Embed Size (px)

Citation preview

MBA – Final Year Project

Customer Satisfaction with technology based services provided

by banking sector

By: Syed Yasir HussainMBA – 08 - 0849

I

FINAL YEAR PROJECT ONCUSTOMER SATISFACTION WITH TECHNOLOGY BASED

SERVICES PROVIDED BY BANKING SECTOR

PREPARED BY:SYED YASIR HUSSAIN (08-0849)

SUPERVISED BY:ZAKI RASHIDI

SUBMISSION DATE:MAY 9, 2009

DEPARTMENT OF MANAGEMENT SCIENCES

MASTERS OF BUSINESS ADMINISTRATION 2008 – BATCH

NATIONAL UNIVERSITY OF COMPUTER AND EMERGING SCIENCES-FAST

II

Acknowledgement

Thanks to Allah for providing me the strength, courage, direction and skills to learn,

acquire knowledge and the ability to accept and meet challenges.

Secondly I would like to thank all those who have helped in performing this research

especially my family members for their support and my colleagues Mr. Mashood &

Mr. Sabih

I would like to appreciate all those people who give their precious time to guide me

and to fill questionnaires. I would like to express my sincere gratitude to my

Supervisor and FYP-Coordinator Mr. Zaki Rashidi for his continuous guidance and

support throughout the FYP.

I hope this project will be beneficial for the students to come in FAST after us. Once

again I would like to thank all those who have been involved directly or indirectly in

this project.

III

Table of Contents

Acknowledgement IIIList of Tables IList of Figures IExecutive Summary II1.0 Chapter – I Introduction 1

1.1 Introduction:..................................................................................................................1

1.1.1 Background.......................................................................................................2

1.1.2 Purpose.............................................................................................................2

1.1.3 Objectives.........................................................................................................3

1.2 Banking Sector:.........................................................................................................4

1.2.1 Overview of Banking Industry of Pakistan........................................................4

1.2.2 Opportunities & Challenges..............................................................................5

1.3 Customer Satisfaction:..............................................................................................8

1.3.1 Customer Satisfaction.......................................................................................8

1.3.2 Customer Satisfaction in Service Industry........................................................8

1.3.3 The Need to Measure Customer Satisfaction...................................................9

1.3.4 Measuring Customer Satisfaction with e-services............................................9

1.3.5 Different models & variables for measuring customer satisfaction................10

1.4 Technology Based Services:....................................................................................11

1.4.1 Overview of e-banking....................................................................................11

1.4.2 Types of e-banking services............................................................................11

1.4.3 Growth of e-banking in Pakistan.....................................................................12

1.4.4 Benefits of e-banking......................................................................................14

1.4.5 Challenges faced by e-banking industry.........................................................14

1.5 Customer Satisfaction with technology based services:.........................................16

1.5.1 Importance of Customer Satisfaction.............................................................16

1.5.2 Customer Satisfaction in Virtual Environment................................................16

1.5.3 Online Service Quality and Customer Satisfaction..........................................17

IV

1.6 Justification:...........................................................................................................18

1.7 Scope & Limitation:................................................................................................18

1.8 Assumptions:..........................................................................................................19

1.9 Disposition of Thesis:..............................................................................................19

2.0 Chapter – II Theoretical Framework 202.1 Banking Sector of Pakistan:..........................................................................................20

2.2 E-banking in Pakistan:..................................................................................................22

2.3 E-commerce implementation in banking industry:......................................................24

2.4 Customer acceptance of online banking:.....................................................................25

2.5 Customer Service:.........................................................................................................26

2.6 Online Environment:....................................................................................................27

2.7 Rationale for Banks to provide online banking services:..............................................28

2.8 Traditional Service Quality Vs Electronic Service Quality:............................................29

2.9 Measurement of eservice quality:................................................................................31

2.10 Relationship between satisfaction & service quality:.................................................33

2.11 Risk associated with e-banking:..................................................................................35

3.0 Chapter – III Research Methodology 363.1 Research Design...........................................................................................................36

3.2 Research Procedure:....................................................................................................36

3.3 Population & Sample:...................................................................................................36

3.3.1 Population.............................................................................................................36

3.3.2 Sample Size & Selection.........................................................................................37

3.4 Measurement/Instrument Selection:...........................................................................37

3.5 Variables:......................................................................................................................38

3.6 Conceptual Framework:...............................................................................................39

3.7 Hypothesis:...................................................................................................................40

3.8 Data Analysis:...............................................................................................................43

3.8.1 Statistical Tools...............................................................................................43

3.8.2 Plan of Data Analysis......................................................................................43

3.8.3 Softwares Employed.......................................................................................43

V

4.0 Chapter – IV Research Analysis & Interpretation 444.1 Data Analysis and Interpretation of ATM:..............................................................44

4.2 Data Analysis and Interpretation of Internet Banking:...........................................49

4.3 Data Analysis and Interpretation of TeleBanking:..................................................54

5.0 Chapter – V Findings & Conclusion 595.1 Findings..................................................................................................................59

5.2 Conclusion..............................................................................................................62

5.3 Recommendations..................................................................................................63

5.4 Further Research....................................................................................................64

References 65Appendix 70

VI

List of TablesTable 1 - Different Models for measuring customer satisfaction...........................................10

Table 2 : Electronic Banking infrastructure............................................................................13

Table 3: Conceptual Framework.............................................................................................39

Table 4: Reliability Statistics of ATM......................................................................................44

Table 5 : Regression Analysis of ATM.....................................................................................45

Table 6 -ATM: Correlation between factors...........................................................................46

Table 7 : Descriptive Statistics of ATM...................................................................................47

Table 8 : Result of Hypothesis testing for ATM......................................................................48

Table 9 - Reliability Statistics of Internet Banking..................................................................49

Table 10 : Regression Analysis of Internet Banking................................................................50

Table 11 : Internet Banking: Correlation between factors.....................................................51

Table 12 : Descriptive Statistics of Internet Banking..............................................................52

Table 13 : Result of Hypothesis testing for Internet Banking.................................................53

Table 14 : Reliability Statistics of TeleBanking........................................................................54

Table 15 : Regression Analysis of TeleBanking.......................................................................55

Table 16 - TeleBanking: Correlation between factors............................................................56

Table 17 : Descriptive Statistics of TeleBanking......................................................................57

Table 18 - Result of Hypothesis testing for TeleBanking........................................................58

List of Figures

Figure 1 – Disposition of Thesis..............................................................................................19

Figure 2- Conceptual Framework...........................................................................................39

I

II

Executive Summary

This research is a part of my Master of Business Administration degree. The purpose

of this research is to gain a better understanding of the service quality dimensions

that affect customer satisfaction with technology based services in the banking

sector. There are ten banks which included foreign, local and national banks have

been selected in this research, from which surveys are conducted.

Electronic banking services are new, and the development and diffusion of these

technologies by financial institutions is expected to result in a more efficient banking

system. This technology offers institution alternative or non-traditional delivery

channels through which banking products & services can be delivered to customers

more conveniently and economically without diminish the existing series level.

Banks are providing technology based services to provide an ease to their customers

and to increase their profitability by reducing the operational cost. But the

technology based services don’t satisfy the customer expectations and sometime

become a cause of trouble to the customers. Satisfaction is also of great interest to

practitioners because of its important effect on customer retention. Customer

satisfaction is major issue for the businesses which are dealing in electronic

commerce because it will determine whether the business will survive or fail in

future.

III

The result of this study reflected that bank customers are satisfied with all three

technology based services that are ATM, Internet Banking and TeleBanking services

provided by banking sector and also by all Efficiency, Reliability, Fulfillment,

Responsiveness and Privacy of ATM, Internet Banking and TeleBanking services

provided by banking sector.

One of the ways for achieving high customer satisfaction and gaining the loyalty of

customers is for banks to offer high quality services. That is why being able to

measure and evaluate the quality of their online banking services is deemed

important for banks in order for them to take action to correct those features of

their online services which customers don’t find that satisfactory. Technology offers

a means to improve internal communication, productivity and efficiency within the

organization to provide seamless service to customers to create new and more

effective service delivery and to enhance customer satisfaction.

IV

1.0 Chapter – I Introduction

1.1 Introduction:

In the world of banking, the development in Information Technology has an

enormous effect on development of more flexible payment methods and more –

user friendly banking services. Electronic banking services are new, and the

development and diffusion of these technologies by financial institutions is expected

to result in a more efficient banking system. This technology offers institution

alternative or non-traditional delivery channels through which banking products &

services can be delivered to customers more conveniently and economically without

diminish the existing series level. In recent years almost one fourth of banks in

Pakistan have starred to offer online banking services to customers and to satisfy

customers with their technology based services is one of the major area of focus for

banks.

The rapid advancement in electronic distribution channels has produced

tremendous changes in the financial industry in recent years, with an increasing rate

of change in technology, competition among players and consumer needs (Hughes,

2001). Increasing competition among banks and from non-bank financial institutions

also raises concerns as to why some people adopt one distributional channel and

others do not, and identifying the factors that may influence this decision is vital for

service providers. It is also important to study the impact of technology based

transactions on bankers’ perceptions and behavior (Lymperopoulos and Chaniotakis

2004). IT-based distribution channels reduce personal contact between the service

providers and the customers, which inevitably leads to a complete transformation of

traditional bank-customers relationships (Barnes and Howlett, 1998).

1

1.1.1 Background

In last few years we have witnessed a substantial growth of technology-based

services provided by banks. One of the key challenges of technology based services

as a delivery channel that how bank manage service quality, which holds significant

importance to customer satisfaction. As the number of technology based services

are increasing its benefits and problems are also increasing. Through the advent of

technology the infrastructure of any type of organization have faced a massive

change, similarly technology in banking sector have also changed the aspects of

doing banking in most areas.

1.1.2 Purpose

Banks are providing technology based services to provide an ease to their customers

and to increase their profitability by reducing the operational cost. But the

technology based services don’t satisfy the customer expectations and sometime

become a cause of trouble to the customers. In a competitive market place

understanding customer’s need become an important factor. As a result companies

have moved from a product centric to a customer centric position. Satisfaction is

also of great interest to practitioners because of its important effect on customer

retention. Customer satisfaction is major issue for the businesses which are dealing

in electronic commerce because it will determine whether the business will survive

or fail in future. The purpose of this research is to gain a better understanding of the

service quality dimensions that affect customer satisfaction with technology based

services in the banking sector. For this research the main research question was;

“What are the service quality dimensions in technology based services and how do

they effect customer satisfaction?”

2

1.1.3 Objectives

The objective of this study is to gain better understanding of service quality

dimensions that affect customer satisfaction with technology based services in the

banking sector from the consumer perspective.

To determine up to what extent technology based services are adopted by bank

customers?

Why people adopt technology for banking?

Adopting a technology, do really fulfill their need?

To explore the problems faced by bank customers in using technology based

services?

What are the problems faced by customers when they use technology for

banking?

What are the solutions to those problems?

To find the level of customer satisfaction with technology based services?

From which services bank customers are satisfied?

From which services bank customers are not satisfied & why?

To identify which service quality dimensions affect customer satisfaction?

Which service quality dimension highly affects customer satisfaction?

How service quality dimensions affect customer satisfaction?

3

1.2 Banking Sector:

1.2.1 Overview of Banking Industry of Pakistan

The financial sector in Pakistan comprises of De-Nationalized Banks (DNB),

Development Financial Institutions (DFI), Foreign Banks (FB) , Investment Banks (IB),

Micro Finance Banks (MFB), Nationalized Commercial Banks (NCB), Private

Scheduled Banks (PSCB), Provincial Banks (PB), Specialized Schedule Banks (SSB).

Under the prevalent legislative structure the supervisory responsibilities in case of

Banks, Development Finance Institutions (DFI), and Microfinance Banks (MFB) falls

within legal range of State Bank of Pakistan while the rest of the financial institutions

are monitored by other authorities such as Securities and Exchange Commission and

Controller of Insurance.

In Pakistan all banks & DFI’s works under the supervision of the State Bank of

Pakistan, the four major sectors in which STATE BANK OF PAKISTAN has divided

banks operations are Corporate, SME, Agriculture and Consumer Banking. STATE

BANK OF PAKISTAN provide regulations according to which all banks should work

and continuously keep a track that banks are complying through the regulations or

not.

The major banking market share is retained by BIG FIVE BANKS which are National

Bank of Pakistan, United Bank Limited, Habib Bank Limited, MCB Bank Limited and

Allied Bank Limited. Our banking industry can be divided into three categories first of

which are five large banks with have branches of more of 700 each. Four of these

4

banks have been denationalized in recent years, secondly of branches foreign banks

in Pakistan and last local private banks.

Pakistan has a highly developed financial sector consisting of 4 public 12 private 21 commercial banks, DFI, leasing companies, mutual funds, Islamic venture capital fund companies. The commercial banks have assets of over one trillion rupees of which about 80% is held by domestic banks. (Alam 2007, p.24)

Banking sector in Pakistan has undergone a significant transformation in the recent

years and has also acted as a catalyst in the revival of the economy. Many

privatization, acquisition and mergers took place during last seven years which

started from privatization of Muslim Commercial Bank and from time to time Allied

Bank Limited, United Bank Limited, Habib Bank Limited were also privatized by the

government.

These years also witnessed acquisition of Union Bank by Standard Chartered Bank,

Prime Bank by ABN Amro, Metropolitan Bank has been merged with Habib Bank AG

Zurich and recently the merger of SaudiPak Commercial Bank & Atlas Bank to took

place came into news. All these privatization, acquisition and mergers resulted in

high foreign investment in Pakistan and improved performance of the banking

industry while its has also helped banks to gain more market share in short time and

to easily meet the high paid-up-capital requirement of STATE BANK OF PAKISTAN

and to meet the minimum branch requirement of commercial banks

1.2.2 Opportunities & Challenges

The banking industry of Pakistan has grown to a significant level in last ten years and

its still on a growth stage. Banks are opening new branches, new foreign & local

banks are entering to market and merger & acquisition between banks are also

5

taking place. On the other side market is becoming more complex, banks are

introducing new innovative products and the market has become more competitive.

As the industry is growing its also getting many opportunities and facing many

challenges few of them are described below;

Interest Rate Variation

Banks are earning high spread by offering low rates on their deposits and high rate

on financing. This increases the bank profitability but the consumer suffers because

of high interest spread.

Maintaining the critical balance between savings, investment and borrowers debt-servicing ability is possible if input prices remain stable affording business to sustain their profitability and interest rates too remain stable to ensure that in the medium term, debt servicing burden remains affordable for both consumers and manufacturers. (Shahid, 2003)

Consumer Financing

The robust growth of auto and mortgage finance in preceding two years has

significantly increased the prices of these assets, and thus has created inflationary

pressures in the economy.

Growth in auto loans has registered an increase of approximately Rs.8 billion from Rs. 97.777 billion to Rs. 105.444 billion during the corresponding period of growth of credit cards and personal loans is more than 20%. Housing loans have also registered an increase of approximately Rs11.0 billion in H1 CY 07 from Rs43.205 billion in H1 CY06. (Sharif, 2007)

E-banking

Although small and medium banks are now offering on-line services to their

customers, the large banks, with more expanded branch network and number of

customers, are required to move more expeditiously so as to optimally utilize the E-

6

banking network. This will not only lower the transaction costs but will also help in

improving the customer services

Islamic Banking

Islamic banking is a relatively new concept in our banking system. More and more

banks are seeking license to open Islamic bank Branches. At present six full fledged

Islamic banks and many Islamic banking branches of conventional banks are

operating in Pakistan. The banks are fully prepared to run Islamic branches with the

help of their Shariah Board, Shariah Advisors, Auditors and trained staff. This is a

sector where growth is expected and the banks should capture this opportunity.

Anti-Money Laundering

With the growth of global financial industry, the misuse of banking industry has

been observed in recent years. These include the use of banking services for

activities like, terrorist financing, drug trafficking and money laundering. There are a

number of countries where the entire regulatory framework is at initial stage, so

there are chance of such activities in the form of reputational, operational, legal and

concentration risks.

Implementation of BASEL-II

STATE BANK OF PAKISTAN has instructed all commercial banks to fully implement

BASEL-II system by 2009 to reduce their risk. This will not only reduce the probability

of defaults in our banking industry but it will also improve the image of our banking

industry by complying with the standards of BIS.

7

1.3 Customer Satisfaction:

1.3.1 Customer Satisfaction

According to Hill, Brierley and MacDougall (2003) ‘Customer satisfaction is measure

of how yours organization total product perform in relation to a set of customer

requirement’. Customer satisfaction is the measurement about how products and

services supplied by any firm meet customer expectations. It is seen as a key

business performance indicator. Bauer, Hammerschmidt and Falk (2005, p.153)

highlighted that ‘Customer satisfaction and customer retention are increasingly

developing into key success factor in e-banking’

1.3.2 Customer Satisfaction in Service Industry

Customer satisfaction has for many years been perceived as key in determining why

customers leave or stay with an organization. Whether a firm is offering products or

services customer satisfaction is important in both. However managing and

measuring customer satisfaction in service industry is much more difficult. On the

other side, satisfied customers may look for other service providers because they

believe they might receive better service elsewhere. According to Dash & Mahapatra

(2007) ‘With the phenomenal increase in the country's population and the increased

demand for banking services; speed, service quality and customer satisfaction are

going to be key differentiators for each bank's future success.’

In businesses where the underlying products have become commodity-like, quality of service depends heavily on the quality of its personnel. This is well documented in a study by Leeds (1992), who documented that approximately 40 percent of customers switched banks because of what they considered to be poor service. (Cohen et al. 2006)

8

1.3.3 The Need to Measure Customer Satisfaction

Satisfied customers are central to optimal performance and financial returns. At

many countries in the world, business organizations have been inspiring the role of

the customer to that of a key stakeholder. Measuring customer satisfaction and

keeping a track of it can become the success factor for any firm.

With better understanding of customers' perceptions, companies can determine the actions required to meet the customers' needs. They can identify their own strengths and weaknesses, where they stand in comparison to their competitors, chart out path future progress and improvement. Customer satisfaction measurement helps to promote an increased focus on customer outcomes and stimulate improvements in the work practices and processes. (Dash & Mahapatra, 2007)

When buyers are powerful, the health and strength of the company's relationship

with its customers – its most critical economic asset – is its best predictor of the

future. Focusing on competition has its place but it is more important for any firm to

pay attention to its customers.

1.3.4 Measuring Customer Satisfaction with e-services

With the increasing application of ecommerce in organizations, the importance of

measuring and monitoring eservice quality in the virtual world has been recognized.

According to Fassnacht & Koese (2006, p.19) ‘For providers of electronic services,

quality is a major driving force on the route to long-term success. Comprehensive

measurement of quality, in turn, is the key to effective quality management.’

Technology offers a means to improve internal communication, productivity and efficiency within the organization to provide seamless service to customers to create new and more effective service delivery and to enhance customer satisfaction. (Hernon & Whitman, 2001)

9

1.3.5 Different models & variables for measuring customer satisfaction

The measurement of the gap between expected and perceived service has been first

operationalized with 10 dimensions: reliability, responsiveness, competence, access,

courtesy, communication, credibility, security, understanding, and tangibles

(Parasuraman et al. 1985). Parasuraman, Zeithaml, and Berry developed and refined

SERVQUAL, a multiple-item instrument to quantify customers’ assessment of a

company’s SQ. This scale contains five dimensions: reliability, responsiveness,

assurance, empathy, and tangibles.

Table 1 - Different Models for measuring customer satisfaction

(Dai & Yi, 2006)

10

1.4 Technology Based Services:

1.4.1 Overview of e-banking

E-banking is the use of electronic means to deliver banking services, mainly through the

Internet. The idea of online banking came into existence, in Europe and America in the

beginning of 1980s. It has been estimated that more than forty percent of banking

transactions are done online. A large variety of services are being rendered by banks using

the electronic media. Banks are operating inter-city transfer of money by DD, mail transfers

and TT from one city to other or even within the same city and also from bank to bank

through telephones from many years. Electronic commerce is very much assisted by the e-

Banking through electronic cash cheques and smart cards.

Worldwide banking is no longer restricted to the four walls. A lot of countries are

ahead of the technology based services being available in our country. The idea in

online banking in our country was taken very late, but now focused efforts are being

made to catch up with rest of the world. Banking, a few years back, was confined to

only four walls of branch but after the entrance of new private commercial banks,

which focused less on number of branches, but investment in technology was

chosen as a main focus point. The arrival and widespread use of Internet, leading to

e-commerce, enforced the banks worldwide to fit in e-banking.

1.4.2 Types of e-banking services

Currently the technology based services provided by banks in Pakistan are Online

Banking, Internet Banking, ATM, Credit/Debit Cards, Online Bill Payment Facility,

Mobile-SMS Banking, TeleBanking/Call Center, etc. During the last five years

banking industry of Pakistan had witnessed a high change this change is not only in

11

its service and capital but also the technology based services that they are offering.

Common embodiments of e-banking include the following:

• Mobile/SMS Banking

• Telephone Banking

• Electronic funds transfers

• Self Service (PC) Banking

• POS Banking (Credit and Debit cards)

• ATMs

• Interactive TV

• Branchless Banking

• Intranet

1.4.3 Growth of e-banking in Pakistan

According to a Report titled ‘Retail Payment Systems of Pakistan - Paper based and‐

E banking (STATE BANK OF PAKISTAN, 2008) ‘A total of 124.6 million E banking‐ ‐

transactions were recorded valuing Rs 13.9 trillion during the last fiscal year (FY08),

showing a growth of 25.4% in numbers and 32.3% in amount when compared with

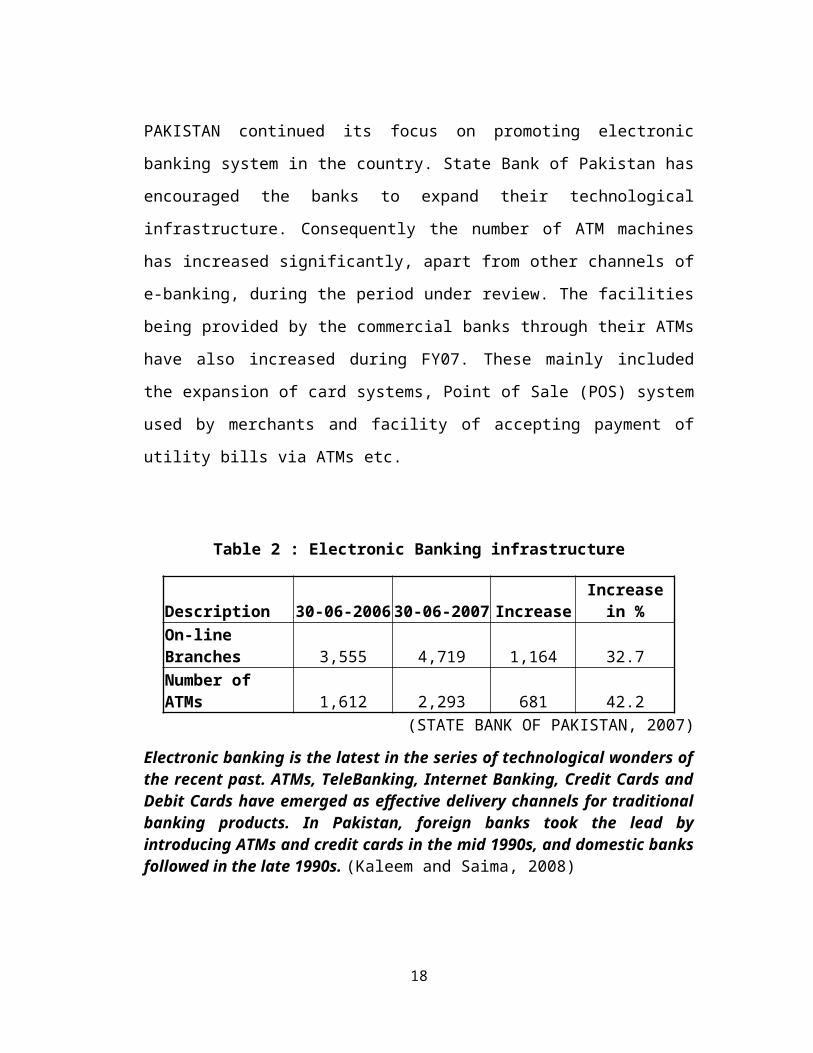

the fiscal year (FY07).’ During FY07, STATE BANK OF PAKISTAN continued its focus

on promoting electronic banking system in the country. State Bank of Pakistan has

encouraged the banks to expand their technological infrastructure. Consequently

the number of ATM machines has increased significantly, apart from other channels

of e-banking, during the period under review. The facilities being provided by the

commercial banks through their ATMs have also increased during FY07. These

mainly included the expansion of card systems, Point of Sale (POS) system used by

merchants and facility of accepting payment of utility bills via ATMs etc.

12

Table 2 : Electronic Banking infrastructure

Description 30-06-2006 30-06-2007 Increase Increase in %On-line Branches 3,555 4,719 1,164 32.7Number of ATMs 1,612 2,293 681 42.2

(STATE BANK OF PAKISTAN, 2007)

Electronic banking is the latest in the series of technological wonders of the recent past. ATMs, TeleBanking, Internet Banking, Credit Cards and Debit Cards have emerged as effective delivery channels for traditional banking products. In Pakistan, foreign banks took the lead by introducing ATMs and credit cards in the mid 1990s, and domestic banks followed in the late 1990s. (Kaleem and Saima, 2008)

The number of ATM transactions stood at 51.5 million during FY07 as compared to

35 million during the preceding year showing an increase of 47.1 percent over the

year. The value of transaction stood at Rs.352.4 billion during FY07 as compared to

Rs.211.0 billion in FY06 reflecting an increase of 67 percent. ATMs were largely used

for cash withdrawals and field offices of STATE BANK OF PAKISTAN-BSC provided

ample quantity of fresh currency notes to the online branches of commercial banks

to conveniently perform electronic transactions through ATMs.

IT is affecting the life of every human being in this current age. Online or e-banking is one of technological service which is getting acknowledgment around the globe. There are a lot of customers around the world who are accepting this technology very quickly but in emerging countries like Pakistan the acceptance ratio is very high. (Qureshi, Zafar & Khan, 2008)

Kaleem & Saima (2008) concluded that it was changing consumer attitudes rather

than bank cost structures that determine the changes in distribution channels; they

added that virtual banks can only be profitable when the segment that prefers

electronic media is approximately twice the size of the segment preferring street

banks.

13

1.4.4 Benefits of e-banking

Technological innovations are having significant importance in human general and

professional life. The rapid expansion of IT has imbibed into the lives of millions of

people. Rapid technology advancement have introduced major changes in the

worldwide economic-business atmosphere. Information technology developments in

the banking sector have speed up communication and transactions for clients.

E-banking is one of the technologies which are rapidly growing banking practices

these days. It is very important to extend this new banking feature to banks clients

for maximizing the advantages of banks and its customers both. Few of the benefits

of e-banking are highlighted below;

Access your account information and transactions. Make electronic funds transfers. View, download and print statements. View CBA’s up-to-date daily exchange rates. Transfer funds between your personal accounts Easy set-up. User-friendly and secure 24-hour access – no more space and time constraints. User support from highly trained and experienced customer service teams.

1.4.5 Challenges faced by e-banking industry

The banking industry sector is one of the most important service sectors for the

whole national economy. Modern, highly developed and technology driven

economies are in danger by higher risks than ever, and individual need to protect

themselves against private risk. From the banks point of view, use of Internet

banking is likely to lead to cost reductions and improved competitiveness. This

service delivery channel is seen as dominant because it can retain current Web-

based customers who continue using banking services from any place. Furthermore,

14

online banking provides opportunities for the banks to develop its market by

attracting a new customer base from existing users.

In Pakistan, foreign banks took the lead by introducing ATMs and credit cards in the mid 1990s, and domestic banks followed in the late 1990s. The STATE BANK OF PAKISTAN Annual Report explained this delayed entry in electronic banking largely by regulatory hurdles, higher start up costs, on-going banking sector reforms and lack of technical skills. (Kaleem & Saima, 2008)

Some key challenges faced by online banking are highlighted below;

Security: Majority of the customer shy away from E-Banking services due to security concerns

Human face: According some analysts, customers still value personalized and responsive services from their bankers

Ignorance: Bank customers do not even know whether their banks provide online services

Poor and/or lack of technological infrastructure and reliable power supply Lack of proper legislation governing e-transactions Preference to paper money, as opposed to “virtual” cash in transactions Balance between convenience and security. Designing products that offer a balance between competitive pricing and

functionality Keeping abreast with dynamism of customer needs & innovation Lack of proper legislative framework to support the growth of e-banking

15

1.5 Customer Satisfaction with technology based services:

1.5.1 Importance of Customer Satisfaction

The trend towards electronic delivery of banking products is occurring partly as a

result of consumer demand and partly because of the increasing competitive

environment in the global banking industry. The internet has changed the customer

behavior who is demanding more customized products/services at lower cost. Banks

are repositioning themselves to accept new visions because they are in people

business and now people demands have changed. If experience of the service

increases the expectations customers had of the service then satisfaction will be

more.

1.5.2 Customer Satisfaction in Virtual Environment

Many firms are moving to make virtual interfaces their primary, or even sole, points of customer contact. Perceived trustworthiness of an online broker is a significant antecedent to investors’ satisfaction, and that perceived environmental security and perceived operational competence impact the formation of trust. (Balasubramanian, Konana & Menon, 2003)

Three factors, quickness, easiness and cheapness have become the catchwords for

the competitiveness and usefulness of all the business operations. Particularly it is

routine today to say that banking is undergoing through a major change. The

symptoms are new products, new players, etc. The change is taking place across all

areas of the banking industry. That is why banks urgently need to improve their

ability, to think strategically about technological investments. Banks which use their

technology resources effectively have the opportunity to secure real competitive

advantage in this changing industry through real products and services

differentiation.

16

1.5.3 Online Service Quality and Customer Satisfaction

During last few years a substantial growth of internet-based services, both from

internet business and from traditional companies that are developing online service

took place. One of the key challenges of online service delivery channel is how they

manage service quality which holds a significant importance to customer

satisfaction. Dash and Mahapatra (2007) highlighted that ‘There is obviously a strong

link between customer satisfaction and customer retention. Customer's perception

of Service and Quality of product will determine the success of the product or

service in the market’

17

1.6 Justification:

The increasing number of advancements took place in technology based services

provided by the banking sector and day by day new technologies are on their way,

there is a need to measure that those services actually satisfy the customer

expectation or not. This study explores the key areas of technology based services

provided by the banking sector in which customers are not satisfied and what are its

reasons, further this report has also recommend solutions for those problems.

This research will be highly beneficial for the banking industry because it will give an

idea to banks that how the service quality dimensions affect customer satisfaction

and what are the causes of problems and how to solve them. The outcomes of this

study will also help the management of banks to do effective strategic planning for

the future of electronic banking in Pakistan.

1.7 Scope & Limitation:

This research is conducted on commercial banks of Pakistan and it is from the

consumer perspective only. Ten commercial banks are selected in Karachi for the

purpose of conducting survey. Only those banks are selected for the purpose of

survey who is offering at least one these three technology based services which are

ATM, Online Banking and TeleBanking. The sample size is restricted to one-city only

namely Karachi and managing non-serious response of people was difficult because

of high sample size i.e. 600 (approx.)

18

1.8 Assumptions:

Customer satisfaction with technology based services can be measured by applying models of measuring electronic service quality.

The implementation and use of technology based services are increasing and most of banks customers are using at least one basic technology based services i.e. ATM.

1.9 Disposition of Thesis:

Figure 1 – Disposition of Thesis

19

Introduction

Theoretical Framework

Methodology

Analysis & Interpretation

Findings & Conclusion

2.0 Chapter – II Theoretical Framework

2.1 Banking Sector of Pakistan:

The State Bank of Pakistan is the Central Bank of Pakistan. The state bank of Pakistan

started its operation on 1st July 1948. State Bank is not only responsible for issuing

domestic currency and regulating foreign currency but also for analyzing domestic

economy. The bank has been operating with a mission of promoting both monetary

and financial stability and to promote the financial system for achieving sustainable

growth by reducing inequality. The relevant provisions of law which vest powers in

State Bank of Pakistan (SBP) to carry out inspection of banks.

Before 1990 public banks dominated the Pakistani financial market. In 1991, two

smaller banks, the Muslim Commercial Bank and the Allied Bank, were privatized as

part of the government's general program of economic liberalization and the

privatization of state enterprises. The government also instructed the State Bank of

Pakistan (SBP) to approve proposals for the establishment of commercial banks in

the private sector since then, the government has continuously advocated the

privatization of the banking sector and the setting up of new private and foreign

banks (Kaleem & Ahmed, 2008). The acquisitions of a local Union Bank by Standard

Chartered Bank and Prime Bank by ABN Amro Bank indicate foreign interest in the

domestic financial market.

Modern history of the Pakistani’s banking industry goes back into the year 1985

when permission for the establishment of commercial banks was granted for the

20

first time in Punjab. The liberalization effort was eagerly taken advantage of and by

1992 there were already 14 banks in Pakistan. The number of banks increased to 39

by end of 2007 (Khan, 2007). Setting up a bank was extremely popular in the

beginning of 1992 because there were basically no legislative restrictions to

establishing a bank. But the scenario has changed a lot in recent years by strict

regulations and monitoring of State Bank of Pakistan. Financial institutions are

offering various types of services besides conventional banking services, such as,

business loans, corporate banking, house financing and car leasing facilities. Over

the last three years, almost 70% banks have converted to online banking, providing

real-time information. Consequently the performance of banking is increasing not

only in urban centers but also in rural areas.

“ In recent years, growth and turn-around in Pakistan’s banking sector has been amazing and exceptional due to online technology exploited by the banking sector” (Qureshi, Zafar & Khan, 2008).

21

2.2 E-banking in Pakistan:

Pakistan has passed through its introductory phase and now it is moving towards

new avenues. After introductory phase customers are well aware of e-products and

are now demanding more sophisticated services. Electronic banking is the latest in

the series of technological wonders of the recent past. ATMs, TeleBanking, Internet

Banking, Credit Cards and Debit Cards have emerged as effective delivery channels

for traditional banking products. In Pakistan, foreign banks took the lead by

introducing ATMs and credit cards in the mid 1990s, and domestic banks followed in

the late 1990s (Kaleem & Ahmad, 2008).

“Online banking is also one of the technologies which are fastest growing banking practices nowadays. It is vital to extend this new banking feature to clients for maximizing the advantages for both clients and service providers” (Qureshi, Zafar & Khan, 2008)

The Government of Pakistan further promoted electronic banking with the

promulgation of the Electronic Transaction Ordinance 2002; this landmark step

provided legal recognition of digital signatures and documentation reducing the risks

associated with the use of electronic media in business. According to Kolachi (2006)

Pakistani banks provides the following online banking services and products. (1)

Inquiry: Account statement inquiry, Account balance inquiry, Check statement

inquiry, Fixed deposit inquiry (2) Payment: Transfer of funds, Credit cards payments,

Direct payments, Utility bills payments (3) Request: Chequebook requests, Stop

payment requests, Demand draft requests, New fixed deposit requests (4)

Download: Customer profile, Statement download, Other information and

guidelines download.

22

Development in human culture has been consummated by the development of new

technologies. The last few years have witnessed supreme changes throughout the

world (Deshmukh S. G et al, 1995). Due to increase in technology usage the banking

sector’s performance increases day by day. Online banking is becoming the

indispensable part of modern day banking services. It is expected that 60 % of retail

banking dealings will be online in ten years' time (Barwise, P. 1997). A financial

institution has a lot of customers around the country; therefore they need their

bank online so that they can easily access it from anywhere. Pakistan is also not

lagging behind in this venture. One would imagine that Pakistani banks would not

only be proactive to give online banking service but would also persuade consumers

to shift to this form of deliverance of banking services.

“An existing bank with physical offices can establish a website and offer internet banking to its customers as an addition to its traditional delivery channels” (Qureshi, Zafar & Khan, 2008)

Electronic distribution channels provide alternatives for faster delivery of banking

services to a wider range of customers. E-channels have gained increasing popularity

and have attracted the attention of both academics and practitioners in Pakistan.

23

2.3 E-commerce implementation in banking industry:

Banks have not only been early adopters of ecommerce, but other businesses’ move

to ecommerce has been highly dependent on the electronic financial infrastructure

that banks provide. Awad defines ecommerce in banking as consisting of;

“Procedures that support commercial activities electronically or via networking to apply to bank-to-bank, bank-to customer or bank-to-vendor” (Awad, 2000)

Technologies such as Automatic Teller Machines (ATMs), electronic funds transfer

and point of service banking via retail terminals, phone banking, intranets and

internet banking have assisted banks and financial organizations to update their

business processes still further.

“In the USA, large organizations such as FleetBoston, Citigroup and Wells Fargo are offering a one-stop shop, which includes real time balances, corporate research and stock trading” (Blount, Castleman & Swatman, 2002)

Controlling costs in the banking sector is a key management objective and this

industry has been keen to convert customers to online media and to utilize

ecommerce, as it is significantly cheaper than face-to-face transactions and has

additional benefits. Internet provides an excellent opportunity for business

communications and transactions as it allows organizations to establish direct links

with current and new customers while being able to deliver new products and

services. Awad (2000) observes that the combination of computers, the internet and

information technology have become a feasible substitute for labour- and paper-

intensive banking processes, the industry holds a positive view of technological

changes such as the ATM, phone banking and the utilization of the internet which do

not require face-to-face interaction between customers and branch staff.

24

2.4 Customer acceptance of online banking:

Banking industry is also one of the influenced industries adopting technologies

which are helpful in providing better services to customers. Quality of service is

improved by using technological innovations. Online banking is time-saving. About

20% of retail and 30 % of businessmen will use some shape of Internet banking

facility within the next five years (Booz et al, 1997). There will be huge acceptance of

online banking with the passage of time with growing awareness and education. A

great many people are shifting to online banking and are readily accepting the

usefulness of it.

Online banking service allows customers to manage their accounts from any place at

any time for minimum cost; it gives abundant compensation to the client in terms of

price and ease (Ekin et al, 2001). It is a fast growing phenomenon among general

public in Pakistan as well. Many factors are attracting the public like ease of use,

perceived usefulness, security and privacy. Perceived usefulness is defined as the

degree to which a person believes that using a particular technology would improve

job performance while perceived ease of use is the degree to which using IT is free

of effort for the user (Davis et al., 1989).

25

2.5 Customer Service:

According to Shariq (2006) in today’s competitive business environment, companies

must understand that the customer hold the key to success. The customer must be

at the very heart of the company’s decision making. The customers want many

things from the companies, they work with. In the language of customer service,

these wants are often referred as needs, most customer need quality products,

quality service and friendly interaction with knowledgeable people who care about

them.

Information technology can and is being used to improve customer services, though

the use of IT is dependent on the understanding of customer services (Shariq, 2006).

Customer service is being influenced by information technology. Regardless of how

one visualizes customer service, either from a logistics or marketing perspective,

information technology now assumes and important role in customer service.

26

2.6 Online Environment:

The web is the primary infrastructure for e-commerce. It is well accepted that

websites provided benefits for both corporation and consumer. A corporation can

display its identity and advertise its products and services to many people. Also,

corporations can get feedback directly from customers. A website can also improve

communications with other corporations thus improving the efficiency of business

processes by increasing direct sales and reducing costs. Online environment not only

include web-sites but it also include all kind on electronic services which don’t

include any physical process.

Usually for e-businesses, too much attention is paid to aesthetic design, which ends

up looking amazing but actually causes frustration because sometime customers

have difficult in finding what they are looking for. The main reason why customer

goes online is to find information or buy products or use service with an emphasis

on convenience and speed. Dabholkar (2000) points out that the concept of Internet

has raised customer’s sensitivity to fast customer service. Any e-business that sticks

to this principle when designing its online environment should be relatively

successful.

According to Donlan (1999), although delivery is highly important in fulfilling

customer needs, perceptions and expectations also needs to be managed and the

website plays a main role in this. Once the basis of online services is clear the type of

customer is hope will be attracted can then be assessed and judgment made on

what graphics, effects and other matter can be added to increase the value

proposed. Clear instructions are needed to avoid confusion and frustration.

27

2.7 Rationale for Banks to provide online banking services:

Rationale for banks to take advantages of Internet Banking services are summarized

and presented as follows: cost savings, increase customer, enable mass

customization for e-business services, extend marketing and communication

channel, search for new innovation services, explore and development of non-core

business. According to Ongkasuwan (2002) customers ability to subscribe to the

Internet-base banking services depend on several factors, such as,

1. user-friendly interface

2. level of Internet experience

3. type of services provided (for example, e-mail, file transfer, news, online financial

services, shopping, and multimedia services)

4. attitude and perception

5. access and delivery time

6. experience (if any) with the Internet.

Therefore, management of customer requirement is vital to development of rational

for the banks to initiate, explore and develop Internet banking services that meet

their needs and changes.

28

2.8 Traditional Service Quality Vs Electronic Service Quality:

Extensive research on traditional SQ has been conducted during the past 20 years. In

contrast, only a limited number of scholarly articles deal directly with how

customers assess e-SQ. A study presented by Gounaris and Dimitriadis (2003) is the

first attempt to investigate the service quality of e-banking portals based on the

SERVQUAL, the authors identify three quality dimensions, namely customer care and

risk reduction benefit, information benefit and interaction facilitation.

By traditional SQ we are referring to the quality of all non-Internet-based customer

interactions and experiences with companies. Parasuraman, Zeithaml, and Berry

(1991) conducted empirical studies in several industry sectors to develop and refine

SERVQUAL, a multiple-item instrument to quantify customers assessment of a

company’s SQ. This scale measures SQ along five dimensions: reliability,

responsiveness, assurance, empathy, and tangibles. The SERVQUAL instrument and

its adaptations have been used for measuring SQ in many published studies.

Three broad conclusions that are potentially relevant to defining, conceptualizing,

and measuring perceived e-SQ emerge from the traditional SQ literature: (a) The

notion that quality of service stems from a comparison of actual service

performance with what it should or would be has broad conceptual support,

although some still question the empirical value of measuring expectations and

operationalizing SQ as a set of gap scores; (b) the five SERVQUAL dimensions of

reliability, responsiveness, assurance, empathy, and tangibles capture the general

domain of SQ fairly well, (c) customer assessments of SQ are strongly linked to

perceived value and behavioral intentions.

29

From studies dealing with people-technology interactions imply that customer

evaluation of new technologies is a distinct process. For instance, findings from an

extensive qualitative study of how customers interact with, and evaluate,

technology-based products (Mick and Fournier 1995) suggest that (a) customer

satisfaction with such products involves a highly complex, meaning-laden, long-term

process; (b) the process might vary across different customer segments; and (c)

satisfaction in such contexts is not always a function of preconsumption comparison

standards. Moreover, other research involving both qualitative and empirical

components demonstrates that customers’ propensity to embrace new technologies

(i.e., their technology readiness) depends on the relative dominance of positive and

negative feelings in their overall technology beliefs (Parasuraman 2000). Over the

past three decades researchers have made efforts to uncover the most important

dimensions of perceived service quality; lately these efforts have also focused on

eservices quality (Yang, 2004).

After extensive literature review ZEITHAML developed the e-SERVQUAL (e-SQ)

measure of electronic service quality to study how customers judge e-service

quality. This new model was drawn up through a three-stage process involving

exploratory focus groups and two phases of empirical data collection and analysis. It

contains five broad sets of criteria as relevant to e-SQ perceptions: (a) information

availability and content; (b) ease of use or usability; (c) privacy/security; (d) graphic

style, and, (e) reliability/fulfillment. Studies reveal important differences in

acceptance and usage of technologies across customers depending on their

technology beliefs and suggest that similar differences might exist in the evaluative

processes used in judging e-SQ. In other words, customer-specific attributes (e.g.,

technology readiness) might influence, for instance, the attributes that customers

desire in an ideal Web site and the performance levels that would signal superior e-

SQ.

30

2.9 Measurement of eservice quality:

With the increasing application of ecommerce in organizations, the importance of

measuring and monitoring service quality in the virtual world has been recognized.

Different studies have been conducted aiming at developing measurement scales

adapted to eservice quality field. It is evident that most of these studies have been

conducted mainly on three different areas: online retailing service quality, web site

design quality and online service quality, and there has been limited attention to

other service contexts. In fact both web site design quality and online retailing

quality are important components of online service quality (Cristoal, 2007).

One of the first definitions of eservice quality is conceptualized by Zeithaml,

Parasuraman, and Malhotra (2000). They state that Internet service quality is the

extent to which a web site facilitates efficient and effective shopping, purchasing,

and delivery of products or services. Zeithaml (2002) state that some dimensions of

the SERVQUAL can be applied to eservice quality, but there are additional

dimensions in eservice, many of which are specifically related to technology. The

ESQUAL scale comprises 11 dimensions in eservice quality, and later Parasuraman et

al. (2005) developed the ESQUAL into to a seven dimensions scale. The seven

dimensions are split into two separated scales the core dimensions and the recovery

dimensions. ESQUAL is the name of the scale for the core dimensions: efficiency,

system availability, fulfillment, and privacy. The second scale is titled ERecSQUAL:

responsiveness, compensation, and contact (Parasuraman et al., 2005). It offers the

surface dimensions of eservice quality based on customers experience and

evaluation perspective, which are viewed also as the antecedents to the adoption of

eservice (Rowley, 2006).

31

Zeithaml, Parasuraman, and Malhotra’s (2000) study identified dozens of Web site

features at the perceptual attribute level and categorized them into 11 e-SQ

dimensions which are;

1. Reliability: Correct technical functioning of the site and the accuracy of service

promises (having items in stock, delivering what is ordered, delivering when

promised), billing, and product information.

2. Responsiveness: Quick response and the ability to get help if there is a problem or

question.

3. Access: Ability to get on the site quickly and to reach the company when needed.

4. Flexibility: Choice of ways to pay, ship, buy, search for, and return items.

5. Ease of navigation: Site contains functions that help customers find what they

need without difficulty, has good search functionality, and allows the customer to

maneuver easily and quickly back and forth through the pages.

6. Efficiency: Site is simple to use, structured properly, and requires a minimum of

information to be input by the customer.

7. Assurance/trust: Confidence the customer feels in dealing with the site and is due

to the reputation of the site and the products or services it sells, as well as clear and

truthful information presented.

8. Security/privacy: Degree to which the customer believes the site is safe from

intrusion and personal information is protected.

9. Price knowledge: Extent to which the customer can determine shipping price,

total price, and comparative prices during the shopping process.

10. Site aesthetics: Appearance of the site.

11. Customization/personalization: How much and how easily the site can be

tailored to individual customers’ preferences, histories, and ways of shopping

32

2.10 Relationship between satisfaction & service quality:

Service quality is the key to measure customer satisfaction (Pitt et.al., 1995). Many

studies to date have been undertaken to indentify service quality dimensions and

detailed aspects of online services and their relationships with customer satisfaction.

One of the most widely used instruments for assessing customer satisfaction is

SERVQUAL developed by Zeithaml. SERVQUAL is a widely recognized and used, and

it is regarded as applicable to number of industries including banking industry. In

businesses where the underlying products have become commodity-like, quality of

service depends heavily on the quality of its personnel. Customer satisfaction has for

many years been perceived as key in determining why customers leave or stay with

an organization (Saha & Zhao, 2005).

The interest in studying satisfaction and service quality as the antecedents of

customer behavioural intentions in this paper has been stimulated, firstly, by the

recognition that customer satisfaction does not, on its own, produce customer

lifetime value (Appiah-Adu, 1999). Secondly, satisfaction and quality are closely

linked to market share and customer retention (Rust and Zahorik, 1993). There are

overwhelming arguments that it is more expensive to win new customers than to

keep existing ones (Hormozi and Giles, 2004). Customer replacement costs, like

advertising, promotion and sales expenses, are high and it takes time for new

customers to become profitable. And lastly, the increase of retention rate implied

greater positive word of mouth (Appiah-Adu, 1999), decrease price sensitivity and

future transaction costs (Reichheld and Sasser, 1990) and, finally, leading to better

business performance.

From the literature that has been reviewed so far, customer satisfaction seems to be

the subject of considerable interest by both marketing practitioners and academics

33

since 1970s (Jones and Suh, 2000). Companies and researchers first tried to measure

customer satisfaction in the early 1970s, on the theory that increasing it would help

them prosper. Throughout the 1980s, researchers relied on customer satisfaction

and quality ratings obtained from surveys for performance monitoring,

compensation as well as resource allocation and began to examine further the

determinants of customer satisfaction.

Reichheld (1996) suggests that unsatisfied customers may choose not to defect,

because they do not expect to receive better service elsewhere but satisfied

customers may look for other providers because they believe they might receive

better service elsewhere. Berry (1984) stressed that employees must be viewed by

the management as ‘internal customers’. Maintenance of high level of employee

satisfaction and retention is important if banks are to achieve high levels of

customer satisfaction and retention. Today, the definition of service quality and its

relationship to other constructs of interest is still being actively researched. Two

main conceptualizations of service quality exist in the literature - one based on the

disconfirmation approach, and the other based on a performance-only approach

(Santos, 2003).

“Bank management tends to differentiate their firm from competitors through

service quality” (Cohen et al., 2006)

34

2.11 Risk associated with e-banking:

Although, electronic banking provides many opportunities for the banks, it is also

the case that the current banking services provided through Internet are limited due

to security concerns, complexity and technological problems (Sathye, 1999).

Reputation of a service provider is another important factor affecting trust. Doney

and Cannon (1997) defined reputation as the extent to which customers believe a

supplier or service provider is honest and concerned about its customers. Tyler and

Stanley (1999) argued that banks can build close and long lasting relationships with

customers only if trust, commitment, honesty and cooperation is developed

between them.

Frequent slow response time and delay of service delivery causes customers to be

unsure that the transaction has been completed (Jun and Cai, 2001). Min and Galle

(1999) found the disruption of information access to be a common factor related to

unwillingness to use Internet channels for commerce. Lack of specific laws to govern

Internet banking is another important concern for both the bankers and the

customers. This relates to issues such as unfair and deceptive trade practice by the

supplier and unauthorized access by hackers. Other risks associated to electronic

banking are job losses, lack of opportunities to socialize and the development of a

lazy society (Black at al., 2001).

35

3.0 Chapter – IIIResearch Methodology

3.1 Research Design

This is an applied and quantitative research because it will help to manage issues

related to customer satisfaction with technology and it involves information

collection and analysis of data obtained from questionnaire.

3.2 Research Procedure:

Secondary data collection has been done from various local and international

journals, books, newspapers, etc for literature review after which primary data

collection through Survey-Questionnaire at branches of different bank have been

conducted. Then the compilation of data collected through Survey-Questionnaire

and data analysis - interpretation is performed.

3.3 Population & Sample:

3.3.1 Population

Currently there are four nationalized, twenty private, five Islamic and seven foreign

commercial banks in Pakistan with a total of 36 commercial banks and almost ninety

percent of banks are providing most of the technology based services.

36

3.3.2 Sample Size & Selection

Out of thirty-six commercial banks in Pakistan ten banks are selected one

nationalized, five privates, two Islamic and two foreign banks by the ratio of 4:1. The

selected banks offer at least one of the technology based services from ATM, Online

Banking or TeleBanking. For the purpose of conducting survey the target sample size

was 800 and the sampling method will be stratified random sampling. However at

end of data collection I was able to collect around 600 (usable) samples.

3.4 Measurement/Instrument Selection:

Both primary and secondary sources are used for data collection, primary data have

been collected through Survey-Questionnaire while secondary data will be collected

from journals, articles, newspapers and magazine.

The model used in this research is taken from study conducted at Lulea University of

Technology on Relationship between Online Service Quality & Customer Satisfaction

the model used in this research is based on different e-SERVQUAL studies conducted

by Zeithaml, Malhotra & Parasuraman. This same model is applied on all three

different QUESTIONNAIRES on ATM, TeleBanking & Internet Banking.

37

3.5 Variables:

The questionnaire designed in this study based on e-SERVQUAL Model by Zeithaml,

Parasuraman & Malhotra in which following e-service quality dimension will be used

to measure customer satisfaction with technology based services;

1. Efficiency

2. Reliability

3. Responsiveness

4. Privacy

5. Fulfillment

6. Customer Satisfaction

Efficiency, Reliability, Responsiveness, Privacy & Fulfillment are used as independent

variables and Customer Satisfaction is used as dependent variable.

38

Customer

Satisfaction

3.6 Conceptual Framework:

The model presented below is taken from research study conducted at Lulea

University of Technology on Relationship between Online Service Quality & Customer

Satisfaction.The five service quality dimensions used have been selected from the

study done by Zeithaml et al. (2000)

Figure 2- Conceptual Framework

Service Quality Dimensions

Table 3: Conceptual Framework

Online Service Quality Dimension

Measurement Criteria

Efficiency The ability of customers to get their desired informationReliability The accuracy of information provided

Responsiveness The ability to provide appropriate information to customer when problem occurs

Fulfillment Accuracy of service promises, delivering the service on time

Privacy Personal information are not shared with anyone, all information is secure

39

Fulfillment

Privacy

Efficiency

Reliability

Responsiveness

3.7 Hypothesis:

Hypothesis for A T M

Customer Satisfaction

Ho : µ ≥3.5 Customers are satisfied with ATM services provided by banking sector

H₁ : µ ≤3.5 Customers are not satisfied ATM services provided by banking sector

Efficiency

Ho : µ ≥3.5 Customers are satisfied with efficiency ATM services provided by banking sector

H₁ : µ ≤3.5 Customers are not satisfied with efficiency of ATM services provided by banking sector

Privacy

Ho : µ ≥3.5 Customers are satisfied with privacy of ATM services provided by banking sector

H₁ : µ ≤3.5 Customers are not satisfied with privacy of ATM services provided by banking sector

Reliability

Ho : µ ≥3.5 Customers are satisfied with reliability of ATM services provided by banking sector

H₁ : µ ≤3.5 Customers are not satisfied with reliability of ATM services provided by banking sector

Fulfillment

Ho : µ ≥3.5 Customers are satisfied with fulfillment of ATM services provided by banking sector

H₁ : µ ≤3.5 Customers are not satisfied with fulfillment of ATM services provided by banking sector

Responsiveness

Ho : µ ≥3.5 Customers are satisfied with responsiveness of ATM services provided by banking sectorH₁ : µ ≤3.5 Customers are not satisfied with responsiveness of ATM services provided by banking sector

40

Hypothesis for Internet Banking

Customer Satisfaction

Ho : µ ≥3.5 Customers are satisfied with Internet Banking services provided by banking sector

H₁ : µ ≤3.5 Customers are not satisfied Internet Banking services provided by banking sector

Efficiency

Ho : µ ≥3.5 Customers are satisfied with efficiency Internet Banking services provided by banking sector

H₁ : µ ≤3.5 Customers are not satisfied with efficiency of InternetBanking services provided by bankingsector

Privacy

Ho : µ ≥3.5 Customers are satisfied with privacy of Internet Banking services provided by banking sector

H₁ : µ ≤3.5 Customers are not satisfied with privacy of Internet Banking services provided by banking sector

Reliability

Ho : µ ≥3.5 Customers are satisfied with reliability of Internet Banking services provided by banking sector

H₁ : µ ≤3.5 Customers are not satisfied with reliability of InternetBanking services provided by banking sector

Fulfillment

Ho : µ ≥3.5 Customers are satisfied with fulfillment of Internet Banking services provided by banking sector

H₁ : µ ≤3.5 Customers are not satisfied with fulfillment of InternetBanking service provided by banking sector

Responsiveness

Ho : µ ≥3.5 Customers are satisfied with responsiveness of Internet Banking services provided by banking sectorH₁ : µ ≤3.5 Customers are not satisfied with responsiveness of Internet Banking services provided by banking sector

41

Hypothesis for TeleBankingCustomer Satisfaction

Ho : µ ≥3.5 Customers are satisfied with TeleBanking services provided by banking sector

H₁ : µ ≤3.5 Customers are not satisfied TeleBanking services provided by banking sector

Efficiency

Ho : µ ≥3.5 Customers are satisfied with efficiency TeleBanking services provided by banking sector

H₁ : µ ≤3.5 Customers are not satisfied with efficiency of TeleBanking services provided by banking sector

Privacy

Ho : µ ≥3.5 Customers are satisfied with privacy of TeleBanking services provided by banking sector

H₁ : µ ≤3.5 Customers are not satisfied with privacy of TeleBanking services provided by banking sector

Reliability

Ho : µ ≥3.5 Customers are satisfied with reliability of TeleBanking services provided by banking sector

H₁ : µ ≤3.5 Customers are not satisfied with reliability of TeleBanking services provided by banking sector

Fulfillment

Ho : µ ≥3.5 Customers are satisfied with fulfillment of TeleBanking services provided by banking sector

H₁ : µ ≤3.5 Customers are not satisfied with fulfillment of TeleBanking services provided by banking sector

Responsiveness

Ho : µ ≥3.5 Customers are satisfied with responsiveness of TeleBanking services provided by banking sectorH₁ : µ ≤3.5 Customers are not satisfied with responsiveness of TeleBanking service provided by banking sector

42

3.8 Data Analysis:

3.8.1 Statistical Tools

Statistical tools used in this research are;

Descriptive Statistics (Mean & SD) Reliability Analysis – Cronbach’s Alpha Linear Regression Analysis Z-test Correlation

3.8.2 Plan of Data Analysis

Z-test Descriptive Statistics (Mean & SD) is used in hypothesis testing, measuring customer satisfaction and to analyze response weightage

Reliability Analysis – Cronbach’s Alpha is used in measuring reliability of among all variables/factors and survey questions

Linear Regression Analysis is used to analyze the effect of independent variables on dependent variables

Correlation is used to analyze which factors/variables have high or low correlation

3.8.3 Softwares Employed

SPSS 13

Microsoft Excel 2007

43

4.0 Chapter – IVResearch Analysis & Interpretation

4.1 Data Analysis and Interpretation of ATM:

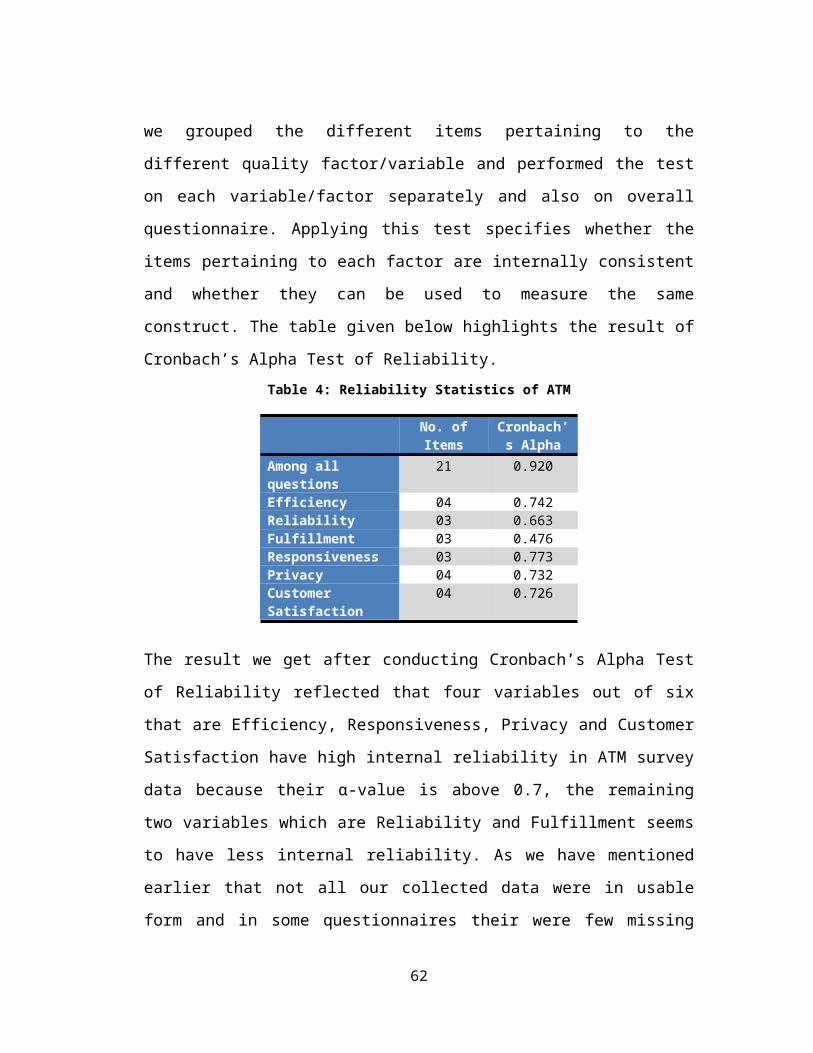

In order to prove the internal reliability of the model used, Cronbach’s Alpha Test of

Reliability has been performed on ATM survey data. When performing this test, we

grouped the different items pertaining to the different quality factor/variable and

performed the test on each variable/factor separately and also on overall

questionnaire. Applying this test specifies whether the items pertaining to each

factor are internally consistent and whether they can be used to measure the same

construct. The table given below highlights the result of Cronbach’s Alpha Test of

Reliability.

Table 4: Reliability Statistics of ATM

No. of Items

Cronbach’s Alpha

Among all questions 21 0.920Efficiency 04 0.742Reliability 03 0.663Fulfillment 03 0.476Responsiveness 03 0.773Privacy 04 0.732Customer Satisfaction 04 0.726