Embed Size (px)

Citation preview

“Agriculture ... is our wisest pursuit, because

it will in the end contribute most to real

wealth, good morals, and happiness.”

Thomas Jefferson

General overview for

investors in Hungary’s

agriculture and food

industry

WHY INVEST?

• Hungary is world famous for its abundant resources of drinking, thermal, mineral and

ground waters. Combined with the country’s excellent geolocation this provides a

unique and remarkable opportunity for various business purposes, such as agriculture

and food industry;

• Research on comparative advantage shows that Hungary has advantages of food

industry product exports and trade opportunities. Cereals, meat, sugar, and livestock

export are especially lucrative segments to invest in;

• Hungarian food production is expected to increase by 20% in the next four years.

Domestic demand is also expected to grow by 20%;

• Hungary’s agricultural and food industry is strongly integrated into the European

markets, giving opportunities for non-EU based companies to reach a huge market of

almost 500 million EU citizens. The Russian, Balkan and Eastern European markets are

also within a close reach;

• Total arable land in Hungary is 7.4 million hectares, with world class soil quality and

crop yields;

• Hungary has a well-structured and logistically planned transportation infrastructure,

with one of the most developed highway network system in the EU;

• Approximately 220 R&D centers are working in the various fields of agriculture,

employing approximately 2,000 researchers and scientists;

PROMISING GLOBAL AND EUROPEAN UNION TRENDS

According to current United Nations (UN) forecasts world population is expected to grow

to 8.3 billion by 2030 and to 9.7 billion by 2050. To provide the optimum nourishment

and healthy living to people, the agriculture and food industry is facing great challenges.

Increasing output, maximizing value added services, improving logistic systems are capital

intensive activities that can also provide substantial returns to investors.

A well-working global marketplace and distribution network of agricultural products are

emerging, where competitive advantage favors countries with established and organized

agriculture sector. Shrinking supply and increasing demand will inevitably generate a

greater inherited value for each hectare arable land. To feed almost 10 billion people,

the current agricultural and food production output have to be increased by at least 70%

compared to its current values.

Agriculture is a dominant industry within the EU that employs 48 million people (together

with food processing, food retail and food services). Total agricultural production reached

410 billion euros in 2015 (decreased by 2.00% compared to 2014).

Hungary, due to its excellent geographical location and well-established agribusiness, has

all the opportunity to become a winner of these external market conditions.

2014 2015

Cereals (including seeds) 2 328 2 055

Industrial crops 903 971

Forage plants 177 185

Vegetables and horticultural products 630 705

Potatoes (including seeds) 115 79

Fruits 348 420

Total crop output (I) 4 620 4 559

Animals 1 758 1 948

Animal products 867 779

Total animal output (II) 2 625 2 728

Total agricultural output (I+II) 7 772 7 836

Total intermediate consumption 4 634 4 695

Gross value added 3 138 3 141

Factor income 3 806 3 660

Net entrepreneurial income 2 458 2 251

SOME IMPRESSIVE FIGURES ABOUT THE

HUNGARIAN AGRO SECTOR

Agricultural production of key sectors

Figures are in million EUR

Hungarian Central Statistical Office (2015): Statistical Yearbook of Agriculture

EXPORT/IMPORT IN 2014 & 2015

2014 2015

Export Import Export Import

Total volume in million EUR 7 796 4 666 7 614 4 806

Source: HCSO (2015): Statistical Yearbook of Hungary

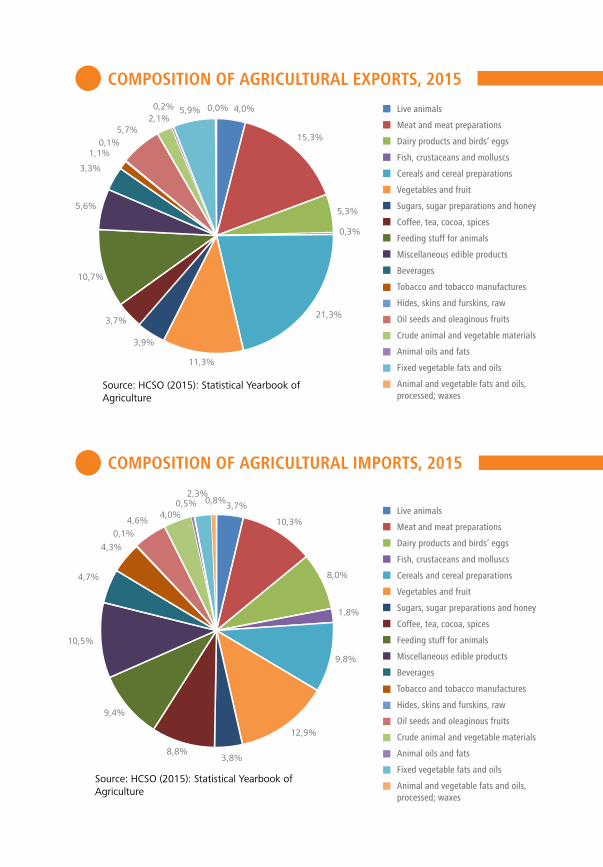

COMPOSITION OF AGRICULTURAL EXPORTS, 2015

COMPOSITION OF AGRICULTURAL IMPORTS, 2015

Live animals

Meat and meat preparations

Dairy products and birds’ eggs

Fish, crustaceans and molluscs

Cereals and cereal preparations

Vegetables and fruit

Sugars, sugar preparations and honey

Coffee, tea, cocoa, spices

Feeding stuff for animals

Miscellaneous edible products

Beverages

Tobacco and tobacco manufactures

Hides, skins and furskins, raw

Oil seeds and oleaginous fruits

Crude animal and vegetable materials

Animal oils and fats

Fixed vegetable fats and oils

Animal and vegetable fats and oils,

processed; waxes

0,0%

0,8%

Source: HCSO (2015): Statistical Yearbook of

Agriculture

4,0%

15,3%

5,3%

21,3%

11,3%

3,9%

3,7%

10,7%

5,6%

3,3%

1,1%0,1%

5,7%

2,1%

0,2% 5,9%

0,3%

Source: HCSO (2015): Statistical Yearbook of

Agriculture

Live animals

Meat and meat preparations

Dairy products and birds’ eggs

Fish, crustaceans and molluscs

Cereals and cereal preparations

Vegetables and fruit

Sugars, sugar preparations and honey

Coffee, tea, cocoa, spices

Feeding stuff for animals

Miscellaneous edible products

Beverages

Tobacco and tobacco manufactures

Hides, skins and furskins, raw

Oil seeds and oleaginous fruits

Crude animal and vegetable materials

Animal oils and fats

Fixed vegetable fats and oils

Animal and vegetable fats and oils,

processed; waxes

3,7%

10,3%

8,0%

1,8%

9,8%

12,9%

3,8%8,8%

9,4%

10,5%

4,7%

4,3%

4,6%

0,1%

4,0%

0,5%2,3%

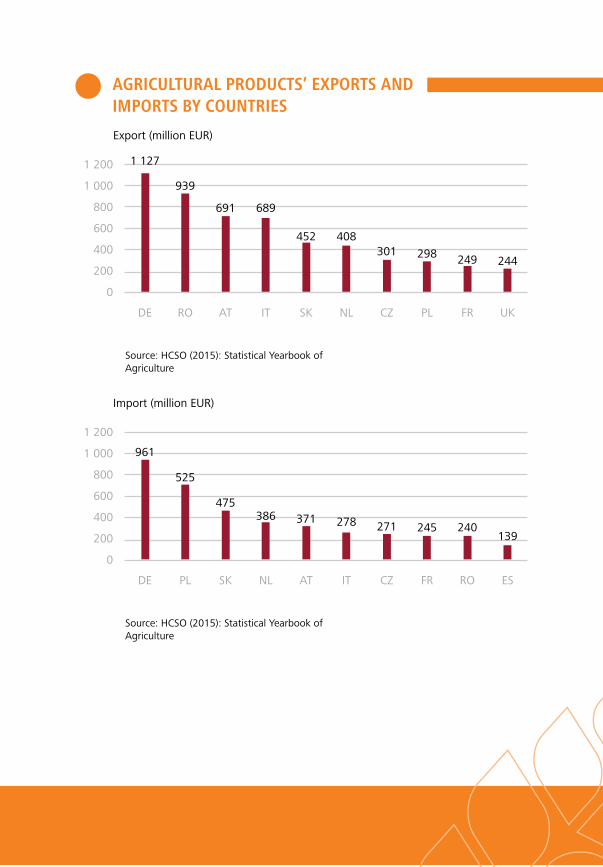

AGRICULTURAL PRODUCTS’ EXPORTS AND

IMPORTS BY COUNTRIES

1 200

1 000

800

600

400

200

0

Export (million EUR)

DE RO AT IT SK NL CZ PL FR UK

Source: HCSO (2015): Statistical Yearbook of

Agriculture

1 127

939

691 689

452 408

301 298249 244

1 200

1 000

800

600

400

200

0

Import (million EUR)

DE PL SK NL AT IT CZ FR RO ES

Source: HCSO (2015): Statistical Yearbook of

Agriculture

961

525

475386 371 278 271 245 240

139

OPPORTUNITIES IN THE HUNGARIAN AGRIBUSINESS

GEOLOCATIONHungary is located in Central and Eastern Europe and has a population of 9.9 million

people. Hungary is the member of the OECD, the NATO and the EU. Due to its strategic

location with an easy access to both EU and non-EU markets, foreign investors have long

been investing into the Hungarian economy. The cumulative stock of FDI since 2000 is

close to 80 billion USD.

The country’s agricultural and food industry is strongly integrated into the European

markets, giving opportunities for non-EU based companies to reach a huge market of

almost 500 million EU citizens. The Russian, Balkan and Eastern European markets are also

within a close reach. The two most important export countries are Germany and Romania,

however Slovakia, Austria, the Netherlands, Italy and Poland are also considerable

importers of Hungarian agricultural and food industry products. Hungary is maintaining

foreign trade relationships with more than 160 countries.

INFRASTRUCTURE

The food industry is not yet exploiting its full growth potential with regard to the production

and the export of high quality semi-finished and finished products. Despite the excellent

soil conditions, irrigation, and crop yields Hungary is not yet taking advantage of its natural

resources and agricultural opportunities.

Total arable land in Hungary is 7.4 million hectares. Agricultural production accounts for

57% and forestry for 21% of land usage. As almost 2/3 of the total available land space is

under farming activities, the opportunities in R&D activities and the adoption of global best

practices provide a lucrative business opportunity for new entrants.

Hungary has a well-structured and logistically planned transportation infrastructure, with

one of the most developed highway network systems in the EU. Among the various

transportation options, rail is the most dominant. It carries more than 20% of total

freight, which is well above the EU average. Hungary also has an intensive logistic center

offering: 195 industrial parks can be accessed countrywide. Logistics is a growing sector

contributing with 6.25% to the country’s GDP (2015).

WATER RESOURCESHungary is world famous for its abundant resources of drinking, thermal, mineral and

ground waters. Combined with the country’s excellent geolocation this provides a unique

and remarkable opportunity for various business purposes. Hungary has built a long lasting

tradition in thermal bathing and recreational tourism. Héviz is a Europe famous bathing

city attracting hundreds of thousands tourists each year. Thermal water is also a great

renewable energy source for the green economy.

Land irrigation is available throughout the country, as groundwater can be exploited with

minimal costs. This is especially important as the global water crisis is already causing

growing tensions worldwide. According to the World Health Organization (WHO) 1.1

billion people have no access to any type of improved drinking source of water.

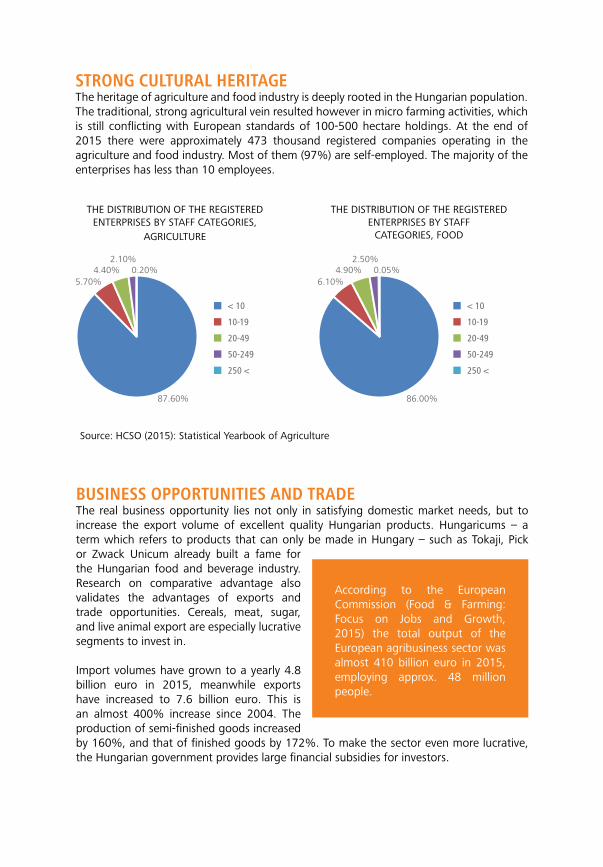

STRONG CULTURAL HERITAGE The heritage of agriculture and food industry is deeply rooted in the Hungarian population.

The traditional, strong agricultural vein resulted however in micro farming activities, which

is still conflicting with European standards of 100-500 hectare holdings. At the end of

2015 there were approximately 473 thousand registered companies operating in the

agriculture and food industry. Most of them (97%) are self-employed. The majority of the

enterprises has less than 10 employees.

< 10

10-19

20-49

50-249

250 <

< 10

10-19

20-49

50-249

250 <

Source: HCSO (2015): Statistical Yearbook of Agriculture

THE DISTRIBUTION OF THE REGISTERED

ENTERPRISES BY STAFF CATEGORIES,

AGRICULTURE

87.60%

5.70%

4.40%2.10%

0.20%

6.10%

4.90%2.50%

0.05%

86.00%

THE DISTRIBUTION OF THE REGISTERED

ENTERPRISES BY STAFF

CATEGORIES, FOOD

BUSINESS OPPORTUNITIES AND TRADEThe real business opportunity lies not only in satisfying domestic market needs, but to

increase the export volume of excellent quality Hungarian products. Hungaricums – a

term which refers to products that can only be made in Hungary – such as Tokaji, Pick

or Zwack Unicum already built a fame for

the Hungarian food and beverage industry.

Research on comparative advantage also

validates the advantages of exports and

trade opportunities. Cereals, meat, sugar,

and live animal export are especially lucrative

segments to invest in.

Import volumes have grown to a yearly 4.8

billion euro in 2015, meanwhile exports

have increased to 7.6 billion euro. This is

an almost 400% increase since 2004. The

production of semi-finished goods increased

by 160%, and that of finished goods by 172%. To make the sector even more lucrative,

the Hungarian government provides large financial subsidies for investors.

According to the European

Commission (Food & Farming:

Focus on Jobs and Growth,

2015) the total output of the

European agribusiness sector was

almost 410 billion euro in 2015,

employing approx. 48 million

people.

The Hungarian EU accession in 2004 had a great impact on the agricultural and food

industry however it could not dramatically change the existing and obsoleted market

structure. Hungary is still highly dependent on raw material export and the high value

added sectors couldn’t expand fast enough. The sector’s total share in the Hungarian GDP

in 2014 was 4.50%.

Due to recently launched reorganizing programs and investment projects, the Hungarian

food production is expected to increase by 20% in the next four years. Domestic demand

is also expected to grow by 20%. This is further supported by the fact that 13 billion euro

worth of EU co-financed projects will be implemented by 2020 in the sector.

The construction of the largest slaughterhouse of Hungary in Mohács (there is only one

comparable in the country owned by Hungary Meat Ltd.) has been launched in 2015 and

will be finished in 2016 with an annual processing capacity of 1 million pigs. An integration

network has been established to foster the sufficient demand for the processed meat.

M&A ACTIVITIES The agriculture and food industry has long been a frequented target of foreign investors.

Global companies such as Danone, Coca-Cola, Nestlé, Heineken and Unilever, to name a

few, have all invested to establish a presence in the Hungarian market. These multinational

companies fueled the growth of not only their local supply chain but the culture and

infrastructure of growing local companies as well.

Lucrative investment opportunities in the sector resulted in significant M&A transactions

in the recent years. Szentkirályi, the leading mineral water and soft drink producer was

acquired by the Czech Karlovánské Minerální Vody. Szentkirályi had been previously

awarded with the golden medal at the prominent Aqua-Eauscar competition in 2004,

showing that the Hungarian companies can successfully compete even in the global

mineral water segment.

Another success story of 2015 is the acquisition of Fornetti, the Hungarian based regional

frozen bakery product company. Fornetti was acquired by a Swiss company, Aryzta, the

global leader in frozen bakery products with the intent to further increase production

capacity and to exploit the growing potential in the CEE region.

BANKING AND FINANCEBanking plays a crucial role in the health of the economy by providing the necessary

finances that stimulate growth. As the returns on agricultural investments are becoming

more dominant, lending activities also increased significantly. One of the major Hungarian

banks is already investing about 10% of its portfolio into the sector, and there is a growing

interest from other major financial institutions as well.

FOREIGN LAND PURCHASES IN HUNGARYThe purchase of agricultural land by foreign citizens and other legal entities is regulated by

Law No. 122 of 2013 on transfer of agricultural lands and lands of forestry (there are also

some other transitional rules).

As a general rule land might be purchased by any natural person (from Hungary or from any

other county within the EU) or legal person, or any association not having legal personality.

Domestic natural persons and EU citizens who can be regarded as “non-farmers” could

only purchase 1 hectare agricultural land. Legal entities considered as “farmers” could

purchase agricultural lands up to 300 hectares. The maximum land that could be rented is

up to 1,200 hectares. In case of livestock enterprises the maximum size of the area cannot

be more than 1,800 hectares.

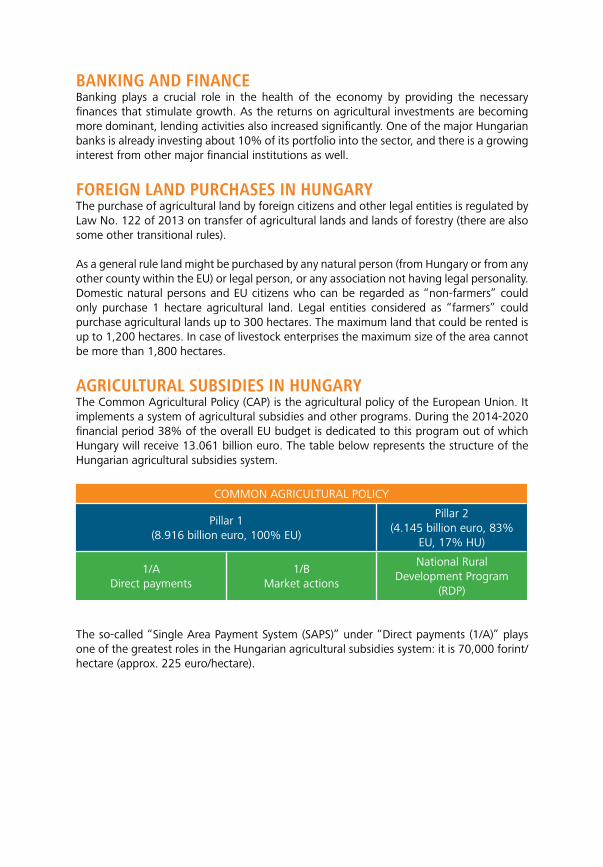

AGRICULTURAL SUBSIDIES IN HUNGARYThe Common Agricultural Policy (CAP) is the agricultural policy of the European Union. It

implements a system of agricultural subsidies and other programs. During the 2014-2020

financial period 38% of the overall EU budget is dedicated to this program out of which

Hungary will receive 13.061 billion euro. The table below represents the structure of the

Hungarian agricultural subsidies system.

COMMON AGRICULTURAL POLICY

Pillar 1

(8.916 billion euro, 100% EU)

Pillar 2

(4.145 billion euro, 83%

EU, 17% HU)

1/A

Direct payments

1/B

Market actions

National Rural

Development Program

(RDP)

The so-called “Single Area Payment System (SAPS)” under “Direct payments (1/A)” plays

one of the greatest roles in the Hungarian agricultural subsidies system: it is 70,000 forint/

hectare (approx. 225 euro/hectare).

AGRICULTURE AND SCIENCESince Prince Albert Casimir of Saxony, Duke of Teschen, established the Agricultural Higher

Educational Private Institution of Magyaróvár in 1818 (now University of West Hungary)

almost 40 agricultural science related institutions had been established in Hungary. The

diverse agriculture fields such as environmental protection, bioenergetics, and rural

development have become more inspiring to young researchers and aspiring professionals.

Approximately 221 R&D centers are working in the various fields of agriculture, employing

more than 2,009 researchers and scientists.

SUCCESS STORIES• There are plenty of famous and well-known Hungarian products.

• The term Hungaricum refers to a unique set of ultimate quality goods – mainly form

the food and beverage industry, which are under community protection law and are

world famous many of the times.

• These world famous, but not yet fully exploited products such as pálinka, Pick Salami,

Tokaji wine, Unicum, Túró Rudi and other agricultural products such as onion form

Makó and paprika are representing great potential for expanding into the global

markets.

• The unique history, craftsmanship and superior quality are lifting Hungaricums into

the group of world class products.

• The new wave of emerging local trendy restaurants and hotels use these agricultural

and food industry products to satisfy their clients’ needs.

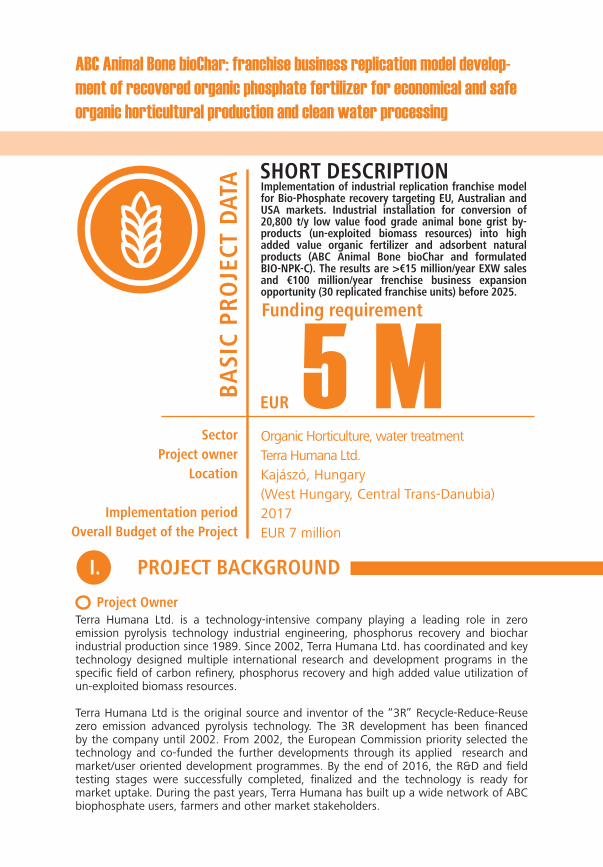

SHORT DESCRIPTION

Funding requirement

ABC Animal Bone bioChar: franchise business replication model develop-

ment of recovered organic phosphate fertilizer for economical and safe

organic horticultural production and clean water processing

Implementation of industrial replication franchise model for Bio-Phosphate recovery targeting EU, Australian and USA markets. Industrial installation for conversion of 20,800 t/y low value food grade animal bone grist by-products (un-exploited biomass resources) into high added value organic fertilizer and adsorbent natural products (ABC Animal Bone bioChar and formulated BIO-NPK-C). The results are >€15 million/year EXW sales and €100 million/year frenchise business expansion opportunity (30 replicated franchise units) before 2025.

EUR 5 MSector

Project owner

Location

Implementation period

Overall Budget of the Project

Organic Horticulture, water treatment

Terra Humana Ltd.

Kajászó, Hungary

(West Hungary, Central Trans-Danubia)

2017

EUR 7 million

BA

SIC

PR

OJE

CT

DA

TA

I. PROJECT BACKGROUND

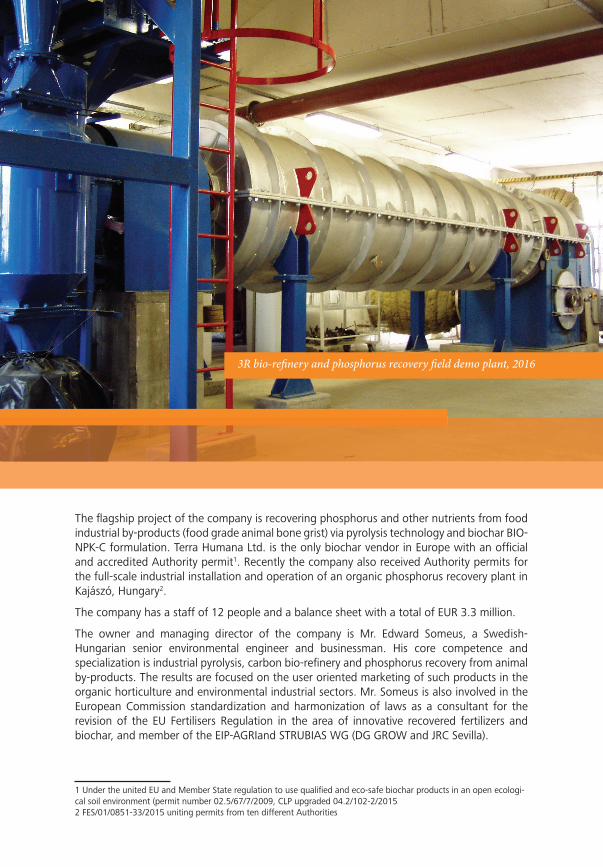

Project OwnerTerra Humana Ltd. is a technology-intensive company playing a leading role in zero emission pyrolysis technology industrial engineering, phosphorus recovery and biochar industrial production since 1989. Since 2002, Terra Humana Ltd. has coordinated and key technology designed multiple international research and development programs in the specifi c fi eld of carbon refi nery, phosphorus recovery and high added value utilization of un-exploited biomass resources.

Terra Humana Ltd is the original source and inventor of the “3R” Recycle-Reduce-Reuse zero emission advanced pyrolysis technology. The 3R development has been fi nanced by the company until 2002. From 2002, the European Commission priority selected the technology and co-funded the further developments through its applied research and market/user oriented development programmes. By the end of 2016, the R&D and fi eld testing stages were successfully completed, fi nalized and the technology is ready for market uptake. During the past years, Terra Humana has built up a wide network of ABC biophosphate users, farmers and other market stakeholders.

The fl agship project of the company is recovering phosphorus and other nutrients from food

industrial by-products (food grade animal bone grist) via pyrolysis technology and biochar BIO-

NPK-C formulation. Terra Humana Ltd. is the only biochar vendor in Europe with an offi cial

and accredited Authority permit1. Recently the company also received Authority permits for

the full-scale industrial installation and operation of an organic phosphorus recovery plant in

Kajászó, Hungary2.

The company has a staff of 12 people and a balance sheet with a total of EUR 3.3 million.

The owner and managing director of the company is Mr. Edward Someus, a Swedish-

Hungarian senior environmental engineer and businessman. His core competence and

specialization is industrial pyrolysis, carbon bio-refi nery and phosphorus recovery from animal

by-products. The results are focused on the user oriented marketing of such products in the

organic horticulture and environmental industrial sectors. Mr. Someus is also involved in the

European Commission standardization and harmonization of laws as a consultant for the

revision of the EU Fertilisers Regulation in the area of innovative recovered fertilizers and

biochar, and member of the EIP-AGRIand STRUBIAS WG (DG GROW and JRC Sevilla).

1 Under the united EU and Member State regulation to use qualifi ed and eco-safe biochar products in an open ecologi-

cal soil environment (permit number 02.5/67/7/2009, CLP upgraded 04.2/102-2/2015

2 FES/01/0851-33/2015 uniting permits from ten different Authorities

3R bio-re� nery and phosphorus recovery � eld demo plant, 2016

Technology

Terra Humana Ltd. has developed an innovative technology and commercialized industrial practice for phosphorus recovery from animal by-products and biochar manufacturing through a series of market oriented applied research and user oriented development projects. The demonstrated and operating complex technology includes:

• the ABC Anim”l Bone bioCh”r, ”n innov”tive ”nd recovered phosphorus fertilizer th”t is produced from food grade animal by-products in line with the EU bio nutrient circular phosphorus economy model,• the comprehensive ”nd high effi cient m”nuf”cturing process by 3R zero emission pyrolysis technology, • m”nuf”cturing, inst”ll”tion ”nd oper”tions of the 3R pyrolysis equipments ”nd infrastructure, • the comprehensive fi eld testing involving independent l”bor”tories ”nd n”tion”l authorities under EU regulations,• leg”l ev”lu”tions ”nd industri”l oper”tions/product ”pplic”tion Authority permits ”nd• economic”l pl”nning, m”rket investig”tion ”nd end-product m”rket upt”ke ev”lu”tion considered for market competitive conditions.

The current investment project aim is the implementation of an ABC processing plant hardware installation (full industrial replication franchise model) for preparation of the global market uptake of ABC biochar technology and products. Full value technology insurance will be available.

Animal Bone bioChar (ABC) is a recovered organic phosphorus fertiliser produced from food grade, category 3 animal bones up to 850°C reductive thermal processing and negative pressure conditions with advanced zero emission environmental performance (3R technology).

ABC has a 92% calcium-phosphate (30% P2O

5) which makes it a signifi cant phosphorus

resource, therefore being a signifi cant alternative to the currently used, but Cadmium/Uranium heavy metal contaminated, mineral phosphate fertilizers. The ABC benefi ts for farmer users are the economical and effi cient applications of this natural product as organic and low-input fertilizer in the horticultural sector (fruit and vegetables); improving soil quality in physical, chemical and biological terms, such as strengthening the bio-activity of the soil; restoration of the natural soil balance, and increasing its drought tolerance and productivity.

II. PROJECT DESCRIPTION

The main agricultural and environmental importance of the ABC is the high effi cient

application and economical benefi ts for organic farming sector users and that it does

not contains heavy metal contamination, toxic elements even according to the strictest

requirements of organic agriculture. (Traditional mineral source phosphate fertilizers

contain cadmium and uranium as inevitable by-products of the production technology).

ABC biochar is manufactured from food quality animal bones and renewable biomass

resources, and is the by-product of the food industry available in large quantities.

In the EU, approximately 21 million tonnes of slaughter by-products are produced by the

meat industry every year, including several million tonnes of food grade bones, which is

far more suffi cient to manufacture the targeted 30 franchise replication projects in the EU,

implemented before 2025. The goal is the production of 375,000 t/y ABC before 2025 in

the main target markets of Italy, Germany, France, Spain and Poland. This is important to

highlight, that ABC processing requires high-end specialized technology for which Terra

Humana Ltd. is the sole and core specialized vendor and complex knowledge center in the

EU and on a global level as well.

The 3R pyrolysis fi eld demonstration equipment with 2000 t/year throughput capacity

is currently in operation in Polgardi, Hungary (Fejer country) since 2004, with focus on

market/user fi eld demonstration, training and applied RTD. For industrial scale production

20,800 t/y throughput (12,500 t/y output ABC product and bio-oil) capacity franchise

replication model pyrolysis plant will be installed in Kajászo Biofarm Manor, Hungary (Fejer

country).

The quality and safety of the ABC produced at the 3R fi eld demonstration plant was

investigated by an independent and accredited laboratory, WESSLING Hungary Ltd., based

on both the European and Member State legislation. The measurements confi rmed that

the biochar produced by the technology of Terra Humana Ltd. is a

• specifi c high end product with specifi c high qu”lity;

• meets ”ll the EU, US ”nd Austr”li”n industri”l, environment”l ”nd s”fety requirements;

• its ”gronomic effi ciency is high;

• he”vy met”l ”nd toxic elements free;

• meets ”ll the requirements for higher st”nd”rds of org”nic ”gricultur”l ”pplic”tions in

the EU, US and Australia; furthermore

• the imp”ct ”ssessment confi rmed the positive high ”dded v”lue imp”cts of the ABC

products on crop yield, quality and food safety.

The ABC is a natural product with high agronomic and economic application effi ciency,

while signifi cantly improving the food and environmental safety/security as well.

Property rights

Edward Someus, owner of Terra Humana Ltd., solely owns all the necessary intellectual

property rights to all the key elements of the ABC biochar manufacturing technology and

its products, most importatly development results, know how and confi dential industrial

design. The technology exploitation objective is to enter the global market through

franchise replication model as a bio-phosphate manufacturer and also as a technology

provider for licensed/franchised partner.

The 2017 Business Opportunity

High nutrient dense Phosphorus products in economical industrial scale and applicability is

available only from two sources: from phosphate mines in mineral form and from animal

bones. Currently, the agricultural sector mainly uses mineral forms for fertilization. However

phosphate fertilizers delivered from mined rock phosphate cause signifi cant problems

for the sector. While rock phosphate raw material can contain high levels of cadmium

and uranium; the European Union is poor in phosphate reserves and imports ~ 95% of

phosphate fertilizers from outside the European Union (from Morocco, Tunisia and Russia).

This makes phosphate a listed (one of twenty) critical raw materials for the EU. In many

cases only approx. 30% of the dissolved phosphorus is utilized by the plants, while this

ratio in the case of controlled release ABC natural substance more closely approximates

full value.

The Terra Humana Ltd. 2017 business opportunity consists of four integrated elements

which are together present in the right time and EU location, including:

a) The need: a strong and rapidly growing EU market demand for pure organic phosphorus

and BIO-NPK-C in the organic horticultural sector and water treatment adsorbent industry.

b) The means to fulfi l the need: the implementation in 2017 of a production franchise model

that will serve as replication model for 30 additional systems to be installed in several

EU countries before 2025,

c) The method to apply the means to fulfi l the need: coherently integrated EU,

Australian and US marketing and sales distribution networking of ABC products and

technology,

d) The benefi t method: franchise technology and sale of ABC products.

Beyond the offered business opportunity in 2017 the ten year-period business opportunity

in the EU includes the production of 375,000 tons of pure ABC per year before 2025

via 2030 installed plants, yet still involves approx. 5% substitution potential substitution

potential only for imported mineral P fertilizers. In the upcoming years, international ABC

business opportunities are planned in the USA and Australia as well.

Up until the innovative technology of Terra Humana Ltd., there was no any effi cient and

modern phosphorus recovery technology to produce high quality, natural and high nutrient

dense innovative phoshorus fertilizer which adhere to the new, strict regulations of the

EU. The solution enables to offer recovered organic phosphate and BIO-NPK-C fertilizer

to the agricultural sector at a reasonable price. The global phosphate fertilizer demand

is expected to grow until 2018 from 41.7 million nutrition tons (P2O5 content) to 46.6

million tons, which results in a global annual market size of approx. EUR 7.2 billion. The

European market is estimated to be 8% of the global market. In 2008 the phosphate

fertilizer prices increased 700% and due to the phosphorus critical raw material status

since 2014 additional similar mega dimension price increase predicted on the market in

2018-2020.

Terra Humana Ltd. plans to enter the global market with its breakthrough technology

and offer an innovative recovered organic phosphorus fertilizer as an alternative of the

currently used mineral phosphate fertilizers. The organic horticultural and low-input

agricultural sectors are signifi cant and rapidly growing open markets , in average over 10%

market increase/year in the EU, in which market scenarion the ABC/BIO-NPK-C is a strategic

innovation fertilizer according to the new EU regulations enter in force 2018-2020.

The project is for the implementation of an ABC processing plant hardware installation

(industrial replication franchise model) in Hungary, Kajászó.

• Ye”r 1: infr”structur”l investments ”nd inst”ll”tion of the fr”nchise replic”tion model pl”nt.

• Ye”r 2: b”sic c”p”city production. Throughput c”p”city: 6,600 t/y ”nim”l bone. Output

production: 4,000 t/y ABC biochar.

• From ye”r 3 onw”rds: full c”p”city production. Nomin”l throughput c”p”city: 20,800 t/y (or

2.6 t/h) food grade animal bone grist. Output production: 12,500 t/y ABC biochar.

WHY INVEST?

• Breakthrough and strategic original solution technology and product system with

professional management, that is placed on the critical raw material market in the EU and

globally as well.

• Rapidly and strongly developing market opportunity in the EU, Australia and USA where

the ABC is in strategic technical, business and market position for long term under any

horticultural market competitive conditions.

• The rapidly changing legal environment in the EU, USA, Australia and Japan requires

changes in technology and products, while encourages the production and market uptake

of the innovative and recovered Phosphorus fertilizer at competitive market costs.

• Providing effi cient, economical and safe product solution for the signifi cant, increasing

and predictable national, European and global markets with high food safety demands at

an affordable cost for the enduser.

• IRR 20% and three years fast payback period.

• The new 3R Phosphorus recovery francise system , opening wide range of new technical,

economical, business and environmental opportunities for all stakeholders in the organic

horticulture fruit/vegetable production and water processing sectors.

2017 2018 2019 2020 2021

Investment (EUR 1,000) 4000 0 0 0 0

Operating costs (EUR

1,000)0 700 2200 2200 2200

Sales quantity (tons) -0 4000 12500 12500 12500

Revenue (EUR 1,000) EXW 0 5000 15625 15625 15625

EBIT (EUR 1,000) -4000 4300 13425 13425 13425

Mineral P useWater use

Time to harvest

Crop yield

& qualityRevenues

Expenses

III. FINANCIAL INDICATORS

Profi tabilityEmployment

Subsides

Impact on

Enviroment/

human health/

use of resources

Impact of food

safety / quality

Improved food

production

safety / security

ABC Impact on AGRICULTURE

Market

replication

ABC market

Take-up

Revenues

Production

cost

Involvements of EU-wide stakeholders, users, customers

Profi tability,

competitiveness

Innovation

Creation of

qualifi ed job

Economical

relevance

ABC Impact on INDUSTRY

AB

C C

ON

TRIB

UTE

S TO

SEV

ERA

L P

OLI

CIE

S

ABC

Unique

Selling

Points

Organic

food

production1 year

ROI for

farmers

Stable &

low price

Meet allstrick

EU/MSregulation

Recovered

P & Ca

30% P2O

5

40% CaO

+ 10-30%

yieldsBiogen origin noharmfulcontami-nation

Quantitative and qualitative indicators

QUANTITATIVE INDICATORS

Mid-term revenues / year expectation EUR 15,6 million

Mid-term market penetration expected (%) 0.1%

IV. INVESTMENT OFFER

Required investment 2017/2018 EUR 5 million

Form of investment Equity investment

Proposed capital/equity structure Minority share

CONTACT DETAILSMR. EDWARD SOMEUS (BIOCHAR S&T SENIOR ENGINEER)

Tel: +36 20 805 4727 Skype: edwardsomeus

E-mail:[email protected]

http://www.3Ragrocarbon.com

Investment schedule

CAPEX: 2017 - plant and technology hardware installation: EUR 4,000,000

(including full value technology insurance)

OPEX: 2018 year one operations costs: EUR 1,000,000

Proposed exit strategy

Trade sale for a strategic investor. Exit after approx. 3-4 years. Terms and conditions to be

flexibly discussed.

Amount to be raised: €5,000,000 (CAPEX €4M, OPEX year 1 €1M). IRR = 20%, pay back =

3 years, full value technology insuranced. Franchise industrial replication model locations

at two sites in West Hungary, located in the center of logistical hubs = (1) 20,800 t/y

throughput capacity commercial production (new installation 2017/2018) and (2) at close

location industrial training/education site for franchise partners (already completed and

operating). EU/MS Authority permits = valid, already available.

SHORT DESCRIPTION

Funding requirement

APICON Zrt.

Capitalization

APICON Zrt. – Company founder Béla Dömöcsök began performing experimental development aiming at the research and development of an apiary and professional bee pollinating technology based on PTC patents eight years ago. The company needs a second capitalization in order to fi nish the test production (prototype), to start serial production, to establish its own production capacity and to accelerate it’s sales activity.

EUR 2.9M Sector

Project owner

Location

Implementation period

Overall Budget of the Project

Agriculture

APICON Zrt. majority shareholder: Béla Dömöcsök (CEO)

Biatorbágy

1 year

2,9001

BA

SIC

PR

OJE

CT

DAT

A

1HUF 310 to the EUR

I. PROJECT BACKGROUND

Short project background

A global pollination crisis has emerged in modern mono-cultural agriculture recently.

Humanity’s provisioning, the crop yields of cross-fertilized fl owered forage and industrial

plants grown in large areas of the world, is very much dependent on the success of the

ecosystem’s pollination service and fertilization. Their acreage has tripled over the past

fi fty years, while as a result of negative environmental impact (climate change, mono-

cultural landscapes and the intensive use of chemicals) wild pollinators have dangerously

diminished. Their guided replacement would only be possible by domesticated honey bees

if apiaries throughout the world did not have to fi ght against aggressive parasites and

incurable bee diseases and the dramatic reduction in the biological activity of colonies.

In modern, up-to-date agriculture it has become necessary to use an industrialized,

intensive bee pollinating technology resulting in the better utilization of genetic yield

potentials, improved crop productivity, safe and reliable availability, reproducibility and the

ability to be integrated into yield technologies.

The apicon™ technology is a breakthrough, a unique, revolutionary apicultural solution,

a PTC patent-protected complex know-how and an all-around technology to optimally

complement the pollination service of the ecosystem’s wild habitat pollinators or, failing

these, an industrialized, guided replacement of pollinators. The technology provides an

effective – preventive and chemical-free – treatment of varroosis and nosemosis (Varroa

destructor and Nosema spp. are the most dangerous parasites). The unique IT-supported

diagnostic solution for beekeeping and environmental issues allows the profi table

apicultural and pollination-service-aimed exploitation of domestic honey bee colonies

unviable without human assistance, reducing the business-related risks of beekeeping,

mechanization, automation and profi table production of premium quality apicultural

products.

WHY INVEST?

• seller’smarket:15%ofhumanfoodon average depends on the services of honey bees and wild pollinators; the production quality andtheplantyieldcanbeimprovedby20%to 70%bycontrolledpollination;

• uniqueness:onabillionaireseller’smarket a real value creation on the client side, with a patent-protected product;

• incrediblegrowthpotential:70.62%Internal Rate of Return

• innovativecapacity:patent-protected,unique pollination/apiary technology with a number of related, defendable business opportunities;

• knowledge-sharingecosystem:patent- protected solutions to facilitate the understanding and rapid promotion of the technology on a large-scale – apiculture academies, franchise demonstration units, interactive IT solutions and conferences.

• internationallymarketableproductsand services tailored to the needs of the local market, facilitating productivity, efficiency and profitability. Flexible production (modular and mobile systems), international technology transfer and cooperation in research and development;

• opportunityforbroadeningtherangeof the activities for many years to come (apiary equipment - pollination service franchise - queen breeding - apiary product integrator);

• complexbusinessstrategyaimedatthe exploitation of innovations serving agriculture and other industries (food, pharmaceutical and cosmetics industry) and supporting the protection of the environment and food security by the global novelty of an apicultural product as well as the franchise system to operate it;

II. PROJECT DESCRIPTION

General background of the management

The founder and majority shareholder of the company is a professional aviation engineer.

He has been engaged in beekeeping for eight years, researching and developing the

apicon™ technology.

Acryltechnika Ltd. is Béla Dömöcsök’s family-owned company, founded in 1991, which

is active in manufacturing and selling special built-in sanitary equipment for modular

containers of mobile offices and mobile homes.

The management and the owners are professionals holding degrees in engineering,

finance, IT, marketing and law, and with a long-term commitment to succeed with the

technology.

The PCT patent-protected technological unit is a bee container consisting of a number of

(two, four or eight) special bee hives and service facilities. It is operated and controlled by

an IT system (both hardware and software), which monitors and evaluates environmental

parameters relating to the device and the environment.

The project is aimed at building a production plant for the prototype, a result of the

experimental development. The containers for manufacturing of the apiary production

units are being manufactured by a strategic partner in a predetermined quantity, but

the key units of the product – bee hives, service facilities and IT background – are being

achieved in the project by the owners.

The production capacity is being set up according to the project schedule by 2017. A

foreign partner has already reserved the first production year of the factory.

Competitive advantages

There are about 200,000 to 300,000 pollinator species in the ecosystem, but human-

controlled pollination is only possible by domesticated honey bees. Ongoing for decades,

apicultural research, however, didn’t fi nd either chemical or genetic solutions to apicultural

problems such as incurable bee diseases, aggressive and resistant parasites, extremely

decreased biological activity, the genetic deterioration of bee colonies, and the continued

loss and disappearance of honey bee colonies in winter and increasingly also in summer.

The USA (about USD 1 billion) and Canada represent the biggest markets for pollination

services by a conventional technology. Insuffi cient pollination has led in the USA to a

signifi cant loss of agricultural production, estimated at USD 10 to 20 billion/year. Current

devices work on the basis of a 100 to 160-year old technology. The frequent and excessive

use of chemicals and signifi cant chemical overload on the bee’s living environment

together carry a signifi cant risk to the safety of food regarding honey. APICON can make

an effi cient entry into this market with its patented and professional solutions, which can

result in monopoly rights as well.

Property rights, licences and certifi cations

APICON Zrt. owns a number of patents without any restriction on area or time:

• PROCESS FOR PREVENTING VARROA MITE REPRODUCTION IN HIVE PROVIDED WITH

ROTATABLE NEST (P1400452/6) NSZO: A01K 47/00, A01K 47/02, A01K 49/00;

• BIODYNAMIC NEST-STRUCTURE FOR APIARIAN HIVES WITH IMPROVED FEATURES

(P1400384/8) NSZO: A01K 47/02, A01K 47/00, A01K 47/06;

• HONEYCOMB CONNECTION FOR HIVES WITH IMPROVED FEATURES (P1300692/10)

NSZO: A01K 47/06, A01K 47/00, A01K 47/02;

• GRATE RINGED NEST FRAME FOR CYLINDRICAL CENTER HIVE (P1300691/10) NSZO:

A01K 47/06, A01K 47/00, A01K 47/02;

• CONTAINER UNIT WITH AIR MOISTURE CHANGING MEANS (P1500004) NSZO: F24F

6/00, A23B 7/02;

• Controlled line breeding of high quality queens (prepared for submission).

Current position in the market – expected share

Specifi cation of the product suitable for series production and its engineering and fi nancial

validation are currently being carried out. The fi rst series-produced products are expected

to appear on the market by 2017.

Key strategic partners

We have launched a strategic partnership with an IT company (in favour of developing the necessary SW and HW technology), furthermore, we have set up a strategic partnership with a container manufacturing company.

Access to foreign markets, export markets, description of key risks and measures to prevent risks

The most signifi cant markets for the product are the USA, Canada, the EU, the Russian

Federation, Ukraine, Central Asia, Australia and New Zealand. Protectionism in the US

markets is to be neutralized by establishing a local production facility (a franchise network

of producers and distributors). The rigid apicultural system of the European market can be

broken by an automated production system available even for small-scale beekeepers, and

the relationship-based Central Asian market can be entered by joint ventures or a franchise

system.

Short market description, main competitors

Current outdated technologies cannot maintain an enhanced beehive hygiene, effectively

protect and support bee colonies and enable an intense operation necessary for productivity.

Scientists have given up on a chemical solution in an attempt to fi nd a treatment, while

genetic research has not been successful so far.

Only the global utilization of the bionic apicon™ technology – imitating natural

mechanisms, creating a similar environment, consistently applying organisational principles

and processes – can attain a breakthrough.

Target groups

The target groups are the following:

• Seed growers • Pollination service providers

• Agricultural integrators • Professional apiaries

• Agricultural producers • Recreational beekeepers

III. FINANCIAL INDICATORS

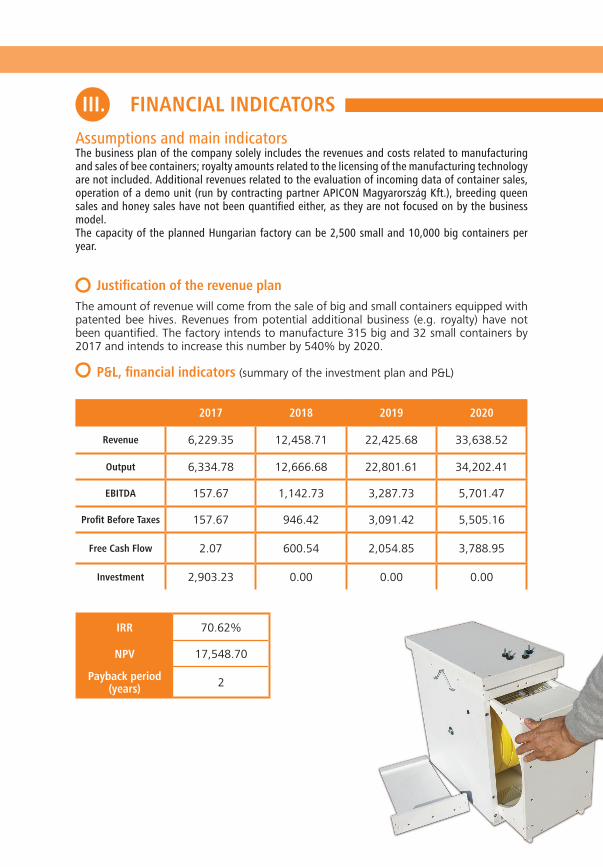

Assumptions and main indicatorsThe business plan of the company solely includes the revenues and costs related to manufacturing and sales of bee containers; royalty amounts related to the licensing of the manufacturing technology are not included. Additional revenues related to the evaluation of incoming data of container sales, operation of a demo unit (run by contracting partner APICON Magyarország Kft.), breeding queen sales and honey sales have not been quantifi ed either, as they are not focused on by the business model.The capacity of the planned Hungarian factory can be 2,500 small and 10,000 big containers per year.

Justifi cation of the revenue plan

The amount of revenue will come from the sale of big and small containers equipped with patented bee hives. Revenues from potential additional business (e.g. royalty) have not been quantifi ed. The factory intends to manufacture 315 big and 32 small containers by 2017 and intends to increase this number by 540% by 2020.

P&L, fi nancial indicators (summary of the investment plan and P&L)

2017 2018 2019 2020

Revenue 6,229.35 12,458.71 22,425.68 33,638.52

Output 6,334.78 12,666.68 22,801.61 34,202.41

EBITDA 157.67 1,142.73 3,287.73 5,701.47

Profi t Before Taxes 157.67 946.42 3,091.42 5,505.16

Free Cash Flow 2.07 600.54 2,054.85 3,788.95

Investment 2,903.23 0.00 0.00 0.00

IRR 70.62%

NPV 17,548.70

Payback period (years) 2

IV. INVESTMENT OFFER

Required amount of investment (EURm) 2.9

Form of investment 10-30% share ownership

Proposed capital/equity structure

Ten per cent of the project company’s shares can be acquired in exchange for an

investment of EUR 2.9 million necessary for the project. Thirty per cent of the project

company’s share is also available in proportional price. Béla Dömöcsök will remain the

main shareholder of the company, the project leader and the owner of the main patents.

Investment schedule

The company needs capitalization by 2017 in order to perform the reserved production

and to establish its own production capacity. In the following years, the business model

will generate benefits in line with the projected revenue, foreseeing a two-year payback

period.

Proposed exit policy

In the long term, an IPO presents an exit opportunity.

Quantitative and Qualitative Indicators

QUANTITATIVE INDICATORS

Revenue/year 2017 (EUR ‘000) 6,229

Expected mid-term revenue/year (EUR ‘000) 13,705

Expectedmid-termmarketpenetration(%) Not relevant

Available shareholder’s resources/available funds (EUR ‘000) Reinvesting

C O N TACT D E TA I L S

BÉLA DÖMÖCSÖK+36(30)9348923

www.apicon.org

SHORT DESCRIPTION

Funding requirement

Lamb, sheep and goat

meat pr ocessing f act or y

The SHEEP-PROJECT aims to set up a complex slaughterhouse and processing plant with the related supply chain. The slaughterhouse will be suitable to slaughter and process animals of organic classifi cation, apply processes complying with EU requirements and also religious (e.g. Halal) stipulations. Following implementation, the predicted annual production output is 200,000 pieces of slaughtered animals per shift.

Professional and / or fi nancial investors can be included in the business.

EUR 1.8 M Sector

Project owner

Location

Implementation period

Overall Budget of the Project

Agriculture, Food-industry

SHEEP-PROJECT Ltd.

Hungary, Bács-Kiskun county and the surrounding Pest and Fejér counties

8 months

EUR 4 million

BA

SIC

PR

OJE

CT

DAT

A

I. PROJECT BACKGROUND

Short background

The project company, SHEEP-PROJECT Ltd. was established in 2015 by recognized experts of the Hungarian lamb, sheep and goat sector. The founders intend to make the company a dominant player that acts in the sector’s interest. As an EU based company, it would like to benefi t from the available EU and national funds and grants.

General background of the management

The management of the SHEEP-PROJECT Ltd. consists of three members who are among the most knowledgeable and experienced people in the lamb and sheep business (market, feeding, slaughtering and sales) in Hungary. The management also actively participates and regularly organizes professional events.

• László MAJOR, Managing Director has several years of experience as director of a slaughterhouse. He has managed his own farm for 12 years and currently has a fl ock of 700 sheep.

• Miklós FÜLÖP, Finance Manager is a professional advisor for the food and agricultural industry in the fi eld of business development and accounting.

• László DOBOS, Brand Manager has experience in managing large livestock farms with several thousand ewes.

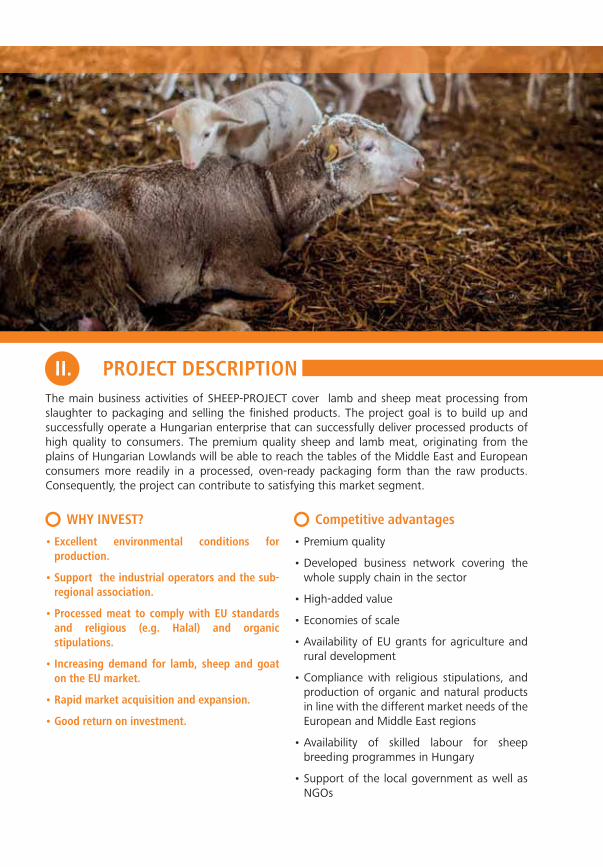

The main business activities of SHEEP-PROJECT cover lamb and sheep meat processing from slaughter to packaging and selling the fi nished products. The project goal is to build up and successfully operate a Hungarian enterprise that can successfully deliver processed products of high quality to consumers. The premium quality sheep and lamb meat, originating from the plains of Hungarian Lowlands will be able to reach the tables of the Middle East and European consumers more readily in a processed, oven-ready packaging form than the raw products. Consequently, the project can contribute to satisfying this market segment.

WHY INVEST?

• Excellent environmental conditions for production.

• Support the industrial operators and the sub-regional association.

• Processed meat to comply with EU standardsand religious (e.g. Halal) and organic stipulations.

• Increasing demand for lamb, sheep and goat on the EU market.

• Rapid market acquisition and expansion.

• Good return on investment.

Competitive advantages

• Premium quality

• Developed business network covering the whole supply chain in the sector

• High-added value

• Economies of scale

• Availability of EU grants for agriculture and rural development

• Compliance with religious stipulations, and production of organic and natural products in line with the different market needs of the European and Middle East regions

• Availability of skilled labour for sheep breeding programmes in Hungary

• Support of the local government as well as NGOs

II. PROJECT DESCRIPTION

Property rights, licenses, certifi cations

The management of the SHEEP-PROJECT hasthe experience and connections to readilyacquire the following necessary permissions:

• building permit

• food safety permit

• technical security clearances

• fi re protection permit

• water permit

Position in the market – expected share

The planned and expected share will be approximately 5 % in the EU premium segment within the lamb-goat and sheep sector, and 40 % in such slaughtered animals in Hungary.

Target markets and groups

According to the business plans, the target markets are the Middle East and Western European countries, including Scandinavia.

On the Hungarian market, the most important target groups for the processed meat products are the large fresh market distribution centres, retail chains and the HORECA (hotels, restaurants, catering) sector. The latter will be an especially important target group for the processed products.

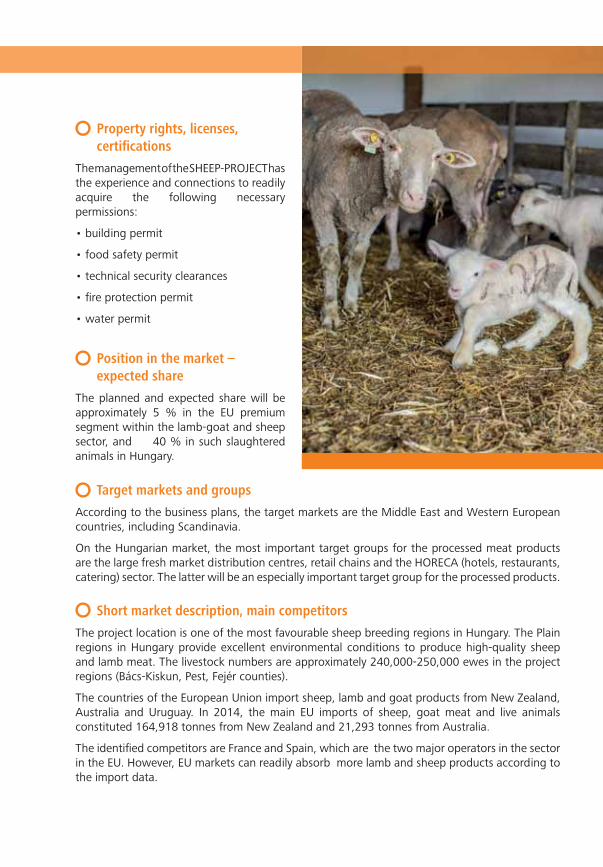

Short market description, main competitors

The project location is one of the most favourable sheep breeding regions in Hungary. The Plain regions in Hungary provide excellent environmental conditions to produce high-quality sheep and lamb meat. The livestock numbers are approximately 240,000-250,000 ewes in the project regions (Bács-Kiskun, Pest, Fejér counties).

The countries of the European Union import sheep, lamb and goat products from New Zealand, Australia and Uruguay. In 2014, the main EU imports of sheep, goat meat and live animals constituted 164,918 tonnes from New Zealand and 21,293 tonnes from Australia.

The identifi ed competitors are France and Spain, which are the two major operators in the sector in the EU. However, EU markets can readily absorb more lamb and sheep products according to the import data.

Key strategic partners

Local government and municipalities.

Producers: Hungarian stockbreeders and shepherds

Designer: AGROPROFIL Engineering Offi ce for Food Industry Ltd. is the biggest designoffi ce in Hungary; it specialises only in the design of food industry plants.

The management of SHEEP-PROJECT is negotiating with the prospective customersto update their letters of intent.

• KonTiki Foods AS• HIPP Ltd.• North Trade Stockholm AB• Nor-Frost AS• Frysekompaniet AS• CBA Trading Ltd.• Auchan Hungary Ltd.

• Organisation of Muslims in Hungary

Access to foreign markets, export markets, description of key risks and measures to prevent risks

The sales primarily focus on the European markets. Special attention will be given to countries where the number of Muslim inhabitants are increasing or relatively high, as sheep, lamb and goat consumption is signifi cant with this target group.

The business plan of the company takes into consideration several scenarios resulting from potential international risks, e.g. the fi nancial crisis. The total effects of risks on the profi tability level can be decreased to 10%.

III. FINANCIAL INDICATORS

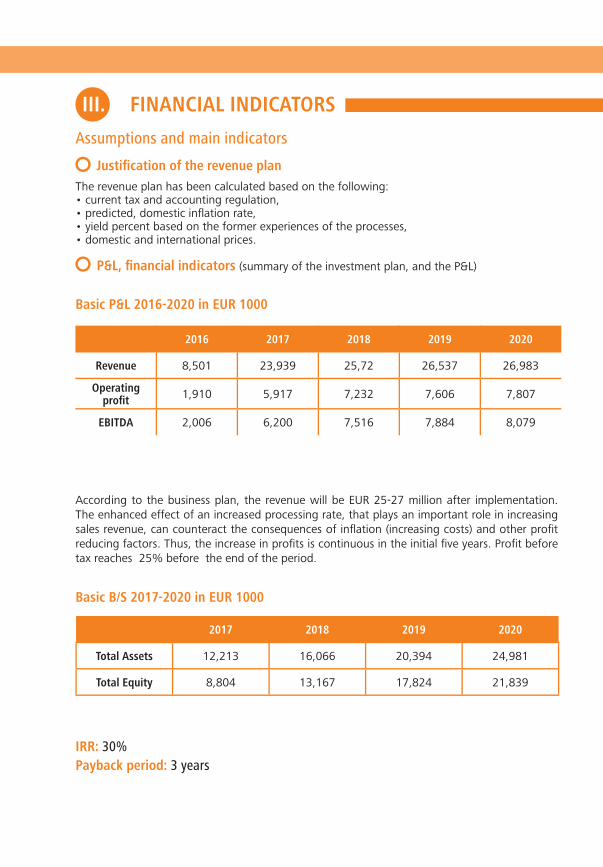

Assumptions and main indicators Justifi cation of the revenue plan

The revenue plan has been calculated based on the following:• current tax and accounting regulation,• predicted, domestic infl ation rate,• yield percent based on the former experiences of the processes,• domestic and international prices.

P&L, fi nancial indicators (summary of the investment plan, and the P&L)

2016 2017 2018 2019 2020

Revenue 8,501 23,939 25,72 26,537 26,983

Operating profi t 1,910 5,917 7,232 7,606 7,807

EBITDA 2,006 6,200 7,516 7,884 8,079

2017 2018 2019 2020

Total Assets 12,213 16,066 20,394 24,981

Total Equity 8,804 13,167 17,824 21,839

According to the business plan, the revenue will be EUR 25-27 million after implementation. The enhanced effect of an increased processing rate, that plays an important role in increasing sales revenue, can counteract the consequences of infl ation (increasing costs) and other profi t reducing factors. Thus, the increase in profi ts is continuous in the initial fi ve years. Profi t before tax reaches 25% before the end of the period.

Basic P&L 2016-2020 in EUR 1000

Basic B/S 2017-2020 in EUR 1000

IRR: 30%

Payback period: 3 years

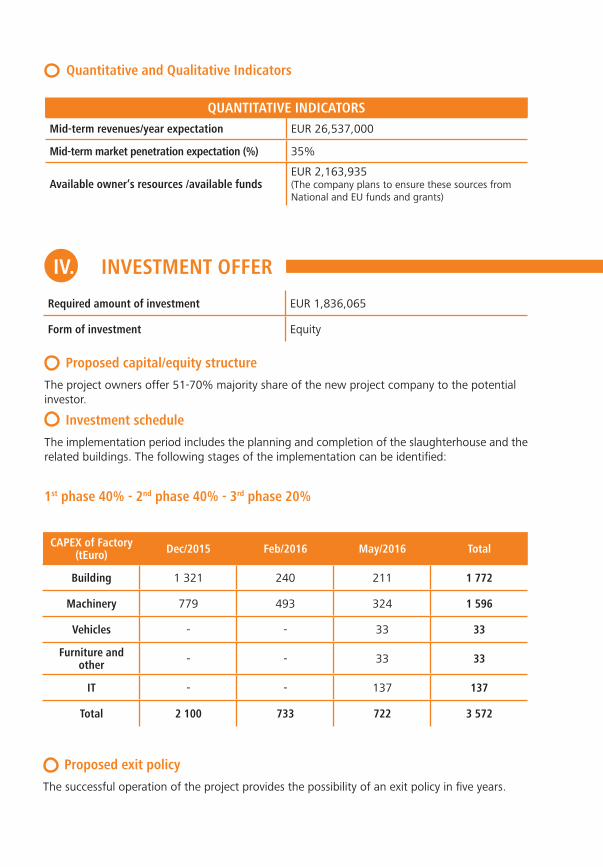

IV. INVESTMENT OFFER

Required amount of investment EUR 1,836,065

Form of investment Equity

Proposed exit policy

The successful operation of the project provides the possibility of an exit policy in fi ve years.

Proposed capital/equity structure

The project owners offer 51-70% majority share of the new project company to the potential investor.

Investment schedule

The implementation period includes the planning and completion of the slaughterhouse and the related buildings. The following stages of the implementation can be identifi ed:

1st phase 40% - 2nd phase 40% - 3rd phase 20%

Quantitative and Qualitative Indicators

QUANTITATIVE INDICATORS

Mid-term revenues/year expectation EUR 26,537,000

Mid-term market penetration expectation (%) 35%

Available owner’s resources /available fundsEUR 2,163,935(The company plans to ensure these sources from National and EU funds and grants)

CAPEX of Factory (tEuro) Dec/2015 Feb/2016 May/2016 Total

Building 1 321 240 211 1 772

Machinery 779 493 324 1 596

Vehicles - - 33 33

Furniture and other - - 33 33

IT - - 137 137

Total 2 100 733 722 3 572

SHORT DESCRIPTION

Funding requirement

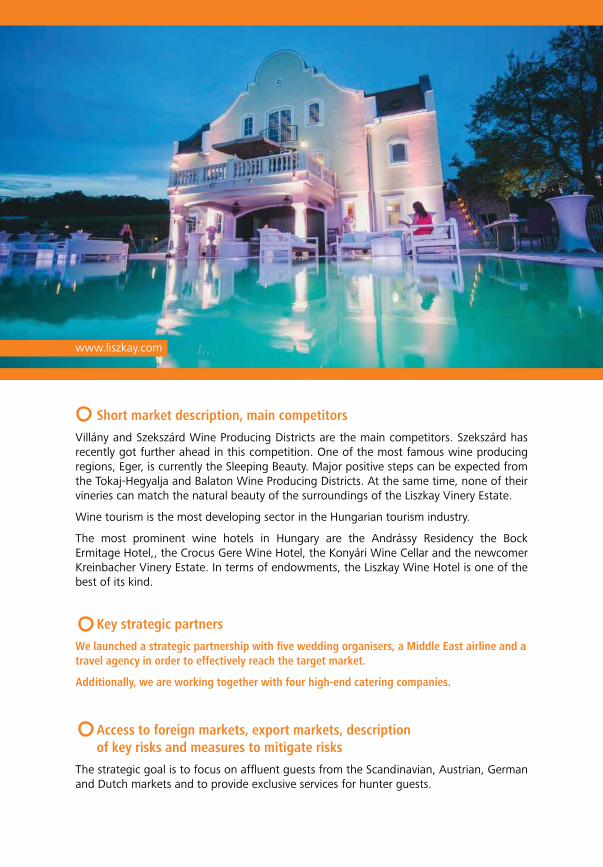

Liszkay Vineyard

and Winery Estate

Tusculanum, or summer cottage in Latin, a popular and admired region even in the ancient Roman period, is located in the most picturesque part on the northern shore of Lake Balaton.The Liszkay Winery is one of Hungary’s most beautiful vineyards with a nine-room wine hotel, award-winning wines and excellent cuisine.

EUR 4.5M Sector

Project owner

Location

Implementation period

Overall Budget of the Project

Agriculture

Nobilis Tusculanum Bortermelő Kft.

Mihály Liszkay, primary producer

H-8273 Monoszló, topographical lot No 048/2

Not relevant

EUR 4.5 million1

BA

SIC

PR

OJE

CT

DAT

A

1HUF 310to the EUR

I. PROJECT BACKGROUND

Short project background

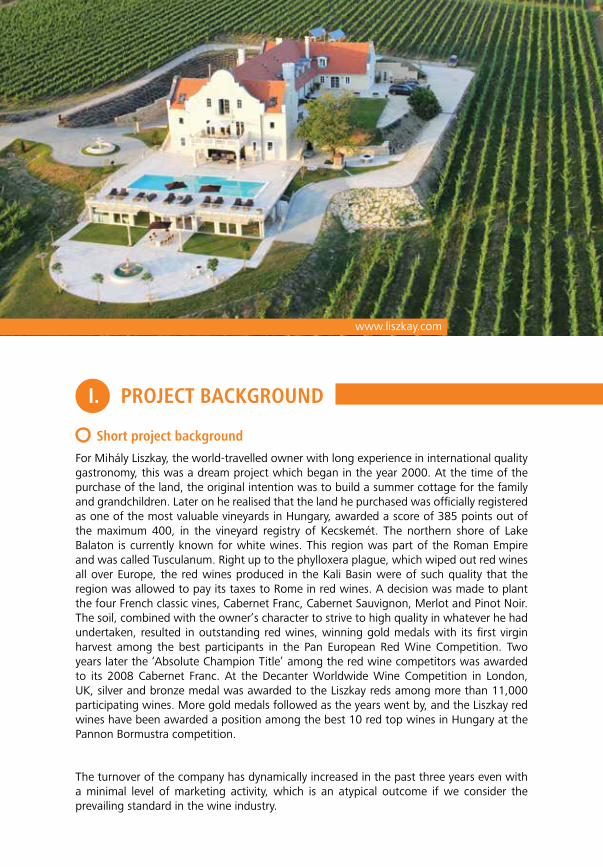

For Mihály Liszkay, the world-travelled owner with long experience in international quality

gastronomy, this was a dream project which began in the year 2000. At the time of the

purchase of the land, the original intention was to build a summer cottage for the family

and grandchildren. Later on he realised that the land he purchased was oficially registered

as one of the most valuable vineyards in Hungary, awarded a score of 385 points out of

the maximum 400, in the vineyard registry of Kecskemét. The northern shore of Lake

Balaton is currently known for white wines. This region was part of the Roman Empire

and was called Tusculanum. Right up to the phylloxera plague, which wiped out red wines

all over Europe, the red wines produced in the Kali Basin were of such quality that the

region was allowed to pay its taxes to Rome in red wines. A decision was made to plant

the four French classic vines, Cabernet Franc, Cabernet Sauvignon, Merlot and Pinot Noir.

The soil, combined with the owner’s character to strive to high quality in whatever he had

undertaken, resulted in outstanding red wines, winning gold medals with its irst virgin

harvest among the best participants in the Pan European Red Wine Competition. Two

years later the ‘Absolute Champion Title’ among the red wine competitors was awarded

to its 2008 Cabernet Franc. At the Decanter Worldwide Wine Competition in London,

UK, silver and bronze medal was awarded to the Liszkay reds among more than 11,000

participating wines. More gold medals followed as the years went by, and the Liszkay red

wines have been awarded a position among the best 10 red top wines in Hungary at the

Pannon Bormustra competition.

The turnover of the company has dynamically increased in the past three years even with

a minimal level of marketing activity, which is an atypical outcome if we consider the

prevailing standard in the wine industry.

www.liszkay.com

WHY INVEST?

• Exquisite hidden private and corporate

holidays, complimented by high-end

gastronomy, five-star accommodation and

Liszkay wines. Regional growth will increase

the project value;

• The natural beauty makes this estate unique

of its kind, and can compete internationally

anywhere in Europe;

• The unique Estate is situated in a remote,

quiet location, with a low number of quality

hotel rooms and a well-established, exclusive

private/corporate clientele;

• Central location in the Upper-Balaton region

and in Europe;

• Thevineyardisoficiallyregisteredamongthe

best terroirs in Hungary;

• Ten-year old French grape clones providing

top wines already, and the best expected

quality is yet to come in five to ten years as

the wines mature;

• Thereareoptionsforexpansion:increase

of the hotel capacity (60 rooms), acquisition

of further vineyards;

• Established brand

• Real estate value to increase as the region

continues its development in quality and

high-end gastronomy related tourism;

• Own helicopter landing for the exquisite

visitor and tourist or corporate management

is to be further capitalised upon;

• Theestateislocatedwithin4,200hectaresof

quality hunting ground.

The project fascinates not only with attractive inancial indicators: the products (wine and

accommodation) themselves, the infrastructure and the established brand make it to a unique investment.

We have to highlight that the potential of the real estate in the wine industry sector, when supported by an appropriate marketing strategy, makes this project worth to invest in (which is not the case for a number of renowned Hungarian wine producers).

II. PROJECT DESCRIPTION

General background of the management

The project owner, Mihály Liszkay, is prepared to support the project for up to one year

depending on the utilisation of the project and the person and objectives of the buyer. There

is management in place for the gastronomy section and the winery, while management

tasks can be outsourced for the long term by hiring a professional manager. Alternatively,

there are well-known management companies, which could run operations, if so required.

The key positions are occupied by experts with many years of relevant work experience

(oenologist, employed for ten years, chef, employed for four years).

The project is basically a lifestyle project with impressive resources: the recent land of 10

ha can be upsized by 5 to 6 ha of adjacent land. The building has nine luxurious rooms, all

different in style and interior. The Winery has a capacity to process 50k bottles a year and

has 135k bottles in stock.

Competitive advantages

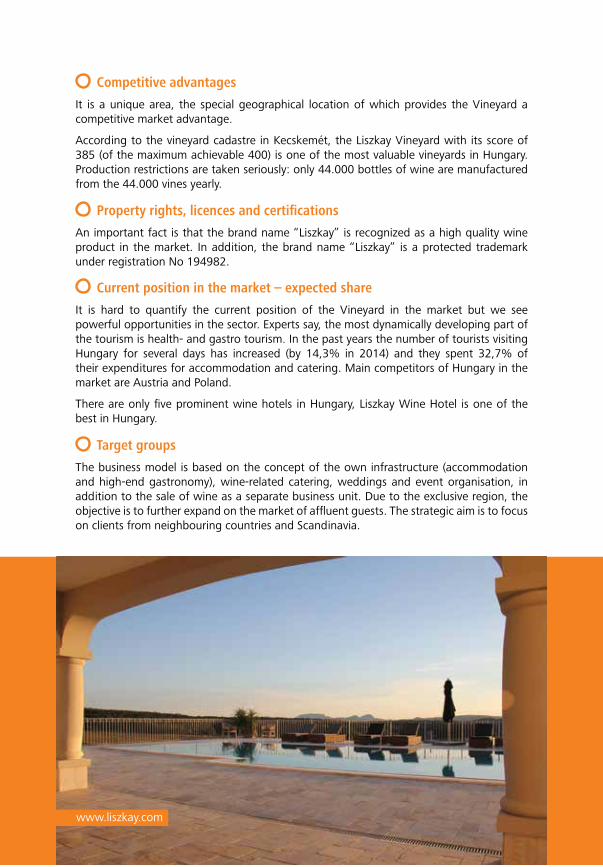

It is a unique area, the special geographical location of which provides the Vineyard a

competitive market advantage.

According to the vineyard cadastre in Kecskemét, the Liszkay Vineyard with its score of

385 (of the maximum achievable 400) is one of the most valuable vineyards in Hungary.

Production restrictions are taken seriously: only 44.000 bottles of wine are manufactured

from the 44.000 vines yearly.

Property rights, licences and certifications

An important fact is that the brand name “Liszkay” is recognized as a high quality wine

product in the market. In addition, the brand name “Liszkay” is a protected trademark

under registration No 194982.

Current position in the market – expected share

It is hard to quantify the current position of the Vineyard in the market but we see

powerful opportunities in the sector. Experts say, the most dynamically developing part of

the tourism is health- and gastro tourism. In the past years the number of tourists visiting

Hungary for several days has increased (by 14,3% in 2014) and they spent 32,7% of

their expenditures for accommodation and catering. Main competitors of Hungary in the

market are Austria and Poland.

There are only ive prominent wine hotels in Hungary, Liszkay Wine Hotel is one of the

best in Hungary.

Target groups

The business model is based on the concept of the own infrastructure (accommodation

and high-end gastronomy), wine-related catering, weddings and event organisation, in

addition to the sale of wine as a separate business unit. Due to the exclusive region, the

objective is to further expand on the market of afluent guests. The strategic aim is to focus

on clients from neighbouring countries and Scandinavia.

www.liszkay.com

Key strategic partners

We launched a strategic partnership with five wedding organisers, a Middle East airline and a travel agency in order to effectively reach the target market.

Additionally, we are working together with four high-end catering companies.

Access to foreign markets, export markets, description of key risks and measures to mitigate risks

The strategic goal is to focus on afluent guests from the Scandinavian, Austrian, German

and Dutch markets and to provide exclusive services for hunter guests.

Short market description, main competitors

Villány and Szekszárd Wine Producing Districts are the main competitors. Szekszárd has

recently got further ahead in this competition. One of the most famous wine producing

regions, Eger, is currently the Sleeping Beauty. Major positive steps can be expected from

the Tokaj-Hegyalja and Balaton Wine Producing Districts. At the same time, none of their

vineries can match the natural beauty of the surroundings of the Liszkay Vinery Estate.

Wine tourism is the most developing sector in the Hungarian tourism industry.

The most prominent wine hotels in Hungary are the Andrássy Residency the Bock

Ermitage Hotel,, the Crocus Gere Wine Hotel, the Konyári Wine Cellar and the newcomer

Kreinbacher Vinery Estate. In terms of endowments, the Liszkay Wine Hotel is one of the

best of its kind.

www.liszkay.com

III. FINANCIAL INDICATORS

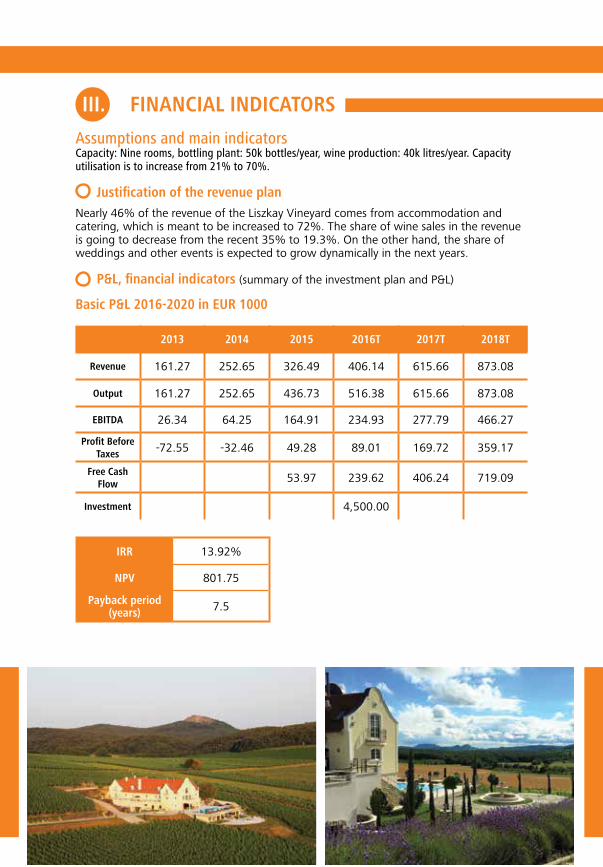

Assumptions and main indicatorsCapacity: Nine rooms, bottling plant: 50k bottles/year, wine production: 40k litres/year. Capacity utilisation is to increase from 21% to 70%. Justification of the revenue plan

Nearly 46% of the revenue of the Liszkay Vineyard comes from accommodation and catering, which is meant to be increased to 72%. The share of wine sales in the revenue is going to decrease from the recent 35% to 19.3%. On the other hand, the share of weddings and other events is expected to grow dynamically in the next years.

P&L, financial indicators (summary of the investment plan and P&L)

2013 2014 2015 2016T 2017T 2018T

Revenue 161.27 252.65 326.49 406.14 615.66 873.08

Output 161.27 252.65 436.73 516.38 615.66 873.08

EBITDA 26.34 64.25 164.91 234.93 277.79 466.27

Profit Before Taxes -72.55 -32.46 49.28 89.01 169.72 359.17

Free Cash Flow 53.97 239.62 406.24 719.09

Investment 4,500.00

IRR 13.92%

NPV 801.75

Payback period (years) 7.5

BasicP&L2016-2020inEUR1000

IV. INVESTMENT OFFER

Required amount of investment (EURm) 4,500

Form of investment Total buyout without deferred payment.

The former owner may participate in man-

agement tasks for one year.

Proposed capital/equity structure

In the project, a 100% interest in Nobilis Tusculanum Bortermelő Kft. and the agricultural

vineyard section (10 hectares of prime vineyard) are part of the total package and will

be sold according to the current legislation on agricultural land relating to the citizens of

Hungary, EU Member States, and some other preferred countries, such as Switzerland,

Greenland and Lichtenstein.

Investment schedule

The project owner wishes to receive the purchase price without deferred payment.

Proposed exit policy

The project owner wishes to withdraw from the company, but not at all costs.

Quantitative and Qualitative Indicators

QUANTITATIVE INDICATORS

Revenues/year2014(EUR‘000) 252.65

Expectedmid-termrevenues/year(EUR‘000) 631.63

Expected mid-term market penetration (%) Not relevant

Available owner’s resources/available funds (EUR‘000)

Not relevant

C O N TACT D E TA I L S

MIHÁLY LISZKAY+36(30)9727456

www.liszkay.com

Video of the Liszkay Vineyard and Winery Estate:

SHORT DESCRIPTION

Funding requirement

Ment alFit ol: Food For Thought

The project owner has developed and produced a novel blend of botanicals to prevent and decrease the risk of developing Alzheimer’s disease and other protein aggregation diseases. The products have successfully entered local markets; internationalization is the next step.

EUR 502,000Sector

Project ownerLocation

Implementation periodOverall Budget of the Project

Biotechnology, Pharmaceutical and Food Industry

Pharmacoidea Ltd. – Dr Tamás Letoha

Hungary

3 years

EUR 605,000

BA

SIC

PR

OJE

CT

DAT

A

Short backgroundPharmacoidea Ltd. is a Hungarian biotech SME specializing in drug discovery and functional food

development. The company has more than nine years of professional experience. Pharmacoidea’s

R&D portfolio covers a wide spectrum of innovative solutions from selective drug delivery methods

to functional food products enhancing mental health.

The company owns a 1,000 m2 factory for the production of innovative, functional food and

pharmaceutical products. The factory is fully equipped with in-line machines as follows:

• Grinding equipment for grinding medicinal and culinary herbs, sugar, etc. (capacity: 100–500 kilograms /

• hour);

• Mixer for blending powdered foods, additives, spices and tea (capacity: 800–1,000 kilograms / hour);

• Motorized dust feeder: we can fi ll powdered products (spices and other

powdered or grained foods) from 50 g up to 5 kg into packaging materials.

• Furthermore, the company plans to install a new automatic capsule-fi lling machine by the end of

March

• 2015 (capacity: 24,000 capsules / hour), which is able to fi ll 00 sized gelatine and hard capsules.

• A Quality Management System is applied to production, which satisfi es the requirements of Hungarian

Standard MSZ EN ISO 9001:2009.

General background of ManagementThe project owner, Tamas LETOHA, M.D., Ph.D., CEO of Pharmacoidea Ltd., coordinates the

scientifi c and fi nancial aspects of Pharmacoidea’s project. He has exceptional experience in

fi nancing R&D from government grants, NGOs, fund raising from corporations, and charities with

5+ years of management and fi scal skills in start-ups.

Dr Letoha was awarded the title of the most successful young Hungarian entrepreneur of the

year in 2014 at the Role Model of the Year Award Gala by the Prime Minister. Dr Letoha obtained

an M.D. and a Ph.D. degree from a medical school. He received several pharmaceutical awards

(Innovative Medicines Initiative) based on his scientifi c work and research. Dr Letoha had also

developed a novel application, which achieved the fi nancial support of Innovative Medicines

Initiative (IMI) for Pharmacoidea Ltd. in 2012.

I. PROJECT BACKGROUND

II. PROJECT DESCRIPTION

Pharmacoidea Ltd. has already released a wide range of own brand products. Its own developed

brand, MentalFitol™, is available in powder and capsule forms for consumers. MentalFitol™

was previously developed by using state-of-the-art chemo- and bioinformatics, furthermore,

molecular biology and pharmacology tools. The product is a novel blend of botanicals containing

scientifi cally validated anti-Alzheimer compounds. The product is also effective against Parkinson’s

disease and diabetes.

MentalFitolTM contains bioactive ingredients that have been successfully tested by Hungarian

health institutions and are in general use with their patents. It has been shown through

blood tests, repeated every three months, that MentalFitol™ is safe and effi cient in multiple

preclinical studies and various clinical trials of Alzheimer’s disease. These clinical trials show that

phytochemicals present in the MentalFitol™ botanical formula can slow down, prevent or halt

the progress of the Alzheimer’s condition.

Pharmacoidea Ltd. has built up partnerships with the local food manufacturer Mary-Ker Pasta and

has successfully placed MentalFitol™ pasta on the market. The company has an extended local

sales network and has established a partnership with the biggest local pharmaceutical distributor.

The aim of Pharmacoidea Ltd. is to detect opportunities in foreign markets and to introduce

MentalFitol™ to the worldwide market.

The phytochemicals of MentalFitol™ can also be commercially sold as tablets, which are the

preferred format for many consumers. In the long run, the compounds can also be registered, in

accordance with international legislation, as new herbal drugs for the prevention and treatment

of protein aggregation diseases like Alzheimer’s. In a few years, an alternative would be for large

food manufacturer companies to acquire the brand and the business model.

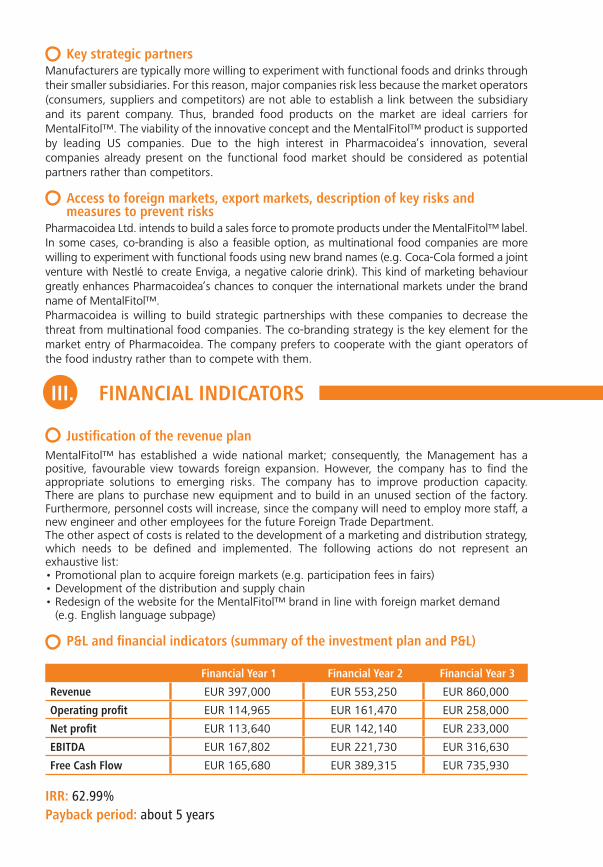

WHY INVEST?Attractive market opportunities:• The market trends for functional food products are more than promising; it continues to be a dyna- mically growing segment of the food industry.•The world market for functional foods and drinks is expected to reach USD 130 billion by 2015.

Promising results of the ongoing project:• The products of Pharmacoidea Ltd. have already been produced and sold on the market proving its merchantable quality and market demand.

Current partnerships with food manufacturers in Hungary are also encouraging. The innovative products of Pharmacoidea Ltd. will be able to access the global market with the required capital investments.

Competitive advantagesPharmacoidea Ltd. has identifi ed a gap in the functional food market. Besides numerous dietary

products, which help to prevent diseases, a functional food against Alzheimer’s is still missing

worldwide. There are similar initiatives, but the working mechanism of these products are only

fl avonoids versus the bioactive ingredients of MentalFitol™.

The ingredients of the working mechanism of MentalFitol™ are the result of the unique

development of bioactive components versus the initiatives of competitors that only use

fl avonoids.

MentalFitol™ and the other products of Pharmacoidea Ltd. are commercially available on local

markets.

Property rights, licenses and certifi catesThe IP of MentalFitol™ is kept as a company secret by Pharmacoidea Ltd. Our company

owns the intellectual property of MentalFitol™.

Position in the market and expected sharePharmacoidea has founded the PharmacoFood Life Sciences & Functional Food

Innovation Cluster to foster the marketing of MentalFitol™ in Hungary. The Cluster

(representing an annual sales revenue of approximately USD 1 billion), incorporating

the most successful food companies from Hungary (Hungerit, Gyermelyi, Ceres, etc.),

targets the production of functional food products with state-of-the-art scientifi c

approaches, which satisfi es the need of health conscious consumers.

Furthermore, the company has built up partnerships with local food manufacturers (e.g.

Hungerit) and successfully released its products to the market.

Target groupsBy incorporating the “plaque buster agents” of MentalFitol™ into daily food products,

Pharmacoidea will be able to reach diverse groups of consumers suffering from various

symptoms:

a) Alzheimer’s disease (5%–8% of individuals over 65, 15%–20% of individuals over

75, and 25%–50% of individuals over 85; the frequency is expected to double by 2030

and triple by 2050)

b) Parkinson’s disease (6.3 million people have Parkinson’s)

c) Type II diabetes (150 million cases worldwide, the number may well double by the

year 2025)

d) Age-related macular degeneration (2% of the population aged 50 and 30% of the

population aged 75 years or more).

Target countriesPharmacoidea Ltd. focuses on the US and Asia Pacifi c markets. The US functional foods

market is estimated to be the largest in the world, representing between 35% and 50%

of global sales. The Asian functional foods market continues to expand with strong

growth prospects. Western Europe is also a target market for our company.