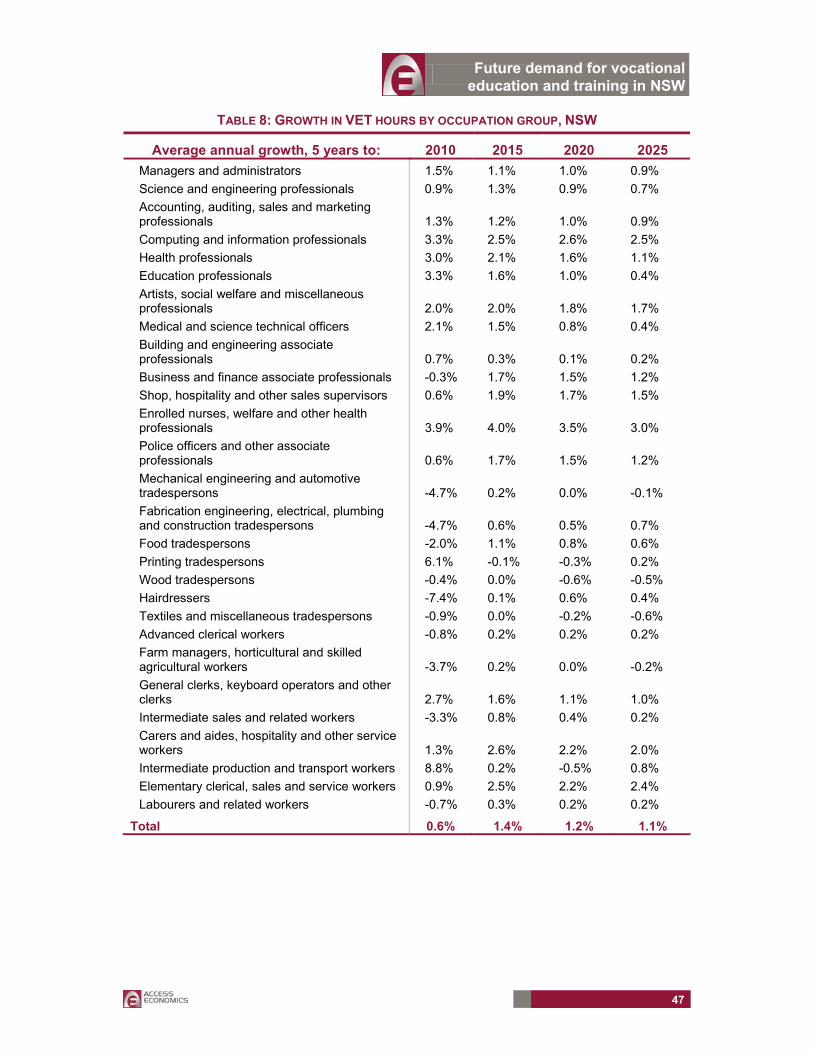

Embed Size (px)

Citation preview

FUTURE DEMAND FOR VOCATIONAL EDUCATION

AND TRAINING IN NEW SOUTH WALES

REPORT BY ACCESS ECONOMICS PTY LIMITED

FOR

THE INDEPENDENT PRICING AND REGULATORY TRIBUNAL (IPART)

16 JUNE 2006

While every effort has been made to ensure the accuracy of this document, the uncertain nature of economic data, forecasting and analysis means that Access Economics Pty Limited is unable to make any warranties in relation to the information contained herein. Access Economics Pty Limited, its employees and agents disclaim liability for any loss or damage which may arise as a consequence of any person relying on the information contained in this document.

Future demand for vocational education and training in NSW

TABLE OF CONTENTS

EXECUTIVE SUMMARY i 1. Introduction 1

1.1 Scope of this report...............................................................................................................1 1.2 Summary of methodology .....................................................................................................2

2. The benefits of skill development 6 2.1 Links between education and work .......................................................................................6 2.2 The effect of education on participation rates .......................................................................9 2.3 The effect of education on unemployment ..........................................................................10

3. Profile of VET activity 12 3.1 Total VET activity................................................................................................................12 3.2 VET activity by category .....................................................................................................15 3.3 Qualifications profile ...........................................................................................................17

4. Baseline scenario – labour market projections 20 4.1 Employment growth ............................................................................................................20 4.2 Labour force participation ...................................................................................................21 4.3 Industry employment forecasts ...........................................................................................23 4.4 Occupational employment forecasts ...................................................................................25 4.5 Regional dimension ............................................................................................................28

5. Additional labour market influences on future training needs 32 5.1 Retirements ........................................................................................................................32 5.2 Other staff turnover.............................................................................................................34 5.3 Part-time share of the workforce.........................................................................................36 5.4 Casual and self employed share of the workforce ..............................................................37 5.5 Productivity .........................................................................................................................39 5.6 Workforce longevity ............................................................................................................39 5.7 Supply side influences on VET activity ...............................................................................39

6. Baseline scenario – projected VET activity 41 7. Specifying the target scenario 48

7.1 Labour market projections ..................................................................................................48 7.2 Additional assumptions on training .....................................................................................52

8. Target scenario – projected VET activity 56 8.1 Scenario results ..................................................................................................................56 8.2 Plausibility of the target scenario ........................................................................................65

9. References 70

Future demand for vocational education and training in NSW

i

EXECUTIVE SUMMARY The Independent Pricing and Regulatory Tribunal (IPART) in New South Wales has commissioned Access Economics to develop projections of the future demand for publicly funded vocational education and training (VET).

Benefits of skill development

Our living standards per head are a function of the effectiveness with which we work (productivity) and the proportion of us working (participation).

Importantly, improved skills development (such as via VET studies to improve work skills) can do both of these. As economists have increasingly noted, not merely does increased investment in skills show up as more productive workers, those workers also tend to stay in the workforce for longer – thereby boosting participation as well as productivity. And, equally importantly, early moves to increase skills development are likely to have their prime years of payoff across the decades when growth will be most at risk from baby boomer retirement.

Profile of VET activity

VET activity ramped up notably in the 1990s in New South Wales, but since 2000 student numbers and the number of hours delivered has levelled off. That decline has been more notable in New South Wales than nationally. In 2004, VET students in New South Wales amounted to 16.3% of total people employed, a participation rate just below the national average.

In part, the recent decline in VET participation reflects a petering out of supply side initiatives which were encouraging greater participation in VET in the 1990s. Other factors here are that (1) productivity growth has also slowed (thereby slowing the need for up-skilling, by slowing the pace of change), (2) higher student fees and until relatively recently, (3) a strong job market negated some short term training needs by offering attractive short term returns to working versus training.

Baseline scenario – labour market projections

Employment growth in Australia is expected to slow notably from recent rates, not only for cyclical reasons, but as a key symptom of our ageing population. In particular, the retirement of the baby boomers is likely to see average labour force participation drop over time.

Over the 20 year forecast period here (2005 to 2025), average growth in jobs is projected at:

0.64% per annum for New South Wales; and

0.87% per annum for Australia.

Those projections are based on an only modest further increase in age cohort labour force participation rates, and with an unemployment rate staying roughly constant at around 5.0%.

While net employment growth trends are a key influence, the gross number of people entering an occupation (including to replace those who retire, or leave for some other reason – normal turnover), may be more important in addressing training requirements. These are accounted for here in the projections for future VET in this report.

Future demand for vocational education and training in NSW

ii

A continuing trend towards a higher share of the workforce working part-time or being casually employed or self-employed is also likely to be a plus for VET demand, as it means that more people have to be trained for any given amount of work for part-time, and because casual employees may receive less on-the job-training (and so may be more likely to seek out the publicly-funded VET training considered here).

Finally, increased workforce longevity as age cohort labour force participation rates rise will also provide a stimulus to VET demand in both the baseline and target scenarios.

Baseline scenario – projected VET activity

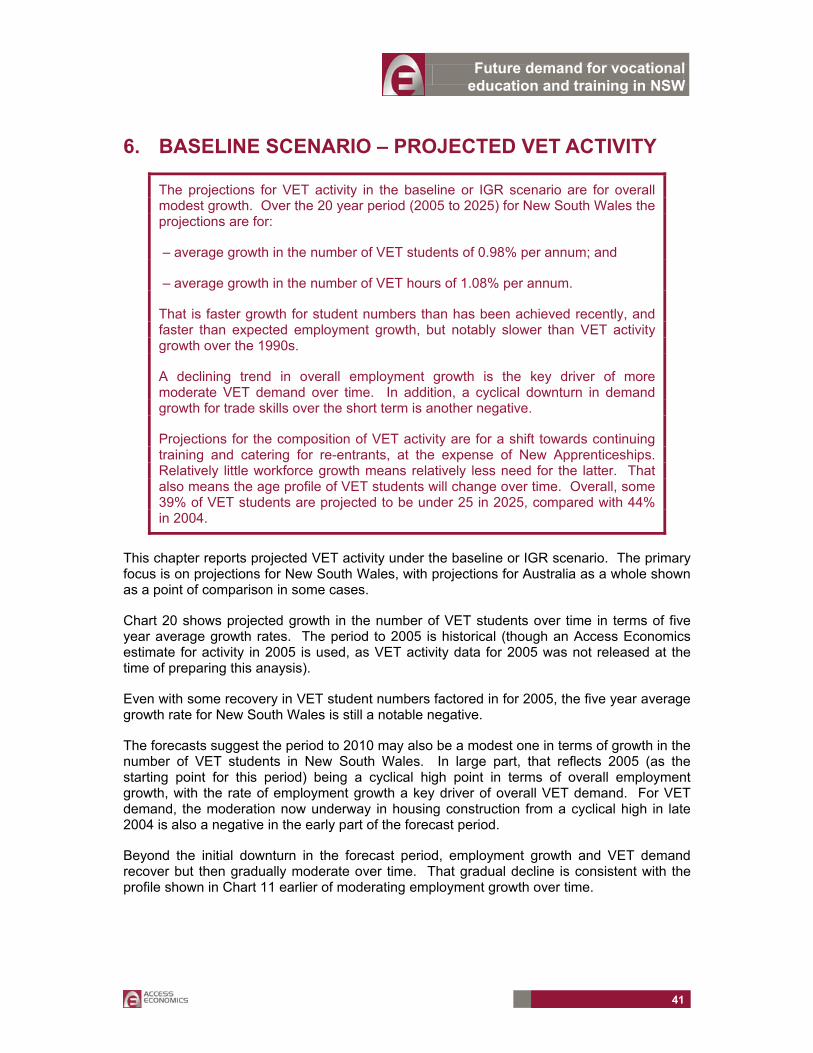

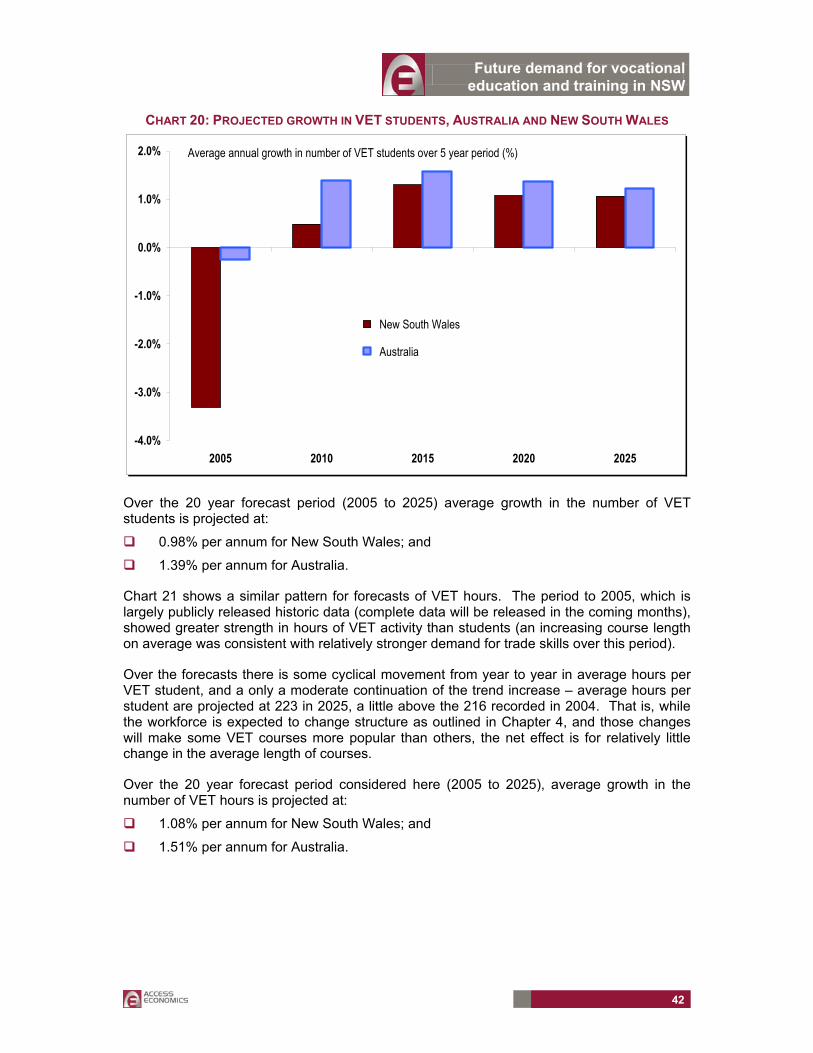

The projections for VET activity in the baseline scenario are for overall modest growth. Over the 20 year period (2005 to 2025) for New South Wales projections are for:

average growth in the number of VET students of 0.98% per annum; and

average growth in the number of VET hours of 1.08% per annum.

That is faster growth for student numbers than has been achieved recently, and faster than projected employment growth, but notably slower than VET activity growth over the 1990s.

Slowing overall job growth is the key driver of more moderate VET demand over time. In addition, a cyclical downturn in demand for trade skills is a negative over the short term.

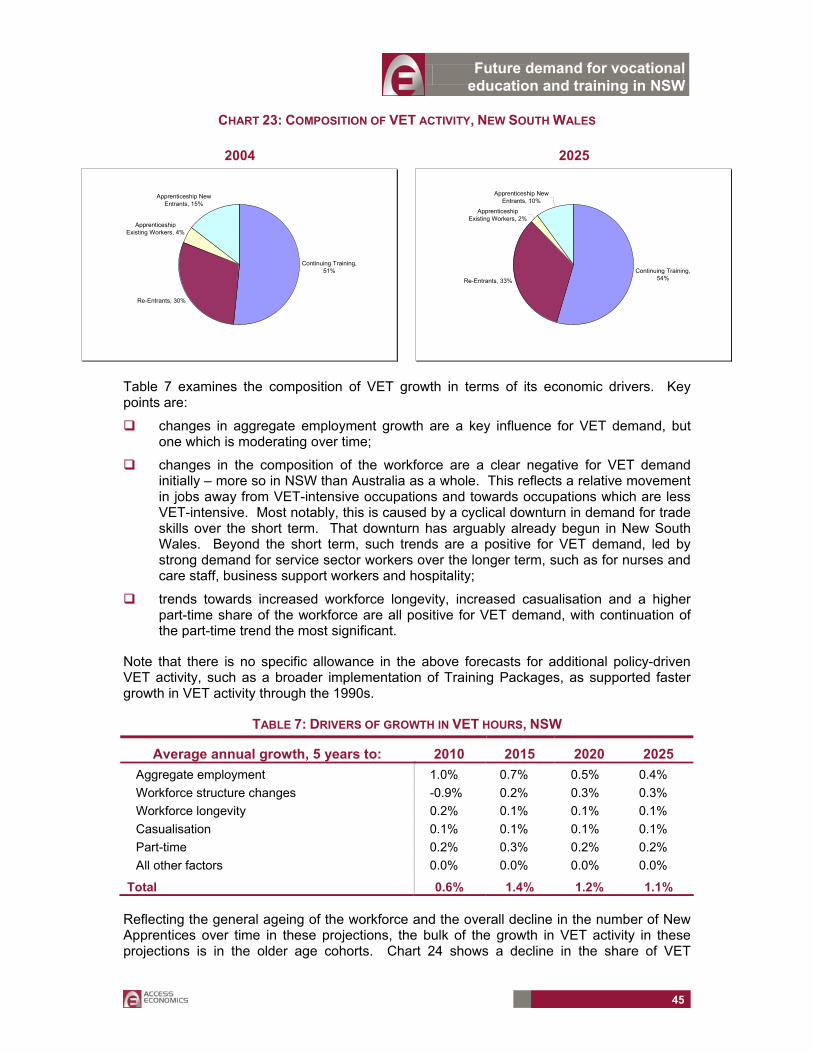

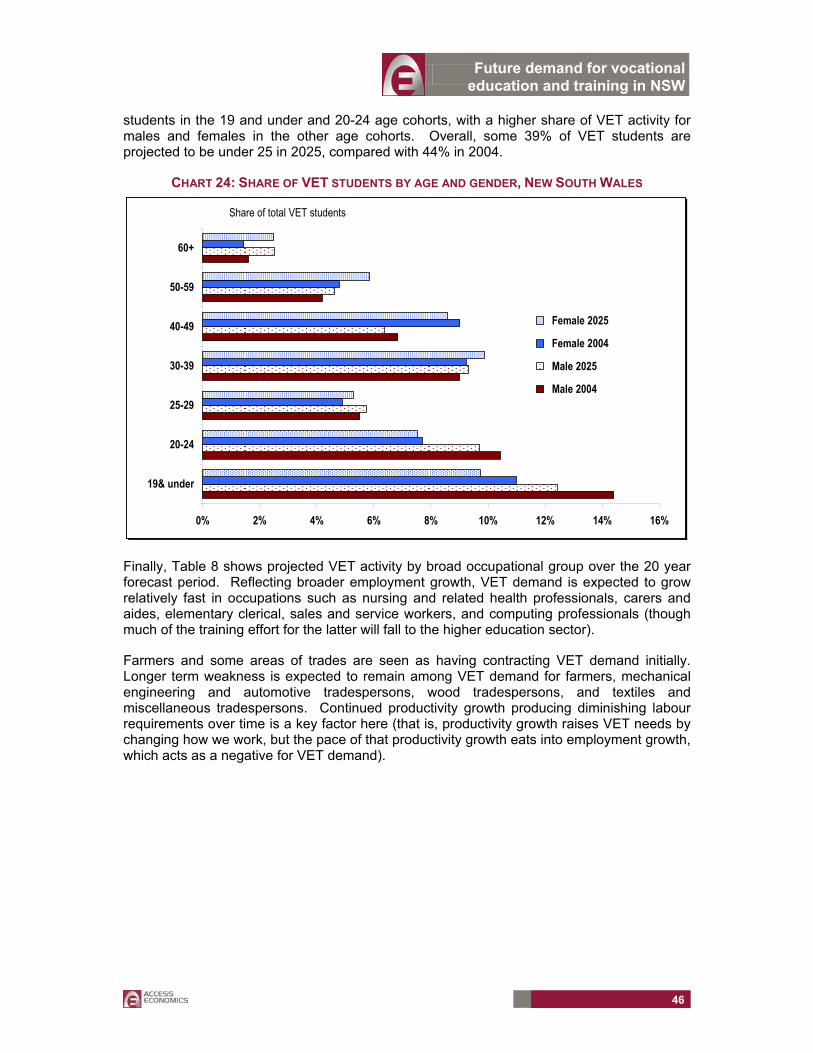

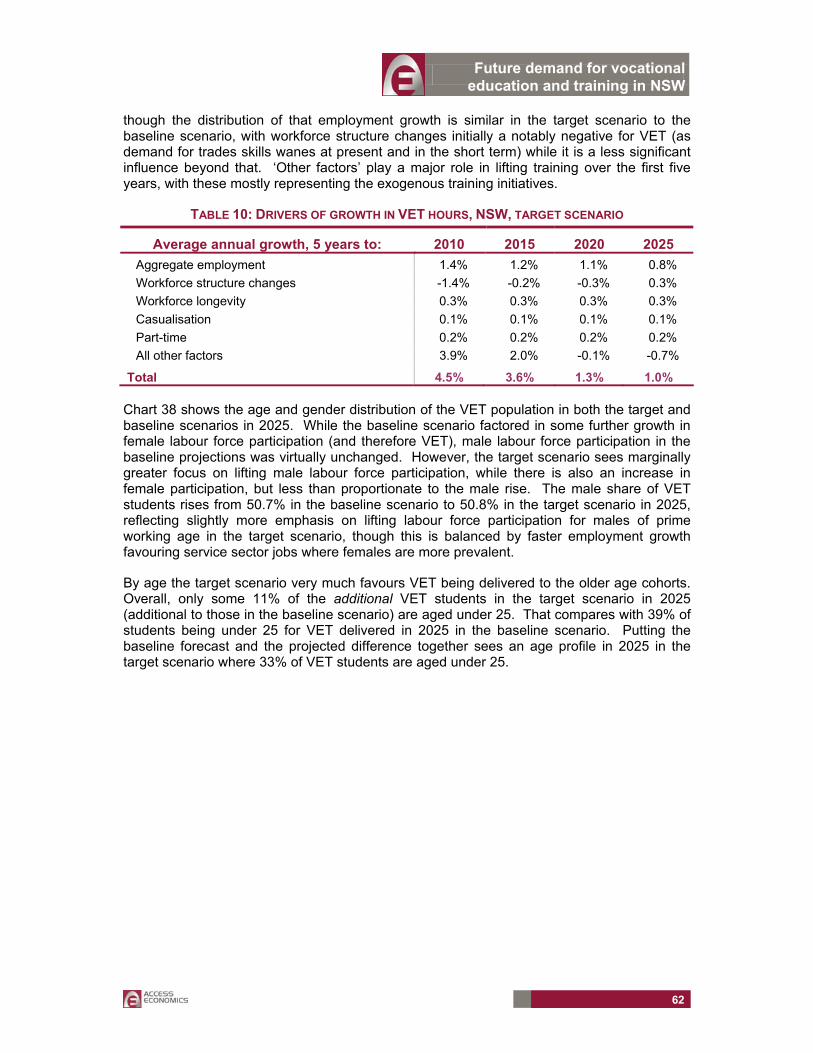

Projections for the composition of VET activity are for a shift towards continuing training and catering for re-entrants, at the expense of New Apprenticeships. Relatively little workforce growth means relatively less need for the latter. It also means that the skewing of the VET age profile towards younger students (44% of students in 2004 were under 25) will become less acute over time (only 39% of students under 25 in 2025).

Specifying the target scenario

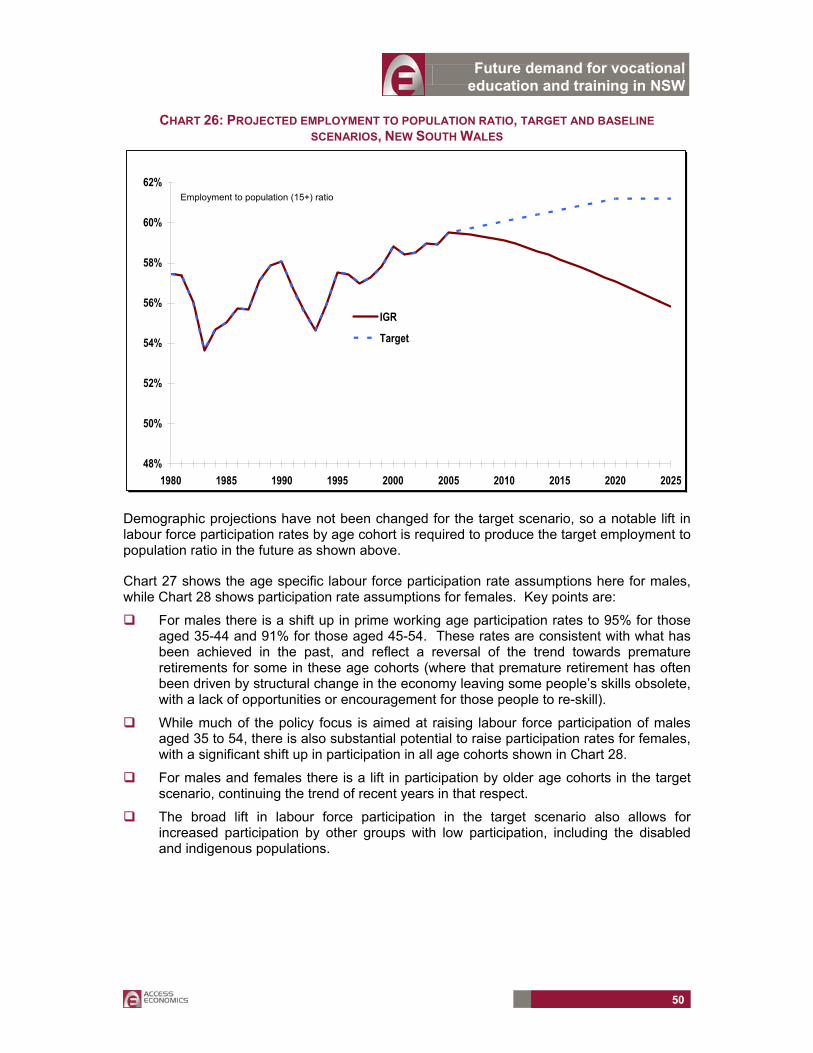

The baseline projections in this report can be compared with VET demand under a ‘target’ scenario. The target scenario is one of economic success. It is defined using the ratio of employed to civilian (15+) population. For Australia that means maintaining the recent level for that ratio, rather than seeing it fall as the population ages. For New South Wales it means moving up to the Australian ratio of employed to civilian population and then maintaining that ratio. As population growth assumptions are the same in the target scenario as in the baseline scenario, these targets are achieved through employment gains, with a substantial lift in labour force participation rates by age cohort required.

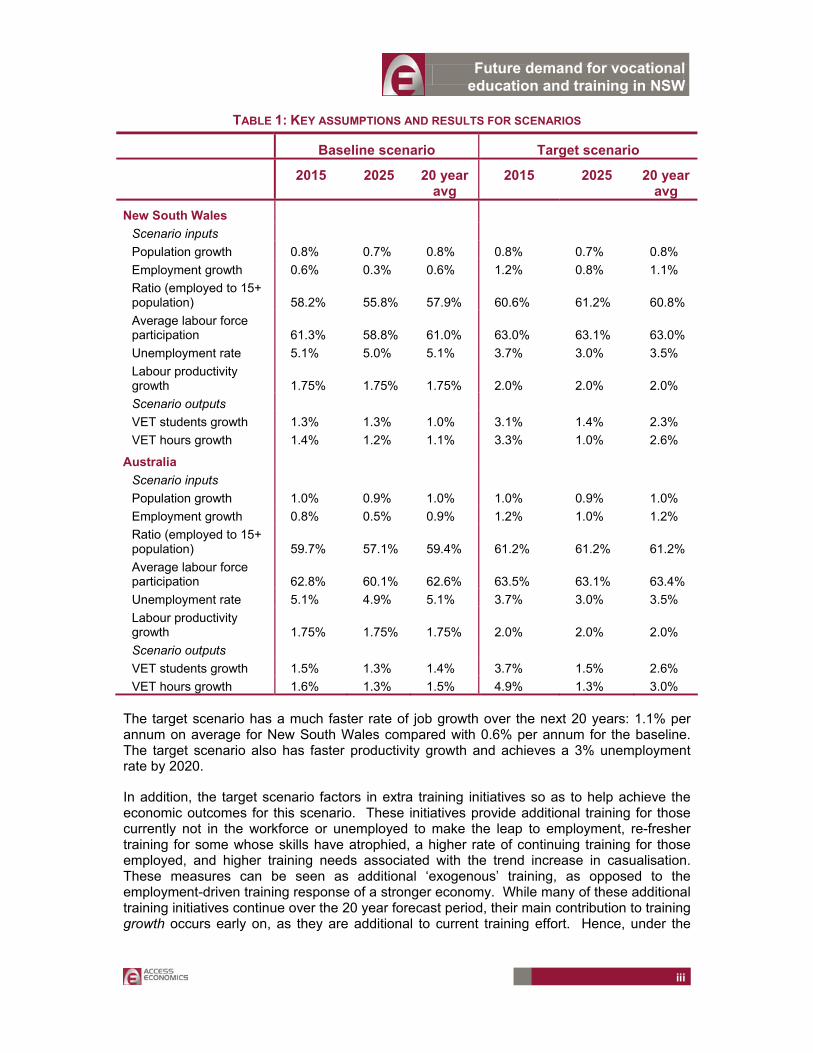

Key assumptions and outputs for the baseline and target scenarios are noted in Table 1.

Future demand for vocational education and training in NSW

iii

TABLE 1: KEY ASSUMPTIONS AND RESULTS FOR SCENARIOS

Baseline scenario Target scenario

2015 2025 20 year avg

2015 2025 20 year avg

New South Wales Scenario inputs Population growth 0.8% 0.7% 0.8% 0.8% 0.7% 0.8% Employment growth 0.6% 0.3% 0.6% 1.2% 0.8% 1.1% Ratio (employed to 15+ population) 58.2% 55.8% 57.9% 60.6% 61.2% 60.8% Average labour force participation 61.3% 58.8% 61.0% 63.0% 63.1% 63.0% Unemployment rate 5.1% 5.0% 5.1% 3.7% 3.0% 3.5% Labour productivity growth 1.75% 1.75% 1.75% 2.0% 2.0% 2.0% Scenario outputs VET students growth 1.3% 1.3% 1.0% 3.1% 1.4% 2.3% VET hours growth 1.4% 1.2% 1.1% 3.3% 1.0% 2.6%

Australia Scenario inputs Population growth 1.0% 0.9% 1.0% 1.0% 0.9% 1.0% Employment growth 0.8% 0.5% 0.9% 1.2% 1.0% 1.2% Ratio (employed to 15+ population) 59.7% 57.1% 59.4% 61.2% 61.2% 61.2% Average labour force participation 62.8% 60.1% 62.6% 63.5% 63.1% 63.4% Unemployment rate 5.1% 4.9% 5.1% 3.7% 3.0% 3.5% Labour productivity growth 1.75% 1.75% 1.75% 2.0% 2.0% 2.0% Scenario outputs VET students growth 1.5% 1.3% 1.4% 3.7% 1.5% 2.6% VET hours growth 1.6% 1.3% 1.5% 4.9% 1.3% 3.0%

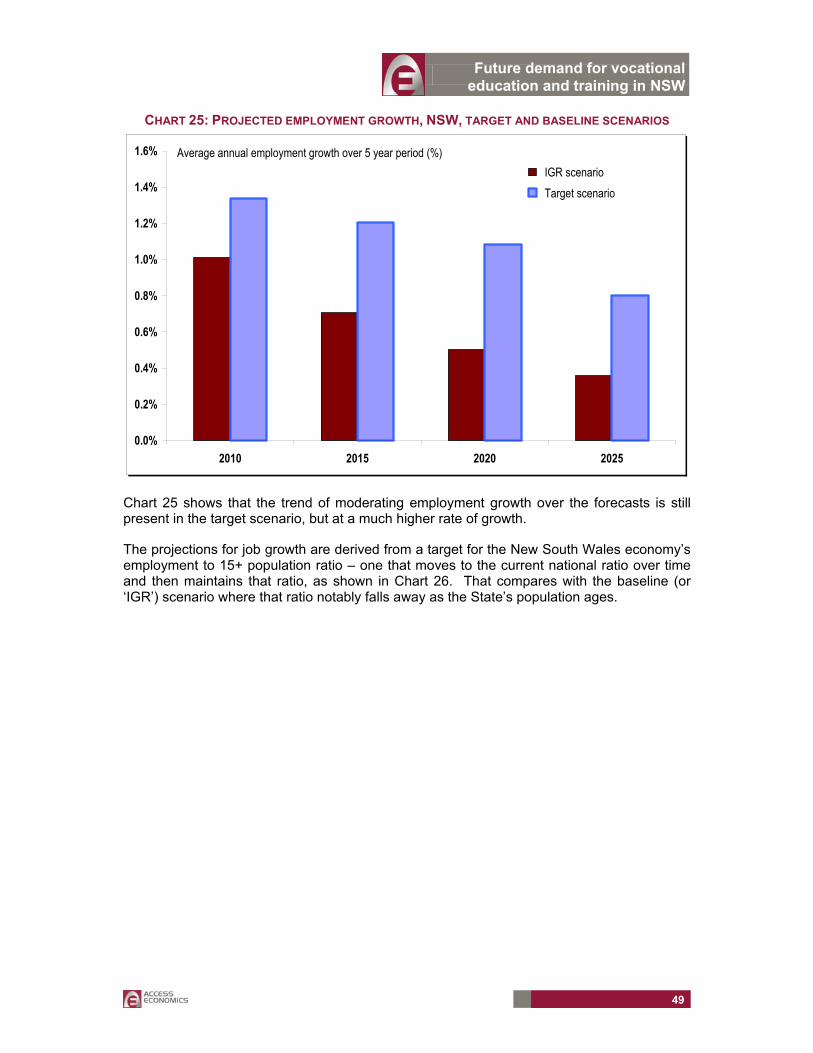

The target scenario has a much faster rate of job growth over the next 20 years: 1.1% per annum on average for New South Wales compared with 0.6% per annum for the baseline. The target scenario also has faster productivity growth and achieves a 3% unemployment rate by 2020.

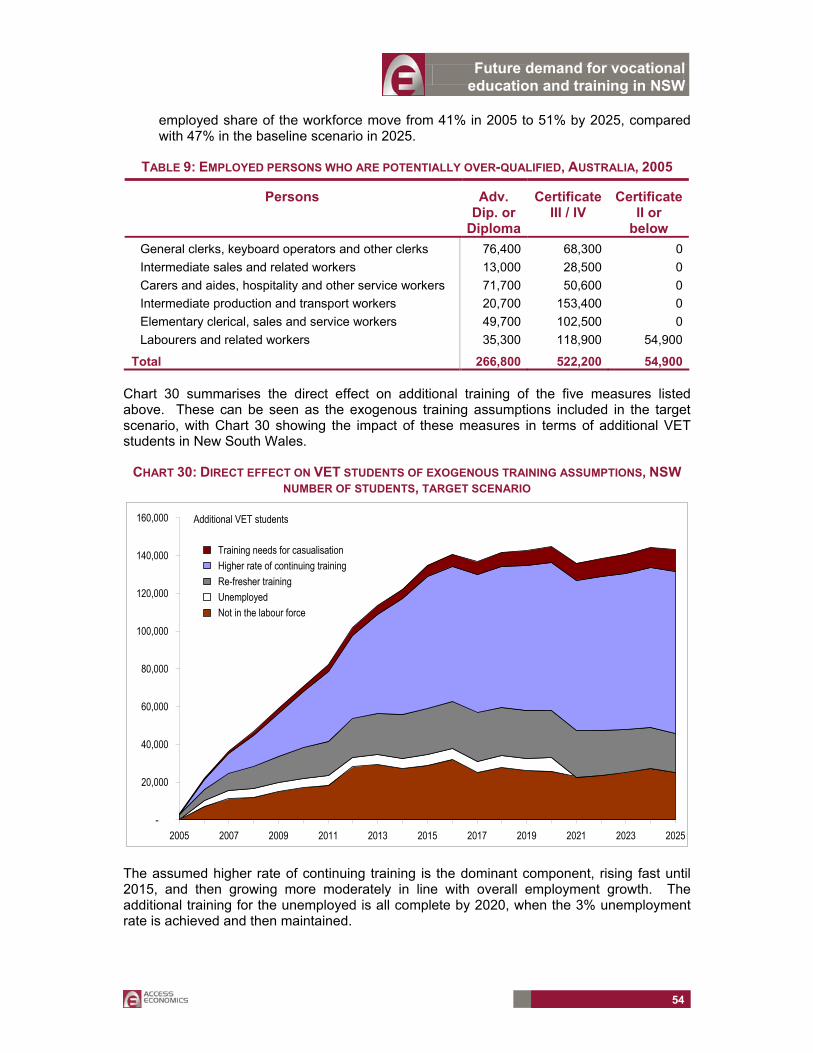

In addition, the target scenario factors in extra training initiatives so as to help achieve the economic outcomes for this scenario. These initiatives provide additional training for those currently not in the workforce or unemployed to make the leap to employment, re-fresher training for some whose skills have atrophied, a higher rate of continuing training for those employed, and higher training needs associated with the trend increase in casualisation. These measures can be seen as additional ‘exogenous’ training, as opposed to the employment-driven training response of a stronger economy. While many of these additional training initiatives continue over the 20 year forecast period, their main contribution to training growth occurs early on, as they are additional to current training effort. Hence, under the

Future demand for vocational education and training in NSW

iv

target scenario, growth in training requirements is faster earlier on, and therefore average VET growth rates over 20 years shown in Table 1 are stronger than those shown for 2025.

Increased VET is seen as a necessary (but far from sufficient) condition to achieve the target scenario – increased skills development is likely to be an important contributing factor to such economic success, but Australia will also need to do well otherwise in terms of policy issues and business performance to achieve the target.

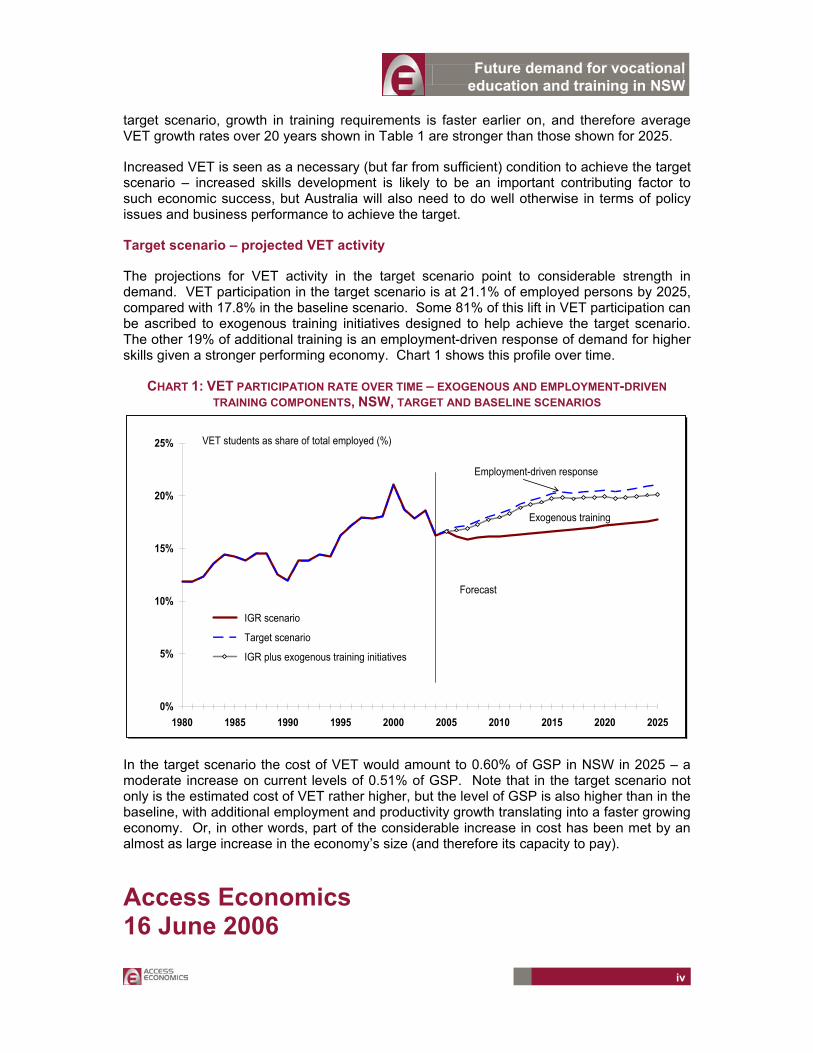

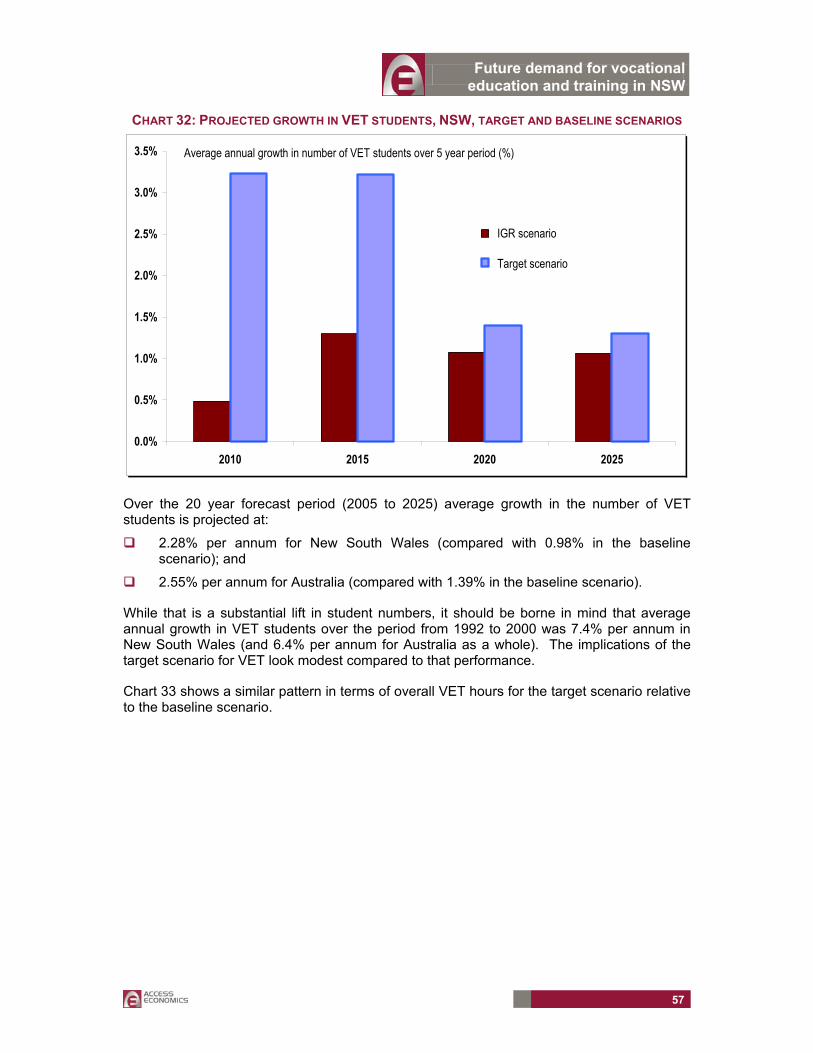

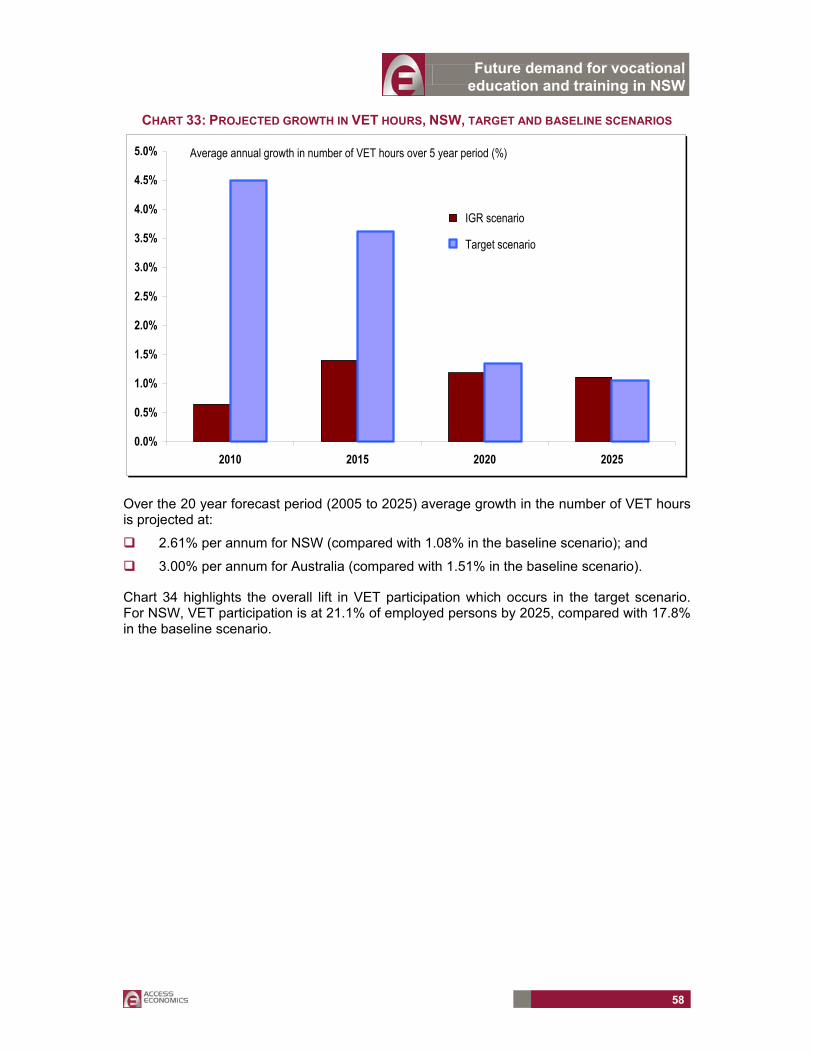

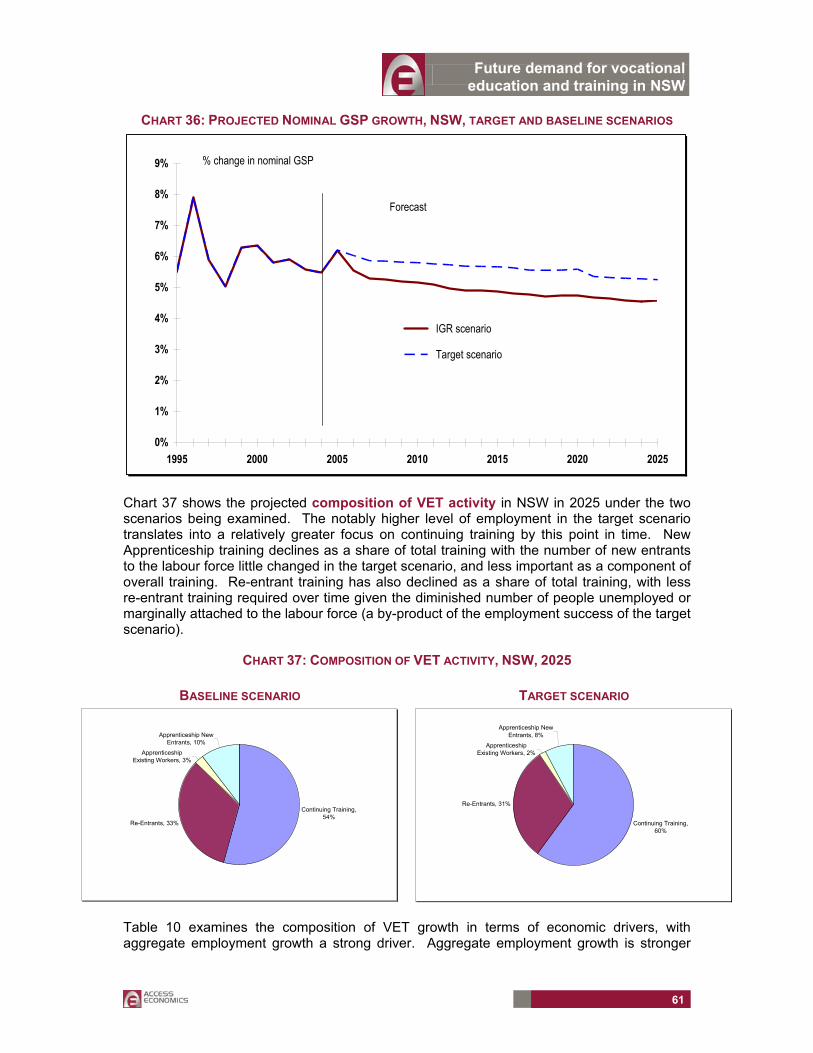

Target scenario – projected VET activity

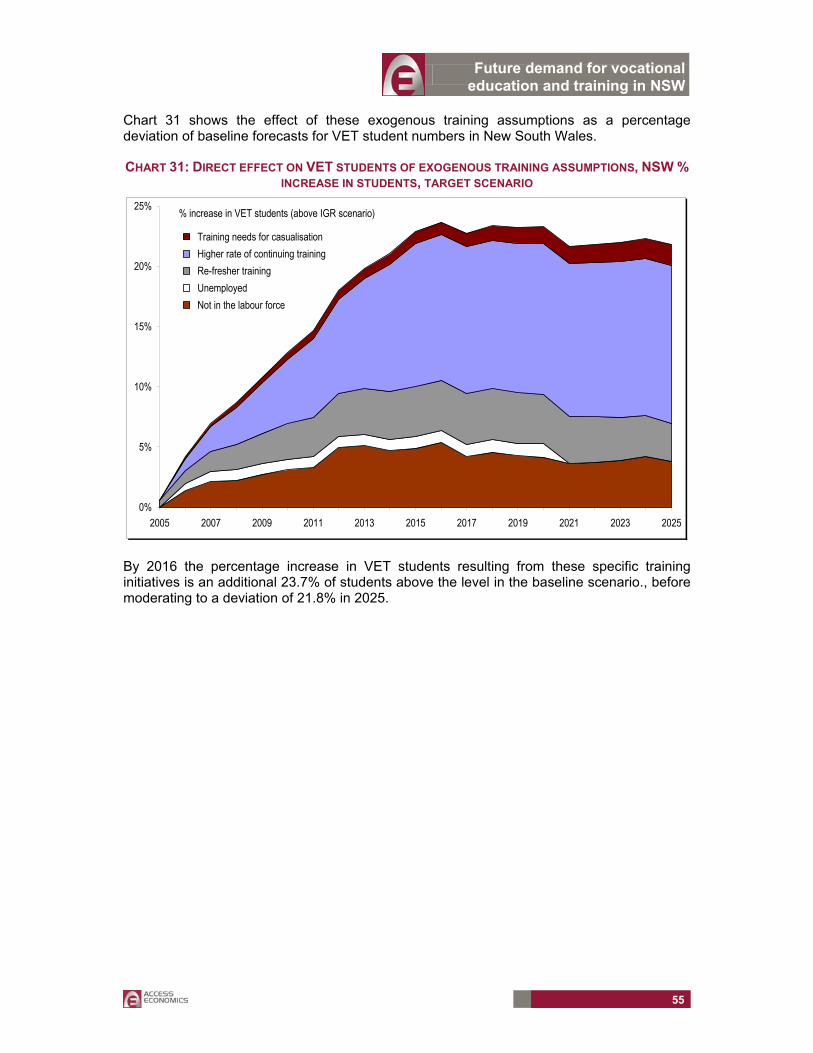

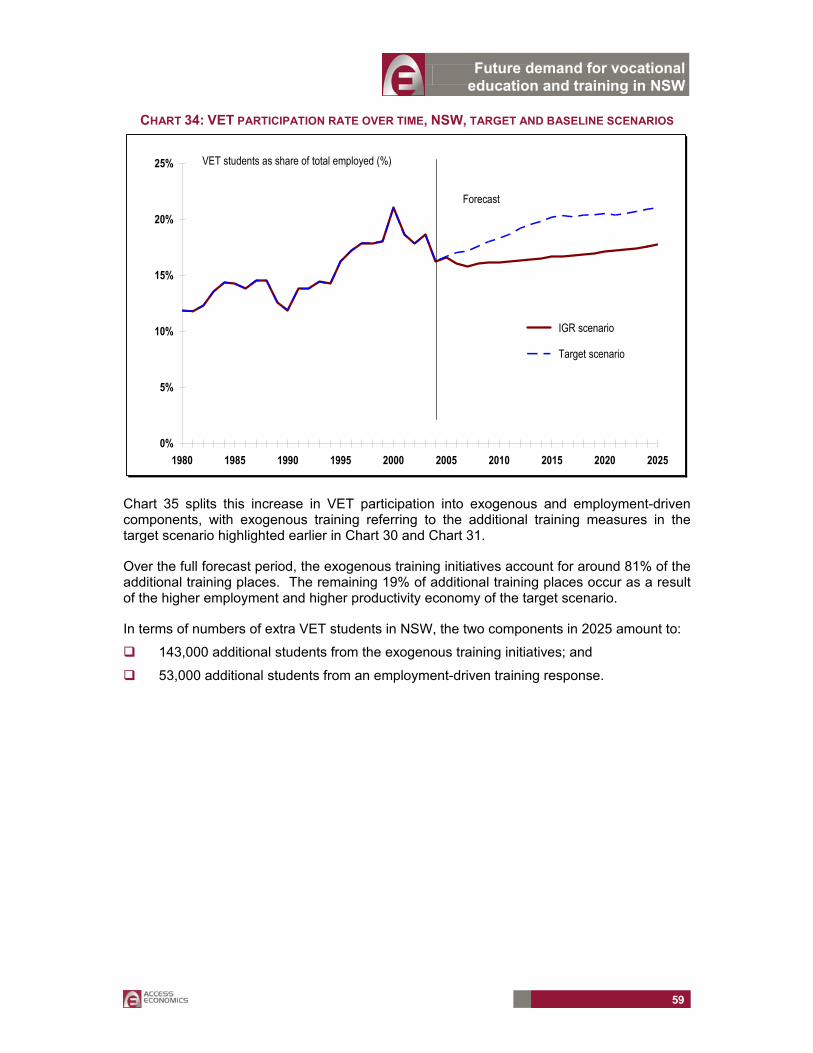

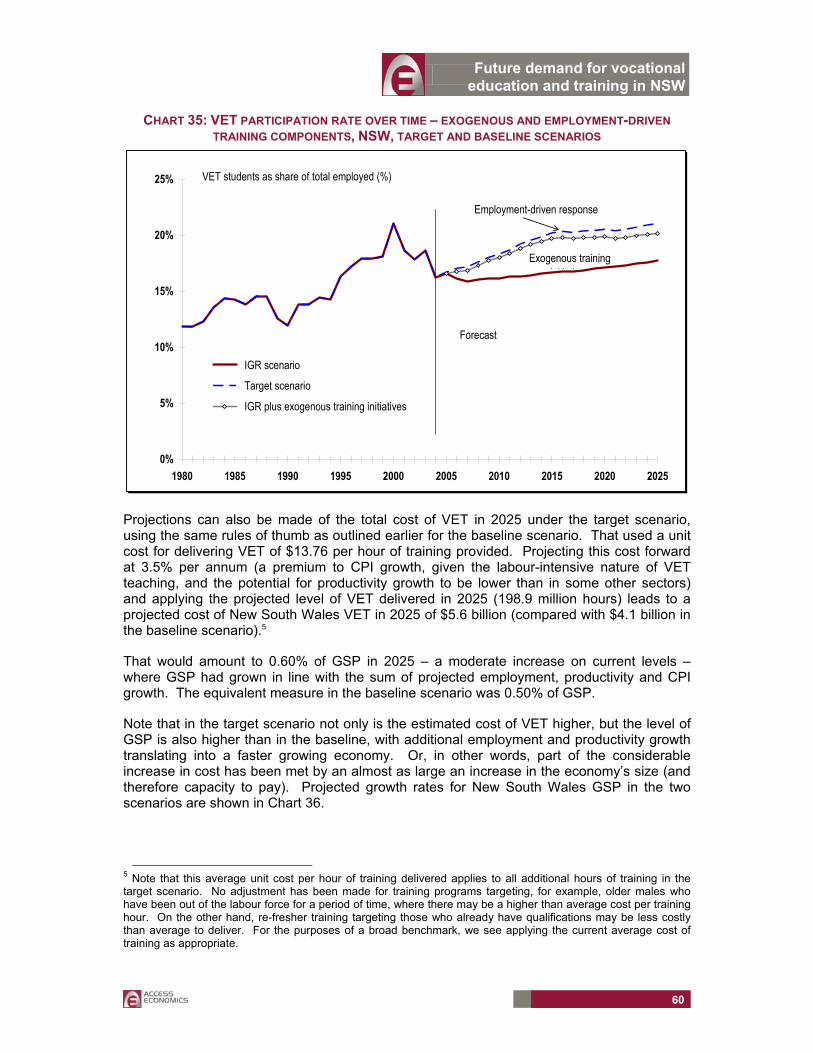

The projections for VET activity in the target scenario point to considerable strength in demand. VET participation in the target scenario is at 21.1% of employed persons by 2025, compared with 17.8% in the baseline scenario. Some 81% of this lift in VET participation can be ascribed to exogenous training initiatives designed to help achieve the target scenario. The other 19% of additional training is an employment-driven response of demand for higher skills given a stronger performing economy. Chart 1 shows this profile over time.

CHART 1: VET PARTICIPATION RATE OVER TIME – EXOGENOUS AND EMPLOYMENT-DRIVEN TRAINING COMPONENTS, NSW, TARGET AND BASELINE SCENARIOS

0%

5%

10%

15%

20%

25%

1980 1985 1990 1995 2000 2005 2010 2015 2020 2025

IGR scenario

Target scenario

IGR plus exogenous training initiatives

VET students as share of total employed (%)

Forecast

Exogenous training i iti ti

Employment-driven response

In the target scenario the cost of VET would amount to 0.60% of GSP in NSW in 2025 – a moderate increase on current levels of 0.51% of GSP. Note that in the target scenario not only is the estimated cost of VET rather higher, but the level of GSP is also higher than in the baseline, with additional employment and productivity growth translating into a faster growing economy. Or, in other words, part of the considerable increase in cost has been met by an almost as large increase in the economy’s size (and therefore its capacity to pay).

Access Economics 16 June 2006

Future demand for vocational education and training in NSW

1

1. INTRODUCTION The Independent Pricing and Regulatory Tribunal (IPART) in New South Wales has commissioned Access Economics to develop projections of the future demand for publicly funded vocational education and training (VET).

The projections of VET are from an employer or demand side perspective – the level of VET which is likely to be required to maintain and grow the skill base of the available workforce.

Access Economics has previously developed a framework for forecasting VET demand based on labour market analysis. This forecasting framework has been updated, critically examined, and improved for this project.

1.1 SCOPE OF THIS REPORT

This report presents projections for VET activity over the next 20 years for both New South Wales and Australia. The key interest is in identifying the skill needs associated with longer term trends, as opposed to a short term forecasting exercise. As a result, the presentation of VET projections in this report focuses on averages over the five year periods:

1 January 2006 to 31 December 2010;

1 January 2011 to 31 December 2015;

1 January 2016 to 31 December 2020; and

1 January 2021 to 31 December 2025.

Two scenarios are presented in this report:

a baseline or IGR scenario showing what employer demand will be if present policies are continued (with long term growth broadly consistent with that in the Federal Government’s 2002 Intergenerational Report); and

a target scenario showing what employer demand will be if policies succeed in raising participation so as to ensure there is no change in the ratio of aged persons to the employed population (this has been interpreted as no change in the ratio of the employed to the civilian (15+) population).

The key data projected for this report is total hours of training and number of students in training in the national provider collection by the National Centre for Vocational Education Research (NCVER).

This covers all VET delivered by providers in receipt of public funding allocations for VET. That is, any VET which is funded wholly or in part from public funds. Providers include TAFE, other government providers, community providers and private providers who have been allocated public funds to deliver VET programs.

VET which is fee for service by private providers is outside the scope of this data collection, as are ‘non-vocational’ programs, and VET delivered in schools where the delivery has been undertaken by schools.

This remainder of this report is organised as follows:

Future demand for vocational education and training in NSW

2

The following section provides an overview of the methodology employed in forecasting employer demand for VET.

Chapter 2 discusses some of the overall economic benefits which accrue from investment in skills development, drawing on recent research.

Chapter 3 provides a brief overview of VET activity growth over the past decade, in terms of students and hours, for New South Wales and Australia as a whole.

Chapter 4 details the labour market projections which underpin the VET demand forecast in the baseline scenario.

Chapter 5 discusses some additional labour market influences on training requirements, including rates of retirement and other turnover, and the possible implications of trends toward both a higher part-time share and a higher casual and self-employed share of the workforce.

Chapter 6 presents projected VET activity in the baseline scenario, including a split of these projections into new labour force entrants, re-entrants, and those undertaking continuing training.

Chapter 7 examines the implications for participation rates and other labour market variables which stem from the target scenario, along with assumed exogenous changes to training participation to help enable the lift in labour force participation.

Chapter 8 reports the implications for skills development under the target scenario, including projections for overall VET activity.

The report is also accompanied by spreadsheet models which provide greater detail on the forecasts, and which also allow IPART to conduct some further sensitivity analysis on the forecasts.

1.2 SUMMARY OF METHODOLOGY

Projections for publicly funded VET activity in this report respond through various different channels to the skill requirements demanded by employers. The same structure is followed for national projections and for those for New South Wales. An overview of the VET forecasting framework follows:

Forecasts for key macro variables are obtained from the Access Economics Macro (AEM) model, a small, dynamic model of the Australian economy, regularly used for macroeconomic forecasts. These key macro variables include components of final demand (such as categories of private consumption and investment) and total employment.

For the baseline or IGR scenario, the projection for total employment is scaled to be broadly consistent with IGR projections on labour force participation rates – with participation rates by age cohort rising gradually over time, but with the economy-wide average participation rate falling as the population ages.

Growth in employment by industry (for 55 industries) is forecast using known relationships between components of final demand and industry employment (based on 1996-97 input-output data, the latest available). For example, if the investment forecasts suggest that residential and construction are gaining strength, then the construction industry will gain strength. Or, say, if rural exports are lifting, then the farm sector is similarly seen lifting.

A counterfactual estimation is conducted on historical data to determine actual employment growth not picked up by this methodology, for example due to changes in

Future demand for vocational education and training in NSW

3

worker productivity and structural changes in the economy. Corresponding adjustments are made to the forecasts. The modelling also allows for some adjustment to be made to the early forecast periods to allow for any jumping-off problems.

Forecasts for industry employment are translated into occupational employment forecasts (for 81 occupations) using 2001 Census data which shows the occupational employment share for each of the industry groups examined. For forecasts, these shares are allowed to change over time, with the change in shares between the 1996 and 2001 Censuses used as a guide.

That framework provides the net employment change demanded by occupation over time.

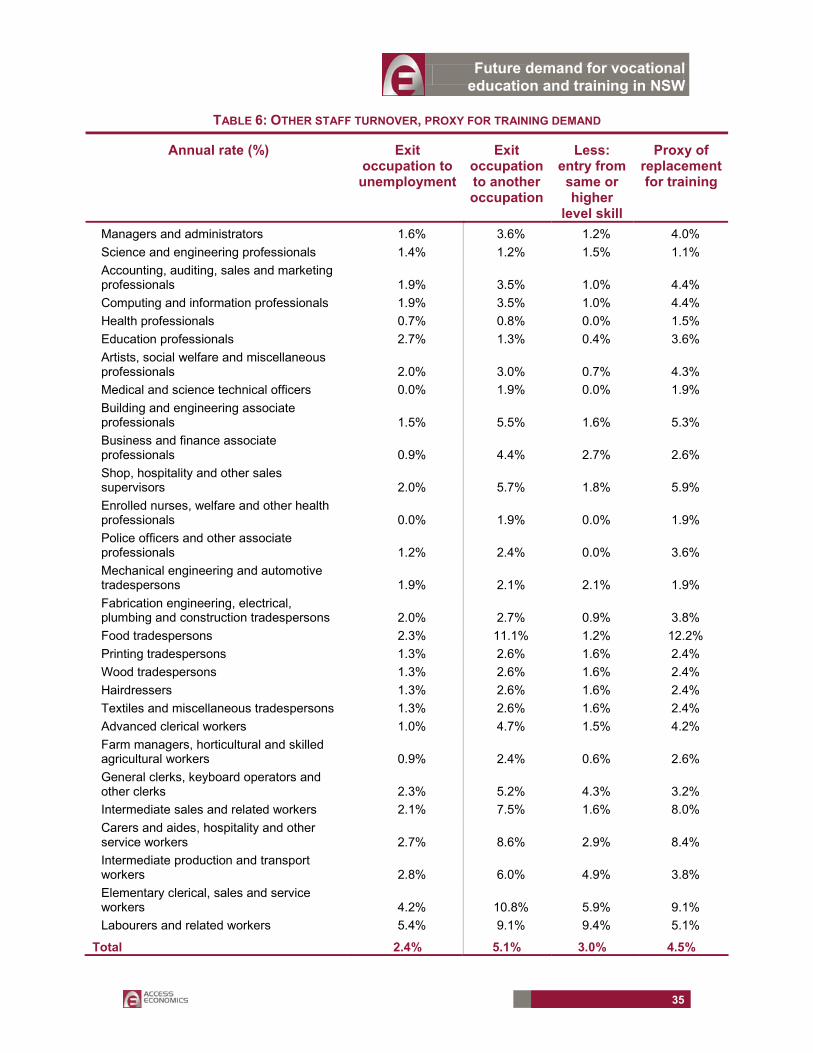

This net change is translated into the gross number of people entering an occupation by allowing for projections of retirements and normal turnover. National workforce participation rates by age and Census data of observed retirements by age are used to estimate the rate of retirement for each occupation, while data from the labour mobility survey allows an estimate of normal turnover (not relating to new workforce entry or retirement) by occupation.

The key outputs from this framework are forecasts by occupation (for 81 occupations) of the level of employment and the number of people entering an occupation, year by year. These outputs are used as a link to measures of VET, allowing projected workforce developments to exert a strong and consistent influence over forecasts of demand for VET.

VET activity by occupation (in terms of both hours and number of students) from the national provider collection is split into four components, each with its own set of VET demand drivers for the forecasts:

New Apprenticeships for new entrants: Formal training associated with New Apprenticeships being undertaken by new entrants to the workforce.

New Apprenticeships for existing workers: Formal training associated with New Apprenticeships being undertaken by existing workers.

Re-entrants: Re-entry training – VET undertaken by those unemployed or not in the workforce.

Continuing training: The balance, undertaken by people currently employed (which includes some recent labour market entrants who are currently employed and not captured through the New Apprenticeships program).

The formal training associated with New Apprenticeships is isolated from total VET activity by using the number of enrolments in a contract of training, and hours of formal training per enrolment derived by the NCVER. This data was available for new entrants to the workforce and existing workers. Total hours for all apprentices and trainees in training were derived from historic relationships of numbers in-training to commencements (incorporating both the duration of programmes and cancellation/withdrawal rates).

VET ‘penetration ratios’ by occupation are derived by combining the measures of VET activity (hours and number of students each for New Apprenticeships for new entrants, New Apprenticeships for new workers, re-entrants and continuing training) as the numerator with the two key workforce measures (employment levels by occupation and number of people entering by occupation) as the denominator.

For the forecasts, the default assumption is to hold penetration ratios at their average ratio over the past three years. The most recent ratio is used where there appears to have been a trend in VET participation up or down.

Future demand for vocational education and training in NSW

4

A portion of VET activity cannot be classified to a specific occupational category, but is instead listed as various categories of ‘general’ training. These categories of activity are projected forwards on the basis of employment in broader occupational groups or total employment.

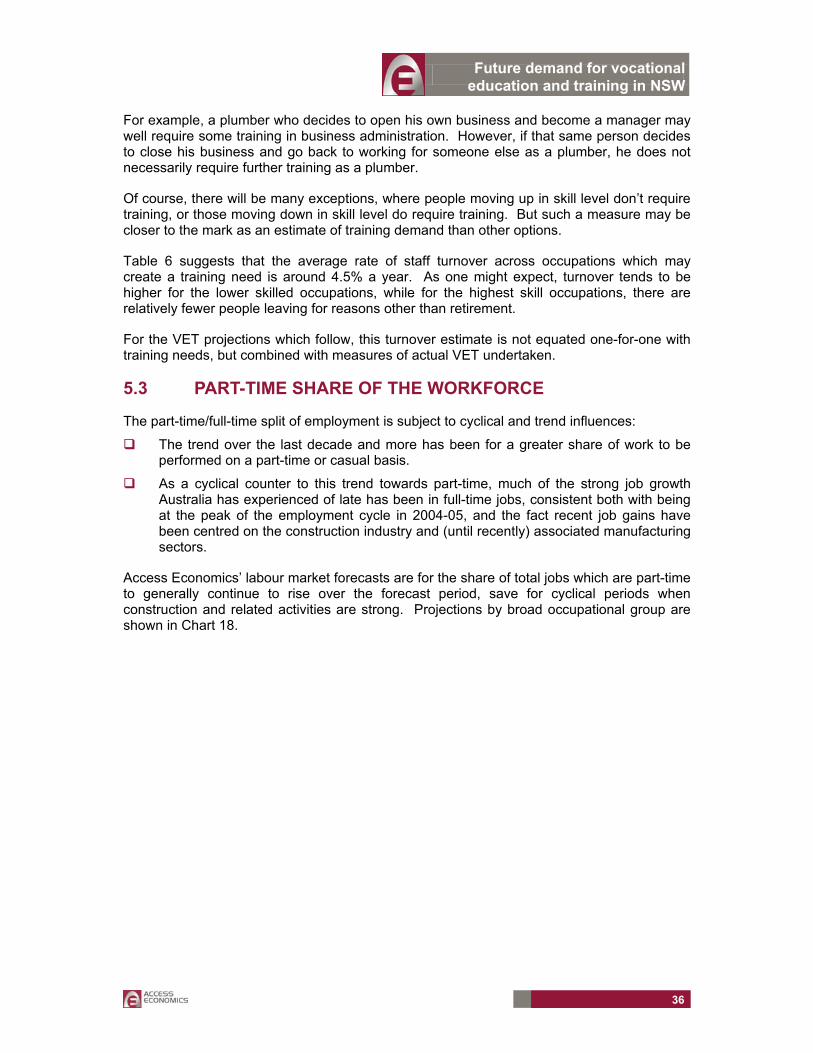

Allowance is made for a continuing trend towards part-time work (estimated from examining past trends by broad occupational group). This raises VET demand as more people, and therefore more skills, are required to perform a given number of hours of work than previously.

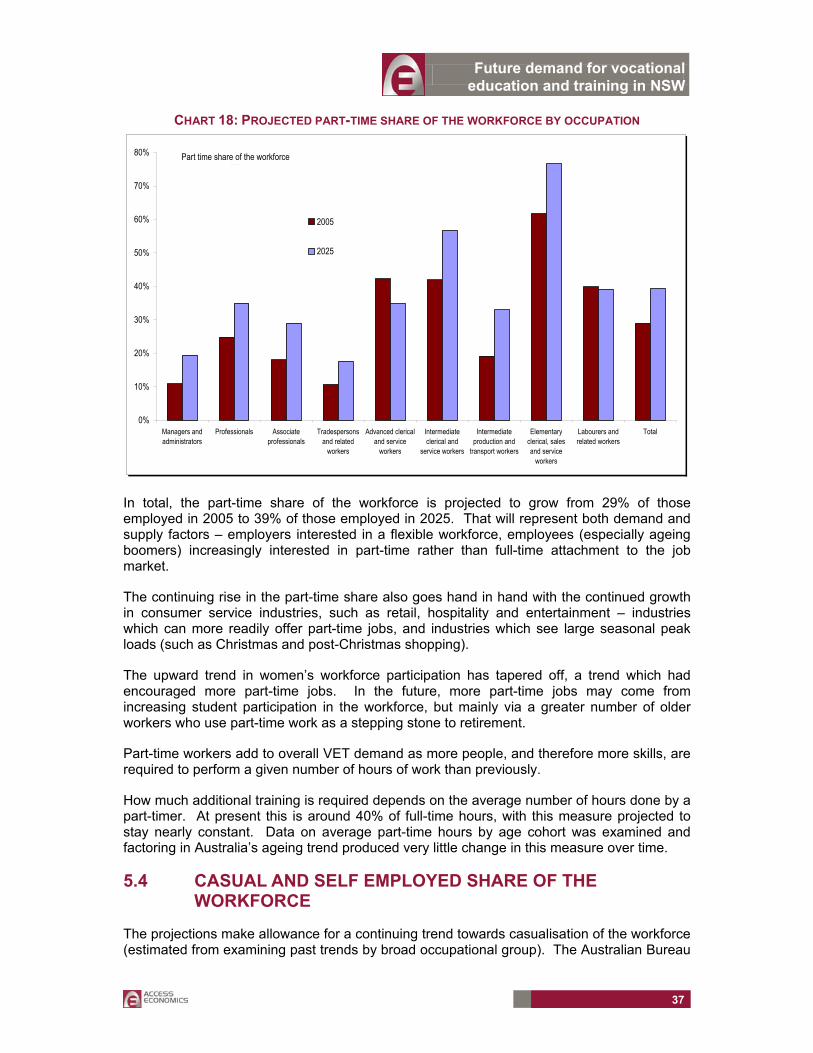

Allowance is made for a continuing trend towards casualisation of the workforce. (estimated from examining past trends of casual employment and self-employment by broad occupational group). This raises demand for publicly funded VET on the view that casual employees may receive less on-the-job training than permanent employees.

Allowance is made for employees to have a longer working life, on average, looking forward. As labour force participation increases among older age cohorts, so will the average working life, which implies some additional continuing training in order to keep skills relevant.

(Note that the baseline scenario has a lift in participation among older age cohorts, consistent with that in the Intergenerational Report. The target scenario increase is higher still.)

Allowance is made for movement to a higher rate of productivity growth to drive additional training needs. Note that only has an effect in the target scenario, as continuation of the same rate of productivity growth (as in the baseline scenario), is consistent with current rates of VET participation for up-skilling.

The model allows for future policy initiatives, such as broader implementation of Training Packages, though none have been specifically factored in to these scenarios.

Finally for the baseline scenario, projections for the various components of VET activity are collated to give a projection for total publicly funded VET demand over time, nationally and for New South Wales.

The target scenario is a scenario rather than a forecast. It uses a different series for the projected level of total employment over time. It is based on labour force participation rates by age cohort rising over time in order to keep the economy’s employment to 15+ population ratio constant (and to lift the ratio in New South Wales to that Australian target level). Changes to other broad economic parameters in this scenario include:

a higher rate of productivity growth (2% per annum rather than 1.75% per annum); and

a lower unemployment rate (down to 3% by 2020).

Projections under the target scenario follow the same set of steps as outlined above using the projected higher level of employment as a basis. In addition, a range of further initiatives are hypothesised to take place in the target scenario, which would help in producing the lift in labour force participation rates projected for this scenario. These training initiatives are:

additional training for those currently not in the labour force (in order to encourage them into the labour force);

additional training for those unemployed (to help move unemployment down to 3%);

additional (re-fresher) training for some people who have VET qualifications but are employed in occupations where they may not be fully utilising them;

Future demand for vocational education and training in NSW

5

a higher rate of continuing training for those employed (a preventative measure to maintain or upgrade the skills of existing workers to avoid premature retirements); and

a faster rate of casualisation of the workforce (with the additional people casually employed seen as having higher training needs).

Finally for the target scenario, using the standard forecast process and applying the initiatives noted above, projections for the various components of VET activity are collated to give a projection for total publicly funded VET demand over time, nationally and for New South Wales.

Future demand for vocational education and training in NSW

6

2. THE BENEFITS OF SKILL DEVELOPMENT

Australia’s living standards per head are a function of the effectiveness with which we work (productivity) and the proportion of us working (participation).

As the Federal Treasury’s Intergenerational Report noted in 2002, the coming decades of baby boomer retirement will see aggregate participation fall. Therefore Treasury and others have argued the need for policies which can help fill that shortfall by increasing either participation or productivity.

Importantly, improved skills developments (such as VET studies to improve work skills) can do both of these. As economists have increasingly noted, not merely does increased investment in skills show up as more productive workers, those workers also tend to stay in the workforce for longer – thereby boosting participation as well as productivity. And, equally importantly, early moves to increase skills development are likely to have their prime years of payoff across the decades when growth will be most at risk from baby boomer retirement.

This chapter sets out some of those linkages.

The ageing of the baby boomers will eat into economic growth, particularly through the years of maximum retirement from 2015-2030.

That point is made at length in Federal Treasury’s 2002 Intergenerational Report and the Productivity Commission’s 2005 Economic Implications of an Ageing Australia.

As a result, Federal Treasury and others have been urging faster productivity growth and higher levels of participation, as the resultant increase in the size of the economy would directly address many of the risks associated with slowing growth.

That point has been hammered home by the Treasury Secretary Ken Henry in several speeches including, for example, his August 2004 Policy Strategies for Future Growth.

And Treasury researchers are now making the point that one way to increase both productivity and participation is to have a higher skilled workforce. Productivity rises due to increased skills, and participation rises as those increased skills lead to higher wages, a reduced likelihood of unemployment and (typically) better working conditions.

Such points have been made by Kennedy and Hedley of Treasury in a 2003 Working Paper, Gruen and Garbutt in a 2004 paper and Davis and Ewing in a 2005 paper.

This chapter joins the above dots.

2.1 LINKS BETWEEN EDUCATION AND WORK

For the economy as a whole more education means more skilled workers, which means:

Higher productivity. Workers with more education bring a higher level of skills to the workplace.

Higher participation. Workers with higher skill levels are more likely to work, and also tend to work for longer by choosing to delay retirement.

Higher employment. Workers with more education are more employable and enjoy lower unemployment rates.

Future demand for vocational education and training in NSW

7

There is a clear and well-established relationship between education levels and productivity. Recently, economists have also emphasised a second and almost as well-established linkage – those with higher levels of education also have higher rates of workforce participation: both during working age and as they approach traditional retirement age.

For society, higher levels of education also mean higher average incomes. That in turn means even faster growth in income tax collections because of our progressive income tax system (which applies higher average tax rates to higher earnings).

Those increased taxes may be spent for the benefit of everyone. These extra taxes – which can then be redistributed to everyone by the government – are perhaps the most direct economic channel by which society benefits from having a more educated workforce.

2.1.1 THE DIRECT EFFECT OF EDUCATION ON PRODUCTIVITY

Education is increasingly becoming the ‘engine room’ of modern economies. If we get this part of the economy right, most other things ought to fall into place, because increased investment in education boosts both productivity and participation.

Education has a direct effect on the level of productivity in the economy (and therefore output growth) because it increases the productivity of individuals. A more educated worker is a more productive worker, and investment in education provides a pool of more skilled labour.

Individuals benefit from investing in higher skills because they can command higher earnings in the labour market place.

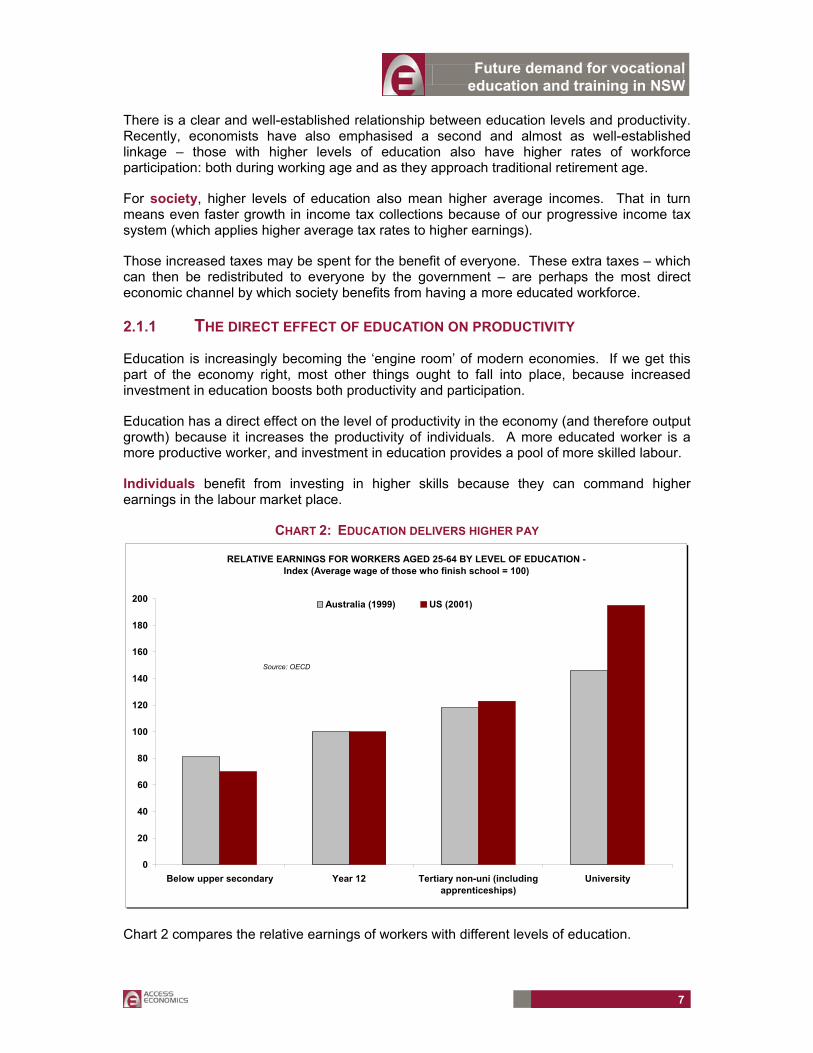

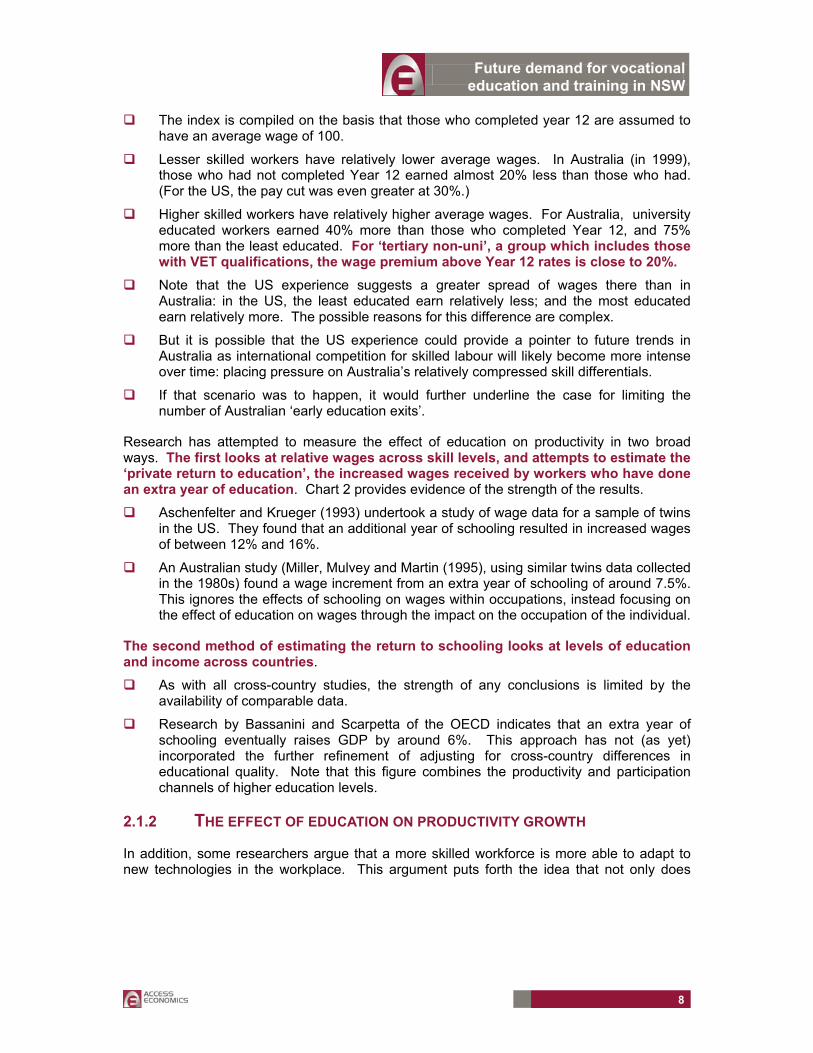

CHART 2: EDUCATION DELIVERS HIGHER PAY

RELATIVE EARNINGS FOR WORKERS AGED 25-64 BY LEVEL OF EDUCATION - Index (Average wage of those who finish school = 100)

0

20

40

60

80

100

120

140

160

180

200

Below upper secondary Year 12 Tertiary non-uni (includingapprenticeships)

University

Australia (1999) US (2001)

Source: OECD

Chart 2 compares the relative earnings of workers with different levels of education.

Future demand for vocational education and training in NSW

8

The index is compiled on the basis that those who completed year 12 are assumed to have an average wage of 100.

Lesser skilled workers have relatively lower average wages. In Australia (in 1999), those who had not completed Year 12 earned almost 20% less than those who had. (For the US, the pay cut was even greater at 30%.)

Higher skilled workers have relatively higher average wages. For Australia, university educated workers earned 40% more than those who completed Year 12, and 75% more than the least educated. For ‘tertiary non-uni’, a group which includes those with VET qualifications, the wage premium above Year 12 rates is close to 20%.

Note that the US experience suggests a greater spread of wages there than in Australia: in the US, the least educated earn relatively less; and the most educated earn relatively more. The possible reasons for this difference are complex.

But it is possible that the US experience could provide a pointer to future trends in Australia as international competition for skilled labour will likely become more intense over time: placing pressure on Australia’s relatively compressed skill differentials.

If that scenario was to happen, it would further underline the case for limiting the number of Australian ‘early education exits’.

Research has attempted to measure the effect of education on productivity in two broad ways. The first looks at relative wages across skill levels, and attempts to estimate the ‘private return to education’, the increased wages received by workers who have done an extra year of education. Chart 2 provides evidence of the strength of the results.

Aschenfelter and Krueger (1993) undertook a study of wage data for a sample of twins in the US. They found that an additional year of schooling resulted in increased wages of between 12% and 16%.

An Australian study (Miller, Mulvey and Martin (1995), using similar twins data collected in the 1980s) found a wage increment from an extra year of schooling of around 7.5%. This ignores the effects of schooling on wages within occupations, instead focusing on the effect of education on wages through the impact on the occupation of the individual.

The second method of estimating the return to schooling looks at levels of education and income across countries.

As with all cross-country studies, the strength of any conclusions is limited by the availability of comparable data.

Research by Bassanini and Scarpetta of the OECD indicates that an extra year of schooling eventually raises GDP by around 6%. This approach has not (as yet) incorporated the further refinement of adjusting for cross-country differences in educational quality. Note that this figure combines the productivity and participation channels of higher education levels.

2.1.2 THE EFFECT OF EDUCATION ON PRODUCTIVITY GROWTH

In addition, some researchers argue that a more skilled workforce is more able to adapt to new technologies in the workplace. This argument puts forth the idea that not only does

Future demand for vocational education and training in NSW

9

education increase the level of productivity in the economy, it also has an effect on the growth of productivity over time1.

Research into this ‘catch up’ phenomenon has produced some interesting results by comparing countries over time, but is yet to produce solid evidence for developed countries.

It is perhaps too early to tell whether productivity growth is improved over and above the direct increase in worker productivity, but to the extent that there are positive ‘spillovers’ from education, there is potential for an increase in broad productivity growth.

2.2 THE EFFECT OF EDUCATION ON PARTICIPATION RATES

Higher education increases the wage an individual can command, giving them a stronger incentive to work, and reduces their likelihood of any spells in unemployment.

To the extent that higher skilled jobs tend to be less ‘back breaking’ and more interesting, it also means that older higher skilled workers are more likely to be willing and able to maintain a connection with the workforce than less skilled workers.

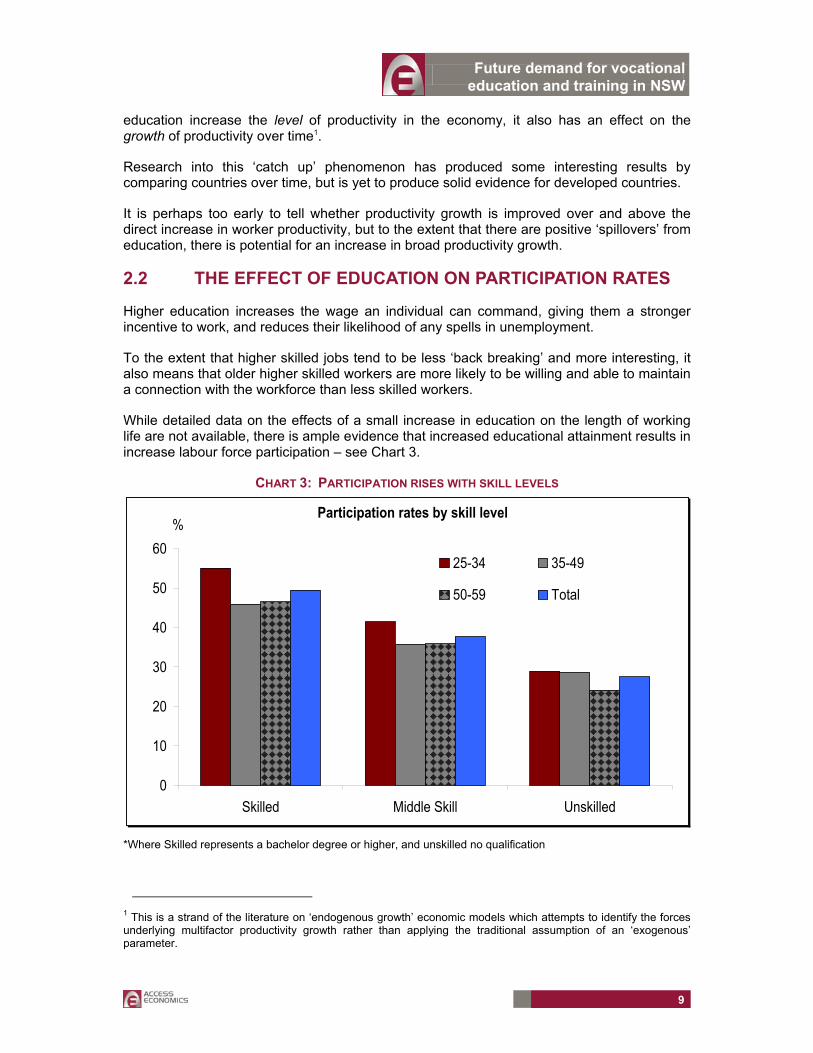

While detailed data on the effects of a small increase in education on the length of working life are not available, there is ample evidence that increased educational attainment results in increase labour force participation – see Chart 3.

CHART 3: PARTICIPATION RISES WITH SKILL LEVELS

Participation rates by skill level

0

10

20

30

40

50

60

Skilled Middle Skill Unskilled

%

25-34 35-49

50-59 Total

*Where Skilled represents a bachelor degree or higher, and unskilled no qualification

1 This is a strand of the literature on ‘endogenous growth’ economic models which attempts to identify the forces underlying multifactor productivity growth rather than applying the traditional assumption of an ‘exogenous’ parameter.

Future demand for vocational education and training in NSW

10

2.3 THE EFFECT OF EDUCATION ON UNEMPLOYMENT

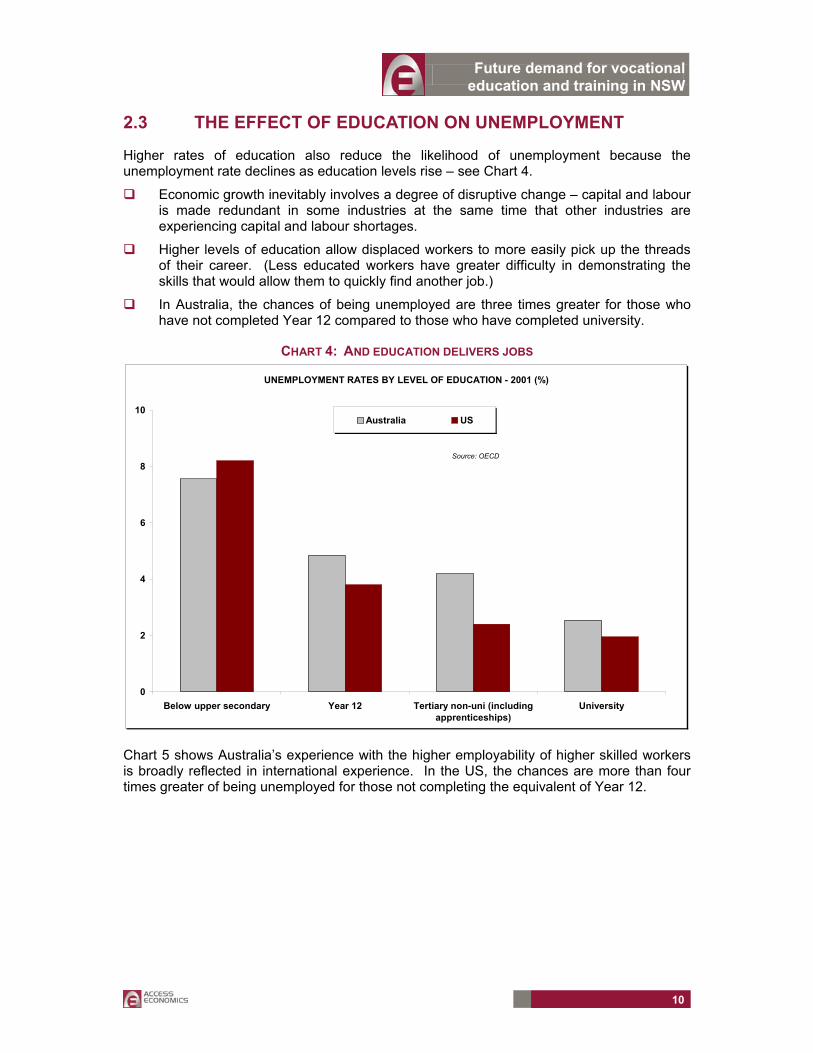

Higher rates of education also reduce the likelihood of unemployment because the unemployment rate declines as education levels rise – see Chart 4.

Economic growth inevitably involves a degree of disruptive change – capital and labour is made redundant in some industries at the same time that other industries are experiencing capital and labour shortages.

Higher levels of education allow displaced workers to more easily pick up the threads of their career. (Less educated workers have greater difficulty in demonstrating the skills that would allow them to quickly find another job.)

In Australia, the chances of being unemployed are three times greater for those who have not completed Year 12 compared to those who have completed university.

CHART 4: AND EDUCATION DELIVERS JOBS

UNEMPLOYMENT RATES BY LEVEL OF EDUCATION - 2001 (%)

0

2

4

6

8

10

Below upper secondary Year 12 Tertiary non-uni (includingapprenticeships)

University

Australia US

Source: OECD

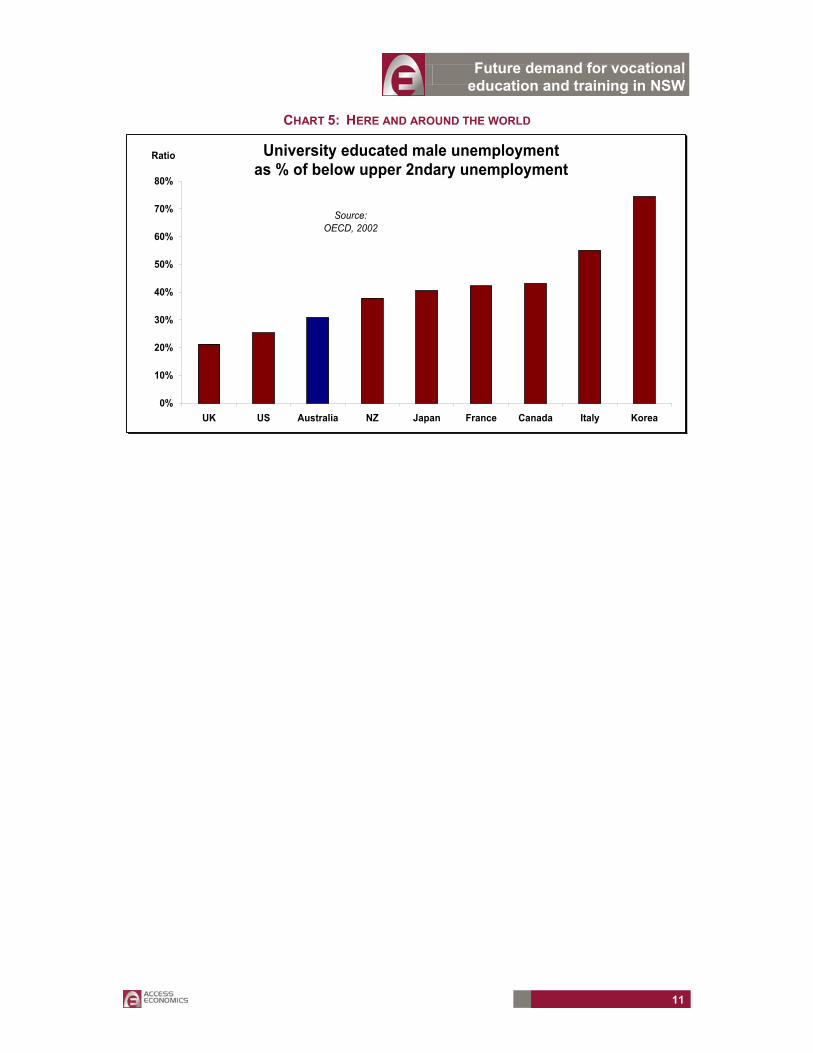

Chart 5 shows Australia’s experience with the higher employability of higher skilled workers is broadly reflected in international experience. In the US, the chances are more than four times greater of being unemployed for those not completing the equivalent of Year 12.

Future demand for vocational education and training in NSW

11

CHART 5: HERE AND AROUND THE WORLD

University educated male unemployment as % of below upper 2ndary unemployment

0%

10%

20%

30%

40%

50%

60%

70%

80%

UK US Australia NZ Japan France Canada Italy Korea

Ratio

Source: OECD, 2002

Future demand for vocational education and training in NSW

12

3. PROFILE OF VET ACTIVITY

VET activity ramped up notably in the 1990s in New South Wales, but since 2000 student numbers and the number of hours delivered has levelled off. That decline has been more notable in New South Wales than nationally.

In part, the recent decline in VET participation reflects a petering out of supply side initiatives which were encouraging greater participation in VET in the 1990s. Other factors here are that (1) productivity growth has also slowed, (2) higher student fees and (3), until relatively recently, a strong labour market negated some short term training needs by offering attractive short term returns.

In 2004, VET students in New South Wales amounted to 16.3% of total people employed, a participation rate just below the national average. The profile of VET delivered was approximately 50% of training as continuing training (for those already in or who have recently joined the workforce), 30% as re-entrant training, and 20% for New Apprenticeships. Overall some 44% of VET students were aged under 25.

This report examines publicly funded VET which is one component of the overall skills development effort. The extent of publicly funded VET is reported in the national provider collection maintained by the National Centre for Vocational Education Research (NCVER).

This covers all VET delivered by providers in receipt of public funding allocations for VET. This includes:

all VET delivered by TAFE and other government providers;

most VET delivered by multi-sector higher education institutions;

public VET delivered by community education providers; and

public VET delivered by registered private providers.

VET which is fee for service by private providers is outside the scope of this report, as is delivery of recreation, leisure and personal enrichment activity (‘non-vocational’ programs), as is VET delivered in schools where the delivery has been undertaken by schools.

3.1 TOTAL VET ACTIVITY

In New South Wales in 2004:

there were 517,500 students undertaking publicly funded VET; and

some 112 million hours of VET was delivered to those students.

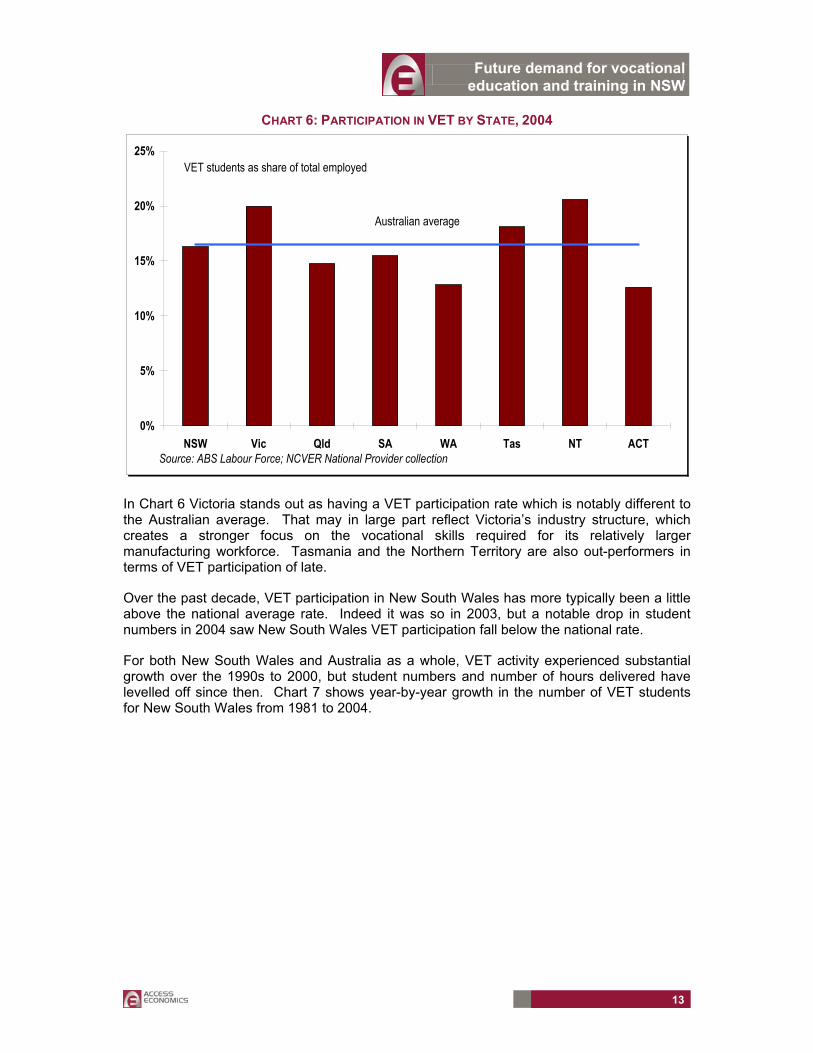

Chart 6 shows VET participation (the number of VET students as a share of those employed) State by State and nationally in 2004. VET participation in New South Wales is marginally lower than that seen for Australia as a whole.

Future demand for vocational education and training in NSW

13

CHART 6: PARTICIPATION IN VET BY STATE, 2004

0%

5%

10%

15%

20%

25%

NSW Vic Qld SA WA Tas NT ACT

VET students as share of total employed

Australian average

Source: ABS Labour Force; NCVER National Provider collection

In Chart 6 Victoria stands out as having a VET participation rate which is notably different to the Australian average. That may in large part reflect Victoria’s industry structure, which creates a stronger focus on the vocational skills required for its relatively larger manufacturing workforce. Tasmania and the Northern Territory are also out-performers in terms of VET participation of late.

Over the past decade, VET participation in New South Wales has more typically been a little above the national average rate. Indeed it was so in 2003, but a notable drop in student numbers in 2004 saw New South Wales VET participation fall below the national rate.

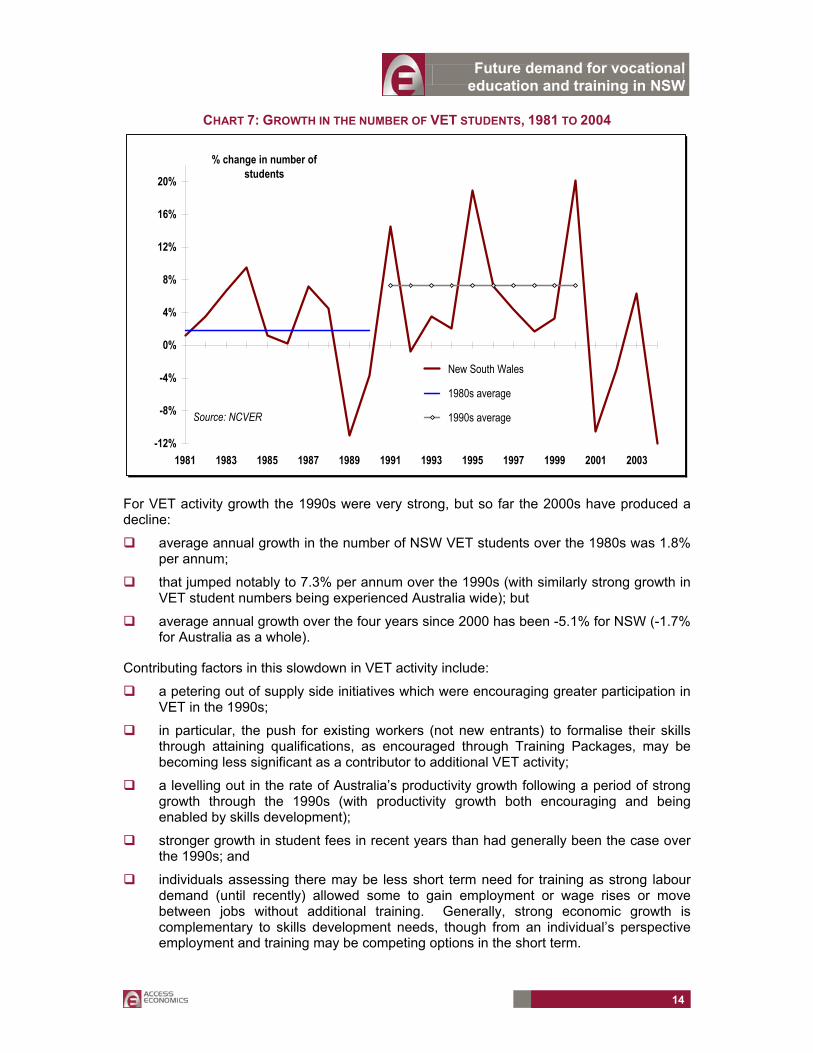

For both New South Wales and Australia as a whole, VET activity experienced substantial growth over the 1990s to 2000, but student numbers and number of hours delivered have levelled off since then. Chart 7 shows year-by-year growth in the number of VET students for New South Wales from 1981 to 2004.

Future demand for vocational education and training in NSW

14

CHART 7: GROWTH IN THE NUMBER OF VET STUDENTS, 1981 TO 2004

-12%

-8%

-4%

0%

4%

8%

12%

16%

20%

1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003

% change in number of students

New South Wales

1980s average

1990s averageSource: NCVER

For VET activity growth the 1990s were very strong, but so far the 2000s have produced a decline:

average annual growth in the number of NSW VET students over the 1980s was 1.8% per annum;

that jumped notably to 7.3% per annum over the 1990s (with similarly strong growth in VET student numbers being experienced Australia wide); but

average annual growth over the four years since 2000 has been -5.1% for NSW (-1.7% for Australia as a whole).

Contributing factors in this slowdown in VET activity include:

a petering out of supply side initiatives which were encouraging greater participation in VET in the 1990s;

in particular, the push for existing workers (not new entrants) to formalise their skills through attaining qualifications, as encouraged through Training Packages, may be becoming less significant as a contributor to additional VET activity;

a levelling out in the rate of Australia’s productivity growth following a period of strong growth through the 1990s (with productivity growth both encouraging and being enabled by skills development);

stronger growth in student fees in recent years than had generally been the case over the 1990s; and

individuals assessing there may be less short term need for training as strong labour demand (until recently) allowed some to gain employment or wage rises or move between jobs without additional training. Generally, strong economic growth is complementary to skills development needs, though from an individual’s perspective employment and training may be competing options in the short term.

Future demand for vocational education and training in NSW

15

Note also that the year 2000 may provide somewhat of an artificial peak for VET activity in New South Wales. Part of the strong growth in training in that year was related to the Olympic Games, with a significant number of people undertaking VET courses associated with volunteer work at the Olympics. The Olympics would also have placed demands on the need for skilled construction workers at that time. However, the recent slowdown in VET in New South Wales is not only against that peak year – the number of VET students in New South Wales in 2004 is even below 1999 levels.

In terms of the number of hours of VET delivered, New South Wales has seen a decline in 2004 of some 5.0%. The level of VET hours delivered however remains a little above year 2000 levels. The average number of VET hours delivered per student in New South Wales has expanded from 169 in 2000 to 216 in 2004, with a similar expansion seen nationally.

The shift to longer courses in recent years may reflect the job cycle which in recent years has favoured blue collar jobs more so than previously, and skills here are often developed through long apprenticeships rather than shorter courses of study.

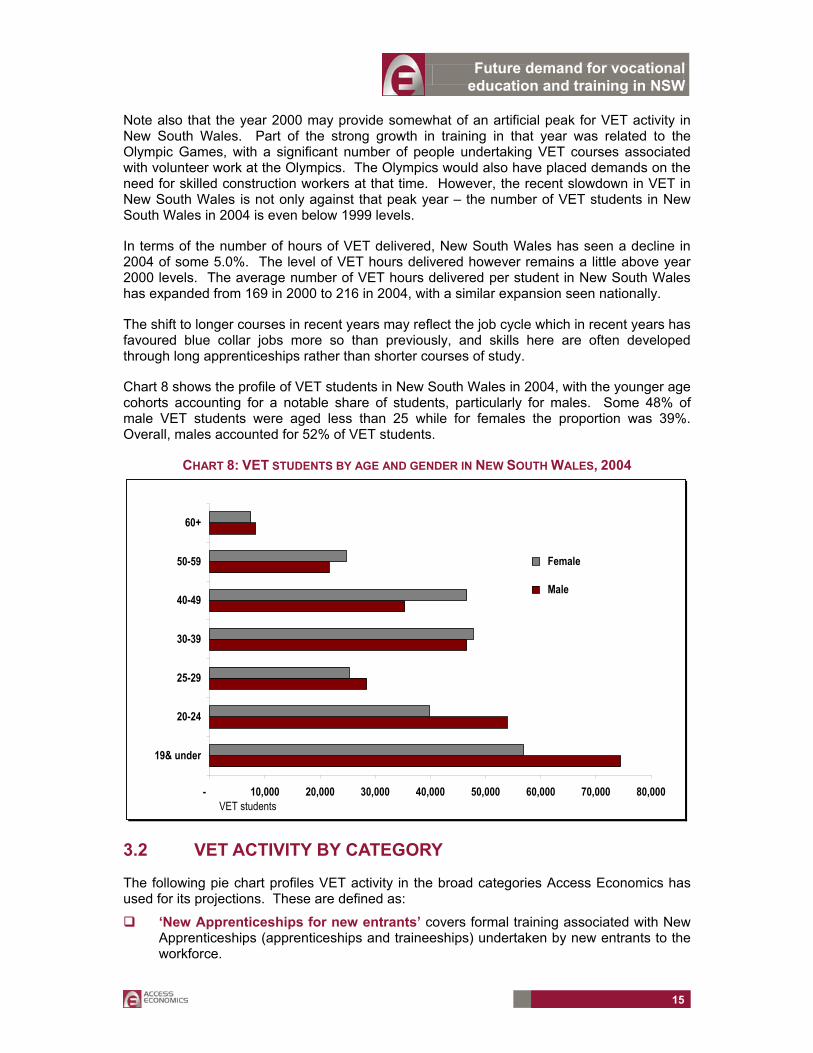

Chart 8 shows the profile of VET students in New South Wales in 2004, with the younger age cohorts accounting for a notable share of students, particularly for males. Some 48% of male VET students were aged less than 25 while for females the proportion was 39%. Overall, males accounted for 52% of VET students.

CHART 8: VET STUDENTS BY AGE AND GENDER IN NEW SOUTH WALES, 2004

- 10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000

19& under

20-24

25-29

30-39

40-49

50-59

60+

Female

Male

VET students

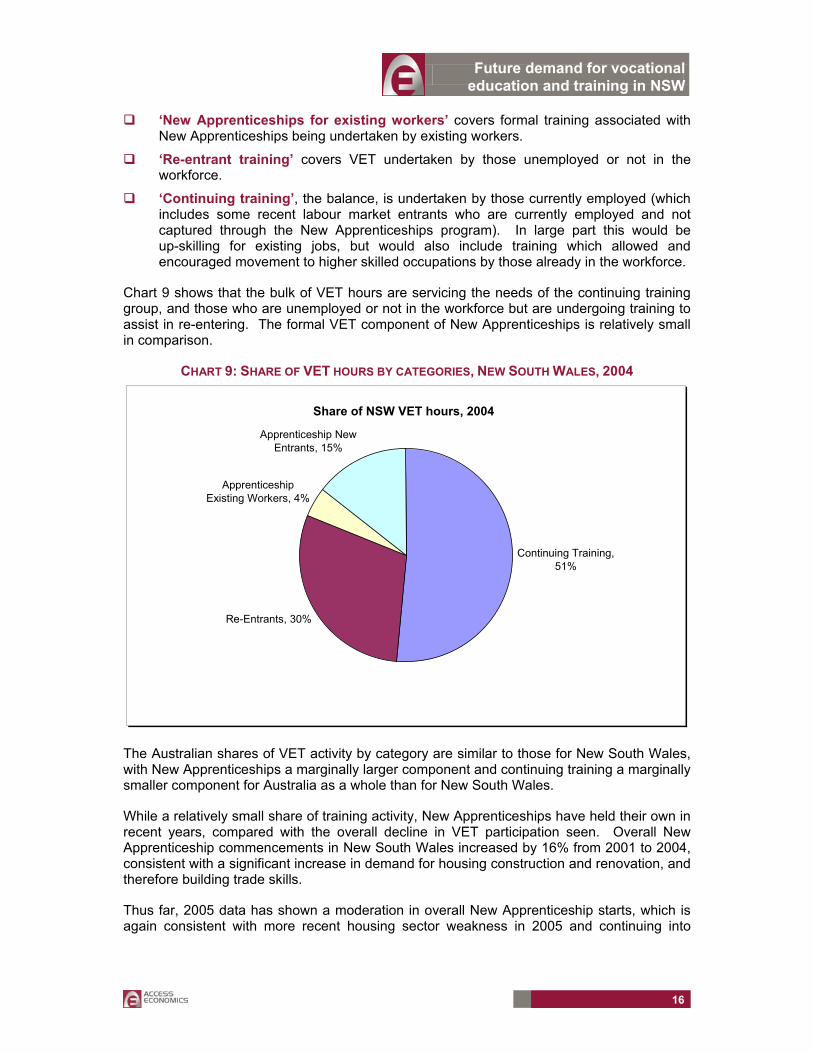

3.2 VET ACTIVITY BY CATEGORY

The following pie chart profiles VET activity in the broad categories Access Economics has used for its projections. These are defined as:

‘New Apprenticeships for new entrants’ covers formal training associated with New Apprenticeships (apprenticeships and traineeships) undertaken by new entrants to the workforce.

Future demand for vocational education and training in NSW

16

‘New Apprenticeships for existing workers’ covers formal training associated with New Apprenticeships being undertaken by existing workers.

‘Re-entrant training’ covers VET undertaken by those unemployed or not in the workforce.

‘Continuing training’, the balance, is undertaken by those currently employed (which includes some recent labour market entrants who are currently employed and not captured through the New Apprenticeships program). In large part this would be up-skilling for existing jobs, but would also include training which allowed and encouraged movement to higher skilled occupations by those already in the workforce.

Chart 9 shows that the bulk of VET hours are servicing the needs of the continuing training group, and those who are unemployed or not in the workforce but are undergoing training to assist in re-entering. The formal VET component of New Apprenticeships is relatively small in comparison.

CHART 9: SHARE OF VET HOURS BY CATEGORIES, NEW SOUTH WALES, 2004

Continuing Training, 51%

Re-Entrants, 30%

Apprenticeship Existing Workers, 4%

Apprenticeship New Entrants, 15%

Share of NSW VET hours, 2004

The Australian shares of VET activity by category are similar to those for New South Wales, with New Apprenticeships a marginally larger component and continuing training a marginally smaller component for Australia as a whole than for New South Wales.

While a relatively small share of training activity, New Apprenticeships have held their own in recent years, compared with the overall decline in VET participation seen. Overall New Apprenticeship commencements in New South Wales increased by 16% from 2001 to 2004, consistent with a significant increase in demand for housing construction and renovation, and therefore building trade skills.

Thus far, 2005 data has shown a moderation in overall New Apprenticeship starts, which is again consistent with more recent housing sector weakness in 2005 and continuing into

Future demand for vocational education and training in NSW

17

2006.2 For the purposes of these projections, interest in New Apprenticeships appears to be starting from a cyclical high point, given the strong influence exerted by building trade skills.

3.3 QUALIFICATIONS PROFILE

Consistent with VET activity data (which showed a significant ramping up in training over the 1990s) is the data on the stock of VET qualifications. This information is drawn from the ABS rather than the National Provider collection, and is only available in occupational detail at the national level.

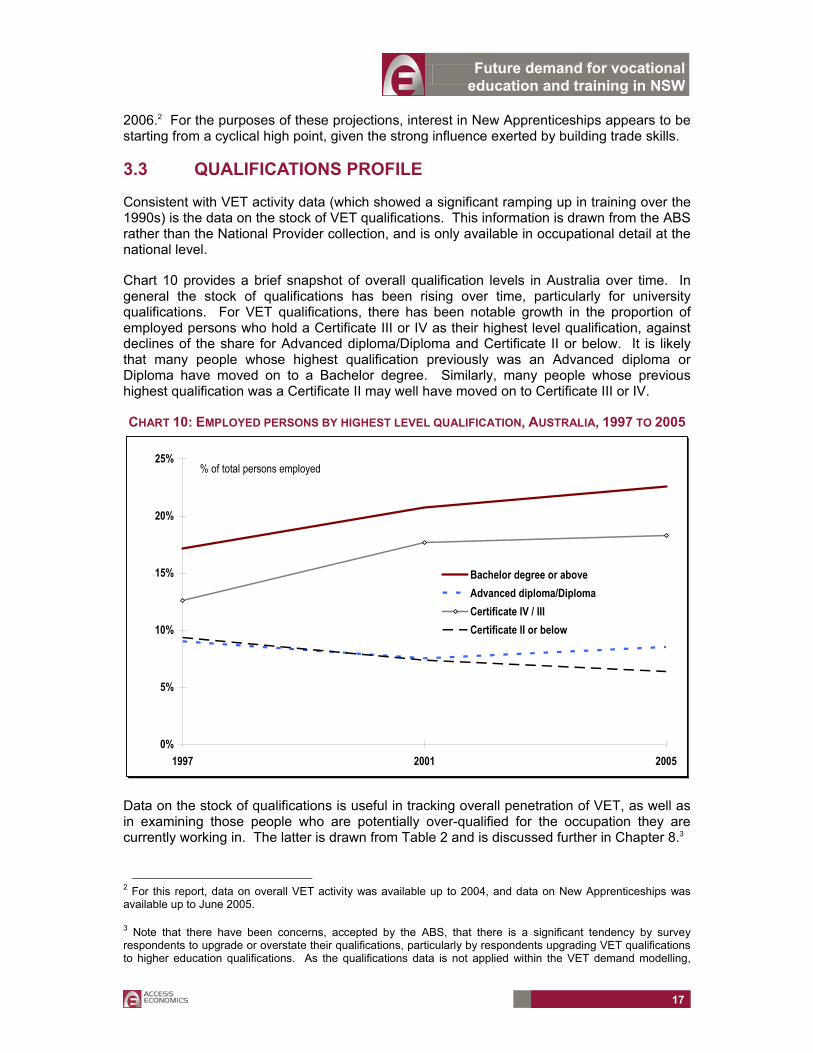

Chart 10 provides a brief snapshot of overall qualification levels in Australia over time. In general the stock of qualifications has been rising over time, particularly for university qualifications. For VET qualifications, there has been notable growth in the proportion of employed persons who hold a Certificate III or IV as their highest level qualification, against declines of the share for Advanced diploma/Diploma and Certificate II or below. It is likely that many people whose highest qualification previously was an Advanced diploma or Diploma have moved on to a Bachelor degree. Similarly, many people whose previous highest qualification was a Certificate II may well have moved on to Certificate III or IV.

CHART 10: EMPLOYED PERSONS BY HIGHEST LEVEL QUALIFICATION, AUSTRALIA, 1997 TO 2005

0%

5%

10%

15%

20%

25%

1997 2001 2005

Bachelor degree or aboveAdvanced diploma/DiplomaCertificate IV / III Certificate II or below

% of total persons employed

Data on the stock of qualifications is useful in tracking overall penetration of VET, as well as in examining those people who are potentially over-qualified for the occupation they are currently working in. The latter is drawn from Table 2 and is discussed further in Chapter 8.3

2 For this report, data on overall VET activity was available up to 2004, and data on New Apprenticeships was available up to June 2005.

3 Note that there have been concerns, accepted by the ABS, that there is a significant tendency by survey respondents to upgrade or overstate their qualifications, particularly by respondents upgrading VET qualifications to higher education qualifications. As the qualifications data is not applied within the VET demand modelling,

Future demand for vocational education and training in NSW

18

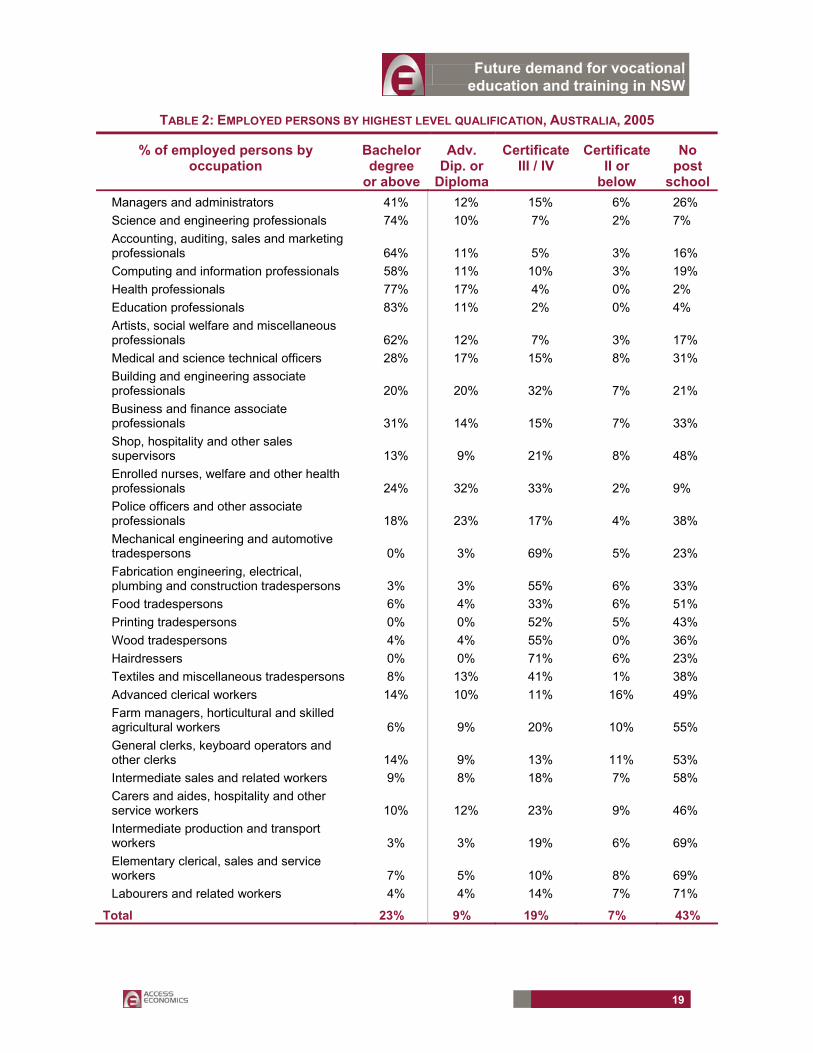

Table 2 shows highest level qualification rates for 28 occupational groups.4 The table can be seen as very broadly in order of skill levels of from top to bottom. Key features include:

as one would expect, higher levels of qualifications are more prevalent for the higher skill occupations;

while the trades occupations show a relatively high proportion of employees with VET qualifications, there are also a considerable number with no post-school qualifications (for example, 51% of food tradespersons and 36% of wood tradespersons); and

with the bottom six occupations in the table representing the least skilled, there are a reasonable proportion of these workers who have post-school qualifications. Arguably, they may not all be using them to the fullest extent.

other than in calibrating one initiative in the target scenario, such overstatement does not materially affect the VET demand projections presented here.

4 These 28 groups are an aggregation of 3-digit ASCO occupational categories, with the classification agreed with IPART for the reporting of occupational information.

Future demand for vocational education and training in NSW

19

TABLE 2: EMPLOYED PERSONS BY HIGHEST LEVEL QUALIFICATION, AUSTRALIA, 2005

% of employed persons by occupation

Bachelor degree

or above

Adv. Dip. or

Diploma

Certificate III / IV

Certificate II or

below

No post

school Managers and administrators 41% 12% 15% 6% 26% Science and engineering professionals 74% 10% 7% 2% 7% Accounting, auditing, sales and marketing professionals 64% 11% 5% 3% 16% Computing and information professionals 58% 11% 10% 3% 19% Health professionals 77% 17% 4% 0% 2% Education professionals 83% 11% 2% 0% 4% Artists, social welfare and miscellaneous professionals 62% 12% 7% 3% 17% Medical and science technical officers 28% 17% 15% 8% 31% Building and engineering associate professionals 20% 20% 32% 7% 21% Business and finance associate professionals 31% 14% 15% 7% 33% Shop, hospitality and other sales supervisors 13% 9% 21% 8% 48% Enrolled nurses, welfare and other health professionals 24% 32% 33% 2% 9% Police officers and other associate professionals 18% 23% 17% 4% 38% Mechanical engineering and automotive tradespersons 0% 3% 69% 5% 23% Fabrication engineering, electrical, plumbing and construction tradespersons 3% 3% 55% 6% 33% Food tradespersons 6% 4% 33% 6% 51% Printing tradespersons 0% 0% 52% 5% 43% Wood tradespersons 4% 4% 55% 0% 36% Hairdressers 0% 0% 71% 6% 23% Textiles and miscellaneous tradespersons 8% 13% 41% 1% 38% Advanced clerical workers 14% 10% 11% 16% 49% Farm managers, horticultural and skilled agricultural workers 6% 9% 20% 10% 55% General clerks, keyboard operators and other clerks 14% 9% 13% 11% 53% Intermediate sales and related workers 9% 8% 18% 7% 58% Carers and aides, hospitality and other service workers 10% 12% 23% 9% 46% Intermediate production and transport workers 3% 3% 19% 6% 69% Elementary clerical, sales and service workers 7% 5% 10% 8% 69% Labourers and related workers 4% 4% 14% 7% 71%

Total 23% 9% 19% 7% 43%

Future demand for vocational education and training in NSW

20

4. BASELINE SCENARIO – LABOUR MARKET PROJECTIONS

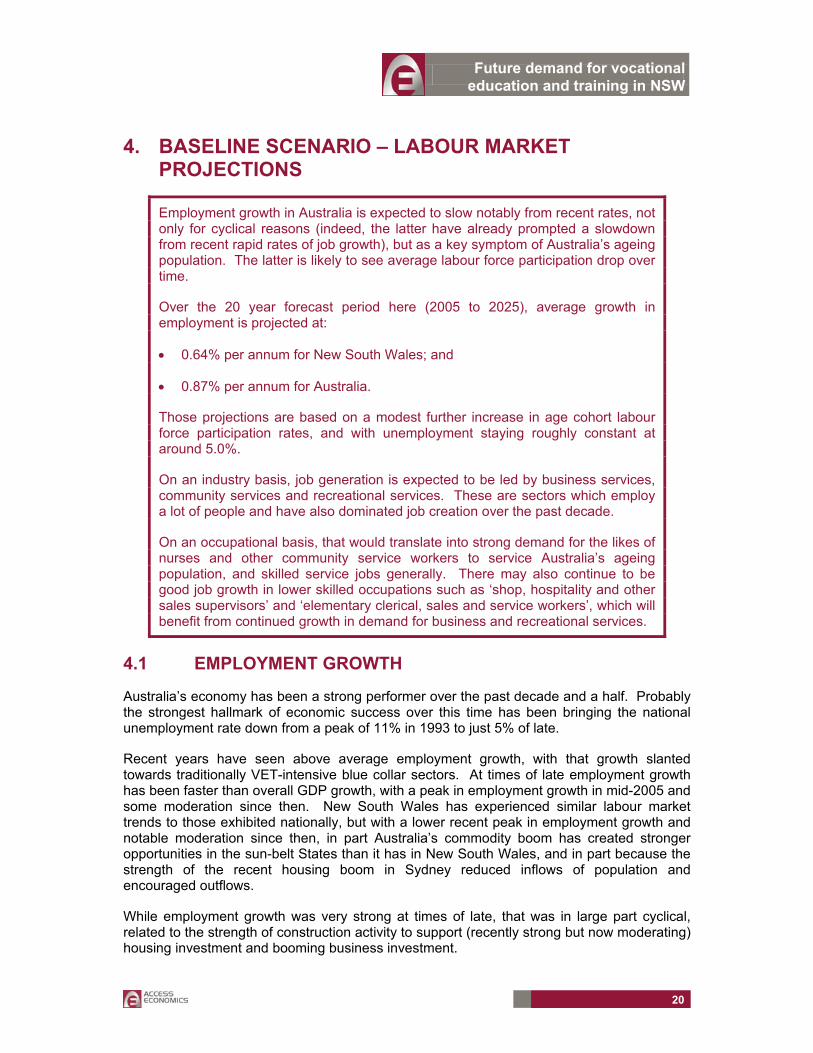

Employment growth in Australia is expected to slow notably from recent rates, not only for cyclical reasons (indeed, the latter have already prompted a slowdown from recent rapid rates of job growth), but as a key symptom of Australia’s ageing population. The latter is likely to see average labour force participation drop over time.

Over the 20 year forecast period here (2005 to 2025), average growth in employment is projected at:

• 0.64% per annum for New South Wales; and

• 0.87% per annum for Australia.

Those projections are based on a modest further increase in age cohort labour force participation rates, and with unemployment staying roughly constant at around 5.0%.

On an industry basis, job generation is expected to be led by business services, community services and recreational services. These are sectors which employ a lot of people and have also dominated job creation over the past decade.

On an occupational basis, that would translate into strong demand for the likes of nurses and other community service workers to service Australia’s ageing population, and skilled service jobs generally. There may also continue to be good job growth in lower skilled occupations such as ‘shop, hospitality and other sales supervisors’ and ‘elementary clerical, sales and service workers’, which will benefit from continued growth in demand for business and recreational services.

4.1 EMPLOYMENT GROWTH

Australia’s economy has been a strong performer over the past decade and a half. Probably the strongest hallmark of economic success over this time has been bringing the national unemployment rate down from a peak of 11% in 1993 to just 5% of late.

Recent years have seen above average employment growth, with that growth slanted towards traditionally VET-intensive blue collar sectors. At times of late employment growth has been faster than overall GDP growth, with a peak in employment growth in mid-2005 and some moderation since then. New South Wales has experienced similar labour market trends to those exhibited nationally, but with a lower recent peak in employment growth and notable moderation since then, in part Australia’s commodity boom has created stronger opportunities in the sun-belt States than it has in New South Wales, and in part because the strength of the recent housing boom in Sydney reduced inflows of population and encouraged outflows.

While employment growth was very strong at times of late, that was in large part cyclical, related to the strength of construction activity to support (recently strong but now moderating) housing investment and booming business investment.

Future demand for vocational education and training in NSW

21

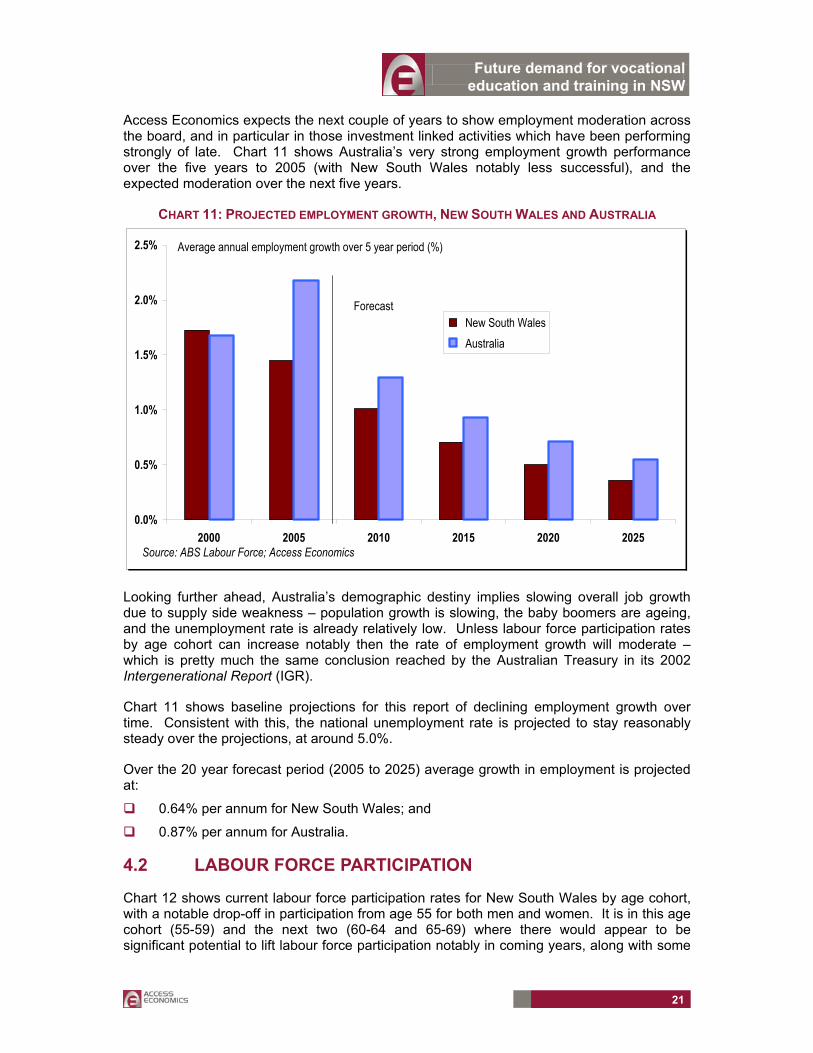

Access Economics expects the next couple of years to show employment moderation across the board, and in particular in those investment linked activities which have been performing strongly of late. Chart 11 shows Australia’s very strong employment growth performance over the five years to 2005 (with New South Wales notably less successful), and the expected moderation over the next five years.

CHART 11: PROJECTED EMPLOYMENT GROWTH, NEW SOUTH WALES AND AUSTRALIA

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

2000 2005 2010 2015 2020 2025

New South Wales Australia

Source: ABS Labour Force; Access Economics

Average annual employment growth over 5 year period (%)

Forecast

Looking further ahead, Australia’s demographic destiny implies slowing overall job growth due to supply side weakness – population growth is slowing, the baby boomers are ageing, and the unemployment rate is already relatively low. Unless labour force participation rates by age cohort can increase notably then the rate of employment growth will moderate – which is pretty much the same conclusion reached by the Australian Treasury in its 2002 Intergenerational Report (IGR).

Chart 11 shows baseline projections for this report of declining employment growth over time. Consistent with this, the national unemployment rate is projected to stay reasonably steady over the projections, at around 5.0%.

Over the 20 year forecast period (2005 to 2025) average growth in employment is projected at:

0.64% per annum for New South Wales; and

0.87% per annum for Australia.

4.2 LABOUR FORCE PARTICIPATION

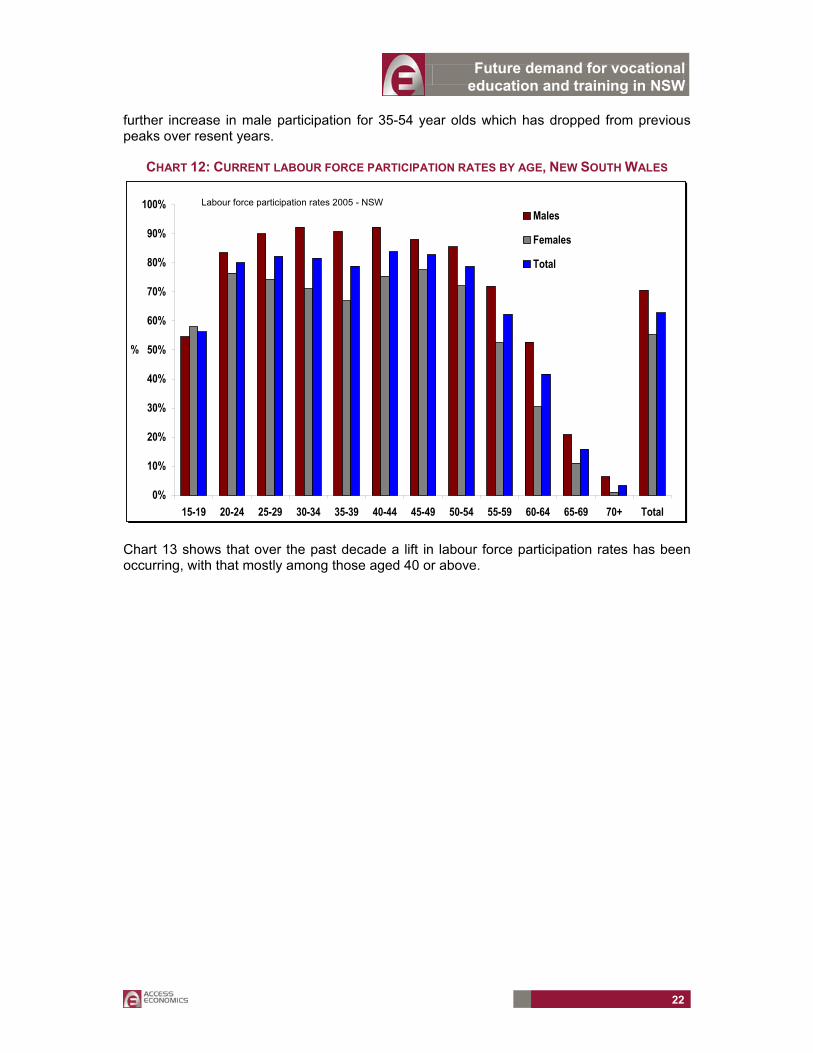

Chart 12 shows current labour force participation rates for New South Wales by age cohort, with a notable drop-off in participation from age 55 for both men and women. It is in this age cohort (55-59) and the next two (60-64 and 65-69) where there would appear to be significant potential to lift labour force participation notably in coming years, along with some

Future demand for vocational education and training in NSW

22

further increase in male participation for 35-54 year olds which has dropped from previous peaks over resent years.

CHART 12: CURRENT LABOUR FORCE PARTICIPATION RATES BY AGE, NEW SOUTH WALES

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

15-19 20-24 25-29 30-34 35-39 40-44 45-49 50-54 55-59 60-64 65-69 70+ Total

%

Males

Females

Total

Labour force participation rates 2005 - NSW

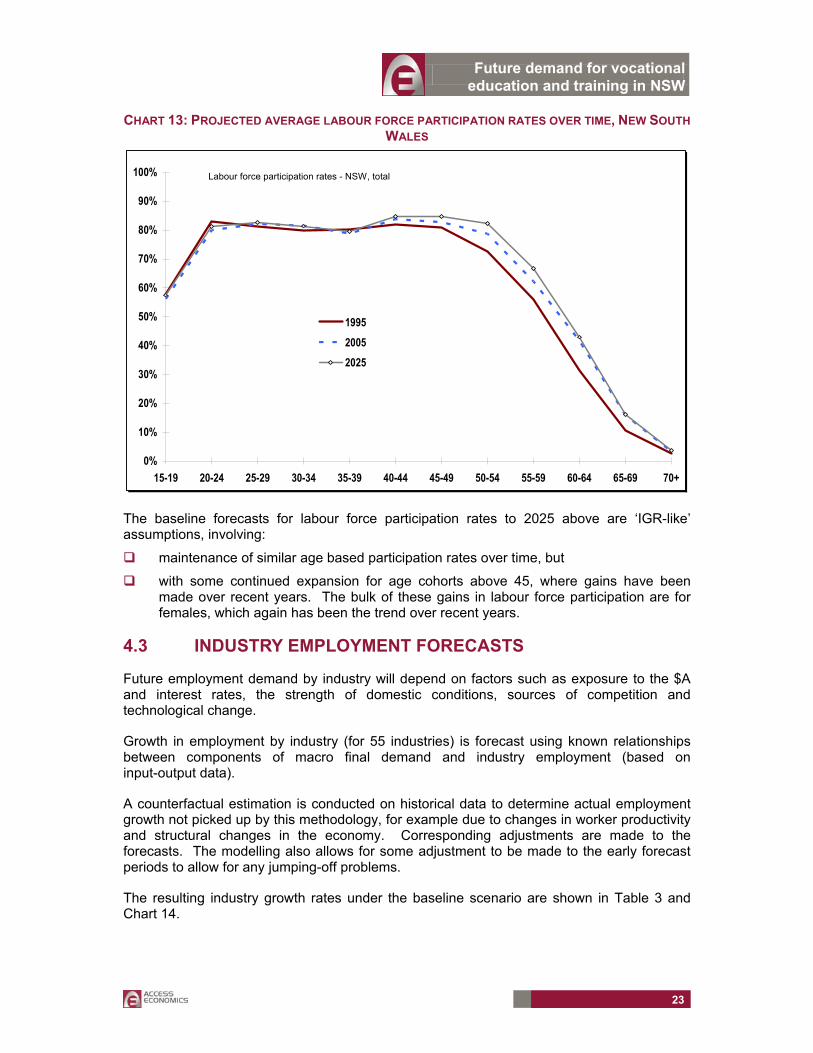

Chart 13 shows that over the past decade a lift in labour force participation rates has been occurring, with that mostly among those aged 40 or above.

Future demand for vocational education and training in NSW

23

CHART 13: PROJECTED AVERAGE LABOUR FORCE PARTICIPATION RATES OVER TIME, NEW SOUTH WALES

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

15-19 20-24 25-29 30-34 35-39 40-44 45-49 50-54 55-59 60-64 65-69 70+

199520052025

Labour force participation rates - NSW, total

The baseline forecasts for labour force participation rates to 2025 above are ‘IGR-like’ assumptions, involving:

maintenance of similar age based participation rates over time, but

with some continued expansion for age cohorts above 45, where gains have been made over recent years. The bulk of these gains in labour force participation are for females, which again has been the trend over recent years.

4.3 INDUSTRY EMPLOYMENT FORECASTS

Future employment demand by industry will depend on factors such as exposure to the $A and interest rates, the strength of domestic conditions, sources of competition and technological change.

Growth in employment by industry (for 55 industries) is forecast using known relationships between components of macro final demand and industry employment (based on input-output data).

A counterfactual estimation is conducted on historical data to determine actual employment growth not picked up by this methodology, for example due to changes in worker productivity and structural changes in the economy. Corresponding adjustments are made to the forecasts. The modelling also allows for some adjustment to be made to the early forecast periods to allow for any jumping-off problems.

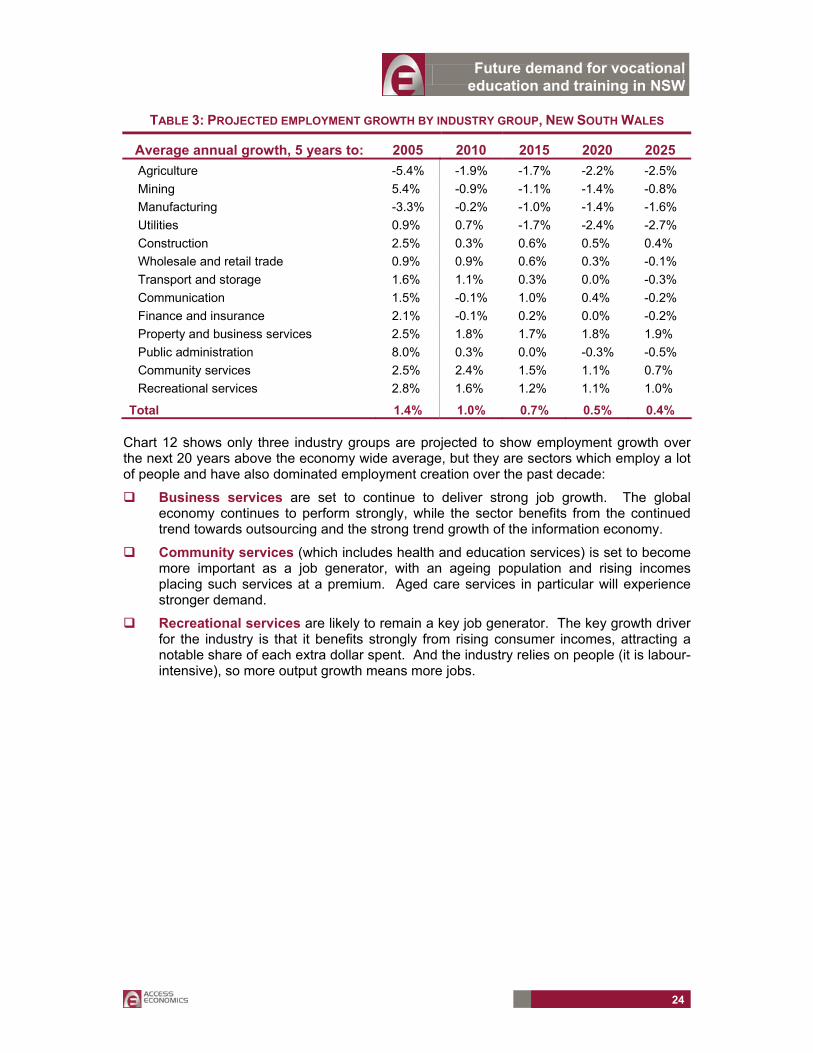

The resulting industry growth rates under the baseline scenario are shown in Table 3 and Chart 14.

Future demand for vocational education and training in NSW

24

TABLE 3: PROJECTED EMPLOYMENT GROWTH BY INDUSTRY GROUP, NEW SOUTH WALES

Average annual growth, 5 years to: 2005 2010 2015 2020 2025 Agriculture -5.4% -1.9% -1.7% -2.2% -2.5% Mining 5.4% -0.9% -1.1% -1.4% -0.8% Manufacturing -3.3% -0.2% -1.0% -1.4% -1.6% Utilities 0.9% 0.7% -1.7% -2.4% -2.7% Construction 2.5% 0.3% 0.6% 0.5% 0.4% Wholesale and retail trade 0.9% 0.9% 0.6% 0.3% -0.1% Transport and storage 1.6% 1.1% 0.3% 0.0% -0.3% Communication 1.5% -0.1% 1.0% 0.4% -0.2% Finance and insurance 2.1% -0.1% 0.2% 0.0% -0.2% Property and business services 2.5% 1.8% 1.7% 1.8% 1.9% Public administration 8.0% 0.3% 0.0% -0.3% -0.5% Community services 2.5% 2.4% 1.5% 1.1% 0.7% Recreational services 2.8% 1.6% 1.2% 1.1% 1.0%

Total 1.4% 1.0% 0.7% 0.5% 0.4%

Chart 12 shows only three industry groups are projected to show employment growth over the next 20 years above the economy wide average, but they are sectors which employ a lot of people and have also dominated employment creation over the past decade:

Business services are set to continue to deliver strong job growth. The global economy continues to perform strongly, while the sector benefits from the continued trend towards outsourcing and the strong trend growth of the information economy.

Community services (which includes health and education services) is set to become more important as a job generator, with an ageing population and rising incomes placing such services at a premium. Aged care services in particular will experience stronger demand.

Recreational services are likely to remain a key job generator. The key growth driver for the industry is that it benefits strongly from rising consumer incomes, attracting a notable share of each extra dollar spent. And the industry relies on people (it is labour-intensive), so more output growth means more jobs.

Future demand for vocational education and training in NSW

25

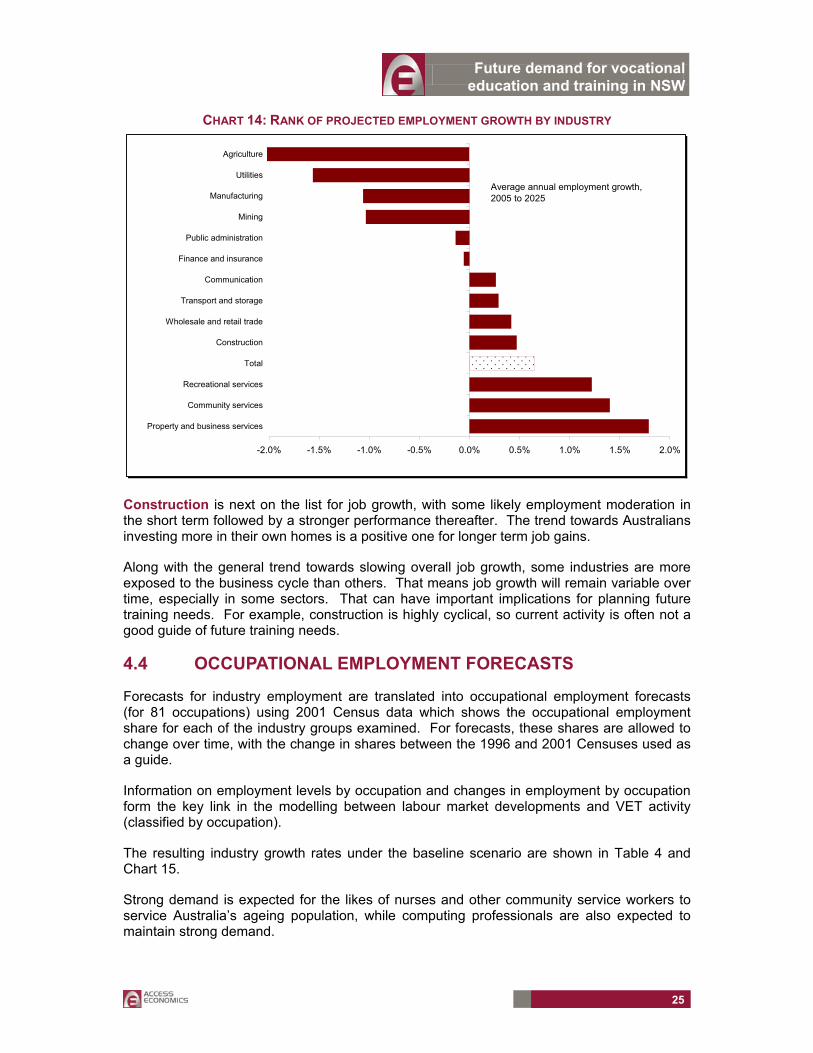

CHART 14: RANK OF PROJECTED EMPLOYMENT GROWTH BY INDUSTRY

-2.0% -1.5% -1.0% -0.5% 0.0% 0.5% 1.0% 1.5% 2.0%

Property and business services

Community services

Recreational services

Total

Construction

Wholesale and retail trade

Transport and storage

Communication

Finance and insurance

Public administration

Mining

Manufacturing

Utilities

Agriculture

Average annual employment growth, 2005 to 2025

Construction is next on the list for job growth, with some likely employment moderation in the short term followed by a stronger performance thereafter. The trend towards Australians investing more in their own homes is a positive one for longer term job gains.

Along with the general trend towards slowing overall job growth, some industries are more exposed to the business cycle than others. That means job growth will remain variable over time, especially in some sectors. That can have important implications for planning future training needs. For example, construction is highly cyclical, so current activity is often not a good guide of future training needs.

4.4 OCCUPATIONAL EMPLOYMENT FORECASTS

Forecasts for industry employment are translated into occupational employment forecasts (for 81 occupations) using 2001 Census data which shows the occupational employment share for each of the industry groups examined. For forecasts, these shares are allowed to change over time, with the change in shares between the 1996 and 2001 Censuses used as a guide.

Information on employment levels by occupation and changes in employment by occupation form the key link in the modelling between labour market developments and VET activity (classified by occupation).

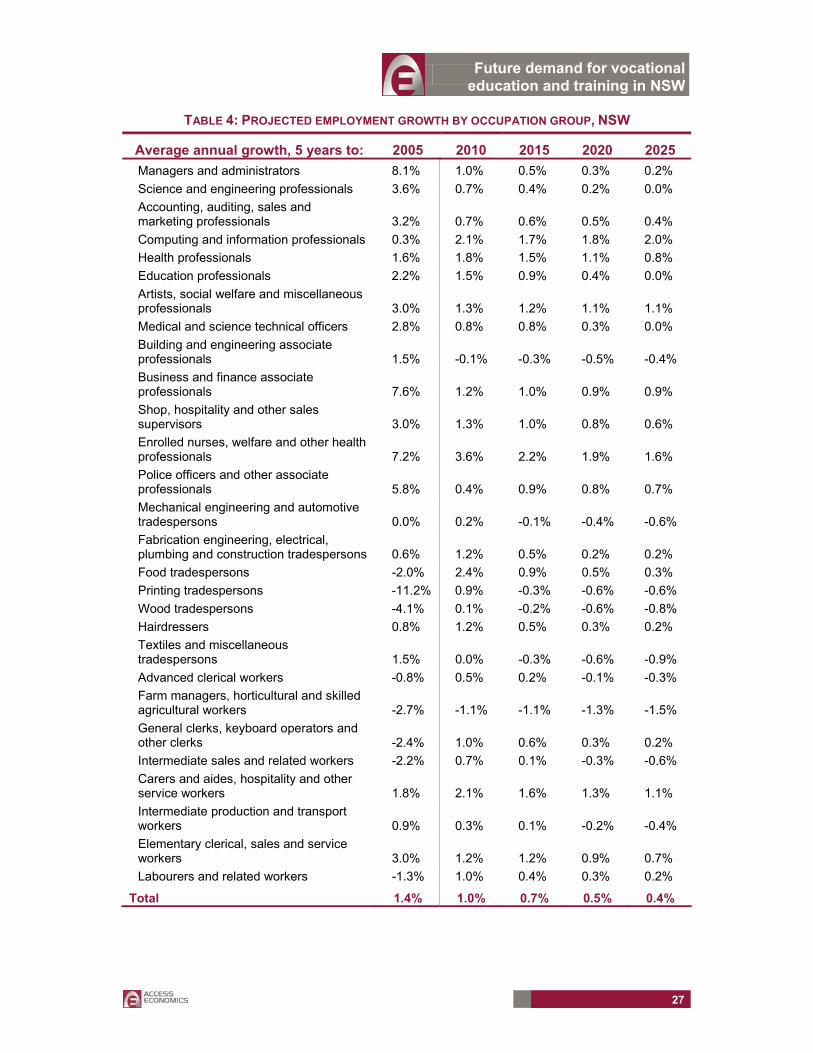

The resulting industry growth rates under the baseline scenario are shown in Table 4 and Chart 15.

Strong demand is expected for the likes of nurses and other community service workers to service Australia’s ageing population, while computing professionals are also expected to maintain strong demand.

Future demand for vocational education and training in NSW

26

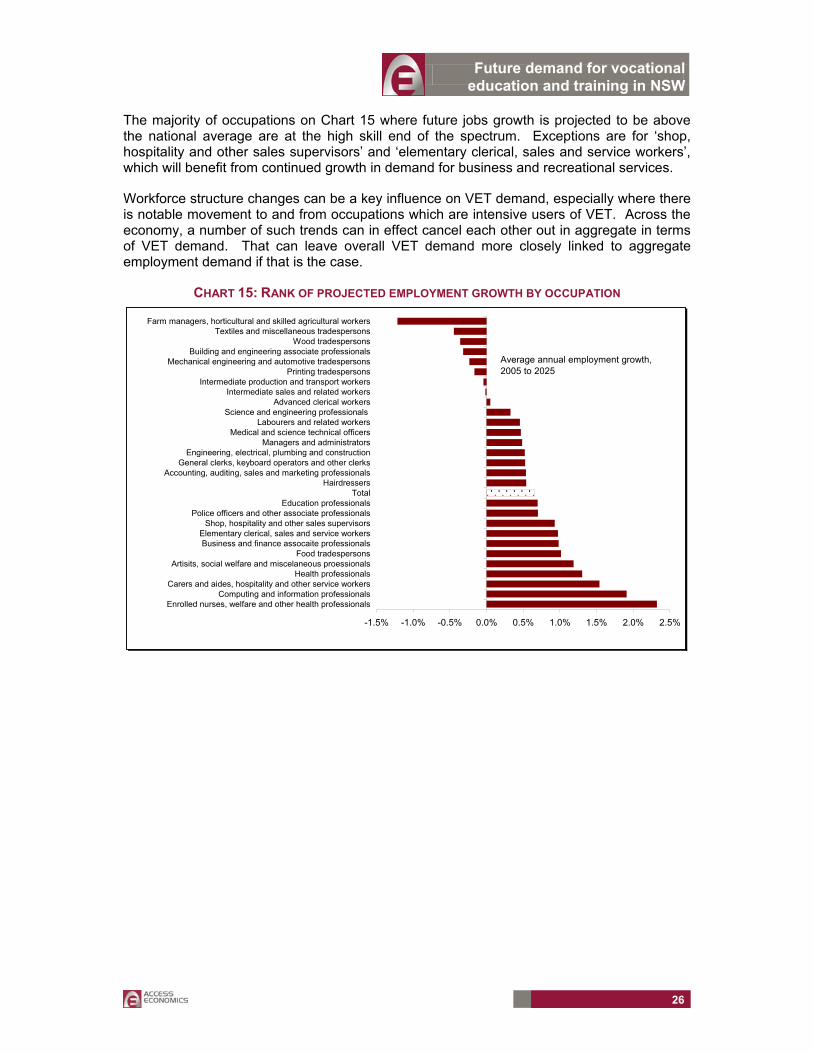

The majority of occupations on Chart 15 where future jobs growth is projected to be above the national average are at the high skill end of the spectrum. Exceptions are for ‘shop, hospitality and other sales supervisors’ and ‘elementary clerical, sales and service workers’, which will benefit from continued growth in demand for business and recreational services.

Workforce structure changes can be a key influence on VET demand, especially where there is notable movement to and from occupations which are intensive users of VET. Across the economy, a number of such trends can in effect cancel each other out in aggregate in terms of VET demand. That can leave overall VET demand more closely linked to aggregate employment demand if that is the case.

CHART 15: RANK OF PROJECTED EMPLOYMENT GROWTH BY OCCUPATION

-1.5% -1.0% -0.5% 0.0% 0.5% 1.0% 1.5% 2.0% 2.5%

Enrolled nurses, welfare and other health professionalsComputing and information professionals

Carers and aides, hospitality and other service workersHealth professionals

Artisits, social welfare and miscelaneous proessionalsFood tradespersons

Business and finance assocaite professionalsElementary clerical, sales and service workers

Shop, hospitality and other sales supervisorsPolice officers and other associate professionals

Education professionalsTotal

HairdressersAccounting, auditing, sales and marketing professionals

General clerks, keyboard operators and other clerksEngineering, electrical, plumbing and construction

Managers and administratorsMedical and science technical officers

Labourers and related workersScience and engineering professionals

Advanced clerical workersIntermediate sales and related workers

Intermediate production and transport workersPrinting tradespersons

Mechanical engineering and automotive tradespersonsBuilding and engineering associate professionals

Wood tradespersonsTextiles and miscellaneous tradespersons

Farm managers, horticultural and skilled agricultural workers

Average annual employment growth, 2005 to 2025

Future demand for vocational education and training in NSW

27

TABLE 4: PROJECTED EMPLOYMENT GROWTH BY OCCUPATION GROUP, NSW

Average annual growth, 5 years to: 2005 2010 2015 2020 2025 Managers and administrators 8.1% 1.0% 0.5% 0.3% 0.2% Science and engineering professionals 3.6% 0.7% 0.4% 0.2% 0.0% Accounting, auditing, sales and marketing professionals 3.2% 0.7% 0.6% 0.5% 0.4% Computing and information professionals 0.3% 2.1% 1.7% 1.8% 2.0% Health professionals 1.6% 1.8% 1.5% 1.1% 0.8% Education professionals 2.2% 1.5% 0.9% 0.4% 0.0% Artists, social welfare and miscellaneous professionals 3.0% 1.3% 1.2% 1.1% 1.1% Medical and science technical officers 2.8% 0.8% 0.8% 0.3% 0.0% Building and engineering associate professionals 1.5% -0.1% -0.3% -0.5% -0.4% Business and finance associate professionals 7.6% 1.2% 1.0% 0.9% 0.9% Shop, hospitality and other sales supervisors 3.0% 1.3% 1.0% 0.8% 0.6% Enrolled nurses, welfare and other health professionals 7.2% 3.6% 2.2% 1.9% 1.6% Police officers and other associate professionals 5.8% 0.4% 0.9% 0.8% 0.7% Mechanical engineering and automotive tradespersons 0.0% 0.2% -0.1% -0.4% -0.6% Fabrication engineering, electrical, plumbing and construction tradespersons 0.6% 1.2% 0.5% 0.2% 0.2% Food tradespersons -2.0% 2.4% 0.9% 0.5% 0.3% Printing tradespersons -11.2% 0.9% -0.3% -0.6% -0.6% Wood tradespersons -4.1% 0.1% -0.2% -0.6% -0.8% Hairdressers 0.8% 1.2% 0.5% 0.3% 0.2% Textiles and miscellaneous tradespersons 1.5% 0.0% -0.3% -0.6% -0.9% Advanced clerical workers -0.8% 0.5% 0.2% -0.1% -0.3% Farm managers, horticultural and skilled agricultural workers -2.7% -1.1% -1.1% -1.3% -1.5% General clerks, keyboard operators and other clerks -2.4% 1.0% 0.6% 0.3% 0.2% Intermediate sales and related workers -2.2% 0.7% 0.1% -0.3% -0.6% Carers and aides, hospitality and other service workers 1.8% 2.1% 1.6% 1.3% 1.1% Intermediate production and transport workers 0.9% 0.3% 0.1% -0.2% -0.4% Elementary clerical, sales and service workers 3.0% 1.2% 1.2% 0.9% 0.7% Labourers and related workers -1.3% 1.0% 0.4% 0.3% 0.2%

Total 1.4% 1.0% 0.7% 0.5% 0.4%

Future demand for vocational education and training in NSW

28

4.5 REGIONAL DIMENSION

The projections of VET demand have been developed at both the Australian and New South Wales levels.

Yet within New South Wales there is likely to be some variability in training demand at the regional level, thanks to different age structures, different population growth rates, different occupational profiles for employment, as well as differences in the regional distribution of the underemployed population and the extent of training infrastructure available.

It is not possible to report VET demand at the regional level in this report, but some broad thoughts on regional employment profiles are noted here.

4.5.1 SYDNEY AND THE REGIONS

Councillor Peter Woods OAM, President of the Local Government Association of NSW, noted at a 2001 Sydney Population Forum that NSW had five distinguishable regions:

Established/global Sydney: the areas closely integrated with the global economy and the information economy – eg CBD, North Sydney, Southern Sydney, Eastern Suburbs, Chatswood and other inner ring suburbs.

Developing Sydney: Western and South Western Sydney and the Central Coast.

Post-industrial regions: the Hunter and Illawarra.

Lifestyle regions: north coast and to a growing extent, south coast of NSW.

Rural NSW: largely west of the Great Dividing Range.

The ‘Greater Sydney’ region (excluding Newcastle and Wollongong, but including Camden, Penrith and Windsor) is now home to well over 4 million people. The city (whose boundaries have gradually expanded) has grown to measure:

50,000 residents by the late 1840s;

100,000 by the mid-1860s;

500,000 by 1900;

1 million by the early 1920s;

2 million by the late 1950s;

3 million by 1990;

4 million in the 2001 census.

Its underlying national population growth rate means that Sydney’s population is likely to rise above 5 million within in the next 20 years. This will occur even with the large outflow of migrants to other States, as Sydney is still the major point of entry to Australia for overseas migrants.

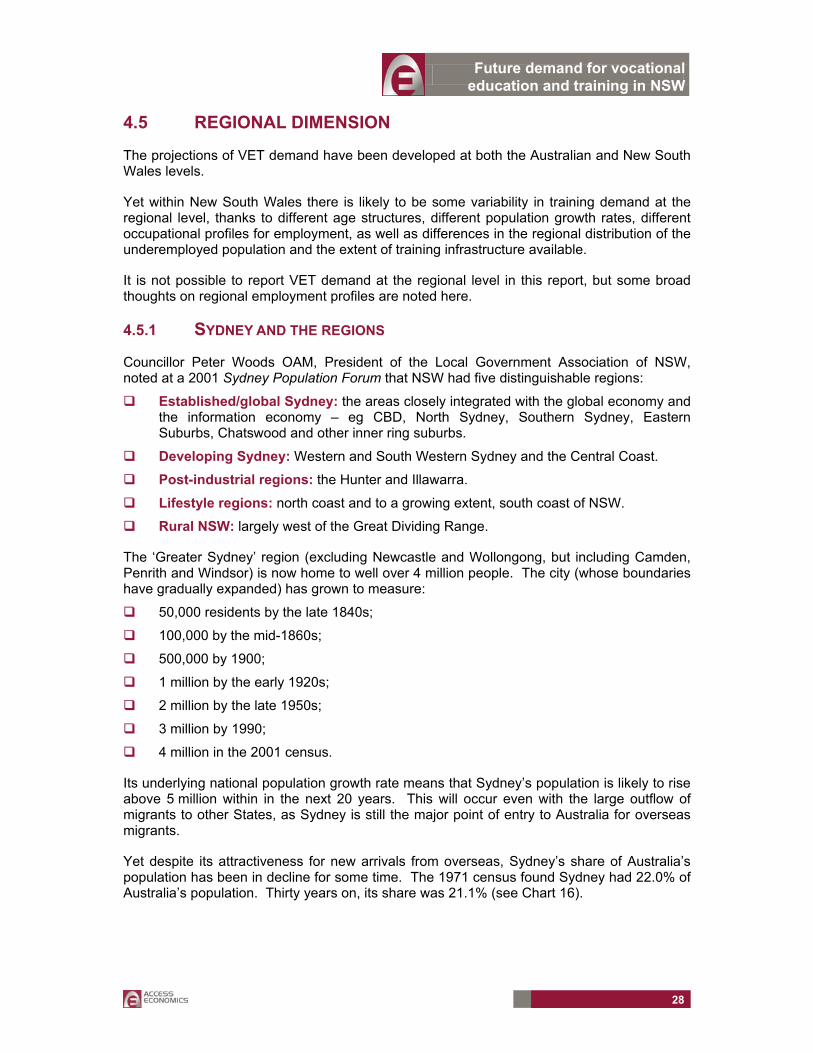

Yet despite its attractiveness for new arrivals from overseas, Sydney’s share of Australia’s population has been in decline for some time. The 1971 census found Sydney had 22.0% of Australia’s population. Thirty years on, its share was 21.1% (see Chart 16).

Future demand for vocational education and training in NSW

29

CHART 16: SYDNEY'S SHARE OF NEW SOUTH WALES’ POPULATION

45

50

55

60

65

70

1941 1951 1961 1971 1981 1991 2001 2011 2021 2031

Base Upside

Source: ABS, Access Economics

Share of NSW (%)

Forecast

Breaks in series due to re-definition of "Sydney region" by ABS

First, how ‘Sydney’ is defined has changed over time – gradually increasing as the city expanded. Chart 16 shows Sydney as a share of the State’s population since 1941. Note that a definition change saw a jump in Sydney’s measure of NSW’s population during the 1950s. There has been little change in the definition of Sydney since 1971, so some actual Sydney growth has occurred outside the geographic boundaries of the city.

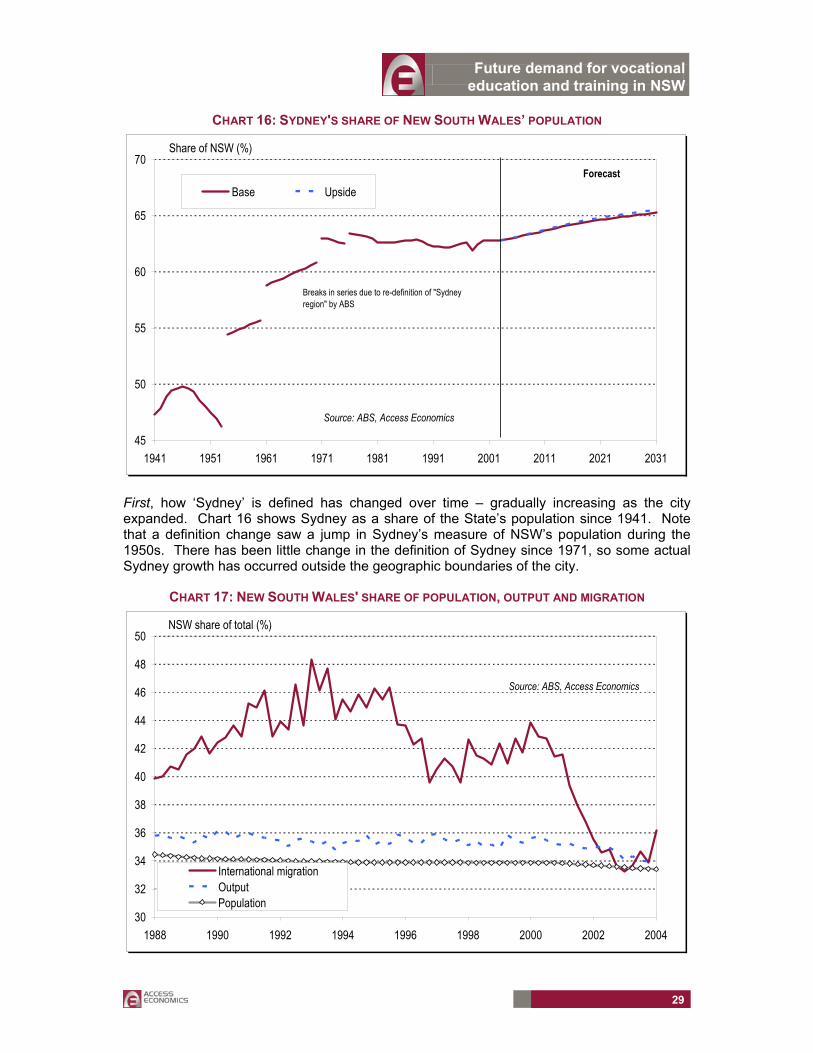

CHART 17: NEW SOUTH WALES' SHARE OF POPULATION, OUTPUT AND MIGRATION

30

32

34

36

38

40

42

44

46

48

50

1988 1990 1992 1994 1996 1998 2000 2002 2004

International migrationOutputPopulation

Source: ABS, Access Economics

NSW share of total (%)

Future demand for vocational education and training in NSW

30

Second, Sydney’s high housing prices have encouraged existing residents to trade-in their Sydney home for a ‘sea-change’ lifestyle elsewhere, either in retirement or while still working. Despite the job opportunities it offers, Sydney’s higher prices have traditionally acted as a barrier to entry for people considering moving from other States.

4.5.2 POSSIBLE REGIONAL DIFFERENCES

Both demand and supply side drivers have an impact on participation – and therefore on the demand for VET at the regional level.

The discussion here starts with demand drivers, including job demand by industry and by region.

Access Economics has developed employment forecasts by industry for NSW. These are based on ABS LFS data, and follow our long-established methodology. Our approach directly links industry output (and employment) with components of final demand.

But NSW’s regions have different industry profiles than does the State as a whole. Some are more exposed to particular industries than others. And that exposure can also change over time. That is important because, as discussed above, some industries are projected to grow faster than others, which may have an impact on job growth (and therefore participation rates) by region.

As noted in the above two sections, Access Economics projects broadly faster job growth in the service sectors than in the goods sectors (farming, manufacturing and mining). Within service sectors, the fastest growth is seen in ‘luxuries’ such as cafes and restaurants and cultural services, or in demographic-driven areas such as health. Given the outlook for farming in particular, the relative industry growth profile here points to faster job gains in Sydney than in regional NSW.

As a result, and partly also in response to the supply side drivers discussed next, Access Economics projects employment growth over the next decade to be rather faster in Sydney than in regional NSW.

Moreover, these results need to be seen within the context of a State-wide and national slowdown in overall employment growth. Or, in other words, regional NSW will not merely see relatively less job gains within a fast growing State total. Rather, it will see particular weakness within an overall slowdown at the State and national levels.

On the supply side, both overall population and the supply of labour are influenced by:

Birth rates.

Migration (including interstate migration).

Life expectancy.

The changing age structure of the population.

Changing relative participation by age, gender, and cultural background.

Education levels.

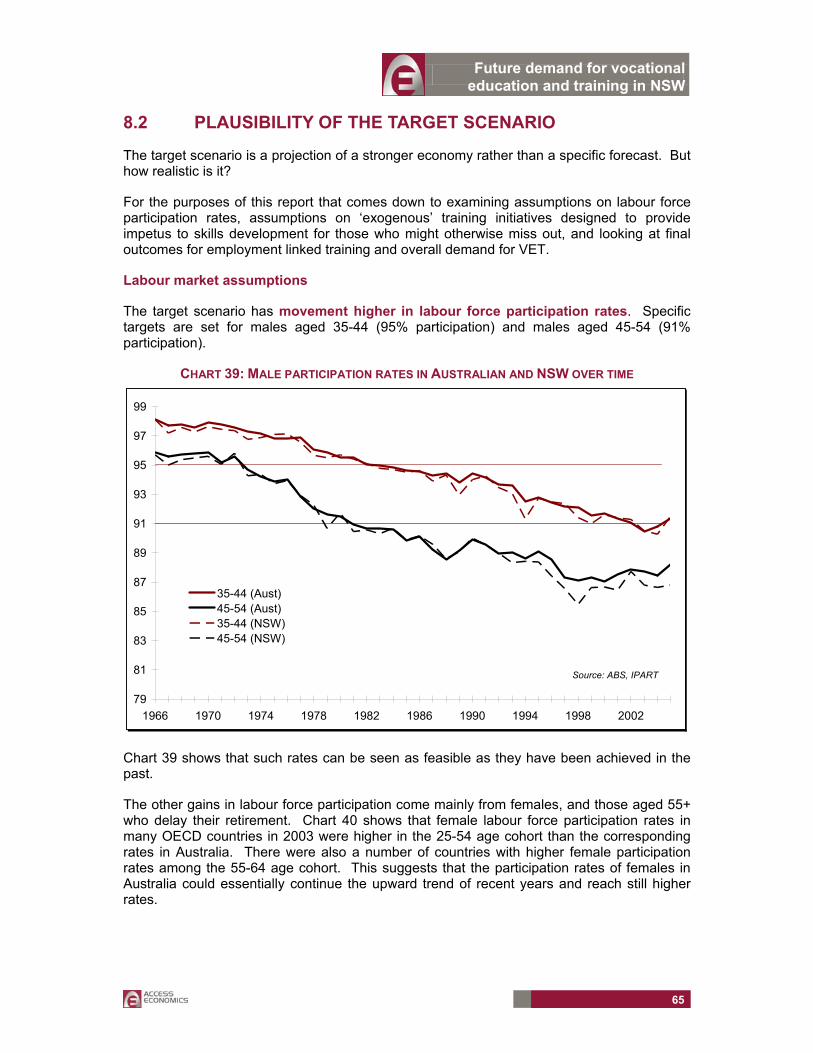

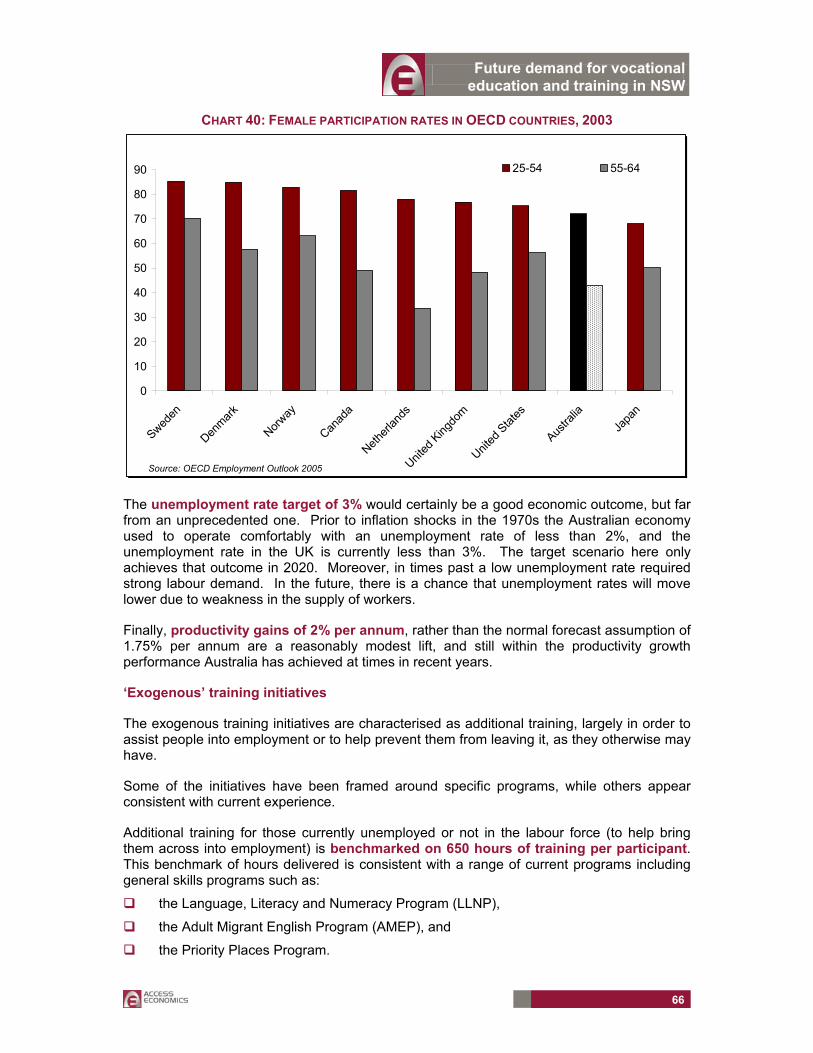

The demand for labour (employment).

Given the first five of the above factors, population growth has already slowed, and it will slow further. In addition, overall participation rates are set to move down in response to the

Future demand for vocational education and training in NSW

31

retirement of the baby boomers. The next decade will therefore be a crunch point in NSW’s demographics.

Access Economics projects a worsening in participation in both Sydney and regional NSW. However, that worsening in participation will be concentrated in regional NSW (especially rural NSW), given both demand pull (its slower job growth) and supply push (its older age profile).

In turn, that points to a greater need for, but probably slower growth in, the use of VET in regional NSW than in Sydney over the next decade.

Future demand for vocational education and training in NSW

32

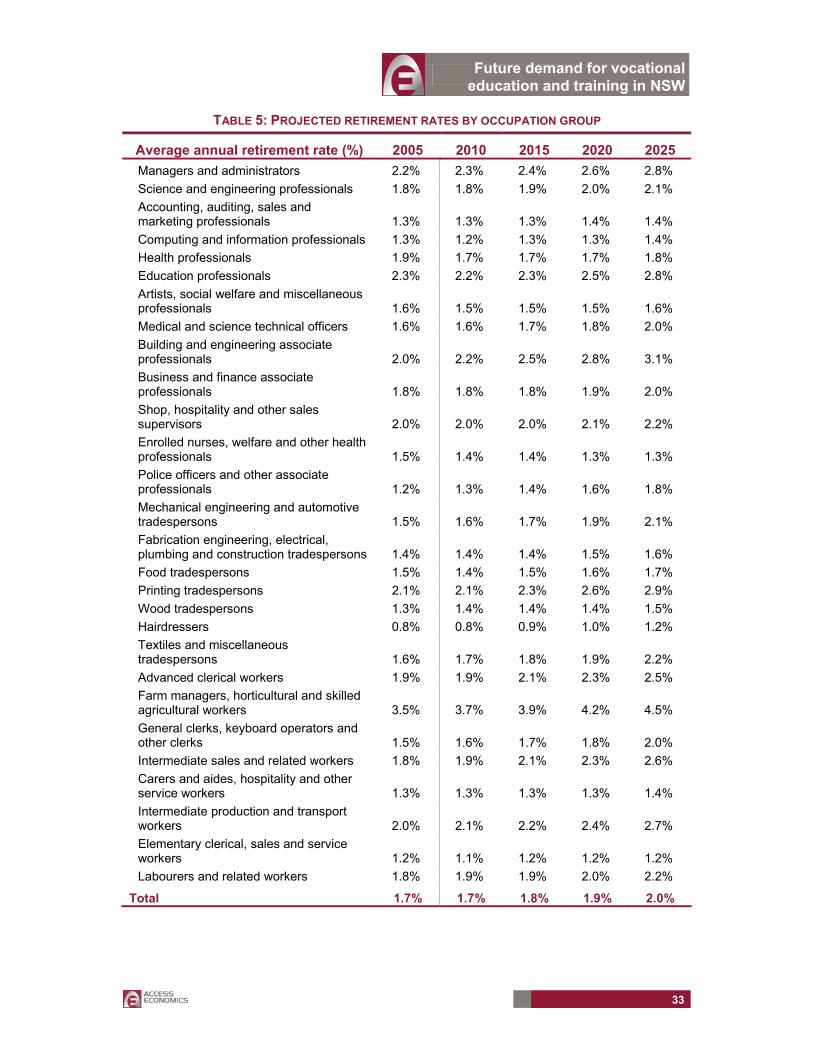

5. ADDITIONAL LABOUR MARKET INFLUENCES ON FUTURE TRAINING NEEDS

While net employment growth trends are a key influence, the gross number of people entering an occupation (including to replace those who retire, or leave for some other reason such as normal turnover), may be more important in assessing training requirements. These are accounted for here in developing projections for future VET.