Embed Size (px)

Citation preview

Future Truck Powertrain Developments

Will Europe Become a Role Model?

Roman MathyssekSenior Truck Analyst & Advisor

Copyright © 2008 Global Insight, Inc. 2

Introduction

• Heart of every truck and key cost driver:

– Component sharing between OEMs is increasing, why?

– European manufacturers play ever more dominant role in truck engine business / setting standards, why?

– Future truck engine developments in Europe, some structural changes, why?

Copyright © 2008 Global Insight, Inc. 3

Presentation Outline

• Introduction

• Global Truck Industry Structure—Implications

• Global Truck Engines—Daimler and Volvo

• Rising Engine Costs—Manufacturer Remedies

• Conclusions

• Powertrain Developments of European Manufacturers—Some Trends

Copyright © 2008 Global Insight, Inc. 4

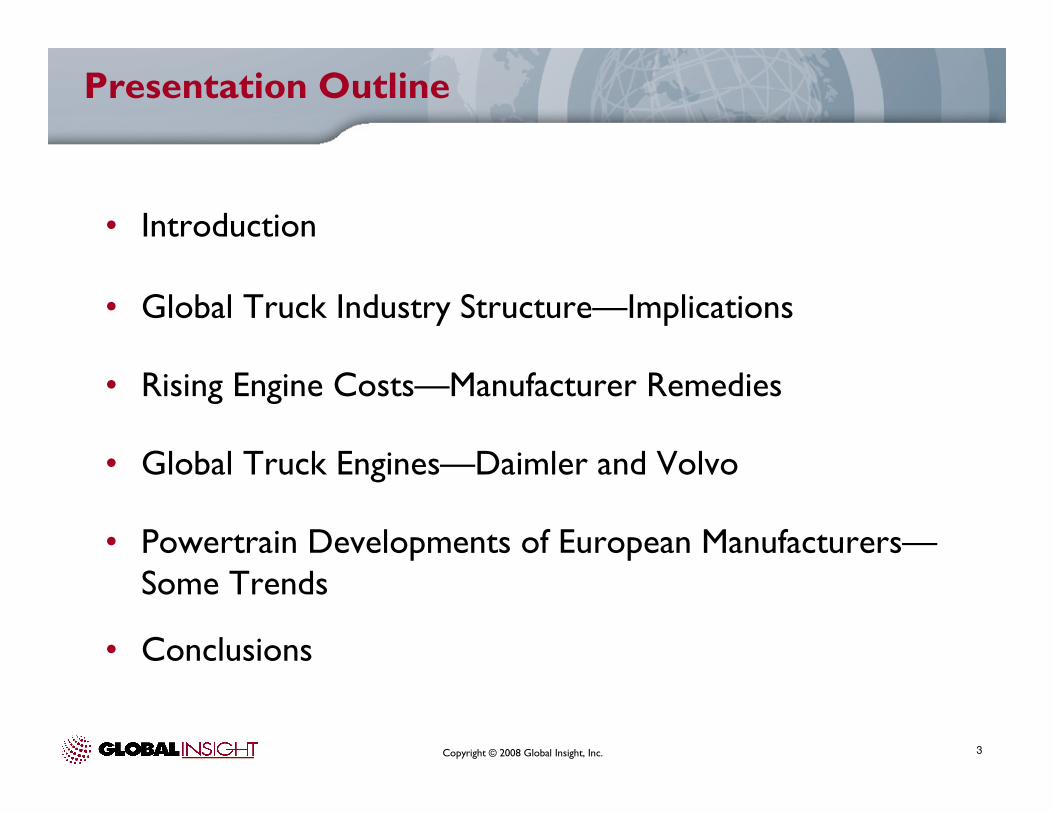

Global Truck Industry Structure (>6t)

Dong Feng

TATA Motors

FAW

KamAz

Volkswagen

Ford

Middle East

General

Motors Inc

Navistar

Intern Inc.

Southern Africa Oceania

Paccar Inc

Hino

Isuzu Motors

MAN

Scania AB

Iveco

Volvo AB

Daimler AG

AsiaEast EuropeWest EuropeSouth AmericaNAFTA

Dong Feng

TATA Motors

FAW

KamAz

Volkswagen

Ford

Middle East

General

Motors Inc

Navistar

Intern Inc.

Southern Africa Oceania

Paccar Inc

Hino

Isuzu Motors

MAN

Scania AB

Iveco

Volvo AB

Daimler AG

AsiaEast EuropeWest EuropeSouth AmericaNAFTA

VW do BrazilVW do BrazilVW do BrazilVW do Brazil VW do BrazilVW do Brazil

Copyright © 2008 Global Insight, Inc. 5

Global Dominance of European Manufacturers

• European OEMs:

– “Export” their norms into many other regions

– Often re-use old technology for emerging markets engines (Euro 2/3)

– Consolidate US: EPA allows Adblue infrastructure –first step to operate EU engines with minimal changes

– Still have potential to benefit from global presence and convergence of standards (Daimler HDEP)

– Those that don’t have sufficient scale internally, search for co-operations and alliances to obtain similar scale externally

Copyright © 2008 Global Insight, Inc. 6

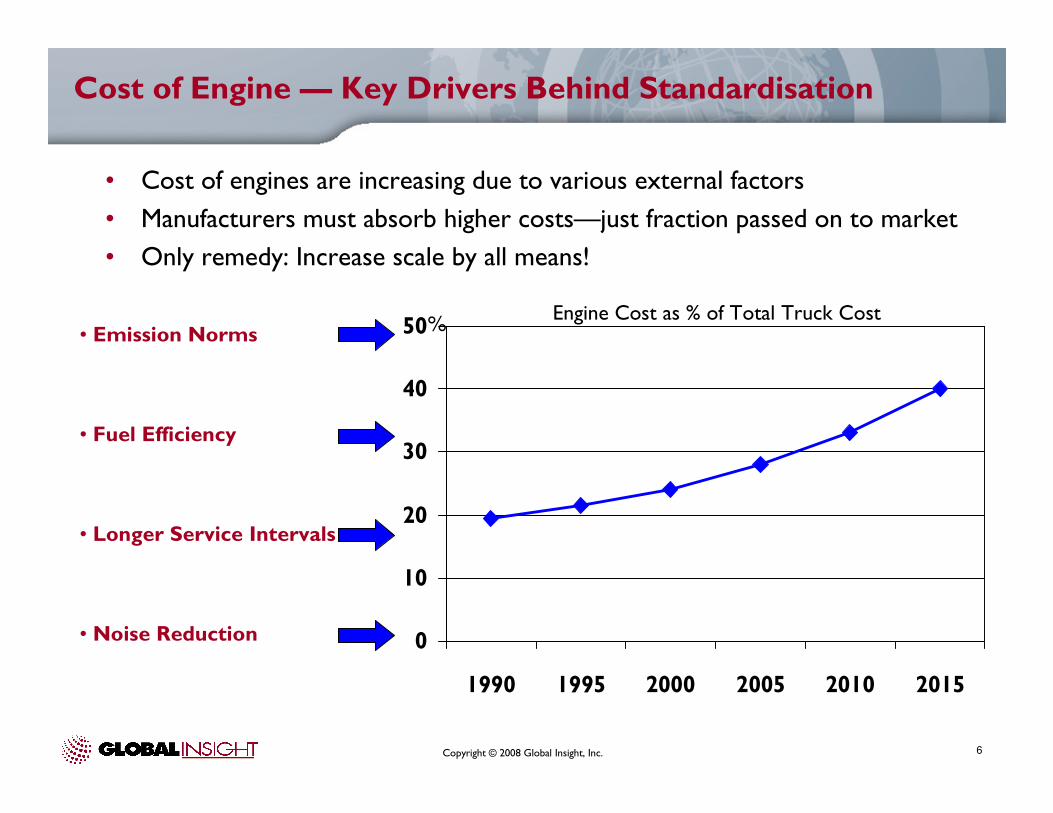

Cost of Engine — Key Drivers Behind Standardisation

• Emission Norms

• Fuel Efficiency

0

10

20

30

40

50

1990 1995 2000 2005 2010 2015

• Noise Reduction

• Longer Service Intervals

• Cost of engines are increasing due to various external factors

• Manufacturers must absorb higher costs—just fraction passed on to market

• Only remedy: Increase scale by all means!

%Engine Cost as % of Total Truck Cost

Copyright © 2008 Global Insight, Inc. 7

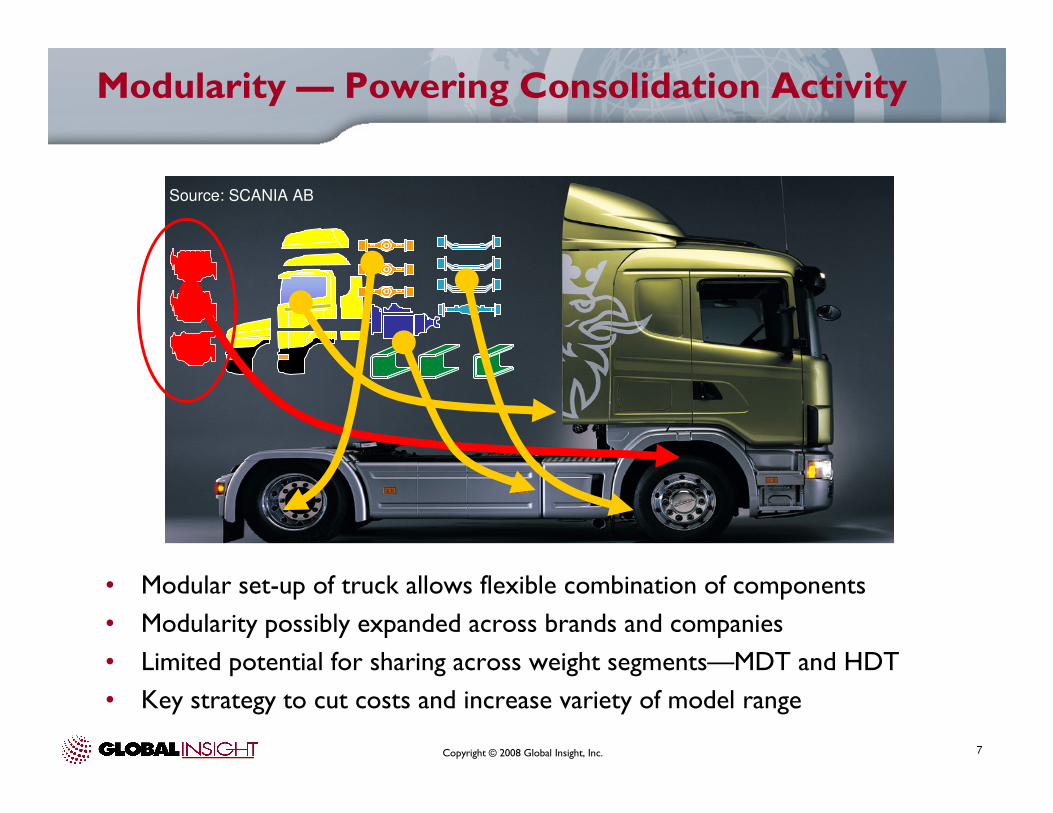

Modularity — Powering Consolidation Activity

Source: SCANIA AB

• Modular set-up of truck allows flexible combination of components

• Modularity possibly expanded across brands and companies

• Limited potential for sharing across weight segments—MDT and HDT

• Key strategy to cut costs and increase variety of model range

Copyright © 2008 Global Insight, Inc. 8

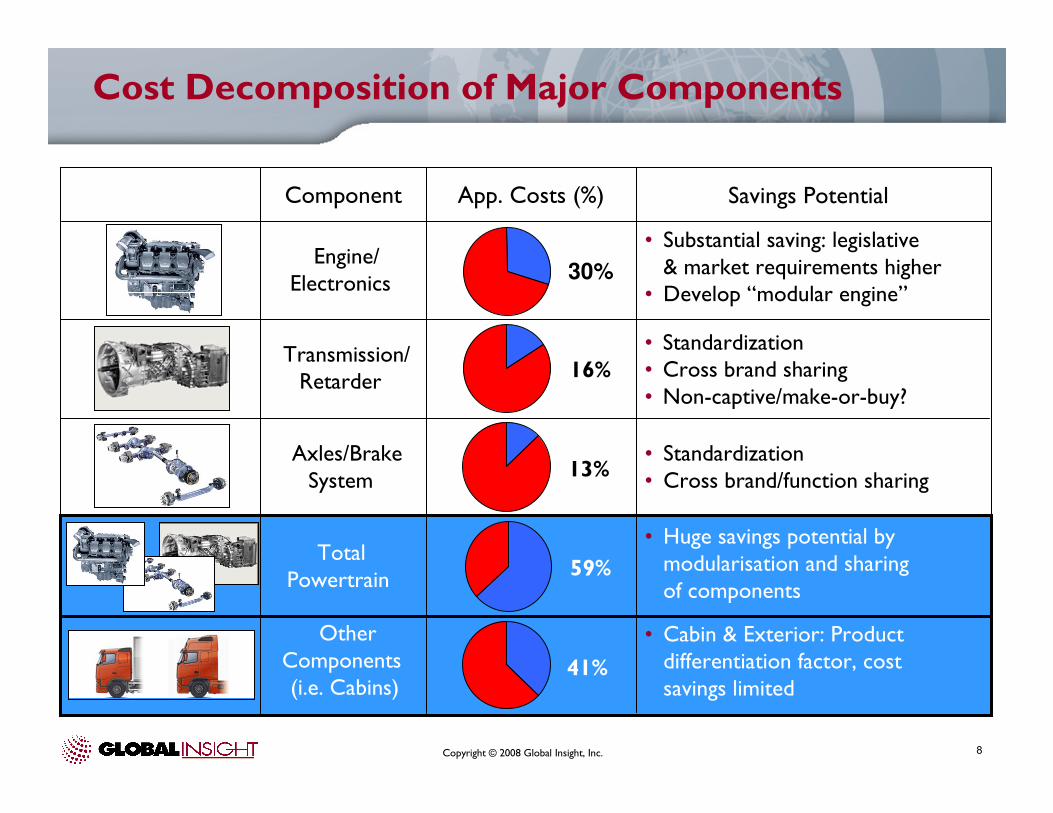

Cost Decomposition of Major Components

Engine/Electronics

Component App. Costs (%) Savings Potential

Transmission/Retarder

Axles/BrakeSystem

TotalPowertrain

OtherComponents (i.e. Cabins)

• Substantial saving: legislative& market requirements higher

• Develop “modular engine”

• Standardization• Cross brand sharing• Non-captive/make-or-buy?

• Standardization• Cross brand/function sharing

• Huge savings potential by modularisation and sharingof components

• Cabin & Exterior: Productdifferentiation factor, cost savings limited

16%

13%

59%

41%

30%

Copyright © 2008 Global Insight, Inc. 9

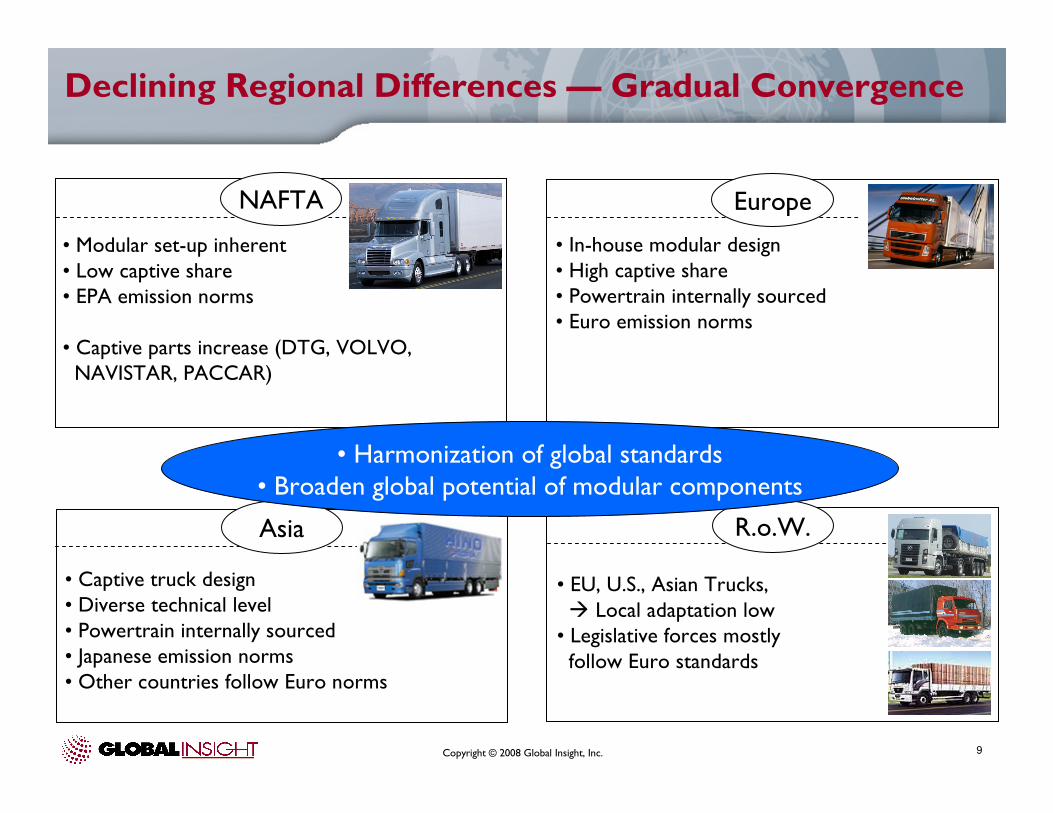

Declining Regional Differences — Gradual Convergence

• Captive truck design• Diverse technical level • Powertrain internally sourced• Japanese emission norms• Other countries follow Euro norms

Asia

• Modular set-up inherent• Low captive share• EPA emission norms

• Captive parts increase (DTG, VOLVO,NAVISTAR, PACCAR)

NAFTA

• EU, U.S., Asian Trucks,� Local adaptation low• Legislative forces mostlyfollow Euro standards

R.o.W.

• In-house modular design• High captive share• Powertrain internally sourced• Euro emission norms

Europe

• Harmonization of global standards• Broaden global potential of modular components

Copyright © 2008 Global Insight, Inc. 10

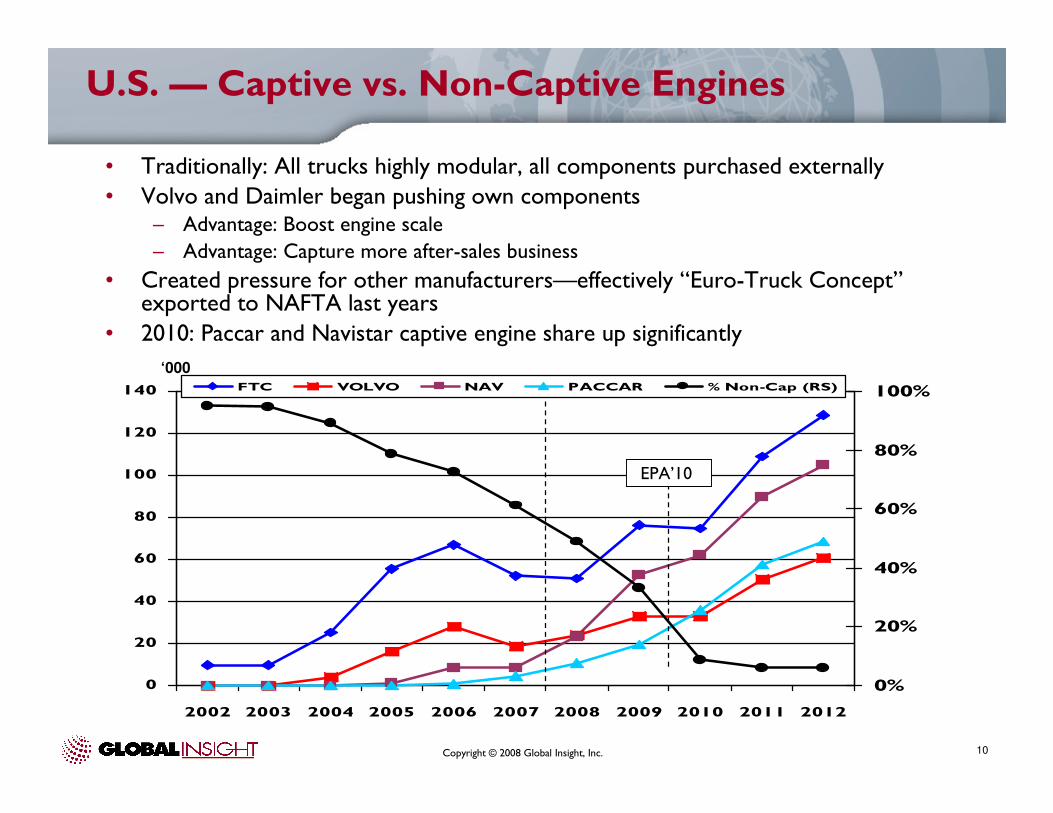

U.S. — Captive vs. Non-Captive Engines

• Traditionally: All trucks highly modular, all components purchased externally

• Volvo and Daimler began pushing own components– Advantage: Boost engine scale

– Advantage: Capture more after-sales business

• Created pressure for other manufacturers—effectively “Euro-Truck Concept”exported to NAFTA last years

• 2010: Paccar and Navistar captive engine share up significantly

0

20

40

60

80

100

120

140

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

0%

20%

40%

60%

80%

100%FTC VOLVO NAV PACCAR % Non-Cap (RS)

EPA’10

‘000

Copyright © 2008 Global Insight, Inc. 11

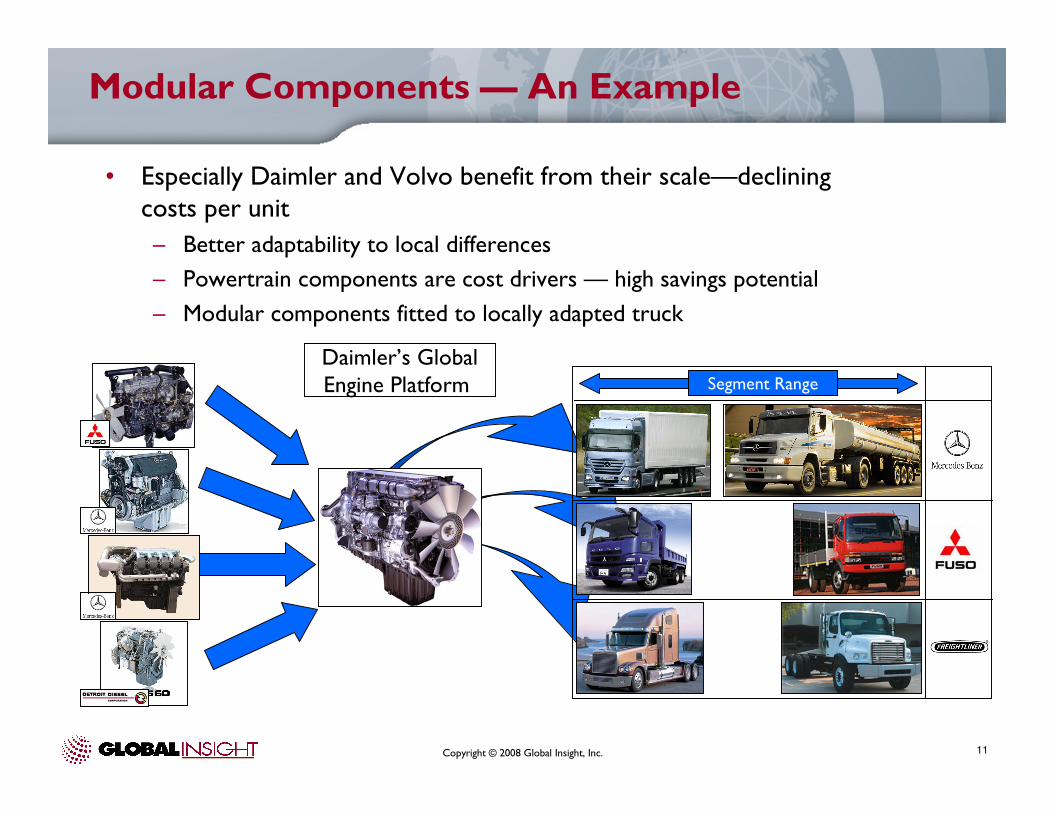

Modular Components — An Example

• Especially Daimler and Volvo benefit from their scale—declining costs per unit

– Better adaptability to local differences

– Powertrain components are cost drivers — high savings potential

– Modular components fitted to locally adapted truck

Daimler’s GlobalEngine Platform Segment Range

Copyright © 2008 Global Insight, Inc. 12

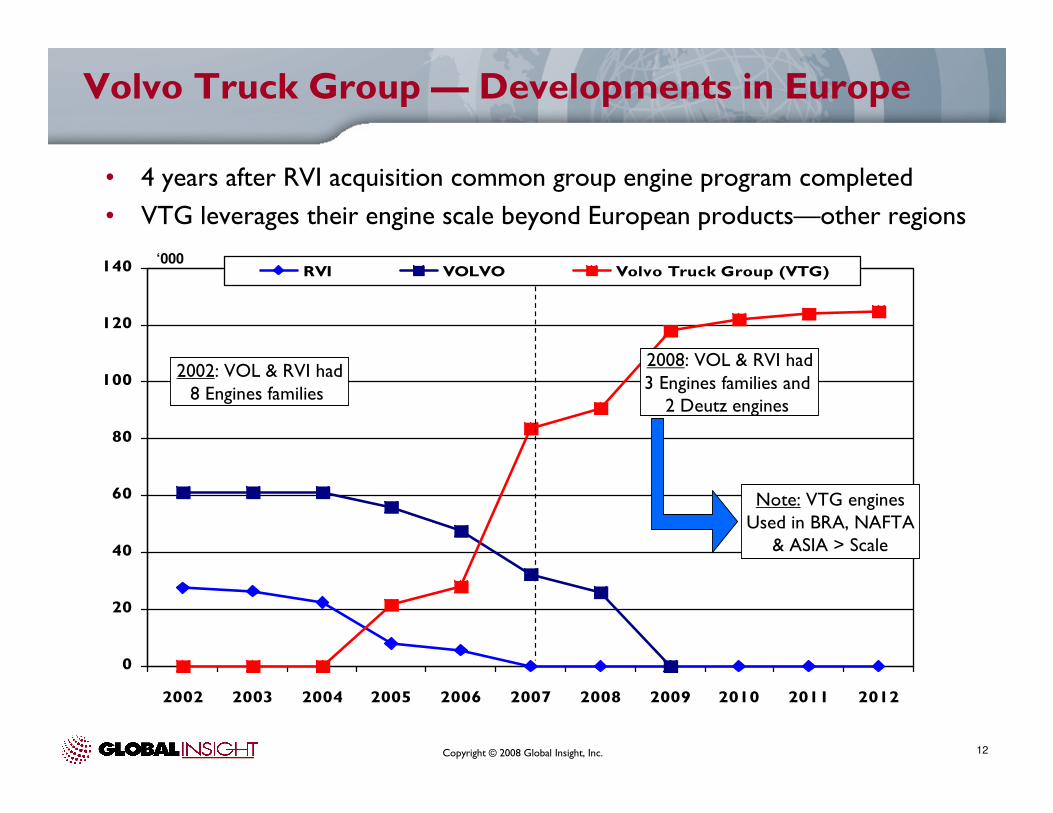

Volvo Truck Group — Developments in Europe

• 4 years after RVI acquisition common group engine program completed

• VTG leverages their engine scale beyond European products—other regions

0

20

40

60

80

100

120

140

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

RVI VOLVO Volvo Truck Group (VTG)

2002: VOL & RVI had8 Engines families

2008: VOL & RVI had3 Engines families and 2 Deutz engines

Note: VTG enginesUsed in BRA, NAFTA& ASIA > Scale

‘000

Copyright © 2008 Global Insight, Inc. 13

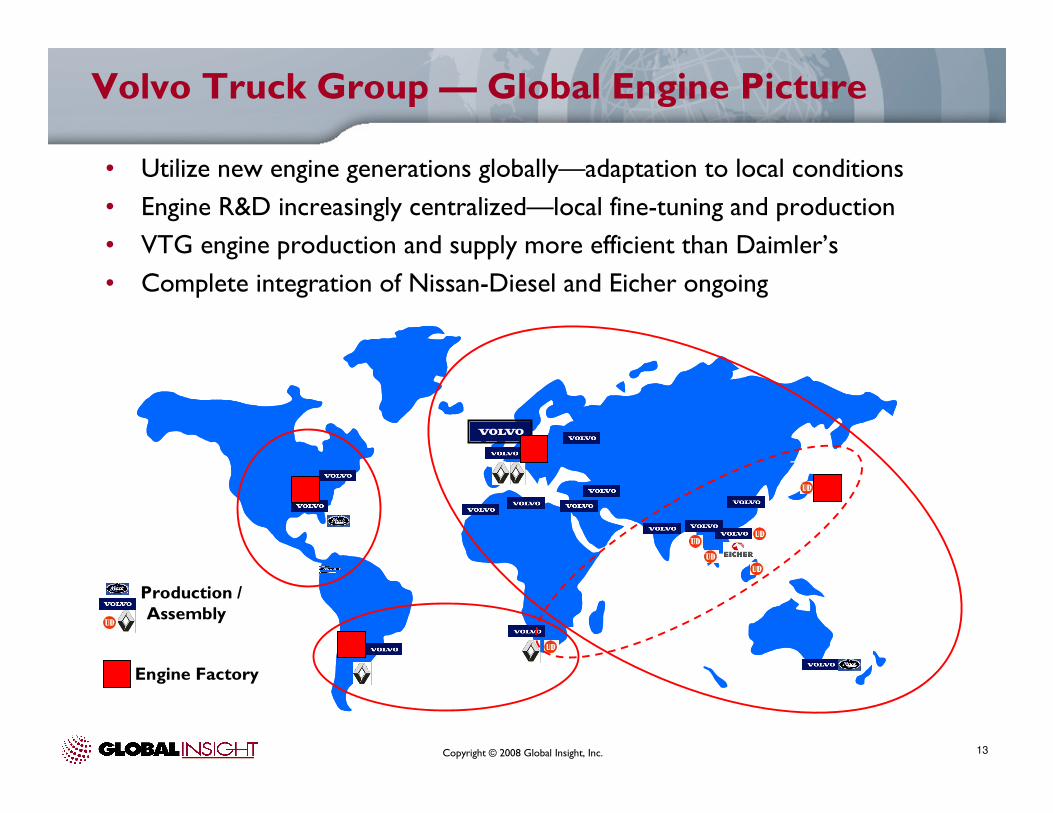

Volvo Truck Group — Global Engine Picture

• Utilize new engine generations globally—adaptation to local conditions

• Engine R&D increasingly centralized—local fine-tuning and production

• VTG engine production and supply more efficient than Daimler’s

• Complete integration of Nissan-Diesel and Eicher ongoing

Engine Factory

Production /Assembly

Copyright © 2008 Global Insight, Inc. 14

Leveraging Global Scale — The Devil Is in the Detail

• Globally active OEMs all work to create global engine families

– Benefit from scale

– Reduce complexity

• Despite convergence of standards, still many differences

– Fuel quality variations

– Different legislations and regulations

– Truck design not suited for engine

– Fine-tuning costly process

• Challenges retard global engines—reduce volumes, add costs

– Directionally, nothing will change, global engines are coming

– Cost/Unit advantage of large OEMs force smaller ones to act

Copyright © 2008 Global Insight, Inc. 15

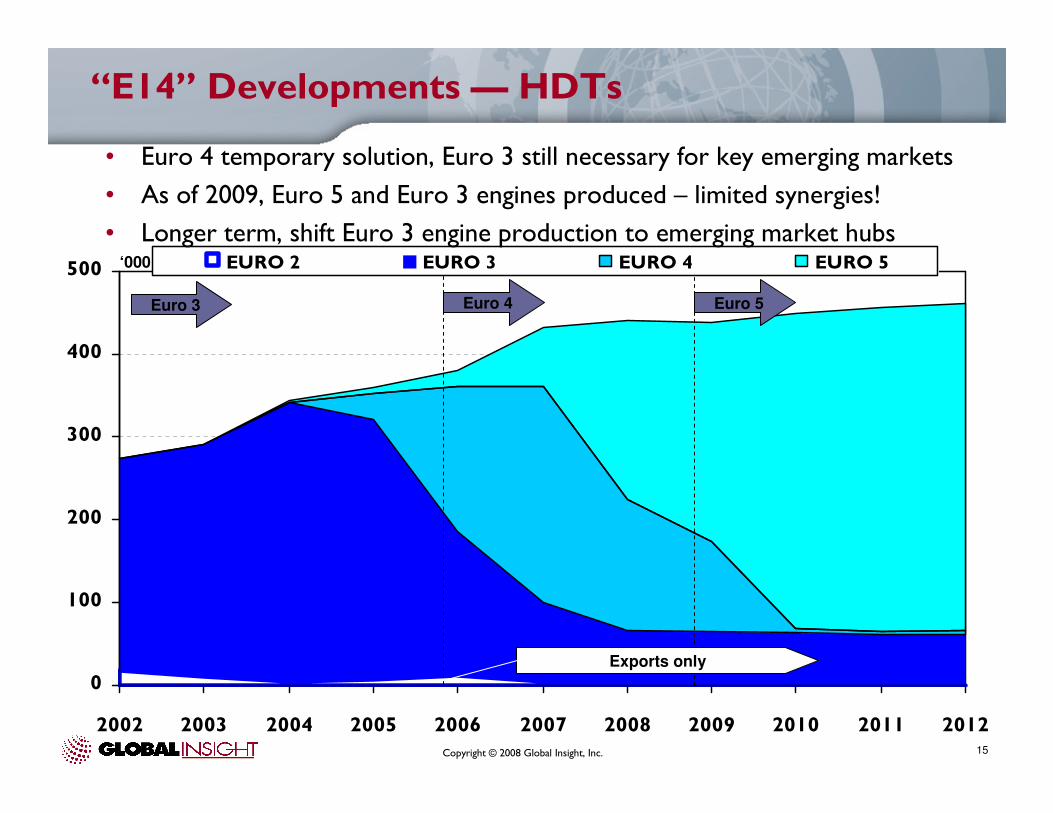

“E14” Developments — HDTs

0

100

200

300

400

500

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

EURO 2 EURO 3 EURO 4 EURO 5

• Euro 4 temporary solution, Euro 3 still necessary for key emerging markets

• As of 2009, Euro 5 and Euro 3 engines produced – limited synergies!

• Longer term, shift Euro 3 engine production to emerging market hubs

Euro 4 Euro 5Euro 3

Exports only

‘000

Copyright © 2008 Global Insight, Inc. 16

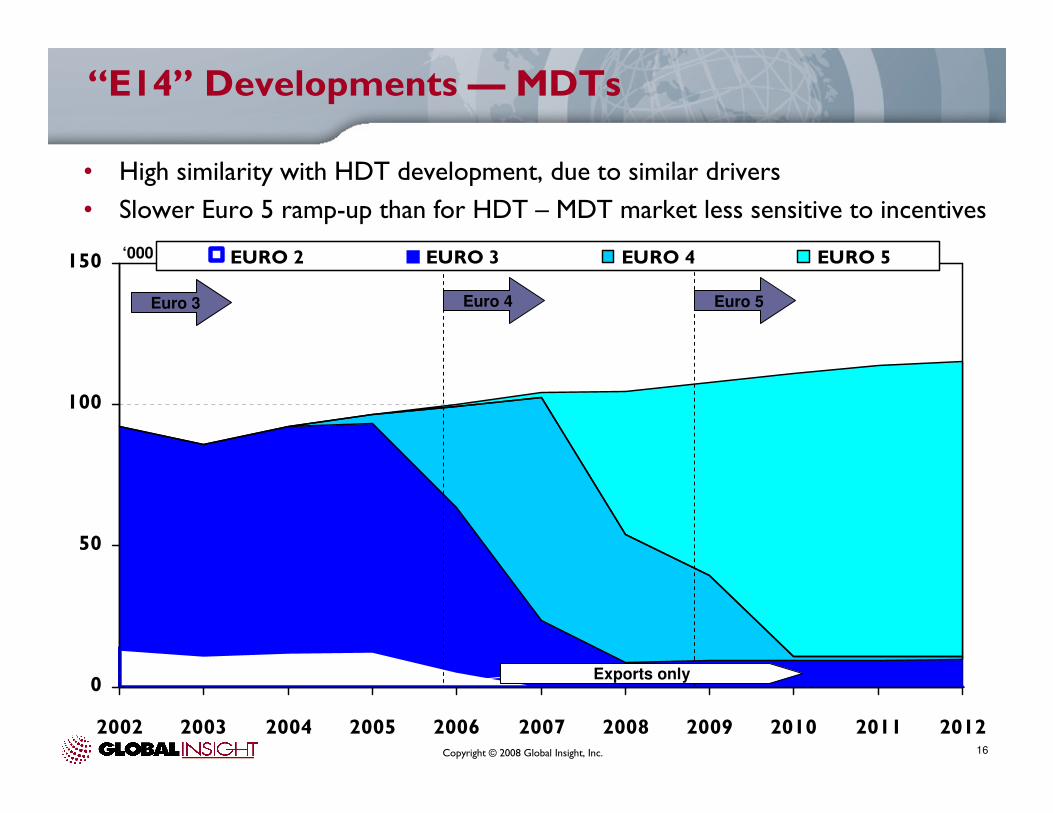

“E14” Developments — MDTs

0

50

100

150

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

EURO 2 EURO 3 EURO 4 EURO 5

• High similarity with HDT development, due to similar drivers

• Slower Euro 5 ramp-up than for HDT – MDT market less sensitive to incentives

Euro 3 Euro 4 Euro 5

Exports only

‘000

Copyright © 2008 Global Insight, Inc. 17

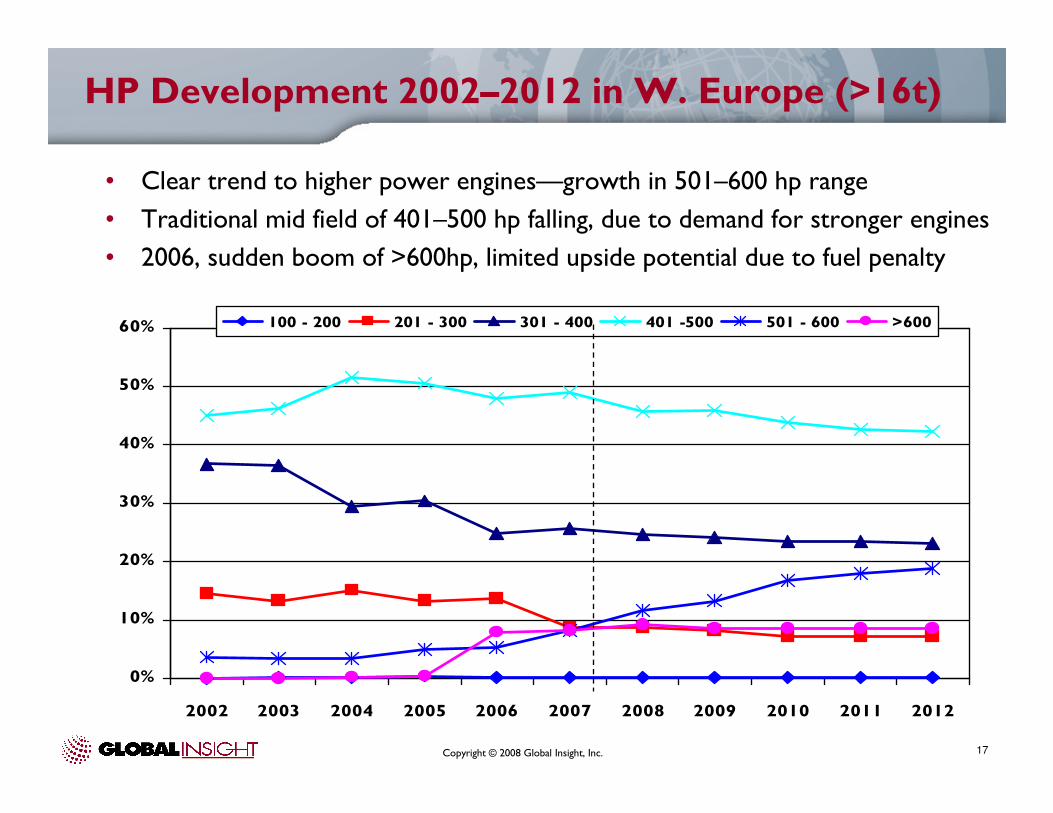

HP Development 2002–2012 in W. Europe (>16t)

0%

10%

20%

30%

40%

50%

60%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

100 - 200 201 - 300 301 - 400 401 -500 501 - 600 >600

• Clear trend to higher power engines—growth in 501–600 hp range

• Traditional mid field of 401–500 hp falling, due to demand for stronger engines

• 2006, sudden boom of >600hp, limited upside potential due to fuel penalty

Copyright © 2008 Global Insight, Inc. 18

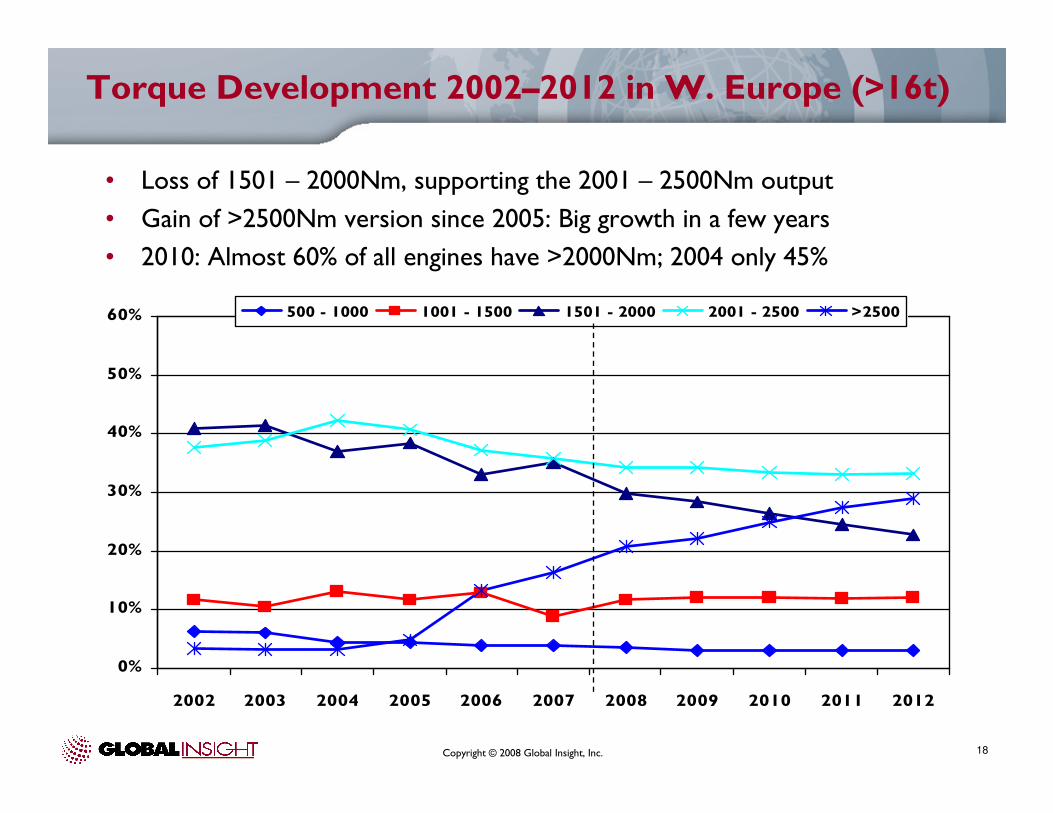

Torque Development 2002–2012 in W. Europe (>16t)

0%

10%

20%

30%

40%

50%

60%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

500 - 1000 1001 - 1500 1501 - 2000 2001 - 2500 >2500

• Loss of 1501 – 2000Nm, supporting the 2001 – 2500Nm output

• Gain of >2500Nm version since 2005: Big growth in a few years

• 2010: Almost 60% of all engines have >2000Nm; 2004 only 45%

Copyright © 2008 Global Insight, Inc. 19

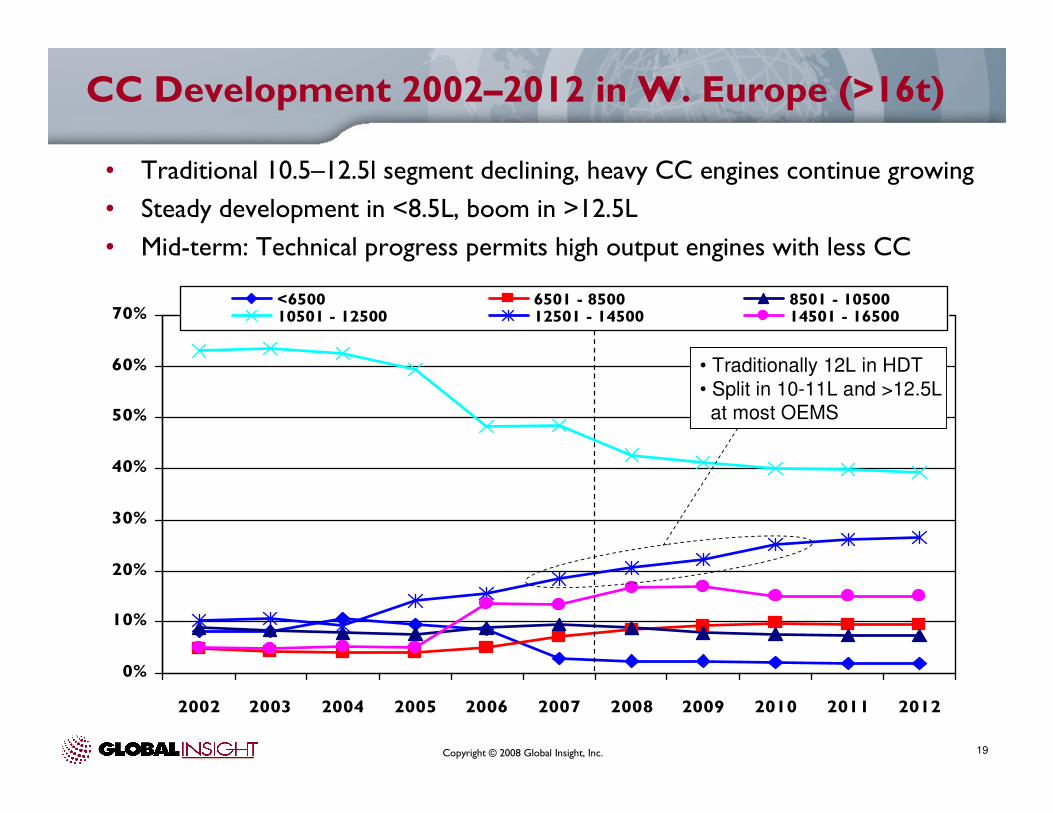

CC Development 2002–2012 in W. Europe (>16t)

• Traditional 10.5–12.5l segment declining, heavy CC engines continue growing

• Steady development in <8.5L, boom in >12.5L

• Mid-term: Technical progress permits high output engines with less CC

0%

10%

20%

30%

40%

50%

60%

70%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

<6500 6501 - 8500 8501 - 1050010501 - 12500 12501 - 14500 14501 - 16500

• Traditionally 12L in HDT

• Split in 10-11L and >12.5L

at most OEMS

Copyright © 2008 Global Insight, Inc. 20

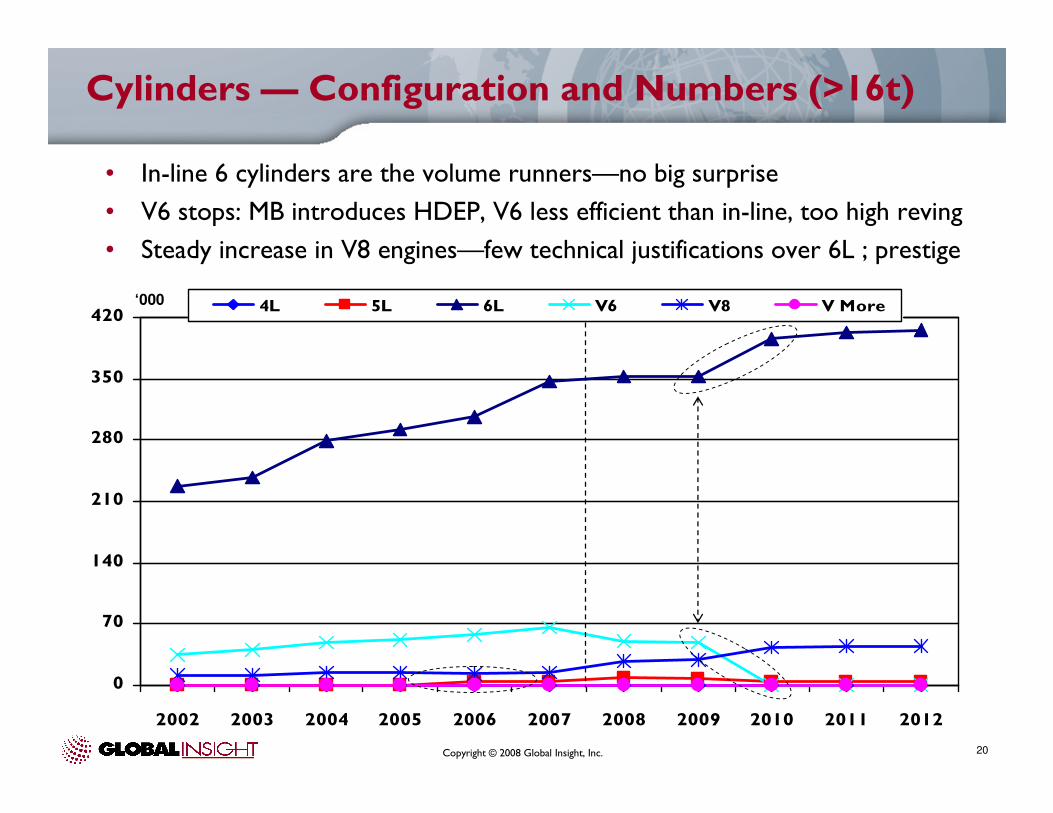

Cylinders — Configuration and Numbers (>16t)

• In-line 6 cylinders are the volume runners—no big surprise

• V6 stops: MB introduces HDEP, V6 less efficient than in-line, too high reving

• Steady increase in V8 engines—few technical justifications over 6L ; prestige

0

70

140

210

280

350

420

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

4L 5L 6L V6 V8 V More‘000

Copyright © 2008 Global Insight, Inc. 21

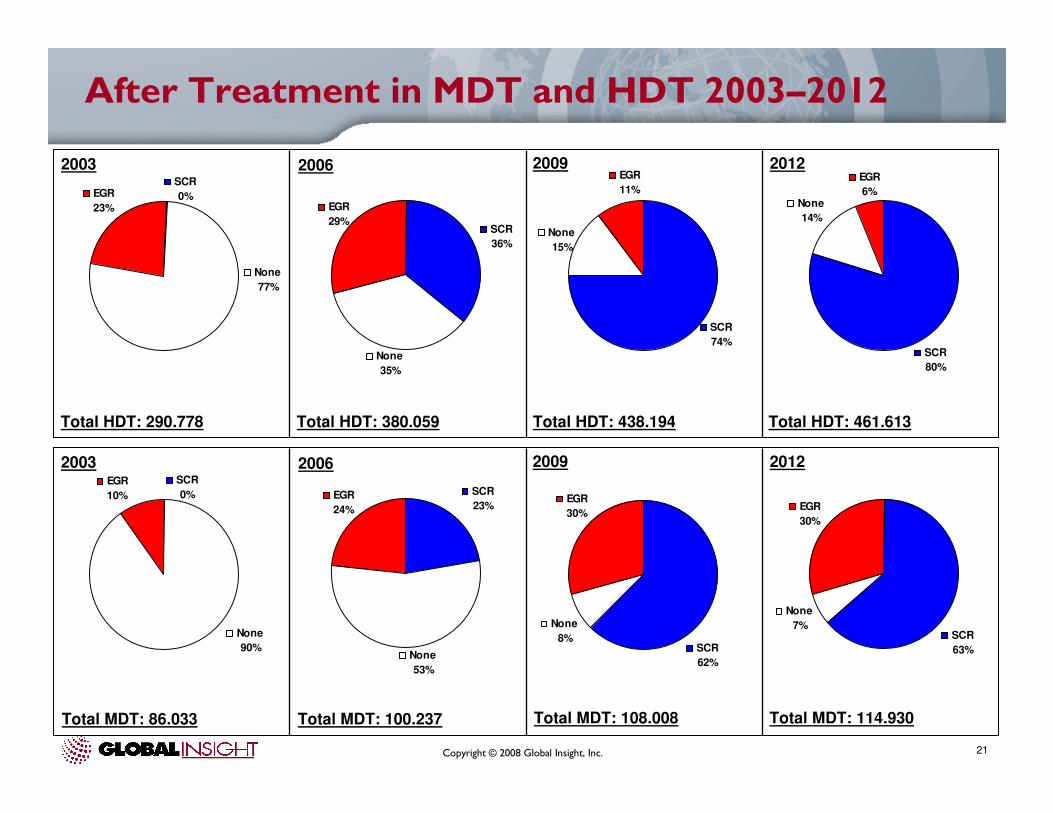

After Treatment in MDT and HDT 2003–2012

EGR

23%

None

77%

SCR

0%

2003 2006

Total HDT: 290.778 Total HDT: 380.059 Total HDT: 438.194 Total HDT: 461.613

SCR

36%

None

35%

EGR

29%

SCR

74%

None

15%

EGR

11%EGR

6%None

14%

SCR

80%

2009 2012

EGR

10%

None

90%

SCR

0%

2003 2006

Total MDT: 86.033 Total MDT: 100.237 Total MDT: 108.008 Total MDT: 114.930

SCR

23%

None

53%

EGR

24%

SCR

62%

None

8%

EGR

30%EGR

30%

None

7%SCR

63%

2009 2012

Copyright © 2008 Global Insight, Inc. 22

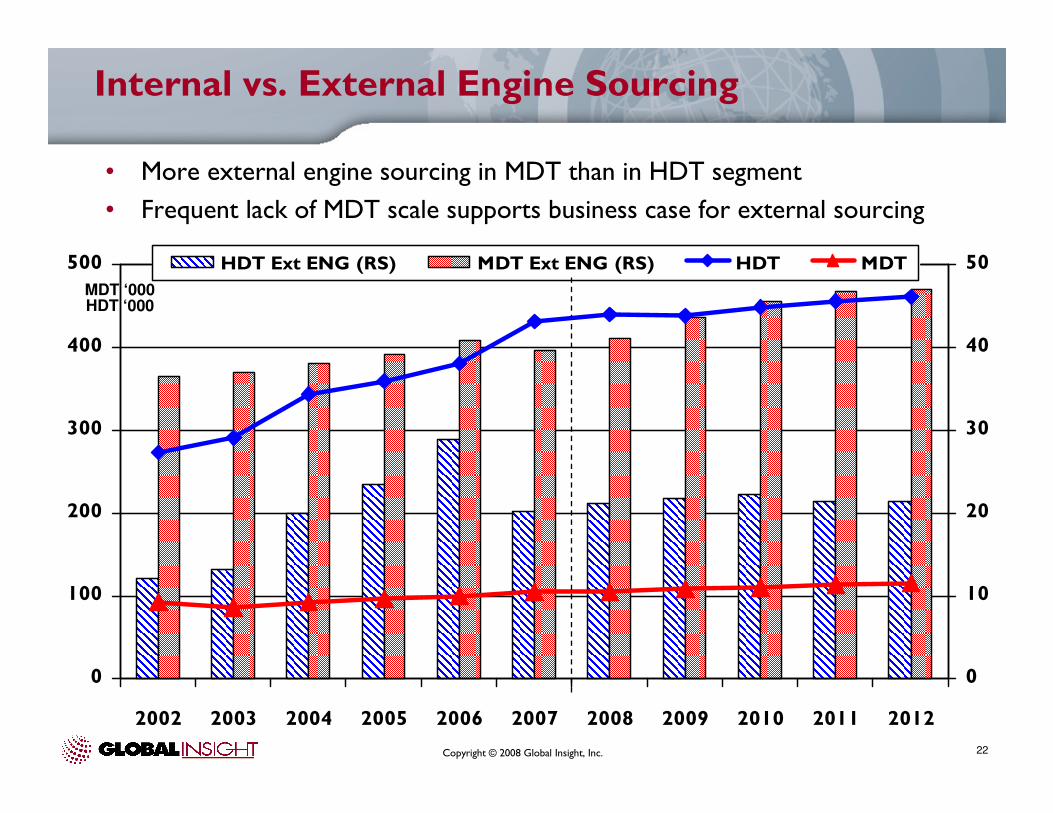

Internal vs. External Engine Sourcing

0

100

200

300

400

500

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

0

10

20

30

40

50HDT Ext ENG (RS) MDT Ext ENG (RS) HDT MDT

• More external engine sourcing in MDT than in HDT segment

• Frequent lack of MDT scale supports business case for external sourcing

MDT ‘000HDT ‘000

Copyright © 2008 Global Insight, Inc. 23

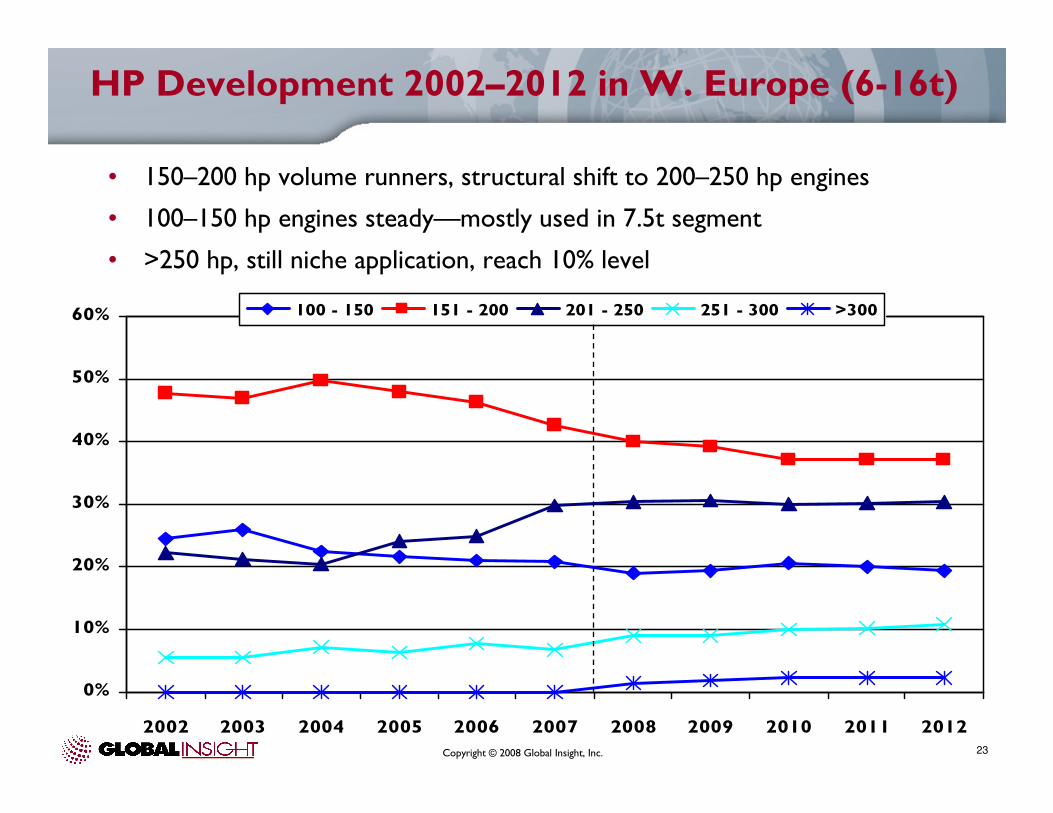

HP Development 2002–2012 in W. Europe (6-16t)

0%

10%

20%

30%

40%

50%

60%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

100 - 150 151 - 200 201 - 250 251 - 300 >300

• 150–200 hp volume runners, structural shift to 200–250 hp engines

• 100–150 hp engines steady—mostly used in 7.5t segment

• >250 hp, still niche application, reach 10% level

Copyright © 2008 Global Insight, Inc. 24

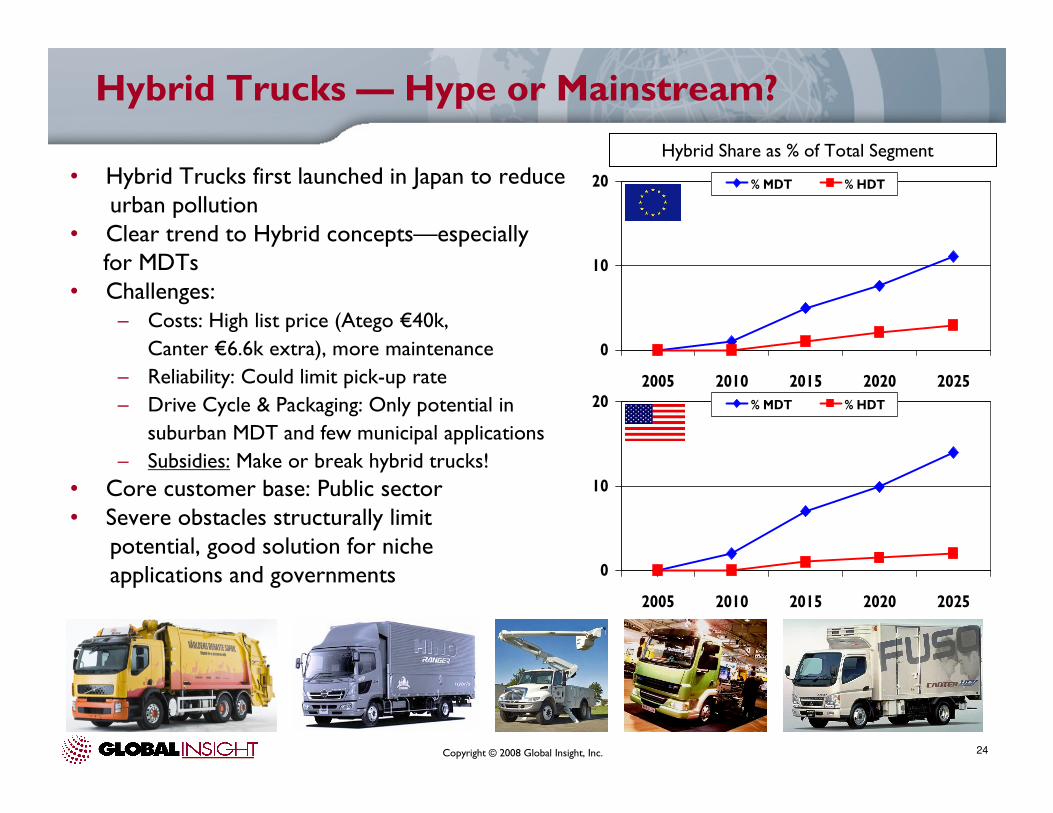

Hybrid Trucks — Hype or Mainstream?

• Hybrid Trucks first launched in Japan to reduce urban pollution

• Clear trend to Hybrid concepts—especially for MDTs

• Challenges:– Costs: High list price (Atego €40k,

Canter €6.6k extra), more maintenance

– Reliability: Could limit pick-up rate

– Drive Cycle & Packaging: Only potential in

suburban MDT and few municipal applications

– Subsidies: Make or break hybrid trucks!

• Core customer base: Public sector• Severe obstacles structurally limit

potential, good solution for niche applications and governments

0

10

20

2005 2010 2015 2020 2025

% MDT % HDT

Hybrid Share as % of Total Segment

0

10

20

2005 2010 2015 2020 2025

% MDT % HDT

Copyright © 2008 Global Insight, Inc. 25

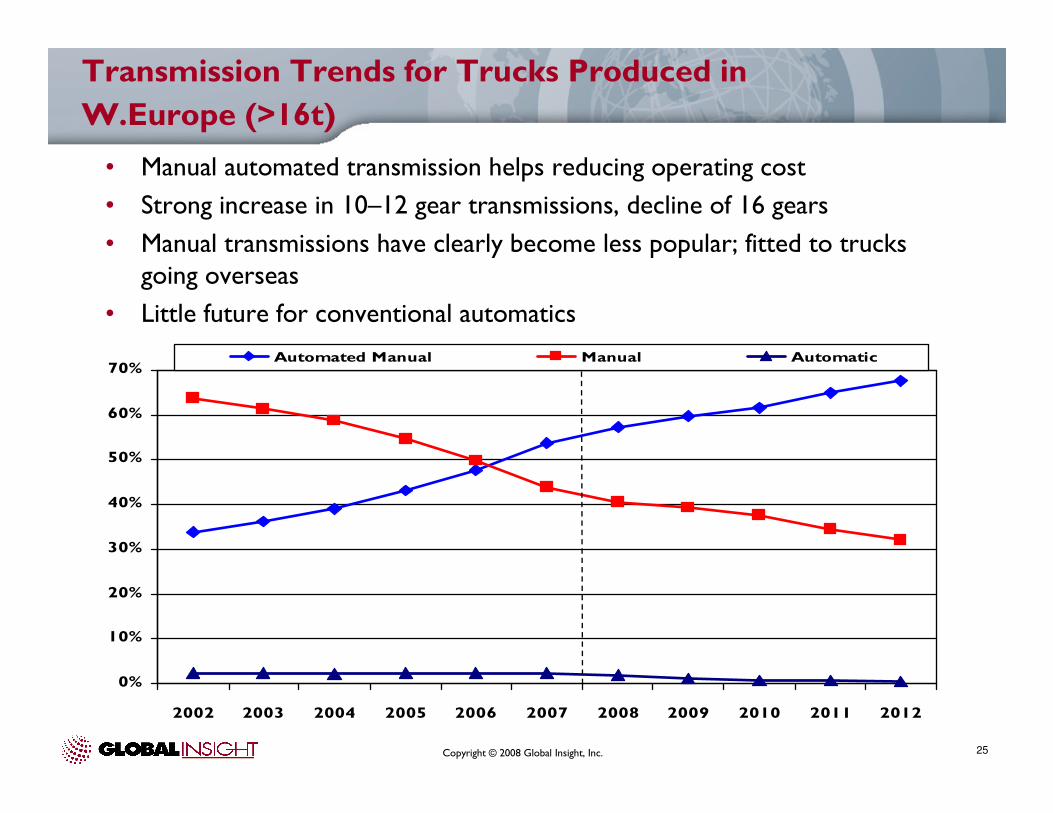

Transmission Trends for Trucks Produced in

W.Europe (>16t)

• Manual automated transmission helps reducing operating cost

• Strong increase in 10–12 gear transmissions, decline of 16 gears

• Manual transmissions have clearly become less popular; fitted to trucks going overseas

• Little future for conventional automatics

0%

10%

20%

30%

40%

50%

60%

70%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Automated Manual Manual Automatic

Copyright © 2008 Global Insight, Inc. 26

European Powertrain Summary

• Key trends are:

– Rising engine power, limited fuel penalty due to technology progress

– Declining traditional 12L segment, growth in slightly larger engines

(+/ 13L) to have sufficient CC to provide higher engine output

– Limited hybrid potential, subsidies are important

– Transmission automation continues at high rate

• European production still influenced by export market demands:

– Export destinations likely to become more similar in terms of engine

– requirements

– Substantially different engine requirements will be supplied from emerging

– market locations – streamlining of engine range in factories

Copyright © 2008 Global Insight, Inc. 27

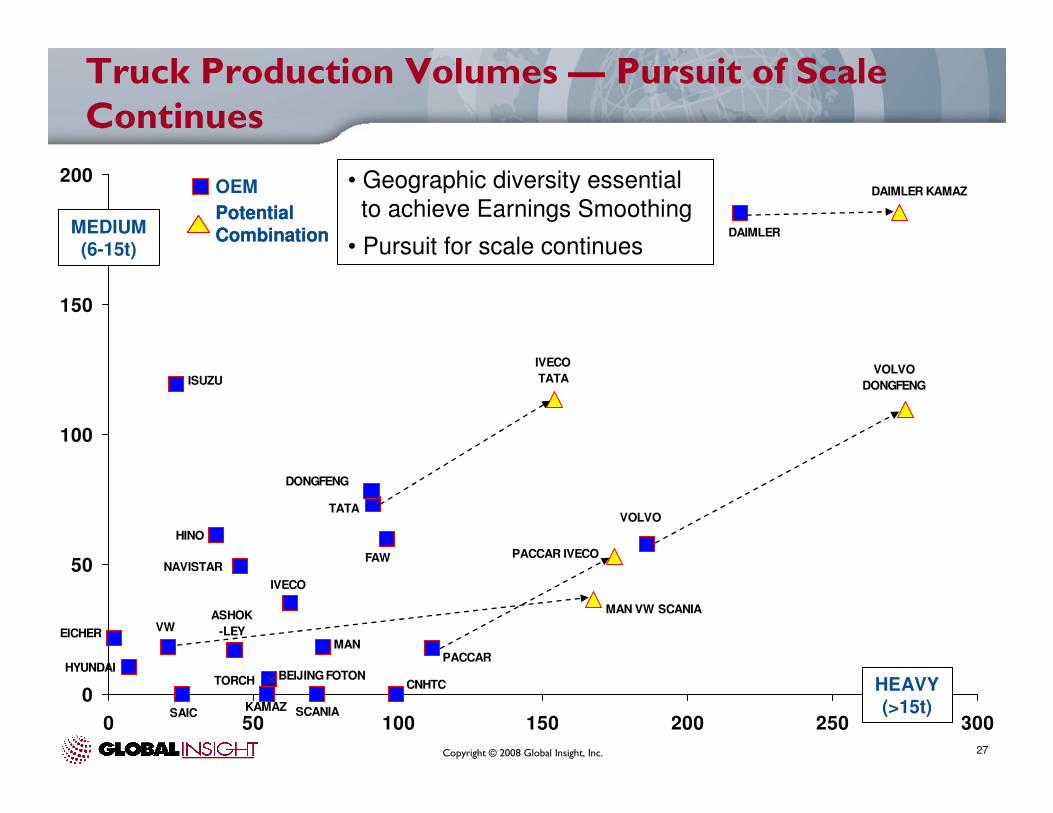

Truck Production Volumes — Pursuit of Scale Continues

DAIMLER

MAN

SCANIA

NAVISTAR

IVECO

HINO

ISUZU

PACCAR

DONGFENG

FAW

TATA

ASHOK

-LEYEICHERVW

MAN VW SCANIA

PACCAR IVECO

VOLVO

DONGFENG

CNHTCBEIJING FOTON

HYUNDAI

SAIC

IVECO

TATA

VOLVO

KAMAZ

TORCH

DAIMLER KAMAZ

0

50

100

150

200

0 50 100 150 200 250 300

• Geographic diversity essential

to achieve Earnings Smoothing

• Pursuit for scale continuesMEDIUM (6-15t)

HEAVY (>15t)

OEM

Potential Combination

OEM

Potential Combination

Copyright © 2008 Global Insight, Inc. 28

• European OEMs are dominating global engine developments—due to strong global presence, introduce domestic standards elsewhere

• More co-operations between manufacturers on the engine level likely to cope with rising costs

• Hunger for more powerful trucks continues—especially in heavy, but also in medium trucks

• Hard times for external engine suppliers, especially as U.S. market changes; “European Model” now dominating

Conclusions

Thank You!

Roman MathyssekSenior Truck Analyst & Advisor

Presentations are available for download at:www.globalinsight.com/events/GAC2008Paris