Embed Size (px)

Citation preview

Gardner DenverInvestor PresentationJune 2017

Disclaimer

Forward-Looking Statements

During the course of this presentation, we may make “forward-looking statements” within themeaning of the US federal securities laws. In fact, all statements made during this presentation otherthan statements of historical fact are forward-looking statements. Words such as “expects,”“anticipates,” “believes,” “estimates,” “plans,” “intends,” “projects” and “indicates” and variations ofsuch words or similar expressions are intended to identify forward-looking statements. Although theyreflect our current expectations, these statements are not guarantees of future performance, andactual results may differ materially from what is expressed in or indicated by these forward-lookingstatements. Forward-looking statements are subject to risks and uncertainties that could causeactual performance or results to differ materially from those expressed in such forward-lookingstatements, including those risks and uncertainties described under the section titled “Risk Factors”in our prospectus dated May 11, 2017, filed with Securities and Exchange Commission (“SEC”) onMay 15, 2017, which risks and uncertainties may be updated from time to time in our periodic filingswith the SEC (accessible on the SEC’s website at www.sec.gov). Forward-looking statements speakonly as of the date the statements are made. The Company does not undertake to update anyforward-looking statements as a result of future developments or new information, except asrequired by law.

Non-GAAP Financial Measures

Included in this presentation are certain non-GAAP financial measures designed to supplement, andnot substitute, the financial information presented in accordance with generally accepted accountingprinciples in the United States of America because management believes such measures are usefulto investors. Examples of non-GAAP measures include Adjusted EBITDA and Unlevered Free CashFlow. For a reconciliation of these non-GAAP measures refer to "Adjusted EBITDA Reconciliation"and “Unlevered Free Cash Flow Conversion Reconciliation” in the Appendix.

2

Company Overview & Strategy

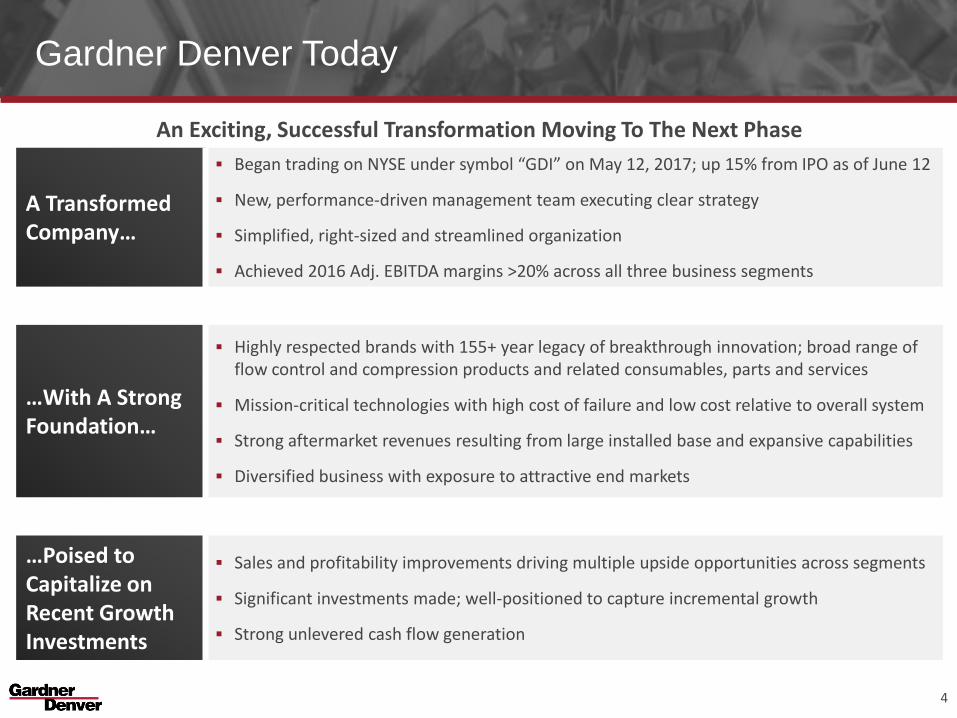

Gardner Denver Today

An Exciting, Successful Transformation Moving To The Next Phase

A Transformed Company…

Began trading on NYSE under symbol “GDI” on May 12, 2017; up 15% from IPO as of June 12

New, performance-driven management team executing clear strategy

Simplified, right-sized and streamlined organization

Achieved 2016 Adj. EBITDA margins >20% across all three business segments

…With A Strong Foundation…

Highly respected brands with 155+ year legacy of breakthrough innovation; broad range of flow control and compression products and related consumables, parts and services

Mission-critical technologies with high cost of failure and low cost relative to overall system

Strong aftermarket revenues resulting from large installed base and expansive capabilities

Diversified business with exposure to attractive end markets

…Poised to Capitalize on Recent Growth Investments

Sales and profitability improvements driving multiple upside opportunities across segments

Significant investments made; well-positioned to capture incremental growth

Strong unlevered cash flow generation

4

Americas41%

EMEA41%

APAC18%

Industrials56%

Energy32%

Medical12%

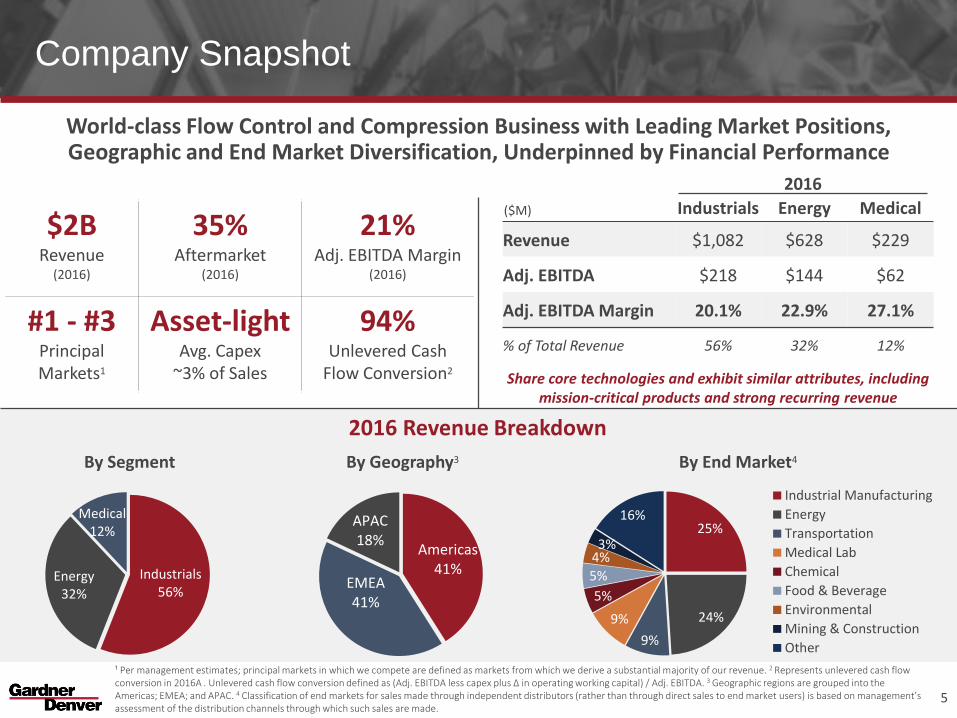

Company Snapshot

World-class Flow Control and Compression Business with Leading Market Positions, Geographic and End Market Diversification, Underpinned by Financial Performance

25%

24%

9%

9%

5%

5%

4%3%

16%

Industrial Manufacturing

Energy

Transportation

Medical Lab

Chemical

Food & Beverage

Environmental

Mining & Construction

Other

By Geography3By Segment By End Market4

$2BRevenue

(2016)

35%Aftermarket

(2016)

21%Adj. EBITDA Margin

(2016)

#1 - #3PrincipalMarkets1

Asset-lightAvg. Capex

~3% of Sales

94%Unlevered Cash

Flow Conversion2

($M) Industrials Energy Medical

Revenue $1,082 $628 $229

Adj. EBITDA $218 $144 $62

Adj. EBITDA Margin 20.1% 22.9% 27.1%

% of Total Revenue 56% 32% 12%

Share core technologies and exhibit similar attributes, including mission-critical products and strong recurring revenue

2016 Revenue Breakdown

¹ Per management estimates; principal markets in which we compete are defined as markets from which we derive a substantial majority of our revenue. 2 Represents unlevered cash flow conversion in 2016A . Unlevered cash flow conversion defined as (Adj. EBITDA less capex plus ∆ in operating working capital) / Adj. EBITDA. 3 Geographic regions are grouped into the Americas; EMEA; and APAC. 4 Classification of end markets for sales made through independent distributors (rather than through direct sales to end market users) is based on management’s assessment of the distribution channels through which such sales are made.

5

2016

Highly Experienced Management Team

Fostering a Culture of Outperformance with an Intense Customer Focus and Bias for Action

45% of Top 100 New to Company; Focused on Executing Strategy to Drive Profitable Growth and Margin Expansion

6Source: Company Filings and Company Website

Cesare TrabattoniVP, Demand Gen.,

Industrials30 Years

Key Corporate Leaders

Vicente ReynalChief Executive Officer

Industry Experience: 22 Years

Todd HerndonChief Financial Officer

Industry Experience: 29 Years

Andrew SchieslGeneral Counsel

22 Years

Vikram KiniVP, Finance &

Investor Relations13 Years

Mark SweeneyChief Accounting Officer

32 Years

Kimberly RubottomVP, Human Resources

30 Years

Sia AbbaszadehVP, Global Product Mgmt.

& Tech., Industrials31 Years

Neil SnyderSVP Strategy, Bus. Dev. & Planning:

19 Years

Key Business Leaders

Larry KerrVP / GM, Petroleum andIndustrial Pumps, Energy

32 Years

Patrick BennettPresident, Medical

25 Years

Enrique ViserasVP / GM,

EMEA, Industrials17 Years

Gary GillespieVP / GM,

Americas, Industrials37 Years

Vince TrupianoVP / GM,

Nash / Garo, Energy30 Years

Ankush KumarVP / GM,

Emco Wheaton, Energy16 Years

Ringo LaiVP / GM,

APAC, Industrials 30 Years

Our Vision and Values

We Will Be the Industry’s First Choice for Innovative and Mission-Critical Flow Control and Compression Products, Services and Solutions Through an Intense Customer Focus and

Disciplined Performance Culture

Customer Focus

Steadfast Integrity

Global Teamwork

Creative Thinking

Bias for Action

7

Industrials Segment OverviewFocused on Additional Value and Emerging Market Growth

▪ Wide range of applications for diverse end markets, including associated aftermarket parts, consumables and services; one of the broadest technology portfolios in the markets we serve

▪ Significant number of manufacturing facilities across industrial sector use air compression, vacuum and/or blower products in a variety of process-critical applications

Revenue $1.1B

Adj. EBITDA $218M

Adj. EBITDA Margin 20.1% 65%

35%

Composition

32%

50%

18%

Geography

Description

2016 Revenue Mix2016 Financials

Manufacturing Pharmaceuticals Bottle Blowing

Food Processing Waste Water Transport

Key End Markets

Compressors Vacuums Blowers

Americas

EMEA

APAC

Equip.

Aftermrkt.

8

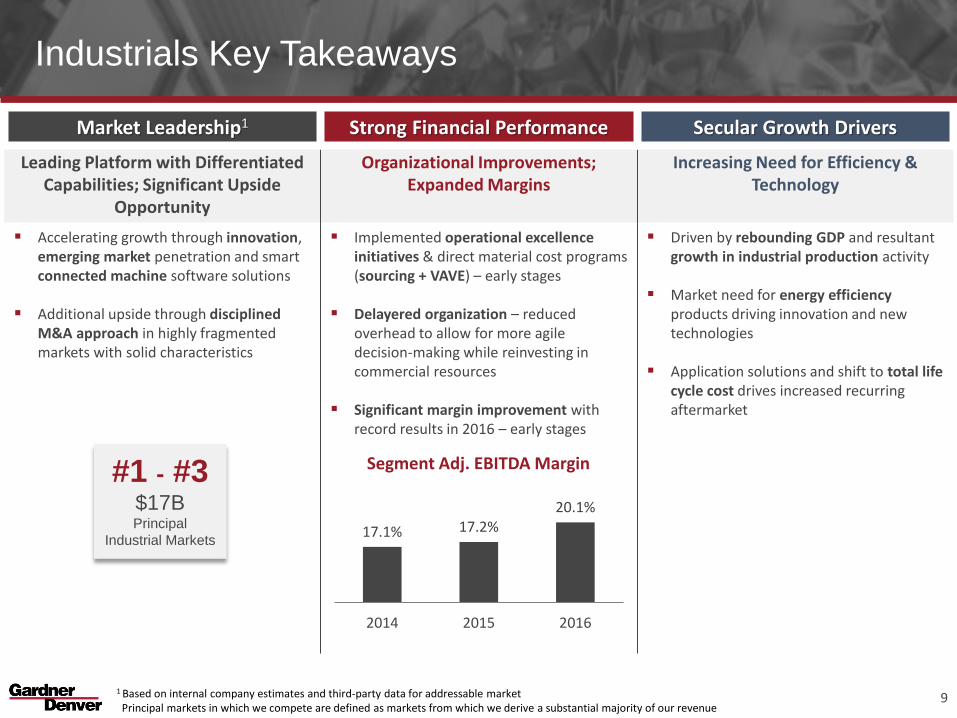

Market Leadership1 Strong Financial Performance Secular Growth Drivers

Leading Platform with Differentiated Capabilities; Significant Upside

Opportunity

Organizational Improvements; Expanded Margins

Increasing Need for Efficiency & Technology

Accelerating growth through innovation, emerging market penetration and smart connected machine software solutions

Additional upside through disciplined M&A approach in highly fragmented markets with solid characteristics

Implemented operational excellence initiatives & direct material cost programs (sourcing + VAVE) – early stages

Delayered organization – reduced overhead to allow for more agile decision-making while reinvesting in commercial resources

Significant margin improvement with record results in 2016 – early stages

Driven by rebounding GDP and resultant growth in industrial production activity

Market need for energy efficiency products driving innovation and new technologies

Application solutions and shift to total life cycle cost drives increased recurring aftermarket

Industrials Key Takeaways

91 Based on internal company estimates and third-party data for addressable marketPrincipal markets in which we compete are defined as markets from which we derive a substantial majority of our revenue

17.1% 17.2%20.1%

2014 2015 2016

Segment Adj. EBITDA Margin#1 - #3$17BPrincipal

Industrial Markets

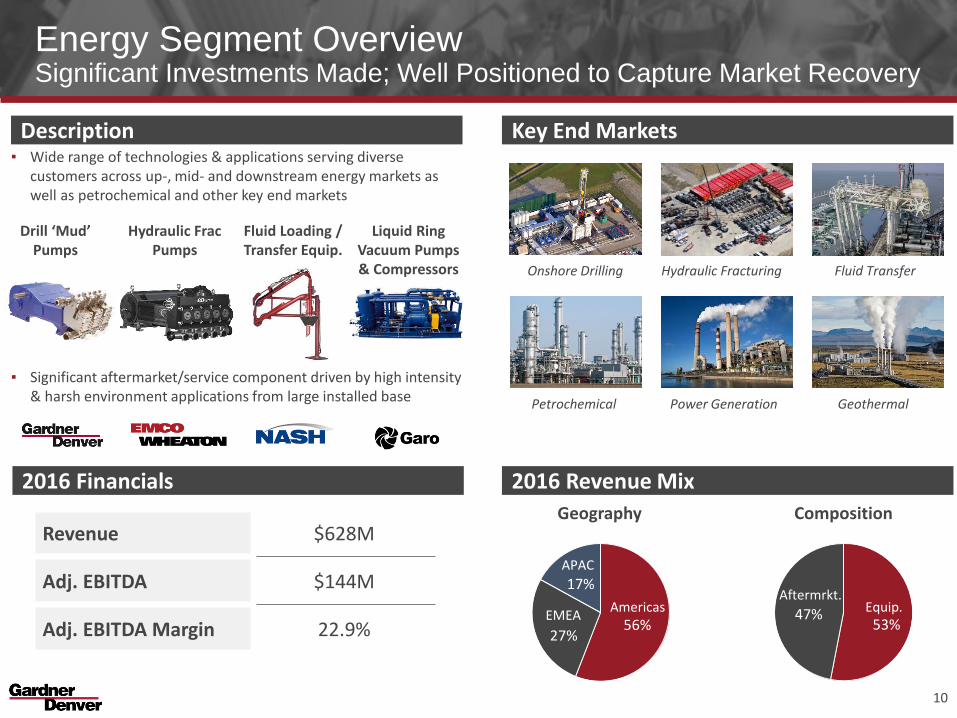

▪ Wide range of technologies & applications serving diverse customers across up-, mid- and downstream energy markets as well as petrochemical and other key end markets

▪ Significant aftermarket/service component driven by high intensity & harsh environment applications from large installed base

Drill ‘Mud’ Pumps

Energy Segment Overview Significant Investments Made; Well Positioned to Capture Market Recovery

Revenue $628M

Adj. EBITDA $144M

Adj. EBITDA Margin 22.9%

Description

2016 Revenue Mix2016 Financials

Key End Markets

Liquid Ring Vacuum Pumps & Compressors

Fluid Loading / Transfer Equip.

Hydraulic Frac Pumps

53%47%

Composition

56%27%

17%

Geography

AmericasEMEA

APAC

Equip.Aftermrkt.

Onshore Drilling Hydraulic Fracturing

Petrochemical Power Generation

Fluid Transfer

Geothermal

10

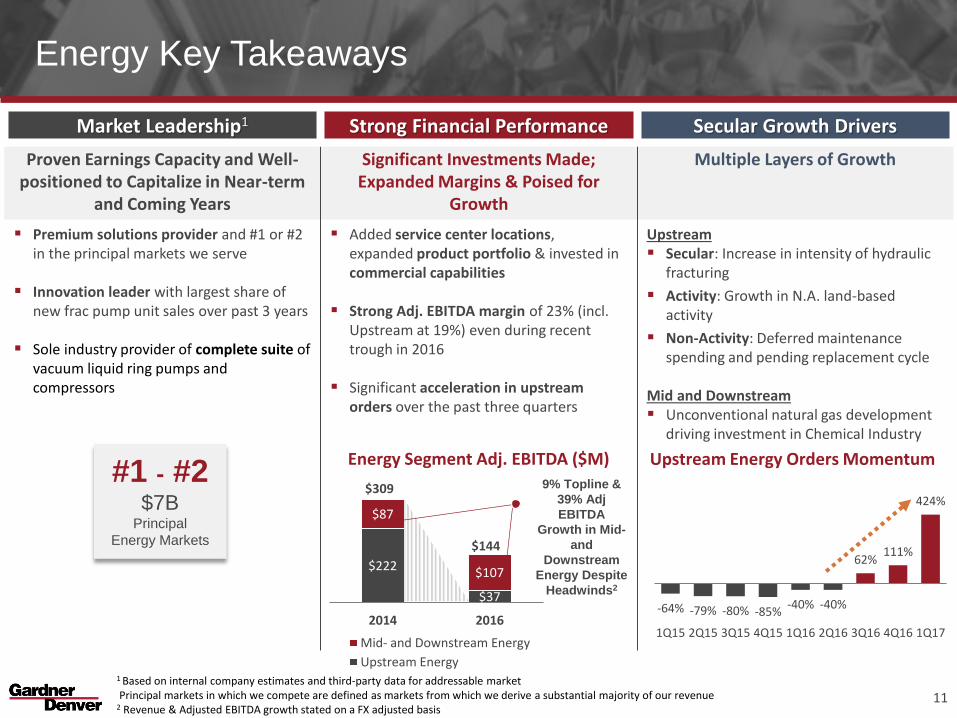

Market Leadership1 Strong Financial Performance Secular Growth Drivers

Proven Earnings Capacity and Well-positioned to Capitalize in Near-term

and Coming Years

Significant Investments Made; Expanded Margins & Poised for

Growth

Multiple Layers of Growth

Premium solutions provider and #1 or #2 in the principal markets we serve

Innovation leader with largest share of new frac pump unit sales over past 3 years

Sole industry provider of complete suite of vacuum liquid ring pumps and compressors

Added service center locations, expanded product portfolio & invested in commercial capabilities

Strong Adj. EBITDA margin of 23% (incl. Upstream at 19%) even during recent trough in 2016

Significant acceleration in upstream orders over the past three quarters

Upstream Secular: Increase in intensity of hydraulic

fracturing

Activity: Growth in N.A. land-based activity

Non-Activity: Deferred maintenance spending and pending replacement cycle

Mid and Downstream Unconventional natural gas development

driving investment in Chemical Industry

Energy Key Takeaways

11

-64% -79% -80% -85%-40% -40%

62%111%

424%

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17

Upstream Energy Orders Momentum

$222

$37

$87

$107

2014 2016

Mid- and Downstream Energy

Upstream Energy

$309

$144

Energy Segment Adj. EBITDA ($M)

9% Topline &

39% Adj

EBITDA

Growth in Mid-

and

Downstream

Energy Despite

Headwinds2

#1 - #2$7B

Principal

Energy Markets

1 Based on internal company estimates and third-party data for addressable marketPrincipal markets in which we compete are defined as markets from which we derive a substantial majority of our revenue

2 Revenue & Adjusted EBITDA growth stated on a FX adjusted basis

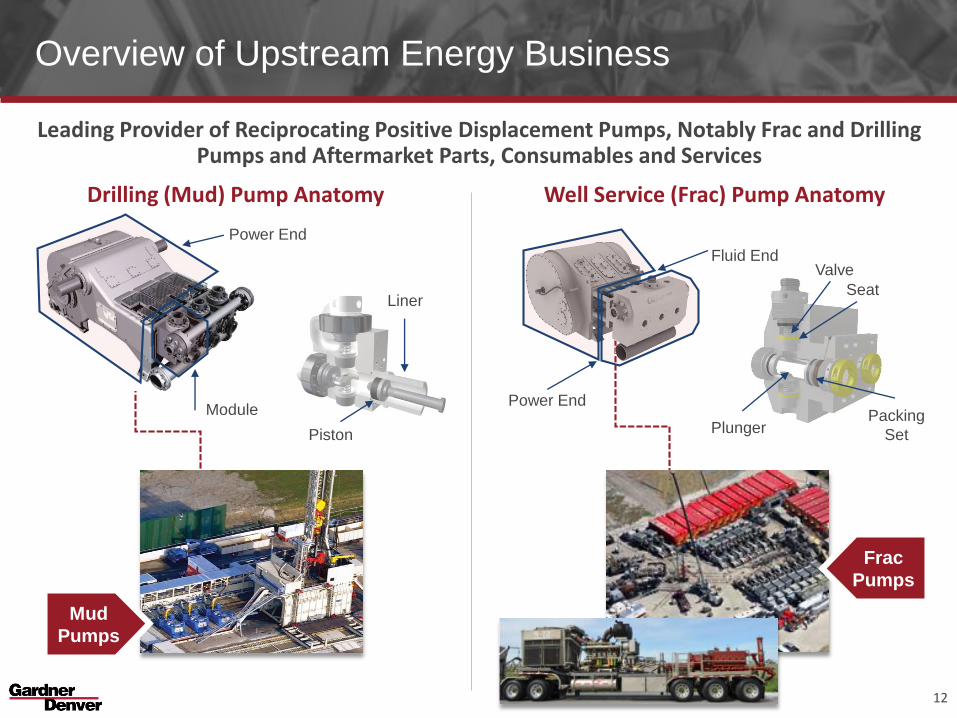

Overview of Upstream Energy Business

Leading Provider of Reciprocating Positive Displacement Pumps, Notably Frac and Drilling Pumps and Aftermarket Parts, Consumables and Services

12

Well Service (Frac) Pump Anatomy

Fluid End

Power End

Valve

Seat

Packing

SetPlunger

Drilling (Mud) Pump Anatomy

Module

Liner

Piston

Power End

Mud

Pumps

Frac

Pumps

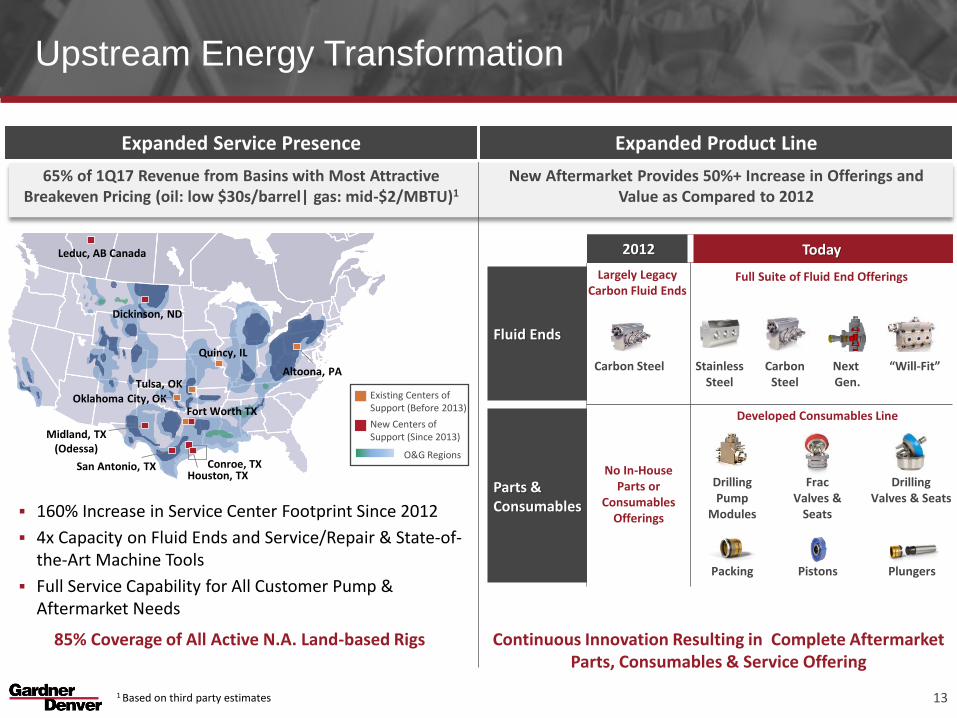

Expanded Service Presence Expanded Product Line

65% of 1Q17 Revenue from Basins with Most Attractive Breakeven Pricing (oil: low $30s/barrel| gas: mid-$2/MBTU)1

New Aftermarket Provides 50%+ Increase in Offerings and Value as Compared to 2012

Upstream Energy Transformation

13

160% Increase in Service Center Footprint Since 2012

4x Capacity on Fluid Ends and Service/Repair & State-of-the-Art Machine Tools

Full Service Capability for All Customer Pump & Aftermarket Needs

2012 Today

Fluid Ends

Full Suite of Fluid End Offerings

Parts &Consumables

No In-House Parts or

Consumables Offerings

Developed Consumables Line

Carbon Steel StainlessSteel

CarbonSteel

Next Gen.

“Will-Fit”

Drilling Pump

Modules

Frac Valves &

Seats

Pistons

Drilling Valves & Seats

Packing Plungers

Continuous Innovation Resulting in Complete Aftermarket Parts, Consumables & Service Offering

85% Coverage of All Active N.A. Land-based Rigs

Tulsa, OK

Conroe, TX

Fort Worth TX

Quincy, IL

Midland, TX(Odessa)

San Antonio, TXHouston, TX

Oklahoma City, OK

Dickinson, ND

Leduc, AB Canada

Altoona, PA

Existing Centers of Support (Before 2013)

New Centers of Support (Since 2013)

O&G Regions

Largely Legacy Carbon Fluid Ends

1 Based on third party estimates

Medical Segment OverviewFocused on Capturing New Addressable Market Opportunities

▪ Products are specified by medical and lab equipment suppliers and integrated into final product; applications include oxygen therapy, blood dialysis, patient monitoring, laboratory sterilization and wound treatment

▪ Recent expansion into liquid pumps and liquid handling solutions opens new addressable markets

Revenue $229M

Adj. EBITDA $62M

Adj. EBITDA Margin 27.1%

Description Key End Markets

Medical

Negative Pressure Wound Therapy

Chemical Laboratory

Chemical Distillation

Diagnostic Laboratory

OIVA Analysis

Gas Pumps Liquid Pumps Liquid Handling Solutions

45%

39%

16%

Geography

Americas

EMEA

APAC

14

2016 Revenue Mix2016 Financials

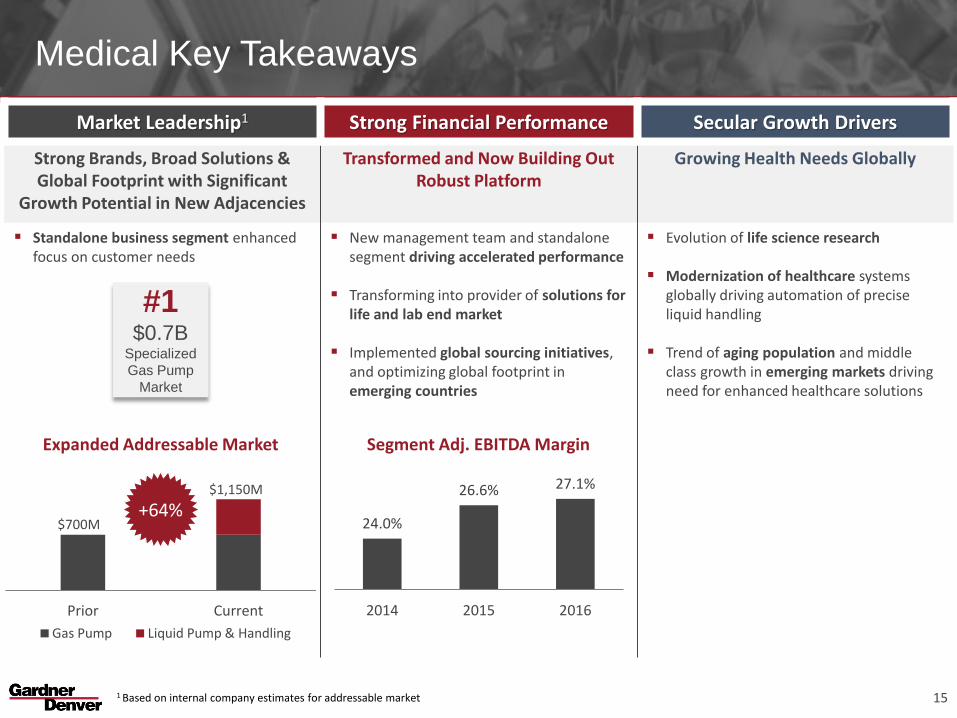

Market Leadership1 Strong Financial Performance Secular Growth Drivers

Strong Brands, Broad Solutions & Global Footprint with Significant

Growth Potential in New Adjacencies

Transformed and Now Building Out Robust Platform

Growing Health Needs Globally

Standalone business segment enhanced focus on customer needs

New management team and standalone segment driving accelerated performance

Transforming into provider of solutions for life and lab end market

Implemented global sourcing initiatives, and optimizing global footprint in emerging countries

Evolution of life science research

Modernization of healthcare systems globally driving automation of precise liquid handling

Trend of aging population and middle class growth in emerging markets driving need for enhanced healthcare solutions

Medical Key Takeaways

15

24.0%

26.6% 27.1%

2014 2015 2016

Segment Adj. EBITDA Margin

Prior Current

Gas Pump Liquid Pump & Handling

$700M

$1,150M

+64%

Expanded Addressable Market

#1$0.7B

Specialized

Gas Pump

Market

1 Based on internal company estimates for addressable market

Our Strategy Will Continue to Drive Results and Shareholder Value

16

Deploy Talent

Expand Margins

Accelerate Growth

Allocate Capital Effectively

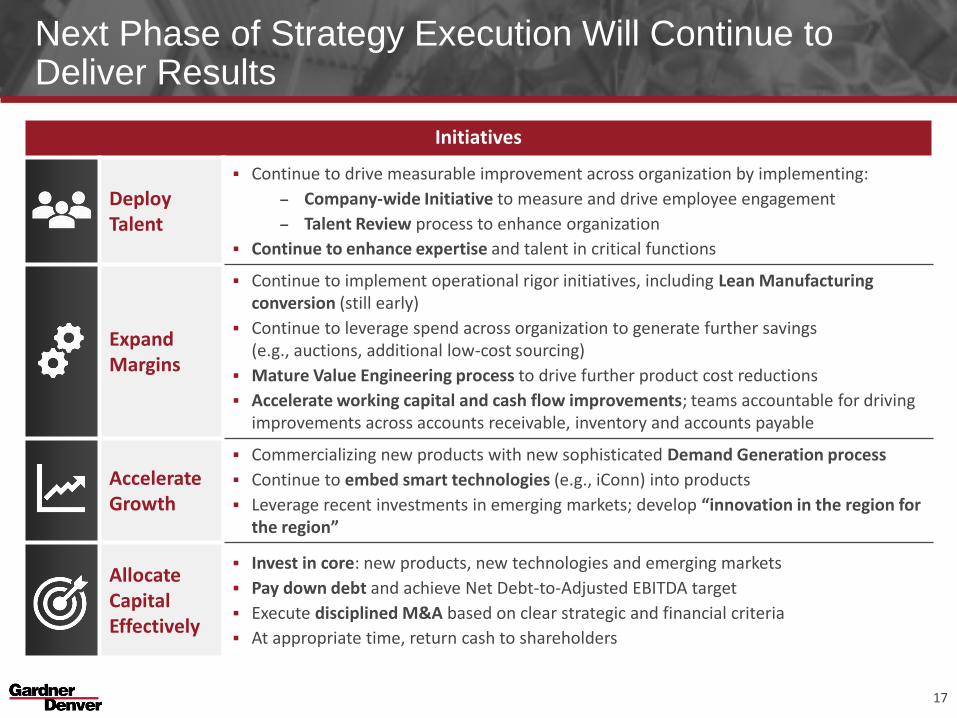

Next Phase of Strategy Execution Will Continue to Deliver Results

Initiatives

Deploy Talent

Continue to drive measurable improvement across organization by implementing:

– Company-wide Initiative to measure and drive employee engagement

– Talent Review process to enhance organization

Continue to enhance expertise and talent in critical functions

Expand Margins

Continue to implement operational rigor initiatives, including Lean Manufacturing conversion (still early)

Continue to leverage spend across organization to generate further savings (e.g., auctions, additional low-cost sourcing)

Mature Value Engineering process to drive further product cost reductions

Accelerate working capital and cash flow improvements; teams accountable for driving improvements across accounts receivable, inventory and accounts payable

Accelerate Growth

Commercializing new products with new sophisticated Demand Generation process

Continue to embed smart technologies (e.g., iConn) into products

Leverage recent investments in emerging markets; develop “innovation in the region for the region”

Allocate Capital Effectively

Invest in core: new products, new technologies and emerging markets

Pay down debt and achieve Net Debt-to-Adjusted EBITDA target

Execute disciplined M&A based on clear strategic and financial criteria

At appropriate time, return cash to shareholders

17

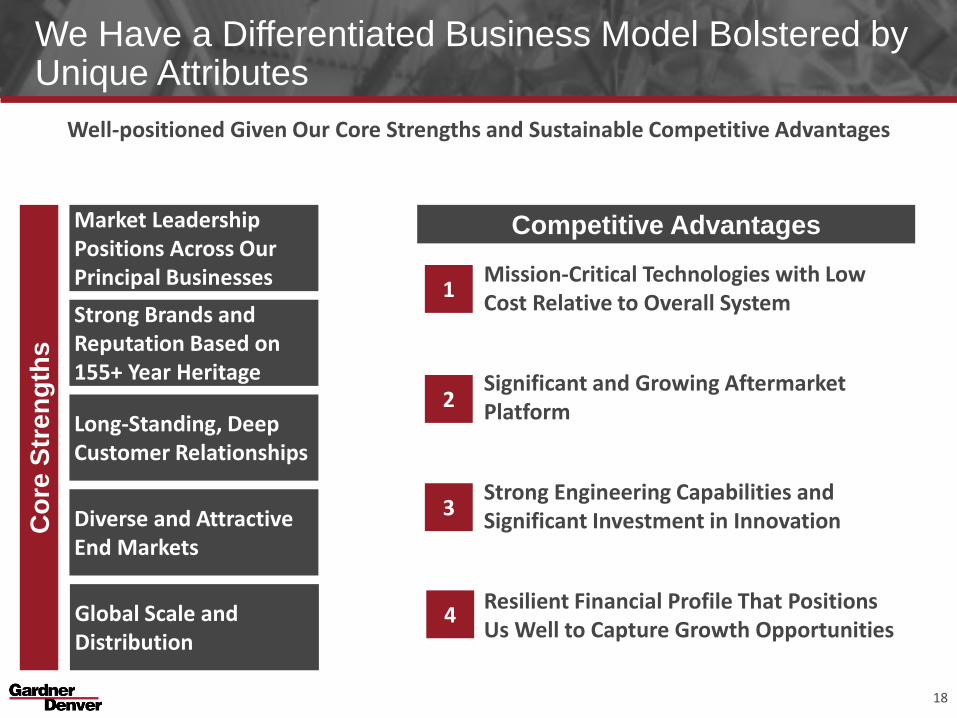

We Have a Differentiated Business Model Bolstered by Unique Attributes

Well-positioned Given Our Core Strengths and Sustainable Competitive Advantages

Co

re S

tre

ng

ths

Market Leadership Positions Across Our Principal Businesses

Strong Brands and Reputation Based on 155+ Year Heritage

Long-Standing, Deep Customer Relationships

Diverse and Attractive End Markets

Global Scale and Distribution

Competitive Advantages

Mission-Critical Technologies with Low Cost Relative to Overall System

Significant and Growing Aftermarket Platform

Strong Engineering Capabilities and Significant Investment in Innovation

Resilient Financial Profile That Positions Us Well to Capture Growth Opportunities

1

2

3

4

18

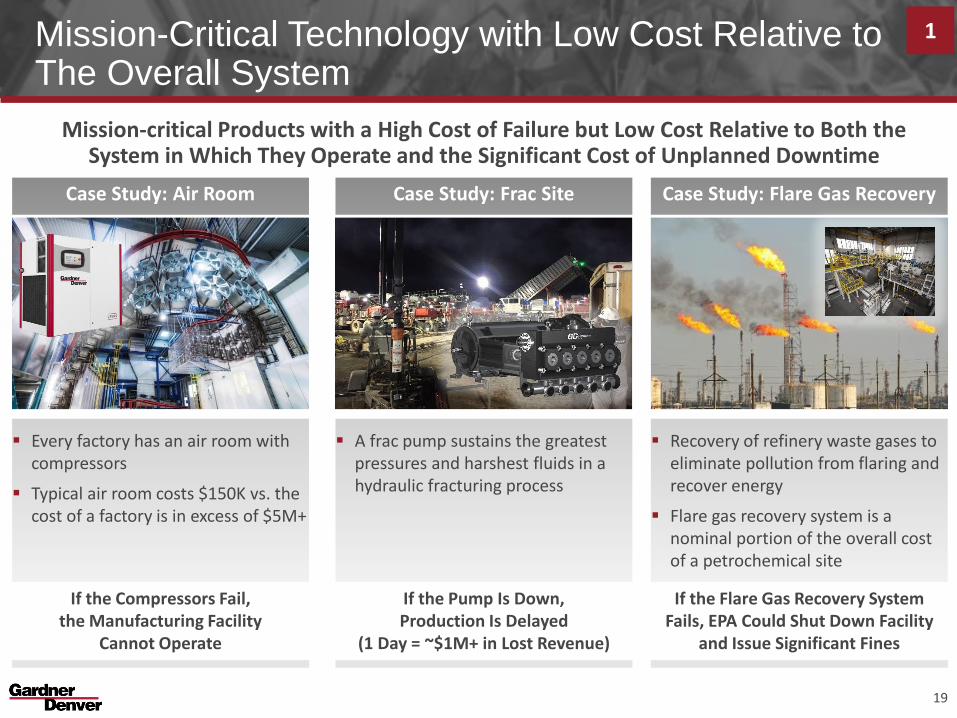

Mission-Critical Technology with Low Cost Relative to The Overall System

Mission-critical Products with a High Cost of Failure but Low Cost Relative to Both the System in Which They Operate and the Significant Cost of Unplanned Downtime

Case Study: Air Room

Every factory has an air room with compressors

Typical air room costs $150K vs. the cost of a factory is in excess of $5M+

Case Study: Frac Site

A frac pump sustains the greatest pressures and harshest fluids in a hydraulic fracturing process

Case Study: Flare Gas Recovery

Recovery of refinery waste gases to eliminate pollution from flaring and recover energy

Flare gas recovery system is a nominal portion of the overall cost of a petrochemical site

1

19

If the Flare Gas Recovery System Fails, EPA Could Shut Down Facility

and Issue Significant Fines

If the Pump Is Down, Production Is Delayed

(1 Day = ~$1M+ in Lost Revenue)

If the Compressors Fail, the Manufacturing Facility

Cannot Operate

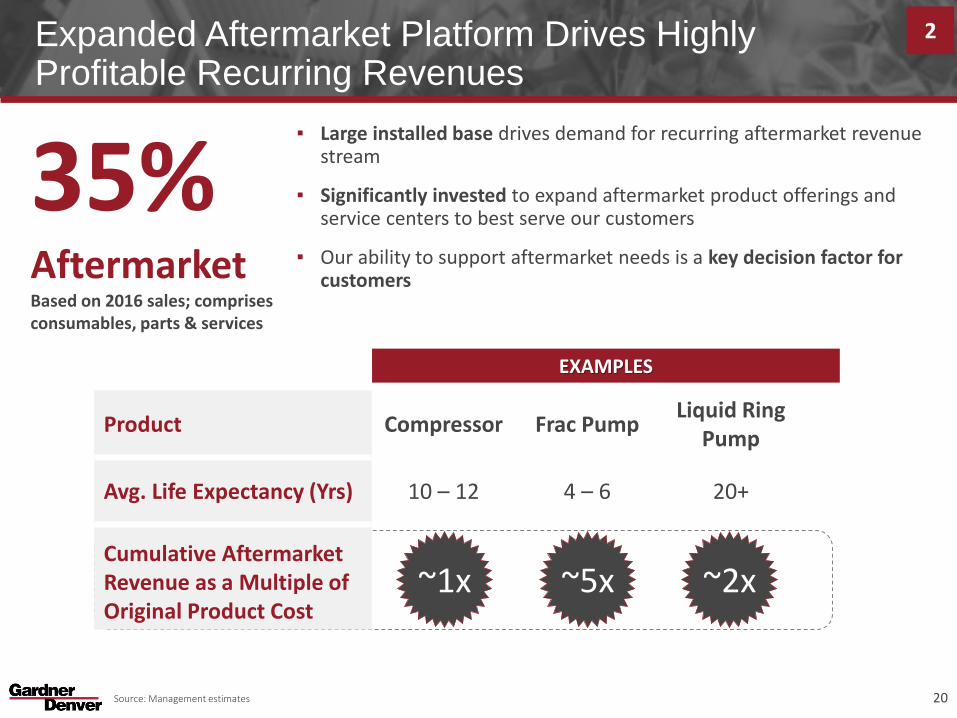

Expanded Aftermarket Platform Drives Highly Profitable Recurring Revenues

▪ Large installed base drives demand for recurring aftermarket revenue stream

▪ Significantly invested to expand aftermarket product offerings and service centers to best serve our customers

▪ Our ability to support aftermarket needs is a key decision factor for customers

Source: Management estimates

EXAMPLES

35% Aftermarket Based on 2016 sales; comprises consumables, parts & services

2

~1x ~5x ~2x

20

Product Compressor Frac PumpLiquid Ring

Pump

Avg. Life Expectancy (Yrs) 10 – 12 4 – 6 20+

Cumulative Aftermarket Revenue as a Multiple of Original Product Cost

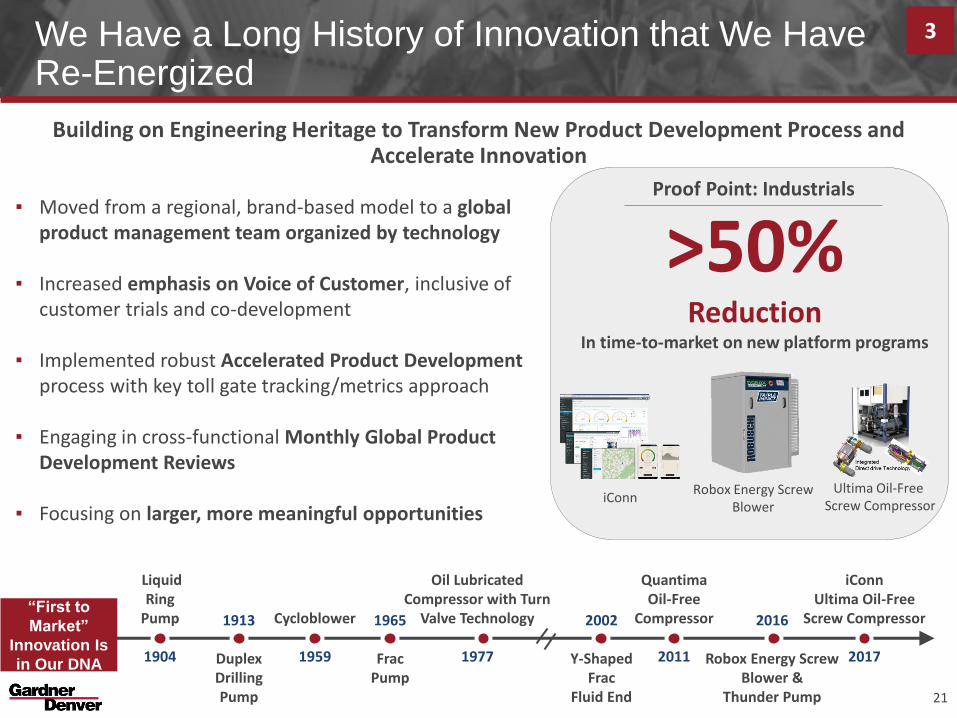

We Have a Long History of Innovation that We Have Re-Energized

Building on Engineering Heritage to Transform New Product Development Process and Accelerate Innovation

▪ Moved from a regional, brand-based model to a global product management team organized by technology

▪ Increased emphasis on Voice of Customer, inclusive of customer trials and co-development

▪ Implemented robust Accelerated Product Development process with key toll gate tracking/metrics approach

▪ Engaging in cross-functional Monthly Global Product Development Reviews

▪ Focusing on larger, more meaningful opportunities

Liquid Ring

Pump

1904

1913

Duplex Drilling Pump

Cycloblower

1959

1965

Frac Pump

“First to

Market”

Innovation Is

in Our DNA

3

2016

Robox Energy Screw Blower &

Thunder Pump

QuantimaOil-Free

Compressor

2011

iConn Ultima Oil-Free

Screw Compressor

2017

21

2002

Y-Shaped Frac

Fluid End

Oil Lubricated Compressor with Turn

Valve Technology

1977

Proof Point: Industrials

>50% Reduction

In time-to-market on new platform programs

iConnRobox Energy Screw

Blower

Ultima Oil-Free Screw Compressor

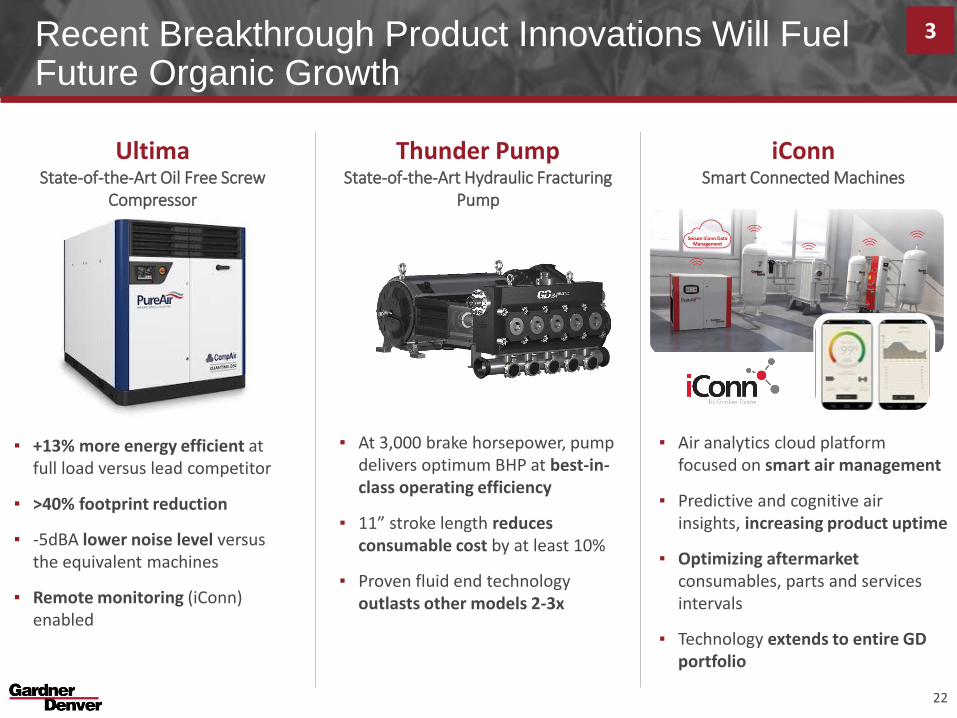

Recent Breakthrough Product Innovations Will Fuel Future Organic Growth

3

22

▪ +13% more energy efficient at full load versus lead competitor

▪ >40% footprint reduction

▪ -5dBA lower noise level versus the equivalent machines

▪ Remote monitoring (iConn) enabled

UltimaState-of-the-Art Oil Free Screw

Compressor

▪ At 3,000 brake horsepower, pump delivers optimum BHP at best-in-class operating efficiency

▪ 11” stroke length reduces consumable cost by at least 10%

▪ Proven fluid end technology outlasts other models 2-3x

Thunder PumpState-of-the-Art Hydraulic Fracturing

Pump

iConnSmart Connected Machines

▪ Air analytics cloud platform focused on smart air management

▪ Predictive and cognitive air insights, increasing product uptime

▪ Optimizing aftermarket consumables, parts and services intervals

▪ Technology extends to entire GD portfolio

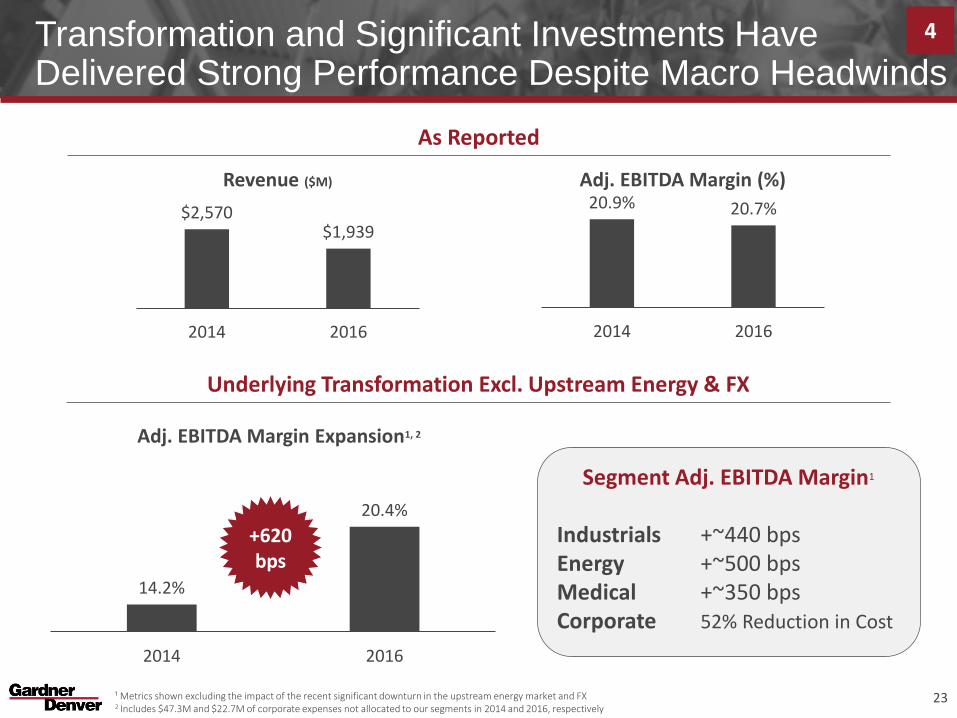

Transformation and Significant Investments Have Delivered Strong Performance Despite Macro Headwinds

$2,570$1,939

2014 2016

Revenue ($M)

20.9% 20.7%

2014 2016

Adj. EBITDA Margin (%)

14.2%

20.4%

2014 2016

Adj. EBITDA Margin Expansion1, 2

+620 bps

Segment Adj. EBITDA Margin1

Industrials +~440 bpsEnergy +~500 bpsMedical +~350 bpsCorporate 52% Reduction in Cost

As Reported

Underlying Transformation Excl. Upstream Energy & FX

23¹ Metrics shown excluding the impact of the recent significant downturn in the upstream energy market and FX2 Includes $47.3M and $22.7M of corporate expenses not allocated to our segments in 2014 and 2016, respectively

4

Financial Overview

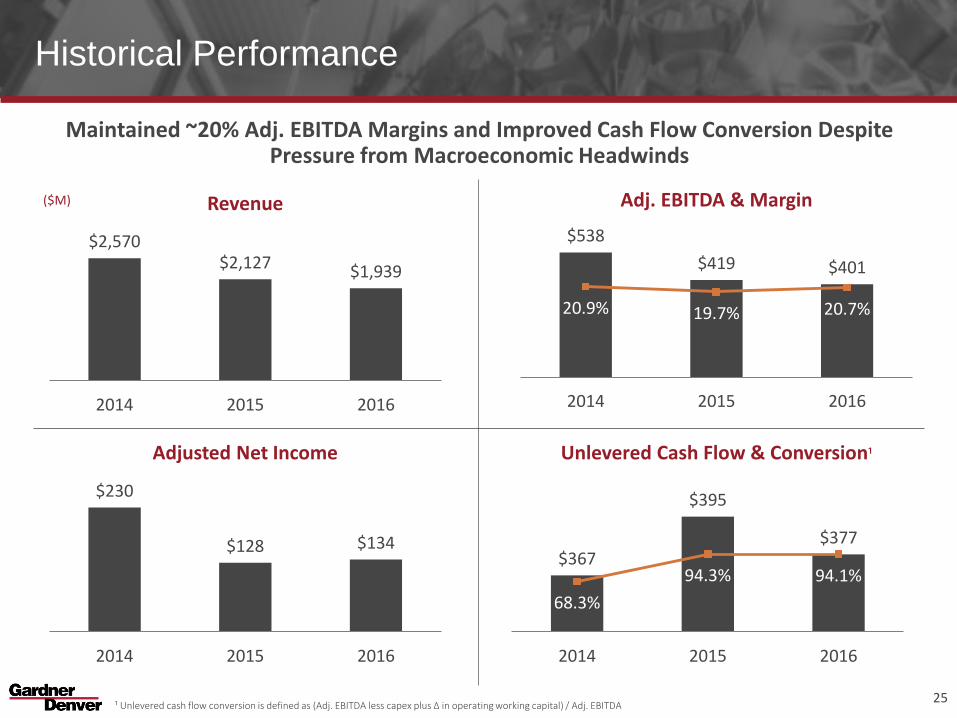

Historical Performance

Maintained ~20% Adj. EBITDA Margins and Improved Cash Flow Conversion Despite Pressure from Macroeconomic Headwinds

Adj. EBITDA & MarginRevenue

Unlevered Cash Flow & Conversion¹Adjusted Net Income

$2,570$2,127 $1,939

2014 2015 2016

$230

$128 $134

2014 2015 2016

$367

$395

$377

68.3%

94.3% 94.1%

$34 0

$35 0

$36 0

$37 0

$38 0

$39 0

$40 0

2014 2015 2016

20. 0%

40. 0%

60. 0%

80. 0%

100 .0%

120 .0%

140 .0%

$538

$419 $401

20.9% 19.7% 20.7%

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$10 0

$11 0

$12 0

$13 0

$14 0

$15 0

$16 0

$17 0

$18 0

$19 0

$20 0

$21 0

$22 0

$23 0

$24 0

$25 0

$26 0

$27 0

$28 0

$29 0

$30 0

$31 0

$32 0

$33 0

$34 0

$35 0

$36 0

$37 0

$38 0

$39 0

$40 0

$41 0

$42 0

$43 0

$44 0

$45 0

$46 0

$47 0

$48 0

$49 0

$50 0

$51 0

$52 0

$53 0

$54 0

$55 0

$56 0

2014 2015 2016

0.0 %

5.0 %

10. 0%

15. 0%

20. 0%

25. 0%

30. 0%

($M)

25¹ Unlevered cash flow conversion is defined as (Adj. EBITDA less capex plus ∆ in operating working capital) / Adj. EBITDA

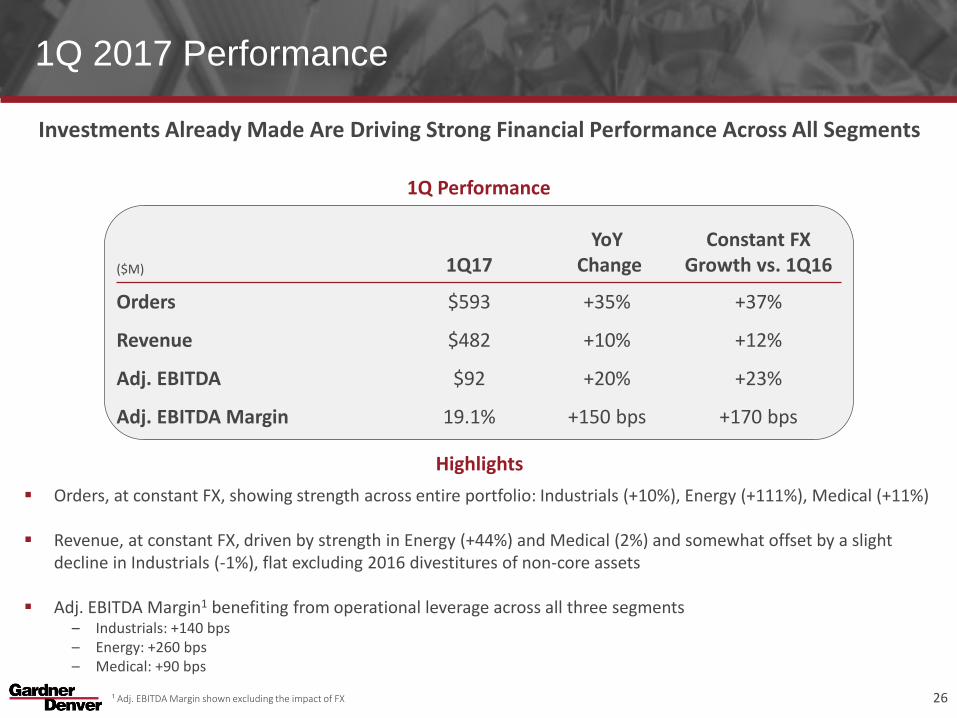

1Q 2017 Performance

Investments Already Made Are Driving Strong Financial Performance Across All Segments

1Q Performance

($M) 1Q17YoY

ChangeConstant FX

Growth vs. 1Q16

Orders $593 +35% +37%

Revenue $482 +10% +12%

Adj. EBITDA $92 +20% +23%

Adj. EBITDA Margin 19.1% +150 bps +170 bps

Highlights

Orders, at constant FX, showing strength across entire portfolio: Industrials (+10%), Energy (+111%), Medical (+11%)

Revenue, at constant FX, driven by strength in Energy (+44%) and Medical (2%) and somewhat offset by a slight decline in Industrials (-1%), flat excluding 2016 divestitures of non-core assets

Adj. EBITDA Margin1 benefiting from operational leverage across all three segments– Industrials: +140 bps – Energy: +260 bps – Medical: +90 bps

26¹ Adj. EBITDA Margin shown excluding the impact of FX

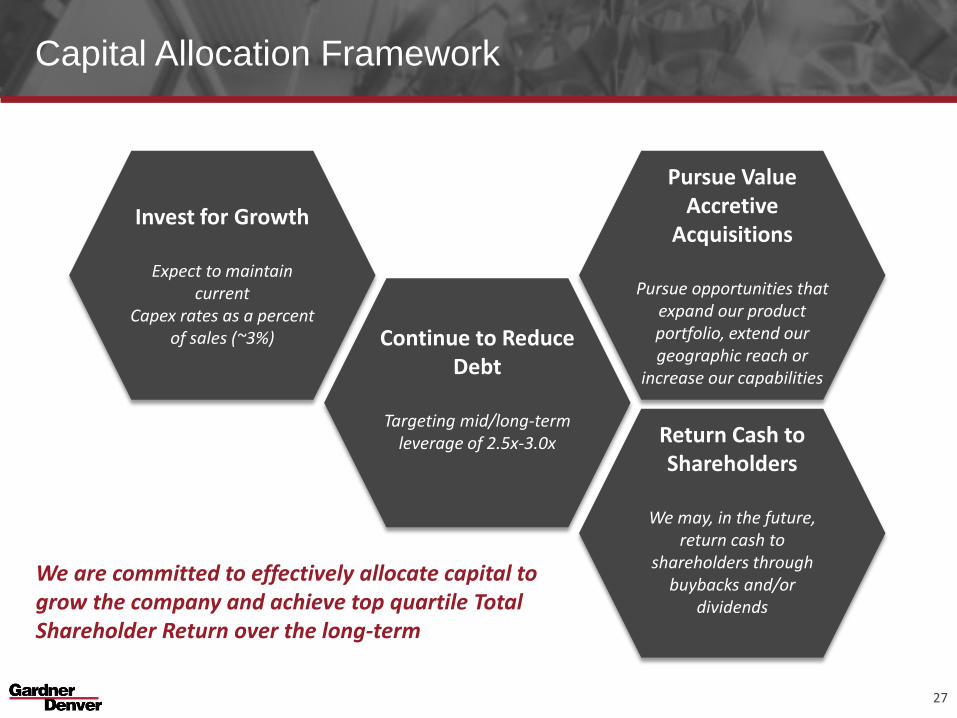

Capital Allocation Framework

We are committed to effectively allocate capital to grow the company and achieve top quartile Total Shareholder Return over the long-term

27

Invest for Growth

Expect to maintain current

Capex rates as a percent of sales (~3%) Continue to Reduce

Debt

Targeting mid/long-term leverage of 2.5x-3.0x

Pursue Value Accretive

Acquisitions

Pursue opportunities that expand our product portfolio, extend our geographic reach or

increase our capabilities

Return Cash to Shareholders

We may, in the future, return cash to

shareholders through buybacks and/or

dividends

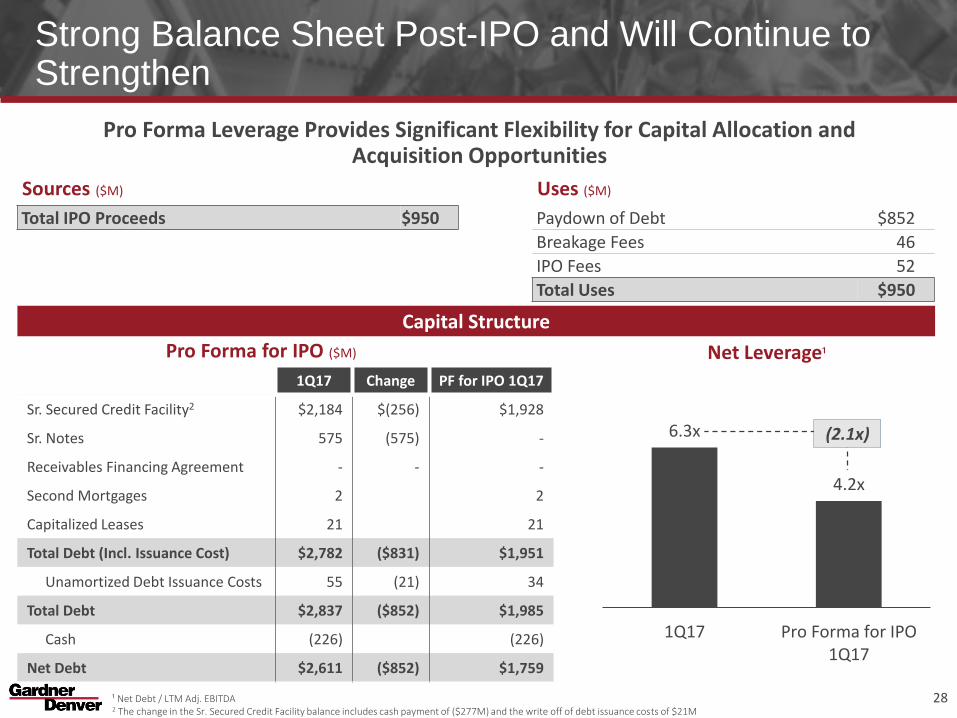

Strong Balance Sheet Post-IPO and Will Continue to Strengthen

Pro Forma Leverage Provides Significant Flexibility for Capital Allocation and Acquisition Opportunities

¹ Net Debt / LTM Adj. EBITDA2 The change in the Sr. Secured Credit Facility balance includes cash payment of ($277M) and the write off of debt issuance costs of $21M

Sources ($M)

Total IPO Proceeds $950

Uses ($M)

Paydown of Debt $852

Breakage Fees 46

IPO Fees 52

Total Uses $950

(2.1x)

Net Leverage¹

1Q17 Change PF for IPO 1Q17

Sr. Secured Credit Facility2 $2,184 $(256) $1,928

Sr. Notes 575 (575) -

Receivables Financing Agreement - - -

Second Mortgages 2 2

Capitalized Leases 21 21

Total Debt (Incl. Issuance Cost) $2,782 ($831) $1,951

Unamortized Debt Issuance Costs 55 (21) 34

Total Debt $2,837 ($852) $1,985

Cash (226) (226)

Net Debt $2,611 ($852) $1,759

Capital Structure

Pro Forma for IPO ($M)

28

6.3x

4.2x

1Q17 Pro Forma for IPO1Q17

Key Investment Highlights

▪ Premier industrial company with market leadership, global premium brands and track record of breakthrough technologies

▪ Strong financial profile with a clear plan to drive further revenue and earnings growth– 2016 Gross Profit Margin: ~37% – 2016 Adj. EBITDA Margin: > 20% across all segments – 2016 Aftermarket: 35% of revenue

▪ Attractive growth levers over the near and long-term– Recent investment in innovation (new products) and new business platforms (medical)– Exposure to secular tailwinds amplified by significant investments in people, presence and

expanded products in U.S. land-based upstream energy– Leverage recent investments in emerging markets to increase penetration and growth

▪ Robust cash flow generation enabling high-return investments both internally and externally; focused on debt paydown and well-positioned to participate in industry consolidation

▪ Energized, experienced management team with a track record of execution and a commitment to drive performance

Strong Foundation, Clear Strategy, Committed Leadership and Early Innings

29

Appendix

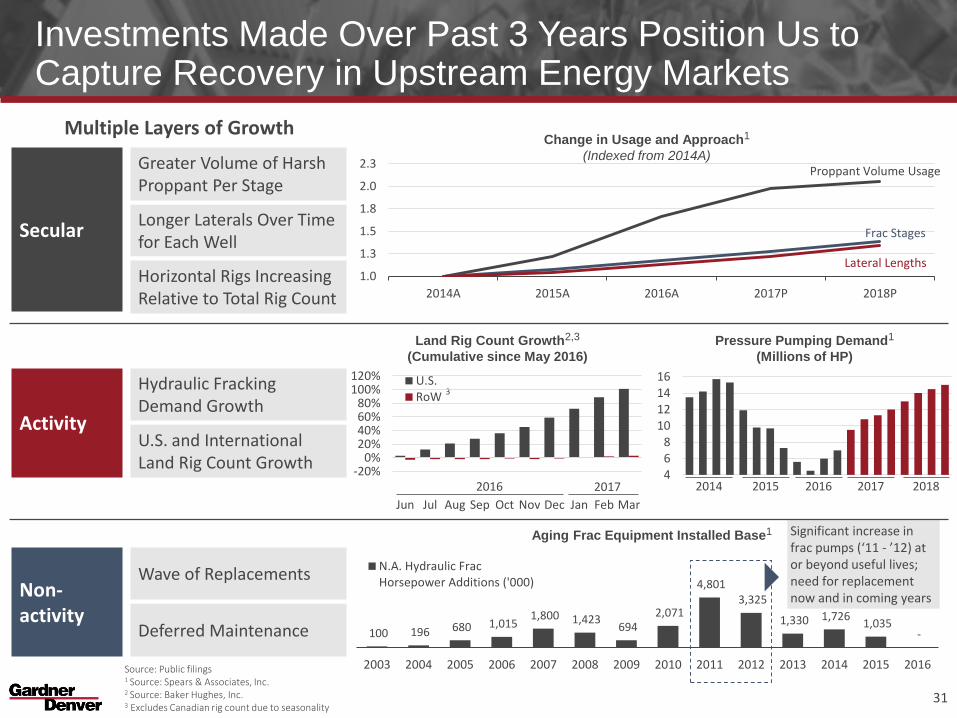

Significant increase in frac pumps (‘11 - ’12) at or beyond useful lives; need for replacement now and in coming years

Investments Made Over Past 3 Years Position Us to Capture Recovery in Upstream Energy Markets

Multiple Layers of Growth

SecularLonger Laterals Over Time for Each Well

Greater Volume of Harsh Proppant Per Stage

Horizontal Rigs Increasing Relative to Total Rig Count

ActivityU.S. and International Land Rig Count Growth

Hydraulic Fracking Demand Growth

Non-activity

Deferred Maintenance

Wave of Replacements

Land Rig Count Growth2,3

(Cumulative since May 2016)

Source: Public filings1 Source: Spears & Associates, Inc.2 Source: Baker Hughes, Inc.3 Excludes Canadian rig count due to seasonality

468

10121416

Change in Usage and Approach1

(Indexed from 2014A)

2016 2017

Pressure Pumping Demand1

(Millions of HP)

100 196 680 1,015 1,800 1,423

694 2,071

4,801 3,325

1,330 1,726 1,035

-

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

N.A. Hydraulic FracHorsepower Additions ('000)

Aging Frac Equipment Installed Base1

31

3

1.0

1.3

1.5

1.8

2.0

2.3

2014A 2015A 2016A 2017P 2018P

Lateral Lengths

Frac Stages

Proppant Volume Usage

2014 2015 2016 2017 2018-20%

0%20%40%60%80%

100%120%

Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

U.S.RoW

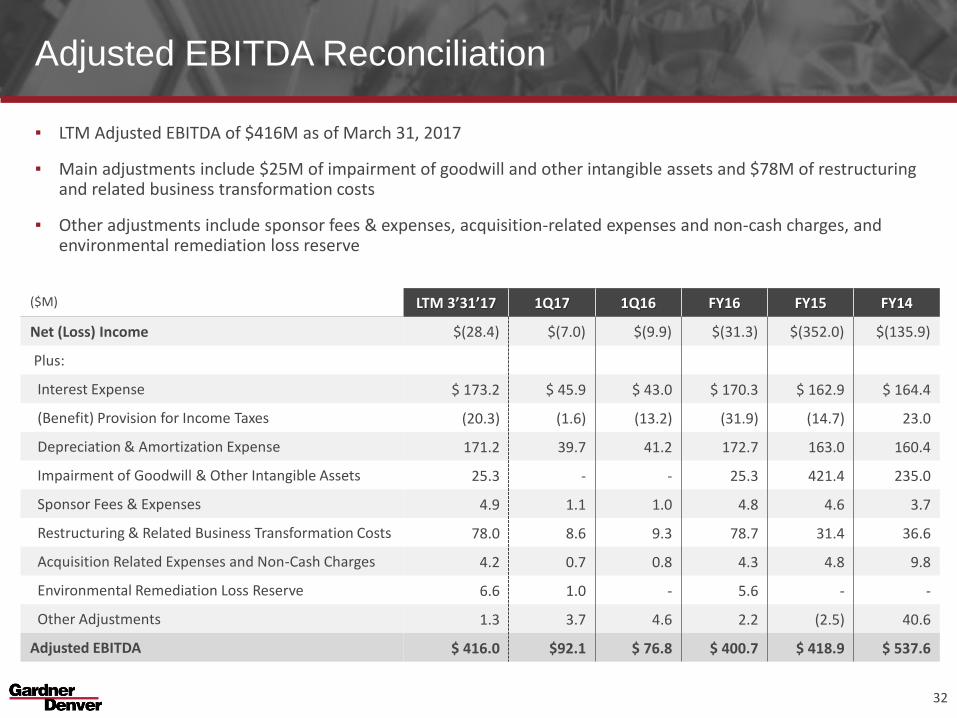

Adjusted EBITDA Reconciliation

▪ LTM Adjusted EBITDA of $416M as of March 31, 2017

▪ Main adjustments include $25M of impairment of goodwill and other intangible assets and $78M of restructuring and related business transformation costs

▪ Other adjustments include sponsor fees & expenses, acquisition-related expenses and non-cash charges, and environmental remediation loss reserve

($M) LTM 3’31’17 1Q17 1Q16 FY16 FY15 FY14

Net (Loss) Income $(28.4) $(7.0) $(9.9) $(31.3) $(352.0) $(135.9)

Plus:

Interest Expense $ 173.2 $ 45.9 $ 43.0 $ 170.3 $ 162.9 $ 164.4

(Benefit) Provision for Income Taxes (20.3) (1.6) (13.2) (31.9) (14.7) 23.0

Depreciation & Amortization Expense 171.2 39.7 41.2 172.7 163.0 160.4

Impairment of Goodwill & Other Intangible Assets 25.3 - - 25.3 421.4 235.0

Sponsor Fees & Expenses 4.9 1.1 1.0 4.8 4.6 3.7

Restructuring & Related Business Transformation Costs 78.0 8.6 9.3 78.7 31.4 36.6

Acquisition Related Expenses and Non-Cash Charges 4.2 0.7 0.8 4.3 4.8 9.8

Environmental Remediation Loss Reserve 6.6 1.0 - 5.6 - -

Other Adjustments 1.3 3.7 4.6 2.2 (2.5) 40.6

Adjusted EBITDA $ 416.0 $92.1 $ 76.8 $ 400.7 $ 418.9 $ 537.6

32

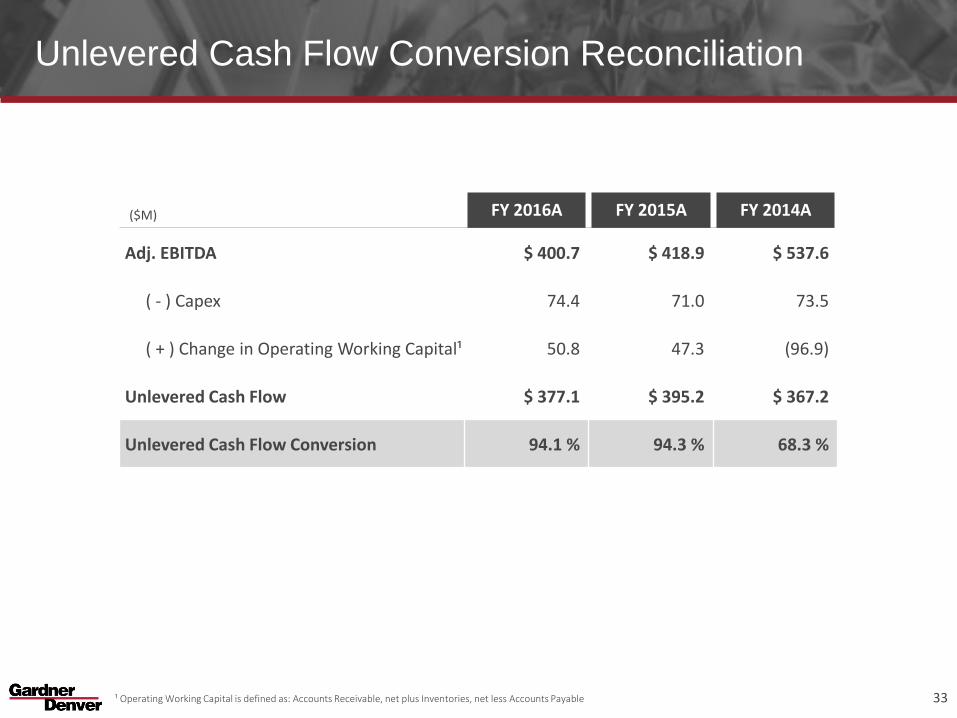

Unlevered Cash Flow Conversion Reconciliation

¹ Operating Working Capital is defined as: Accounts Receivable, net plus Inventories, net less Accounts Payable

($M) FY 2016A FY 2015A FY 2014A

Adj. EBITDA $ 400.7 $ 418.9 $ 537.6

( - ) Capex 74.4 71.0 73.5

( + ) Change in Operating Working Capital¹ 50.8 47.3 (96.9)

Unlevered Cash Flow $ 377.1 $ 395.2 $ 367.2

Unlevered Cash Flow Conversion 94.1 % 94.3 % 68.3 %

33

![Gardner Denver PZ-11revF3[1].Ppt](https://img.pdfslide.us/doc/110x75/552fb3f94a795943298b4570/gardner-denver-pz-11revf31ppt.jpg)