Embed Size (px)

Citation preview

GASB 65: Items Previously Reported

Presented by:

GASB 65: Items Previously Reported as Assets and Liabilities

Presented by: Heather Acker, CPA, PartnerJodi Dobson, CPA, Senior Manager

February 27, 2013

© Baker Tilly Virchow Krause, LLPBaker Tilly refers to Baker Tilly Virchow Krause, LLP,

an independently owned and managed member of Baker Tilly International.

1

WebEx guide

> Everyone is muted to avoid background noise. Please use the chat box if you need to Chat Windowcommunicate with the host.

> Asking questions: In the chat screen, ask questions by choosing “All Panelists” in lower right chat window. Type your message in

Chat Window

the chat box and hit “send.”

> If disconnected: Refer to your e-mail and reconnect. If audio is disconnected ,click the Communicate tab in the upper left ppto find the dial in numbers and access code or refer back to your e-mail for the dial-in #.

> Support #: If you have any technical problems, call WebEx Chat Boxp ,Support at 866 229 3239.

> We will be recording today.

2

Choose “All Panelists”Refresh button

CPE credit

This webinar qualifies for one hour of ContinuingProfessional Education (CPE)Professional Education (CPE).

To qualify for the CPE credit, you must be in attendance for the entireq y , ywebinar, answer the polling questions, and complete the evaluation form atthe end of the webinar.

Qualified attendees will receive a CPE certificate.

Q ti di th CPE f thi bi b t tQuestions regarding the CPE for this webinar can be sent to [email protected] Tilly Virchow Krause, LLP is not registered with NASBA’s National Registry of CPE Sponsors as a provider of CPE. CPE credits should not be claimed for this program in states where the licensing authorityprovider of CPE. CPE credits should not be claimed for this program in states where the licensing authority requires all CPE credits claimed to be provided by CPE providers registered with the National Registry of CPE Sponsors.

3

Presenters

Heather Acker, CPAPartner,

State and Local Government

Jodi Dobson, CPASenior Manager,

Energy and Utilities

44

Goals for this session

>Di th b k d f thi t d d>Discuss the background of this standard

>Understand the definitions of the new elements of the financial statementsthe financial statements

>Identify classification of assets, deferred outflows, liabilities, and deferred inflowsliabilities, and deferred inflows

>Highlight changes in accounting treatment for certain items

5

Effective Date

GASB 65: Items Previously Recognized as Assets and Li bilitiLiabilities

Effective for period beginning after December 15, 2012 (fiscal years ending on or after 12/31/13)

Restatement may be necessary, if material.

6

Background

GASB Concepts Statement No. 4 and created a fi i l ti d l hfinancial reporting model where:

A tAssets+ Deferred outflows of resources- Liabilities- Deferred inflows of resourcesDeferred inflows of resources= Net position

7

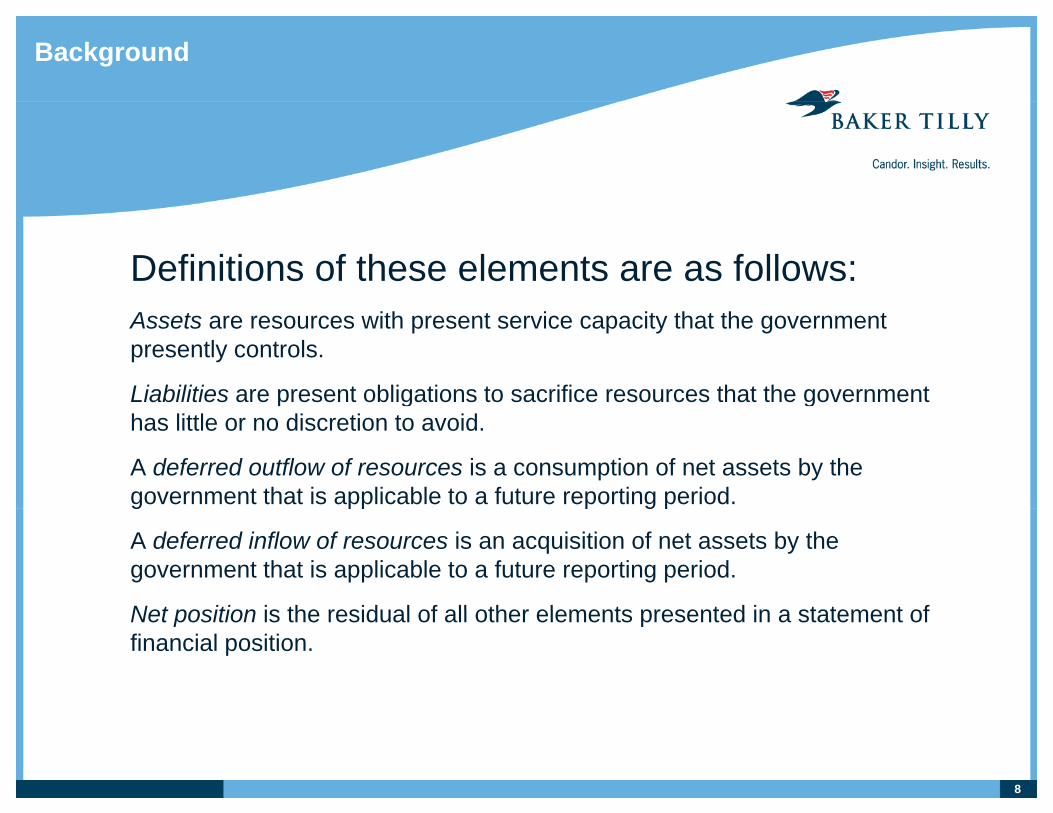

Background

Definitions of these elements are as follows:Assets are resources with present service capacity that the government presently controls.

Liabilities are present obligations to sacrifice resources that the government g ghas little or no discretion to avoid.

A deferred outflow of resources is a consumption of net assets by the government that is applicable to a future reporting period.g pp p g p

A deferred inflow of resources is an acquisition of net assets by the government that is applicable to a future reporting period.

Net position is the residual of all other elements presented in a statement ofNet position is the residual of all other elements presented in a statement of financial position.

8

Background

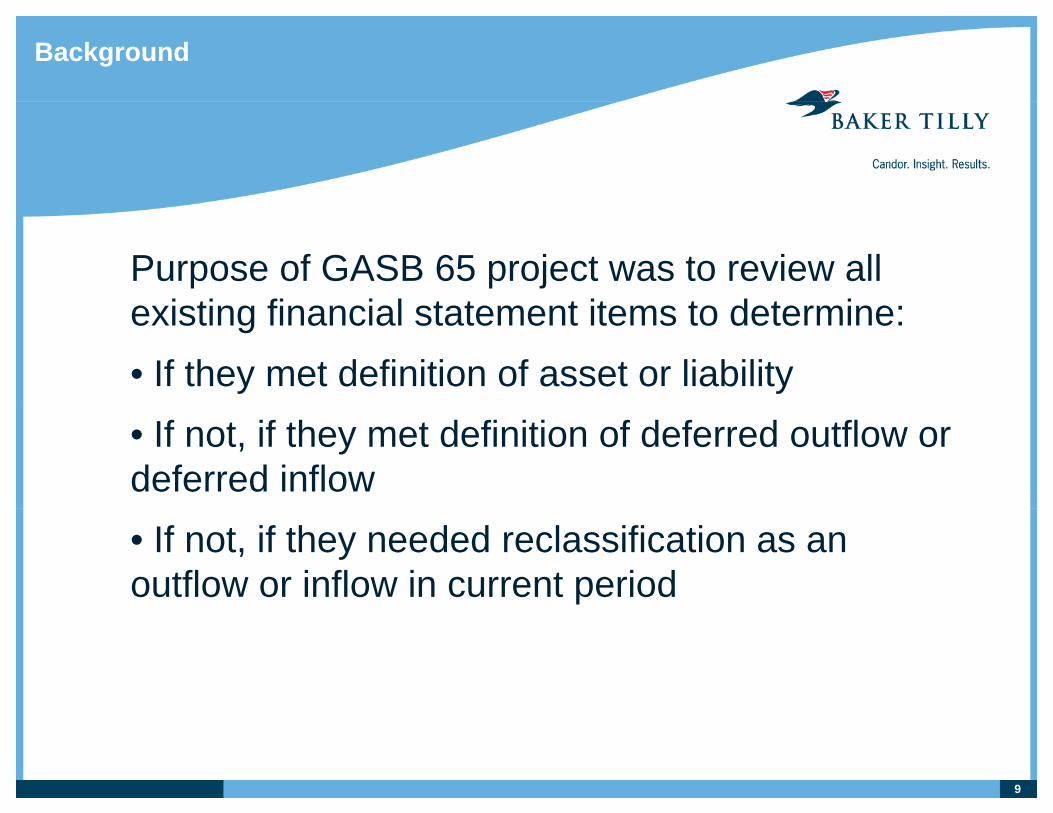

Purpose of GASB 65 project was to review all i ti fi i l t t t it t d t iexisting financial statement items to determine:

• If they met definition of asset or liability• If not, if they met definition of deferred outflow or deferred inflow• If not, if they needed reclassification as an outflow or inflow in current period

9

Polling question #1

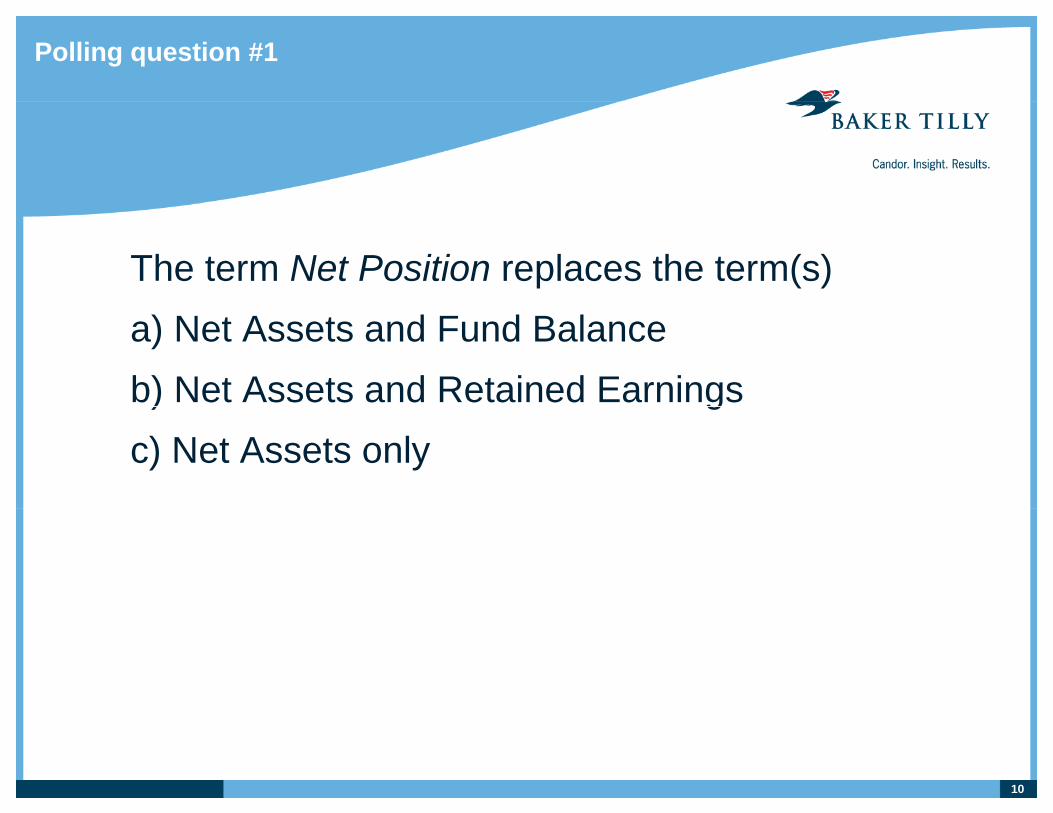

The term Net Position replaces the term(s)a) Net Assets and Fund Balanceb) Net Assets and Retained Earnings) gc) Net Assets only

10

Assets

Items that retain the classification as an asset i l dinclude:• Prepaid items

• Grants paid to another government in advance of meeting eligibility requirements (other than time).

P h f f t f th t• Purchase of future revenues from another government (GASB 48)

• Regulatory assets resulting from regulatory operations• Regulatory assets resulting from regulatory operations under GASB 62

• Pension assetsPension assets

11

Deferred Outflows

Items previously classified as assets (or contra li biliti ) th t ill b l ifi d d f dliabilities) that will be reclassified as deferred outflows include:• Deferred amounts on debt refundings

• Grants paid to other governments in advance of meeting time requirementstime requirements.

• Payments to acquire rights to future intra-entity revenues (GASB 48)(GASB 48)

• Loss from a sale of property that is subsequently leased back

12

Liabilities

Items that retain the classification as a liability i l dinclude:• Regulatory credits which result in refunds in future periods (GASB 62)periods (GASB 62)

• Grants received before eligibility requirements (excluding time) are mettime) are met

• Resources received in advance of an exchange transaction

13

Deferred Inflows

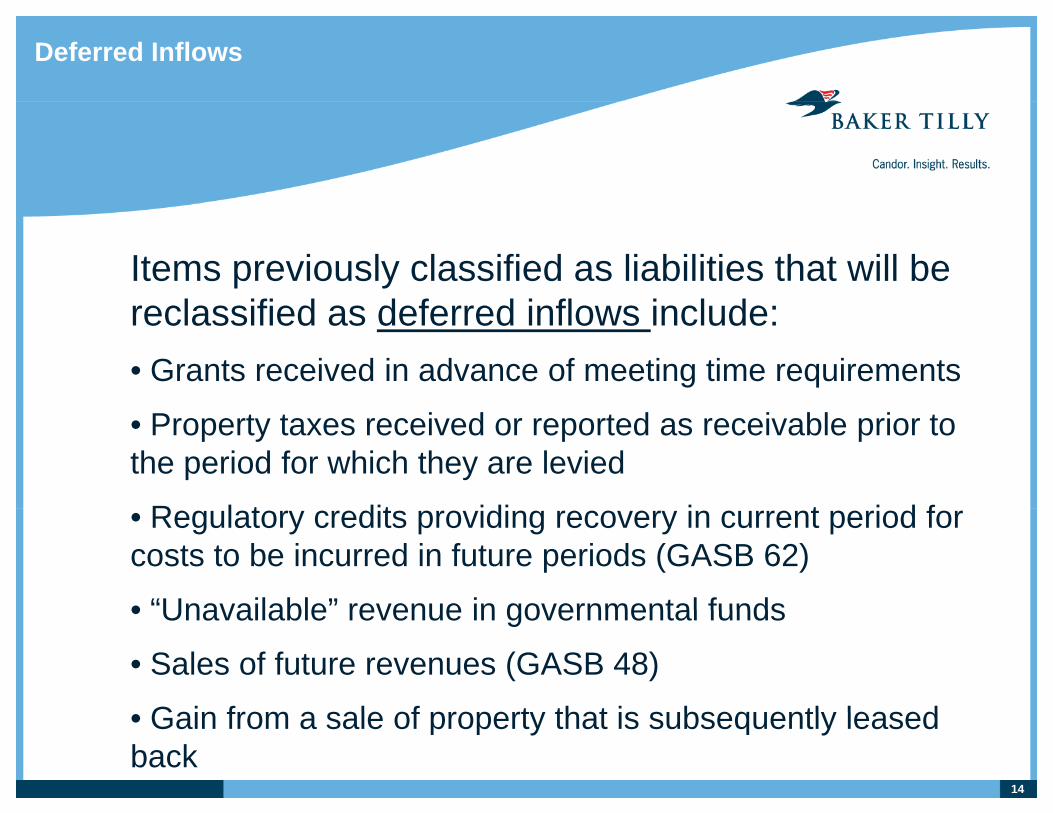

Items previously classified as liabilities that will be l ifi d d f d i fl i l dreclassified as deferred inflows include:

• Grants received in advance of meeting time requirements

• Property taxes received or reported as receivable prior to the period for which they are levied

R l t dit idi i t i d f• Regulatory credits providing recovery in current period for costs to be incurred in future periods (GASB 62)

• “Unavailable” revenue in governmental funds• Unavailable revenue in governmental funds

• Sales of future revenues (GASB 48)

Gain from a sale of propert that is s bseq entl leased• Gain from a sale of property that is subsequently leased back

14

Recognize in Current Period Revenues

Transactions which should be recognized as th t i l l ifi drevenues that were previously classified as

liabilities:V i l di ti iti l t d t l i i ti f• Various lending activities related to loan origination fees

and commitment fees

• Refer to standard if you do significant government lending• Refer to standard if you do significant government lending activities

15

Recognize in Current Period Expenses

Transactions which should be recognized as th t i l l ifi dexpenses that were previously classified as

assets:D bt i t !!!• Debt issuance costs !!!

One potential exception to be discussed

• Initial indirect costs incurred by lessor in an operating• Initial indirect costs incurred by lessor in an operating lease

• Acquisition costs of insurance contracts should beAcquisition costs of insurance contracts should be expensed in the period incurred

• Any fees paid in the purchase of a loan(s) should be y p p ( )expensed in the period the loan(s) was purchased

16

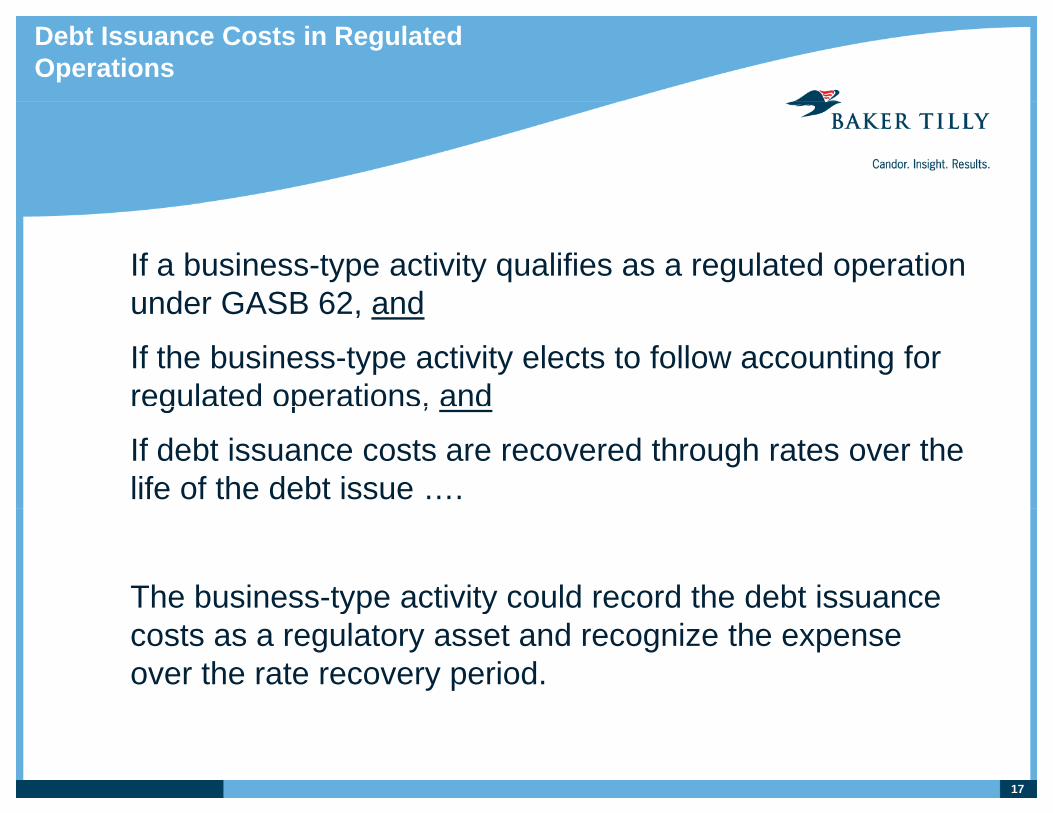

Debt Issuance Costs in Regulated Operations

If a business-type activity qualifies as a regulated operation under GASB 62 andunder GASB 62, and

If the business-type activity elects to follow accounting for regulated operations, andg p ,

If debt issuance costs are recovered through rates over the life of the debt issue ….

The business-type activity could record the debt issuance yp ycosts as a regulatory asset and recognize the expense over the rate recovery period.

17

Polling question #2

One of the most common reclassifications from li bilit t d f d i fl ill bliability to deferred inflow will be:a) Accrued payrollb) Depositsc) Property taxes reported as receivable prior to ) p y p p

the period for which they are levied

18

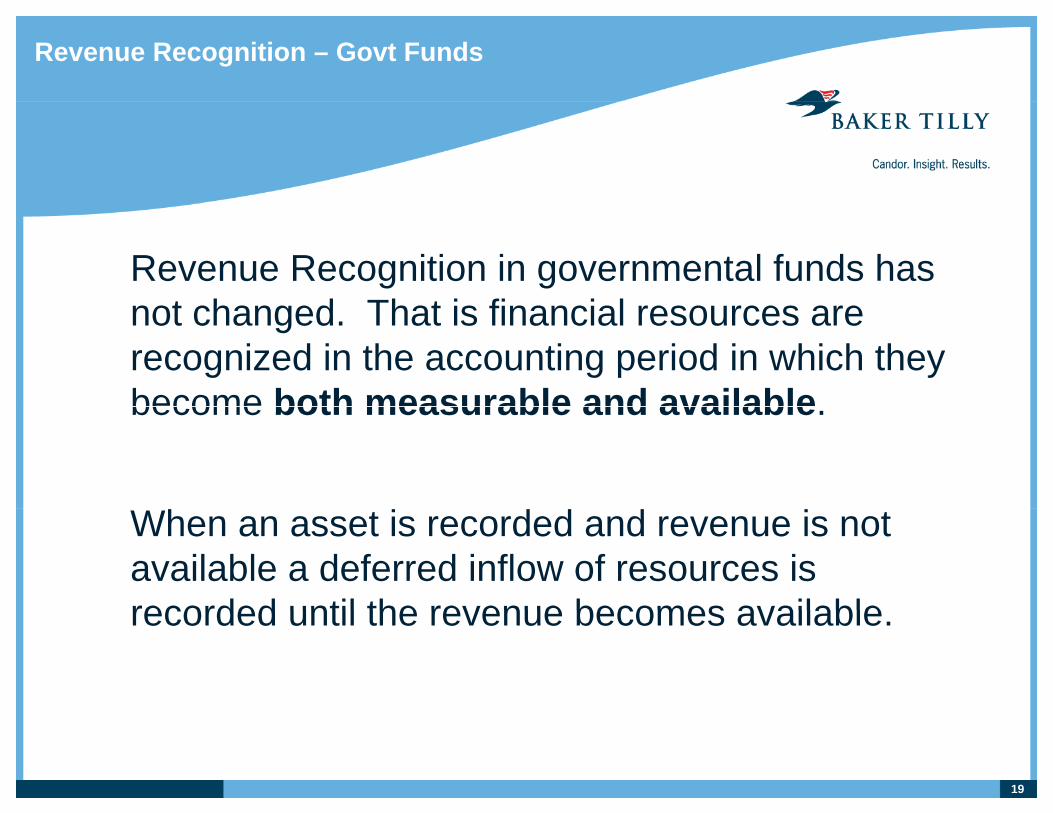

Revenue Recognition – Govt Funds

Revenue Recognition in governmental funds has t h d Th t i fi i lnot changed. That is financial resources are

recognized in the accounting period in which they become both measurable and availablebecome both measurable and available.

When an asset is recorded and revenue is not available a deferred inflow of resources is recorded until the revenue becomes availablerecorded until the revenue becomes available.

19

Impacts to GWFS and Proprietary FS

Summary of most significant changes impacting l f ll l t t tonly full accrual statements:

• Debt issuance costs expensed in current period

• Losses on refunding of debt now a deferred outflow

• Regulatory credits• Refunds in future periods = liability

• Current recovery of future costs = deferred inflow

• Gains and other revenues received in current period to be applied to recoverable future costs = deferred inflow

20

Impacts to all Financial Statement Schedules

Summary of most significant changes impacting ll fi i l t t t ( t id dall financial statements (government-wide and

fund statements):• Property taxes received or receivable in advance of levy are now deferred inflows

Grants received in advance of meeting time requirements• Grants received in advance of meeting time requirements are now deferred inflows

21

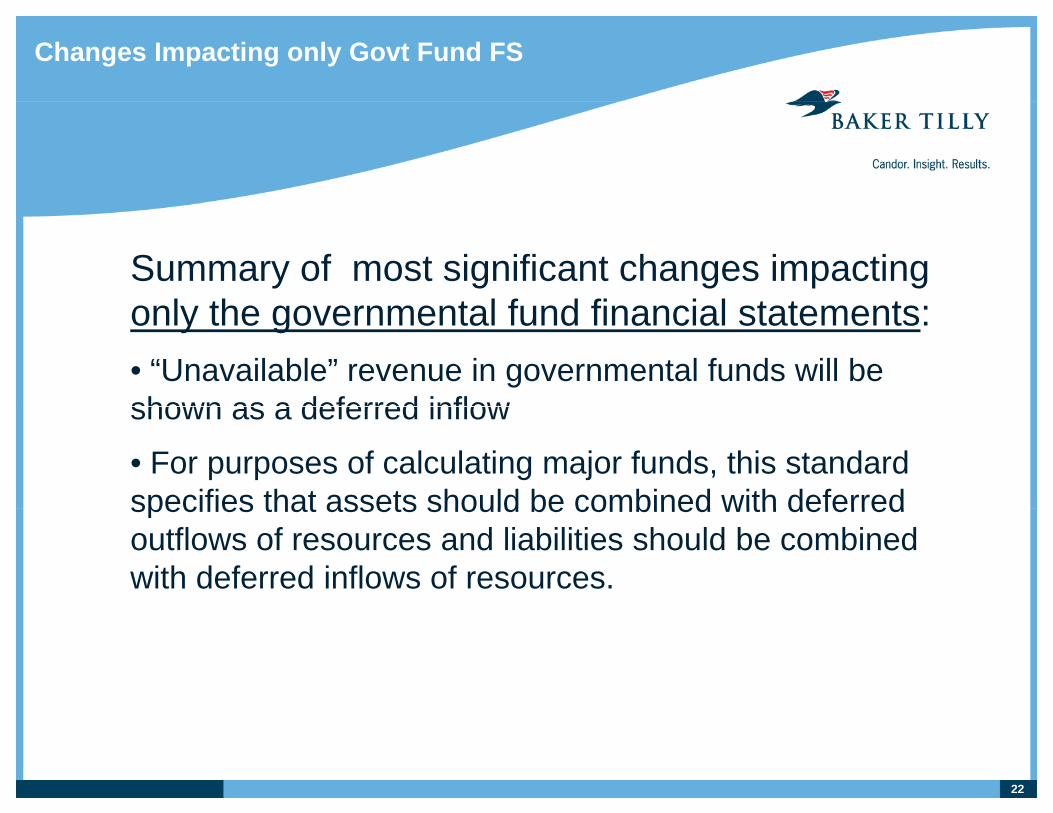

Changes Impacting only Govt Fund FS

Summary of most significant changes impacting l th t l f d fi i l t t tonly the governmental fund financial statements:

• “Unavailable” revenue in governmental funds will be shown as a deferred inflowshown as a deferred inflow

• For purposes of calculating major funds, this standard specifies that assets should be combined with deferredspecifies that assets should be combined with deferred outflows of resources and liabilities should be combined with deferred inflows of resources.

22

Use of Term “Deferred”

GASB No. 65 restricts the use of the term "d f d" t l th it d i t d"deferred" to only those items designated as deferred outflows or deferred inflows of resources by the standards As such other items may needby the standards. As such, other items may need to be relabeled on the financial statements.

23

Polling question #3

Based on what we have discussed, will your fi i l t t t b i t d b GASB 65?financial statements be impacted by GASB 65?a) Yesb) Noc) I’m still not sure)

24

Questions and comments

25

Contact information

Heather Acker, CPA, PartnerH th A k @b k tillHeather. [email protected] 240 2374312 729 8188

J di D b CPA S i MJodi Dobson, CPA, Senior [email protected] 240 2469

26

Resources

GASB No. 65: Items Previously Reported as Assets and Liabilities

Available on www.GASB.org

27

Disclosure

Pursuant to the rules of professional conduct set forth in Circular 230, as promulgated by the United States Department of Treasury, nothing p g y p y, gcontained in this communication was intended or written to be used by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer by the Internal Revenue Service, and it cannot be used by any taxpayer for such purpose. No one, without our express prior written permission, may use or refer to any tax advice in this communication in promoting, marketing, or recommending a

t hi th tit i t t l t tpartnership or other entity, investment plan or arrangement to any other party.

Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an y yindependently owned and managed member of Baker Tilly International. The information provided here is of a general nature and is not intended to address the specific circumstances of any individual or entity. In specific circumstances, the services of a professional should be sought. © 2013 Baker Tilly Virchow Krause, LLP

28

![WV GASB Conference GAAP Update [Read-Only]wvde.state.wv.us/finance/documents/GASBUpdatePresentation.pdf · The Great GASB Conference ... implementation of GASB 47 • All other termination](https://img.pdfslide.us/doc/110x75/5b2a1f147f8b9ad6458b9054/wv-gasb-conference-gaap-update-read-onlywvdestatewvusfinancedocumentsga.jpg)