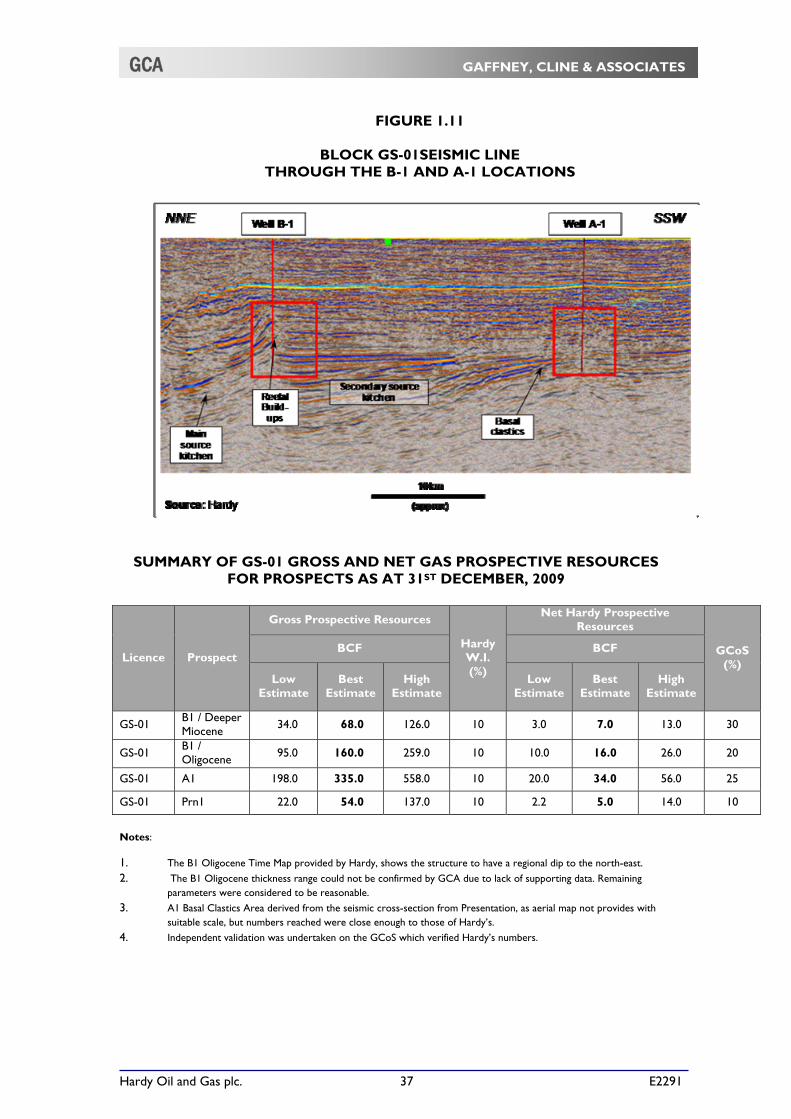

Embed Size (px)

Citation preview

Hardy Oil and Gas plc. Copy No. E2291

GCA GAFFNEY, CLINE & ASSOCIATES

COMPETENT PERSON’S REPORT

Prepared for

HARDY OIL AND GAS PLC

APRIL, 2010

The Americas Europe, Africa, FSU Asia Pacific and the Middle East 1360 Post Oak Blvd., Bentley Hall, Blacknest 80 Anson Road Suite 2500 Alton, Hampshire 31-01C IBM Towers Houston, Texas 77056 United Kingdom GU34 4PU Singapore 079907 Tel: +1 713 850 9955 Tel: +44 1420 525366 Tel: +65 225 6951 Fax: +1 713 850-9966 Fax: +44 1420 525367 Fax: +65 224 0842 email: [email protected] email: [email protected] email: [email protected] and at Caracas – Rio de Janeiro – Buenos Aires – Sydney www.gaffney-cline.com

Hardy Oil and Gas plc. E2291

GCA GAFFNEY, CLINE & ASSOCIATES

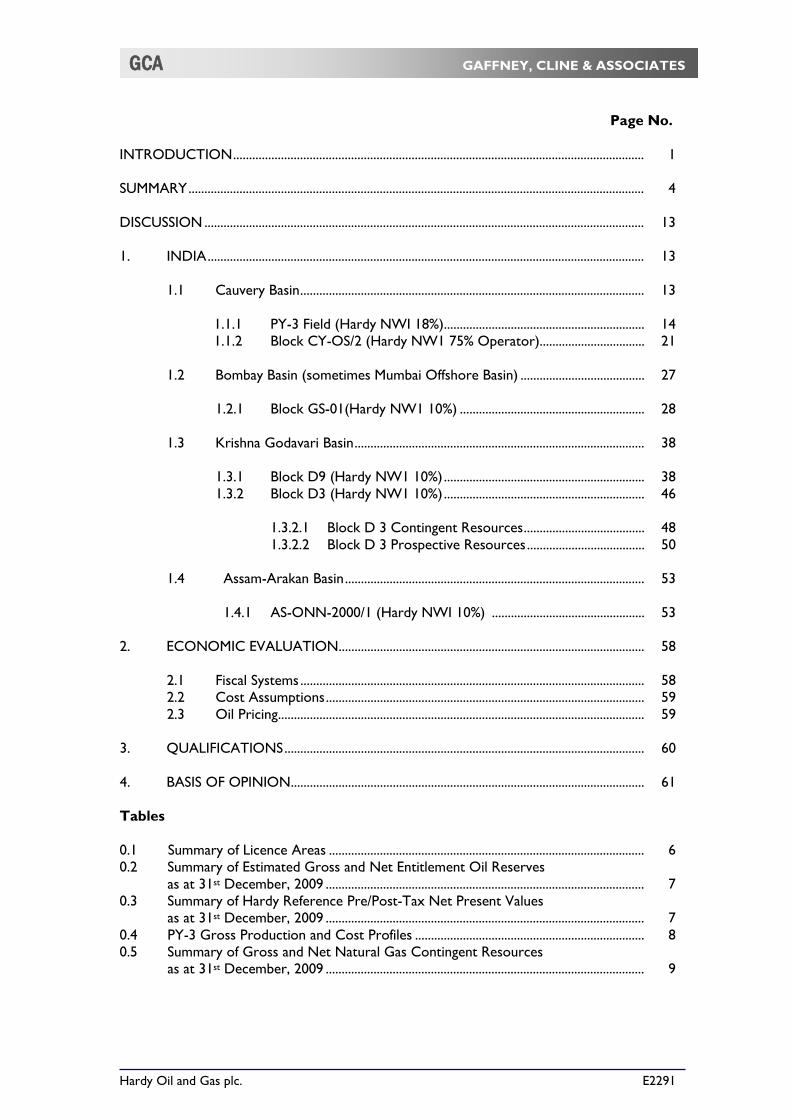

Page No. INTRODUCTION ................................................................................................................................. 1 SUMMARY ............................................................................................................................................... 4 DISCUSSION .......................................................................................................................................... 13 1. INDIA ......................................................................................................................................... 13 1.1 Cauvery Basin ............................................................................................................ 13

1.1.1 PY-3 Field (Hardy NWI 18%)............................................................... 14 1.1.2 Block CY-OS/2 (Hardy NW1 75% Operator)................................. 21

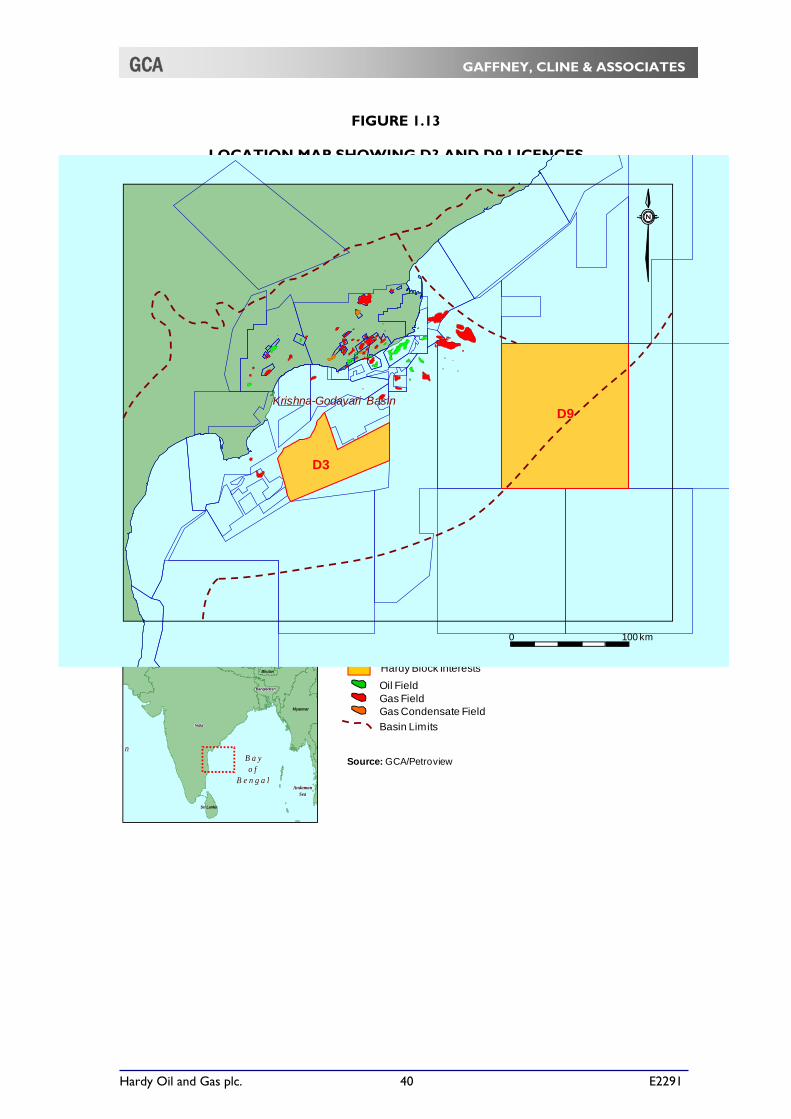

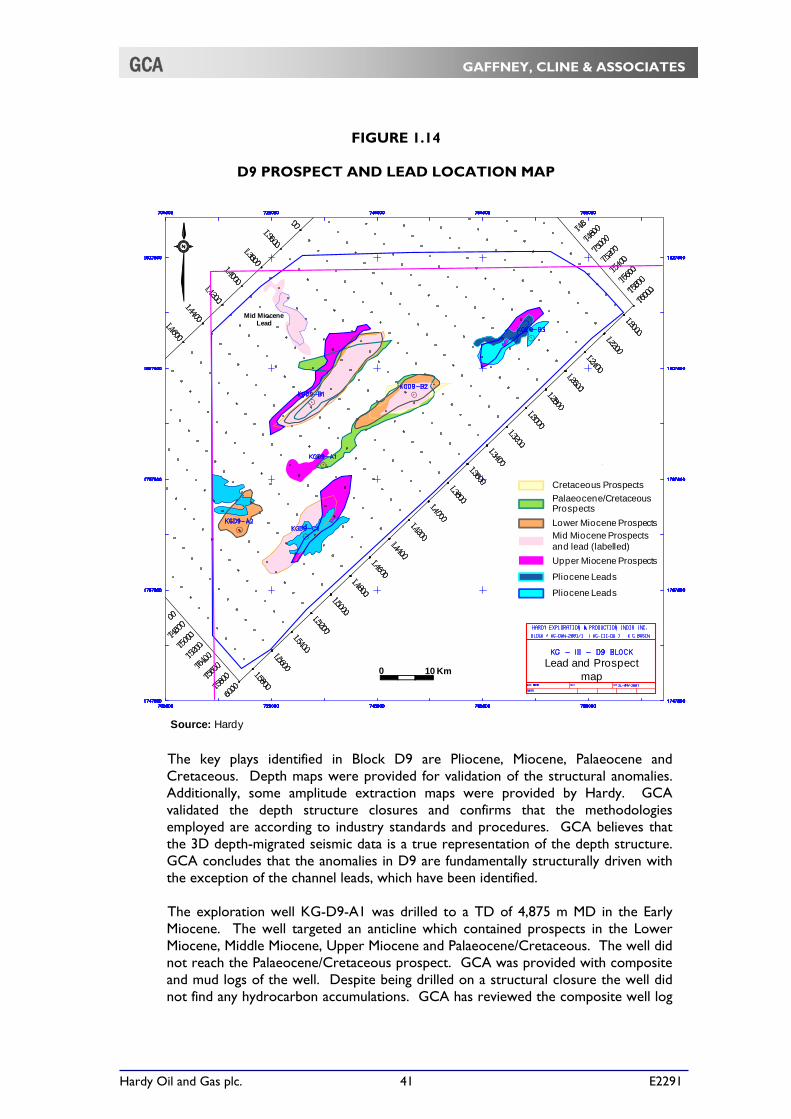

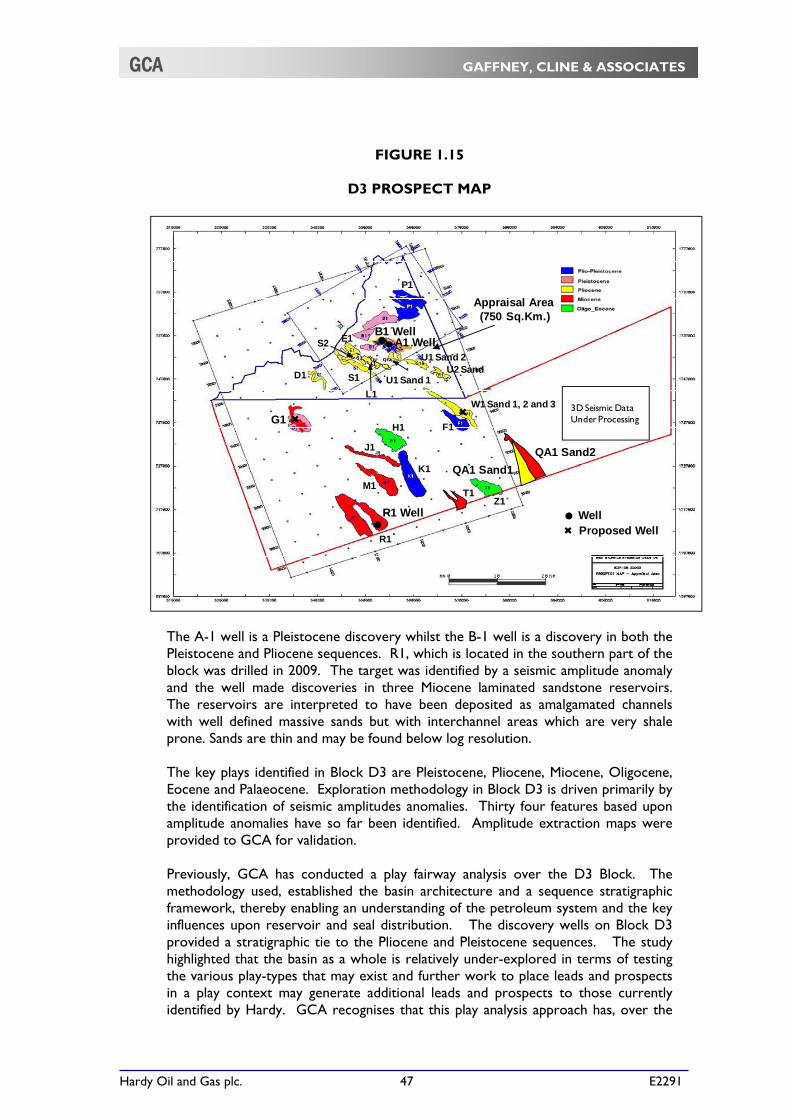

1.2 Bombay Basin (sometimes Mumbai Offshore Basin) ....................................... 27 1.2.1 Block GS-01(Hardy NW1 10%) .......................................................... 28 1.3 Krishna Godavari Basin ........................................................................................... 38 1.3.1 Block D9 (Hardy NW1 10%) ............................................................... 38 1.3.2 Block D3 (Hardy NW1 10%) ............................................................... 46 1.3.2.1 Block D 3 Contingent Resources ...................................... 48 1.3.2.2 Block D 3 Prospective Resources ..................................... 50

1.4 Assam-Arakan Basin .............................................................................................. 53

1.4.1 AS-ONN-2000/1 (Hardy NWI 10%) ................................................ 53 2. ECONOMIC EVALUATION ................................................................................................ 58 2.1 Fiscal Systems ............................................................................................................ 58 2.2 Cost Assumptions .................................................................................................... 59 2.3 Oil Pricing ................................................................................................................... 59 3. QUALIFICATIONS ................................................................................................................. 60 4. BASIS OF OPINION ............................................................................................................... 61 Tables 0.1 Summary of Licence Areas ................................................................................................... 6 0.2 Summary of Estimated Gross and Net Entitlement Oil Reserves as at 31st December, 2009 .................................................................................................... 7 0.3 Summary of Hardy Reference Pre/Post-Tax Net Present Values as at 31st December, 2009 .................................................................................................... 7 0.4 PY-3 Gross Production and Cost Profiles ........................................................................ 8 0.5 Summary of Gross and Net Natural Gas Contingent Resources as at 31st December, 2009 .................................................................................................... 9

Hardy Oil and Gas plc. E2291

GCA TABLE OF CONTENTS

Page No. 0.6 Summary of Gross and Net Gas Prospective Resources for Prospects as at 31st December, 2009 .................................................................................................... 10 0.7 Summary of Gross and Net Oil Prospective Resources for Prospects as at 31st December, 2009 .................................................................................................... 13 Figures 0.1 Location Map of Hardy’s Interests in India ....................................................................... 2 1.1 Location of PY-3 Field and Block CY-OS/2, Offshore Cauvery Basin, India ........... 15 1.2 Cauvery Basin Lithostratigraphic Column ....................................................................... 16 1.3 PY-3 Pay Top Structure Map with OWC @3,505 m SS ............................................... 17 1.4 PY-3 Pay Top Structure Map _Volumetric Polygons ...................................................... 19 1.5 PY-3 Field Production Performance and Forecast .......................................................... 20 1.6 CY-OS/2 Prospect Location Map ........................................................................................ 26 1.7 Bombay Basin Lithostratigraphic Column ......................................................................... 29 1.8 GS-01 Block Location ............................................................................................................. 30 1.9 GS-01 3D Area Depth Structure Map At Top Bassein Formation ............................. 32 1.10 GS-OSN-1 Map ........................................................................................................................ 33 1.11 Block GS-01 Seismic Line Through the B-1 and A-1 Locations ................................... 37 1.12 Blocks D9/D3 Post-Mesozoic Stratigraphy ....................................................................... 39 1.13 Location Map Showing D3 and D9 Licences .................................................................... 40 1.14 D9 Prospect and Lead Location Map ................................................................................. 41 1.15 D3 Prospect Map..................................................................................................................... 47 1.16 Oil Fields South Of Brahmaputra River AS-ONN-2000/1 ............................................ 54 1.17 Stratigraphic Column Assam-Arakan Basin ....................................................................... 55 1.18 Seismic Line As-17-08 In Assam Block ............................................................................... 56 1.19 AS-ONN-2000/1 Prospect and Lead Location Map Sylhet Formation Time Structure Map .......................................................................................................................... 57 Appendices I. Glossary II. SPE/WPC/AAPG/SPEE, Petroleum Resources Management System Definitions and

Guidelines

Bentley Hall Blacknest, Alton Hampshire GU34 4PU United Kingdom

Telephone: +44 (0) 1420 525366 Facsimile: +44 (0) 1420 525367

email: [email protected] www.gaffney-cline.com

Gaffney, Cline & Associates Ltd

Technical and Management Advisers to the Petroleum Industry Internationally Since 1962

Registered London No. 1122740

UNITED KINGDOM UNITED STATES SINGAPORE AUSTRALIA ARGENTINA UAE RUSSIA KAZAKHSTAN

MIH/E2291/ngk/0418 9th April, 2010 The Directors, Hardy Oil & Gas Plc, Lincoln House, 37-143 Hammersmith Road, London, W14 0QL. Dear Sirs,

COMPETENT PERSON’S REPORT (CPR) INTRODUCTION

In accordance with the instruction letter of Hardy Oil & Gas Plc (Hardy) dated 29th January, 2010 Gaffney, Cline & Associates Ltd (GCA) has reviewed the petroleum interests owned by Hardy in India (Figure 0.1). These assets include producing properties, potential developments, discoveries and duly licensed exploration interests. Hardy has made available to GCA a data-set of technical information, including geological, geophysical, and engineering data and reports, together with financial data and the fiscal terms applicable to each of the assets. GCA has also had meetings and discussions with Hardy technical and managerial personnel. In carrying out this review GCA has relied on the accuracy and completeness of the information received from Hardy.

GCA has not been requested to perform a site visit, nor has GCA considered this necessary for the purposes of this CPR.

Industry Standard abbreviations are contained in the attached Appendix I Glossary, some or all of which may have been used in this report. GCA uses the Petroleum Resources Management System (SPE PRMS) published by the Society of Petroleum Engineers/World Petroleum Congresses/ American Association of Petroleum Geologists/Society of Petroleum Evaluation Engineers (SPE/WPC/AAPG/SPEE) in March, 2007 as the basis for its classification and categorization of hydrocarbon volumes. An abbreviated form of the SPE PRMS is appended as Appendix II.

Hardy Oil and Gas plc. 2 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

FIGURE 0.1

LOCATION MAP OF HARDY’S INTERESTS IN INDIA

MaduraiMaduraiMaduraiMaduraiMaduraiMaduraiMaduraiMaduraiMadurai

MangaluruMangaluruMangaluruMangaluruMangaluruMangaluruMangaluruMangaluruMangaluru BengaluruBengaluruBengaluruBengaluruBengaluruBengaluruBengaluruBengaluruBengaluru

CochinCochinCochinCochinCochinCochinCochinCochinCochin

ChennaiChennaiChennaiChennaiChennaiChennaiChennaiChennaiChennai

MumbaiMumbaiMumbaiMumbaiMumbaiMumbaiMumbaiMumbaiMumbai

PunePunePunePunePunePunePunePunePune

PanajiPanajiPanajiPanajiPanajiPanajiPanajiPanajiPanaji

HyderabadHyderabadHyderabadHyderabadHyderabadHyderabadHyderabadHyderabadHyderabadVishakhapatnamVishakhapatnamVishakhapatnamVishakhapatnamVishakhapatnamVishakhapatnamVishakhapatnamVishakhapatnamVishakhapatnam

achiachiachiachiachirachirachirachiachi

AhmadabadAhmadabadAhmadabadAhmadabadAhmadabadAhmadabadAhmadabadAhmadabadAhmadabad

DamanDamanDamanDamanDamanDamanDamanDamanDaman

NagpurNagpurNagpurNagpurNagpurNagpurNagpurNagpurNagpur

BhopalBhopalBhopalBhopalBhopalBhopalBhopalBhopalBhopal RanchiRanchiRanchiRanchiRanchiRanchiRanchiRanchiRanchi

KhulnaKhulnaKhulnaKhulnaKhulnaKhulnaKhulnaKhulnaKhulna

BhubaneshwarBhubaneshwarBhubaneshwarBhubaneshwarBhubaneshwarBhubaneshwarBhubaneshwarBhubaneshwarBhubaneshwar

ImphalImphalImphalImphalImphalImphalImphalImphalImphal

AgartalaAgartalaAgartalaAgartalaAgartalaAgartalaAgartalaAgartalaAgartala

ChittagongChittagongChittagongChittagongChittagongChittagongChittagongChittagongChittagong

JaipurJaipurJaipurJaipurJaipurJaipurJaipurJaipurJaipur LucknowLucknowLucknowLucknowLucknowLucknowLucknowLucknowLucknow

VaranasiVaranasiVaranasiVaranasiVaranasiVaranasiVaranasiVaranasiVaranasi

GangtokGangtokGangtokGangtokGangtokGangtokGangtokGangtokGangtok

SaidpurSaidpurSaidpurSaidpurSaidpurSaidpurSaidpurSaidpurSaidpurPatnaPatnaPatnaPatnaPatnaPatnaPatnaPatnaPatna

ItanagarItanagarItanagarItanagarItanagarItanagarItanagarItanagarItanagar

KohimaKohimaKohimaKohimaKohimaKohimaKohimaKohimaKohimaShillongShillongShillongShillongShillongShillongShillongShillongShillong

ColomboColomboColomboColomboColomboColomboColomboColomboColombo

New DelhiNew DelhiNew DelhiNew DelhiNew DelhiNew DelhiNew DelhiNew DelhiNew Delhi

KathmanduKathmanduKathmanduKathmanduKathmanduKathmanduKathmanduKathmanduKathmandu

I N D I A

D9

D3

CY-OS/2PY-3 Field

GS-01

Sri Lanka

nnn

IndiaIndiaIndiaIndiaIndiaIndiaIndiaIndiaIndia

NepalakistanakistanakistanPakistanPakistanPakistanPakistanPakistanPakistan

B a yB a yB a yB a yB a yB a yB a yB a yB a yo fo fo fo fo fo fo fo fo f

B e n g a lB e n g a lB e n g a lB e n g a lB e n g a lB e n g a lB e n g a lB e n g a lB e n g a l

Bhutan

Myanmar

AndamanAndamanAndamanAndamanAndamanAndamanAndamanAndamanAndamanSeaSeaSeaSeaSeaSeaSeaSeaSea

BangladeshBangladeshBangladeshBangladeshBangladeshBangladeshBangladeshBangladeshBangladesh

0 500 km

Hardy Block Interests

Source: GCA/Petroview

Bay of Bengal

AS-ONN-2000/1

Hardy Oil and Gas plc. 3 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

It must be clearly understood that any determination of reserves volumes,

particularly involving continuing field development, will be subject to significant variations over short periods of time as new information becomes available and perceptions change.

Reserves are those quantities of petroleum that are anticipated to be commercially

recoverable by application of development projects to known accumulations from a given date forward under defined conditions. Reserves must further satisfy four criteria: they must be discovered, recoverable, commercial and remaining (as of the evaluation date) based on the development project(s) applied. Reserves are further categorized in accordance with the level of certainty associated with the estimates and may be sub-classified based on project maturity and/or characterized by development and production status. All categories of Reserve volumes quoted herein have been determined within the context of an economic limit test (pre-tax and exclusive of accumulated depreciation amounts) assessment prior to any Net Present Value analysis.

Contingent Resources are those quantities of petroleum estimated, as of a given

date, to be potentially recoverable from known accumulations, but the applied project(s) are not yet considered mature enough for commercial development due to one or more contingencies. Contingent Resources may include, for example, projects for which there are currently no evident viable markets, or where commercial recovery is dependent on technology under development, or where evaluation of the accumulation is insufficient to clearly assess commerciality. Contingent Resources are further categorized in accordance with the level of certainty associated with the estimates and may be sub-classified based on project maturity and/or characterized by their economic status.

It must be appreciated that the Contingent Resources reported herein are unrisked

in terms of economic uncertainty and commerciality. Prospective Resources are those quantities of petroleum that are estimated, as of a

given date, to be potentially recoverable from undiscovered accumulations by application of future development projects. Prospective Resources have both an associated chance of discovery and a chance of development. Prospective Resources are further subdivided in accordance with the level of certainty associated with recoverable estimates assuming their discovery and development and may be sub-classified based on project maturity. Prospective Resources include Prospects and Leads. Prospects are features that have been sufficiently well defined, on the basis of geological and geophysical data, to the point that they are considered drillable. Leads, on the other hand, are not sufficiently well defined to be drillable, and need further work and/or data. In general, leads are significantly more risky than prospects and therefore are not suitable for explicit quantification.

Prospective Resource volumes are presented as unrisked. It must be appreciated that Prospective Resources are risk assessed only in the context of applying the stated 'Geological Chance of Success', a percentage which pertains to the percentage probability of achieving the status of a Contingent Resource (where the Geological Chance of Success is unity). This dimension of risk assessment does not incorporate the considerations of economic uncertainty and commerciality.

Proved, Proved plus Probable and Proved plus Probable plus Possible Reserves net

to Hardy are quoted as Net Entitlement Reserves reflecting the terms of the applicable Production Sharing Contracts (PSCs). Contingent Resources are presented at a gross field level and a net working interest level, as it is not possible to estimate net entitlements under the relevant PSCs.

Hardy Oil and Gas plc. 4 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

It must be clearly understood that any determination of resources volumes,

particularly involving continuing field development, will be subject to significant variations over short periods of time as new information becomes available and perceptions change. Not only are such estimates of Reserves and Contingent and Prospective Resources based on that information which is currently available, but such estimates are also subject to uncertainties inherent in the application of judgmental factors in interpreting such information. Contingent and Prospective Resources quantities should not be confused with those quantities that are associated with Reserves due to the additional risks involved. Those quantities that might actually be recovered may differ significantly from the estimates presented herein. A possibility exists that the accumulations and prospects will not result in successful discovery and development, in which case there could be no positive potential present worth. It should be clearly noted that the reference Net Present Values (NPVs) of future revenue potential of a petroleum property, such as those discussed in this report, do not represent GCA’s perception of the market value of that property, or any interest in it. In assessing a likely market value, it would be necessary to take into account a number of additional factors including: reserves risk (i.e. that Proved and or Probable Reserves may not be realised within the anticipated timeframe for their exploitation); perceptions of economic and sovereign risk; potential upside, such as in this case exploitation of reserves beyond the Proved and the Probable level; other benefits, encumbrances or charges that may pertain to a particular interest and the competitive state of the market at the time. GCA has explicitly not taken such factors into account in deriving the reference NPVs presented herein. GCA is an energy consultancy specialising in independent petroleum advice on resource evaluation and economic analysis. In the preparation of this report, GCA has maintained, and continues to maintain, a strict consultant-client relationship with Hardy. The management and employees of GCA have been, and continue to be, independent of Hardy in the services they provide to the company including the provision of the opinion expressed in this review. Furthermore, the management and employees of GCA have no interest in any assets or share capital of Hardy, or in the promotion of the company. This report must only be used for the purpose for which it was intended. SUMMARY Hardy has interests in a number of assets in India that comprise production, potential development, discoveries and exploration. Hardy’s Indian assets and the pertinent Net Working Interest (NWI) fractions are comprised of the following: PY-3 producing oil asset, located in the CY-OS-90/1 Production Licence sub-block of

CY-OS/2 in the Cauvery Basin, offshore Tamil Nadu in south-western India (Hardy NWI 18%);

Block CY-OS/2, located in the Cauvery Basin, offshore Tamil Nadu (Hardy NWI 75%);

Block GS-OSN-2000/1 (NELP II), located in the Bombay offshore Basin, to the West and Northwest of the ONGC operated Bombay High field (Hardy NWI 10%);

Block KG-DWN-2001/1(or D9) (NELP III) in the offshore Krishna-Godavari Basin (Hardy NWI 10%), located immediately to the east of Reliance's 2003 gas discoveries in Block KG-DWN-98/3;

Hardy Oil and Gas plc. 5 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

Block KG-DWN-2003/1 (or D3) (NELP V), in the offshore Krishna-Godavari Basin due west and some 50 km inshore of the Reliance concession mentioned above (Hardy NWI 10%); and

Assam block (AS-ONN-2000/1), located onshore in the northeast part of India in the Assam-Arakan Basin, immediately north of the Brahmaputra River and south of the Eastern Himalaya (Hardy NWI 10%).

These concession areas are all shown on the regional location maps, Figure 0.1. A

summary of licence areas and water depth ranges (where appropriate) is given in Table 0.1. GCA has reviewed various data and technical studies presented by Hardy, including

seismic interpretations and dynamic reservoir simulation studies, as well as studies performed by independent third parties and other information available from the public domain. GCA has visited the office of Hardy in Chennai in India February, 2010 for discussions with technical and managerial staff. Based on the information made available, GCA has considered the assessments performed by the operators and other third parties and, in some cases, has derived its own estimates of Reserves, Contingent Resources and Prospective Resources where appropriate.

GCA has not visited the PY-3 field production facilities and cannot, therefore, attests

to the reliability or integrity of these facilities.

The technical and economic conclusions presented herein are based on the technical and commercial information provided and represent GCA’s opinions as of the effective date of 31st December, 2009. The conclusions are estimates based upon professional geoscience and engineering judgment and they will be subject to future revisions as additional information becomes available. Reserves Summary

The "Proved", "Proved plus Probable" and "Proved plus Probable plus Possible" Reserves attributed to Hardy's interests in India as at 31st December, 2009 are for the producing field PY-3 as summarised in Table 0.2. All categories of Reserve volumes quoted herein have been determined within the context of an economic limit test. Net Present Value Summary Net Present Values (NPVs) have been attributed to the ‘Proved’, the ‘Proved plus Probable’ and the ‘Proved plus Probable plus Possible’ Reserves. These references Pre/Post-Tax NPVs are summarised in Table 0.3 based on GCA’s 1Q 2010 Brent price scenario. All NPVs quoted are those exclusively attributable to Hardy's net entitlement interests in the property reviewed. Production Forecasts Forecasts of gross oil production and costs are summarised in Table 0.4. Resource Summary

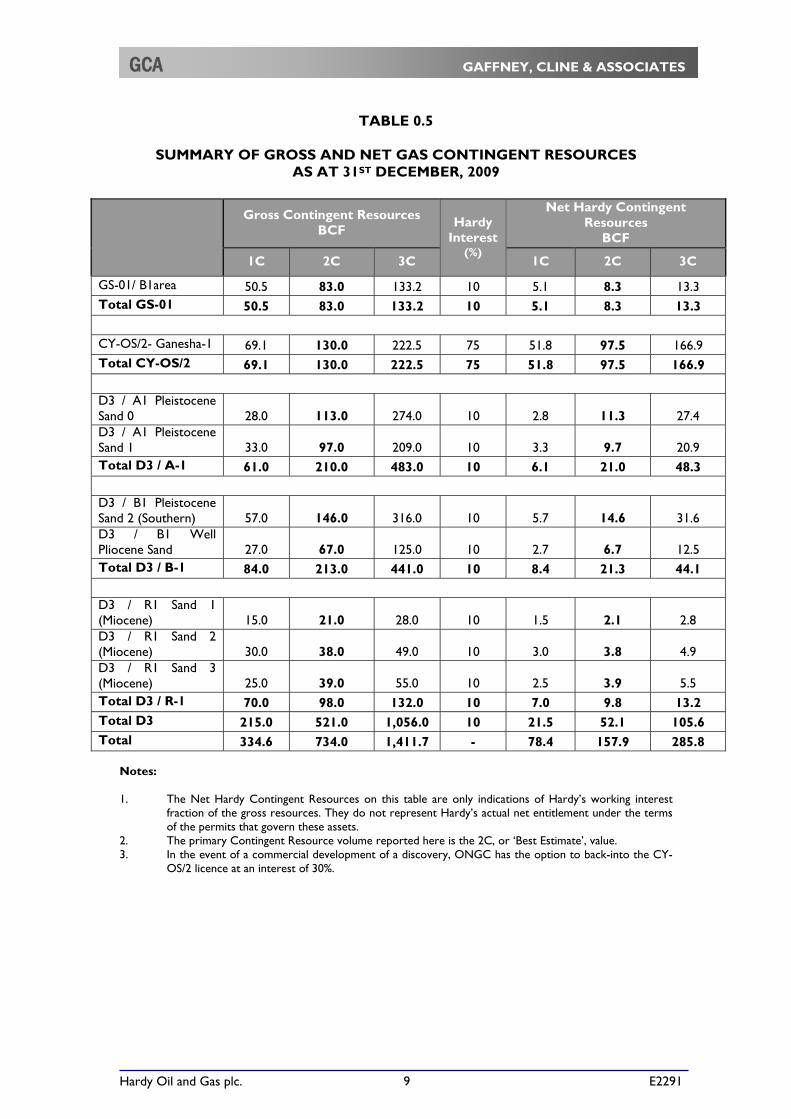

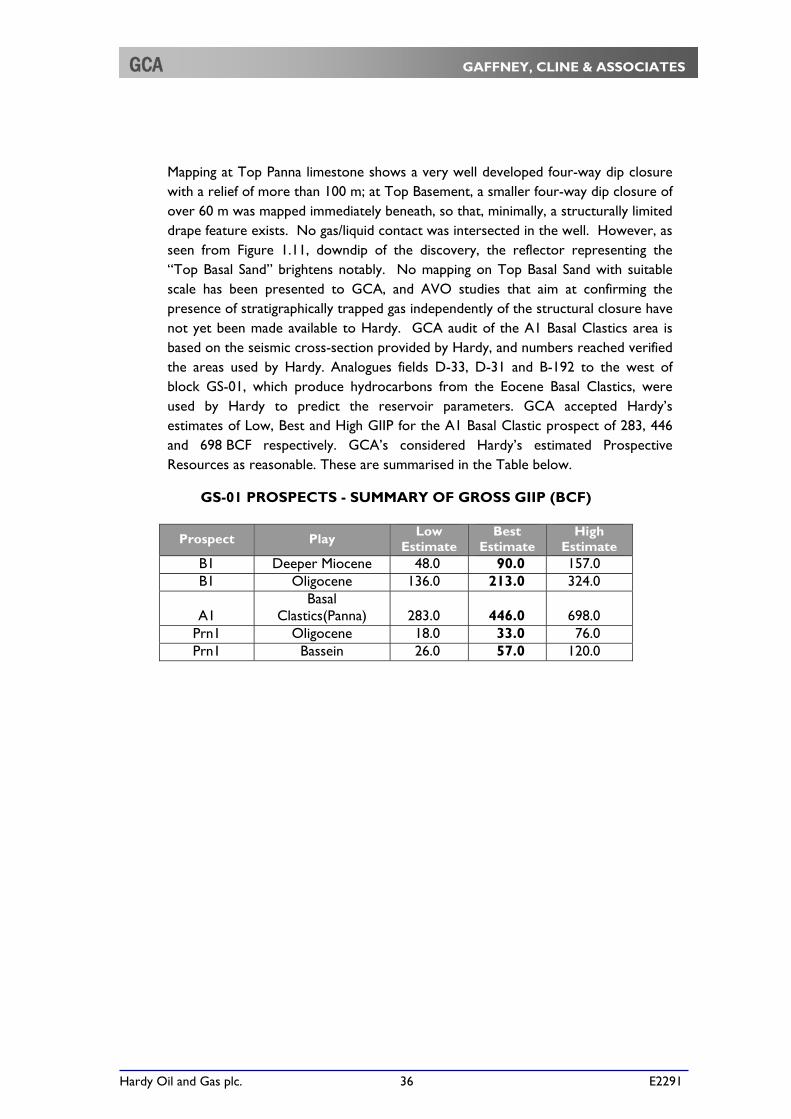

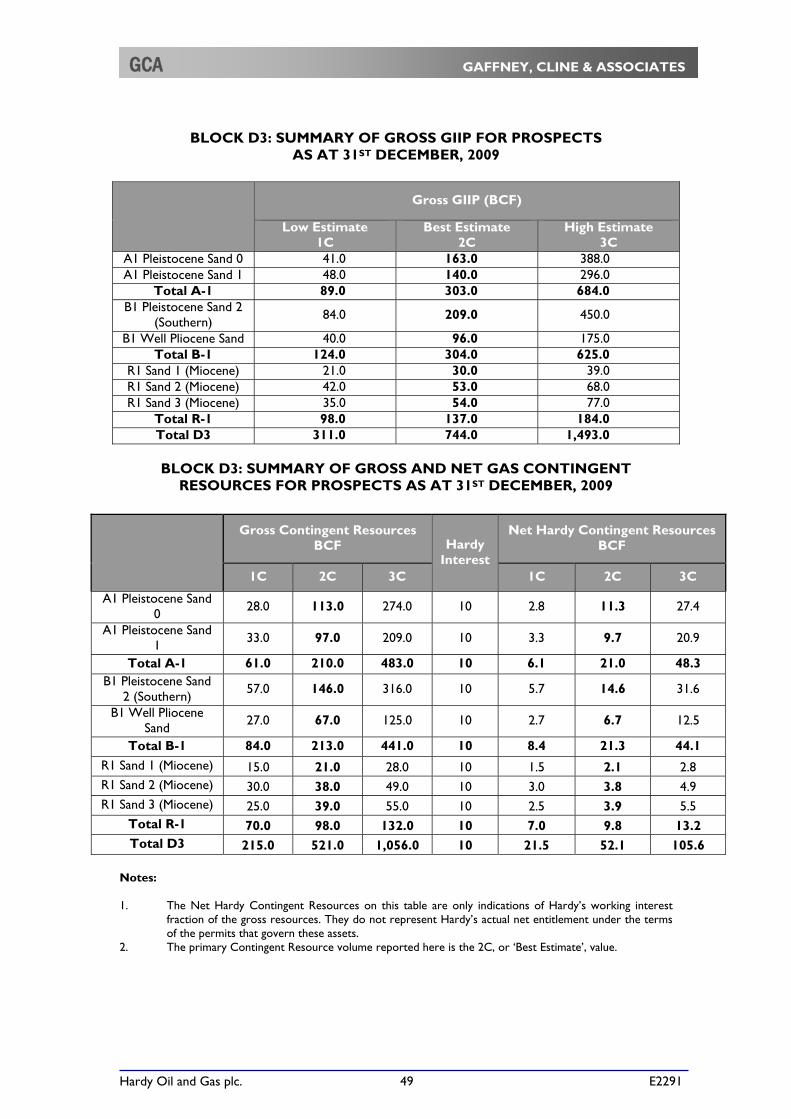

Apart from the producing assets, Hardy holds licences with discoveries and a

number of exploration areas. GCA audited the estimates of Contingent Resources as of 31st December, 2009 and these are discussed in Section 1.1.2 (CY-OS/2), Section 1.2.1 (GS-01/B1 area) and Section 1.3.2 (block D3) of this report. See Table 0.5.

Hardy Oil and Gas plc. 6 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

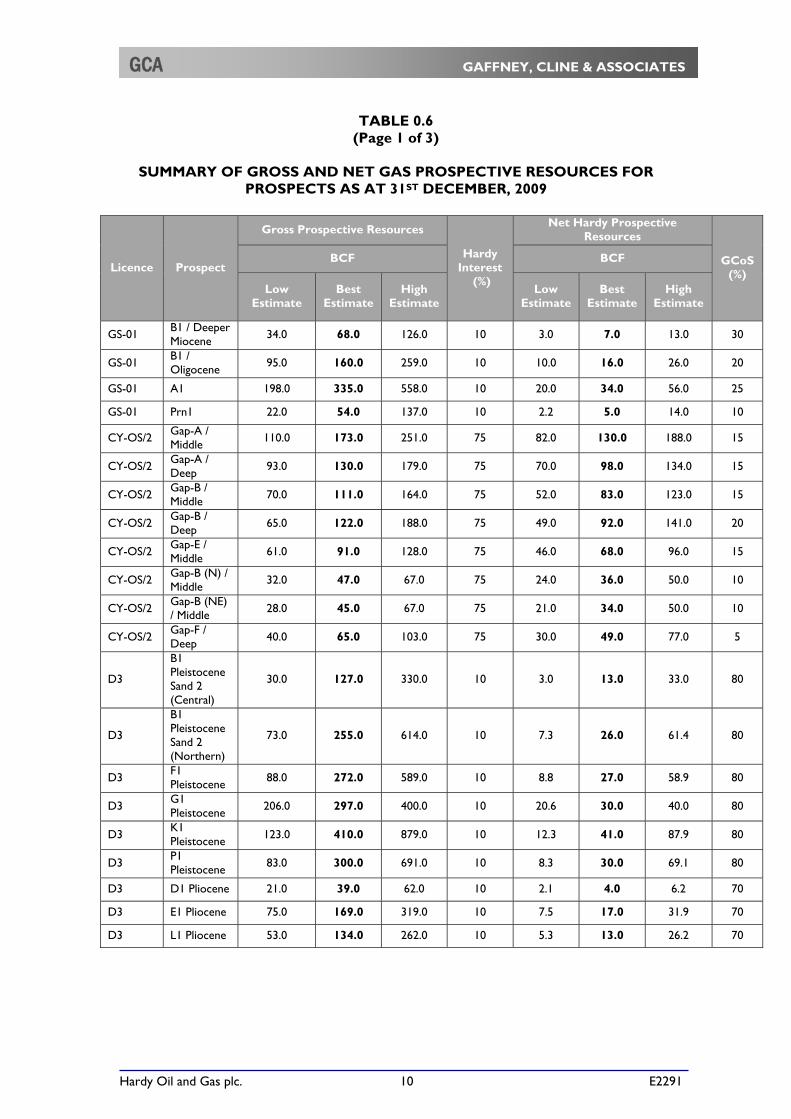

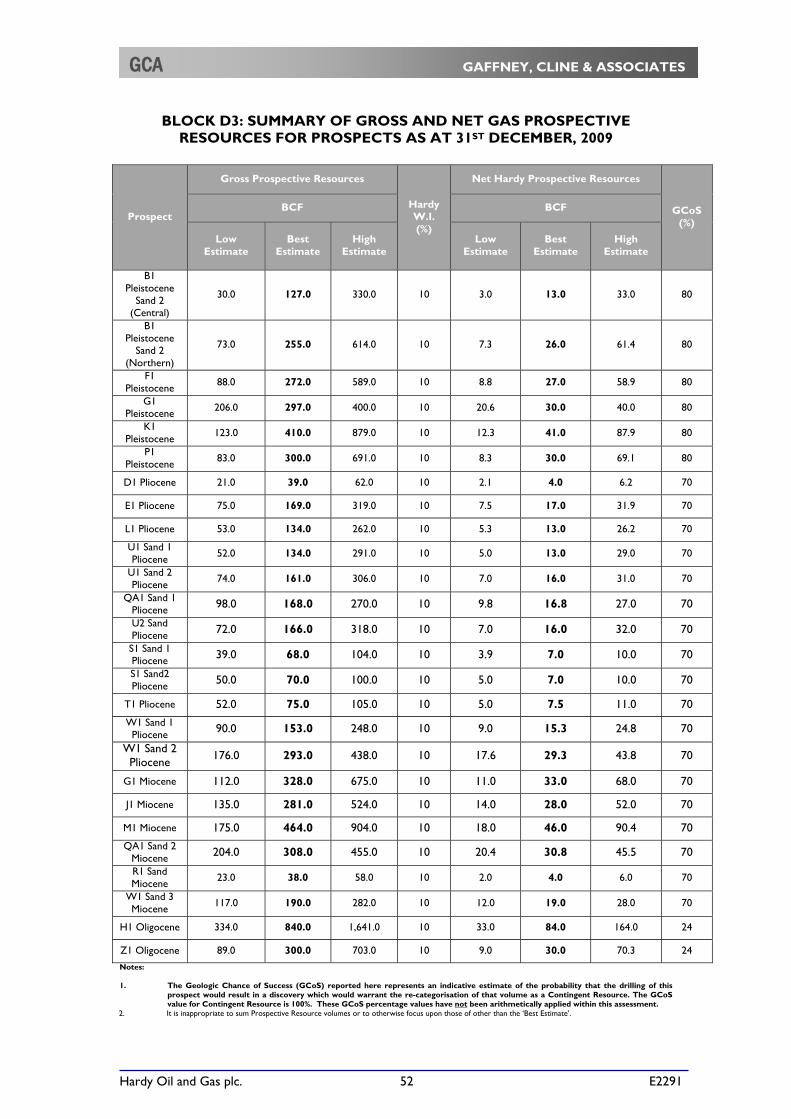

In addition, a determination has been made as to the Prospective Resources that may be attributed to a number of undrilled Prospects, together with the associated geological chance of success (GCoS) that they may be found to contain hydrocarbons, and thereafter be at least regarded as a candidate for inclusion in the Contingent Resource category. A significant number of Leads have been identified in Block D-9 in the emerging petroleum province of the continental slope off India’s eastern coast. The materiality of this potential will evolve through identification and subsequent maturation of Leads into “drillable prospects”. The estimates of Hardy’s Prospective Resources as of 31st December, 2009 are shown in Tables 0.6 and 0.7. Exploration Potential Hardy recognizes that the exploration of D3 and D9 merits sequence stratigraphic analysis to better define the plays. This play analysis approach is being used to determine depositional systems and consequently the distribution of lithofacies within a chronostratigraphic envelope to give a better understanding of reservoir distribution and allow a more effective evaluation of existing prospectivity. Placing leads in a play context will facilitate ranking in terms of GCoS. GCA endorses this approach and postulates that additional leads to those currently identified by Hardy may be generated. This work is already in progress in Block D3 and over the past year has resulted in the successful test of a Miocene play. In summary, the overall resource potential in BlockD3 has therefore improved relative to GCA’s evaluation of 2009.

TABLE 0.1

SUMMARY OF LICENCE AREAS

Field/Block Contract Operator Hardy NWI

%

Permit/PSC Granted

Date

Permit/PSC Expiry Date

Block Area (km2)

Water Depth

(m)

PY-3 CY-OS 90/1

Hardy 18 Dec, 1994 Dec, 2019 81 40 - 450

CY-OS/2 CY-OS/2 Hardy 75 Nov, 1996 Mar, 2007 859 50 - 900

GS-01 GS-OSN-

2000/1 Reliance 10 Jul, 2001 May, 2010 8,841 80 - 150

D9 KG-DWN-

2001/1 Reliance 10 Feb, 2003 Feb, 2011 11,850 2,300-3,100

D3 KG-DWN-

2003/1 Reliance 10 Sep, 2005 Sep, 2013 3,288 400-2,100

Assam AS-ONN-2000/1

Reliance 10 Jan, 2008 Jan, 2015 5,754 onshore

Notes: 1. GS-01 in appraisal phase to finish in May, 2010. 2. CY-OS/2 permit extension is pending with the Minstry of Petroleum and Natural Gas, Government of

India (MOPNG, GOI) regarding the discovery type. 3. In the event of a commercial development of a discovery, ONGC has the option to back-into the CY-

OS/2 licence at an interest of 30%.

Hardy Oil and Gas plc. 7 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

TABLE 0.2

SUMMARY OF ESTIMATED GROSS AND NET ENTITLEMENT OIL

RESERVES AS AT 31ST DECEMBER, 2009

Area

Gross Oil Reserves

Hardy Interest

Net Entitlement Reserves MMBbl MMBbl

Proved Proved

plus Probable

Proved plus

Probable plus

Possible

Proved Proved

plus Probable

Proved plus

Probable plus

Possible PY-3 3.7 16.3 21.0 18% 0.6 2.5 3.4 Notes: 1. Net Entitlements are Reserves based on Hardy’s entitlement to Cost Oil plus share of Profit Oil.

TABLE 0.3

SUMMARY OF HARDY REFERENCE PRE / POST-TAX NET PRESENT VALUES AS AT 31ST DECEMBER, 2009

Notes: 1. Post-Tax values assume no prior tax position as at 31st December, 2009. 2. The above NPVs are Hardy’s Net Entitlement.

Asset Reserves Category

Pre-Tax NPVs Net to Hardy (U.S.$ MM)

Post-Tax NPVs Net to Hardy (U.S.$ MM)

7.5% 10.0% 12.5% 7.5% 10.0% 12.5%

PY-3

Proved 18.91 18.35 17.82 11.00 10.67 10.37

Proved plus Probable

85.77 78.62 72.31 45.00 40.48 36.52

Proved plus Probable plus Possible

107.04 96.03 86.39 52.51 45.43 39.29

Hardy Oil and Gas plc. 8 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

TABLE 0.4

PY-3 GROSS PRODUCTION AND COST PROFILES

Year

Proved Proved plus Probable Proved plus Probable plus Possible

Oil Production

MBbl

CAPEX U.S.$ MM

OPEX U.S.$ MM

Oil Production

MBbl

CAPEX U.S.$ MM

OPEX U.S.$ MM

Oil Production

MBbl

CAPEX U.S.$ MM

OPEX U.S.$ MM

2010 1,136.0 - 35 1,136.0 85 35 1,136.0 115 35

2011 1,151.0 - 35 2,488.0 107 37 2,488.0 268 40

2012 807.0 - 35 3,208.0 - 37 4,138.0 - 40

2013 589.0 - 35 2,644.0 - 37 4,059.0 - 40

2014 - - - 1,831.0 - 37 2,646.0 - 37

2015 - - - 1,336.0 - 37 1,894.0 - 37

2016 - - - 1,096.0 - 37 1,512.0 - 37

2017 - - - 954.0 - 37 1,262.0 - 37

2018 - - - 861.0 - 37 1,025.0 - 37

2019 - - - 779.0 - 37 832.0 - 37

2020 - - - - - - - - -

2021 - - - - - - - - -

Total MBbl

3,682.0 - 140 16,334.0 192 368 20,991.0 383 377

Note: 1. Costs are in U.S.$ 2010. 2. Production is reported in annual quantities.

Hardy Oil and Gas plc. 9 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

TABLE 0.5

SUMMARY OF GROSS AND NET GAS CONTINGENT RESOURCES AS AT 31ST DECEMBER, 2009

Gross Contingent Resources BCF

Hardy Interest

(%)

Net Hardy Contingent Resources

BCF

1C 2C 3C 1C 2C 3C

GS-01/ B1area 50.5 83.0 133.2 10 5.1 8.3 13.3 Total GS-01 50.5 83.0 133.2 10 5.1 8.3 13.3

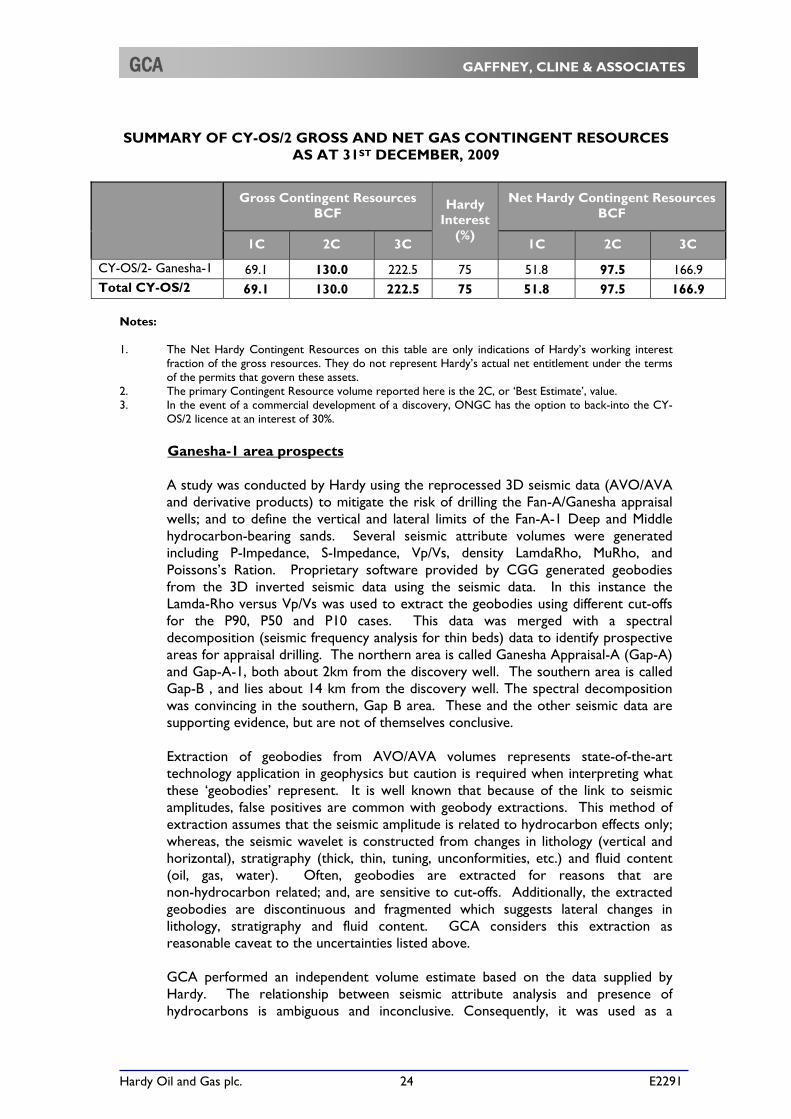

CY-OS/2- Ganesha-1 69.1 130.0 222.5 75 51.8 97.5 166.9 Total CY-OS/2 69.1 130.0 222.5 75 51.8 97.5 166.9

D3 / A1 Pleistocene Sand 0 28.0 113.0 274.0 10 2.8 11.3 27.4 D3 / A1 Pleistocene Sand 1 33.0 97.0 209.0 10 3.3 9.7 20.9 Total D3 / A-1 61.0 210.0 483.0 10 6.1 21.0 48.3

D3 / B1 Pleistocene Sand 2 (Southern) 57.0 146.0 316.0 10 5.7 14.6 31.6 D3 / B1 Well Pliocene Sand 27.0 67.0 125.0 10 2.7 6.7 12.5 Total D3 / B-1 84.0 213.0 441.0 10 8.4 21.3 44.1

D3 / R1 Sand 1 (Miocene) 15.0 21.0 28.0 10 1.5 2.1 2.8 D3 / R1 Sand 2 (Miocene) 30.0 38.0 49.0 10 3.0 3.8 4.9 D3 / R1 Sand 3 (Miocene) 25.0 39.0 55.0 10 2.5 3.9 5.5 Total D3 / R-1 70.0 98.0 132.0 10 7.0 9.8 13.2 Total D3 215.0 521.0 1,056.0 10 21.5 52.1 105.6 Total 334.6 734.0 1,411.7 - 78.4 157.9 285.8

Notes: 1. The Net Hardy Contingent Resources on this table are only indications of Hardy’s working interest

fraction of the gross resources. They do not represent Hardy’s actual net entitlement under the terms of the permits that govern these assets.

2. The primary Contingent Resource volume reported here is the 2C, or ‘Best Estimate’, value. 3. In the event of a commercial development of a discovery, ONGC has the option to back-into the CY-

OS/2 licence at an interest of 30%.

Hardy Oil and Gas plc. 10 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

TABLE 0.6 (Page 1 of 3)

SUMMARY OF GROSS AND NET GAS PROSPECTIVE RESOURCES FOR

PROSPECTS AS AT 31ST DECEMBER, 2009

Licence Prospect

Gross Prospective Resources

Hardy Interest

(%)

Net Hardy Prospective Resources

GCoS (%)

BCF BCF

Low Estimate

Best Estimate

High Estimate

Low Estimate

Best Estimate

High Estimate

GS-01 B1 / Deeper Miocene

34.0 68.0 126.0 10 3.0 7.0 13.0 30

GS-01 B1 / Oligocene

95.0 160.0 259.0 10 10.0 16.0 26.0 20

GS-01 A1 198.0 335.0 558.0 10 20.0 34.0 56.0 25

GS-01 Prn1 22.0 54.0 137.0 10 2.2 5.0 14.0 10

CY-OS/2 Gap-A / Middle

110.0 173.0 251.0 75 82.0 130.0 188.0 15

CY-OS/2 Gap-A / Deep

93.0 130.0 179.0 75 70.0 98.0 134.0 15

CY-OS/2 Gap-B / Middle

70.0 111.0 164.0 75 52.0 83.0 123.0 15

CY-OS/2 Gap-B / Deep

65.0 122.0 188.0 75 49.0 92.0 141.0 20

CY-OS/2 Gap-E / Middle

61.0 91.0 128.0 75 46.0 68.0 96.0 15

CY-OS/2 Gap-B (N) / Middle

32.0 47.0 67.0 75 24.0 36.0 50.0 10

CY-OS/2 Gap-B (NE) / Middle

28.0 45.0 67.0 75 21.0 34.0 50.0 10

CY-OS/2 Gap-F / Deep

40.0 65.0 103.0 75 30.0 49.0 77.0 5

D3

B1 Pleistocene Sand 2 (Central)

30.0 127.0 330.0 10 3.0 13.0 33.0 80

D3

B1 Pleistocene Sand 2 (Northern)

73.0 255.0 614.0 10 7.3 26.0 61.4 80

D3 F1 Pleistocene

88.0 272.0 589.0 10 8.8 27.0 58.9 80

D3 G1 Pleistocene

206.0 297.0 400.0 10 20.6 30.0 40.0 80

D3 K1 Pleistocene

123.0 410.0 879.0 10 12.3 41.0 87.9 80

D3 P1 Pleistocene

83.0 300.0 691.0 10 8.3 30.0 69.1 80

D3 D1 Pliocene 21.0 39.0 62.0 10 2.1 4.0 6.2 70

D3 E1 Pliocene 75.0 169.0 319.0 10 7.5 17.0 31.9 70

D3 L1 Pliocene 53.0 134.0 262.0 10 5.3 13.0 26.2 70

Hardy Oil and Gas plc. 11 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

TABLE 0.6 (Page 2 of 3)

SUMMARY OF GROSS AND NET GAS PROSPECTIVE RESOURCES FOR

PROSPECTS AS AT 31ST DECEMBER, 2009

Licence Prospect

Gross Prospective Resources

Hardy Interest

(%)

Net Hardy Prospective Resources

GCoS (%)

BCF BCF

Low Estimate

Best Estimate

High Estimate

Low Estimate

Best Estimate

High Estimate

D3 U1 Sand 1 Pliocene

52.0 134.0 291.0 10 5.0 13.0 29.0 70

D3 U1 Sand 2 Pliocene

74.0 161.0 306.0 10 7.0 16.0 31.0 70

D3 QA1 Sand 1 Pliocene

98.0 168.0 270.0 10 9.8 16.8 27.0 70

D3 U2 Sand Pliocene

72.0 166.0 318.0 10 7.0 16.0 32.0 70

D3 S1 Sand 1 Pliocene

39.0 68.0 104.0 10 3.9 7.0 10.0 70

D3 S1 Sand2 Pliocene

50.0 70.0 100.0 10 5.0 7.0 10.0 70

D3 T1

Pliocene 52.0 75.0 105.0 10 5.0 7.5 11.0 70

D3 W1 Sand 1 Pliocene

90.0 153.0 248.0 10 9.0 15.3 24.8 70

D3 W1 Sand 2 Pliocene

176.0 293.0 438.0 10 17.6 29.3 43.8 70

D3 G1

Miocene 112.0 328.0 675.0 10 11.0 33.0 68.0 70

D3 J1 Miocene 135.0 281.0 524.0 10 14.0 28.0 52.0 70

D3 M1

Miocene 175.0 464.0 904.0 10 18.0 46.0 90.4 70

D3 QA1 Sand 2 Miocene

204.0 308.0 455.0 10 20.4 30.8 45.5 70

D3 R1 Sand Miocene

23.0 38.0 58.0 10 2.0 4.0 6.0 70

D3 W1 Sand 3 Miocene

117.0 190.0 282.0 10 12.0 19.0 28.0 70

D3 H1

Oligocene 334.0 840.0 1,641.0 10 33.0 84.0 164.0 24

D3 Z1

Oligocene 89.0 300.0 703.0 10 9.0 30.0 70.3 24

D9

Northern Anticline

(NW Flank B1) / U. Miocene

800.0 2,500.0 5,600.0 10 80.0 250.0 560.0 20

Hardy Oil and Gas plc. 12 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

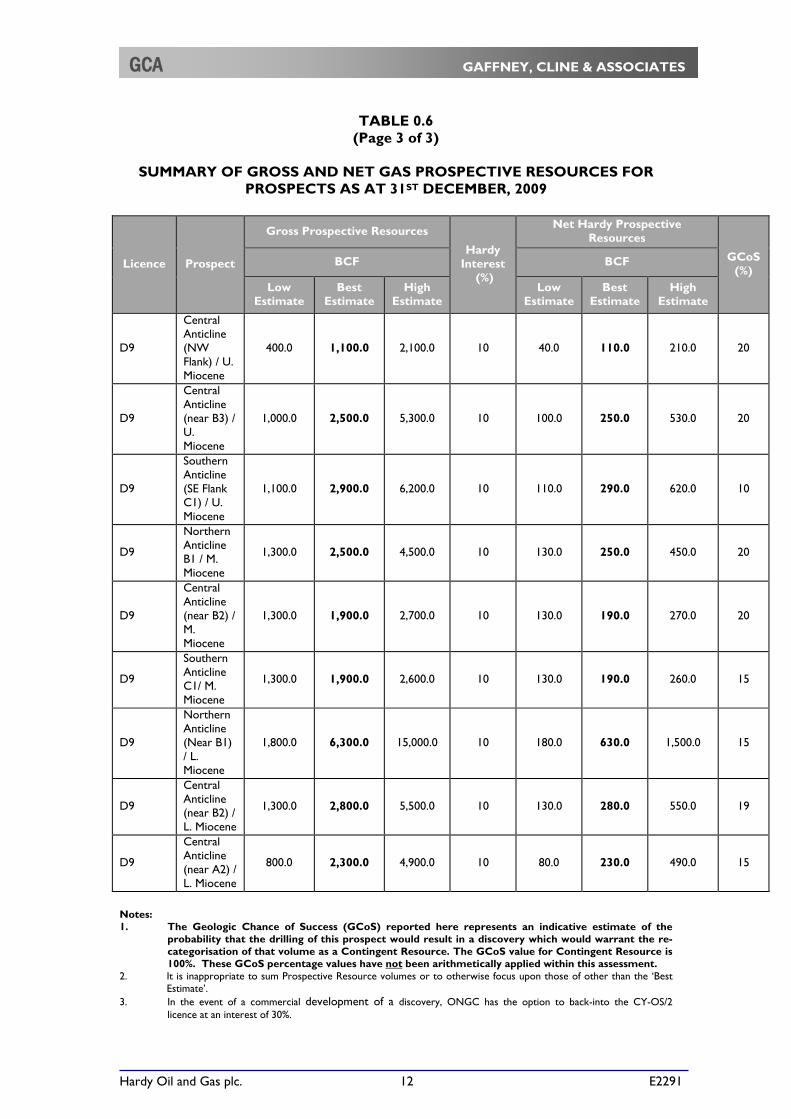

TABLE 0.6 (Page 3 of 3)

SUMMARY OF GROSS AND NET GAS PROSPECTIVE RESOURCES FOR

PROSPECTS AS AT 31ST DECEMBER, 2009

Licence Prospect

Gross Prospective Resources

Hardy Interest

(%)

Net Hardy Prospective Resources

GCoS (%)

BCF BCF

Low Estimate

Best Estimate

High Estimate

Low Estimate

Best Estimate

High Estimate

D9

Central Anticline (NW Flank) / U. Miocene

400.0 1,100.0 2,100.0 10 40.0 110.0 210.0 20

D9

Central Anticline (near B3) / U. Miocene

1,000.0 2,500.0 5,300.0 10 100.0 250.0 530.0 20

D9

Southern Anticline (SE Flank C1) / U. Miocene

1,100.0 2,900.0 6,200.0 10 110.0 290.0 620.0 10

D9

Northern Anticline B1 / M. Miocene

1,300.0 2,500.0 4,500.0 10 130.0 250.0 450.0 20

D9

Central Anticline (near B2) / M. Miocene

1,300.0 1,900.0 2,700.0 10 130.0 190.0 270.0 20

D9

Southern Anticline C1/ M. Miocene

1,300.0 1,900.0 2,600.0 10 130.0 190.0 260.0 15

D9

Northern Anticline (Near B1) / L. Miocene

1,800.0 6,300.0 15,000.0 10 180.0 630.0 1,500.0 15

D9

Central Anticline (near B2) / L. Miocene

1,300.0 2,800.0 5,500.0 10 130.0 280.0 550.0 19

D9

Central Anticline (near A2) / L. Miocene

800.0 2,300.0 4,900.0 10 80.0 230.0 490.0 15

Notes: 1. The Geologic Chance of Success (GCoS) reported here represents an indicative estimate of the

probability that the drilling of this prospect would result in a discovery which would warrant the re-categorisation of that volume as a Contingent Resource. The GCoS value for Contingent Resource is 100%. These GCoS percentage values have not been arithmetically applied within this assessment.

2. It is inappropriate to sum Prospective Resource volumes or to otherwise focus upon those of other than the ‘Best Estimate’.

3. In the event of a commercial development of a discovery, ONGC has the option to back-into the CY-OS/2 licence at an interest of 30%.

Hardy Oil and Gas plc. 13 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

TABLE 0.7

SUMMARY OF GROSS AND NET OIL PROSPECTIVE RESOURCES FOR PROSPECTS AS AT 31ST DECEMBER, 2009

Notes: 1. The Geologic Chance of Success (GCoS) reported here represents an indicative estimate of the

probability that the drilling of this prospect would result in a discovery which would warrant the re-categorisation of that volume as a Contingent Resource. The GCoS value for Contingent Resource is 100%. These GCoS percentage values have not been arithmetically applied within this assessment.

2. It is inappropriate to sum Prospective Resource volumes or to otherwise focus upon those of other than the ‘Best Estimate’.

DISCUSSION 1. INDIA

Hardy has five assets offshore India as shown in Figure 0.1. Most of these lie in the Bay of Bengal on the eastern side of the sub-continent. In and beyond the Krishna-Godavari Basin, are the deepwater exploration blocks KG-DWN-2003/1 (or KG D3) (NELP V) and KG-DWN-2001/1(or KG D9) (NELP III), while further south, in the Cauvery Basin is exploration licence CY-OS/2, within the geographical limits of which lies the producing field PY-3. On the western margin, in the Arabian Sea, lies licence GS-OSN-2000/1 (NELP II in the Bombay Basin. In addition, Hardy has the onshore Assam block (AS-ONN-2000/1) exploration licence within the Assam-Arakan Basin, north-east India. 1.1 Cauvery Basin The Cauvery Basin is the sedimentary basin located on and offshore Tamil Nadu State, south-east India. It is the most southerly basin on the east coast and encloses an area of more than 50,000 km2, of which about half is onshore. The rift basin was formed during Late Jurassic/Early Cretaceous as a result of the break-up of eastern Gondwanaland. NE-SW trending horst and graben structures formed during this period and dominated the structural grain of the basin, following which these features were buried to form a single passive margin setting. The dominant structure was formed by a north/south dextral strike-slip movement between the main Indian sub-continent and Sri Lanka. The basement is Pre-cambrian

Licence Prospect

Gross Prospective Resources

Hardy W.I. (%)

Net Hardy Prospective Resources

GCoS (%)

MMBbl MMBbl

Low Estimate

Best Estimate

High Estimate

Low Estimate

Best Estimate

High Estimate

D9

Central Anticline (4 way fault

closure B2) / Palaeocene

142.0 420.0 961.0 10 14.2 42.0 96.1 18

D9

Central Anticline

(Fault Closure B2) /

Cretaceous

44.0 122.0 260.0 10 4.4 12.2 26.0 18

Hardy Oil and Gas plc. 14 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

(Archean), and sediment fill, which in places reaches a thickness of 7 km, ranges from Permo-Carboniferous to Recent. The NE-SW-orientated sub-basins characterising the Cauvery Basin are an en-echelon array of rift basins offset by basement highs. In the Hardy acreage lie the Ariyalur-Pondicherry and Tranquebar sub-basins, separated by the Porto Novo High (on which lies the gasfield PY-1) as shown in Figure 1.1. Rifting in the Barremian-Aptian started with fluvio-lacustrine deposition in half-grabens followed in the early Albian by a marine transgression. The main extensional phase occurred in the mid-Albian, when faulting led to uplift and erosion. Material reworked at the basin edges flowed into the low sub-basinal areas as fault-scarp conglomerates. The existence of turbidite sand bodies downdip of organic marine shales constituted a viable petroleum exploration play. Rifting ceased in the Cenomanian or Turonian after which thermal subsidence predominated. The post-rift stratigraphy consists of packages of mainly shallow marine and fluvial sandstones and sand-rich carbonates, separated by unconformities (see the lithostratigraphic column Figure 1.2). The source rocks in the basin are organic-rich marine black shales of the Karai Clay Formation deposited in Albian/Aptian to Turonian times. These organic shales can be 100 m thick. They are overlain by major reservoir sand bodies such as the Bhuvanagiri, Nannilam (the reservoir in the PY-3 Field), and Kamalapuram ranging in age from Cenomanian to Eocene (Figure 1.2). The reservoir units are sealed by shales and limestones in a cyclic sequence. Exploration targets have progressed from the structural graben-horst features, to deepwater sands and stratigraphic traps such as those drilled by Hardy in wells Fan E-1 and Fan A-1 (subsequently known as Ganesha-1) in 2006. 1.1.1 PY-3 Field (Hardy NWI 18%)

The PY-3 field is located in the Cauvery offshore basin. It commenced production in July, 1997, and is presently the only producing oil field in Production Licence CY-OS-90/1 (Figure 1.1). The Licence covers some 81 km2 and the water depth ranges from 40 m to about 450 m. The field is operated by Hardy, which holds an 18% Net Working Interest under a Production Sharing Contract (PSC) with The Government of India. The other licensees are ONGC (40%), Tata Petrodyne (21%) and HOEC (21%). The PSC expires in December, 2019, but can be extended by mutual agreement for a further five years. Hardy has made available to GCA a dataset of technical information that included the Hardy PY-3 PETREL Project and seismic data, velocity cube, petrophysical summary, ECLIPSE model, artificial lift selection study, well test analysis plus all available production and injection data together with financial data, including the PSC and cost data.

Hardy Oil and Gas plc. 15 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

FIGURE 1.1

LOCATION OF PY-3 FIELD AND BLOCK CY-OS/2,

OFFSHORE CAUVERY BASIN, INDIA

CY-DWN2001/2CY-DWN2001/2CY-DWN2001/2CY-DWN2001/2CY-DWN2001/2CY-DWN2001/2CY-DWN2001/2CY-DWN2001/2CY-DWN2001/2

BHUVANAGI.02BHUVANAGI.02BHUVANAGI.02BHUVANAGI.02BHUVANAGI.02BHUVANAGI.02BHUVANAGI.02BHUVANAGI.02BHUVANAGI.02

CY-ONN2002/1CY-ONN2002/1CY-ONN2002/1CY-ONN2002/1CY-ONN2002/1CY-ONN2002/1CY-ONN2002/1CY-ONN2002/1CY-ONN2002/1

CY-ONN2002/2CY-ONN2002/2CY-ONN2002/2CY-ONN2002/2CY-ONN2002/2CY-ONN2002/2CY-ONN2002/2CY-ONN2002/2CY-ONN2002/2

CY-ONN2004/1CY-ONN2004/1CY-ONN2004/1CY-ONN2004/1CY-ONN2004/1CY-ONN2004/1CY-ONN2004/1CY-ONN2004/1CY-ONN2004/1

CY-ONN2004/2CY-ONN2004/2CY-ONN2004/2CY-ONN2004/2CY-ONN2004/2CY-ONN2004/2CY-ONN2004/2CY-ONN2004/2CY-ONN2004/2 KALIKALIKALIKALIKALIKALIKALIKALIKALI

KUTHALAMKUTHALAMKUTHALAMKUTHALAMKUTHALAMKUTHALAMKUTHALAMKUTHALAMKUTHALAM

L-IL-IL-IL-IL-IL-IL-IL-IL-I

L-I (EXTN.)L-I (EXTN.)L-I (EXTN.)L-I (EXTN.)L-I (EXTN.)L-I (EXTN.)L-I (EXTN.)L-I (EXTN.)L-I (EXTN.)

L-XIL-XIL-XIL-XIL-XIL-XIL-XIL-XIL-XI

MADANAM

MYILADUTHURAI

NEYVELI

Sri Lanka

nnnnnnnnn

IndiaIndiaIndiaIndiaIndiaIndiaIndiaIndiaIndia

NepalPakistanPakistanPakistanPakistanPakistanPakistanPakistanPakistanPakistan

B a yB a yB a yB a yB a yB a yB a yB a yB a yo fo fo fo fo fo fo fo fo f

B e n g a lB e n g a lB e n g a lB e n g a lB e n g a lB e n g a lB e n g a lB e n g a lB e n g a l

Bhutan

Myanmar

AndamanAndamanAndamanAndamanAndamanAndamanAndamanAndamanAndamanSeaSeaSeaSeaSeaSeaSeaSeaSea

BangladeshBangladeshBangladeshBangladeshBangladeshBangladeshBangladeshBangladeshBangladesh

0 30 Km

CY-OS-2

PY-3 Field

Ganesha-1 Well

Hardy Block Interests

Oil Field

LEGEND

Gas FieldGas Condensate Field

Karaikal High

MadanamHigh

Porto NovoHigh

Indian Craton

T r a n q u e b a r S u b b a s I n

High Areas

Source: GCA/Petroview

CY-OS-90/1

PY-1 Field

Fan E-1 Well

CY-OS-2

Porto NovoHigh

Hardy Oil and Gas plc. 16 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

FIGURE 1.2

CAUVERY BASIN LITHOSTRATIGRAPHIC COLUMN

Age LithostratigraphyRegional / BasinalTectonic Events U

nit Play /

Play Fairways

Res

ervo

ir

So

urc

e

Sea

l

Post Mid-Miocene

Eocene to Mid-Miocene

Paleocene to Eocene

Coniacian to Maastrichtian

Uni

t 6U

nit 5

Uni

t 4U

nit 3

Uni

t 2U

nit 1

Bas

emen

t

Albian/Cenomanian/

Turonian

Pre-Albian

Pre-Cambrian

Rif ting of EastGondwanaland

Madagascarseparated f rom

India/Reactivationof Basement Highs

S Y

N R

I F

TP

O

S

T

-R

I

F

T

Deccan trapvolcanism/basin tilt SE

Indian platecollided withTibetan plate

Indian platecollided with

Eurasian plate/basin tilt E

Niravi Play

Kamalapuram

Nannilam(PY-3 Reservoir)

Bhuvanagiri

Syn Rif t

FracturedBasement

(PY-1 Reservoir)

UNCONFORMITY

UNCONFORMITY

UNCONFORMITY

UNCONFORMITY

UNCONFORMITY

UNCONFORMITY

+

Source: Hardy

Hardy Oil and Gas plc. 17 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

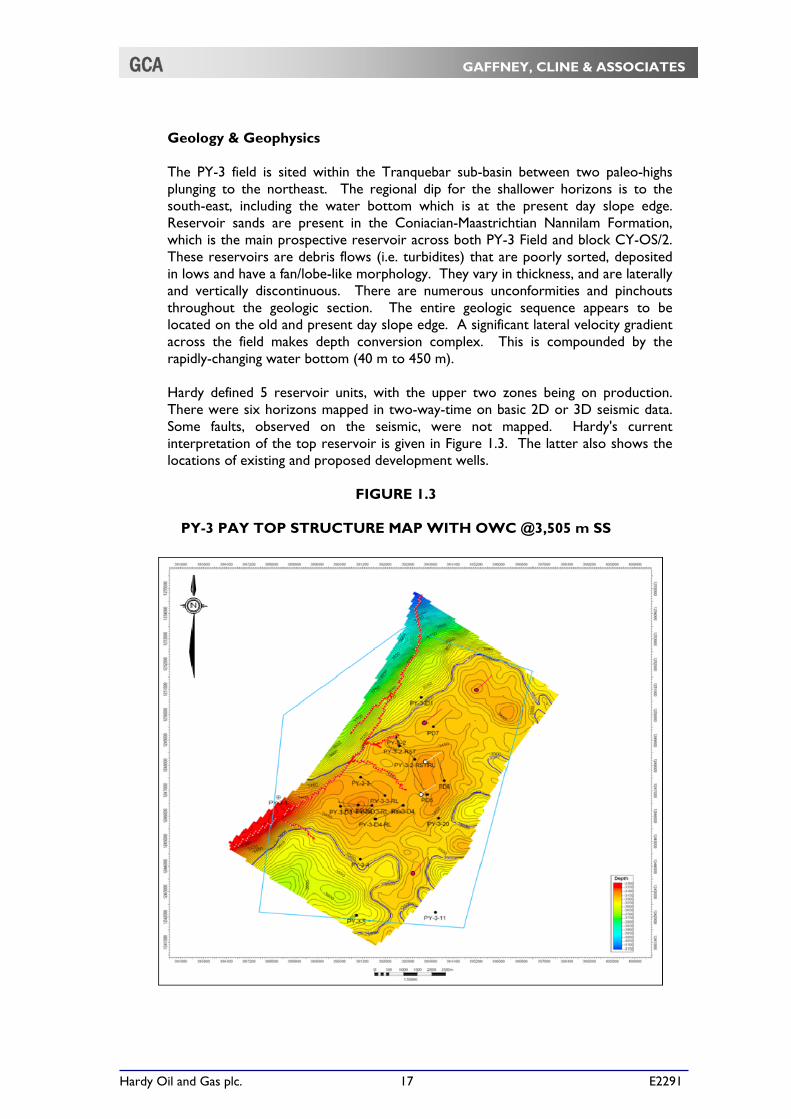

Geology & Geophysics

The PY-3 field is sited within the Tranquebar sub-basin between two paleo-highs plunging to the northeast. The regional dip for the shallower horizons is to the south-east, including the water bottom which is at the present day slope edge. Reservoir sands are present in the Coniacian-Maastrichtian Nannilam Formation, which is the main prospective reservoir across both PY-3 Field and block CY-OS/2. These reservoirs are debris flows (i.e. turbidites) that are poorly sorted, deposited in lows and have a fan/lobe-like morphology. They vary in thickness, and are laterally and vertically discontinuous. There are numerous unconformities and pinchouts throughout the geologic section. The entire geologic sequence appears to be located on the old and present day slope edge. A significant lateral velocity gradient across the field makes depth conversion complex. This is compounded by the rapidly-changing water bottom (40 m to 450 m).

Hardy defined 5 reservoir units, with the upper two zones being on production. There were six horizons mapped in two-way-time on basic 2D or 3D seismic data. Some faults, observed on the seismic, were not mapped. Hardy's current interpretation of the top reservoir is given in Figure 1.3. The latter also shows the locations of existing and proposed development wells.

FIGURE 1.3

PY-3 PAY TOP STRUCTURE MAP WITH OWC @3,505 m SS

Hardy Oil and Gas plc. 18 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

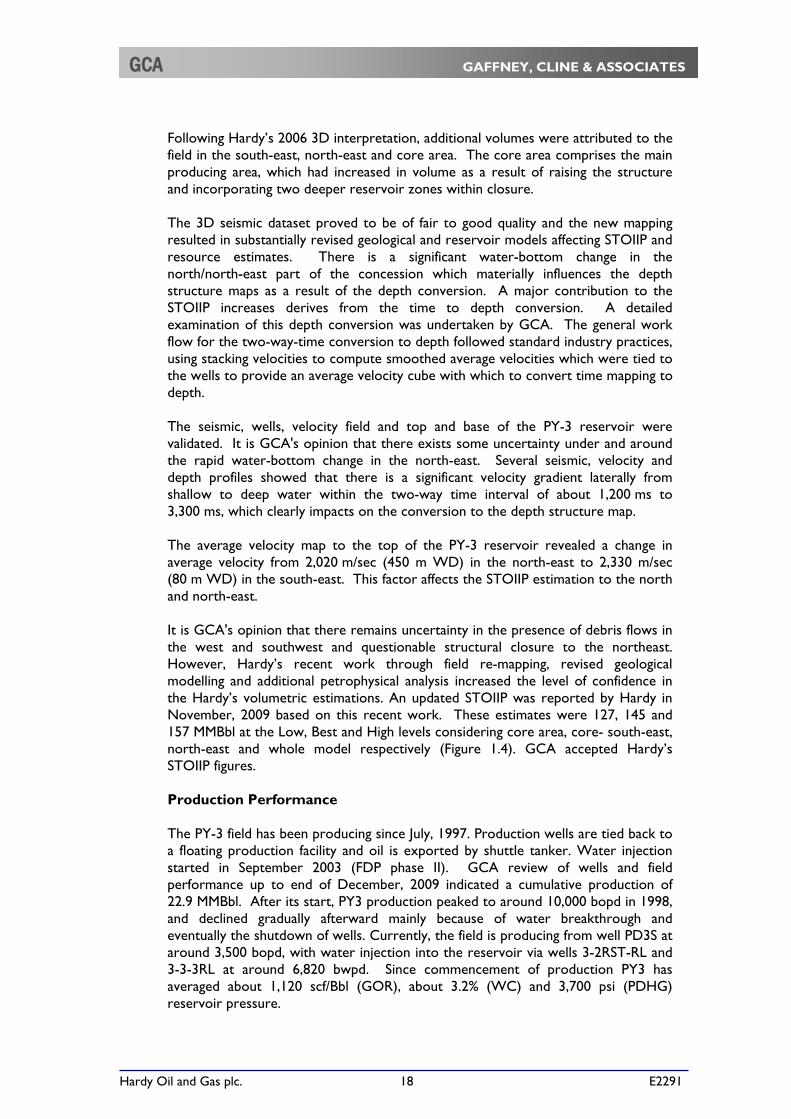

Following Hardy’s 2006 3D interpretation, additional volumes were attributed to the field in the south-east, north-east and core area. The core area comprises the main producing area, which had increased in volume as a result of raising the structure and incorporating two deeper reservoir zones within closure.

The 3D seismic dataset proved to be of fair to good quality and the new mapping resulted in substantially revised geological and reservoir models affecting STOIIP and resource estimates. There is a significant water-bottom change in the north/north-east part of the concession which materially influences the depth structure maps as a result of the depth conversion. A major contribution to the STOIIP increases derives from the time to depth conversion. A detailed examination of this depth conversion was undertaken by GCA. The general work flow for the two-way-time conversion to depth followed standard industry practices, using stacking velocities to compute smoothed average velocities which were tied to the wells to provide an average velocity cube with which to convert time mapping to depth.

The seismic, wells, velocity field and top and base of the PY-3 reservoir were validated. It is GCA's opinion that there exists some uncertainty under and around the rapid water-bottom change in the north-east. Several seismic, velocity and depth profiles showed that there is a significant velocity gradient laterally from shallow to deep water within the two-way time interval of about 1,200 ms to 3,300 ms, which clearly impacts on the conversion to the depth structure map. The average velocity map to the top of the PY-3 reservoir revealed a change in average velocity from 2,020 m/sec (450 m WD) in the north-east to 2,330 m/sec (80 m WD) in the south-east. This factor affects the STOIIP estimation to the north and north-east.

It is GCA's opinion that there remains uncertainty in the presence of debris flows in the west and southwest and questionable structural closure to the northeast. However, Hardy’s recent work through field re-mapping, revised geological modelling and additional petrophysical analysis increased the level of confidence in the Hardy’s volumetric estimations. An updated STOIIP was reported by Hardy in November, 2009 based on this recent work. These estimates were 127, 145 and 157 MMBbl at the Low, Best and High levels considering core area, core- south-east, north-east and whole model respectively (Figure 1.4). GCA accepted Hardy’s STOIIP figures.

Production Performance

The PY-3 field has been producing since July, 1997. Production wells are tied back to a floating production facility and oil is exported by shuttle tanker. Water injection started in September 2003 (FDP phase II). GCA review of wells and field performance up to end of December, 2009 indicated a cumulative production of 22.9 MMBbl. After its start, PY3 production peaked to around 10,000 bopd in 1998, and declined gradually afterward mainly because of water breakthrough and eventually the shutdown of wells. Currently, the field is producing from well PD3S at around 3,500 bopd, with water injection into the reservoir via wells 3-2RST-RL and 3-3-3RL at around 6,820 bwpd. Since commencement of production PY3 has averaged about 1,120 scf/Bbl (GOR), about 3.2% (WC) and 3,700 psi (PDHG) reservoir pressure.

Hardy Oil and Gas plc. 19 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

FIGURE 1.4

PY-3 PAY TOP STRUCTURE MAP _VOLUMETRIC POLYGONS

Until July, 2008, water injection was insufficient (from one injector) to maintain reservoir withdrawals and the wells were often choked back to control GOR. At present, Hardy is injecting at around double voidage replacement which is supporting an increased oil rate and at the same time keeps GOR at a practical level of 1,150 scf/Bbl.

Dynamic Reservoir Modelling

Hardy’s history match process up to September, 2006 has only been applied to the oil production and GOR because there have been no reservoir pressure data since 2004 and no significant water production. Hardy, however, has recently updated its simulation model by including history match to BHP, THP and adding lift curves which added more confidence to the dynamic model. However, GCA considers that the water production data collected to date are still insufficient to allow the establishment of a reliable water cut history match. Hardy continues to analyse the water production to determine the scenario that best represents PY3’s water cut performance. In its audit of Hardy’s dynamic model, GCA found that the Hardy’s history match for oil rate, GOR and the few pressure data is reasonable and considers it suitable for forecasting purposes.

Northeast

Southeast

Southwest

Core + NE + SE

Core

Whole Model

Hardy Oil and Gas plc. 20 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

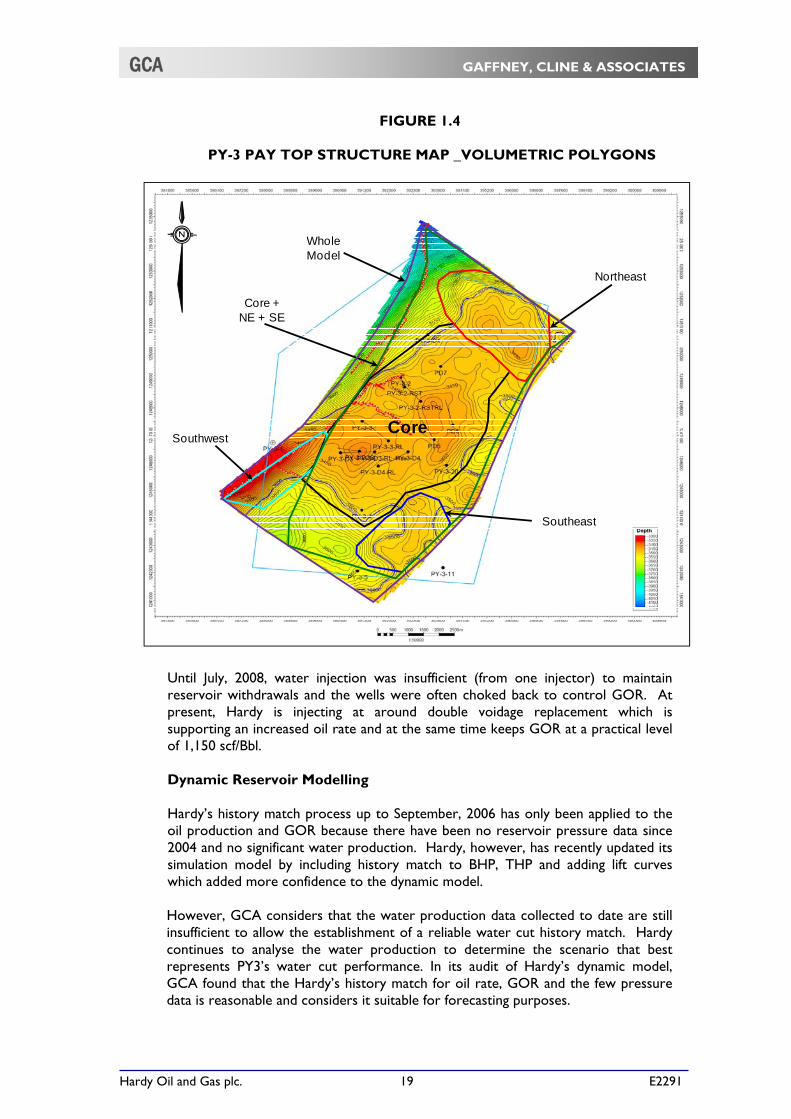

Production Forecast

Hardy’s Phase III development of the PY-3 field envisages the drilling of two further wells. Hardy’s approach to the estimates of remaining recoverable oil is based on the following two cases:

Case 1: Do nothing; and Case 2: Phase III, 2 new producers and the activation of well PD-4RL. Hardy’s simulation results support the implementation of the Phase III development plan and should lead to a significant increase in the volume of oil produced, and thereby enhance oil recovery (Figure 1.5)

FIGURE 1.5

PY-3 FIELD PRODUCTION PERFORMANCE AND FORECAST

Oil Reserves

Proved Reserves This is based on field historical performance and assumes a do nothing case where oil production is allowed to decline from its current rates. The Gross Proved Reserves as at 31st December, 2009 are estimated at 3.68 MMBbl (0.55 MMBbl Net Entitlement to Hardy).

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

Jul-9

7

May

-98

Mar

-99

Jan-

00

No

v-00

Se p

-01

Jul-0

2

Ma y

-03

Mar

-04

Jan-

05

No

v-05

Se p

-06

Jul-0

7

Ma y

-08

Mar

-09

Jan-

10

No

v-10

Se p

-11

Jul-1

2

Ma y

-13

Mar

-14

Jan-

15

No

v-15

Se p

-16

Jul-1

7

Ma y

-18

Mar

-19

Jan-

20

Mo

nth

ly o

il (B

bl)

History 1P 2P 3P

Hardy Oil and Gas plc. 21 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

Proved plus Probable Reserves

For the Proved plus Probable Reserves case, GCA incorporated Hardy’s Phase III field development plan by including two further producers to be drilled in January, 2011 and the activation of well PD-4RL. The resulting estimated Gross Proved plus Probable Reserves as at 31st December, 2009 are 16.33 MMBbl (2.53 MMBbl Net Entitlement to Hardy). Proved plus Probable plus Possible Reserves

This is based on PY-3 field performance, Hardy’s Phase III activities, and three further producers in the north, north-east & south-east parts of the field that are to come on stream end 2011. For this case, however, Hardy assumed that all five wells (of the probable and the possible cases) will be drilled in one campaign as reflected by the forecast profile for the Proved plus Probable plus Possible case in Figure 1.5. GCA estimated Gross Proved plus Probable plus Possible Reserves are at 20.99 MMBbl (3.37 MMBbl Net Entitlement to Hardy as at 31st December, 2009).

1.1.2 Block CY-OS/2 (Hardy NWI 75%, Operator)

The CY-OS/2 Block is located in the Cauvery Basin and encompasses an area of 859 km2. The CY-OS/2 block which after various relinquishments is now split into northern and southern sectors, (Figure 1.1), is operated by Hardy. Hardy has a 75% WI, and remaining 25% is held by GAIL. Water depths over the retained areas range from a few tens of metres at points where the acreage is 2 km from the shore, to almost 500 m at its remotest point (Figure 1.1).

The Block was awarded in 1996 under a PSC, the terms of which provided for three exploration phases, the last of which expired, with all commitments fulfilled, on 23rd March, 2007. The PSC provides for 100% Cost Recovery and Profit Oil sharing. As the PSC pre-dates the NELP, in the event of a commercial discovery, ONGC has the option to back-into the block at an interest of 30%. At the time of this report, a proposed appraisal programme (approved by the operating committee) is being reviewed by the Directorate General of Hydrocarbons (DGH). Hardy is involved in a debate on the nature of fluid in well Fan-A-I (aka Ganesha-1) discovery with the DGH. Hardy maintains the discovery as gas based on the test results and the results of DST-2 where it flowed around 10.7 MMscfd of gas with some condensate. DST-1 was inconclusive because the tubing became plugged while testing and the well flowed small quantity of fluids but was predominantly gas with condensate. The DGH has restricted the appraisal period to 24 months from discovery date interpreting the discovery as oil. Hardy has submitted all the relevant documents to the MOPNG and the DGH supporting the nature of the discovery as gas. The documents provided to the DGH, included the DST reports by Schlumberger, the CPCL (Chennai Petroleum Corporation Limited) laboratory reports on the liquid samples collected from DST#1 & #2 and the ISM University report. Hardy has submitted to the DGH the legal opinions from an independent lawyer and from the Attorney General of India, which opines that Hardy should get 60 months extension under the PSC. The significance of this is that if it is only oil, then there is a twenty four month appraisal period from January, 2007; if it is oil and gas where gas predominates, then there is a five year appraisal period from January, 2007. Hardy is currently awaiting the decision of the MOPNG, GOI.

Hardy Oil and Gas plc. 22 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

In the preparation of this CPR, GCA has accepted Hardy’s explanation but acknowledges that the decision of the MOPNG, GOI could have a significant impact on the CY-OS/2 license. The CY-OS/2 block contains 12,000 line km of 2D seismic, 1,381 km of which have been re-processed. Four 3D seismic surveyshave been shot totaling almost 830 km2.

Two relinquishments have been made, one at the end of each of the first two exploration phases. In the final exploration phase, from May, 2005 to March, 2007, Hardy has acquired 653 km2 of the above 3D (617 km on-block) and drilled two wells; Fan E-1, which was dry (the main Eocene reservoir was absent), and Fan A-1, as described earlier. This well is now renamed Ganesha-1. Well Fan E-1 is in the Tranquebar sub-basin, and well Ganesha-1 is in the Araiyalur-Pondicherry sub-basin to the north (Figure 1.1). Subsequent to the publication of GCA’s CPR of 2008, several studies have been undertaken including a Pre-Stack Depth Migration (PSDM), Hardy/CGG report of reservoir characterization through the analysis of the seismic inversion volumes and the conducting a pore pressure study.

Well Fan A-1 (now Ganesha-1)

The Ganesha-1 well was spudded on 26th September, 2006, and drilled as a vertical hole to a depth of 4,089 m MD where it terminated in Turonian Sattapadi shales, having intersected all prognosed targets. Hydrocarbon shows were logged in the Nannilam (Campanian) and Bhuvanagiri (Turonian) Formations, and between these a thin sand flow-tested gas. The prospective intervals were seismically identified fans that relied upon updip pinchout of the re-worked shelfal sands against shale-prone deepwater slope sediments. Top seal was provided by transgressive deepwater shale. The dual nature of the potential targets – Campanian sands of the Nannilam Formation underlain by Turonian sands of the Bhuvangiri Formation – is seen very clearly, partly because of anomalous seismic amplitude response, particularly at the shallower level.

The well encountered both the Campanian sands (Top Fan sand), a Middle Fan sand, consisting of Santonian and Coniacian sands developed as thin intervals within the Kudavasal Shale Formation and the Turonian sands (Deep Fan sand). Shows were observed in the cuttings while drilling through each sand. Flow tests were run on the Deep Fan sand and the Middle Fan sand. According to the Final Geological Report for the well, the Top Fan sand, in which 50 m of net sand were intersected, was not tested because of heavy mud losses experienced while drilling. Two MDT samples in this sand provided no representative formation fluid (though they revealed the presence of gas). Hydrocarbon shows were encountered during drilling, at three (possibly four) zones in the Top Fan sand.

Hardy Oil and Gas plc. 23 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

The Deep Fan sand, occurred at 3,759 m MD as two sand bodies each about 20 m thick separated by 15 m of shale: net sand was about 35 m, with log-derived porosity 14-17%. The zone from 3,800 m to 3,809 m was tested, producing a weak flow of gas and condensate, and anomalously ‘fresh’ water (all test results are summarised below). DST-1, in the Deep Fan sand, is considered unreliable due to the reported heavy mud losses. This may have been contributed to poor casing cementation, so the well was sidetracked a horizontal distance of about 250 m at the target level. This time the Bhuvanagiri sandstone occurred as a single 45 m sand. Two tests were run, opening perforations from 3,775-3,795 m (DST-4), and then 3,779-3,785 m plus 3,805-3,812 m (DST-4A). The results essentially replicated those of DST-1; as before, the cement bond log indicated poor cementation.

Well Ganesha-1: Summary of DST Results

Interval Test Depth (m MD)

Results

Deep Fan Sand DST-1 3,800 – 3,809 Max gas 0.47 MMscfd, Max cond. 2.4 bcpd, Freshwater c. 120 bpd

Middle Fan Sand DST-2 3,565 – 3,569 Max gas 10.7 MMscfd, Max gas 10.7 MMscfd falling to 1.47 MMscfd

Middle Fan Sand DST-3 3,336 – 3,341 Intermittent gas 0.1 MMscfd

Deep Fan Sand DST-4 (in ST) 3,775 – 3,795 100 bpd freshwater with weak gas flow

Deep Fan Sand DST-4A (in ST) 3,779 -3,785 & 3,805 – 3,812

Gas flow 0.47 MMscfd plus freshwater

The water produced in DST’s 1, 4 and 4A was typically of salinity 2,500 – 2,800 mg/litre. GCA petrophysical analysis has shown that this does not correspond to the formation water. The Middle Fan sand was encountered between 3,565 to 3,569 m. The zone flowed gas (DST-2) at rates which declined from a maximum of 10.7 MMscfd to 1.47 MMscfd showing that a small permeable reservoir was tested and depleted on production. The reservoir had a channel-like morphology: long (119 m) and narrow (37 to 58 m) and thin (1 m). This tight reservoir may recharge from surrounding low permeable sandstones but the stable flow rate would be less than 1.14 MMscfd based on a reservoir engineering study. A further 5 m section, at 3,336-3,341 m was tested by DST3, but also yielded disappointing results. GCA agrees with Hardy’s interpretation of hydrocarbon presence in both the Deep Fan sand and in the Middle Fan sand. GCA also supports Hardy’s gas case based upon well test results. GCA’s analysis confirms 217 BCF as Best Estimate GIIP figure for the accumulation. GCA’s estimated Contingent Resources for the Genesha-1discovery is shown in the Table below

Hardy Oil and Gas plc. 24 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

SUMMARY OF CY-OS/2 GROSS AND NET GAS CONTINGENT RESOURCES

AS AT 31ST DECEMBER, 2009

Gross Contingent Resources BCF

Hardy Interest

(%)

Net Hardy Contingent Resources BCF

1C 2C 3C 1C 2C 3C

CY-OS/2- Ganesha-1 69.1 130.0 222.5 75 51.8 97.5 166.9 Total CY-OS/2 69.1 130.0 222.5 75 51.8 97.5 166.9

Notes: 1. The Net Hardy Contingent Resources on this table are only indications of Hardy’s working interest

fraction of the gross resources. They do not represent Hardy’s actual net entitlement under the terms of the permits that govern these assets.

2. The primary Contingent Resource volume reported here is the 2C, or ‘Best Estimate’, value. 3. In the event of a commercial development of a discovery, ONGC has the option to back-into the CY-

OS/2 licence at an interest of 30%.

Ganesha-1 area prospects A study was conducted by Hardy using the reprocessed 3D seismic data (AVO/AVA and derivative products) to mitigate the risk of drilling the Fan-A/Ganesha appraisal wells; and to define the vertical and lateral limits of the Fan-A-1 Deep and Middle hydrocarbon-bearing sands. Several seismic attribute volumes were generated including P-Impedance, S-Impedance, Vp/Vs, density LamdaRho, MuRho, and Poissons’s Ration. Proprietary software provided by CGG generated geobodies from the 3D inverted seismic data using the seismic data. In this instance the Lamda-Rho versus Vp/Vs was used to extract the geobodies using different cut-offs for the P90, P50 and P10 cases. This data was merged with a spectral decomposition (seismic frequency analysis for thin beds) data to identify prospective areas for appraisal drilling. The northern area is called Ganesha Appraisal-A (Gap-A) and Gap-A-1, both about 2km from the discovery well. The southern area is called Gap-B , and lies about 14 km from the discovery well. The spectral decomposition was convincing in the southern, Gap B area. These and the other seismic data are supporting evidence, but are not of themselves conclusive.

Extraction of geobodies from AVO/AVA volumes represents state-of-the-art technology application in geophysics but caution is required when interpreting what these ‘geobodies’ represent. It is well known that because of the link to seismic amplitudes, false positives are common with geobody extractions. This method of extraction assumes that the seismic amplitude is related to hydrocarbon effects only; whereas, the seismic wavelet is constructed from changes in lithology (vertical and horizontal), stratigraphy (thick, thin, tuning, unconformities, etc.) and fluid content (oil, gas, water). Often, geobodies are extracted for reasons that are non-hydrocarbon related; and, are sensitive to cut-offs. Additionally, the extracted geobodies are discontinuous and fragmented which suggests lateral changes in lithology, stratigraphy and fluid content. GCA considers this extraction as reasonable caveat to the uncertainties listed above. GCA performed an independent volume estimate based on the data supplied by Hardy. The relationship between seismic attribute analysis and presence of hydrocarbons is ambiguous and inconclusive. Consequently, it was used as a

Hardy Oil and Gas plc. 25 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

guideline for the GCA area estimates. Gross/Net thickness, porosity and water saturation were obtained from logs where available. Thickness estimates used by GCA to compute volumetrics are lower than those used by Hardy to reflect the broken distribution of the strong attributes and indeed areas of no seismic response, the lack of supporting evidence for fluid trapping mechanism within potential reservoir imaged, and the limited confidence that can be placed on the calibration via a single control point. It should be noted that in the various Ganesha area probabilistic cases, the extracted geobodies did not always intersect the discovery well so extrapolating lithology and fluid content is risky. It should also be mentioned that not all the geobodies seemed geological in form, nor to be associated with an obvious structural trap. The amplitude derived geobodies in some cases parallel structural contours in a way more usual with tuning, than with stratigraphic or structural traps therefore GCA have lowered the GCOS for these prospects compared to the GCOS originally proposed by Hardy.

Prospective Resources can be attributed to Block CY-OS/2 based on the results of Fan-A-1 well and geobody analysis discussed above (Figure 1.6). These are considered as prospects. There are 4 locations, Gap-A, Gap-B, Gap-E and Gap-F that are related to appraising the Ganesha discovery. GCA audited Hardy’s volume estimates for these prospects and made changes where appropriate. GCA’s GIIP estimates – at this stage of evaluation - are as listed below:

GENESHA-1 : SUMMARY PROSPECTS GROSS GIIP (BCF)

Prospect Horizon GIIP

Low Estimate

Best Estimate

High Estimate

Gap-A Middle Sand 183 288 418 Gap-A Deep Sand 155 217 298 Gap-B Middle Sand 116 185 273 Gap-B Deep Sand 115 209 320 Gap-E Middle Sand 102 152 214 Gap-B (N) Middle Sand 53 79 111 Gap-B (NE) Middle Sand 47 75 111 Gap-F Deep Sand 67 109 171

Notes: 1. It is inappropriate to focus on any of these volume postulations other than the ‘Best Estimate’. 2. The aggregation of Prospective Resources is not appropriate due to mathematical dependency.

.

Hardy Oil and Gas plc. 26 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

FIGURE 1.6

CY-OS/2 PROSPECT LOCATION MAP

Deep Fan

Middle Fan

Source: Hardy

Hardy Oil and Gas plc. 27 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

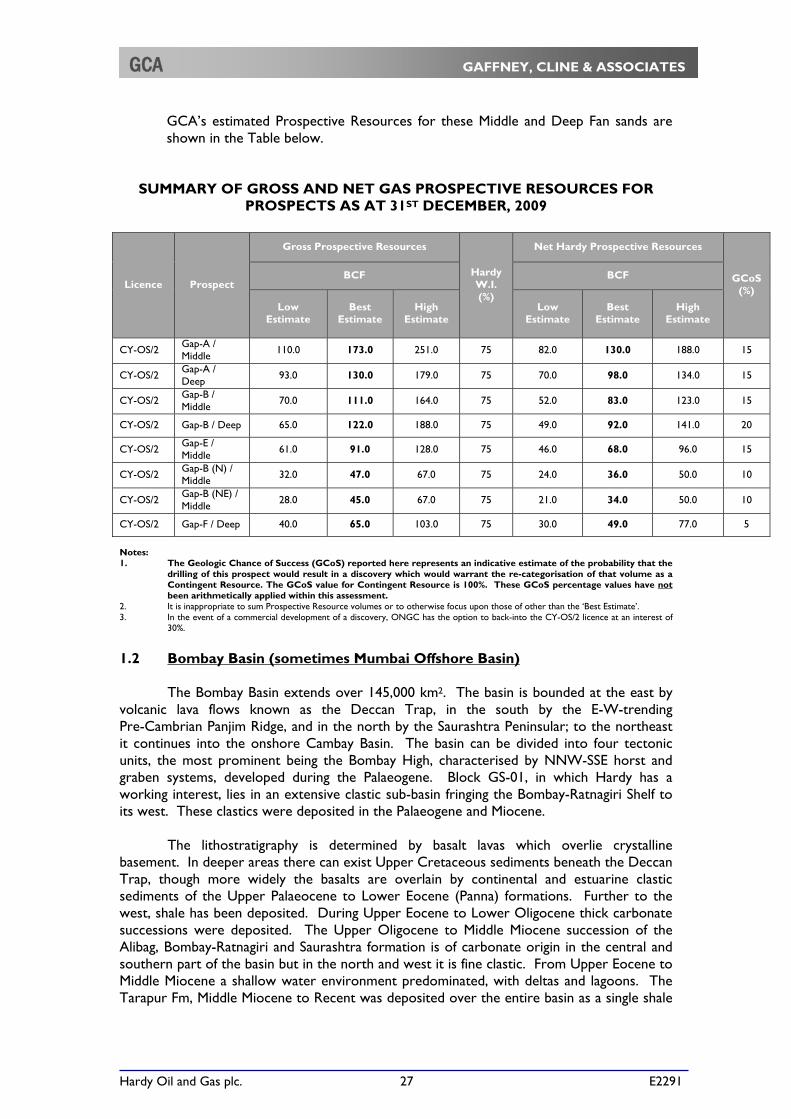

GCA’s estimated Prospective Resources for these Middle and Deep Fan sands are shown in the Table below.

SUMMARY OF GROSS AND NET GAS PROSPECTIVE RESOURCES FOR PROSPECTS AS AT 31ST DECEMBER, 2009

Licence Prospect

Gross Prospective Resources

Hardy W.I. (%)

Net Hardy Prospective Resources

GCoS (%)

BCF BCF

Low Estimate

Best Estimate

High Estimate

Low Estimate

Best Estimate

High Estimate

CY-OS/2 Gap-A / Middle 110.0 173.0 251.0 75 82.0 130.0 188.0 15

CY-OS/2 Gap-A / Deep 93.0 130.0 179.0 75 70.0 98.0 134.0 15

CY-OS/2 Gap-B / Middle

70.0 111.0 164.0 75 52.0 83.0 123.0 15

CY-OS/2 Gap-B / Deep 65.0 122.0 188.0 75 49.0 92.0 141.0 20

CY-OS/2 Gap-E / Middle 61.0 91.0 128.0 75 46.0 68.0 96.0 15

CY-OS/2 Gap-B (N) / Middle 32.0 47.0 67.0 75 24.0 36.0 50.0 10

CY-OS/2 Gap-B (NE) / Middle 28.0 45.0 67.0 75 21.0 34.0 50.0 10

CY-OS/2 Gap-F / Deep 40.0 65.0 103.0 75 30.0 49.0 77.0 5

Notes: 1. The Geologic Chance of Success (GCoS) reported here represents an indicative estimate of the probability that the

drilling of this prospect would result in a discovery which would warrant the re-categorisation of that volume as a Contingent Resource. The GCoS value for Contingent Resource is 100%. These GCoS percentage values have not been arithmetically applied within this assessment.

2. It is inappropriate to sum Prospective Resource volumes or to otherwise focus upon those of other than the ‘Best Estimate’. 3. In the event of a commercial development of a discovery, ONGC has the option to back-into the CY-OS/2 licence at an interest of

30%.

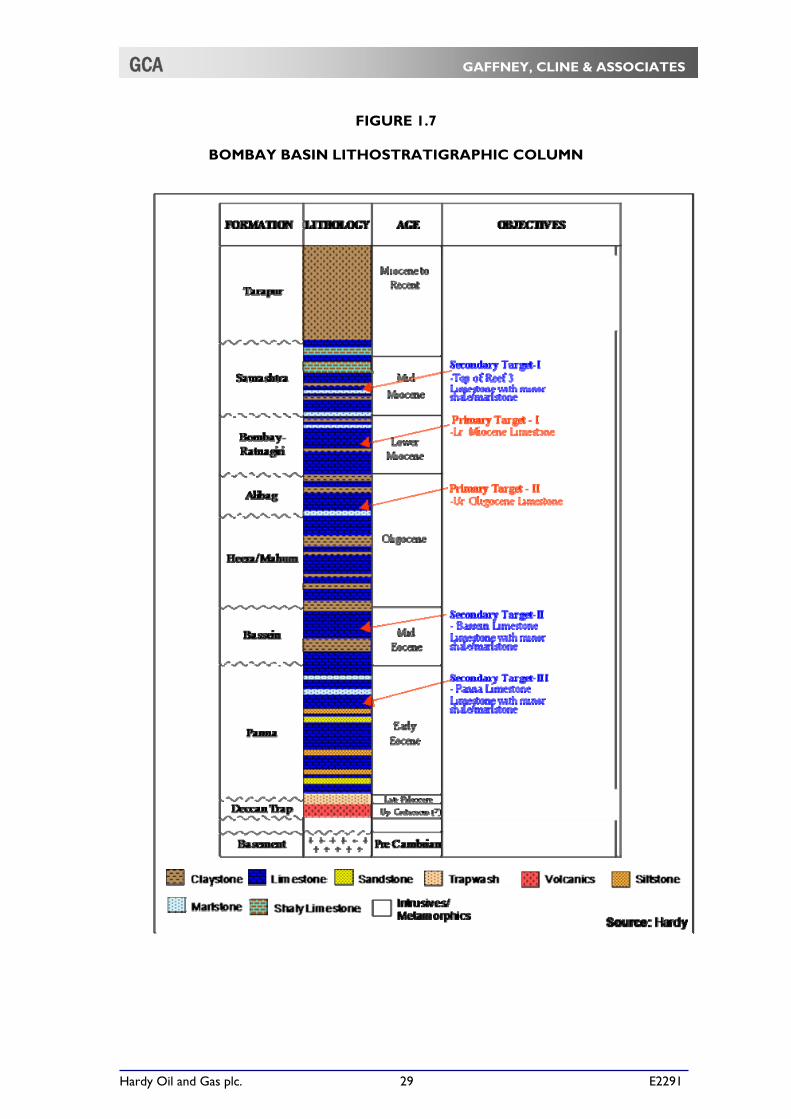

1.2 Bombay Basin (sometimes Mumbai Offshore Basin) The Bombay Basin extends over 145,000 km2. The basin is bounded at the east by volcanic lava flows known as the Deccan Trap, in the south by the E-W-trending Pre-Cambrian Panjim Ridge, and in the north by the Saurashtra Peninsular; to the northeast it continues into the onshore Cambay Basin. The basin can be divided into four tectonic units, the most prominent being the Bombay High, characterised by NNW-SSE horst and graben systems, developed during the Palaeogene. Block GS-01, in which Hardy has a working interest, lies in an extensive clastic sub-basin fringing the Bombay-Ratnagiri Shelf to its west. These clastics were deposited in the Palaeogene and Miocene. The lithostratigraphy is determined by basalt lavas which overlie crystalline basement. In deeper areas there can exist Upper Cretaceous sediments beneath the Deccan Trap, though more widely the basalts are overlain by continental and estuarine clastic sediments of the Upper Palaeocene to Lower Eocene (Panna) formations. Further to the west, shale has been deposited. During Upper Eocene to Lower Oligocene thick carbonate successions were deposited. The Upper Oligocene to Middle Miocene succession of the Alibag, Bombay-Ratnagiri and Saurashtra formation is of carbonate origin in the central and southern part of the basin but in the north and west it is fine clastic. From Upper Eocene to Middle Miocene a shallow water environment predominated, with deltas and lagoons. The Tarapur Fm, Middle Miocene to Recent was deposited over the entire basin as a single shale

Hardy Oil and Gas plc. 28 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

interval (see lithostratigraphic section, Figure 1.7). The thickness of basin fill can exceed 8,000 m. Major oilfields such as Bombay High, Mukta, Heera, Ratna and others produce from Lower and Middle Miocene limestones. These are wackestones, deposited in a lagoonal setting. The main source rocks are the Palaeogene and Miocene pro-delta muds deposited in major low areas in the basin, the main such ‘kitchen’ being the Dahanu Depression, extending for around 500 km parallel to the present-day coastline east of the Bombay High. There is also a source area west of the Bombay High, underlying the Hardy block. Here the source horizons below 3,500 m are overmature and mainly gas-prone. There are no carrier beds, and the (proximal) source needs to be connected to the reservoirs by either faulting or juxtaposition. Migration began in early Miocene into Palaeogene reservoirs, and continued in a second phase into lower and middle Miocene reservoirs during the Pliocene, when traps were already formed. Typical trap types are rollover anticlines, fault-bounded monoclines and stratigraphic carbonate traps (including reefal structures). 1.2.1 Block GS-01 (Hardy NWI 10%)

Block GS-01 is located in both Bombay and Saurashtra Basins off the west coast of India: it lies 220 km west of Bombay and 60 km south of the Saurashtra Peninsular. The Bombay High oilfield lies 40 km east of the eastern boundary of the block (see Figure 1.8). This was the first discovery in the basin, made in 1974, in Miocene carbonates. Since then the basin has experienced continuous exploration, which has resulted in the discovery of many other oilfields, including Ratna, Heera, Panna, Mukta, and Neelam, and the gasfields of Bassein, South Bassein, Mid Tapti and South Tapti. The majority of the 600 exploration and appraisal wells that have been drilled in the Basin have tested the section down to the Deccan Trap or Precambrian granitic basement (Figure 1.7).

Hardy Oil and Gas plc. 29 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

FIGURE 1.7

BOMBAY BASIN LITHOSTRATIGRAPHIC COLUMN

Hardy Oil and Gas plc. 30 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

FIGURE 1.8

GS-01 BLOCK LOCATION

Sub-sea Oil Pipeline (Existing)

Oil FieldLEGEND

Sub-sea Gas Pipeline (Existing)

BOMBAY HIGH

C24

MID. TAPTI

S. TAPTI

PANNA

BASSEIN

HEERA

RATNA

Arabian Sea

DIU

MUKTA

UranTerminal

Mumbai

To Hazira

36" 42"

26"

26"

0 25 50 75 100 Km

30"

Gas Field

C23

Bombay Basin

Gujarat-SaurashtraBasin

Basin Limits

Sri Lanka

nnnnnnnnn

IndiaIndiaIndiaIndiaIndiaIndiaIndiaIndiaIndia

NepalPakistanPakistanPakistanPakistanPakistanPakistanPakistanPakistanPakistan

B a yB a yB a yB a yB a yB a yB a yB a yB a yo fo fo fo fo fo fo fo fo f

B e n g a lB e n g a lB e n g a lB e n g a lB e n g a lB e n g a lB e n g a lB e n g a lB e n g a l

Bhutan

Myanmar

AndamanAndamanAndamanAndamanAndamanAndamanAndamanAndamanAndamanSeaSeaSeaSeaSeaSeaSeaSeaSea

BangladeshBangladeshBangladeshBangladeshBangladeshBangladeshBangladeshBangladeshBangladesh

GS-01

BASSEIN S.

Source: GCA/Petroview

Hardy Oil and Gas plc. 31 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

The block is operated by Reliance (Reliance International Limited) whose working interest is 90%. It encompasses 8,841 km2, and water depths vary from 50 m to 90 m. The Block is under appraisal until 13th May, 2010, therefore Hardy and RIL are committed to drilling a well to declare commerciality by this date. The exploration concession (PEL) was awarded on 16th August, 2001 under NELP II terms, comprising: Three exploration phases, each not exceeding three years, for a total period

of seven years; A Phase-1 work programme of:

a) Seismic data acquisition (1,200 km 2D plus 1,020 km2 3D), processing, re-processing (4,291 km 2D) and interpretation. This commitment has been completed, with the acquisition of 2,363 km 2D, 1,711 km2 3D, and reprocessing of 4,391 km 2D; and

b) A drilling programme of 5 exploration wells; to-date, four wells have been drilled, and one remains.

A PSC allowing for Cost Recovery and Profit Oil sharing

(signed 17th July, 2001). The block has been extensively covered by gravity, magnetic and seismic surveys. Approximately 12,000 km of 2D seismic (over 600 lines, of which 50, totalling 2,363 km, by Reliance/Hardy) have been acquired, processed and interpreted (Figure 1.9). A 3D survey of 1,216 km2 was gathered over the east-central part of the block in 2005. A further 3D survey of 1,000 km2 is scheduled for later in 2007.

Prior to Hardy’s involvement in the licence, six exploration wells had been drilled in the northern half of the block. None of these wells encountered commercial hydrocarbons. However, B-107-1 well, drilled by ONGC in 1990, is reported to have oil shows. Of the original Phase-1 work programme part a) has been completed, and four of the five commitment wells have been drilled. Phase-1 was initially extended two years to August, 2006, and a further extension of 22 months was granted, extending to July, 2008. At present the Block is under appraisal phase until 13th May, 2010.

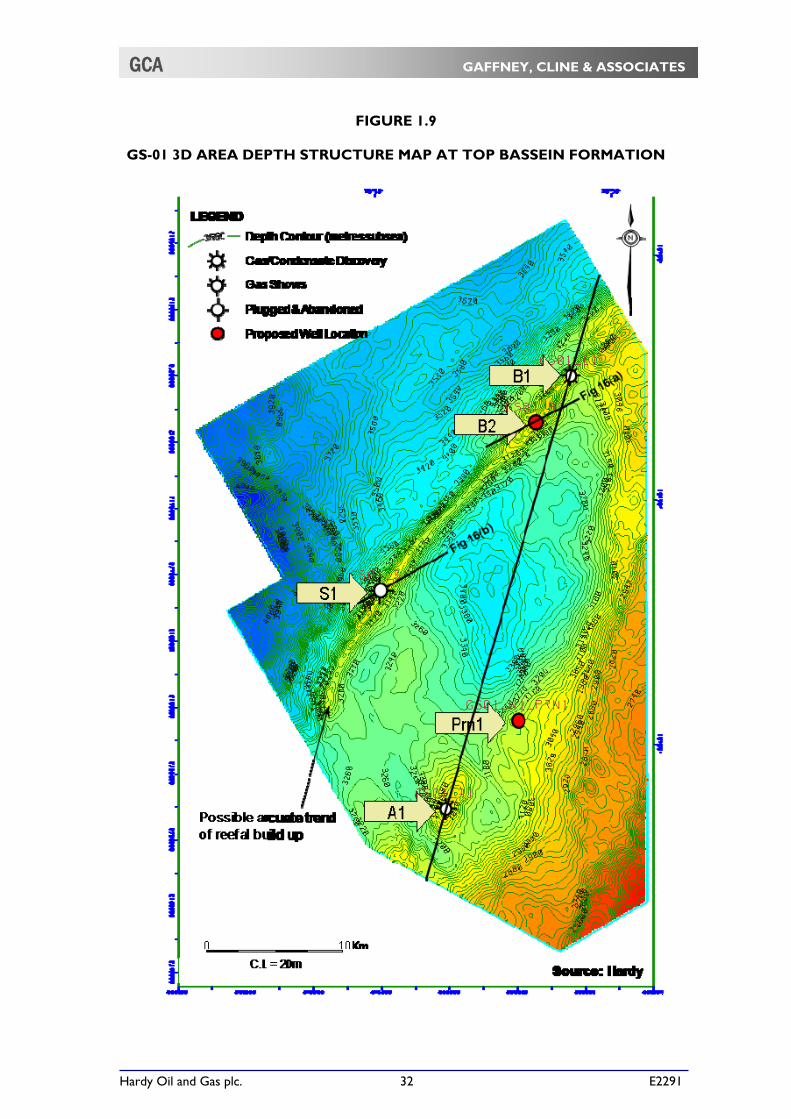

Figure 1.10 shows the locations of prospective wells GS-01-A1, GS-01-B1, as well as the recent dry holes S1 and M1, which have been plugged and abandoned.

Hardy Oil and Gas plc. 32 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

FIGURE 1.9

GS-01 3D AREA DEPTH STRUCTURE MAP AT TOP BASSEIN FORMATION

Hardy Oil and Gas plc. 33 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

FIGURE 1.10

GS-OSN-1 MAP

Hardy Oil and Gas plc. 34 E2291

GCA GAFFNEY, CLINE & ASSOCIATES

Discovery Well GS-01-B1

The B1 well spudded on 2nd March, 2007, 240 km northwest of Mumbai in 79 m of water. It terminated in Lower Miocene reefal carbonates at a depth of 2,282 m MD (2,256 m TVDSS). The well had multiple limestone targets, including Middle and Lower Miocene, Upper Oligocene, Middle Eocene (Bassein Fm) and Lower Eocene (Panna Fm). The location is shown on the map of Figure 1.10. The well terminated prematurely in the Lower Miocene because of mud losses/lost circulation, having encountered gas and condensate in Lower Miocene limestones before entering reefal material of high vuggy porosity and permeability. 24 m of perforations were opened within the Lower Miocene limestone above the reef, and following acidisation the well flowed gas at 18.6 MMscfd and condensate at 415 bcpd through a 56/64” choke with a FTHP of 1,346 psi. A recent Paleontological study confirmed that the B1discovery is of Lower Miocene age (previously thought to be Middle Miocene). The operator officially notified the government of a discovery named Dhirubai 33, on 14th May, 2007. It is the most westerly discovery in India to date and is currently under appraisal.

Levels of hydrogen sulphide between 1,700 ppm and 3,800 ppm, and CO2 up to 7% were noted in the produced gas. An estimate of Contingent Resources for the tested zone is presented in the Table below. The structure at the H1A level (Top Middle Miocene) is a four-way dip-closed anticline. Hardy’s 1C, 2C and 3C estimates of GIIP, 72, 111 and 167 BCF respectively, seem reasonable based on the data provided to GCA. Recovery factory of 70%, 75% & 80% were accepted based on analogue cases.

GS-01 SUMMARY OF GROSS AND NET GAS CONTINGENT RESOURCES

AS AT 31ST DECEMBER, 2009

Gross Contingent Resources BCF

Hardy Interest

(%)

Net Hardy Contingent Resources BCF

1C 2C 3C 1C 2C 3C

GS-01/ B1area 50.5 83.0 133.2 10 5.1 8.3 13.3 Total GS-01 50.5 83.0 133.2 10 5.1 8.3 13.3

Notes: 1. The Net Hardy Contingent Resources on this table are only indications of Hardy’s working interest

fraction of the gross resources. They do not represent Hardy’s actual net entitlement under the terms of the permits that govern these assets.

2. The primary Contingent Resource volume reported here is the 2C, or ‘Best Estimate’, value.

Hardy Oil and Gas plc. 35 E2291

GCA GAFFNEY, CLINE & ASSOCIATES