Embed Size (px)

Citation preview

1

GCC Fixed Income Chart Book: Q1-Q3 2016 Review

06 October, 2016

Chavan Bhogaita / Rakesh Sahu

Market Insights & Strategy

NBAD Global Markets

22

To the fullest extent allowed by applicable laws and regulations, National Bank of Abu Dhabi PJSC (the “Bank”) and any otheraffiliate or subsidiary of the Bank, expressly disclaim all warranties and representations in respect of this communication. Thecontent is confidential and is provided for your information purposes only on an “as is” and “as available” basis and noliability is accepted for or representation is made by the Bank in respect of the quality, completeness or accuracy of theinformation and the Bank has undertaken no independent verification in relation thereto nor is it under any duty to do sowhether prepared in part or in full by the Bank or any third party. Furthermore, the Bank shall be under no obligation toprovide you with any change or update in relation to said content. It is not intended for distribution to private investors orprivate clients and is not intended to be relied upon as advice; whether financial, legal, tax or otherwise. To the extent thatyou deem necessary to obtain such advice, you should consult with your independent advisors. Any content has beenprepared by personnel of the Global Markets at the Bank and does not reflect the views of the Bank as a whole or otherpersonnel of the Bank.

Disclaimer

33

Welcome to our 9M 2016 chart book for the GCC fixed income market. The idea is very simple – to give those of you who follow this market a quick snapshot of some of the key points in terms of the following:

Overview of spread performance in this market during the first nine months of FY 2016

Primary Market issuance (and performance of these deals since they were printed)

Secondary Market performance of key instruments (snapshot from 31st December 2015 to 30th September 2016)

We have deliberately made the report text-light in an attempt to make it easier to digest. Hopefully you will find it both interesting and useful.

If you have any feedback on the report, or indeed would like to discuss any of the points highlighted, please do contact me.

Regards,

Chavan BhogaitaManaging Director & Head of Market Insights & StrategyGlobal [email protected]+971 2 6110 127

Foreword

44

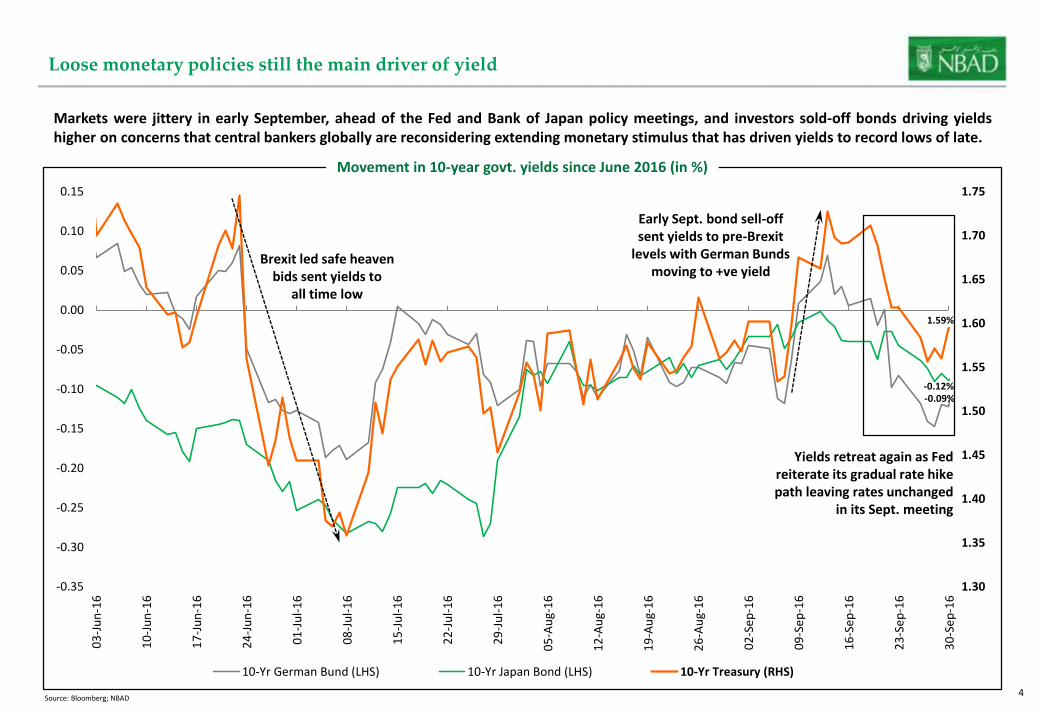

Loose monetary policies still the main driver of yield

Markets were jittery in early September, ahead of the Fed and Bank of Japan policy meetings, and investors sold-off bonds driving yieldshigher on concerns that central bankers globally are reconsidering extending monetary stimulus that has driven yields to record lows of late.

1.30

1.35

1.40

1.45

1.50

1.55

1.60

1.65

1.70

1.75

-0.35

-0.30

-0.25

-0.20

-0.15

-0.10

-0.05

0.00

0.05

0.10

0.15

03

-Ju

n-1

6

10

-Ju

n-1

6

17

-Ju

n-1

6

24

-Ju

n-1

6

01

-Ju

l-1

6

08

-Ju

l-1

6

15

-Ju

l-1

6

22

-Ju

l-1

6

29

-Ju

l-1

6

05

-Au

g-1

6

12

-Au

g-1

6

19

-Au

g-1

6

26

-Au

g-1

6

02

-Se

p-1

6

09

-Se

p-1

6

16

-Se

p-1

6

23

-Se

p-1

6

30

-Se

p-1

6

10-Yr German Bund (LHS) 10-Yr Japan Bond (LHS) 10-Yr Treasury (RHS)

Movement in 10-year govt. yields since June 2016 (in %)

Source: Bloomberg; NBAD

Early Sept. bond sell-off sent yields to pre-Brexit

levels with German Bunds moving to +ve yield

Brexit led safe heaven bids sent yields to

all time low

Yields retreat again as Fed reiterate its gradual rate hike path leaving rates unchanged

in its Sept. meeting

-0.12% -0.09%

1.59%

55

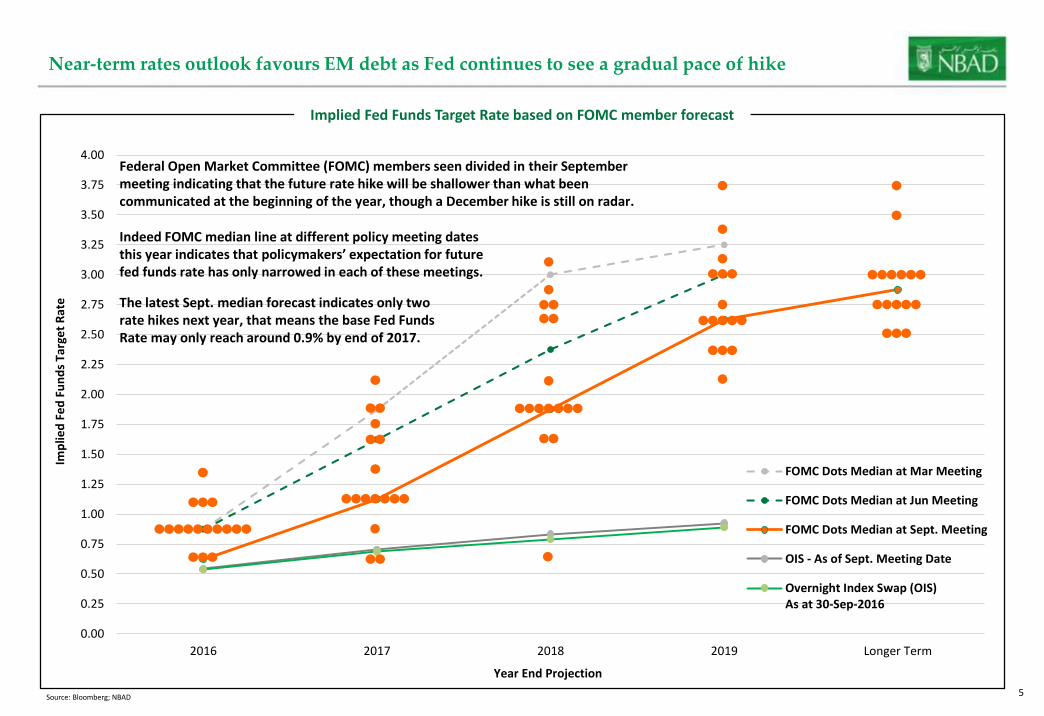

Near-term rates outlook favours EM debt as Fed continues to see a gradual pace of hike

0.00

0.25

0.50

0.75

1.00

1.25

1.50

1.75

2.00

2.25

2.50

2.75

3.00

3.25

3.50

3.75

4.00

2016 2017 2018 2019 Longer Term

Imp

lied

Fe

d F

un

ds

Targ

et

Rat

e

Year End Projection

FOMC Dots Median at Mar Meeting

FOMC Dots Median at Jun Meeting

FOMC Dots Median at Sept. Meeting

OIS - As of Sept. Meeting Date

Overnight Index Swap (OIS)As at 30-Sep-2016

Implied Fed Funds Target Rate based on FOMC member forecast

Source: Bloomberg; NBAD

Federal Open Market Committee (FOMC) members seen divided in their September meeting indicating that the future rate hike will be shallower than what been communicated at the beginning of the year, though a December hike is still on radar.

Indeed FOMC median line at different policy meeting dates this year indicates that policymakers’ expectation for future fed funds rate has only narrowed in each of these meetings.

The latest Sept. median forecast indicates only two rate hikes next year, that means the base Fed Funds Rate may only reach around 0.9% by end of 2017.

66

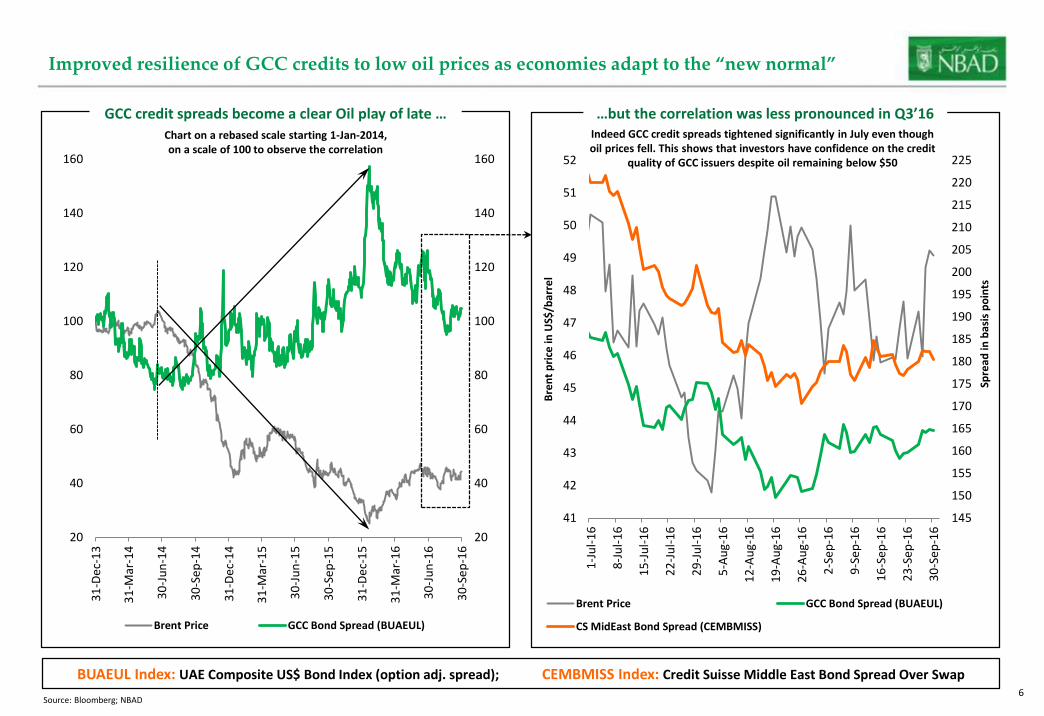

Improved resilience of GCC credits to low oil prices as economies adapt to the “new normal”

BUAEUL Index: UAE Composite US$ Bond Index (option adj. spread); CEMBMISS Index: Credit Suisse Middle East Bond Spread Over Swap

145

150

155

160

165

170

175

180

185

190

195

200

205

210

215

220

225

41

42

43

44

45

46

47

48

49

50

51

52

1-J

ul-

16

8-J

ul-

16

15

-Ju

l-1

6

22

-Ju

l-1

6

29

-Ju

l-1

6

5-A

ug-

16

12

-Au

g-1

6

19

-Au

g-1

6

26

-Au

g-1

6

2-S

ep

-16

9-S

ep

-16

16

-Se

p-1

6

23

-Se

p-1

6

30

-Se

p-1

6

Spre

ad in

bas

is p

oin

ts

Bre

nt

pri

ce in

US$

/bar

rel

Brent Price GCC Bond Spread (BUAEUL)

CS MidEast Bond Spread (CEMBMISS)

…but the correlation was less pronounced in Q3’16

Source: Bloomberg; NBAD

20

40

60

80

100

120

140

160

20

40

60

80

100

120

140

160

31

-De

c-1

3

31

-Mar

-14

30

-Ju

n-1

4

30

-Se

p-1

4

31

-De

c-1

4

31

-Mar

-15

30

-Ju

n-1

5

30

-Se

p-1

5

31

-De

c-1

5

31

-Mar

-16

30

-Ju

n-1

6

30

-Se

p-1

6

Brent Price GCC Bond Spread (BUAEUL)

GCC credit spreads become a clear Oil play of late …

Chart on a rebased scale starting 1-Jan-2014,on a scale of 100 to observe the correlation

Indeed GCC credit spreads tightened significantly in July even though oil prices fell. This shows that investors have confidence on the credit

quality of GCC issuers despite oil remaining below $50

77

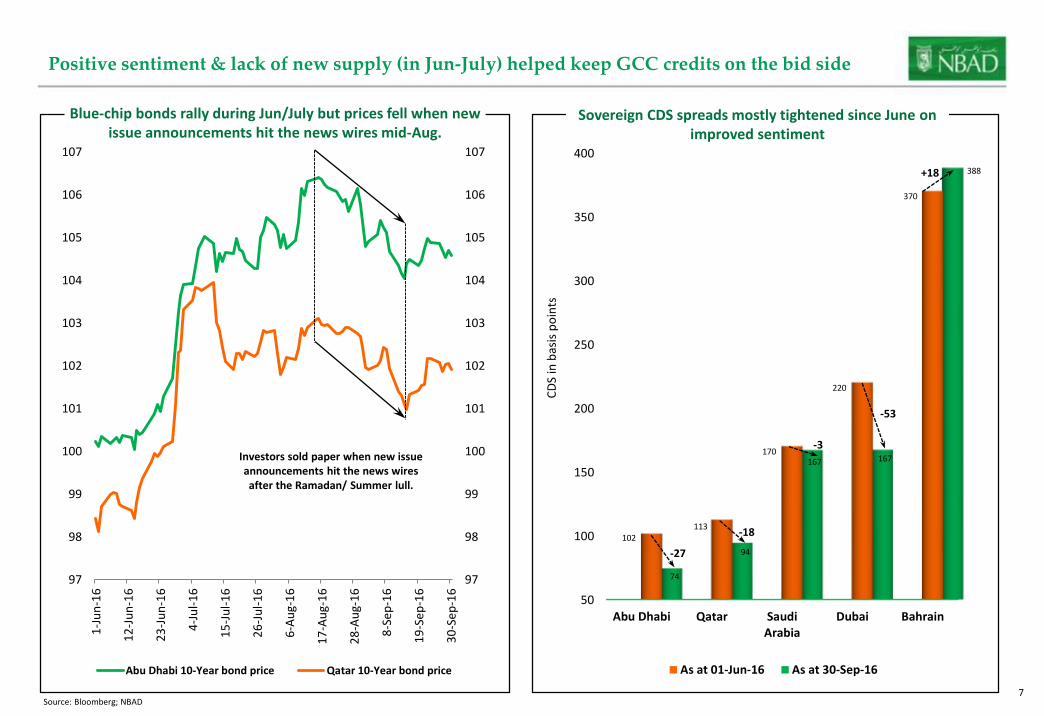

Positive sentiment & lack of new supply (in Jun-July) helped keep GCC credits on the bid side

Source: Bloomberg; NBAD

97

98

99

100

101

102

103

104

105

106

107

97

98

99

100

101

102

103

104

105

106

107

1-J

un

-16

12

-Ju

n-1

6

23

-Ju

n-1

6

4-J

ul-

16

15

-Ju

l-1

6

26

-Ju

l-1

6

6-A

ug-

16

17

-Au

g-1

6

28

-Au

g-1

6

8-S

ep

-16

19

-Se

p-1

6

30

-Se

p-1

6

Abu Dhabi 10-Year bond price Qatar 10-Year bond price

Blue-chip bonds rally during Jun/July but prices fell when new issue announcements hit the news wires mid-Aug.

Investors sold paper when new issue announcements hit the news wires after the Ramadan/ Summer lull.

50

100

150

200

250

300

350

400

Abu Dhabi Qatar SaudiArabia

Dubai Bahrain

CD

S in

bas

is p

oin

ts

As at 01-Jun-16 As at 30-Sep-16

Sovereign CDS spreads mostly tightened since June on improved sentiment

102113

170

220

370

74

94

167 167

388

-27

-18

-3

-53

+18

88

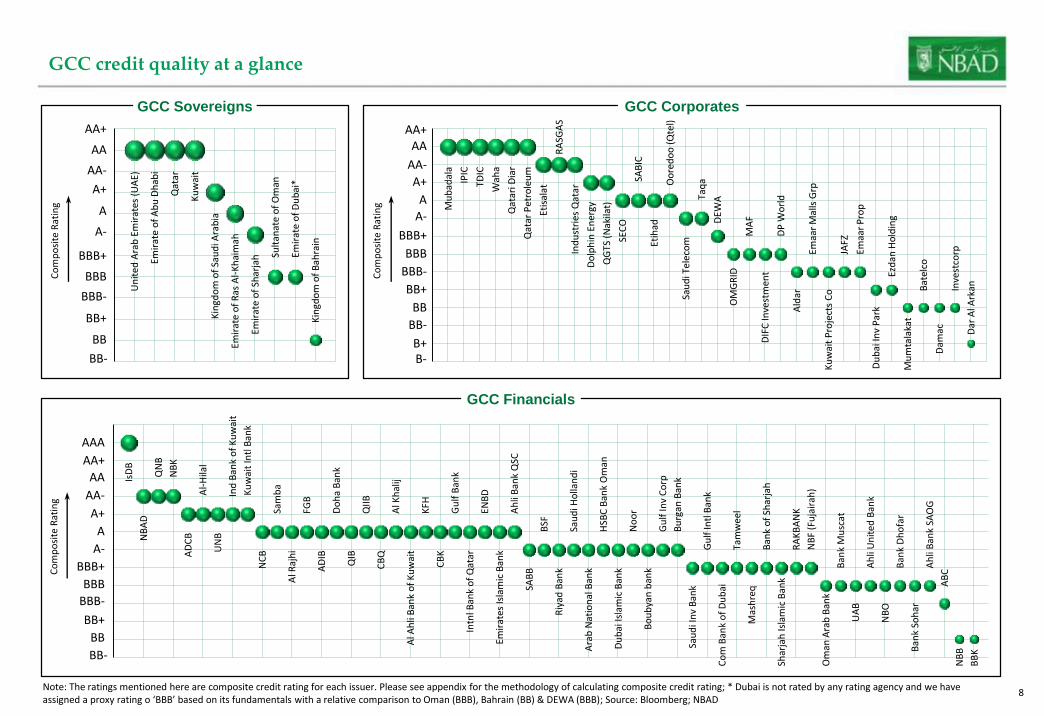

GCC credit quality at a glance

Note: The ratings mentioned here are composite credit rating for each issuer. Please see appendix for the methodology of calculating composite credit rating; * Dubai is not rated by any rating agency and we have assigned a proxy rating o ‘BBB’ based on its fundamentals with a relative comparison to Oman (BBB), Bahrain (BB) & DEWA (BBB); Source: Bloomberg; NBAD

Un

ited

Ara

b E

mir

ates

(U

AE)

Emir

ate

of

Ab

u D

hab

i

Qat

ar

Ku

wai

t

Kin

gdo

m o

f Sa

ud

i Ara

bia

Emir

ate

of

Ras

Al-

Kh

aim

ah

Emir

ate

of

Shar

jah Su

ltan

ate

of

Om

an

Emir

ate

of

Du

bai

*

Kin

gdo

m o

f B

ahra

in

4

5

6

7

8

9

10

11

12

13

14

15

Co

mp

osi

te R

atin

g

AA+

AA

AA-

A+

A

A-

BBB+

BBB

BBB-

BB+

BB

Mu

bad

ala

IPIC

TDIC

Wah

a

Qat

ari D

iar

Qat

ar P

etro

leu

m

Etis

alat

RA

SGA

S

Ind

ust

ries

Qat

ar

Do

lph

in E

ner

gy

QG

TS (

Nak

ilat)

SEC

O

SAB

IC

Etih

ad

Oo

red

oo

(Q

tel)

Sau

di T

elec

om

Taq

a

DEW

A

OM

GR

ID

MA

F

DIF

C In

vest

men

t

DP

Wo

rld

Ald

ar

Emaa

r M

alls

Grp

Ku

wai

t P

roje

cts

Co

JAFZ

Emaa

r P

rop

Du

bai

Inv

Par

k

Ezd

an H

old

ing

Mu

mta

laka

t

Bat

elco

Dam

ac

Inve

stco

rp

Dar

Al A

rkan

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Co

mp

osi

te R

atin

g

AA

AA-

A+

A

A-

BBB+

BBB

BBB-

BB+

BB

BB-

B+

AA+

B-

IsD

B

NB

AD

QN

B

NB

K

AD

CB

Al-

Hila

l

UN

B

Ind

Ban

k o

f K

uw

ait

Ku

wai

t In

tl B

ank

NC

B

Sam

ba

Al R

ajh

i

FGB

AD

IB

Do

ha

Ban

k

QIB

QII

B

CB

Q

Al K

hal

ij

Al A

hli

Ban

k o

f K

uw

ait

KFH

CB

K

Gu

lf B

ank

Intn

l Ban

k o

f Q

atar

ENB

D

Emir

ates

Isla

mic

Ban

k

Ah

li B

ank

QSC

SAB

B

BSF

Riy

ad B

ank

Sau

di H

olla

nd

i

Ara

b N

atio

nal

Ban

k

HSB

C B

ank

Om

an

Du

bai

Isla

mic

Ban

k

No

or

Bo

ub

yan

ban

k

Gu

lf In

v C

orp

Bu

rgan

Ban

k

Sau

di I

nv

Ban

k

Gu

lf In

tl B

ank

Co

m B

ank

of

Du

bai

Tam

wee

l

Mas

hre

q

Ban

k o

f Sh

arja

h

Shar

jah

Isla

mic

Ban

k

RA

KB

AN

K

NB

F (F

uja

irah

)

Om

an A

rab

Ban

k

Ban

k M

usc

at

UA

B

Ah

li U

nit

ed B

ank

NB

O

Ban

k D

ho

far

Ban

k So

har

Ah

li B

ank

SAO

G

AB

C

NB

B

BB

K4

5

6

7

8

9

10

11

12

13

14

15

16

17

Co

mp

osi

te R

atin

g

AAA

AA+

AA

AA-

A+

A

A-

BBB+

BBB

BBB-

BB+

BB

GCC Sovereigns GCC Corporates

GCC Financials

BB-

BB-

99

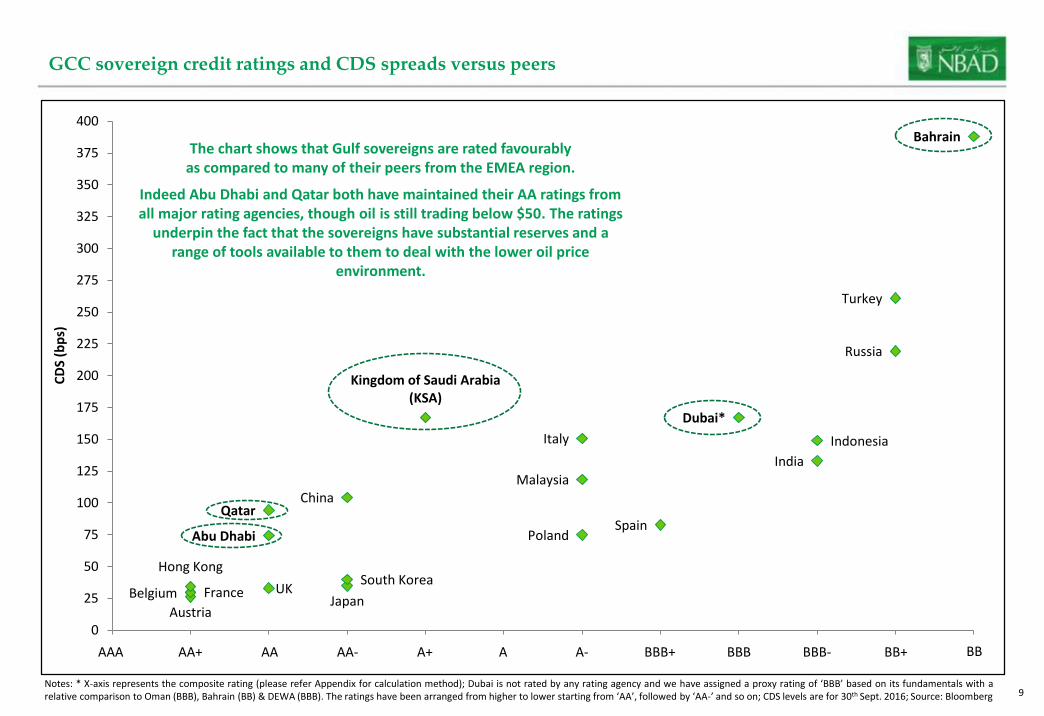

GCC sovereign credit ratings and CDS spreads versus peers

Bahrain

Turkey

Russia

Indonesia

India

Dubai*

Spain

Malaysia

Italy

Poland

Kingdom of Saudi Arabia (KSA)

China

Japan

South Korea

Abu Dhabi

Qatar

UKFrance

Austria

Belgium

Hong Kong

0

25

50

75

100

125

150

175

200

225

250

275

300

325

350

375

400

CD

S (b

ps)

AA+ AA AA- A+ A A-AAA BBB BBB-BBB+ BB+ BB

The chart shows that Gulf sovereigns are rated favourably as compared to many of their peers from the EMEA region.

Notes: * X-axis represents the composite rating (please refer Appendix for calculation method); Dubai is not rated by any rating agency and we have assigned a proxy rating of ‘BBB’ based on its fundamentals with arelative comparison to Oman (BBB), Bahrain (BB) & DEWA (BBB). The ratings have been arranged from higher to lower starting from ‘AA’, followed by ‘AA-’ and so on; CDS levels are for 30th Sept. 2016; Source: Bloomberg

Indeed Abu Dhabi and Qatar both have maintained their AA ratings from all major rating agencies, though oil is still trading below $50. The ratings

underpin the fact that the sovereigns have substantial reserves and a range of tools available to them to deal with the lower oil price

environment.

1010

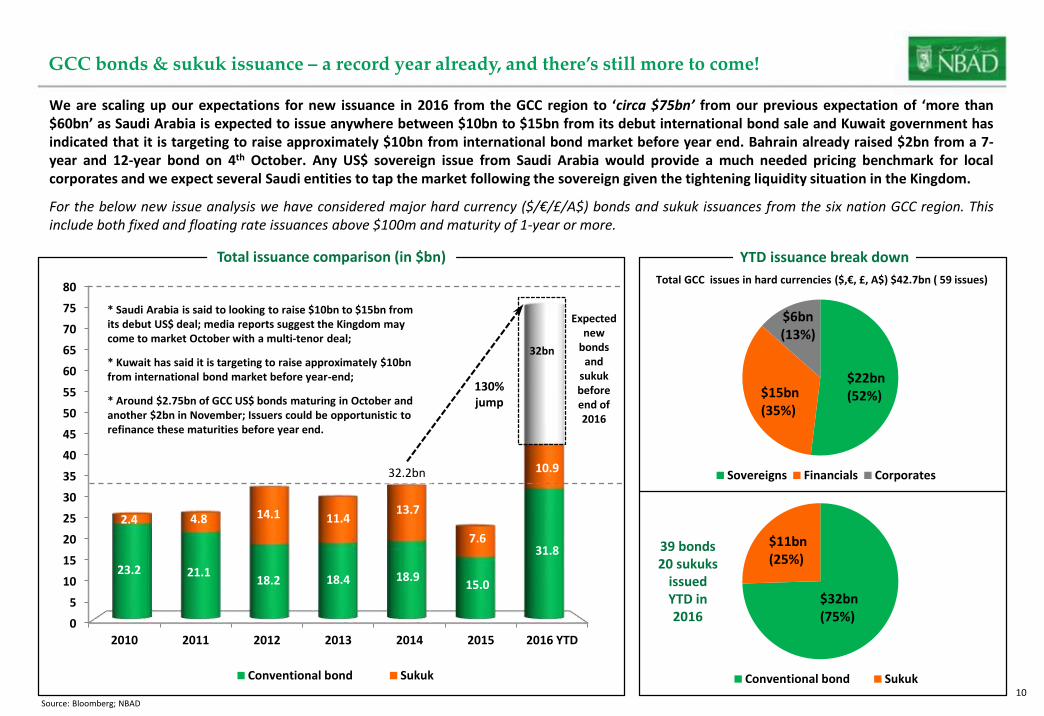

GCC bonds & sukuk issuance – a record year already, and there’s still more to come!

Source: Bloomberg; NBAD

We are scaling up our expectations for new issuance in 2016 from the GCC region to ‘circa $75bn’ from our previous expectation of ‘more than$60bn’ as Saudi Arabia is expected to issue anywhere between $10bn to $15bn from its debut international bond sale and Kuwait government hasindicated that it is targeting to raise approximately $10bn from international bond market before year end. Bahrain already raised $2bn from a 7-year and 12-year bond on 4th October. Any US$ sovereign issue from Saudi Arabia would provide a much needed pricing benchmark for localcorporates and we expect several Saudi entities to tap the market following the sovereign given the tightening liquidity situation in the Kingdom.

For the below new issue analysis we have considered major hard currency ($/€/£/A$) bonds and sukuk issuances from the six nation GCC region. Thisinclude both fixed and floating rate issuances above $100m and maturity of 1-year or more.

0

5

10

15

20

25

30

35

40

45

50

55

60

65

70

75

80

2010 2011 2012 2013 2014 2015 2016 YTD

23.2 21.118.2 18.4 18.9

15.0

31.8

2.4 4.8 14.1 11.413.7

7.6

10.9

Conventional bond Sukuk

Total issuance comparison (in $bn)

32bn

130%jump

32.2bn

Expected new

bonds and

sukuk before end of 2016

* Saudi Arabia is said to looking to raise $10bn to $15bn from its debut US$ deal; media reports suggest the Kingdom may come to market October with a multi-tenor deal;

* Kuwait has said it is targeting to raise approximately $10bn from international bond market before year-end;

* Around $2.75bn of GCC US$ bonds maturing in October and another $2bn in November; Issuers could be opportunistic to refinance these maturities before year end.

$22bn(52%)$15bn

(35%)

$6bn(13%)

Sovereigns Financials Corporates

Total GCC issues in hard currencies ($,€, £, A$) $42.7bn ( 59 issues)

YTD issuance break down

$32bn(75%)

$11bn(25%)

Conventional bond Sukuk

39 bonds20 sukuks

issuedYTD in2016

1111

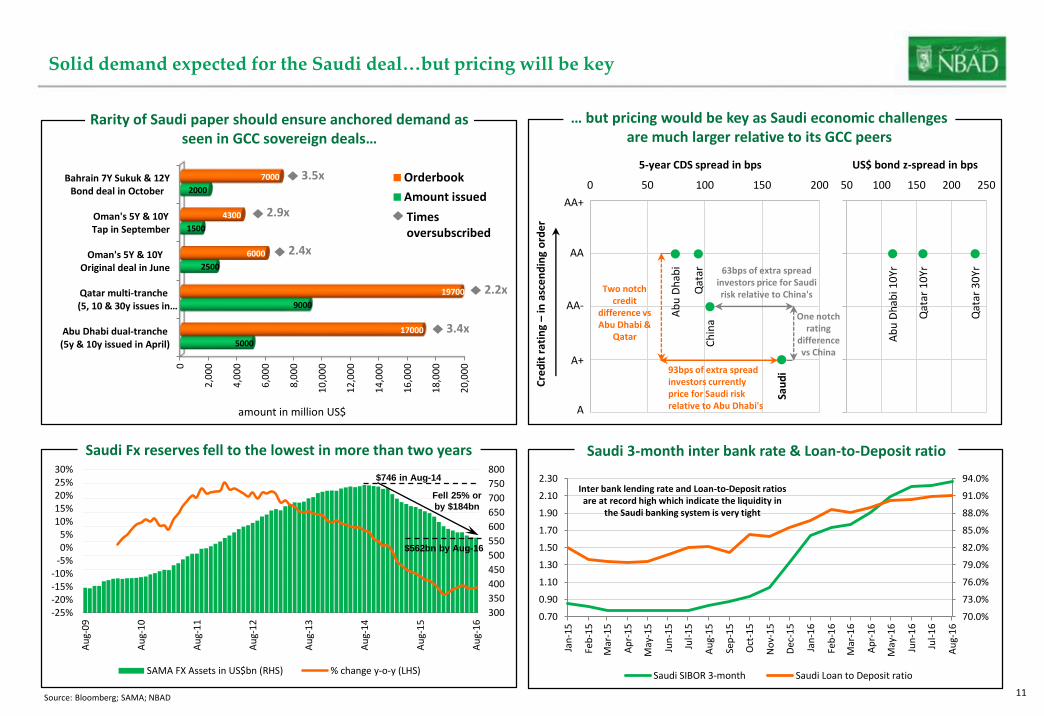

Solid demand expected for the Saudi deal…but pricing will be key

Ab

u D

hab

i

Qat

arC

hin

a

Sau

di

0

1

2

3

4

0 50 100 150 200

Ab

u D

hab

i 10

Yr

Qat

ar 1

0Yr

Qat

ar 3

0Yr

50 100 150 200 250

AA+

AA

AA-

A+

A

… but pricing would be key as Saudi economic challenges are much larger relative to its GCC peers

Cre

dit

rat

ing

–in

asc

en

din

g o

rde

r

5-year CDS spread in bps US$ bond z-spread in bps

Two notch credit

difference vs Abu Dhabi &

Qatar

One notch rating

difference vs China

93bps of extra spreadinvestors currentlyprice for Saudi riskrelative to Abu Dhabi's

63bps of extra spread investors price for Saudi risk relative to China's

0

2,0

00

4,0

00

6,0

00

8,0

00

10

,00

0

12

,00

0

14

,00

0

16

,00

0

18

,00

0

20

,00

0

Abu Dhabi dual-tranche(5y & 10y issued in April)

Qatar multi-tranche(5, 10 & 30y issues in…

Oman's 5Y & 10YOriginal deal in June

Oman's 5Y & 10YTap in September

Bahrain 7Y Sukuk & 12YBond deal in October

5000

9000

2500

1500

2000

17000

19700

6000

4300

7000

amount in million US$

Orderbook

Amount issued

Rarity of Saudi paper should ensure anchored demand as seen in GCC sovereign deals…

Timesoversubscribed

2.9x

2.4x

2.2x

3.4x

3.5x

Saudi Fx reserves fell to the lowest in more than two years

-25%-20%-15%-10%

-5%0%5%

10%15%20%25%30%

300

350

400

450

500

550

600

650

700

750

800A

ug-

16

Au

g-1

5

Au

g-1

4

Au

g-1

3

Au

g-1

2

Au

g-1

1

Au

g-1

0

Au

g-0

9

SAMA FX Assets in US$bn (RHS) % change y-o-y (LHS)

$746 in Aug-14

$562bn by Aug-16

Fell 25% or

by $184bn

70.0%

73.0%

76.0%

79.0%

82.0%

85.0%

88.0%

91.0%

94.0%

0.70

0.90

1.10

1.30

1.50

1.70

1.90

2.10

2.30

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

Jul-

15

Au

g-1

5

Sep

-15

Oct

-15

No

v-1

5

Dec

-15

Jan

-16

Feb

-16

Mar

-16

Ap

r-1

6

May

-16

Jun

-16

Jul-

16

Au

g-1

6

Saudi SIBOR 3-month Saudi Loan to Deposit ratio

Saudi 3-month inter bank rate & Loan-to-Deposit ratio

Inter bank lending rate and Loan-to-Deposit ratios are at record high which indicate the liquidity in

the Saudi banking system is very tight

Source: Bloomberg; SAMA; NBAD

1212

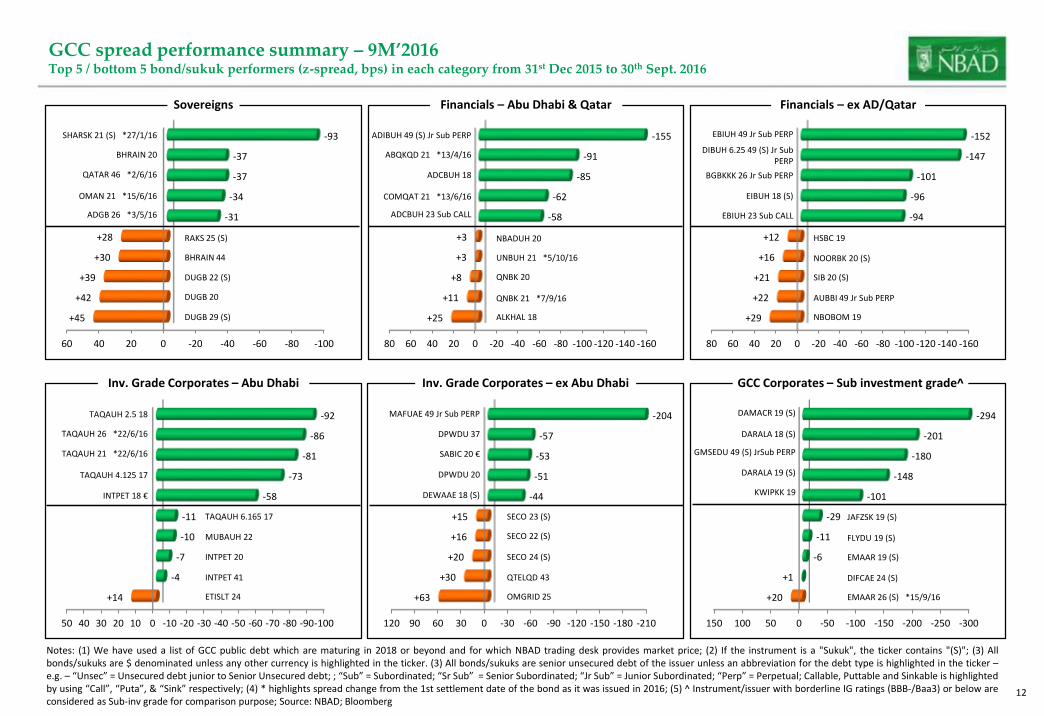

GCC spread performance summary – 9M’2016Top 5 / bottom 5 bond/sukuk performers (z-spread, bps) in each category from 31st Dec 2015 to 30th Sept. 2016

Notes: (1) We have used a list of GCC public debt which are maturing in 2018 or beyond and for which NBAD trading desk provides market price; (2) If the instrument is a "Sukuk", the ticker contains "(S)"; (3) Allbonds/sukuks are $ denominated unless any other currency is highlighted in the ticker. (3) All bonds/sukuks are senior unsecured debt of the issuer unless an abbreviation for the debt type is highlighted in the ticker –e.g. – “Unsec” = Unsecured debt junior to Senior Unsecured debt; ; “Sub” = Subordinated; “Sr Sub” = Senior Subordinated; “Jr Sub” = Junior Subordinated; “Perp” = Perpetual; Callable, Puttable and Sinkable is highlightedby using “Call”, “Puta”, & “Sink” respectively; (4) * highlights spread change from the 1st settlement date of the bond as it was issued in 2016; (5) ^ Instrument/issuer with borderline IG ratings (BBB-/Baa3) or below areconsidered as Sub-inv grade for comparison purpose; Source: NBAD; Bloomberg

-100-80-60-40-200204060

+45

+42

+39

+30

+28

-31

-34

-37

-37

-93

Sovereigns

SHARSK 21 (S) *27/1/16

BHRAIN 20

QATAR 46 *2/6/16

OMAN 21 *15/6/16

ADGB 26 *3/5/16

RAKS 25 (S)

BHRAIN 44

DUGB 22 (S)

DUGB 20

DUGB 29 (S)

-160-140-120-100-80-60-40-20020406080

+25

+11

+8

+3

+3

-58

-62

-85

-91

-155

Financials – Abu Dhabi & Qatar

ADIBUH 49 (S) Jr Sub PERP

ABQKQD 21 *13/4/16

ADCBUH 18

COMQAT 21 *13/6/16

ADCBUH 23 Sub CALL

NBADUH 20

UNBUH 21 *5/10/16

QNBK 20

QNBK 21 *7/9/16

ALKHAL 18

-160-140-120-100-80-60-40-20020406080

+29

+22

+21

+16

+12

-94

-96

-101

-147

-152

Financials – ex AD/Qatar

EBIUH 49 Jr Sub PERP

DIBUH 6.25 49 (S) Jr Sub PERP

BGBKKK 26 Jr Sub PERP

EIBUH 18 (S)

EBIUH 23 Sub CALL

HSBC 19

NOORBK 20 (S)

SIB 20 (S)

AUBBI 49 Jr Sub PERP

NBOBOM 19

-100-90-80-70-60-50-40-30-20-1001020304050

+14

-4

-7

-10

-11

-58

-73

-81

-86

-92

Inv. Grade Corporates – Abu Dhabi

TAQAUH 2.5 18

TAQAUH 26 *22/6/16

TAQAUH 21 *22/6/16

TAQAUH 4.125 17

INTPET 18 €

TAQAUH 6.165 17

MUBAUH 22

INTPET 20

INTPET 41

ETISLT 24

-210-180-150-120-90-60-300306090120

+63

+30

+20

+16

+15

-44

-51

-53

-57

-204

Inv. Grade Corporates – ex Abu Dhabi

MAFUAE 49 Jr Sub PERP

DPWDU 37

SABIC 20 €

DPWDU 20

DEWAAE 18 (S)

SECO 23 (S)

SECO 22 (S)

SECO 24 (S)

QTELQD 43

OMGRID 25

-300-250-200-150-100-50050100150

+20

+1

-6

-11

-29

-101

-148

-180

-201

-294

GCC Corporates – Sub investment grade^

DAMACR 19 (S)

DARALA 18 (S)

GMSEDU 49 (S) JrSub PERP

DARALA 19 (S)

KWIPKK 19

JAFZSK 19 (S)

FLYDU 19 (S)

DIFCAE 24 (S)

EMAAR 26 (S) *15/9/16

EMAAR 19 (S)

1313

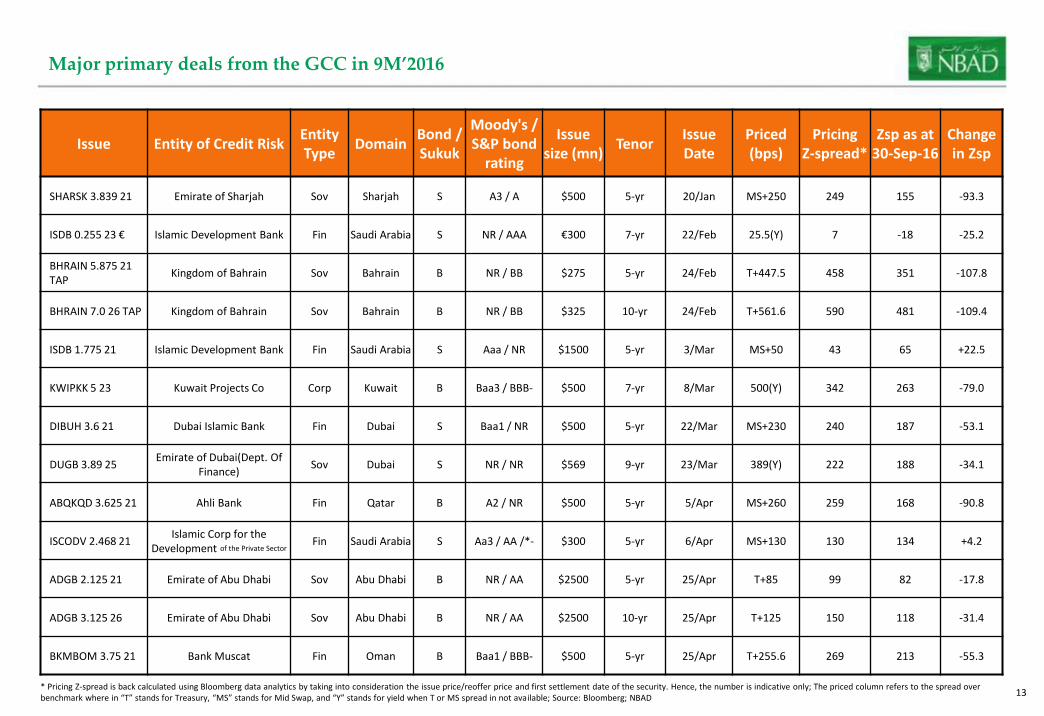

Major primary deals from the GCC in 9M’2016

Issue Entity of Credit RiskEntityType

DomainBond / Sukuk

Moody's / S&P bond

rating

Issuesize (mn)

TenorIssue Date

Priced (bps)

PricingZ-spread*

Zsp as at30-Sep-16

Change in Zsp

SHARSK 3.839 21 Emirate of Sharjah Sov Sharjah S A3 / A $500 5-yr 20/Jan MS+250 249 155 -93.3

ISDB 0.255 23 € Islamic Development Bank Fin Saudi Arabia S NR / AAA €300 7-yr 22/Feb 25.5(Y) 7 -18 -25.2

BHRAIN 5.875 21 TAP

Kingdom of Bahrain Sov Bahrain B NR / BB $275 5-yr 24/Feb T+447.5 458 351 -107.8

BHRAIN 7.0 26 TAP Kingdom of Bahrain Sov Bahrain B NR / BB $325 10-yr 24/Feb T+561.6 590 481 -109.4

ISDB 1.775 21 Islamic Development Bank Fin Saudi Arabia S Aaa / NR $1500 5-yr 3/Mar MS+50 43 65 +22.5

KWIPKK 5 23 Kuwait Projects Co Corp Kuwait B Baa3 / BBB- $500 7-yr 8/Mar 500(Y) 342 263 -79.0

DIBUH 3.6 21 Dubai Islamic Bank Fin Dubai S Baa1 / NR $500 5-yr 22/Mar MS+230 240 187 -53.1

DUGB 3.89 25Emirate of Dubai(Dept. Of

Finance)Sov Dubai S NR / NR $569 9-yr 23/Mar 389(Y) 222 188 -34.1

ABQKQD 3.625 21 Ahli Bank Fin Qatar B A2 / NR $500 5-yr 5/Apr MS+260 259 168 -90.8

ISCODV 2.468 21Islamic Corp for the

Development of the Private SectorFin Saudi Arabia S Aa3 / AA /*- $300 5-yr 6/Apr MS+130 130 134 +4.2

ADGB 2.125 21 Emirate of Abu Dhabi Sov Abu Dhabi B NR / AA $2500 5-yr 25/Apr T+85 99 82 -17.8

ADGB 3.125 26 Emirate of Abu Dhabi Sov Abu Dhabi B NR / AA $2500 10-yr 25/Apr T+125 150 118 -31.4

BKMBOM 3.75 21 Bank Muscat Fin Oman B Baa1 / BBB- $500 5-yr 25/Apr T+255.6 269 213 -55.3

* Pricing Z-spread is back calculated using Bloomberg data analytics by taking into consideration the issue price/reoffer price and first settlement date of the security. Hence, the number is indicative only; The priced column refers to the spread over benchmark where in “T” stands for Treasury, “MS” stands for Mid Swap, and “Y” stands for yield when T or MS spread in not available; Source: Bloomberg; NBAD

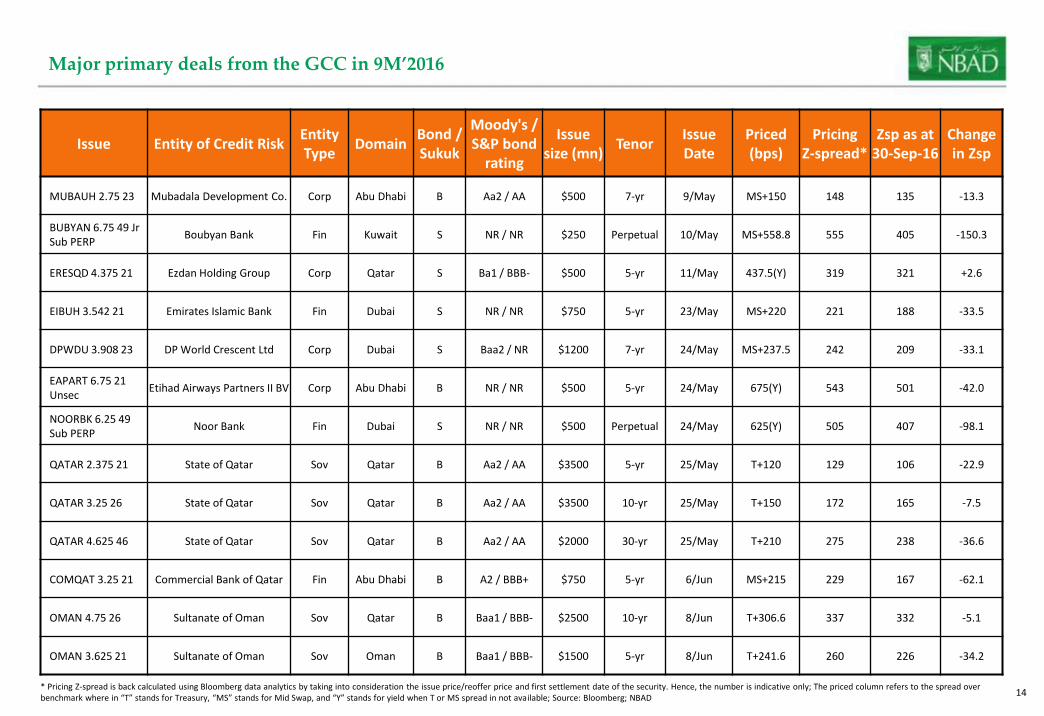

1414

Major primary deals from the GCC in 9M’2016

Issue Entity of Credit RiskEntityType

DomainBond / Sukuk

Moody's / S&P bond

rating

Issuesize (mn)

TenorIssue Date

Priced (bps)

PricingZ-spread*

Zsp as at30-Sep-16

Change in Zsp

MUBAUH 2.75 23 Mubadala Development Co. Corp Abu Dhabi B Aa2 / AA $500 7-yr 9/May MS+150 148 135 -13.3

BUBYAN 6.75 49 Jr Sub PERP

Boubyan Bank Fin Kuwait S NR / NR $250 Perpetual 10/May MS+558.8 555 405 -150.3

ERESQD 4.375 21 Ezdan Holding Group Corp Qatar S Ba1 / BBB- $500 5-yr 11/May 437.5(Y) 319 321 +2.6

EIBUH 3.542 21 Emirates Islamic Bank Fin Dubai S NR / NR $750 5-yr 23/May MS+220 221 188 -33.5

DPWDU 3.908 23 DP World Crescent Ltd Corp Dubai S Baa2 / NR $1200 7-yr 24/May MS+237.5 242 209 -33.1

EAPART 6.75 21 Unsec

Etihad Airways Partners II BV Corp Abu Dhabi B NR / NR $500 5-yr 24/May 675(Y) 543 501 -42.0

NOORBK 6.25 49Sub PERP

Noor Bank Fin Dubai S NR / NR $500 Perpetual 24/May 625(Y) 505 407 -98.1

QATAR 2.375 21 State of Qatar Sov Qatar B Aa2 / AA $3500 5-yr 25/May T+120 129 106 -22.9

QATAR 3.25 26 State of Qatar Sov Qatar B Aa2 / AA $3500 10-yr 25/May T+150 172 165 -7.5

QATAR 4.625 46 State of Qatar Sov Qatar B Aa2 / AA $2000 30-yr 25/May T+210 275 238 -36.6

COMQAT 3.25 21 Commercial Bank of Qatar Fin Abu Dhabi B A2 / BBB+ $750 5-yr 6/Jun MS+215 229 167 -62.1

OMAN 4.75 26 Sultanate of Oman Sov Qatar B Baa1 / BBB- $2500 10-yr 8/Jun T+306.6 337 332 -5.1

OMAN 3.625 21 Sultanate of Oman Sov Oman B Baa1 / BBB- $1500 5-yr 8/Jun T+241.6 260 226 -34.2

* Pricing Z-spread is back calculated using Bloomberg data analytics by taking into consideration the issue price/reoffer price and first settlement date of the security. Hence, the number is indicative only; The priced column refers to the spread over benchmark where in “T” stands for Treasury, “MS” stands for Mid Swap, and “Y” stands for yield when T or MS spread in not available; Source: Bloomberg; NBAD

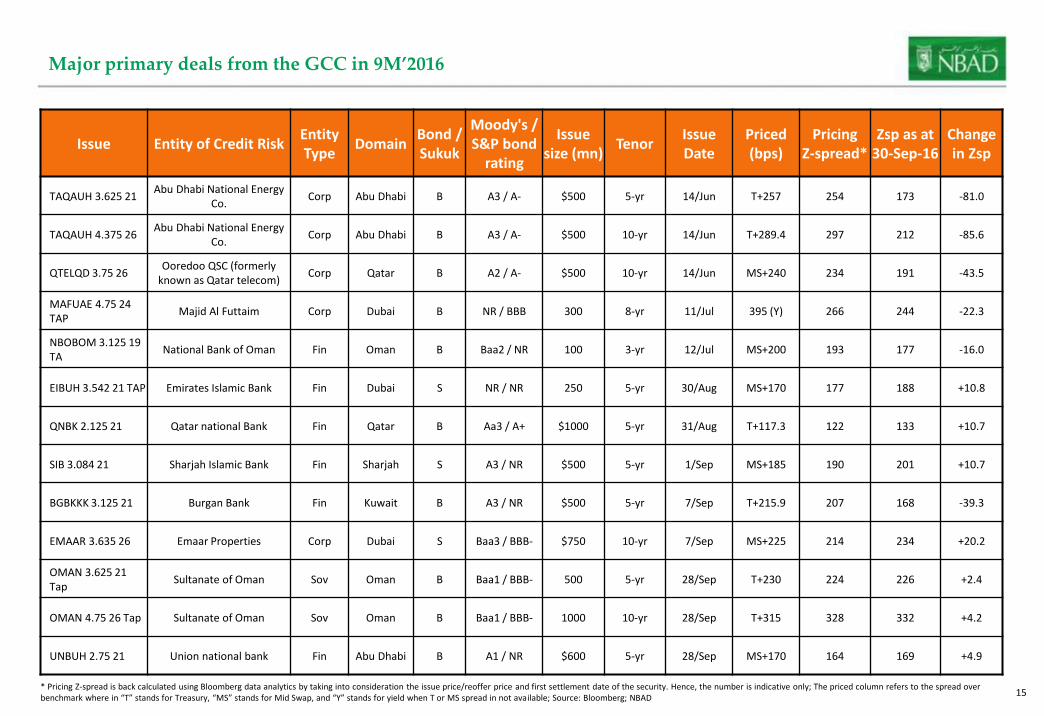

1515

Major primary deals from the GCC in 9M’2016

Issue Entity of Credit RiskEntityType

DomainBond / Sukuk

Moody's / S&P bond

rating

Issuesize (mn)

TenorIssue Date

Priced (bps)

PricingZ-spread*

Zsp as at30-Sep-16

Change in Zsp

TAQAUH 3.625 21Abu Dhabi National Energy

Co.Corp Abu Dhabi B A3 / A- $500 5-yr 14/Jun T+257 254 173 -81.0

TAQAUH 4.375 26Abu Dhabi National Energy

Co.Corp Abu Dhabi B A3 / A- $500 10-yr 14/Jun T+289.4 297 212 -85.6

QTELQD 3.75 26Ooredoo QSC (formerly

known as Qatar telecom)Corp Qatar B A2 / A- $500 10-yr 14/Jun MS+240 234 191 -43.5

MAFUAE 4.75 24 TAP

Majid Al Futtaim Corp Dubai B NR / BBB 300 8-yr 11/Jul 395 (Y) 266 244 -22.3

NBOBOM 3.125 19 TA

National Bank of Oman Fin Oman B Baa2 / NR 100 3-yr 12/Jul MS+200 193 177 -16.0

EIBUH 3.542 21 TAP Emirates Islamic Bank Fin Dubai S NR / NR 250 5-yr 30/Aug MS+170 177 188 +10.8

QNBK 2.125 21 Qatar national Bank Fin Qatar B Aa3 / A+ $1000 5-yr 31/Aug T+117.3 122 133 +10.7

SIB 3.084 21 Sharjah Islamic Bank Fin Sharjah S A3 / NR $500 5-yr 1/Sep MS+185 190 201 +10.7

BGBKKK 3.125 21 Burgan Bank Fin Kuwait B A3 / NR $500 5-yr 7/Sep T+215.9 207 168 -39.3

EMAAR 3.635 26 Emaar Properties Corp Dubai S Baa3 / BBB- $750 10-yr 7/Sep MS+225 214 234 +20.2

OMAN 3.625 21 Tap

Sultanate of Oman Sov Oman B Baa1 / BBB- 500 5-yr 28/Sep T+230 224 226 +2.4

OMAN 4.75 26 Tap Sultanate of Oman Sov Oman B Baa1 / BBB- 1000 10-yr 28/Sep T+315 328 332 +4.2

UNBUH 2.75 21 Union national bank Fin Abu Dhabi B A1 / NR $600 5-yr 28/Sep MS+170 164 169 +4.9

* Pricing Z-spread is back calculated using Bloomberg data analytics by taking into consideration the issue price/reoffer price and first settlement date of the security. Hence, the number is indicative only; The priced column refers to the spread over benchmark where in “T” stands for Treasury, “MS” stands for Mid Swap, and “Y” stands for yield when T or MS spread in not available; Source: Bloomberg; NBAD

1616

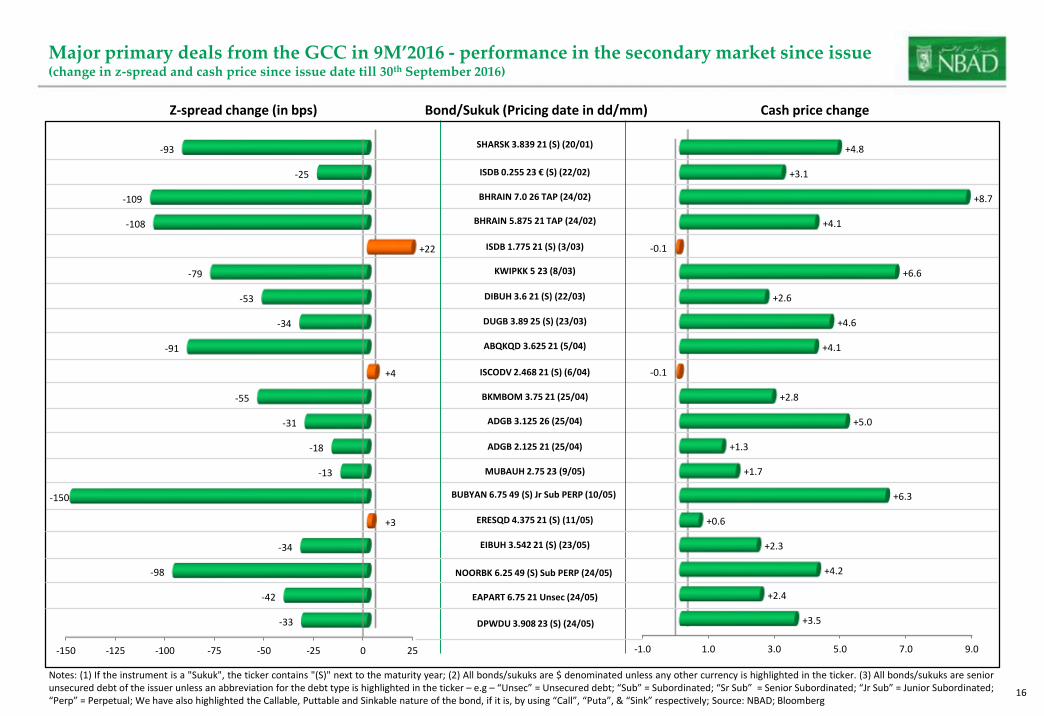

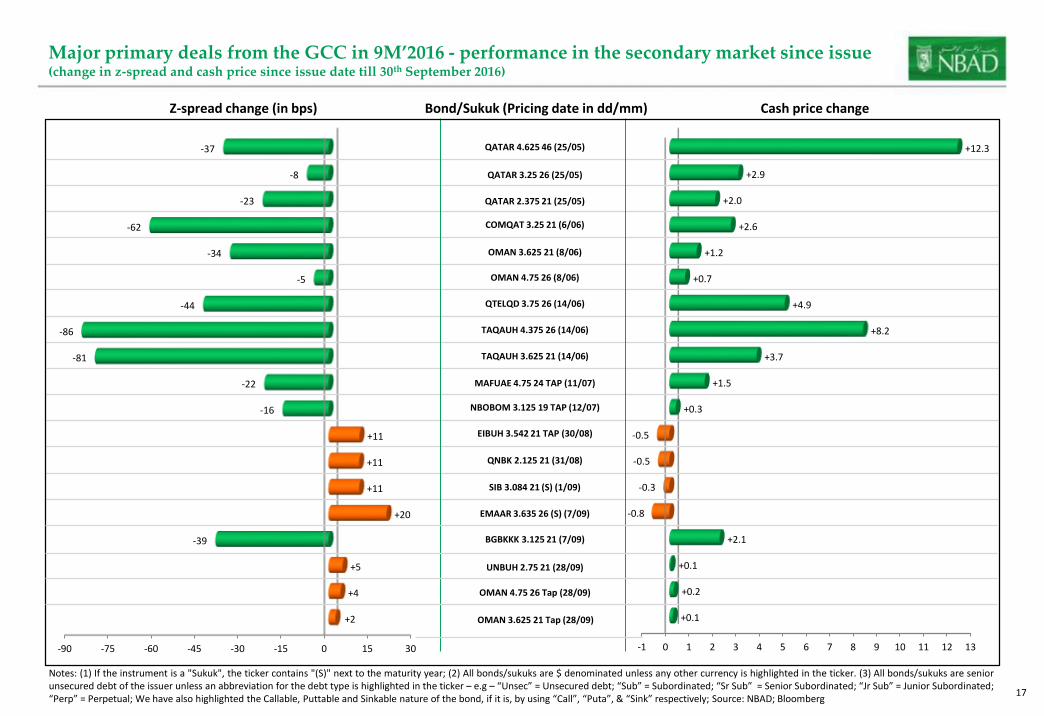

Major primary deals from the GCC in 9M’2016 - performance in the secondary market since issue(change in z-spread and cash price since issue date till 30th September 2016)

-1.0 1.0 3.0 5.0 7.0 9.0

+3.5

+2.4

+4.2

+2.3

+0.6

+6.3

+1.7

+1.3

+5.0

+2.8

-0.1

+4.1

+4.6

+2.6

+6.6

-0.1

+4.1

+8.7

+3.1

+4.8

Notes: (1) If the instrument is a "Sukuk", the ticker contains "(S)" next to the maturity year; (2) All bonds/sukuks are $ denominated unless any other currency is highlighted in the ticker. (3) All bonds/sukuks are seniorunsecured debt of the issuer unless an abbreviation for the debt type is highlighted in the ticker – e.g – “Unsec” = Unsecured debt; “Sub” = Subordinated; “Sr Sub” = Senior Subordinated; “Jr Sub” = Junior Subordinated;“Perp” = Perpetual; We have also highlighted the Callable, Puttable and Sinkable nature of the bond, if it is, by using “Call”, “Puta”, & “Sink” respectively; Source: NBAD; Bloomberg

Z-spread change (in bps) Cash price change

-150 -125 -100 -75 -50 -25 0 25

-33

-42

-98

-34

+3

-150

-13

-18

-31

-55

+4

-91

-34

-53

-79

+22

-108

-109

-25

-93

Bond/Sukuk (Pricing date in dd/mm)

SHARSK 3.839 21 (S) (20/01)

ISDB 0.255 23 € (S) (22/02)

BHRAIN 7.0 26 TAP (24/02)

BHRAIN 5.875 21 TAP (24/02)

KWIPKK 5 23 (8/03)

DIBUH 3.6 21 (S) (22/03)

ABQKQD 3.625 21 (5/04)

DUGB 3.89 25 (S) (23/03)

ISCODV 2.468 21 (S) (6/04)

ADGB 3.125 26 (25/04)

BKMBOM 3.75 21 (25/04)

ERESQD 4.375 21 (S) (11/05)

ADGB 2.125 21 (25/04)

MUBAUH 2.75 23 (9/05)

BUBYAN 6.75 49 (S) Jr Sub PERP (10/05)

NOORBK 6.25 49 (S) Sub PERP (24/05)

EIBUH 3.542 21 (S) (23/05)

ISDB 1.775 21 (S) (3/03)

EAPART 6.75 21 Unsec (24/05)

DPWDU 3.908 23 (S) (24/05)

1717

Major primary deals from the GCC in 9M’2016 - performance in the secondary market since issue(change in z-spread and cash price since issue date till 30th September 2016)

-1 0 1 2 3 4 5 6 7 8 9 10 11 12 13

+0.1

+0.2

+0.1

+2.1

-0.8

-0.3

-0.5

-0.5

+0.3

+1.5

+3.7

+8.2

+4.9

+0.7

+1.2

+2.6

+2.0

+2.9

+12.3

Notes: (1) If the instrument is a "Sukuk", the ticker contains "(S)" next to the maturity year; (2) All bonds/sukuks are $ denominated unless any other currency is highlighted in the ticker. (3) All bonds/sukuks are seniorunsecured debt of the issuer unless an abbreviation for the debt type is highlighted in the ticker – e.g – “Unsec” = Unsecured debt; “Sub” = Subordinated; “Sr Sub” = Senior Subordinated; “Jr Sub” = Junior Subordinated;“Perp” = Perpetual; We have also highlighted the Callable, Puttable and Sinkable nature of the bond, if it is, by using “Call”, “Puta”, & “Sink” respectively; Source: NBAD; Bloomberg

Z-spread change (in bps) Cash price change

-90 -75 -60 -45 -30 -15 0 15 30

+2

+4

+5

-39

+20

+11

+11

+11

-16

-22

-81

-86

-44

-5

-34

-62

-23

-8

-37

Bond/Sukuk (Pricing date in dd/mm)

QATAR 4.625 46 (25/05)

QATAR 3.25 26 (25/05)

QATAR 2.375 21 (25/05)

COMQAT 3.25 21 (6/06)

OMAN 4.75 26 (8/06)

QTELQD 3.75 26 (14/06)

TAQAUH 4.375 26 (14/06)

TAQAUH 3.625 21 (14/06)

NBOBOM 3.125 19 TAP (12/07)

MAFUAE 4.75 24 TAP (11/07)

EMAAR 3.635 26 (S) (7/09)

EIBUH 3.542 21 TAP (30/08)

QNBK 2.125 21 (31/08)

SIB 3.084 21 (S) (1/09)

UNBUH 2.75 21 (28/09)

BGBKKK 3.125 21 (7/09)

OMAN 3.625 21 (8/06)

OMAN 4.75 26 Tap (28/09)

OMAN 3.625 21 Tap (28/09)

1818

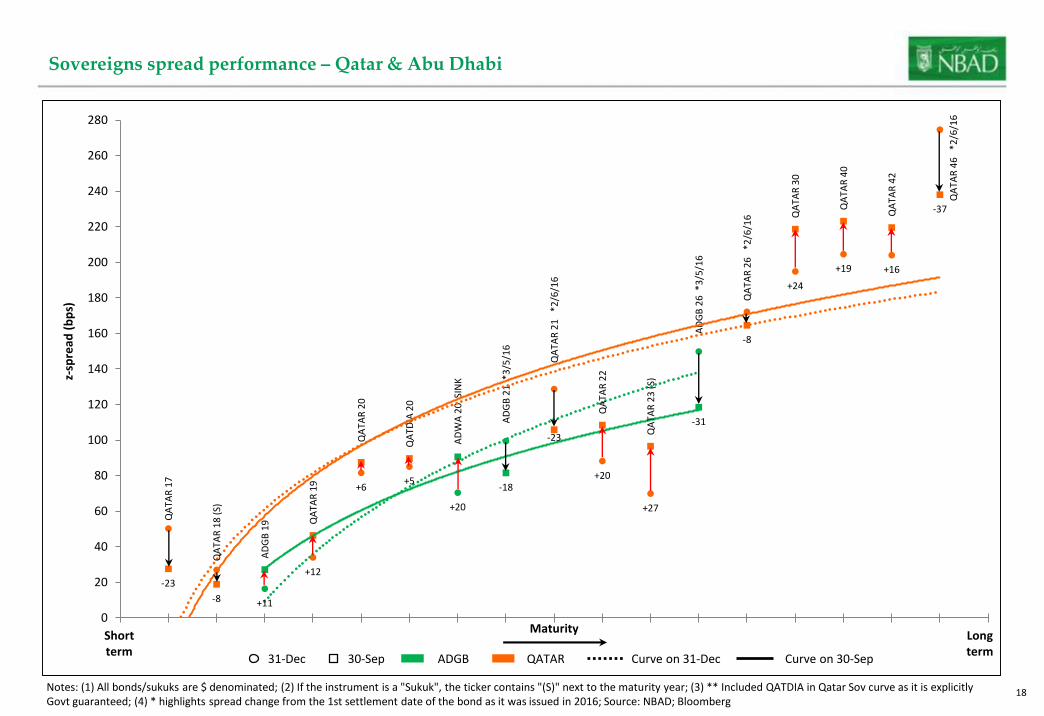

Sovereigns spread performance – Qatar & Abu Dhabi

AD

GB

19

AD

WA

20

SIN

K

AD

GB

21

*3

/5/1

6

AD

GB

26

*3

/5/1

6

QA

TAR

17

QA

TAR

18

(S)

QA

TAR

19

QA

TAR

20

QA

TDIA

20

QA

TAR

22

QA

TAR

23

(S)

QA

TAR

30

QA

TAR

40

QA

TAR

42

QA

TAR

21

*2

/6/1

6

QA

TAR

26

*2

/6/1

6

QA

TAR

46

*2

/6/1

6

+11

+20

-18

-31

-23

-8

+12

+6+5

+20

+27

+24

+19 +16

-23

-8

-37

0

20

40

60

80

100

120

140

160

180

200

220

240

260

280

z-sp

read

(b

ps)

Maturity

30-Sep31-Dec ADGB QATAR

Longterm

Shortterm

Notes: (1) All bonds/sukuks are $ denominated; (2) If the instrument is a "Sukuk", the ticker contains "(S)" next to the maturity year; (3) ** Included QATDIA in Qatar Sov curve as it is explicitly Govt guaranteed; (4) * highlights spread change from the 1st settlement date of the bond as it was issued in 2016; Source: NBAD; Bloomberg

Curve on 31-Dec Curve on 30-Sep

1919

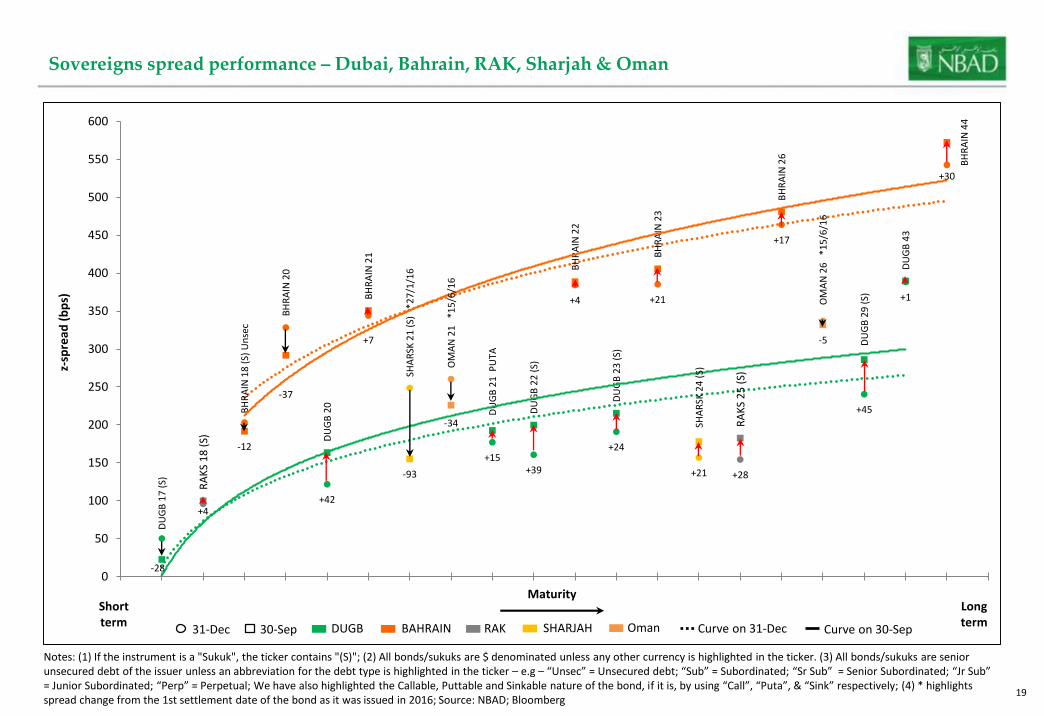

Sovereigns spread performance – Dubai, Bahrain, RAK, Sharjah & Oman

DU

GB

17

(S)

DU

GB

20

DU

GB

21

PU

TA

DU

GB

22

(S)

DU

GB

23

(S)

DU

GB

29

(S)

DU

GB

43

BH

RA

IN 1

8 (

S) U

nse

c

BH

RA

IN 2

0

BH

RA

IN 2

1

BH

RA

IN 2

2

BH

RA

IN 2

3

BH

RA

IN 2

6

BH

RA

IN 4

4

RA

KS

18

(S)

RA

KS

25

(S)

SHA

RSK

21

(S)

*2

7/1

/16

SHA

RSK

24

(S)

OM

AN

21

*1

5/6

/16

OM

AN

26

*1

5/6

/16

-28

+42

+15+39

+24

+45

+1

-12

-37

+7

+4 +21

+17

+30

+4

+28-93 +21

-34

-5

0

50

100

150

200

250

300

350

400

450

500

550

600

z-sp

read

(b

ps)

MaturityLongterm

Shortterm

Notes: (1) If the instrument is a "Sukuk", the ticker contains "(S)"; (2) All bonds/sukuks are $ denominated unless any other currency is highlighted in the ticker. (3) All bonds/sukuks are senior unsecured debt of the issuer unless an abbreviation for the debt type is highlighted in the ticker – e.g – “Unsec” = Unsecured debt; “Sub” = Subordinated; “Sr Sub” = Senior Subordinated; “Jr Sub” = Junior Subordinated; “Perp” = Perpetual; We have also highlighted the Callable, Puttable and Sinkable nature of the bond, if it is, by using “Call”, “Puta”, & “Sink” respectively; (4) * highlights spread change from the 1st settlement date of the bond as it was issued in 2016; Source: NBAD; Bloomberg

30-Sep31-Dec DUGB BAHRAIN Curve on 31-Dec Curve on 30-SepRAK SHARJAH Oman

2020

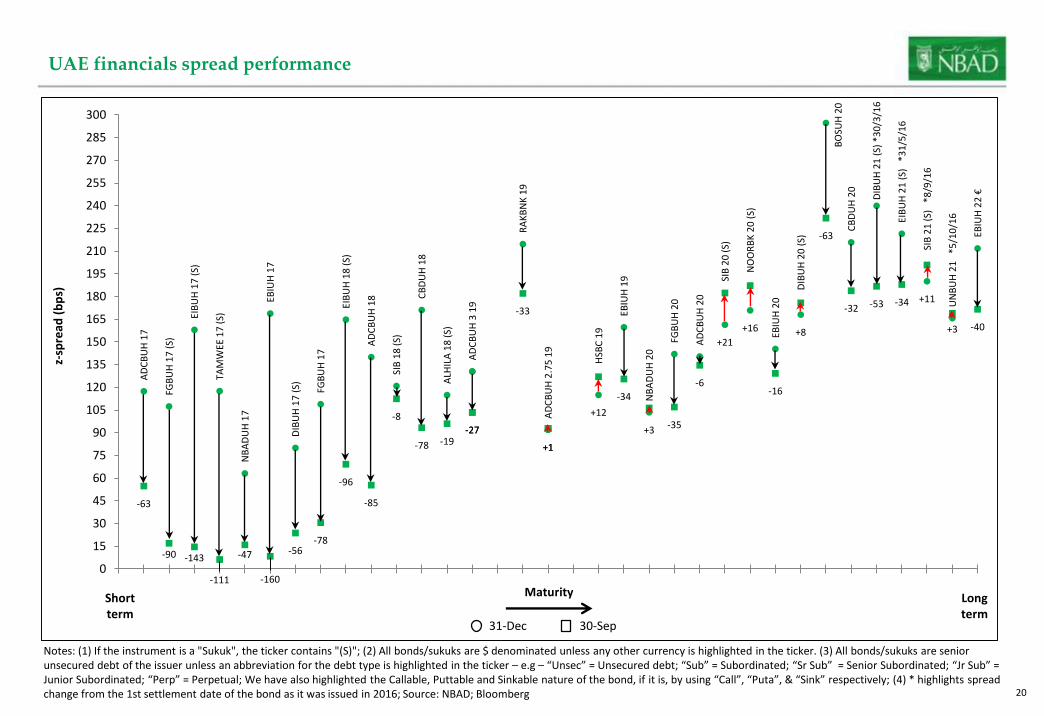

UAE financials spread performance

Notes: (1) If the instrument is a "Sukuk", the ticker contains "(S)"; (2) All bonds/sukuks are $ denominated unless any other currency is highlighted in the ticker. (3) All bonds/sukuks are senior unsecured debt of the issuer unless an abbreviation for the debt type is highlighted in the ticker – e.g – “Unsec” = Unsecured debt; “Sub” = Subordinated; “Sr Sub” = Senior Subordinated; “Jr Sub” = Junior Subordinated; “Perp” = Perpetual; We have also highlighted the Callable, Puttable and Sinkable nature of the bond, if it is, by using “Call”, “Puta”, & “Sink” respectively; (4) * highlights spread change from the 1st settlement date of the bond as it was issued in 2016; Source: NBAD; Bloomberg

AD

CB

UH

17

FGB

UH

17

(S)

EIB

UH

17

(S)

TAM

WEE

17

(S)

NB

AD

UH

17

EBIU

H 1

7

DIB

UH

17

(S)

FGB

UH

17

EIB

UH

18

(S)

AD

CB

UH

18

SIB

18

(S)

CB

DU

H 1

8

ALH

ILA

18

(S)

AD

CB

UH

3 1

9

RA

KB

NK

19

AD

CB

UH

2.7

5 1

9

HSB

C 1

9

EBIU

H 1

9

NB

AD

UH

20

FGB

UH

20

AD

CB

UH

20

SIB

20

(S)

NO

OR

BK

20

(S)

EBIU

H 2

0

DIB

UH

20

(S)

BO

SUH

20

C

BD

UH

20

DIB

UH

21

(S)

*3

0/3

/16

EIB

UH

21

(S)

*3

1/5

/16

SIB

21

(S)

*8

/9/1

6

UN

BU

H 2

1

*5/1

0/1

6

EBIU

H 2

2 €

-63

-90 -143

-111

-47

-160

-56-78

-96

-85

-8

-78 -19-27-27

-33

+1+1

+12

-34

+3 -35

-6

+21

+16

-16

+8

-63

-32 -53 -34 +11

+3 -40

0

15

30

45

60

75

90

105

120

135

150

165

180

195

210

225

240

255

270

285

300

z-sp

read

(b

ps)

Maturity Longterm

Shortterm

30-Sep31-Dec

2121

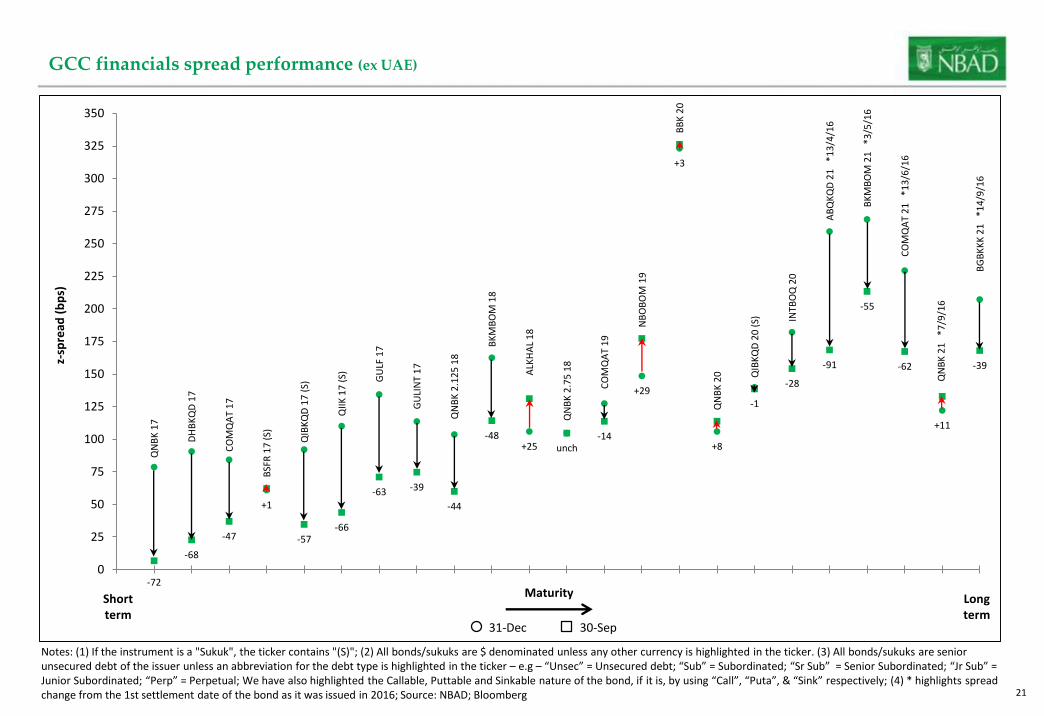

GCC financials spread performance (ex UAE)

Notes: (1) If the instrument is a "Sukuk", the ticker contains "(S)"; (2) All bonds/sukuks are $ denominated unless any other currency is highlighted in the ticker. (3) All bonds/sukuks are senior unsecured debt of the issuer unless an abbreviation for the debt type is highlighted in the ticker – e.g – “Unsec” = Unsecured debt; “Sub” = Subordinated; “Sr Sub” = Senior Subordinated; “Jr Sub” = Junior Subordinated; “Perp” = Perpetual; We have also highlighted the Callable, Puttable and Sinkable nature of the bond, if it is, by using “Call”, “Puta”, & “Sink” respectively; (4) * highlights spread change from the 1st settlement date of the bond as it was issued in 2016; Source: NBAD; Bloomberg

QN

BK

17

DH

BK

QD

17

CO

MQ

AT

17

BSF

R 1

7 (

S)

QIB

KQ

D 1

7 (

S)

QII

K 1

7 (

S)

GU

LF 1

7

GU

LIN

T 1

7

QN

BK

2.1

25

18

BK

MB

OM

18

ALK

HA

L 1

8

QN

BK

2.7

5 1

8

CO

MQ

AT

19

NB

OB

OM

19

BB

K 2

0

QN

BK

20

QIB

KQ

D 2

0 (

S)

INTB

OQ

20

AB

QK

QD

21

*1

3/4

/16

BK

MB

OM

21

*3

/5/1

6

CO

MQ

AT

21

*1

3/6

/16

QN

BK

21

*7

/9/1

6

BG

BK

KK

21

*1

4/9

/16

-72

-68

-47

+1

-57-66

-63 -39

-44

-48+25 unch

-14

+29

+3

+8

-1

-28

-91

-55

-62

+11

-39

0

25

50

75

100

125

150

175

200

225

250

275

300

325

350

z-sp

read

(b

ps)

Maturity Longterm

Shortterm

30-Sep31-Dec

2222

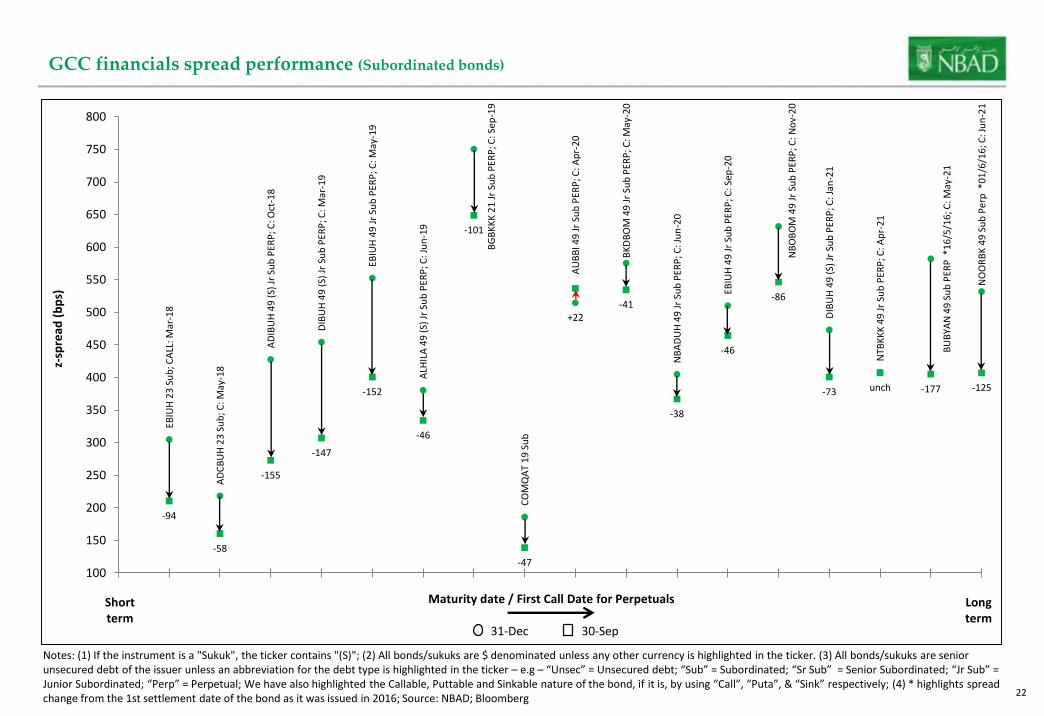

GCC financials spread performance (Subordinated bonds)

Notes: (1) If the instrument is a "Sukuk", the ticker contains "(S)"; (2) All bonds/sukuks are $ denominated unless any other currency is highlighted in the ticker. (3) All bonds/sukuks are senior unsecured debt of the issuer unless an abbreviation for the debt type is highlighted in the ticker – e.g – “Unsec” = Unsecured debt; “Sub” = Subordinated; “Sr Sub” = Senior Subordinated; “Jr Sub” = Junior Subordinated; “Perp” = Perpetual; We have also highlighted the Callable, Puttable and Sinkable nature of the bond, if it is, by using “Call”, “Puta”, & “Sink” respectively; (4) * highlights spread change from the 1st settlement date of the bond as it was issued in 2016; Source: NBAD; Bloomberg

EBIU

H 2

3 S

ub

; CA

LL: M

ar-1

8

AD

CB

UH

23

Su

b; C

: May

-18

AD

IBU

H 4

9 (

S) J

r Su

b P

ERP

; C: O

ct-1

8

DIB

UH

49

(S)

Jr

Sub

PER

P; C

: Mar

-19

EBIU

H 4

9 J

r Su

b P

ERP

; C: M

ay-1

9

ALH

ILA

49

(S)

Jr

Sub

PER

P; C

: Ju

n-1

9

BG

BK

KK

21

Jr

Sub

PER

P; C

: Sep

-19

CO

MQ

AT

19

Su

b

AU

BB

I 49

Jr

Sub

PER

P; C

: Ap

r-2

0

BK

DB

OM

49

Jr

Sub

PER

P; C

: May

-20

NB

AD

UH

49

Jr

Sub

PER

P; C

: Ju

n-2

0

EBIU

H 4

9 J

r Su

b P

ERP

; C: S

ep-2

0

NB

OB

OM

49

Jr

Sub

PER

P; C

: No

v-2

0

DIB

UH

49

(S)

Jr

Sub

PER

P; C

: Jan

-21

NTB

KK

K 4

9 J

r Su

b P

ERP

; C: A

pr-

21

BU

BYA

N 4

9 S

ub

PER

P *

16

/5/1

6; C

: May

-21

NO

OR

BK

49

Su

b P

erp

*0

1/6

/16

; C: J

un

-21

-94

-58

-155

-147

-152

-46

-101

-47

+22-41

-38

-46

-86

-73 unch -177 -125

100

150

200

250

300

350

400

450

500

550

600

650

700

750

800

z-sp

read

(b

ps)

Maturity date / First Call Date for Perpetuals Longterm

Shortterm

30-Sep31-Dec

2323

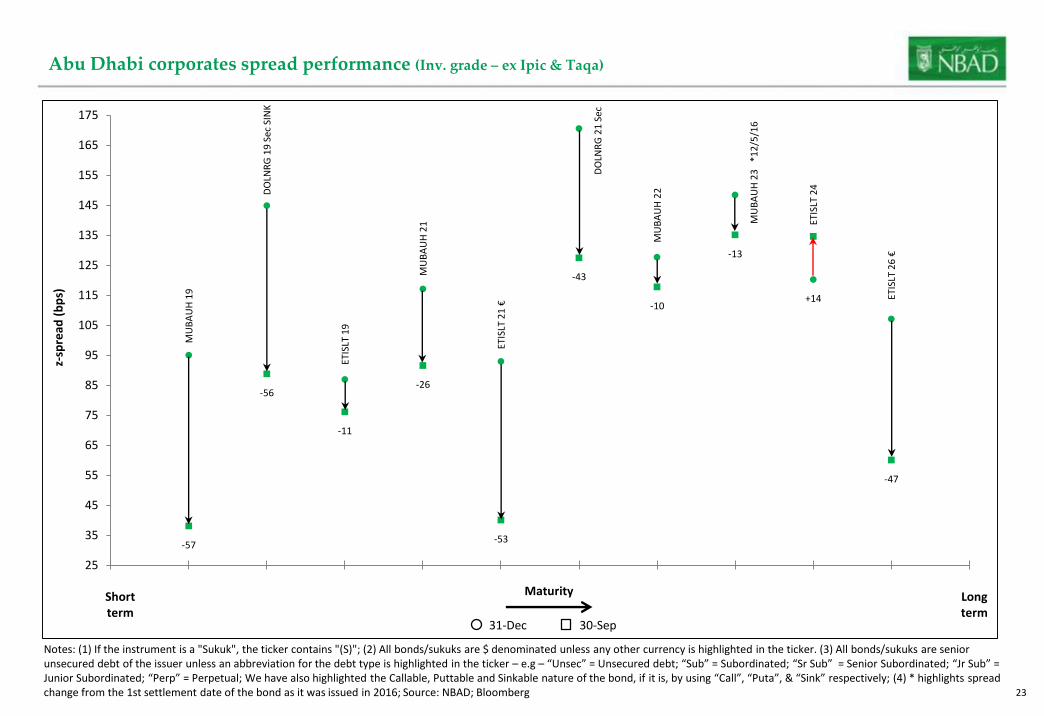

Abu Dhabi corporates spread performance (Inv. grade – ex Ipic & Taqa)

Notes: (1) If the instrument is a "Sukuk", the ticker contains "(S)"; (2) All bonds/sukuks are $ denominated unless any other currency is highlighted in the ticker. (3) All bonds/sukuks are senior unsecured debt of the issuer unless an abbreviation for the debt type is highlighted in the ticker – e.g – “Unsec” = Unsecured debt; “Sub” = Subordinated; “Sr Sub” = Senior Subordinated; “Jr Sub” = Junior Subordinated; “Perp” = Perpetual; We have also highlighted the Callable, Puttable and Sinkable nature of the bond, if it is, by using “Call”, “Puta”, & “Sink” respectively; (4) * highlights spread change from the 1st settlement date of the bond as it was issued in 2016; Source: NBAD; Bloomberg

MU

BA

UH

19

DO

LNR

G 1

9 S

ec S

INK

ETIS

LT 1

9

MU

BA

UH

21

ETIS

LT 2

1 €

DO

LNR

G 2

1 S

ec

MU

BA

UH

22

MU

BA

UH

23

*1

2/5

/16

ETIS

LT 2

4

ETIS

LT 2

6 €

-57

-56

-11

-26

-53

-43

-10

-13

+14

-47

25

35

45

55

65

75

85

95

105

115

125

135

145

155

165

175

z-sp

read

(b

ps)

Maturity Longterm

Shortterm

30-Sep31-Dec

2424

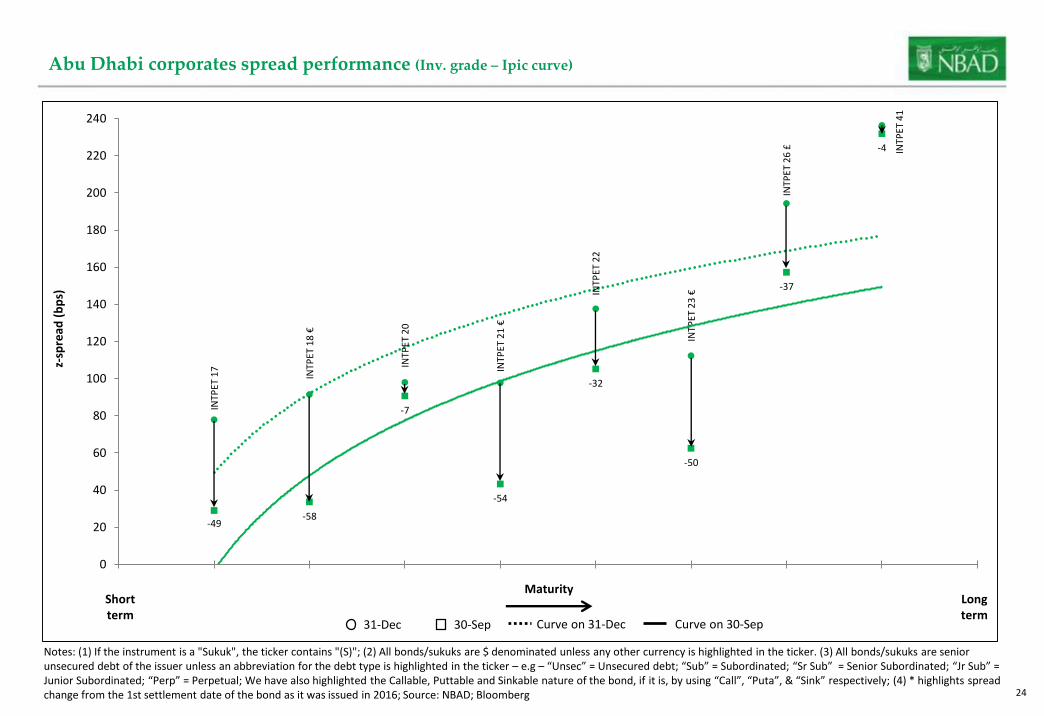

Abu Dhabi corporates spread performance (Inv. grade – Ipic curve)

Notes: (1) If the instrument is a "Sukuk", the ticker contains "(S)"; (2) All bonds/sukuks are $ denominated unless any other currency is highlighted in the ticker. (3) All bonds/sukuks are senior unsecured debt of the issuer unless an abbreviation for the debt type is highlighted in the ticker – e.g – “Unsec” = Unsecured debt; “Sub” = Subordinated; “Sr Sub” = Senior Subordinated; “Jr Sub” = Junior Subordinated; “Perp” = Perpetual; We have also highlighted the Callable, Puttable and Sinkable nature of the bond, if it is, by using “Call”, “Puta”, & “Sink” respectively; (4) * highlights spread change from the 1st settlement date of the bond as it was issued in 2016; Source: NBAD; Bloomberg

INTP

ET 1

7

INTP

ET 1

8 €

INTP

ET 2

0

INTP

ET 2

1 €

INTP

ET 2

2

INTP

ET 2

3 €

INTP

ET 2

6 £

INTP

ET 4

1

-49-58

-7

-54

-32

-50

-37

-4

0

20

40

60

80

100

120

140

160

180

200

220

240

z-sp

read

(b

ps)

MaturityLongterm

Shortterm

30-Sep31-Dec Curve on 31-Dec Curve on 30-Sep

2525

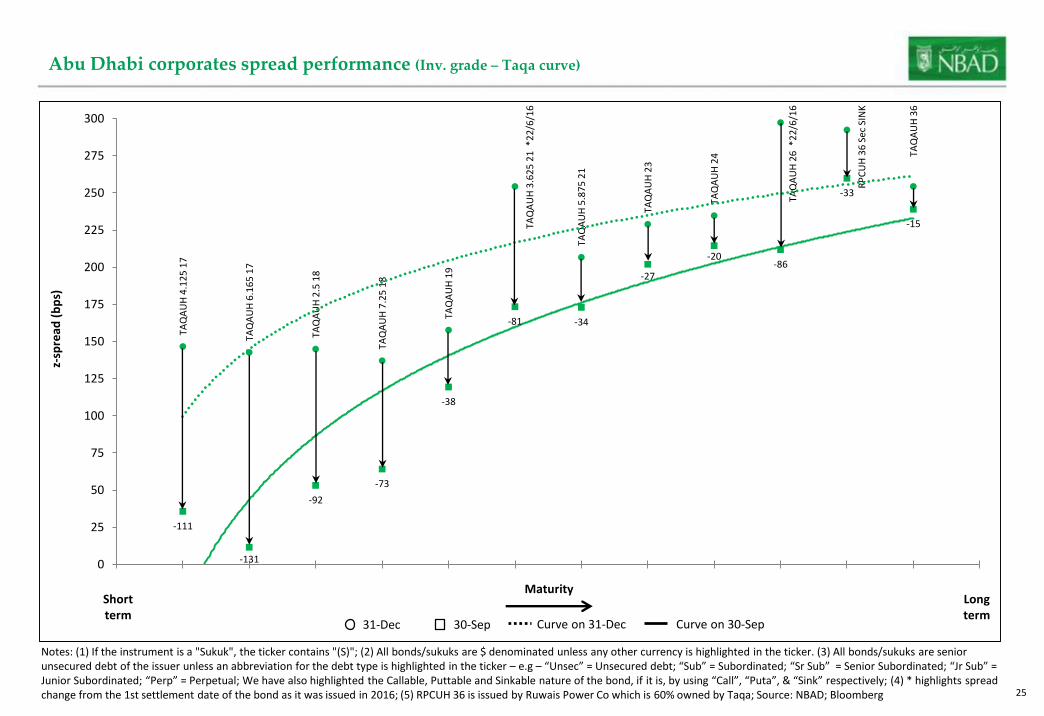

Abu Dhabi corporates spread performance (Inv. grade – Taqa curve)

TAQ

AU

H 4

.12

5 1

7

TAQ

AU

H 6

.16

5 1

7

TAQ

AU

H 2

.5 1

8

TAQ

AU

H 7

.25

18

TAQ

AU

H 1

9

TAQ

AU

H 3

.62

5 2

1 *

22

/6/1

6

TAQ

AU

H 5

.87

5 2

1

TAQ

AU

H 2

3

TAQ

AU

H 2

4

TAQ

AU

H 2

6 *

22

/6/1

6

RP

CU

H 3

6 S

ec S

INK

TAQ

AU

H 3

6

-111

-131

-92

-73

-38

-81 -34

-27

-20-86

-33

-15

0

25

50

75

100

125

150

175

200

225

250

275

300

z-sp

read

(b

ps)

Maturity

Notes: (1) If the instrument is a "Sukuk", the ticker contains "(S)"; (2) All bonds/sukuks are $ denominated unless any other currency is highlighted in the ticker. (3) All bonds/sukuks are senior unsecured debt of the issuer unless an abbreviation for the debt type is highlighted in the ticker – e.g – “Unsec” = Unsecured debt; “Sub” = Subordinated; “Sr Sub” = Senior Subordinated; “Jr Sub” = Junior Subordinated; “Perp” = Perpetual; We have also highlighted the Callable, Puttable and Sinkable nature of the bond, if it is, by using “Call”, “Puta”, & “Sink” respectively; (4) * highlights spread change from the 1st settlement date of the bond as it was issued in 2016; (5) RPCUH 36 is issued by Ruwais Power Co which is 60% owned by Taqa; Source: NBAD; Bloomberg

Longterm

Shortterm

30-Sep31-Dec Curve on 31-Dec Curve on 30-Sep

2626

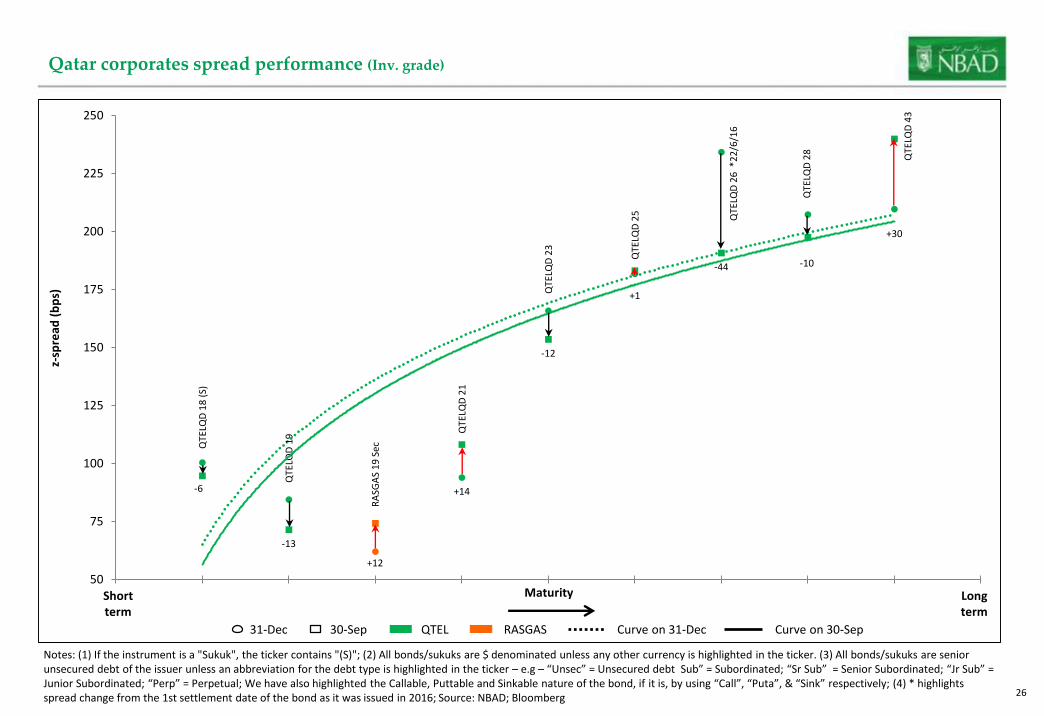

Qatar corporates spread performance (Inv. grade)

RA

SGA

S 1

9 S

ec

QTE

LQD

18

(S)

QTE

LQD

19

QTE

LQD

21

QTE

LQD

23

QTE

LQD

25

QTE

LQD

26

*2

2/6

/16

QTE

LQD

28

QTE

LQD

43

+12

-6

-13

+14

-12

+1

-44 -10

+30

50

75

100

125

150

175

200

225

250

z-sp

read

(b

ps)

Maturity

Notes: (1) If the instrument is a "Sukuk", the ticker contains "(S)"; (2) All bonds/sukuks are $ denominated unless any other currency is highlighted in the ticker. (3) All bonds/sukuks are senior unsecured debt of the issuer unless an abbreviation for the debt type is highlighted in the ticker – e.g – “Unsec” = Unsecured debt Sub” = Subordinated; “Sr Sub” = Senior Subordinated; “Jr Sub” = Junior Subordinated; “Perp” = Perpetual; We have also highlighted the Callable, Puttable and Sinkable nature of the bond, if it is, by using “Call”, “Puta”, & “Sink” respectively; (4) * highlights spread change from the 1st settlement date of the bond as it was issued in 2016; Source: NBAD; Bloomberg

Longterm

Shortterm

30-Sep31-Dec RASGASQTEL Curve on 31-Dec Curve on 30-Sep

2727

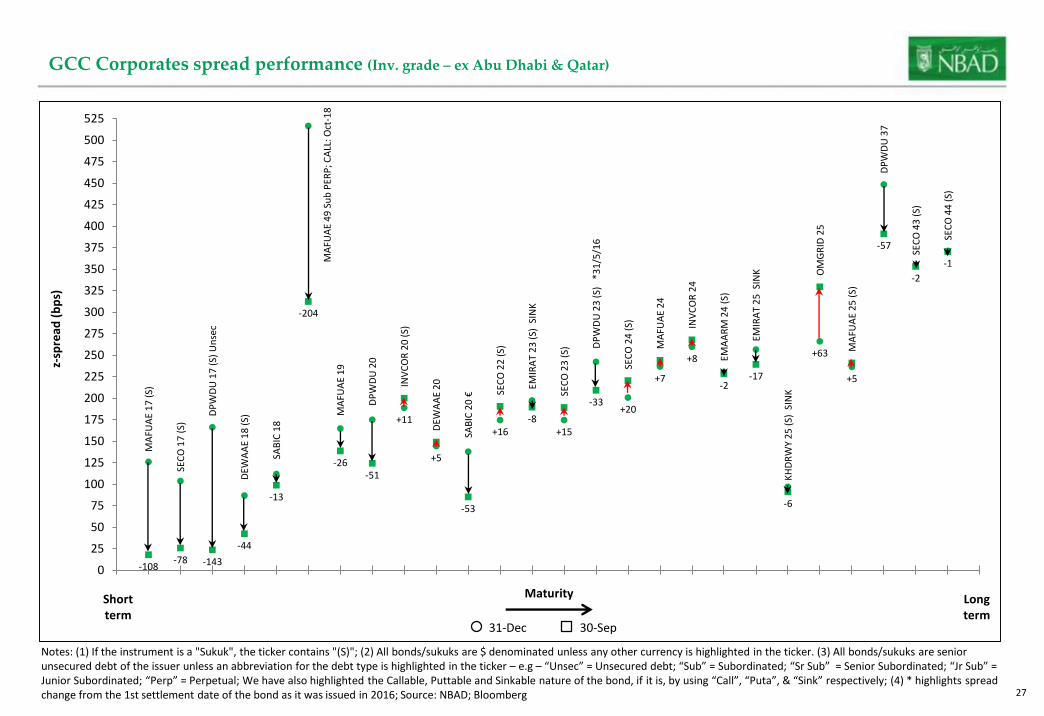

GCC Corporates spread performance (Inv. grade – ex Abu Dhabi & Qatar)

Notes: (1) If the instrument is a "Sukuk", the ticker contains "(S)"; (2) All bonds/sukuks are $ denominated unless any other currency is highlighted in the ticker. (3) All bonds/sukuks are senior unsecured debt of the issuer unless an abbreviation for the debt type is highlighted in the ticker – e.g – “Unsec” = Unsecured debt; “Sub” = Subordinated; “Sr Sub” = Senior Subordinated; “Jr Sub” = Junior Subordinated; “Perp” = Perpetual; We have also highlighted the Callable, Puttable and Sinkable nature of the bond, if it is, by using “Call”, “Puta”, & “Sink” respectively; (4) * highlights spread change from the 1st settlement date of the bond as it was issued in 2016; Source: NBAD; Bloomberg

MA

FUA

E 1

7 (

S)

SEC

O 1

7 (

S)

DP

WD

U 1

7 (

S) U

nse

c

DEW

AA

E 1

8 (

S)

SAB

IC 1

8

MA

FUA

E 4

9 S

ub

PER

P; C

ALL

: Oct

-18

MA

FUA

E 1

9

DP

WD

U 2

0

INV

CO

R 2

0 (

S)

DEW

AA

E 2

0

SAB

IC 2

0 € SE

CO

22

(S)

EMIR

AT

23

(S)

SIN

K

SEC

O 2

3 (

S) DP

WD

U 2

3 (

S)

*31

/5/1

6

SEC

O 2

4 (

S)

MA

FUA

E 2

4

INV

CO

R 2

4

EMA

AR

M 2

4 (

S)

EMIR

AT

25

SIN

K

KH

DR

WY

25

(S)

SIN

K

OM

GR

ID 2

5

MA

FUA

E 2

5 (

S)

DP

WD

U 3

7

SEC

O 4

3 (

S)

SEC

O 4

4 (

S)

-108-78 -143

-44

-13

-204

-26-51

+11

+5

-53

+16-8

+15

-33+20

+7

+8

-2-17

-6

+63

+5

-57

-2

-1

0

25

50

75

100

125

150

175

200

225

250

275

300

325

350

375

400

425

450

475

500

525

z-sp

read

(b

ps)

Maturity Longterm

Shortterm

30-Sep31-Dec

2828

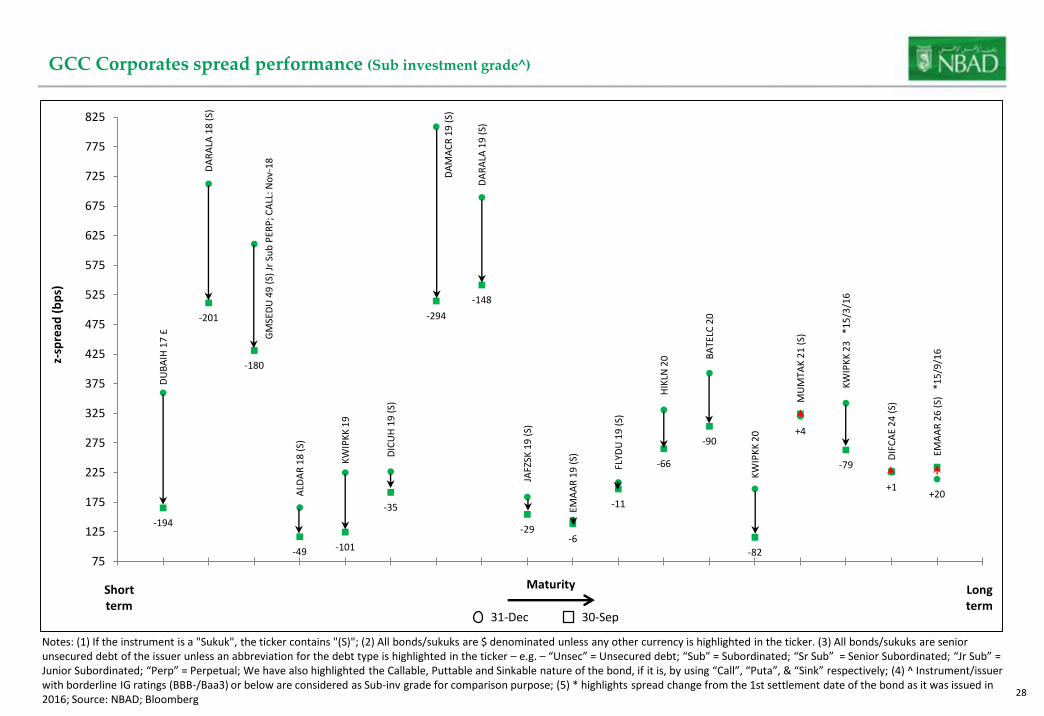

GCC Corporates spread performance (Sub investment grade^)

Notes: (1) If the instrument is a "Sukuk", the ticker contains "(S)"; (2) All bonds/sukuks are $ denominated unless any other currency is highlighted in the ticker. (3) All bonds/sukuks are senior unsecured debt of the issuer unless an abbreviation for the debt type is highlighted in the ticker – e.g. – “Unsec” = Unsecured debt; “Sub” = Subordinated; “Sr Sub” = Senior Subordinated; “Jr Sub” = Junior Subordinated; “Perp” = Perpetual; We have also highlighted the Callable, Puttable and Sinkable nature of the bond, if it is, by using “Call”, “Puta”, & “Sink” respectively; (4) ^ Instrument/issuer with borderline IG ratings (BBB-/Baa3) or below are considered as Sub-inv grade for comparison purpose; (5) * highlights spread change from the 1st settlement date of the bond as it was issued in 2016; Source: NBAD; Bloomberg

DU

BA

IH 1

7 £

DA

RA

LA 1

8 (

S)

GM

SED

U 4

9 (

S) J

r Su

b P

ERP

; CA

LL: N

ov-

18

ALD

AR

18

(S)

KW

IPK

K 1

9

DIC

UH

19

(S)

DA

MA

CR

19

(S)

DA

RA

LA 1

9 (

S)

JAFZ

SK 1

9 (

S)

EMA

AR

19

(S)

FLYD

U 1

9 (

S)

HIK

LN 2

0 BA

TELC

20

KW

IPK

K 2

0

MU

MTA

K 2

1 (

S)

KW

IPK

K 2

3

*15

/3/1

6

DIF

CA

E 2

4 (

S)

EMA

AR

26

(S)

*1

5/9

/16

-194

-201

-180

-49 -101

-35

-294

-148

-29-6

-11

-66

-90

-82

+4

-79

+1+20

75

125

175

225

275

325

375

425

475

525

575

625

675

725

775

825

z-sp

read

(b

ps)

Maturity Longterm

Shortterm

30-Sep31-Dec

2929

As mentioned in slide # 7 & 8, we have used “composite ratings” for the credit quality analysis – i.e. the average of the ratings assigned by three leading rating agencies Moody’s, S&P and Fitch – in order to provide a more representative view of the credit strength of each bank.

The composite rating is calculated as follows:

A score is assigned to the rating from each rating agency: AAA or equivalent being the best with a score of “1”, followed by AA+ or equivalent as “2”, AA or equivalent as “3”, AA- or equivalent as “4” and so on;

For example NBAD is rated Aa3/AA-/AA- by Moody’s/S&P/Fitch. So the scores are 4/4/4;

Hence the average of the scores is “4” which indicates a composite rating of “AA-” for NBAD;

In case the average score is not an absolute number – e.g. 4.33 (average of 4, 5, & 4 ) – the final score is derived by rounding off the average score to the nearest whole number. In this case “4”.

Appendix

3030

Rakesh Sahu / Chavan BhogaitaMarket Insights & StrategyGlobal MarketsNational Bank of Abu DhabiTel: +971 2 6110 [email protected]

Contact