Embed Size (px)

Citation preview

Investment Research

www.danskebank.com/CI

FX Forecast Update 18 January 2016

Living with lower oil and a weaker China

Thomas Harr Global Head of FICC Research, +45 45 13 67 31 Stefan Mellin Jens Nærvig Pedersen Kristoffer Lomholt Allan von Mehren

Senior Analyst Senior Analyst Analyst Chief Analyst

Morten Helt Christin Tuxen Vladimir Miklashevsky Jakob Ekholdt Christensen Senior Analyst Senior Analyst Analyst Chief Analyst www.danskebank.com/research

Important disclosures and certifications are contained from page 29 of this report

2 www.danskebank.com/CI

Forecast review part I

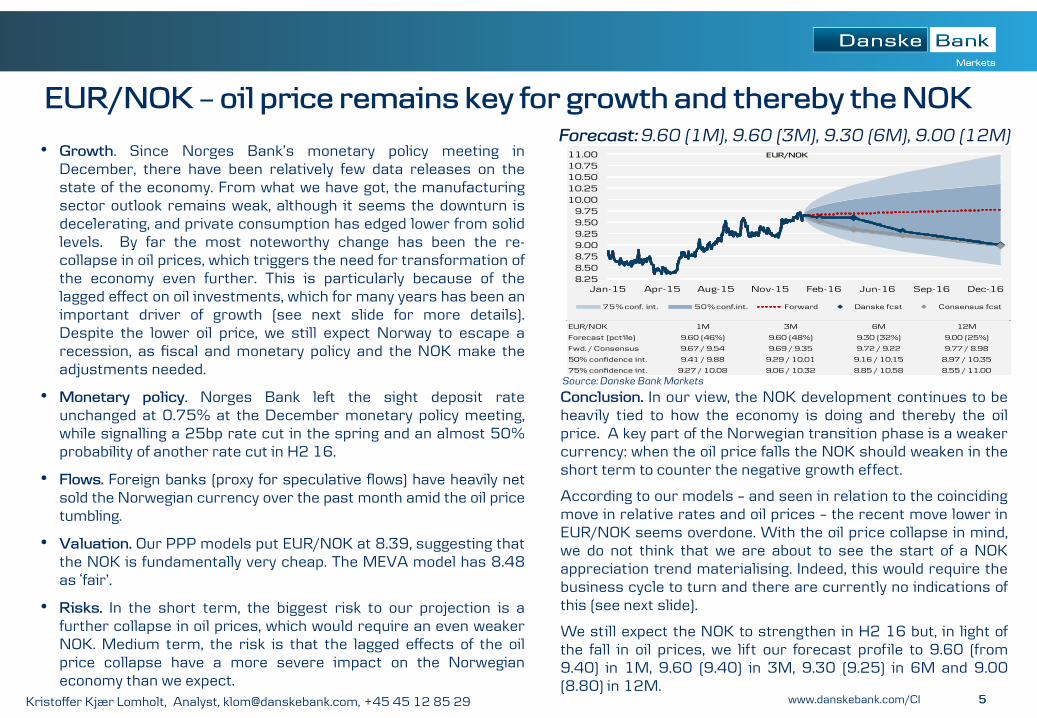

• EUR/NOK. The NOK development continues to be heavily tied to how the economy is doing and thereby the oil price. A key part of the Norwegian transition phase is a weaker currency. We still expect the NOK to strengthen in H2 16, when we expect the business cycle to turn, but, in light of the fall in oil prices over the past month, we lift our forecast profile to 9.60 (from 9.40) in 1M, 9.60 (9.40) in 3M, 9.30 (9.25) in 6M and 9.00 (8.80) in 12M.

• EUR/SEK. The cross has edged higher after the Riksbank stressed its determination to pursue its inflation target, highlighting the risk of a need for intervention to curb SEK strength, and we now look for a February rate cut as the more likely easing option. EUR/SEK will be trapped short term between the risk of Riksbank intervention if SEK appreciates too fast and strong Swedish fundamentals supporting the krona. Any intervention which could be relevant if EUR/SEK hits the 9.10-9.00 level within 3M say, should be 'defensive' in nature, i.e. no floor for EUR/SEK is likely. We have kept our 1M target intact at 9.30 and, based on recent communication from the Riksbank regarding its 'SEK preferences', we raise our forecasts further out to 9.30 (9.20) in 3M, 9.20 (9.10) in 6M and 9.00 (8.90) in 12M.

• EUR/DKK. We expect EUR/DKK to fall to 7.4550 on a 1M horizon and stay at this level on a 3-12M horizon (revised down from 7.4600) on the back of a risk of further ECB easing, a lower net position and the risk of the market pricing in an additional DN hike.

• EUR/USD. While relative rates could still weigh near term on markets pricing more in the way of Fed-ECB divergence, we continue to see the cross staying within the 1.05-1.10 range on a 1-3M horizon. We stress that the key story for 2016 will be that of a EUR/USD rebound as cyclical, valuation, flows and positioning are set to be supportive of the cross. We have left our forecasts unchanged and thus still project the pair at 1.16 in 12M.

• USD/CNY. We look for further depreciation of the CNY as market pressure will persist and diverging monetary policy continues to move in favour of the USD versus CNY. We see USD/CNY rising to 7.00 on 12m.

• NZD/USD. The NZD has had a rough start to the year on the China-commodities combo. We keep our 6-12M forecasts unchanged but highlight the risk of downside near term as commodity prices are set to remain under pressure still and as USD should see some Fed support. However, NZD/USD should see some support medium term (12M forecast of 0.68) as the USD rally fades and as RBNZ easing speculations fade.

3 www.danskebank.com/CI

Forecast review part II

• USD/JPY. With the BoJ expected to continue its current QQE program at JPY80trn until 2017 and additional hikes from the Fed to some extend already priced, we expect USD/JPY to be caught in a 118-123 range in the coming 12 months. We have lowered our forecast profile (main scenario) and now look for a gradual increase to118 ( 124) in 1M, and 120 in 3, 6 and 12M (was 124, 125 and 125, respectively) as relative rates is expected to be less supportive for USD/JPY going forward. However, we stress that risk remain skewed to the upside in the event of additional BoJ easing.

• EUR/GBP. GBP has started the new year on a very weak note, and GBP is likely to remain under pressure in a negative risk environment. We have therefore raised our 1M forecast to 0.75 (0.74). However, GBP is significantly oversold at the moment, and while Brexit concerns might weigh on the currency going forward, we still look for a rebound in the coming three-six months driven by a repricing of the BoE, as the UK economy is expected to continue to grow above trend. We target 0.73 in 3M and 0.71 in 6M. In H2 16, the Brexit theme should gather further pace as the referendum moves closer and weigh increasingly on GBP, while the euro, to a greater extent, should benefit from fundamentals and we now target EUR/GBP at 0.75 in 12M.

• EUR/CHF. SNB was left unchallenged by the ECB’s light easing package in December and will, in our view, be on hold for the foreseeable future as the ECB should be easing. EUR/CHF should stay in the 1.07-1.10 range in coming months but we continue to see the cross tick higher towards 1.15 in 12M, as a range of valuation metrics suggest CHF remains heavily overvalued.

• USD/CAD. Following the latest oil-price rout CAD has taken a serious beating as markets are now pricing in more than a 50/50 chance of a near-term Bank of Canada rate cut. We acknowledge that it is a close call, but we think the BoC will keep rates unchanged at the January meeting as the USD/CAD uptick should do a lot of the rebalancing work. One possibility is that the BoC could re-introduce a form of forward guidance as governor Poloz's predecessor, Carney, pursued with some success in order to anchor rate expectations. While unchanged rates could send USD/CAD a tad lower near term, we still expect the cross to be supported by Fed hiking and oil prices that will stay low for longer. Thus, we have upped our near-term forecasts, now forecasting the cross at 1.45 in 3M (1.36) while keeping our 12M projection at 1.30.

4 www.danskebank.com/CI

Forecast review part III

• USD/RUB. As the Fed’s historical hike in December 2015 is left behind being mostly priced in to EM assets and the RUB, the deteriorating oil story and global volatility in risk sentiment on China woes have become the main driver for the RUB and will dominate in both the short and medium term. Yet, we have become slightly bullish on the RUB in the long run as the free float is protecting Russia’s current account surplus and economy despite the challenging economic situation. Rising oil prices and marginal FX redemptions by the corporate sector should also be RUB supportive. We have significantly upped our USD/RUB profile and now see the cross at 79.80 in 1M, 82.00 in 3M (71.00 previously), 84.50 in 6M (72.50 previously), while cutting the long-end to 72.00 in 12M (73.00 previously).

• USD/TRY. We expect the lira to weaken on a 3M horizon to 3.10 (2.90 previously) as we expect political uncertainty and the Fed’s possible hikes to weigh on sentiment. However, we forecast a slight improvement in the TRY spot in the long run on Turkey’s sustainable macro indicators as the low oil price eases pressure on the current account deficit. We expect the cross to hit 2.95 in 6M (2.80 previously) and 2.85 in 12M (2.80 previously).

• EMEA. We are seeing a weaker path than we had expected for the PLN and HUF due to global and domestic (only in the case of the PLN) risks. The new path for the EUR/PLN is 4.48 (1M), 4.40 (3M), 4.30 (6M) and 4.15 (12M). We expect the political risk premium to dissipate over time and the relatively strong growth prospects increasingly to support the zloty. On the HUF, we expect global market volatility to have a negative impact in the short term and, therefore, we increase our 1M forecast to 4.12 (from 4.10) but maintain our expectation of a strengthening of the HUF versus the EUR to 300 in 12M.

5 www.danskebank.com/CI

Forecast: 9.60 (1M), 9.60 (3M), 9.30 (6M), 9.00 (12M)

EUR/NOK – oil price remains key for growth and thereby the NOK

• Growth. Since Norges Bank’s monetary policy meeting in December, there have been relatively few data releases on the state of the economy. From what we have got, the manufacturing sector outlook remains weak, although it seems the downturn is decelerating, and private consumption has edged lower from solid levels. By far the most noteworthy change has been the re-collapse in oil prices, which triggers the need for transformation of the economy even further. This is particularly because of the lagged effect on oil investments, which for many years has been an important driver of growth (see next slide for more details). Despite the lower oil price, we still expect Norway to escape a recession, as fiscal and monetary policy and the NOK make the adjustments needed.

• Monetary policy. Norges Bank left the sight deposit rate unchanged at 0.75% at the December monetary policy meeting, while signalling a 25bp rate cut in the spring and an almost 50% probability of another rate cut in H2 16.

• Flows. Foreign banks (proxy for speculative flows) have heavily net sold the Norwegian currency over the past month amid the oil price tumbling.

• Valuation. Our PPP models put EUR/NOK at 8.39, suggesting that the NOK is fundamentally very cheap. The MEVA model has 8.48 as ‘fair’.

• Risks. In the short term, the biggest risk to our projection is a further collapse in oil prices, which would require an even weaker NOK. Medium term, the risk is that the lagged effects of the oil price collapse have a more severe impact on the Norwegian economy than we expect.

5

Conclusion. In our view, the NOK development continues to be heavily tied to how the economy is doing and thereby the oil price. A key part of the Norwegian transition phase is a weaker currency: when the oil price falls the NOK should weaken in the short term to counter the negative growth effect.

According to our models – and seen in relation to the coinciding move in relative rates and oil prices – the recent move lower in EUR/NOK seems overdone. With the oil price collapse in mind, we do not think that we are about to see the start of a NOK appreciation trend materialising. Indeed, this would require the business cycle to turn and there are currently no indications of this (see next slide).

We still expect the NOK to strengthen in H2 16 but, in light of the fall in oil prices, we lift our forecast profile to 9.60 (from 9.40) in 1M, 9.60 (9.40) in 3M, 9.30 (9.25) in 6M and 9.00 (8.80) in 12M.

Kristoffer Kjær Lomholt, Analyst, [email protected], +45 45 12 85 29

Source: Danske Bank Markets

EUR/NOK 1M 3M 6M 12M

Forecast (pct'ile) 9.60 (46%) 9.60 (48%) 9.30 (32%) 9.00 (25%)

Fwd. / Consensus 9.67 / 9.54 9.69 / 9.35 9.72 / 9.22 9.77 / 8.98

50% confidence int. 9.41 / 9.88 9.29 / 10.01 9.16 / 10.15 8.97 / 10.35

75% confidence int. 9.27 / 10.08 9.06 / 10.32 8.85 / 10.58 8.55 / 11.00

k

8.258.508.759.009.259.509.75

10.0010.2510.5010.7511.00

Jan-15 Apr-15 Aug-15 Nov-15 Feb-16 Jun-16 Sep-16 Dec-16

EUR/NOK

75% conf. int. 50% conf.int. Forward Danske fcst Consensus fcst

6 www.danskebank.com/CI

EUR/NOK – important issues to watch

Oil investments challenge Norwegian growth...

• The oil price collapse challenges the economy through lower oil investments, with oil investments an important driver of growth in previous years, both directly and indirectly via the service and supply sectors living off the petroleum industry. Norwegian oil investments are dominated by a few very large projects,. While oil prices remain highly volatile in the short term, the forward curve still points to the major fields being profitable in coming years (see chart to the right).

• The 2016 projects are less vulnerable to short-term changes in the oil price. While we expect oil investments to fall significantly in the coming year, the negative effect on growth is offset by the highly expansionary fiscal policy and the positive contributions from public consumption and public investments.

...but we expect the economy to escape recession, partly due to a weaker NOK

• The three Norges Bank rates cuts over the past 13 months have substantially lowered the household interest burden, which is a supportive factor for the housing market and private consumption. Also, the substantial weakening of the NOK over the past years benefits Norwegian producers and keeps a floor under nominal income. In summary, our main view on Norway is a macroeconomic story: we expect Norway to escape a recession as monetary policy, fiscal policy and the currency take the adjustment.

• Although the NOK is substantially undervalued from a long-term perspective, the short-term outlook is tied closely to how the economy is doing and thereby the oil price. As a result, we expect the NOK to trade at weak levels until the business cycle turns and Norges Bank can signal that there is no longer a need to cut rates further. We think this will be the case in H2 16.

Kristoffer Kjær Lomholt, Analyst, [email protected], +45 45 12 85 29

Source: Rystad Energy, Ucube, Oljedirektoratet, Oslo Market Solutions

Expected future oil price is key for oil investments

0

10

20

30

40

50

60

70

80

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000 USD/bblMillion barrels

in oil equivalent Norwegian oil field investment overview

Ressources (lhs) HighB/E oil price (rhs) Current oil price (rhs)2Y Forward oil

NOK appreciation trend set to materialise

When business cycle turns

Source: Macrobond Financial, Danske Bank Markets

7 www.danskebank.com/CI

Forecast: 9.30 (1M), 9.30 (3M), 9.20 (6M), 9.00 (12M)

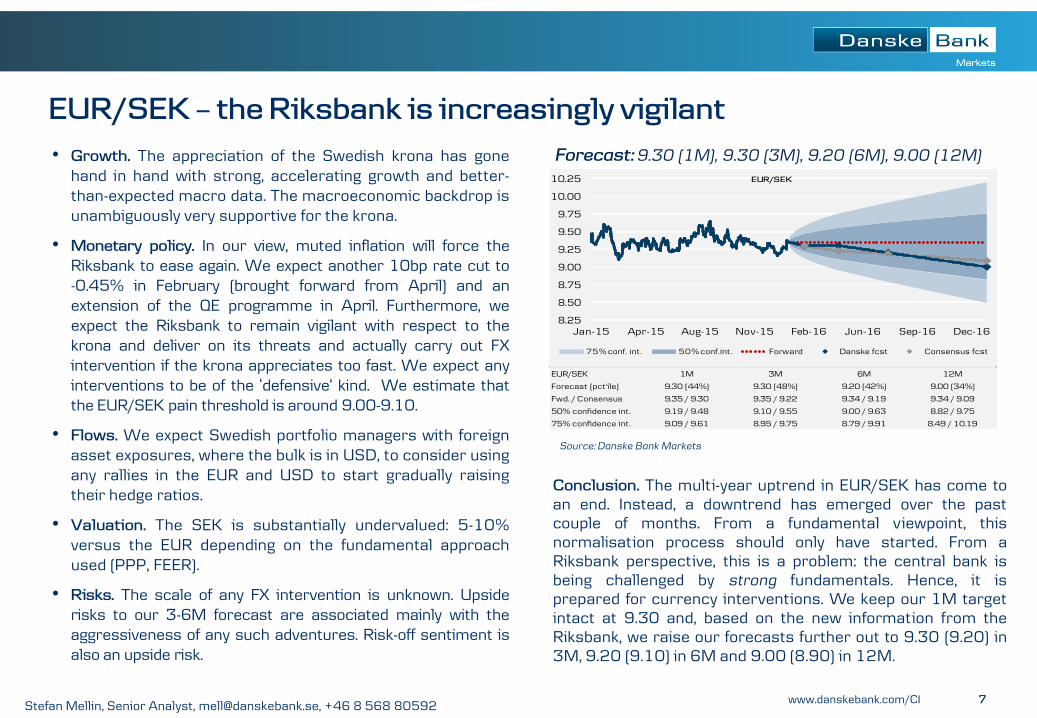

EUR/SEK – the Riksbank is increasingly vigilant

• Growth. The appreciation of the Swedish krona has gone hand in hand with strong, accelerating growth and better-than-expected macro data. The macroeconomic backdrop is unambiguously very supportive for the krona.

• Monetary policy. In our view, muted inflation will force the Riksbank to ease again. We expect another 10bp rate cut to -0.45% in February (brought forward from April) and an extension of the QE programme in April. Furthermore, we expect the Riksbank to remain vigilant with respect to the krona and deliver on its threats and actually carry out FX intervention if the krona appreciates too fast. We expect any interventions to be of the ‘defensive’ kind. We estimate that the EUR/SEK pain threshold is around 9.00-9.10.

• Flows. We expect Swedish portfolio managers with foreign asset exposures, where the bulk is in USD, to consider using any rallies in the EUR and USD to start gradually raising their hedge ratios.

• Valuation. The SEK is substantially undervalued: 5-10% versus the EUR depending on the fundamental approach used (PPP, FEER).

• Risks. The scale of any FX intervention is unknown. Upside risks to our 3-6M forecast are associated mainly with the aggressiveness of any such adventures. Risk-off sentiment is also an upside risk.

7

Conclusion. The multi-year uptrend in EUR/SEK has come to an end. Instead, a downtrend has emerged over the past couple of months. From a fundamental viewpoint, this normalisation process should only have started. From a Riksbank perspective, this is a problem: the central bank is being challenged by strong fundamentals. Hence, it is prepared for currency interventions. We keep our 1M target intact at 9.30 and, based on the new information from the Riksbank, we raise our forecasts further out to 9.30 (9.20) in 3M, 9.20 (9.10) in 6M and 9.00 (8.90) in 12M.

Source: Danske Bank Markets

Stefan Mellin, Senior Analyst, [email protected], +46 8 568 80592

EUR/SEK 1M 3M 6M 12M

Forecast (pct'ile) 9.30 (44%) 9.30 (48%) 9.20 (42%) 9.00 (34%)

Fwd. / Consensus 9.35 / 9.30 9.35 / 9.22 9.34 / 9.19 9.34 / 9.09

50% confidence int. 9.19 / 9.48 9.10 / 9.55 9.00 / 9.63 8.82 / 9.75

75% confidence int. 9.09 / 9.61 8.95 / 9.75 8.79 / 9.91 8.49 / 10.19

k

8.25

8.50

8.75

9.00

9.25

9.50

9.75

10.00

10.25

Jan-15 Apr-15 Aug-15 Nov-15 Feb-16 Jun-16 Sep-16 Dec-16

EUR/SEK

75% conf. int. 50% conf.int. Forward Danske fcst Consensus fcst

8 www.danskebank.com/CI

EUR/SEK – important issues to watch

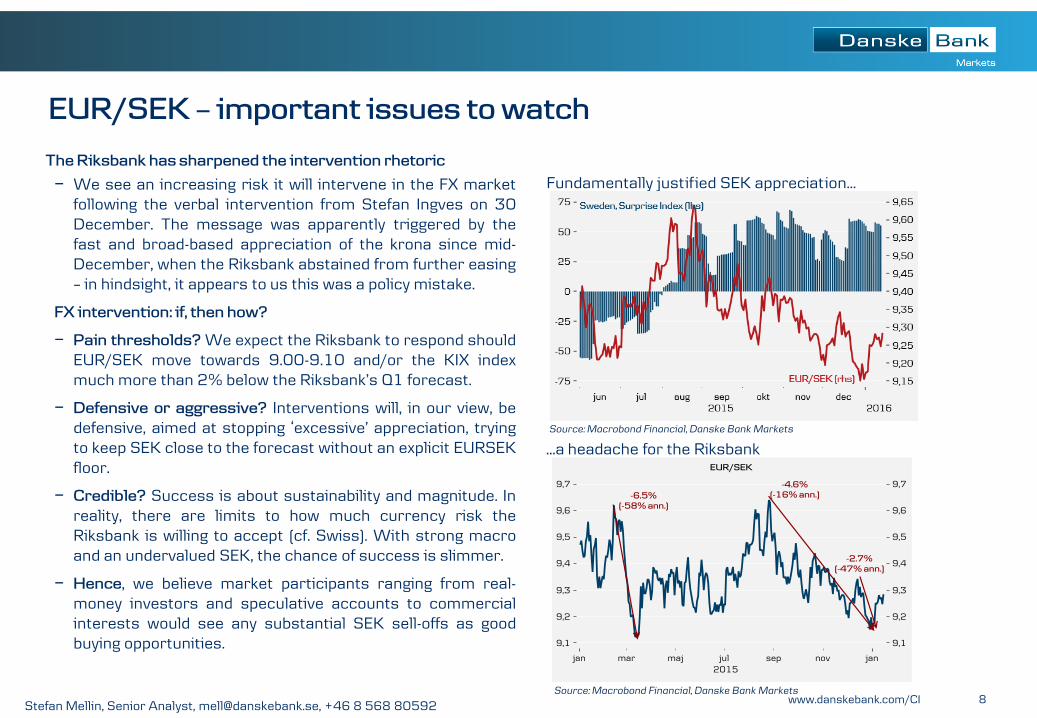

The Riksbank has sharpened the intervention rhetoric

− We see an increasing risk it will intervene in the FX market following the verbal intervention from Stefan Ingves on 30 December. The message was apparently triggered by the fast and broad-based appreciation of the krona since mid-December, when the Riksbank abstained from further easing – in hindsight, it appears to us this was a policy mistake.

FX intervention: if, then how?

− Pain thresholds? We expect the Riksbank to respond should EUR/SEK move towards 9.00-9.10 and/or the KIX index much more than 2% below the Riksbank’s Q1 forecast.

− Defensive or aggressive? Interventions will, in our view, be defensive, aimed at stopping ‘excessive’ appreciation, trying to keep SEK close to the forecast without an explicit EURSEK floor.

− Credible? Success is about sustainability and magnitude. In reality, there are limits to how much currency risk the Riksbank is willing to accept (cf. Swiss). With strong macro and an undervalued SEK, the chance of success is slimmer.

− Hence, we believe market participants ranging from real-money investors and speculative accounts to commercial interests would see any substantial SEK sell-offs as good buying opportunities.

Fundamentally justified SEK appreciation...

Source: Macrobond Financial, Danske Bank Markets

Source: Macrobond Financial, Danske Bank Markets

...a headache for the Riksbank

Stefan Mellin, Senior Analyst, [email protected], +46 8 568 80592

9 www.danskebank.com/CI

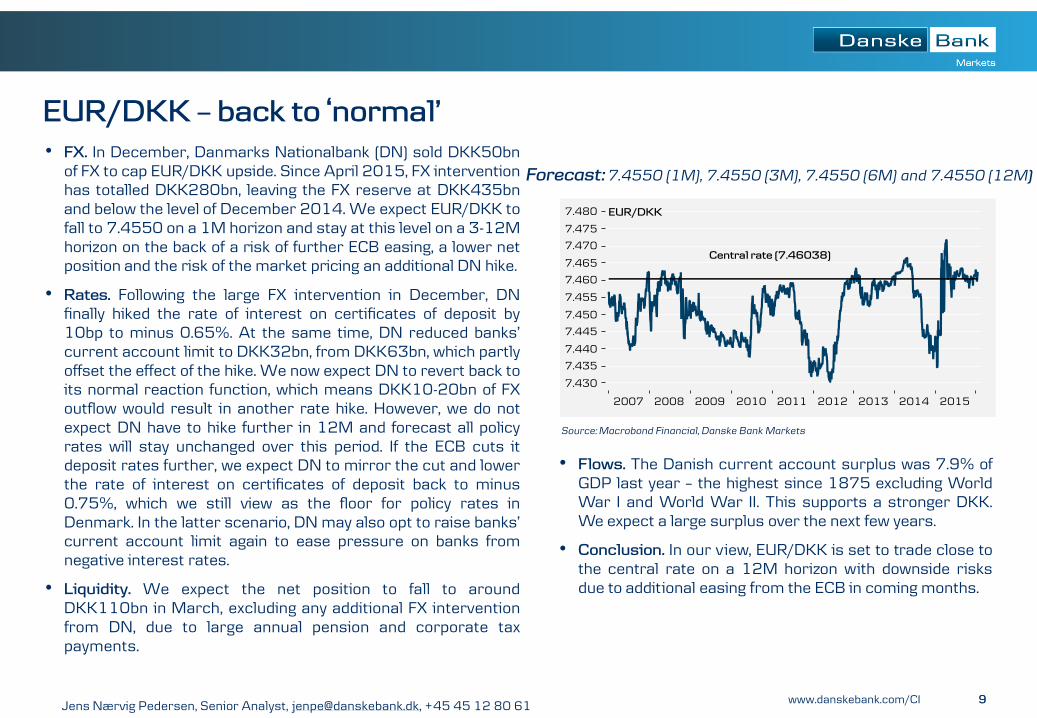

EUR/DKK – back to ‘normal’

• FX. In December, Danmarks Nationalbank (DN) sold DKK50bn of FX to cap EUR/DKK upside. Since April 2015, FX intervention has totalled DKK280bn, leaving the FX reserve at DKK435bn and below the level of December 2014. We expect EUR/DKK to fall to 7.4550 on a 1M horizon and stay at this level on a 3-12M horizon on the back of a risk of further ECB easing, a lower net position and the risk of the market pricing an additional DN hike.

• Rates. Following the large FX intervention in December, DN finally hiked the rate of interest on certificates of deposit by 10bp to minus 0.65%. At the same time, DN reduced banks’ current account limit to DKK32bn, from DKK63bn, which partly offset the effect of the hike. We now expect DN to revert back to its normal reaction function, which means DKK10-20bn of FX outflow would result in another rate hike. However, we do not expect DN have to hike further in 12M and forecast all policy rates will stay unchanged over this period. If the ECB cuts it deposit rates further, we expect DN to mirror the cut and lower the rate of interest on certificates of deposit back to minus 0.75%, which we still view as the floor for policy rates in Denmark. In the latter scenario, DN may also opt to raise banks’ current account limit again to ease pressure on banks from negative interest rates.

• Liquidity. We expect the net position to fall to around DKK110bn in March, excluding any additional FX intervention from DN, due to large annual pension and corporate tax payments.

9

• Flows. The Danish current account surplus was 7.9% of GDP last year – the highest since 1875 excluding World War I and World War II. This supports a stronger DKK. We expect a large surplus over the next few years.

• Conclusion. In our view, EUR/DKK is set to trade close to the central rate on a 12M horizon with downside risks due to additional easing from the ECB in coming months.

Source: Macrobond Financial, Danske Bank Markets

Jens Nærvig Pedersen, Senior Analyst, [email protected], +45 45 12 80 61

Forecast: 7.4550 (1M), 7.4550 (3M), 7.4550 (6M) and 7.4550 (12M)

10 www.danskebank.com/CI

Forecast: 1.06 (1M), 1.06 (3M), 1.10 (6M), 1.16 (12M)

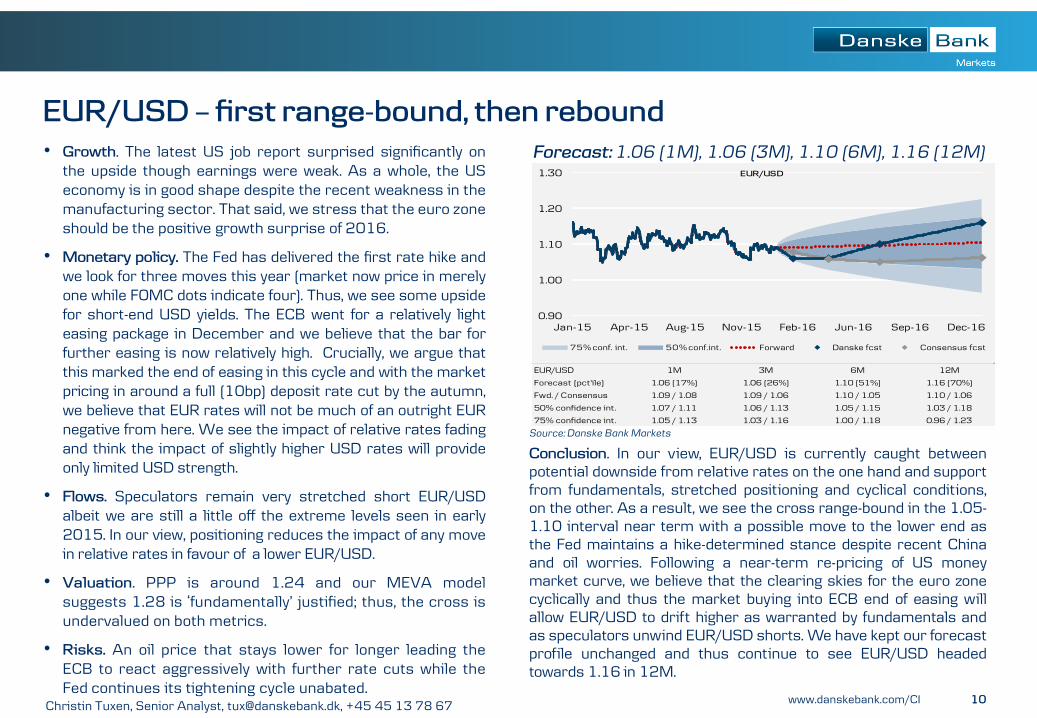

EUR/USD – first range-bound, then rebound

• Growth. The latest US job report surprised significantly on the upside though earnings were weak. As a whole, the US economy is in good shape despite the recent weakness in the manufacturing sector. That said, we stress that the euro zone should be the positive growth surprise of 2016.

• Monetary policy. The Fed has delivered the first rate hike and we look for three moves this year (market now price in merely one while FOMC dots indicate four). Thus, we see some upside for short-end USD yields. The ECB went for a relatively light easing package in December and we believe that the bar for further easing is now relatively high. Crucially, we argue that this marked the end of easing in this cycle and with the market pricing in around a full (10bp) deposit rate cut by the autumn, we believe that EUR rates will not be much of an outright EUR negative from here. We see the impact of relative rates fading and think the impact of slightly higher USD rates will provide only limited USD strength.

• Flows. Speculators remain very stretched short EUR/USD albeit we are still a little off the extreme levels seen in early 2015. In our view, positioning reduces the impact of any move in relative rates in favour of a lower EUR/USD.

• Valuation. PPP is around 1.24 and our MEVA model suggests 1.28 is ‘fundamentally’ justified; thus, the cross is undervalued on both metrics.

• Risks. An oil price that stays lower for longer leading the ECB to react aggressively with further rate cuts while the Fed continues its tightening cycle unabated.

10

Conclusion. In our view, EUR/USD is currently caught between potential downside from relative rates on the one hand and support from fundamentals, stretched positioning and cyclical conditions, on the other. As a result, we see the cross range-bound in the 1.05-1.10 interval near term with a possible move to the lower end as the Fed maintains a hike-determined stance despite recent China and oil worries. Following a near-term re-pricing of US money market curve, we believe that the clearing skies for the euro zone cyclically and thus the market buying into ECB end of easing will allow EUR/USD to drift higher as warranted by fundamentals and as speculators unwind EUR/USD shorts. We have kept our forecast profile unchanged and thus continue to see EUR/USD headed towards 1.16 in 12M.

Source: Danske Bank Markets

Christin Tuxen, Senior Analyst, [email protected], +45 45 13 78 67

EUR/USD 1M 3M 6M 12M

Forecast (pct'ile) 1.06 (17%) 1.06 (26%) 1.10 (51%) 1.16 (70%)

Fwd. / Consensus 1.09 / 1.08 1.09 / 1.06 1.10 / 1.05 1.10 / 1.06

50% confidence int. 1.07 / 1.11 1.06 / 1.13 1.05 / 1.15 1.03 / 1.18

75% confidence int. 1.05 / 1.13 1.03 / 1.16 1.00 / 1.18 0.96 / 1.23

k

0.90

1.00

1.10

1.20

1.30

Jan-15 Apr-15 Aug-15 Nov-15 Feb-16 Jun-16 Sep-16 Dec-16

EUR/USD

75% conf. int. 50% conf.int. Forward Danske fcst Consensus fcst

11 www.danskebank.com/CI

EUR/USD – important issues to watch

EUR/USD – important factors to watch this year

− Relative rates: favouring EUR/USD downside still but impact waning due to stretched positioning a EUR/USD negative only in the short term.

− Valuation: EUR/USD is fundamentally undervalued on both PPP and the Danske MEVA model EUR/USD positive.

− Flows: current account differential set to favour EUR versus USD still EUR/USD positive.

− Positioning: speculators remain very short EUR/USD EUR/USD positive.

− The Fed: history suggests first hike does not steer a clear direction for USD EUR/USD neutral.

− The ECB: we think December marked the end of easing and thus see current pricing of a 10bp deposit cut by the autumn as excessive EUR/USD positive.

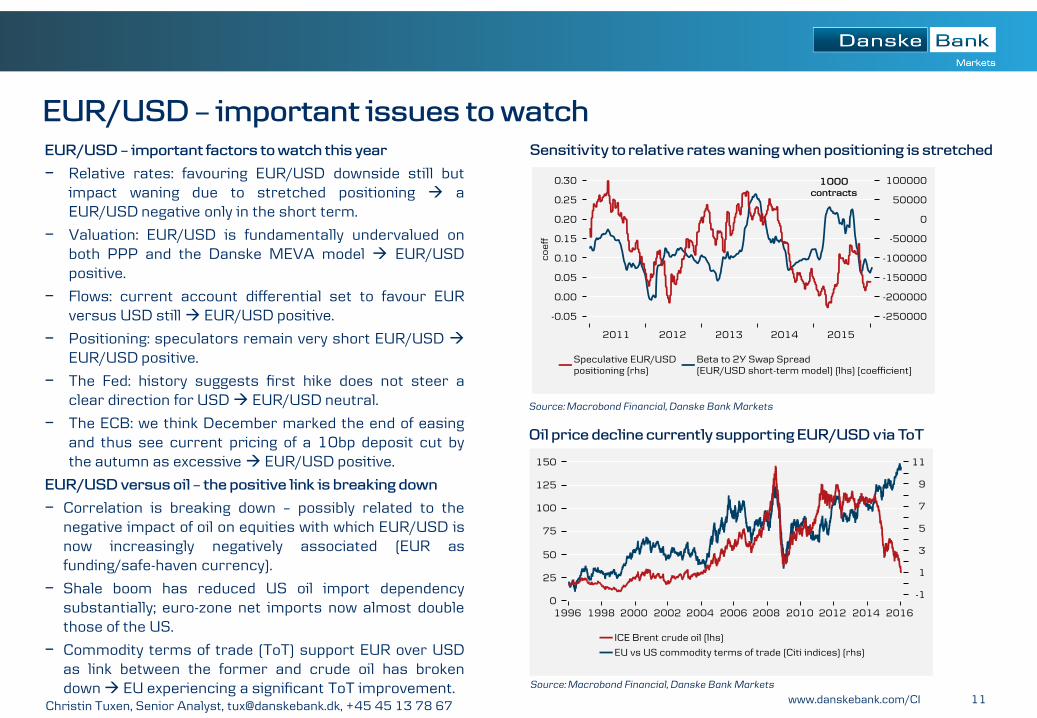

EUR/USD versus oil – the positive link is breaking down

− Correlation is breaking down – possibly related to the negative impact of oil on equities with which EUR/USD is now increasingly negatively associated (EUR as funding/safe-haven currency).

− Shale boom has reduced US oil import dependency substantially; euro-zone net imports now almost double those of the US.

− Commodity terms of trade (ToT) support EUR over USD as link between the former and crude oil has broken down EU experiencing a significant ToT improvement.

Source: Macrobond Financial, Danske Bank Markets

Source: Macrobond Financial, Danske Bank Markets

Oil price decline currently supporting EUR/USD via ToT

Sensitivity to relative rates waning when positioning is stretched

Christin Tuxen, Senior Analyst, [email protected], +45 45 13 78 67

12 www.danskebank.com/CI

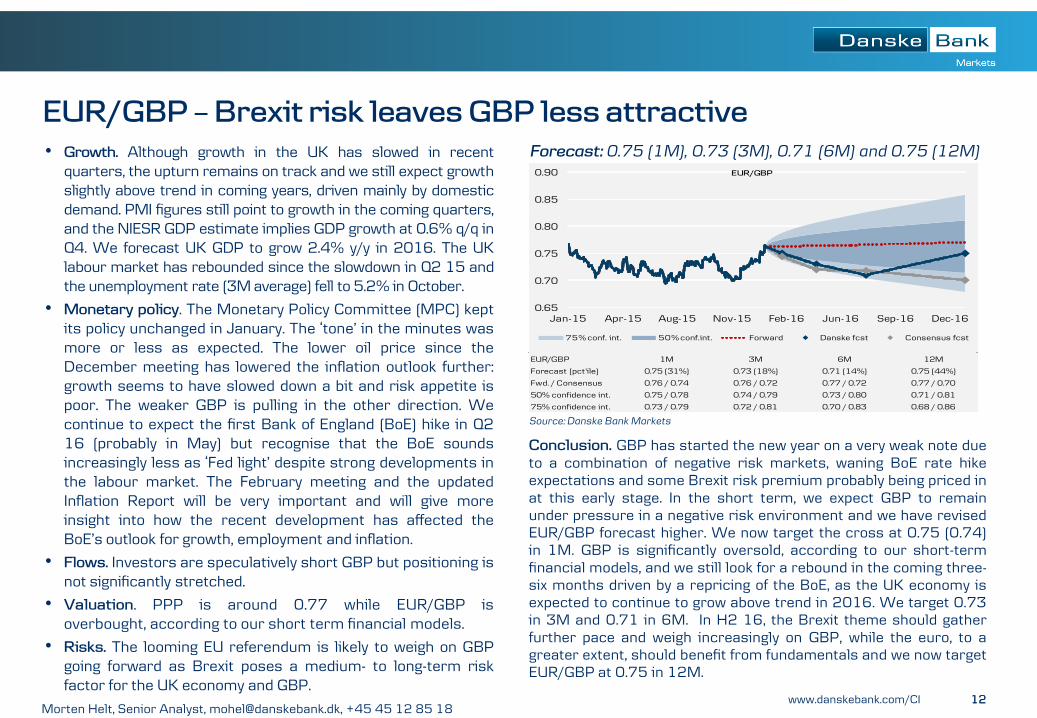

Forecast: 0.75 (1M), 0.73 (3M), 0.71 (6M) and 0.75 (12M)

EUR/GBP – Brexit risk leaves GBP less attractive

• Growth. Although growth in the UK has slowed in recent quarters, the upturn remains on track and we still expect growth slightly above trend in coming years, driven mainly by domestic demand. PMI figures still point to growth in the coming quarters, and the NIESR GDP estimate implies GDP growth at 0.6% q/q in Q4. We forecast UK GDP to grow 2.4% y/y in 2016. The UK labour market has rebounded since the slowdown in Q2 15 and the unemployment rate (3M average) fell to 5.2% in October.

• Monetary policy. The Monetary Policy Committee (MPC) kept its policy unchanged in January. The ‘tone’ in the minutes was more or less as expected. The lower oil price since the December meeting has lowered the inflation outlook further: growth seems to have slowed down a bit and risk appetite is poor. The weaker GBP is pulling in the other direction. We continue to expect the first Bank of England (BoE) hike in Q2 16 (probably in May) but recognise that the BoE sounds increasingly less as ‘Fed light’ despite strong developments in the labour market. The February meeting and the updated Inflation Report will be very important and will give more insight into how the recent development has affected the BoE’s outlook for growth, employment and inflation.

• Flows. Investors are speculatively short GBP but positioning is not significantly stretched.

• Valuation. PPP is around 0.77 while EUR/GBP is overbought, according to our short term financial models.

• Risks. The looming EU referendum is likely to weigh on GBP going forward as Brexit poses a medium- to long-term risk factor for the UK economy and GBP.

12

Conclusion. GBP has started the new year on a very weak note due to a combination of negative risk markets, waning BoE rate hike expectations and some Brexit risk premium probably being priced in at this early stage. In the short term, we expect GBP to remain under pressure in a negative risk environment and we have revised EUR/GBP forecast higher. We now target the cross at 0.75 (0.74) in 1M. GBP is significantly oversold, according to our short-term financial models, and we still look for a rebound in the coming three-six months driven by a repricing of the BoE, as the UK economy is expected to continue to grow above trend in 2016. We target 0.73 in 3M and 0.71 in 6M. In H2 16, the Brexit theme should gather further pace and weigh increasingly on GBP, while the euro, to a greater extent, should benefit from fundamentals and we now target EUR/GBP at 0.75 in 12M.

Source: Danske Bank Markets

Morten Helt, Senior Analyst, [email protected], +45 45 12 85 18

EUR/GBP 1M 3M 6M 12M

Forecast (pct'ile) 0.75 (31%) 0.73 (18%) 0.71 (14%) 0.75 (44%)

Fwd. / Consensus 0.76 / 0.74 0.76 / 0.72 0.77 / 0.72 0.77 / 0.70

50% confidence int. 0.75 / 0.78 0.74 / 0.79 0.73 / 0.80 0.71 / 0.81

75% confidence int. 0.73 / 0.79 0.72 / 0.81 0.70 / 0.83 0.68 / 0.86

k

0.65

0.70

0.75

0.80

0.85

0.90

Jan-15 Apr-15 Aug-15 Nov-15 Feb-16 Jun-16 Sep-16 Dec-16

EUR/GBP

75% conf. int. 50% conf.int. Forward Danske fcst Consensus fcst

13 www.danskebank.com/CI

EUR/GBP – important issues to watch

Brexit risk to weigh on GBP

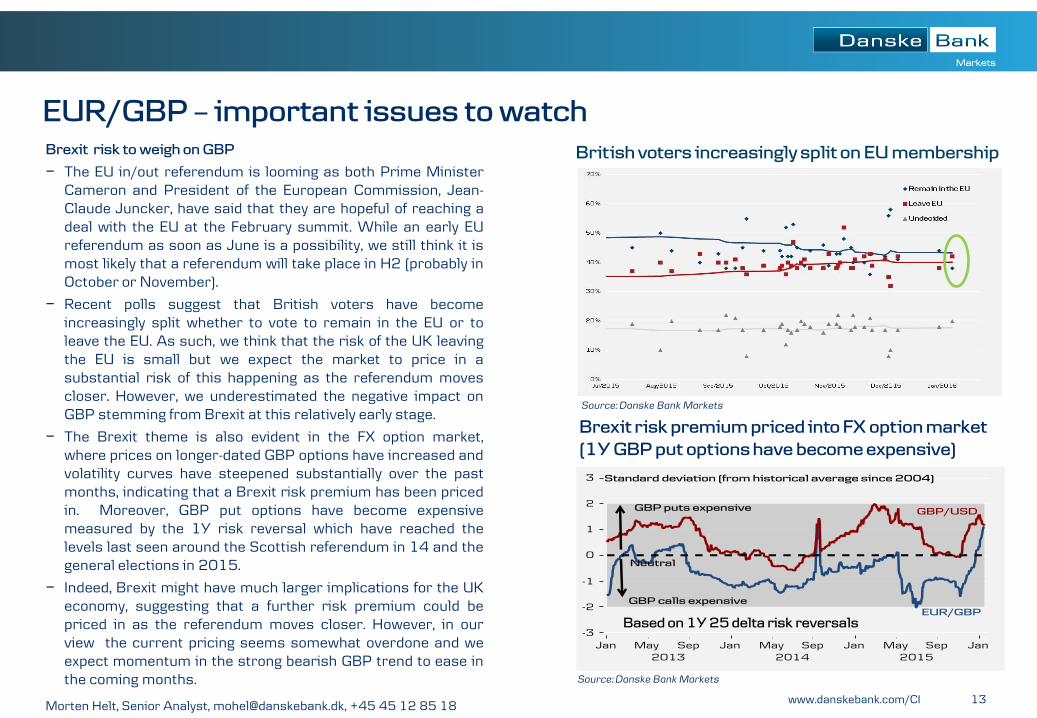

− The EU in/out referendum is looming as both Prime Minister Cameron and President of the European Commission, Jean-Claude Juncker, have said that they are hopeful of reaching a deal with the EU at the February summit. While an early EU referendum as soon as June is a possibility, we still think it is most likely that a referendum will take place in H2 (probably in October or November).

− Recent polls suggest that British voters have become increasingly split whether to vote to remain in the EU or to leave the EU. As such, we think that the risk of the UK leaving the EU is small but we expect the market to price in a substantial risk of this happening as the referendum moves closer. However, we underestimated the negative impact on GBP stemming from Brexit at this relatively early stage.

− The Brexit theme is also evident in the FX option market, where prices on longer-dated GBP options have increased and volatility curves have steepened substantially over the past months, indicating that a Brexit risk premium has been priced in. Moreover, GBP put options have become expensive measured by the 1Y risk reversal which have reached the levels last seen around the Scottish referendum in 14 and the general elections in 2015.

− Indeed, Brexit might have much larger implications for the UK economy, suggesting that a further risk premium could be priced in as the referendum moves closer. However, in our view the current pricing seems somewhat overdone and we expect momentum in the strong bearish GBP trend to ease in the coming months. Source: Danske Bank Markets

British voters increasingly split on EU membership

Brexit risk premium priced into FX option market

(1Y GBP put options have become expensive)

Morten Helt, Senior Analyst, [email protected], +45 45 12 85 18

Source: Danske Bank Markets

Based on 1Y 25 delta risk reversals

14 www.danskebank.com/CI

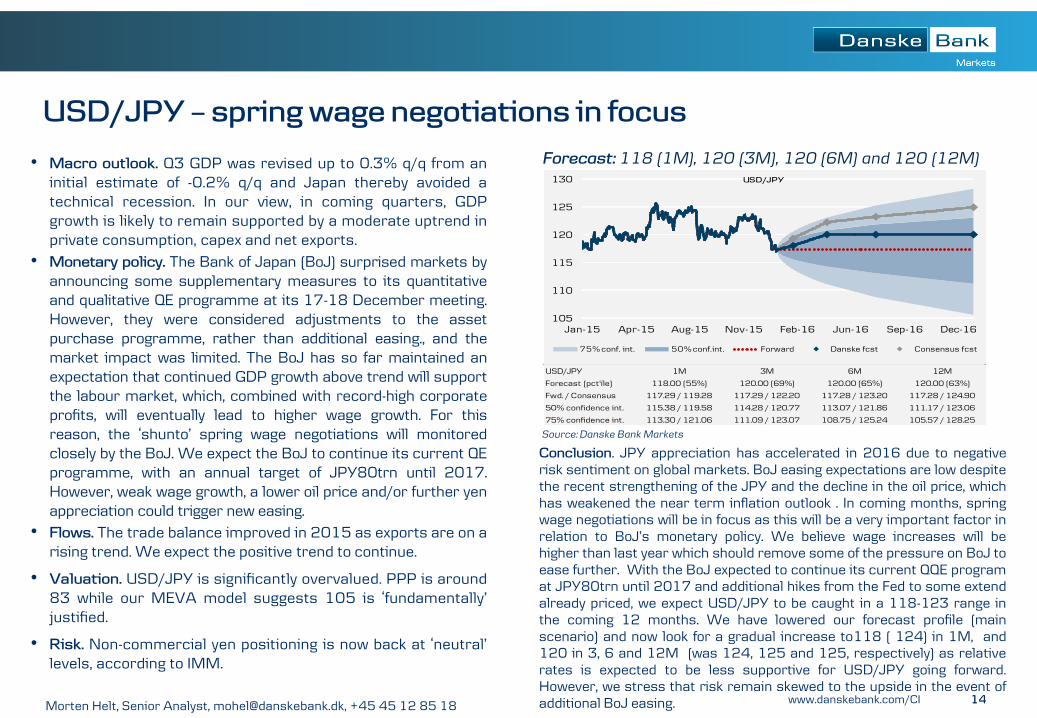

Forecast: 118 (1M), 120 (3M), 120 (6M) and 120 (12M)

USD/JPY – spring wage negotiations in focus

• Macro outlook. Q3 GDP was revised up to 0.3% q/q from an initial estimate of -0.2% q/q and Japan thereby avoided a technical recession. In our view, in coming quarters, GDP growth is likely to remain supported by a moderate uptrend in private consumption, capex and net exports.

• Monetary policy. The Bank of Japan (BoJ) surprised markets by announcing some supplementary measures to its quantitative and qualitative QE programme at its 17-18 December meeting. However, they were considered adjustments to the asset purchase programme, rather than additional easing., and the market impact was limited. The BoJ has so far maintained an expectation that continued GDP growth above trend will support the labour market, which, combined with record-high corporate profits, will eventually lead to higher wage growth. For this reason, the ‘shunto’ spring wage negotiations will monitored closely by the BoJ. We expect the BoJ to continue its current QE programme, with an annual target of JPY80trn until 2017. However, weak wage growth, a lower oil price and/or further yen appreciation could trigger new easing.

• Flows. The trade balance improved in 2015 as exports are on a rising trend. We expect the positive trend to continue.

• Valuation. USD/JPY is significantly overvalued. PPP is around 83 while our MEVA model suggests 105 is ‘fundamentally’ justified.

• Risk. Non-commercial yen positioning is now back at ‘neutral’ levels, according to IMM.

14

Conclusion. JPY appreciation has accelerated in 2016 due to negative risk sentiment on global markets. BoJ easing expectations are low despite the recent strengthening of the JPY and the decline in the oil price, which has weakened the near term inflation outlook . In coming months, spring wage negotiations will be in focus as this will be a very important factor in relation to BoJ’s monetary policy. We believe wage increases will be higher than last year which should remove some of the pressure on BoJ to ease further. With the BoJ expected to continue its current QQE program at JPY80trn until 2017 and additional hikes from the Fed to some extend already priced, we expect USD/JPY to be caught in a 118-123 range in the coming 12 months. We have lowered our forecast profile (main scenario) and now look for a gradual increase to118 ( 124) in 1M, and 120 in 3, 6 and 12M (was 124, 125 and 125, respectively) as relative rates is expected to be less supportive for USD/JPY going forward. However, we stress that risk remain skewed to the upside in the event of additional BoJ easing.

Source: Danske Bank Markets

Morten Helt, Senior Analyst, [email protected], +45 45 12 85 18

USD/JPY 1M 3M 6M 12M

Forecast (pct'ile) 118.00 (55%) 120.00 (69%) 120.00 (65%) 120.00 (63%)

Fwd. / Consensus 117.29 / 119.28 117.29 / 122.20 117.28 / 123.20 117.28 / 124.90

50% confidence int. 115.38 / 119.58 114.28 / 120.77 113.07 / 121.86 111.17 / 123.06

75% confidence int. 113.30 / 121.06 111.09 / 123.07 108.75 / 125.24 105.57 / 128.25

k

105

110

115

120

125

130

Jan-15 Apr-15 Aug-15 Nov-15 Feb-16 Jun-16 Sep-16 Dec-16

USD/JPY

75% conf. int. 50% conf.int. Forward Danske fcst Consensus fcst

15 www.danskebank.com/CI

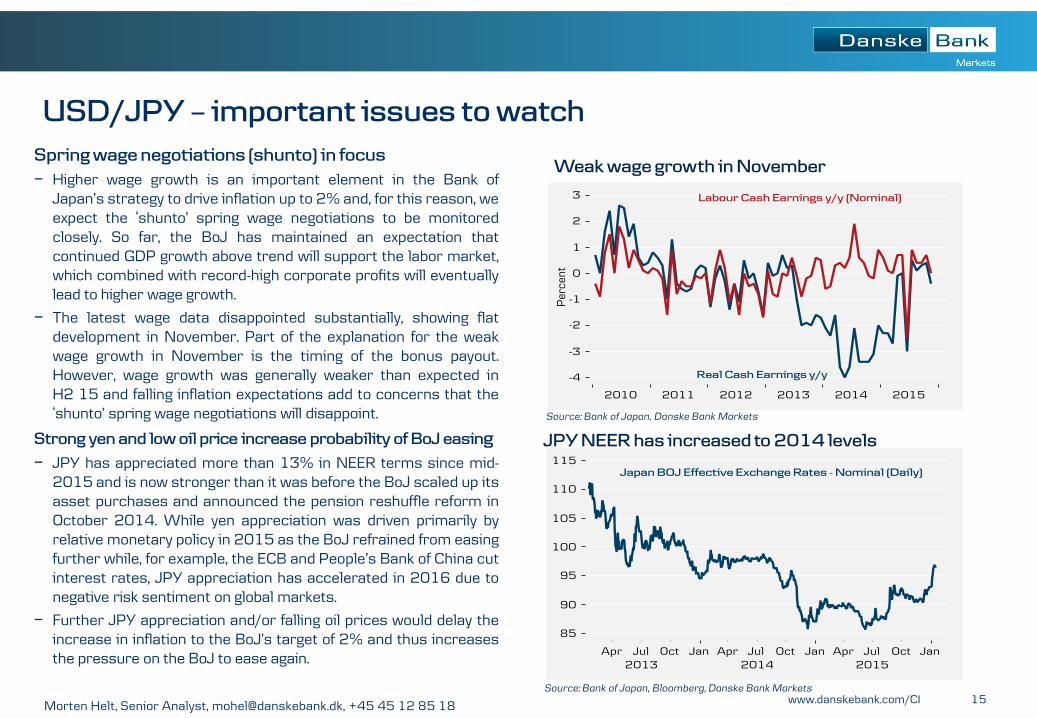

USD/JPY – important issues to watch

Spring wage negotiations (shunto) in focus

− Higher wage growth is an important element in the Bank of Japan’s strategy to drive inflation up to 2% and, for this reason, we expect the ‘shunto’ spring wage negotiations to be monitored closely. So far, the BoJ has maintained an expectation that continued GDP growth above trend will support the labor market, which combined with record-high corporate profits will eventually lead to higher wage growth.

− The latest wage data disappointed substantially, showing flat development in November. Part of the explanation for the weak wage growth in November is the timing of the bonus payout. However, wage growth was generally weaker than expected in H2 15 and falling inflation expectations add to concerns that the ‘shunto’ spring wage negotiations will disappoint.

Strong yen and low oil price increase probability of BoJ easing

− JPY has appreciated more than 13% in NEER terms since mid-2015 and is now stronger than it was before the BoJ scaled up its asset purchases and announced the pension reshuffle reform in October 2014. While yen appreciation was driven primarily by relative monetary policy in 2015 as the BoJ refrained from easing further while, for example, the ECB and People’s Bank of China cut interest rates, JPY appreciation has accelerated in 2016 due to negative risk sentiment on global markets.

− Further JPY appreciation and/or falling oil prices would delay the increase in inflation to the BoJ’s target of 2% and thus increases the pressure on the BoJ to ease again.

Source: Bank of Japan, Bloomberg, Danske Bank Markets

Source: Bank of Japan, Danske Bank Markets

Weak wage growth in November

Morten Helt, Senior Analyst, [email protected], +45 45 12 85 18

JPY NEER has increased to 2014 levels

16 www.danskebank.com/CI

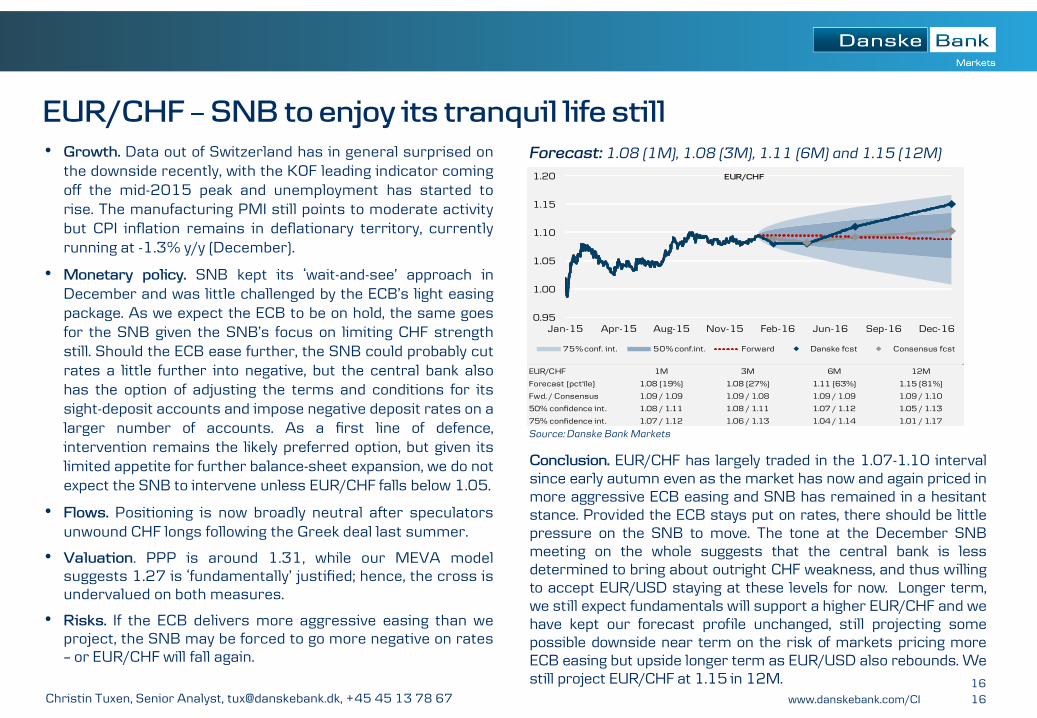

Forecast: 1.08 (1M), 1.08 (3M), 1.11 (6M) and 1.15 (12M)

EUR/CHF – SNB to enjoy its tranquil life still

• Growth. Data out of Switzerland has in general surprised on the downside recently, with the KOF leading indicator coming off the mid-2015 peak and unemployment has started to rise. The manufacturing PMI still points to moderate activity but CPI inflation remains in deflationary territory, currently running at -1.3% y/y (December).

• Monetary policy. SNB kept its ‘wait-and-see’ approach in December and was little challenged by the ECB’s light easing package. As we expect the ECB to be on hold, the same goes for the SNB given the SNB’s focus on limiting CHF strength still. Should the ECB ease further, the SNB could probably cut rates a little further into negative, but the central bank also has the option of adjusting the terms and conditions for its sight-deposit accounts and impose negative deposit rates on a larger number of accounts. As a first line of defence, intervention remains the likely preferred option, but given its limited appetite for further balance-sheet expansion, we do not expect the SNB to intervene unless EUR/CHF falls below 1.05.

• Flows. Positioning is now broadly neutral after speculators unwound CHF longs following the Greek deal last summer.

• Valuation. PPP is around 1.31, while our MEVA model suggests 1.27 is ‘fundamentally’ justified; hence, the cross is undervalued on both measures.

• Risks. If the ECB delivers more aggressive easing than we project, the SNB may be forced to go more negative on rates – or EUR/CHF will fall again.

16

Conclusion. EUR/CHF has largely traded in the 1.07-1.10 interval since early autumn even as the market has now and again priced in more aggressive ECB easing and SNB has remained in a hesitant stance. Provided the ECB stays put on rates, there should be little pressure on the SNB to move. The tone at the December SNB meeting on the whole suggests that the central bank is less determined to bring about outright CHF weakness, and thus willing to accept EUR/USD staying at these levels for now. Longer term, we still expect fundamentals will support a higher EUR/CHF and we have kept our forecast profile unchanged, still projecting some possible downside near term on the risk of markets pricing more ECB easing but upside longer term as EUR/USD also rebounds. We still project EUR/CHF at 1.15 in 12M.

Source: Danske Bank Markets

Christin Tuxen, Senior Analyst, [email protected], +45 45 13 78 67

EUR/CHF 1M 3M 6M 12M

Forecast (pct'ile) 1.08 (19%) 1.08 (27%) 1.11 (63%) 1.15 (81%)

Fwd. / Consensus 1.09 / 1.09 1.09 / 1.08 1.09 / 1.09 1.09 / 1.10

50% confidence int. 1.08 / 1.11 1.08 / 1.11 1.07 / 1.12 1.05 / 1.13

75% confidence int. 1.07 / 1.12 1.06 / 1.13 1.04 / 1.14 1.01 / 1.17

k

0.95

1.00

1.05

1.10

1.15

1.20

Jan-15 Apr-15 Aug-15 Nov-15 Feb-16 Jun-16 Sep-16 Dec-16

EUR/CHF

75% conf. int. 50% conf.int. Forward Danske fcst Consensus fcst

17 www.danskebank.com/CI

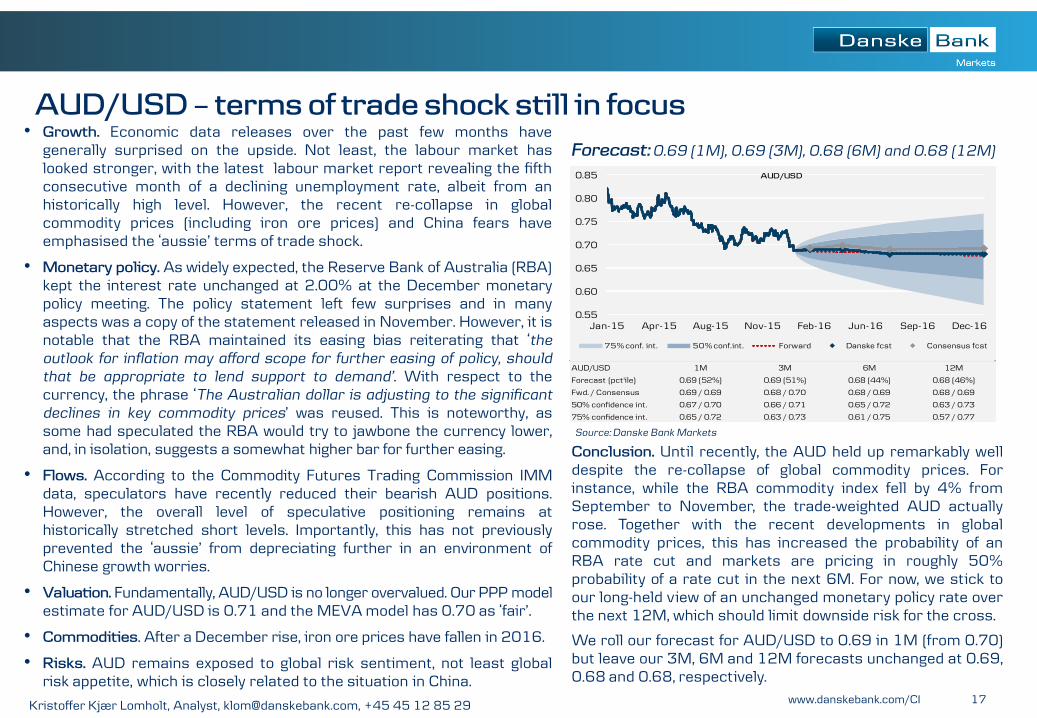

Forecast: 0.69 (1M), 0.69 (3M), 0.68 (6M) and 0.68 (12M)

AUD/USD – terms of trade shock still in focus

• Growth. Economic data releases over the past few months have generally surprised on the upside. Not least, the labour market has looked stronger, with the latest labour market report revealing the fifth consecutive month of a declining unemployment rate, albeit from an historically high level. However, the recent re-collapse in global commodity prices (including iron ore prices) and China fears have emphasised the ‘aussie’ terms of trade shock.

• Monetary policy. As widely expected, the Reserve Bank of Australia (RBA) kept the interest rate unchanged at 2.00% at the December monetary policy meeting. The policy statement left few surprises and in many aspects was a copy of the statement released in November. However, it is notable that the RBA maintained its easing bias reiterating that ‘the

outlook for inflation may afford scope for further easing of policy, should

that be appropriate to lend support to demand’. With respect to the currency, the phrase ‘The Australian dollar is adjusting to the significant

declines in key commodity prices’ was reused. This is noteworthy, as some had speculated the RBA would try to jawbone the currency lower, and, in isolation, suggests a somewhat higher bar for further easing.

• Flows. According to the Commodity Futures Trading Commission IMM data, speculators have recently reduced their bearish AUD positions. However, the overall level of speculative positioning remains at historically stretched short levels. Importantly, this has not previously prevented the ‘aussie’ from depreciating further in an environment of Chinese growth worries.

• Valuation. Fundamentally, AUD/USD is no longer overvalued. Our PPP model estimate for AUD/USD is 0.71 and the MEVA model has 0.70 as ‘fair’.

• Commodities. After a December rise, iron ore prices have fallen in 2016.

• Risks. AUD remains exposed to global risk sentiment, not least global risk appetite, which is closely related to the situation in China.

Conclusion. Until recently, the AUD held up remarkably well despite the re-collapse of global commodity prices. For instance, while the RBA commodity index fell by 4% from September to November, the trade-weighted AUD actually rose. Together with the recent developments in global commodity prices, this has increased the probability of an RBA rate cut and markets are pricing in roughly 50% probability of a rate cut in the next 6M. For now, we stick to our long-held view of an unchanged monetary policy rate over the next 12M, which should limit downside risk for the cross.

We roll our forecast for AUD/USD to 0.69 in 1M (from 0.70) but leave our 3M, 6M and 12M forecasts unchanged at 0.69, 0.68 and 0.68, respectively.

Source: Danske Bank Markets

Kristoffer Kjær Lomholt, Analyst, [email protected], +45 45 12 85 29

AUD/USD 1M 3M 6M 12M

Forecast (pct'ile) 0.69 (52%) 0.69 (51%) 0.68 (44%) 0.68 (46%)

Fwd. / Consensus 0.69 / 0.69 0.68 / 0.70 0.68 / 0.69 0.68 / 0.69

50% confidence int. 0.67 / 0.70 0.66 / 0.71 0.65 / 0.72 0.63 / 0.73

75% confidence int. 0.65 / 0.72 0.63 / 0.73 0.61 / 0.75 0.57 / 0.77

k

0.55

0.60

0.65

0.70

0.75

0.80

0.85

Jan-15 Apr-15 Aug-15 Nov-15 Feb-16 Jun-16 Sep-16 Dec-16

AUD/USD

75% conf. int. 50% conf.int. Forward Danske fcst Consensus fcst

18 www.danskebank.com/CI

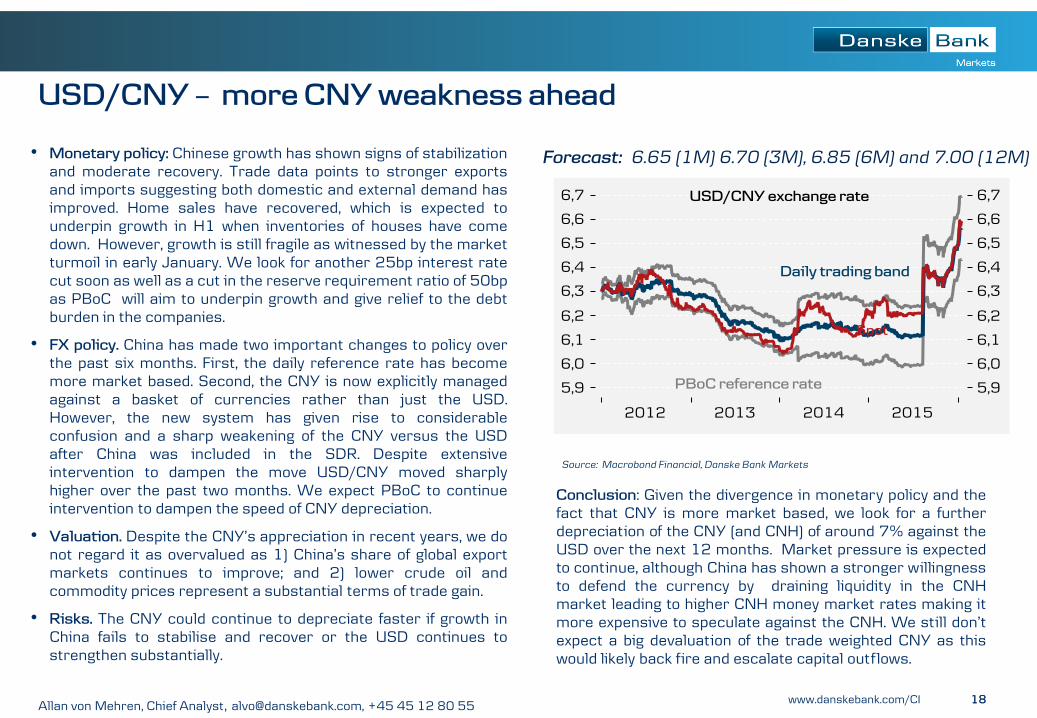

Forecast: 6.65 (1M) 6.70 (3M), 6.85 (6M) and 7.00 (12M)

USD/CNY – more CNY weakness ahead

• Monetary policy: Chinese growth has shown signs of stabilization and moderate recovery. Trade data points to stronger exports and imports suggesting both domestic and external demand has improved. Home sales have recovered, which is expected to underpin growth in H1 when inventories of houses have come down. However, growth is still fragile as witnessed by the market turmoil in early January. We look for another 25bp interest rate cut soon as well as a cut in the reserve requirement ratio of 50bp as PBoC will aim to underpin growth and give relief to the debt burden in the companies.

• FX policy. China has made two important changes to policy over the past six months. First, the daily reference rate has become more market based. Second, the CNY is now explicitly managed against a basket of currencies rather than just the USD. However, the new system has given rise to considerable confusion and a sharp weakening of the CNY versus the USD after China was included in the SDR. Despite extensive intervention to dampen the move USD/CNY moved sharply higher over the past two months. We expect PBoC to continue intervention to dampen the speed of CNY depreciation.

• Valuation. Despite the CNY’s appreciation in recent years, we do not regard it as overvalued as 1) China’s share of global export markets continues to improve; and 2) lower crude oil and commodity prices represent a substantial terms of trade gain.

• Risks. The CNY could continue to depreciate faster if growth in China fails to stabilise and recover or the USD continues to strengthen substantially.

18

Conclusion: Given the divergence in monetary policy and the fact that CNY is more market based, we look for a further depreciation of the CNY (and CNH) of around 7% against the USD over the next 12 months. Market pressure is expected to continue, although China has shown a stronger willingness to defend the currency by draining liquidity in the CNH market leading to higher CNH money market rates making it more expensive to speculate against the CNH. We still don’t expect a big devaluation of the trade weighted CNY as this would likely back fire and escalate capital outflows.

Source: Macrobond Financial, Danske Bank Markets

Allan von Mehren, Chief Analyst, [email protected], +45 45 12 80 55

19 www.danskebank.com/CI

Forecast: 79.80(1M), 82.00(3M), 84.50 (6M) and 72.00 (12M)

USD/RUB – amid oil and Chinese woes

• Growth. According to the final data, Russia’s GDP shrank 4.1% y/y in Q3 15 versus -4.6% y/y a quarter earlier. We expect our base case scenario forecast of 0.5% y/y growth to face significant downside risk in 2016 as crude price has dipped almost 20% YTD and the tight monetary stance continues.

• Monetary policy. Russia’s central bank (CBR) kept its key rate unchanged on 11 December at 11.0%. The main reasons given by the central bank to hold rates were ‘growing inflation risks’ despite continuing disinflation (12.9% y/y in December 2015 vs. 15.0% y/y a month earlier). As the weakening RUB keeps the inflation pressure on, we expect the CBR to stay on hold at its next meeting on 29 January 2016.

• Flows. In Q3 15, Russia saw capital inflows (USD5.4bn) for the first time since Q2 10 as remittances sent out dropped on low energy prices and locals are less involved in FX runs. We expect the current account surplus to continue in 2016 despite shrinking export revenues as imports are falling further.

• Valuation. Given the 30-day average of Brent price at USD35.6, the RUB continued to adjust to low oil price levels, yet staying overvalued at 73.1 versus the USD. Pressure for the USD/RUB upward correction remains.

• Risks. A further drop in oil price, China’s economy worsening woes and weak risk sentiment are clear downside risks for our RUB forecasts. A sudden oil price rebound and CBR’s rate hikes are the upside risks.

19

Conclusion. As the Fed’s historical hike is now behind us, being mostly well priced in to EM assets and the RUB, the deteriorating oil story and global volatility in risk sentiment on China woes have become the main driver for the RUB and are likely to dominate in both the short and medium term.

Yet, we have become slightly bullish on the RUB in the long run as the free f loat is protecting Russia’s current account surplus and economy despite the challenging economic situation. The rising oil price prospects given an upward oil futures curve and marginal FX redemptions by the corporate sector should also be RUB supportive.

Source: Danske Bank Markets

USD/RUB 1M 3M 6M 12M

Forecast (pct'ile) 79.80 (58%) 82.00 (64%) 84.50 (67%) 72.00 (31%)

Fwd. / Consensus 79.53 / 75.19 80.86 / 70.00 82.85 / 69.11 86.74 / 65.15

50% confidence int. 76.04 / 82.13 74.46 / 84.68 72.67 / 87.43 69.53 / 91.12

75% confidence int. 73.90 / 85.06 70.95 / 89.88 67.60 / 95.21 56.49 / 103.33

k

4550556065707580859095

100105

Jan-15 Apr-15 Aug-15 Nov-15 Feb-16 Jun-16 Sep-16 Dec-16

USD/RUB

75% conf. int. 50% conf.int. Forward Danske fcst Consensus fcst

Vladimir Miklashevsky, Economist/Trading Desk Strategist, [email protected], +358 10 546 75 22

20 www.danskebank.com/CI

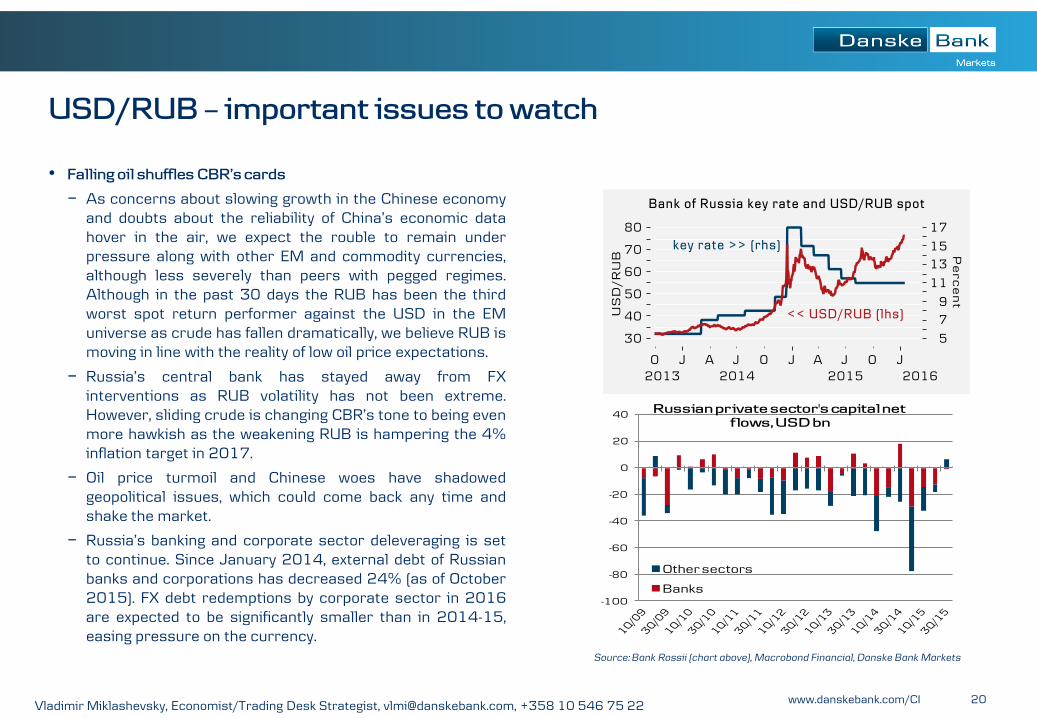

USD/RUB – important issues to watch

• Falling oil shuffles CBR’s cards

− As concerns about slowing growth in the Chinese economy and doubts about the reliability of China’s economic data hover in the air, we expect the rouble to remain under pressure along with other EM and commodity currencies, although less severely than peers with pegged regimes. Although in the past 30 days the RUB has been the third worst spot return performer against the USD in the EM universe as crude has fallen dramatically, we believe RUB is moving in line with the reality of low oil price expectations.

− Russia’s central bank has stayed away from FX interventions as RUB volatility has not been extreme. However, sliding crude is changing CBR’s tone to being even more hawkish as the weakening RUB is hampering the 4% inflation target in 2017.

− Oil price turmoil and Chinese woes have shadowed geopolitical issues, which could come back any time and shake the market.

− Russia’s banking and corporate sector deleveraging is set to continue. Since January 2014, external debt of Russian banks and corporations has decreased 24% (as of October 2015). FX debt redemptions by corporate sector in 2016 are expected to be significantly smaller than in 2014-15, easing pressure on the currency.

Vladimir Miklashevsky, Economist/Trading Desk Strategist, [email protected], +358 10 546 75 22

Source: Bank Rossii (chart above), Macrobond Financial, Danske Bank Markets

-100

-80

-60

-40

-20

0

20

40 Russian private sector's capital net

flows, USD bn

Other sectors

Banks

21 www.danskebank.com/CI

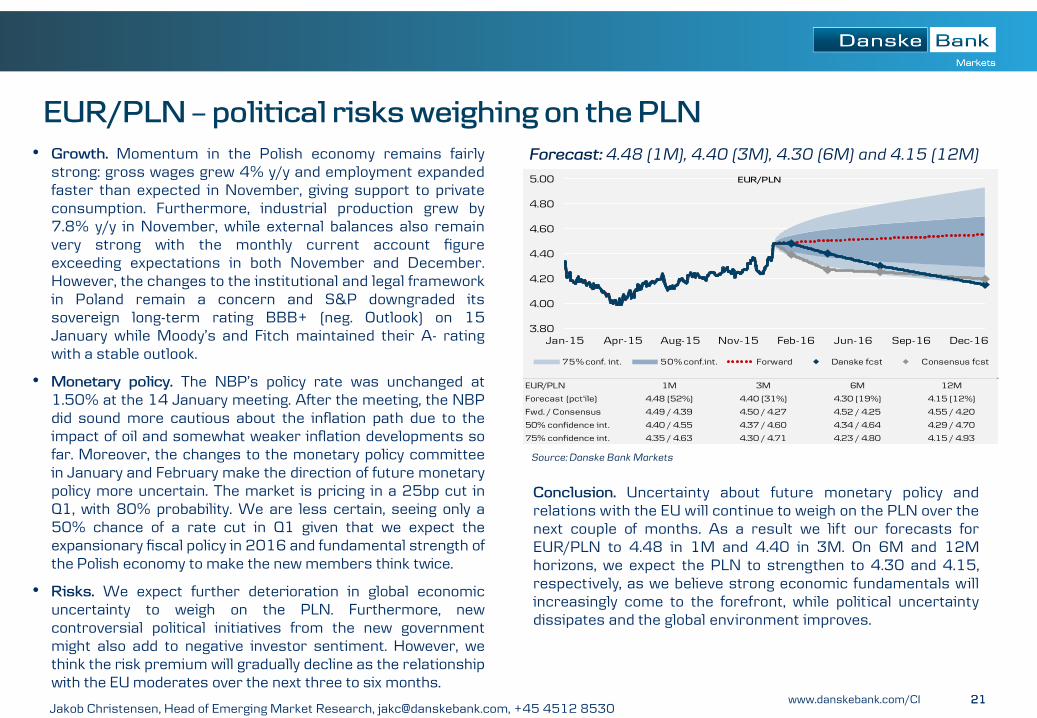

Forecast: 4.48 (1M), 4.40 (3M), 4.30 (6M) and 4.15 (12M)

EUR/PLN – political risks weighing on the PLN

• Growth. Momentum in the Polish economy remains fairly strong: gross wages grew 4% y/y and employment expanded faster than expected in November, giving support to private consumption. Furthermore, industrial production grew by 7.8% y/y in November, while external balances also remain very strong with the monthly current account figure exceeding expectations in both November and December. However, the changes to the institutional and legal framework in Poland remain a concern and S&P downgraded its sovereign long-term rating BBB+ (neg. Outlook) on 15 January while Moody’s and Fitch maintained their A- rating with a stable outlook.

• Monetary policy. The NBP’s policy rate was unchanged at 1.50% at the 14 January meeting. After the meeting, the NBP did sound more cautious about the inflation path due to the impact of oil and somewhat weaker inflation developments so far. Moreover, the changes to the monetary policy committee in January and February make the direction of future monetary policy more uncertain. The market is pricing in a 25bp cut in Q1, with 80% probability. We are less certain, seeing only a 50% chance of a rate cut in Q1 given that we expect the expansionary fiscal policy in 2016 and fundamental strength of the Polish economy to make the new members think twice.

• Risks. We expect further deterioration in global economic uncertainty to weigh on the PLN. Furthermore, new controversial political initiatives from the new government might also add to negative investor sentiment. However, we think the risk premium will gradually decline as the relationship with the EU moderates over the next three to six months.

21

Conclusion. Uncertainty about future monetary policy and relations with the EU will continue to weigh on the PLN over the next couple of months. As a result we lift our forecasts for EUR/PLN to 4.48 in 1M and 4.40 in 3M. On 6M and 12M horizons, we expect the PLN to strengthen to 4.30 and 4.15, respectively, as we believe strong economic fundamentals will increasingly come to the forefront, while political uncertainty dissipates and the global environment improves.

Jakob Christensen, Head of Emerging Market Research, [email protected], +45 4512 8530

Source: Danske Bank Markets

EUR/PLN 1M 3M 6M 12M

Forecast (pct'ile) 4.48 (52%) 4.40 (31%) 4.30 (19%) 4.15 (12%)

Fwd. / Consensus 4.49 / 4.39 4.50 / 4.27 4.52 / 4.25 4.55 / 4.20

50% confidence int. 4.40 / 4.55 4.37 / 4.60 4.34 / 4.64 4.29 / 4.70

75% confidence int. 4.35 / 4.63 4.30 / 4.71 4.23 / 4.80 4.15 / 4.93

k

3.80

4.00

4.20

4.40

4.60

4.80

5.00

Jan-15 Apr-15 Aug-15 Nov-15 Feb-16 Jun-16 Sep-16 Dec-16

EUR/PLN

75% conf. int. 50% conf.int. Forward Danske fcst Consensus fcst

22 www.danskebank.com/CI

Forecast: 312 (1M), 310 (3M), 305 (6M) and 300 (12M)

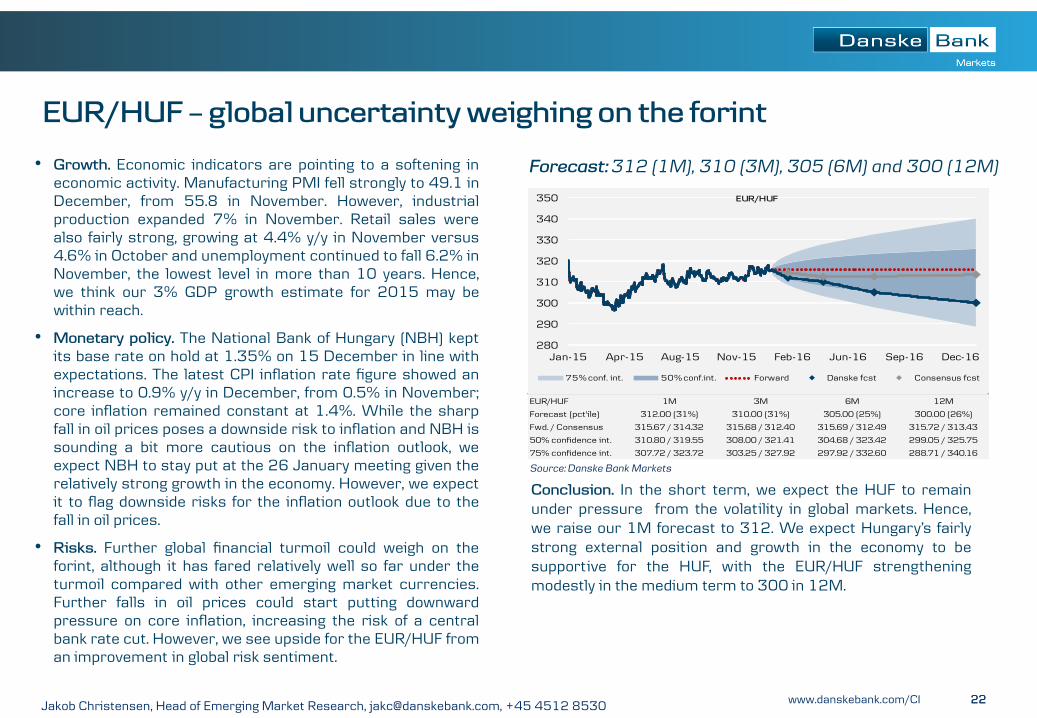

EUR/HUF – global uncertainty weighing on the forint

• Growth. Economic indicators are pointing to a softening in economic activity. Manufacturing PMI fell strongly to 49.1 in December, from 55.8 in November. However, industrial production expanded 7% in November. Retail sales were also fairly strong, growing at 4.4% y/y in November versus 4.6% in October and unemployment continued to fall 6.2% in November, the lowest level in more than 10 years. Hence, we think our 3% GDP growth estimate for 2015 may be within reach.

• Monetary policy. The National Bank of Hungary (NBH) kept its base rate on hold at 1.35% on 15 December in line with expectations. The latest CPI inflation rate figure showed an increase to 0.9% y/y in December, from 0.5% in November; core inflation remained constant at 1.4%. While the sharp fall in oil prices poses a downside risk to inflation and NBH is sounding a bit more cautious on the inflation outlook, we expect NBH to stay put at the 26 January meeting given the relatively strong growth in the economy. However, we expect it to flag downside risks for the inflation outlook due to the fall in oil prices.

• Risks. Further global financial turmoil could weigh on the forint, although it has fared relatively well so far under the turmoil compared with other emerging market currencies. Further falls in oil prices could start putting downward pressure on core inflation, increasing the risk of a central bank rate cut. However, we see upside for the EUR/HUF from an improvement in global risk sentiment.

22

Conclusion. In the short term, we expect the HUF to remain under pressure from the volatility in global markets. Hence, we raise our 1M forecast to 312. We expect Hungary’s fairly strong external position and growth in the economy to be supportive for the HUF, with the EUR/HUF strengthening modestly in the medium term to 300 in 12M.

Source: Danske Bank Markets

Jakob Christensen, Head of Emerging Market Research, [email protected], +45 4512 8530

EUR/HUF 1M 3M 6M 12M

Forecast (pct'ile) 312.00 (31%) 310.00 (31%) 305.00 (25%) 300.00 (26%)

Fwd. / Consensus 315.67 / 314.32 315.68 / 312.40 315.69 / 312.49 315.72 / 313.43

50% confidence int. 310.80 / 319.55 308.00 / 321.41 304.68 / 323.42 299.05 / 325.75

75% confidence int. 307.72 / 323.72 303.25 / 327.92 297.92 / 332.60 288.71 / 340.16

k

280

290

300

310

320

330

340

350

Jan-15 Apr-15 Aug-15 Nov-15 Feb-16 Jun-16 Sep-16 Dec-16

EUR/HUF

75% conf. int. 50% conf.int. Forward Danske fcst Consensus fcst

23 www.danskebank.com/CI

Forecast: 3.05 (1M), 3.10 (3M), 2.95 (6M) and 2.85 (12M)

USD/TRY – political uncertainty is back again

• Growth. Turkey's positive economic surprises continued as Q3 15 GDP expanded 4.0% y/y versus 3.8% y/y a quarter earlier, while consensus expected a slowdown to 2.7% y/y. Government expenditures rocketed during the election period supporting fixed investments. We raise our 2015 GDP forecast to 3.2% y/y from 2.8% y/y previously. We expect the growth to slowdown to 2.7% y/y in 2016 from 3.0% y/y previously.

• Monetary policy. Inflation accelerated to 8.8% y/y in December 2015, its 13-month highest, as the lira weakness moved into prices. The Turkish central bank kept its policy rate unchanged at 7.50% in December as we expected, while consensus expected a 50bp hike. As inflation has not eased and lira devaluation continues on high (geo)political woes and corporate sector FX debt vulnerability to the Fed’s tightening, monetary tightening is very likely, in our view.

• Valuation. A ‘fear premium’ has returned, in our view, due to renewed uncertainty on Turkey’s geopolitical prospects and the lira diverged from its fair value.

• Risks. Uncertainty around Turkey's cross-border military operations, increasing political risks and low appetite for EM assets could fuel a deterioration in sentiment. A rising oil price would put renewed pressure on the current account. Unexpected central bank rate hikes to curb inflation and support the lira would also be a risk.

23

Conclusion. While the election results stabilised the situation and improved sentiment in late 2015. the coin has been f lipped by recent (geo)political developments on fights against Kurds and increasing tension with Russia. We expect the lira to weaken on a 3M horizon as we expect political uncertainty and the Fed’s possible hikes to weigh on sentiment. However, we forecast a slight improvement in the TRY spot in the long run due to Turkey’s sustainable macro indicators, as low oil prices ease the pressure on the current account deficit.

Source: Danske Bank Markets

Vladimir Miklashevsky, Economist/Trading Desk Strategist, [email protected], +358 10 546 7522

USD/TRY 1M 3M 6M 12M

Forecast (pct'ile) 3.05 (50%) 3.10 (57%) 2.95 (27%) 2.85 (22%)

Fwd. / Consensus 3.07 / 3.04 3.12 / 3.06 3.20 / 3.09 3.36 / 3.10

50% confidence int. 2.97 / 3.13 2.95 / 3.21 2.94 / 3.31 2.90 / 3.48

75% confidence int. 2.93 / 3.21 2.87 / 3.36 2.80 / 3.53 2.50 / 3.82

k

2.00

2.50

3.00

3.50

4.00

Jan-15 Apr-15 Aug-15 Nov-15 Feb-16 Jun-16 Sep-16 Dec-16

USD/TRY

75% conf. int. 50% conf.int. Forward Danske fcst Consensus fcst

24 www.danskebank.com/CI

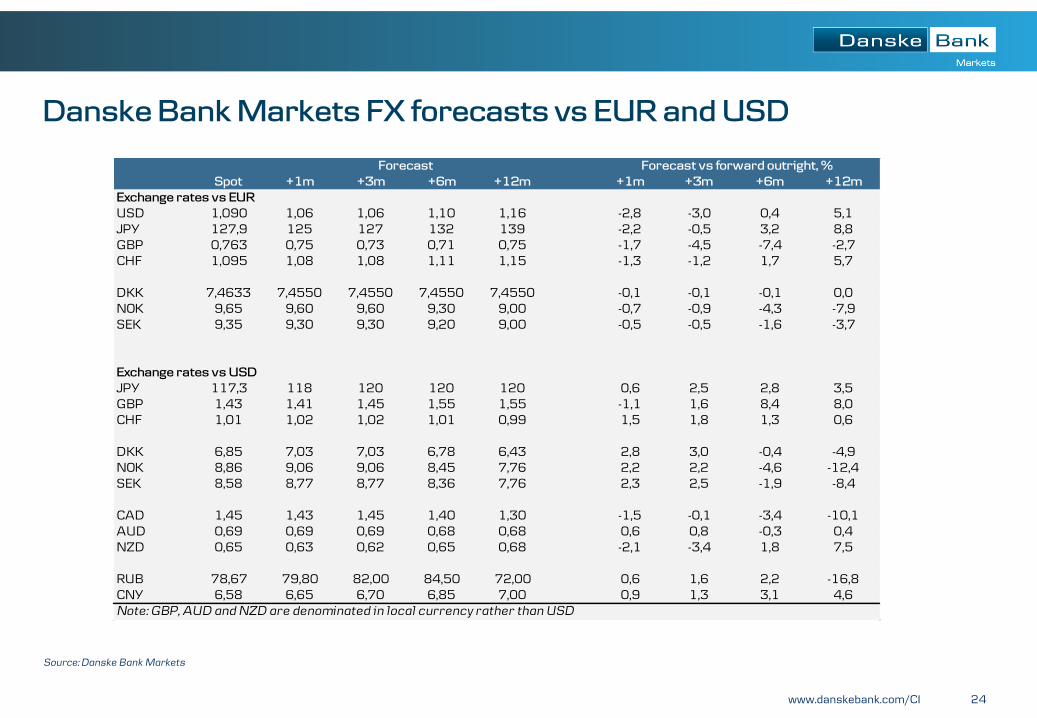

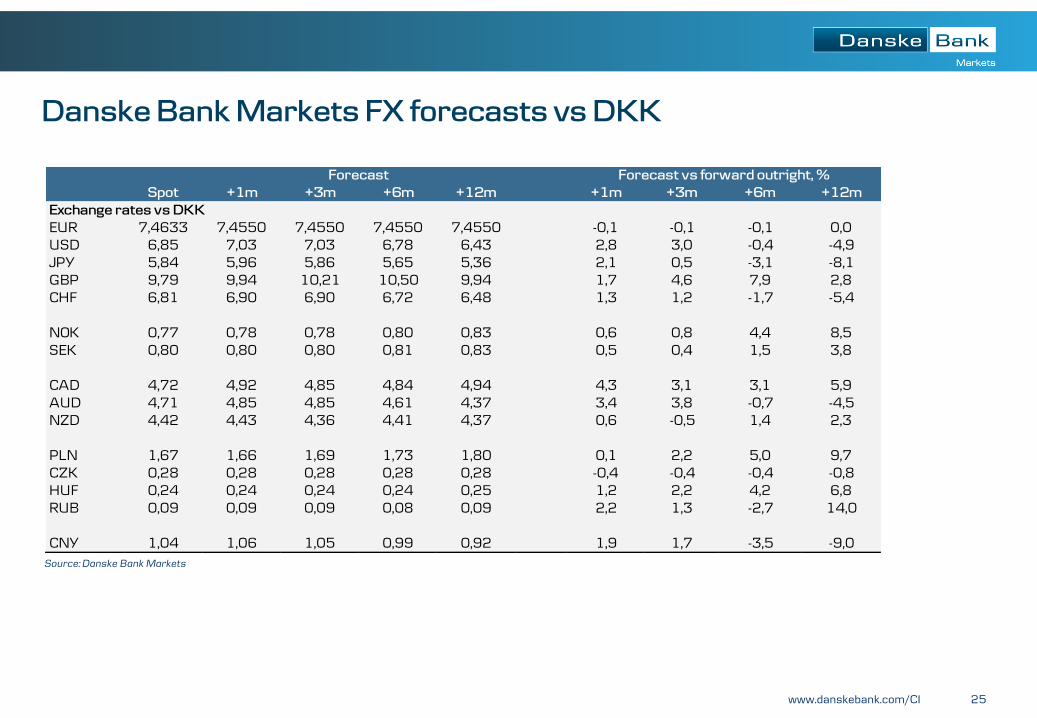

Danske Bank Markets FX forecasts vs EUR and USD

Source: Danske Bank Markets

Spot +1m +3m +6m +12m +1m +3m +6m +12m

Exchange rates vs EUR

USD 1,090 1,06 1,06 1,10 1,16 -2,8 -3,0 0,4 5,1JPY 127,9 125 127 132 139 -2,2 -0,5 3,2 8,8GBP 0,763 0,75 0,73 0,71 0,75 -1,7 -4,5 -7,4 -2,7CHF 1,095 1,08 1,08 1,11 1,15 -1,3 -1,2 1,7 5,7

DKK 7,4633 7,4550 7,4550 7,4550 7,4550 -0,1 -0,1 -0,1 0,0NOK 9,65 9,60 9,60 9,30 9,00 -0,7 -0,9 -4,3 -7,9SEK 9,35 9,30 9,30 9,20 9,00 -0,5 -0,5 -1,6 -3,7

Exchange rates vs USD

JPY 117,3 118 120 120 120 0,6 2,5 2,8 3,5GBP 1,43 1,41 1,45 1,55 1,55 -1,1 1,6 8,4 8,0CHF 1,01 1,02 1,02 1,01 0,99 1,5 1,8 1,3 0,6

DKK 6,85 7,03 7,03 6,78 6,43 2,8 3,0 -0,4 -4,9NOK 8,86 9,06 9,06 8,45 7,76 2,2 2,2 -4,6 -12,4SEK 8,58 8,77 8,77 8,36 7,76 2,3 2,5 -1,9 -8,4

CAD 1,45 1,43 1,45 1,40 1,30 -1,5 -0,1 -3,4 -10,1AUD 0,69 0,69 0,69 0,68 0,68 0,6 0,8 -0,3 0,4NZD 0,65 0,63 0,62 0,65 0,68 -2,1 -3,4 1,8 7,5

RUB 78,67 79,80 82,00 84,50 72,00 0,6 1,6 2,2 -16,8CNY 6,58 6,65 6,70 6,85 7,00 0,9 1,3 3,1 4,6Note: GBP, AUD and NZD are denominated in local currency rather than USD

Forecast Forecast vs forward outright, %

25 www.danskebank.com/CI

Danske Bank Markets FX forecasts vs DKK

Source: Danske Bank Markets

Spot +1m +3m +6m +12m +1m +3m +6m +12m

Exchange rates vs DKK

EUR 7,4633 7,4550 7,4550 7,4550 7,4550 -0,1 -0,1 -0,1 0,0USD 6,85 7,03 7,03 6,78 6,43 2,8 3,0 -0,4 -4,9JPY 5,84 5,96 5,86 5,65 5,36 2,1 0,5 -3,1 -8,1GBP 9,79 9,94 10,21 10,50 9,94 1,7 4,6 7,9 2,8CHF 6,81 6,90 6,90 6,72 6,48 1,3 1,2 -1,7 -5,4

NOK 0,77 0,78 0,78 0,80 0,83 0,6 0,8 4,4 8,5SEK 0,80 0,80 0,80 0,81 0,83 0,5 0,4 1,5 3,8

CAD 4,72 4,92 4,85 4,84 4,94 4,3 3,1 3,1 5,9AUD 4,71 4,85 4,85 4,61 4,37 3,4 3,8 -0,7 -4,5NZD 4,42 4,43 4,36 4,41 4,37 0,6 -0,5 1,4 2,3

PLN 1,67 1,66 1,69 1,73 1,80 0,1 2,2 5,0 9,7CZK 0,28 0,28 0,28 0,28 0,28 -0,4 -0,4 -0,4 -0,8HUF 0,24 0,24 0,24 0,24 0,25 1,2 2,2 4,2 6,8RUB 0,09 0,09 0,09 0,08 0,09 2,2 1,3 -2,7 14,0

CNY 1,04 1,06 1,05 0,99 0,92 1,9 1,7 -3,5 -9,0

Forecast Forecast vs forward outright, %

26 www.danskebank.com/CI

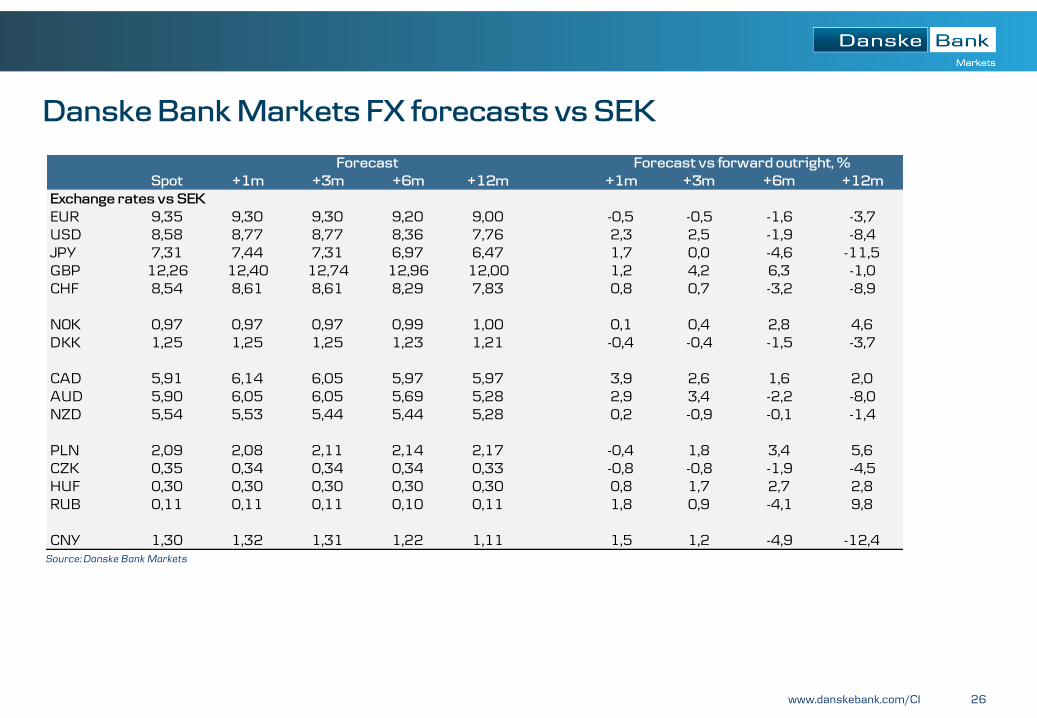

Danske Bank Markets FX forecasts vs SEK

Source: Danske Bank Markets

Spot +1m +3m +6m +12m +1m +3m +6m +12m

Exchange rates vs SEK

EUR 9,35 9,30 9,30 9,20 9,00 -0,5 -0,5 -1,6 -3,7USD 8,58 8,77 8,77 8,36 7,76 2,3 2,5 -1,9 -8,4JPY 7,31 7,44 7,31 6,97 6,47 1,7 0,0 -4,6 -11,5GBP 12,26 12,40 12,74 12,96 12,00 1,2 4,2 6,3 -1,0CHF 8,54 8,61 8,61 8,29 7,83 0,8 0,7 -3,2 -8,9

NOK 0,97 0,97 0,97 0,99 1,00 0,1 0,4 2,8 4,6DKK 1,25 1,25 1,25 1,23 1,21 -0,4 -0,4 -1,5 -3,7

CAD 5,91 6,14 6,05 5,97 5,97 3,9 2,6 1,6 2,0AUD 5,90 6,05 6,05 5,69 5,28 2,9 3,4 -2,2 -8,0NZD 5,54 5,53 5,44 5,44 5,28 0,2 -0,9 -0,1 -1,4

PLN 2,09 2,08 2,11 2,14 2,17 -0,4 1,8 3,4 5,6CZK 0,35 0,34 0,34 0,34 0,33 -0,8 -0,8 -1,9 -4,5HUF 0,30 0,30 0,30 0,30 0,30 0,8 1,7 2,7 2,8RUB 0,11 0,11 0,11 0,10 0,11 1,8 0,9 -4,1 9,8

CNY 1,30 1,32 1,31 1,22 1,11 1,5 1,2 -4,9 -12,4

Forecast Forecast vs forward outright, %

27 www.danskebank.com/CI

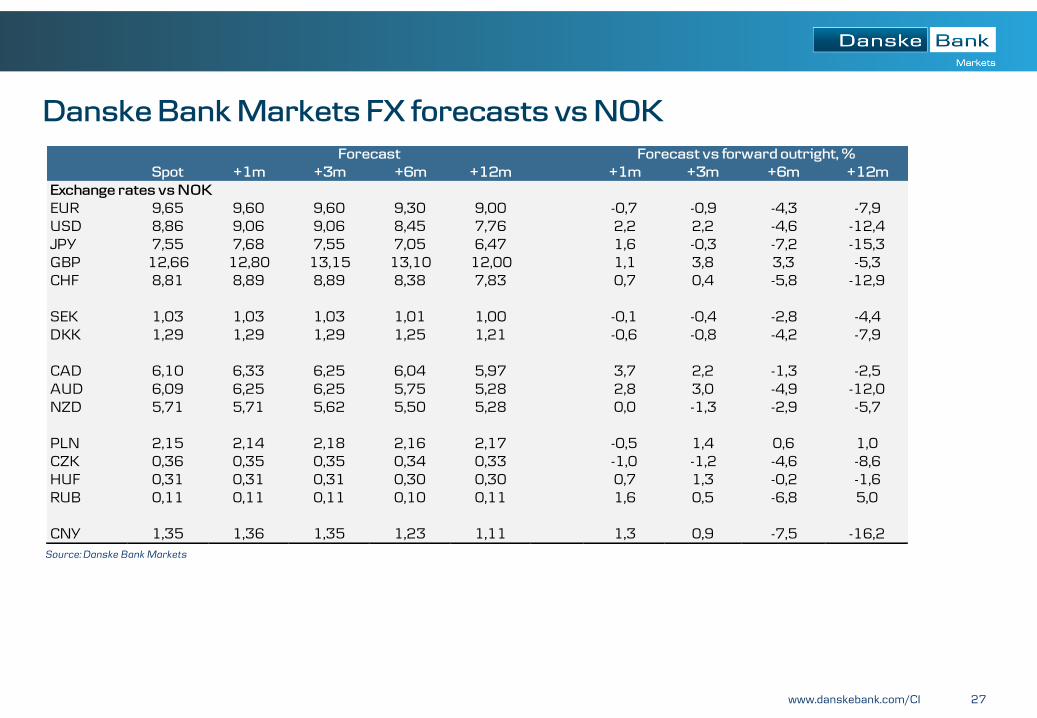

Danske Bank Markets FX forecasts vs NOK

Source: Danske Bank Markets

Spot +1m +3m +6m +12m +1m +3m +6m +12m

Exchange rates vs NOK

EUR 9,65 9,60 9,60 9,30 9,00 -0,7 -0,9 -4,3 -7,9USD 8,86 9,06 9,06 8,45 7,76 2,2 2,2 -4,6 -12,4JPY 7,55 7,68 7,55 7,05 6,47 1,6 -0,3 -7,2 -15,3GBP 12,66 12,80 13,15 13,10 12,00 1,1 3,8 3,3 -5,3CHF 8,81 8,89 8,89 8,38 7,83 0,7 0,4 -5,8 -12,9

SEK 1,03 1,03 1,03 1,01 1,00 -0,1 -0,4 -2,8 -4,4DKK 1,29 1,29 1,29 1,25 1,21 -0,6 -0,8 -4,2 -7,9

CAD 6,10 6,33 6,25 6,04 5,97 3,7 2,2 -1,3 -2,5AUD 6,09 6,25 6,25 5,75 5,28 2,8 3,0 -4,9 -12,0NZD 5,71 5,71 5,62 5,50 5,28 0,0 -1,3 -2,9 -5,7

PLN 2,15 2,14 2,18 2,16 2,17 -0,5 1,4 0,6 1,0CZK 0,36 0,35 0,35 0,34 0,33 -1,0 -1,2 -4,6 -8,6HUF 0,31 0,31 0,31 0,30 0,30 0,7 1,3 -0,2 -1,6RUB 0,11 0,11 0,11 0,10 0,11 1,6 0,5 -6,8 5,0

CNY 1,35 1,36 1,35 1,23 1,11 1,3 0,9 -7,5 -16,2

Forecast Forecast vs forward outright, %

28 www.danskebank.com/CI

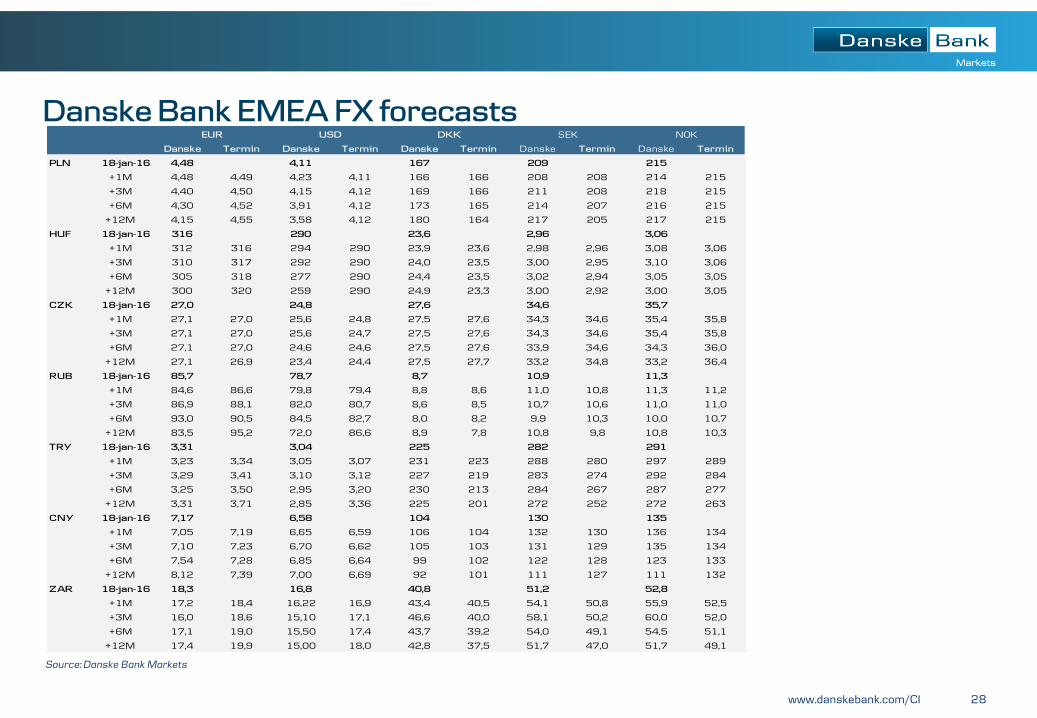

Danske Bank EMEA FX forecasts

Source: Danske Bank Markets

Danske Termin Danske Termin Danske Termin Danske Termin Danske Termin

PLN 18-jan-16 4,48 4,11 167 209 215

+1M 4,48 4,49 4,23 4,11 166 166 208 208 214 215

+3M 4,40 4,50 4,15 4,12 169 166 211 208 218 215

+6M 4,30 4,52 3,91 4,12 173 165 214 207 216 215

+12M 4,15 4,55 3,58 4,12 180 164 217 205 217 215

HUF 18-jan-16 316 290 23,6 2,96 3,06

+1M 312 316 294 290 23,9 23,6 2,98 2,96 3,08 3,06

+3M 310 317 292 290 24,0 23,5 3,00 2,95 3,10 3,06

+6M 305 318 277 290 24,4 23,5 3,02 2,94 3,05 3,05

+12M 300 320 259 290 24,9 23,3 3,00 2,92 3,00 3,05

CZK 18-jan-16 27,0 24,8 27,6 34,6 35,7

+1M 27,1 27,0 25,6 24,8 27,5 27,6 34,3 34,6 35,4 35,8

+3M 27,1 27,0 25,6 24,7 27,5 27,6 34,3 34,6 35,4 35,8

+6M 27,1 27,0 24,6 24,6 27,5 27,6 33,9 34,6 34,3 36,0

+12M 27,1 26,9 23,4 24,4 27,5 27,7 33,2 34,8 33,2 36,4

RUB 18-jan-16 85,7 78,7 8,7 10,9 11,3

+1M 84,6 86,6 79,8 79,4 8,8 8,6 11,0 10,8 11,3 11,2

+3M 86,9 88,1 82,0 80,7 8,6 8,5 10,7 10,6 11,0 11,0

+6M 93,0 90,5 84,5 82,7 8,0 8,2 9,9 10,3 10,0 10,7

+12M 83,5 95,2 72,0 86,6 8,9 7,8 10,8 9,8 10,8 10,3

TRY 18-jan-16 3,31 3,04 225 282 291

+1M 3,23 3,34 3,05 3,07 231 223 288 280 297 289

+3M 3,29 3,41 3,10 3,12 227 219 283 274 292 284

+6M 3,25 3,50 2,95 3,20 230 213 284 267 287 277

+12M 3,31 3,71 2,85 3,36 225 201 272 252 272 263

CNY 18-jan-16 7,17 6,58 104 130 135

+1M 7,05 7,19 6,65 6,59 106 104 132 130 136 134

+3M 7,10 7,23 6,70 6,62 105 103 131 129 135 134

+6M 7,54 7,28 6,85 6,64 99 102 122 128 123 133

+12M 8,12 7,39 7,00 6,69 92 101 111 127 111 132

ZAR 18-jan-16 18,3 16,8 40,8 51,2 52,8

+1M 17,2 18,4 16,22 16,9 43,4 40,5 54,1 50,8 55,9 52,5

+3M 16,0 18,6 15,10 17,1 46,6 40,0 58,1 50,2 60,0 52,0

+6M 17,1 19,0 15,50 17,4 43,7 39,2 54,0 49,1 54,5 51,1

+12M 17,4 19,9 15,00 18,0 42,8 37,5 51,7 47,0 51,7 49,1

NOKEUR USD DKK SEK

29 www.danskebank.com/CI

Disclosures

This research report has been prepared by Danske Bank Markets, a division of Danske Bank A/S (‘Danske Bank’). The authors of this research report are Thomas Harr (Global Head of FICC Research), Stefan Mellin (Senior Analyst), Jens Naervig Pedersen (Senior Analyst), Kristoffer Lomholt (Analyst), Allan von Mehren (Chief Analyst), Morten Helt (Senior Analyst), Christin Tuxen (Senior Analyst), Vladimir Miklashevsky (Analyst) and Jakob Ekholdt Christensen (Chief Analyst).

Analyst certification

Each research analyst responsible for the content of this research report certifies that the views expressed in the research report accurately reflect the research analyst’s personal view about the financial instruments and issuers covered by the research report. Each responsible research analyst further certifies that no part of the compensation of the research analyst was, is or will be, directly or indirectly, related to the specific recommendations expressed in the research report.

Regulation

Danske Bank is authorised and subject to regulation by the Danish Financial Supervisory Authority and is subject to the rules and regulation of the relevant regulators in all other jurisdictions where it conducts business. Danske Bank is subject to limited regulation by the Financial Conduct Authority and the Prudential Regulation Authority (UK). Details on the extent of the regulation by the Financial Conduct Authority and the Prudential Regulation Authority are available from Danske Bank on request.

The research reports of Danske Bank are prepared in accordance with the Danish Society of Financial Analysts’ rules of ethics and the recommendations of the Danish Securities Dealers Association.

Conflicts of interest

Danske Bank has established procedures to prevent conflicts of interest and to ensure the provision of high-quality research based on research objectivity and independence. These procedures are documented in Danske Bank’s research policies. Employees within Danske Bank’s Research Departments have been instructed that any request that might impair the objectivity and independence of research shall be referred to Research Management and the Compliance Department. Danske Bank’s Research Departments are organised independently from and do not report to other business areas within Danske Bank.

Research analysts are remunerated in part based on the overall profitability of Danske Bank, which includes investment banking revenues, but do not receive bonuses or other remuneration linked to specific corporate finance or debt capital transactions.

Financial models and/or methodology used in this research report

Calculations and presentations in this research report are based on standard econometric tools and methodology as well as publicly available statistics for each individual security, issuer and/or country. Documentation can be obtained from the authors on request.

Risk warning

Major risks connected with recommendations or opinions in this research report, including as sensitivity analysis of relevant assumptions, are stated throughout the text.

Date of first publication

See the front page of this research report for the date of first publication.

30 www.danskebank.com/CI

General disclaimer This research has been prepared by Danske Bank Markets (a division of Danske Bank A/S). It is provided for informational purposes only. It does not constitute or form part of, and shall under no circumstances be considered as, an offer to sell or a solicitation of an offer to purchase or sell any relevant financial instruments (i.e. financial instruments mentioned herein or other financial instruments of any issuer mentioned herein and/or options, warrants, rights or other interests with respect to any such financial instruments) (‘Relevant Financial Instruments’).

The research report has been prepared independently and solely on the basis of publicly available information that Danske Bank considers to be reliable. While reasonable care has been taken to ensure that its contents are not untrue or misleading, no representation is made as to its accuracy or completeness and Danske Bank, its affiliates and subsidiaries accept no liability whatsoever for any direct or consequential loss, including without limitation any loss of profits, arising from reliance on this research report.

The opinions expressed herein are the opinions of the research analysts responsible for the research report and reflect their judgement as of the date hereof. These opinions are subject to change, and Danske Bank does not undertake to notify any recipient of this research report of any such change nor of any other changes related to the information provided in this research report.

This research report is not intended for retail customers in the United Kingdom or the United States.

This research report is protected by copyright and is intended solely for the designated addressee. It may not be reproduced or distributed, in whole or in part, by any recipient for any purpose without Danske Bank’s prior written consent.

Disclaimer related to distribution in the United States This research report is distributed in the United States by Danske Markets Inc., a U.S. registered broker-dealer and subsidiary of Danske Bank, pursuant to SEC Rule 15a-6 and related interpretations issued by the U.S. Securities and Exchange Commission. The research report is intended for distribution in the United States solely to ‘U.S. institutional investors’ as defined in SEC Rule 15a-6. Danske Markets Inc. accepts responsibility for this research report in connection with distribution in the United States solely to ‘U.S. institutional investors’.

Danske Bank is not subject to U.S. rules with regard to the preparation of research reports and the independence of research analysts. In addition, the research analysts of Danske Bank who have prepared this research report are not registered or qualified as research analysts with the NYSE or FINRA but satisfy the applicable requirements of a non-U.S. jurisdiction.

Any U.S. investor recipient of this research report who wishes to purchase or sell any Relevant Financial Instrument may do so only by contacting Danske Markets Inc. directly and should be aware that investing in non-U.S. financial instruments may entail certain risks. Financial instruments of non-U.S. issuers may not be registered with the U.S. Securities and Exchange Commission and may not be subject to the reporting and auditing standards of the U.S. Securities and Exchange Commission.