p × q)(x, y) =

∫Y

(∫X

f (x, y)dp(x))

dq(y).

We note that there exists several variants of Fubini’s theorem. One of them can be used to swapsummation with an integral given that the considered function is positive, or thus if, for all xand n ≥ 0, fn(x) ≥ 0 we have that∫ ∑

n

fn(x)dx =∑

n

∫fn(x)dx.

For further basics on stochastic calculus we refer to Shreve (2004a), Shreve (2004b), Cont andTankov (2004) and Bjork (2009).

14 Pricing and hedging of life insurance portfolios H. De Coninck

Chapter 3

The risk-minimizing theory

3.1 The basicsWe first note that throughout the first part of this thesis, the following definitions are used unlessstated otherwise. Most of it can be found in Dahl et al. (2011).

Our goal is to trade assets in the general setting, introduced in chapter 2, in such a way thatthe risk we are exposed to, is minimal. This boils down to finding a trading strategy that min-imizes the risk.Consider a setting that contains d + 1 assets with X(t)t∈[0,T ] the d-dimensional discounted priceprocess of the first d assets and Y(t)t∈[0,T ] the discounted price process of the last asset. Weassume that all necessary integrability conditions are satisfied. Assume further that we have asavings account B and a payment process A(t)t∈[0,T ] of the hedger.

Definition 3.1.1In agreement with proposition 2.0.1, the corresponding discounted payment process A∗(t)t∈[0,T ]

is given by

A∗(t) = A(0) +

∫ t

0B−1(s)dA(s).

Instead of working under the original P-measure, we assume that there is an equivalent martin-gale measure Q such that (X(t),Y(t))t∈[0,T ] is a (d + 1)-dimensional martingale.

Definition 3.1.2A strategy ϕ is a sufficiently integrable process ϕ(t)t∈[0,T ] = (ξ(t), ϑ(t), η(t))t∈[0,T ], where ξ(t)t∈[0,T ]

is a d-dimensional, F-predictable process that gives the number of the first d assets held,ϑ(t)tt∈[0,T ] is a one-dimensional, F-predictable process that gives the number of the last assetheld and η(t)t∈[0,T ] is a one-dimensional, F-adapted process giving the discounted deposit in thesavings account.

Definition 3.1.3The discounted value process V∗(t, ϕ)t∈[0,T ] associated with the trading strategy ϕ is defined by

V∗(t, ϕ) = ξ(t)X(t) + ϑ(t)Y(t) + η(t).

Definition 3.1.4The intrinsic value process V∗,Q(t)t∈[0,T ] is defined as

(EQ[A∗(T )|F (t)]

)t∈[0,T ]

, with A∗(t)t∈[0,T ] thediscounted payment process given in Definition 3.1.1.

15

CHAPTER 3. THE RISK-MINIMIZING THEORY

Definition 3.1.5A strategy ϕ is called x-admissible if the discounted value process has an end value x, in otherwords V∗(T, ϕ) = x.

Definition 3.1.6The cost process C(t, ϕ)t∈[0,T ] is defined by

C(t, ϕ) = V∗(t, ϕ) −∫ t

0ξ(s)dX(s) −

∫ t

0ϑ(s)dY(s) + A∗(t).

Definition 3.1.7The risk process R(t, ϕ)t∈[0,T ] is defined by

R(t, ϕ) = EQ[(C(T, ϕ) −C(t, ϕ))2

∣∣∣F (t)].

The theory of risk-minimization now states that a strategy ϕ is risk-minimizing if it minimizesthe risk process. This means that we have to find the strategy ϕ so that R(t, ϕ) is minimal for allt ∈ [0,T ].

In the remaining of this chapter we will briefly look at the discrete- and the continuous-timetrading case. Afterwards we will take a closer look at the mixed case, where we have bothdiscrete- and continuous-time trading.

3.2 The discrete-time trading caseThis section is mainly based on Follmer and Schweizer (1989).We consider a general setting but assume that all of our d + 1 assets can only be traded at fixedtimes in [0,T ]. We will denote these fixed trading times with 0 = t0 < t1 < . . . < tn−1 < tn = T .We now wish to find the optimal trading strategy ϕ(ti)i∈0,...,n = (ξ(ti), ϑ(ti), η(ti))i∈0,...,n, wherewe assume that ϕ is piecewise constant on each interval and F-measurable. We could just useone notation ϕ = (ξ, η) for all d + 1 assets, but we will not do so, in view of further comparison(see section 3.5). Note that for i = n, ξ(tn) and ϑ(tn) are zero since we stop our trading strategyat time T = tn. The theory of risk-minimization tells us that we can find the optimal strategy ϕby minimizing the risk process. In the discrete case the risk process is given by

R(ti, ϕ) = EQ[(C(ti+1, ϕ) −C(ti, ϕ))2

∣∣∣F (ti)],

with i = 0, . . . , n − 1.For simplicity we also assume that the covariance of the increments of X and Y terms are zero.

We will not make use of the discounted payment process from section 3.1. Instead we work witha payoff H such that the discounted value process V∗(ti, ϕ)i=0,...,n and cost process C(ti, ϕ)i=0,...,n

in the discrete setting reduce to:V∗(0, ϕ) = η(0)V∗(ti, ϕ) = ξ(ti−1)X(ti) + ϑ(ti−1)Y(ti) + η(ti), i = 1, . . . , n − 1V∗(tn, ϕ) = V∗(T, ϕ) = H,

16 Pricing and hedging of life insurance portfolios H. De Coninck

CHAPTER 3. THE RISK-MINIMIZING THEORY

andC(0, ϕ) = V∗(0, ϕ) = η(0)

C(ti, ϕ) = V∗(ti, ϕ) −i∑

j=1

ξ(t j−1) (X(t j) − X(t j−1))︸ ︷︷ ︸∆X(t j)

−

i∑j=1

ϑ(t j−1) (Y(t j) − Y(t j−1))︸ ︷︷ ︸∆Y(t j)

, i = 1, . . . , n.

We want (ξ(ti), ϑ(ti), η(ti))i=0,...,n to minimize the conditional risk, thus

minϕR(ti, ϕ) = min

ϕ

EQ

[(C(ti+1, ϕ) −C(ti, ϕ))2

∣∣∣F (ti)]

= minϕ

EQ

[(V∗(ti+1, ϕ) −

i+1∑j=1

(ξ(t j−1)∆X(t j) + ϑ(t j−1)∆Y(t j)

)− V∗(ti, ϕ) +

i∑j=1

(ξ(t j−1)∆X(t j) + ϑ(t j−1)∆Y(t j)

) )2∣∣∣∣∣∣F (ti)

]= min

ϕ

EQ

[(V∗(ti+1, ϕ) − V∗(ti, ϕ) − ξ(ti)∆X(ti+1) − ϑ(ti)∆Y(ti+1))2

∣∣∣F (ti)].

The idea is to choose V∗(ti, ϕ) (because we can calculate η(ti) using the solutions for V∗(ti, ϕ),ξ(ti−1) and ϑ(ti−1)), ξ(ti) and ϑ(ti) such that we achieve this minimum. In order to do so, we haveto calculate the first order conditions. Thus by taking the derivatives with respect to V∗(ti, ϕ),ξ(ti) and ϑ(ti) and solving them, we can solve the minimization problem. We first start with thederivation with respect to ξ(ti):

∂

∂ξ(ti)EQ

[(V∗(ti+1, ϕ) − V∗(ti, ϕ) − ξ(ti)∆X(ti+1) − ϑ(ti)∆Y(ti+1))2

∣∣∣F (ti)]

= 0

⇔ EQ[2 (V∗(ti+1, ϕ) − V∗(ti, ϕ) − ξ(ti)∆X(ti+1) − ϑ(ti)∆Y(ti+1)) (−∆X(ti+1))

∣∣∣F (ti)]

= 0

⇔ EQ[∆X(ti+1)

(V∗(ti+1, ϕ) − V∗(ti, ϕ)︸ ︷︷ ︸

F (ti)-measurable

− ξ(ti)︸︷︷︸F (ti)-measurable

∆X(ti+1) − ϑ(ti)︸︷︷︸F (ti)-measurable

∆Y(ti+1))∣∣∣F (ti)

]= 0

⇔ EQ[∆X(ti+1)V∗(ti+1, ϕ)|F (ti)

]− V∗(ti, ϕ)EQ

[∆X(ti+1)|F (ti)

]− ξ(ti)EQ

[(∆X(ti+1))2

∣∣∣F (ti)]

− ϑ(ti)EQ [∆X(ti+1)∆Y(ti+1)|F (ti)] = 0.

Since X(t)t∈[0,T ] is a Q-martingale, its expectation conditional on F (ti) is just X(ti). Thereforewe have that EQ[∆X(ti+1)|F (ti)] = 0:

EQ[∆X(ti+1)V∗(ti+1, ϕ)|F (ti)

]− V∗(ti, ϕ) EQ

[∆X(ti+1)|F (ti)

]︸ ︷︷ ︸0

−ξ(ti)EQ[(∆X(ti+1))2

∣∣∣F (ti)]

− ϑ(ti)EQ [∆X(ti+1)∆Y(ti+1)|F (ti)] = 0

⇔ ξ(ti)(EQ

[(∆X(ti+1))2

∣∣∣F (ti)]−

(EQ [∆X(ti+1)|F (ti)]

)2︸ ︷︷ ︸0

)= EQ

[∆X(ti+1)V∗(ti+1, ϕ)|F (ti)

]− EQ [∆X(ti+1)|F (ti)] EQ

[V∗(ti+1, ϕ)|F (ti)

]︸ ︷︷ ︸0

− ϑ(ti)(EQ [∆X(ti+1)∆Y(ti+1)|F (ti)] − EQ [∆X(ti+1)|F (ti)] EQ [∆Y(ti+1)|F (ti)]︸ ︷︷ ︸

0

)

H. De Coninck Pricing and hedging of life insurance portfolios 17

CHAPTER 3. THE RISK-MINIMIZING THEORY

⇔ ξ(ti) var (∆X(ti+1)|F (ti)) = cov (V∗(ti+1, ϕ),∆X(ti+1)|F (ti)) − ϑ(ti) cov (∆X(ti+1),∆Y(ti+1)|F (ti))︸ ︷︷ ︸0 due to the assumption

⇔ ξ(ti) =cov (V∗(ti+1, ϕ),∆X(ti+1)|F (ti))

var (∆X(ti+1)|F (ti)).

By interchanging the role of ξ and ϑ and of X and Y we have

ϑ(ti) =cov (V∗(ti+1, ϕ),∆Y(ti+1)|F (ti))

var (∆Y(ti+1)|F (ti))=

EQ[V∗(ti+1, ϕ)∆Y(ti+1)|F (ti)

]EQ

[(∆Y(ti1))2

∣∣∣F (ti)] .

Before calculating the formula for η, we consider the partial derivative with respect to V∗(ti, ϕ)in

EQ[(V∗(ti+1, ϕ) − V∗(ti, ϕ) − ξ(ti)∆X(ti+1) − ϑ(ti)∆Y(ti+1))2

∣∣∣F (ti)].

Setting this equal to zero we get

V∗(ti, ϕ) = EQ[V∗(ti+1, ϕ)

∣∣∣F (ti)]− ξ(ti) EQ

[∆X(ti+1)

∣∣∣F (ti)]︸ ︷︷ ︸

0 since X(t)t∈[0,T ] is a Q-martingale

−ϑ(ti) EQ[∆Y(ti+1)

∣∣∣F (ti)]︸ ︷︷ ︸

0 since Y(t)t∈[0,T ] is a Q-martingale

⇔ C(ti, ϕ) +

i∑j=1

ξ(t j−1)∆X(t j) +

i∑j=1

ϑ(t j−1)∆Y(t j)

= EQC(ti+1, ϕ) +

i+1∑j=1

ξ(t j−1)∆X(t j) +

i+1∑j=1

ϑ(t j−1)∆Y(t j)

∣∣∣∣∣∣F (ti)

= EQ

[C(ti+1, ϕ)

∣∣∣F (ti)]

+

i∑j=1

ξ(t j−1)∆X(t j) +

i∑j=1

ϑ(t j−1)∆Y(t j)

+ EQ[

ξ(ti)︸︷︷︸F (ti)-measurable

∆X(ti+1)∣∣∣F (ti)

]− EQ

[ϑ(ti)︸︷︷︸

F (ti)-measurable

∆Y(ti+1)∣∣∣F (ti)

]⇔ C(ti, ϕ) = EQ

[C(ti+1, ϕ)

∣∣∣F (ti)]

+ ξ(ti) EQ [∆X(ti+1)|F (ti)]︸ ︷︷ ︸0 since X(t)t∈[0,T ] is a Q-martingale

+ϑ(ti) EQ [∆Y(ti+1)|F (ti)]︸ ︷︷ ︸0 since Y(t)t∈[0,T ] is a Q-martingale

= EQ[C(ti+1, ϕ)

∣∣∣F (ti)].

The first equation shows that the discounted value process V∗(ti, ϕ)i=0,...,n is a martingale underQ, while the last equation shows that the cost process C(ti, ϕ)i=0,...,n is a Q-martingale.

We can now compute the discounted deposit.

η(ti) = V∗(ti, ϕ) − ξ(ti−1)X(ti) − ϑ(ti−1)Y(ti)= EQ

[V∗(T, ϕ)|F (ti)

]− ξ(ti−1)X(ti) − ϑ(ti−1)Y(ti). since V∗(ti, ϕ)i=1,...,n is a Q-martingale

Since V∗(T, ϕ) is given, we can easily calculate V∗(ti, ϕ) for i ∈ 0, . . . , n − 1. This allows us todetermine η(0), ξ(ti) and ϑ(ti). Based on the optimal values for ξ(ti−1) and ϑ(ti−1), we can thenfind η(ti) with i ∈ 1, . . . , n. We thus have solved the discrete-time trading case.

18 Pricing and hedging of life insurance portfolios H. De Coninck

CHAPTER 3. THE RISK-MINIMIZING THEORY

Conclusion

The optimal strategy ϕ = (ξ, ϑ, η) is given by

ξ(ti) =EQ

[V∗(ti+1, ϕ)∆X(ti+1)|F (ti)

]EQ

[(∆X(ti+1))2

∣∣∣F (ti)] ,

ϑ(ti) =EQ

[V∗(ti+1, ϕ)∆Y(ti+1)|F (ti)

]EQ

[(∆Y(ti+1))2

∣∣∣F (ti)] ,

with i = 0, . . . , n − 1,

η(ti) = EQ[V∗(T, ϕ)|F (ti)

]− ξ(ti−1)X(ti) − ϑ(ti−1)Y(ti),

with i = 0, . . . , n.

3.3 The continuous-time trading caseThis section has been inspired by Dahl et al. (2011). We consider our general setting and assumethat all of the d + 1 assets are continuously tradeable. We also demand that ϕ is a 0-admissiblestrategy, since we make use of a payment process which implicitly captivates the payoff H.

Note that just as in the discrete case (see section 3.2) we can rewrite (ξ, ϑ) as ξ because weassume all assets to be liquid. Nevertheless we shall not do this in view of further comparison.

Recall Definition 3.1.4 for the intrinsic value process in section 3.1. We can rewrite this defini-tion by using the GKW decomposition (see Theorem 2.0.2) as follows:

A∗(T ) = EQ[A∗(T )] +

∫ T

0ξA∗(s)dX(s) +

∫ T

0ϑA∗(s)dY(s) + NA∗(T ).

Note that ξA∗(t)t∈[0,T ] and ϑA∗(t)t∈[0,T ] are predictable processes and that NA∗(t)t∈[0,T ] is a Q-martingale which is orthogonal to (X(t),Y(t))t∈[0,T ] and has NA∗(0) = 0.

So the intrinsic value process V∗,Q(t) becomes

V∗,Q(t) = EQ[EQ[A∗(T )]

∣∣∣F (t)]

+ EQ[ ∫ T

0ξA∗(s)dX(s)︸ ︷︷ ︸martingale

∣∣∣∣∣∣F (t)]

+ EQ[ ∫ T

0ϑA∗(s)dY(s)︸ ︷︷ ︸martingale

∣∣∣∣∣∣F (t)]

+ EQ[NA∗(T )

∣∣∣F (t)]

by Proposition 2.0.6

= EQ[A∗(T )]︸ ︷︷ ︸V∗,Q(0)

+

∫ t

0ξA∗(s)dX(s) +

∫ t

0ϑA∗(s)dY(s) + EQ

[NA∗(T )

∣∣∣F (t)]︸ ︷︷ ︸

NA∗ (t)

= V∗,Q(0) +

∫ t

0ξA∗(s)dX(s) +

∫ t

0ϑA∗(s)dY(s) + NA∗(t). (3.1)

H. De Coninck Pricing and hedging of life insurance portfolios 19

CHAPTER 3. THE RISK-MINIMIZING THEORY

In this setting we can find a unique strategy ϕ that fulfills the 0-admissibility and minimizesthe risk process. We will give the form of this strategy (see also Møller (2001)), but first weconsider next lemma, taken from Follmer and Sondermann (1986).

Remember that in the discrete case (see section 3.2) we showed that the cost process C(ti, ϕ)i=0,...,n

is a Q-martingale. In the continuous case we can derive the same property for the cost processC(t, ϕ)t∈[0,T ] given that ϕ is admissible and risk-minimizing.

Lemma 3.3.1If ϕ is a 0-admissible, risk-minimizing strategy then C(t, ϕ)t∈[0,T ] will be a Q-martingale.

Proof. Consider a 0-admissible strategy ϕ = (ξ, ϑ, η) and fix a time t0 with 0 ≤ t0 ≤ T . Defineη(t) as follows:

η(t) if t < t0

C(t, ϕ) +

∫ t

0ξ(s)dX(s) +

∫ t

0ϑ(s)dY(s) − ξ(t)X(t) − ϑ(t)Y(t) if t0 ≤ t ≤ T,

where C(t, ϕ) is the right-continuous version of C(t, ϕ) = EQ[C(T, ϕ)

∣∣∣F (t)]

such that its pro-cess is a Q-martingale. The 0-admissibility is needed since we want C(T, ϕ) to equal A∗(T ) −∫ T

0ξ(s)dX(s) −

∫ T

0ϑ(s)dY(s).

This way ϕ = (ξ, ϑ, η) is an admissible continuation of ϕ at time t0. The remaining cost nowbecomes

C(T, ϕ) − C(t0, ϕ) = EQ[C(T, ϕ)

∣∣∣F (T )]− C(t0, ϕ)

= C(T, ϕ) − C(t0, ϕ)= (C(T, ϕ) −C(t0, ϕ)) − (C(t0, ϕ) −C(t0, ϕ)).

Or thusC(T, ϕ) −C(t0, ϕ) = (C(T, ϕ) − C(t0, ϕ)) − (C(t0, ϕ) − C(t0, ϕ)). (3.2)

The associated risk is then determined by

EQ[(C(T, ϕ) −C(t0, ϕ))2

∣∣∣∣∣F (t0)]

= EQ[(

(C(T, ϕ) − C(t0, ϕ)) − (C(t0, ϕ) − C(t0, ϕ)))2

∣∣∣∣∣F (t0)]

by equation (3.2)

= EQ[(

C(T, ϕ) − C(t0, ϕ))2

∣∣∣∣∣F (t0)]− 2EQ

[ (C(T, ϕ) − C(t0, ϕ)

) (C(t0, ϕ) − C(t0, ϕ)

)︸ ︷︷ ︸F (t0)-measurable

∣∣∣∣∣F (t0)]

+ EQ[ (

C(t0, ϕ) − C(t0, ϕ))2︸ ︷︷ ︸

F (t0)-measurable

∣∣∣∣∣F (t0)]

= EQ[(

C(T, ϕ) − C(t0, ϕ))2

∣∣∣∣∣F (t0)]− 2

(C(t0, ϕ) − C(t0, ϕ)

)EQ

[C(T, ϕ) − C(t0, ϕ)

∣∣∣F (t0)]

+(C(t0, ϕ) − C(t0, ϕ)

)2.

20 Pricing and hedging of life insurance portfolios H. De Coninck

CHAPTER 3. THE RISK-MINIMIZING THEORY

Noting that since C(t, ϕ)t∈[0,T ] is a martingale under Q, we have that

EQ[C(T, ϕ) − C(t0, ϕ)

∣∣∣F (t0)]

= EQ[C(T, ϕ)

∣∣∣F (t0)]− C(t0, ϕ) = 0

and thus we get

EQ[(C(T, ϕ) −C(t0, ϕ))2

∣∣∣F (t0)]

= EQ[(

C(T, ϕ) − C(t0, ϕ))2

∣∣∣∣∣F (t0)]

+(C(t0, ϕ) − C(t0, ϕ)

)2.

In order for ϕ to be risk-minimizing we need the left hand side to be minimal, thus

EQ[(C(T, ϕ) −C(t0, ϕ))2

∣∣∣F (t0)]

has to be equal to EQ[(

C(T, ϕ) − C(t0, ϕ))2

∣∣∣∣∣F (t0)]. We accom-

plish this by choosing C(t0, ϕ) = C(t0, ϕ) = EQ[C(T, ϕ)|F (t0)].

Because we chose t0 ∈ [0,T ] arbitrary, this implies that C(t, ϕ)t∈[0,T ] is a Q-martingale.

Theorem 3.3.1There exists a unique, 0-admissible, risk-minimizing strategy ϕ = (ξ, ϑ, η) for the discountedpayment process A∗(t)t∈[0,T ].Moreover, for t ∈ [0,T ], it is given by

(ξ(t), ϑ(t), η(t)) = (ξA∗(t), ϑA∗(t),V∗,Q(t) − ξA∗(t)X(t) − ϑA∗(t)Y(t) − A∗(t)).

The minimal obtainable risk for t ∈ [0,T ] is given by

R(t, ϕ) = EQ[(

NA∗(T ) − NA∗(t))2

∣∣∣∣∣F (t)].

Proof. Take a random t ∈ [0,T ]. We have two formulas for the intrinsic value process V∗,Q(t),see section 3.1 and equation (3.1):

V∗,Q(t) = EQ[A∗(T )|F (t)] (3.3)

and

V∗,Q(t) = V∗,Q(0) +

∫ t

0ξA∗(s)dX(s) +

∫ t

0ϑA∗(s)dY(s) + NA∗(t). (3.4)

For t = T we find

A∗(T ) = EQ[A∗(T )|F (T )]= V∗,Q(T ) by equation (3.3)

= V∗,Q(0) +

∫ T

0ξA∗(s)dX(s) +

∫ T

0ϑA∗(s)dY(s) + NA∗(T ) by equation (3.4) with t = T

= V∗,Q(t) −∫ t

0ξA∗(s)dX(s) −

∫ t

0ϑA∗(s)dY(s) − NA∗(t) +

∫ T

0ξA∗(s)dX(s)

+

∫ T

0ϑA∗(s)dY(s) + NA∗(T ) by equation (3.4)

= V∗,Q(t) +

∫ T

tξA∗(s)dX(s) +

∫ T

tϑA∗(s)dY(s) +

(NA∗(T ) − NA∗(t)

). (3.5)

H. De Coninck Pricing and hedging of life insurance portfolios 21

CHAPTER 3. THE RISK-MINIMIZING THEORY

The difference in cost is then given by

C(T, ϕ) −C(t, ϕ)

= V∗(T, ϕ)︸ ︷︷ ︸0 since 0-admissible

−

∫ T

0ξ(s)dX(s) −

∫ T

0ϑ(s)dY(s) + A∗(T ) − V∗(t, ϕ) +

∫ t

0ξ(s)dX(s)

+

∫ t

0ϑ(s)dY(s) − A∗(t)

= −

∫ T

tξ(s)dX(s) −

∫ T

tϑ(s)dY(s) + V∗,Q(t) +

∫ T

tξA∗(s)dX(s) +

∫ T

tϑA∗(s)dY(s)

+(NA∗(T ) − NA∗(t)

)− V∗(t, ϕ) − A∗(t) by equation (3.5)

=(V∗,Q(t) − V∗(t, ϕ) − A∗(t)

)+

∫ T

t

(ξA∗(s) − ξ(s)

)dX(s) +

∫ T

t

(ϑA∗(s) − ϑ(s)

)dY(s)

+(NA∗(T ) − NA∗(t)

). (3.6)

Substituting equation (3.6) in the risk process

R(t, ϕ) = EQ[(C(T, ϕ) −C(t, ϕ))2

∣∣∣F (t)]

leads to

R(t, ϕ) = EQ[ (

V∗,Q(t) − V∗(t, ϕ) − A∗(t))2︸ ︷︷ ︸

F (t)-measurable

∣∣∣∣∣F (t)]

+ EQ(∫ T

t

(ξA∗(s) − ξ(s)

)dX(s)

)2 ∣∣∣∣∣∣F (t)

+ EQ

(∫ T

t

(ϑA∗(s) − ϑ(s)

)dY(s)

)2 ∣∣∣∣∣∣F (t)

+ EQ[(

NA∗(T ) − NA∗(t))2

∣∣∣∣∣F (t)]

+ 2EQ[ (

V∗,Q(t) − V∗(t, ϕ) − A∗(t))︸ ︷︷ ︸

F (t)-measurable

(∫ T

t

(ξA∗(s) − ξ(s)

)dX(s)

) ∣∣∣∣∣∣F (t)]

+ 2EQ[ (

V∗,Q(t) − V∗(t, ϕ) − A∗(t))︸ ︷︷ ︸

F (t)-measurable

(∫ T

t

(ϑA∗(s) − ϑ(s)

)dY(s)

) ∣∣∣∣∣∣F (t)]

+ 2EQ[ (

V∗,Q(t) − V∗(t, ϕ) − A∗(t))︸ ︷︷ ︸

F (t)-measurable

(NA∗(T ) − NA∗(t)

) ∣∣∣∣∣F (t)]

+ 2EQ[(∫ T

t

(ξA∗(s) − ξ(s)

)dX(s)

) (∫ T

t

(ϑA∗(s) − ϑ(s)

)dY(s)

) ∣∣∣∣∣∣F (t)]

+ 2EQ[(∫ T

t

(ξA∗(s) − ξ(s)

)dX(s)

) (NA∗(T ) − NA∗(t)

) ∣∣∣∣∣∣F (t)]

+ 2EQ[(∫ T

t

(ϑA∗(s) − ϑ(s)

)dY(s)

) (NA∗(T ) − NA∗(t)

) ∣∣∣∣∣∣F (t)].

Using the F-measurability, we can drop the expectation in the first term. Using the F-measurabilityand Proposition 2.0.6, the fifth and sixth term disappear. Using the F-measurability and the mar-tingale property on the seventh term, we see that it also disappears. The two last terms disappear

22 Pricing and hedging of life insurance portfolios H. De Coninck

CHAPTER 3. THE RISK-MINIMIZING THEORY

because of the orthogonality (see Theorem 2.0.2). Last, we rewrite the second and third termand so we get

R(t, ϕ) =(V∗,Q(t) − V∗(t, ϕ) − A∗(t)

)2+ EQ

[∫ T

t

(ξA∗(s) − ξ(s)

)2d[X, X](s)

∣∣∣∣∣∣F (t)]

+ EQ[∫ T

t

(ϑA∗(s) − ϑ(s)

)2d[Y,Y](s)

∣∣∣∣∣∣F (t)]

+ EQ[(

NA∗(T ) − NA∗(t))2

∣∣∣∣∣F (t)]

+ 2EQ[∫ T

t

(ξA∗(s) − ξ(s)

) (ϑA∗(s) − ϑ(s)

)d[X,Y](s)

∣∣∣∣∣∣F (t)]. (3.7)

The risk process R(t, ϕ) will be minimal, if we choose (ξ, ϑ) such that the three terms containingξ and ϑ vanish. This is satisfied for (ξ, ϑ) equal to

(ξA∗ , ϑA∗

). Next we choose η such that the

first term disappears

V∗,Q(t) − V∗(t, ϕ) − A∗(t) = 0

⇔ V∗(t, ϕ) = V∗,Q(t) − A∗(t)

⇔ ξ(t)X(t) + ϑ(t)Y(t) + η(t) = V∗,Q(t) − A∗(t) by Definition 3.1.3

⇔ η(t) = V∗,Q(t) − A∗(t) − ξ(t)︸︷︷︸ξA∗ (t)

X(t) − ϑ(t)︸︷︷︸ϑA∗ (t)

Y(t)

= V∗,Q(t) − A∗(t) − ξA∗(t)X(t) − ϑA∗(t)Y(t).

So, we have proven that there exists a risk-minimizing strategy ϕ, with (ξ(t), ϑ(t))t∈[0,T ] =(ξA∗(t), ϑA∗(t)

)t∈[0,T ]

η(t)t∈[0,T ] =(V∗,Q(t) − A∗(t) − ξA∗(t)X(t) − ϑA∗(t)Y(t)

)t∈[0,T ]

.

Note that we also have the 0-admissibility since

V∗(T, ϕ) = ξ(T )X(T ) + ϑ(T )Y(T ) + η(T ) by Definition 3.1.3

= ξA∗(T )X(T ) + ϑA∗(T )Y(T ) + V∗,Q(T ) − A∗(T ) − ξA∗(T )X(T ) − ϑA∗(T )Y(T )= 0. by equation (3.3)

We now proof the uniqueness of this strategy. Consider a random, risk-minimizing strategy ϕ.Because it is risk-minimizing R (t, ϕ) must be minimal for all t ∈ [0,T ], in particular R (0, ϕ)must be minimal which implies that

(ξ, ϑ

)=

(ξA∗ , ϑA∗

)(consider equation (3.7) with ϕ = ϕ and

t = 0).Lemma 3.3.1 states that C (t, ϕ)t∈[0,T ] is a martingale under Q, thus (C (T, ϕ) −C (t, ϕ))t∈[0,T ] is aQ-martingale as well. Using equation (3.6), we see that the martingale property is preserved ifV∗,Q(t) − V∗ (t, ϕ) − A∗(t) equals zero or if η = V∗,Q − A∗ − ξA∗X − ϑA∗Y .So we see that the 0-admissible, risk-minimizing strategy ϕ has the same form as the 0-admissible,risk-minimizing strategy ϕ we found in the previous part of the proof. In other words, we havethe uniqueness of the strategy.

H. De Coninck Pricing and hedging of life insurance portfolios 23

CHAPTER 3. THE RISK-MINIMIZING THEORY

Conclusion

The 0-admissible, unique, optimal strategy ϕ = (ξ, ϑ, η), with t ∈ [0,T ] is given by

ξ(t) = ξA∗(t),

ϑ(t) = ϑA∗(t),

η(t) = V∗,Q(t) − ξA∗(t)X(t) − ϑA∗(t)Y(t) − A∗(t),

where ξA∗ and ϑA∗ are predictable processes in the GKW decomposition of A∗.

3.4 The mixed continuous-discrete-time trading caseWe consider our general setting and assume that our first d assets are liquid, so we can tradethem continuously while the last asset is illiquid. Denote the trading times of this asset by0 = t0 < t1 < . . . < tn−1 < tn = T . Since we will again make use of a payment process, weassume that we have 0-admissibility. We therefore have the following market: (B∗, X,Y) withB∗ = 1 the discounted savings account.We will look for a trading strategy ϕ = (ξ, ϑ, η) where now (ξ, ϑ) is F-predictable and ϑ is piece-wise constant on the intervals ]ti, ti+1] for i = 0, . . . , n − 1 and η is F-adapted. We also assumethat the necessary integrability conditions are satisfied.Note that in this way we can only trade the last asset on fixed times, but that we can observe itsprice process continuously!

We will use a slightly different definition for a strategy than we used previously (see section3.1, Definition 3.1.2). It is given in Dahl et al. (2011). We also used Dahl et al. (2011) as astarting point for this section.

Definition 3.4.1A strategy ϕ = (ξ, ϑ, η) with ϑ piecewise constant on the intervals ]ti, ti+1] for i = 0, . . . , n − 1 issaid to be mixed continuous- and discrete-time risk-minimizing if ϕ = (ξ, ϑ, η) minimizes therisk process R(ti, ϕ) = R(ti, ξ, ϑ, η) for i = 0, . . . , n − 1 and if (ξ, η) minimizes R(t, ξ, ϑ, η) witht ∈ [0,T ] and for all strategies with ϑ = ϑ.

Previous definition states that the optimal strategy is the one minimizing the risk process at thediscrete trading times as well as minimizing the risk process in all remaining points given theoptimal ϑ.

In the previous section (section 3.3) we used the GKW decomposition (see Theorem 2.0.2)to derive the optimal trading strategy. As a consequence of the GKW decomposition we havethat NA∗(t)t∈[0,T ] is orthogonal to the discounted price processes (X(t),Y(t))t∈[0,T ]. Unfortunatelywe don’t necessarily have information about the orthogonality of X(t)t∈[0,T ] and Y(t)t∈[0,T ]. Thiscan be solved by applying the GKW decomposition to the discounted price process Y(t)t∈[0,T ]

with respect to the Q-measure.

Y(t) = EQ[Y(t)] +

∫ t

0ξY(s)dX(s) + NY(t) (3.8)

24 Pricing and hedging of life insurance portfolios H. De Coninck

CHAPTER 3. THE RISK-MINIMIZING THEORY

⇔ dY(t) = ξY(t)dX(t) + dNY(t). (3.9)

We now have decomposed the discounted price process Y(t)t∈[0,T ] into a part related to the dis-counted price process X(t)t∈[0,T ] and a part orthogonal to this process, namely the part NY(t).Note that since (X(t),Y(t))t∈[0,T ] is orthogonal to NA∗(t)t∈[0,T ] and Y(t)t∈[0,T ] can be decomposedinto parts

(X(t),NY(t)

)t∈[0,T ]

we have that(X(t),NY(t)

)t∈[0,T ]

is orthogonal to NA∗(t)t∈[0,T ].

In the previous section (see section 3.3, equation (3.4)) we had the following formula:

V∗,Q(t) = V∗,Q(0) +

∫ t

0ξA∗(s)dX(s) +

∫ t

0ϑA∗(s)dY(s) + NA∗(t)

= V∗,Q(0) +

∫ t

0ξA∗(s)dX(s) +

∫ t

0ϑA∗(s)

(ξY(s)dX(s) + dNY(s)

)+ NA∗(t) by equation (3.9)

= V∗,Q(0) +

∫ t

0

(ξA∗(s) + ϑA∗(s)ξY(s)

)dX(s) +

∫ t

0ϑA∗(s)dNY(s) + NA∗(t). (3.10)

The cost process C(t, ϕ) can be rewritten, again by using equation (3.9):

C(t, ϕ) = V∗(t, ϕ) −∫ t

0ξ(s)dX(s) −

∫ t

0ϑ(s)dY(s) + A∗(t)

= V∗(t, ϕ) −∫ t

0ξ(s)dX(s) −

∫ t

0ϑ(s)

(ξY(s)dX(s) + dNY(s)

)+ A∗(t)

= V∗(t, ϕ) −∫ t

0

(ξ(s) + ϑ(s)ξY(s)

)dX(s) −

∫ t

0ϑ(s)dNY(s) + A∗(t). (3.11)

For t = T the cost process reduces, since we assume 0-admissibility, to

C(T, ϕ) = −

∫ T

0

(ξ(s) + ϑ(s)ξY(s)

)dX(s) −

∫ T

0ϑ(s)dNY(s) + A∗(T ). (3.12)

We now derive a formula for the discounted payment process in T as follows:

A∗(T ) = EQ[A∗(T )|F (T )]= V∗,Q(T ) by equation (3.3) with t = T

= V∗,Q(0) +

∫ T

0

(ξA∗(s) + ϑA∗(s)ξY(s)

)dX(s) +

∫ T

0ϑA∗(s)dNY(s) + NA∗(T ). (3.13)

by equation (3.10) with t = T

Subtracting equation (3.10) from equation (3.13) we get

A∗(T ) = V∗,Q(t) +

∫ T

t

(ξA∗(s) + ϑA∗(s)ξY(s)

)dX(s) +

∫ T

tϑA∗(s)dNY(s) +

(NA∗(T ) − NA∗(t)

).

(3.14)

We can now look at the future costs. By subtracting equation (3.11) from equation (3.12) wefind

C(T, ϕ) −C(t, ϕ)

H. De Coninck Pricing and hedging of life insurance portfolios 25

CHAPTER 3. THE RISK-MINIMIZING THEORY

= A∗(T ) − A∗(t) − V∗(t, ϕ) −∫ T

t

(ξ(s) + ϑ(s)ξY(s)

)dX(s) +

∫ T

tϑ(s)dNY(s)

= V∗,Q(t) +

∫ T

t

(ξA∗(s) + ϑA∗(s)ξY(s)

)dX(s) +

∫ T

tϑA∗(s)dNY(s) +

(NA∗(T ) − NA∗(t)

)− A∗(t) − V∗(t, ϕ) −

∫ T

t

(ξ(s) + ϑ(s)ξY(s)

)dX(s) +

∫ T

tϑ(s)dNY(s) by equation (3.14)

= V∗,Q(t) − V∗(t, ϕ) − A∗(t) +

∫ T

t

[(ξA∗(s) + ϑA∗(s)ξY(s)

)−

(ξ(s) + ϑ(s)ξY(s)

)]dX(s)

+

∫ T

t

(ϑA∗(s) − ϑ(s)

)dNY(s) +

(NA∗(T ) − NA∗(t)

). (3.15)

We can now substitute expression (3.15) in the risk process R(t, ϕ)

R(t, ϕ) = EQ[(C(T, ϕ) −C(t, ϕ))2

∣∣∣∣∣F (t)]

which leads to

R(t, ϕ) = EQ[ (

V∗,Q(t) − V∗(t, ϕ) − A∗(t))2︸ ︷︷ ︸

F (t)-measurable

∣∣∣∣∣F (t)]

+ EQ[(

NA∗(T ) − NA∗(t))2

∣∣∣∣∣F (t)]

+ EQ(∫ T

t

[(ξA∗(s) + ϑA∗(s)ξY(s)

)−

(ξ(s) + ϑ(s)ξY(s)

)]dX(s)

)2 ∣∣∣∣∣∣F (t)

+ EQ

(∫ T

t

(ϑA∗(s) − ϑ(s)

)dNY(s)

)2 ∣∣∣∣∣∣F (t)

+ 2EQ

[ (V∗,Q(t) − V∗(t, ϕ) − A∗(t)

)︸ ︷︷ ︸F (t)-measurable

×

(∫ T

t

[(ξA∗(s) + ϑA∗(s)ξY(s)

)−

(ξ(s) + ϑ(s)ξY(s)

)]dX(s)

) ∣∣∣∣∣∣F (t)]

+ 2EQ[ (

V∗,Q(t) − V∗(t, ϕ) − A∗(t))︸ ︷︷ ︸

F (t)-measurable

(∫ T

t

(ϑA∗(s) − ϑ(s)

)dNY(s)

) ∣∣∣∣∣∣F (t)]

+ 2EQ[ (

V∗,Q(t) − V∗(t, ϕ) − A∗(t))︸ ︷︷ ︸

F (t)-measurable

(NA∗(T ) − NA∗(t)

) ∣∣∣∣∣F (t)]

+ 2EQ[ (∫ T

t

[(ξA∗(s) + ϑA∗(s)ξY(s)

)−

(ξ(s) + ϑ(s)ξY(s)

)]dX(s)

)×

(∫ T

t

(ϑA∗(s) − ϑ(s)

)dNY(s)

) ∣∣∣∣∣∣F (t)]

+ 2EQ[ (∫ T

t

[(ξA∗(s) + ϑA∗(s)ξY(s)

)−

(ξ(s) + ϑ(s)ξY(s)

)]dX(s)

)×

(NA∗(T ) − NA∗(t)

) ∣∣∣∣∣∣F (t)]

26 Pricing and hedging of life insurance portfolios H. De Coninck

CHAPTER 3. THE RISK-MINIMIZING THEORY

+ 2EQ[(∫ T

t

(ϑA∗(s) − ϑ(s)

)dNY(s)

) (NA∗(T ) − NA∗(t)

) ∣∣∣∣∣∣F (t)].

Using the F-measurability, we can leave out the expectation in the first term. By applying the F-measurability and Proposition 2.0.6 we have that the fifth and sixth term disappear. The seventhterm vanishes because of the F-measurability and the martingale property. The last three termsare zero by the orthogonality (see Theorem 2.0.2). So finally we get

R(t, ϕ) =(V∗,Q(t) − V∗(t, ϕ) − A∗(t)

)2+ EQ

[(NA∗(T ) − NA∗(t)

)2∣∣∣∣∣F (t)

]+ EQ

(∫ T

t

[(ξA∗(s) + ϑA∗(s)ξY(s)

)−

(ξ(s) + ϑ(s)ξY(s)

)]dX(s)

)2 ∣∣∣∣∣∣F (t)

+ EQ

(∫ T

t

(ϑA∗(s) − ϑ(s)

)dNY(s)

)2 ∣∣∣∣∣∣F (t)

. (3.16)

If we would be in the continuous case, we could choose ξ, ϑ and η freely so that they wouldminimize the risk process. However, since we do not have continuity for all assets, we cannotapply this technique. The fact is, we must have a ϑ that is piecewise constant on the intervals]ti, ti+1].Once we have found the optimal, piecewise constant ϑ we can derive the optimal ξ by demand-ing that the integrand of the third term is equal to zero or(

ξA∗(t) + ϑA∗(t)ξY(t))−

(ξ(t) + ϑ(t)ξY(t)

)= 0

⇔ ξ(t) = ξA∗(t) + ϑA∗(t)ξY(t) − ϑ(t)ξY(t)

= ξA∗(t) +(ϑA∗(t) − ϑ(t)

)ξY(t).

In order for η to be optimal we need the first term to be equal to zero, so

V∗,Q(t) − V∗(t, ϕ) − A∗(t) = 0

⇔ V∗(t, ϕ) = V∗,Q(t) − A∗(t)

⇔ ξ(t)X(t) + ϑ(t)Y(t) + η(t) = V∗,Q(t) − A∗(t) by Definition 3.1.3

⇔ η(t) = V∗,Q(t) − A∗(t) − ξ(t)︸︷︷︸ξA∗ (t)+(ϑA∗ (t)−ϑ(t))ξY (t)

X(t) − ϑ(t)Y(t).

Theorem 3.4.1The unique mixed continuous- and discrete-time trading risk-minimizing strategy ϕ = (ξ, ϑ, η)associated with the discounted payment process A∗(t)t∈[0,T ], for t ∈]ti, ti+1] with i = 0, . . . , n − 1is given by

ϑ(t) = ϑ(ti) =

EQ[∫ ti+1

tiϑA∗(s)dNY(s)∆NY(ti+1)

∣∣∣∣∣∣F (ti)]

EQ[(∆NY(ti+1))2

∣∣∣F (ti)] ,

ξ(t) = ξA∗(t) +(ϑA∗(t) − ϑ(t)

)ξY(t),

η(t) = V∗,Q(t) − A∗(t) − ξ(t)X(t) − ϑ(t)Y(t).

H. De Coninck Pricing and hedging of life insurance portfolios 27

CHAPTER 3. THE RISK-MINIMIZING THEORY

Proof. From the previous exposition we already have the last two equations. Only the proof ofthe first statement remains. Hereto we explicitly make use of the illiquidity of the (d +1)th asset.First we reconsider the discounted value process (see equation (3.10)). We have that ϑ(t) = ϑ(ti)for t ∈]ti, ti+1] and i = 0, . . . , n − 1 and thus

V∗,Q(ti) = V∗,Q(0) +

∫ ti

0

(ξA∗(s) + ϑA∗(s)ξY(s)

)dX(s) +

∫ ti

0ϑA∗(s)dNY(s) + NA∗(ti)

= V∗,Q(0) +

∫ ti

0

(ξA∗(s) + ϑA∗(s)ξY(s)

)dX(s) +

i∑j=1

∫ t j

t j−1

ϑA∗(s)dNY(s)

+

i∑j=1

(NA∗(t j) − NA∗(t j−1)

)︸ ︷︷ ︸∆NA∗ (t j)

= V∗,Q(0) +

∫ ti

0

(ξA∗(s) + ϑA∗(s)ξY(s)

)dX(s) +

i∑j=1

(∫ t j

t j−1

ϑA∗(s)dNY(s) + ∆NA∗(t j)).

(3.17)

We also reconsider the risk process (see equation (3.16))

R(ti, ϕ) =(V∗,Q(ti) − V∗(ti, ϕ) − A∗(ti)

)2+ EQ

[(NA∗(T ) − NA∗(ti)

)2∣∣∣∣∣F (ti)

]+ EQ

(∫ T

ti

[(ξA∗(s) + ϑA∗(s)ξY(s)

)−

(ξ(s) + ϑ(s)ξY(s)

)]dX(s)

)2 ∣∣∣∣∣∣F (ti)

+ EQ

(∫ T

ti

(ϑA∗(s) − ϑ(s)

)dNY(s)

)2 ∣∣∣∣∣∣F (ti)

.Only the last term is completely ϑ-dependent. So by definition of a mixed continuous- anddiscrete-time trading risk-minimizing strategy we need to minimize R(ti, ϕ), or more specificwe have to find the ϑ that minimizes the last term, thus

EQ(∫ T

ti

(ϑA∗(s) − ϑ(s)

)dNY(s)

)2 ∣∣∣∣∣∣F (ti)

= EQ

n−1∑

j=i

∫ t j+1

t j

(ϑA∗(s) − ϑ(s)dNY(s)

)2 ∣∣∣∣∣∣F (ti)

=

n−1∑j=i

EQ(∫ t j+1

t j

(ϑA∗(s) − ϑ(s)

)dNY(s)

)2 ∣∣∣∣∣∣F (ti)

+ 2n−1∑j,k=ij<k

EQ[(∫ t j+1

t j

(ϑA∗(s) − ϑ(s)

)dNY(s)

) (∫ tk+1

tk

(ϑA∗(s) − ϑ(s)

)dNY(s)

) ∣∣∣∣∣∣F (ti)].

We can now use the tower property to resolve the double product. We note that F (t j+1) ⊆ F (tk),therefore we condition immediately on F (tk), which gives us

EQ[(∫ t j+1

t j

(ϑA∗(s) − ϑ(s)

)dNY(s)

) (∫ tk+1

tk

(ϑA∗(s) − ϑ(s)

)dNY(s)

) ∣∣∣∣∣∣F (ti)]

28 Pricing and hedging of life insurance portfolios H. De Coninck

CHAPTER 3. THE RISK-MINIMIZING THEORY

= EQ[EQ

[ (∫ t j+1

t j

(ϑA∗(s) − ϑ(s)

)dNY(s)

)︸ ︷︷ ︸

F (tk)-measurable

(∫ tk+1

tk

(ϑA∗(s) − ϑ(s)

)dNY(s)

) ∣∣∣∣∣∣F (tk)]∣∣∣∣∣∣F (ti)

]

= EQ[ ∫ t j+1

t j

(ϑA∗(s) − ϑ(s)

)dNY(s) EQ

[ ∫ tk+1

tk

(ϑA∗(s) − ϑ(s)

)dNY(s)

∣∣∣∣∣∣F (tk)]

︸ ︷︷ ︸0 since martingale

∣∣∣∣∣∣F (ti)]

= 0.

by Proposition 2.0.6

And thus we find

EQ(∫ T

ti

(ϑA∗(s) − ϑ(s)

)dNY(s)

)2 ∣∣∣∣∣∣F (ti)

=

n−1∑j=i

EQ(∫ t j+1

t j

(ϑA∗(s) − ϑ(s)

)dNY(s)

)2 ∣∣∣∣∣∣F (ti) .

We know that ϑ(s) is constant and equal to ϑ(t j) on each interval ]t j, t j+1] thus we get

EQ(∫ T

ti

(ϑA∗(s) − ϑ(s)

)dNY(s)

)2 ∣∣∣∣∣∣F (ti)

=

n−1∑j=i

EQ(∫ t j+1

t j

(ϑA∗(s) − ϑ(s)

)dNY(s)

)2 ∣∣∣∣∣∣F (ti)

=

n−1∑j=i

EQ[( ∫ t j+1

t j

ϑA∗(s)dNY(s) − ϑ(t j)(NY(t j+1) − NY(t j)

)︸ ︷︷ ︸∆NY (t j+1)

)2∣∣∣∣∣∣F (ti)]

=

n−1∑j=i

EQ(∫ t j+1

t j

ϑA∗(s)dNY(s) − ϑ(t j)∆NY(t j+1))2 ∣∣∣∣∣∣F (ti)

.So minimizing the last term in R(ti, ϕ) is equivalent to minimizing the sum above which in turnis equivalent to minimizing each term in it. Thus for j = i, . . . , n − 1 we have to minimize

EQ(∫ t j+1

t j

ϑA∗(s)dNY(s) − ϑ(t j)∆NY(t j+1))2 ∣∣∣∣∣∣F (ti)

.Note that ϑA∗(t)t∈[0,t] is F-predictable and that ϑ(t j) is F (t j)-measurable. Again by using thetower property we have

EQ(∫ t j+1

t j

ϑA∗(s)dNY(s) − ϑ(t j)∆NY(t j+1))2 ∣∣∣∣∣∣F (ti)

= EQ

EQ (∫ t j+1

t j

ϑA∗(s)dNY(s) − ϑ(t j)∆NY(t j+1))2 ∣∣∣∣∣∣F (t j)

∣∣∣∣∣∣F (ti) .

We find the minimizing ϑ(t j) by taking the derivative of the inner term above with respect toϑ(t j) and setting this equal to zero.

∂

∂ϑ(t j)

EQ(∫ t j+1

t j

ϑA∗(s)dNY(s) − ϑ(t j)∆NY(t j+1))2 ∣∣∣∣∣∣F (t j)

= 0

H. De Coninck Pricing and hedging of life insurance portfolios 29

CHAPTER 3. THE RISK-MINIMIZING THEORY

⇔ EQ ∂

∂ϑ(t j)

(∫ t j+1

t j

ϑA∗(s)dNY(s) − ϑ(t j)∆NY(t j+1))2 ∣∣∣∣∣∣F (t j)

= 0

⇔ EQ[2(∫ t j+1

t j

ϑA∗(s)dNY(s) − ϑ(t j)∆NY(t j+1)) (−∆NY(t j+1)

) ∣∣∣∣∣∣F (t j)]

= 0

⇔ EQ[∆NY(t j+1)

∫ t j+1

t j

ϑA∗(s)dNY(s)

∣∣∣∣∣∣F (t j)]− EQ

∆NY(t j+1) ϑ(t j)︸︷︷︸F (t j)-measurable

∆NY(t j+1)

∣∣∣∣∣∣F (t j)

= 0

⇔ ϑ(t j)EQ[(

∆NY(t j+1))2

∣∣∣∣∣F (t j)]

= EQ[∆NY(t j+1)

∫ t j+1

t j

ϑA∗(s)dNY(s)

∣∣∣∣∣∣F (t j)]

⇔ ϑ(t j) =

EQ[∆NY(t j+1)

∫ t j+1

t jϑA∗(s)dNY(s)

∣∣∣∣∣∣F (t j)]

EQ[(

∆NY(t j+1))2

∣∣∣∣∣F (t j)] .

Conclusion

The 0-admissible, unique, optimal strategy ϕ = (ξ, ϑ, η), with t ∈]ti, ti+1] and i = 0, . . . , n−1is given by

ϑ(t) = ϑ(ti) =

EQ[∫ ti+1

tiϑA∗(s)dNY(s)∆NY(ti+1)

∣∣∣∣∣∣F (ti)]

EQ[(∆NY(ti+1))2

∣∣∣F (ti)] ,

ξ(t) = ξA∗(t) +(ϑA∗(t) − ϑ(t)

)ξY(t),

η(t) = V∗,Q(t) − A∗(t) − ξ(t)X(t) − ϑ(t)Y(t),

where ξA∗ and ϑA∗ are predictable processes in the GKW decomposition of A∗.

3.5 ComparisonIn the previous sections we have derived formulas for the discrete case, the continuous case andthe mixed continuous-discrete case. We now will compare the three solutions, therefore we listall strategies with respect to their setting. But first we note that we consider V∗(T, ϕ) + A∗(T ) =

A∗(T ) = V∗,Q(T ) ≡ H in the continuous and mixed case, while V∗(T, ϕ) ≡ H in the discretesetting.

Discrete-time trading caseWe do not consider a payment process, but assume H-admissibility.

ξ(ti) =EQ

[V∗(ti+1, ϕ)∆X(ti+1)

∣∣∣F (ti)]

EQ[(∆X(ti+1))2

∣∣∣F (ti)] with i = 0, . . . , n − 1

30 Pricing and hedging of life insurance portfolios H. De Coninck

CHAPTER 3. THE RISK-MINIMIZING THEORY

ϑ(ti) =EQ

[V∗(ti+1, ϕ)∆Y(ti+1)

∣∣∣F (ti)]

EQ[(∆Y(ti+1))2

∣∣∣F (ti)] with i = 0, . . . , n − 1

η(ti) = EQ [H|F (ti)] − ξ(ti−1)X(ti) − ϑ(ti−1)Y(ti) with i = 0, . . . , n

Continuous-time trading caseWe consider a payment process and assume 0-admissibility.

ξ(t) = ξA∗(t)

ϑ(t) = ϑA∗(t)

η(t) = V∗,Q(t) − ξA∗(t)X(t) − ϑA∗(t)Y(t) − A∗(t)

Mixed continuous-discrete-time trading caseWe consider a payment process and assume 0-admissibility.

ϑ(t) = ϑ(ti) =

EQ[∫ ti+1

tiϑA∗(s)dNY(s)∆NY(ti+1)

∣∣∣∣∣∣F (ti)]

EQ[(∆NY(ti+1))2

∣∣∣F (ti)]

ξ(t) = ξA∗(t) +(ϑA∗(t) − ϑ(t)

)ξY(t)

η(t) = V∗,Q(t) − A∗(t) − ξ(t)X(t) − ϑ(t)Y(t)

with t ∈]ti, ti+1] and i = 0, . . . , n − 1

We see that the mixed continuous-discrete case has elements from both the continuous case andthe discrete case. The formula for η in the mixed case is the same as in the continuous case withthat difference that the formulas for (ξ, ϑ) are different in both settings.The expression for ξ in the mixed case equals the original strategy ξA∗ plus an extra correctionterm because we don’t have full continuity. The form of ϑ shows less resemblance with thecontinuous strategy ϑA∗ , and more with the one coming from the discrete case. We show this asfollows.Consider

ϑ(ti) =

EQ[V∗(ti+1, ϕ)∆Y(ti+1)

∣∣∣F (ti)]

EQ[(∆Y(ti+1))2

∣∣∣F (ti)] .

We choose the price process Y(t)t∈[0,T ] to be equal to NY(t)t∈[0,T ] and we note that the value ofthe discounted process at time T should equal the discounted value process at a random timein [0,T ] plus all discounted, future values. More particular, the proof of the second equality isgiven in appendix B. We now find

ϑ(ti) =

EQ[V∗(ti+1, ϕ)∆Y(ti+1)

∣∣∣F (ti)]

EQ[(∆Y(ti+1))2

∣∣∣F (ti)]

H. De Coninck Pricing and hedging of life insurance portfolios 31

CHAPTER 3. THE RISK-MINIMIZING THEORY

=EQ

[(V∗(T, ϕ) −

∑n−1j=i+1 ϑ(t j)∆NY(t j+1)

)∆NY(ti+1)

∣∣∣F (ti)]

EQ[(∆NY(ti+1))2

∣∣∣F (ti)]

=EQ

[(A∗(T ) −

∑n−1j=i+1 ϑ(t j)∆NY(t j+1)

)∆NY(ti+1)

∣∣∣F (ti)]

EQ[(∆NY(ti+1))2

∣∣∣F (ti)]

=

EQ[V∗,Q(t)∆NY(ti+1)

∣∣∣∣∣F (ti)]

EQ[(∆NY(ti+1))2

∣∣∣∣∣F (ti)] +

EQ[∫ T

t

(ξA∗(s) + ϑA∗(s)ξY(s)

)dX(s)∆NY(ti+1)

∣∣∣∣∣F (ti)]

EQ[(∆NY(ti+1))2

∣∣∣∣∣F (ti)]

+

EQ[∫ T

tϑA∗(s)dNY(s)∆NY(ti+1)

∣∣∣∣∣F (ti)]

EQ[(∆NY(ti+1))2

∣∣∣∣∣F (ti)] +

E[(

NA∗(T ) − NA∗(t))∆NY(ti+1)

∣∣∣F (ti)]

EQ[(∆NY(ti+1))2

∣∣∣∣∣F (ti)]

−

EQ[∑n−1

j=i+1 ϑ(t j)∆NY(t j+1)∆NY(ti+1)∣∣∣∣∣F (ti)

]EQ

[(∆NY(ti+1))2

∣∣∣∣∣F (ti)] . by equation (3.14)

As a consequence of the GKW decomposition (see Theorem 2.0.2) and more specific becauseof the orthogonality between NY and (X,NA∗) the second and fourth term vanish.Equation (3.14) is valid for arbitrary t ∈ [0,T ]. So we can specifically take a t = ti such thatV∗,Q(ti) = V∗,Q(t) is F (ti)-measurable. Next we apply the martingale property of NY and thusthe first term also disappears. We obtain

ϑ(ti) =

EQ[∫ T

tiϑA∗(s)dNY(s)∆NY(ti+1)

∣∣∣∣∣F (ti)]

EQ[(∆NY(ti+1))2

∣∣∣∣∣F (ti)] −

EQ[∑n−1

j=i+1 ϑ(t j)∆NY(t j+1)∆NY(ti+1)∣∣∣∣∣F (ti)

]EQ

[(∆NY(ti+1))2

∣∣∣∣∣F (ti)]

=

EQ[∫ ti+1

tiϑA∗(s)dNY(s)∆NY(ti+1)

∣∣∣∣∣F (ti)]

EQ[(∆NY(ti+1))2

∣∣∣∣∣F (ti)] +

EQ[∫ T

ti+1ϑA∗(s)dNY(s)∆NY(ti+1)

∣∣∣∣∣F (ti)]

EQ[(∆NY(ti+1))2

∣∣∣∣∣F (ti)]

−

EQ[∑n−1

j=i+1 ϑ(t j)∆NY(t j+1)∆NY(ti+1)∣∣∣∣∣F (ti)

]EQ

[(∆NY(ti+1))2

∣∣∣∣∣F (ti)] .

We now apply the tower property and use Proposition 2.0.6 to find

ϑ(ti) =

EQ[∫ ti+1

tiϑA∗(s)dNY(s)∆NY(ti+1)

∣∣∣∣∣F (ti)]

EQ[(∆NY(ti+1))2

∣∣∣∣∣F (ti)]

+

EQ[EQ

[ ∫ T

ti+1ϑA∗(s)dNY(s)

F (ti+1)-measurable︷ ︸︸ ︷∆NY(ti+1)

∣∣∣∣∣F (ti+1)]∣∣∣∣∣F (ti)

]EQ

[(∆NY(ti+1))2

∣∣∣F (ti)]

32 Pricing and hedging of life insurance portfolios H. De Coninck

CHAPTER 3. THE RISK-MINIMIZING THEORY

−

EQ[EQ

[∑n−1j=i+1 ϑ(t j)∆NY(t j+1)

F (ti+1)-measurable︷ ︸︸ ︷∆NY(ti+1)

∣∣∣∣∣F (ti+1)]∣∣∣∣∣F (ti)

]EQ

[(∆NY(ti+1))2

∣∣∣∣∣F (ti)]

=

EQ[∫ ti+1

tiϑA∗(s)dNY(s)∆NY(ti+1)

∣∣∣∣∣F (ti)]

EQ[(∆NY(ti+1))2

∣∣∣∣∣F (ti)]

+

EQ[∆NY(ti+1)

0 since martingale︷ ︸︸ ︷EQ

[ ∫ T

ti+1

ϑA∗(s)dNY(s)∣∣∣∣∣F (ti+1)

] ∣∣∣∣∣F (ti)]

EQ[(∆NY(ti+1))2

∣∣∣F (ti)]

−

EQ[∆NY(ti+1)

0 since martingale︷ ︸︸ ︷EQ

[ n−1∑j=i+1

ϑ(t j)∆NY(t j+1)∣∣∣∣∣F (ti+1)

] ∣∣∣∣∣F (ti)]

EQ[(∆NY(ti+1))2

∣∣∣∣∣F (ti)] by Proposition 2.0.6

=

EQ[∫ ti+1

tiϑA∗(s)dNY(s)∆NY(ti+1)

∣∣∣∣∣F (ti)]

EQ[(∆NY(ti+1))2

∣∣∣∣∣F (ti)] .

This expression is exactly the same as in the mixed continuous-discrete-time trading case.

3.6 Reconsideration of the GKW decompositionThe goal of this section is to derive a version of the GKW decomposition for the intrinsic valueprocess that corresponds with the mixed continuous-discrete-time trading case (see section 3.4).

Theorem 3.6.1Consider the market (B∗, X,Y) and the continuous time GKW for the intrinsic value processV∗,Q(t). Assume that X can be traded continuously, but Y can only be traded at discrete times0 = t0 < t1 < . . . < tn−1 < tn = T. The corresponding mixed continuous-discrete time version ofthe GKW for i = 1, . . . , n is given by

V∗,Q(ti) = V∗,Q(0) +

∫ ti

0ξA∗(s)dX(s) +

i∑j=1

(ϑA∗(t j−1)∆Y(t j) + ∆NA∗(t j)

),

with, for t ∈]t j−1, t j],

ϑA∗(t j−1) = ϑA∗(t) = ϑ(t j−1) =

EQ[∫ t j

t j−1ϑA∗(s)dNY(s)∆NY(t j)

∣∣∣∣∣∣F (t j−1)]

EQ[(

∆NY(t j))2

∣∣∣∣∣F (t j−1)] , (3.18)

H. De Coninck Pricing and hedging of life insurance portfolios 33

CHAPTER 3. THE RISK-MINIMIZING THEORY

ξA∗(t) = ξA∗(t) + ξY(t)(ϑA∗(t) − ϑA∗(t j−1)

), (3.19)

∆NA∗(t j) =

∫ t j

t j−1

ϑA∗(s)dNY(s) − ϑA∗(t j−1)∆NY(t j) + ∆NA∗(t j). (3.20)

Proof. We reconsider the discrete version for V∗,Q(ti) with i = 0, . . . , n.

V∗,Q(ti) = V∗,Q(0) +

∫ ti

0

(ξA∗(s) + ϑA∗(s)ξY(s)

)dX(s) +

i∑j=1

(∫ t j

t j−1

ϑA∗(s)dNY(s) + ∆NA∗(t j))

by equation (3.17)

= V∗,Q(0) +

∫ ti

0

(ξA∗(s) + ϑA∗(s)ξY(s)

)dX(s) +

i∑j=1

(ϑA∗(t j−1)∆NY(t j)

)−

i∑j=1

(ϑA∗(t j−1)∆NY(t j)

)+

i∑j=1

(∫ t j

t j−1

ϑA∗(s)dNY(s) + ∆NA∗(t j))

= V∗,Q(0) +

∫ ti

0

(ξA∗(s) + ϑA∗(s)ξY(s)

)dX(s) +

i∑j=1

(ϑA∗(t j−1)∆NY(t j)

)+

i∑j=1

( ∫ t j

t j−1

ϑA∗(s)dNY(s) + ∆NA∗(t j) − ϑA∗(t j−1)∆NY(t j)︸ ︷︷ ︸∆NA∗ (t j)

).

Because the last asset is only traded at fixed times we can rewrite expression (3.9) as follows:

dY(t) = ξY(t)dX(t) + dNY(t)

⇔ ∆Y(t j) =

∫ t j

t j−1

ξY(s)dX(s) + ∆NY(t j)

⇔ ∆NY(t j) = ∆Y(t j) −∫ t j

t j−1

ξY(s)dX(s).

Thus

V∗,Q(ti) = V∗,Q(0) +

∫ ti

0

(ξA∗(s) + ϑA∗(s)ξY(s)

)dX(s) +

i∑j=1