Embed Size (px)

Citation preview

Futures and Options on Foreign Exchange

Chapter 7 (165-179)

Lecture Objectives

Futures Contracts: Preliminaries

Currency Futures Markets

Basic Currency Futures Relationships

Options Contracts: Preliminaries

Currency Options Markets

Currency Futures Options

Basic Option Pricing Relationships at Expiry

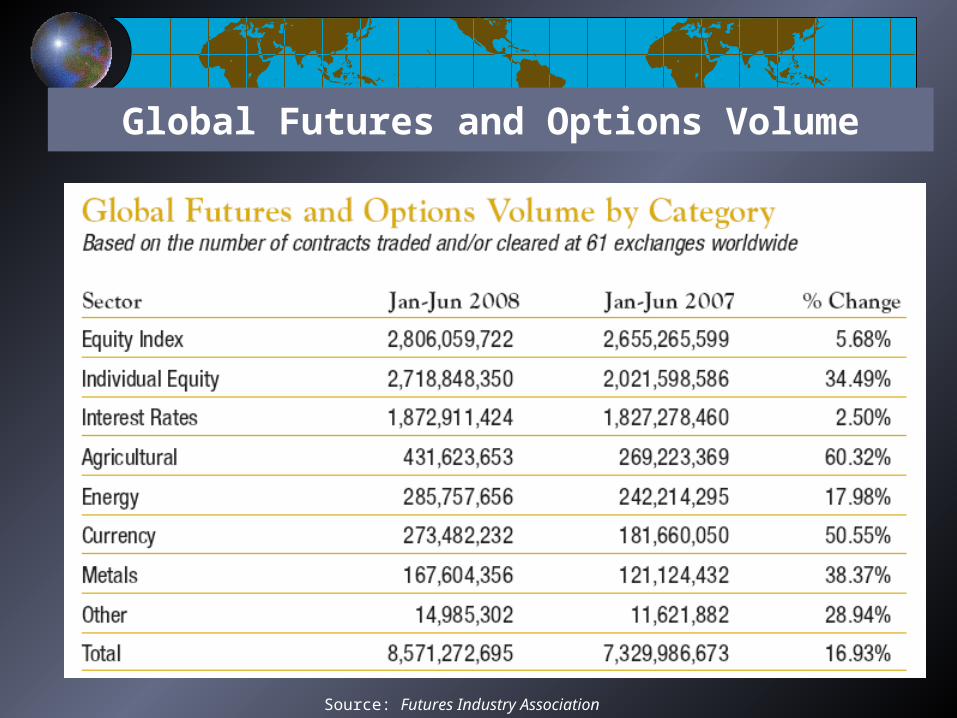

Global Futures and Options Volume

Source: Futures Industry Association

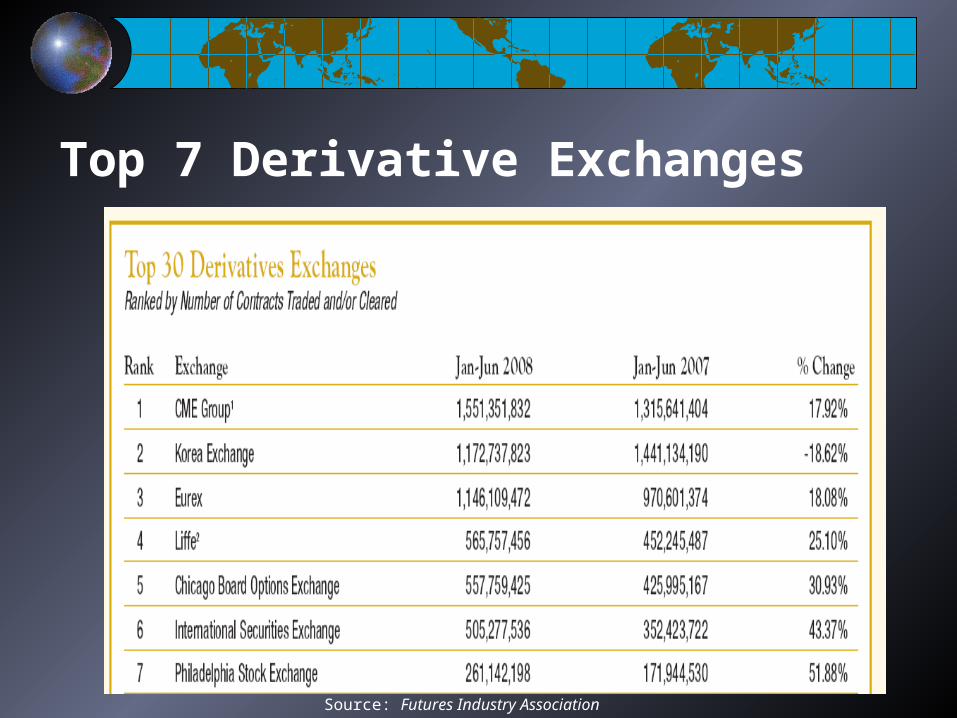

Top 7 Derivative Exchanges

Source: Futures Industry Association

Top 5 Most Actively Traded Contracts Worldwide

Source: Futures Industry Association

Survey of Derivative Usage

From the Wharton School derivative surveySurvey of 350 US firms (ended 1998)

Firms were selected randomly, grouped by size into large capitalization (capitalization greater than 250 million), medium capitalization (between 50 and 250 million), and small (less than 50 million)

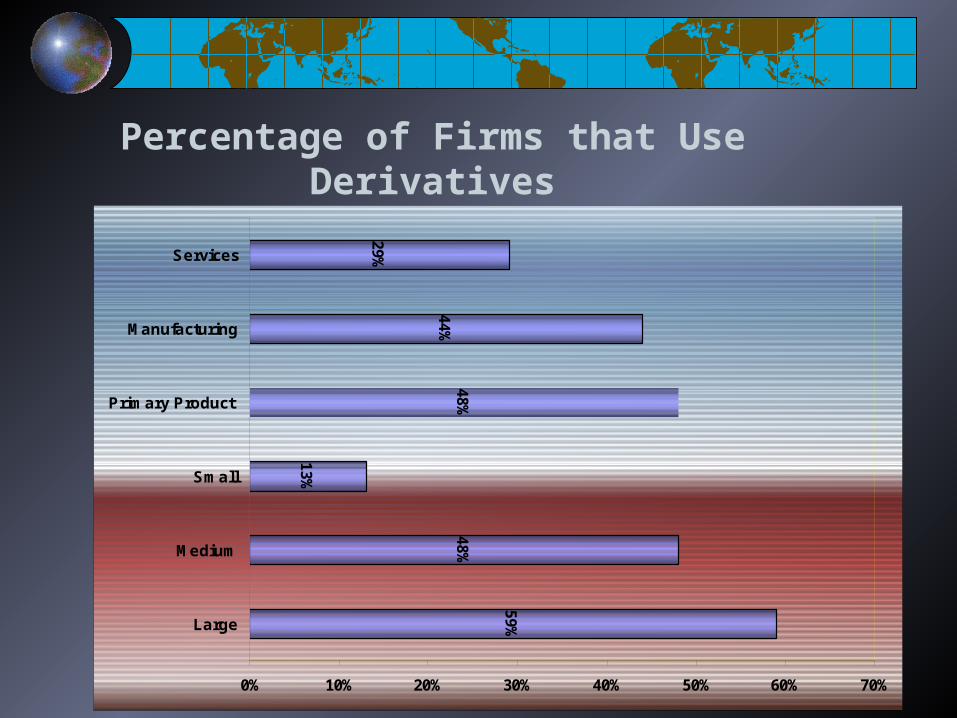

Percentage of Firms that Use Derivatives

59%

48%

13%

48%44%

29%

0% 10% 20% 30% 40% 50% 60% 70%

Large

Medium

Small

Primary Product

Manufacturing

Services

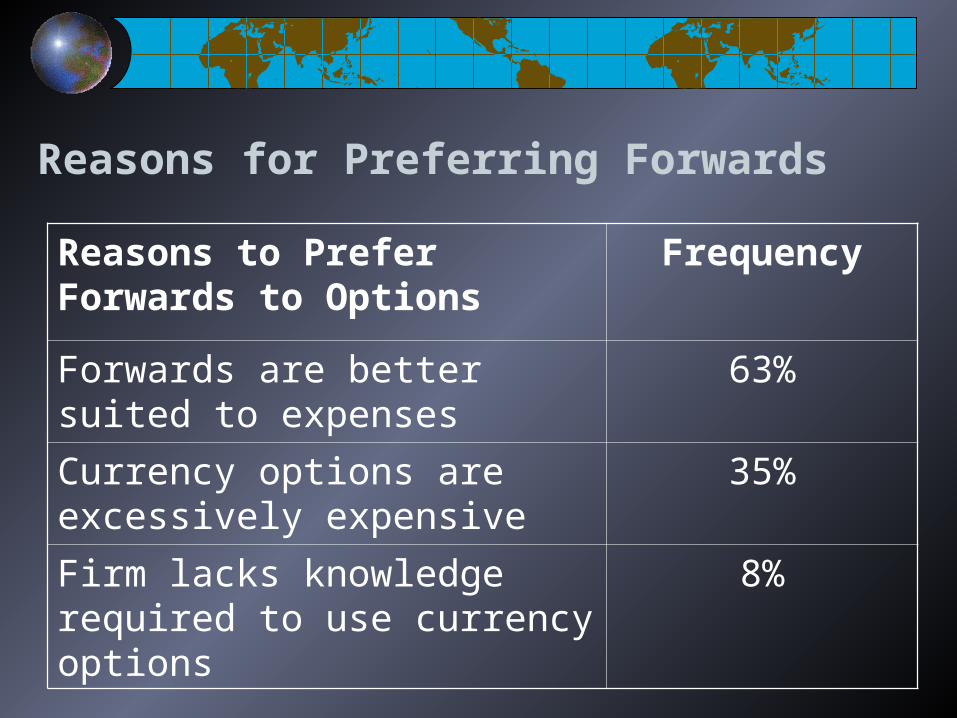

Reasons for Preferring Forwards

Reasons to Prefer Forwards to Options

Frequency

Forwards are better suited to expenses

63%

Currency options are excessively expensive

35%

Firm lacks knowledge required to use currency options

8%

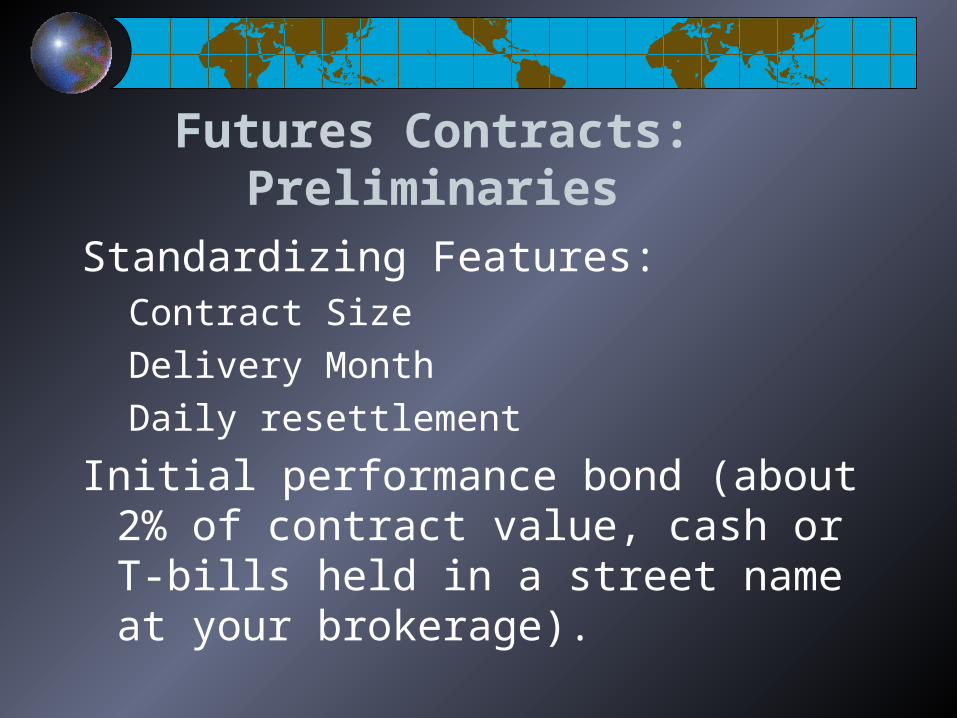

Futures Contracts: PreliminariesA futures contract is like a forward contract:

It specifies that a certain currency will be exchanged for another at a specified time in the future at prices specified today.

A futures contract is different from a forward contract:Futures are standardized contracts trading on organized

exchanges with daily resettlement through a clearinghouse.

http://www.pbs.org/itvs/openoutcry/thepit.html

http://www.youtube.com/watch?v=VwfCwG1-y60&NR=1

Futures Contracts: Preliminaries

Standardizing Features:Contract Size

Delivery Month

Daily resettlement

Initial performance bond (about 2% of contract value, cash or T-bills held in a street name at your brokerage).

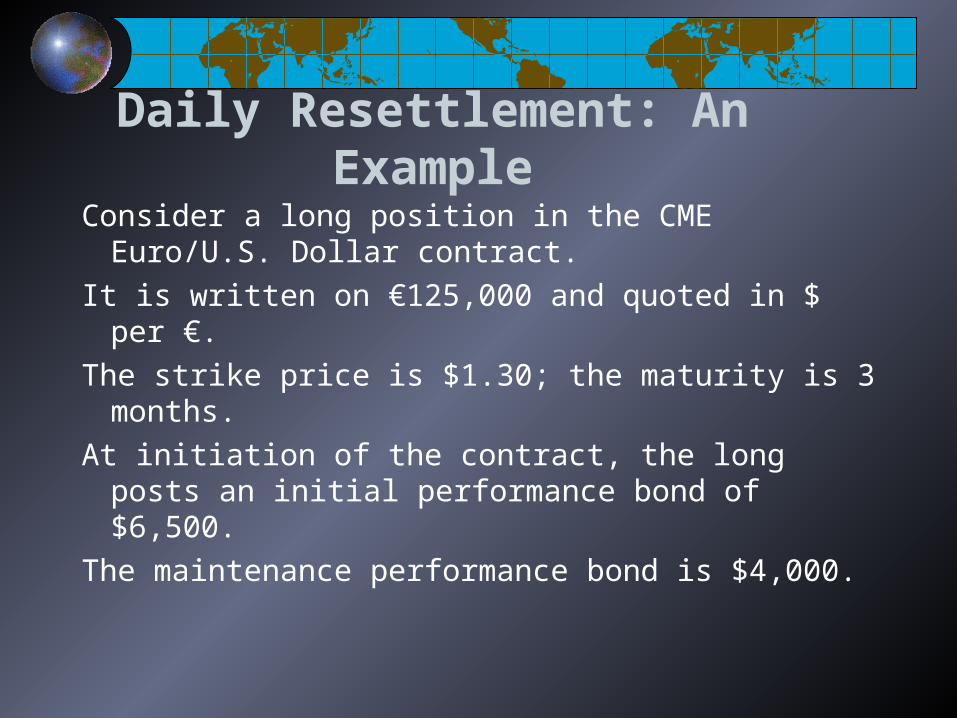

Daily Resettlement: An Example

Consider a long position in the CME Euro/U.S. Dollar contract.

It is written on €125,000 and quoted in $ per €.

The strike price is $1.30; the maturity is 3 months.

At initiation of the contract, the long posts an initial performance bond of $6,500.

The maintenance performance bond is $4,000.

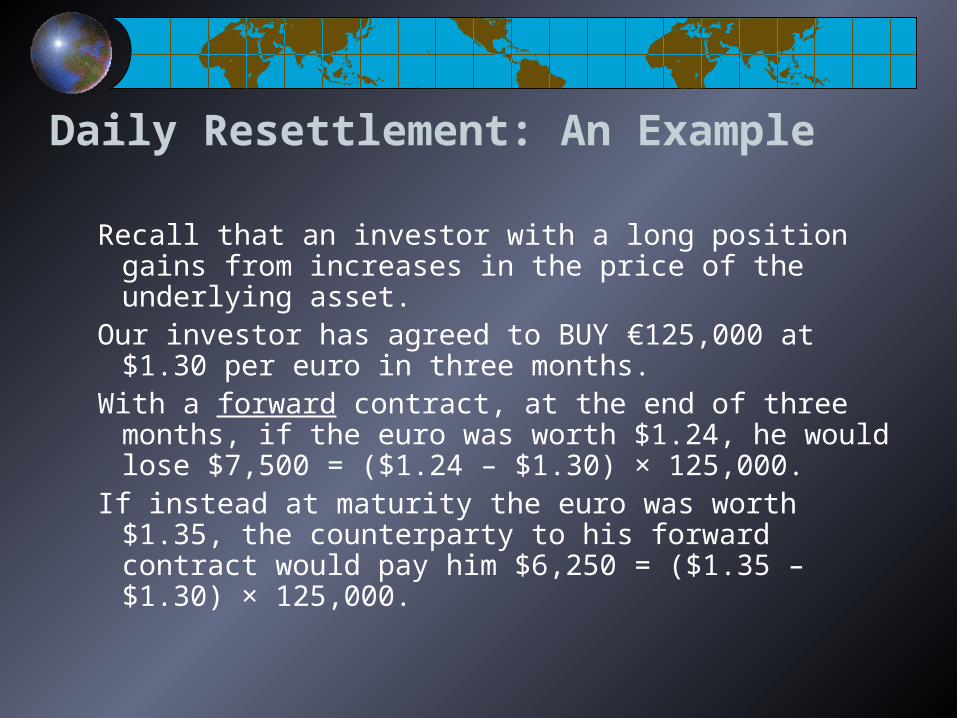

Daily Resettlement: An Example

Recall that an investor with a long position gains from increases in the price of the underlying asset.

Our investor has agreed to BUY €125,000 at $1.30 per euro in three months.

With a forward contract, at the end of three months, if the euro was worth $1.24, he would lose $7,500 = ($1.24 – $1.30) × 125,000.

If instead at maturity the euro was worth $1.35, the counterparty to his forward contract would pay him $6,250 = ($1.35 – $1.30) × 125,000.

Daily Resettlement: An Example

With futures, we have daily resettlement of gains and losses rather than one big settlement at maturity.

Every trading day:

if the price goes down, the long pays the short

if the price goes up, the short pays the long

Performance Bond Money

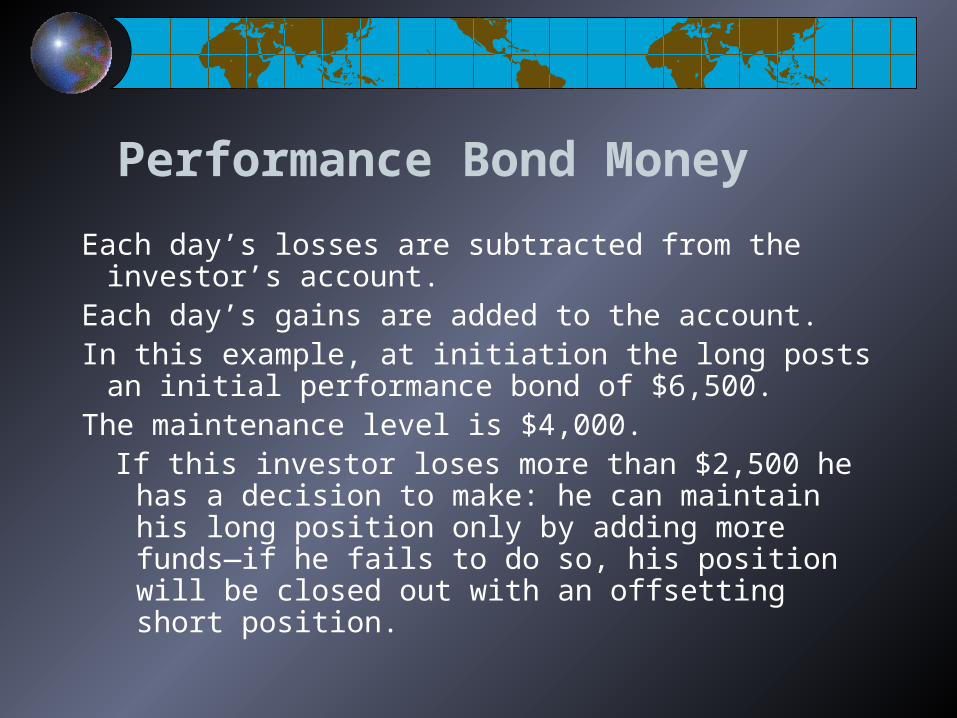

Each day’s losses are subtracted from the investor’s account.

Each day’s gains are added to the account.In this example, at initiation the long posts an initial

performance bond of $6,500.The maintenance level is $4,000.

If this investor loses more than $2,500 he has a decision to make: he can maintain his long position only by adding more funds—if he fails to do so, his position will be closed out with an offsetting short position.

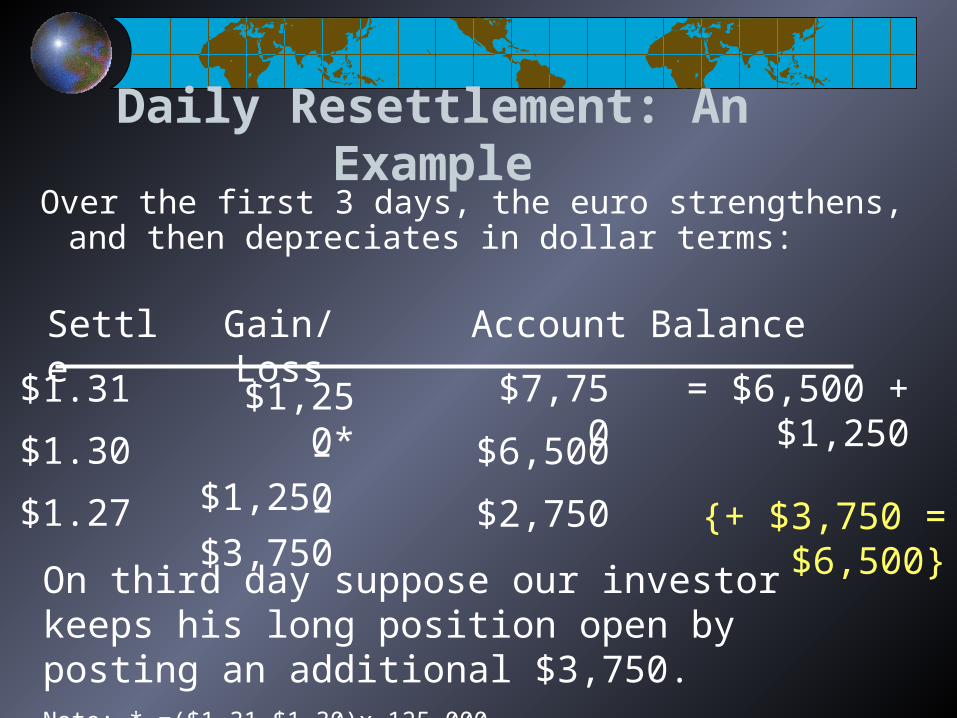

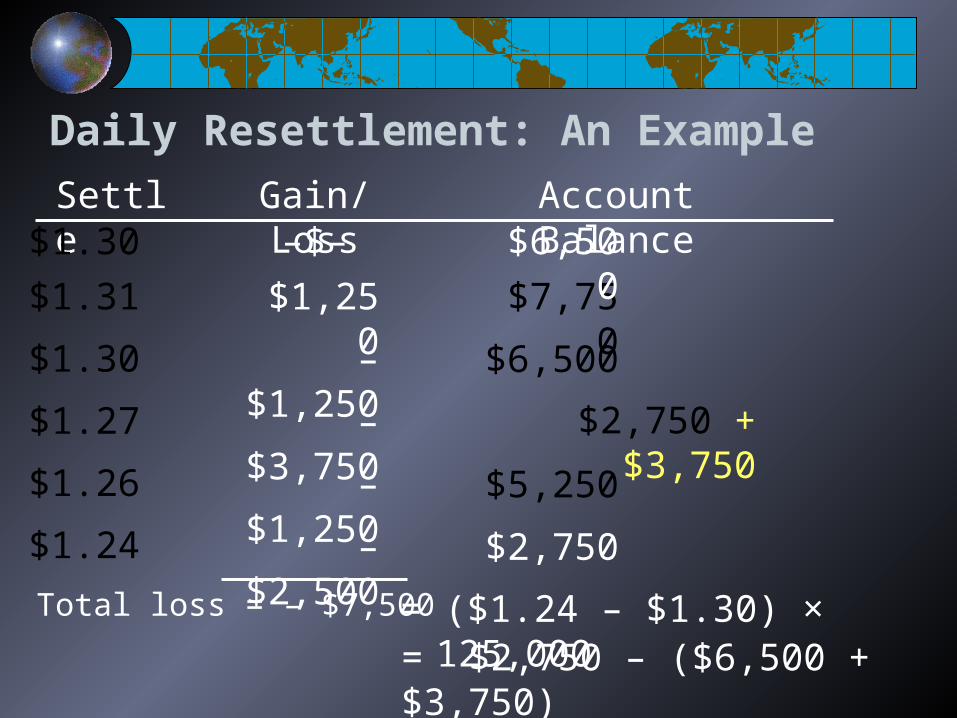

Daily Resettlement: An ExampleOver the first 3 days, the euro strengthens, and then

depreciates in dollar terms:

$1,250*

–$1,250

$1.31

$1.30

$1.27 –$3,750

Gain/LossSettle

$7,750

$6,500

$2,750

Account Balance

= $6,500 + $1,250

On third day suppose our investor keeps his long position open by posting an additional $3,750.Note: * =($1.31-$1.30)x 125,000

{+ $3,750 = $6,500}

Daily Resettlement: An Example

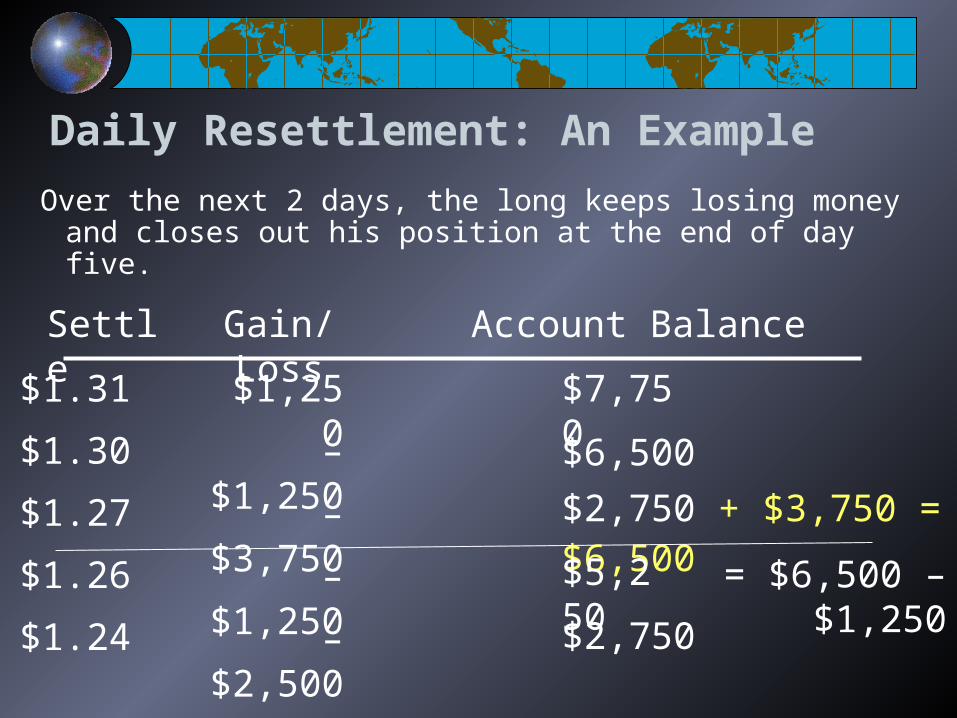

Over the next 2 days, the long keeps losing money and closes out his position at the end of day five.

$1,250

–$1,250

$1.31

$1.30

$1.27

$1.26

$1.24

–$3,750

–$1,250

–$2,500

Gain/LossSettle

$7,750

$6,500

$2,750 + $3,750 = $6,500 $5,250

$2,750

Account Balance

= $6,500 – $1,250

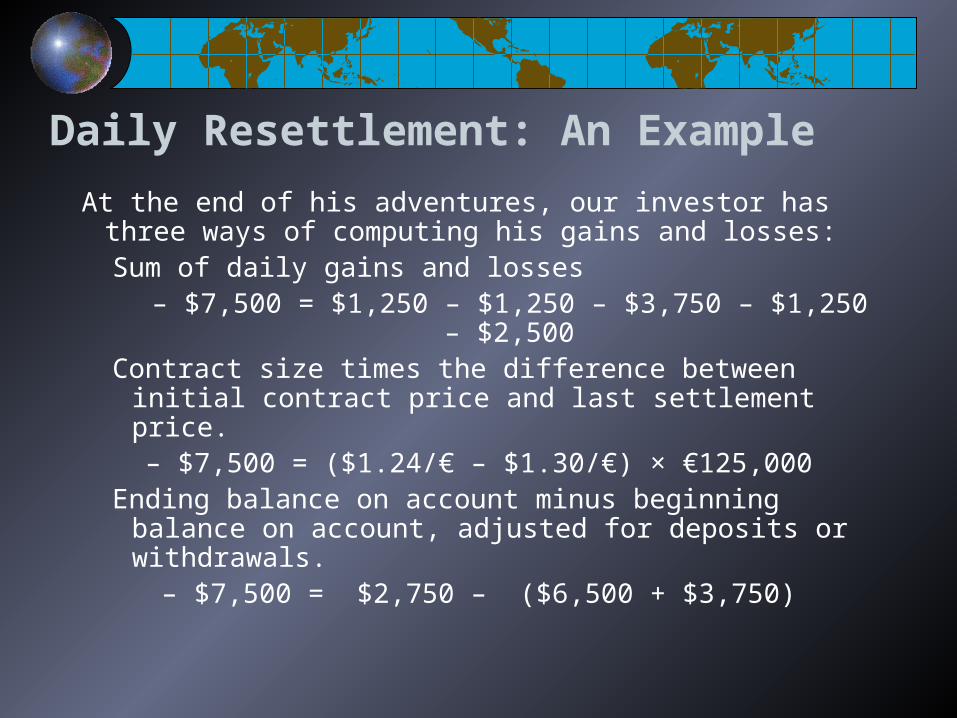

Daily Resettlement: An Example

At the end of his adventures, our investor has three ways of computing his gains and losses:Sum of daily gains and losses

– $7,500 = $1,250 – $1,250 – $3,750 – $1,250 – $2,500

Contract size times the difference between initial contract price and last settlement price.

– $7,500 = ($1.24/€ – $1.30/€) × €125,000Ending balance on account minus beginning balance on

account, adjusted for deposits or withdrawals.– $7,500 = $2,750 – ($6,500 + $3,750)

Daily Resettlement: An Example

Total loss = – $7,500

$1,250

–$1,250

$1.31

$1.30

$1.27

$1.26

$1.24

–$3,750

–$1,250

–$2,500

Gain/LossSettle

$7,750

$6,500

$2,750 + $3,750

$5,250

$2,750

Account Balance

= $2,750 – ($6,500 + $3,750)

–$–$1.30 $6,500

= ($1.24 – $1.30) × 125,000

Currency Futures Markets

The Chicago Mercantile Exchange (CME) is by far the largest.

Others include:The Philadelphia Board of Trade (PBOT)

The Tokyo International Financial Futures Exchange

The London International Financial Futures Exchange

Singapore International Monetary Exchange (SIMEX)

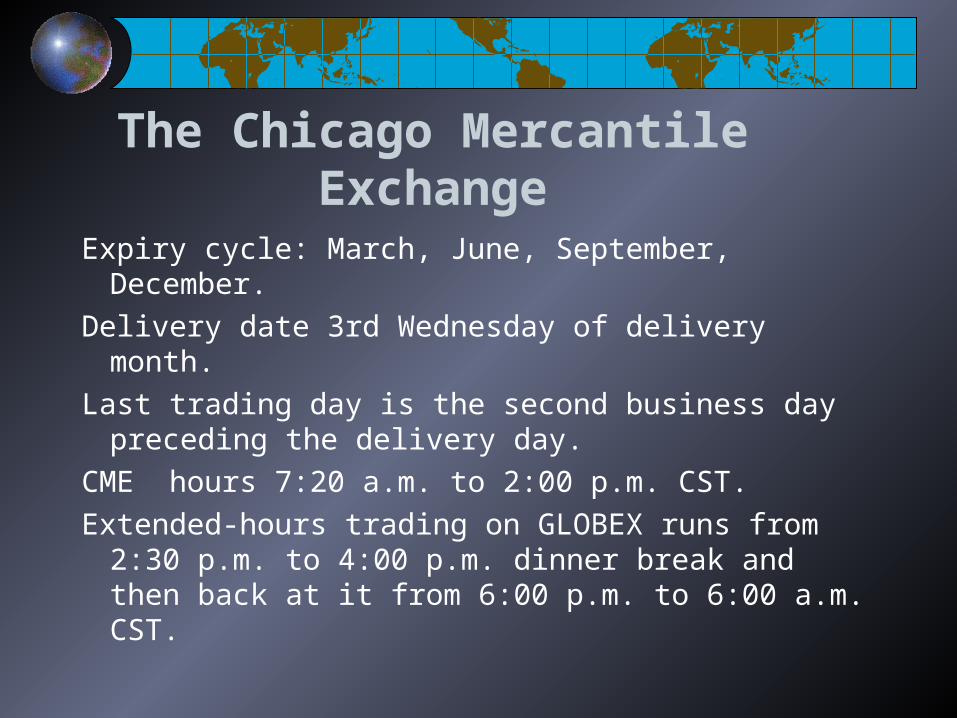

The Chicago Mercantile Exchange

Expiry cycle: March, June, September, December.

Delivery date 3rd Wednesday of delivery month.

Last trading day is the second business day preceding the delivery day.

CME hours 7:20 a.m. to 2:00 p.m. CST.

Extended-hours trading on GLOBEX runs from 2:30 p.m. to 4:00 p.m. dinner break and then back at it from 6:00 p.m. to 6:00 a.m. CST.

Basic Currency Futures Relationships

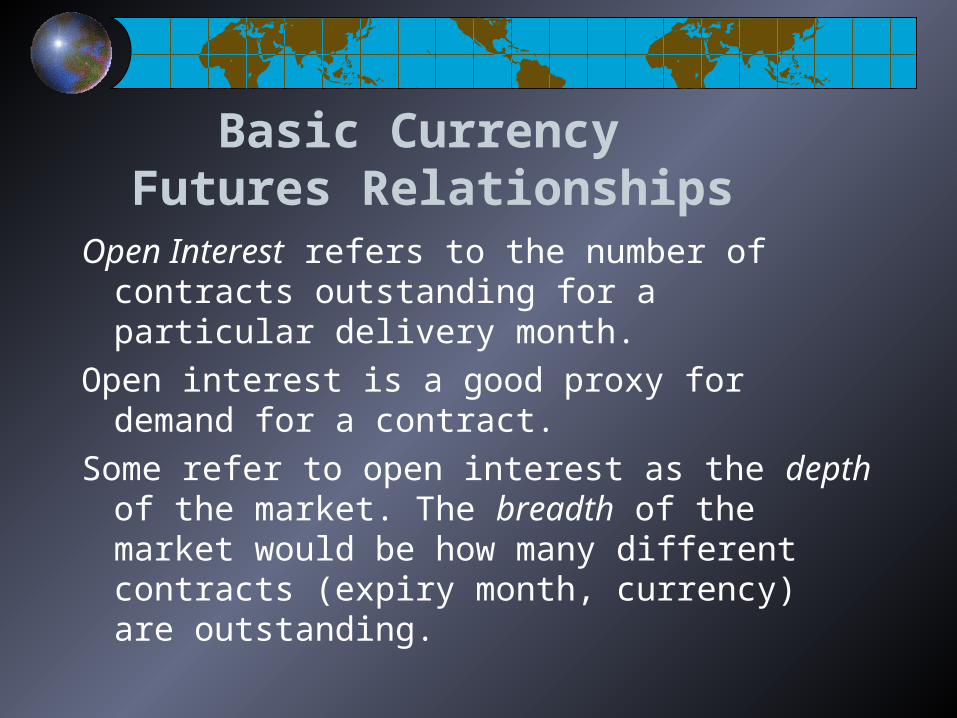

Open Interest refers to the number of contracts outstanding for a particular delivery month.

Open interest is a good proxy for demand for a contract.

Some refer to open interest as the depth of the market. The breadth of the market would be how many different contracts (expiry month, currency) are outstanding.

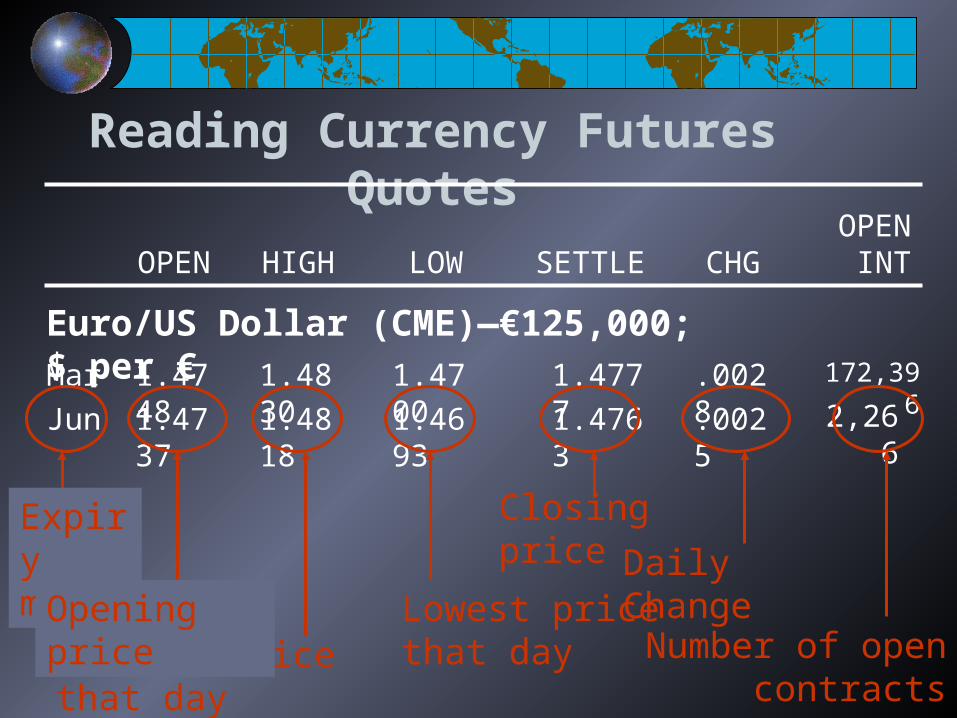

Reading Currency Futures Quotes

OPEN HIGH LOW SETTLE CHGOPEN

INT

Euro/US Dollar (CME)—€125,000; $ per €

1.4748 1.4830 1.4700 1.4777 .0028Mar 172,396

1.4737 1.4818 1.4693 1.4763 .0025Jun 2,266

Highest price that dayLowest price that day

Closing price Daily Change

Number of open contracts

Expiry month

Opening price

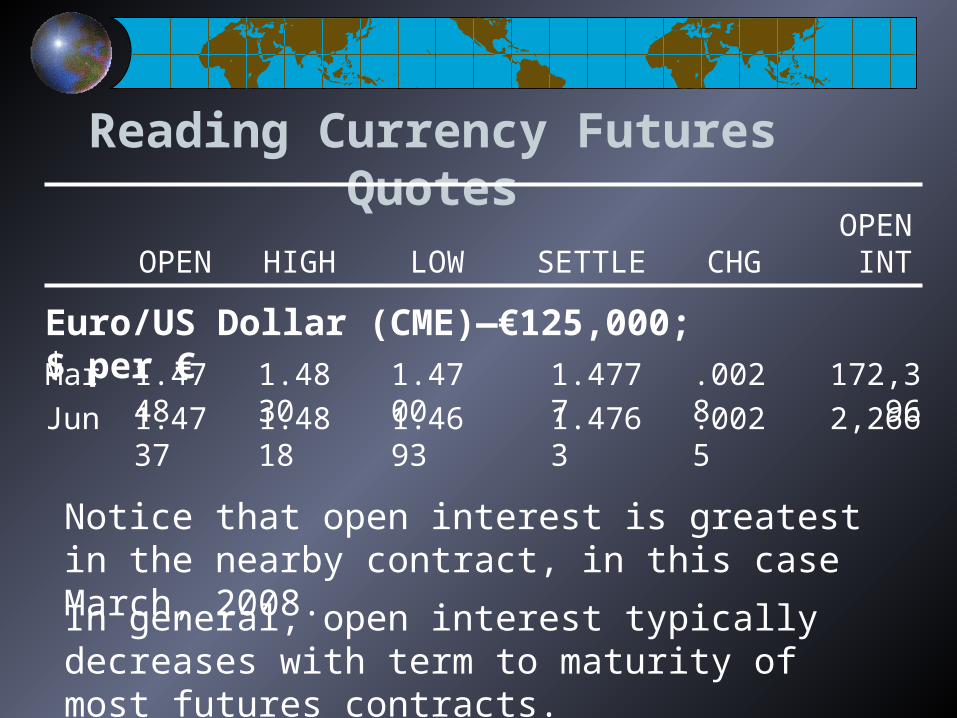

Reading Currency Futures Quotes

Notice that open interest is greatest in the nearby contract, in this case March, 2008.

In general, open interest typically decreases with term to maturity of most futures contracts.

OPEN HIGH LOW SETTLE CHGOPEN

INT

Euro/US Dollar (CME)—€125,000; $ per €

1.4748 1.4830 1.4700 1.4777 .0028Mar 172,396

1.4737 1.4818 1.4693 1.4763 .0025Jun 2,266

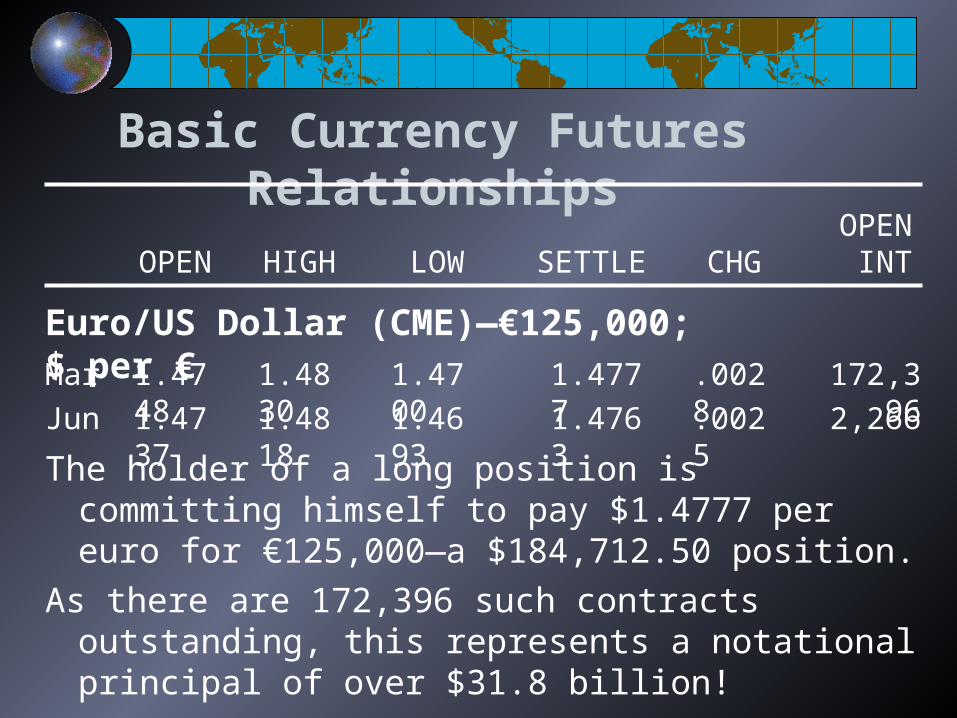

Basic Currency Futures Relationships

The holder of a long position is committing himself to pay $1.4777 per euro for €125,000—a $184,712.50 position.

As there are 172,396 such contracts outstanding, this represents a notational principal of over $31.8 billion!

OPEN HIGH LOW SETTLE CHGOPEN

INT

Euro/US Dollar (CME)—€125,000; $ per €

1.4748 1.4830 1.4700 1.4777 .0028Mar 172,396

1.4737 1.4818 1.4693 1.4763 .0025Jun 2,266

Options Contracts: Preliminaries

An option gives the holder the right, but not the obligation, to buy or sell a given quantity of an asset in the future, at prices agreed upon today.

Calls vs. PutsCall options gives the holder the right, but not the

obligation, to buy a given quantity of some asset at some time in the future, at prices agreed upon today.

Put options gives the holder the right, but not the obligation, to sell a given quantity of some asset at some time in the future, at prices agreed upon today.

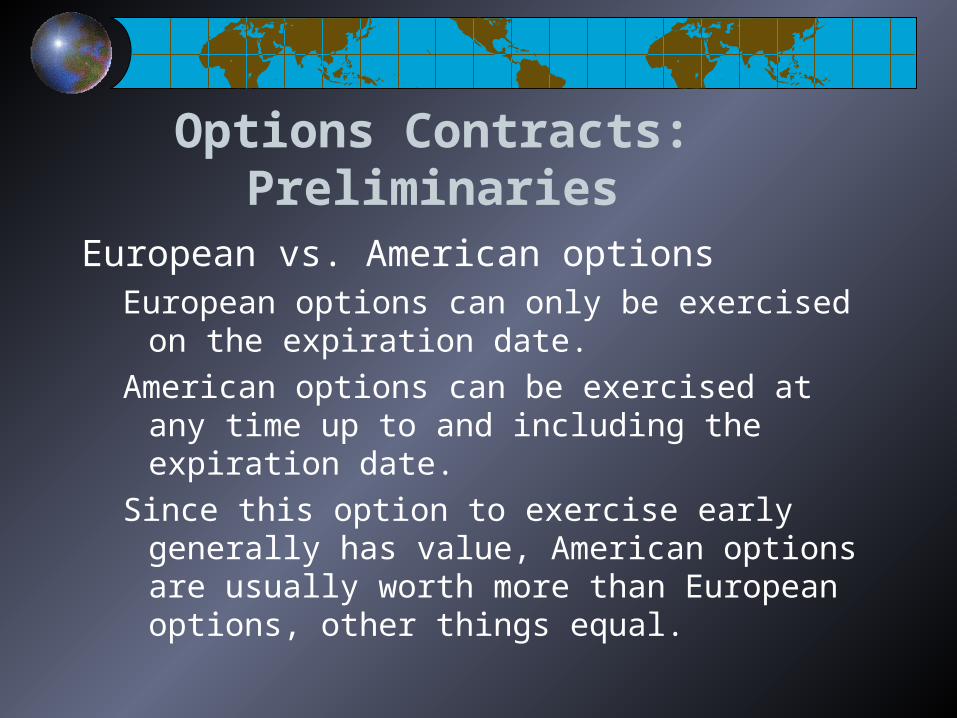

Options Contracts: Preliminaries

European vs. American optionsEuropean options can only be exercised on the

expiration date.

American options can be exercised at any time up to and including the expiration date.

Since this option to exercise early generally has value, American options are usually worth more than European options, other things equal.

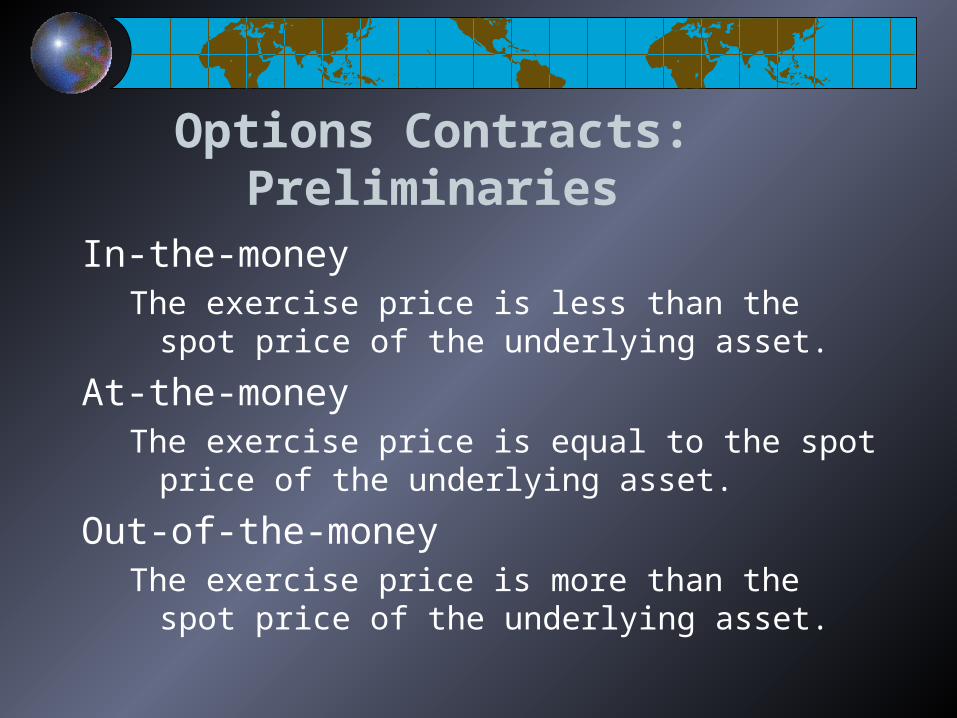

Options Contracts: Preliminaries

In-the-moneyThe exercise price is less than the spot price of the

underlying asset.

At-the-moneyThe exercise price is equal to the spot price of the

underlying asset.

Out-of-the-moneyThe exercise price is more than the spot price of the

underlying asset.

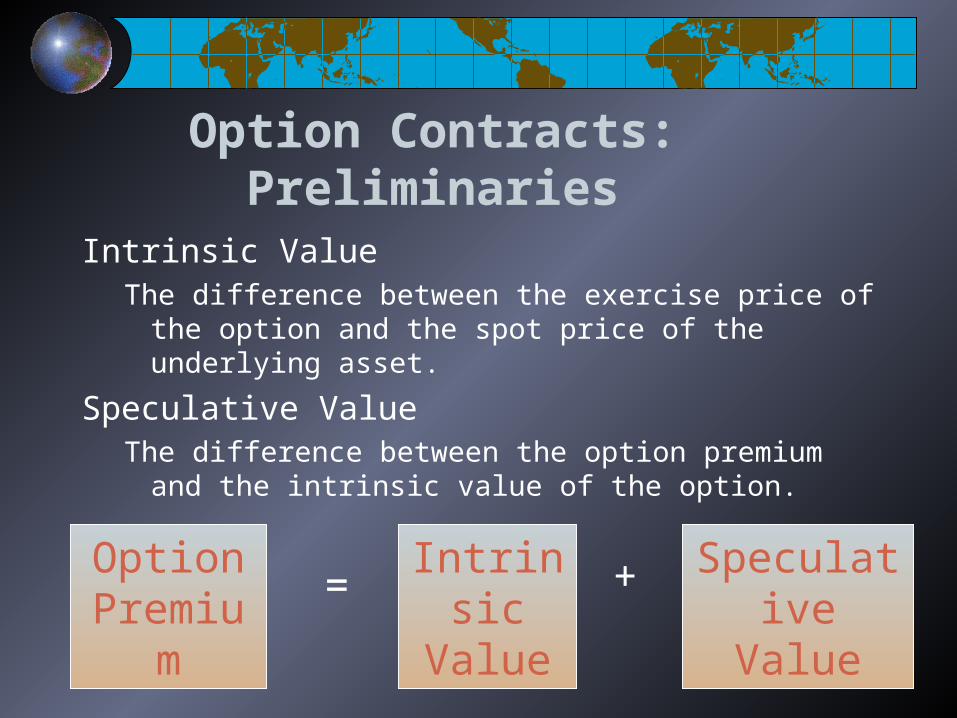

Option Contracts: Preliminaries

Intrinsic ValueThe difference between the exercise price of the option

and the spot price of the underlying asset.

Speculative ValueThe difference between the option premium and the

intrinsic value of the option.

Option Premium =

Intrinsic Value

Speculative Value

+

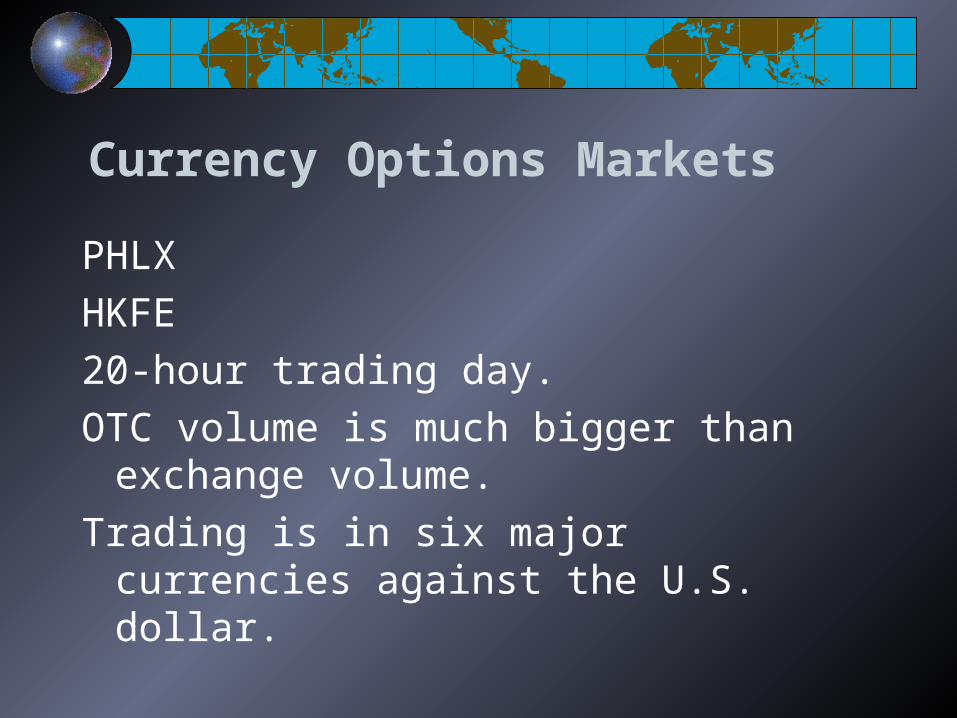

Currency Options Markets

PHLX

HKFE

20-hour trading day.

OTC volume is much bigger than exchange volume.

Trading is in six major currencies against the U.S. dollar.

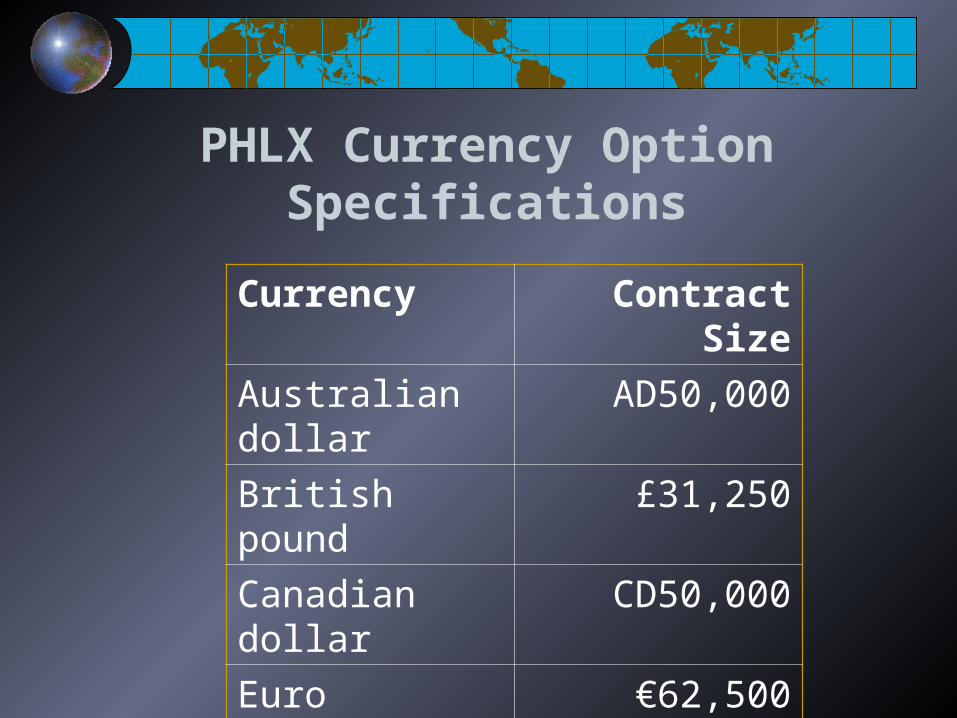

PHLX Currency Option Specifications

Currency Contract Size

Australian dollar AD50,000

British pound £31,250

Canadian dollar CD50,000

Euro €62,500

Japanese yen ¥6,250,000

Swiss franc SF62,500

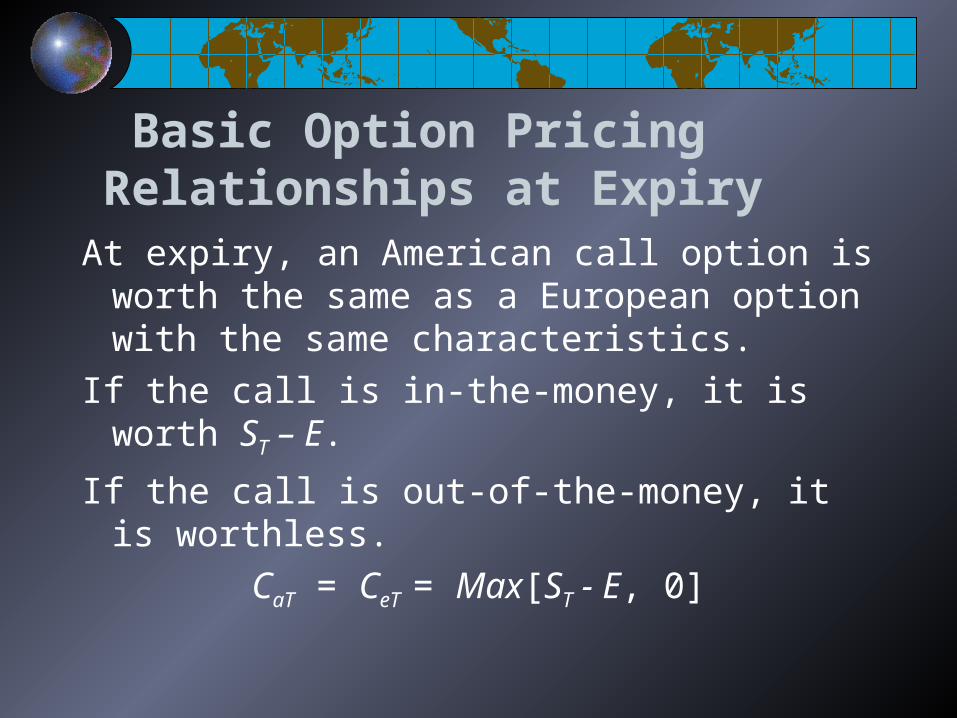

Basic Option Pricing Relationships at Expiry

At expiry, an American call option is worth the same as a European option with the same characteristics.

If the call is in-the-money, it is worth ST – E.

If the call is out-of-the-money, it is worthless.

CaT = CeT = Max[ST - E, 0]

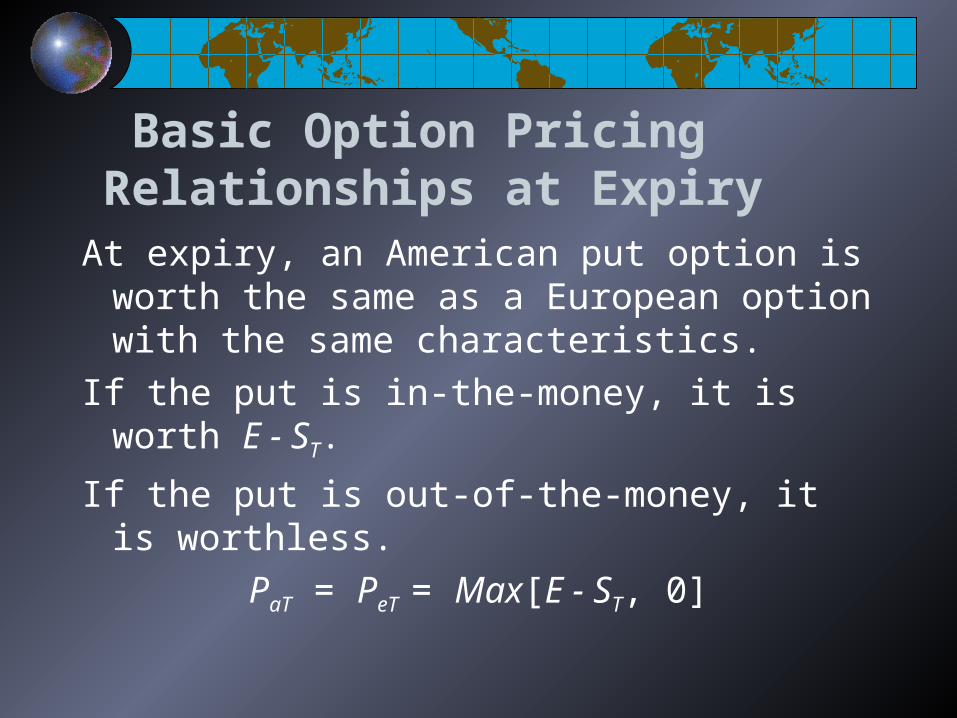

Basic Option Pricing Relationships at Expiry

At expiry, an American put option is worth the same as a European option with the same characteristics.

If the put is in-the-money, it is worth E - ST.

If the put is out-of-the-money, it is worthless.

PaT = PeT = Max[E - ST, 0]

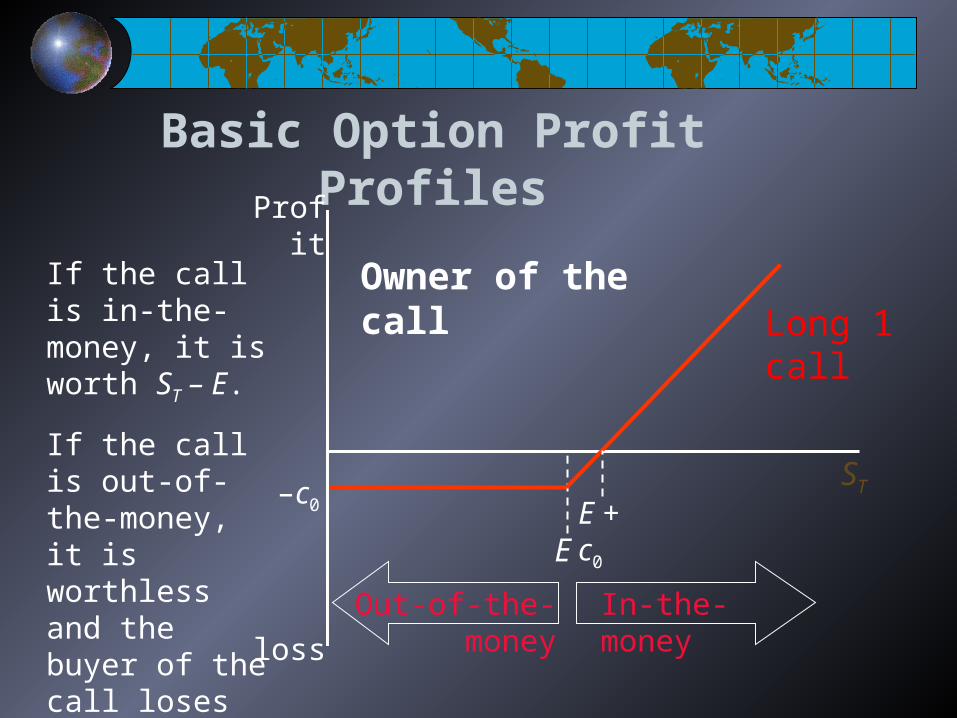

Basic Option Profit Profiles

E

ST

Profit

loss

–c0 E + c0

Long 1 call

If the call is in-the-money, it is worth ST – E.

If the call is out-of-the-money, it is worthless and the buyer of the call loses his entire investment of c0. In-the-moneyOut-of-the-money

Owner of the call

Basic Option Profit Profiles

E

ST

Profit

loss

c0

E + c0

short 1 call

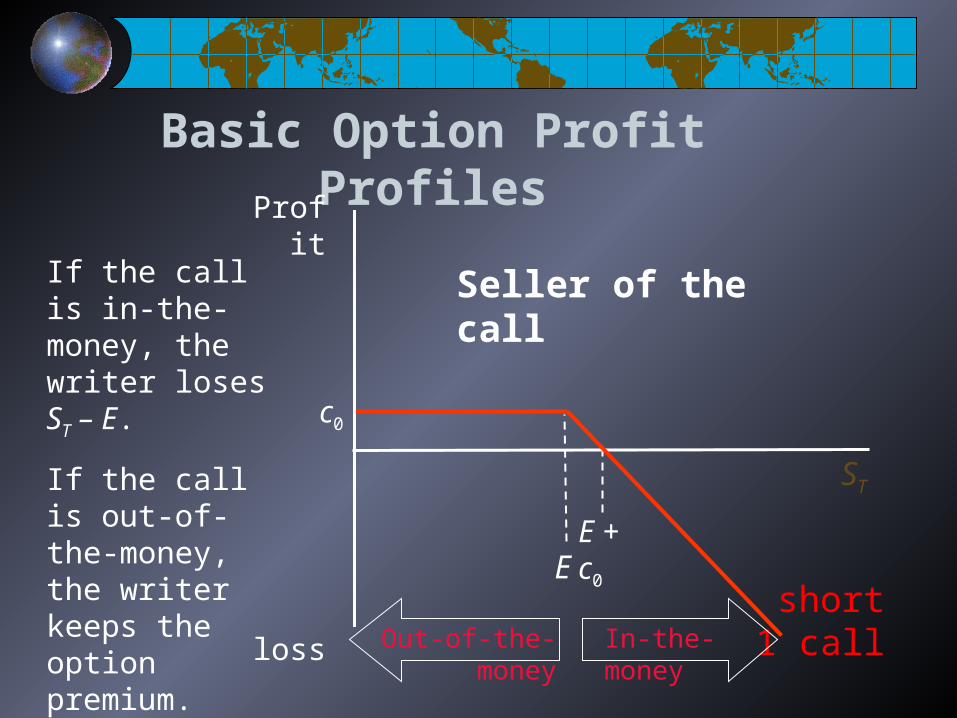

If the call is in-the-money, the writer loses ST – E.

If the call is out-of-the-money, the writer keeps the option premium.

In-the-moneyOut-of-the-money

Seller of the call

Basic Option Profit Profiles

E

ST

Profit

loss

– p0

E – p0long 1 put

E – p0

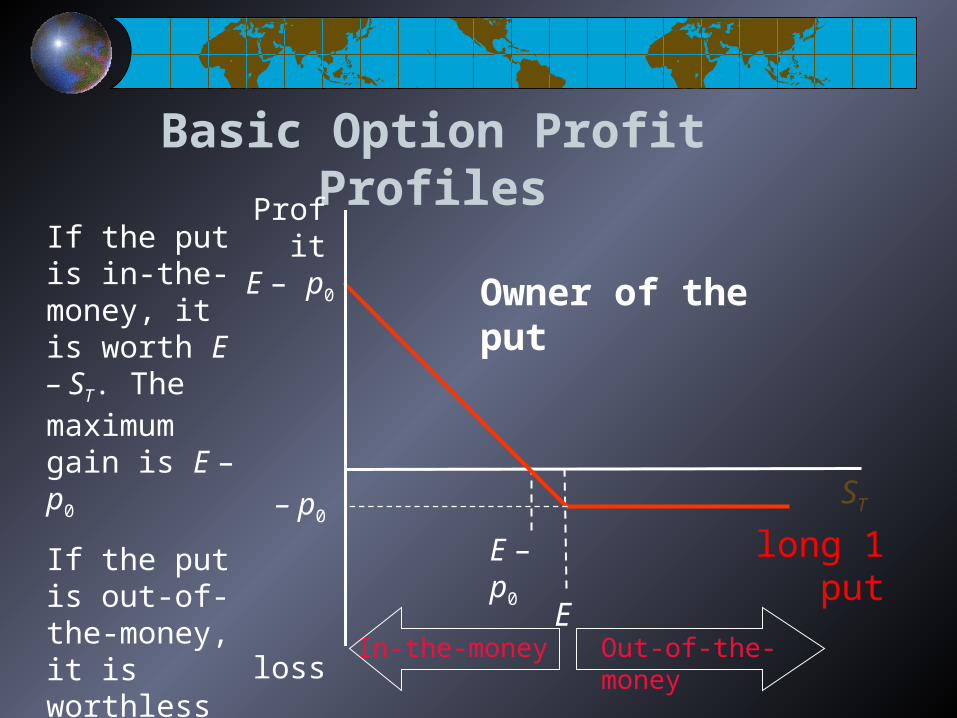

If the put is in-the-money, it is worth E – ST. The maximum gain is E – p0

If the put is out-of-the-money, it is worthless and the buyer of the put loses his entire investment of p0.

Out-of-the-moneyIn-the-money

Owner of the put

Basic Option Profit Profiles

E

ST

Profit

loss

p0

E – p0short 1 put

– E + p0

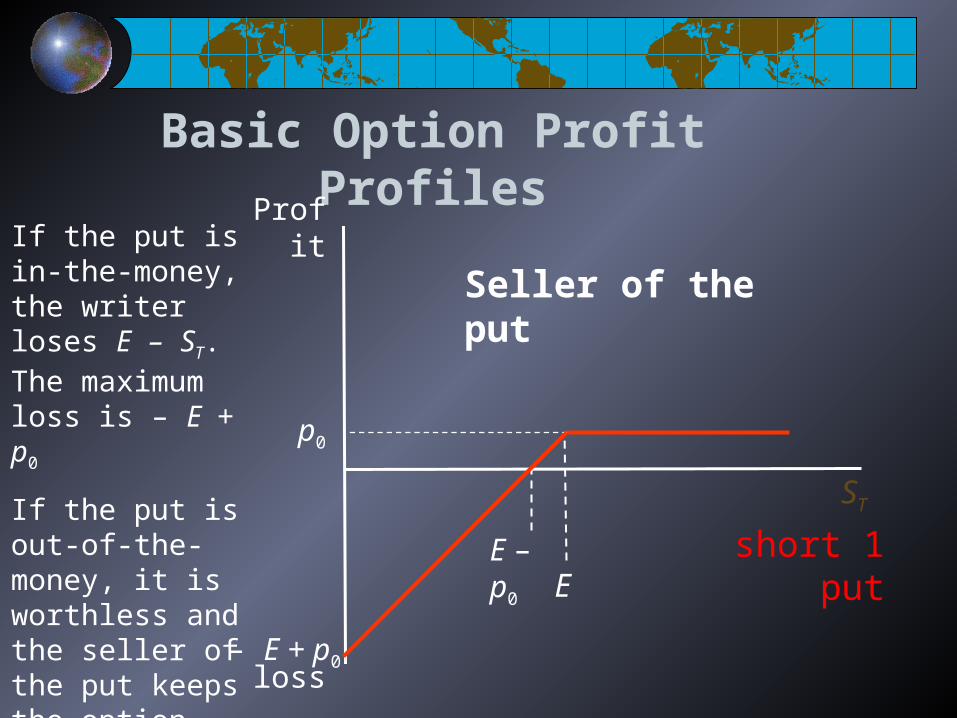

If the put is in-the-money, the writer loses E – ST. The maximum loss is – E + p0

If the put is out-of-the-money, it is worthless and the seller of the put keeps the option premium of p0.

Seller of the put

Example

$1.50

ST

Profit

loss

–$0.25

$1.75

Long 1 call on 1 pound

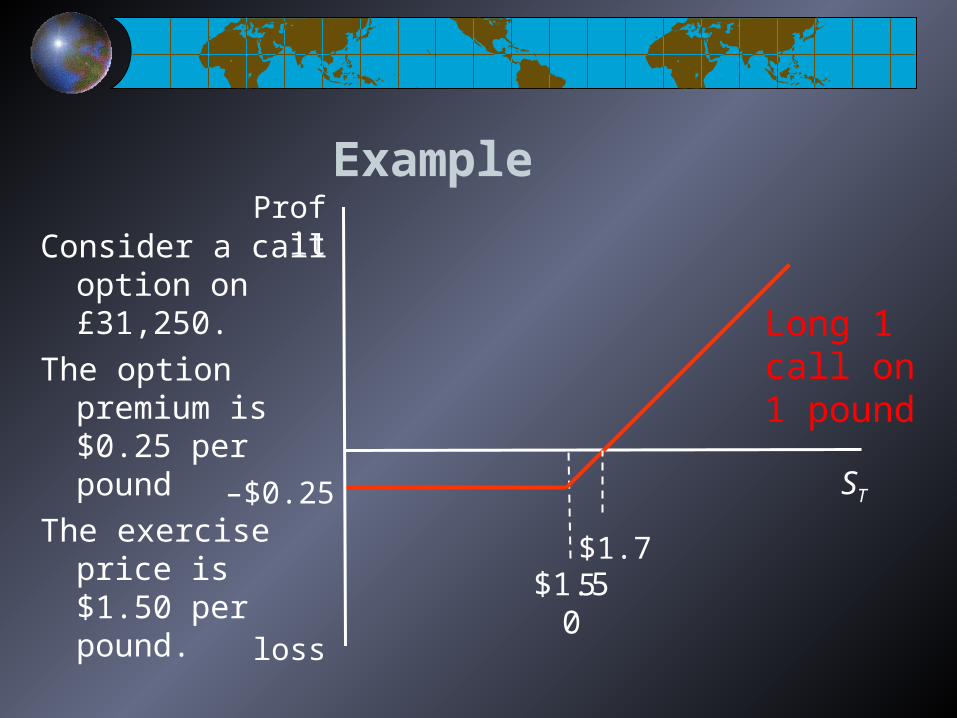

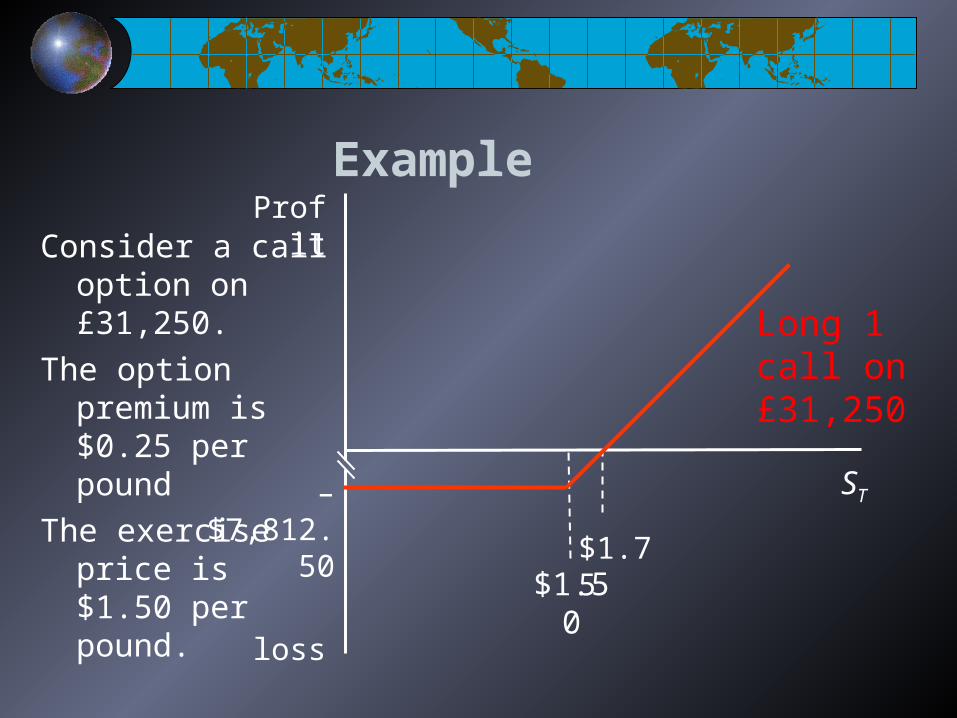

Consider a call option on £31,250.

The option premium is $0.25 per pound

The exercise price is $1.50 per pound.

Example

$1.50

ST

Profit

loss

–$7,812.50

$1.75

Long 1 call on £31,250

Consider a call option on £31,250.

The option premium is $0.25 per pound

The exercise price is $1.50 per pound.

Example

$1.50

ST

Profit

loss

$42,187.50

$1.35 Long 1 put on £31,250

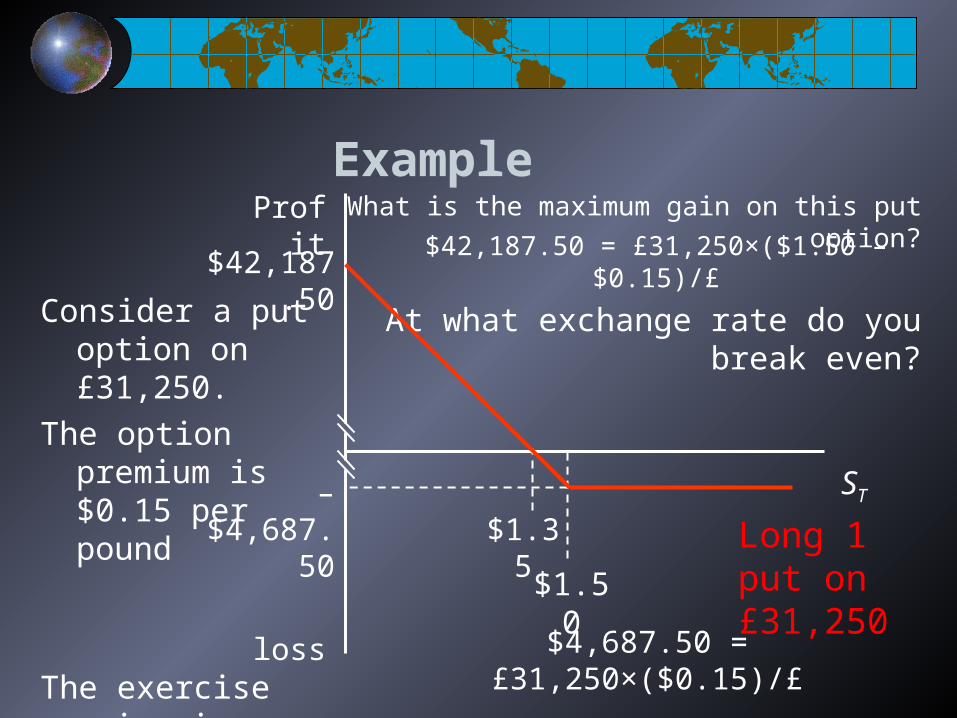

Consider a put option on £31,250.

The option premium is $0.15 per pound

The exercise price is $1.50 per pound.

What is the maximum gain on this put option?

At what exchange rate do you break even?

–$4,687.50

$42,187.50 = £31,250×($1.50 – $0.15)/£

$4,687.50 = £31,250×($0.15)/£

Market Value, Time Value and Intrinsic Value for an American Call

E

ST

Profit

loss

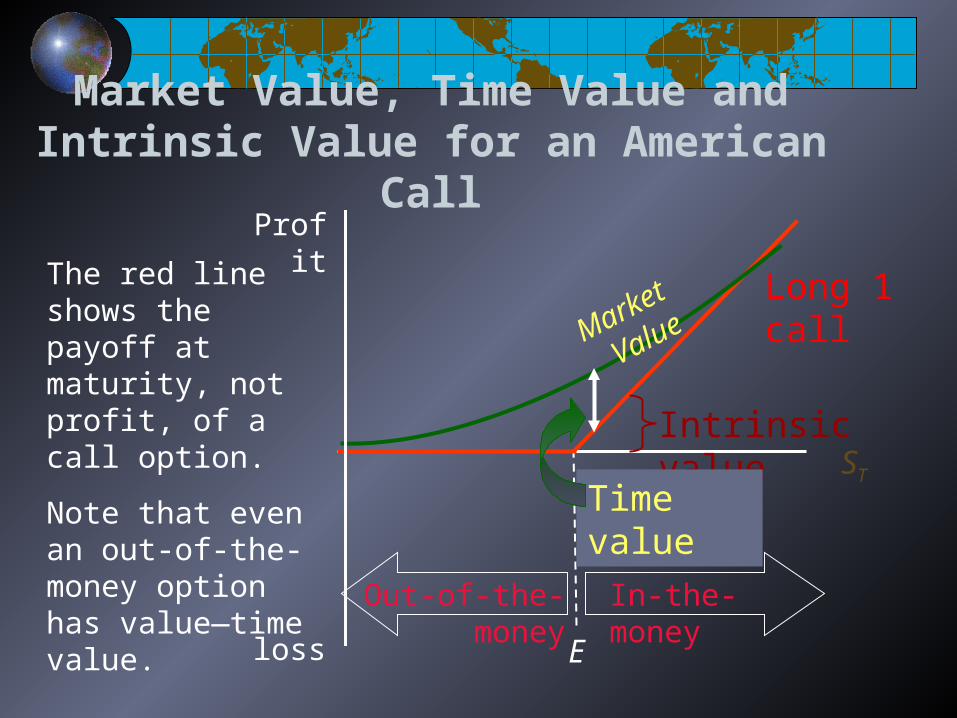

Long 1 callThe red line shows the payoff at maturity, not profit, of a call option.

Note that even an out-of-the-money option has value—time value.

Intrinsic value

Time value

Market Value

In-the-moneyOut-of-the-money

Example

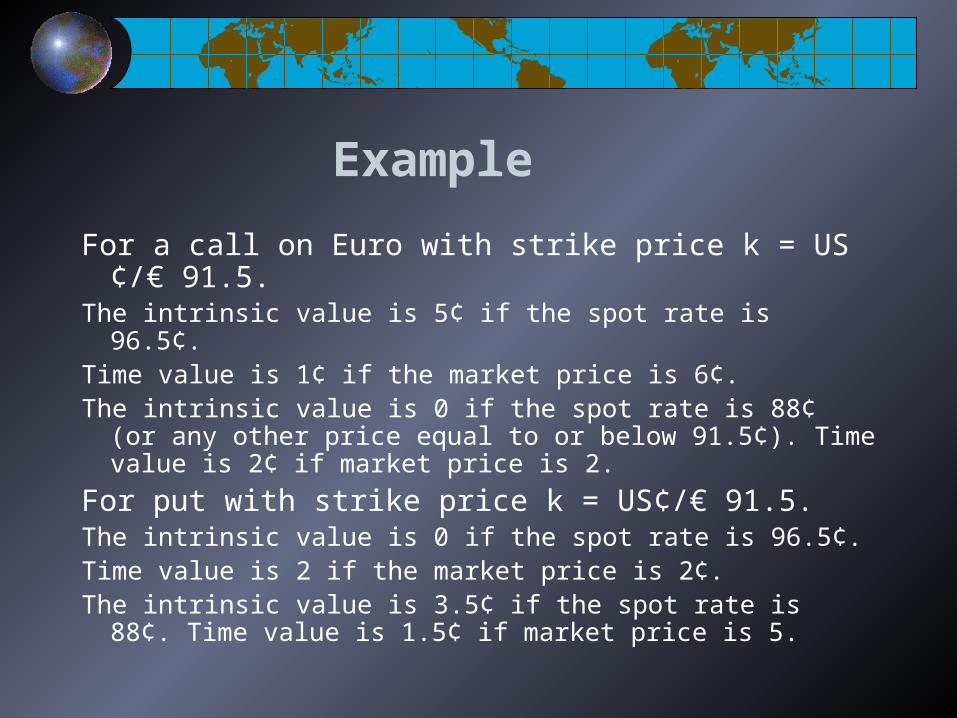

For a call on Euro with strike price k = US¢/€ 91.5.The intrinsic value is 5¢ if the spot rate is 96.5¢.Time value is 1¢ if the market price is 6¢.The intrinsic value is 0 if the spot rate is 88¢ (or any other price

equal to or below 91.5¢). Time value is 2¢ if market price is 2.

For put with strike price k = US¢/€ 91.5.The intrinsic value is 0 if the spot rate is 96.5¢.Time value is 2 if the market price is 2¢.The intrinsic value is 3.5¢ if the spot rate is 88¢. Time value is

1.5¢ if market price is 5.

Learning outcomesLearning outcomes

• Discuss the similarities and differences between forward and futures.• Explain the difference between hedgers and speculators• Explain why most futures positions are closed out through a reversing trade rather than held to delivery• Define the call and put options; the rights of the buyers and obligations of the sellers• Explain the differences between European and American options• Know the basic option pricing relationships at expiration• Basic option profit profiles (all four of them)• Know how to calculate the intrinsic value and time value of the options• Know how to calculate the profit/loss of long/short call and put speculative positions (for example, see the numerical examples done in class)