Embed Size (px)

Citation preview

G89.2247 Lecture 8 1

G89.2247Lecture 8

• Comparing Measurement Models across Groups

• Reducing Bias with Hybrid Models

• Setting the Scale of Latent Variables

• Thinking about Hybrid Model Fit

• Recap of Measurement Model Issues

G89.2247 Lecture 8 2

Strategies for Comparing Groups

• Are all paths exactly the same?

• Are all paths except the residual variances the same?

• Are residual variances and factor variances different?

• Are loadings the same, but factor correlations, variances and residual variances different?

• Are correlations the same, but variances and loadings different?

G89.2247 Lecture 8 3

Payoff of Measurement Models in SEMBias Reduction

• Measures often are contaminated by noise Transient changes in subjects, random variation in rater

selection, instrument failures, and so on.

• Noise in explanatory variables leads to biased structural effects

• Noise in covariates or control variables leads to underadjusted (biased) structural effects of variables that are measured perfectly

• Hybrid models (when properly specified) reduce or eliminate bias

G89.2247 Lecture 8 4

Psychometric details of bias

• Suppose we have the simple structural model Y = b0 + b1X + r.

b0 and b1 can be estimated without bias if X is measured without error

• Suppose X*=X+e is a contaminated version of XSuppose e~N(0,), Then E(X*)=X

• If we estimate Y = b*0 + b*

1X* + r*

• b*1 = RXXb1 , where RXX is the reliability coefficient for X*

G89.2247 Lecture 8 5

Example of Bias: Single Predictor

• I simulated a data set with N=1000 withX2 = 24 .5*X1 + r

I then created added a version X1A of X (by adding error variance equal to the variance of X). Several noisy versions can be created.

• These have RXX of .50

• See SPSS listing

Compare regressions of error free variables with noisy variables

G89.2247 Lecture 8 6

Example of Bias: Single Predictor

• Simulated (true) model:X2 = 24 - .5*X1

• Estimate of true modelX2 = 25.154 + .480*X1

• Estimate of model when variables have reliability of .5X2A = 20.863 + .273*X1A

• Note that coefficient is about .5 less than true value

G89.2247 Lecture 8 7

Example of Bias: Two Predictors

• Measurement error of an independent variable in multiple regression has two effectsIts own coefficient is biasedIt incompletely adjusts other variables for its effect

• Adjustment is an important reason for multiple regressionWe may want to adjust for selection effects by

including measures of social class, IQ, depressed affect and so on

G89.2247 Lecture 8 8

Example of Bias continued:Two Predictors

• Simulated (true) model:Y = -14.1 + .4*X1 + .6*X2

• Estimate of true modelY = -12.76 + .375*X1 + .546*X2

• Estimate of model when variables have reliability of .5Y = -1.587 + .096*X1 + .194*X2

• Note that the bias is not a simple function of RXX

G89.2247 Lecture 8 9

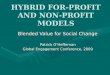

Hybrid Model: Taking Measurement Error into Account

1.02

LV1

DV1A

.94

E1

1.00

1

DV1B

.96

E2

1.04

1

DV1C

1.03

E3

.92

1

1.15

LV2

DV2A

.86

E6

1.00

1DV2B

1.10

E5

.85

1DV2C

1.02

E4

.94

1

LV3

DV3A

1.04

E71.001

DV3B

.92

E81.09 1

DV3C

1.02

E9

1.031

.45

.30

-.53

.67

RES3

1

G89.2247 Lecture 8 10

Setting the Scale of Latent Variables

• The latent variables can be scaled to have variance 1

• They can also be scaled to have units like the original indicators

• The indicators themselves do not have to be in the same units, so long as the units are linearly relatedE.G. inches, mm, cm

G89.2247 Lecture 8 11

Setting the Scale, Continued

• In simple confirmatory factor analysis we tend to set the variance of latent variables to 1.0

• In hybrid models, we tend to set the scale of the latent variables to the units that have meaning for the structural modelChoosing the "best" indicator to have loading set to

1.0Standardized versions of the analysis are always

available as well

G89.2247 Lecture 8 12

Fit of Hybrid Models

• Hybrid models may not fit for two reasonsMeasurement partStructural part

• Kline and others recommend a two step model fit exerciseTest fit of CFA with no structural modelImpose additional constraints due to structural

modelDon't claim validity for structural model that arises

from a good fitting measurement model

G89.2247 Lecture 8 13

How Fitted Variances and Covariances are Represented in EQS, AMOS, LISREL

• Consider nine variable system with three latent variables

EQS LISREL

E5

V1

V2

V3

V4

V5

V6

V7

V8

V9

F1

F2

F3

E1

E9

E8

E7

E6

E4

E3

E2

D3

D2

X1

X2

X3

Y1

Y2

Y3

Y4

Y5

Y6

G89.2247 Lecture 8 14

Structural Equation Forms

EQS LISREL V1 = *F1 + E1 X1 = X V2 = *F1 + E2 X2 = X V3 = *F1 + E3 X3 = X V4 = *F2 + E4 Y1 = Y V5 = *F2 + E5 Y2 = Y V6 = *F2 + E6 Y3 = Y V7 = *F3 + E7 Y4 = Y V8 = *F3 + E8 Y5 = Y V9 = *F3 + E9 Y6 = Y F2 = *F1 + D2 F3 = *F1 + *F2 + D3

G89.2247 Lecture 8 15

Matrix Algebra Version of LISRELLISREL

X1 = X X2 = X X3 = X Y1 = Y Y2 = Y Y3 = Y Y4 = Y Y5 = Y Y6 = Y

X = X

Y = Y

=

G89.2247 Lecture 8 16

Variances of Exogenous Variables (in LISREL)

• The variances of the predicted (endogenous) variables are calculated from the structural models

• The variances of the exogenous variables, however, must be specified (defined):Var(

Var(

Var(Var

G89.2247 Lecture 8 17

Variances of Endogenous Variables Can be Expressed as Functions of Parameters

• Var(X) = Var(X) = XXT

• Var(Y) = Var(Y) = Y[Var()]YT

• Var() = Var)]

= Var()[]T

=[T[]T

G89.2247 Lecture 8 18

Voila! The Fitted Variance/Covariance Matrix Can Be Written

εTY

T1T1Y

T1Y

TY

T1TXδ

TXX

θΛΒΙΨΓΦΓΒΙΛΓΦΛΒΙΛ

ΛΒΙΦΓΛθΦΛΛ

X

)()(

)()(

YVarYXCov

XYCovXVarT

T

• Once the form of the model is specified, and the parameters indicated, we can begin to fit the variance covariance matrix of the data.

G89.2247 Lecture 8 19

Issues in Measurement Models

• Model identification• Number of factors• Second order factor models?• Scaling of latent variables • Influence of parts of model on overall fit• Naming of latent variables• Reification of latent variables• Items, Item parcels• Overly simple factor models