Embed Size (px)

Citation preview

Gas Regional InitiativeNorth West Region

-Gas Target Model

-BNetzA/Ofgem

Pre-Comitology MeetingBonn – 26 May 2011

2 Pre-Comitology MeetingBonn – 26 May 2011

Introduction

The Target Model (Madrid Conclusions) should:

provide support for FG and NC development to reach 2014 goal for completing the internal market

guidance also for Commission´s guidelines and Regional Initiative / Int. Projects

Internal market means: real choice, more cross-border trade, competitive prices…

provide an outlook on the EU gas market beyond that date

Starting Point is problems the gas market faces

3 Pre-Comitology MeetingBonn – 26 May 2011

Status of Project

Series of public workshops Vienna (December 3rd 2010) Bonn (February 22nd 2011) London (April 11th 2011) Brussels (June 28th 2011)

Stakeholder roundtables

Input from two external studies LECG Florence School of Regulation in co-operation with the Clingendael

Energy Programme and Wagner, Elbling & Co. MECO-S Model

CEER Paper is currently being drafted Final draft version to be presented at 4th workshop in Brussels

4 Pre-Comitology MeetingBonn – 26 May 2011

Setting the scene

?

Challenges: Internal market by 2014 Competition

EU 20-20-20, integration of RES more CCGT’s? Power to Gas?

Security of Supply N-1, Reverse Flow, access to diff. supply sourcesless domestic gas production more transit, new investment

LNGLNG

LNG

5 Pre-Comitology MeetingBonn – 26 May 2011

Problem Identification

3rd Package makes Entry-Exit systems obligatory: Large Entry-Exit Systems may reduce firm capacity

- Internal congestion may lead to cross-subsidisation Small Entry-Exit systems are not market capable

- problem of “pan-caking” for long-distance transport

For gas to flow where it is needed (price signal) there needs to be available capacity

Contractual Congestion identified as a major problem, but not for all IPs

Recital 21: “There is substantial contractual congestion in the gas networks.”

Definition: "contractual congestion" means a situation where the level of firm capacity demand exceeds the technical capacity, Art. 2(21) Reg. 715/2009

Commission proposal on Congestion Management

6 Pre-Comitology MeetingBonn – 26 May 2011

Status of market integration in the NW region

Significant indigenous gas production, but increasingly import dependent Decoupled entry-exit zones implemented in almost every country NBP most liquid hub (churn rate:14-15), Zeebrugge (4-6), TTF (3-4), NCG (2-3)

Gaspool (2-2,5), PEG Nord (1,5), trading volumes increasing Increasing price convergence but still price differences Significant infrastructure investments of European dimension (e.g. Northstream)

Source: European Commission

Traded Gas Volumes on European Hubs

0 GWh

20.000 GWh

40.000 GWh

60.000 GWh

80.000 GWh

100.000 GWh

120.000 GWh

140.000 GWh

Aug

06

Okt

06

Dez

06

Feb

07

Apr 0

7

Jun

07

Aug

07

Okt

07

Dez

07

Feb

08

Apr 0

8

Jun

08

Aug

08

Okt

08

Dez

08

Feb

09

Apr 0

9

Jun

09

Aug

09

Okt

09

Dez

09

Feb

10

Apr 1

0

Jun

10

Aug

10

Okt

10

Dez

10

Feb

11

PEG North TTF NCG GPL (bis 01.10.2009 MG H-Gas Norddtl.) ZEE

7 Pre-Comitology MeetingBonn – 26 May 2011

Overview of high level options

Enable Markets: Connecting markets:• Market areas (sub-) national or

cross-border• Full vertical integration• Merging of market areas

• Taking physical connection into account

• Trading region• Merger of entry-exit systems

• Taking physical connection into account

• Seperate end-user zones with national balancing system

• Bundling of capacity• Harmonisation of products, Gas-day• Explicit Auctions• Make capacity available via UIOLI and/or

Overbooking

• Market coupling• Day-ahead implicit auctions/allocation as

possible element to be tested in pilots first

LECG + MECO-S

LECG + MECO-S

only MECO-S

LECG + MECO-S

MECO-S & LECG

Improve effectiveness by realising economic pipeline investments

8 Pre-Comitology MeetingBonn – 26 May 2011

How to enable functioning wholesale markets?

Different pictures all over Europe call for different approaches which are not mutually exclusive

If a country is capable of establishing a functioning market itself the establishment of one (or two, based on C/B analysis) zone within this country is important (e.g. GB, Germany, France, Spain);

If a country is not capable of establishing a functioning market itself (e.g. due to lack of liquidity or size) - Cross-border market areas (full merger) is one solution; or - Accession to a larger, already functioning market; or- Trading Regions – a single cross-border zone for wholesale markets with

congestion-free interconnection to national end-user zones.

9 Pre-Comitology MeetingBonn – 26 May 2011

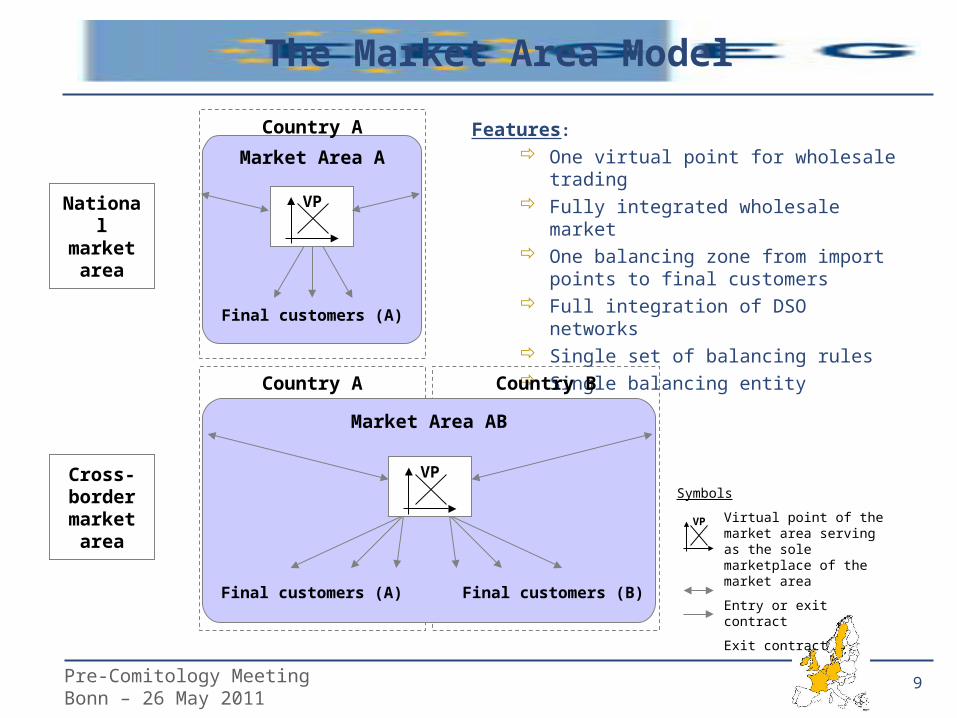

The Market Area Model

Features:

One virtual point for wholesale trading Fully integrated wholesale market One balancing zone from import points to

final customers Full integration of DSO networks Single set of balancing rules Single balancing entity

Symbols

Virtual point of the market area serving as the sole marketplace of the market area

Entry or exit contract

Exit contract

Market Area A

Country A

Country A Country B

Market Area AB

Cross-border market

area

National market

area

VP

Final customers (A) Final customers (B)

VP

Final customers (A)

VP

10 Pre-Comitology MeetingBonn – 26 May 2011

The Trading Region Model

Country A Country B

Trading Region AB

End userzone A

End userzone B

Final customers (A) Final customers (B)

VP

Legend and Symbols

End user zone = National balancing zone for national final customers, no matter the system (distribution or transmission) they are connected to

Trading Region AB = Cross-border entry/exit system including all nominated points on the transmission systems of countries A and B

Entry or exit contract

Exit contract

Virtual point of the trading region serving as the sole marketplace of the trading region and all attached end user zones. Shifting of gas between trading region and end user zone is done by nominating a virtual exit on the VP.

VP

Features: One virtual point for wholesale

trading Fully integrated wholesale market Trading region is basically kept free

of imbalances Final customers are balanced in

national end user zones that may reflect national specifics

End-user balancing may be done by national balancing entity

Congestion-free interconnection between trading region and end user zones through the common virtual point ( virtual exit to end user zone)

11 Pre-Comitology MeetingBonn – 26 May 2011

What needs to be done in all approaches?

Prerequisite for merging market areas and creating trading regions:

Absence or at least limited physical congestion

As soon as we are talking about cross-border integration the following issues have to be analysed

Entry / Exit Tariffication Redistribution of revenues and costs Alignment of regulatory framework Investments TSO as well as NRA cooperation

12 Pre-Comitology MeetingBonn – 26 May 2011

How to connect markets? Option 1

Option 1 : Explicit capacity allocation with continuous trading

Example for “overselling”: -Shipper A books 100 units of capacity -Shipper A nominates 50 units -TSO assumes that shipper A will not use remaining 50 units, TSO sells them day-ahead -Shipper B buys remaining 50 units off TSO-Shipper A has paid for 100, but only used 50 units Capacity hoarding is a bad deal! TSO takes a risk and needs appropriate incentives

Explicit auctions (CAM FG) Bundled Products No gate closure, no restriction

of renomination rights Overselling Interruptible Use It Or Lose It All capacity is financially firm

(not necessarily physically firm)

Has been effective in GB, but requires NRAs to set appropriate incentives

13 Pre-Comitology MeetingBonn – 26 May 2011

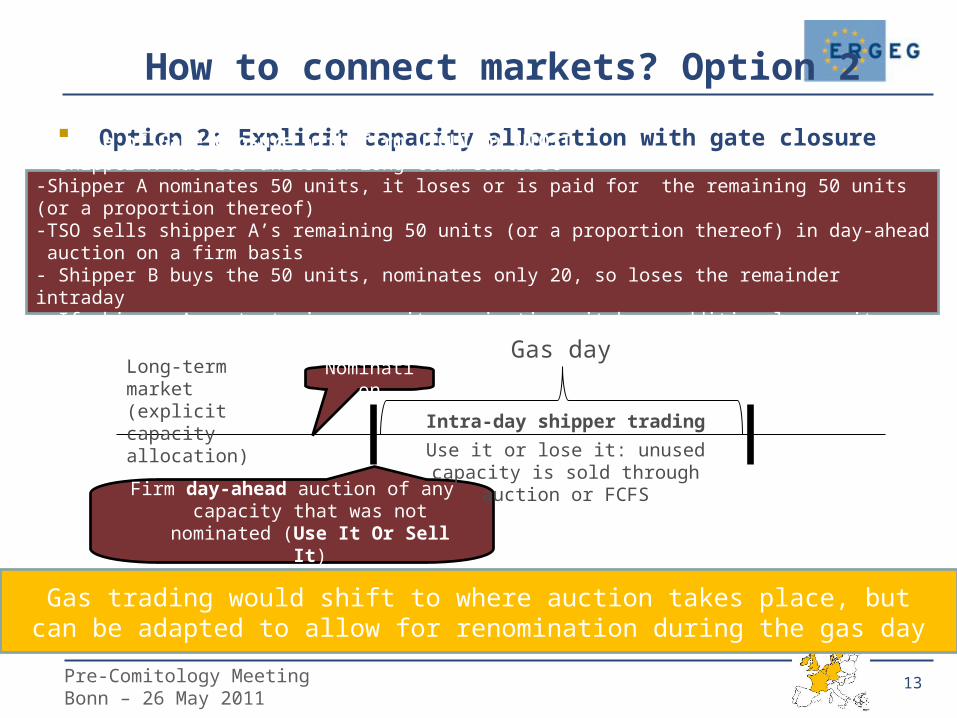

Option 2: Explicit capacity allocation with gate closure

How to connect markets? Option 2

Gas trading would shift to where auction takes place, butcan be adapted to allow for renomination during the gas day

Example of Gate Closure with firm UIOLI or UIOSI- Shipper A has 100 units in long-term contract-Shipper A nominates 50 units, it loses or is paid for the remaining 50 units (or a proportion thereof) -TSO sells shipper A’s remaining 50 units (or a proportion thereof) in day-ahead auction on a firm basis- Shipper B buys the 50 units, nominates only 20, so loses the remainder intraday - If shipper A wants to increase its nomination, it buys additional capacity intraday

Intra-day shipper trading

Long-term market (explicit capacity allocation)

Nomination

Firm day-ahead auction of any capacity that was not nominated (Use It Or

Sell It)

Use it or lose it: unused capacity is sold through auction or FCFS

Gas day

14 Pre-Comitology MeetingBonn – 26 May 2011

More efficient than explicit capacity auctions as it removes risk of separate transactions and allows markets to merge where no physical congestion

How to connect markets? Option 3

Option 3: implicit auctions

15 Pre-Comitology MeetingBonn – 26 May 2011

Option 4: implicit, continuous

Can be used FCFS or implicit auctions

FCFS day-ahead not compatible with CAM FGs?

Series of implicit auctions may disperse liquidity but more auctions allow for flexibility

Arbitrages realised by the TSO from low price area to high price area with implicit allocation of capacity valued at the day-ahead price spread (GRTgaz-Powernext market coupling work)

How to connect markets? Option 4

Continuous implicit allocation may be a solution to allow for efficient gas flows while keeping the flexibility provided by continuous trading?

Day-ahead/ intra-dayLong-term market (explicit capacity allocation)

Auction gate

closures

Implicit allocation

16 Pre-Comitology MeetingBonn – 26 May 2011

Further issues: Interaction with long-term gas trading (1/2)

If short term capacity is freed-up, what should be the reserve price?

Zero reserve price allows capacity to be re-allocated at 0 cost if there is no congestion

If congestion, auction price will rise above zero

Will a zero reserve price change shippers behaviour and move markets towards the short term?

In non-peak periods maybe more reliance on short term

Peak period: long-term capacity still needed

Some markets have higher proportion of transit than others

Con

gest

ion

reve

nues

No interconnection

High level of interconnection capacity

0

Hig

h r

even

ues

Surplus inter-

connection capacity

Interconnection capacity

17 Pre-Comitology MeetingBonn – 26 May 2011

Further issues: Interaction with long-term gas trading (2/2)

Options for reserve prices for short term capacity

1. No reserve price (solution in electricity) but in gas domestic tariffs subsidise transit flows?

2. Set a reserve price to recover costs- impact on price convergence at congested points?

3. Set a reserve price at non-congested points but not at congested

4. No reserve price at interconnection points but a ’membership fee’ at end-user exit points

a. Flat rate

b. Based on flows

Need a redistribution mechanism

18 Pre-Comitology MeetingBonn – 26 May 2011

Thank You!