Embed Size (px)

Citation preview

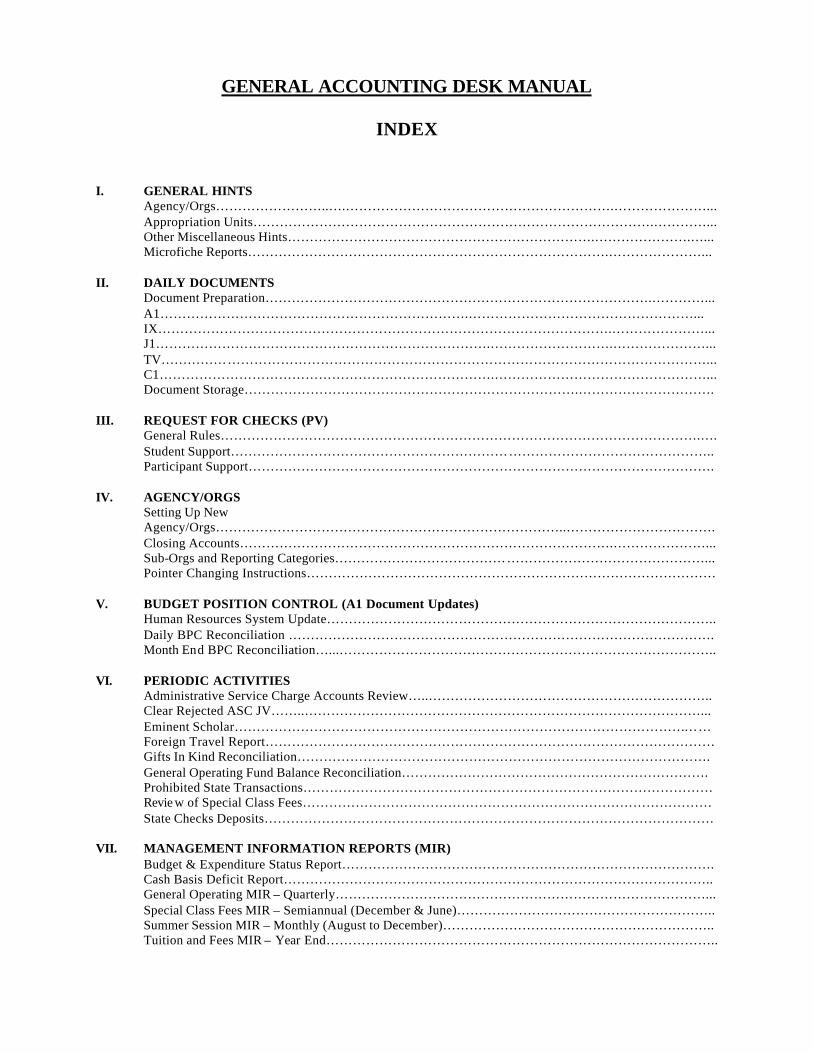

GENERAL ACCOUNTING DESK MANUAL

INDEX

I. GENERAL HINTS Agency/Orgs……………………..….…………………………………………………….…………………... Appropriation Units……………………………………………………………………………….…………... Other Miscellaneous Hints…………………………………………………………….………………….…... Microfiche Reports……………………………………………………………………….…………………...

II. DAILY DOCUMENTS

Document Preparation…………………………………………………………………………….…………... A1…………………………………………………………….……………………………………………... IX………………………………………………………………………………………….…………………... J1………………………………………………………………….……………………….…………………... TV……………………………………………………………………………………………………………... C1………………………………………………………………….…………………………………………... Document Storage………………………………………………………………….………………………….

III. REQUEST FOR CHECKS (PV)

General Rules……………………………………………………………………………………………….…. Student Support……………………………………………………………………………………………….. Participant Support…………………………………………………………………………………………….

IV. AGENCY/ORGS

Setting Up New Agency/Orgs……………………………………………………………………..……………………………. Closing Accounts………………………………………………………………………….…………………... Sub-Orgs and Reporting Categories…………………………………………………………………………...

Pointer Changing Instructions………………………………………………………………………………… V. BUDGET POSITION CONTROL (A1 Document Updates)

Human Resources System Update…………………………………………………………………………….. Daily BPC Reconciliation ……………………………………………………………………………………. Month End BPC Reconciliation…...…………………………………………………………………………..

VI. PERIODIC ACTIVITIES

Administrative Service Charge Accounts Review…..……………………………………………………….. Clear Rejected ASC JV……..………………………………………………………………………………... Eminent Scholar……………………………………………………………………………………………… Foreign Travel Report………………………………………………………………………………………… Gifts In Kind Reconciliation…………………………………………………………………………………. General Operating Fund Balance Reconciliation……………………………………………………………. Prohibited State Transactions………………………………………………………………………………… Revie w of Special Class Fees………………………………………………………………………………… State Checks Deposits…………………………………………………………………………………………

VII. MANAGEMENT INFORMATION REPORTS (MIR)

Budget & Expenditure Status Report…………………………………………………………………………. Cash Basis Deficit Report…………………………………………………………………………………….. General Operating MIR – Quarterly…………………………………………………………………………... Special Class Fees MIR – Semiannual (December & June)………………………………………………….. Summer Session MIR – Monthly (August to December)…………………………………………………….. Tuition and Fees MIR – Year End……………………………………………………………………………..

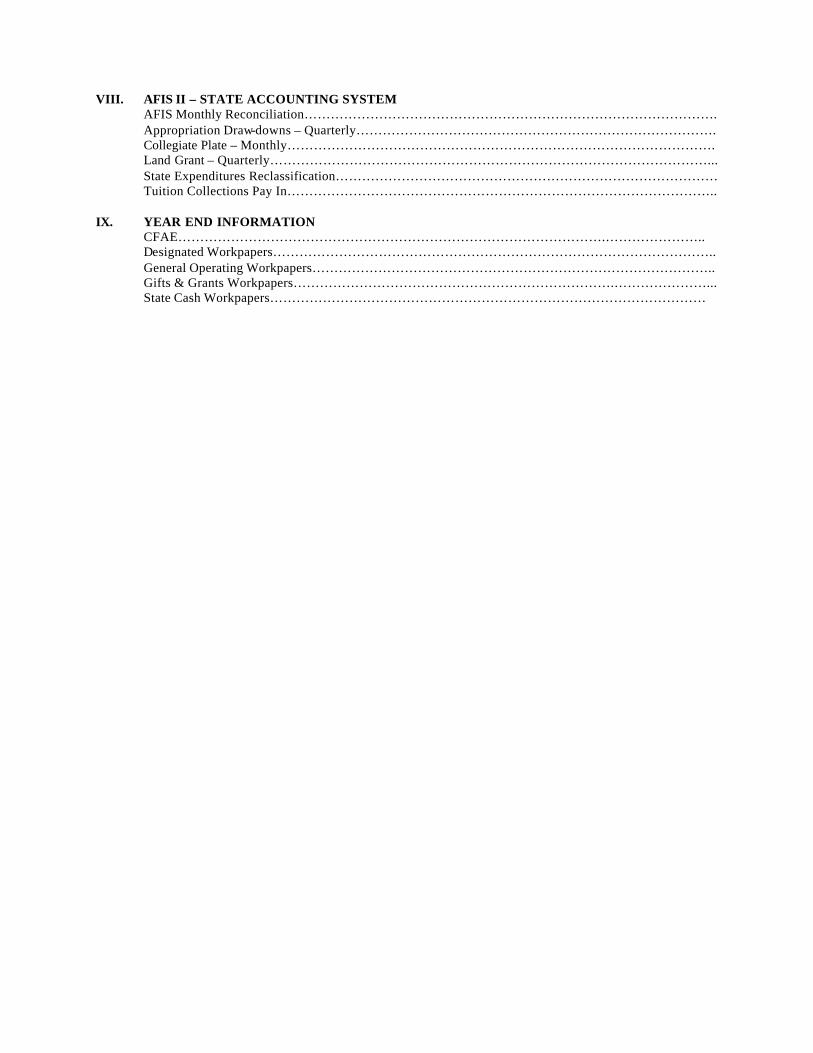

VIII. AFIS II – STATE ACCOUNTING SYSTEM

AFIS Monthly Reconciliation…………………………………………………………………………………. Appropriation Draw-downs – Quarterly………………………………………………………………………. Collegiate Plate – Monthly……………………………………………………………………………………. Land Grant – Quarterly………………………………………………………………………………………... State Expenditures Reclassification…………………………………………………………………………… Tuition Collections Pay In……………………………………………………………………………………..

IX. YEAR END INFORMATION

CFAE…………………………………………………………………………………….………………….. Designated Workpapers……………………………………………………………………………………….. General Operating Workpapers……………………………………………………………………………….. Gifts & Grants Workpapers……………………………………………………………….…………………... State Cash Workpapers………………………………………………………………………………………

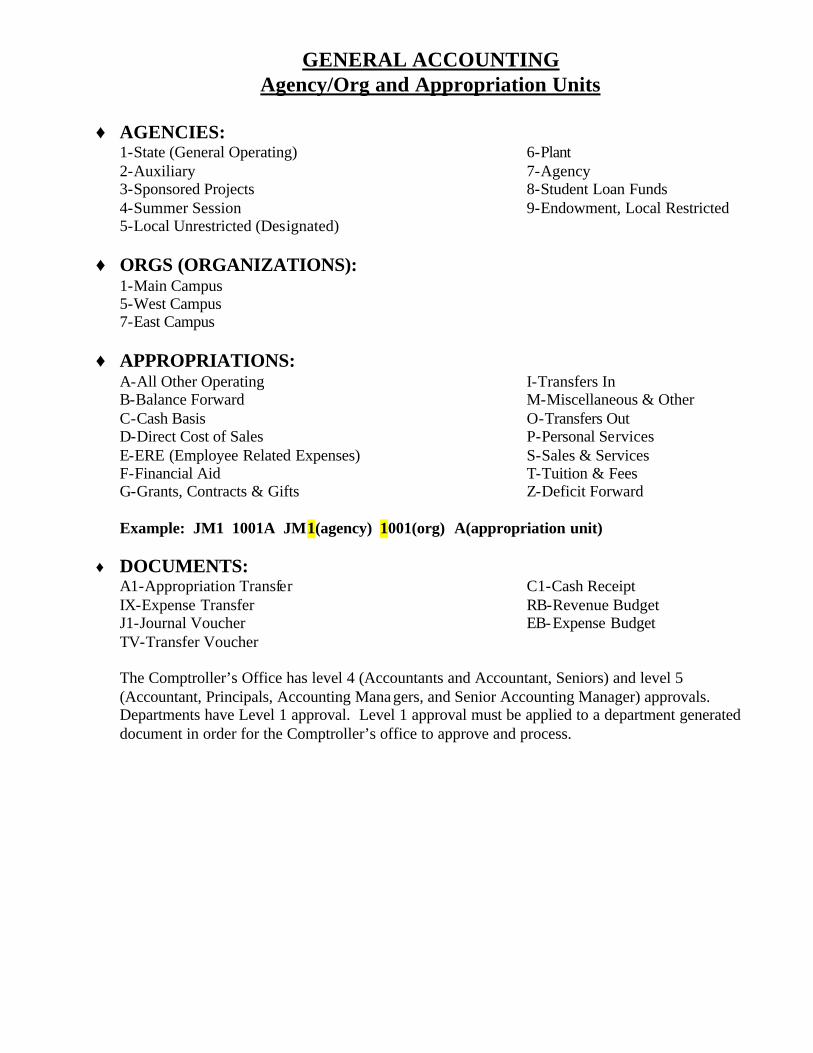

GENERAL ACCOUNTING Agency/Org and Appropriation Units

♦ AGENCIES:

1-State (General Operating) 6-Plant 2-Auxiliary 7-Agency 3-Sponsored Projects 8-Student Loan Funds 4-Summer Session 9-Endowment, Local Restricted 5-Local Unrestricted (Designated)

♦ ORGS (ORGANIZATIONS): 1-Main Campus 5-West Campus 7-East Campus

♦ APPROPRIATIONS: A-All Other Operating I-Transfers In B-Balance Forward M-Miscellaneous & Other C-Cash Basis O-Transfers Out D-Direct Cost of Sales P-Personal Services E-ERE (Employee Related Expenses) S-Sales & Services F-Financial Aid T-Tuition & Fees G-Grants, Contracts & Gifts Z-Deficit Forward Example: JM1 1001A JM1(agency) 1001(org) A(appropriation unit)

♦ DOCUMENTS: A1-Appropriation Transfer C1-Cash Receipt IX-Expense Transfer RB-Revenue Budget J1-Journal Voucher EB-Expense Budget TV-Transfer Voucher The Comptroller’s Office has level 4 (Accountants and Accountant, Seniors) and level 5 (Accountant, Principals, Accounting Managers, and Senior Accounting Manager) approvals. Departments have Level 1 approval. Level 1 approval must be applied to a department generated document in order for the Comptroller’s office to approve and process.

K:/data/general accounting/fiche reports and uses

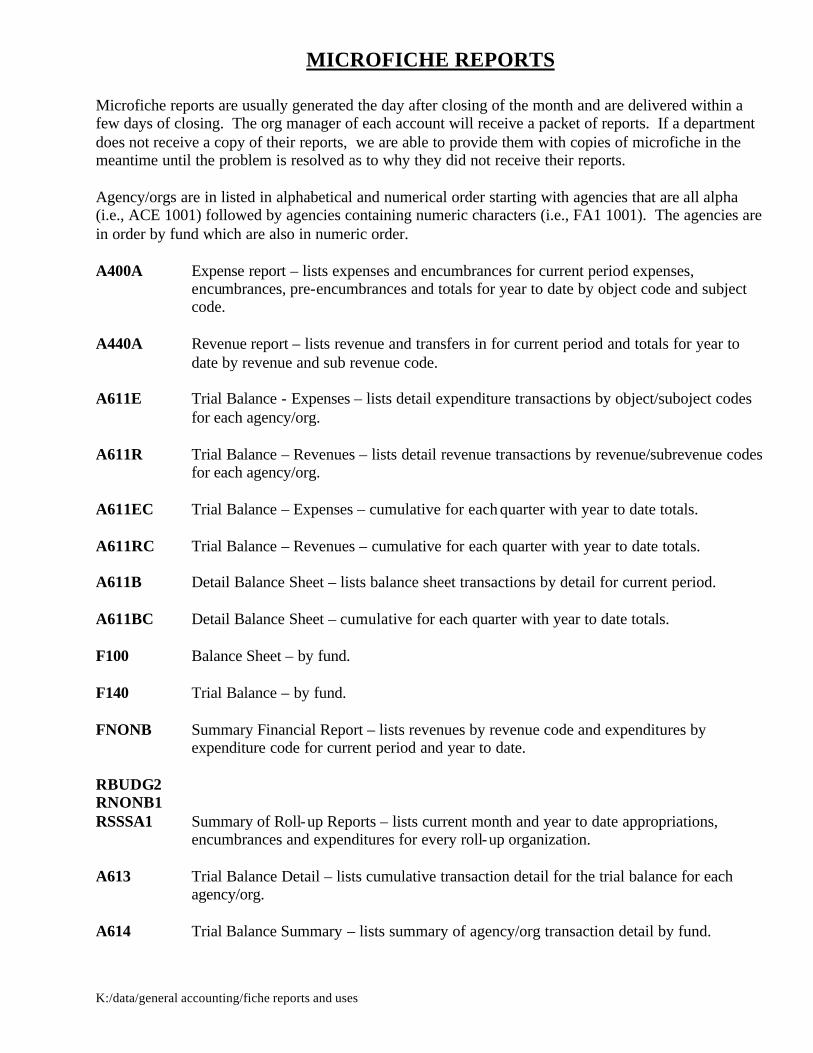

MICROFICHE REPORTS

Microfiche reports are usually generated the day after closing of the month and are delivered within a few days of closing. The org manager of each account will receive a packet of reports. If a department does not receive a copy of their reports, we are able to provide them with copies of microfiche in the meantime until the problem is resolved as to why they did not receive their reports. Agency/orgs are in listed in alphabetical and numerical order starting with agencies that are all alpha (i.e., ACE 1001) followed by agencies containing numeric characters (i.e., FA1 1001). The agencies are in order by fund which are also in numeric order. A400A Expense report – lists expenses and encumbrances for current period expenses,

encumbrances, pre-encumbrances and totals for year to date by object code and subject code.

A440A Revenue report – lists revenue and transfers in for current period and totals for year to

date by revenue and sub revenue code. A611E Trial Balance - Expenses – lists detail expenditure transactions by object/suboject codes

for each agency/org. A611R Trial Balance – Revenues – lists detail revenue transactions by revenue/subrevenue codes

for each agency/org. A611EC Trial Balance – Expenses – cumulative for each quarter with year to date totals. A611RC Trial Balance – Revenues – cumulative for each quarter with year to date totals. A611B Detail Balance Sheet – lists balance sheet transactions by detail for current period. A611BC Detail Balance Sheet – cumulative for each quarter with year to date totals. F100 Balance Sheet – by fund. F140 Trial Balance – by fund. FNONB Summary Financial Report – lists revenues by revenue code and expenditures by

expenditure code for current period and year to date. RBUDG2 RNONB1 RSSSA1 Summary of Roll-up Reports – lists current month and year to date appropriations,

encumbrances and expenditures for every roll-up organization. A613 Trial Balance Detail – lists cumulative transaction detail for the trial balance for each

agency/org. A614 Trial Balance Summary – lists summary of agency/org transaction detail by fund.

K:/data/general accounting/general hints

GENERAL HINTS

♦ A1’S: If increase/decrease budgets-original to account file (not master file for A1’s) and a copy to Marilyn. Local budget changes require VP Office approval, Budget Office approval if revenue comes from general university, and the assistant comptroller’s approval. ♦ PROHIBITED TRANSACTIONS: (COM 111 AND 401-03) Food on state (except for recruitment, COM 420-02). Student support on state. Holiday celebration expenditures on state. Gifts & Contributions to organizations and/or individuals. Liquor/Alcohol. Parking decals. Flowers unless for official events (i.e., convocations, conferences). Fines-library, Parking, etc. University Club Membership. ♦ VP APPROVAL: (COM 111 AND 401-02) Food greater than $200.00 if charge incurred by Dean or Director. Employee non-monetary performance based awards greater than $100 per person. Holiday celebrations on local accounts. Expenditure authority increase (will need UFPA’S approval- if account receives funding from General University sources (i.e., local collections, ASC)). Live plants. Milton Glick, Senior VP and Provost Elaine Maimon, Provost, VP of ASU West Charles Backus, Provost, VP of ASU East Jonathan Fink, VP of Research and Strategic Initiations Allan Price, VP of Institutional Advancement Christine Wilkinson, VP of Student Affairs Mernoy Harrison, Associate VP of Administrative Services ♦ FOOD EXPENDITURES: (COM 420-02) Not allowed on state unless for ASU, interviewees, or independent contractors in travel status. Business meal form is required if the amount is greater than $25; except for conferences, workshop, retreat, on-campus receptionunts. Dean approvals greater than $200.00, for local accounts. If charge incurred by Dean, then VP approval is required. Liquor/Alcohol prohibited. ♦ STUDENT SUPPORT ON STATE ACCOUNTS: (COM 422-01) All non-payroll student support (object 7700) is prohibited on state agency/orgs. ♦ INDEPENDENT CONTRACTOR (ICC): (COM 421-01) Departmental Professional Services order (less than or equal to $5000), except guest lecturer (less than $10,000 or 2 weeks).

K:/data/general accounting/general hints

P.O., bidding documentation, & written contract (greater than $5000.00 or greater than 2 weeks). All independent contractors except guest lectures visiting less than 2 weeks, performers with limited number of performances, and payments of $100 or less, need determination checklist. Non-residence alien, must complete form 8233 or 4224. The Independent Contractor Certification must be used for ANY payment request to an independent contractor unless payment amount is less than $100. This form applies to businesses as well as individuals. The purpose is to identify non-resident aliens and non-domestic partnerships/corporations. Nominal payments of $100 or less do not require forms. ♦ EMPLOYMENT REIMBURSEMENT: (COM 420-01) $500 or less process on PV’S and send directly to Accounts Payables. Greater than $500 will need Dean level approval and greater than $1,000 will need VP and purchasing approval. Employee should not pay for services (payments for services are subject to 1099 reporting). If goods are paid for on a credit card, then the employee will be reimbursed. DO NOT pay the credit card company directly. ♦ GIFTS/DONATIONS: (COM 303/304) Must be deposited by the Development Office to the appropriate agency/org. Gift/Donations are not allowed to be PAID from the University (state or local). ♦ DEPOSITS: (COM 301-01) Accountants approval is needed for any one check greater than $10,000, make sure it’s not gifts/donations or against personal services. ♦ ASC: (COM 206) Administrative Service Charges allowes local agency orgs to share in the cost of University administrative services that benefit local agency orgs. ASC is not charged to student support (7700), transfer out (8001), and Direct Cost of Sales (7010). Automatically generated at the end of the month. If expenses are transfer to/from accounts subject to ASC, related ASC charges/credits will be system generated at month end. ♦ SPONSORED ACCOUNTS Documents with transactions effecting a sponsored account must receive approva l or processed by Grant and Contract Accounting. If the sponsored account is benefiting from the transaction, a written or verbal approval needs to be documented and the document may be processed in the Comptroller’s Office. If the non sponsored account is benefiting from the transaction, then the Grant and Contract Accountant must approve and process the document. ♦ DOCUMENT SUPPORT The type of the support documentation and/or narrative required for a transaction depends upon the nature of the transaction and the materiality of it. In some circumstances, the document is not self explanatory and/or the dollar amount warrants additional documentation. If the documentation has not been supplied by the originating department it will be requested by the Comptroller’s Office before the document is processed. Even though additional support is not always required, it is expected that departments originating documents maintain complete support for all transactions they originate. The accountant/financial accounting managers are allowed to use their judgements as to how much

K:/data/general accounting/general hints

additional support, if any is needed before a document is processed. Documentation requirements will vary per each accountant/review. Documents should be able to stand on their own. ♦ OTHERS:

• On-campus PO’s are closed by the department by modifying the encumbrance down to zero. • RX or off-campus PC’s/PO’s can only be closed by purchasing, contact buyer. • II questions need to be directed to the servicing department. • CR COD…information is obtained from the cashiers office. • Copies of PV’s are obtained from Account Payable. • Accounts Receivable questions, go to Peggy Jueden. • Missing Advantage reports, direct department to the helpline. • Any Advantage problems report to Wu Jian Zhu. • Payroll questions either go directly to payroll or the accountant senior payroll liaison. • Plant fund, Auxiliary, Financial Aid, direct them to the appropriate person. • SR, OC, and CI documents (new inventory system) direct department to Stores. • All staff & faculty awards need to be paid through the payroll system. • Prior year commitments carry appropriations forward to new fiscal year. • Soft encumbrances need to be legitimate circumstances behind their occurrence; need specific

RX, PC, etc. involved. Then they need to be forwarded to the assistant comptroller for approval. • Fine Arts local budgets are loaded manually to various accounts. • Agency/Org authorized signers must initiate request for Comptroller generated documents via e-

mail or other hard copy documentation. Look on the ORG1 tables to find authorized signers. • Direct billings to hotels for consultants/speaker’s hotel bills should be coded to 7310 13

(documented expense reimbursement) which is where they would be coded if we were reimbursing the consultant rather than making the payment directly. 7390 99 should not be used, since it is not appropriate. This logic would also hold for any related expense which we are direct billing.

• Original receipts are required when reimbursing consultants, etc. for their travel expenses. If original receipts are not provided then the payment of the expenses needs to be included in their consultant fee and would be reported on a 1099 form. This policy would hold true for any reimbursements being made to independent contractors (consultants, lecturers and speakers).

• Payments for dinners/conferences where the words “benefit” and “donation” appear give weight to the position that it will be charitable contribution. This would be a violation of state statute and would not be an appropriate use of university funds. The department should process through the Foundation. If there is not any Foundation money, the department should contact the Provost’s office (Lynn Carpenter) to discuss other options.

Monthly Prohibited State Transactions

Background: Certain disbursement transactions are prohibited on state accounts according to University policy, COM 401–03: Prohibited Transactions. Included in these prohibited transactions are expenses for food (7390 06), interest (7390 01), and student support (7700). The purpose of “The Monthly Prohibited State Transactions Report” is to periodically monitor all state accounts for Main (1150), East (1160), and West (1180) campuses for any expenses that fall into the restricted categories, so that they can be re-coded or transferred off state accounts. Procedure:

• Run a query on the data warehouse to include these fields: Account Acceptance Date and/or Fiscal Month Transaction Document Code Transaction Number Fund Account Type Line Description Expenditure Code $ Amount

• Of these fields, the following will need to be limited:

Fund Code: 1150, 1160, 1180 Account Type Code: 22, 23, 24 Expenditure Code: 739001, 739006, 7700XX

• Copy query information into a spreadsheet program and arrange in report format.

• Identify transactions that need to be corrected and forward

copies of the report to the corresponding accountant.

• Place a final copy of the monthly report in the Prohibited Transaction Binder.

Cross-References

For information on student support, refer to COM 422–01: Student Financial Support For information on food policies and procedures, refer to COM 420–02: Business Meals, Food Expenses

Budget Position Control Daily Reconciliation Instructions

The budget position control report is generated on a daily basis and comprises a list of appropriation transactions (A1) that have posted to the advantage system, however, did not interface into the HRMS system. The procedures below are followed to manually input into the HRMS system, those transactions that did not interface into HRMS. The procedures listed below are only done for state accounts with the ‘P’ appropriation. Procedures: -Report HR0424-02 is produced on a daily basis -Logon to HRMS system -Select ‘81’(position control) -Select ‘35’(current budget detail update) -Enter info from BPC report (only state accounts with ‘P’ appr code) ENTER -Print screen of ‘Current Budget Detail Update’ -Tab down to ‘budget adjustment’ enter amount (positive # if debit, negative # if credit) (Add amounts together and enter in sequential order all transactions that have the EXACT same info. This will include any amount listed in the budget adjustment field prior to new adjustment.) -Tab to ‘adjustment reference’, type number 1 if no number is in field, if there is a number in the field, type the next consecutive number. ENTER -Print screen. ENTER -Continue steps until all transactions on BPC report for state accounts with ‘P’ appr have been entered. - File copies of the before and after screens of the adjustments behind the HR0424-02 report.

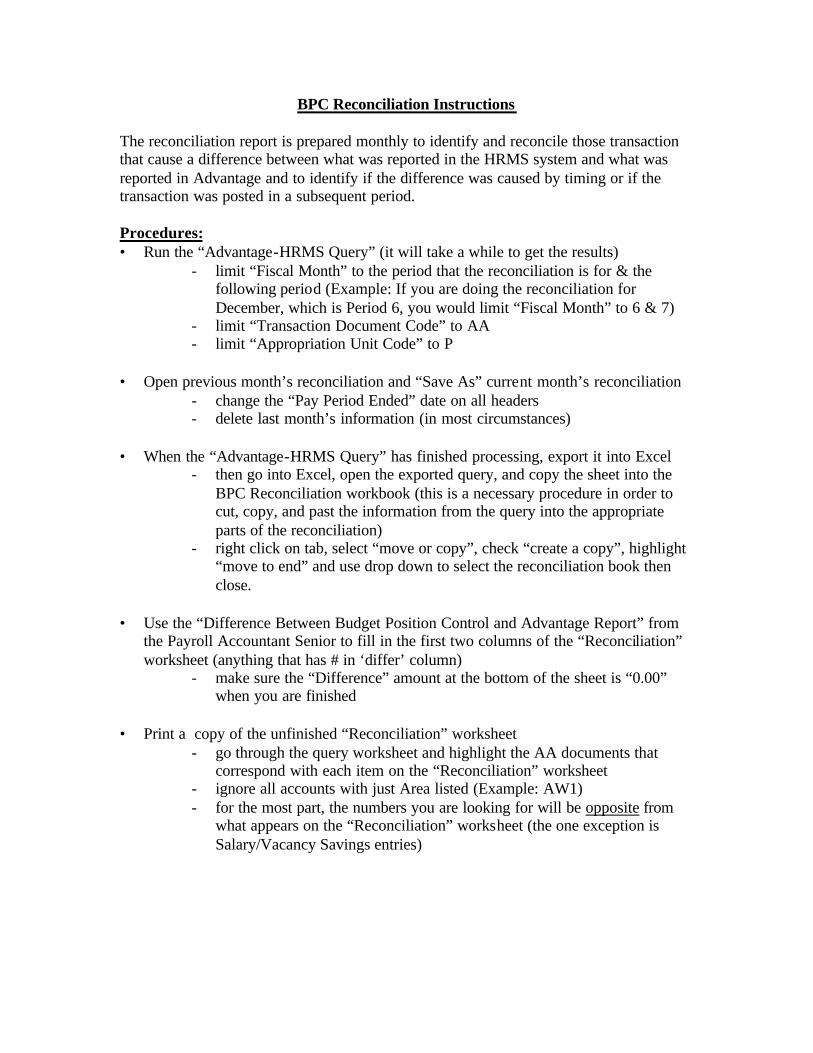

BPC Reconciliation Instructions The reconciliation report is prepared monthly to identify and reconcile those transaction that cause a difference between what was reported in the HRMS system and what was reported in Advantage and to identify if the difference was caused by timing or if the transaction was posted in a subsequent period. Procedures: • Run the “Advantage-HRMS Query” (it will take a while to get the results)

- limit “Fiscal Month” to the period that the reconciliation is for & the following period (Example: If you are doing the reconciliation for December, which is Period 6, you would limit “Fiscal Month” to 6 & 7)

- limit “Transaction Document Code” to AA - limit “Appropriation Unit Code” to P

• Open previous month’s reconciliation and “Save As” current month’s reconciliation

- change the “Pay Period Ended” date on all headers - delete last month’s information (in most circumstances)

• When the “Advantage-HRMS Query” has finished processing, export it into Excel

- then go into Excel, open the exported query, and copy the sheet into the BPC Reconciliation workbook (this is a necessary procedure in order to cut, copy, and past the information from the query into the appropriate parts of the reconciliation)

- right click on tab, select “move or copy”, check “create a copy”, highlight “move to end” and use drop down to select the reconciliation book then close.

• Use the “Difference Between Budget Position Control and Advantage Report” from

the Payroll Accountant Senior to fill in the first two columns of the “Reconciliation” worksheet (anything that has # in ‘differ’ column)

- make sure the “Difference” amount at the bottom of the sheet is “0.00” when you are finished

• Print a copy of the unfinished “Reconciliation” worksheet

- go through the query worksheet and highlight the AA documents that correspond with each item on the “Reconciliation” worksheet

- ignore all accounts with just Area listed (Example: AW1) - for the most part, the numbers you are looking for will be opposite from

what appears on the “Reconciliation” worksheet (the one exception is Salary/Vacancy Savings entries)

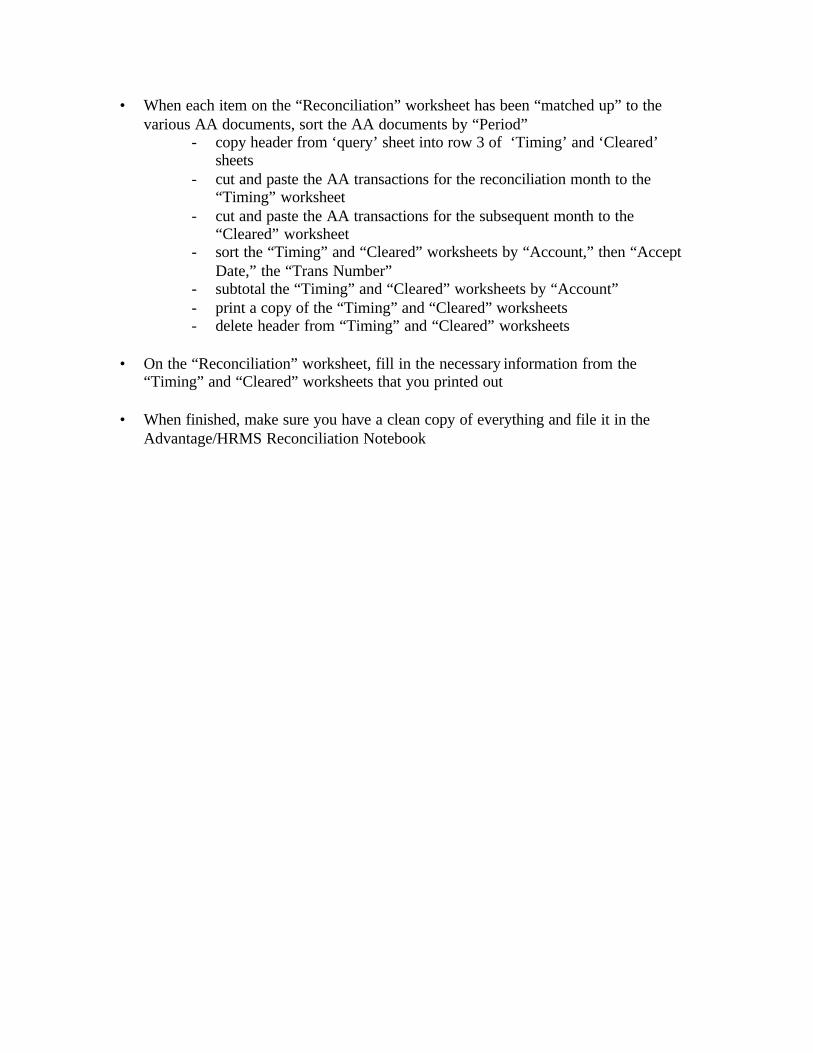

• When each item on the “Reconciliation” worksheet has been “matched up” to the various AA documents, sort the AA documents by “Period”

- copy header from ‘query’ sheet into row 3 of ‘Timing’ and ‘Cleared’ sheets

- cut and paste the AA transactions for the reconciliation month to the “Timing” worksheet

- cut and paste the AA transactions for the subsequent month to the “Cleared” worksheet

- sort the “Timing” and “Cleared” worksheets by “Account,” then “Accept Date,” the “Trans Number”

- subtotal the “Timing” and “Cleared” worksheets by “Account” - print a copy of the “Timing” and “Cleared” worksheets - delete header from “Timing” and “Cleared” worksheets

• On the “Reconciliation” worksheet, fill in the necessary information from the

“Timing” and “Cleared” worksheets that you printed out • When finished, make sure you have a clean copy of everything and file it in the

Advantage/HRMS Reconciliation Notebook

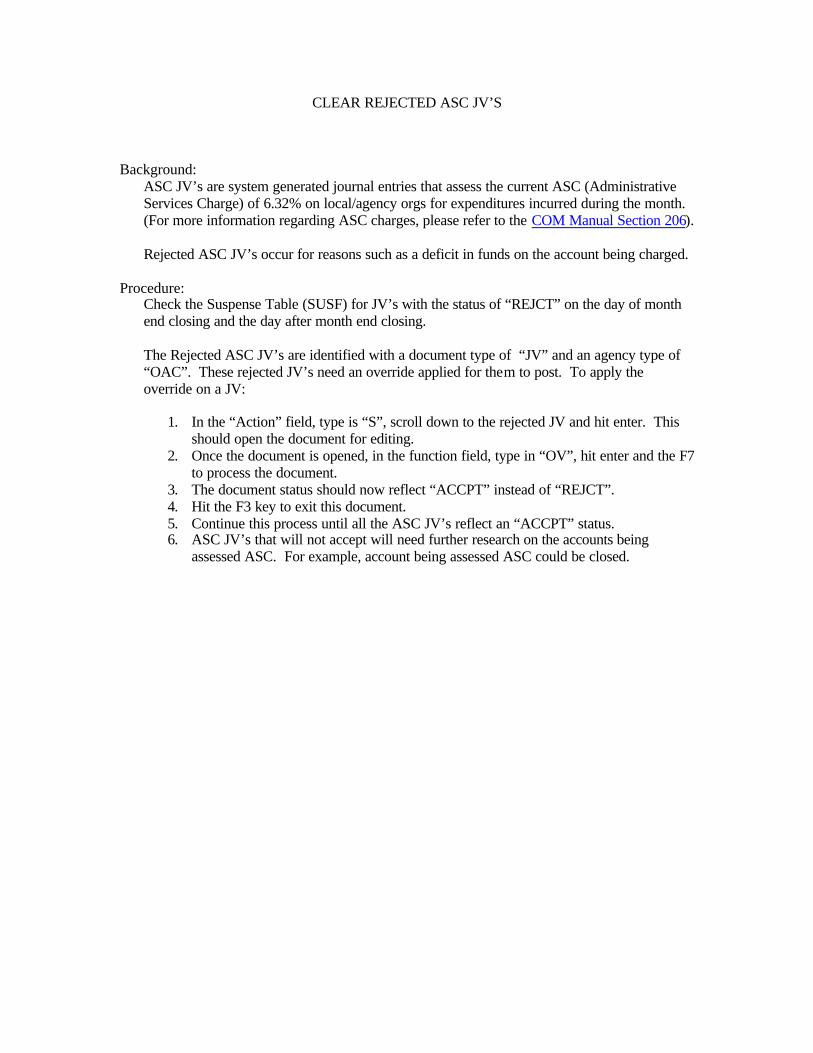

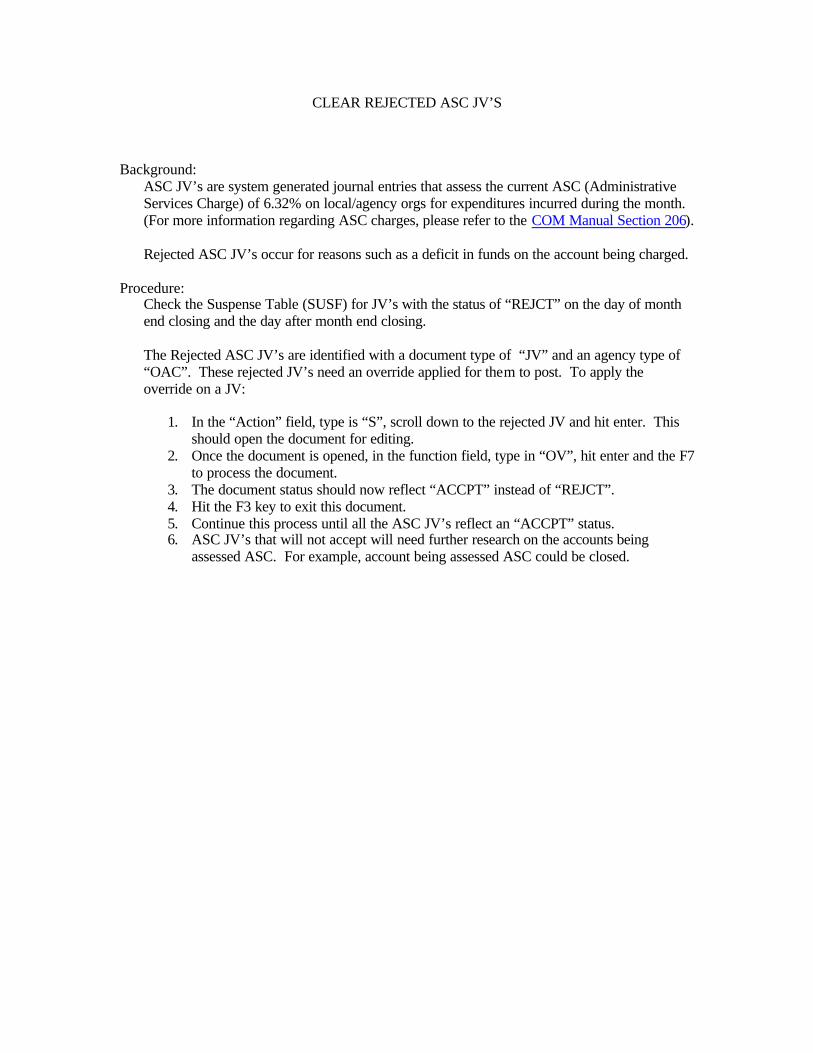

CLEAR REJECTED ASC JV’S Background:

ASC JV’s are system generated journal entries that assess the current ASC (Administrative Services Charge) of 6.32% on local/agency orgs for expenditures incurred during the month. (For more information regarding ASC charges, please refer to the COM Manual Section 206). Rejected ASC JV’s occur for reasons such as a deficit in funds on the account being charged.

Procedure:

Check the Suspense Table (SUSF) for JV’s with the status of “REJCT” on the day of month end closing and the day after month end closing.

The Rejected ASC JV’s are identified with a document type of “JV” and an agency type of “OAC”. These rejected JV’s need an override applied for them to post. To apply the override on a JV:

1. In the “Action” field, type is “S”, scroll down to the rejected JV and hit enter. This

should open the document for editing. 2. Once the document is opened, in the function field, type in “OV”, hit enter and the F7

to process the document. 3. The document status should now reflect “ACCPT” instead of “REJCT”. 4. Hit the F3 key to exit this document. 5. Continue this process until all the ASC JV’s reflect an “ACCPT” status. 6. ASC JV’s that will not accept will need further research on the accounts being

assessed ASC. For example, account being assessed ASC could be closed.

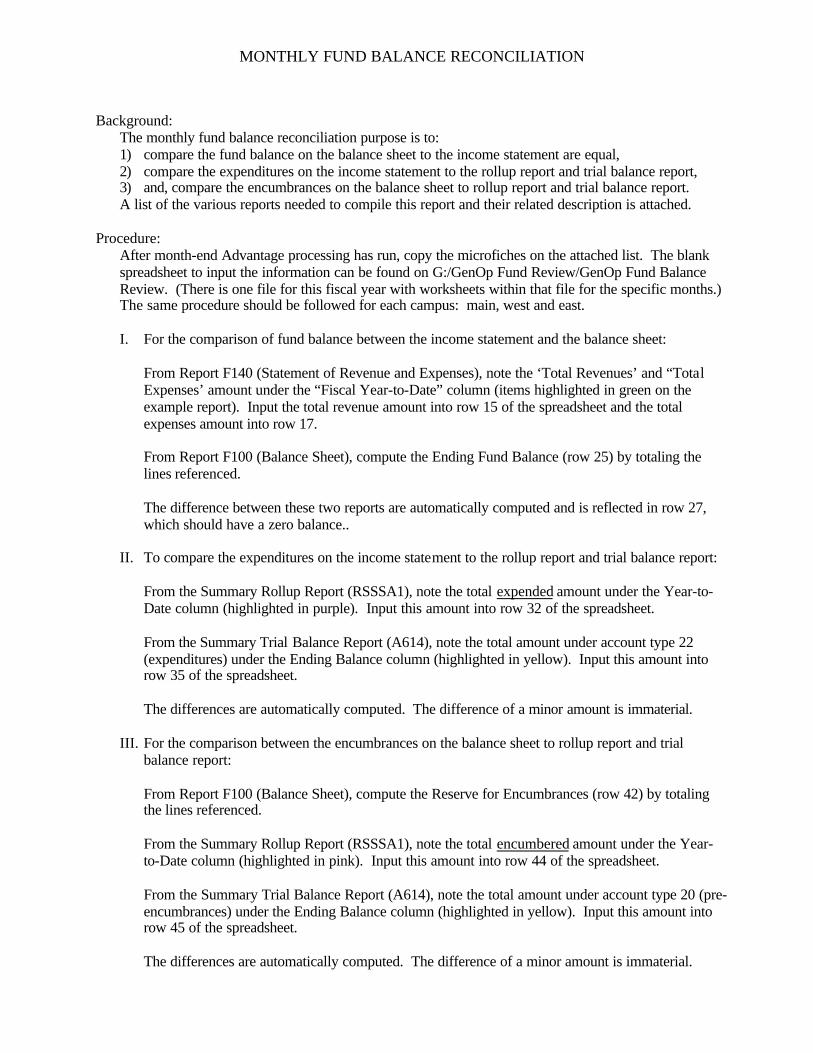

MONTHLY FUND BALANCE RECONCILIATION Background: The monthly fund balance reconciliation purpose is to:

1) compare the fund balance on the balance sheet to the income statement are equal, 2) compare the expenditures on the income statement to the rollup report and trial balance report, 3) and, compare the encumbrances on the balance sheet to rollup report and trial balance report. A list of the various reports needed to compile this report and their related description is attached.

Procedure: After month-end Advantage processing has run, copy the microfiches on the attached list. The blank spreadsheet to input the information can be found on G:/GenOp Fund Review/GenOp Fund Balance Review. (There is one file for this fiscal year with worksheets within that file for the specific months.) The same procedure should be followed for each campus: main, west and east.

I. For the comparison of fund balance between the income statement and the balance sheet:

From Report F140 (Statement of Revenue and Expenses), note the ‘Total Revenues’ and “Total Expenses’ amount under the “Fiscal Year-to-Date” column (items highlighted in green on the example report). Input the total revenue amount into row 15 of the spreadsheet and the total expenses amount into row 17.

From Report F100 (Balance Sheet), compute the Ending Fund Balance (row 25) by totaling the lines referenced.

The difference between these two reports are automatically computed and is reflected in row 27, which should have a zero balance..

II. To compare the expenditures on the income statement to the rollup report and trial balance report:

From the Summary Rollup Report (RSSSA1), note the total expended amount under the Year-to-Date column (highlighted in purple). Input this amount into row 32 of the spreadsheet. From the Summary Trial Balance Report (A614), note the total amount under account type 22 (expenditures) under the Ending Balance column (highlighted in yellow). Input this amount into row 35 of the spreadsheet. The differences are automatically computed. The difference of a minor amount is immaterial.

III. For the comparison between the encumbrances on the balance sheet to rollup report and trial balance report:

From Report F100 (Balance Sheet), compute the Reserve for Encumbrances (row 42) by totaling the lines referenced. From the Summary Rollup Report (RSSSA1), note the total encumbered amount under the Year-to-Date column (highlighted in pink). Input this amount into row 44 of the spreadsheet. From the Summary Trial Balance Report (A614), note the total amount under account type 20 (pre-encumbrances) under the Ending Balance column (highlighted in yellow). Input this amount into row 45 of the spreadsheet. The differences are automatically computed. The difference of a minor amount is immaterial.

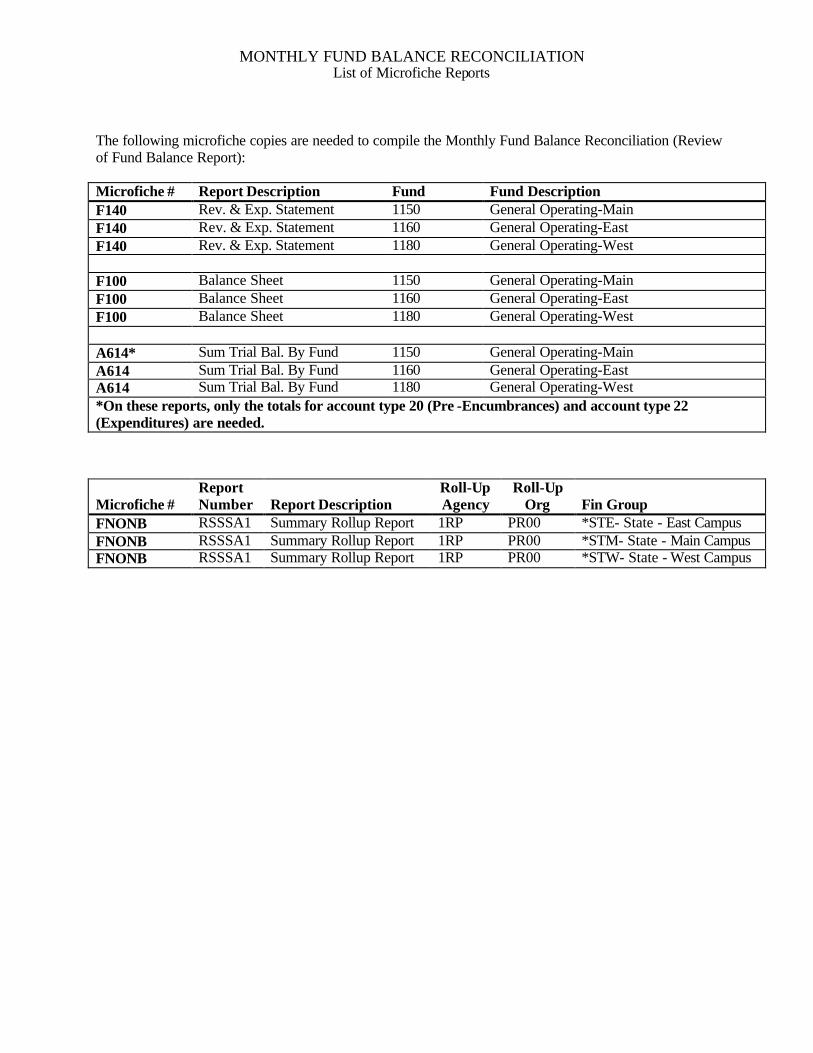

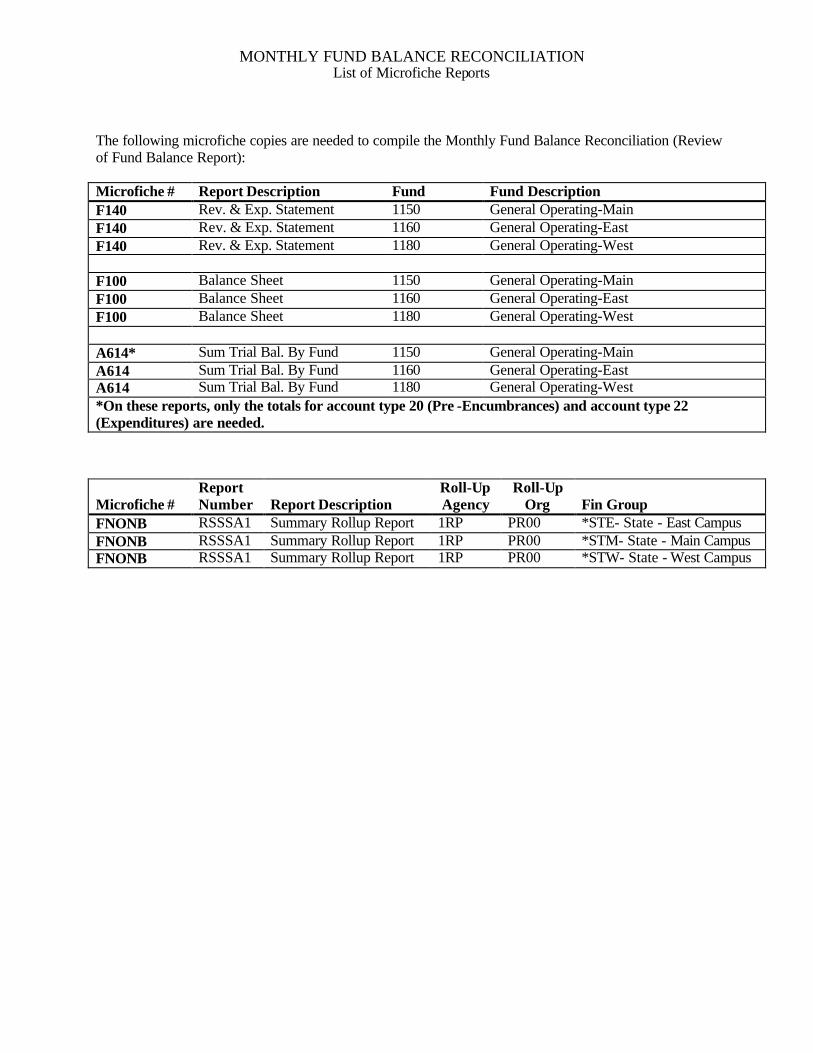

MONTHLY FUND BALANCE RECONCILIATION List of Microfiche Reports

The following microfiche copies are needed to compile the Monthly Fund Balance Reconciliation (Review of Fund Balance Report): Microfiche # Report Description Fund Fund Description F140 Rev. & Exp. Statement 1150 General Operating-Main F140 Rev. & Exp. Statement 1160 General Operating-East F140 Rev. & Exp. Statement 1180 General Operating-West F100 Balance Sheet 1150 General Operating-Main F100 Balance Sheet 1160 General Operating-East F100 Balance Sheet 1180 General Operating-West A614* Sum Trial Bal. By Fund 1150 General Operating-Main A614 Sum Trial Bal. By Fund 1160 General Operating-East A614 Sum Trial Bal. By Fund 1180 General Operating-West *On these reports, only the totals for account type 20 (Pre -Encumbrances) and account type 22 (Expenditures) are needed. Microfiche #

Report Number

Report Description

Roll-Up Agency

Roll-Up Org

Fin Group

FNONB RSSSA1 Summary Rollup Report 1RP PR00 *STE- State - East Campus FNONB RSSSA1 Summary Rollup Report 1RP PR00 *STM- State - Main Campus FNONB RSSSA1 Summary Rollup Report 1RP PR00 *STW- State - West Campus

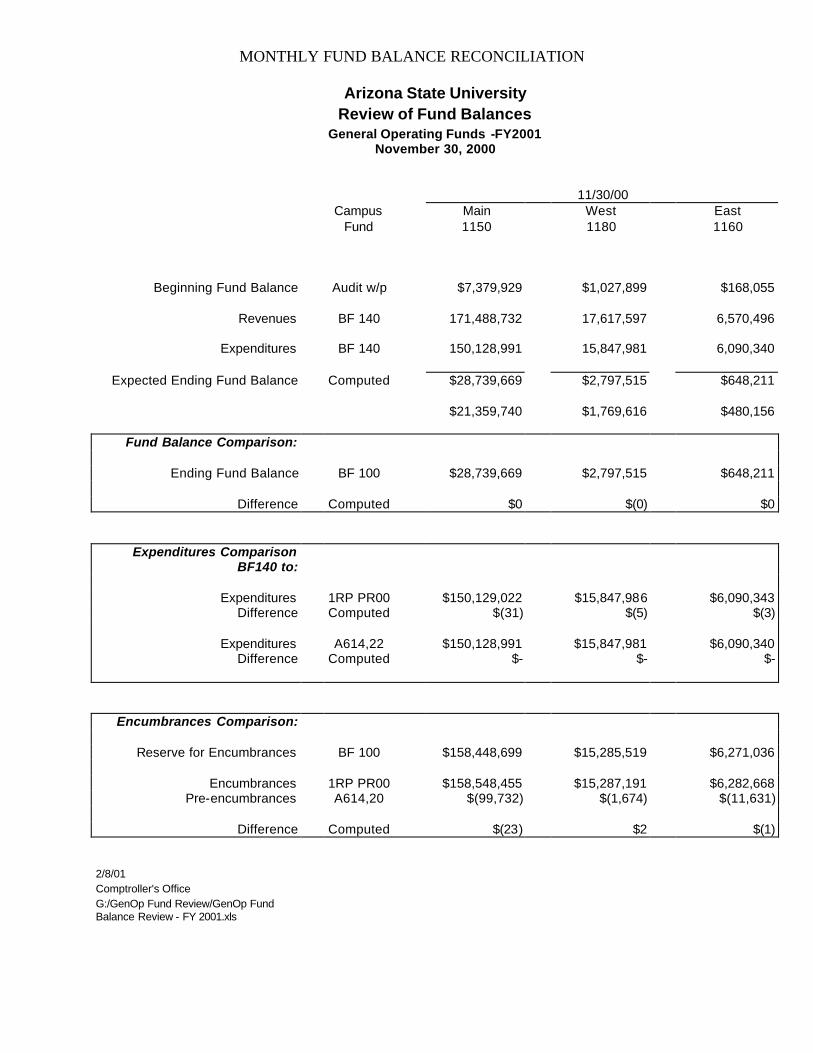

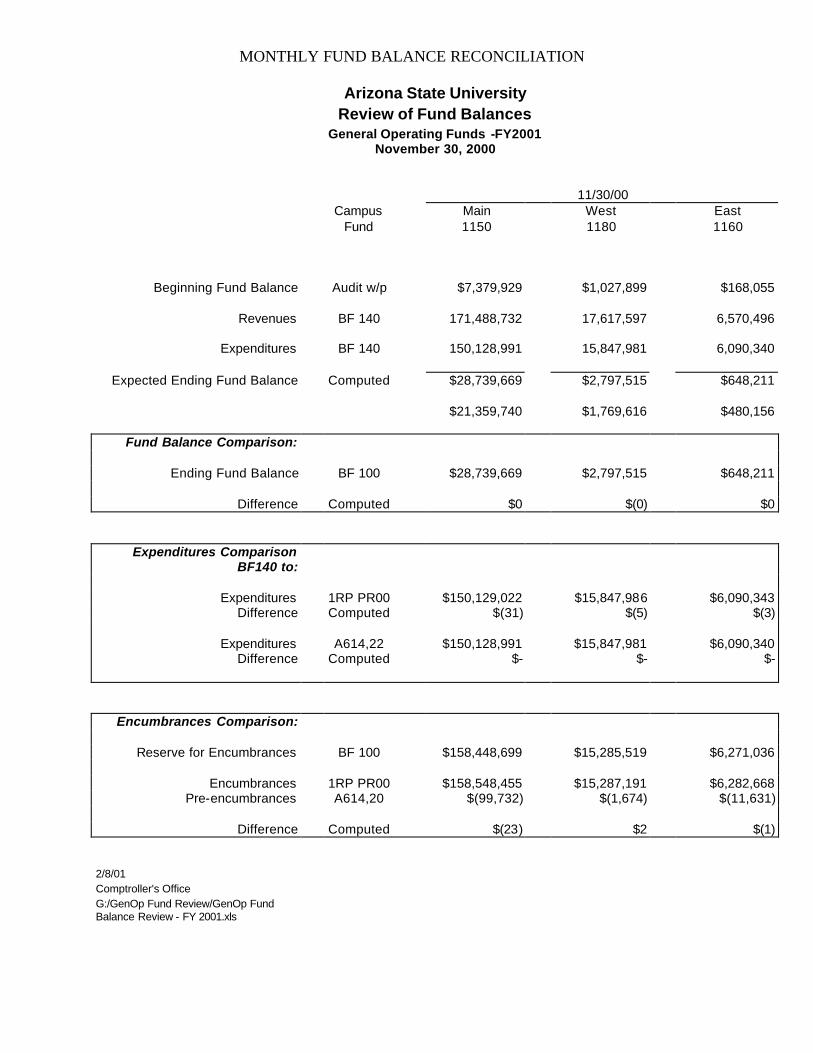

MONTHLY FUND BALANCE RECONCILIATION

Arizona State University

Review of Fund Balances General Operating Funds -FY2001

November 30, 2000 11/30/00 Campus Main West East Fund 1150 1180 1160

Beginning Fund Balance Audit w/p $7,379,929 $1,027,899 $168,055

Revenues BF 140 171,488,732 17,617,597 6,570,496

Expenditures BF 140 150,128,991 15,847,981 6,090,340

Expected Ending Fund Balance Computed $28,739,669 $2,797,515 $648,211 $21,359,740 $1,769,616 $480,156

Fund Balance Comparison:

Ending Fund Balance BF 100 $28,739,669 $2,797,515 $648,211

Difference Computed $0 $(0) $0

Expenditures Comparison BF140 to:

Expenditures 1RP PR00 $150,129,022 $15,847,986 $6,090,343

Difference Computed $(31) $(5) $(3)

Expenditures A614,22 $150,128,991 $15,847,981 $6,090,340 Difference Computed $- $- $-

Encumbrances Comparison:

Reserve for Encumbrances BF 100 $158,448,699 $15,285,519 $6,271,036

Encumbrances 1RP PR00 $158,548,455 $15,287,191 $6,282,668 Pre-encumbrances A614,20 $(99,732) $(1,674) $(11,631)

Difference Computed $(23) $2 $(1)

2/8/01 Comptroller's Office G:/GenOp Fund Review/GenOp Fund Balance Review - FY 2001.xls

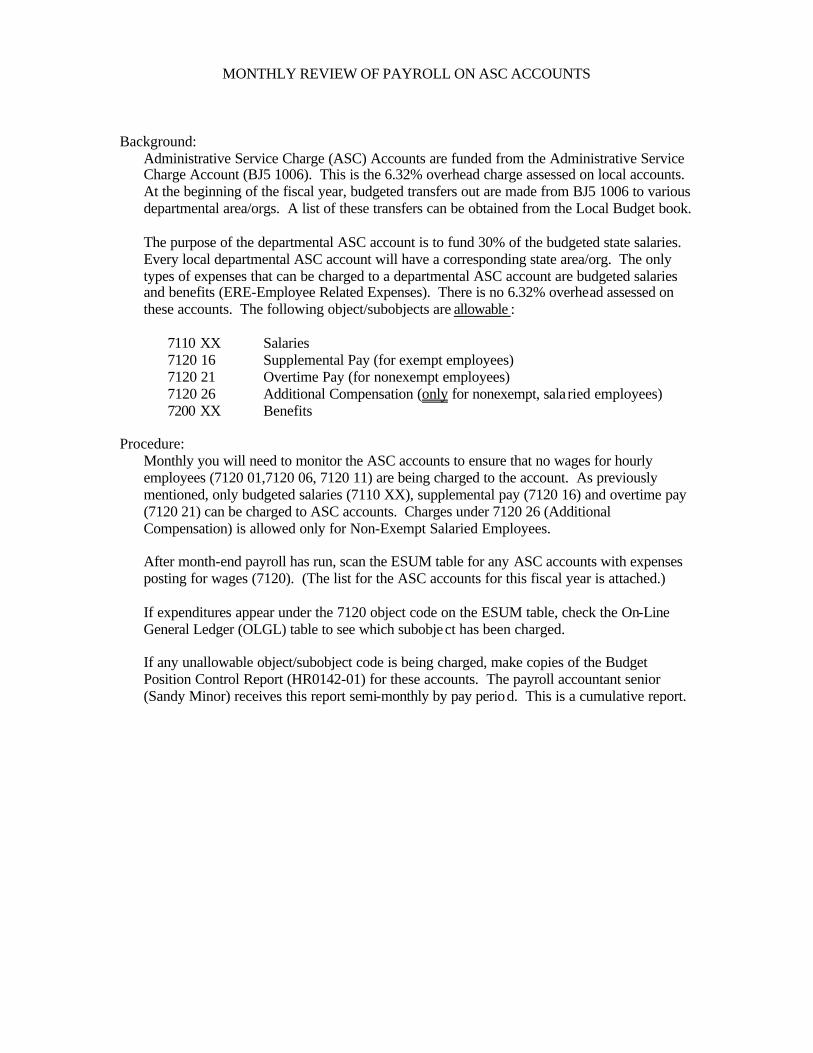

MONTHLY REVIEW OF PAYROLL ON ASC ACCOUNTS Background:

Administrative Service Charge (ASC) Accounts are funded from the Administrative Service Charge Account (BJ5 1006). This is the 6.32% overhead charge assessed on local accounts. At the beginning of the fiscal year, budgeted transfers out are made from BJ5 1006 to various departmental area/orgs. A list of these transfers can be obtained from the Local Budget book. The purpose of the departmental ASC account is to fund 30% of the budgeted state salaries. Every local departmental ASC account will have a corresponding state area/org. The only types of expenses that can be charged to a departmental ASC account are budgeted salaries and benefits (ERE-Employee Related Expenses). There is no 6.32% overhead assessed on these accounts. The following object/subobjects are allowable : 7110 XX Salaries 7120 16 Supplemental Pay (for exempt employees) 7120 21 Overtime Pay (for nonexempt employees) 7120 26 Additional Compensation (only for nonexempt, sala ried employees) 7200 XX Benefits

Procedure: Monthly you will need to monitor the ASC accounts to ensure that no wages for hourly employees (7120 01,7120 06, 7120 11) are being charged to the account. As previously mentioned, only budgeted salaries (7110 XX), supplemental pay (7120 16) and overtime pay (7120 21) can be charged to ASC accounts. Charges under 7120 26 (Additional Compensation) is allowed only for Non-Exempt Salaried Employees. After month-end payroll has run, scan the ESUM table for any ASC accounts with expenses posting for wages (7120). (The list for the ASC accounts for this fiscal year is attached.) If expenditures appear under the 7120 object code on the ESUM table, check the On-Line General Ledger (OLGL) table to see which subobject has been charged. If any unallowable object/subobject code is being charged, make copies of the Budget Position Control Report (HR0142-01) for these accounts. The payroll accountant senior (Sandy Minor) receives this report semi-monthly by pay period. This is a cumulative report.

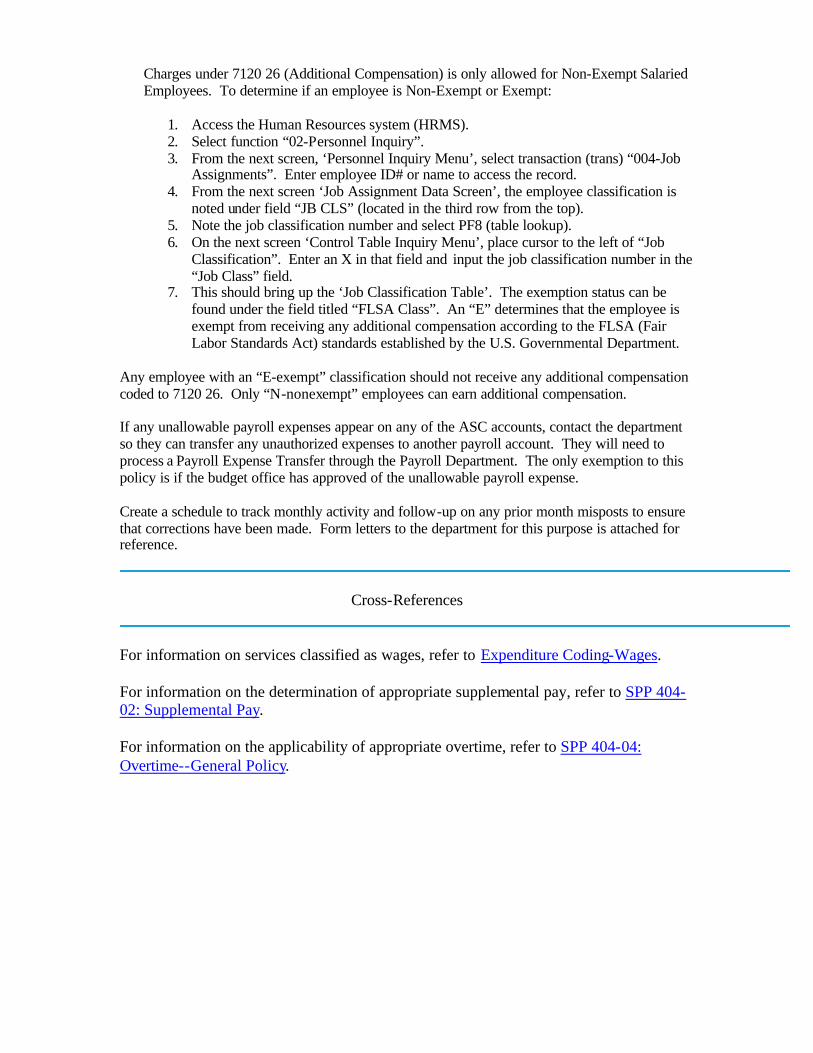

Charges under 7120 26 (Additional Compensation) is only allowed for Non-Exempt Salaried Employees. To determine if an employee is Non-Exempt or Exempt:

1. Access the Human Resources system (HRMS). 2. Select function “02-Personnel Inquiry”. 3. From the next screen, ‘Personnel Inquiry Menu’, select transaction (trans) “004-Job

Assignments”. Enter employee ID# or name to access the record. 4. From the next screen ‘Job Assignment Data Screen’, the employee classification is

noted under field “JB CLS” (located in the third row from the top). 5. Note the job classification number and select PF8 (table lookup). 6. On the next screen ‘Control Table Inquiry Menu’, place cursor to the left of “Job

Classification”. Enter an X in that field and input the job classification number in the “Job Class” field.

7. This should bring up the ‘Job Classification Table’. The exemption status can be found under the field titled “FLSA Class”. An “E” determines that the employee is exempt from receiving any additional compensation according to the FLSA (Fair Labor Standards Act) standards established by the U.S. Governmental Department.

Any employee with an “E-exempt” classification should not receive any additional compensation coded to 7120 26. Only “N-nonexempt” employees can earn additional compensation. If any unallowable payroll expenses appear on any of the ASC accounts, contact the department so they can transfer any unauthorized expenses to another payroll account. They will need to process a Payroll Expense Transfer through the Payroll Department. The only exemption to this policy is if the budget office has approved of the unallowable payroll expense. Create a schedule to track monthly activity and follow-up on any prior month misposts to ensure that corrections have been made. Form letters to the department for this purpose is attached for reference.

Cross-References

For information on services classified as wages, refer to Expenditure Coding-Wages. For information on the determination of appropriate supplemental pay, refer to SPP 404-02: Supplemental Pay. For information on the applicability of appropriate overtime, refer to SPP 404-04: Overtime--General Policy.

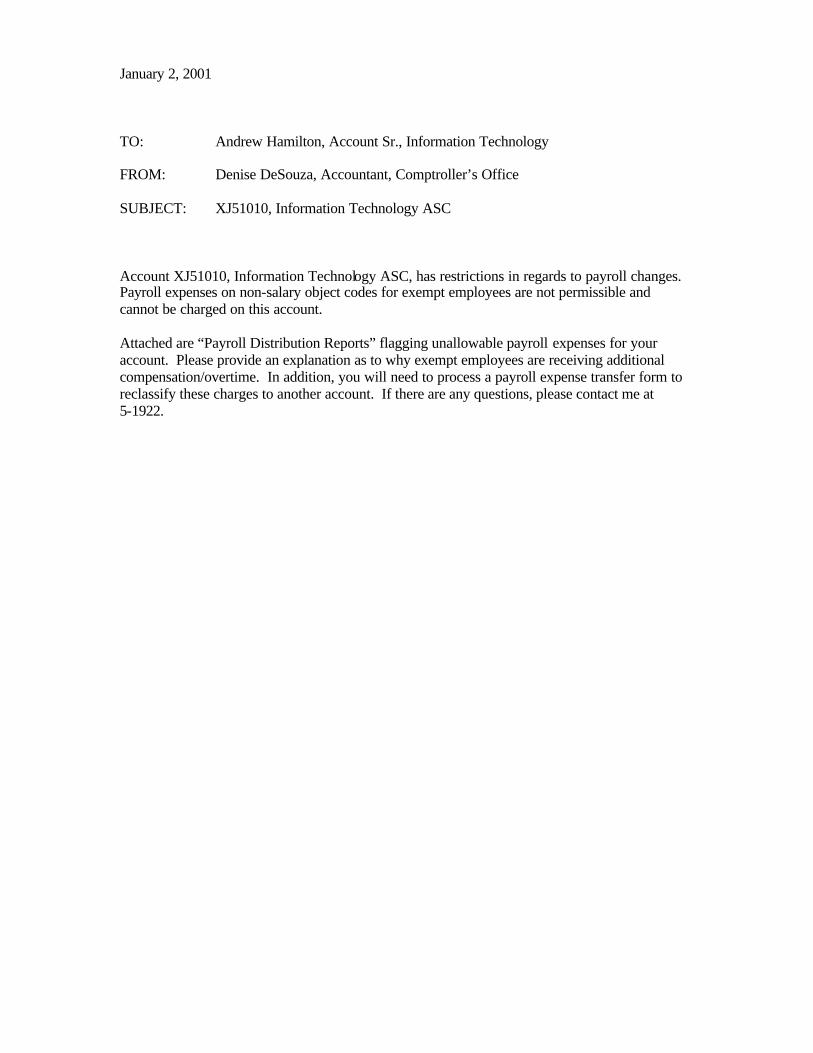

January 2, 2001 TO: Andrew Hamilton, Account Sr., Information Technology FROM: Denise DeSouza, Accountant, Comptroller’s Office SUBJECT: XJ51010, Information Technology ASC Account XJ51010, Information Technology ASC, has restrictions in regards to payroll changes. Payroll expenses on non-salary object codes for exempt employees are not permissible and cannot be charged on this account. Attached are “Payroll Distribution Reports” flagging unallowable payroll expenses for your account. Please provide an explanation as to why exempt employees are receiving additional compensation/overtime. In addition, you will need to process a payroll expense transfer form to reclassify these charges to another account. If there are any questions, please contact me at 5-1922.

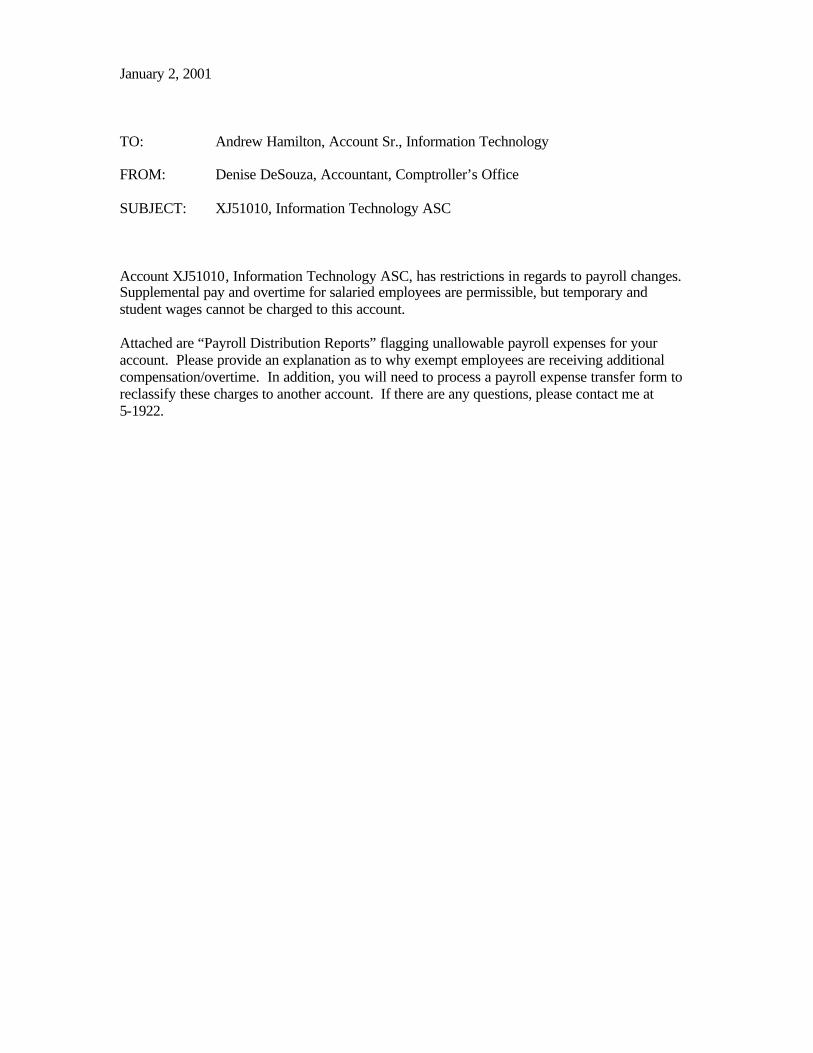

January 2, 2001 TO: Andrew Hamilton, Account Sr., Information Technology FROM: Denise DeSouza, Accountant, Comptroller’s Office SUBJECT: XJ51010, Information Technology ASC Account XJ51010, Information Technology ASC, has restrictions in regards to payroll changes. Supplemental pay and overtime for salaried employees are permissible, but temporary and student wages cannot be charged to this account. Attached are “Payroll Distribution Reports” flagging unallowable payroll expenses for your account. Please provide an explanation as to why exempt employees are receiving additional compensation/overtime. In addition, you will need to process a payroll expense transfer form to reclassify these charges to another account. If there are any questions, please contact me at 5-1922.

ASC Accounts - FY 2001 Review:____________

AK5 1001 News Bureau BJ5 1005 President's Office CG5 1004 Purchasing CG5 1005 Purchasing Info Systems CG5 1007 Receiving Operations DT5 1001 EEO/Affirmative Action EX5 1004 Development Office FA5 1002 Academic & Administrative Docs FA5 1006 Senior Vice Pres./Provost FA5 1030 Continuous Improvement Initiative HE5 1001 General Counsel Office HG5 1002 Community Relations JC5 1013 Facilities Plan & Construct. JC5 1014 Facilities Mgmt Computer Support JC5 1015 Facilities Mgmt Program Support JC5 1016 Facilities Mgmt Gen & Supv. JW5 1003 Public Safety JW5 1009 Public Safety Info Systems JW5 1011 Academic Building Security JW5 1013 COPS Grant KT5 1019 HR-Office KT5 1023 HR-Compensation KT5 1025 HR-Employee Asst. Program KT5 1027 HR-Career Enrichment KT5 1028 HR-Employee Orientation KT5 1029 HR-Service Center KT5 1030 HR-Computer Technology KT5 1032 HR-Partners KT5 1033 HR-Employee Development KV5 1001 Fiscal Plan & Analysis MN5 1002 Univ. Telecommunications MN5 1003 Data Communication RK5 1002 Risk Management RV5 1001 Mailroom Services TC5 1001 Institutional Analysis TC5 1003 Data Administration TN5 1005 Property Control TN5 1011 Surplus Property WG5 1001 Academic Facilities Mgmt WV5 1014 Comptroller Office WV5 1019 Comptroller Office Information Systems WY5 1003 Vice Provost Admin Services WY5 1009 Internal Audit & Mgmt Services XG5 1003 Alumni Association XJ5 1010 Information Technology XJ5 1011 Admin Information Tech. YT5 1003 Institutional. Advancement--Vice President YT5 1011 Institutional Advancement--Info. Resource Mgmt.

CLEAR REJECTED ASC JV’S Background:

ASC JV’s are system generated journal entries that assess the current ASC (Administrative Services Charge) of 6.32% on local/agency orgs for expenditures incurred during the month. (For more information regarding ASC charges, please refer to the COM Manual Section 206). Rejected ASC JV’s occur for reasons such as a deficit in funds on the account being charged.

Procedure:

Check the Suspense Table (SUSF) for JV’s with the status of “REJCT” on the day of month end closing and the day after month end closing.

The Rejected ASC JV’s are identified with a document type of “JV” and an agency type of “OAC”. These rejected JV’s need an override applied for them to post. To apply the override on a JV:

1. In the “Action” field, type is “S”, scroll down to the rejected JV and hit enter. This

should open the document for editing. 2. Once the document is opened, in the function field, type in “OV”, hit enter and the F7

to process the document. 3. The document status should now reflect “ACCPT” instead of “REJCT”. 4. Hit the F3 key to exit this document. 5. Continue this process until all the ASC JV’s reflect an “ACCPT” status. 6. ASC JV’s that will not accept will need further research on the accounts being

assessed ASC. For example, account being assessed ASC could be closed.

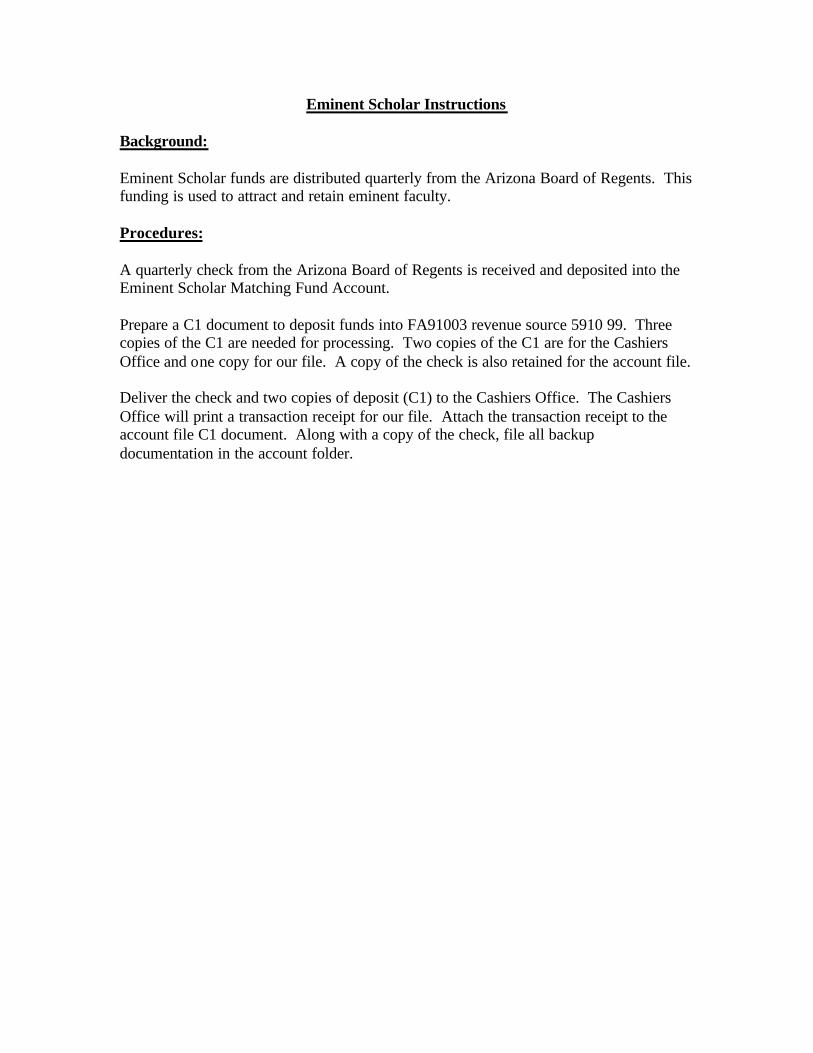

Eminent Scholar Instructions

Background: Eminent Scholar funds are distributed quarterly from the Arizona Board of Regents. This funding is used to attract and retain eminent faculty. Procedures: A quarterly check from the Arizona Board of Regents is received and deposited into the Eminent Scholar Matching Fund Account. Prepare a C1 document to deposit funds into FA91003 revenue source 5910 99. Three copies of the C1 are needed for processing. Two copies of the C1 are for the Cashiers Office and one copy for our file. A copy of the check is also retained for the account file. Deliver the check and two copies of deposit (C1) to the Cashiers Office. The Cashiers Office will print a transaction receipt for our file. Attach the transaction receipt to the account file C1 document. Along with a copy of the check, file all backup documentation in the account folder.

Foreign Travel Report Instructions Background: All foreign travel is reported on a quarterly basis to State Risk Management. University employees who travel on authorized university business outside of the United States have liability insurance and worker’s compensation coverage provided through the university’s self insurance administrator, the State of Arizona Department of Administration, Risk Management Section, in accordance with state law. Procedures: The systems area downloads foreign travel data and a database file is forwarded to general accounting on a monthly basis. The foreign travel report is located in the General Accounting drive under the file folder “Foreign Travel Report”. Open the monthly download file from the systems area and copy ‘text only’ and paste the information in the current month’s spreadsheet. Delete any unneeded columns and rearrange the remaining columns. The foreign travel data should be sorted by name of traveler. Once sorted, review the spreadsheet for any description fields with ‘Other’. Change ‘Other’ in the description field to ‘Meetings, Conference’. A traveler may have more than one transaction line. Review for any duplicate lines and delete the duplicate lines. Certain information may have been omitted from the original transaction. Any missing information can be found in Advantage OTH1 table and fill in the missing information on the report. Research any items that appear incorrect and prepare a JV to make corrections. At the end of each quarter, combine each month in the quarterly spreadsheet for report submission. Prepare an internal memo letterhead with the report and submit the report to Cheryl Carlyle in Risk Management. Place a copy of the report in the foreign travel file.

GIFT IN KIND (GIK) RECONCILIATION Background:

The Gift In Kind Reconciliation, done quarterly, compares ASU Foundation records to those maintained by Property Control. ASU Foundation sends documentation to Property Control of new gifts. Property Control has the items tagged and then inputs the gift into Advantage. These gifts are posted to KS61001 and ET51009 under revenue code 534008.

Procedure:

• When month end closing is complete for the quarter, contact Deborah Monninger at ASU Foundation for the “Gift in Kind Download”.

• Copy microfiche (BA611RC) for ET51009 and KS61001, revenue source 5340 and highlight the items with sub rev 08.

• Compare microfiche to the download received from ASU Foundation. • If item is on microfiche but not on the ASU Foundation download, have student worker

pull and copy those JV’s. (JV’s are located in Fran Matzdorff’s office in ADM B, Rm. 160, ext 5-1577) Send copies of JV’s to Deborah and have her investigate.

• If dollar amount is not on microfiche, means JV has not been posted – put on reconciliation.

• Contact Fran Rynne-Matzdorff at Property Control and have her investigate those items that are not posted on the Microfiche. (Deborah at Foundation verifies that all the items on the download have been received by Property Control before they are sent.)

Cross-References

For information on in-kind gifts, refer to COM 303: Gift Deposits.

MONTHLY FUND BALANCE RECONCILIATION Background: The monthly fund balance reconciliation purpose is to:

1) compare the fund balance on the balance sheet to the income statement are equal, 2) compare the expenditures on the income statement to the rollup report and trial balance report, 3) and, compare the encumbrances on the balance sheet to rollup report and trial balance report. A list of the various reports needed to compile this report and their related description is attached.

Procedure: After month-end Advantage processing has run, copy the microfiches on the attached list. The blank spreadsheet to input the information can be found on G:/GenOp Fund Review/GenOp Fund Balance Review. (There is one file for this fiscal year with worksheets within that file for the specific months.) The same procedure should be followed for each campus: main, west and east.

I. For the comparison of fund balance between the income statement and the balance sheet:

From Report F140 (Statement of Revenue and Expenses), note the ‘Total Revenues’ and “Total Expenses’ amount under the “Fiscal Year-to-Date” column (items highlighted in green on the example report). Input the total revenue amount into row 15 of the spreadsheet and the total expenses amount into row 17.

From Report F100 (Balance Sheet), compute the Ending Fund Balance (row 25) by totaling the lines referenced.

The difference between these two reports are automatically computed and is reflected in row 27, which should have a zero balance..

II. To compare the expenditures on the income statement to the rollup report and trial balance report:

From the Summary Rollup Report (RSSSA1), note the total expended amount under the Year-to-Date column (highlighted in purple). Input this amount into row 32 of the spreadsheet. From the Summary Trial Balance Report (A614), note the total amount under account type 22 (expenditures) under the Ending Balance column (highlighted in yellow). Input this amount into row 35 of the spreadsheet. The differences are automatically computed. The difference of a minor amount is immaterial.

III. For the comparison between the encumbrances on the balance sheet to rollup report and trial balance report:

From Report F100 (Balance Sheet), compute the Reserve for Encumbrances (row 42) by totaling the lines referenced. From the Summary Rollup Report (RSSSA1), note the total encumbered amount under the Year-to-Date column (highlighted in pink). Input this amount into row 44 of the spreadsheet. From the Summary Trial Balance Report (A614), note the total amount under account type 20 (pre-encumbrances) under the Ending Balance column (highlighted in yellow). Input this amount into row 45 of the spreadsheet. The differences are automatically computed. The difference of a minor amount is immaterial.

MONTHLY FUND BALANCE RECONCILIATION List of Microfiche Reports

The following microfiche copies are needed to compile the Monthly Fund Balance Reconciliation (Review of Fund Balance Report): Microfiche # Report Description Fund Fund Description F140 Rev. & Exp. Statement 1150 General Operating-Main F140 Rev. & Exp. Statement 1160 General Operating-East F140 Rev. & Exp. Statement 1180 General Operating-West F100 Balance Sheet 1150 General Operating-Main F100 Balance Sheet 1160 General Operating-East F100 Balance Sheet 1180 General Operating-West A614* Sum Trial Bal. By Fund 1150 General Operating-Main A614 Sum Trial Bal. By Fund 1160 General Operating-East A614 Sum Trial Bal. By Fund 1180 General Operating-West *On these reports, only the totals for account type 20 (Pre -Encumbrances) and account type 22 (Expenditures) are needed. Microfiche #

Report Number

Report Description

Roll-Up Agency

Roll-Up Org

Fin Group

FNONB RSSSA1 Summary Rollup Report 1RP PR00 *STE- State - East Campus FNONB RSSSA1 Summary Rollup Report 1RP PR00 *STM- State - Main Campus FNONB RSSSA1 Summary Rollup Report 1RP PR00 *STW- State - West Campus

MONTHLY FUND BALANCE RECONCILIATION

Arizona State University

Review of Fund Balances General Operating Funds -FY2001

November 30, 2000 11/30/00 Campus Main West East Fund 1150 1180 1160

Beginning Fund Balance Audit w/p $7,379,929 $1,027,899 $168,055

Revenues BF 140 171,488,732 17,617,597 6,570,496

Expenditures BF 140 150,128,991 15,847,981 6,090,340

Expected Ending Fund Balance Computed $28,739,669 $2,797,515 $648,211 $21,359,740 $1,769,616 $480,156

Fund Balance Comparison:

Ending Fund Balance BF 100 $28,739,669 $2,797,515 $648,211

Difference Computed $0 $(0) $0

Expenditures Comparison BF140 to:

Expenditures 1RP PR00 $150,129,022 $15,847,986 $6,090,343

Difference Computed $(31) $(5) $(3)

Expenditures A614,22 $150,128,991 $15,847,981 $6,090,340 Difference Computed $- $- $-

Encumbrances Comparison:

Reserve for Encumbrances BF 100 $158,448,699 $15,285,519 $6,271,036

Encumbrances 1RP PR00 $158,548,455 $15,287,191 $6,282,668 Pre-encumbrances A614,20 $(99,732) $(1,674) $(11,631)

Difference Computed $(23) $2 $(1)

2/8/01 Comptroller's Office G:/GenOp Fund Review/GenOp Fund Balance Review - FY 2001.xls

Monthly Prohibited State Transactions

Background: Certain disbursement transactions are prohibited on state accounts according to University policy, COM 401–03: Prohibited Transactions. Included in these prohibited transactions are expenses for food (7390 06), interest (7390 01), and student support (7700). The purpose of “The Monthly Prohibited State Transactions Report” is to periodically monitor all state accounts for Main (1150), East (1160), and West (1180) campuses for any expenses that fall into the restricted categories, so that they can be re-coded or transferred off state accounts. Procedure:

• Run a query on the data warehouse to include these fields: Account Acceptance Date and/or Fiscal Month Transaction Document Code Transaction Number Fund Account Type Line Description Expenditure Code $ Amount

• Of these fields, the following will need to be limited:

Fund Code: 1150, 1160, 1180 Account Type Code: 22, 23, 24 Expenditure Code: 739001, 739006, 7700XX

• Copy query information into a spreadsheet program and arrange in report format.

• Identify transactions that need to be corrected and forward

copies of the report to the corresponding accountant.

• Place a final copy of the monthly report in the Prohibited Transaction Binder.

Cross-References

For information on student support, refer to COM 422–01: Student Financial Support For information on food policies and procedures, refer to COM 420–02: Business Meals, Food Expenses

MONTHLY REVIEW OF SPECIAL CLASS FEES PROCEDURES

Under Board of Regent’s policy, special class fees and deposits may be imposed only for expenses necessary for the successful completion of course objectives. Such necessary fees and deposits are limited to charges for:

1. off-campus field trip expenses 2. specialized use of equipment or facilities 3. private instruction 4. expendable materials 5. technology expense fees 6. models and 7. deposits

Expenses and revenues are restricted on class fees accounts. Therefore, only certain object and revenue codes are set up on class fees accounts.

Revenue Codes 5000 – carry forward balance 5220 – other student fees Object Codes 7310 – services 7320 – materials and supplies 7325 – non-capital equipment 7330 – communications 7340 – rentals/licenses 7390 – miscellaneous 7510 – travel/in state 7520 – travel/out of state 7530 – travel/foreign 7900 – carry forward deficit

REVIEW PROCEDURES:

- run brio query for expenditures for each campus(fund 5910,5920, 5960) for month/s you want to review. List FY, period, transaction code, transaction number, reference code, reference number, accept date, document description, line description, acct type, fund, account, sub-org, expenditure code, description, and amount.

- run brio query for revenue for each campus for month/s you want to review. List FY, period, transaction code, transaction number, reference code, reference number, accept date, document description, line description, acct type, fund, account, sub-org, revenue code, description, and amount.

- export each query into an excel document

- open excel document and sort by ‘fund’, then by ‘account’ then by ‘expenditure’ or ‘revenue code’

- review object/revenue codes for appropriateness/allowability - review line description for appropriateness/allowability - contact department for explanation of any expenditures/revenues that are

questionable - transfer off any unallowable expenditures/revenues

State Cash Reconciliation

State cash transaction information is entered into The Arizona Financial Information System (AFIS) on a monthly basis. AFIS is the primary comprehensive statewide accounting and financial Management information system. This reconciliation ensures that the transactions entered reconcile to ASU’s internal accounting records. As a part of internal control this reconciliation is required to be documented, (Authority A.R.S. 35-131; 41-722). To ensure proper controls, the reconciliation should be completed by an individual who is separate from the preparation and entry of the transactions.

1. Copy DAFR 7470 off the state microfiche for the proper period. 2. Copy Microfiche A611B (Detail Trial Balances by Balance Sheet) for the balance sheet

account 1000 for funds: 1150, 1160, and 1180. 3. Go onto the General Accounting drive and find the folder named “FY XX Payins”

(XX—current fiscal year), then find the Excel file “Pay In FY XX” (or titled “Schedule of Collection Pay Ins) print a clean copy. From the totals by campuses subtract any activity that happened in the current month, detailed out in the body of the paper.

4. Pull the state microfiche that coincides with this page. This includes, but is not limited to:

DAFR 7470 Exp: Rev: 11000 13000 15000 16000 16000 16000 1411 1411 1411 1411 1411 1411 1411 1411 1411 1411 1411 1411 0001 0002 0003 0001 0002 0003 0011 0011 0011 0007 0007 0007

5. On the DAFR 7470 compare the Cash Rev/Exp Oper Trsf column to the Schedule of

Collections Pay Ins. See schedule A for example of how to tie documents. (numbers represent individual items, letters signify sums and totals). Follow this for Main, East, and West campuses.

6. To reconcile the A611B compare the revenues and expenditures by campus. The revenue comes from the totals by campus on the Schedule of Collections Pay Ins, which ties to the state microfiche at the organizational level. See attachment B.

7. The expense side of each campus comes from the state microfiche collections (Appropriation Numbers: 11000, 13000, 15000) look at “Organizational LVL”. See Attachment C.

8. Finally, the “Schedule of State Expenditure by State Program” by campus needs to be reconciled. Compare the AFIS fiche (Main campus lump sum appropriation-general fund) to the Excel spreadsheet. Each campus is divided into seven areas:

• Instruction 1000 • Research 2000 • Public service 3000 • Academic Support 4000 • Student Services 5000

Appropriation Number Appropriation Fund Fund Org Level Program Level

• Institutional Support 6000 • Collections 7000

Terms and Cross References: Funds 1411-Collections Funds 1100-general Fund Appropriation Numbers 16000- Revenue Collector

SUMMER SESSION MIR Summer Sessions MIR is prepared monthly during the period August through December. The December MIR is the only one that is issued. The other months are for informational purposes for the Summer Session office. The summer session reporting period is calendar year, which means our information comes from two fiscal years, periods 7 through 12 in the previous fiscal year and periods 1 through 6 in the current fiscal year. Queries have been set up in Access and there are two databases. One database for the summer session funds 4110 and 4111 and one database for the residual fund 4112. The Summer Sessions MIR report consists of three separate reports: Statement of Revenues, Expenditures and Changes in Fund Balance (103.1), Summary of College Residual Accounts Activity (103.2), and Schedule of Waivers (103.3).

Database for 4110/4111 This database consists of a “Make Table” where information is “appended” each month for updating the monthly information. There are two append queries. One query is for appending information from January through June and is used once throughout the whole reporting period. The other query is to append data on a monthly basis; however, it is also used to append the data for July through August for the first reporting month. To append data monthly, open the query in the design view. Change the fiscal month criteria to the current month that you are reporting through, for example, for the reporting period January through September, the period would be “3”. Save changes, then run the query. Once the query has run, you will get a message that will say, “you are about to append XXXX rows”. Click yes and your table has been updated. Run each of the other queries and export them into Excel by clicking on “tools”, “office links”, and “analyze it with MS Excel”. Once the report is in Excel, change the headings, summarize the report, and print the report. The list of queries to run are:

Revenue Sum Personal Services ERE Operations ASC ADMINEXP

The information from the queries are reported in the Statement of Revenues, Expenditures, and Changes in Fund Balance (103.1).

Database for Residual Fund This table is updated the same way as the Database for 4110/4111. The list of queries to run are:

Revenue Transfer In Sum Transfer In 00 Transfer In 99 Transfer Out Personal Services ERE Operations

The information from the queries are reported in the Summary of College Residual Accounts Activity (103.2).

Schedule of Waivers (103.3) This information comes from the A440A for the current year’s remission waiver revenue summer sessions account, which starts with ET4 12XX. The list of function codes can be found on the Advantage function table. The Function code will describe which category the waiver falls under. Other information needed to prepare the report are: F100 for funds 4110, 4111, 4112 611E for the current year account RF4 10XX, example RF4 1099. This is to find the transfers out information. Budget Book page for RF4 10XX. Occupancy Charge JV must be processed as soon as possible (September or October). Also, there should not be any major changes to the report from October to December. If there are major changes to the expenditures or revenue, we must notify Carol Switzer. Once the report is complete, a copy of the reports and a copy of the back up queries for 103.1 are sent to Carol Switzer. Only the December MIR is issued.

Other Summer Session Duties

• Process Transfers-in June and December of each year The Summer Sessions Office will send requests to transfer funds. The accountant should process the request. Copies of these transfers should be sent to the Summer Sessions office as well as placed in the current Summer Sessions Binder.

• Set up new accounts -Since Summer Sessions bases it’s reporting period off of the calendar year rather than the fiscal year, new accounts will need to be set up after December 31st for the next year. Administrative Summer Session accounts for Main, West, and Eat campuses will need to be set up manually by the accountant immediately after December 31st. The budget load information should be requested from Summer Sessions (Carol Switzer) and approved by The Provost’s Office (Lynn Carpenter) before the budgets are loaded. --Note: The fund and account numbers will be even for the even years and odd for the odd years (i.e. 4110/4111). The rest of the Summer Sessions accounts will be set up and the budgets loaded by the Systems area. Summer Sessions will need to provide the budget load information before this can be done. The accountant will need to coordinate between the two areas in order to get the new accounts set up.

• Create new Binders-Set up new binders for each new Summer Session Year.

Tuition and MIR Work Paper Instructions

The Tuition and MIR Work Papers are the last of the work papers to be completed. This is because data from the General, Endowment, Auxiliary, Designated, and Restricted work papers is needed to complete the Tuition and MIR Work Papers. Once the tuition and MIR data is collected from the various sources, it is compiled into a schedule that ties directly to the financials. 1. Copies of the following will need to be obtained:

Reports from microfiche (A440A) for period ending June 30th

Main Campus ET1 1016-Remission/Waiver Revenue ET1 1017-Gen Operating Collections ET5 1006-Local Collections East Campus

CB1 7023-ASU East Waivers Revenue CB1 7021-ASUE Collections Revenue CB5 7001-ASUE Local Collections West Campus CA1 5003-ASU West Waivers Revenue CA1 5001-ASUW Collections Revenue CA5 5001-ASUW-Local Collections

Documents from other work papers

General Operating Schedule A (Main, East, and West) Resident and Non-Resident Tuition Waiver Reclassification Entries Endowment Statement of Changes in Fund Balance-Combined (E-2) Auxiliary Combined Statement of Rev, Expenditures. & Changes in Fund Bal. (A-4) Designated Stmt of Curr Oper Funds & Expenditures by Prog (DR/2) Reclassification Entries (D/RJE-M) Restricted Combined Statement of Changes in Fund Balance (R-2) 2. The tuit_mirxx file can be found on the General Operating drive in

Excel in the folder titled “year end XX.” Open the file from the previous year and save it into the new year end folder. Schedules O-20, O-21, O-22, and O-24 in the tuit_mir file contain information for more than one fiscal year. Copy and move the information from the previous fiscal year over to the left to make room for the new year’s information (be careful not to alter formulas).

3. For each microfiche report, calculate the total Resident and Non-

Resident tuition separately for Spring and Fall semesters. Also separate out the College of Business MBA fees and the Law fees.

4. Data will only need to be entered into the blue highlighted cells. Data is entered from the microfiche and work paper sources as documented in the work copy. NOTE: schedule O-23 requires no entries. Its calculations are derived from the O-23 backup worksheet. Certain cells in the O-23 backup may have a –1 or +1 in the formula to compensate for rounding errors. These should initially be removed and can be added back where necessary.

5. Upon completion the amounts from each work sheet should all tie to each other. Amounts should also match totals on the “Statement of Current Operating Funds Revenues, Expenditures, and Other Changes.”—See example included with work copy.

State Cash Reconciliation

State cash transaction information is entered into The Arizona Financial Information System (AFIS) on a monthly basis. AFIS is the primary comprehensive statewide accounting and financial Management information system. This reconciliation ensures that the transactions entered reconcile to ASU’s internal accounting records. As a part of internal control this reconciliation is required to be documented, (Authority A.R.S. 35-131; 41-722). To ensure proper controls, the reconciliation should be completed by an individual who is separate from the preparation and entry of the transactions.

1. Copy DAFR 7470 off the state microfiche for the proper period. 2. Copy Microfiche A611B (Detail Trial Balances by Balance Sheet) for the balance sheet

account 1000 for funds: 1150, 1160, and 1180. 3. Go onto the General Accounting drive and find the folder named “FY XX Payins”

(XX—current fiscal year), then find the Excel file “Pay In FY XX” (or titled “Schedule of Collection Pay Ins) print a clean copy. From the totals by campuses subtract any activity that happened in the current month, detailed out in the body of the paper.

4. Pull the state microfiche that coincides with this page. This includes, but is not limited to:

DAFR 7470 Exp: Rev: 11000 13000 15000 16000 16000 16000 1411 1411 1411 1411 1411 1411 1411 1411 1411 1411 1411 1411 0001 0002 0003 0001 0002 0003 0011 0011 0011 0007 0007 0007

5. On the DAFR 7470 compare the Cash Rev/Exp Oper Trsf column to the Schedule of

Collections Pay Ins. See schedule A for example of how to tie documents. (numbers represent individual items, letters signify sums and totals). Follow this for Main, East, and West campuses.

6. To reconcile the A611B compare the revenues and expenditures by campus. The revenue comes from the totals by campus on the Schedule of Collections Pay Ins, which ties to the state microfiche at the organizational level. See attachment B.

7. The expense side of each campus comes from the state microfiche collections (Appropriation Numbers: 11000, 13000, 15000) look at “Organizational LVL”. See Attachment C.

8. Finally, the “Schedule of State Expenditure by State Program” by campus needs to be reconciled. Compare the AFIS fiche (Main campus lump sum appropriation-general fund) to the Excel spreadsheet. Each campus is divided into seven areas:

• Instruction 1000 • Research 2000 • Public service 3000 • Academic Support 4000 • Student Services 5000

Appropriation Number Appropriation Fund Fund Org Level Program Level

• Institutional Support 6000 • Collections 7000

Terms and Cross References: Funds 1411-Collections Funds 1100-general Fund Appropriation Numbers 16000- Revenue Collector

State Expenditures Reclassification This report is prepared to reclassify the state expenditures. Procedures:

• Run queries per “AFIS Monthly Expense Entries” procedures. • Subtotal each expense classification by campus. • For services, highlight and subtotal, for each function, the sub objects listed on the

Expense Entries procedures. • For operations, subtract from each function subtotal the services subtotal for that

function. • East campus is reported as one total and is not broken down by function. • Capital amounts are less the library amounts, and library amounts should be under

function 4000 only. • ERE is figured by taking (function personnel services divided by total personnel services)

multiplied by the total ERE amount. • Enter amounts rounded to the nearest 100. • Compare your subtotals for each expense classification and the total to the appropriate

campus roll-up report. • Compare the subtotal of each function to the Breakdown by Function query. You will

need to take the amount for each function from the query and add-in the ERE amount you figured to see if the amounts are close. For function 6000, subtract out the entire ERE amount for the campus and then add back in the amount of ERE figured for that function.

• From the Pay-In spreadsheet, take an appropriate amount of personnel services and ERE from function 1000 to get as close to the total amount paid in per campus for the year-to-date total without going over. Whatever amount you choose for personnel services, use 15% of that number for the ERE amount. The year-to-date amount of the personnel services and ERE cannot go over the total amount paid in on the Pay-In spreadsheet for each campus.

• Use the roll-up reports to verify the year-to-date numbers are on track for each expense category and for the total.

• Each month, add the previous year’s year-to-date numbers to the spreadsheet for an accurate comparison of expenses from year to year for each function expense category.

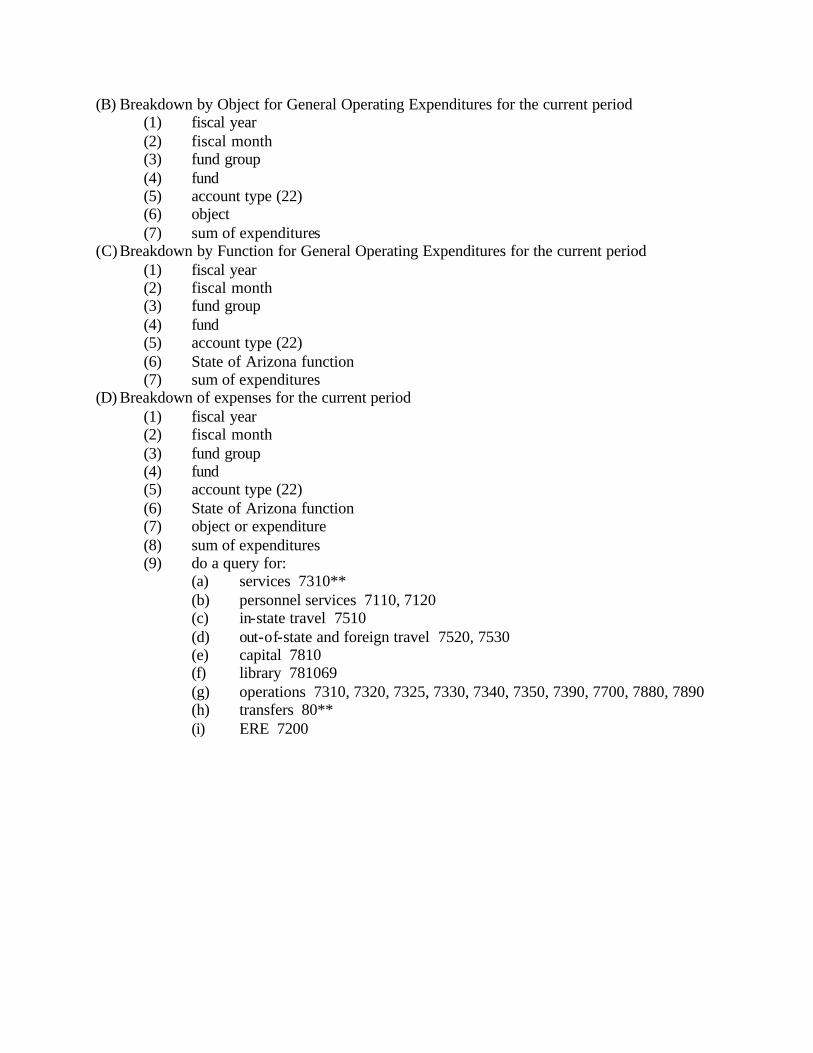

AFIS Monthly Expense Entries Queries:

(A) Total General Operating Expenditures for the current period (1) fiscal year (2) fiscal month (3) fund group (4) fund (5) account type (22) (6) sum of expenditures

(B) Breakdown by Object for General Operating Expenditures for the current period (1) fiscal year (2) fiscal month (3) fund group (4) fund (5) account type (22) (6) object (7) sum of expenditures

(C) Breakdown by Function for General Operating Expenditures for the current period (1) fiscal year (2) fiscal month (3) fund group (4) fund (5) account type (22) (6) State of Arizona function (7) sum of expenditures

(D) Breakdown of expenses for the current period (1) fiscal year (2) fiscal month (3) fund group (4) fund (5) account type (22) (6) State of Arizona function (7) object or expenditure (8) sum of expenditures (9) do a query for:

(a) services 7310** (b) personnel services 7110, 7120 (c) in-state travel 7510 (d) out-of-state and foreign travel 7520, 7530 (e) capital 7810 (f) library 781069 (g) operations 7310, 7320, 7325, 7330, 7340, 7350, 7390, 7700, 7880, 7890 (h) transfers 80** (i) ERE 7200

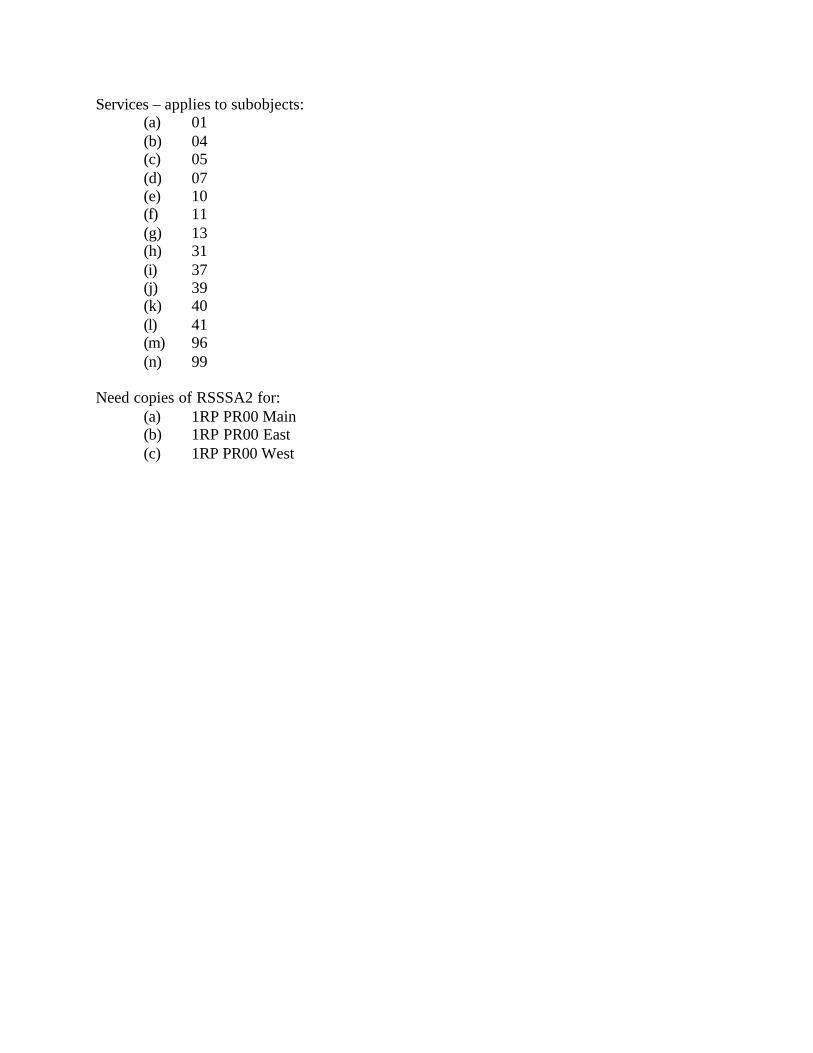

Services – applies to subobjects: (a) 01 (b) 04 (c) 05 (d) 07 (e) 10 (f) 11 (g) 13 (h) 31 (i) 37 (j) 39 (k) 40 (l) 41 (m) 96 (n) 99

Need copies of RSSSA2 for:

(a) 1RP PR00 Main (b) 1RP PR00 East (c) 1RP PR00 West

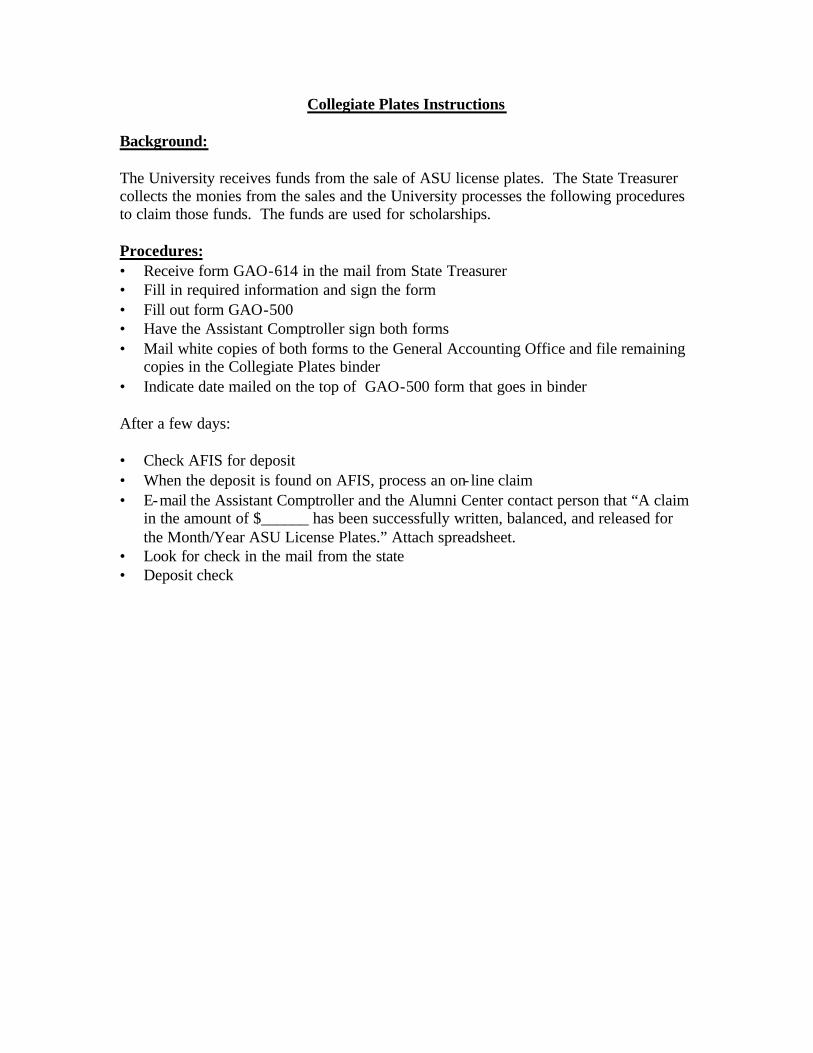

Collegiate Plates Instructions Background: The University receives funds from the sale of ASU license plates. The State Treasurer collects the monies from the sales and the University processes the following procedures to claim those funds. The funds are used for scholarships. Procedures: • Receive form GAO-614 in the mail from State Treasurer • Fill in required information and sign the form • Fill out form GAO-500 • Have the Assistant Comptroller sign both forms • Mail white copies of both forms to the General Accounting Office and file remaining

copies in the Collegiate Plates binder • Indicate date mailed on the top of GAO-500 form that goes in binder After a few days: • Check AFIS for deposit • When the deposit is found on AFIS, process an on- line claim • E-mail the Assistant Comptroller and the Alumni Center contact person that “A claim

in the amount of $______ has been successfully written, balanced, and released for the Month/Year ASU License Plates.” Attach spreadsheet.

• Look for check in the mail from the state • Deposit check

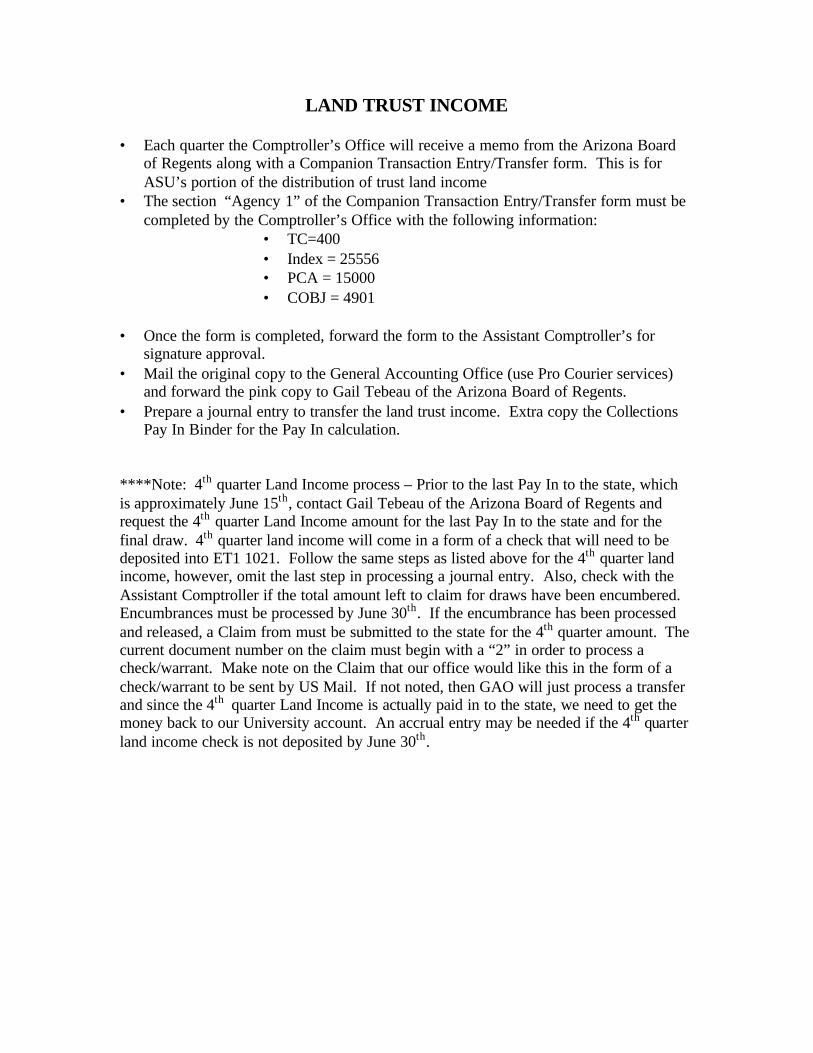

LAND TRUST INCOME • Each quarter the Comptroller’s Office will receive a memo from the Arizona Board

of Regents along with a Companion Transaction Entry/Transfer form. This is for ASU’s portion of the distribution of trust land income

• The section “Agency 1” of the Companion Transaction Entry/Transfer form must be completed by the Comptroller’s Office with the following information:

• TC=400 • Index = 25556 • PCA = 15000 • COBJ = 4901

• Once the form is completed, forward the form to the Assistant Comptroller’s for

signature approval. • Mail the original copy to the General Accounting Office (use Pro Courier services)

and forward the pink copy to Gail Tebeau of the Arizona Board of Regents. • Prepare a journal entry to transfer the land trust income. Extra copy the Collections

Pay In Binder for the Pay In calculation. ****Note: 4th quarter Land Income process – Prior to the last Pay In to the state, which is approximately June 15th, contact Gail Tebeau of the Arizona Board of Regents and request the 4th quarter Land Income amount for the last Pay In to the state and for the final draw. 4th quarter land income will come in a form of a check that will need to be deposited into ET1 1021. Follow the same steps as listed above for the 4th quarter land income, however, omit the last step in processing a journal entry. Also, check with the Assistant Comptroller if the total amount left to claim for draws have been encumbered. Encumbrances must be processed by June 30th. If the encumbrance has been processed and released, a Claim from must be submitted to the state for the 4th quarter amount. The current document number on the claim must begin with a “2” in order to process a check/warrant. Make note on the Claim that our office would like this in the form of a check/warrant to be sent by US Mail. If not noted, then GAO will just process a transfer and since the 4th quarter Land Income is actually paid in to the state, we need to get the money back to our University account. An accrual entry may be needed if the 4th quarter land income check is not deposited by June 30th.

COLLECTION PAY IN PROCEDURES Sources: Monthly - F140A (1150, 1160, and 1180)

A440A (ET11017, ET11021, CA15001, and CB17021) or Data Warehouse Queries with the same information.

AR1400-02 (1st page of fund 7900, Aging Schedule)

Weekly - Data Warehouse queries from the Revenue Table for revenue code breakdown of total revenue (ET11017, ET11021, CA15001, and CB17021)

APP2 screen-prints (ET11017, ET11021, CA15001, and CB17021) Spreadsheets: Pay In Reconciliation

Schedule of Collection Pay In Schedule of Budgeted Collections Compared to State Pay In and CUFS Revenues

For each A440A, summarize revenue by resident tuition, non-resident tuition, and student fees. Here is a list of revenue source and sub-source codes for each category of revenue:

Resident Tuition Non-Resident Tuition Student Fees

5210 07 5210 01 5220 15 5210 13 5210 04 5220 17

5210 76 5210 09 5220 46 5210 15 5220 51

Miscellaneous revenue consists of Land Grant – 5910 99 LAND and Summer Sessions Occupancy Charge – 5920 06. Compare the total revenue from the A440A for each campus to the F140A to verify that all tuition revenue is included for the pay in calculation. Pay In Reconciliation This page is to reconcile and calculate the current period pay in amount. It also keeps track of all items that have been taken into consideration when making the current pay in estimate. Enter the total tuition and fees collected for each account listed on the reconciliation page. From the total, deduct any previous pay ins, accounts receivable (total amount from AR1400-02), refunds (estimate $10,000,000 during the 1st six weeks of each semester and $2,000,000 thereafter, per Hank Spomer), and any other adjustments as necessary (i.e., beginning of each semester withholding of tuition and fees for the local portion transfers for main, west, and east or the pending SMCC payment). The balance after all the deductions will be the current period pay in amount. Insert a line to deduct the current period pay in amount and the balance should be approximately zero. Note: Per Hank Spomer, use estimates of $10,000,000 for Accounts Receivable during the 1st 6 weeks of each semester, thereafter, use the

AR 1400-02 and use estimates of $4,000,000 for Refunds during the 1st 4 weeks of each semester, thereafter, use an estimate of $2,000,000. Music Fees should be transferred to correct account by the A/R Accountant Senior. These fees are not paid to the state. The bottom section of the page is used to calculate the allocation for accounts receivable and refunds between resident and non-resident tuition. Also in the bottom section is a quick reconciliation on the current pay in for ET11017. Schedule of Budgeted Collections Compared to State Pay In and CUFS Revenue This schedule compares actual revenue received to the total pay in to date to the approved state collections budget. It also helps prevent overpayment to the state. For each campus, enter the tuition revenue information from the A440As to the bottom half of the schedule by revenue source and sub-source codes. The approved budget amounts can be found on the annual memorandum from the Budget Office, listing the allocation of collections, other receipts, and balance forward for all three campuses. The pay in to date amount is formula fed from the total amounts on the Schedule of Collection Pay Ins. Schedule of Collections Pay In This schedule breaks down each pay in by campus and between resident, non-resident, and MBA & Law fees. The schedule also shows total pay in by campuses. The source information is from the Pay In Reconciliation page and A440As. Other Items to Note Land grant is also included on this schedule; however, those amounts are not paid in to the state, except for the 4th quarter land grant amount. See the Land Grant procedures for instructions on how to process land grants. Main, west, and east campus local transfers are processed at the beginning of each semester when revenue is available to be transferred and half of the budgeted local amounts for each campus are transferred each semester. West and east campus tuition revenue are transferred from ET11017 into CA15001 and CB17021 as soon as the west and east campus amounts are known, which is normally after the 1st 6 weeks of each semester. There are additional items at yearend to look for. These are: -Allowance for doubtful accounts (registration clearing accounts) -East campus payments made to Chandler/Gilbert Community College and MCC -Adjustments for yearend entries on A/R balance sheet accounts Once the pay in amounts have been calculated, submit the pay in spreadsheets and backup to the Assistant Comptroller for review. Prepare a GAO deposit form and batch header and enter the pay in information on AFIS, then send the deposit form and batch header by Pro Courier to the:

Treasurer’s Office 1700 West Washington 1st Floor, West Wing Phoenix, AZ 85007 Request a draw to be processed by the Accountant, Principal in the Treasury Services area. Prepare and approve a JV Wire document for the pay in amount (Exhibit E, the original JV is filed in Laura James’ office).

GAO Deposit Form information Indexes Cobj Main – 25556 4330 – Education Registration and Tuition - Resident West – 27778 4331 – Education Registration and Tuition – Non-resident East – 26667 4332 – Other Education Fees 4699 - Miscellaneous Receipts

![GAPMS [GENERAL ACCOUNTING & PAYROLL MANAGEMENT SYSTEM ] Running Project On BCMCL](https://img.pdfslide.us/doc/110x75/5511c2ac4a7959ca028b4753/gapms-general-accounting-payroll-management-system-running-project-on-bcmcl.jpg)