Embed Size (px)

Citation preview

El

Ec

tIo

n s

PE

cIa

l

Game changer? What the Indonesian presidential election means for the country’s oil and gas future.

03

RIsco InsIghts QuaRtERly: 01Risco Energy

Actor react

What can the oil and gas industry expect from Indonesia’s new president?

aRtIclE no.

Angus Graham, Risco Energy

01

No. 01: ELEcTION – act oR REact

On October 20th, Jakarta Governor Joko Widodo (“Jokowi”) will be inaugurated as Indonesia’s seventh president, having secured an absolute majority in the world’s biggest direct presidential election in July. To help inform debate about the election and its impact on the energy industry, we asked two independent experts, in Indonesian politics and investment respectively, for their views on the president-elect’s policies and ability to affect the country’s oil and gas future.

04E

lE

ct

Ion

sP

Ec

Ial

RIsco InsIghts QuaRtERly: 01

RIsco InsIghts QuaRtERly: 01Risco Energy

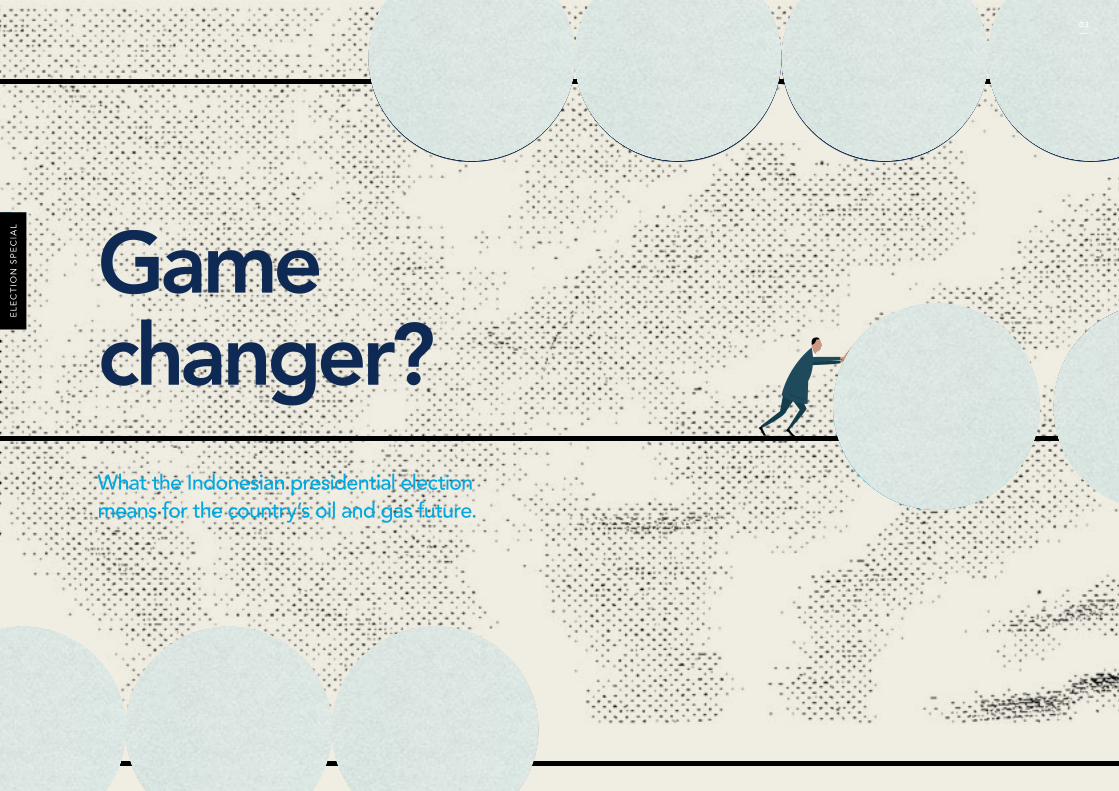

A critical element to Jokowi’s campaign

is Indonesia’s ongoing economic

prosperity and increased growth rate

targets. Indonesia’s energy sector is

a significant economic constituent,

representing 15.6% of GDP in 2012

with oil and gas alone providing 16%

of state revenues. However, production

in ASEAN’s historically dominant oil

and gas producer is stagnating in the

face of soaring demand, prompting an

ever-expanding deficit gap currently

being filled by imports. Imports have

fuelled pressure on the country’s

current and trade accounts, which will

only increase without increased oil

and gas production. This pressure is

exacerbated by fuel subsidies dating

back to Indonesia’s OPEC membership

(it exited in 2009), which currently cost

the government more than oil and

gas revenues.

In his analysis for Risco, Indonesian

political expert and commentator Kevin

Evans highlights the unique nature of the

president-elect as Indonesia’s democratic

evolution continues. For the first time,

Indonesia will have a president who

doesn’t hail from a traditional elite – the

former furniture maker, and subsequently

mayor of both Solo and Jakarta, entered

local politics less than a decade ago.

Indonesia’s oil and gas revenue vs fuel subsidy cost

The cost of fuel subsidies wipes out revenue from oil and gas

No. 01: ELEcTION – act oR REact

RIsco InsIghts QuaRtERly: 01

Source: CLSA

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

350

300

250

200

150

100

50

0

Oil and gas revenue

Energy subsidy

Year

Rup

iah

(tn)

Structural change

is needed

05

RIsco InsIghts QuaRtERly: 01Risco Energy

Kevin observes key attributes

engendering a strong ability to deliver

results, absent of historical hang-ups

and constraints. The question is the

direction such execution will take.

Kevin expects early action in reducing

fuel subsidies and ultimately an

incremental improvement in the

investment attractiveness of upstream

oil and gas for both domestic and

foreign participants, recognising the

significant execution hurdles for the

latter. Where Kevin diverges from the

currently accepted outlook of “positive

expectation, questionable timing on

delivery” is in Jokowi’s ability to

overcome these hurdles within a few

years, aided by vice-presidential

facilitator Jusuf Kalla.

Jayden Vantarakis, Deputy Head of

Indonesian Research at CLSA, Asia’s

leading independent equity brokerage,

sees change occurring more quickly.

He views GDP growth of 7%+ pa as a

priority for Jokowi. The current structural

energy trade deficit and fuel subsidies

represent significant barriers to achieving

this and will have to be dealt with. Jayden

believes this will compel the new president

and his government to implement

positive structural reform to encourage

oil and gas investment to in turn stimulate

higher production.

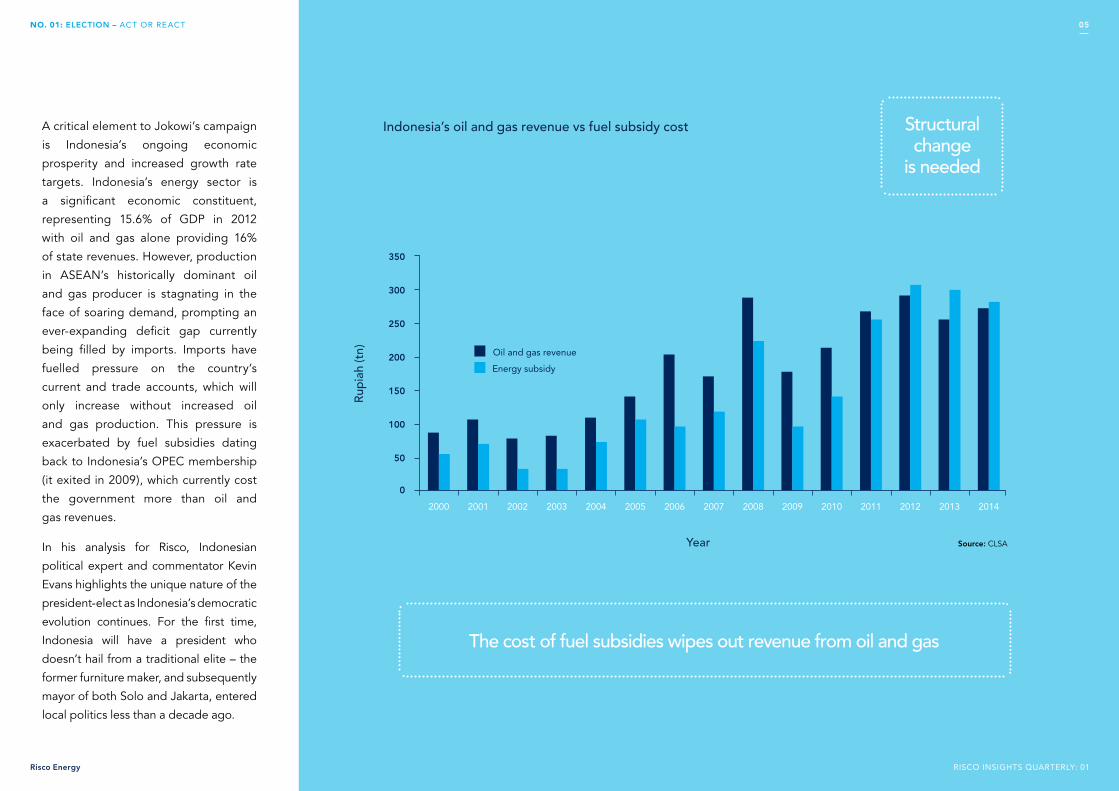

Oil and gas revenue as a proportion of total Indonesian government revenue

1990

40% 42%

28%

21%

16%

2000 2005 2010 2014

10%

15%

20%

25%

30%

35%

40%

45%

5%

0%

No. 01: ELEcTION – act oR REact

RIsco InsIghts QuaRtERly: 01

Year

% o

f tot

al g

over

nmen

t re

venu

e

Oil and gas are material to Indonesia – albeit proportionately less than before

06

Source: CLSA

Risco Energy

Both Kevin and Jayden see Indonesia’s overall economic performance as a key motivator for action. History would support this view, expressed by the outgoing administration’s articulate Minister of Finance as “good times lead to bad policy and bad times lead to good policy”. Both expect a first step of subsidy reduction. The difference in their views lies in the implicit timing: Jayden is confident the next government’s primary desire to protect targeted growth will quickly catalyse the creation of a more attractive oil and gas investment environment, while Kevin is quietly optimistic for improvement over the next few years.

One area of oil and gas investment that clearly seems set to receive greater support is domestic participants. This is potentially a welcome source of investment, although it is not a singular solution and is unlikely to make material impact on such a significant (and expanding) energy shortfall. Domestic oil and gas participants naturally face balance sheet, funding and skill constraints in an

00

industry that is highly capital and skills intensive. For Indonesia, it is set to become even more so as the industry seeks resources in the more challenging eastern and deepwater areas of the country. The president-elect recognises the part global capital and skills have to play if Indonesia’s oil and gas production is to be increased to deliver corresponding support to the country’s economy. The issue is whether the hurdles can be overcome. The traditional comment on this would be “time will tell” but recent history of Indonesia’s president-elect suggests that directional clarity will come quickly.

—

Angus Graham Risco Energy Strategy & Research

W: www.riscoenergy.com

RIsco InsIghts QuaRtERly: 01Risco Energy

No. 01: ELEcTION – act oR REact 07

RIsco InsIghts QuaRtERly: 01Risco Energy

And now the real work begins

What to expect after Indonesia’s presidential elections

aRtIclE no.

Kevin Evans, www.pemilu.asia

02

While the final “mop-up” of Indonesia’s post-election contestation unfolds, the presidential election has been won by Joko Widodo (Jokowi) and his vice- presidential partner Jusuf Kalla (former VP in the first Yudhoyono presidency from 2004 to 2009). The scale of victory for Jokowi, 53% versus the 47% obtained by his competitors Prabowo Subianto and his vice-presidential running mate Hatta Rajasa, was by far the closest in Indonesia’s history. Now the country, and the oil and gas industry, await Jokowi’s early actions as president and their impacts on Indonesia’s economy and energy industry.

No. 02: ELEcTION – and now thE REal woRk bEgIns

RIsco InsIghts QuaRtERly: 01

El

Ec

tIo

n s

PE

cIa

l08

RIsco InsIghts QuaRtERly: 01Risco Energy

No. 02: ELEcTION – and now thE REal woRk bEgIns

the new president What kind of president will Jokowi make? A unique one on many levels. Unlike all former presidents of Indonesia, Jokowi does not originate from any of the traditional elites, be that from an aristocratic, wealthy corporate or military background.

Arguably more important is that he is the first national-level leader to emerge since Indonesia’s transition to presidential democracy at the turn of the century. His political experiences are therefore very different to those of his predecessors, all of whom believed they needed a “majority” on the floor of the Parliament to be effective. Given Indonesia’s natural political pluralism, this has translated into multi-party presidential cabinets that traditionally deliver little coherence and no guarantee of parliamentary support when needed. As governor, Jokowi led the Region of Jakarta with only 20% party support in the Provincial Council but managed to make

progress on critical issues in less than two years where even former strongman President Soeharto failed to effect change. While Jokowi’s Jakarta-insider detractors may denigrate his lack of familiarity with national politics, I believe they are severely underestimating him. He has shown himself to be an effective mobiliser of political capital, adept at making an often lethargic and risk-adverse bureaucracy move forward.

Jokowi will be supported by his vice-presidential partner, a man already seen as a successful and can-do former vice president and the relationship between them will be an important dynamic during the next five years. Jokowi’s leadership model as mayor and governor has been to enjoy close, effective and mutually supportive relationships with his deputies, engendering loyalty and support for him and his programs.

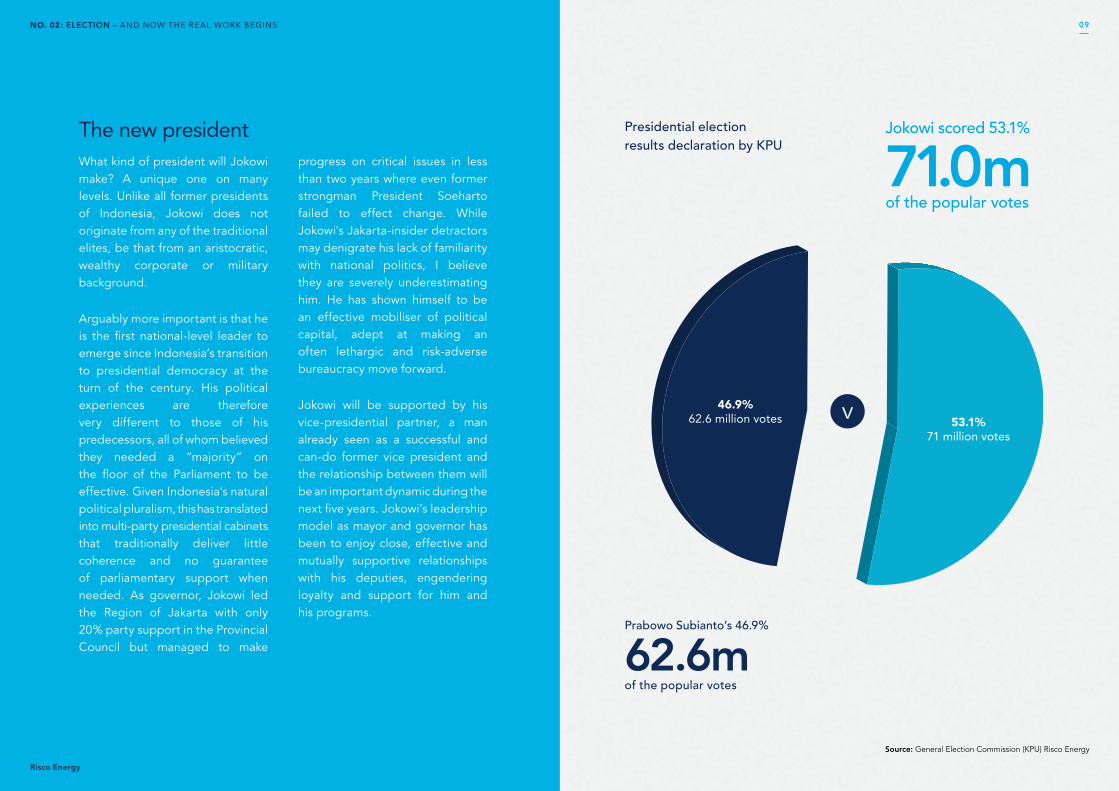

Presidential election results declaration by KPU

Jokowi scored 53.1%

71.0mof the popular votes

Source: General Election Commission (KPU) Risco Energy

Jokowi scored 53.15% (71m) of the popular votes, against his opponent Prabowo Subianto’s 46.85% (62.6m).Source: General Election Commission (KPU)

Presidential election results declaration by KPU

46.9%62.6 million votes 53.1%

71 million votes

v

Prabowo Subianto’s 46.9%

62.6mof the popular votes

Risco Energy

09

RIsco InsIghts QuaRtERly: 01Risco Energy

“Many members of both parties appear happy to align with the new president, but replacing their party leaders looks set to be a messy affair.”

the next stepsThe new president will be inaugurated around 20th October with a new Cabinet announced within the following week. As the inauguration approaches, Jokowi will focus on putting together a parliamentary support coalition, developing a “kitchen cabinet” to prepare for the transition, and identifying possible Cabinet ministers. Among the usually annoying distractions at the time of the inauguration of a new president is the clamour for instant results. No president since President Soeharto has managed to disregard this pressure so we should expect the incoming government to submit to demands for a 100 day program of initiatives.

At this stage critical components of the incoming coalition include Jokowi’s party PDIP, still led by former President Megawati, the National Democratic Party (a new party led by former Golkar heavyweight Surya Paloh) and the National Awakening Party founded by former President Wahid and now led by the current Minister of Manpower, Muhaimin Iskandar. Developments in parties that did not support Jokowi’s campaign will also be important.

Particular attention should be focused on the Golkar Party, currently led by big businessman, Aburizal Bakrie. His humiliating failure to launch his own presidential (or even vice-presidential)

candidacy, his party’s loss of 15 seats in the April legislative elections and his failure to align Golkar with the winning presidential candidate will not fall easy on this party that has enjoyed a place in every Cabinet since its foundation 50 years ago. The Islamist United Development Party, PPP, will also face great stress as its current leader has been named a suspect in a corruption case. Many members of both parties appear happy to align with the new president, but replacing their party leaders looks set to be a messy affair.

“we should expect the incoming government to submit to demands for a 100 day program of initiatives...”

No. 02: ELEcTION – and now thE REal woRk bEgIns 10

RIsco InsIghts QuaRtERly: 01Risco Energy

No. 02: ELEcTION – and now thE REal woRk bEgIns

Early impacts for oil and gasBased on positive experiences as Jakarta’s governor, Jokowi may look to place his stamp on the national bureaucracy early to make clear that a number of comfortable old practices are to be left behind. His firmly declared vision that Indonesia recall its maritime identity indicates an early and sustained focus on improvements in port and sea transport and related infrastructure.

One potential development that has particular relevance to Indonesia’s oil and gas industry, and significant impact on the country’s economy, is early action to slash fuel subsidies. Incoming Vice President Jusuf Kalla spearheaded the most daring program to redress the fiscal hole created by the fuel subsidies in 2005 when the government literally doubled the price of fuel. To head off the destabilising demonstrations that normally accompany fuel price rises, the government implemented an historic new move with direct cash payments to poor citizens.

The result was, in many respects, a revolution nobody noticed. It was an historic breakthrough in a country where poverty had always been defined collectively. For the first time in history

poor citizens were provided with cash payments for an adjustment period with the country’s extensive and trusted post office network providing the backbone for delivery. The roll out of price increases late in the Fasting Month certainly dented public enthusiasm for wild demonstrations while the payments to poor citizens cushioned the impact of fuel cost rises.

A major increase in fuel prices, even with targeted support for poor citizens, would certainly create space in the tight budget for the new government to look at other medium-term initiatives. Indirect impacts would also see the exchange rate improve (which in itself would be a net positive for the budget) although 1% to 2% would likely be added to inflation during the next year.

“It was an historic breakthrough in a country where poverty had always been defined collectively.”

RIsco InsIghts QuaRtERly: 01Risco Energy

11

RIsco InsIghts QuaRtERly: 01Risco Energy

wider oil and gas prospectsPresident-elect Jokowi recognises Indonesia’s need to prioritise energy self-sufficiency. In addition to addressing fuel pricing, his platform proposes to redress the long-term decline in national oil and gas production. Recognising that national oil production has halved over the past 20 years, Jokowi proposes a number of measures including accelerating the switch from oil to gas in the transport sector, promoting enhanced oil recovery in existing sites and implementing a major overhaul of the existing Oil and Gas Law. To kick-start the process he proposes an emergency government regulation in lieu of a law to redress some of the weaknesses in the existing legal regime that have created legal uncertainty.

While these moves look promising, a number of issues could unhinge efforts. Even an emergency government regulation requires initial in-principle acceptance from the Speakership of the Parliament and must then be endorsed by the Parliament as normal legislation by the end of the existing session. Failure to do so means the emergency regulation is deemed rejected and is abandoned in favour of the previous legislation. While this is rare, it is not impossible, and

may be used by a parliament seeking to impose its authority on a new president. Questions over the security of the passage of legislative changes will add to the legal uncertainty in the sector, certainly in the short term.

The role of foreign capital in the oil and gas sector is another issue. The recent rise of natural resource nationalism, while most aggressively felt in the mining sector, has also impacted the oil and gas sector. The president-elect has issued statements reflecting a view that foreign capital and expertise will help Indonesia boost its production. The countervailing view from those more closely aligned with his political opponents, suggests that Jokowi may need to expend some political capital to push back against these nationalist sentiments.

where policy making discretion is criminalisedOne further dynamic for the president-elect to face is his call for more “calibration” of the risks between reward and investment by private and state investments. This includes a call to update the fiscal payments and royalties system to take into account issues such as the realities of each oil field, net present value, internal rates of return, payback period, profitability ratio as well as geological factors.

Complicating the effective implementation of these very progressive breakthroughs relates, ironically, to another key and positive development in Indonesia over the past few years – the fight against corruption. In practical terms, the proposal to provide flexibility in determining conditions for revenue extraction from different production sites would fill almost all rational Indonesian policy makers these days with dread.

Any decision made using discretion in determining rates of royalties or production cuts, could be argued as a “corrupt” deal even where there was no evidence that either party misappropriated funds or resources for personal benefit. The simple assertion that the “state lost revenue”, arguing the state could have secured more money from the deal, could warrant the launch of a legitimate anti-corruption investigation.

The very broad interpretation of what amounts to corruption in Indonesia, while clearly designed to reduce the “wiggle room” for the corrupt, has also made it difficult for honest public servants and political leaders to make use of the policy-making discretion necessary to make good, fast and secure decisions.

“Even an emergency government regulation requires initial in-principle acceptance from the speakership of the Parliament.”

No. 02: ELEcTION – and now thE REal woRk bEgIns

RIsco InsIghts QuaRtERly: 01Risco Energy

12

RIsco InsIghts QuaRtERly: 01Risco Energy

capital “frenemies”Given the capital and technology intensity of operations in the oil and gas sector, it is almost impossible to imagine how expansion or transformation of the oil and gas sector can take place in Indonesia without foreign capital. While economic nationalists may dream

of using state funds to support the sector’s growth, the reality of tight fiscal conditions and the battle for these funds from other sectors limit this. Embracing reality means recognition that boosting national levels of production requires investments of capital and technology that the domestic market simply lacks. This is often easier said than done. Even so, as noted above, the president-elect does enjoy some autonomy from the national commercial vested interests associated with

the oil and gas sector and other nationalist groups that argue the country can have its cake (expand domestic production) and eat it too (do so without external capital and technology).

In many respects, the heaviest cloud over the Indonesian sky for investors is not new laws, adjustments in revenue sharing or the size of the fuel subsidy. Given experiences over the past few years, certainly in the mining sector, the key question facing foreign investors is whether the new president will be setting a welcome mat or a “keep out” sign in front of all these potentially positive Indonesian developments. While recent history might suggest the latter, the president-elect’s reputation as a problem solver may well come to the fore in dealing with a problem like long-term declines in production. I believe there is finally reason for quiet optimism that a welcome mat may unfold within a couple of years.

“the key question facing foreign investors is whether the new president will be setting a welcome mat or a ‘keep out’ sign.”

—

kevin Evans Founder, Pemilu

E: [email protected]: www.pemilu.asia

No. 02: ELEcTION – and now thE REal woRk bEgIns

Risco Energy

13

RIsco InsIghts QuaRtERly: 01Risco Energy

Oil and gas reform is essential for growth

How the sector will help the new government lift Indonesia’s economy

aRtIclE no.

Jayden Vantarakis, CLSA

03

No. 03: ELEcTION – oIl and gas REFoRM

It is difficult to assess the likely impact of the recent presidential election on Indonesia’s oil and gas industry without first considering the country’s broader economy and its recent performance. We consider broader economic factors to be key in determining the potential for structural reform in Indonesia’s oil and gas sector following the election of the nation’s new president.

El

Ec

tIo

n s

PE

cIa

l

RIsco InsIghts QuaRtERly: 01

14

RIsco InsIghts QuaRtERly: 01Risco Energy

Indonesia was given a shock in the second half of 2013 that rekindled memories of the painful Asian financial crisis of the late 90s. The Indonesian Rupiah – seen rightly as a barometer of confidence in the country – swiftly declined 24% to levels above Rp12,000 against the US dollar. The currency has since hovered between Rp11,000 and Rp12,000 during 2014. The key reason for the decline is Indonesia’s growing current account deficit and international investors’ aversion to funding deficit countries – and particularly emerging markets – as the global economic situation shows signs of recovering. Indonesia’s current account deficit widened during 2013 to 4.5% of GDP. The Central Bank has now set about keeping it in check at a maximum 2.5% of GDP, a level it argues is supported by a baseline portfolio and foreign direct investment flows.

The inevitable consequence of narrowing the current account deficit is slower imports and consumption and therefore slower economic growth. Higher interest rates have dampened imports (the Central Bank has lifted the policy rate by 1.75% to 7.5% and there is talk of more tightening) and a failure by Indonesia to address infrastructure bottlenecks and labour laws during the past four years of cheap global money means exports are not taking up the slack. After enjoying

years of above 6% real GDP growth, Indonesia has become complacent. In the first quarter of 2014 real GDP growth slowed to 5.2% and looks set to remain subdued.

Turning our attention to the performance of the country’s energy market within this broader economic context, we estimate that Indonesia will become a net importer of energy, in monetary terms,

sometime between 2014 and 2017. This is driven by continued subdued thermal coal prices, rising unchecked oil consumption fuelled by wasteful subsidies, and stagnating oil and gas output. If Indonesia pursues a path of industrial development to drive further growth, we estimate that its energy needs will continue to rise, increasing from an estimated US$100bn in 2012 to US$190bn in five years’ time. On the production

side, oil output continues to slide, now 20% short of Indonesia’s elusive one million barrels per day target with less than 10 years’ reserves and flat gas production.

Without addressing the structural energy trade deficit Indonesia is now saddled with thanks to years of regressive policy in the oil and gas sector, the country is facing the prospect of even slower economic growth in the years to come. It also restricts state finance and the ability of the new president to carry out other economic programs.

The Indonesian rupiah

swiftly declined

24% to levels above 12,000against the US dollar late 2013

00

RIsco InsIghts QuaRtERly: 01Risco Energy

No. 03: ELEcTION – oIl and gas REFoRM 15

RIsco InsIghts QuaRtERly: 01Risco Energy

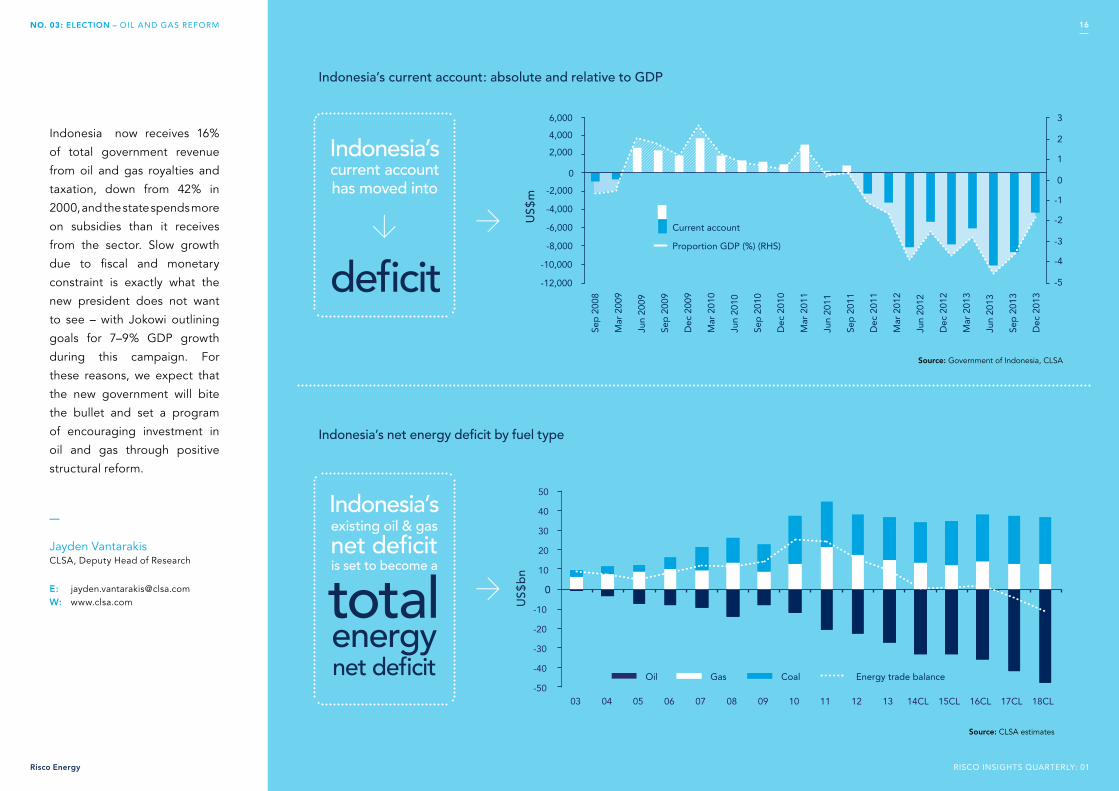

Indonesia now receives 16%

of total government revenue

from oil and gas royalties and

taxation, down from 42% in

2000, and the state spends more

on subsidies than it receives

from the sector. Slow growth

due to fiscal and monetary

constraint is exactly what the

new president does not want

to see – with Jokowi outlining

goals for 7–9% GDP growth

during this campaign. For

these reasons, we expect that

the new government will bite

the bullet and set a program

of encouraging investment in

oil and gas through positive

structural reform.

6,000 3

2

1

0

-1

-2

-3

-4

-5

4,000

2,000

0

-2,000

-4,000

-6,000

-8,000

-10,000

-12,000

Current account

Proportion GDP (%) (RHS)

Sep

200

8

Mar

200

9

Jun

2009

Sep

200

9

Dec

200

9

Mar

201

0

Jun

2010

Sep

201

0

Dec

201

0

Mar

201

1

Jun

2011

Sep

201

1

Dec

201

1

Mar

201

2

Jun

2012

Dec

201

2

Mar

201

3

Jun

2013

Sep

201

3

Dec

201

3

-50

-40

-30

-20

-10

0

10

20

30

40

50

03 04 05 06 07 08 09 10 11 12 13 14CL 15CL 16CL 17CL 18CL

Oil Gas Coal Energy trade balance

Indonesia’s net energy deficit by fuel type

Source: Government of Indonesia, CLSA

Source: CLSA estimates

Indonesia’s current account: absolute and relative to GDP

Indonesia’scurrent accounthas moved into

deficit

Indonesia’sexisting oil & gas

net deficitis set to become a

totalenergynet deficit

—

Jayden VantarakisCLSA, Deputy Head of Research

E: [email protected]: www.clsa.com

No. 03: ELEcTION – oIl and gas REFoRM

RIsco InsIghts QuaRtERly: 01

US$

bn

US$

m

16

RIsco InsIghts QuaRtERly: 01Risco Energy

Read more insights and commentary from Risco at riscoenergy.com/insightsthis report is prepared for general information purposes only. any third party seeking to rely upon this report should seek separate professional advice in relation

to any of the facts or opinions set out herein. Risco Energy Investments Pte ltd, its affiliates, its and their directors, officers and employees, and the consultants

producing this report (“Risco”) do not assume and hereby expressly disclaim any liability to any third party in respect of the contents of this report or any opinions

or conclusions which might be drawn from it. any third party using or otherwise relying upon the contents of this report does so entirely at its own risk, and any such

reliance shall be construed as a waiver of any claim against any party comprising Risco in respect of the contents of this report.

Risco Energy is an investment company focused on upstream oil and gas in ASEAN