Embed Size (px)

Citation preview

Report to Congressional Addressees

March 2011

GAO-11-318SP

United States Government Accountability Office

GAO

Opportunities toReduce PotentialDuplication inGovernmentPrograms, Save Tax Dollars, and EnhanceRevenue

1

Contents

Letter

Section I GAO Identified Areas of Potential Duplication,

Overlap, and Fragmentation, Which, if Effectively

Addressed, Could Provide Financial and

Other Benefits 5

Section II Other GAO-Identified Cost-Saving and

Revenue-Enhancing Areas 155

Appendix I List of Congressional Addressees 334

Appendix II Objectives, Scope, and Methodology 336

Page i GAO-11-318SP

Abbreviations

AC Bureau of Arms Control AFR Agency Financial Report AFV alternative fuel vehicle AHLTA Armed Forces Health Longitudinal Technology

Application ARS Agricultural Research Service ATF Bureau of Alcohol, Tobacco, Firearms and Explosives AUR Automated Underreporter Program BEA business enterprise architecture BEST Border Enforcement Security Task Force BLM Bureau of Land Management BOEMRE Bureau of Ocean Energy Management, Regulation and

Enforcement BPA blanket purchase agreement BRAC base realignment and closure CBP Customs and Border Protection CDE Community Development Entities CFDA Catalog of Federal Domestic Assistance CDFI Community Development Financial Institution CERP Commander’s Emergency Response Program CIO Chief Information Officer CMS Centers for Medicare & Medicaid Services COBRA Consolidated Omnibus Budget Reconciliation Act of

1985 Commerce Department of Commerce Corrosion Office Office of Corrosion Policy and Oversight DHS Department of Homeland Security DLA Defense Logistics Agency DNDO Domestic Nuclear Detection Office DOD Department of Defense DOT Department of Transportation DSH Disproportionate Share Hospital EAS Essential Air Service Education Department of Education EDA Economic Development Administration EHR Electronic Health Record Energy Department of Energy EPA Environmental Protection Agency EPAct Energy Policy Act FAM Foreign Affairs Manual

Page ii GAO-11-318SP

FBI Federal Bureau of Investigation FCC Federal Communications Commission FDA Food and Drug Administration FEMA Federal Emergency Management Agency FFS fee-for-service FMCSA Federal Motor Carrier Safety Administration FPDS-NG Federal Procurement Data System-Next Generation FSIS Food Safety and Inspection Service FSSI Federal Strategic Sourcing Initiative FTA Federal Transit Administration FTHBC First-Time Homebuyer Credit Fund Universal Service Fund GAGAS generally accepted government auditing standards GHG greenhouse gas GPO Government Pension Offset GPRA Government Performance and Results Act GSA General Services Administration HHA home health agency HHS Department of Health and Human Services HUBZone Historically Underutilized Business Zone HUD Department of Housing and Urban Development IBET Integrated Border Enforcement Team IED improvised explosive device IG Inspector General Interior Department of the Interior IPERA Improper Payments Elimination and Recovery Act IRS Internal Revenue Service ISN Bureau of International Security and Nonproliferation ISR intelligence, surveillance, and reconnaissance IT information technology JIEDDO Joint IED Defeat Organization Justice Department of Justice Labor Department of Labor MAS Multiple Award Schedule MEA math error authority MHS Military Health System MPPR multiple procedure payment reduction NAFTA North American Free Trade Agreement NASA National Aeronautics and Space Administration NMTC New Markets Tax Credit NP Bureau of Nonproliferation NSLP National School Lunch Program

Page iii GAO-11-318SP

OFPP Office of Federal Procurement Policy OMB Office of Management and Budget ONRR Office of Natural Resources and Revenue O&S operating and support PAR Performance and Accountability Report PBL performance-based logistics PMS Payment Management System RAC recovery audit contractor RFS renewable fuel standard ROI return on investment S&T Science and Technology Directorate SBA Small Business Administration SNAP Supplemental Nutrition Assistance Program SPOT Screening of Passengers by Observation Techniques SSA Social Security Administration State Department of State STEM science, technology, engineering, and mathematics TANF Temporary Assistance for Needy Families Treasury Department of the Treasury TSA Transportation Security Administration USAC Universal Service Administrative Company USAID U.S. Agency for International Development USDA Department of Agriculture USICH U.S. Interagency Council on Homelessness VA Department of Veterans Affairs VC Bureau of Verification and Compliance VCI Bureau of Verification, Compliance and

Implementation VEETC Volumetric Ethanol Excise Tax Credit VistA Veterans Health Information Systems and Technology

Architecture WEP Windfall Elimination Provision WIA Workforce Investment Act WIC Special Supplemental Nutrition Program for Women,

Infants, and Children

This is a work of the U.S. government and is not subject to copyright protection in the United States. The published product may be reproduced and distributed in its entirety without further permission from GAO. However, because this work may contain copyrighted images or other material, permission from the copyright holder may be necessary if you wish to reproduce this material separately.

Page iv GAO-11-318SP

Page 1 GAO-11-318SP

United States Government Accountability Office

Washington, DC 20548

March 1, 2011

Congressional Addressees:

This is GAO’s first annual report to Congress in response to a new statutory requirement that GAO identify federal programs, agencies, offices, and initiatives, either within departments or governmentwide, which have duplicative goals or activities. Congress asked GAO to conduct this work and to report annually on our findings.1 This work will inform government policymakers as they address the rapidly building fiscal pressures facing our national government. GAO’s most recent update of its annual simulations of the federal government’s fiscal outlook underscores the need to address the long-term sustainability of the federal government’s fiscal policies. 2 Since the end of the recent recession, the gross domestic product has grown slowly and unemployment has remained at a high level. While the economy is still recovering and in need of careful attention, there is widespread agreement on the need to look not only at the near term but also at steps that begin to change the long-term fiscal path as soon as possible without slowing the recovery. With the passage of time, the window to address the challenge narrows and the magnitude of the required changes grows. GAO’s simulations show continually increasing levels of debt that are unsustainable over time absent changes in current fiscal policies.

The objectives of this report are to (1) identify federal programs or functional areas where unnecessary duplication, overlap, or fragmentation exists, the actions needed to address such conditions, and the potential financial and other benefits of doing so; and (2) highlight other opportunities for potential cost savings or enhanced revenues. To meet these objectives, we are including 81 areas for consideration based on related GAO work. This report is divided into two sections. Section I presents 34 areas where agencies, offices, or initiatives have similar or overlapping objectives or provide similar services to the same populations; or where government missions are fragmented across multiple agencies or

1Pub. L. No. 111-139, § 21, 124 Stat. 29 (2010), 31 U.S.C. § 712 Note.

2GAO, The Federal Government’s Long-Term Fiscal Outlook: Fall 2010 Update,

GAO-11-201SP (Washington, D.C.: Nov. 15, 2010). Additional information on the federal fiscal outlook, federal debt, and the outlook for the state and local government sector is available at: www.gao.gov/special.pubs/longterm/.

Comptroller General

of the United States

programs. These areas span a range of government missions: agriculture, defense, economic development, energy, general government, health, homeland security, international affairs, and social services. Within and across these missions, this report touches on hundreds of federal programs, affecting virtually all major federal departments and agencies. Overlap and fragmentation among government programs or activities can be harbingers of unnecessary duplication. Reducing or eliminating duplication, overlap, or fragmentation could potentially save billions of tax dollars annually and help agencies provide more efficient and effective services. The areas identified in this report are not intended to represent the full universe of duplication, overlap, or fragmentation within the federal government. We will continue to identify additional issues in future reports.

Given today’s fiscal environment, Section II of this report summarizes 47 additional areas—beyond those directly related to duplication, overlap, or fragmentation—describing other opportunities for agencies or Congress to consider taking action that could either reduce the cost of government operations or enhance revenue collections for the Treasury. These cost-savings and revenue opportunities also span a wide range of federal government agencies and mission areas. The issues raised in both sections were drawn from GAO’s prior and ongoing work.

Many of the issues included in this report are focused on activities that are contained within single departments or agencies. In those cases, agency officials can generally achieve cost savings or other benefits by implementing existing GAO recommendations or by undertaking new actions suggested in this report. However, a number of issues we have identified, particularly in the duplication area, span multiple organizations and therefore may require higher-level attention by the executive branch or enhanced congressional oversight or legislative action.

In some cases, there is sufficient information available today to show that if actions are taken to address individual issues summarized in this report, financial benefits ranging from the tens of millions to several billion dollars annually may be realized by addressing that single issue. For example, while the Department of Defense is making limited changes to the governance of its military health care system, broader restructuring could result in annual savings of up to $460 million. Similarly, we developed a range of options that could reduce federal revenue losses by up to $5.7 billion annually by addressing potentially duplicative policies designed to boost domestic ethanol production. Likewise, we identified a number of other opportunities for cost savings or enhanced revenues such

Page 2 GAO-11-318SP

as reducing improper federal payments totaling billions of dollars, or addressing the gap between taxes owed and paid, potentially involving billions of dollars. Collectively, these savings and revenues could result in tens of billions of dollars in annual savings, depending on the extent of actions taken.

In other cases, precise estimates of the extent of unnecessary duplication among certain programs, and the cost savings that can be achieved by eliminating any such duplication, are difficult to specify in advance of congressional and executive branch decision making. In some instances, needed information on program performance is not readily available; the level of funding in agency budgets devoted to overlapping or fragmented programs is not clear; and the implementation costs that might be associated with program consolidations or terminations, among other variables, are difficult to predict. For example, we identified 44 federal employment and training programs that overlap with at least one other program in that they provide at least one similar service to a similar population. However, our review of three of the largest programs showed that the extent to which individuals receive the same services from these programs is unknown due to program data limitations. In addition, Congress’ determinations in making policy decisions and actions that agencies may take would affect the potential savings associated with any given option.3 Nevertheless, considering the amount of program dollars involved in the issues we have identified, even limited adjustments could result in significant savings.

Given the challenges noted above, careful, thoughtful actions will be needed to address many of the issues discussed in this report, particularly those involving potential duplication. Additionally, in January 2011, the President signed the GPRA Modernization Act of 2010,4 updating the almost two-decades-old Government Performance and Results Act (GPRA).5 Implementing provisions of the new act—such as its emphasis on establishing outcome-oriented goals covering a limited number of crosscutting policy areas—could play an important role in clarifying

3The mandate calling for this report also asked GAO to identify specific areas where Congress may wish to cancel budget authority it has previously provided—a process known as rescission. To date, GAO’s work has not identified a basis for proposing specific funding rescissions.

4Pub. L. No. 111-352, 124 Stat. 3866 (2011).

5Pub. L. No. 103-62, 107 Stat. 285 (1993).

Page 3 GAO-11-318SP

desired outcomes, addressing program performance spanning multiple organizations, and facilitating future actions to reduce unnecessary duplication, overlap, and fragmentation.

As the nation rises to meet the current fiscal challenges, GAO will continue to assist Congress and federal agencies in reducing duplication, overlap, or fragmentation; achieving cost savings; and enhancing revenues. In GAO’s future annual reports, we will look at additional federal programs to identify further instances of duplication, overlap, or fragmentation, as well as other opportunities to reduce the cost of government operations or increase revenues to the government. Likewise, we will continue to monitor developments in the areas we have already identified. Issues of duplication, overlap, and fragmentation will be addressed in our routine audit work during the year as appropriate and summarized in our annual reports.

This report is based substantially upon work conducted for ongoing audits and previously completed GAO products, which were conducted in accordance with generally accepted government auditing standards or with GAO’s quality assurance framework, as appropriate. We conducted the work for the overall report from February 2010 through February 2011. For issues being reported on for the first time, GAO sought comments from the agencies involved and incorporated those comments as appropriate. Appendix II contains additional details of our scope and methodology.

This report was prepared under the coordination of Patricia Dalton, Chief Operating Officer, who may be reached at (202) 512-5600, or [email protected]; and Janet St. Laurent, Managing Director, Defense Capabilities and Management, who may be reached at (202) 512-4300, or [email protected]. Specific questions about individual issues may be directed to the area contact listed at the end of each summary.

Gene L. Dodaro Comptroller General of the United States

Page 4 GAO-11-318SP

Section I: GAO Identified Areas of Potential

Duplication, Overlap, and Fragmentation,

Which, if Effectively Addressed, Could

Provide Financial and Other Benefits

Section I: GAO Identified Areas of Potential Duplication, Overlap, and Fragmentation, Which, if Effectively Addressed, Could Provide Financial and Other Benefits

Table 1 presents 34 areas for consideration related to duplication, overlap, or fragmentation from GAO’s recently completed and ongoing work. In some cases, there is sufficient information to estimate potential savings or other benefits if actions are taken to address individual issues. In those cases, as noted below, financial benefits ranging from hundreds of millions to several billion dollars annually may be realized. In other cases, estimates of cost savings or other benefits would depend upon what congressional and executive branch decisions were made, including how certain GAO recommendations are implemented. Additionally, information on program performance, the level of funding in agency budgets devoted to overlapping or fragmented programs, and the implementation costs that might be associated with program consolidations or terminations, are factors that could impact actions to be taken as well as potential savings. Following the table are summaries for each of the 34 areas listed. In addition to summarizing what GAO has found, each area presents actions for the executive branch or Congress to consider. Each of the summaries contains a “Framework for Analysis” providing the methodology used to conduct the work and a list of related GAO products for further information.

Table 1: Duplication, Overlap, or Fragmentation Areas Identified in This Report

Missions Agriculture

Defense

Areas identified 1. Fragmented food safety system has caused inconsistent

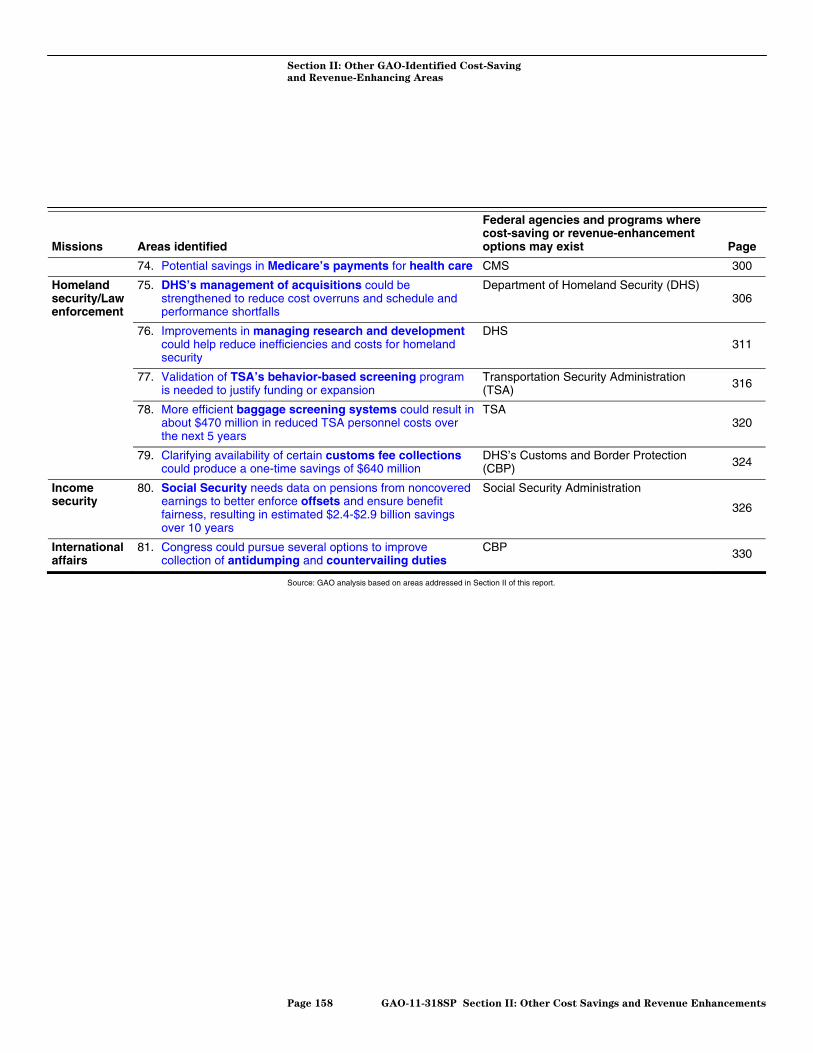

oversight, ineffective coordination, and inefficient use of resources

2. Realigning DOD’s military medical command structures and consolidating common functions could increase efficiency and result in projected savings ranging from $281 million to $460 million annually

3. Opportunities exist for consolidation and increased efficiencies to maximize response to warfighter urgent needs

Federal agencies and programs where duplication, overlap, or fragmentation may occur The Department of Agriculture’s (USDA) Food Safety and Inspection Service and the Food and Drug Administration are the primary food safety agencies, but 15 agencies are involved in some way Department of Defense (DOD), including the Office of the Assistant Secretary for Health Affairs, the Army, the Navy, and the Air Force At least 31 entities within DOD

Page

8

13

18

4. Opportunities exist to avoid unnecessary redundancies and improve the coordination of counter-improvised explosive device efforts

The services and other components within DOD 23

5. Opportunities exist to avoid unnecessary redundancies and maximize the efficient use of intelligence, surveillance, and reconnaissance capabilities

6. A departmentwide acquisition strategy could reduce DOD’s risk of costly duplication in purchasing Tactical Wheeled Vehicles

Multiple intelligence organizations within DOD

DOD, including Army and Marine Corps

26

31

Page 5 GAO-11-318SP Section I: Duplication, Overlap, or Fragmentation

Section I: GAO Identified Areas of Potential

Duplication, Overlap, and Fragmentation,

Which, if Effectively Addressed, Could

Provide Financial and Other Benefits

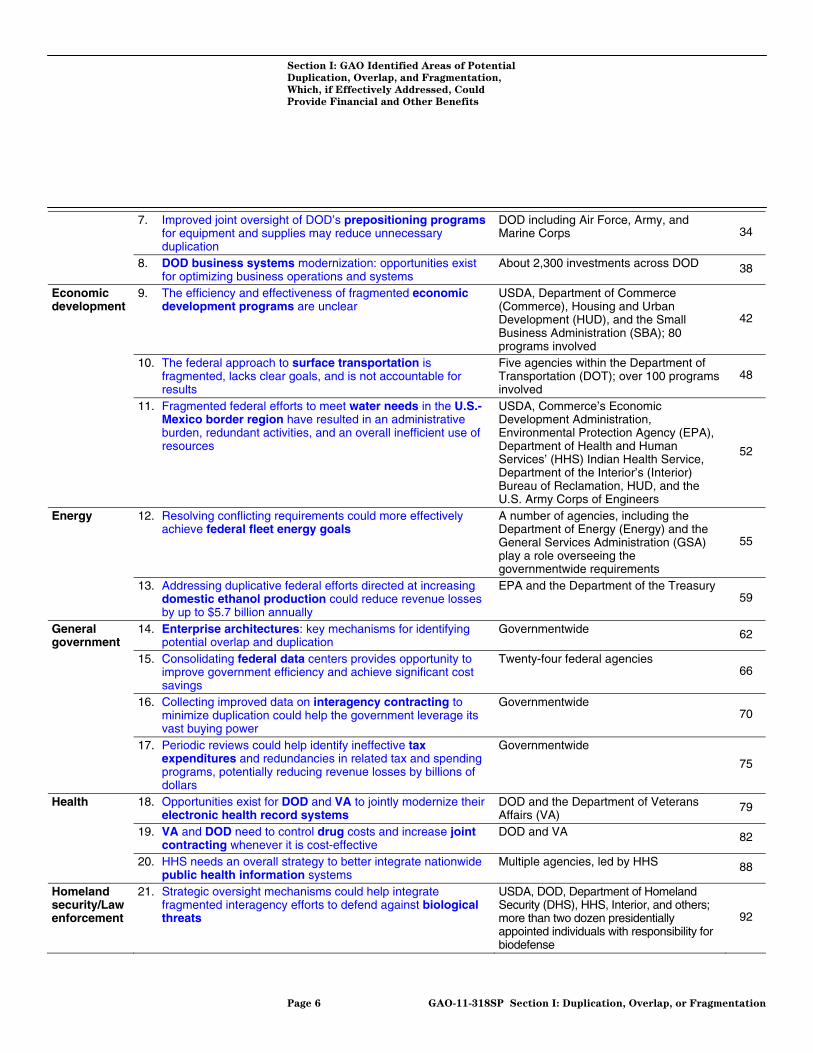

7. Improved joint oversight of DOD’s prepositioning programs for equipment and supplies may reduce unnecessary duplication

DOD including Air Force, Army, and Marine Corps 34

8. DOD business systems modernization: opportunities exist for optimizing business operations and systems

About 2,300 investments across DOD 38

Economic development

9. The efficiency and effectiveness of fragmented economic development programs are unclear

USDA, Department of Commerce (Commerce), Housing and Urban Development (HUD), and the Small Business Administration (SBA); 80 programs involved

42

10. The federal approach to surface transportation is fragmented, lacks clear goals, and is not accountable for

Five agencies within the Department of Transportation (DOT); over 100 programs 48

results involved 11. Fragmented federal efforts to meet water needs in the U.S. USDA, Commerce’s Economic

Mexico border region have resulted in an administrative Development Administration, burden, redundant activities, and an overall inefficient use of Environmental Protection Agency (EPA), resources Department of Health and Human

Services’ (HHS) Indian Health Service, 52

Department of the Interior’s (Interior) Bureau of Reclamation, HUD, and the U.S. Army Corps of Engineers

Energy 12. Resolving conflicting requirements could more effectively A number of agencies, including the achieve federal fleet energy goals Department of Energy (Energy) and the

General Services Administration (GSA) 55 play a role overseeing the governmentwide requirements

13. Addressing duplicative federal efforts directed at increasing EPA and the Department of the Treasury domestic ethanol production could reduce revenue losses 59 by up to $5.7 billion annually

General government

14. Enterprise architectures: key mechanisms for identifying potential overlap and duplication

Governmentwide 62

15. Consolidating federal data centers provides opportunity to Twenty-four federal agencies improve government efficiency and achieve significant cost 66 savings

16. Collecting improved data on interagency contracting to Governmentwide minimize duplication could help the government leverage its 70 vast buying power

17. Periodic reviews could help identify ineffective tax Governmentwide expenditures and redundancies in related tax and spending programs, potentially reducing revenue losses by billions of

75

dollars Health 18. Opportunities exist for DOD and VA to jointly modernize their

electronic health record systems DOD and the Department of Veterans Affairs (VA)

79

19. VA and DOD need to control drug costs and increase joint contracting whenever it is cost-effective

DOD and VA 82

20. HHS needs an overall strategy to better integrate nationwide public health information systems

Multiple agencies, led by HHS 88

Homeland 21. Strategic oversight mechanisms could help integrate USDA, DOD, Department of Homeland security/Law fragmented interagency efforts to defend against biological Security (DHS), HHS, Interior, and others; enforcement threats more than two dozen presidentially 92

appointed individuals with responsibility for biodefense

Page 6 GAO-11-318SP Section I: Duplication, Overlap, or Fragmentation

Section I: GAO Identified Areas of Potential

Duplication, Overlap, and Fragmentation,

Which, if Effectively Addressed, Could

Provide Financial and Other Benefits

22. DHS oversight could help eliminate potential duplicating DHS and other federal law enforcement efforts of interagency forums in securing the northern partners 96 border

23. The Department of Justice plans actions to reduce overlap in Department of Justice’s Federal Bureau explosives investigations, but monitoring is needed to of Investigation and Bureau of Alcohol, 101 ensure successful implementation Tobacco, Firearms and Explosives

24. TSA’s security assessments on commercial trucking DHS’s Transportation Security companies overlap with those of another agency, but efforts are Administration (TSA) and DOT 105 under way to address the overlap

25. DHS could streamline mechanisms for sharing security- Three information-sharing mechanisms related information with public transit agencies to help funded by DHS and TSA 111 address overlapping information

26. FEMA needs to improve its oversight of grants and establish DHS’s Federal Emergency Management a framework for assessing capabilities to identify gaps and Agency (FEMA); 17 programs involved 116 prioritize investments

International 27. Lack of information sharing could create the potential for Principally DOD and the U.S. Agency for affairs duplication of efforts between U.S. agencies involved in International Development 120

development efforts in Afghanistan 28. Despite restructuring, overlapping roles and functions still

exist at State’s Arms Control and Nonproliferation Bureaus Two bureaus within the Department of State (State)

123

Social 29. Actions needed to reduce administrative overlap among USDA, DHS, and HHS; 18 programs services domestic food assistance programs involved 125

30. Better coordination of federal homelessness programs may Seven federal agencies, including minimize fragmentation and overlap Department of Education (Education),

HHS, and HUD; over 20 programs 129

involved 31. Further steps needed to improve cost-effectiveness and USDA, DOT, Education, Interior, HHS,

enhance services for transportation-disadvantaged persons HUD, Department of Labor (Labor), and 134 VA; 80 programs involved

Training, 32. Multiple employment and training programs: providing Education, HHS, and Labor, among employment, and

information on colocating services and consolidating administrative structures could promote efficiencies

others; 44 programs involved 140

education 33. Teacher quality: proliferation of programs complicates Ten agencies including DOD, Education,

federal efforts to invest dollars effectively Energy, National Aeronautics and Space Administration, and the National Science

144

Foundation; 82 programs involved 34. Fragmentation of financial literacy efforts makes

coordination essential More than 20 different agencies; about 56 programs involved

151

Source: GAO analysis based on areas addressed in Section I of this report.

Page 7 GAO-11-318SP Section I: Duplication, Overlap, or Fragmentation

Fragmented Food Safety System Has Caused

Inconsistent Oversight, Ineffective

Coordination, and Inefficient Use of

Resources

Fragmented Food Safety System Has Caused Inconsistent Oversight, Ineffective Coordination, and Inefficient Use of Resources

Why GAO Is Focusing on This Area

The fragmented federal oversight of food safety has caused inconsistent oversight, ineffective coordination, and inefficient use of resources. Fifteen federal agencies collectively administer at least 30 food related laws. Budget obligations for the two primary food safety agencies—the Food and Drug Administration (FDA) and the U.S. Department of Agriculture’s (USDA) Food Safety and Inspection Service (FSIS)—totaled over $1.6 billion in fiscal year 2009. USDA is responsible for the safety of meat, poultry, processed egg products, and catfish and FDA is responsible for virtually all other food, including seafood. Three major trends also create food safety challenges: (1) a substantial and increasing portion of the U.S. food supply is imported, (2) consumers are eating more raw and minimally processed foods, and (3) segments of the population that are particularly susceptible to food-borne illnesses, such as older adults and immune-compromised individuals, are growing.

What GAO Has Found to Indicate Duplication, Overlap, or Fragmentation

For more than a decade, GAO has reported on the fragmented nature of federal food safety oversight. The 2010 nationwide recall of more than 500 million eggs due to Salmonella contamination highlights this fragmentation. FDA is generally responsible for ensuring that shell eggs, including eggs at farms such as those where the outbreak occurred, are safe, wholesome, and properly labeled and FSIS is responsible for the safety of eggs processed into egg products. In addition, while USDA’s Agricultural Marketing Service sets quality and grade standards for the eggs, such as Grade A, it does not test the eggs for microbes such as Salmonella. Further, USDA’s Animal and Plant Health Inspection Service helps ensure the health of the young chicks that are supplied to egg farms, but FDA oversees the safety of the feed they eat.

Oversight is also fragmented in other areas of the food safety system. For example, the 2008 Farm Bill assigned USDA responsibility for catfish, thus splitting seafood oversight between USDA and FDA. In September 2009, GAO also identified gaps in food safety agencies’ enforcement and collaboration on imported food. Specifically, the import screening system used by the Department of Homeland Security’s Customs and Border Protection (CBP) does not notify FDA’s or FSIS’s systems when imported food shipments arrive at U.S. ports. Without access to time-of-arrival information, FDA and FSIS may not know when shipments that require examinations arrive at the port, which could increase the risk that unsafe food could enter U.S. commerce. GAO recommended that the CBP Commissioner ensure that CBP’s new screening system communicates time-of-arrival information to FDA’s and FSIS’s screening systems and GAO continues to monitor their actions.

Page 8 GAO-11-318SP Section I: Duplication, Overlap, or Fragmentation

Fragmented Food Safety System Has Caused

Inconsistent Oversight, Ineffective

Coordination, and Inefficient Use of

Resources

Actions Needed and Potential Financial or Other Benefits

GAO has made numerous recommendations intended to address the fragmented federal oversight of the nation’s food supply. One key recommendation in October 2001 was to reconvene the President’s Council on Food Safety, which disbanded earlier that year. In response, the President created the Food Safety Working Group in 2009 to coordinate federal efforts and develop goals to make food safer. Through the working group, which is co-chaired by the Secretaries of Health and Human Services and Agriculture, federal agencies have begun collaborating in certain areas that cross regulatory jurisdictions— improving produce safety, reducing Salmonella contamination, and developing food safety performance measures. However, as a presidentially appointed working group its future is uncertain, and the experience of the Council on Food Safety, which disbanded less than 3 years after it was created, illustrates that this type of approach can be short lived. In addition, developing a results-oriented governmentwide performance plan for food safety, commissioning a detailed analysis of alternative organizational structures, and enacting comprehensive risk-based food safety legislation could help address fragmentation. In January 2007, GAO said that what remains to be done is to develop a governmentwide performance plan that is mission based, has a results orientation, and provides a cross-agency perspective. In July 2009, the Food Safety Working Group issued its key findings—a set of goals and actions for improving food safety. While the key findings are mission based and offer a cross-agency perspective, they are not fully results oriented. Further, the working group has not provided information about the resources that are needed to achieve its goals. As a next step, the Director of the Office of Management and Budget, in consultation with the federal agencies that have food safety responsibilities, should develop a governmentwide performance plan for food safety that includes results-oriented goals and performance measures and a discussion of strategies and resources. Without a governmentwide performance plan for food safety, decision makers do not have a comprehensive picture of the federal government’s performance on this crosscutting issue. In addition, the federal government does not formulate an overall budget for food safety, making it difficult for Congress to monitor the federal resources allocated to federal food safety oversight.

GAO, in October 2001, suggested that Congress consider commissioning the National Academy of Sciences or a blue ribbon panel to conduct a detailed analysis of alternative food safety organizational structures. A detailed analysis has yet to be commissioned and GAO reiterated its suggestion to Congress in February 2011. GAO and other organizations

Page 9 GAO-11-318SP Section I: Duplication, Overlap, or Fragmentation

Fragmented Food Safety System Has Caused

Inconsistent Oversight, Ineffective

Coordination, and Inefficient Use of

Resources

have identified alternative organizational structures that could be analyzed in more detail, including:

• a single food safety agency, either housed within an existing agency or established as an independent entity, that assumes responsibility for all aspects of food safety at the federal level;

• a single food safety inspection agency that assumes responsibility for food safety inspection activities, but not other activities, under an existing department, such as USDA or FDA;

• a data collection and risk analysis center for food safety that consolidates data collected from a variety of sources and analyzes it at the national level to support risk-based decision making; and

• a coordination mechanism that provides centralized, executive leadership for the existing organizational structure, led by a central chair who would be appointed by the president and have control over resources.

GAO, the National Academy of Sciences, and others have also suggested that Congress enact comprehensive risk-based food safety legislation. In May 2004, GAO reported that such legislation can provide the foundation for focusing federal oversight and resources on the most important food safety problems from a public health perspective. New food safety legislation that was signed into law in January 2011 strengthens a major part of the food safety system and expands FDA’s oversight authority. However, the law does not apply to the federal food safety system as a whole and GAO reiterated its suggestion for comprehensive, risk-based food safety legislation in February 2011. The European Union adopted comprehensive food safety legislation in 2004 intended to create a single, transparent set of food safety rules.

Although reducing fragmentation in federal food safety oversight is not expected to result in significant cost savings, new costs may be avoided by preventing further fragmentation, as illustrated by the approximately $30 million for fiscal years 2011 and 2012 that USDA officials had said they would have to spend developing and implementing the agency’s new congressionally mandated catfish inspection program. Subsequently, no funding was proposed for the program in the President’s fiscal year 2012 budget because of the need for considerable stakeholder engagement and regulatory development before its adoption and implementation. In addition, GAO has reported that user fees are means of financing federal

Page 10 GAO-11-318SP Section I: Duplication, Overlap, or Fragmentation

Fragmented Food Safety System Has Caused

Inconsistent Oversight, Ineffective

Coordination, and Inefficient Use of

Resources

services that can be designed to reduce the burden on tax payers and promote economic efficiency and equity. The Congressional Budget Office has estimated that if FSIS charged user fees, federal revenues would increase by $902 million in fiscal year 2011 and could offset inspection costs. FDA has proposed user fees in its fiscal year 2011 congressional budget request that it estimates could increase revenues by almost $194 million and could enable the agency to expand its food safety efforts.

GAO recognizes that reorganizing federal food safety responsibilities is a complex process. Further, GAO’s work on other agency mergers and transformations indicates that reorganizing food safety could have short-term disruptions and transition costs. However, reducing fragmentation and overlap could result in a number of nonfinancial benefits. GAO reported in March 2004 that integrating food safety oversight can create synergy and economies of scale and can provide more focused and efficient efforts to protect the nation’s food supply. In June 2008, GAO also reported that other countries that reorganized their food safety systems have experienced additional benefits, such as improved public confidence in the systems. For example, GAO reported that industry and consumer stakeholders generally had positive views of the reorganized food safety systems and said that transparency had improved.

Framework for Analysis

The information contained in this analysis is based on the related GAO products listed below. In addition, GAO reviewed relevant food safety reports and legislation, and interviewed officials from USDA, FDA, and the Office of Management and Budget. GAO also collected and analyzed information about the Food Safety Working Group, its activities, and its plan for food safety, as well as alternative organizational structures for food safety oversight.

Related GAO Products

High-Risk Series: An Update. GAO-11-278. Washington, D.C.: February 16, 2011.

Live Animal Imports: Agencies Need Better Collaboration to Reduce the

Risk of Animal-Related Diseases. GAO-11-9. Washington, D.C.: November 8, 2010.

Food Safety: Agencies Need to Address Gaps in Enforcement and

Collaboration to Enhance Safety of Imported Food. GAO-09-873. Washington, D.C.: September 15, 2009.

Page 11 GAO-11-318SP Section I: Duplication, Overlap, or Fragmentation

Fragmented Food Safety System Has Caused

Inconsistent Oversight, Ineffective

Coordination, and Inefficient Use of

Resources

Seafood Fraud: FDA Program Changes and Better Collaboration among

Key Federal Agencies Could Improve Detection and Prevention. GAO-09-258. Washington, D.C.: February 19, 2009.

Food Safety: Selected Countries’ Systems Can Offer Insights into

Ensuring Import Safety and Responding to Foodborne Illness. GAO-08-794. Washington, D.C.: June 10, 2008.

Oversight of Food Safety Activities: Federal Agencies Should Pursue

Opportunities to Reduce Overlap and Better Leverage Resources. GAO-05-213. Washington, D.C.: March 30, 2005.

Food Safety and Security: Fundamental Changes Needed to Ensure Safe

Food. GAO-02-47T. Washington, D.C.: October 10, 2001.

For additional information about this area, contact Lisa Shames at Area Contact (202) 512-3841 or [email protected].

Page 12 GAO-11-318SP Section I: Duplication, Overlap, or Fragmentation

Realigning DOD’s Military Medical Command

Structures and Consolidating Common

Functions Could Increase Efficiency and

Reduce Costs

Realigning DOD’s Military Medical Command Structures and Consolidating Common Functions Could Increase Efficiency and Reduce Costs

Why GAO Is Focusing on This Area

Department of Defense (DOD) components provide health care to over 9.6 million eligible beneficiaries, including U.S. military personnel, retirees, and their family members. With more than 130,000 military and government medical professionals, a large network of private health care providers, 59 DOD hospitals, and hundreds of clinics worldwide, DOD’s collective Military Health System (MHS) manages more than 200,000 medical visits and fills more than 300,000 prescriptions per day. Additionally, the MHS is an important source for education, military medical training, and research and development. However, MHS costs have more than doubled from $19 billion in fiscal year 2001 to $49 billion in 2010 and are expected to increase to over $62 billion by 2015. Studies by GAO and others over many years have identified opportunities to gain efficiencies and save costs by consolidating administrative, management, and clinical functions.

What GAO Has Found to Indicate Duplication, Overlap, or Fragmentation

The responsibilities and authorities for DOD’s military health system are distributed among several organizations within DOD with no central command authority or single entity accountable for minimizing costs and achieving efficiencies. Under the MHS’s current command structure, the Office of the Assistant Secretary of Defense for Health Affairs, the Army, the Navy, and the Air Force each has its own headquarters and associated support functions, such as information technology, human capital management, financial activities, and contracting. Additionally, the three services each have Surgeons General to oversee their deployable medical forces and operate their own health care systems. Moreover, while the Assistant Secretary of Defense for Health Affairs controls the Defense Health Program budget, this office does not directly supervise the services’ medical personnel.

In 2005, GAO identified DOD’s health care system as an example of a key challenge facing the U.S. government in the 21st century as well as an area in which DOD could achieve economies of scale and improve delivery by combining, realigning, or otherwise changing selected support functions. In 2001, a RAND Corporation study on reorganizing the MHS uncovered at least 13 studies since the 1940s that had addressed military health care organization. All but three of those studies had either favored a unified system or recommended a stronger central authority to improve coordination among the services. However, DOD has taken limited actions to date to consolidate common administrative, management, and clinical functions within its MHS.

Page 13 GAO-11-318SP Section I: Duplication, Overlap, or Fragmentation

Realigning DOD’s Military Medical Command

Structures and Consolidating Common

Functions Could Increase Efficiency and

Reduce Costs

In 2005, DOD formed a working group to develop an implementation plan for a joint medical command. This group in 2006 developed and evaluated several reorganization alternatives to promote effectiveness and efficiency in its medical command structure by increased sharing of resources, use of common operating processes, and reduction in duplicative functions and organizations. One alternative would have established a unified medical command similar to DOD’s unified transportation command; the second alternative would have established two separate commands—one to provide operational/deployable medicine and another to provide beneficiary care through military hospitals and contracted providers; and a third alternative would have designated one of the military services to provide all health care services across DOD.

Because of an inability to obtain a consensus among the services on which alternative to implement, the Under Secretary of Defense for Personnel and Readiness and the Assistant Secretary of Defense for Health Affairs presented a new concept which, in November 2006, the Deputy Secretary of Defense approved. This chosen concept directed seven smaller scale, incremental reorganization efforts designed to minimize duplicative layers of command and control where possible; reduce redundant efforts, personnel, and expenses; and leverage efficiencies through combining common service support functions being performed within each of the services, such as finance, information management and technology, human capital management, support, and logistics. However, the concept left the existing command structures of the three services’ medical departments over all military treatment facilities essentially unchanged. In updating its previous reviews, GAO found that DOD officials have made varying levels of progress in implementing four of the seven incremental steps.

More specifically, DOD is taking actions to (1) create a command, control, and management structure in DOD’s base realignment and closure (BRAC) markets (National Capital Area and San Antonio); (2) realign command and control of the Joint Medical Education Training Center in San Antonio; (3) colocate the Military Health System and service medical headquarters; and (4) consolidate all medical research and development under the Army Medical Research and Material Command. Progress on these actions has been facilitated by the fact that three of them are related to BRAC recommendations made in 2005 that DOD must complete by the BRAC statutory deadline of September 2011. According to officials, DOD has not implemented actions to (1) establish a Joint Military Health Service Directorate under Assistant Secretary of Defense for Health Affairs; (2) consolidate command and control in other locations with more than one DOD component providing military health care services; and

Page 14 GAO-11-318SP Section I: Duplication, Overlap, or Fragmentation

Realigning DOD’s Military Medical Command

Structures and Consolidating Common

Functions Could Increase Efficiency and

Reduce Costs

(3) realign current TRICARE Management Activity to focus on health plan management. The Office of the Assistant Secretary of Defense for Health Affairs has not provided guidance on how and when to accomplish the three remaining steps, and officials indicated that further action is not likely to occur until the results of a broader, ongoing DOD-wide organizational and efficiency assessment is completed.

For the three BRAC-related steps under way, DOD’s BRAC budget reporting1 indicates a net annual savings of $275 million after full implementation. However, DOD medical officials have expressed uncertainty as to whether these savings will be achieved because of changes that occurred within the MHS since the BRAC decision was made. For example, they point out that the care of casualties from operations in Iraq and Afghanistan and the congressional direction to provide “world class health care” in the National Capital Region have all significantly increased MHS costs.

Finally, GAO reported in July 2010 that DOD would benefit from enhanced collaboration among the services in their medical personnel requirements determination processes and recommended that DOD identify, develop, and implement cross-service medical personnel standards for common capabilities. The report made recommendations to each of the services to improve their medical personnel requirements determination processes. That report also recognized that while each of the services has unique operational medical capabilities, the day-to-day operations at military treatment facilities are very similar across the services and could be more collaboratively managed, and that DOD should identify the common medical capabilities that are shared across the services in their military treatment facilities that would benefit from the development of cross-service medical personnel standards. DOD replied that developing cross-service standards in specific medical functional areas where there is measurable benefit makes good sense, and the services generally agreed with the need for improvements to their respective requirements determination processes.

1DOD is required by section 2907 of the Defense Base Closure and Realignment Act of 1990, Pub. L. No. 101-510 (as amended by section 2831(b) of Pub. L. No. 109-163 (2006) and section 2711 of Pub. L. No. 110-417 (2008)) to, among other reporting requirements, estimate the total expenditures required and cost savings to be achieved by each closure and realignment. To calculate DOD’s expected BRAC annual savings, GAO used dollar amounts obtained from DOD’s budget submission for fiscal year 2011.

Page 15 GAO-11-318SP Section I: Duplication, Overlap, or Fragmentation

Realigning DOD’s Military Medical Command

Structures and Consolidating Common

Functions Could Increase Efficiency and

Reduce Costs

Actions Needed and Potential Financial and Other Benefits

To reduce duplication in its command structure and eliminate redundant processes that add to growing defense health care costs, DOD could take action to further assess alternatives for restructuring the governance structure of the military health care system. In 2007, GAO recommended that DOD needed to demonstrate a sound business case for proceeding with its chosen concept, including an analysis of benefits, costs, and risks of implementing that choice. Although not explicitly stated, such an analysis, to be complete, would require analyzing other alternatives such as a unified medical command. These analyses have not been conducted, and GAO’s ongoing review will seek to determine the extent to which DOD has developed an approach for implementing the remaining actions in its chosen concept. Without such actions, DOD is not in a sound position to assure the Secretary of Defense and Congress that it made an informed decision in implementing its chosen concept over other alternatives or whether it will have the desired impact on DOD’s MHS or achieve anticipated results.

In 2006, if DOD and the services had chosen to implement one of the three other alternatives studied by the DOD working group, a May 2006 report by the Center for Naval Analyses showed DOD could have achieved significant savings. GAO’s adjustment of those projected savings from 2005 into 2010 dollars indicates those savings could range from $281 million to $460 million annually depending on the alternative chosen and numbers of military, civilian, and contractor positions eliminated. The report largely focused on personnel as the primary source of potential savings or costs.2

However, the report indicated that these savings would require a long and potentially costly transition period to be realized. Additionally, the report stated that DOD’s ability to realize the potential savings depended crucially on clear command and control to make the necessary changes.

In his selection of the chosen option in 2006, the Deputy Secretary of Defense acknowledged that implementing the chosen concept may not achieve the estimated level of savings of implementing a unified medical structure but believed minimum annual savings of about $200 million ($221 million in 2010 dollars) was a realistic goal. Additionally, significant cost avoidance from improved performance once changes had been

2The Center for Naval Analyses categorized the potential savings into the following 10 areas: health care operations; comptroller operations; information management and information technologies; education and training; research and development; logistics; strategic planning; human capital management; force health protection and environmental health; and general headquarters.

Page 16 GAO-11-318SP Section I: Duplication, Overlap, or Fragmentation

Realigning DOD’s Military Medical Command

Structures and Consolidating Common

Functions Could Increase Efficiency and

Reduce Costs

implemented was anticipated. For example, in September 2010, DOD officials told GAO that they had identified about $30 million in annual savings from the reduction in contract medical staff among the newly established joint hospitals in the National Capital Region—one of the seven incremental steps of the chosen concept. Additionally, officials believe the colocation of the medical headquarters will provide improved collaboration and opportunities for consolidating their operations where possible.

Framework for Analysis

The information contained in this analysis is based on the GAO reports listed below as well as work updating the extent to which DOD has (1) conducted a cost benefit analysis of its chosen concept and (2) implemented its 2006 chosen concept. To do this, GAO obtained, reviewed, and discussed with DOD officials any analyses performed related to the chosen concept or other alternatives subsequently considered. Additionally, GAO reviewed DOD documents, policies, directives, briefings, and concept papers related to DOD’s 2006 chosen concept, as well as GAO’s prior findings and recommendations associated with this effort. In meetings with officials from OSD, the services’ medical departments, and other relevant offices, GAO obtained, analyzed, and discussed documents related to the status, costs, and results of the seven steps in the chosen concept. In obtaining oral comments, DOD officials said that they generally agreed with the facts and findings in this analysis.

Related GAO Products

Military Personnel: Enhanced Collaboration and Process Improvements

Needed for Determining Military Treatment Facility Medical Personnel

Requirements. GAO-10-696. Washington, D.C.: July 29, 2010.

Defense Health Care: DOD Needs to Address the Expected Benefits, Costs,

and Risks for Its Newly Approved Medical Command Structure. GAO-08-122. Washington, D.C.: October 12, 2007.

Defense Health Care: Tri-Service Strategy Needed to Justify Medical

Resources for Readiness and Peacetime Care. GAO/HEHS-00-10. Washington, D.C.: November 3, 1999.

For additional information about this area, contact Brenda S. Farrell at Area Contact (202) 512-3604 or [email protected].

Page 17 GAO-11-318SP Section I: Duplication, Overlap, or Fragmentation

Opportunities Exist for Consolidation and

Increased Efficiencies to Maximize Response

to Warfighter

Urgent Needs

Opportunities Exist for Consolidation and Increased Efficiencies to Maximize Response to Warfighter Urgent Needs

Why GAO Is Focusing on This Area

Forces in Iraq and Afghanistan have faced significant risks of mission failure and loss of life due to rapidly changing enemy threats. In response, the Department of Defense (DOD) established urgent needs processes to rapidly develop, modify, and field new capabilities, such as intelligence, surveillance, and reconnaissance (ISR) technology, and counter-improvised explosive devices (IED) systems. GAO identified at least 31 entities that play a role in DOD’s urgent needs processes and has estimated funding for addressing urgent needs through those entities to be at least $76.9 billion, since 2005.

GAO has identified challenges with the department’s fragmented guidance and GAO and others have raised concerns about the numbers and roles of the various entities and processes involved and the potential of overlap and duplication. With the shift in priority for overseas operations from Iraq to Afghanistan—a theater that may pose more complex long-term challenges—deployed or soon-to-deploy units will likely continue to request critical capabilities to help them accomplish their missions.

What GAO Has Found to Indicate Duplication, Overlap, or Fragmentation

Over the past two decades, the fulfillment of urgent needs has evolved as a set of complex processes within the Joint Staff, the Office of the Secretary of Defense, each of the military services, and the combatant commands to rapidly develop, equip, and field solutions and critical capabilities to the warfighter. DOD’s experience with the rapidly evolving threats in Iraq and Afghanistan has led to the expanded use of existing urgent needs processes, the creation of new policies, and establishment of new organizations to manage urgent needs and to expedite the development of solutions to address them. However, DOD has not comprehensively evaluated opportunities for consolidation across the department, even though concerns have been raised by the Defense Science Board, GAO, and others about the numbers and roles of the various entities and processes involved and the potential of overlap and duplication. For example, the Defense Science Board, in July and September 2009 reports, found that DOD has done little to adopt urgent needs as a critical, ongoing DOD institutional capability essential to addressing future threats, and has provided recommendations to the department about potential consolidations. Many DOD and military service officials stated that higher-level senior leadership needs to take decisive action to evaluate the breadth of DOD’s urgent needs activities to determine what opportunities may exist for reducing unnecessary duplication in staff, information technology, support, and funding.

Page 18 GAO-11-318SP Section I: Duplication, Overlap, or Fragmentation

Opportunities Exist for Consolidation and

Increased Efficiencies to Maximize Response

to Warfighter

Urgent Needs

Additionally, GAO found that overlap exists among urgent needs entities in the roles they play as well as the capabilities for which they are responsible. For example:

• There are numerous places for the warfighter to submit a request for an urgently needed capability. Warfighters may submit urgent needs, depending on their military service and the type of need, to one of the following different entities: Joint Staff J/8, Army Deputy Chief of Staff G/3/5/7, Army Rapid Equipping Force, Navy Fleet Forces Command or Commander Pacific Fleet, Marine Corps Deputy Commandant for Combat Development and Integration, Air Force Major Commands, Special Operations Requirements and Resources, or the Joint IED Defeat Organization. These entities then validate the submitted urgent need request and thus allow it to proceed through their specific process.

• Multiple entities reported a role in responding to similar types of urgently needed capabilities. GAO identified eight entities focused on responding to ISR capabilities, five entities focused on responding to counter-IED capabilities, and six entities focused on responding to communications, command and control, and computer technology. In some cases, duplication of efforts may have occurred—see related summaries in this report on the subjects of intelligence, surveillance, and reconnaissance systems and counter-improvised explosive devices.

The department is hindered in its ability to identify key improvements, including consolidation to reduce any overlap, duplication, or fragmentation because it lacks a comprehensive approach to manage and oversee the breadth of its urgent needs efforts. Specifically, DOD does not have a comprehensive, DOD-wide policy that establishes a baseline and provides a common approach for how all joint and military service urgent needs are to be addressed—including key activities of the process such as validation, execution, or tracking. For example, the Joint Staff, the Joint IED Defeat Organization, the military services, and the Special Operations Command have issued their own guidance that varies in terms of the key activities associated with processing and meeting urgent needs—including how an urgent needs statement is generated by the warfighter, validated as an urgent requirement, and tracked after a solution is provided. Furthermore, DOD does not have visibility over the full range of its urgent needs efforts. For example, DOD cannot readily identify the cost of its

Page 19 GAO-11-318SP Section I: Duplication, Overlap, or Fragmentation

Opportunities Exist for Consolidation and

Increased Efficiencies to Maximize Response

to Warfighter

Urgent Needs

departmentwide urgent needs efforts, which is at least $76.9 billion1 since 2005 based on GAO’s analysis. Additionally, DOD does not have a comprehensive tracking system, a set of universal metrics, and a senior-level focal point to lead the department’s efforts to fulfill validated urgent needs requirements. Without DOD-wide guidance and a focal point to lead its efforts, DOD risks having duplicative, overlapping, and fragmented efforts, which can result in avoidable costs.

Actions Needed and Potential Financial or Other Benefits

In the absence of a comprehensive DOD evaluation, GAO’s March 2011 report identified and analyzed several options, aimed at potential consolidations and increased efficiencies in an effort intended to provide ideas for the department to consider in streamlining its urgent needs entities and processes. These options include the following:

• Consolidate into one entity, within the Office of the Secretary of Defense, all the urgent needs processes of the services and DOD, while keeping at the services’ program offices the development of solutions.

• Consolidate entities that have overlapping mission or capability portfolios regarding urgent needs solutions.

• Establish a gatekeeper within each service to oversee all key activities to fulfill a validated urgent needs requirement.

• Consolidate within each service any overlapping activities in the urgent needs process.

The options GAO identified are not meant to be exhaustive or mutually exclusive. Rather, DOD would need to perform its own analysis, carefully weighing the advantages and disadvantages of options it identifies to determine the optimal course of action. Additionally, it must be recognized that many entities involved in the fulfillment of urgent needs have other roles as well. However, until DOD performs such an evaluation, it will remain unaware of opportunities for consolidation and increased efficiencies in the fulfillment of urgent needs.

1Estimate is based on funding data provided by urgent needs-related entities responding to our data collection instrument and includes funding for processing of urgent needs as well as development of solutions and some acquisition costs.

Page 20 GAO-11-318SP Section I: Duplication, Overlap, or Fragmentation

Opportunities Exist for Consolidation and

Increased Efficiencies to Maximize Response

to Warfighter

Urgent Needs

GAO’s March 2011 report recommended that the department develop comprehensive guidance that, among other things, creates a focal point to lead its urgent needs efforts. Additionally, GAO recommended that DOD’s Chief Management Officer evaluate potential options for consolidation to reduce overlap, duplication, and fragmentation and take appropriate action. DOD concurred with these recommendations. This is an issue that may warrant continuing congressional oversight. Timely and effective actions on these recommendations should improve DOD’s ability to address urgent warfighter needs in the most efficient and cost-effective manner by minimizing the risks of duplication, overlap, and fragmentation.

The information contained in this analysis is based on the related GAO Framework for products below.

Analysis

Related GAO Products

Warfighter Support: DOD’s Urgent Needs Processes Need a More

Comprehensive Approach and Evaluation for Potential Consolidation.

GAO-11-273. Washington, D.C.: March 1, 2011.

Warfighter Support: Improvements to DOD’s Urgent Needs Processes

Would Enhance Oversight and Expedite Efforts to Meet Critical

Warfighter Needs. GAO-10-460. Washington, D.C.: April 30, 2010.

Warfighter Support: Actions Needed to Improve Visibility and

Coordination of DOD’s Counter-Improvised Explosive Device Efforts.

GAO-10-95. Washington, D.C.: October 29, 2009.

Warfighter Support: Challenges Confronting DOD’s Ability to Coordinate

and Oversee Its Counter-Improvised Explosive Devices Efforts.

GAO-10-186T. Washington, D.C.: October 29, 2009.

Defense Management: More Transparency Needed over the Financial

and Human Capital Operations of the Joint Improvised Explosive

Device Defeat Organization. GAO-08-342. Washington, D.C.: March 6, 2008.

Defense Logistics: Lack of a Synchronized Approach between the Marine

Corps and Army Affected the Timely Production and Installation of

Marine Corps Truck Armor. GAO-06-274. Washington, D.C.: June 22, 2006.

Page 21 GAO-11-318SP Section I: Duplication, Overlap, or Fragmentation

Opportunities Exist for Consolidation and

Increased Efficiencies to Maximize Response

to Warfighter

Urgent Needs

Defense Logistics: Several Factors Limited the Production and

Installation of Army Truck Armor during Current Wartime Operations.

GAO-06-160. Washington, D.C.: March 22, 2006.

Defense Logistics: Actions Needed to Improve the Availability of Critical

Items during Current and Future Operations. GAO-05-275. Washington, D.C.: April 8, 2005.

Defense Logistics: Preliminary Observations on the Effectiveness of

Logistics Activities during Operation Iraqi Freedom. GAO-04-305R. Washington, D.C.: December 18, 2003.

For additional information about this area, contact William M. Solis at Area Contact (202) 512-8365 or [email protected].

Page 22 GAO-11-318SP Section I: Duplication, Overlap, or Fragmentation

Opportunities Exist to Avoid Unnecessary

Redundancies and Improve the Coordination

of Counter-Improvised Explosive Device

Efforts

Opportunities Exist to Avoid Unnecessary Redundancies and Improve the Coordination of Counter-Improvised Explosive Device Efforts

Why GAO Is Focusing on This Area

Improvised explosive devices (IED) continue to be the number one threat to U.S. troops. IED incidents in Afghanistan numbered 1,128 in the month of May 2010—a 120 percent increase over the prior year. In addition to Afghanistan incidents, the IED threat is increasingly expanding throughout the globe with over 300 IED events per month worldwide, according to the Joint IED Defeat Organization (JIEDDO). The Department of Defense (DOD) created this organization in 2006, reporting directly to the Deputy Secretary of Defense, to lead and coordinate all of DOD’s counter-IED efforts. While Congress has appropriated over $17 billion to JIEDDO through fiscal year 2010 to address the IED threat, other DOD components, including the Armed Services, have devoted at least $1.5 billion to develop their own counter-IED solutions.

What GAO Has Found to Indicate Duplication, Overlap, or Fragmentation

DOD created JIEDDO to lead and coordinate all of DOD’s counter-IED efforts, but many of the organizations engaged in the counter-IED-defeat effort prior to the creation of JIEDDO have continued to develop, maintain, and expand their own IED-defeat capabilities. GAO has preliminarily identified several instances in which DOD entities operate independently and may have developed duplicate counter-IED capabilities. For example, both the Army and the Marine Corps continue to develop their own counter-IED mine rollers with full or partial JIEDDO funding. The Marine Corps’ mine roller per unit cost is about $85,000 versus a cost range of $77,000 to $225,000 per unit for the Army mine roller. However officials disagree about which system is most effective, and DOD has not conducted comparative testing and evaluation of the two systems. Additionally, JIEDDO does not adequately involve the Services in its process to select initiatives. For example, the Navy developed a directed energy technology to fill a critical theater capability gap, yet JIEDDO later underwrote the Air Force’s development of the same technology for use in a different system. However, the Air Force has now determined that its system will not meet requirements and has deferred fielding it pending further study. This may have a negative impact on the continued development of this technology by the Navy or others for use in theater. For example, according to DOD officials, during the recent testing of the Air Force’s system, safety concerns were noted unique to that system that may limit warfighters’ willingness to accept the technology.

Eliminating unnecessary duplication and enabling effective coordination in counter-IED efforts is hindered, in part, because neither JIEDDO nor any other DOD organization has full visibility over all of DOD’s counter-IED efforts. GAO has recommended that DOD establish a DOD-wide database for all counter-IED initiatives to establish comprehensive visibility,

Page 23 GAO-11-318SP Section I: Duplication, Overlap, or Fragmentation

Opportunities Exist to Avoid Unnecessary

Redundancies and Improve the Coordination

of Counter-Improvised Explosive Device

Efforts

however, DOD has yet to develop such a tool. According to DOD officials, DOD had initiated a database—the Technology Matrix—to establish a comprehensive list of counter-IED efforts and the organizations sponsoring these efforts; however, DOD has not required its various organizations involved in developing counter-IED solutions to use this database nor otherwise taken action to ensure these organizations provide information to JIEDDO on their respective counter-IED efforts. Therefore, the database has not been as comprehensive as intended. To date, DOD’s senior leadership has not taken adequate action to facilitate improved visibility, coordination, and authority for JIEDDO to address these shortcomings. This lack of leadership attention may be another key factor contributing to the lack of full visibility and effective coordination of the wide range of counter-IED measures conducted throughout DOD. Consequently, DOD components and the Services continue to pursue counter-IED efforts independent of one another that may be redundant or overlapping.

Actions Needed and Potential Financial or Other Benefits

DOD has taken steps to address several of GAO’s prior recommendations regarding the improvement of its counter-IED programs, such as revising JIEDDO’s process for evaluating and implementing counter-IED solutions. However, 5 years after its coordination efforts began through JIEDDO, DOD has still not achieved full visibility over all of its counter-IED investments and resources nor has it required comprehensive data from all DOD components and the Services to enable effective coordination. JIEDDO has encountered difficulty obtaining information on all counter-IED efforts, in part, because according to JIEDDO officials, the Services and components are not inclined to share this information. Therefore, DOD’s senior leadership, to include the Deputy Secretary of Defense, should consider what actions the department can take to assure that JIEDDO can centrally collect information and coordinate efforts and whether it should enhance JIEDDO’s tools to ensure all information on DOD-wide counter-IED programs is centrally collected and evaluated to limit unnecessary duplication, overlap, and fragmentation. DOD leadership should also take a more active role to ensure investment decisions of each of the individual counter-IED activities are consistent with DOD’s overarching counter-IED goals and objectives and that they are pursued in a coordinated and efficient manner.

The information contained in this analysis is based on prior GAO products Framework for below, as well as GAO’s ongoing work on DOD’s counter-IED efforts. As part

Analysis of this ongoing work GAO will comprehensively identify, to the extent possible, all counter-IED organizations and efforts within DOD, and collect

Page 24 GAO-11-318SP Section I: Duplication, Overlap, or Fragmentation

Opportunities Exist to Avoid Unnecessary

Redundancies and Improve the Coordination

of Counter-Improvised Explosive Device

Efforts

quantitative data on these efforts such as the funds invested and the number of persons engaged in these efforts. Using these data, GAO will evaluate the nature and extent of any overlap or duplication, as well as the potential for consolidation, improved coordination, or other efficiencies. GAO is also evaluating DOD’s progress in improving visibility over all counter-IED efforts.

Related GAO Products

Warfighter Support: DOD’s Urgent Needs Processes Need a More

Comprehensive Approach and Evaluation for Potential Consolidation.

GAO-11-273. Washington, D.C.: March 1, 2011.

Warfighter Support: Actions Needed to Improve Visibility and

Coordination of DOD’s Counter-Improvised Explosive Device Efforts. GAO-10-95. Washington, D.C.: October 29, 2009.

Warfighter Support: Challenges Confronting DOD's Ability to Coordinate

and Oversee Its Counter-Improvised Explosive Devices Efforts. GAO-10-186T. Washington, D.C.: October 29, 2009.

Defense Management: More Transparency Needed over the Financial

and Human Capital Operations of the Joint Improvised Explosive

Device Defeat Organization. GAO-08-342. Washington, D.C.: March 6, 2008.

Defense Logistics: Lack of a Synchronized Approach between the Marine

Corps and Army Affected the Timely Production and Installation of

Marine Corps Truck Armor. GAO-06-274. Washington, D.C.: June 22, 2006.

Defense Logistics: Several Factors Limited the Production and

Installation of Army Truck Armor during Current Wartime Operations. GAO-06-160. Washington, D.C.: March 22, 2006.

Defense Logistics: Actions Needed to Improve the Availability of Critical

Items during Current and Future Operations. GAO-05-275. Washington, D.C.: April 8, 2005.

Defense Logistics: Preliminary Observations on the Effectiveness of Logistics Activities during Operation Iraqi Freedom. GAO-04-305R. Washington, D.C.: December 18, 2003.

For additional information about this area, contact William M. Solis at Area Contact (202) 512-8365 or [email protected].

Page 25 GAO-11-318SP Section I: Duplication, Overlap, or Fragmentation

Opportunities Exist to Avoid Unnecessary

Redundancies and Maximize the Efficient Use

of Intelligence, Surveillance, and

Reconnaissance Capabilities

Opportunities Exist to Avoid Unnecessary Redundancies and Maximize the Efficient Use of Intelligence, Surveillance, and Reconnaissance Capabilities

Why GAO Is Focusing on This Area

To plan and execute military operations in Iraq and Afghanistan, military commanders depend on intelligence, surveillance, and reconnaissance (ISR) systems to collect, process, and disseminate timely and accurate information on adversaries’ capabilities and vulnerabilities. The Department of Defense’s (DOD) ISR enterprise consists of multiple intelligence organizations that individually plan for, acquire, and operate manned and unmanned airborne, space-borne, maritime, and ground-based ISR systems. The success of ISR systems at providing key information has led to increased demand, and DOD continues to invest in ISR programs. For example, DOD requested about $6.1 billion in fiscal year 2010 for unmanned aircraft programs alone. DOD is further examining its airborne ISR budget needs for fiscal year 2012 and beyond. Further, GAO has reported since 2005 that ISR activities are not integrated and efficient; effectiveness may be compromised by lack of visibility into operational use of ISR assets; and agencies could better collaborate in the acquisition of new capabilities.

What GAO Has Found to Indicate Duplication, Overlap, or Fragmentation

ISR activities cut across services and defense agencies, and no single entity at the departmental level has responsibility, authority, and control over investments to prioritize resources to meet joint priority requirements. The ISR enterprise exhibits extensive, structural fragmentation with a high number of separate organizations sharing the same roles. For example, multiple ISR organizations conduct strategic planning, budgeting, and data analysis across intelligence disciplines. Although DOD has designated the Under Secretary of Defense for Intelligence to manage ISR investments as a departmentwide portfolio, the Under Secretary of Defense for Acquisition, Technology, and Logistics has been designated to lead the task force responsible for oversight of issues related to the management and acquisition of unmanned aircraft systems that collect ISR data. In addition, as the ISR portfolio manager, the Under Secretary of Defense for Intelligence has only advisory authority and cannot direct the services or agencies to make changes in their investment plans.

Further, two key factors make tracking DOD’s ISR spending difficult. First, funding for DOD’s ISR capabilities can come from several sources, including the Military Intelligence Program, the National Intelligence Program, and service budgets. Second, each service maintains or develops its own requirements process, budget, and strategic plans. For example, each service identifies its requirements and prioritizes spending for its equipment and personnel needs, and tracks and accounts for ISR funding differently.

Page 26 GAO-11-318SP Section I: Duplication, Overlap, or Fragmentation

Opportunities Exist to Avoid Unnecessary

Redundancies and Maximize the Efficient Use

of Intelligence, Surveillance, and

Reconnaissance Capabilities

The Secretary of Defense has identified ISR as an area of scrutiny for potential cost savings in the military intelligence program budget, which totals $27 billion in spending for fiscal year 2010 including ISR capabilities and personnel. In addition, the National Intelligence Program budget of $53.1 billion includes some resources for DOD ISR activities. Since 1988, GAO has reported on the potential for duplication and fragmentation in DOD’s unmanned ISR systems. Service-driven requirements and funding processes continue to hinder integration and efficiency and contribute to unnecessary duplication in addressing warfighter needs. Although several unmanned aircraft systems have achieved some commonality among the airframes they use, most are pursuing service-unique subsystems and components. The lack of collaboration and commonality among the services has led to duplicative costs for designing and manufacturing ISR systems, and has resulted in inefficiencies in the contracting and acquisition processes. For example in 2005, the Army initiated a development program with the same contractor for a variant of the Air Force Predator estimated to cost nearly $570 million, although the Predator was already successfully providing capabilities to the warfighter. Similarly, in 2009 GAO reported that, although the Navy expected to save time and money by using the Air Force’s existing Global Hawk airframe, the Navy also planned to spend over $3 billion to develop maritime surveillance capabilities. Conversely, the Marine Corps avoided the cost of initial system development and was able to quickly deliver a useful capability to the warfighter by choosing to procure existing Army Shadow systems rather than developing its own unmanned aircraft.

DOD has established numerous organizations and initiatives intended to integrate the determination of requirements, development, acquisition, and operation of ISR systems to address joint and service-specific needs, but these efforts have not had the desired effect of minimizing fragmentation and overlap in its ISR enterprise. For example, although the Under Secretary of Defense for Intelligence, as capability portfolio manager, updated the congressionally directed ISR Integration Roadmap, the Roadmap does not represent a comprehensive ISR architecture to guide service investments to meet joint needs. For example, the Roadmap does not enable comparison and tradeoffs between intelligence platforms and capabilities. In addition, the Joint Requirements Oversight Council, which is charged with validating requirements and approving proposals for new capabilities to meet joint capability gaps, has been generally ineffective in ensuring that the services collaborate in developing capabilities for joint requirements.

Page 27 GAO-11-318SP Section I: Duplication, Overlap, or Fragmentation

Opportunities Exist to Avoid Unnecessary

Redundancies and Maximize the Efficient Use

of Intelligence, Surveillance, and

Reconnaissance Capabilities