Embed Size (px)

Citation preview

Geoffrey HalePolitical Science 3170

The University of LethbridgeNovember 9, 2010

OutlineThe automotive sector and Canadian trade

policiesMedium-term trends in the automotive sector

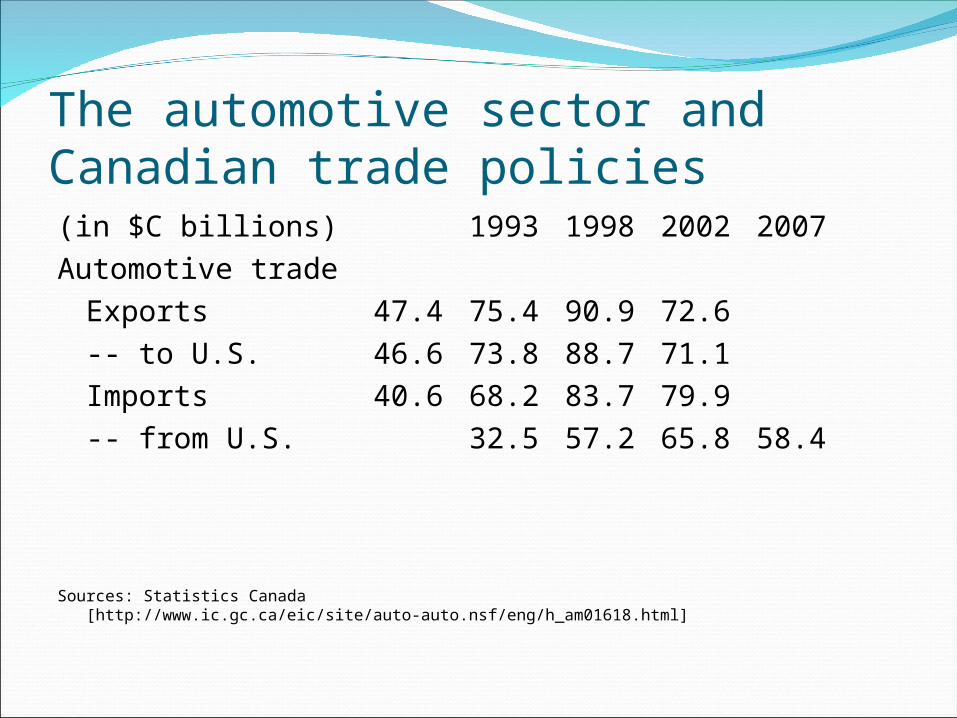

The automotive sector and Canadian trade policies (in $C billions) 1993 1998 2002 2007Automotive trade

Exports 47.4 75.4 90.9 72.6-- to U.S. 46.6 73.8 88.7 71.1Imports 40.6 68.2 83.7 79.9-- from U.S. 32.5 57.2 65.8 58.4

Sources: Statistics Canada [http://www.ic.gc.ca/eic/site/auto-auto.nsf/eng/h_am01618.html]

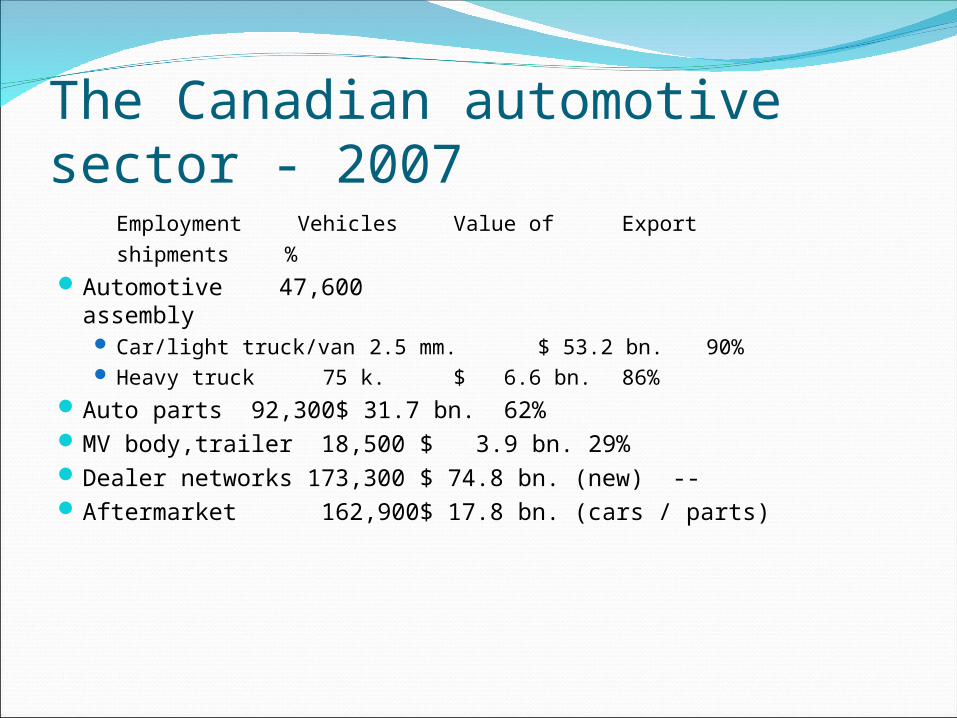

The Canadian automotive sector - 2007Employment Vehicles Value of Export

shipments %Automotive 47,600

assembly Car/light truck/van 2.5 mm. $ 53.2 bn.

90% Heavy truck 75 k. $ 6.6 bn. 86%

Auto parts 92,300 $ 31.7 bn. 62%MV body,trailer 18,500 $ 3.9 bn. 29%Dealer networks 173,300 $ 74.8 bn. (new) --Aftermarket 162,900 $ 17.8 bn. (cars / parts)

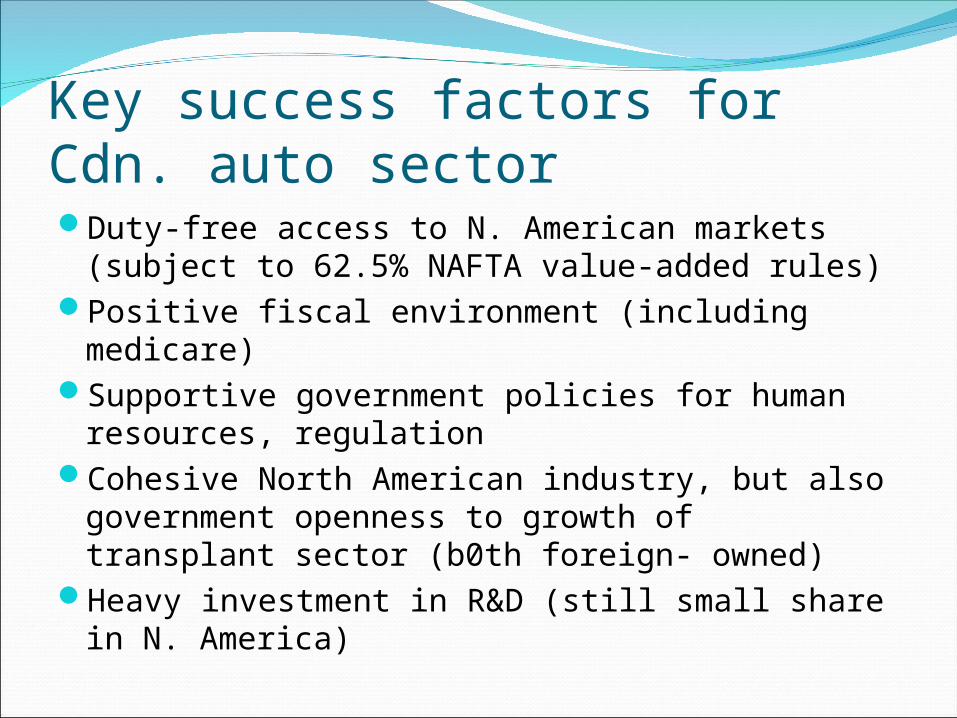

Key success factors for Cdn. auto sectorDuty-free access to N. American markets (subject

to 62.5% NAFTA value-added rules)Positive fiscal environment (including medicare)Supportive government policies for human

resources, regulationCohesive North American industry, but also

government openness to growth of transplant sector (b0th foreign- owned)

Heavy investment in R&D (still small share in N. America)

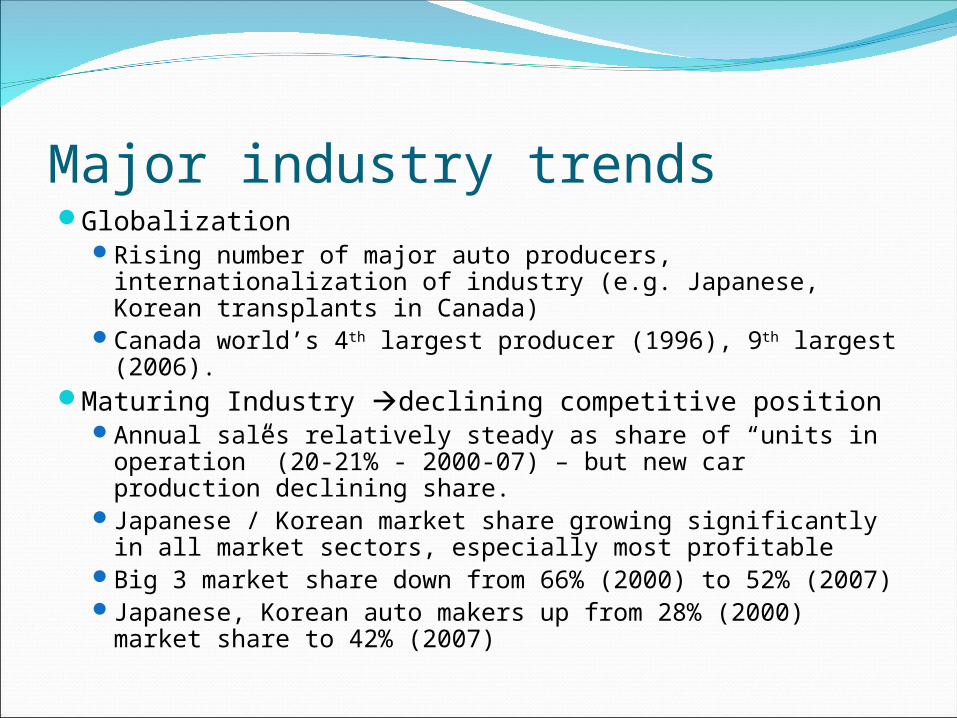

Major industry trendsGlobalization

Rising number of major auto producers, internationalization of industry (e.g. Japanese, Korean transplants in Canada)

Canada world’s 4th largest producer (1996), 9th largest (2006).

Maturing Industry declining competitive positionAnnual sales relatively steady as share of “units in

operation” (20-21% - 2000-07) – but new car production declining share.

Japanese / Korean market share growing significantly in all market sectors, especially most profitable

Big 3 market share down from 66% (2000) to 52% (2007)Japanese, Korean auto makers up from 28% (2000) market

share to 42% (2007)

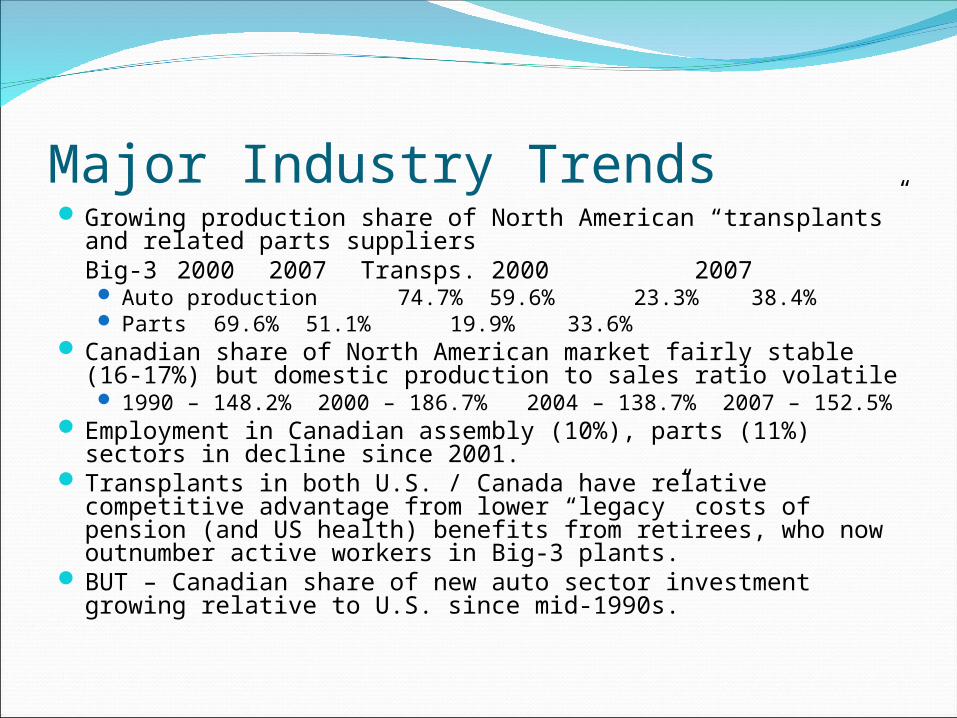

Major Industry Trends Growing production share of North American “transplants”

and related parts suppliersBig-3 2000 2007 Transps. 2000 2007

Auto production 74.7% 59.6% 23.3% 38.4% Parts 69.6% 51.1% 19.9% 33.6%

Canadian share of North American market fairly stable (16-17%) but domestic production to sales ratio volatile 1990 – 148.2% 2000 – 186.7% 2004 – 138.7% 2007 – 152.5%

Employment in Canadian assembly (10%), parts (11%) sectors in decline since 2001.

Transplants in both U.S. / Canada have relative competitive advantage from lower “legacy” costs of pension (and US health) benefits from retirees, who now outnumber active workers in Big-3 plants.

BUT – Canadian share of new auto sector investment growing relative to U.S. since mid-1990s.

The auto sector crisis of 2008-09Key factors in auto sector collapse

Financial crisis collapse of short-term financing market for big-3 automakers undercut most profitable part of business reinforced by U.S. sub-prime mortgage crisis undercutting consumer demand

Steady decline in market share vs. Transplants Reinforced by Chrysler’s excessive dependence on mini-van /

SUV marketsMarket shock for high end products resulting from

record oil prices (2008)Cash flow crisis impending bankruptcy for GM,

Chrysler(Ford mortgaged virtually all assets before financial crisis)

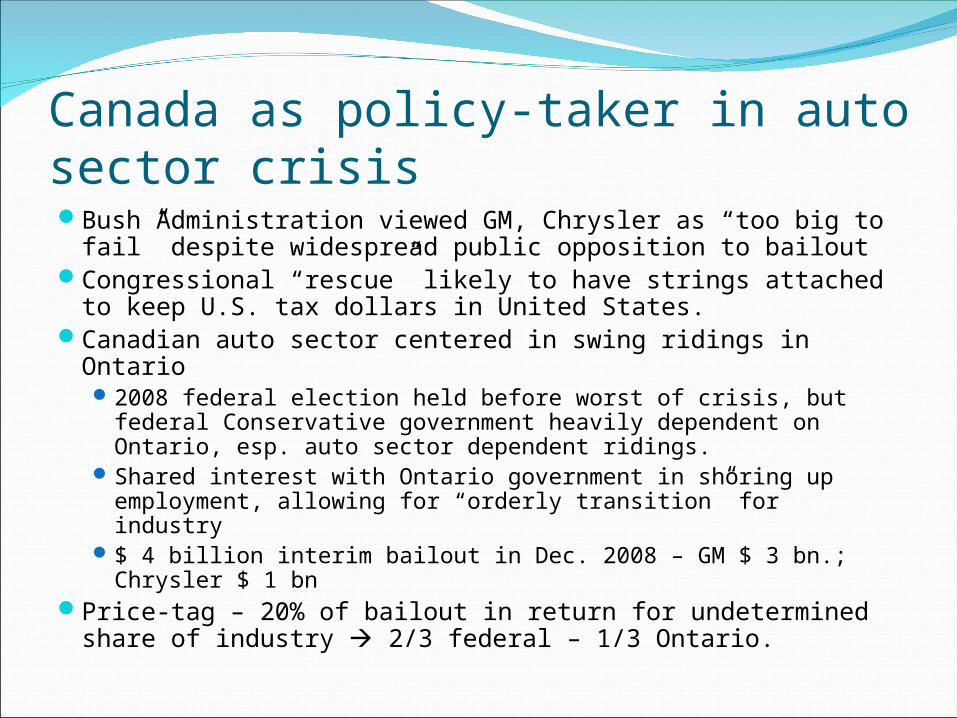

Canada as policy-taker in auto sector crisisBush Administration viewed GM, Chrysler as “too big to

fail” despite widespread public opposition to bailoutCongressional “rescue” likely to have strings attached to

keep U.S. tax dollars in United States.Canadian auto sector centered in swing ridings in Ontario

2008 federal election held before worst of crisis, but federal Conservative government heavily dependent on Ontario, esp. auto sector dependent ridings.

Shared interest with Ontario government in shoring up employment, allowing for “orderly transition” for industry

$ 4 billion interim bailout in Dec. 2008 – GM $ 3 bn.; Chrysler $ 1 bn

Price-tag – 20% of bailout in return for undetermined share of industry 2/3 federal – 1/3 Ontario.

Auto sector bailout as multi-level gameThree sets of overlapping negotiations

Ottawa + Ontario with Bush / Obama Administrations Auto sector only one of several crises facing incoming

administration (sub-prime crisis / U.S. recession / Wall Street bailouts)

Canadian dimension marginal to broader U.S. political processes in executive branch, Congress

Canada bought a seat at the table, not a “microphone”.Ottawa + Ontario with GM / Chrysler (separate

negotiations) Chrysler negotiating with Fiat as key component of bailout GM, Chrysler also negotiating with unions for “competitive”

contractOttawa + Ontario with Canadian Auto Workers

CAW position undercut by negotiating position of UAW UAW position strengthened by union influence in governing

Democratic Party, Obama admin’s willingness to discount bondholders, dismiss GM management.

OutcomesGM, Chrysler declare bankruptcy in both

countriesNew firms have minority government ownership,

plurality (GM), majority (Chrysler) ownership to union pension, benefit funds

Total Canadian funding – Chrysler $ 3.8 bn. for 2% of equity in restructured company, 20% production guarantee – GM - $ 10.5 bn. for 11.5% equity in restructured company, 16% production guarantee.

Major policy challenges for governmentsMaintaining neutrality among individual corporations

Too-big-to-fail sets dangerous precedents Ongoing turbulence likely in industry – governments can be

seen to play favouritesProduction guarantees hard to enforce

Federal lawsuit against U.S. Steel possible warning signal to GM, Chrysler about political risks

Fostering efficiency, competitiveness critical, especially with prospect of high exchange rate environment Investment promotion to get new technologies for Canadian

plants Infrastructure $ 550 mm. loan offer to Michigan for new

Detroit-Windsor bridge (on hold pending state-level political deal)

Human Resources investments in specialized skills to shift into “high wage / high skill” global market niche.

Taxation commitment to CIT rate reductions