Embed Size (px)

Citation preview

Generation Z – impact on life insurance and pension industry: UK and Poland

Karol Raźniewski

Jason Whyte

May 2019

2

Generation Z. Who are they?

► Born 1981-1996

► Self-centered

► Entitled

► Idealist

► Creative

► Dependent

Skin-color-blind, living and working in diversified and inclusive environment

Born into technology (C-generation), Interconnected. No need to ask

Mostly children of Gen X

In Poland: a generation born and brought up in free society and free market, not burdened with history, political limitations or even early years of Polish capitalism

Prefer socializing online than in real life

MILLENNIALS (GEN Y) GEN Z

► Born 1997-2003

► Self-aware

► Persistent

► Realist

► Innovative

► Self-reliant

3

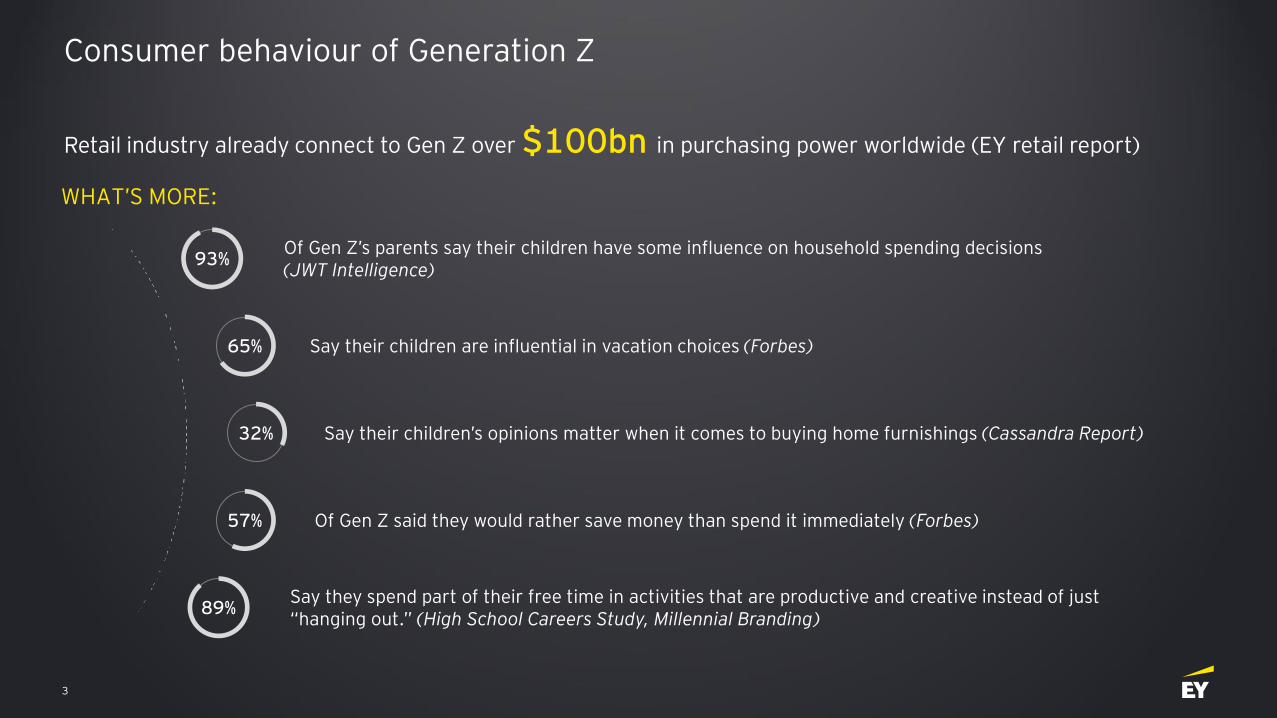

Consumer behaviour of Generation Z

Retail industry already connect to Gen Z over $100bn in purchasing power worldwide (EY retail report)

Of Gen Z’s parents say their children have some influence on household spending decisions (JWT Intelligence)

93%

WHAT’S MORE:

Say their children are influential in vacation choices (Forbes)65%

32% Say their children’s opinions matter when it comes to buying home furnishings (Cassandra Report)

57% Of Gen Z said they would rather save money than spend it immediately (Forbes)

89%Say they spend part of their free time in activities that are productive and creative instead of just “hanging out.” (High School Careers Study, Millennial Branding)

4

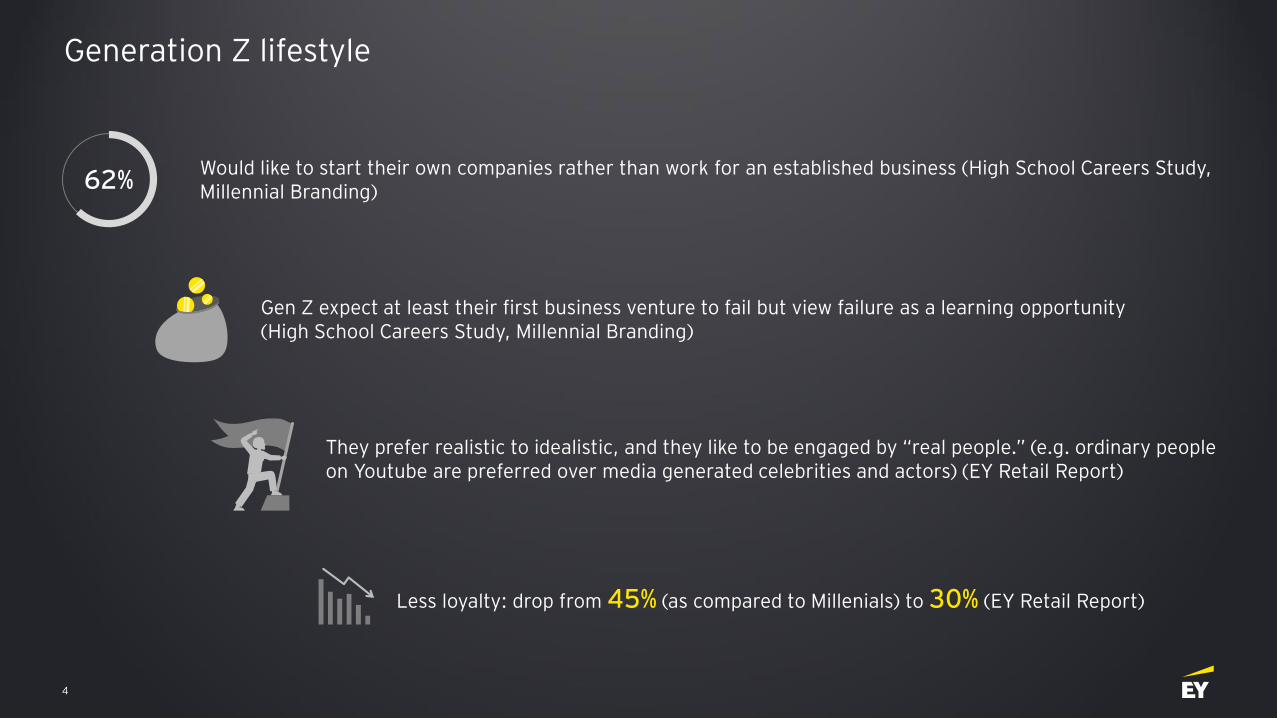

Generation Z lifestyle

Would like to start their own companies rather than work for an established business (High School Careers Study, Millennial Branding)

Gen Z expect at least their first business venture to fail but view failure as a learning opportunity (High School Careers Study, Millennial Branding)

They prefer realistic to idealistic, and they like to be engaged by “real people.” (e.g. ordinary people on Youtube are preferred over media generated celebrities and actors) (EY Retail Report)

62%

Less loyalty: drop from 45% (as compared to Millenials) to 30% (EY Retail Report)

5

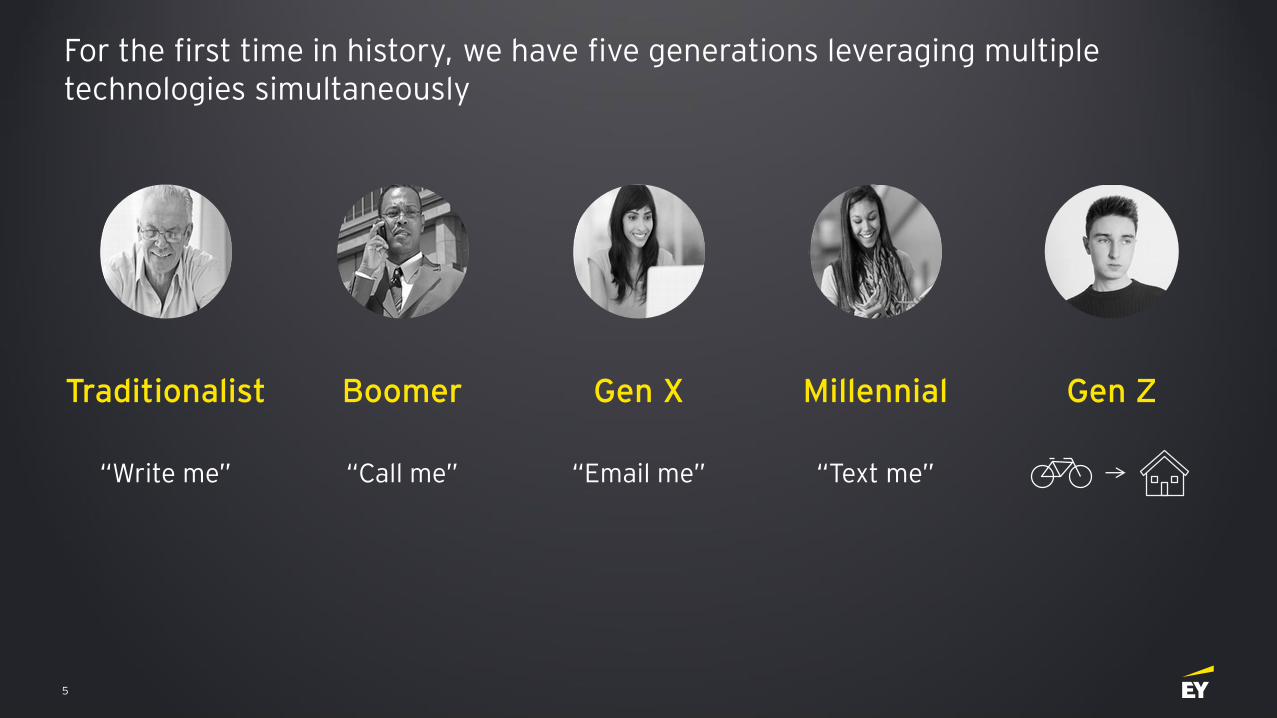

“Write me” “Call me” “Email me” “Text me”

MillennialBoomer Gen XTraditionalist Gen Z

For the first time in history, we have five generations leveraging multiple technologies simultaneously

6

Gen Z will have 10 to 14 jobs in their career …

Source: Rise of Gen Z. New Challenge for retailers. EY Report 2017

by age of 38

Research suggests that Gen Z are already adapting their aspirations to the realities of the new digital economy

7

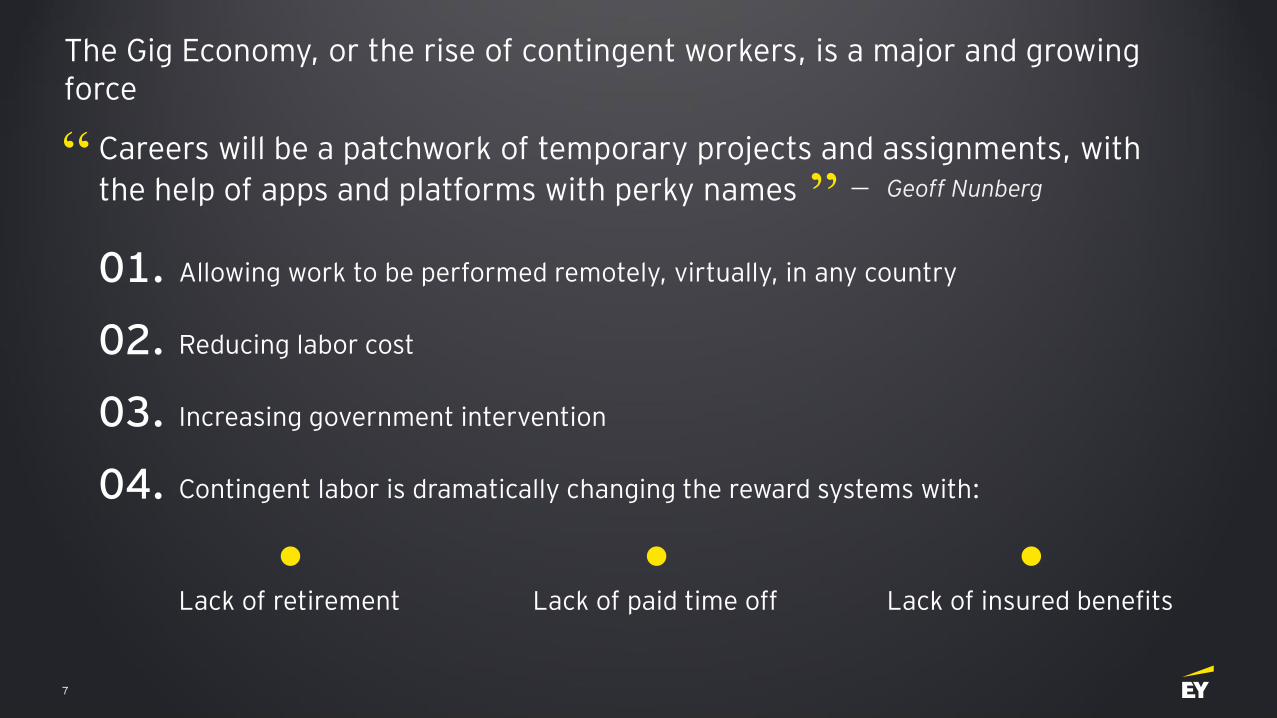

The Gig Economy, or the rise of contingent workers, is a major and growing force

Careers will be a patchwork of temporary projects and assignments, with

the help of apps and platforms with perky names “

” Geoff Nunberg

01. Allowing work to be performed remotely, virtually, in any country

02. Reducing labor cost

03. Increasing government intervention

04. Contingent labor is dramatically changing the reward systems with:

Lack of retirement Lack of insured benefitsLack of paid time off

8

Get their apartment cleaned

Get their groceries bought and delivered

Get their clothes washed Get their flowers delivered

Get a personal assistant

Get presents wrapped and delivered

Gen Z creates and consumes gig work

9

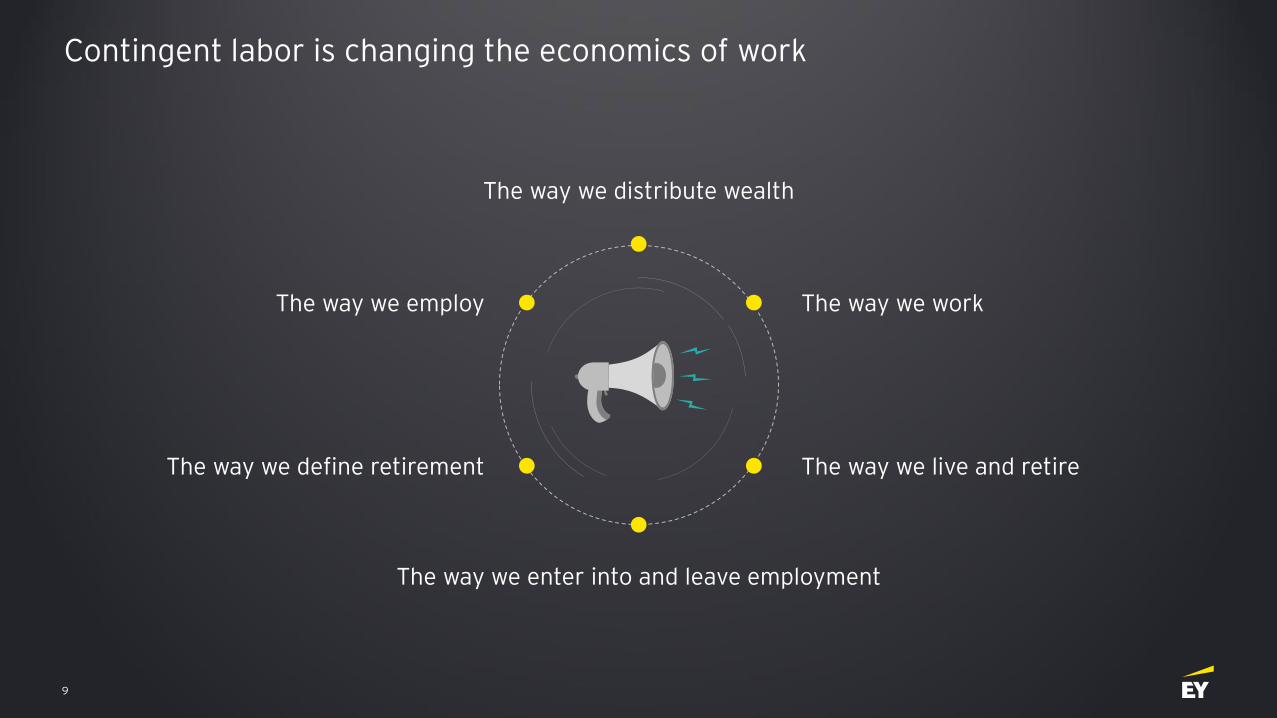

Contingent labor is changing the economics of work

The way we work

The way we enter into and leave employment

The way we define retirement The way we live and retire

The way we employ

The way we distribute wealth

10

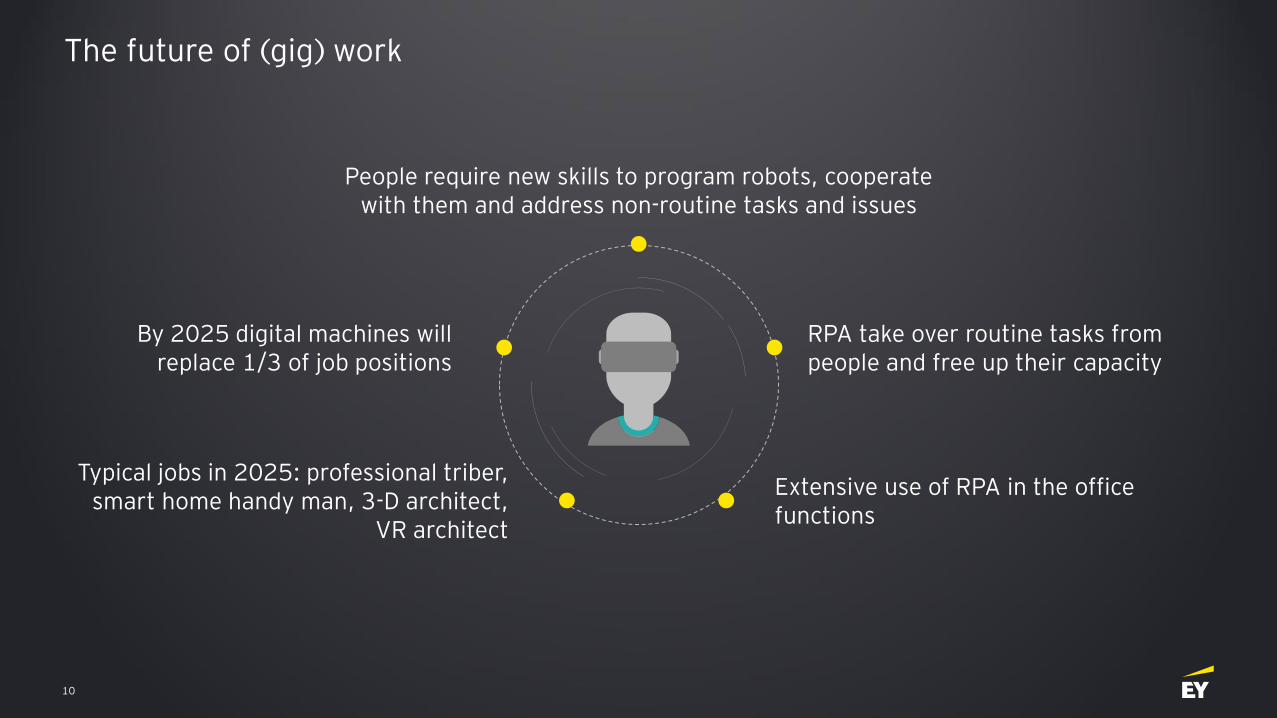

The future of (gig) work

RPA take over routine tasks from people and free up their capacity

Typical jobs in 2025: professional triber, smart home handy man, 3-D architect,

VR architect

Extensive use of RPA in the office functions

By 2025 digital machines will replace 1/3 of job positions

People require new skills to program robots, cooperate with them and address non-routine tasks and issues

11

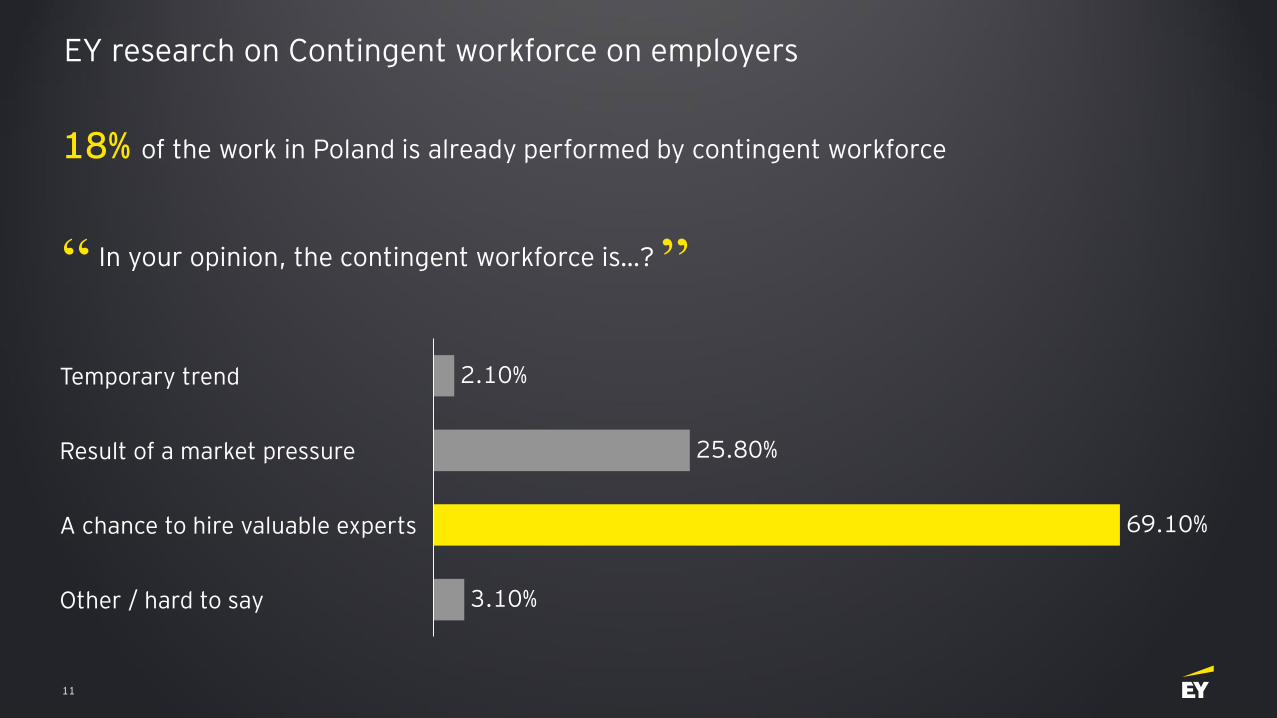

EY research on Contingent workforce on employers

18% of the work in Poland is already performed by contingent workforce

In your opinion, the contingent workforce is…?“ ”

69.10%A chance to hire valuable experts

Temporary trend

3.10%

Result of a market pressure

Other / hard to say

25.80%

2.10%

12

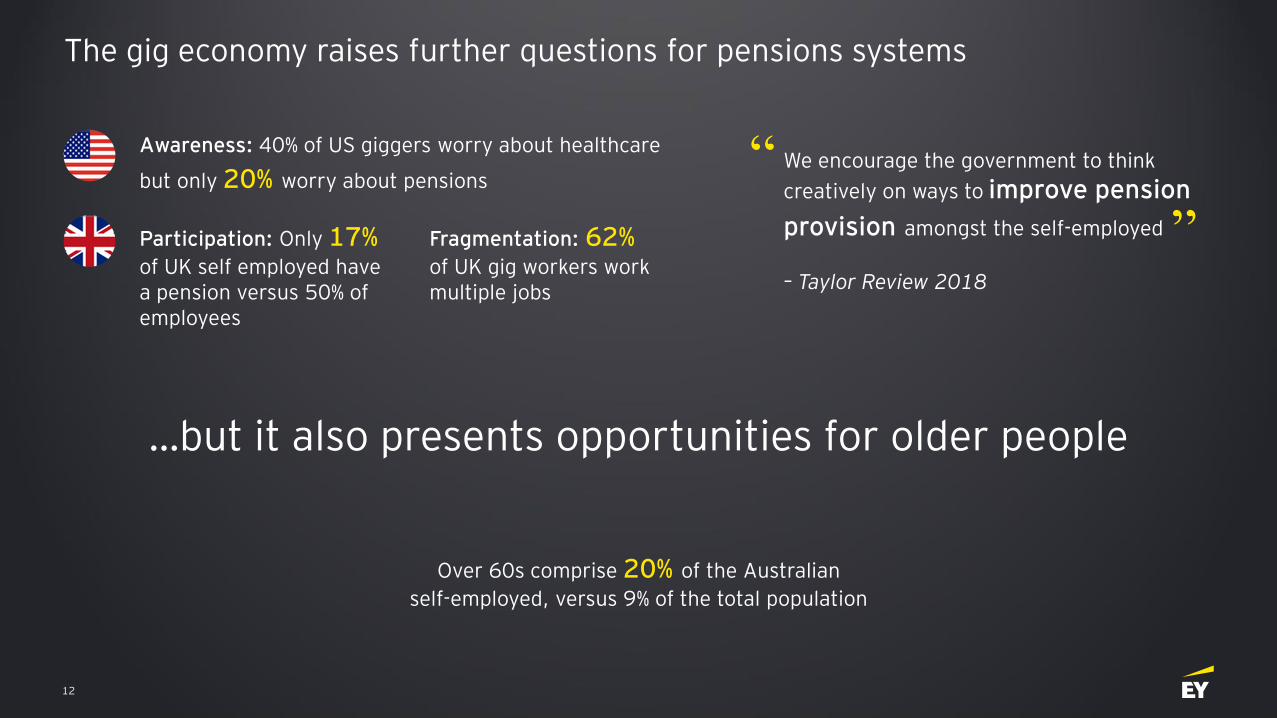

The gig economy raises further questions for pensions systems

Fragmentation: 62%of UK gig workers work multiple jobs

Awareness: 40% of US giggers worry about healthcare

but only 20% worry about pensions

Over 60s comprise 20% of the Australian

self-employed, versus 9% of the total population

Participation: Only 17%of UK self employed have a pension versus 50% of employees

…but it also presents opportunities for older people

We encourage the government to think

creatively on ways to improve pension

provision amongst the self-employed

– Taylor Review 2018

“

”

13

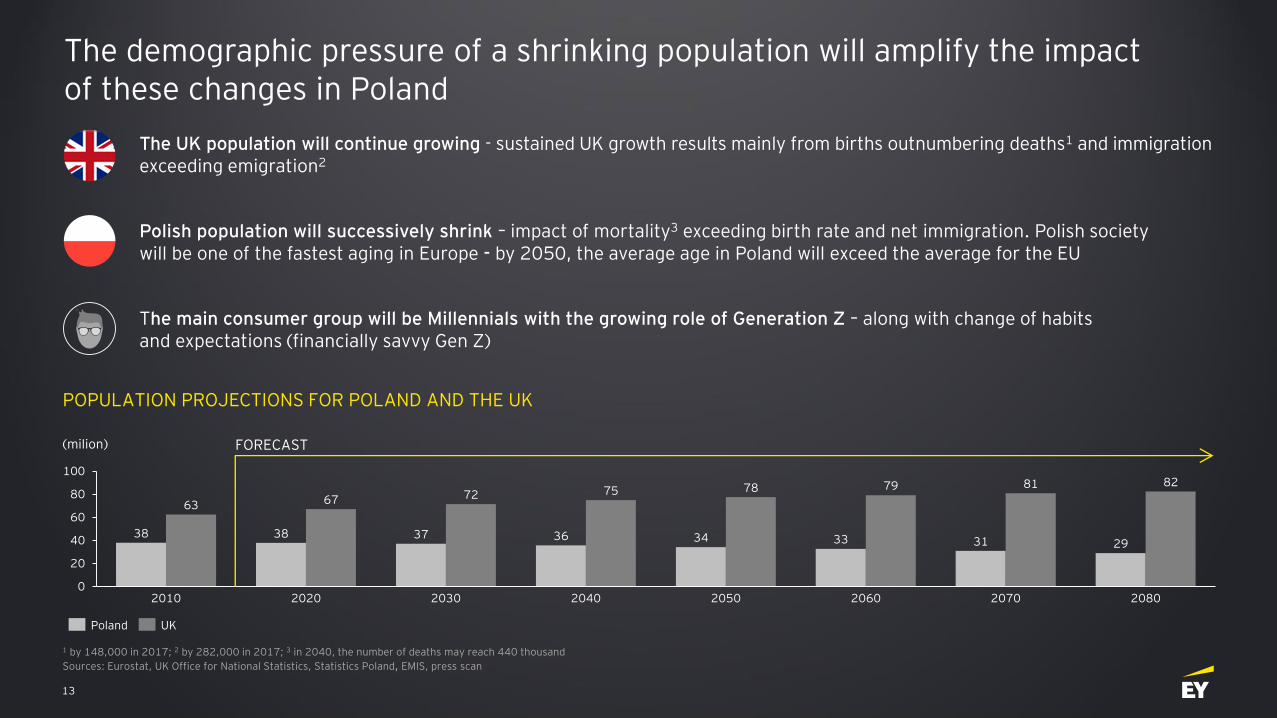

The demographic pressure of a shrinking population will amplify the impact of these changes in Poland

38 38 37 36 34 33 31 29

63 67 72 75 78 79 81 82

0

20

40

60

80

100

2060 208020702010 2020 2030 2040 2050

POPULATION PROJECTIONS FOR POLAND AND THE UK

Sources: Eurostat, UK Office for National Statistics, Statistics Poland, EMIS, press scan

Poland UK

The main consumer group will be Millennials with the growing role of Generation Z – along with change of habits and expectations (financially savvy Gen Z)

Polish population will successively shrink – impact of mortality3 exceeding birth rate and net immigration. Polish society will be one of the fastest aging in Europe - by 2050, the average age in Poland will exceed the average for the EU

The UK population will continue growing - sustained UK growth results mainly from births outnumbering deaths1 and immigration exceeding emigration2

(milion)

1 by 148,000 in 2017; 2 by 282,000 in 2017; 3 in 2040, the number of deaths may reach 440 thousand

FORECAST

14

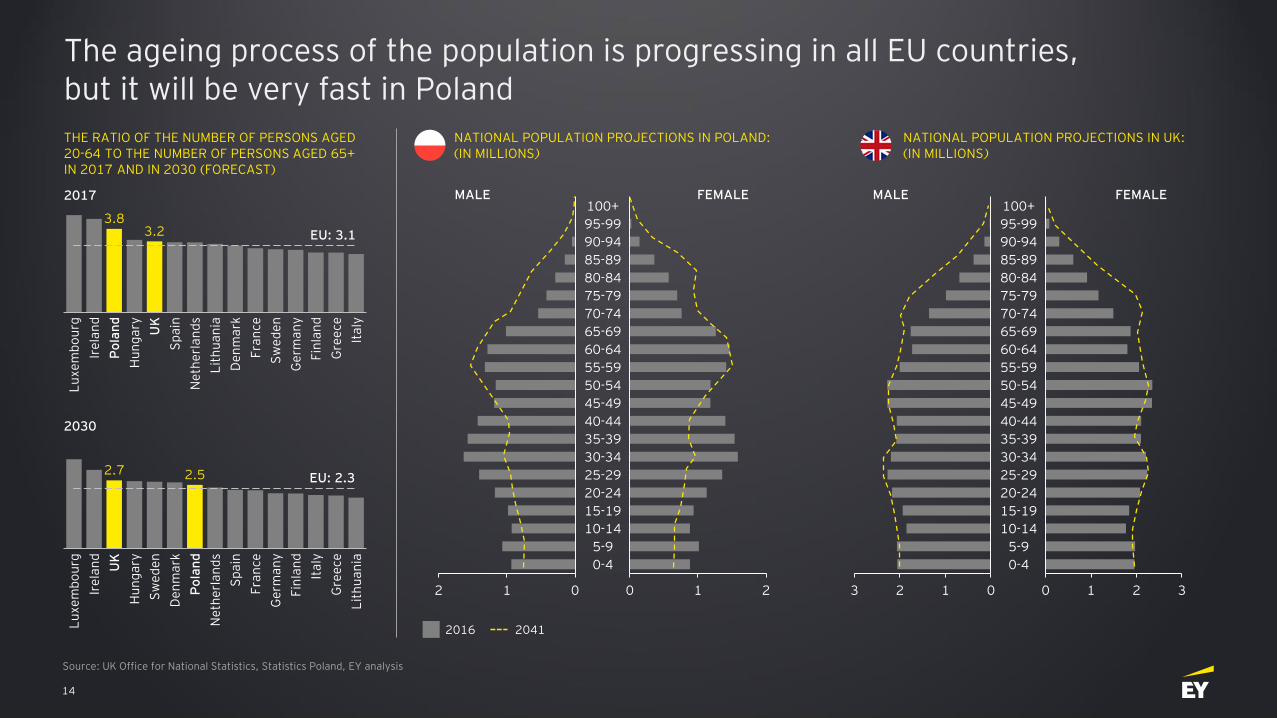

The ageing process of the population is progressing in all EU countries, but it will be very fast in Poland

Lit

hu

an

ia

Po

lan

d

Lu

xe

mb

ou

rg

Ire

lan

d

Hu

ng

ary

Sp

ain

3.2

UK

Ne

the

rla

nd

s

De

nm

ark

Fra

nce

Sw

ed

en

Gre

ece

Ge

rma

ny

Fin

lan

d

EU: 3.1

Ita

ly

3.8

Sw

ed

en

Hu

ng

ary

Lu

xe

mb

ou

rg

Fra

nce

Ne

the

rla

nd

s

Ire

lan

d

2.7

UK

De

nm

ark

Po

lan

d

Sp

ain

Ge

rma

ny

Fin

lan

d

Ita

ly

Gre

ece

EU: 2.3

Lit

hu

an

ia

2.5

THE RATIO OF THE NUMBER OF PERSONS AGED 20-64 TO THE NUMBER OF PERSONS AGED 65+ IN 2017 AND IN 2030 (FORECAST)

2017

2030

NATIONAL POPULATION PROJECTIONS IN POLAND:(IN MILLIONS)

NATIONAL POPULATION PROJECTIONS IN UK:(IN MILLIONS)

012

5-9

90-94

50-54

100+

80-84

95-99

85-89

75-79

70-74

65-69

60-64

55-59

45-49

40-44

35-39

30-34

25-29

20-24

15-19

10-14

0-4

0 1 2 2 013

50-54

45-49

90-94

100+

20-24

85-89

95-99

30-34

80-84

75-79

70-74

65-69

60-64

55-59

25-29

40-44

35-39

15-19

10-14

5-9

0-4

10 2 3

MALE FEMALE MALE FEMALE

2016 2041

Source: UK Office for National Statistics, Statistics Poland, EY analysis

15

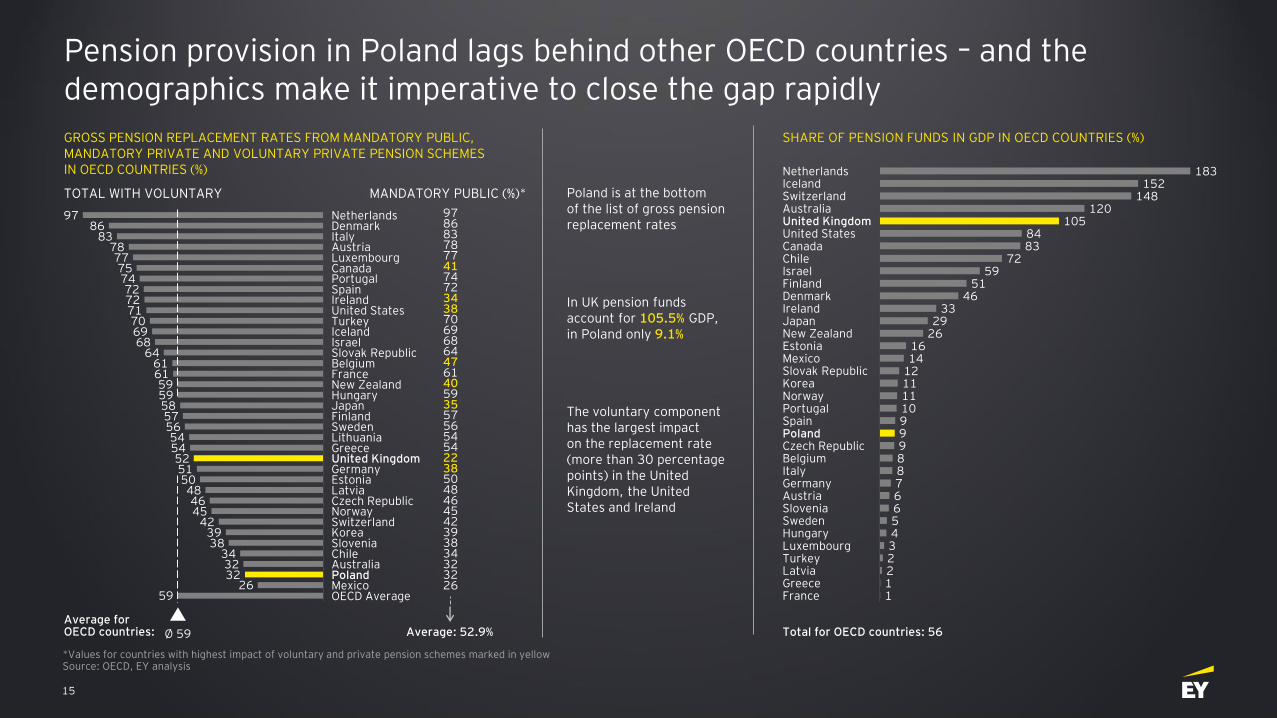

Pension provision in Poland lags behind other OECD countries – and the demographics make it imperative to close the gap rapidly

Average for OECD countries:

183152

148120

1058483

7259

5146

3329

261614

12111110999887665432211

Denmark

NetherlandsIceland

Hungary

SwitzerlandAustralia

Canada

United Kingdom

Israel

United States

Chile

Japan

Finland

Turkey

Czech Republic

Ireland

New Zealand

France

Slovenia

Estonia

Luxembourg

MexicoSlovak RepublicKoreaNorwayPortugalSpainPoland

BelgiumItaly

Greece

GermanyAustria

Sweden

Latvia

Total for OECD countries: 56

MANDATORY PUBLIC (%)* Poland is at the bottom of the list of gross pension replacement rates

In UK pension funds account for 105.5% GDP, in Poland only 9.1%

The voluntary component has the largest impact on the replacement rate (more than 30 percentage points) in the United Kingdom, the United States and Ireland

978683787741747234387069686447614059355756545422385048464542393834323226

Average: 52.9%

TOTAL WITH VOLUNTARY

9786

8378777574727271706968

64616159595857565454525150484645

423938

343232

2659

Denmark

Ø 59

Spain

OECD Average

United Kingdom

Italy

Portugal

Luxembourg

France

Canada

IrelandUnited States

Norway

Turkey

Mexico

Australia

Czech Republic

IcelandIsraelSlovak RepublicBelgium

New ZealandHungaryJapanFinlandSwedenLithuania

Austria

Greece

GermanyEstonia

Korea

Latvia

Chile

Poland

Switzerland

Netherlands

Slovenia

GROSS PENSION REPLACEMENT RATES FROM MANDATORY PUBLIC, MANDATORY PRIVATE AND VOLUNTARY PRIVATE PENSION SCHEMES IN OECD COUNTRIES (%)

SHARE OF PENSION FUNDS IN GDP IN OECD COUNTRIES (%)

Source: OECD, EY analysis*Values for countries with highest impact of voluntary and private pension schemes marked in yellow

16

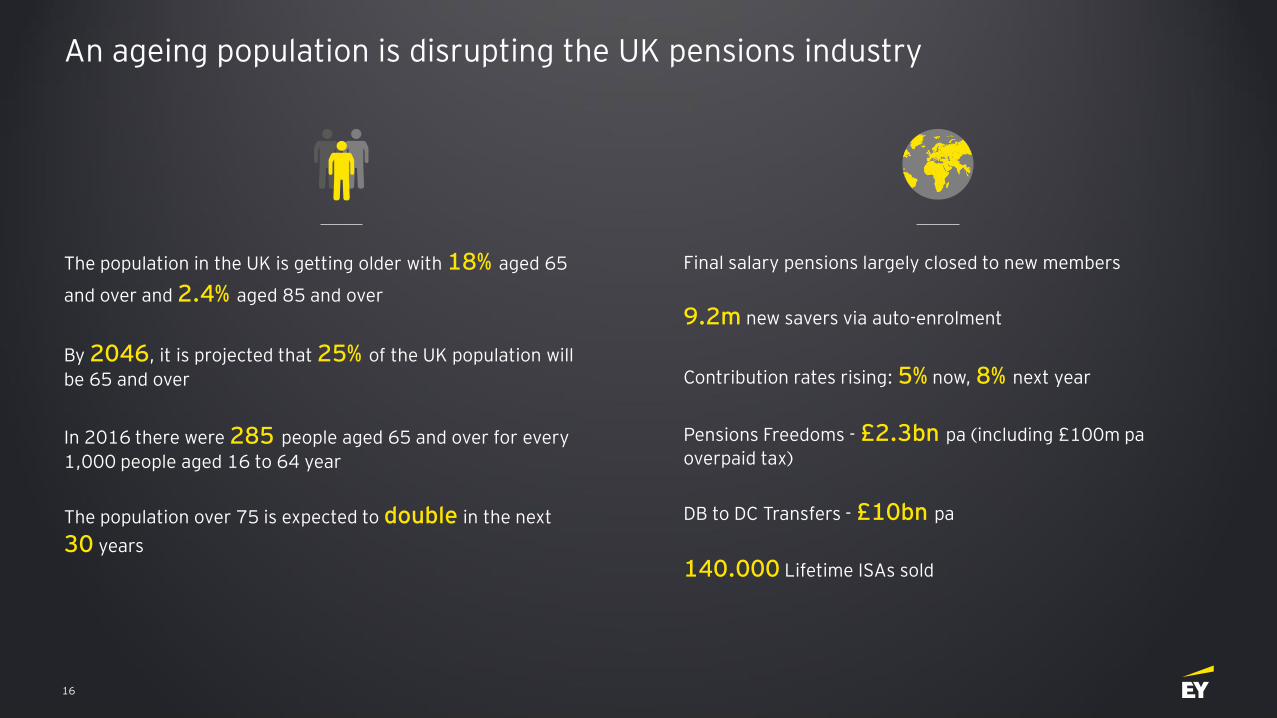

An ageing population is disrupting the UK pensions industry

The population in the UK is getting older with 18% aged 65

and over and 2.4% aged 85 and over

By 2046, it is projected that 25% of the UK population will

be 65 and over

In 2016 there were 285 people aged 65 and over for every

1,000 people aged 16 to 64 year

The population over 75 is expected to double in the next

30 years

Final salary pensions largely closed to new members

9.2m new savers via auto-enrolment

Contribution rates rising: 5% now, 8% next year

Pensions Freedoms - £2.3bn pa (including £100m pa

overpaid tax)

DB to DC Transfers - £10bn pa

140.000 Lifetime ISAs sold

17

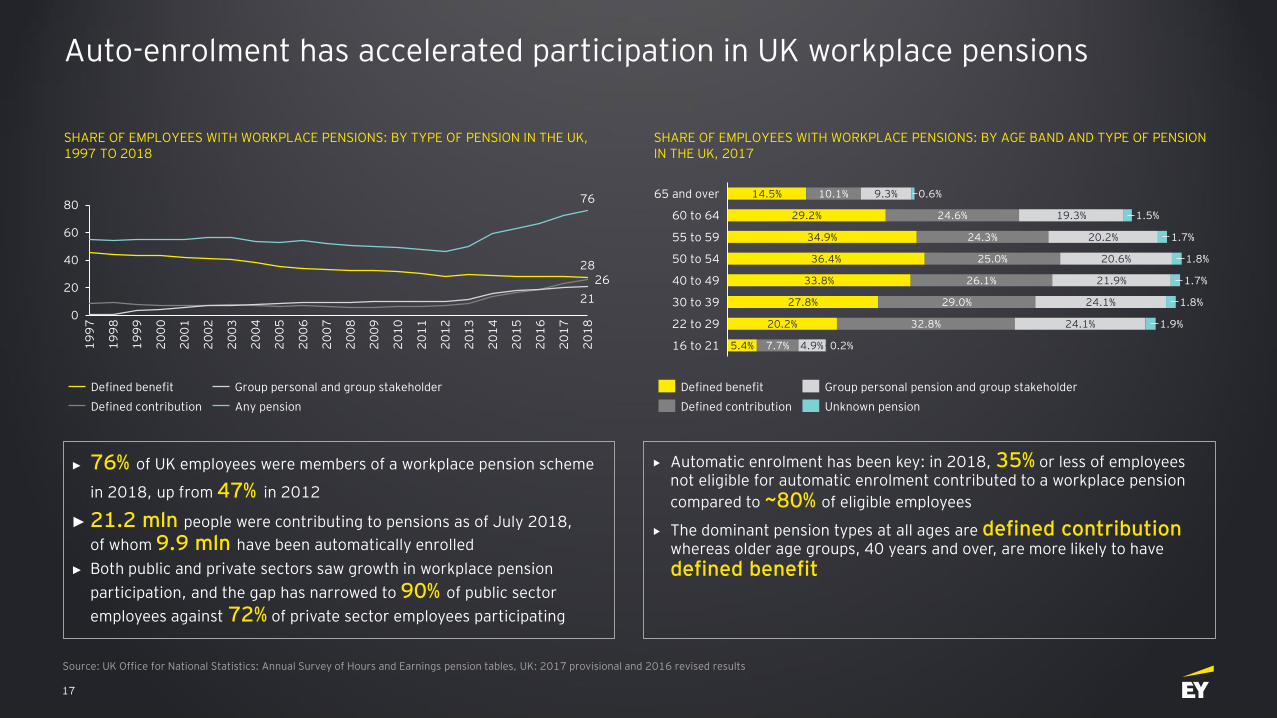

Auto-enrolment has accelerated participation in UK workplace pensions

2826

21

76

0

20

40

60

802

00

2

20

00

19

97

20

14

19

98

19

99

20

04

20

17

20

01

20

03

20

07

20

05

20

06

20

08

20

09

20

10

20

11

20

12

20

13

20

15

20

16

20

18

Any pension

Defined benefit Group personal and group stakeholder

Defined contribution

► 76% of UK employees were members of a workplace pension scheme

in 2018, up from 47% in 2012

► 21.2 mln people were contributing to pensions as of July 2018,

of whom 9.9 mln have been automatically enrolled

► Both public and private sectors saw growth in workplace pension

participation, and the gap has narrowed to 90% of public sector

employees against 72% of private sector employees participating

1.8%

24.3%

65 and over

5.4%

9.3%10.1%

19.3%24.6%

16 to 21

29.2%60 to 64

1.7%20.2%34.9%55 to 59

20.2%

1.5%

14.5%

20.6%25.0%

24.1%

24.1%

36.4%50 to 54

26.1% 1.7%33.8%40 to 49

1.8%

1.9%

29.0%27.8%30 to 39

21.9%

22 to 29

4.9%

0.6%

0.2%7.7%

32.8%

Defined benefit

Unknown pensionDefined contribution

Group personal pension and group stakeholder

SHARE OF EMPLOYEES WITH WORKPLACE PENSIONS: BY TYPE OF PENSION IN THE UK, 1997 TO 2018

SHARE OF EMPLOYEES WITH WORKPLACE PENSIONS: BY AGE BAND AND TYPE OF PENSION IN THE UK, 2017

Automatic enrolment has been key: in 2018, 35% or less of employees not eligible for automatic enrolment contributed to a workplace pension

compared to ~80% of eligible employees

The dominant pension types at all ages are defined contribution whereas older age groups, 40 years and over, are more likely to have

defined benefit

Source: UK Office for National Statistics: Annual Survey of Hours and Earnings pension tables, UK: 2017 provisional and 2016 revised results

18

There is more to do: confidence and understanding among UK adults is low

35% of the adult population in UK say they don’t have a pension

43% of the population admit they don’t know how much they will need

55% of people feel that £100,000 is enough to retire comfortably

28% of people think they are on track to meet this

80%Of Millennials don’t believe they will meet their predicted pension amount needed to retire comfortably (average prediction £126,400)

59%Of Baby Boomers don’t believe they will meet their predicted pension amount needed to retire comfortably (average prediction £211,800)

55

32

32

20

33

44

25

25

24

32

19

41

% of population who say they don’t have pension

% of population who think GBP 50,000 is enough to retire comfortably

% of population who are not sure how much pension they have

% of population who think they are on track to achieve their minimum pension amount

Millenials Baby BoomersGen X

ENGAGEMENT IN PENSION SAVINGS BY AGE

75%Of Gen X don’t believe they will meet their predicted pension amount needed to retire comfortably (average prediction £188,300)

42.6% Of 18-23 year-olds find pensions too complicated

11.6% Of people close to retirement age state that pensions are too complicated

Source: ABI, Global Data 2018, Statista, press scan Source: Aegon UK readiness report: How savers are behaving in the new pensions world (April 2017)

19

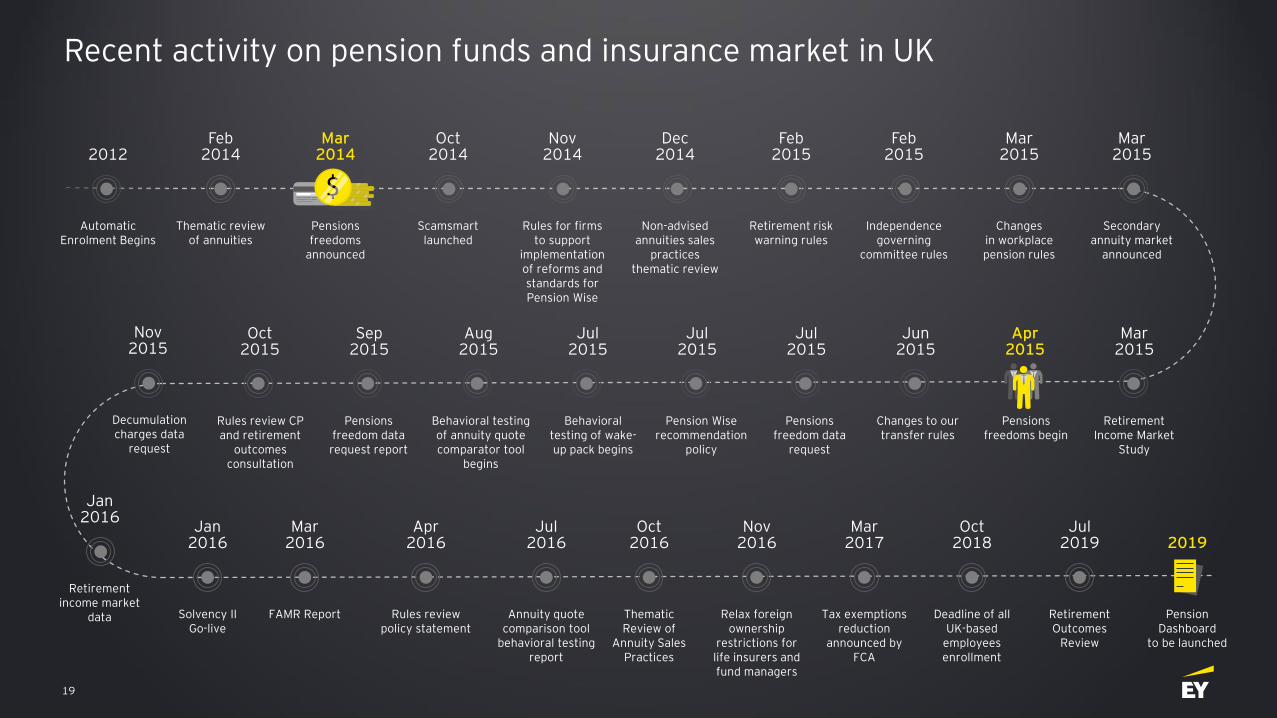

Recent activity on pension funds and insurance market in UK

Automatic Enrolment Begins

Thematic review of annuities

2012Feb

2014

Pensions freedoms

announced

Scamsmartlaunched

Mar 2014

Oct 2014

Rules for firms to support

implementation of reforms and standards for Pension Wise

Non-advised annuities sales

practices thematic review

Nov 2014

Dec 2014

Retirement risk warning rules

Independence governing

committee rules

Feb 2015

Feb 2015

Changes in workplace pension rules

Secondary annuity market

announced

Mar 2015

Mar 2015

Retirement Income Market

Study

Mar 2015

Pensions freedoms begin

Apr 2015

Changes to our transfer rules

Jun 2015

Pensions freedom data

request

Jul 2015

Pension Wise recommendation

policy

Jul 2015

Behavioral testing of wake-up pack begins

Jul 2015

Behavioral testing of annuity quote comparator tool

begins

Aug 2015

Pensions freedom data request report

Sep 2015

Rules review CP and retirement

outcomes consultation

Oct 2015

Decumulationcharges data

request

Retirement income market

data

Nov 2015

Jan 2016

Solvency II Go-live

FAMR Report

Jan 2016

Mar 2016

Rules review policy statement

Apr 2016

Thematic Review of

Annuity Sales Practices

Oct 2016

Pension Dashboard

to be launched

2019

Relax foreign ownership

restrictions for life insurers and fund managers

Nov 2016

Tax exemptions reduction

announced by FCA

Mar2017

Deadline of all UK-based

employees enrollment

Oct 2018

Retirement Outcomes

Review

Jul 2019

Annuity quote comparison tool

behavioral testing report

Jul 2016

20

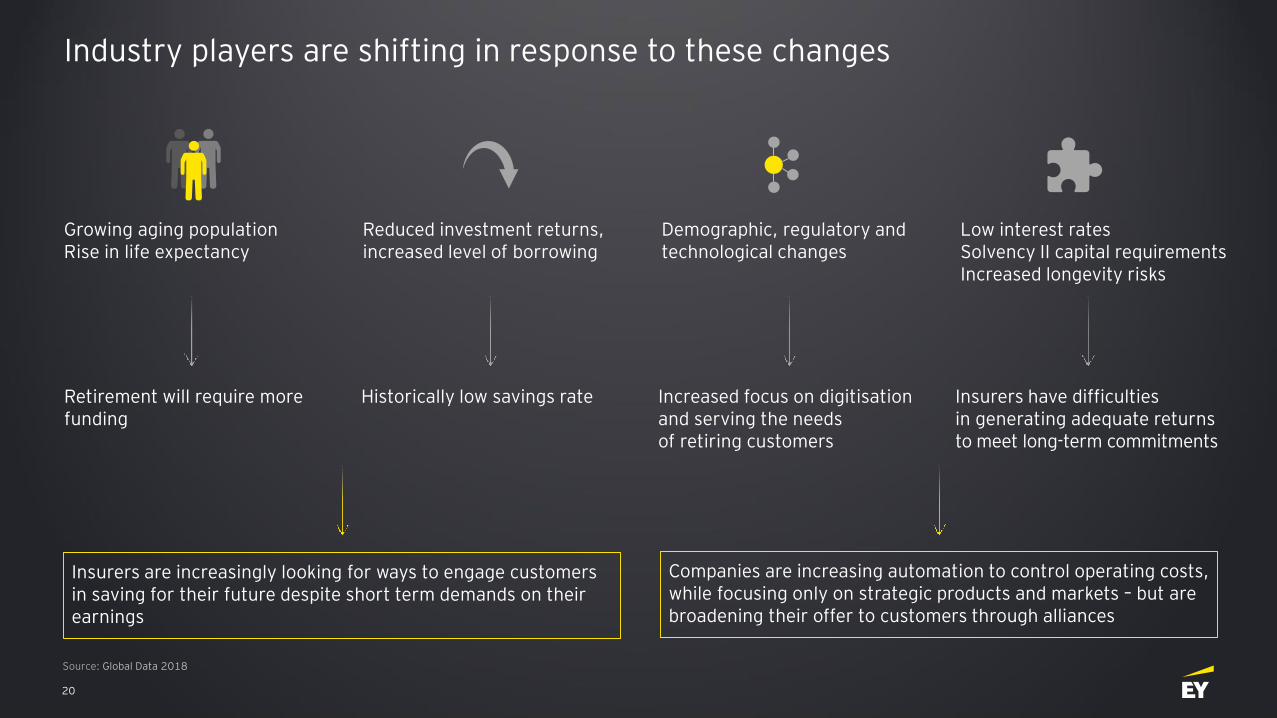

Industry players are shifting in response to these changes

Insurers are increasingly looking for ways to engage customers in saving for their future despite short term demands on their earnings

Companies are increasing automation to control operating costs, while focusing only on strategic products and markets – but are broadening their offer to customers through alliances

Demographic, regulatory and technological changes

Low interest rates Solvency II capital requirements Increased longevity risks

Growing aging populationRise in life expectancy

Reduced investment returns, increased level of borrowing

Retirement will require more funding

Historically low savings rate Increased focus on digitisationand serving the needs of retiring customers

Insurers have difficulties in generating adequate returns to meet long-term commitments

Source: Global Data 2018

21

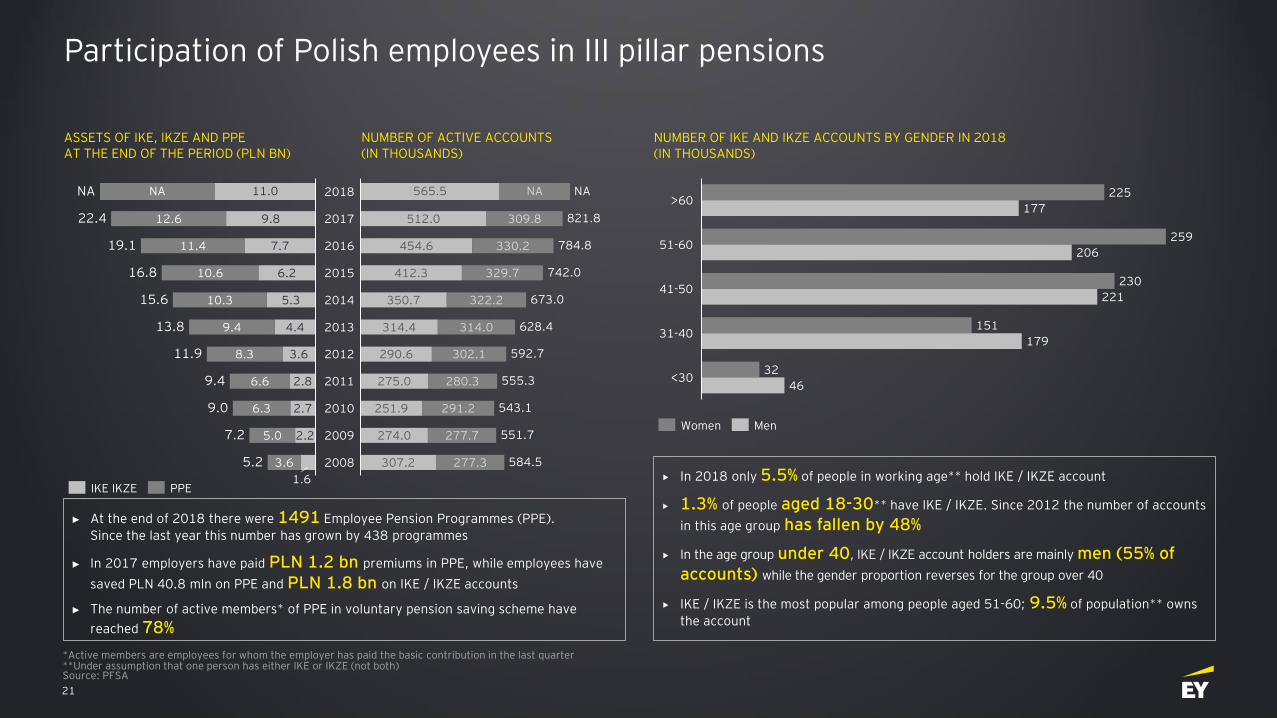

Participation of Polish employees in III pillar pensions

454.6

NA565.5

274.0

309.8

673.0

412.3

277.7

512.0

329.7

330.2

322.2350.7

314.0314.4

302.1290.6

307.2

280.3 555.3

251.9

275.0

291.2

277.3

551.7

NA

821.8

784.8

742.0

628.4

592.7

543.1

584.5

2017

NA

5.3

2018

7.7

12.6 9.8

2.2

11.4

2011

2016

13.8

10.6

6.6

6.2 2015

10.3 2014

9.4 4.4 2013

8.3 20123.6

2.8

6.3 2.7

2009

2010

5.0

3.6

15.6

1.6

11.0NA

9.0

22.4

19.1

2008

9.4

11.9

7.2

5.2

16.8

IKE IKZE PPE

51-60

>60

46

41-50

31-40

<30

177

225

259

206

230

221

151

179

32

Women Men

► At the end of 2018 there were 1491 Employee Pension Programmes (PPE).

Since the last year this number has grown by 438 programmes

► In 2017 employers have paid PLN 1.2 bn premiums in PPE, while employees have

saved PLN 40.8 mln on PPE and PLN 1.8 bn on IKE / IKZE accounts

► The number of active members* of PPE in voluntary pension saving scheme have

reached 78%

In 2018 only 5.5% of people in working age** hold IKE / IKZE account

1.3% of people aged 18-30** have IKE / IKZE. Since 2012 the number of accounts

in this age group has fallen by 48%

In the age group under 40, IKE / IKZE account holders are mainly men (55% of accounts) while the gender proportion reverses for the group over 40

IKE / IKZE is the most popular among people aged 51-60; 9.5% of population** owns

the account

ASSETS OF IKE, IKZE AND PPEAT THE END OF THE PERIOD (PLN BN)

NUMBER OF IKE AND IKZE ACCOUNTS BY GENDER IN 2018 (IN THOUSANDS)

NUMBER OF ACTIVE ACCOUNTS (IN THOUSANDS)

*Active members are employees for whom the employer has paid the basic contribution in the last quarter**Under assumption that one person has either IKE or IKZE (not both)Source: PFSA

22

Life insurance market data

GROSS LIFE PREMIUMS WRITTEN AND LIFE INSURANCE PENETRATION IN POLAND AND UK

Source: BMI, OECD

0

1

2

3

4

5

0

2

4

6

8

102

01

0

20

11

20

09

20

08

6.0

20

12

5.1

%

6.7

20

13

20

14

6.8

20

15

20

16

6.9

20

17

20

18

9.9

7.6

6.3 6.65.5 5.8

-6.4%

Gross life premiums penetration (% of GDP) Gross life premiums written (EUR bn)

Poland

0

5

10

15

20

25

30

35

0

100

200

300

400

20

08

213.6

%

20

12

20

09

20

14

20

10

20

11

20

13

20

15

20

16

20

17

148.8

20

18

233.4

174.7181.7 167.1201.7

168.4 184.2 200.3 181.5

-2.5%

UK

In the UK life insurance was the largest segment in the insurance

industry accounting for 68.1% of the gross written premiums

(in 2018). In Poland this ratio amounts to only 34.9%

Both in Poland and in UK, gross life insurance penetration

is gradually falling from 2.7% in Poland in 2008 to 1.0% ten years later. In the UK the peak was reached in 2008 (almost

12%) to current 7.6%

Since the financial crisis in 2008, GWP in life segment has

dropped by 2.5% annually in the UK and by 6.4% annually in Poland, respectively

In Europe weak performance in life insurance business was

mainly due to low interest rates, complex products and economic slowdown. However, margins have improved

Group life insurance in UK is recording a positive growth compared to an individual offering. It was mainly driven by demand for work-based pension products

In Poland, decrease in GWP in life insurance is mainly connected

with fast decreasing investment products premiums

23

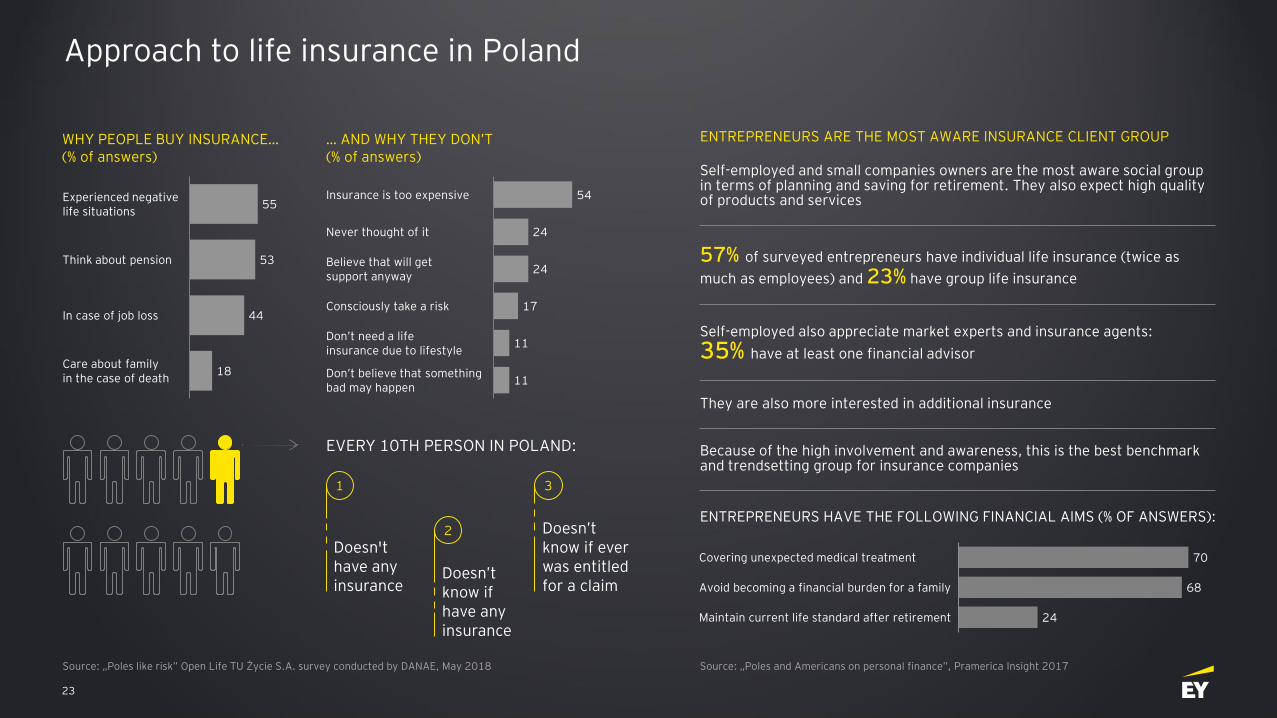

Approach to life insurance in Poland

WHY PEOPLE BUY INSURANCE…(% of answers)

55

53

44

18

Experienced negative life situations

Think about pension

Care about family in the case of death

In case of job loss

… AND WHY THEY DON’T(% of answers)

54

24

24

17

11

11

Consciously take a risk

Insurance is too expensive

Never thought of it

Believe that will get support anyway

Don’t need a life insurance due to lifestyle

Don’t believe that something bad may happen

EVERY 10TH PERSON IN POLAND:

70

68

24Maintain current life standard after retirement

Covering unexpected medical treatment

Avoid becoming a financial burden for a family

Doesn'thave any insurance

1

Doesn’t know if have any insurance

2 Doesn’t know if ever was entitled for a claim

3

ENTREPRENEURS HAVE THE FOLLOWING FINANCIAL AIMS (% OF ANSWERS):

Self-employed and small companies owners are the most aware social group in terms of planning and saving for retirement. They also expect high quality of products and services

57% of surveyed entrepreneurs have individual life insurance (twice as

much as employees) and 23% have group life insurance

Self-employed also appreciate market experts and insurance agents:

35% have at least one financial advisor

They are also more interested in additional insurance

Because of the high involvement and awareness, this is the best benchmark and trendsetting group for insurance companies

Source: „Poles like risk” Open Life TU Życie S.A. survey conducted by DANAE, May 2018 Source: „Poles and Americans on personal finance”, Pramerica Insight 2017

ENTREPRENEURS ARE THE MOST AWARE INSURANCE CLIENT GROUP

24

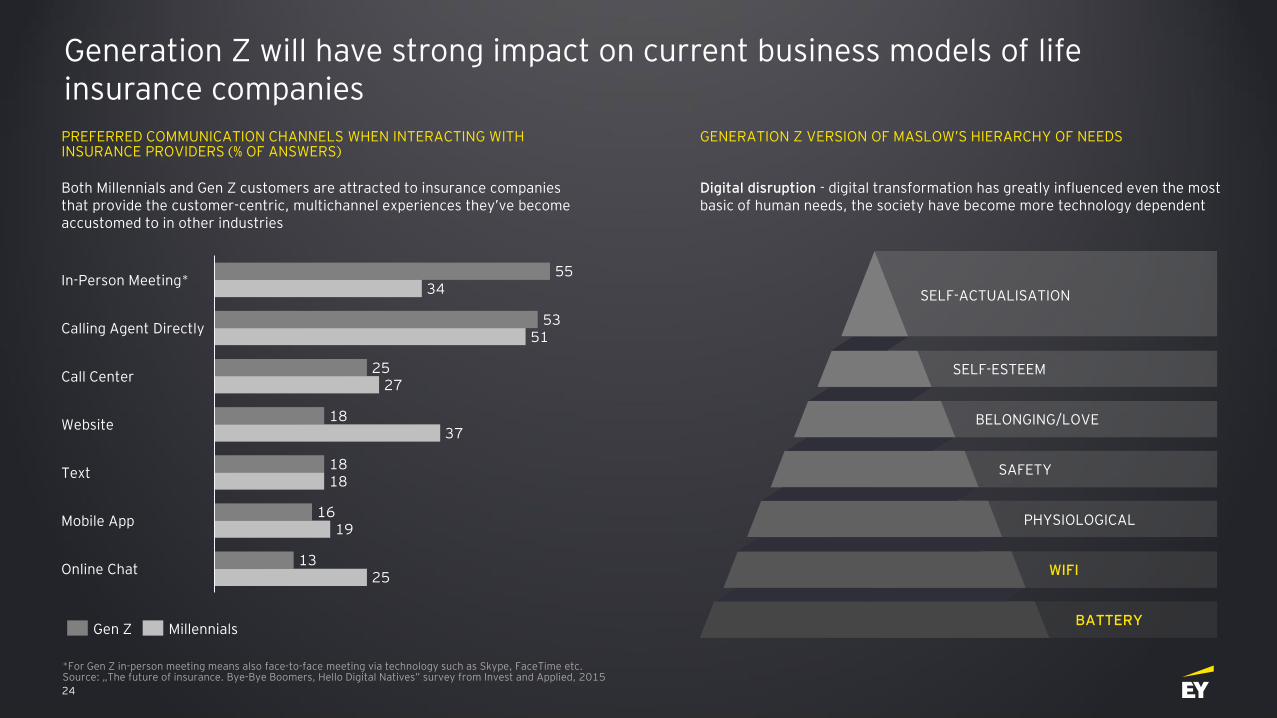

Generation Z will have strong impact on current business models of lifeinsurance companies

PREFERRED COMMUNICATION CHANNELS WHEN INTERACTING WITH INSURANCE PROVIDERS (% OF ANSWERS)

Both Millennials and Gen Z customers are attracted to insurance companies that provide the customer-centric, multichannel experiences they’ve become accustomed to in other industries

55

53

25

18

18

16

13

34

51

27

37

18

19

25Online Chat

Mobile App

Call Center

Calling Agent Directly

Website

In-Person Meeting*

Text

Gen Z Millennials

*For Gen Z in-person meeting means also face-to-face meeting via technology such as Skype, FaceTime etc.Source: „The future of insurance. Bye-Bye Boomers, Hello Digital Natives” survey from Invest and Applied, 2015

Digital disruption - digital transformation has greatly influenced even the most basic of human needs, the society have become more technology dependent

SELF-ACTUALISATION

SELF-ESTEEM

BELONGING/LOVE

SAFETY

PHYSIOLOGICAL

WIFI

BATTERY

GENERATION Z VERSION OF MASLOW’S HIERARCHY OF NEEDS

25

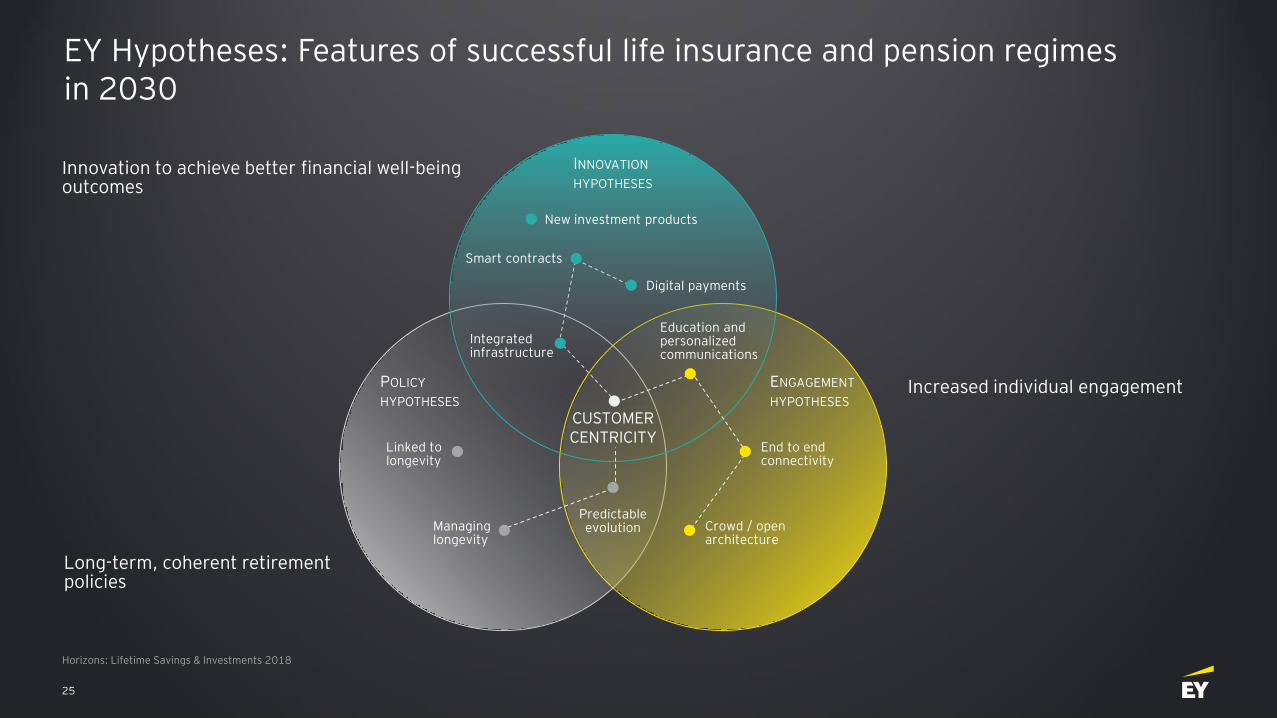

EY Hypotheses: Features of successful life insurance and pension regimesin 2030

Horizons: Lifetime Savings & Investments 2018

Innovation to achieve better financial well-being outcomes

Increased individual engagement

Long-term, coherent retirement policies

POLICY

HYPOTHESES

INNOVATION

HYPOTHESES

Digital payments

New investment products

Smart contracts

Integrated infrastructure

CUSTOMER CENTRICITY

Education and personalized communications

Linked to longevity

ENGAGEMENT

HYPOTHESES

End to end connectivity

Crowd / open architecture

Predictable evolutionManaging

longevity

26

Karol RaźniewskiAssociate Partner

[email protected]+48 504 112 771

Jason WhyteAssociate Partner

[email protected]+44 7973 193 715

Wojciech SoleniecPartner

[email protected]+48 660 440 085

Marcin SadekPartner

[email protected]+48 519 404 991

Contact: