Embed Size (px)

Citation preview

COMPREHENSIVE ANNUAL FINANCIAL REPORT

OF THE

COUNTY OF DANE WISCONSIN

As of and for the Year Ended December 31, 2012

CONTROLLER’S OFFICE

Charles Hicklin, Controller Margaret L. Krohn, CPA, Assistant Controller

COUNTY OF DANE

COMPREHENSIVE ANNUAL FINANCIAL REPORT As of and for the Year Ended December 31, 2012 TABLE OF CONTENTS

I. INTRODUCTORY SECTION Page

Letter of Transmittal i – v

List of Principal Officials vi – viii

Organization Chart ix

Certificate of Achievement for Excellence in Financial Reporting x

II. FINANCIAL SECTION

INDEPENDENT AUDITORS' REPORT 1 – 3

MANAGEMENT’S DISCUSSION AND ANALYSIS 4 – 16

BASIC FINANCIAL STATEMENTS

Government-wide Financial Statements

Statement of Net Position 17

Statement of Activities 18 – 19

Fund Financial Statements

Balance Sheet – Governmental Funds 20

Statement of Revenues, Expenditures and Changes in Fund Balances – Governmental Funds 21

Reconciliation of the Statement of Revenues, Expenditures, and Changes in Fund Balances of Governmental Funds to the Statement of Activities 22

Statement of Net Position – Proprietary Funds 23 – 26

Statement of Revenues, Expenses, and Changes in Net Position – Proprietary Funds 27 – 28

Statement of Cash Flows – Proprietary Funds 29 – 32

Statement of Net Position – Fiduciary Funds 33

Statement of Changes in Net Position – Fiduciary Funds 34

Statement of Net Position – Component Units 35

Statement of Activities – Component Units 36 Notes to the Financial Statements 37 – 96

COUNTY OF DANE

COMPREHENSIVE ANNUAL FINANCIAL REPORT As of and for the Year Ended December 31, 2012 TABLE OF CONTENTS (cont.)

II. FINANCIAL SECTION (cont.) Page

REQUIRED SUPPLEMENTARY INFORMATION

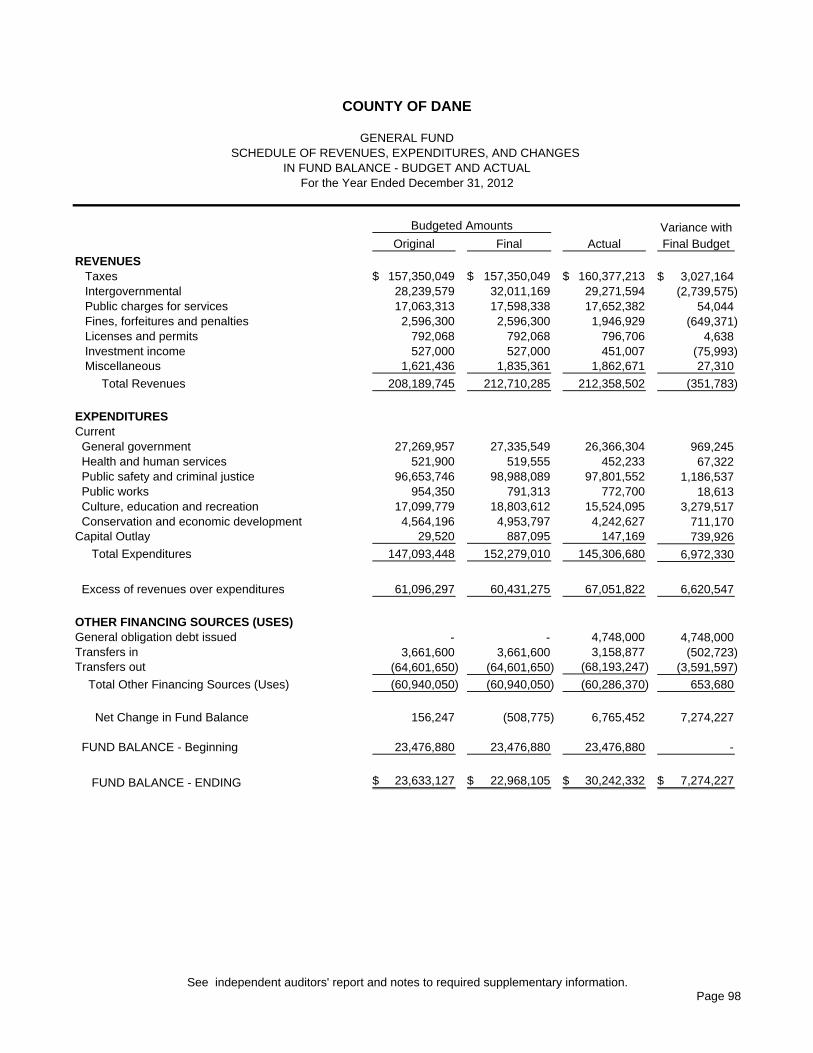

Other Postemployment Benefits Plan – Schedule of Funding Progress 97 Schedule of Revenues, Expenditures and Changes in Fund Balances – Budget and Actual – General Fund 98

Schedule of Revenues, Expenditures and Changes in Fund Balances – Budget and Actual – Human Services Special Revenue Fund 99

Notes to Required Supplementary Information 100

SUPPLEMENTARY INFORMATION

Schedule of Expenditures Compared to Budget – General Fund 101 – 102 Combining Balance Sheet – Nonmajor Governmental Funds 104 – 105

Combining Statement of Revenues, Expenditures and Changes in Fund Balances (Deficit) – Nonmajor Governmental Funds 106 – 107

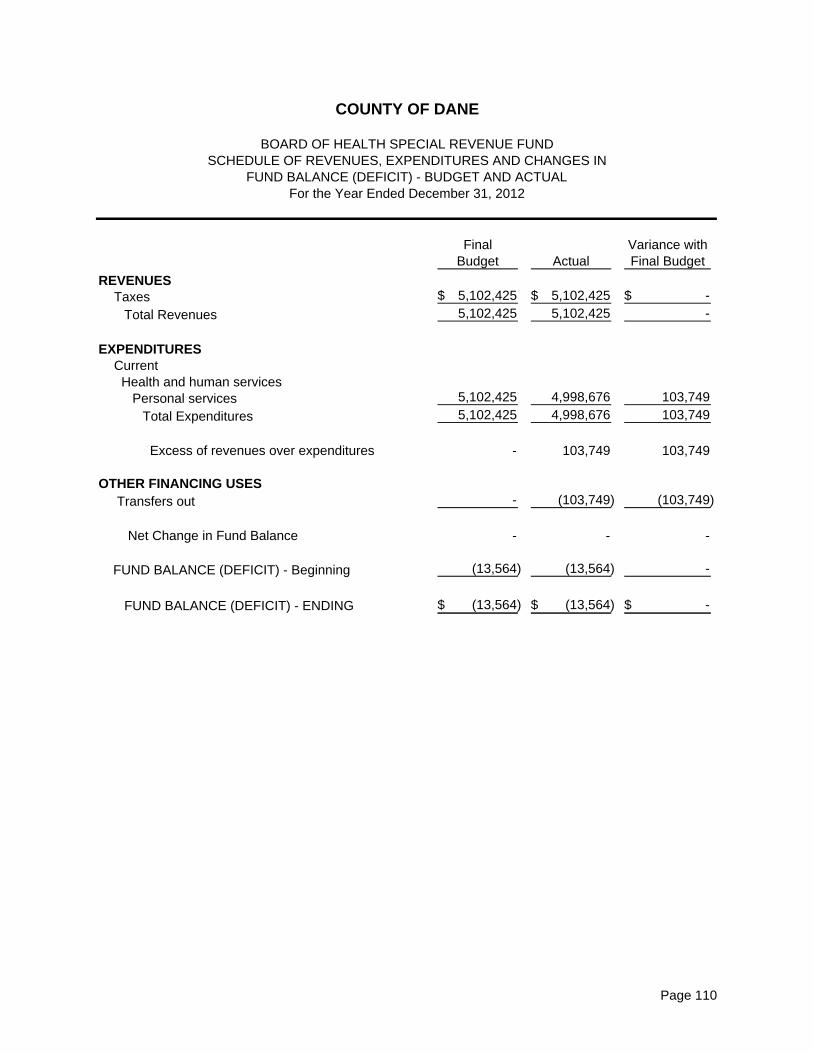

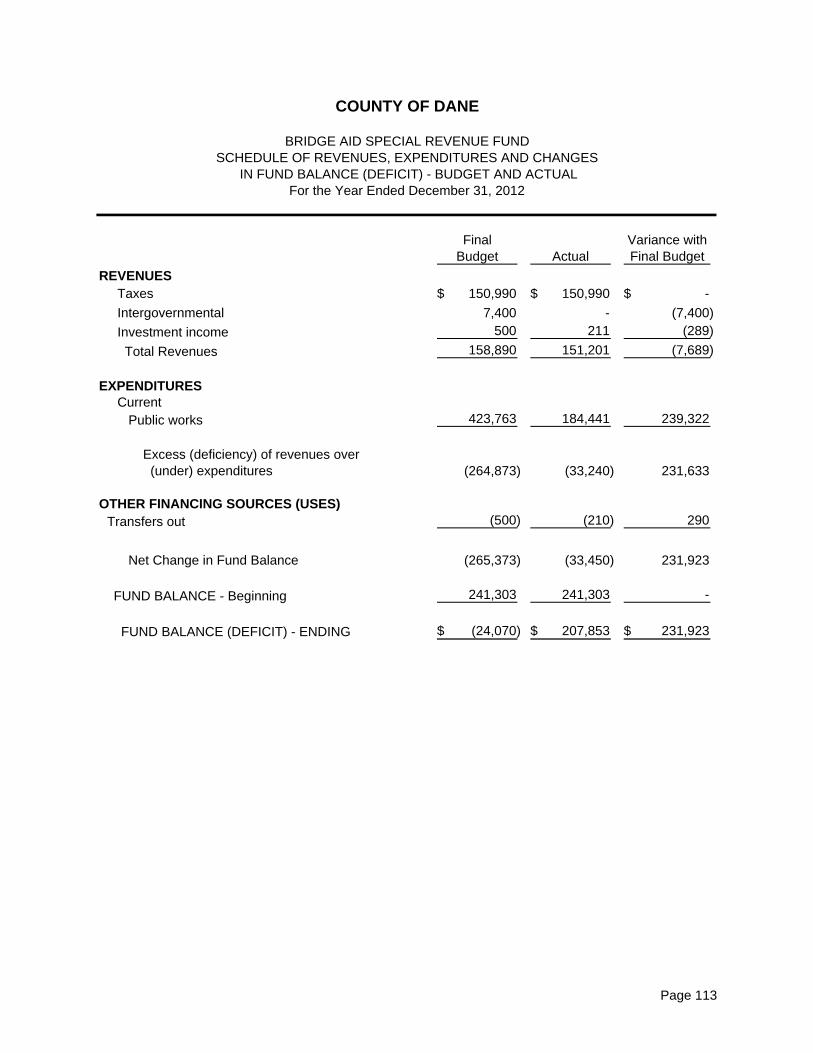

Schedules of Revenues, Expenditures, and Changes in Fund Balances (Deficit) – Budget and Actual Debt Service Fund – Major Fund 108 Capital Projects Fund – Major Fund 109 Board of Health Special Revenue Fund 110 Library Special Revenue Fund 111 Land Information Special Revenue Fund 112 Bridge Aid Special Revenue Fund 113 CDBG Loans Special Revenue Fund 114 HOME Special Revenue Fund 115 Commerce Revolving Loan Special Revenue Fund 116 Social Security Redaction Special Revenue Fund 117 Combining Statement of Net Position – Nonmajor Proprietary Funds 119 Combining Statement of Revenues, Expenses, and Changes in Net Position – Nonmajor Proprietary Funds 120 Combining Statement of Cash Flows – Nonmajor Proprietary Funds 121 – 122

COUNTY OF DANE

COMPREHENSIVE ANNUAL FINANCIAL REPORT As of and for the Year Ended December 31, 2012 TABLE OF CONTENTS (cont.)

II. FINANCIAL SECTION (cont.) Page

SUPPLEMENTARY INFORMATION (cont.)

Combining Statement of Net Position – Internal Service Funds 124 – 125 Combining Statement of Revenues, Expenses and Changes in Net Position – Internal Service Funds 126 Combining Statement of Cash Flows – Internal Service Funds 127 – 128 Combining Statement of Net Position – Fiduciary Funds 130 Combining Statement of Changes in Net Position – Fiduciary Funds 131 Combining Statement of Changes in Assets and Liabilities – All Agency Funds 132 – 133 Dane County Interoperable Radio System – Schedule of Revenues, Expenditures and Changes in Fund Balance (Deficit) – Operating Fund 134 III. STATISTICAL SECTION

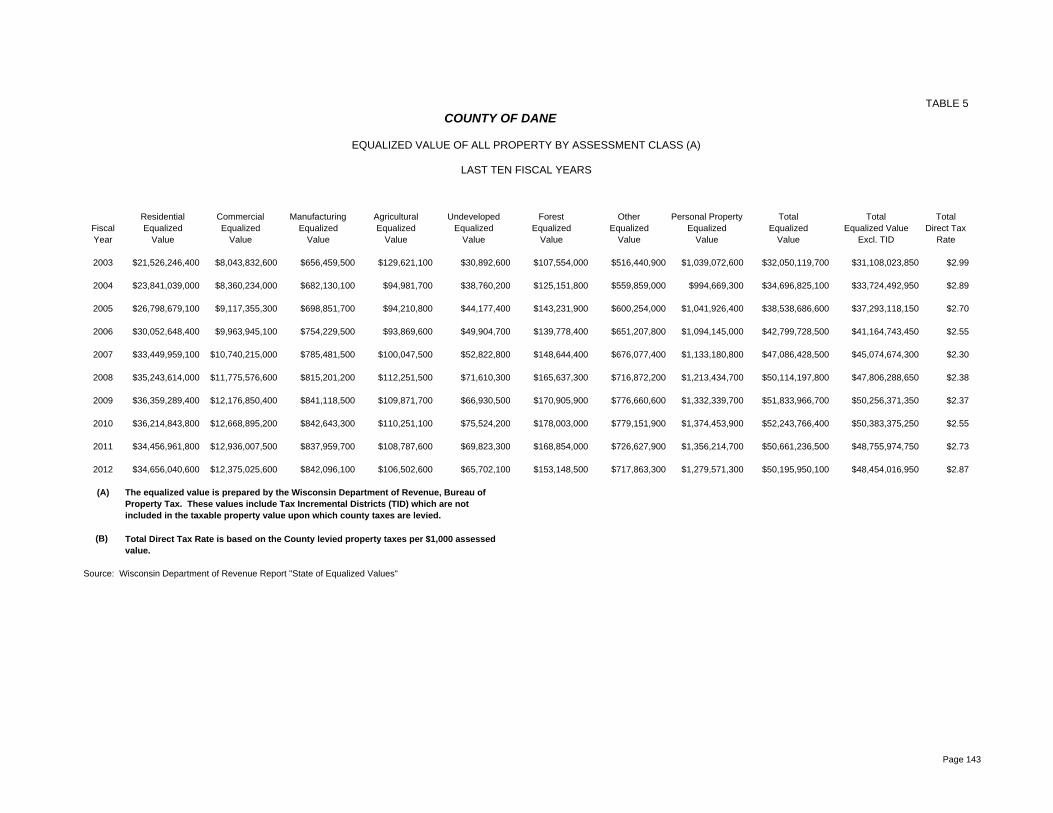

Table Index 135 – 136 Table 1 – Net Position by Component 137 Table 2 – Changes in Net Position 138 – 139 Table 3 – Fund Balance, Governmental Funds 140 Table 4 – Statement of Revenues, Expenditures and Changes in Fund Balance – Governmental Funds 141 – 142 Table 5 – Equalized Value of All Property by Assessment Class 143 Table 6 – Tax Revenue by Source, Governmental Funds 144 Table 7 – Direct and Overlapping Property Tax Rates 145 – 146 Table 8 – Principal Property Taxpayers 147 Table 9 – Property Tax Levies and Collections 148 Table 10 – Ratios of Outstanding Bonded Debt 149 Table 11 – Computation of Direct and Overlapping Debt 150 – 151 Table 12 – Computation of Legal Debt Margin 152 Table 13 – Demographic Statistics 153

COUNTY OF DANE

COMPREHENSIVE ANNUAL FINANCIAL REPORT As of and for the Year Ended December 31, 2012 TABLE OF CONTENTS (cont.)

III. STATISTICAL SECTION (cont.) Page

Table 14 – Principal Employers 154 Table 15 – Full-Time Equivalent Positions by Activity 155 Table 16 – Operating Indicators by Activity/Department 156 Table 17 – Capital Asset Statistics by Function 157 Table 18 – Schedule of Insurance in Force 158 – 159

i

COUNTY OF DANE DEPARTMENT OF ADMINISTRATION

CONTROLLER DIVISION 210 Martin Luther King, Jr. Boulevard, Room 426

Madison, Wisconsin 53703 608/266-4131 TDD 608/266-9253

CHARLES HICKLIN TRAVIS MYREN Controller Director of Administration

June 21, 2013 To the Citizens, Executive Joseph Parisi and Board of Supervisors of the County of Dane The Controller’s office is pleased to present the Comprehensive Annual Financial Report (CAFR) for the County of Dane for the fiscal year ended December 31, 2012. This CAFR is prepared by the Dane County Controller’s office and audited by the independent certified public accounting firm of Baker Tilly Virchow Krause, LLP. Wisconsin Statutes and the Wisconsin Administrative Code require counties to prepare a complete set of audited financial statements for each fiscal year. This CAFR is provided to fulfill that requirement for 2012. The financial statements included in the CAFR conform with generally accepted accounting principles (GAAP) as established by the Governmental Accounting Standards Board (GASB). The letter of transmittal is designed to complement the Management Discussion & Analysis (MD&A) and should be read in conjunction with the financial statements. MANAGEMENT REPRESENTATIONS Responsibility for both the accuracy of the data presented and the completeness and fairness of the presentation, including all disclosures, rests with the County. We believe the financial information, as presented: is accurate in all material aspects; is presented in a manner designed to fairly set forth the financial position and results of operations of the

County as measured by the financial activity of its various funds; and includes all disclosures necessary to enable the reader to gain the maximum understanding of the

County's financial affairs. INTERNAL CONTROLS In developing the County's accounting system, much consideration was given to the adequacy of internal accounting controls. Internal accounting controls are designed to provide reasonable, but not absolute assurance regarding: (1) the safeguarding of assets against loss from unauthorized use or disposition and (2) the reliability of financial records for preparing financial statements and maintaining accountability for assets. The concept of reasonable assurance is based on the assumption that the costs of internal accounting controls should not exceed the benefits expected to be derived from their implementation. We believe that the County's internal accounting controls, along with the audit performed by independent auditors, provide the County with reasonable assurance that financial transactions are properly recorded and assets adequately safeguarded. INDEPENDENT AUDIT The County has retained the services of Baker Tilly Virchow Krause, LLP to perform an independent audit of the County’s financial records. The goal of the independent audit was to provide reasonable assurance that the financial statements of the County of Dane for the fiscal year ended December 31, 2012, are free of material misstatement. The independent audit involved examining, on a test basis, evidence supporting the

ii

amounts and disclosures in the financial statements; assessing the accounting principles used and significant estimates made by the county; and evaluating the overall financial statement presentation. The independent auditor concluded, based upon the audit, that there was a reasonable basis for rendering an unqualified opinion that the County of Dane’s financial statements for the fiscal year ended December 31, 2012, are fairly presented in conformity with GAAP. The independent auditor’s report is presented as the first component of the financial section of this report. As part of their examination, the independent auditor is also issuing an internal control letter covering the review of the county’s system of internal control over financial reporting and tests of compliance with certain provision of laws, regulations, contracts, and grants. The management and compliance letter will not modify or affect, in any way, this report. The county is required to undergo an annual single audit in conformity with the provisions of the Single Audit Act Amendments of 1996 and U.S. Office of Management and Budget Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations. Information related to this single audit—including the schedule of expenditures of federal awards, findings and recommendations, and auditor’s reports on internal control over financial reporting and tests of compliance with certain provisions of laws, regulations, contracts, and grants—will be included in the County of Dane’s separately issued Single Audit Report. CERTIFICATE OF ACHIEVEMENT The Government Finance Officers Association of the United States and Canada (GFOA) awarded a Certificate of Achievement for Excellence in Financial Reporting to Dane County, Wisconsin for its comprehensive annual financial report for the fiscal year ended December 31, 2011. This was the twenty-ninth consecutive year that Dane County has achieved this prestigious award. In order to be awarded a Certificate of Achievement, a government must publish an easily readable and efficiently organized comprehensive annual financial report. This report must satisfy both generally accepted accounting principles and applicable legal requirements. A Certificate of Achievement is valid for a period of one year only. We believe that our current comprehensive annual financial report continues to meet the Certificate of Achievement Program’s requirements, and we are submitting it to the GFOA to determine its eligibility for another certificate. PROFILE OF GOVERNMENT Basic Information Dane County was created by the first Wisconsin territorial legislature in 1836 and was organized as a separate governmental unit in 1839. With a population of 491,555, the County is second only to Milwaukee County in terms of size in Wisconsin. Within the County's 1,238 square miles, there are 34 towns, 19 villages, and eight cities. The City of Madison is the largest with 48% of the County’s population and 44.5% of the equalized value. The City of Madison is the Capitol of Wisconsin and the site of the 42,454 student University of Wisconsin-Madison. The County provides a range of governmental services authorized by state statute, under the direction of an elected Executive and a thirty-seven member Board of Supervisors. The County Executive is elected to a four-year term and the thirty-seven Board Supervisors are elected to two-year terms. The Chair of the County Board of Supervisors is elected by the other members of the Board and services for a two-year term. There are six elected department heads whose offices are established by the Wisconsin Constitution. These offices are the Clerk of Courts, County Clerk, District Attorney, Register of Deeds, Sheriff and Treasurer. In addition, the county has numerous non-elected department heads that administer the county, state and federal regulations specific to their departments. A list of principal officers and organization chart begins on page vi. The services provided by the County are categorized into the following six functions. General government function includes the executive, clerk, administration, treasurer, register of deeds

and corporation counsel; Public safety & criminal justice function, including a 17-branch court system; the district attorney, the

sheriff, jail and work release facility and public safety communications; Health and human services function, including care for children, mental health services,

developmentally disabled, the aged and disabled;

iii

Conservation & economic development function, including solid waste program, land regulation & records and land conservation;

Culture, education & recreation function including an exposition center, zoo, park system and library services;

Public works function, including a regional airport, highway system, and transportation system assistance.

Component Units In addition to the primary government operations of the County, the basic financial statements include the Dane County Housing Authority and the Henry Vilas Park Zoological Society as Component Units. These units are included within the County’s financial report in accordance with GAAP because of various factors including financial dependencies and powers of appointment or removal of officers. Budget The County of Dane prepares an annual budget as required by State of Wisconsin Statutes. Budgetary control is maintained at the agency level. Encumbrances are made against appropriations prior to the issuance of purchase orders or consummation of contracts. Purchase orders outstanding at the end of the year where the goods and/or services have not been received are recognized in the accompanying financial statements as reservations of fund balance as they do not constitute expenditures or liabilities. The Board of Supervisors has designated certain accounts as non-lapsing, and those unexpended appropriations have been carried forward for use in 2013. Debt Administration All debt outstanding is a general obligation of the County for which an irrepealable, irrevocable tax has been levied at the time of the borrowing to be included in future tax levies, sufficient to repay the principal and interest payments as they become due. Under Wisconsin State Statutes, Chapter 67, Dane County’s aggregate indebtedness may not exceed 5% of the equalized value of taxable property located in the County.

ECONOMIC CONDITION AND OUTLOOK Dane County is the home office of the Oscar Mayer Foods Corporation, a leading national meat processing company; Cuna Mutual & Subsidiaries, providing insurance and services to credit unions throughout the world; American Family Insurance; Epic Systems; and many other businesses and industries. In addition, Dane County is a leading county in many agricultural crops including corn, tobacco, soybeans and milk. The County is also a leading county in the number of farms and amount of land used for farms. Dane County has a rapidly growing high-tech business community that currently includes more than 600 firms employing more than 32,500 in 2012. Biotechnology, medical/biomedical research, micro-electronics, pharmaceuticals, contract research and development, software and other computer-related firms dominate the list of high-tech firms. This reflects the University of Wisconsin-Madison's worldwide leadership in research and academic teaching in these areas. In fiscal year 2011, the University of Wisconsin-Madison received more than $1,184.9 million in extramural support for research from federal, state and private sources. According to latest figures available from the National Science Foundation, the University of Wisconsin-Madison is the third largest funded research university in the country. Various national magazines have recognized Madison and the Dane County metropolitan area as one of the best places to live in the Midwestern United States.

iv

The 2012 annual average unemployment rate in Dane County, at 4.7% is consistently below state and national averages. The low unemployment rate can be attributed to the stability of the workforce and type of business located in the County.

Dane County Unemployment (Source: State of Wisconsin Department of Workforce Development)

2.8%2.6%

3.1% 3.2%3.5%

3.3%

5.7% 5.6%

5.0%4.7%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Unemployment Rates

Dane County Employment by Industry

(Source: Wisconsin Department of Workforce Development)

Industry Type 2011 2012

Number % Total Number % TotalConstruction 10,860 3.68% 10,797 3.61%Education & Health 77,342 26.23% 77,698 25.95%Financial Activities 24,822 8.42% 24,668 8.24%Information 10,424 3.54% 11,451 3.82%Leisure & Hospitality 27,313 9.26% 27,888 9.31%Manufacturing 22,652 7.68% 23,493 7.85%Natural Resources 1,662 0.56% 1,710 0.57%Other Services 11,096 3.76% 11,110 3.71%Professional & Business Services 35,982 12.20% 37,833 12.64%Public Administration 23,558 7.99% 23,276 7.77%Trade, Transportation, Utilities 49,084 16.65% 49,490 16.53%Other 32 0.01% 3 0.00%

Totals 294,827 100.00% 299,417 100.00%

v

MAJOR INITIATIVES Radio System Replacement Project - The county continued work on the Radio System Replacement project for the 911 Center. The new radio system will provide interoperability among the county’s public safety and public safety radio users. The new system will also bring the system into compliance with FCC requirement. Highway Construction Projects – The county budgeted over $5.3 million in 2012 for planning, reconstruction, and resurfacing of county highways. Planning and design of a new East Side Garage Facility for the Highway department began in 2012. The project is budgeted at $7.5 million. ACKNOWLEDGMENTS The preparation of this report could not have been accomplished without the efficient and dedicated services of the entire staff of the Controller's Office, especially Assistant Controller Margaret Krohn, other County Departments and the capable assistance of our independent auditors. I would like to express my appreciation to everyone that assisted and contributed in its preparation. Respectfully submitted,

Charles Hicklin Controller

COUNTY OF DANE

LIST OF PRINCIPAL OFFICIALS

AS OF DECEMBER 31, 2012

vi

COUNTY OF DANE LIST OF PRINCIPAL OFFICIALS AS OF DECEMBER 31, 2012 ELECTED OFFICIALS Office Name County Executive Joseph Parisi Clerk of Courts Carlos Esqueda Medical Examiner Raymond Tranchida County Clerk Karen Peters District Attorney Ismael Ozanne Register of Deeds Kristi Chlebowski Sheriff David Mahoney Treasurer David Worzala COUNTY BOARD SUPERVISORS Supervisory District Name 1 Scott A. McDonell, Chair 2 Heidi Wegleitner 3 Nick Zweifel

4 Kyle Richmond 5 Leland Pan

6 John E. Hendrick 7 Matt Veldran 8 Carousel Andrea Bayrd 9 Diane Hesselbein 10 Jeremy Levin 11 Alfred Matano 12 Paul Rusk 13 Chuck Erickson 14 Melanie Hampton 15 Ronn Ferrell 16 Dave de Felice 17 Jeff Pertl 18 Melissa Sargent 19 Bill Clausius 20 Dennis O’Loughlin 21 David E. Wiganowsky 22 Maureen McCarville 23 Shelia Stubbs

(Continued on next page)

vii

COUNTY OF DANE LIST OF PRINCIPAL OFFICIALS AS OF DECEMBER 31, 2012 (Continued) COUNTY BOARD SUPERVISORS Supervisory District Name 24 Robin Schmidt 25 Tim Kiefer 26 Sharon Corrigon 27 Dorothy Krause 28 Kurt Schlicht 29 David Ripp 30 Patrick Downing 31 Jerome Bollig 32 Erika Hotchkiss 33 Jenni Dye 34 Patrick Miles 35 Carl Chenoweth 36 Cynda Solberg 37 Robert Salov NONELECTED OFFICIALS Activity Name Administration Travis Myren Adult Community Services Louis F. Genter Airport Bradley Livingston Badger Prairie Health Care Center Steve Handrich Children, Youth & Family Services Bob Lee Controller Charles Hicklin Corporation Counsel Marcia Mackenzie Economic Assistance & Work Services Amy Mendel-Clemens Emergency Management Charles Tubbs Exposition Center Mark Clarke Extension Carrie Edgar (Continued from previous page)

viii

COUNTY OF DANE LIST OF PRINCIPAL OFFICIALS AS OF DECEMBER 31, 2012 (Continued) NONELECTED OFFICIALS Activity Name Family Court Counseling Kristen Ryan Public Works, Highway & Transportation Gerald Mandli Human Services Lynn Green Juvenile Court Program John Bauman Land & Water Resources Kevin F. Connors Library Julie A. Chase Planning & Development Todd Violante Public Health Service Janel Heinrich Public Safety Communications John Dejung Veterans Service BJ Ganem Zoo Ronda Schwetz (Continued from previous page)

DA

NE

CO

UN

TY, W

ISC

ON

SIN

OR

GA

NIZ

AT

ION

OF

DA

NE

CO

UN

TY

GO

VE

RN

ME

NT

Saf

ety

& W

orki

ng

Co

nd

ition

s S

tud

y C

om

mitt

ee

So

lid W

aste

&

Re

cycl

ing

Com

mis

sion

So

uth

Ce

ntra

l L

ibra

ry S

yste

m

Bo

ard

So

uth

Ce

ntra

l W

isco

nsi

n R

ail

Tra

nsi

t C

omm

issi

on

So

uth

we

st D

an

e

Tra

nsp

ort

atio

n

Adv

isor

y C

om

mitt

ee

Sp

eci

aliz

ed

T

ran

spo

rtat

ion

C

omm

issi

on

V

ete

ran

s S

erv

ice

C

omm

issi

on

W-2

Com

mu

nity

S

tee

ring

Co

mm

ittee

W

omen

's I

ssue

s C

om

mitt

ee

Y

ou

th

Com

mis

sion

B

oa

rd o

f H

ealth

Em

erg

en

cy

Me

dic

al S

erv

ice

s C

om

mis

sio

n

Join

t Pu

blic

H

ealth

Ad

viso

ry

Co

mm

ittee

Pu

blic

Saf

ety

C

om

mu

nic

atio

ns

Ce

nte

r B

oa

rd

T

ree

Boa

rd

Adm

inis

trat

ion

A

irpor

t A

llian

t Ene

rgy

Cen

ter

Ext

ensi

on

Offi

ce

Fam

ily C

ourt

C

ouns

elin

gH

uman

Ser

vice

s

Land

& W

ater

R

esou

rces

BO

AR

DS

& C

OM

MIS

SIO

NS

CIT

IZE

NS

CO

UN

TY

E

XE

CU

TIV

E

B

OA

RD

OF

S

UP

ER

VIS

OR

S

BO

AR

D

CH

AIR

PE

RS

ON

C

OU

NT

Y B

OA

RD

S

ER

VIC

ES

ST

AN

DIN

G C

OM

MIT

TE

ES

Exe

cutiv

e

Pe

rso

nne

l &

Fin

ance

H

ea

lth &

Hum

an

N

ee

ds

Pu

blic

Pro

tect

ion

&

Ju

dic

iary

Env

ironm

ent,

Ag

&

Nat

ural

Res

ourc

es

Pu

blic

Wor

ks &

T

ran

spo

rtat

ion

Zo

nin

g &

La

nd

Re

gula

tion

C

OM

MIT

TE

ES

OF

TH

E C

OU

NT

Y B

OA

RD

C

ity-C

ou

nty

L

iais

on

Info

rma

tion

R

esou

rces

M

an

age

me

nt

L

and

C

on

serv

atio

n

U

niv

ers

ity

Ext

en

sio

n

S

tra

tegi

c G

row

th

Ma

na

gem

en

t

Cor

pora

tion

Cou

nsel

Em

erge

ncy

Ma

nage

men

t

Land

Info

rmat

ion

Pub

lic S

afet

y C

omm

unic

atio

ns

DE

PA

RT

ME

NT

S

Join

t Bo

ard

of

Hea

lth

Libr

ary

Ser

vice

Pub

lic W

orks

, H

wy

& T

rans

p.

Me

dica

l E

x am

ine

r

Vet

eran

s S

ervi

ce

Co

mm

un

ity

De

velo

pm

ent

Blo

ck G

rant

C

omm

issi

on

EL

EC

TE

D O

FF

ICE

S

DIS

TR

ICT

A

TT

OR

NE

Y

CLE

RK

OF

C

OU

RT

S

RE

GIS

TE

R

OF

DE

ED

S

CO

UN

TY

C

LER

K

SH

ER

IFF

T

RE

AS

UR

ER

C

om

mis

sio

n o

n

Agi

ng

C

om

mis

sio

n o

n

Se

nsi

tive

Crim

es

E

lect

ion

C

om

mis

sio

n E

con

omic

Sum

mit

Cou

ncil

C

ultu

ral A

ffairs

C

om

mis

sio

n

Co

ord

ina

ting

Co

un

cil

C

hild

ren

Com

e

Firs

t C

om

mis

sion

C

ivil

Se

rvic

e

Com

mis

sion

B

.U.I

.L.D

. C

om

mitt

ee

His

toric

P

rese

rva

tion

C

om

mitt

ee

Lo

cal E

me

rge

ncy

P

lan

nin

g C

om

mitt

ee

H

ou

sin

g A

uth

orit

y

Lo

ng

Te

rm

Su

ppo

rt

Co

mm

ittee

H

um

an S

erv

ice

s B

oa

rd

Join

t C

ity-C

ou

nty

S

ect

ion

8 R

enta

l H

ou

sin

g P

rovi

de

r A

dvi

sory

Co

mm

.

Mo

no

na T

err

ace

C

on

ven

tion

&

Co

mm

un

ity

Ce

nte

r B

oa

rd

A

gric

ultu

ral

Adv

isor

y C

ounc

il

A

irpo

rt

Com

mis

sion

A

llia

nt

En

erg

y C

en

ter

Com

mis

sion

B

oa

rd o

f A

dju

stm

ent

Ta

sk F

orce

on

Chr

onic

Was

ting

Dis

ea

se

No

rth

Me

ndo

ta

Pa

rkw

ay

Ad

viso

ry

Co

mm

ittee

Join

t O

vers

igh

t A

dvis

ory

Co

mm

ittee

T

raff

ic S

afe

ty

Com

mis

sion

P

ark

Co

mm

issi

on

H

en

ry V

ilas

Zo

o

Com

mis

sion

L

ibra

ry B

oa

rd

E

thic

s B

oa

rd

L

ivin

g W

age

R

evi

ew

Co

un

cil

La

kes

&

Wat

ers

he

d C

omm

issi

on

E

nvi

ron

me

nta

l C

ou

nci

l

L

and

Inf

orm

atio

n

Off

ice

Com

mitt

ee

Equ

al

Op

po

rtu

niti

es

Com

mis

sion

Wis

con

sin

Riv

er

Ra

il T

ran

sit

Com

mis

sion

Pu

blic

Saf

ety

C

om

m.

Op

er.

P

ract

ices

Ad

viso

ry

Co

mm

ittee

Just

ice

Cen

ter

Pla

nn

ing

Ove

rsig

ht

Co

mm

ittee

Em

plo

yee

Mgm

t.

Insu

ran

ce

Adv

isor

y C

om

mitt

ee

R

ecla

ssifi

catio

n A

pp

eals

Bo

ard

Juve

nile

Cou

rt

Pr o

gram

Pla

nnin

g &

D

eve

lop

men

t

Hen

ry V

ilas

Zo

o

Page 4

COUNTY OF DANE, WISCONSIN

MANAGEMENT’S DISCUSSION AND ANALYSIS (UNAUDITED)

For Year Ended December 31, 2012 As management of the County of Dane, Wisconsin we offer readers of the County’s financial statements this narrative overview and analysis of the financial activities of the County for the fiscal year ended December 31, 2012. We encourage readers to consider the information presented here in conjunction with the County’s financial statements and the additional information that we have furnished in our letter of transmittal, which can be found on pages i to v of this report. FINANCIAL HIGHLIGHTS

The assets of the County of Dane exceeded its liabilities at the close of the most recent fiscal year by

$459,074,494 (net position). Of this amount, ($16,939,285) are classified as unrestricted net position. The total net position includes all major infrastructure networks.

The County’s total net position increased by $5,760,750.

As of the close of the current fiscal year, the County of Dane’s governmental funds reported combined ending fund balances of $51,361,681, an increase of $1,724,307 in comparison with the prior year. Approximately 84% of this amount, $43,074,231, is spendable and available for use within the County’s designations, policies, or agreements.

At the end of the current fiscal year, unassigned fund balance for the general fund was $18,895,829 or approximately 13% of total general fund expenditures.

OVERVIEW OF THE FINANCIAL STATEMENTS This discussion and analysis is intended to serve as an introduction to the County’s basic financial statements. The County’s basic financial statements are comprised of three components: 1) government-wide financial statements, 2) fund financial statements and 3) notes to the financial statements. This report also contains other supplementary information in addition to the basic financial statements themselves. Government-Wide Statements The government-wide financial statements are designed to provide readers with a broad overview of the County’s finances, in a manner similar to a private – sector business.

Page 5

COUNTY OF DANE, WISCONSIN

MANAGEMENT’S DISCUSSION AND ANALYSIS (cont.) (UNAUDITED)

For Year Ended December 31, 2012 OVERVIEW OF THE FINANCIAL STATEMENTS (cont.)

The Statement of Net Position presents information on all of the County’s assets and liabilities, with the difference between the two reported as net position. Over time, increases or decreases in net position may serve as a useful indicator of whether the financial position of the County is improving or deteriorating. To assess the overall health of the County one must consider additional non-financial factors such as changes in the County’s property tax base and the condition of the County’s infrastructure. The Statement of Activities presents information showing how the County’s net position changed during the fiscal year. All changes in net position are reported when the underlying event giving rise to the change occurs, regardless of the timing of the related cash flows. Thus, revenues and expenses are reported in this statement for some items that will only result in cash flows in the future fiscal periods (e.g., uncollected taxes and earned but unused compensated absences). Both of the government-wide financial statements distinguish functions of the County that are principally supported by taxes and intergovernmental revenues (governmental activities) from functions that are intended to recover all or a significant portion of their costs through user fees and charges (business-type activities). The governmental activities of the County include general government; health and human services; public safety and criminal justice; public works; culture, education and recreation; and conservation and economic development. The business-type activities of the County of Dane include the airport, highway, sanitary landfill, Badger Prairie health care, printing and services, and methane gas. The government-wide financial statements include not only the County of Dane itself (known as the primary government), but also the Henry Vilas Zoological Society, Inc. and the Dane County Housing Authority which are separate legal entities for which the County of Dane is financially accountable. Financial information for these component units are reported separately from the financial information presented for the primary government itself. The government-wide financial statements can be found on pages 17 to 19 of this report. Fund Financial Statements A fund is a grouping of related accounts that is used to maintain control over resources that have been segregated for specific activities or objectives. The County, like other state and local governments, uses fund accounting to ensure and demonstrate compliance with finance-related legal requirements. All of the funds of the County can be divided into three categories: governmental funds, proprietary funds, and fiduciary funds. Governmental Funds – Governmental funds are used to account for essentially the same functions reported as governmental activities in the government-wide financial statements. However, unlike the government-wide financial statements, governmental fund financial statements focus on near-term inflows and outflows of spendable resources, as well as on balances of spendable resources available at the end of the fiscal year. Such information may be useful in evaluating a government’s near-term financing requirements.

Page 6

COUNTY OF DANE, WISCONSIN

MANAGEMENT’S DISCUSSION AND ANALYSIS (cont.) (UNAUDITED)

For Year Ended December 31, 2012 OVERVIEW OF THE FINANCIAL STATEMENTS (cont.)

Because the focus of governmental funds is narrower than that of the government-wide financial statements, it is useful to compare the information presented for governmental funds with similar information presented for governmental activities in the government-wide financial statements. By doing so, readers may better understand the long-term impact of the government’s near-term financing decisions. Both the governmental fund balance sheet and the governmental fund statement of revenues, expenditures, and changes in fund balances provide a reconciliation to facilitate this comparison between governmental funds and governmental activities. The County maintains 13 individual governmental funds. Information is presented separately in the governmental fund balance sheet and in the governmental fund statement of revenues, expenditures, and changes in fund balances for the General Fund, Human Services Special Revenue Fund, Debt Service Fund and the Capital Projects Fund, all of which are considered to be major funds. Data from the other governmental funds are combined into a single, aggregated presentation. Individual fund data for each of these non-major governmental funds is provided in the form of combining statements elsewhere in this report. The basic governmental fund financial statements can be found on pages 20 to 22 of this report. Proprietary Funds – The County maintains two different types of proprietary funds. Enterprise funds are used to report the same functions presented as business-type activities in the government-wide financial statements. The County uses enterprise funds to account for its Airport, Highway, Sanitary Landfill, Badger Prairie Health Care Center, Printing and Services, and Methane Gas activities. Internal service funds are an accounting device used to accumulate and allocate costs internally among the County’s various functions. The County uses its internal service funds to account for its Workers’ Compensation, Liability Insurance, Employee Benefits, and Consolidated Food Service programs. The services provided by these funds predominately benefit the governmental rather than the business-type functions. They have been included within governmental activities in the government-wide financial statements. Proprietary funds provide the same type of information as the government-wide financial statements, only in more detail. The proprietary fund financial statements provide separate information for the Airport, Highway, Sanitary Landfill, and Badger Prairie Health Care, since they are considered to be major funds of the County. Data from other proprietary enterprise funds are combined into a single, aggregated presentation. All internal service funds are combined into a single aggregated presentation in the proprietary fund financial statements. Individual fund data for the internal services funds is provided in the form of combining statements elsewhere in this report. The basic proprietary fund financial statements can be found on pages 23 to 32 of this report. Fiduciary Funds – Fiduciary funds are used to account for resources held for the benefit of parties outside the government. Fiduciary funds are not reflected in the government-wide financial statements because the resources of those funds are not available to support the County’s own programs. The accounting used for fiduciary funds is much like that used for proprietary funds. The basic fiduciary fund financial statements can be found on pages 33 to 34 of this report.

Page 7

COUNTY OF DANE, WISCONSIN

MANAGEMENT’S DISCUSSION AND ANALYSIS (cont.) (UNAUDITED)

For Year Ended December 31, 2012 OVERVIEW OF THE FINANCIAL STATEMENTS (cont.)

Notes to the Financial Statements – The notes provide additional information that is essential to a full understanding of the data provided in the government-wide and fund financial statements. The notes to the financial statements can be found on pages 37 to 96 of this report. Other Information – In addition to the basic financial statements and accompanying notes, required supplementary information presents a schedule of funding progress for the other postemployment benefits plan, as well as, a budgetary comparison schedule for the General Fund and the Human Services Special Revenue Fund to demonstrate compliance with the budget. These schedules can be found on pages 98 to 100 of this report. The combining statements referred to earlier in connection with nonmajor governmental funds, proprietary funds, internal service funds and other information related to the individual funds are presented immediately following the required supplementary information. Combining and individual statements and schedules can be found on pages 101 to 134 of this report. FINANCIAL ANALYSIS OF THE COUNTY AS A WHOLE

An analysis of the County’s financial position begins with a review of the Statement of Net Position and the Statement of Revenues, Expenses and Changes in Net Position. These two statements report the County’s net position and changes therein. It should be noted that the financial position can also be affected by non-financial factors, including economic conditions, population growth and new regulations. As noted earlier, net position may serve over time as a useful indicator of government’s financial position. In the case of the County of Dane, assets exceeded liabilities by $459,074,494 as of December 31, 2012. The largest portion of the County’s net position reflects its investments in capital assets (e.g., land, building, equipment, improvements, construction in progress and infrastructure), less any debt used to acquire those assets that is still outstanding. The County uses these capital assets to provide service to citizens; consequently these assets are not available for future spending. Although the County’s investment in its capital assets is reported net of related debt, it should be noted that the resources needed to repay this debt must be provided from other sources, since the capital assets themselves cannot be used to liquidate these liabilities. An additional portion of the County’s net position (approximately 3.0%) represents resources that are subject to external restrictions on how they may be used.

Page 8

COUNTY OF DANE, WISCONSIN

MANAGEMENT’S DISCUSSION AND ANALYSIS (cont.) (UNAUDITED)

For Year Ended December 31, 2012 FINANCIAL ANALYSIS OF THE COUNTY AS A WHOLE (cont.)

COUNTY OF DANE’S NET POSITION

(in millions)

Government ActivitiesBusiness-type

Activities

Total

2011

2012

2011

2012

2011

2012 Current and Other Assets $ 235.1 $ 236.9 $ 71.0 $ 68.5 $ 306.1 $ 305.4Capital Assets 347.4 361.8 299.7 302.7 647.1 664.5

Total Assets 582.5 598.7 370.7 371.2 953.2 969.9

Long-term Liabilities 219.9 229.8 98.7 97.6 318.6 327.4Other Liabilities 170.8 169.9 10.5 13.5 181.3 183.4

Total Liabilities 390.7 399.7 109.2 111.2 499.9 510.9

Net Position:

Net investment in capital assets 227.0

231.7

224.0 230.4 451.1 462.1

Restricted 9.9 11.4 0.2 2.6 10.1 14.0Unrestricted (deficit) (45.1) (44.1) 37.2 27.1 (7.9) (17.0) Total Net Position $ 191.8 $ 199.0 $ 261.5 $ 260.1 $ 453.3 $ 459.1

Note: Some amounts throughout the Management’s Discussion and Analysis may be different due to rounding. Overall net position for the County increased by $5.8 million. The increase in the net investment in capital assets of $11 million was combined with a decrease in unrestricted net position of $9.1 million. Analysis of the County’s Operations – The following table provides a summary of the County’s operations for the year ended December 31, 2012. Governmental activities increased the County of Dane’s net position by $7.1 million. Business-type activities decreased the County’s net position by $1.4 million. The majority of the governmental activities increase was due to a $6.7 million positive change in the general fund’s fund balance. The majority of the business-type decrease was due to a $1.8 million decrease in net position for the sanitary landfill fund, primarily due to additional expenses for depreciation and future closure costs taken in the current year, and a $4.0 million decrease in the highway fund which more than offset the increase of $4.7 million in the airport fund.

Page 9

COUNTY OF DANE, WISCONSIN

MANAGEMENT’S DISCUSSION AND ANALYSIS (cont.) (UNAUDITED)

For Year Ended December 31, 2012 FINANCIAL ANALYSIS OF THE COUNTY AS A WHOLE (cont.)

COUNTY OF DANE CONDENSED STATEMENT OF REVENUES,

EXPENSES AND CHANGES IN NET POSITION (in millions)

Government ActivitiesBusiness-type

Activities Total Primary

Government

Revenues: 2011 2012 2011 2012 2011 2012 Program Revenues

Charges for services $ 33.5 $ 36.6 $ 47.3 $ 49.4 $ 80.8 $ 86.0Operating grants 189.8 191.3 5.6 6.4 195.4 197.7Capital grants 8.4 5.7 3.8 6.6 12.2 12.3

General Revenues: Property taxes 127.4 132.3 5.5 6.2 132.9 138.5Sales taxes 43.7 45.1 - - 43.7 45.1Other taxes 6.6 6.5 - - 6.6 6.5Intergovernmental 5.8 5.3 - - 5.8 5.3Public gifts & grants 0.2 0.2 - - 0.2 0.2Investment income 1.0 0.5 0.2 0.1 1.2 0.6Gain on the sale of assets 0.1 - 0.2 0.7 0.3 0.7Miscellaneous 4.5 0.6 0.2 - 4.7 0.6

Total Revenues 421.0 424.1 62.8 69.4 483.8 493.5

Expenses: General Government 29.1 31.1 - - 29.1 31.1Health and human services 226.2 235.8 - - 226.2 235.8Public safety & criminal justice 102.3 106.9 - - 102.3 106.9Public works 5.7 6.7 - - 5.7 6.7Culture, education & recreation 21.9 24.7 - - 21.9 24.7Conservation & econ. devel. 8.5 6.5 - - 8.5 6.5Interest & fiscal charges 4.9 5.0 - - 4.9 5.0Highway - - 18.5 18.5 18.5 18.5Airport - - 22.3 21.7 22.3 21.7Badger Prairie Health Care Cnt. - - 18.7 18.9 18.7 18.9Sanitary Landfill - - 11.4 9.2 11.4 9.2Other non-major proprietary funds - - 2.2 2.8 2.2 2.8

Total Expenses 398.6 416.7 73.1 71.1 471.7 487.8 Increase (decrease) in net position before transfers

22.4 7.4 (10.3) (1.7) 12.1 5.7

Transfers (7.5) (0.3) 7.5 0.3 - -Change in net position 14.9 7.1 (2.8) (1.4) 12.1 5.7Net Position - January 1 176.9 191.8 264.3 261.5 441.2 453.3Net Position - December 31 $ 191.8 198.9 $ 261.5 $ 260.1 $ 453.3 $ 459.0

Page 10

COUNTY OF DANE, WISCONSIN

MANAGEMENT’S DISCUSSION AND ANALYSIS (cont.)

(UNAUDITED) For Year Ended December 31, 2012

FINANCIAL ANALYSIS OF THE COUNTY AS A WHOLE (cont.)

Governmental Activities Total revenues increased by 0.7%, and total expenses increased by 4.5% in the Governmental Activities of the County of Dane. After transfers, total Governmental Activities net position increased by $7.1 million. Operating grants for Health and Human Services increased by $6.1 million and charges for services increased by $0.5 million, while expenses in this category increased by $9.5 million. Net expenses and revenues for Human Services programs increased by $4.7 million as a result. Operating grants and contributions in the General Government program areas decreased by $0.3 million in 2012. Property tax revenue increased by $4.9 million, and sales taxes increased by $1.3 million. Capital grants in the public works area increased by $1.1 million and decreased by $5.0 million in conservation and economic development. The increase in public works represents changes in aid for highway construction, and the change in conservation and economic development represents a one-time impact fee payment from American Transmission Company made in 2011. Business-type Activities Total revenues for Business-type Activities increased by 10.5% while expenses decreased by 2.7%. Revenue for charges for services increased by 4.4%. While charges for services at the airport increased by $1.4 million, charges for services at the landfill also increased by $0.2 million and by $0.2 million in the methane gas fund. The increase at the airport is primarily due to increased parking revenue. The increase at the landfill is due to increased tipping fees. The increase in the methane fund is due to higher production of electricity.

Page 11

COUNTY OF DANE, WISCONSIN

MANAGEMENT’S DISCUSSION AND ANALYSIS (cont.) (UNAUDITED)

For Year Ended December 31, 2012 FINANCIAL ANALYSIS OF THE COUNTY AS A WHOLE (cont.)

Charges for Service8.6%

Operating Grants & Contributions

45.1%

Capital Grants & Contributions

1.3%

Property Taxes31.2

Other2.0%

Sales Taxes10.6%

Intergovernmental, Non-restricted

1.2%

Revenue by Source-Gov. Activities

$-

$50,000,000

$100,000,000

$150,000,000

$200,000,000

$250,000,000

General Government

Health and Human Services

Public Safety & Criminal Justice

Public Works Culture, Education & Recreation

Conservation & Econ. Devel.

Interest & Fiscal Charges

Expenses & Program Revenues-Governmental Activities

Expenses Program Revenues

Page 12

COUNTY OF DANE, WISCONSIN

MANAGEMENT’S DISCUSSION AND ANALYSIS (cont.) (UNAUDITED)

For Year Ended December 31, 2012 FINANCIAL ANALYSIS OF THE COUNTY AS A WHOLE (cont.)

$-

$5,000,000

$10,000,000

$15,000,000

$20,000,000

$25,000,000

$30,000,000

Airport Highway Sanitary Landfill Badger Prairie Health Center

Expenses & Program Revenues-Business-type Activities

Expenses Program Revenues

Charges for Service71.2%

Capital Grants & Contributions

9.5%

Operating Grants & Contributions

9.2%

Property Taxes8.9%

Investment Income0.1%

Misc (Gain on Sale of Assets)

1.1%

Revenues by Source-Business-type Activities

Page 13

COUNTY OF DANE, WISCONSIN

MANAGEMENT’S DISCUSSION AND ANALYSIS (cont.) (UNAUDITED)

For Year Ended December 31, 2012 FINANCIAL ANALYSIS OF THE GOVERNMENT’S FUNDS

Governmental Funds The focus of the County of Dane’s governmental funds is to provide information on near-term inflows, outflows, and balances of spendable resources. Such information is useful in assessing the County’s financing requirements. In particular, unassigned fund balance may serve as a useful measure of the government’s net resources available for spending at the end of the fiscal year. At the end of the current fiscal year, the County of Dane’s governmental funds reported combined ending fund balances of $51,361,681. Approximately 36.8% of this total amount, $18,882,265 constitutes unassigned fund balance. The remainder of the fund balance is nonspendable, restricted or assigned to indicate that it is not available for new spending. Nonspendable items include amounts 1) for inventories and prepaid items ($155,429), 2) delinquent property taxes ($7,355,135) and 3) long-term receivables/advances ($776,886). Restricted items total $21,130,364, 85.9% of this category, $18,158,953 is for funds restricted for Capital Projects. Assigned items total $3,061,602. General Fund The County’s General Fund is used to account for the preponderance of the County’s operations with the exception of the Human Services Department and the business type activities recorded in other major funds. Operations included in the General Fund include the departments of Administration, Parks, Land Conservation, Family Court Counseling, Family Court Commissioner, Emergency Management, Public Safety Communications, Corporation Counsel, Planning and Development and Public Works. This fund also accounts for the activity of the elected officers of the County Executive, the Sheriff’s Office, the Clerk of Courts, the County Treasurer, the Register of Deeds, and the County Clerk. The General fund balance increased $6.7 million from 2011 to 2012. This was primarily due to sales tax revenue exceeding budget and human service revenues from the state exceeding budget and thereby reducing its reliance upon the general fund. Human Services The Human Services Fund is used to account for the revenues and expenditures associated with the Human Services Department. Human Services is the largest department within County government and receives a wide variety of intergovernmental revenues. General purpose revenue is transferred annually from the General Fund to the Human Services Fund to supplement these intergovernmental revenues in support of Human Service Department services. The Human Services Fund balance decreased $48,524 from 2011.

Page 14

COUNTY OF DANE, WISCONSIN

MANAGEMENT’S DISCUSSION AND ANALYSIS (cont.) (UNAUDITED)

For Year Ended December 31, 2012 FINANCIAL ANALYSIS OF THE GOVERNMENT’S FUNDS (cont.) Governmental Funds (cont.) Debt Service The Debt Service Fund accounts for the accumulation of resources for, and the payment of, general long-term debt principal, interest and related costs. The Debt Service fund balance decreased $183,986 from 2011. Capital Projects The capital projects fund is used to account for financial resources to be used for the acquisition or construction of major capital facilities (other than those financed by proprietary funds). Included in this report is the Dane County Conservation capital projects fund, the Land and Water Legacy Fund and general capital projects fund. The Capital Projects Fund fund balance decreased by $5,355,099 from 2011. This decrease is due to the spending of bond proceeds received in the prior year for a variety of capital projects in 2012. Proprietary Funds The County of Dane’s proprietary funds provide the same type of information found in the government-wide financial statements, but in more detail. Airport The Airport Fund is used to account for the enterprises of the Dane County Regional Airport. Airport operations are not supported with general purpose revenue. The Airport Net Position increased $4,670,455 from 2011. Highway The Highway Fund is used to account for the operations of the Dane County Highway Department. The Highway Department maintains County highways using state highway aids and general purpose revenue. However, the Highway Department also maintains state and town roadways on a contract basis with the State of Wisconsin and other local governments. The Highway Department is reimbursed for these services from the State and local governments. The Highway Fund Net Position decreased $3,992,247 from 2011. Sanitary Landfill The Solid Waste Fund is used to account for the operations of the County landfill and recycling operations. These operations are not supported with general purpose revenue from the County. The Sanitary Landfill Net Position decreased $1,867,094 from 2011. This decrease was due primarily to charges for long-term care and closure of the landfill and increased accumulated depreciation. Badger Prairie Health Care Center The BPHCC fund is used to account for the operations of the County nursing home. This operation receives approximately 1/2 of its operating revenue from a transfer of general purpose revenue from the General Fund. Badger Prairie Health Care Center Net Position decreased $105,939 from 2011.

Page 15

COUNTY OF DANE, WISCONSIN

MANAGEMENT’S DISCUSSION AND ANALYSIS (cont.) (UNAUDITED)

For Year Ended December 31, 2012 GENERAL FUND BUDGETARY HIGHLIGHTS

The final amended General Fund budget had total appropriations of $5,185,562 more than the original budget. The total original appropriations, including those for transfers out, were $211,695,098, while the final appropriations were $216,880,660. Of the difference, $4,037,073 was related to the appropriation carry forwards for projects not completed by year-end. The remaining increase of approximately $1,148,489 was for various items legislated by County Board of Supervisors throughout the year. The increase in appropriations was budgeted from available fund balance or additional funding sources such as grant funds. CAPITAL ASSETS

At the end of 2012, the County had invested a total of $664,509,318 in capital assets (net of accumulated depreciation). This investment in capital assets includes land, land improvements, buildings, machinery and equipment, intangibles, infrastructure and construction work in progress. Major capital asset events during the current fiscal year included the following: The decrease in land improvements was impacted by the depreciation of landfill related improvements. The increase in construction work in progress is due primarily to the Public Safety Communications Interoperable Radio System of $6.7 million and various Airport projects including a new Maintenance Building and development at Anderson Street and International Lane.

CAPITAL ASSETS AT YEAR-END NET OF ACCUMULATED DEPRECIATION

(in millions)

Governmental

Activities Business-Type

Activities

Total 2011 2012 2011 2012 2011 2012

Land $ 106.17 $ 107.92 $ 28.64 $ 28.54 $ 134.81 $ 136.48Land Improvements 41.27 42.33 109.17 104.50 150.44 146.82Buildings 118.26 116.22 134.59 135.04 252.85 251.26Machinery & Equipment 14.05 16.25 24.63 26.35 38.68 42.60Infrastructure 57.34 61.87 - - 57.34 61.87Construction in Progress 9.99 16.89 2.69 8.28 12.68 25.17Intangibles 0.35 0.31 - 0.02 0.35 0.33 Total $ 347.43 $ 361.78 $ 299.72 $ 302.73 $ 647.15 $ 664.51 Additional information on the County of Dane’s capital assets can be found in note IV.D. of this report.

Page 16

COUNTY OF DANE, WISCONSIN

MANAGEMENT’S DISCUSSION AND ANALYSIS (cont.) (UNAUDITED)

For Year Ended December 31, 2012 LONG-TERM DEBT

During 2012, the County issued $39.6 million in bonds and notes and retired debt of $41.9 million resulting in a decrease of $2.3 million in outstanding bonds payable at the end of 2012. This results in a per capita general obligation debt of $483.51/person. Of the bonded debt, $164.96 million is to be repaid with general property taxes. Under Wisconsin State Statutes, Chapter 67, Dane County’s aggregate indebtedness may not exceed 5% of the equalized value of taxable property located in the County. The net amount of debt that is applicable to the statutory limit is $237,670,000, which is considerably below the maximum of $2,475,591,000. The general obligation notes and bonds issued in 2012 received an Aa1 rating from Moody’s Investors Service and an AA+ from Fitch Ratings.

COUNTY OF DANE’S OUTSTANDING DEBT GENERAL OBLIGATION BONDS (in millions)

Governmental

Activities Business-Type

Activities

Total

Percent 2011 2012 2011 2012 2011 2012 Change

General Obligation Debt Outstanding $ 164.3 $ 165.0 $ 75.7 $ 72.7 $ 240.0 $ 237.7 (0.96%)

Additional information on the County of Dane’s long-term debt can be found in footnote IV.F. of this report. REQUESTS FOR INFORMATION

The financial report is designed to provide our citizens, customers, investors and creditors with general overview of the County’s finances. If you have questions about this report or need any additional information, contact the Controller’s Office, Attn: Charles Hicklin, at Department of Administration, Controller Division, 210 Martin Luther King Jr. Boulevard, Room 426, Madison, Wisconsin, 53703, call 608.266.4109, or e-mail [email protected]. General information relating to the County of Dane, Wisconsin, can be found at the County’s website, www.co.dane.wi.us.

Business-Governmental type Component

Activities Activities Totals Units

ASSETS Cash and investments 26,547,293$ 50,481,707$ 77,029,000$ 5,406,919$ Receivables (net of allowance for uncollectibles) Taxes 136,630,309 6,530,354 143,160,663 - Delinquent taxes 14,423,466 - 14,423,466 - Accounts 15,743,649 3,295,784 19,039,433 762,438 Loans 9,064,333 - 9,064,333 137,442 Other 1,503 - 1,503 - Due from other governmental units 23,588,425 2,684,079 26,272,504 36,140 Internal balances 7,991,578 (7,991,578) - - Inventories 7,100 1,589,490 1,596,590 129,506 Prepaid items 148,329 1,595 149,924 24,790 Deposits 50,000 - 50,000 - Restricted Assets Cash and investments - 11,619,711 11,619,711 748,966 Deposits with Wisconsin Municipal Mutual Insurance Company 2,359,760 - 2,359,760 - Other assets 350,298 297,838 648,136 - Capital Assets Land 107,921,129 28,921,234 136,842,363 755,352 Construction in progress 16,888,245 8,281,384 25,169,629 - Land Improvements (non-depreciable) 33,128,006 - 33,128,006 - Land Improvements (depreciable) 16,751,073 185,377,331 202,128,404 536,250 Buildings 176,427,094 170,183,643 346,610,737 6,374,244 Machinery and equipment 35,681,821 52,203,319 87,885,140 303,361

Primary Government

COUNTY OF DANE

STATEMENT OF NET POSITIONAs of December 31, 2012

y q p Intangibles 1,093,212 122,972 1,216,184 - Infrastructure 120,731,238 - 120,731,238 - Less: Accumulated depreciation/amortization (146,843,252) (142,359,131) (289,202,383) (6,377,220)

Total Assets 598,684,609 371,239,732 969,924,341 8,838,188

LIABILITIESAccounts payable 11,794,383 2,422,161 14,216,544 145,283 Accrued payroll and payroll taxes 7,728,689 1,575,829 9,304,518 - Other accrued liabilities and deposits 8,004,384 269,946 8,274,330 81,640 Due to other governmental units 5,696,706 2,711,120 8,407,826 - Unearned revenue 136,664,355 6,534,420 143,198,775 15,533 Noncurrent Liabilities Due within one year 32,743,603 12,511,114 45,254,717 22,821 Due in more than one year 197,063,878 85,129,259 282,193,137 376,258

Total Liabilities 399,695,998 111,153,849 510,849,847 641,535

NET POSITIONNet investment in capital assets 231,674,572 230,376,353 462,050,925 1,591,987 Restricted for: General government 764,504 - 764,504 - Culture, education and recreation 23,718 - 23,718 1,776,656 Conservation and economic development 10,342,621 - 10,342,621 - Public works 207,853 - 207,853 - Health and human services 42,618 - 42,618 - Capital projects - 2,581,540 2,581,540 - Housing programs - - - 1,204,567 Unrestricted (deficit) (44,067,275) 27,127,990 (16,939,285) 3,623,443

TOTAL NET POSITION 198,988,611$ 260,085,883$ 459,074,494$ 8,196,653$

See accompanying notes to financial statements.Page 17

Program Revenues

Operating CapitalCharges for Grants and Grants and

Functions/Programs Expenses Services Contributions Contributions

Primary Government Governmental Activities General government 31,096,646$ 7,841,657$ 6,329,987$ 5,565$ Health and human services 235,780,402 3,731,562 175,266,523 - Public safety and criminal justice 106,861,775 10,808,278 6,535,259 1,045,818 Public works 6,739,324 1,019,528 987 3,876,067 Culture, education and recreation 24,729,980 10,886,324 991,803 530,509 Conservation and economic development 6,487,866 2,306,414 2,168,696 86,500 Interest and fiscal charges 5,046,416 - - 198,416

Total Governmental Activities 416,742,409 36,593,763 191,293,255 5,742,875

Business-type Activities Airport 21,713,544 19,735,917 - 6,614,858 Highway 18,540,047 9,333,870 4,904,133 - Sanitary landfill 9,166,009 7,416,458 23,908 - Badger Prairie Health Care Center 18,927,883 8,008,471 1,432,470 - Printing and services 1,284,923 1,165,789 - - Methane gas 1,471,247 3,717,889 - -

Total Business-type Activities 71,103,653 49,378,394 6,360,511 6,614,858

Total Primary Government 487,846,062$ 85,972,157$ 197,653,766$ 12,357,733$

Component Units

Henry Vilas Park Zoological Society, Inc. 2,048,794 866,661 1,634,873 - Dane County Housing Authority 9,924,007 286,632 9,523,959 -

Total Component Units 11,972,801$ 1,153,293$ 11,158,832$ -$

General Revenues Taxes Property taxes, levied for general purposes Property taxes, levied for debt service Property taxes, levied for highway purposes Sales taxes Other taxes Intergovernmental revenues not restricted to specific programs Public gifts and/or grants Investment income Gain on the sale of assets MiscellaneousTransfers

Total General Revenues and Transfers

Change in Net Position

NET POSITION - Beginning

NET POSITION - ENDING

COUNTY OF DANE

STATEMENT OF ACTIVITIES

For the Year Ended December 31, 2012

See accompanying notes to financial statements.Page 18

Changes in Net Position

Governmental Business-type Component Activities Activities Totals Units

(16,919,437)$ -$ (16,919,437)$ -$ (56,782,317) - (56,782,317) - (88,472,420) - (88,472,420) - (1,842,742) - (1,842,742) -

(12,321,344) - (12,321,344) - (1,926,256) - (1,926,256) - (4,848,000) - (4,848,000) -

(183,112,516) - (183,112,516) -

- 4,637,231 4,637,231 - - (4,302,044) (4,302,044) - - (1,725,643) (1,725,643) - - (9,486,942) (9,486,942) - - (119,134) (119,134) - - 2,246,642 2,246,642 -

- (8,749,890) (8,749,890) -

(183,112,516) (8,749,890) (191,862,406) -

- - - 452,740 - - - (113,416)

117,175,243 - 117,175,243 - 15,141,308 - 15,141,308 -

- 6,161,400 6,161,400 - 45,062,964 - 45,062,964 - 6,518,628 - 6,518,628 -

5,349,911 - 5,349,911 - 229,579 - 229,579 - 484,812 100,516 585,328 43,579

- 757,483 757,483 2,500 641,312 - 641,312 69,425

(311,387) 311,387 - -

190,292,370 7,330,786 197,623,156 115,504

7,179,854 (1,419,104) 5,760,750 454,828

191,808,757 261,504,987 453,313,744 7,741,825

198,988,611$ 260,085,883$ 459,074,494$ 8,196,653$

Primary Government

Net (Expense) Revenue and

See accompanying notes to financial statements.Page 19

Non-major TotalHuman Capital Governmental Governmental

General Services Debt Service Projects Funds Funds

ASSETSCash and investments 4,611,212$ 789,288$ 868,698$ 18,535,037$ 1,742,073$ 26,546,308$ Receivables Taxes 110,191,416 - 16,626,516 - 9,812,377 136,630,309 Delinquent taxes 14,423,466 - - - - 14,423,466 Accounts 2,881,421 11,252,053 - 1,143,957 2,024 15,279,455 Loans 82,599 - - - 8,981,734 9,064,333 Other 1,503 - - - - 1,503

Due from other governments 10,899,402 10,085,745 - 586,500 2,016,175 23,587,822 Due from other funds 11,194,524 - - - 11,194,524 Advance to other funds - - - - 693,542 693,542 Inventories 7,100 - - - - 7,100 Prepaid items 144,835 2,831 - 663 - 148,329

Total Assets 154,437,478 22,129,917 17,495,214 20,266,157 23,247,925 237,576,691

LIABILITIES AND FUND BALANCESLiabilities Accounts payable 1,988,037 7,498,334 18,391 1,912,640 240,113 11,657,515 Accrued payroll and payroll taxes 5,510,073 1,583,867 - - 543,666 7,637,606 Other accrued liabilities and deposits 1,312,590 - - - - 1,312,590 Due to other governments 1,526,107 3,637,089 - 154,975 368,326 5,686,497 Due to other funds 52,219 9,365,178 495,877 4,880 1,041,855 10,960,009 Deferred revenue 113,806,120 - 16,626,516 34,046 18,494,111 148,960,793

Total Liabilities 124,195,146 22,084,468 17,140,784 2,106,541 20,688,071 186,215,010

Fund Balances Nonspendable 8,283,956 2,831 - 663 - 8,287,450 Restricted 945 42,618 354,430 18,158,953 2,573,418 21,130,364 Assigned 3,061,602 - - - - 3,061,602 Unassigned (deficit) 18,895,829 - - - (13,564) 18,882,265

Total Fund Balances 30,242,332 45,449 354,430 18,159,616 2,559,854 51,361,681

Total Liabilities and Fund Balances 154,437,478$ 22,129,917$ 17,495,214$ 20,266,157$ 23,247,925$

Amounts reported for governmental activities in the statement of net position are different because:

Capital assets used in governmental funds are not financial resources and, therefore, are not reported in the funds. See Note II.A. 360,396,311

Some receivables that are not currently available are reported as deferred revenue in the fund financial

statements but are recognized as revenue when earned in the government-wide statements. See Note IV. B. 12,296,438

Internal service funds are reported in the statement of net position as governmental activities. 4,295,752

Some liabilities, including long-term debt, are not due and payable in the current period and, therefore, are not

reported in the funds. See Note II.A. (229,361,571)

NET POSITION OF GOVERNMENTAL ACTIVITIES 198,988,611$

COUNTY OF DANE

BALANCE SHEET - GOVERNMENTAL FUNDSAs of December 31, 2012

See accompanying notes to financial statements.Page 20

Non-major TotalHuman Capital Governmental Governmental

General Services Debt Service Projects Funds Funds

REVENUES Taxes 160,377,213$ -$ 15,141,308$ -$ 9,261,797$ 184,780,318$ Intergovernmental 29,271,594 176,186,945 181,744 2,276,644 1,951,331 209,868,258 Public charges for services 17,652,382 197,794 - 88,448 1,531,586 19,470,210 Fines, forfeitures and penalties 1,946,929 - - - - 1,946,929 Licenses and permits 796,706 - - - - 796,706 Investment income (loss) 451,007 1,507 (6,545) 19,097 (2,868) 462,198 Miscellaneous 1,862,671 2,618,784 300,547 5,158 158,722 4,945,882

Total Revenues 212,358,502 179,005,030 15,617,054 2,389,347 12,900,568 422,270,501

EXPENDITURES Current General government 26,366,304 - - - 348,518 26,714,822 Health and human services 452,233 229,458,904 - - 4,998,676 234,909,813 Public safety and criminal justice 97,801,552 - - - - 97,801,552 Public works 772,700 - - - 184,441 957,141 Culture, education and recreation 15,524,095 - - - 4,343,441 19,867,536 Conservation and economic development 4,242,627 - - - 2,370,583 6,613,210 Capital Outlay 147,169 - - 21,716,410 - 21,863,579 Debt Service Principal retirement - - 17,694,289 - - 17,694,289 Interest and fees - - 5,194,108 - - 5,194,108

Total Expenditures 145,306,680 229,458,904 22,888,397 21,716,410 12,245,659 431,616,050

Excess (deficiency) of revenues over (under) expenditures 67,051,822 (50,453,874) (7,271,343) (19,327,063) 654,909 (9,345,549)

OTHER FINANCING SOURCES (USES) General obligation debt issued 4,748,000 - 58,235 13,918,515 - 18,724,750 Refunding bonds issued - - 14,450,000 - - 14,450,000 Payments to refunded bond escrow agent - - (15,701,200) - - (15,701,200) Debt premium - - 2,005,875 - - 2,005,875 Transfers in 3,158,877 50,685,946 6,344,108 72,546 63,920 60,325,397 Transfers out (68,193,247) (280,596) (69,661) (19,097) (172,365) (68,734,966)

Total Other Financing Sources (Uses) (60,286,370) 50,405,350 7,087,357 13,971,964 (108,445) 11,069,856

Net Change in Fund Balance 6,765,452 (48,524) (183,986) (5,355,099) 546,464 1,724,307

FUND BALANCES - Beginning 23,476,880 93,973 538,416 23,514,715 2,013,390 49,637,374

FUND BALANCES - ENDING 30,242,332$ 45,449$ 354,430$ 18,159,616$ 2,559,854$ 51,361,681$

COUNTY OF DANE

STATEMENT OF REVENUES, EXPENDITURESAND CHANGES IN FUND BALANCES - GOVERNMENTAL FUNDS

For the Year Ended December 31, 2012

See accompanying notes to financial statements.Page 21

COUNTY OF DANE

RECONCILIATION OF THE STATEMENT OF REVENUES, EXPENDITURES AND CHANGES IN FUND BALANCES OF GOVERNMENTAL FUNDS

TO THE STATEMENT OF ACTIVITIESFor the Year Ended December 31, 2012

Net change in fund balances - total governmental funds 1,724,307$

Amounts reported for governmental activities in the statement of activities are different because:

Governmental funds report capital outlays as expenditures. However, in the statement of net position the cost of these assets is capitalized and they are depreciated over their estimated useful lives with depreciation expense reported in the statement of activities. Capital outlay is reported as an expenditure in the fund financial statements but is capitalized in the government-wide financial statements 21,863,579 Less: Some items are reported as capital outlay but are not capitalized (5,668,685) Depreciation is reported in the government-wide statements - less internal service funds (10,601,814) Capital contributions reported in the government-wide statements 3,563,383 Infrastructure financed by the highway fund 8,121,188

Net effect of various miscellaneous transactions involving capital assets (i.e., sales, trade-ins) is to decrease net position. (2,862,810)

Receivables not currently available are reported as deferred revenue in the fund financial statements but are recognized as revenue when earned in the government-wide financial statements. (38,665)

Debt and lease proceeds provide current financial resources to governmental funds, but issuing these obligations increases long-term liabilities in the statement of net position. Repayment of principal is an expenditure in the governmental funds, but the repayment reduces long-term liabilities in the statement of net position. Refer to note II.B. (653,393)

Governmental funds report the effect of issuance costs, premiums, discounts, and similar items when debt is first issued, whereas these amounts are deferred and amortized in the statement of activities. (1,071,916)

Some expenses in the statement of activities do not require the use of current financial resources and, therefore, are not reported as expenditures in the governmental funds. Compensated absences (3,135,809) Other postemployment benefits (5,037,291) Disability benefits 10,615 Accrued interest on debt 94,933

Internal service funds are used by management to charge the costs of printing, workers compensation, liability insurance, employee benefits and food service costs to individual funds. The increase in net position of the internal service funds is reported with governmental activities. 872,232

CHANGE IN NET POSITION OF GOVERNMENTAL ACTIVITIES 7,179,854$

See accompanying notes to financial statements.Page 22

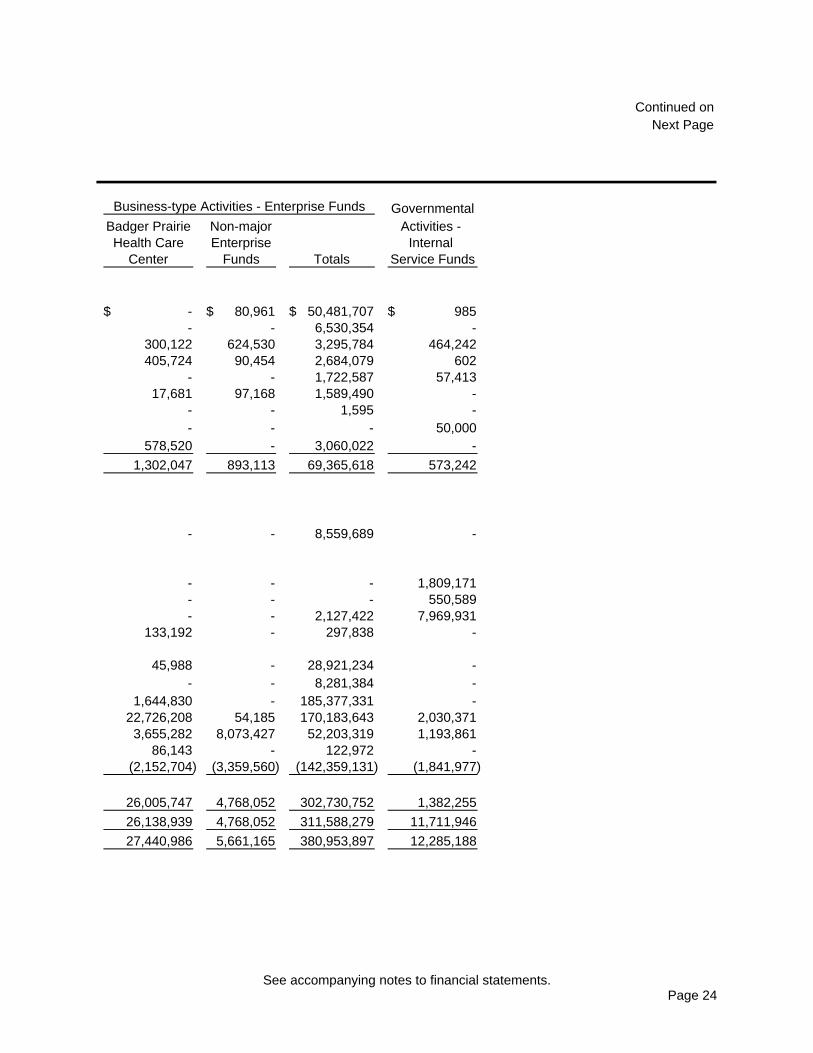

SanitaryAirport Highway Landfill

ASSETSCurrent Assets Cash and investments 50,400,695$ -$ 51$ Taxes receivable - 6,530,354 - Accounts receivable, net 1,931,923 2,243 436,966 Due from other governments - 1,876,379 311,522 Due from other funds - 112,083 1,610,504 Inventories - 1,474,641 - Prepaid items 1,595 - - Deposits - - -

Restricted cash and investments - 2,481,502 -

Total Current Assets 52,334,213 12,477,202 2,359,043

Noncurrent Assets Restricted Assets Cash and investments 100,038 - 8,459,651 Deposits with Wisconsin Municipal

Mutual Insurance Company Initial investment - - - Self-insured retention account - - - Advance to other funds - - 2,127,422 Other assets 164,646 - - Capital Assets Land 27,420,479 127,717 1,327,050 Construction in progress 5,954,792 2,010,344 316,248 Land improvements 166,258,329 491,771 16,982,401 Buildings 136,743,982 5,772,501 4,886,767 Machinery and equipment 11,600,850 19,734,137 9,139,623 Intangibles 36,829 - - Less: Accumulated depreciation/amortization (101,345,846) (13,295,951) (22,205,070)

Total Capital Assets (Net of Accumulated Depreciation/amortization) 246,669,415 14,840,519 10,447,019

Total Noncurrent Assets 246,934,099 14,840,519 21,034,092

Total Assets 299,268,312 27,317,721 23,393,135

COUNTY OF DANE

STATEMENT OF NET POSITION - PROPRIETARY FUNDSAs of December 31, 2012

Business-type Activities - Enterprise Funds

Page 23

Continued onNext Page

GovernmentalBadger Prairie Non-major Activities - Health Care Enterprise Internal

Center Funds Totals Service Funds

-$ 80,961$ 50,481,707$ 985$ - - 6,530,354 -

300,122 624,530 3,295,784 464,242 405,724 90,454 2,684,079 602

- - 1,722,587 57,413 17,681 97,168 1,589,490 -

- - 1,595 - - - - 50,000

578,520 - 3,060,022 -

1,302,047 893,113 69,365,618 573,242

- - 8,559,689 -

- - - 1,809,171 - - - 550,589 - - 2,127,422 7,969,931

133,192 - 297,838 -

45,988 - 28,921,234 - - - 8,281,384 -

1,644,830 - 185,377,331 - 22,726,208 54,185 170,183,643 2,030,371 3,655,282 8,073,427 52,203,319 1,193,861

86,143 - 122,972 - (2,152,704) (3,359,560) (142,359,131) (1,841,977)

26,005,747 4,768,052 302,730,752 1,382,255

26,138,939 4,768,052 311,588,279 11,711,946

27,440,986 5,661,165 380,953,897 12,285,188

Business-type Activities - Enterprise Funds

See accompanying notes to financial statements.Page 24

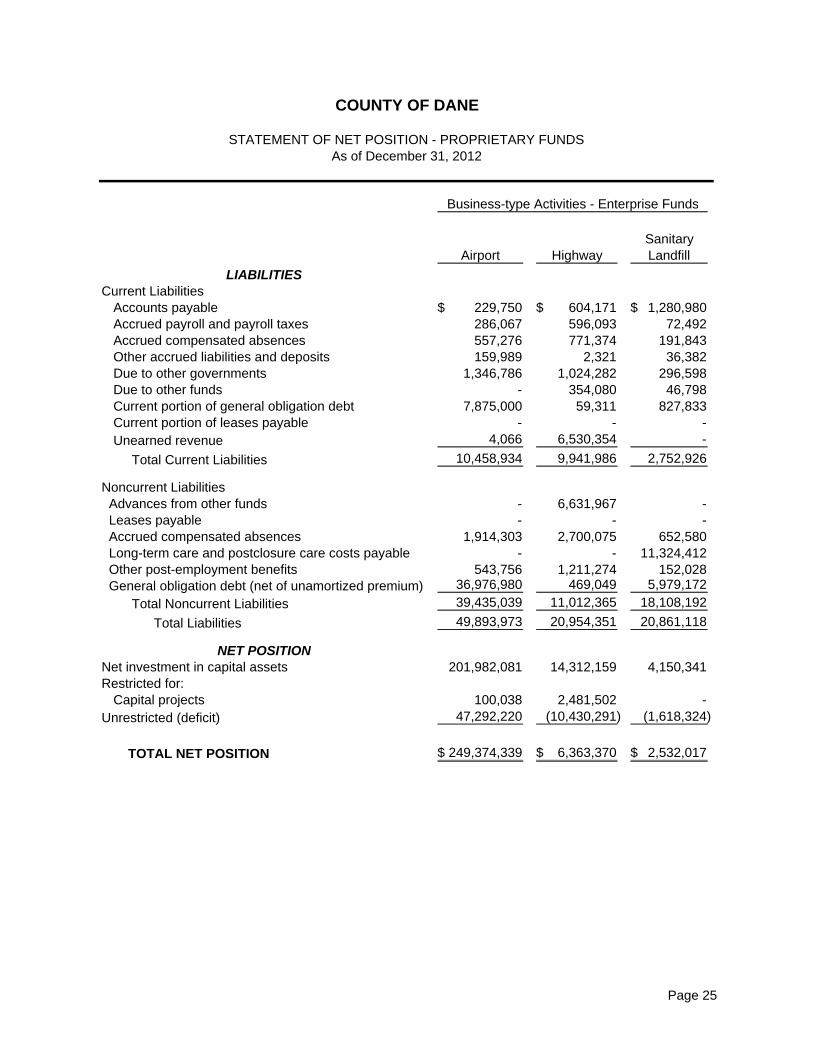

Sanitary Airport Highway Landfill

LIABILITIESCurrent Liabilities Accounts payable 229,750$ 604,171$ 1,280,980$ Accrued payroll and payroll taxes 286,067 596,093 72,492 Accrued compensated absences 557,276 771,374 191,843 Other accrued liabilities and deposits 159,989 2,321 36,382 Due to other governments 1,346,786 1,024,282 296,598 Due to other funds - 354,080 46,798 Current portion of general obligation debt 7,875,000 59,311 827,833 Current portion of leases payable - - - Unearned revenue 4,066 6,530,354 -

Total Current Liabilities 10,458,934 9,941,986 2,752,926

Noncurrent Liabilities Advances from other funds - 6,631,967 - Leases payable - - - Accrued compensated absences 1,914,303 2,700,075 652,580 Long-term care and postclosure care costs payable - - 11,324,412 Other post-employment benefits 543,756 1,211,274 152,028 General obligation debt (net of unamortized premium) 36,976,980 469,049 5,979,172

Total Noncurrent Liabilities 39,435,039 11,012,365 18,108,192

Total Liabilities 49,893,973 20,954,351 20,861,118

NET POSITION Net investment in capital assets 201,982,081 14,312,159 4,150,341 Restricted for: Capital projects 100,038 2,481,502 -

Unrestricted (deficit) 47,292,220 (10,430,291) (1,618,324)

TOTAL NET POSITION 249,374,339$ 6,363,370$ 2,532,017$

As of December 31, 2012

COUNTY OF DANE

STATEMENT OF NET POSITION - PROPRIETARY FUNDS

Business-type Activities - Enterprise Funds

Page 25

Continued FromPrevious Page

GovernmentalBadger Prairie Non-major Activities - Health Care Enterprise Internal

Center Funds Totals Service Funds

199,022$ 108,238$ 2,422,161$ 137,292$ 587,762 33,415 1,575,829 91,403 702,417 86,627 2,309,537 101,633 69,109 2,145 269,946 6,141,708 22,290 21,164 2,711,120 10,209

505 1,611,756 2,013,139 1,376 1,021,179 418,254 10,201,577 -

- - - 4,233 - - 6,534,420 -

2,602,284 2,281,599 28,037,729 6,487,854

2,640,322 556,159 9,828,448 962,447 - - - 9,336

1,792,906 216,494 7,276,358 357,538 - - 11,324,412 -

978,567 95,409 2,981,034 172,261 19,405,019 717,235 63,547,455 - 24,816,814 1,585,297 94,957,707 1,501,582

27,419,098 3,866,896 122,995,436 7,989,436

6,218,248 3,713,524 230,376,353 1,368,686

- - 2,581,540 - (6,196,360) (1,919,255) 27,127,990 2,927,066

21,888$ 1,794,269$ 260,085,883$ 4,295,752$

Business-type Activities - Enterprise Funds

See accompanying notes to financial statements.Page 26

Sanitary Airport Highway Landfill

OPERATING REVENUES Charges for services 11,496,712$ 9,285,693$ 7,333,446$ Intergovernmental charges for services - 3,342,088 - Parking and rental fees, tolls, and fines 8,239,205 - - Other - 48,177 83,012

Total Operating Revenues 19,735,917 12,675,958 7,416,458

OPERATING EXPENSES Personal services 6,215,206 10,311,105 1,699,884 Contractual services 2,368,191 742,892 751,943 Highway operations - 14,428,914 - Insurance services - - - Other 2,722,798 - 4,871,604 Depreciation 9,136,643 1,172,593 1,724,431

Total Operating Expenses 20,442,838 26,655,504 9,047,862

Operating Income (Loss) (706,921) (13,979,546) (1,631,404)

NONOPERATING REVENUES (EXPENSES) Taxes - 6,161,400 - Intergovernmental grants - 1,562,045 23,908 Investment income 69,925 4,385 24,667 Interest expense (1,491,658) (2,321) (118,147) Amortization of bond premium 261,591 - - Amortization of issuance costs and bond discount (40,639) (3,410) - Gain (loss) on sale or disposal of capital assets 12,029 - 745,454

Passenger facility charges 3,302,703 - -

Total Nonoperating Revenues (Expenses) 2,113,951 7,722,099 675,882

Income (Loss) Before Contributions and Transfers 1,407,030 (6,257,447) (955,522)