Embed Size (px)

Citation preview

Gearing strategies January 2012

What is gearing ?

Borrowing money to invest

Not all gearing is negative

Gearing increases profits but also increases losses

Gearing is not a short-term strategy

Cash flow effects are very important

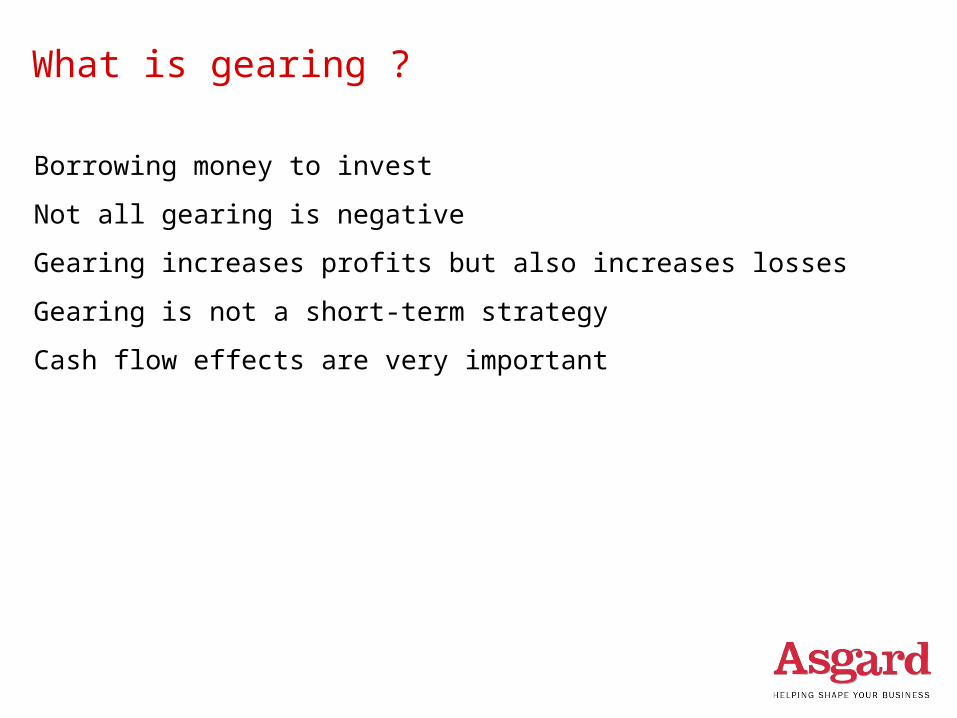

How it works?

Non-Geared Geared

Capital $10,000.00 $10,000.00

Loan $30,000.00

Share portfolio value $10,000.00 $40,000.00

3% Dividends $300.00 $1,200.00

100% Franking $128.57 $514.29

Interest deduction @ 9% $2,700.00

Taxable income $428.57 -$985.71

Tax paid/saved 46.5% MTR $199.29 -$458.36

Franking credits/refund $128.57 $514.29

Net tax paid/saved $70.71 -$972.64

4% Growth $400.00 $1,600.00

Net investment after loan $10,629.29 $11,072.64

Net return before CGT 6.29% 10.73%

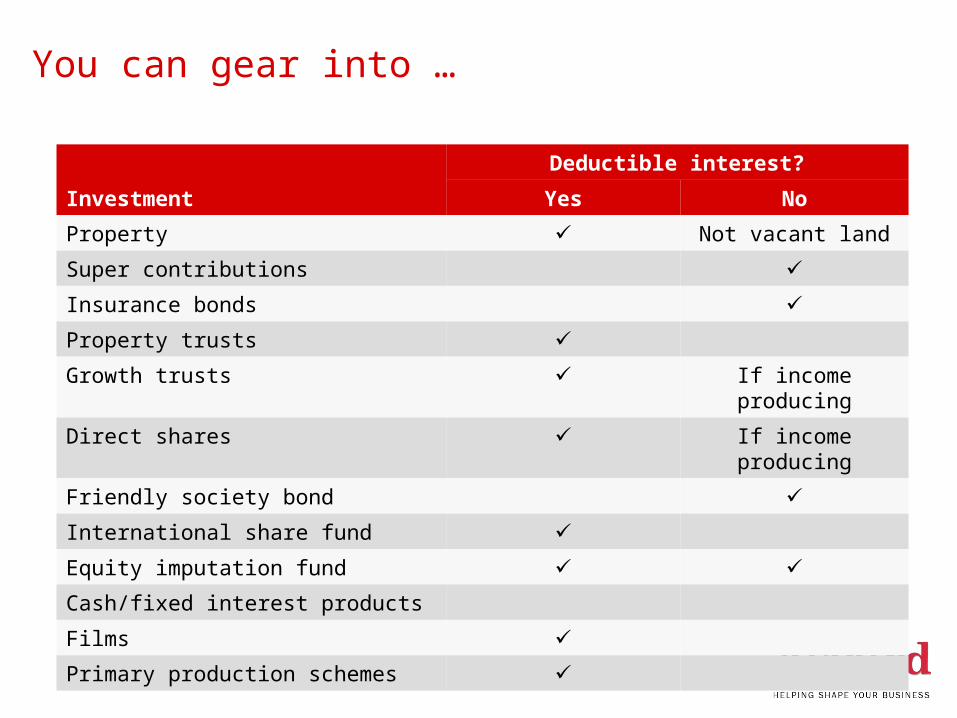

You can gear into …

Investment

Deductible interest?

Yes No

Property Not vacant land

Super contributions

Insurance bonds

Property trusts

Growth trusts If income producing

Direct shares If income producing

Friendly society bond

International share fund

Equity imputation fund

Cash/fixed interest products

Films

Primary production schemes

Lets take Gary and Jill for example

Gary and Jill aged 45

Would like to set up a savings strategy that will help them make the most of the money they have to invest

They have an initial lump sum of $5,000 to invest

They also can afford to invest $250 p.m.

What might be the results if they geared these funds

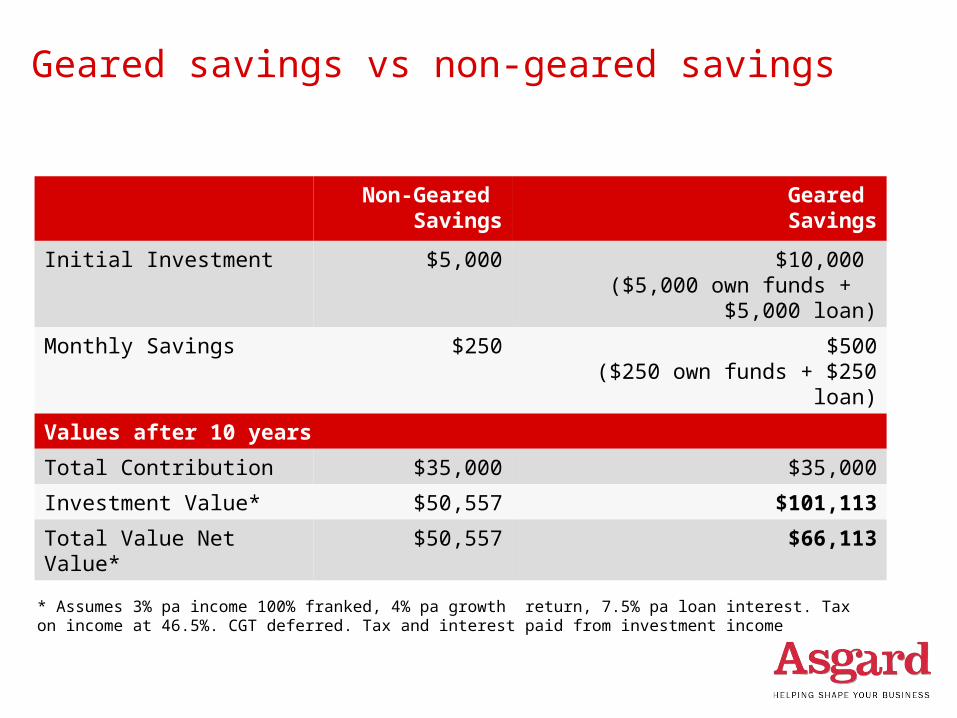

Geared savings vs non-geared savings

Non-Geared Savings

Geared Savings

Initial Investment $5,000 $10,000 ($5,000 own funds + $5,000

loan)

Monthly Savings $250 $500($250 own funds + $250 loan)

Values after 10 years

Total Contribution $35,000 $35,000

Investment Value* $50,557 $101,113

Total Value Net Value* $50,557 $66,113

* Assumes 3% pa income 100% franked, 4% pa growth return, 7.5% pa loan interest. Tax on income at 46.5%. CGT deferred. Tax and interest paid from investment income

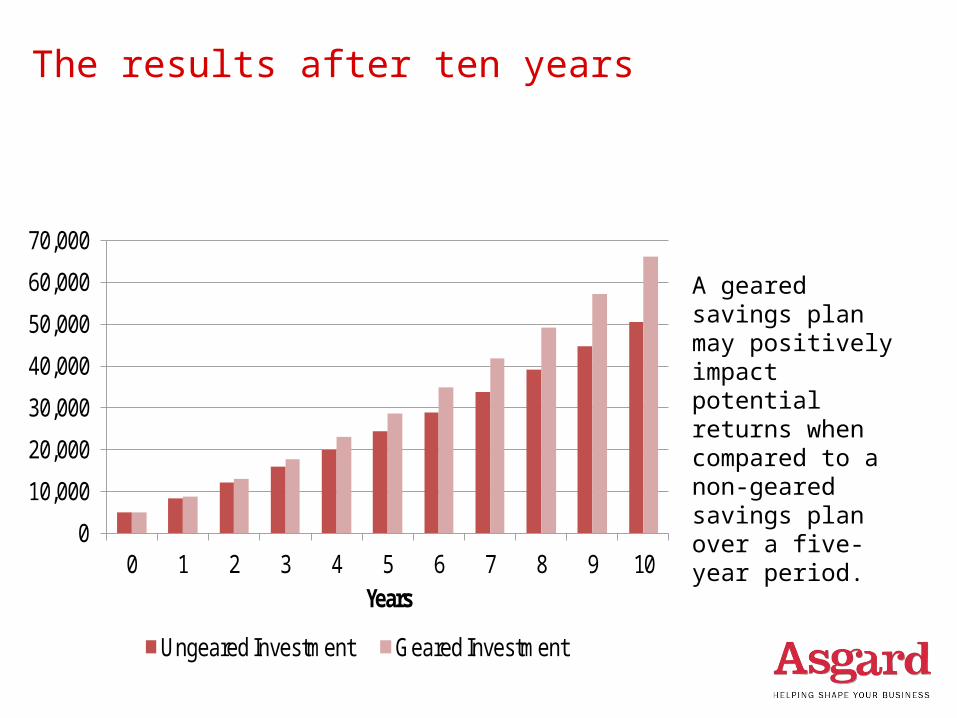

The results after ten years

A geared savings plan may positively impact potential returns when compared to a non-geared savings plan over a five-year period.

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

0 1 2 3 4 5 6 7 8 9 10Years

Ungeared Investment Geared Investment

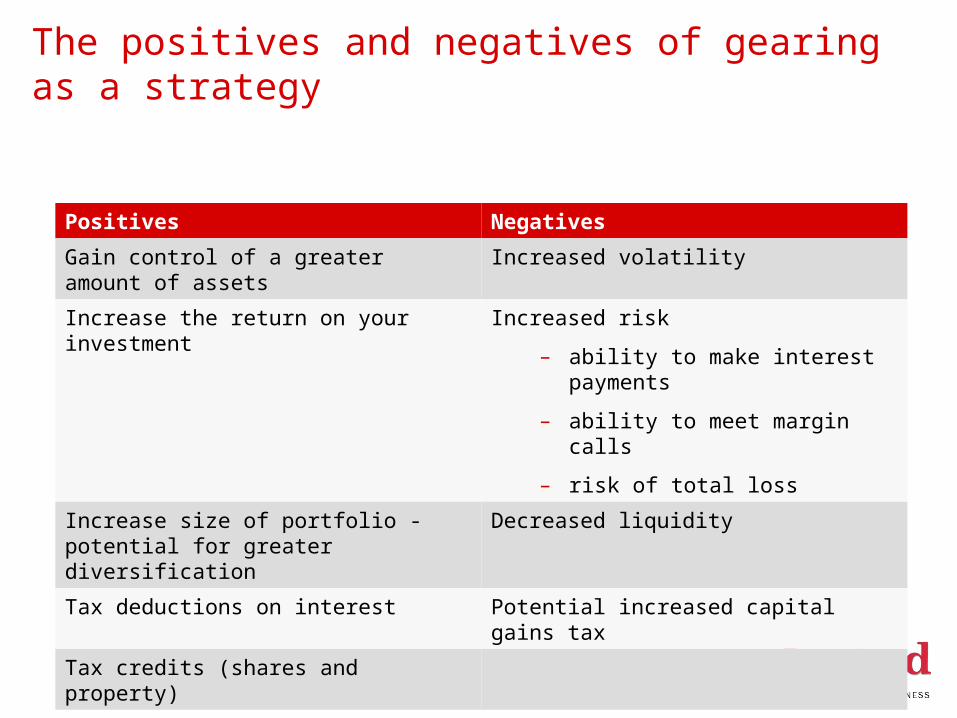

The positives and negatives of gearing as a strategy

Positives Negatives

Gain control of a greater amount of assets

Increased volatility

Increase the return on your investment

Increased risk

– ability to make interest payments

– ability to meet margin calls

– risk of total loss

Increase size of portfolio - potential for greater diversification

Decreased liquidity

Tax deductions on interest Potential increased capital gains tax

Tax credits (shares and property)

9

Asgard Capital Management Limited ABN 009 279 592, AFSL 240695 (Asgard). Information current as at 1 January 2012. This publication provides an overview or summary only and it should not be considered a comprehensive statement on any matter or relied upon as such. This presentation contains general information only and does not take into account your personal objectives, financial situation or needs. You should therefore consider whether information or advice contained in this presentation is appropriate to you having regard to these factors before acting on it. You should seek personalised advice from a financial adviser and your accountant before making any financial decision in relation to matters discussed in this presentation. The taxation position described is a general statement and should only be used as a guide. It does not constitute tax advice and is based on current tax laws and our interpretation. Your individual situation may differ and you should seek independent professional tax advice. Consider our disclosure documents which include our Financial Services Guide available on www.asgard.com.au. © Asgard Capital Management Limited 2012.