Embed Size (px)

Citation preview

GAZPROM NEFT

INVESTOR DAY

December 17, 2012, Moscow

GAZPROM NEFT INVESTOR DAY 2

Disclaimer

This presentation contains forward-looking statements concerning the financial condition, results of operations and businesses of Gazprom Neft and its consolidated subsidiaries. All statements other than statements of historical fact are, or may be deemed to be, forward-looking statements. Forward-looking statements are statements of future expectations that are based on management’s current expectations and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in these statements.

Forward-looking statements include, among other things, statements concerning the potential exposure of Gazprom Neft to market risks and statements expressing management’s expectations, beliefs, estimates, forecasts, projections and assumptions. These forward-looking statements are identified by their use of terms and phrases such as ‘‘anticipate’’, ‘‘believe’’, ‘‘could’’, ‘‘estimate’’, ‘‘expect’’, ‘‘intend’’, ‘‘may’’, ‘‘plan’’, ‘‘objectives’’, ‘‘outlook’’, ‘‘probably’’, ‘‘project’’, ‘‘will’’, ‘‘seek’’, ‘‘target’’, ‘‘risks’’, ‘‘goals’’, ‘‘should’’ and similar terms and phrases. There are a number of factors that could affect the future operations of Gazprom Neft and could cause those results to differ materially from those expressed in the forward-looking statements included in this presentation, inclusively (without limitation): (a) price fluctuations in crude oil and oil products; (b) changes in demand for the Company’s products; (c) currency fluctuations; (d) drilling and production results; (e) reserve estimates; (f) loss of market and industry competition; (g) environmental and physical risks; (h) risks associated with the identification of suitable potential acquisition properties and targets, and successful negotiation and completion of such transactions; (i) economic and financial market conditions in various countries and regions; (j) political risks, project delay or advancement, approvals and cost estimates; and (k) changes in trading conditions.

All forward-looking statements contained in this presentation are expressly qualified in their entirety by the cautionary statements contained or referred to in this section. Readers should not place undue reliance on these forward-looking statements. Each forward-looking statement speaks only as of the date of this presentation. Neither Gazprom Neft nor any of its subsidiaries undertake any obligation to publicly update or revise any forward-looking statement as a result of new information, future events or other information.

GAZPROM NEFT INVESTOR DAY 3

INTRODUCTION

1. Operational and financial results

and 2012 outlook

2. Strategy

3. Operations – Upstream

4. Operations – Downstream

5. Financial outlook

Alexey Yankevich Member of the Management

Committee, Deputy General Director

for Economics and Finance

Sergey Vakulenko Head of Strategic Planning

Department

Vadim Yakovlev Deputy Chairman of the Management

Committee, First Deputy General

Director for Exploration, Production,

Strategic Planning and M&A

Anatoly Cherner Deputy Chairman of the Management

Committee, Deputy General Director

for Logistics, Processing and Sales

Table of content Speakers

GAZPROM NEFT INVESTOR DAY 4

Operational and Financial Results and

2012 Outlook

Alexey Yankevich

GAZPROM NEFT INVESTOR DAY 5

Record Financial & Operating Results

Gazprom Oil Licenses Transfer on Track

Technological Progress

Certainty on Major Tax Breaks

Refineries Well Positioned for Upgrade

Retail Market Outstanding Growth

New Phase for Greenfield Developmnet

Investments Nearing Peak

Dividends remain at 22%IFRS payout

Net Debt / EBITDA not to exceed 1.5X

INVESTOR DAY SUMMARY

GAZPROM NEFT INVESTOR DAY 6

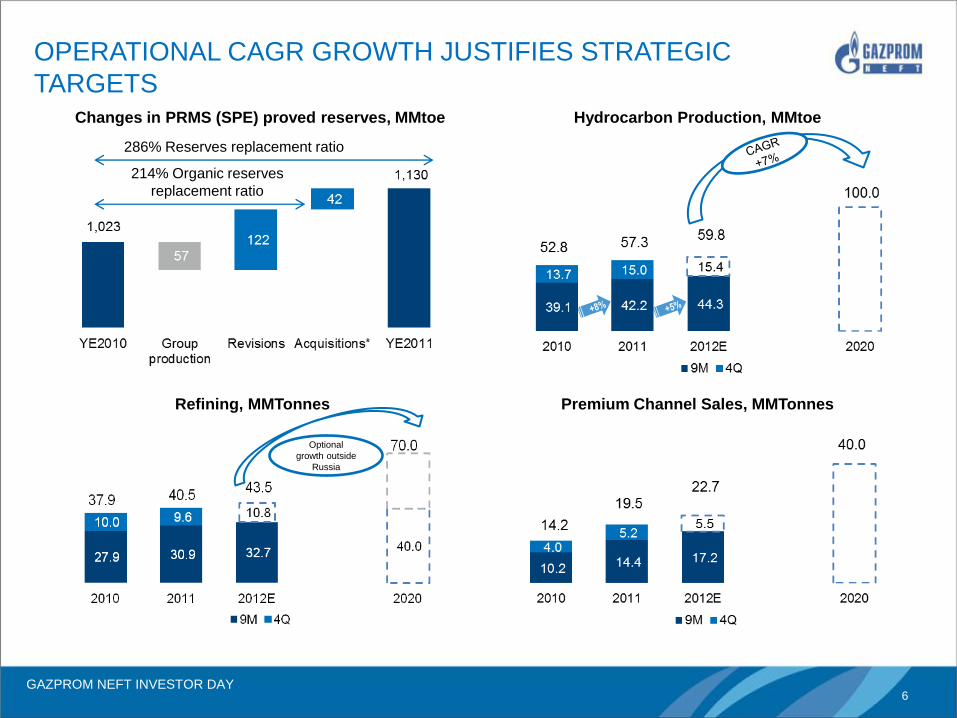

Changes in PRMS (SPE) proved reserves, MMtoe

OPERATIONAL CAGR GROWTH JUSTIFIES STRATEGIC

TARGETS

286% Reserves replacement ratio

214% Organic reserves

replacement ratio

Hydrocarbon Production, MMtoe

Refining, MMTonnes

Optional

growth outside

Russia

Premium Channel Sales, MMTonnes

GAZPROM NEFT INVESTOR DAY 7

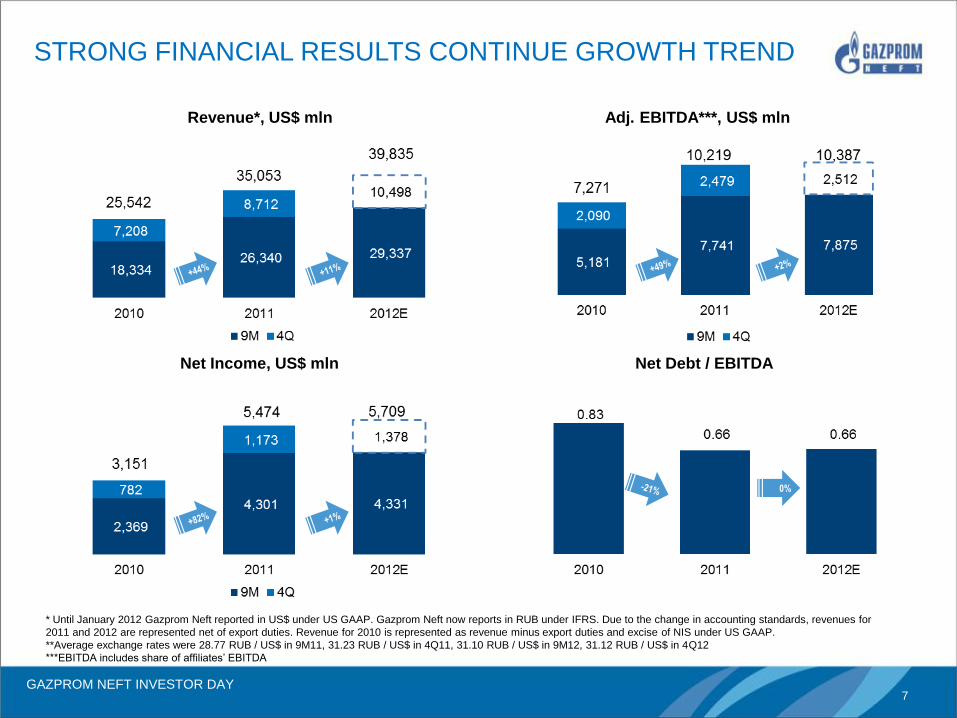

Revenue*, US$ mln

STRONG FINANCIAL RESULTS CONTINUE GROWTH TREND

Adj. EBITDA***, US$ mln

Net Income, US$ mln Net Debt / EBITDA

* Until January 2012 Gazprom Neft reported in US$ under US GAAP. Gazprom Neft now reports in RUB under IFRS. Due to the change in accounting standards, revenues for

2011 and 2012 are represented net of export duties. Revenue for 2010 is represented as revenue minus export duties and excise of NIS under US GAAP.

**Average exchange rates were 28.77 RUB / US$ in 9M11, 31.23 RUB / US$ in 4Q11, 31.10 RUB / US$ in 9M12, 31.12 RUB / US$ in 4Q12

***EBITDA includes share of affiliates’ EBITDA

0%

GAZPROM NEFT INVESTOR DAY 8

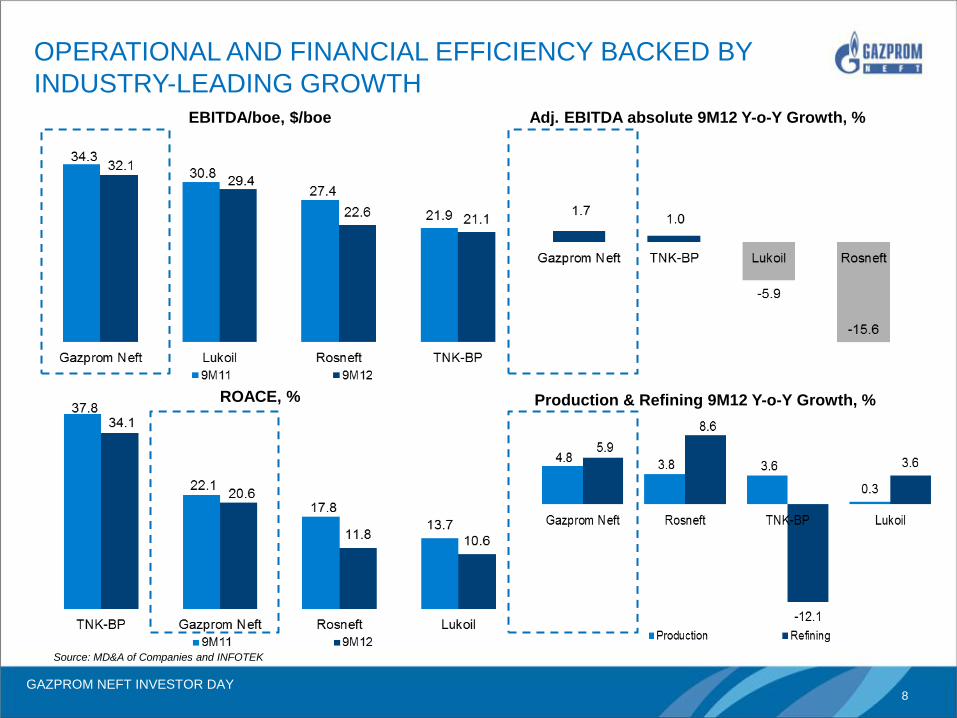

EBITDA/boe, $/boe

OPERATIONAL AND FINANCIAL EFFICIENCY BACKED BY

INDUSTRY-LEADING GROWTH Adj. EBITDA absolute 9M12 Y-o-Y Growth, %

ROACE, % Production & Refining 9M12 Y-o-Y Growth, %

Source: MD&A of Companies and INFOTEK

GAZPROM NEFT INVESTOR DAY 9

Strategy

Sergey Vakulenko

GAZPROM NEFT INVESTOR DAY 10

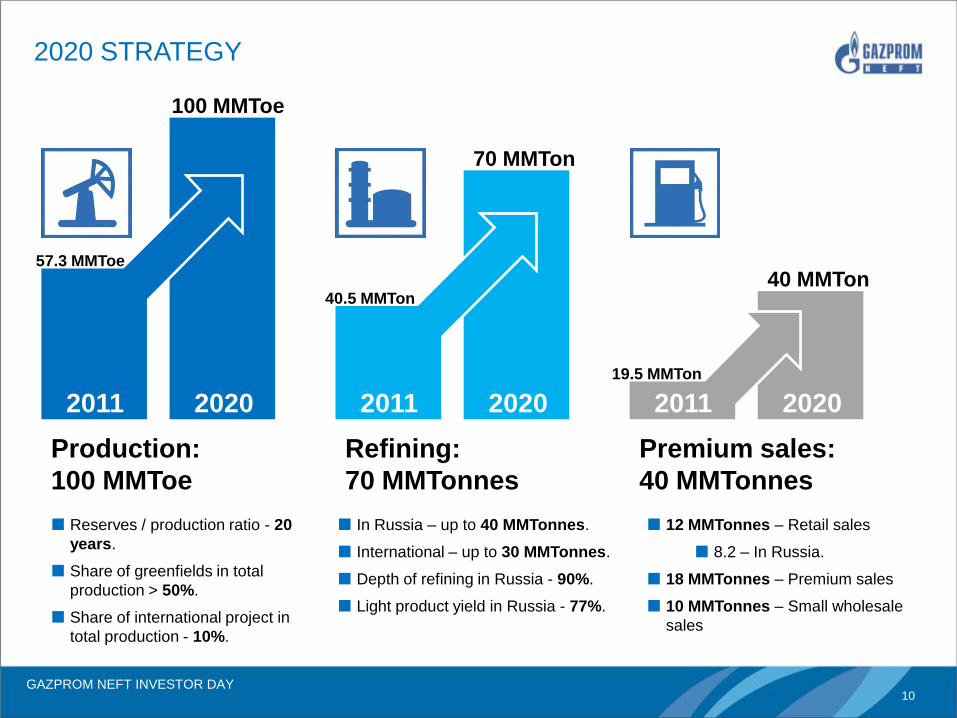

2020

19.5 MMTon

40 MMTon

Premium sales:

40 MMTonnes

2020

40.5 MMTon

70 MMTon

Refining:

70 MMTonnes

57.3 MMToe

100 MMToe

Production:

100 MMToe

Reserves / production ratio - 20

years.

Share of greenfields in total

production > 50%.

Share of international project in

total production - 10%.

2011 2020 2011 2011

In Russia – up to 40 MMTonnes.

International – up to 30 MMTonnes.

Depth of refining in Russia - 90%.

Light product yield in Russia - 77%.

12 MMTonnes – Retail sales

8.2 – In Russia.

18 MMTonnes – Premium sales

10 MMTonnes – Small wholesale

sales

2020 STRATEGY

GAZPROM NEFT INVESTOR DAY 11

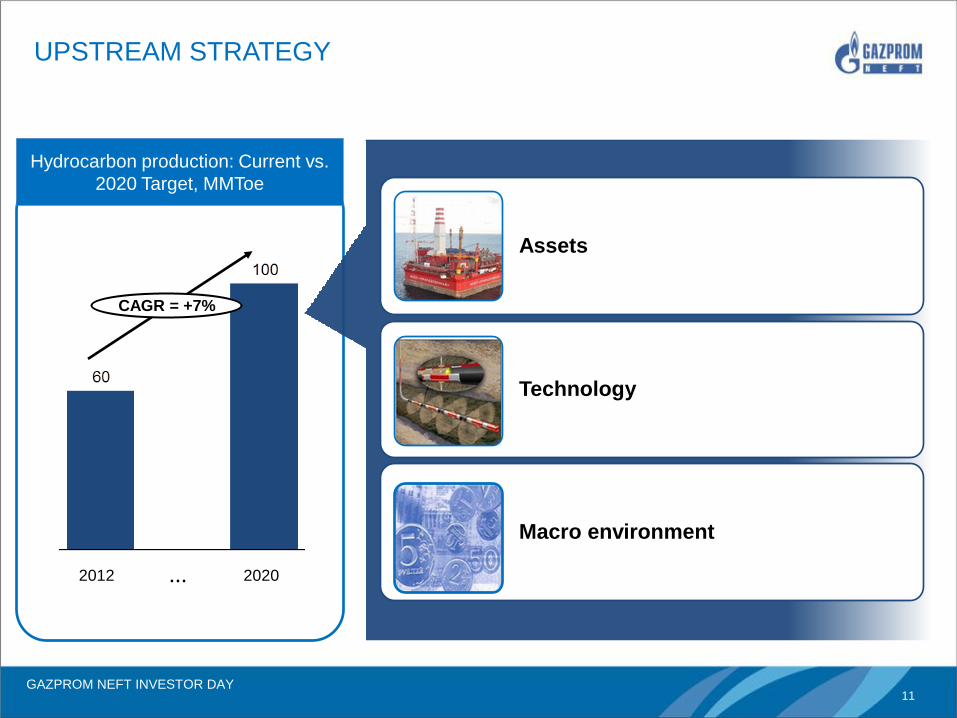

UPSTREAM STRATEGY

Hydrocarbon production: Current vs.

2020 Target, MMToe

Technology

Assets

Macro environment

...

CAGR = +7%

2020 2012

GAZPROM NEFT INVESTOR DAY 12

UPSTREAM GROWTH OPPORTUNITIES IN RUSSIA

Traditional and new production centers in Russia

- Traditional production centers

- New growth opportunities

Orenburg region:

an example of successful regional expansion

SeverEnergia

Messoyakha

Novoportovskoe

Prirazlomnoye

Dolginskoye

Chonskiy project

Kuyumba

North of YNAO

Arctic Shelf

East Siberia

• Autumn 2011 – Control over the

Eastern part of the Orenburg field

acquired;

• Autumn 2011 – Tsarichanskoye and

Kapitonovskoye fields acquired;

• Autumn 2012 – Baleykinskoye field

acquired.

• Production in Orenburg regions

exceeded 2 MMToe in 2012;

• Within five years production is

targeted to amount 6 MMToe

GAZPROM NEFT INVESTOR DAY 13

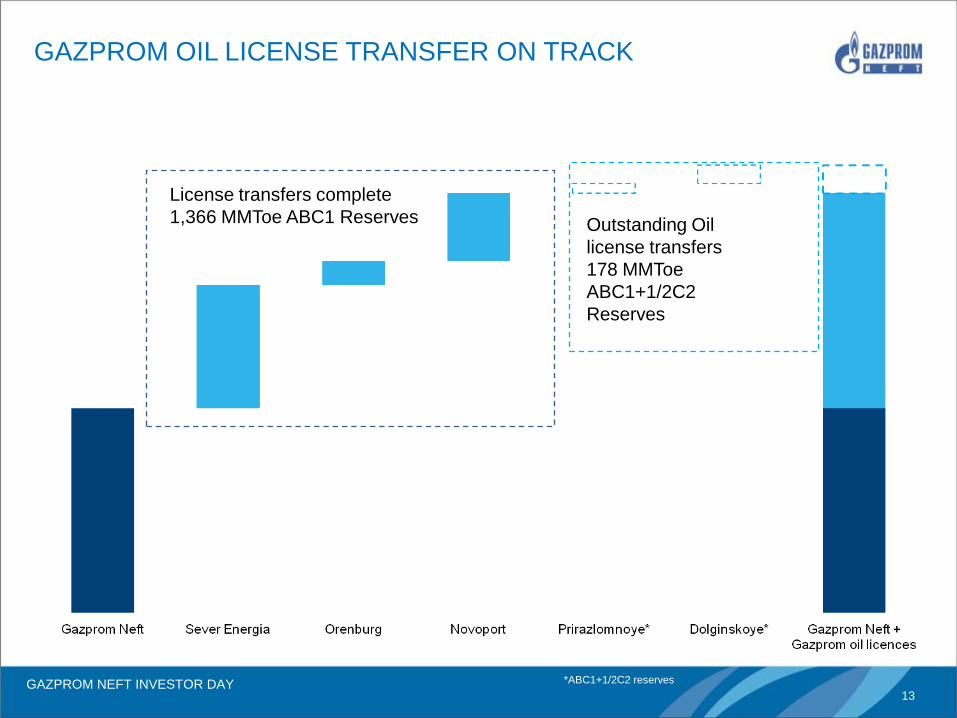

GAZPROM OIL LICENSE TRANSFER ON TRACK

Outstanding Oil

license transfers

178 MMToe

ABC1+1/2C2

Reserves

License transfers complete

1,366 MMToe ABC1 Reserves

*ABC1+1/2C2 reserves

GAZPROM NEFT INVESTOR DAY 14

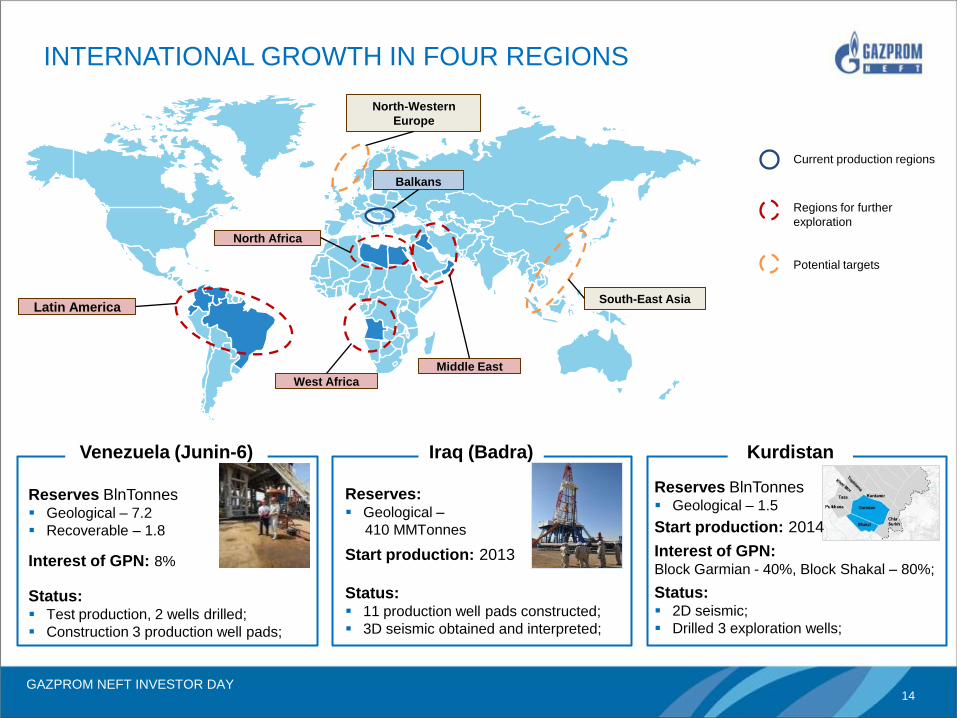

Balkans

Latin America

West Africa

North Africa

Middle East

South-East Asia

North-Western

Europe

Current production regions

Regions for further

exploration

Potential targets

Venezuela (Junin-6) Iraq (Badra) Kurdistan

Reserves: Geological –

410 MMTonnes

Start production: 2013

Status: 11 production well pads constructed;

3D seismic obtained and interpreted;

Reserves BlnTonnes Geological – 7.2

Recoverable – 1.8

Interest of GPN: 8%

Status: Test production, 2 wells drilled;

Construction 3 production well pads;

Reserves BlnTonnes Geological – 1.5

Start production: 2014

Interest of GPN: Block Garmian - 40%, Block Shakal – 80%;

Status: 2D seismic;

Drilled 3 exploration wells;

INTERNATIONAL GROWTH IN FOUR REGIONS

GAZPROM NEFT INVESTOR DAY 15

СОДЕРЖАНИЕ

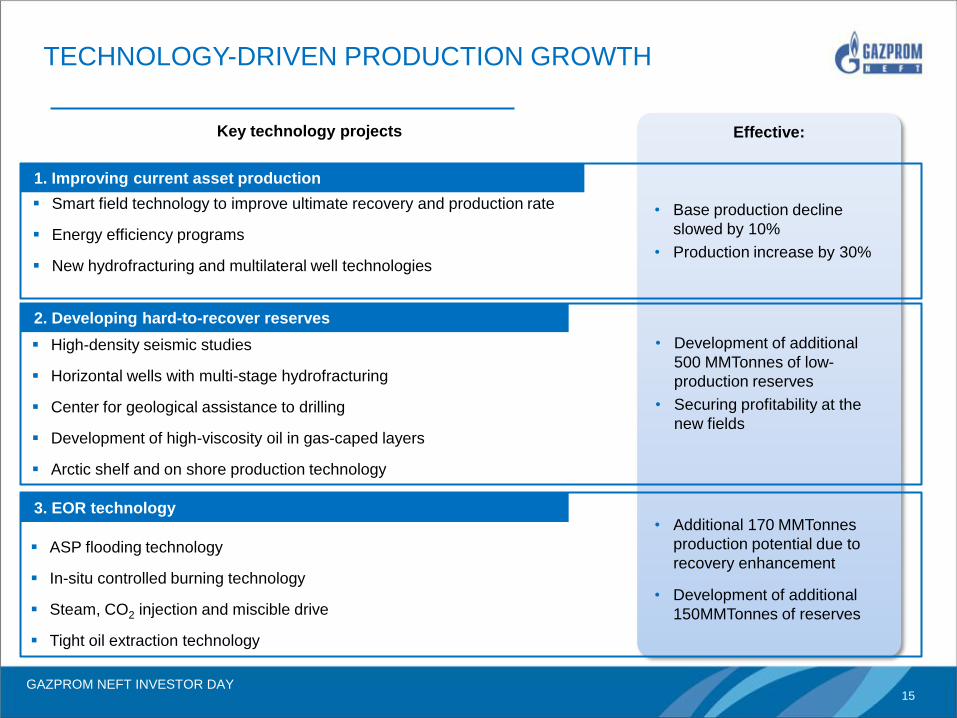

Effective:

1. Improving current asset production

2. Developing hard-to-recover reserves

3. EOR technology

Smart field technology to improve ultimate recovery and production rate

Energy efficiency programs

New hydrofracturing and multilateral well technologies

High-density seismic studies

Horizontal wells with multi-stage hydrofracturing

Center for geological assistance to drilling

Development of high-viscosity oil in gas-caped layers

Arctic shelf and on shore production technology

ASP flooding technology

In-situ controlled burning technology

Steam, CO2 injection and miscible drive

Tight oil extraction technology

• Base production decline

slowed by 10%

• Production increase by 30%

• Development of additional

500 MMTonnes of low-

production reserves

• Securing profitability at the

new fields

• Development of additional

150MMTonnes of reserves

• Additional 170 MMTonnes

production potential due to

recovery enhancement

Key technology projects

TECHNOLOGY-DRIVEN PRODUCTION GROWTH

GAZPROM NEFT INVESTOR DAY 16

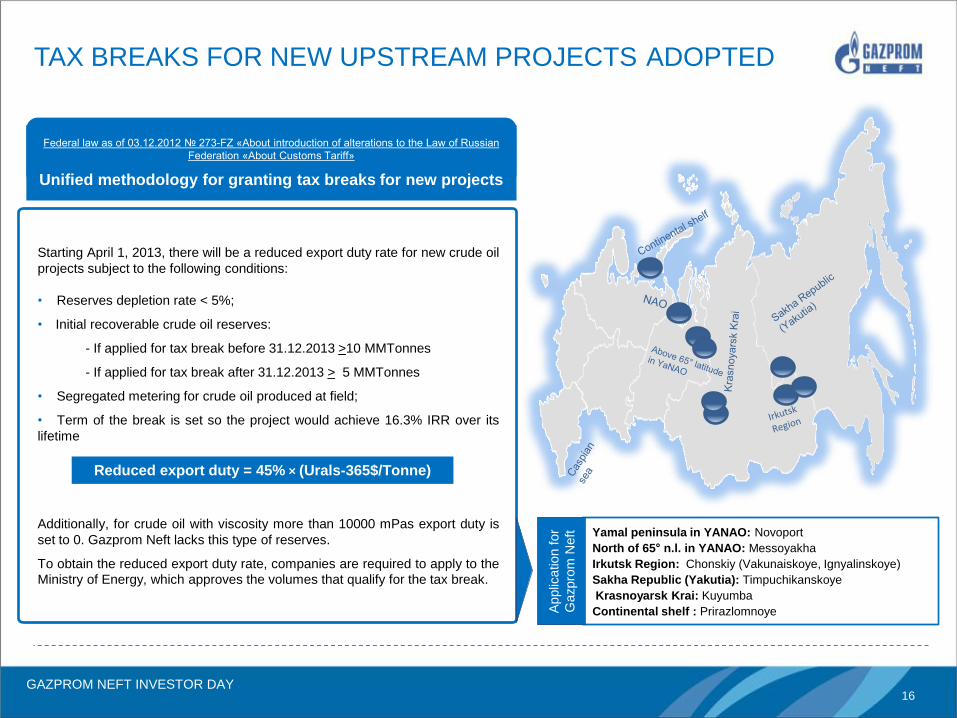

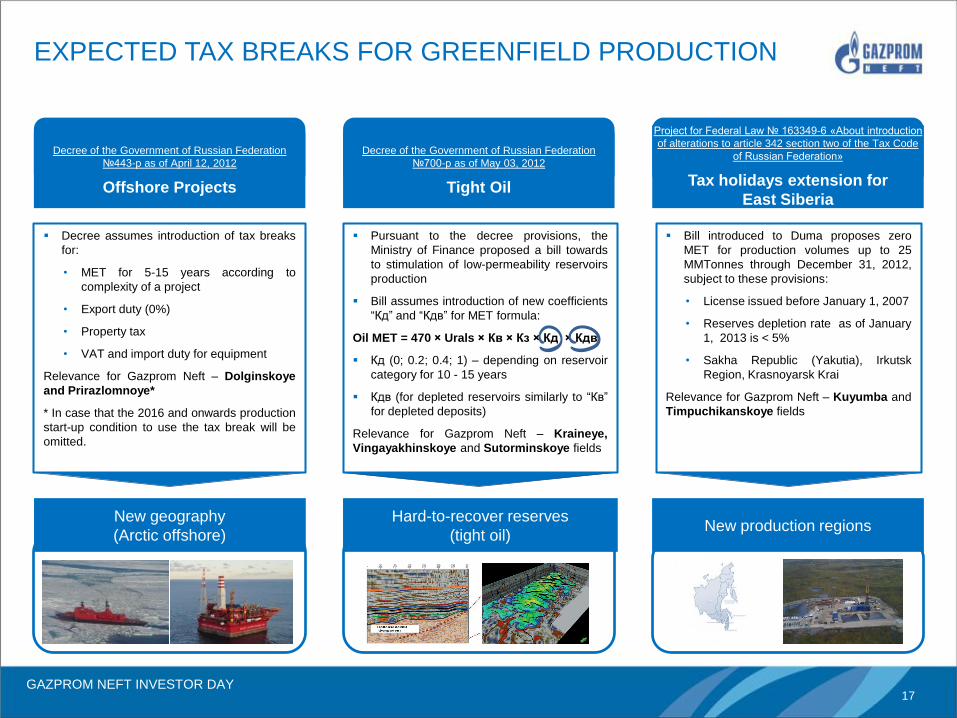

TAX BREAKS FOR NEW UPSTREAM PROJECTS ADOPTED

Формула пониженной ЭП: 45% × (Ц-365$/т), где

Starting April 1, 2013, there will be a reduced export duty rate for new crude oil

projects subject to the following conditions:

• Reserves depletion rate < 5%;

• Initial recoverable crude oil reserves:

- If applied for tax break before 31.12.2013 >10 MMTonnes

- If applied for tax break after 31.12.2013 > 5 MMTonnes

• Segregated metering for crude oil produced at field;

• Term of the break is set so the project would achieve 16.3% IRR over its

lifetime

Additionally, for crude oil with viscosity more than 10000 mPas export duty is

set to 0. Gazprom Neft lacks this type of reserves.

To obtain the reduced export duty rate, companies are required to apply to the

Ministry of Energy, which approves the volumes that qualify for the tax break.

Reduced export duty = 45% × (Urals-365$/Tonne)

Yamal peninsula in YANAO: Novoport

North of 65° n.l. in YANAO: Messoyakha

Irkutsk Region: Chonskiy (Vakunaiskoye, Ignyalinskoye)

Sakha Republic (Yakutia): Timpuchikanskoye

Krasnoyarsk Krai: Kuyumba

Continental shelf : Prirazlomnoye

Applic

ation f

or

Gazpro

m N

eft

Federal law as of 03.12.2012 № 273-FZ «About introduction of alterations to the Law of Russian

Federation «About Customs Tariff»

Unified methodology for granting tax breaks for new projects

GAZPROM NEFT INVESTOR DAY 17

New production regions

EXPECTED TAX BREAKS FOR GREENFIELD PRODUCTION

Decree of the Government of Russian Federation

№443-р as of April 12, 2012

Offshore Projects

Decree assumes introduction of tax breaks

for:

• MET for 5-15 years according to

complexity of a project

• Export duty (0%)

• Property tax

• VAT and import duty for equipment

Relevance for Gazprom Neft – Dolginskoye

and Prirazlomnoye*

* In case that the 2016 and onwards production

start-up condition to use the tax break will be

omitted.

Pursuant to the decree provisions, the

Ministry of Finance proposed a bill towards

to stimulation of low-permeability reservoirs

production

Bill assumes introduction of new coefficients

―Кд‖ and ―Кдв‖ for MET formula:

Oil MET = 470 × Urals × Кв × Кз × Кд × Кдв

Кд (0; 0.2; 0.4; 1) – depending on reservoir

category for 10 - 15 years

Кдв (for depleted reservoirs similarly to ―Кв‖

for depleted deposits)

Relevance for Gazprom Neft – Kraineye,

Vingayakhinskoye and Sutorminskoye fields

Bill introduced to Duma proposes zero

MET for production volumes up to 25

MMTonnes through December 31, 2012,

subject to these provisions:

• License issued before January 1, 2007

• Reserves depletion rate as of January

1, 2013 is < 5%

• Sakha Republic (Yakutia), Irkutsk

Region, Krasnoyarsk Krai

Relevance for Gazprom Neft – Kuyumba and

Timpuchikanskoye fields

Hard-to-recover reserves

(tight oil)

New geography

(Arctic offshore)

Decree of the Government of Russian Federation

№700-р as of May 03, 2012

Tight Oil

Project for Federal Law № 163349-6 «About introduction

of alterations to article 342 section two of the Tax Code

of Russian Federation»

Tax holidays extension for

East Siberia

GAZPROM NEFT INVESTOR DAY 18

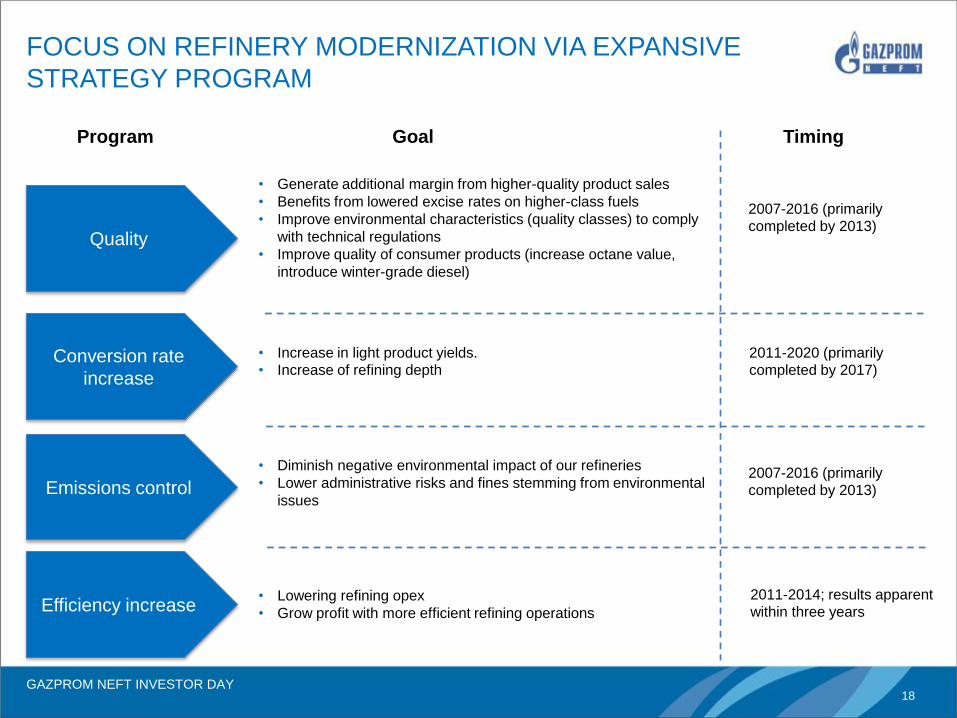

FOCUS ON REFINERY MODERNIZATION VIA EXPANSIVE

STRATEGY PROGRAM

Quality

Conversion rate

increase

Emissions control

Program Goal Timing

• Generate additional margin from higher-quality product sales

• Benefits from lowered excise rates on higher-class fuels

• Improve environmental characteristics (quality classes) to comply

with technical regulations

• Improve quality of consumer products (increase octane value,

introduce winter-grade diesel)

• Increase in light product yields.

• Increase of refining depth

• Diminish negative environmental impact of our refineries

• Lower administrative risks and fines stemming from environmental

issues

2007-2016 (primarily

completed by 2013)

2011-2020 (primarily

completed by 2017)

2007-2016 (primarily

completed by 2013)

Efficiency increase • Lowering refining opex

• Grow profit with more efficient refining operations

2011-2014; results apparent

within three years

GAZPROM NEFT INVESTOR DAY 19

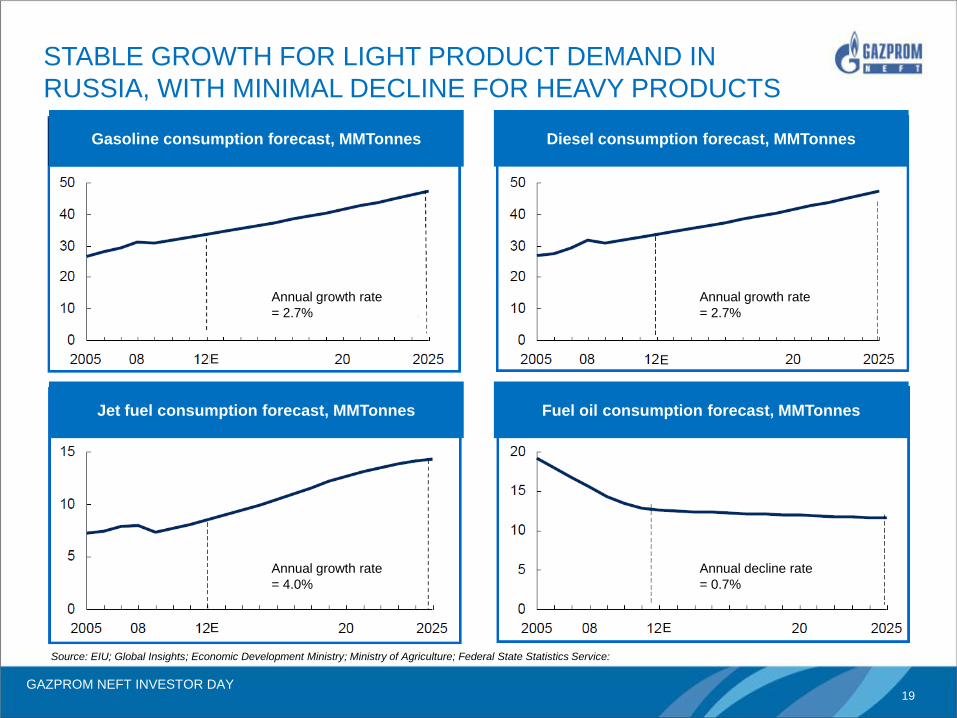

STABLE GROWTH FOR LIGHT PRODUCT DEMAND IN

RUSSIA, WITH MINIMAL DECLINE FOR HEAVY PRODUCTS

Gasoline consumption forecast, MMTonnes Diesel consumption forecast, MMTonnes

Jet fuel consumption forecast, MMTonnes Fuel oil consumption forecast, MMTonnes

Annual growth rate

= 2.7%

Annual growth rate

= 2.7%

Annual growth rate

= 4.0%

Annual decline rate

= 0.7%

E E

E E

Source: EIU; Global Insights; Economic Development Ministry; Ministry of Agriculture; Federal State Statistics Service:

GAZPROM NEFT INVESTOR DAY 20

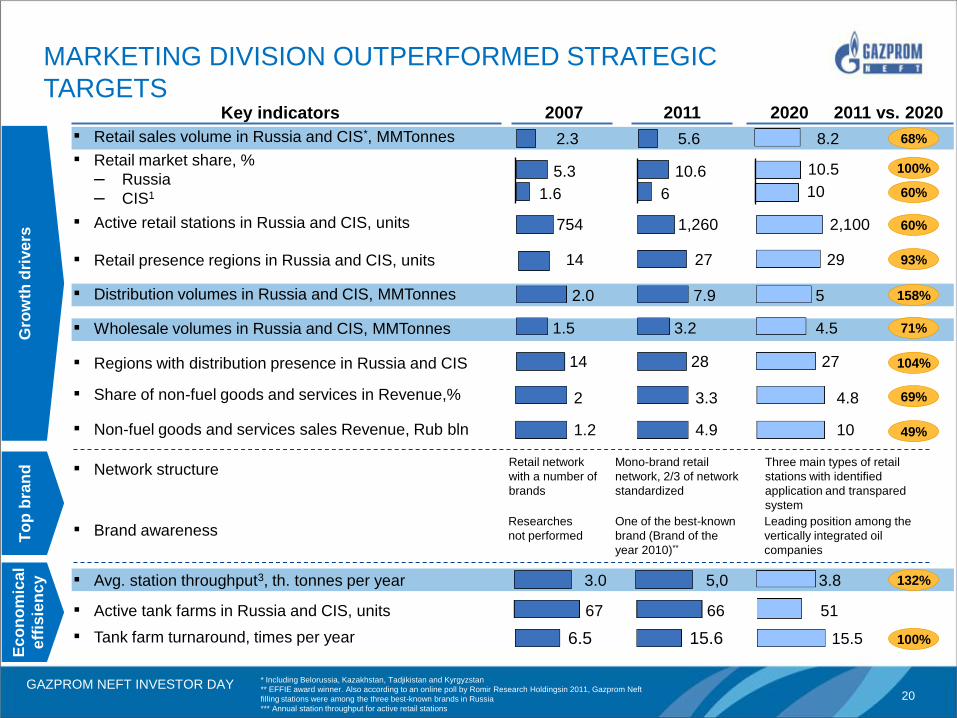

3.0

Key indicators

▪ Retail sales volume in Russia and CIS*, MMTonnes

▪ Retail market share, %

– Russia

– CIS1

▪ Active retail stations in Russia and CIS, units

▪ Distribution volumes in Russia and CIS, MMTonnes

2011

▪ Regions with distribution presence in Russia and CIS

▪ Tank farm turnaround, times per year

2.3

5.3

14

▪ Wholesale volumes in Russia and CIS, MMTonnes

▪ Active tank farms in Russia and CIS, units

▪ Avg. station throughput3, th. tonnes per year

▪ Share of non-fuel goods and services in Revenue,%

▪ Retail presence regions in Russia and CIS, units

Gro

wth

dri

ve

rs

To

p b

ran

d

Ec

on

om

ica

l

eff

isie

ncy

1.6

2.0

1.5

67

2

6.5

14

754

* Including Belorussia, Kazakhstan, Tadjikistan and Kyrgyzstan

** EFFIE award winner. Also according to an online poll by Romir Research Holdingsin 2011, Gazprom Neft

filling stations were among the three best-known brands in Russia

*** Annual station throughput for active retail stations

2020

68%

60%

93%

158%

71%

104%

132%

69%

100%

2007

51

8.2

10.5

2,100

29

10

5

4.5

3.8

15.5

4.8

27

5,0

5.6

10.6

27

6

7.9

3.2

66

3.3

15.6

28

1,260

2011 vs. 2020

▪ Brand awareness Researches

not performed

Leading position among the

vertically integrated oil

companies

One of the best-known

brand (Brand of the

year 2010)**

▪ Non-fuel goods and services sales Revenue, Rub bln 1.2 49% 10 4.9

▪ Network structure Retail network

with a number of

brands

Mono-brand retail

network, 2/3 of network

standardized

100%

60%

Three main types of retail

stations with identified

application and transpared

system

MARKETING DIVISION OUTPERFORMED STRATEGIC

TARGETS

GAZPROM NEFT INVESTOR DAY 21

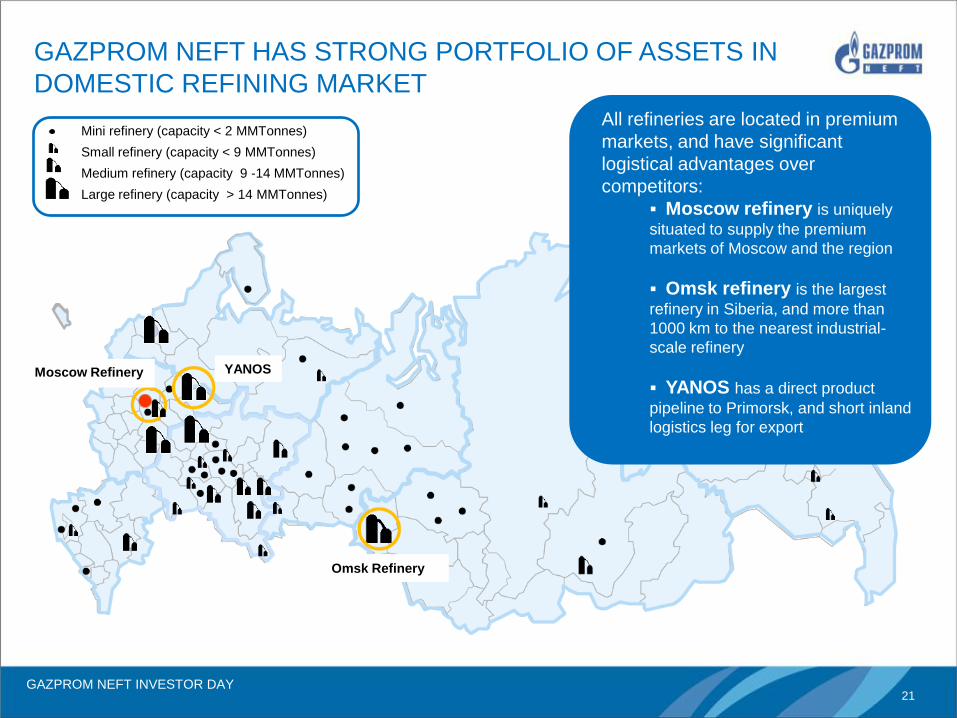

GAZPROM NEFT HAS STRONG PORTFOLIO OF ASSETS IN

DOMESTIC REFINING MARKET

Mini refinery (capacity < 2 MMTonnes)

Small refinery (capacity < 9 MMTonnes)

Medium refinery (capacity 9 -14 MMTonnes)

Large refinery (capacity > 14 MMTonnes)

Moscow Refinery YANOS

Omsk Refinery

All refineries are located in premium

markets, and have significant

logistical advantages over

competitors:

Moscow refinery is uniquely

situated to supply the premium

markets of Moscow and the region

Omsk refinery is the largest

refinery in Siberia, and more than

1000 km to the nearest industrial-

scale refinery

YANOS has a direct product

pipeline to Primorsk, and short inland

logistics leg for export

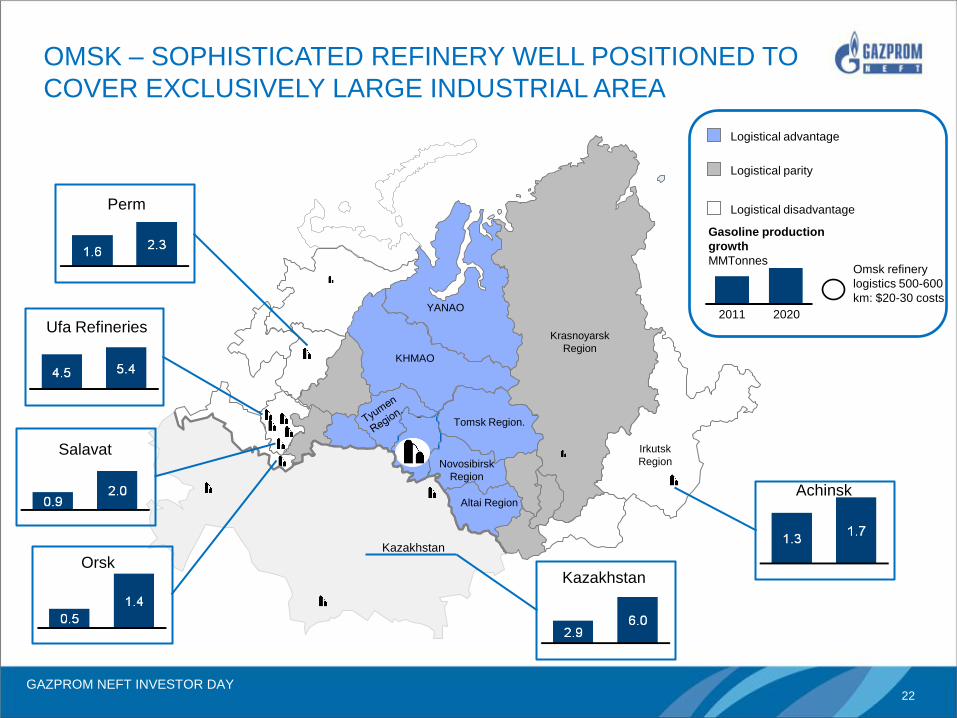

GAZPROM NEFT INVESTOR DAY 22

5,7 4,7

Krasnoyarsk

Region

Irkutsk

Region

YANAO

KHMAO

Tomsk Region.

Altai Region

Novosibirsk

Region

Kazakhstan

2020 2011

Gasoline production

growth

MMTonnes

Logistical advantage

Logistical parity

Logistical disadvantage

Omsk refinery

logistics 500-600

km: $20-30 costs

Perm

Ufa Refineries

Salavat

Orsk Kazakhstan

Achinsk

OMSK – SOPHISTICATED REFINERY WELL POSITIONED TO

COVER EXCLUSIVELY LARGE INDUSTRIAL AREA

GAZPROM NEFT INVESTOR DAY 23

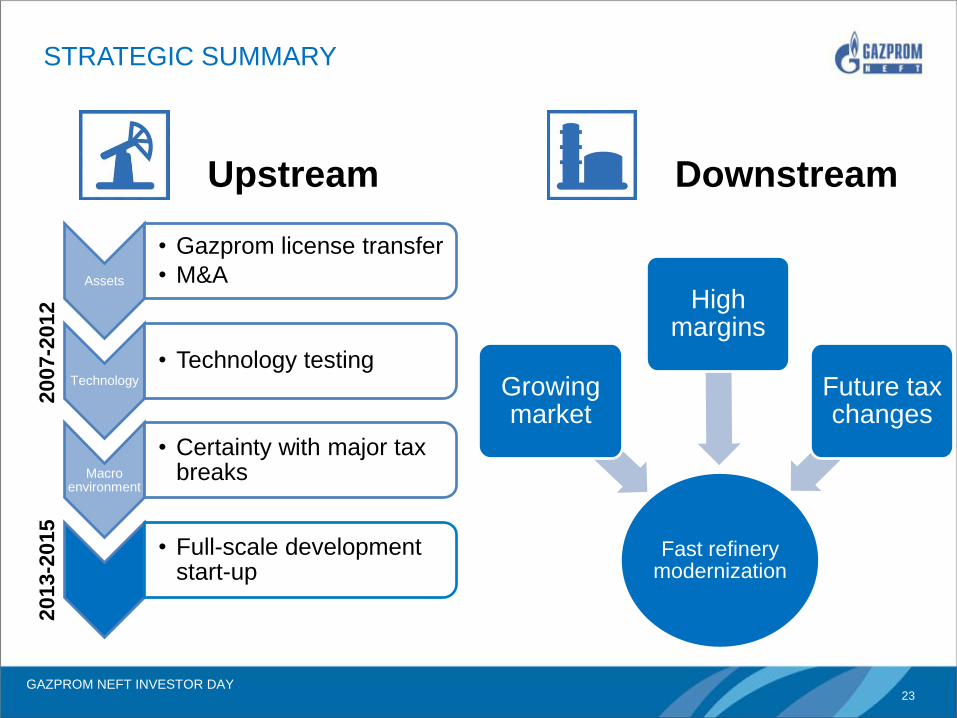

Upstream Downstream

Assets

• Gazprom license transfer

• M&A

Technology

• Technology testing

Macro environment

• Certainty with major tax breaks

• Full-scale development start-up

20

07-2

01

2

20

13

-20

15

Fast refinery modernization

Growing market

High margins

Future tax changes

STRATEGIC SUMMARY

GAZPROM NEFT INVESTOR DAY 24

Upstream

Vadim Yakovlev

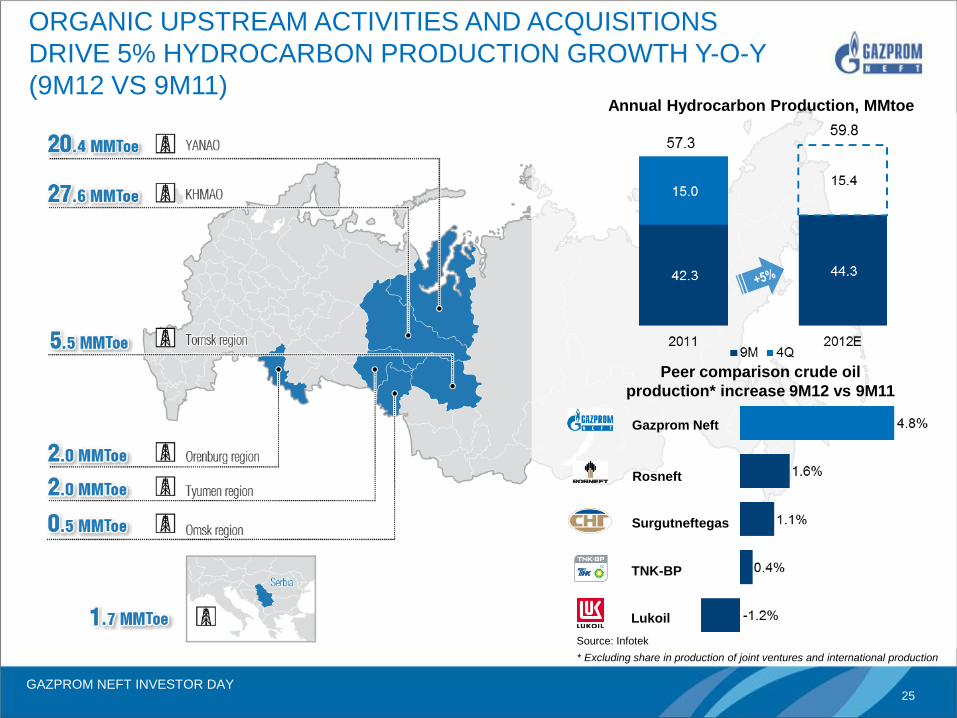

GAZPROM NEFT INVESTOR DAY 25

Annual Hydrocarbon Production, MMtoe

Peer comparison crude oil

production* increase 9M12 vs 9M11

Lukoil

ORGANIC UPSTREAM ACTIVITIES AND ACQUISITIONS

DRIVE 5% HYDROCARBON PRODUCTION GROWTH Y-O-Y

(9M12 VS 9M11)

* Excluding share in production of joint ventures and international production

Gazprom Neft

Lukoil

Rosneft

Surgutneftegas

TNK-BP

Source: Infotek

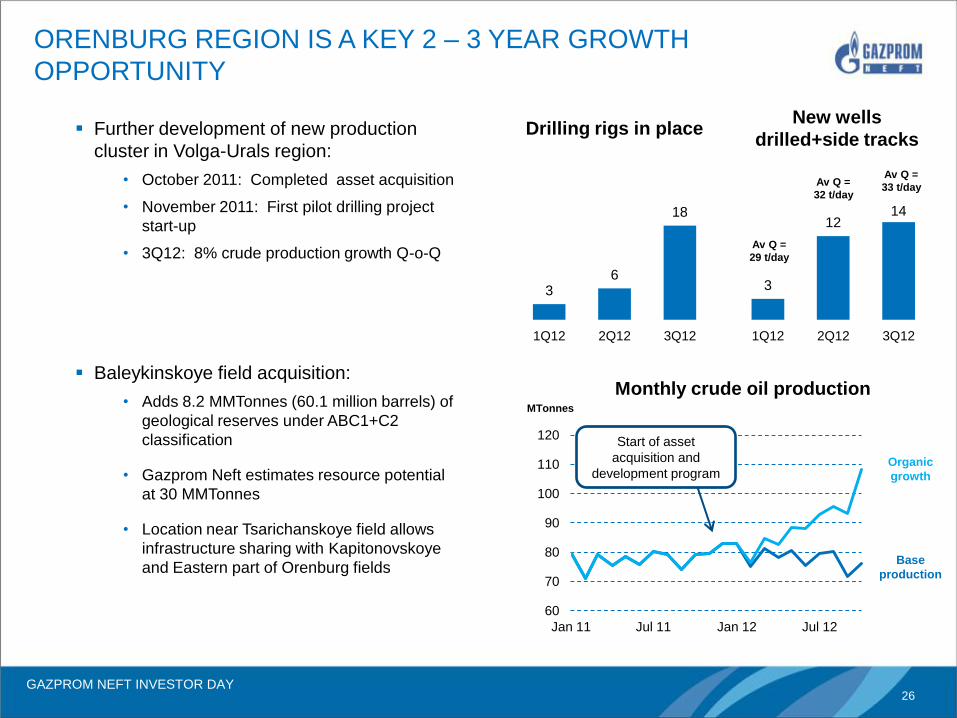

GAZPROM NEFT INVESTOR DAY 26

Further development of new production

cluster in Volga-Urals region:

• October 2011: Completed asset acquisition

• November 2011: First pilot drilling project

start-up

• 3Q12: 8% crude production growth Q-o-Q

Baleykinskoye field acquisition:

• Adds 8.2 MMTonnes (60.1 million barrels) of

geological reserves under ABC1+C2

classification

• Gazprom Neft estimates resource potential

at 30 MMTonnes

• Location near Tsarichanskoye field allows

infrastructure sharing with Kapitonovskoye

and Eastern part of Orenburg fields

ORENBURG REGION IS A KEY 2 – 3 YEAR GROWTH

OPPORTUNITY

60

70

80

90

100

110

120

Jan 11 Jul 11 Jan 12 Jul 12

3 6

18

1Q12 2Q12 3Q12

3

12 14

1Q12 2Q12 3Q12

Drilling rigs in place New wells

drilled+side tracks

Start of asset

acquisition and

development program

Monthly crude oil production MTonnes

Av Q =

29 t/day

Av Q =

32 t/day

Av Q =

33 t/day

Organic

growth

Base

production

GAZPROM NEFT INVESTOR DAY 27

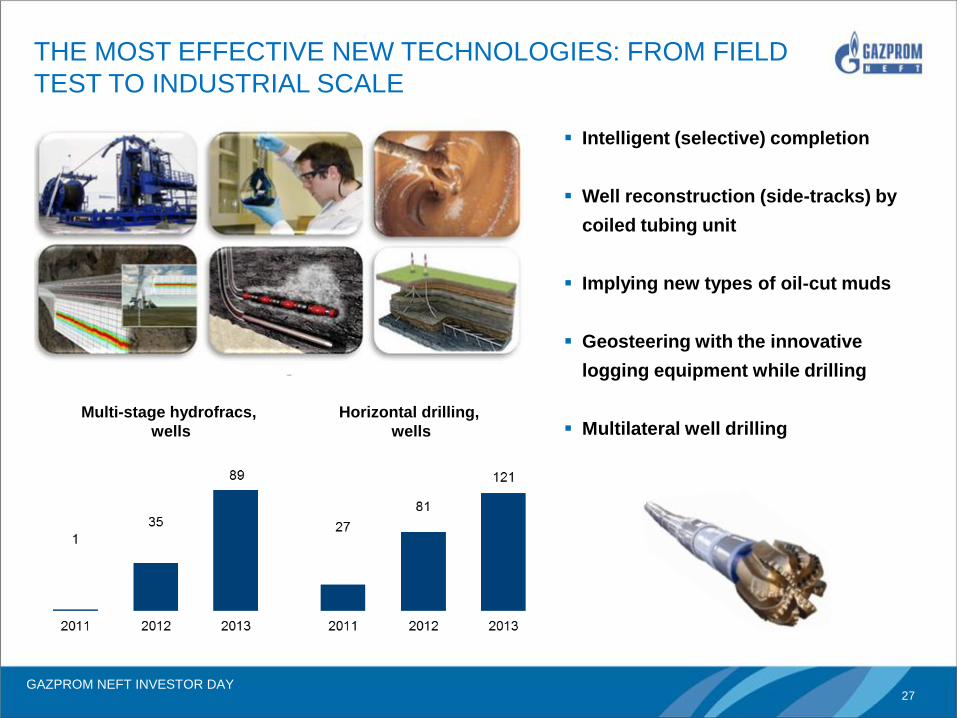

THE MOST EFFECTIVE NEW TECHNOLOGIES: FROM FIELD

TEST TO INDUSTRIAL SCALE

Intelligent (selective) completion

Well reconstruction (side-tracks) by

coiled tubing unit

Implying new types of oil-cut muds

Geosteering with the innovative

logging equipment while drilling

Multilateral well drilling

Multi-stage hydrofracs,

wells

Horizontal drilling,

wells

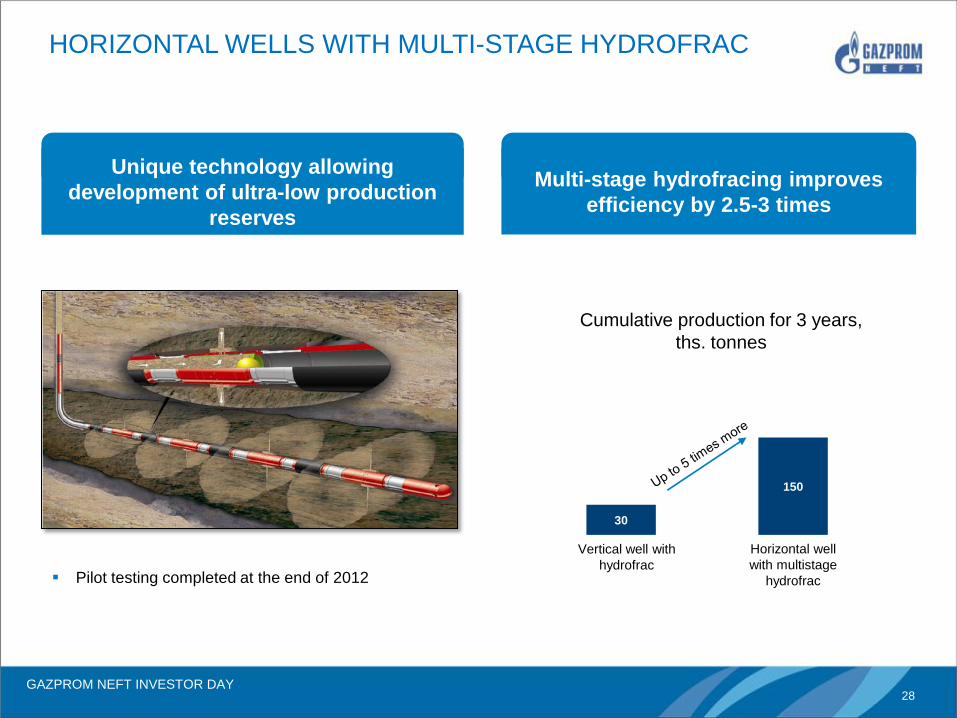

GAZPROM NEFT INVESTOR DAY 28

Pilot testing completed at the end of 2012

HORIZONTAL WELLS WITH MULTI-STAGE HYDROFRAC

30

150

Vertical well with

hydrofrac

Horizontal well

with multistage

hydrofrac

Unique technology allowing

development of ultra-low production

reserves

Multi-stage hydrofracing improves

efficiency by 2.5-3 times

Cumulative production for 3 years,

ths. tonnes

GAZPROM NEFT INVESTOR DAY 29

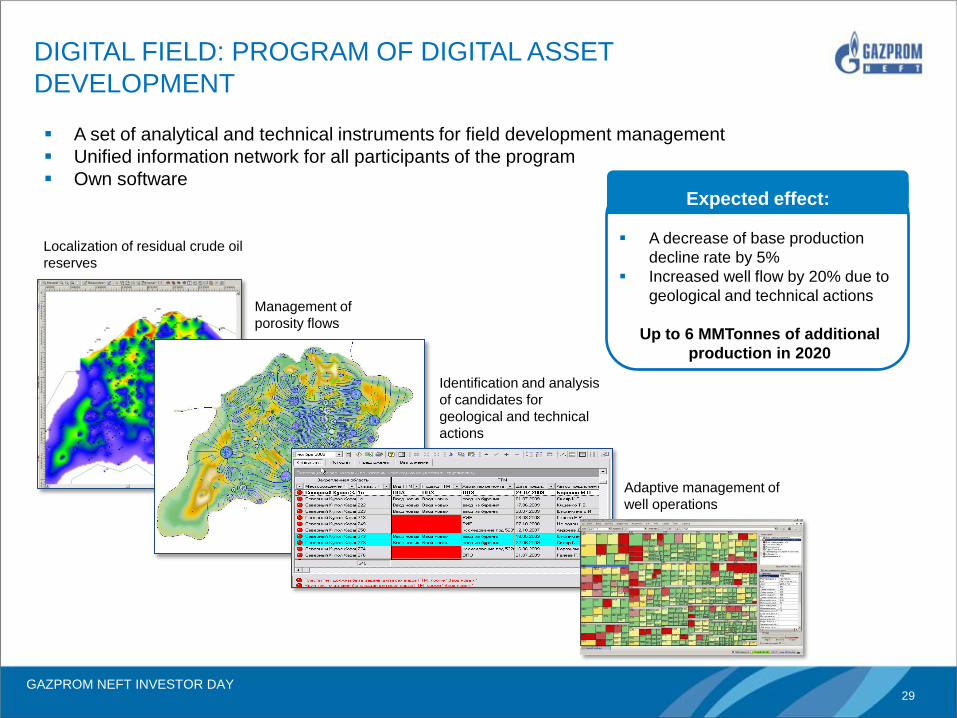

DIGITAL FIELD: PROGRAM OF DIGITAL ASSET

DEVELOPMENT

Localization of residual crude oil

reserves

Management of

porosity flows

Identification and analysis

of candidates for

geological and technical

actions

Adaptive management of

well operations

A set of analytical and technical instruments for field development management

Unified information network for all participants of the program

Own software

Expected effect:

A decrease of base production

decline rate by 5%

Increased well flow by 20% due to

geological and technical actions

Up to 6 MMTonnes of additional

production in 2020

GAZPROM NEFT INVESTOR DAY 30

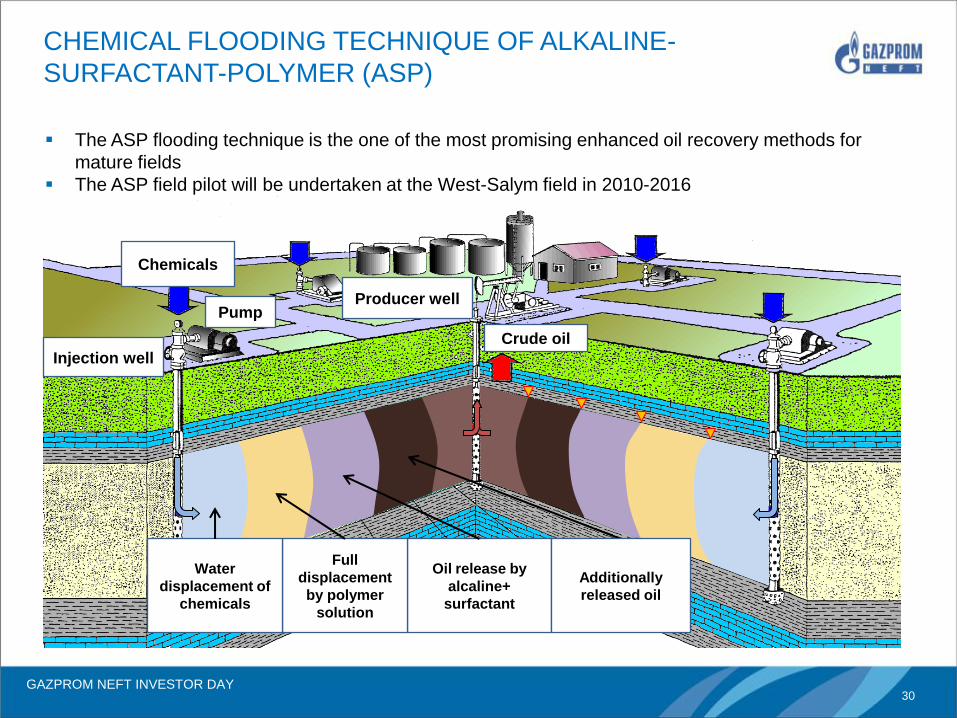

CHEMICAL FLOODING TECHNIQUE OF ALKALINE-

SURFACTANT-POLYMER (ASP)

Producer well

Crude oil

Chemicals

Injection well

Pump

Oil release by

alcaline+

surfactant

Full

displacement

by polymer

solution

Water

displacement of

chemicals

Additionally

released oil

The ASP flooding technique is the one of the most promising enhanced oil recovery methods for

mature fields

The ASP field pilot will be undertaken at the West-Salym field in 2010-2016

GAZPROM NEFT INVESTOR DAY 31

Resource potential, production profile (Kapiton-oe)

Resource potential, production profile (Tsarich-oe)

ORENBURG

1.6

2011

3

2

1

0

2030

0.2 0.5

2025

1.1

2020

2.1 2.3

2015

Oil+Condensate

Gas

Добыча УВ, млн.т.н.э.

С3

2.3

С2

16.4

С1

7.6 2.1

С1 С3

0.3

С2

1.0

Resource potential, production profile (Orenburg)

5

4

3

2

1

0

2030

2.1 2.6

2025

3.4

2020

4.6

2015

3.3

2011

Oil+Condensate

Gas

Добыча УВ, млн.т.н.э. С2

0.5

С1

97.6

С2

2.1

С1

51.1

С2

0.1

С1

9.8

Crude oil, MMTonnes Gas, bcm Gas, bcm Dissolved gas, bcm

2011 2015

0.6 1

0

2030

0.1 0.1

2025

0.2

2020

0.3 0.4

Oil+Condensate

Gas

Добыча УВ, млн.т.н.э.

С2

0.4

С1

4.8

С2

0.1

С1

2.4

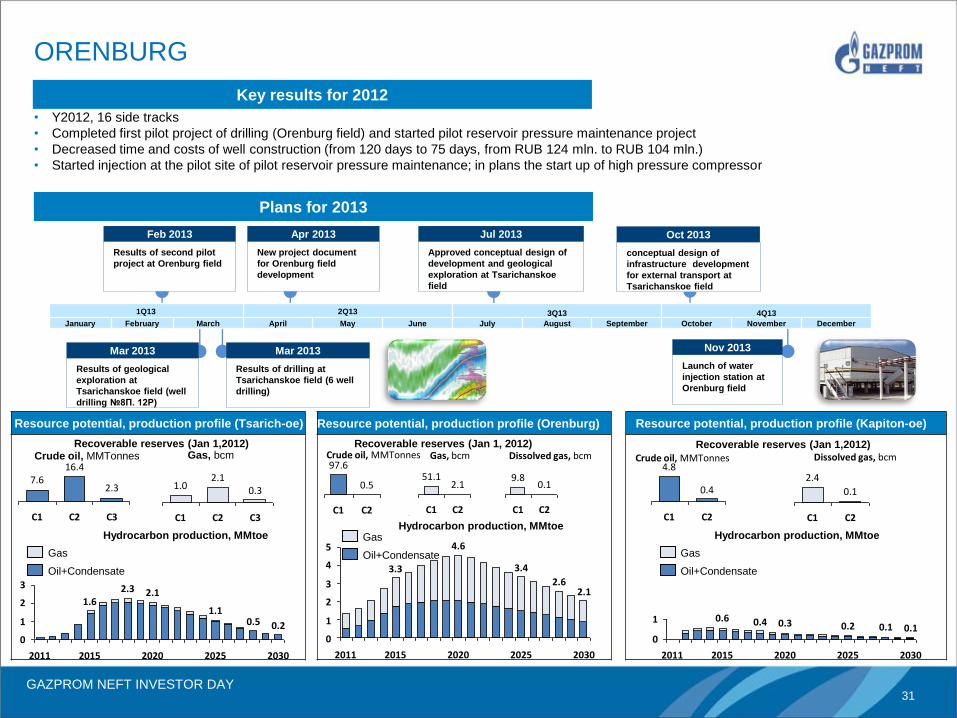

Key results for 2012

Plans for 2013

1Q13 2Q13 3Q13 4Q13

January February March April May June July August September October November December

Results of second pilot

project at Orenburg field

Feb 2013

• Y2012, 16 side tracks

• Completed first pilot project of drilling (Orenburg field) and started pilot reservoir pressure maintenance project

• Decreased time and costs of well construction (from 120 days to 75 days, from RUB 124 mln. to RUB 104 mln.)

• Started injection at the pilot site of pilot reservoir pressure maintenance; in plans the start up of high pressure compressor

Recoverable reserves (Jan 1,2012) Recoverable reserves (Jan 1, 2012) Recoverable reserves (Jan 1,2012) Crude oil, MMTonnes Crude oil, MMTonnes Dissolved gas, bcm

Hydrocarbon production, MMtoe Hydrocarbon production, MMtoe Hydrocarbon production, MMtoe

New project document

for Orenburg field

development

Apr 2013

Approved conceptual design of

development and geological

exploration at Tsarichanskoe

field

Jul 2013

conceptual design of

infrastructure development

for external transport at

Tsarichanskoe field

Oct 2013

Results of drilling at

Tsarichanskoe field (6 well

drilling)

Mar 2013

Results of geological

exploration at

Tsarichanskoe field (well

drilling №8П. 12Р)

Mar 2013

Launch of water

injection station at

Orenburg field

Nov 2013

GAZPROM NEFT INVESTOR DAY 32

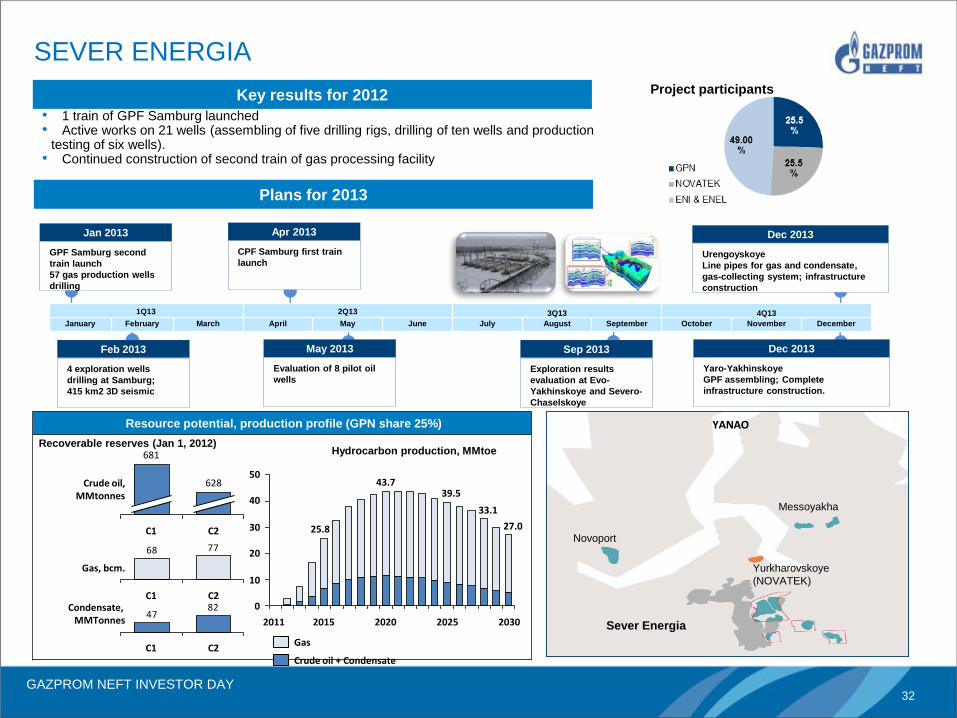

Resource potential, production profile (GPN share 25%)

• 1 train of GPF Samburg launched • Active works on 21 wells (assembling of five drilling rigs, drilling of ten wells and production

testing of six wells). • Continued construction of second train of gas processing facility

SEVER ENERGIA

30

20

10

0

2030

50

40

27.0

33.1

2025

39.5

2020

43.7

2015

25.8

2011

Crude oil + Condensate

Gas

Hydrocarbon production, MMtoe Recoverable reserves (Jan 1, 2012)

Crude oil, MMtonnes

С2

628

С1

681

7768

Gas, bcm.

С2 С1 82

47Condensate,

MMTonnes

С2 С1

Novoport

Yurkharovskoye

(NOVATEK)

Sever Energia

Messoyakha

YANAO

Key results for 2012

Plans for 2013

1Q13 2Q13 3Q13 4Q13

January February March April May June July August September October November December

GPF Samburg second

train launch

57 gas production wells

drilling

Jan 2013

CPF Samburg first train

launch

Apr 2013

Urengoyskoye

Line pipes for gas and condensate,

gas-collecting system; infrastructure

construction

Dec 2013

4 exploration wells

drilling at Samburg;

415 km2 3D seismic

Feb 2013

Evaluation of 8 pilot oil

wells

May 2013

Exploration results

evaluation at Evo-

Yakhinskoye and Severo-

Chaselskoye

Sep 2013

Yaro-Yakhinskoye

GPF assembling; Complete

infrastructure construction.

Dec 2013

Project participants

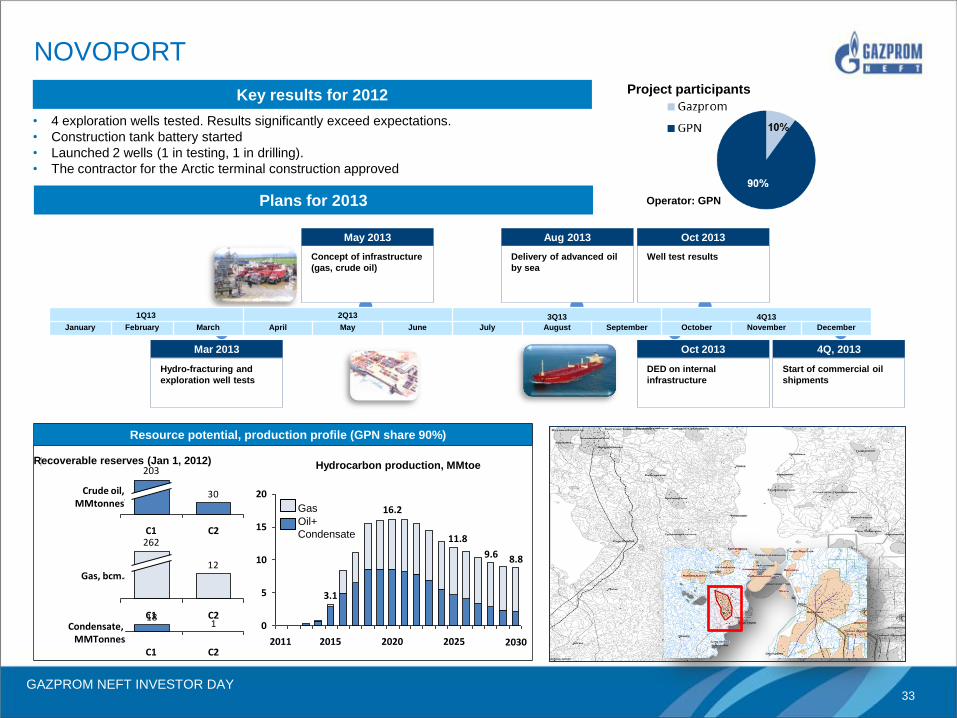

GAZPROM NEFT INVESTOR DAY 33

Resource potential, production profile (GPN share 90%)

• 4 exploration wells tested. Results significantly exceed expectations.

• Construction tank battery started

• Launched 2 wells (1 in testing, 1 in drilling).

• The contractor for the Arctic terminal construction approved

NOVOPORT

20

15

10

5

0

2030

8.8 9.6

2025

11.8

2020

16.2

2015

3.1

2011

Нефть +конденсат

Газ

Добыча УВ, млн.т.н.э. Извлекаемые запасы (01.01.12г.)

30Нефть, Млн. т.

С2 С1

203

Oil+

Condensate

Gas

12Газ, млрд. м3.

С2 С1

262

118

С2

Конденсат, Млн. т.

С1

Key results for 2012

Plans for 2013

Concept of infrastructure

(gas, crude oil)

May 2013

Hydrocarbon production, MMtoe

Crude oil, MMtonnes

Gas, bcm.

Condensate, MMTonnes

Recoverable reserves (Jan 1, 2012)

1Q13 2Q13 3Q13 4Q13

January February March April May June July August September October November December

Start of commercial oil

shipments

4Q, 2013

Hydro-fracturing and

exploration well tests

Mar 2013

Well test results

Oct 2013

Delivery of advanced oil

by sea

Aug 2013

DED on internal

infrastructure

Oct 2013

Project participants

Operator: GPN

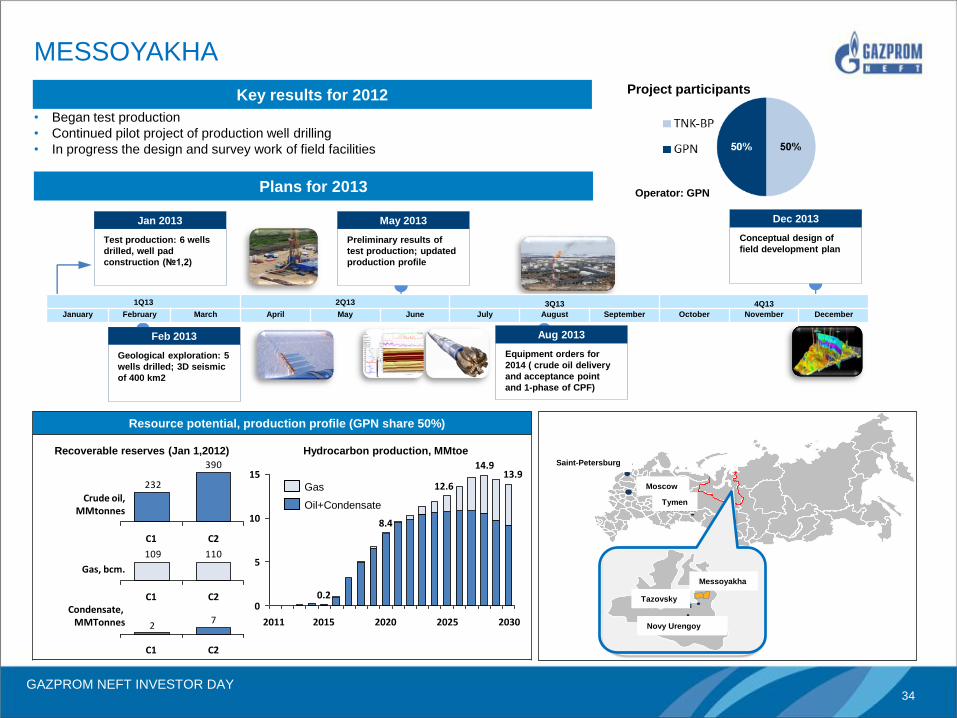

GAZPROM NEFT INVESTOR DAY 34

Resource potential, production profile (GPN share 50%)

MESSOYAKHA

Тюмень

Москва

Мессояха

Новый-Уренгой

Тазовский

Санкт-Петербург

Project participants

Operator: GPN

15

10

5

0

2030

13.9 14.9

2025

12.6

2020

8.4

2015

0.2

2011

Oil+Condensate

Gas

Hydrocarbon production, MMtoe

390

232

Crude oil, MMtonnes

С2 С1

110109

С2 С1

Gas, bcm.

72

Condensate, MMTonnes

С2 С1

Key results for 2012

• Began test production

• Continued pilot project of production well drilling

• In progress the design and survey work of field facilities

Plans for 2013

1Q13 2Q13 3Q13 4Q13

January February March April May June July August September October November December

Recoverable reserves (Jan 1,2012) Saint-Petersburg

Messoyakha

Tazovsky

Novy Urengoy

Tymen

Moscow

Test production: 6 wells

drilled, well pad

construction (№1,2)

Jan 2013

Preliminary results of

test production; updated

production profile

May 2013

Conceptual design of

field development plan

Dec 2013

Geological exploration: 5

wells drilled; 3D seismic

of 400 km2

Feb 2013

Equipment orders for

2014 ( crude oil delivery

and acceptance point

and 1-phase of CPF)

Aug 2013

GAZPROM NEFT INVESTOR DAY 35

Resource potential, production profile

0

1000

2000

3000

4000

2014 2017 2020 2023 2026 2029 2032

―North unit‖

• Well re-entry completed: 120 cm/day of oil natural flow rate after hydrofrac at

Timpuchikanskiy block

• Engineering data sheet drawing for test production at Timpuchikanskiy block

approved

―South unit‖

• 300 km2 3D seismic, 1500 km electric exploration

CHONSKIY

―South unit‖

Phase-1

5

125

С2

Crude oil,

MMtonnes

С1

Gas, bcm 287

1356

Crude oil Gas

Hydrocarbon production, MMtoe

3.1

1.3

1.9

2.6

3.6

0.8

Key results for 2012

Plans for 2013

Recoverable reserves (Jan 1, 2012)

Financing structure

1Q13 2Q13 3Q13 4Q13

January February March April May June July August September October November December

Test production at 96 Р

Timpuchikanskiy block

Jan 2013

Concepts of development strategy

and production technology

Sep 2013

Preliminary results for

2012-2013 exploration

Aug 2013

Exploration: «North unit»

Drilling 2 wells, 350 km2 3D seismic;

Exploration: «South unit»

Drilling 2 wells, 150 km2 3D seismic

Jan 2013

2013 – 2014 exploration

Nov 2013

Chita

Irkutsk

Balagansk

Ilimsk

Ust-Kut Noviy

Uoyan

Bratsk

Nighnyaya

Poyma

Chuya

Chayandinskoe

Chonskiy

Sobinsko-

Payginskoe

Kovikhtinskoe

―North unit‖

GAZPROM NEFT INVESTOR DAY 36

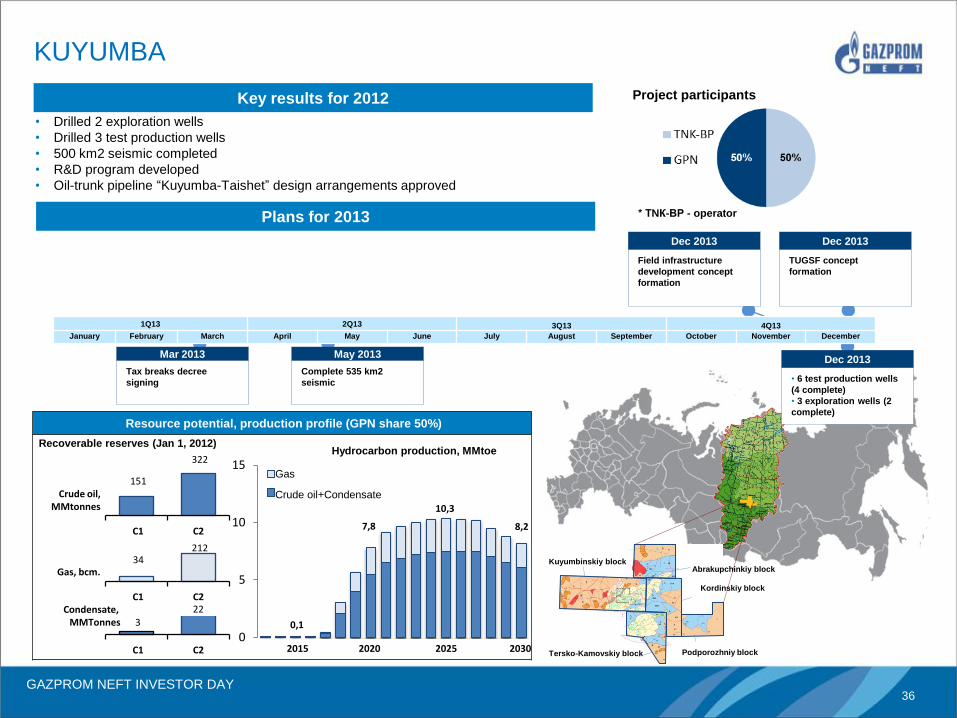

Resource potential, production profile (GPN share 50%)

• Drilled 2 exploration wells

• Drilled 3 test production wells

• 500 km2 seismic completed

• R&D program developed

• Oil-trunk pipeline ―Kuyumba-Taishet‖ design arrangements approved

KUYUMBA

Hydrocarbon production, MMtoe

151

322

Crude oil, MMtonnes

С2 С1

34 212

Gas, bcm.

С2

3 Condensate,

MMTonnes

С2 С1

50%

Kuyumbinskiy block

Kordinskiy block

Abrakupchinkiy block

Podporozhniy block Tersko-Kamovskiy block

50%

Crude oil + Condensate

22 С1

0

5

10

15 Газ

Нефть+конденсат

2030 2025

10,3

2020 2015

8,2 7,8

0,1

Key results for 2012

Plans for 2013

1Q13 2Q13 3Q13 4Q13

January February March April May June July August September October November December

Project participants

* ТNК-ВР - operator

Recoverable reserves (Jan 1, 2012)

Gas

Crude oil+Condensate

Field infrastructure

development concept

formation

Dec 2013

TUGSF concept

formation

Dec 2013

• 6 test production wells

(4 complete)

• 3 exploration wells (2

complete)

Dec 2013 Complete 535 km2

seismic

May 2013

Tax breaks decree

signing

Mar 2013

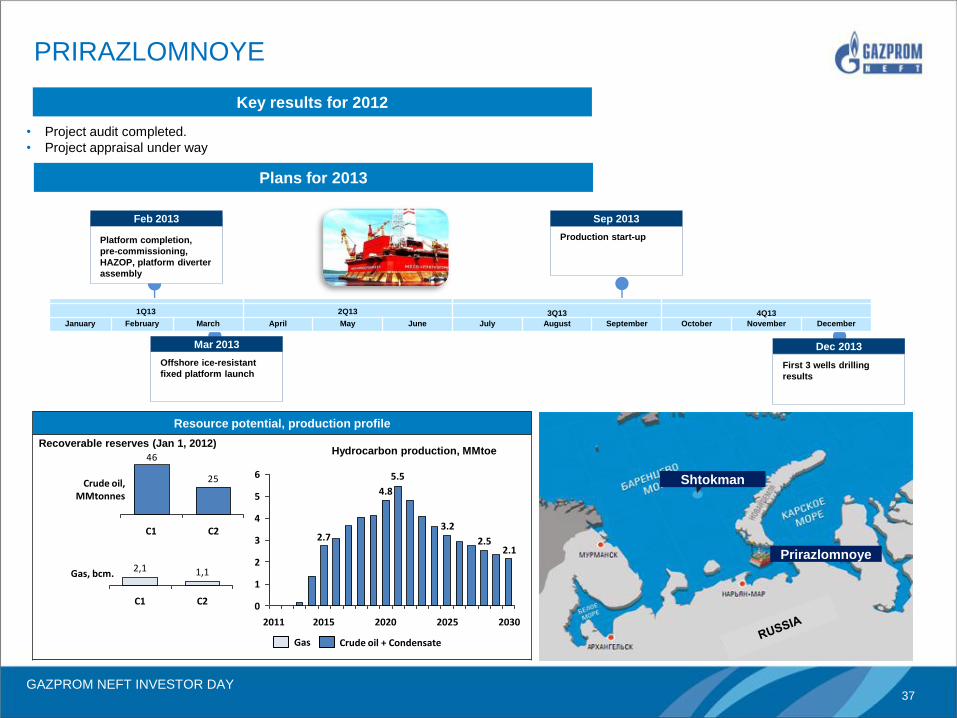

GAZPROM NEFT INVESTOR DAY 37

Resource potential, production profile

PRIRAZLOMNOYE

2025

3.2

5.5

2020

4.8

2015

2.7

2011

6

5

4

3

2

1

0

2030

2.1 2.5

Crude oil + Condensate Gas

Hydrocarbon production, MMtoe Recoverable reserves (Jan 1, 2012)

25

46

Crude oil, MMtonnes

С2 С1

Gas, bcm.

С2

1,1

С1

2,1

Key results for 2012

Plans for 2013

1Q13 2Q13 3Q13 4Q13

January February March April May June July August September October November December

Shtokman

Prirazlomnoye

• Project audit completed.

• Project appraisal under way

Offshore ice-resistant

fixed platform launch

Mar 2013

First 3 wells drilling

results

Dec 2013

Production start-up

Sep 2013

Platform completion,

pre-commissioning,

HAZOP, platform diverter

assembly

Feb 2013

1Q13 2Q13 3Q13 4Q13

January February March April May June July August September October November December

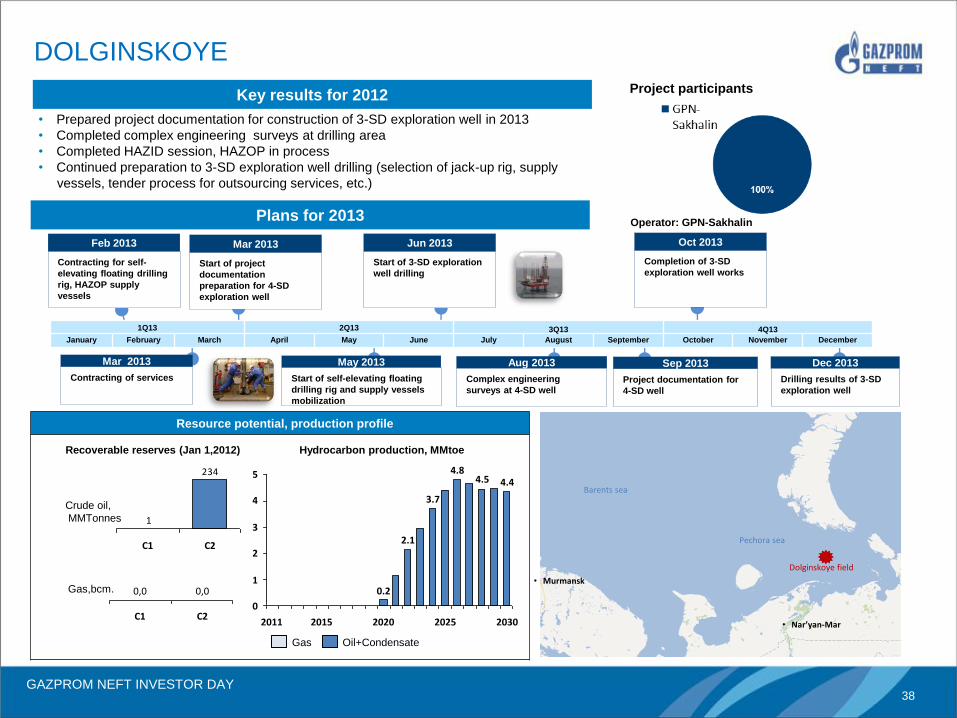

GAZPROM NEFT INVESTOR DAY 38

Resource potential, production profile

DOLGINSKOYE

4

3

2

1

0

2030

4.4 4.5 4.8

2025

3.7

2.1

2020

0.2

2015 2011

5

Oil+Condensate Gas

234

1

Crude oil,

MMTonnes

С2 С1

Gas,bcm.

С2

0,0

С1

0,0

• Nar’yan-Mar

Barents sea

Pechora sea

• Murmansk

Dolginskoye field

Key results for 2012

Plans for 2013

Project participants

Operator: GPN-Sakhalin

1Q13 2Q13 3Q13 4Q13

January February March April May June July August September October November December

• Prepared project documentation for construction of 3-SD exploration well in 2013

• Completed complex engineering surveys at drilling area

• Completed HAZID session, HAZOP in process

• Continued preparation to 3-SD exploration well drilling (selection of jack-up rig, supply

vessels, tender process for outsourcing services, etc.)

Hydrocarbon production, MMtoe Recoverable reserves (Jan 1,2012)

Contracting for self-

elevating floating drilling

rig, HAZOP supply

vessels

Feb 2013

Start of project

documentation

preparation for 4-SD

exploration well

Mar 2013

Start of 3-SD exploration

well drilling

Jun 2013

Completion of 3-SD

exploration well works

Oct 2013

Contracting of services

Mar 2013

Start of self-elevating floating

drilling rig and supply vessels

mobilization

May 2013

Complex engineering

surveys at 4-SD well

Aug 2013

Project documentation for

4-SD well

Sep 2013

Drilling results of 3-SD

exploration well

Dec 2013

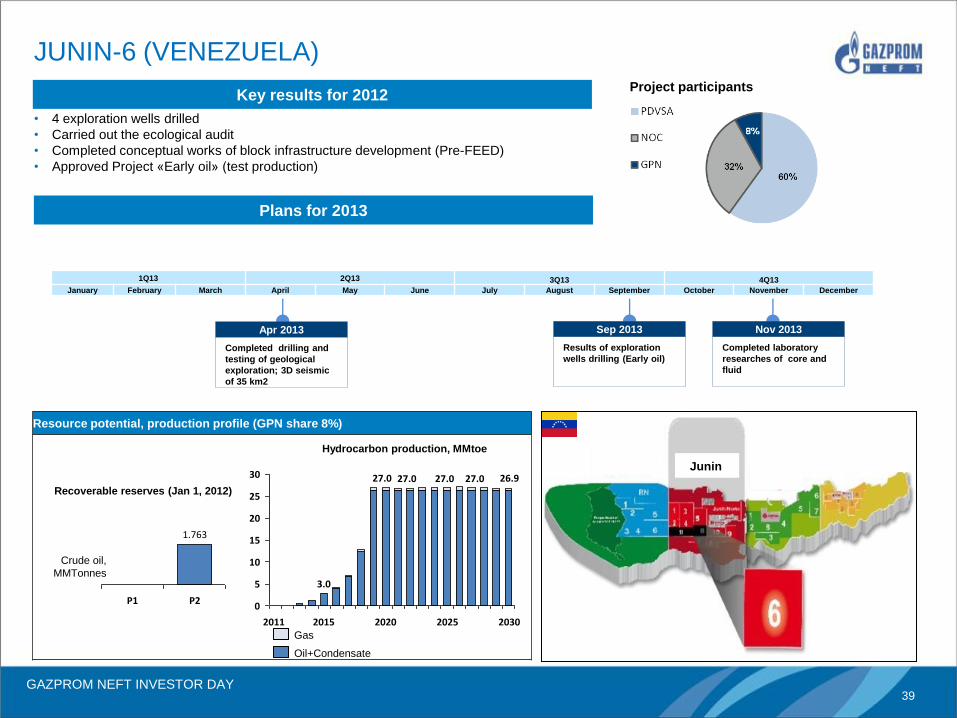

GAZPROM NEFT INVESTOR DAY 39

Resource potential, production profile (GPN share 8%)

• 4 exploration wells drilled

• Carried out the ecological audit

• Completed conceptual works of block infrastructure development (Pre-FEED)

• Approved Project «Early oil» (test production)

JUNIN-6 (VENEZUELA)

27.0

2020 2015 2025

30

25

20

15

10

5

0

2030

26.9

3.0

2011

Oil+Condensate

Gas

P1

1.763

Crude oil,

MMTonnes

P2

Key results for 2012

Plans for 2013

1Q13 2Q13 3Q13 4Q13

January February March April May June July August September October November December

Project participants

Completed drilling and

testing of geological

exploration; 3D seismic

of 35 km2

Apr 2013

Results of exploration

wells drilling (Early oil)

Sep 2013

Completed laboratory

researches of core and

fluid

Nov 2013

Recoverable reserves (Jan 1, 2012)

Hydrocarbon production, MMtoe

Junin 27.0 27.0 27.0

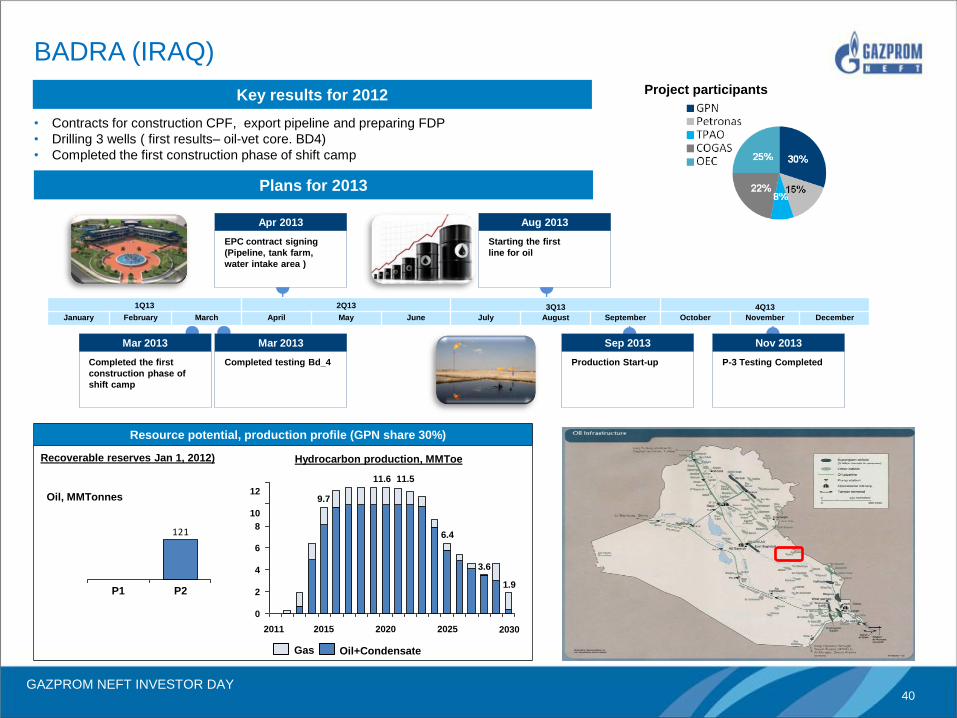

GAZPROM NEFT INVESTOR DAY 40

Resource potential, production profile (GPN share 30%)

121

• Contracts for construction CPF, export pipeline and preparing FDP

• Drilling 3 wells ( first results– oil-vet core. BD4)

• Completed the first construction phase of shift camp

BADRA (IRAQ)

4

12

8

10

6

0

2030

1.9

3.6

2025

6.4

11.5

2020

11.6

2015

9.7

2011

2

Gas Oil+Condensate

Hydrocarbon production, MMToe Recoverable reserves Jan 1, 2012)

Oil, MMTonnes

P2 P1

Key results for 2012

Plans for 2013

1Q13 2Q13 3Q13 4Q13

January February March April May June July August September October November December

P-3 Testing Completed

Nov 2013

Production Start-up

Sep 2013

Starting the first

line for oil

Aug 2013

EPC contract signing

(Pipeline, tank farm,

water intake area )

Apr 2013

Completed the first

construction phase of

shift camp

Mar 2013

Completed testing Bd_4

Mar 2013

Project participants

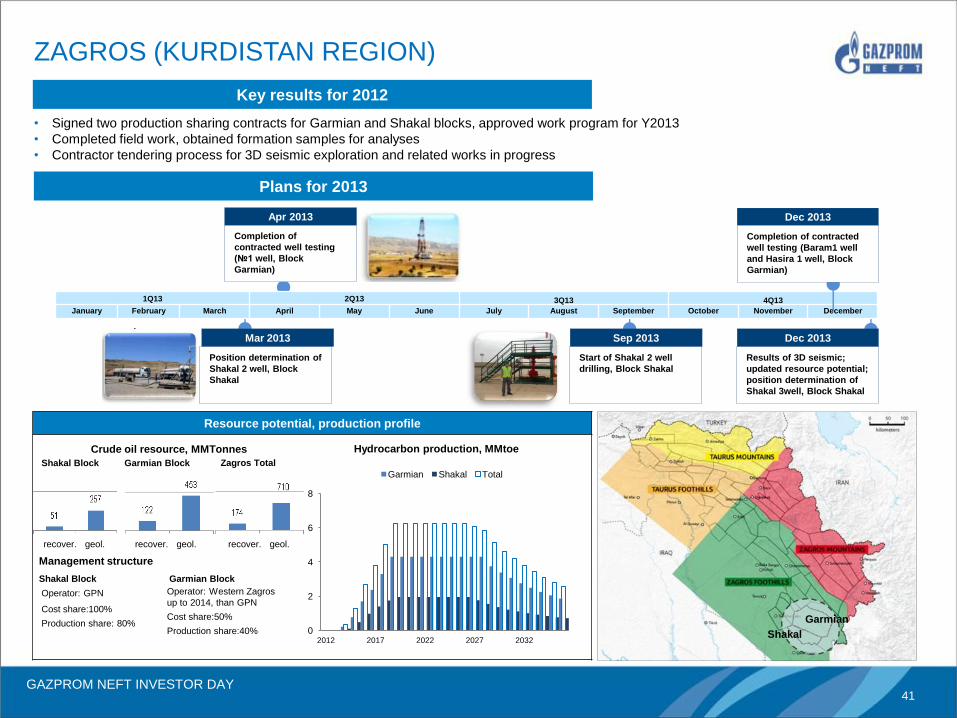

GAZPROM NEFT INVESTOR DAY 41

Position determination of

Shakal 2 well, Block

Shakal

Mar 2013

Resource potential, production profile

ZAGROS (KURDISTAN REGION)

Hydrocarbon production, MMtoe Crude oil resource, MMTonnes

1Q13 2Q13 3Q13 4Q13

January February March April May June July August September October November December

Management structure

Operator: GPN

Completion of

contracted well testing

(№1 well, Block

Garmian)

Apr 2013

23% 15%

30%

Shakal Block Garmian Block

0

2

4

6

8

2012 2017 2022 2027 2032

Garmian Shakal Total

Zagros Total

Shakal Block Garmian Block

Cost share:100%

Production share: 80% Garmian

Shakal

Key results for 2012

Completion of contracted

well testing (Baram1 well

and Hasira 1 well, Block

Garmian)

Dec 2013

Plans for 2013

Start of Shakal 2 well

drilling, Block Shakal

Sep 2013

Results of 3D seismic;

updated resource potential;

position determination of

Shakal 3well, Block Shakal

Dec 2013

Operator: Western Zagros

up to 2014, than GPN

Cost share:50%

Production share:40%

recover. geol. recover. geol. recover. geol.

• Signed two production sharing contracts for Garmian and Shakal blocks, approved work program for Y2013

• Completed field work, obtained formation samples for analyses

• Contractor tendering process for 3D seismic exploration and related works in progress

GAZPROM NEFT INVESTOR DAY 42

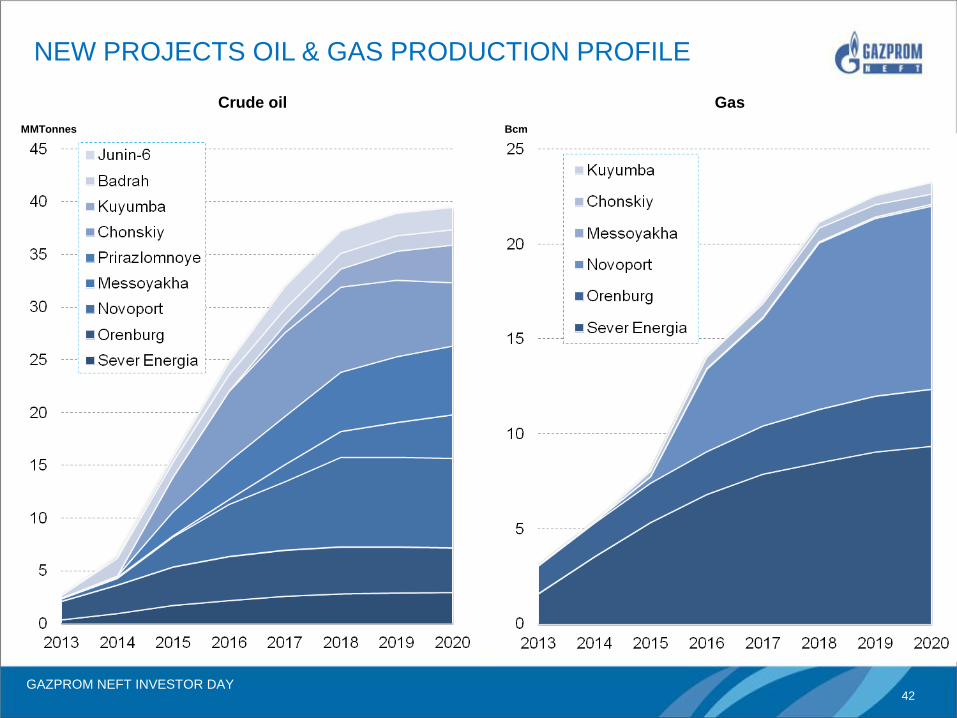

NEW PROJECTS OIL & GAS PRODUCTION PROFILE

MMTonnes Bcm

Crude oil Gas

GAZPROM NEFT INVESTOR DAY 43

Downstream

Anatoly Cherner

GAZPROM NEFT INVESTOR DAY 44

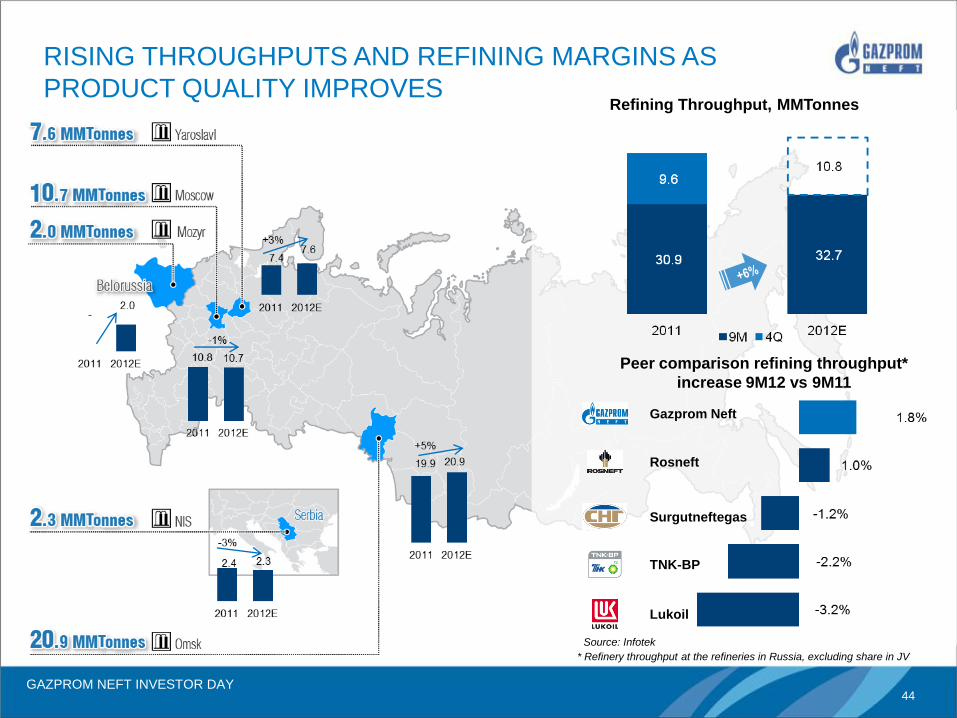

* Refinery throughput at the refineries in Russia, excluding share in JV

Peer comparison refining throughput*

increase 9M12 vs 9M11

Gazprom Neft

Rosneft

Surgutneftegas

TNK-BP

Lukoil

Source: Infotek

RISING THROUGHPUTS AND REFINING MARGINS AS

PRODUCT QUALITY IMPROVES Refining Throughput, MMTonnes

GAZPROM NEFT INVESTOR DAY 45

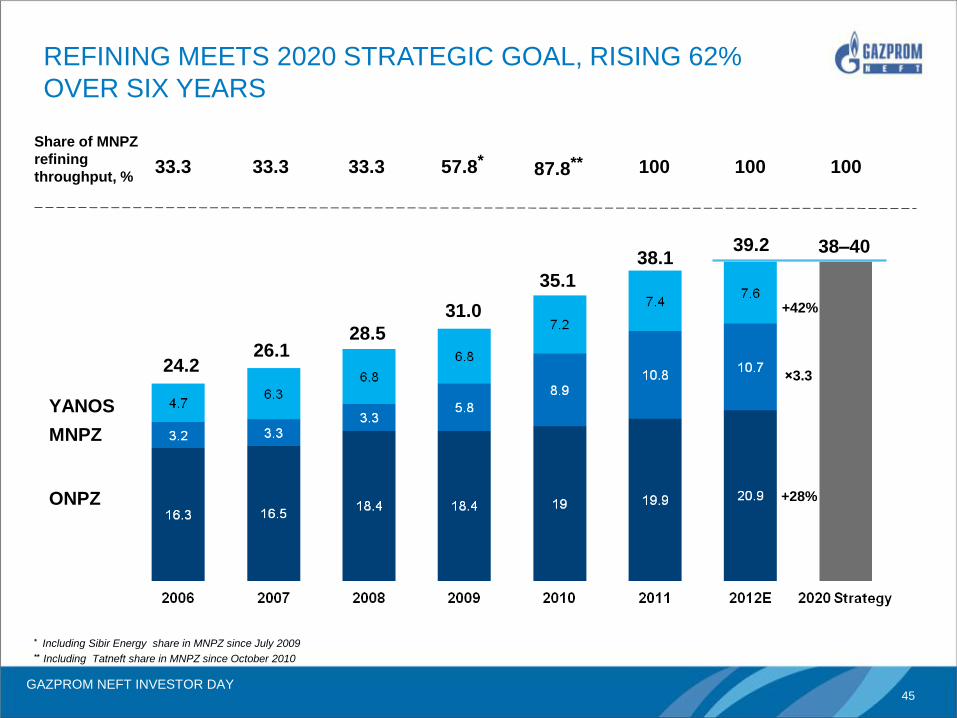

REFINING MEETS 2020 STRATEGIC GOAL, RISING 62%

OVER SIX YEARS

YANOS

MNPZ

ONPZ

Share of MNPZ

refining

throughput, % 33.3 33.3 33.3 57.8*

87.8** 100 100 100

24.2 26.1

28.5

31.0

35.1

38.1 39.2 38–40

+42%

×3.3

+28%

* Including Sibir Energy share in MNPZ since July 2009 ** Including Tatneft share in MNPZ since October 2010

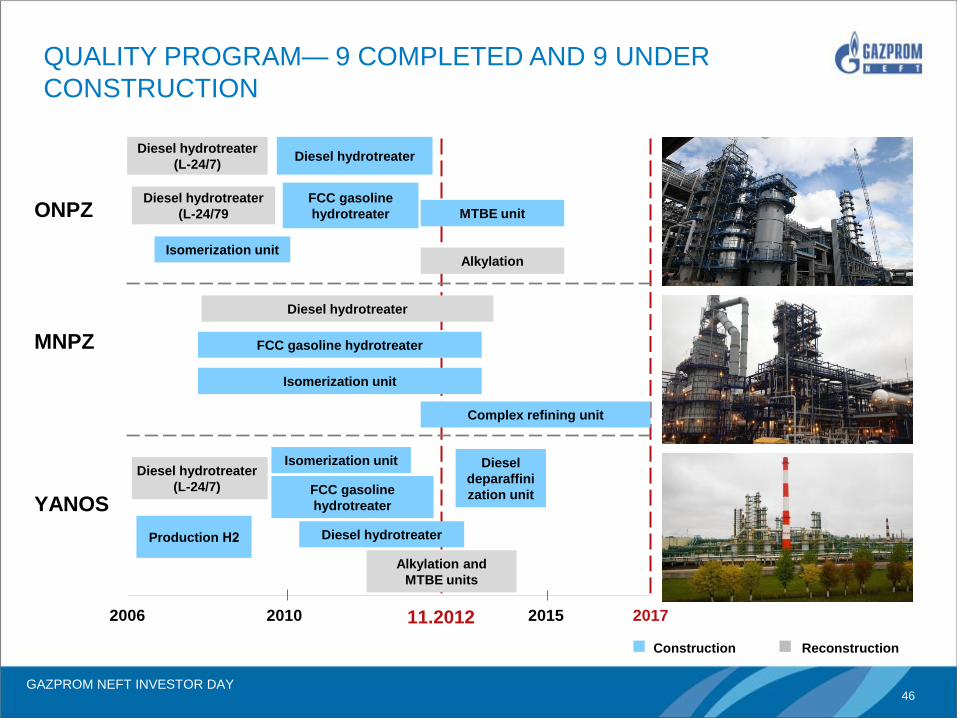

GAZPROM NEFT INVESTOR DAY 46

MNPZ

YANOS

ONPZ

2006 2017 2010 11.2012 2015

Diesel hydrotreater

(L-24/7)

Diesel hydrotreater

(L-24/79

Isomerization unit

Diesel hydrotreater

FCC gasoline hydrotreater

Isomerization unit

Complex refining unit

FCC gasoline

hydrotreater

Diesel hydrotreater

FCC gasoline

hydrotreater MTBE unit

Production Н2 Diesel hydrotreater

Alkylation and

MTBE units

Isomerization unit Diesel hydrotreater

(L-24/7)

Diesel

deparaffini

zation unit

Alkylation

QUALITY PROGRAM— 9 COMPLETED AND 9 UNDER

CONSTRUCTION

Construction Reconstruction

GAZPROM NEFT INVESTOR DAY 47

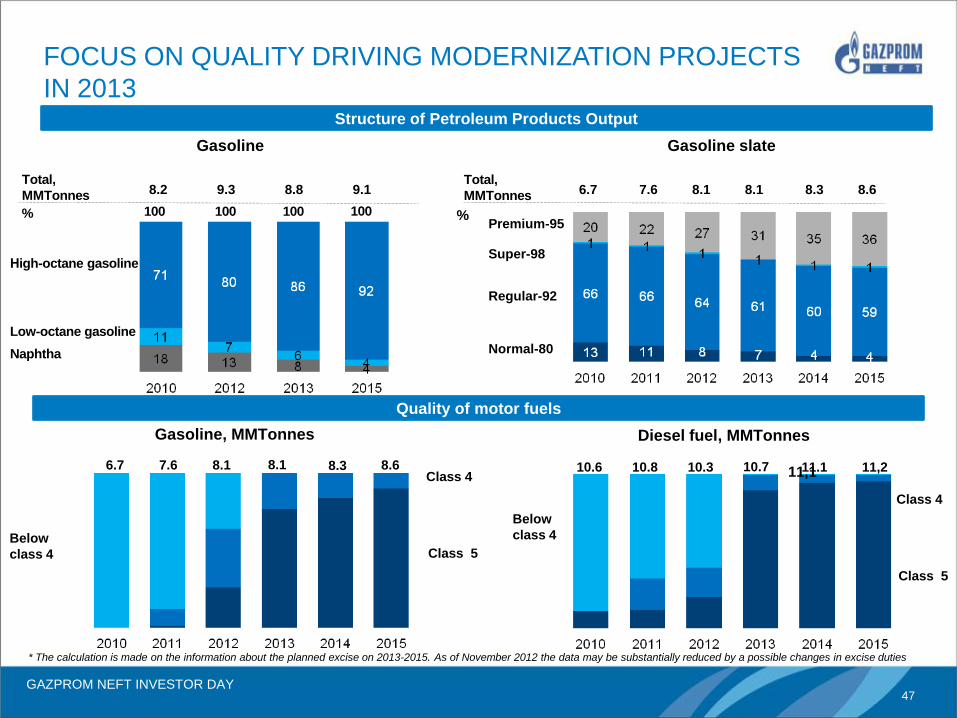

Structure of Petroleum Products Output

Super-98

Gasoline, MMTonnes

8.6 7.6 8.1 8.1 6.7 8.3 11,2 10.8 10.3 10.7 10.6 11,1

Diesel fuel, MMTonnes

Regular-92

Premium-95

Normal-80

8.3 7.6 8.1 8.1 6.7 8.6

Gasoline slate Gasoline

Class 5

Class 4

Below

class 4

* The calculation is made on the information about the planned excise on 2013-2015. As of November 2012 the data may be substantially reduced by a possible changes in excise duties

Total,

MMTonnes

% %

Нigh-octane gasoline

Low-octane gasoline

Naphtha

100 100 100 100

9.3 8.8 9.1 8.2 Total,

MMTonnes

Below

class 4 Class 5

Class 4 11.1

FOCUS ON QUALITY DRIVING MODERNIZATION PROJECTS

IN 2013

Quality of motor fuels

GAZPROM NEFT INVESTOR DAY 48

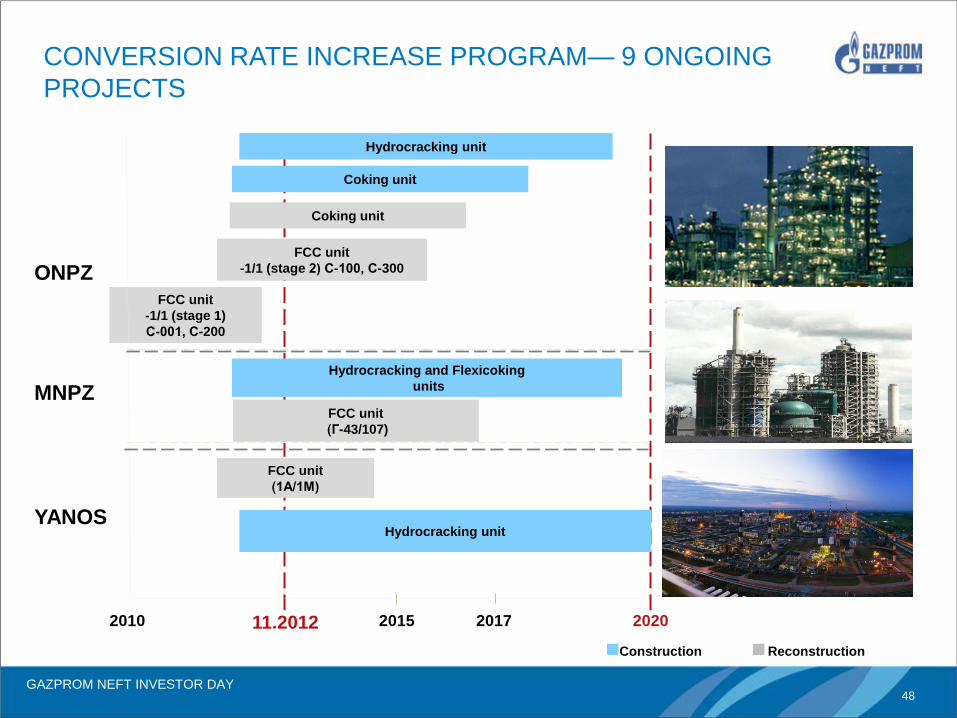

MNPZ

YANOS

ONPZ

Hydrocracking unit

Coking unit

Coking unit

FCC unit

-1/1 (stage 1)

С-001, С-200

FCC unit

-1/1 (stage 2) С-100, С-300

Hydrocracking and Flexicoking

units

FCC unit

(Г-43/107)

FCC unit

(1А/1М)

Hydrocracking unit

2010 2020 11.2012 2015 2017

Construction Reconstruction

CONVERSION RATE INCREASE PROGRAM— 9 ONGOING

PROJECTS

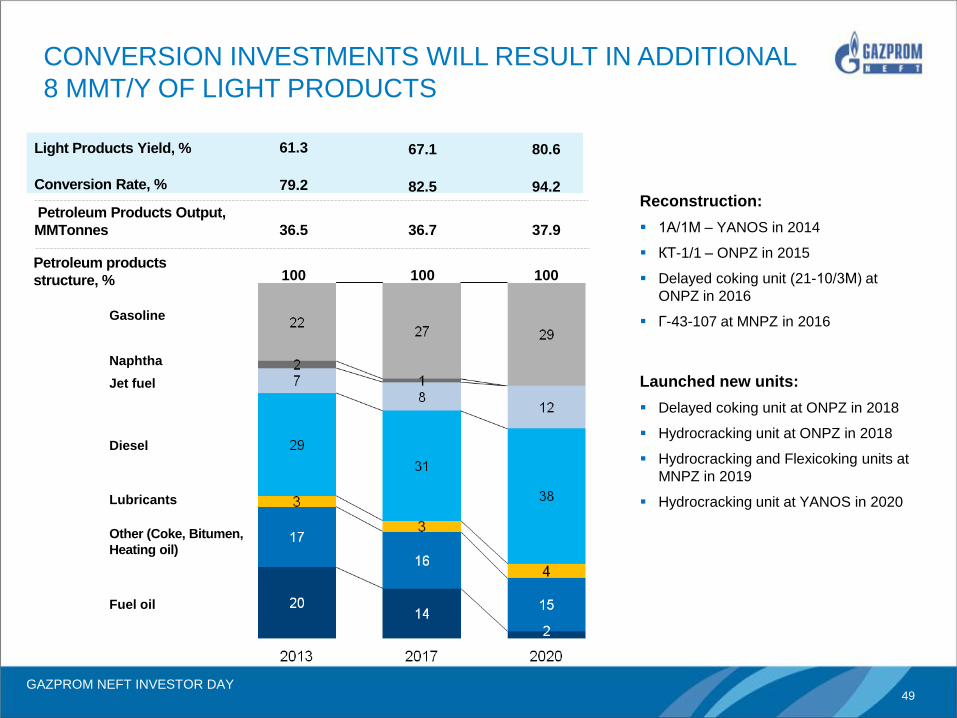

GAZPROM NEFT INVESTOR DAY 49

CONVERSION INVESTMENTS WILL RESULT IN ADDITIONAL

8 MMT/Y OF LIGHT PRODUCTS

Diesel

Lubricants

Other (Coke, Bitumen,

Heating oil)

Light Products Yield, %

Conversion Rate, %

Fuel oil

Naphtha

Gasoline

Jet fuel

Reconstruction:

1А/1М – YANOS in 2014

КТ-1/1 – ONPZ in 2015

Delayed coking unit (21-10/3М) at

ONPZ in 2016

Г-43-107 at MNPZ in 2016

Launched new units:

Delayed coking unit at ONPZ in 2018

Hydrocracking unit at ONPZ in 2018

Hydrocracking and Flexicoking units at

MNPZ in 2019

Hydrocracking unit at YANOS in 2020

Petroleum Products Output,

MMTonnes

79.2 82.5 94.2

36.5 36.7 37.9

61.3 67.1 80.6

100 100 100 Petroleum products

structure, %

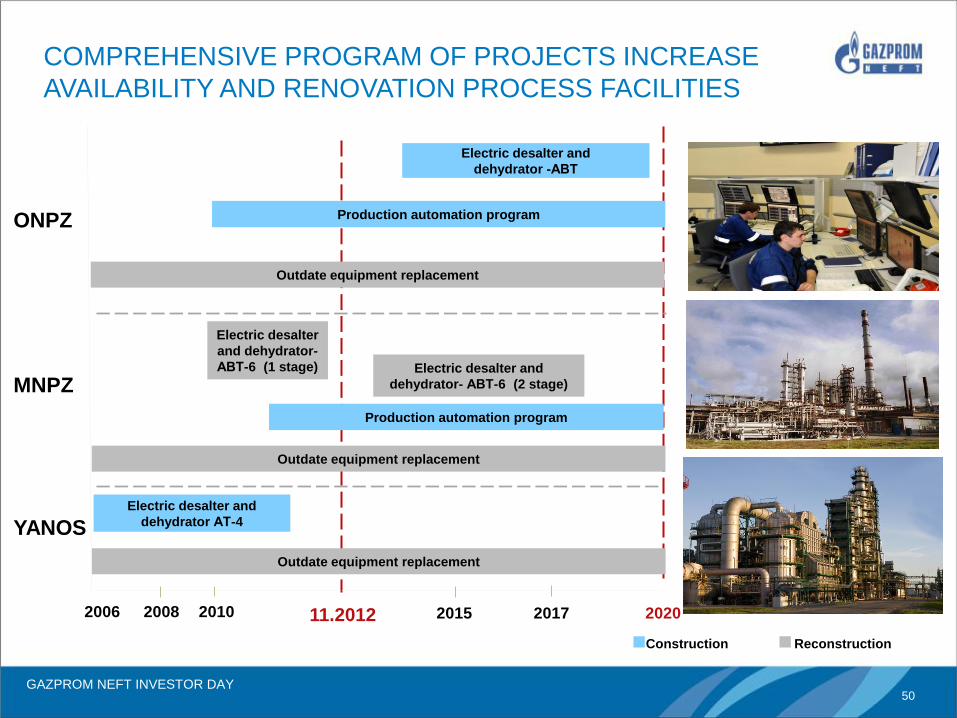

GAZPROM NEFT INVESTOR DAY 50

MNPZ

YANOS

ONPZ

Electric desalter and

dehydrator -АВТ

Production automation program

Outdate equipment replacement

Electric desalter

and dehydrator-

АВТ-6 (1 stage)

Electric desalter and

dehydrator АТ-4

2006 2020 11.2012 2015 2017

Electric desalter and

dehydrator- АВТ-6 (2 stage)

Production automation program

2008 2010

Outdate equipment replacement

Outdate equipment replacement

Construction Reconstruction

COMPREHENSIVE PROGRAM OF PROJECTS INCREASE

AVAILABILITY AND RENOVATION PROCESS FACILITIES

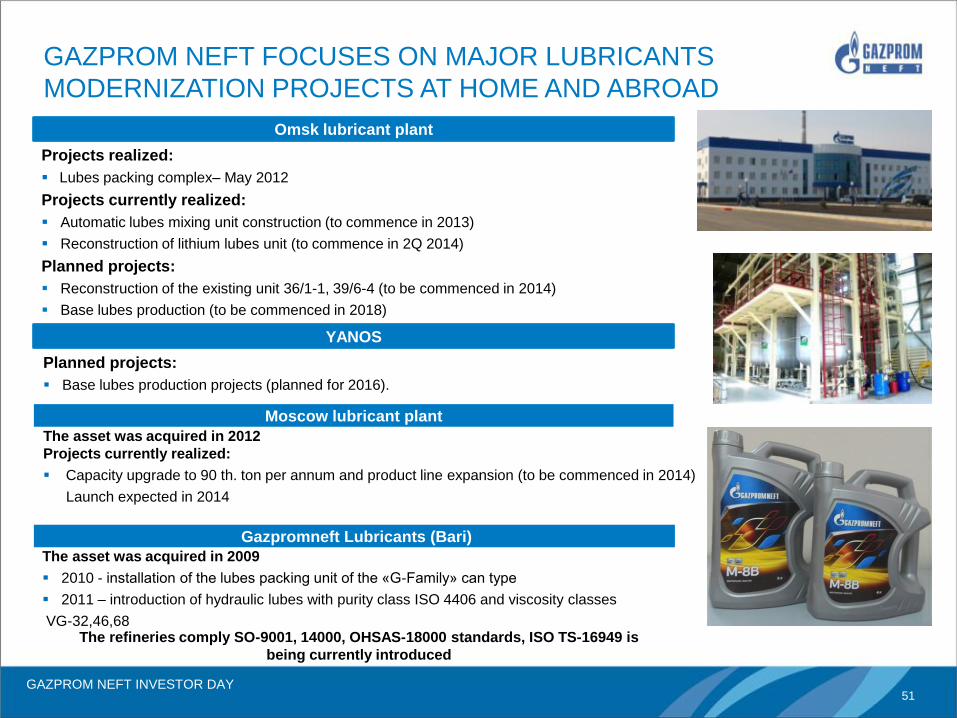

GAZPROM NEFT INVESTOR DAY 51

Omsk lubricant plant

YANOS

Moscow lubricant plant

Projects realized:

Lubes packing complex– May 2012

Projects currently realized:

Automatic lubes mixing unit construction (to commence in 2013)

Reconstruction of lithium lubes unit (to commence in 2Q 2014)

Planned projects:

Reconstruction of the existing unit 36/1-1, 39/6-4 (to be commenced in 2014)

Base lubes production (to be commenced in 2018)

The asset was acquired in 2012

Projects currently realized:

Capacity upgrade to 90 th. ton per annum and product line expansion (to be commenced in 2014)

Launch expected in 2014

Planned projects:

Base lubes production projects (planned for 2016).

Gazpromneft Lubricants (Bari)

The asset was acquired in 2009

2010 - installation of the lubes packing unit of the «G-Family» can type

2011 – introduction of hydraulic lubes with purity class ISO 4406 and viscosity classes

VG-32,46,68 The refineries comply SO-9001, 14000, OHSAS-18000 standards, ISO TS-16949 is

being currently introduced

GAZPROM NEFT FOCUSES ON MAJOR LUBRICANTS

MODERNIZATION PROJECTS AT HOME AND ABROAD

GAZPROM NEFT INVESTOR DAY 52

2009–2012: 19 new items added to the product line

Ordinary +10 Innovative +9

Road asphalt +8 BPP +6

Bitumen +2 BE +3

Total sales of bitumen, MTonnes

784 906

1,415

Key projects to improve bitumen technology

PBB and BE

15

47*

2

71 22

Main results

1,882

42

125

* - decline vs. 2012 due to reconstruction.

1,624

THE MAIN GOAL OF BITUMEN MODERNIZATION –

INCREASED PRODUCTION OF INNOVATIVE MATERIALS

packed filling Omsk refinery:

Commenced:

Plant for the production of polymer-

bitumen binders (PBB) and bituminous

emulsions (BE)

System for loading of raw materials

for the production of road asphalt

Bagging line for road and construction

bitumen

Work in progress and planed:

Reconstruction of the bitumen unit

Construction of asphalt loading racks

Moscow refinery:

Commenced:

Reconstruction of the bitumen unit

Work in progress and planed:

PBB and BE unit

Bitumen loading system

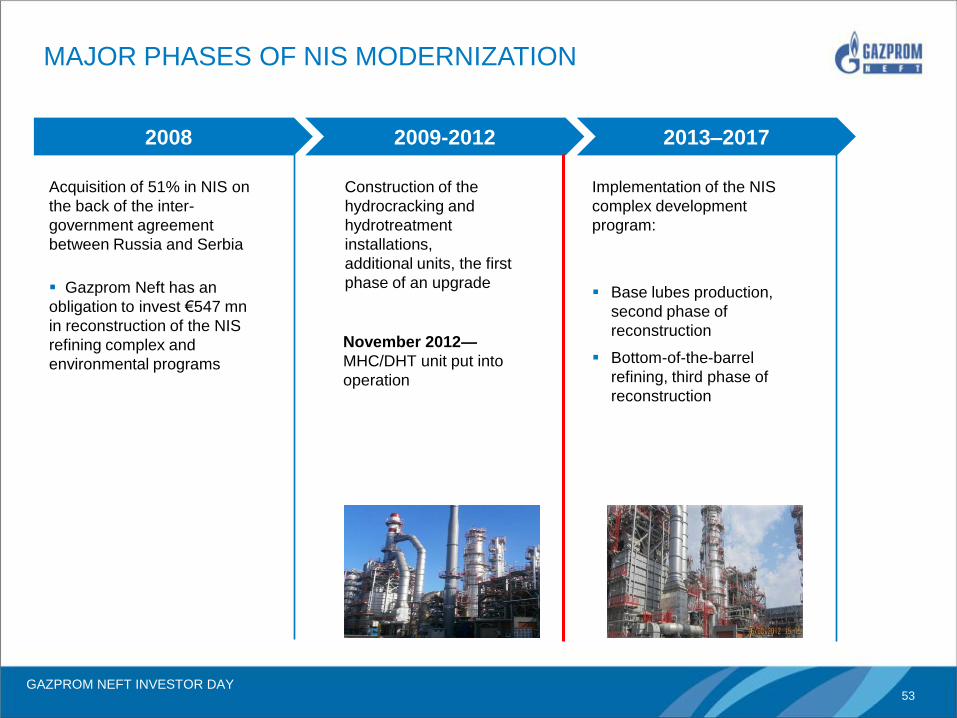

GAZPROM NEFT INVESTOR DAY 53

2008 2009-2012 2013–2017

Acquisition of 51% in NIS on

the back of the inter-

government agreement

between Russia and Serbia

Gazprom Neft has an

obligation to invest €547 mn

in reconstruction of the NIS

refining complex and

environmental programs

Construction of the

hydrocracking and

hydrotreatment

installations,

additional units, the first

phase of an upgrade

November 2012—

MHC/DHT unit put into

operation

Implementation of the NIS

complex development

program:

Base lubes production,

second phase of

reconstruction

Bottom-of-the-barrel

refining, third phase of

reconstruction

MAJOR PHASES OF NIS MODERNIZATION

GAZPROM NEFT INVESTOR DAY 54

Financial Outlook

Alexey Yankevich

GAZPROM NEFT INVESTOR DAY 55

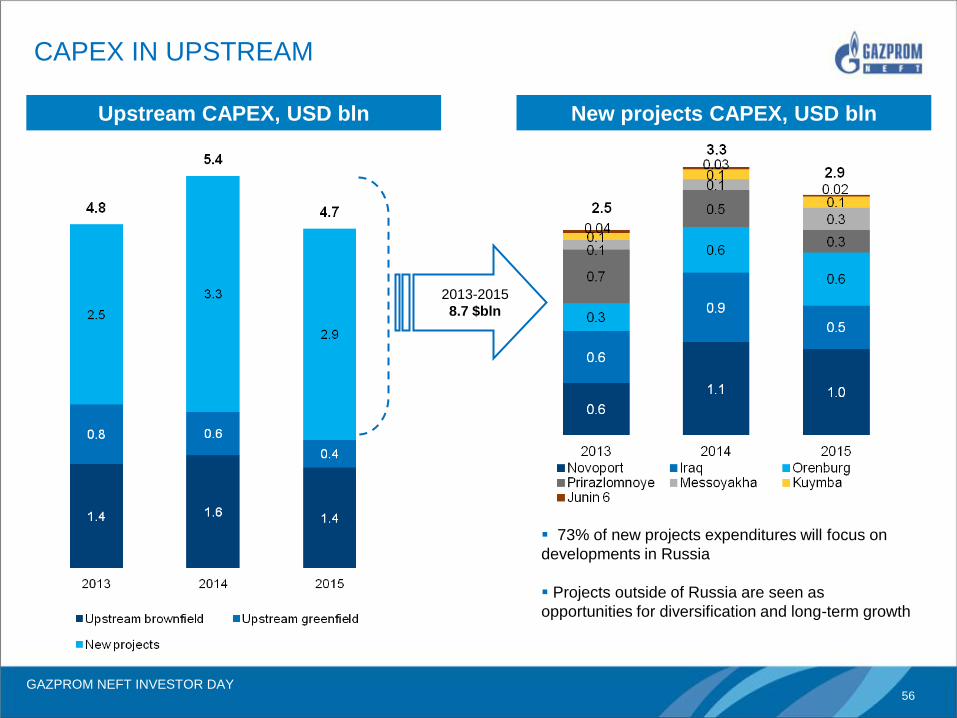

2013-2015

CAPEX outlook 2013-2015, USD bln

Upstream

brownfield

Upstream

greenfield*

Refining

Marketing and

distribution

Other

Badrah Novoport

Messoyakha Orenburg

Omsk Moscow Moscow

Junin 6

Retail Avia Bunkering Lubricants

Kuymba

CAPEX AND INVESTMENTS SUPPORT STRATEGIC GOALS

*Including investments in JV projects

Noyabrsk Vostok Zapolyarneft

44% of three-year cycle capex will be spent on

new upstream projects

21% will be invested in refinery upgrade

Remaining investment will focus on expanding

marketing segment and business improvement

projects

GAZPROM NEFT INVESTOR DAY 56

New projects CAPEX, USD bln Upstream CAPEX, USD bln

2013-2015

8.7 $bln

CAPEX IN UPSTREAM

73% of new projects expenditures will focus on

developments in Russia

Projects outside of Russia are seen as

opportunities for diversification and long-term growth

GAZPROM NEFT INVESTOR DAY 57

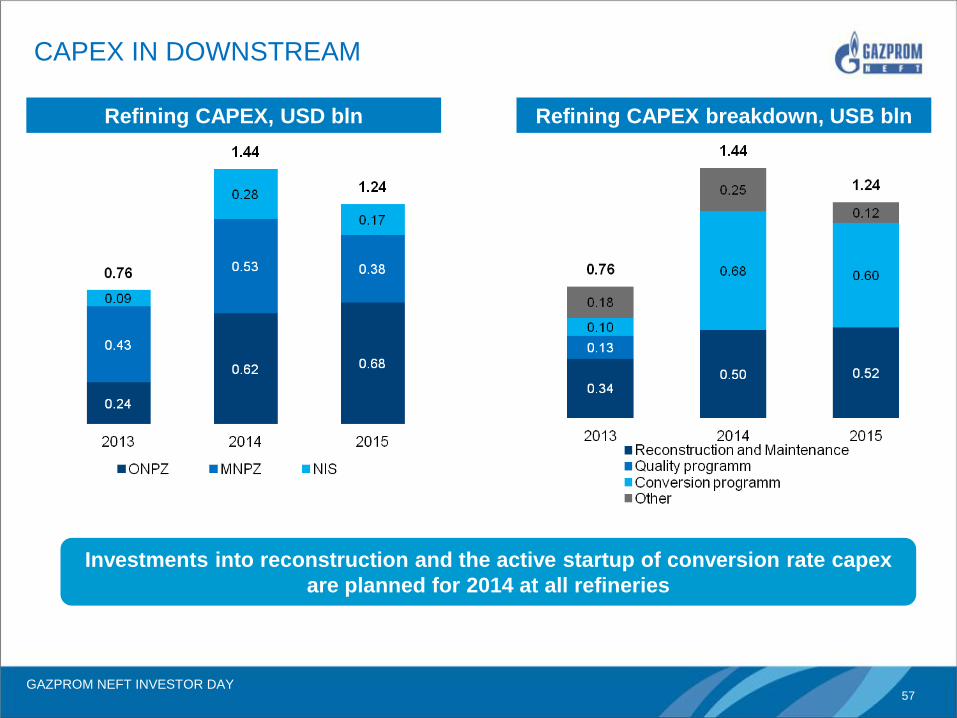

Refining CAPEX breakdown, USB bln Refining CAPEX, USD bln

CAPEX IN DOWNSTREAM

Investments into reconstruction and the active startup of conversion rate capex

are planned for 2014 at all refineries

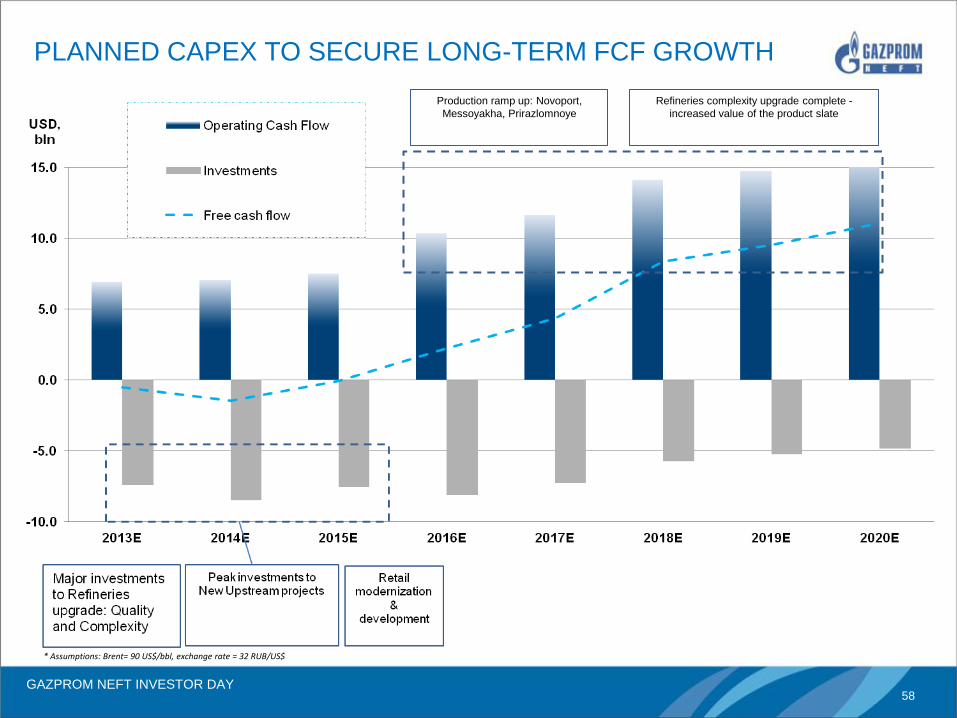

GAZPROM NEFT INVESTOR DAY 58

Production ramp up: Novoport,

Messoyakha, Prirazlomnoye

Refineries complexity upgrade complete -

increased value of the product slate

* Assumptions: Brent= 90 US$/bbl, exchange rate = 32 RUB/US$

PLANNED CAPEX TO SECURE LONG-TERM FCF GROWTH

GAZPROM NEFT INVESTOR DAY 59

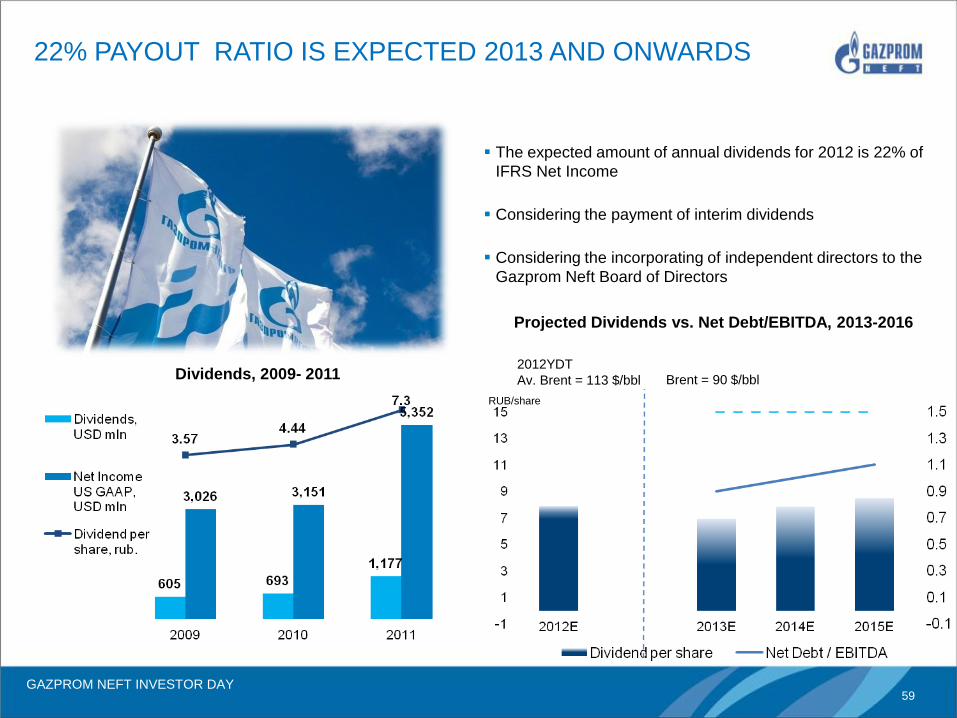

22% PAYOUT RATIO IS EXPECTED 2013 AND ONWARDS

Dividends, 2009- 2011

The expected amount of annual dividends for 2012 is 22% of

IFRS Net Income

Considering the payment of interim dividends

Considering the incorporating of independent directors to the

Gazprom Neft Board of Directors

2012YDT

Av. Brent = 113 $/bbl Brent = 90 $/bbl

RUB/share

Projected Dividends vs. Net Debt/EBITDA, 2013-2016

GAZPROM NEFT INVESTOR DAY 60

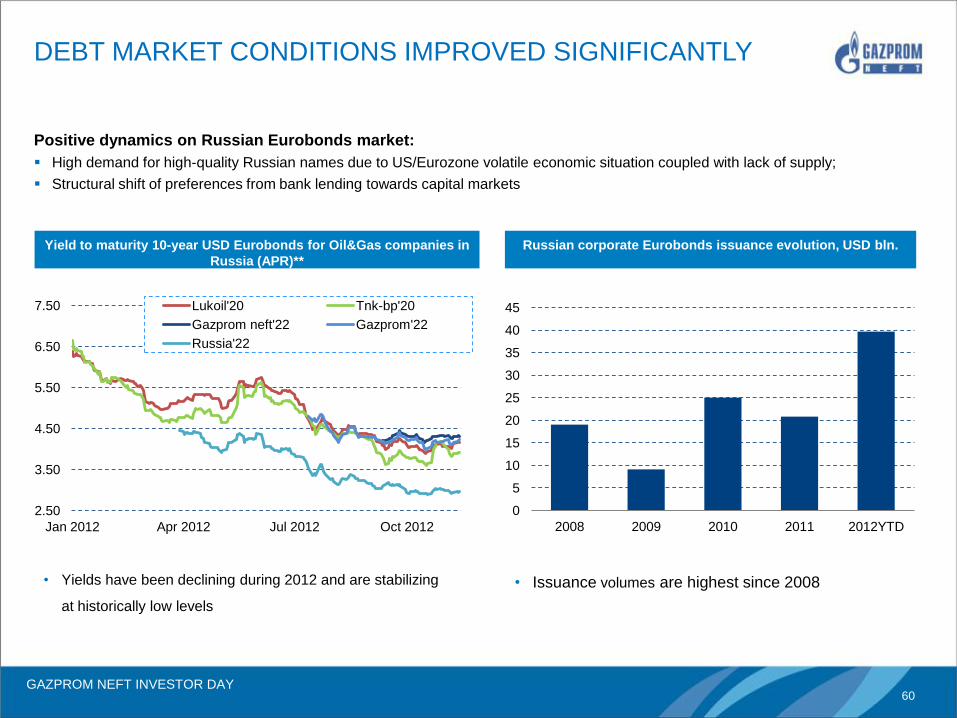

DEBT MARKET CONDITIONS IMPROVED SIGNIFICANTLY

Positive dynamics on Russian Eurobonds market:

High demand for high-quality Russian names due to US/Eurozone volatile economic situation coupled with lack of supply;

Structural shift of preferences from bank lending towards capital markets

Yield to maturity 10-year USD Eurobonds for Oil&Gas companies in

Russia (APR)**

2.50

3.50

4.50

5.50

6.50

7.50

Jan 2012 Apr 2012 Jul 2012 Oct 2012

Lukoil'20 Tnk-bp'20

Gazprom neft'22 Gazprom'22

Russia'22

Russian corporate Eurobonds issuance evolution, USD bln.

0

5

10

15

20

25

30

35

40

45

2008 2009 2010 2011 2012YTD

• Yields have been declining during 2012 and are stabilizing

at historically low levels

• Issuance volumes are highest since 2008

GAZPROM NEFT INVESTOR DAY 61

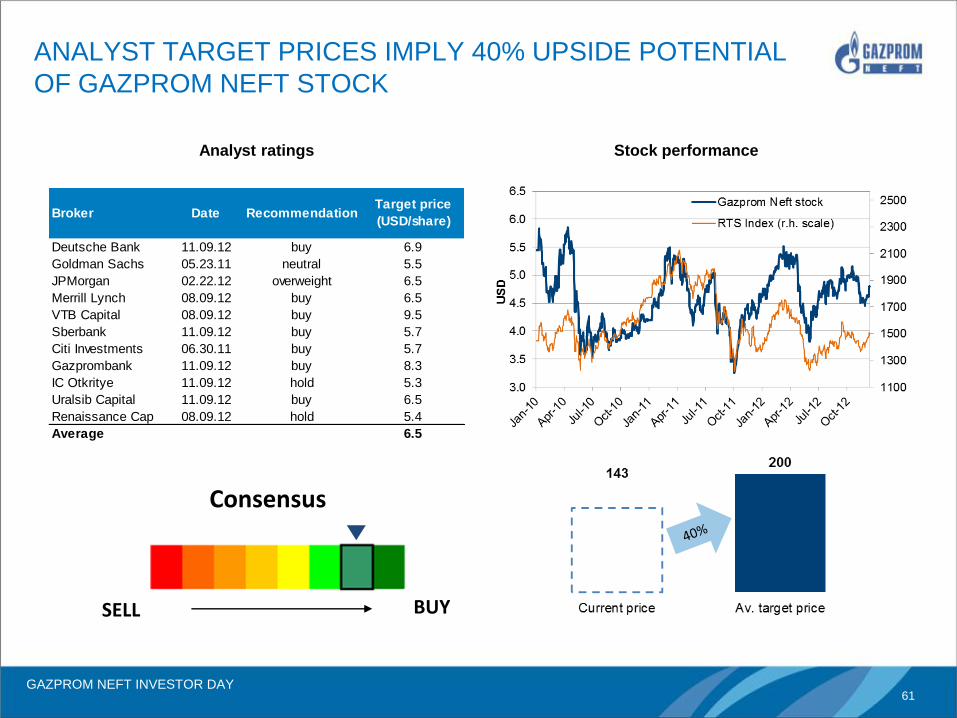

ANALYST TARGET PRICES IMPLY 40% UPSIDE POTENTIAL

OF GAZPROM NEFT STOCK

Consensus

SELL BUY

Analyst ratings Stock performance

Deutsche Bank 11.09.12 buy 6.9

Goldman Sachs 05.23.11 neutral 5.5

JPMorgan 02.22.12 overweight 6.5

Merrill Lynch 08.09.12 buy 6.5

VTB Capital 08.09.12 buy 9.5

Sberbank 11.09.12 buy 5.7

Citi Investments 06.30.11 buy 5.7

Gazprombank 11.09.12 buy 8.3

IC Otkritye 11.09.12 hold 5.3

Uralsib Capital 11.09.12 buy 6.5

Renaissance Cap 08.09.12 hold 5.4

Average 6.5

Broker Date RecommendationTarget price

(USD/share)

GAZPROM NEFT INVESTOR DAY 62

THANK YOU!

QUESTIONS&ANSWERS

GAZPROM NEFT INVESTOR DAY 63

APPENDIX

GAZPROM NEFT INVESTOR DAY 64

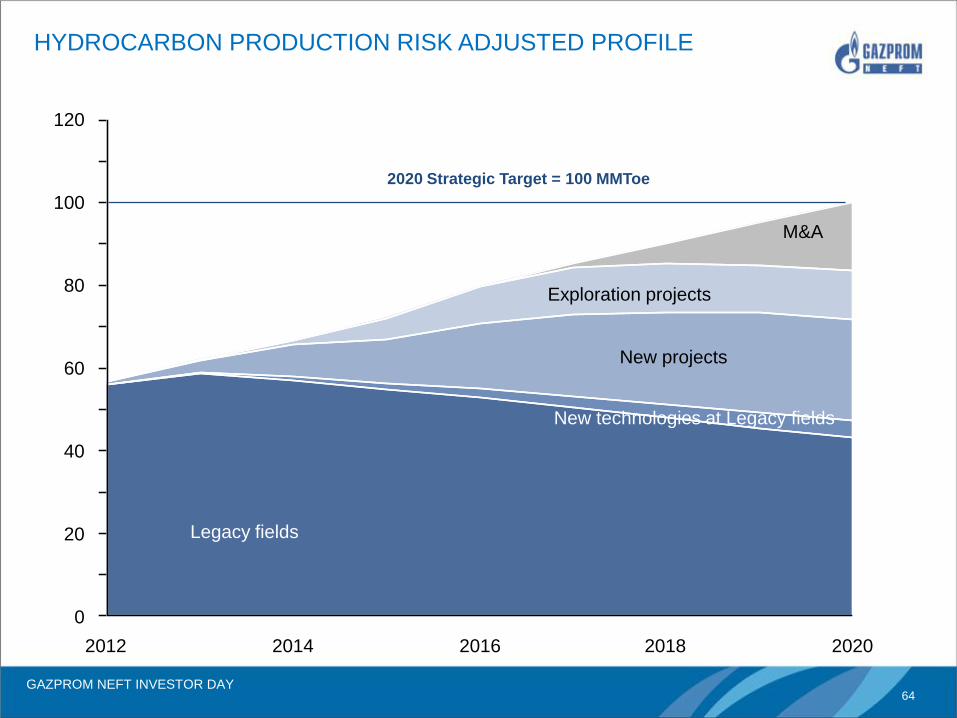

HYDROCARBON PRODUCTION RISK ADJUSTED PROFILE

0

20

120

100

80

60

40

2012 2018 2020 2014 2016

Exploration projects

New projects

New technologies at Legacy fields

M&A

Legacy fields

2020 Strategic Target = 100 MMToe