Embed Size (px)

Citation preview

FUTURAROYALTIES

FOLLOWING THE SMART MONEYIN THE OIL PATCH,

ONE MINERAL AT A TIME.

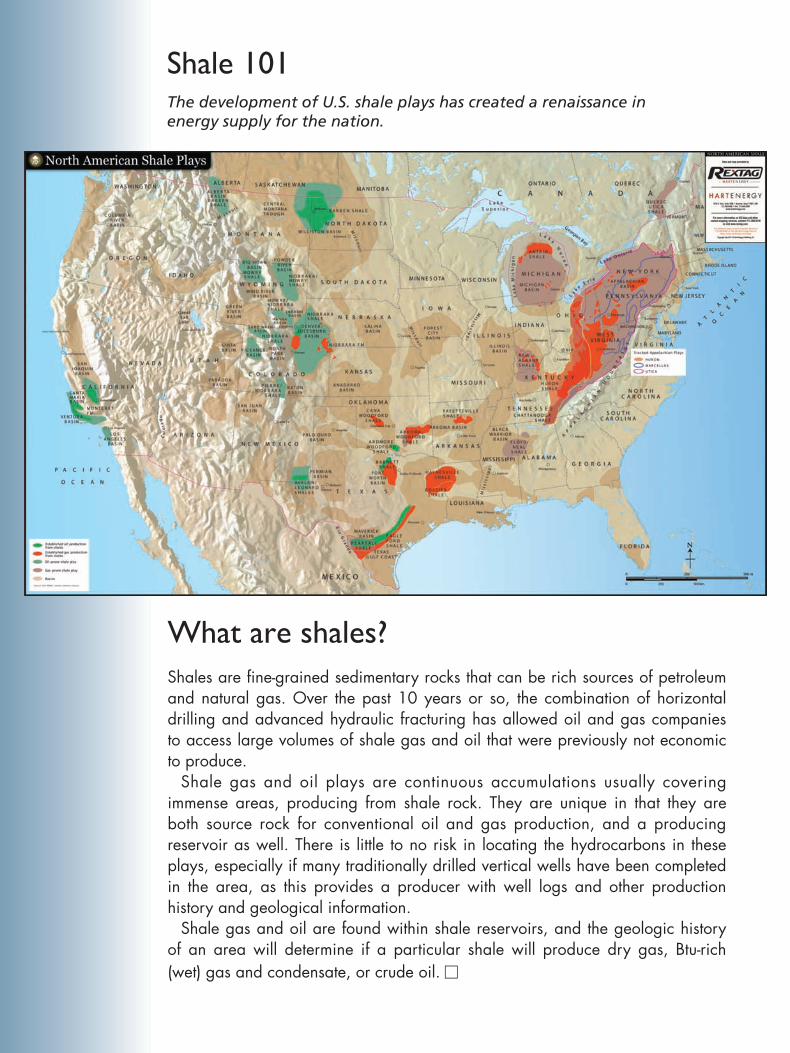

The development of U.S. shale plays has created a renaissance inenergy supply for the nation.

Shale 101

What are shales?Shales are fine-grained sedimentary rocks that can be rich sources of petroleumand natural gas. Over the past 10 years or so, the combination of horizontaldrilling and advanced hydraulic fracturing has allowed oil and gas companiesto access large volumes of shale gas and oil that were previously not economicto produce.

Shale gas and oil plays are continuous accumulations usually coveringimmense areas, producing from shale rock. They are unique in that they areboth source rock for conventional oil and gas production, and a producingreservoir as well. There is little to no risk in locating the hydrocarbons in theseplays, especially if many traditionally drilled vertical wells have been completedin the area, as this provides a producer with well logs and other productionhistory and geological information.

Shale gas and oil are found within shale reservoirs, and the geologic historyof an area will determine if a particular shale will produce dry gas, Btu-rich(wet) gas and condensate, or crude oil. !

June 2013 • futuraroyalties.com 1

The energy industry in the U.S. is booming. The expansion inunconventional resource development, driven by vast shaleplays such as the Marcellus, the Bakken and more, hascompletely rewritten the U.S. energy book. In fact, the shaleboom has vaulted the U.S. into the top tier of energy

producing nations, and many experts believe the U.S. will be self-sufficientin oil and natural gas by 2020.

Oil and liquids production is reaching new heights. The pros and cons ofexporting natural gas as liquefied natural gas are being debated, a reflectionof the massive supplies of natural gas being contributed from the shales.And, the investments being made to fund exploration, development andtransportation of these huge resources are just as impressive.

One of the reasons so much investment is flowing into the resource playsin the U.S. is that drilling risk has been significantly lowered. The geologyin the shales is for the most part well known, and technologies such ashorizontal drilling and fracture stimulation have enhanced drilling andcompletion of wells.

Buying mineral royalties has for years offered an avenue for individualsto participate in the energy industry in the U.S. This report focuses on aninnovative approach developed by Futura Royalties for sophisticatedinvestors to invest in the shale boom. The company purchases mineralsunderneath where some of the largest publicly traded companies aredrilling. The idea is to invest in pre-producing wells, or “early royalties.”

Read on to find out more about today’s investment climate; how royaltyinterests work and the role they can play in a sophisticated investor’sportfolio; and a shale play that offers a case study of resource royaltyinvesting.

—Leslie Haines, Editor-In-Chief

Information contained herein is believed to be accurate; however, its accuracy is notguaranteed. Investment opinions presented are not to be construed as advice or en-dorsement by Oil and Gas Investor. This report was underwritten by FuturaRoyalties.

Introduction1616 S. Voss, Suite 1000Houston, Texas 77057-2627713-260-6400 Fax: 713-840-8585www.oilandgasinvestor.com

Editor-In-ChiefLESLIE HAINES713-260-6428, [email protected]

Managing EditorSUSAN KLANN303-377-8378, [email protected]

Contributing EditorGREGORY DL MORRIS

Art DirectorMARC CONLY

Production DirectorJO POOL713-260-6404, [email protected]

For additional copies of this publication,contact customer service at [email protected]

PublisherSHELLEY LAMB713-260-6430, [email protected]

Director Business DevelopmentPHIL THOMPSON713-260-6466, [email protected]

Copyright 2013, Oil and Gas InvestorHart Energy Publishing LP, Houston, Texas

Table Of Contents

RESOURCE ROYALTIES IN AN UNCERTAIN INVESTMENT CLIMATE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2

FUTURA ROYALTIES: BUILDING WEALTH ONE MINERAL AT A TIME . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4

MINERAL RIGHTS & ROYALTY INTERESTS . . . . . . . . . . . . . . .6

FOCUS ON THE NIOBRARA . . . . . . . . . . . . . . . . . . . . . . . . . . . . .7

2 Futura Royalties • June 2013

One of the most telling stories from the stockmarket crash of 1929 was told by financierand film impresario Joseph P. Kennedy Sr.,father of the future president. He sold offmost of his holdings well in advance of the

collapse, and explained afterward that he knew the stockmarket had become overrun with people who did notknow what they were doing, because he was given stocktips by shoeshine boys and cab drivers.

At the time, of course, it seemed lunacy to sell out. Stockswere soaring to all-time highs, and money was piling intothe market. But beyond Wall Street, there were signs thatthe economy was laboring, and there were sharp disagree-ments in Washington as to whether to stoke up the econ-omy or to put down the damper.

In short, there was uncertainty, much as there is today.Over the first quarter of 2013, the Dow Jones Industrial Av-erage, which is neither industrial nor an average, recoveredto levels not seen since before the financial-sector meltdown

in late 2008. Despite those lofty valuations, however, unem-ployment remains stubbornly high, and wages are stagnant.Many question stock prices, but with interest rates at rockbottom, bonds are no haven for returns.

“The time is right for commodities,” says Juan Espinosa,chief executive officer of Futura Royalties, based in Dallas.To be sure, he is an advocate of most commodities, from pre-cious metals to raw materials to energy, but it is energy heknows best and an energy company he runs. Futura pur-

chases minerals under which the major publicly traded en-ergy companies have elected to drill their multimillion-dol-lar wells. At that time, the rights can be acquired at asignificant discount.

“We are in the early stages of an energy renaissance in theU.S.,” says Espinosa, “and it is happening in people’s back-yards.” He is referring to the shale boom, which has vaultedthe U.S. into the top tier of oil and gas producing nations.The International Energy Agency (IEA) has forecast thatthe U.S. could pass Saudi Arabia as the top oil producer by2020. Most industry analysts expect the U.S. to be self-suffi-cient in oil and gas by then, and there are already plans toexport natural gas. Oil exports are not beyond consideration.

There are several ways that sophisticated investors can in-vest in the shale boom. Some of the major oil and gas pro-ducing companies, as well as some drilling and service firms,are publicly traded. But many of the smaller operators thatare making big gains are privately held, either by thefounders or by hedge funds and private-equity interests.

There are also exchange-traded funds and other vehiclesfor buying oil and gas directly, but in realitymost of them do not hold physical hydrocar-bons. They only trade against an indexlinked to the prices of the commodities.

In rare cases it is possible for a wealthy in-vestor to take a working interest in a well,but that is an extremely complex and illiquidposition. Direct investment also put the in-vestor on the hook for capital calls: whenthere is a need for fresh cash, all participantsare required to contribute in proportion totheir holdings.

Royalties RationaleIt might seem odd that for an industry as

old as oil and gas, there has not been a readyway for high-net-worth investors to partici-pate. But as Espinosa explains, in the old

business model, dry holes, wells from which no commercialoil or gas could be recovered, were a serious risk. To investin one well was more than one person, even a wealthy in-vestor could do, and more risk than any prudent investorwould take.

Now, however, in the shale plays, the geology is wellknown. There is little risk of a dry hole. The profitability ofa well or a field is in the skill of the operator, the executionof the well completion, and the economies of scale that can

Resource Royalties In An Uncertain Climate

“When sophisticated

investors buy royalty rights,

they don’t have to bet the

farm,” says Juan Espinosa,

chief executive officer,

Futura Royalties.

Investment Strategies

Regardless of stock market ups and downs, high net-worth investorsseek steady streams of returns from their portfolios.

be realized from infilling, drilling wells between those alreadycompleted to increase total production.

“When sophisticated investors buy royalty rights, theydon’t have to bet the farm. It is very diversified, and whilethere is always some risk, they can spread their investmentacross multiple wells, different shale basins, and several dif-ferent operators. There is some cash flow, but primarily, it is along-term play, for patient investors, not for hot money.”

That said, there is a ready secondary market if investors dohave to liquidate part or even all of their holdings. “We dis-courage hot money, we want investors, not traders,” says Es-pinosa. “But we understand that things come up and evenlong-term investors can need liquidity. There is an activemarket for royalties from producing wells. Anyone can lookat websites and see all the familiar logos. We love that mar-ket because they love to buy what we like to sell.”

Returning to his original theme of commodities, Espinosasays it is important for investors to see the writing on thewall. “Real things matter, minerals and energy. That is thebig picture.”

He explains that it is easy for investors to become discour-aged when they see stock valuations inflated, bond yields de-pressed, gridlock in Washington, and interest rates held atvery low levels to facilitate the debt.

“I am a realist, not an alarmist,” says Espinosa, “but any pru-dent investor would be concerned about some of the thingsgoing on in finance around the world. Take Cyprus: It is an ex-periment on a little Mediterranean island to see if a bailout forbanks can be funded in part by giving wealthy Europeans ahaircut. People who have their savings in a bank are morethan just depositors, they are almost like shareholders. It is get-ting harder and harder to trust the system.

“What investors—especially wealthy investors—need is tan-gible assets.”

Indeed, one of the cardinal rules of investing is diversifica-tion, and not just among stocks or bonds but across all assetclasses. The challenge for investors who seek to follow thatprudent advice is that while stocks and bonds are easy to buyand sell, the same is not always true of other asset classes,particularly commodities.

“There is a new awareness among affluent investors,” saysEspinosa. “Students of history know that we are in new terri-tory. We are seeing behavior from our financial institutionsthat we have never seen before.”

He explains that even if deposits are safe, interest rates areat historic lows, so returns are scant. In contrast, the stockmarket is hitting new highs, despite chronic high unemploy-ment and poor returns in many sectors. Clearly, there aremany disconnects in the financial sector, and prudent in-vestors need to protect themselves. !

June 2013 • futuraroyalties.com 3

Life is what happens to you while you are busy making other plans. That saying is often attributed to singer John Lennon,but the oldest documented citation is from Readers Digest in 1957. Regardless of its provenance, it is as popular as it istrue, and it especially applies to retirement planning.

Even investors who know about and practice diversification find it hard to follow the only rule that is more important:pay yourself first. The vast majority of people save for retirement out of what is left after all the bills are paid, which oftenmeans there is nothing left. Those that do manage to save almost universally save too little. Some financial services firmshave been raising awareness on this vital issue; one asks in its ads, “what’s your number?” as in, how much does a personor a couple need to retire?

The answer is often a shock, because thanks to high living standards and ready access to premier medical care, a personplanning to retire at 65 could easily be looking at 20 years of active retirement. Planning for that long a stretch, especiallyfor active people, is beyond the scope of this article, but long-term stable investments are the foundation of any retire-ment plan.

Juan Espinosa, chief executive officer of Futura Royalties, notes that within an Individual Retirement Account (IRA)or other such tax-deferred vehicle, the income stream that comes from oil and gas royalties becomes a retirement-savingsmachine. He stresses that he is not a retirement planner, but he adds that an investment that throws off cash, as pre-pro-duction royalties do, can act like a mill within an IRA.

“Dollar-cost averaging is another basic tool in investment, especially true in retirement planning,” says Espinosa.“Within an IRA, the royalty checks investors get can be that regular, reliable source of cash for investing in other assets,all tax-deferred under the retirement plan.” Outside an IRA the only tax advantage to royalties is a 15% federal depletionallowance, he adds. That still makes them a good investment, but offering no special tax advantage.

Futura uses the services of Advanta IRA, a specialist firm based in Fort Lauderdale, Florida, working specifically withsenior associate Doug Robertson. “We do business only with them because they are very professional,” says Espinosa.“They are experts at execution and can handle an IRA transfer in just a few days.” !

Relating Royalties To Retirement

PH

OTO

BY

PET

ER P

IAZZ

A

4 Futura Royalties • June 2013

One of the greatest insights in American busi-ness history came from the California GoldRush of 1849. There was fabulous wealth tobe made by a very lucky very few who hitgold, but most of the miners barely covered

their expenses with the yellow metal they could wrest fromthe ground, and many thousands went bust entirely. Theonly reliable way to make money was not to mine the earthbut to mine the miners: supplying them with tools and ser-vices. The expression has been attributed to Levi Strauss,who patented copper-rivet denim pants, but it was a com-mon expression of the time.

A similar revelation led to the founding of Futura Royal-ties in 2002. Juan Espinosa, whose father had been involvedin the oil and gas business in their native Colombia formore than 40 years, came to the U.S. and worked his wayup to being one of the top producers, despite being theyoungest, at the largest independent oil and gas royalty pur-chaser in the country.

“My father and I were investors in that company,” saysEspinosa, now chief executive officer of Futura.

The realization Espinosa had was not literally to mine theminers but if several companies had built such a thrivingbusiness buying oil and gas royalties, then there was money

to be made selling those royalties. Espinosa explains thatmost royalty buyers are only interested in flowing wells, onewith at least six months of production history.

“At that point you are buying a clear stream of revenueand it is fully valued,” says Espinosa. “When it was time togo out on my own my thought was that if people are buyingthese proven royalties, there must be an opportunity to getin ahead of the drillbit before the well is flowing when thereis more risk so the royalty rights can be acquired at a deepdiscount, sometimes 10 to 15 cents on the dollar.”

At the time, many people were buying royalties on theGulf Coast of Louisiana, Espinosa recalls. “I contacted mycolleague Danny Tabally and he thought the idea of acquir-ing pre-producing, or early royalties was great. The onlytrouble was, we did not have a dime. We put our first privateplacement memo on our credit cards.”

In that present-at-the-creation story there is another simi-larity to the Levi Strauss legend, this part of it true: Straussnever claimed to have invented the copper-rivet idea. Fromthe start, he credited a tailor in Reno, Nevada, Jacob Davis,who wrote to Strauss to report success with the innovation. Inthose Wild West days Strauss likely could have just taken theidea as his own. But he collaborated with Davis on the patent,then took the tailor into the company as production manager.

In the same way, Espinosa says the idea of buying and sell-ing all or part of a royalty right in a pre-producing well isnothing new. “People buy and sell them all the time. It is astandard way of compensating lawyers and accountants andothers who work on a mineral development project.”

A Dedicated BusinessWhat Espinosa did was to make an off-hand transaction

the focus of a dedicated business, to bring in a talented andtrusted partner, and to stress transparency in a business notexactly celebrated for full and clear disclosure.

Futura hummed along buying conventional oil and gasroyalties primarily on the Gulf Coast for seven years. Thenin 2008 the company followed one of the biggest names inindependent exploration and production, Chesapeake En-ergy Corp., into northern Louisiana to an unconventionalgas play called the Haynesville shale. Shale development,where producers drill into the thin, dense layers where oiland gas are actually created by geological processes, was pio-neered in Futura’s back yard, the Barnett shale west of FortWorth.

“We had a practice of following the big names, the suc-

“Futura has been successful

following the top names

in the industry and acquiring

pre-producing royalties in the

areas where they are concentrating

their development efforts,” notes

Juan Espinosa, chief executive officer,

Futura Royalties.

Futura Royalties: Building WealthOne Mineral At A TimeThe company’s strategy is buying and selling all or part of a royalty right in pre-producingwells to high-net-worth investors.

Profile

cessful developers,” says Espinosa. To be clear, there is no for-mal relationship between Futura and the oil and gas produc-ing companies like Chesapeake. Espinosa stresses that when aproducer buys or leases mineral rights, it usually pays a sign-ing bonus to the owner, along with a monthly lease payment,as well as a royalty payment. That royalty is a percentage,often 12.5%, of the value of whatever oil and gas flows out ofthe well. The rights to that monthly royalty check from theproducer can be bought and sold, traded or inherited, justlike any other property.

“When we were in the business of buying early royalties inconventional wells, on the Gulf Coast or wherever,” Es-pinosa recalls, “there was always the risk of a dry hole. Wewent on runs where there were a lot of dry holes, and thenruns where there were big hits, big producers. That was justthe nature of the business. When we got into the Haynes -ville and we got to know shales we knew we had to reviseour business model.”

Espinosa notes that by drilling into source rock, producingcompanies almost always find commercial hydrocarbons. Dryholes do occasionally happen, but they are rare. “Wechanged our philosophy,” he says. “We got out of that tradermentality because we did not have to move from well to well,from dry hole to producer. Just about every well is a pro-ducer.”

Oil and gas companies that concentrate on shale produc-tion talk in terms more common to manufacturing or evenfarming. They drill wells all around their shale acreage, findthe best producing zones and sections, then try to fill in asmany wells as they can in those hot spots. Directionaldrilling makes it possible to drill down one vertical wellboreand then out in several different directions around the com-pass, pushing the bore laterally through the plane of theshale.

The Smart MoneyReiterating that there is no formal collaboration between

oil and gas companies and royalty firms like his, Espinosa

notes that Futura has been successful following the top namesin the industry and acquiring pre-producing royalties in theareas where they are concentrating their development efforts.For example, Futura followed Chesapeake and EOG Re-sources into the Niobrara play in Colorado and Wyoming.

There is plenty of outside corroboration. In an April 11feature, CNBC featured Noble Energy Inc., an oil and gascompany. The profile started highlighting Noble Energy’s in-ternational position, but quickly turned to emphasizing itsU.S. shale plays, especially the Niobrara.

“Look at Noble Energy,” Espinosa adds. “They are putting45 cents of every dollar into that play. That is their money,their shareholders’ money. And that is the smart money. Welike to think that we are a smart company, and that we havesmart investors with us.”

Specifically he means that select high-net-worth individu-als can become investors with Futura. Espinosa or one of hissmall staff vet each potential investor personally. “We don’t

want traders,” he says. “There are other places where theycan do that. We don’t want gamblers. We want people whounderstand the importance of real, tangible assets as an in-vestment class. People who have net worth of at least $1 mil-lion exclusive of their residence, and income of at least$200,000 for an individual, $300,000 for a couple.”

Espinosa says that Futura is in the market every day buyingearly royalties at discount. “We buy up front with our owncapital. We buy and hold, but if the need to liquidate cameup, we can access the secondary market with six months’worth of check stubs,” he says.

“We have a large base, and we make some of that availableto the accredited investors who work with us,” Espinosa ex-plains.

“We allow them to purchase slivers of the mineral rightswe have purchased with our own capital, then they have theroyalty right free and clear. They get the royalty check everymonth from the producer. We never touch other people’smoney. We just show them what we have bought and whatwe are making available to them.” !

June 2013 • futuraroyalties.com 5

PH

OTO

BY

LOW

ELL

GEO

RG

IA

6 Futura Royalties • June 2013

Mneral rights and royalty interests, common ifsometimes complex investments in the U.S.,are a prime example of what is sometimes de-rided as American exceptionalism. In this case,at least, the U.S. is truly exceptional: In most

of the rest of the world, the government owns all the mineralrights to metals, coal, oil and gas. If real estate is owned byprivate individuals or companies, it is only the surface rightsthey actually hold. But in the U.S., private property rights gostraight to the core of the Earth, a principle that goes straightto the core of Futura’s business model.

“People hear about surface rights and mineral rights androyalties all the time,” says Juan Espinosa, chief executive offi-cer of Futura Royalties, based in Dallas. “Land owners in tradi-tional oil and gas producing areas have heard about them alltheir lives. People in areas that are just now being developedfor unconventional resources like shale are just starting tohear about them. But they don’t think they are unusual.

“I come from Colombia, where my father was in the oilbusiness for 40 years, and sometimes it takes someone fromanother country to realize that what Americans have isunique and valuable.”

As with most business concepts, the basic ideas are simple,but they get increasingly complex as operators and investorsrespond to needs for capital and return. In most cases, on pri-vate land, the owners of the surface also own the mineralsbelow their surface holding. They own not just the flat squareof land on the surface, but the whole cube of Earth below, in-cluding any minerals. For all practical purposes, “rights” and“interests” mean the same thing, but for clarity, the termsmineral rights and royalty interests will be kept constant inthis article.

In many states, the ownership of those minerals can beseparated, or severed, from the surface ownership. In somestates they cannot be separated. Ownership of mineral inter-ests includes the right of access—the legal ability to get atthe minerals and bring them to the surface and to market.

Importantly, neither mineral rights owners nor royalty in-terest holders pay anything for development. Quite to thecontrary, they are paid by the developers. That is a signifi-cant difference from taking a working interest in a well orfield. A working interest means just that: investing in thecosts of development—including the payments to mineralowners and royalty interests—and taking a proportionalshare of any profits.

How The Business WorksIn oil and gas development, oil companies and the ser-

vice companies they hire to drill wells usually only need a

few acres on the surface to gain access to vast deposits of hy-drocarbons. With new directional-drilling techniques, thedrillbit can be steered in any direction once it is at depthand running horizontally for miles through oil- or gas-richformations.

Rights to oil and gas are usually leased, rather than boughtoutright. Sometimes ownership itself is sold; other times, par-tial access rights are sold or leased. Leases always have terms,and usually the rights revert to the owner upon expiration.

In areas where there has been little or no historical devel-opment, mineral rights may be bought or leased from theoriginal surface owners. In areas with historic development,rights may have changed hands many times, been subdividedand combined, inherited and transferred over and over.

Typically a landman representing an oil and gas companywill acquire ownership or lease mineral rights for the devel-oper in an area where the company believes it can make aprofit producing hydrocarbons. Usually the owner of themineral rights will get a signing bonus, cash up front alongwith a lease payment of some kind, and also usually a royaltyinterest in whatever oil or gas is produced from the lease.

That is an essential difference. The mineral owner or lessorusually gets the signing bonus and lease payments regardlessof whether the minerals are developed. The royalties onlycome from actual extraction and sale of the hydrocarbons.Lease rates and signing bonuses vary greatly, from a few hun-dred dollars per acre to thousands, depending on how surethe development company is of finding commercial quanti-ties of oil.

Time FactorThe important fourth dimension in all development is

time. Three-dimensional seismic surveys have become in-credibly sophisticated and detailed in the last decade, but un-like coal or ore deposits that can be estimated with highcertainly, the commercial viability of an oil and gas field isonly known for sure once wells are drilled.

Because of that, royalty payments can be estimated but notassured until the hydrocarbon molecules are flowing up out ofthe well and off to market. Clearly, then, there is some dis-counted value to a potential royalty interest before and evenduring development.

An investor can pay someone who has a royalty interest anup-front payment for all or part of that royalty. The up-frontpayment will be some discount to the full value of the royaltystream, and the discount will vary with the uncertainty ofproduction. Ideally, the royalty owner benefits by havingcash in hand, and the royalty investor benefits from buying apotentially lucrative stream of income at a discount. !

Mineral Rights & Royalty InterestsHere’s a quick walk through the basics of oil and gas ownership,development and payment.

Royalty Primer

June 2013 • futuraroyalties.com 7

Imagine rocket science—incredible high technologywith sophisticated computer analysis, remote controland advanced materials—done not in the cold vac-uum of space, but in the high heat and pressures ofmiles underground. That is the reality of the shale-

gas and oil boom in the U.S.But while the space race was followed closely in headlines

and live broadcasts, the new era of energy production, withthree-dimensional (3-D) seismic imaging, directionaldrilling and hydraulic fracturing, has been changing theworld of oil and natural gas production since the 1980s,without any fanfare. If current predictions for the outputfrom the new techniques are even close, the new era of oiland gas production will change national and global energyeconomics for decades to come.

Commercial oil and gas production in the U.S. predatesthe Civil War. And for almost a century and a half, the tar-gets for drilling were pools of oil and gas that had migratedfrom the rocks where they were formed and become trappedin what became reservoirs. Often these were porous forma-tions such as sandstone that acted like a sponge. The largepore spaces allowed the oil to flow easily within and thenout of the rock when it was tapped. When there was suffi-cient natural gas pressure, or “drive,” as drillers call it, the oil

would shoot out of the well as a gusher—spectacular, butdirty, dangerous and wasteful.

Oil companies knew about the kerogenic formationswhere oil and gas were formed. Organic material was trappedin silt and clay that was heated and compressed over hun-dreds of millions of years. In many cases, huge amounts of oiland gas were still trapped in those shales, because the poresin the rock were so small that the oil and gas couldn’t mi-grate out of the rock. That is why the layers are called“tight” formations.

Shale is often found in layers that may be only a few feet

or a few dozen feet thick, but cover vast areas. Hundreds ofthousands of wells had penetrated into and through suchshales over the years, but despite the shales’ rich hydrocar-bon content, they were not commercially viable for severalreasons. In vertical wells, not enough of the thin formationwas exposed to the wellbore, and as noted, the hydrocarbonscould not flow easily out of the rock.

Directional drilling made it possible to drill horizontallyalong the plane of a shale formation, running the bore as faras two miles laterally through the shale. Hydraulic fracturingcracked the rock for a few dozen feet around the borehole inevery direction, opening tiny fissures that allowed the oiland gas to flow out of the tight formation.

Shale Development BeginsThose techniques were pioneered in the Barnett shale westof Fort Worth, Texas, and much of that formation is still inproduction 30 years after the first wells were drilled. Afterthe viability of shales was established, oil companies anddrilling operators looked back at their maps and surveys andwent after shales everywhere: in the Haynesville inLouisiana, the Bakken in North Dakota, the Eagle Ford inSouth Texas, the Utica in Ohio, and the Marcellus in Penn-sylvania, New York, and West Virginia. And they went afterthe Niobrara shale in Colorado and Wyoming.

Some of the shales produce mostly gas, others mostly oil,others a mix. The Niobrara is a predominantly liquids-richplay of oil and natural gas liquids in eastern Colorado. Re-cent wells in one area, the Piceance (PEE-ahnse) Basin ofwestern Colorado, have produced dry gas from the Niobrara.

While the Niobrara formation extends from Canada toMexico, only certain parts of the formation are capable ofproducing oil and gas. According to the Colorado Oil & GasAssociation, the most productive zones are in the Denver-Julesburg Basin (D-J Basin) in northeast Colorado andsoutheastern Wyoming. Exploration activities in Coloradoare occurring around the state, including the northwesterncounty of Moffatt, the Piceance Basin, and southeasternColorado’s El Paso County. The Niobrara formation is com-posed of two structural units: the Smoky Hill Chalk, and theFort Hays Limestone below.

The average depth for Niobrara petroleum-producingzones is about 7,000 feet. As the Niobrara extends east, theplay becomes shallower, only reaching depths of around3,000 feet. The Niobrara is still a relatively new play—stillin the exploration phase. Consequently, estimated reservefigures vary greatly. Some analysts have assessed the play atapproximately 2 billion barrels of recoverable oil reserves.

Two of the most notable wells drilled in the formationare EOG’s Jake well and Noble Energy’s Gemini well. The

Producers have high expectations for Colorado and Wyoming’s Niobrara shaleplay, as development ramps up.

Focus On The Niobrara

For the Niobrara, one outsideperspective comes from how

prominently that play figures in theanalysis of companies that are activein many producing areas across the

country and around the world.

Niobrara Shale

8 Futura Royalties • June 2013

Jake, which was drilled in October 2009, produced an aver-age of 1,750 barrels of oil per day for the first few days, pro-ducing 50,000 barrels over 90 days. Noble Energy’s Geminiwas completed using a 16-stage fracture treatment and pro-duced 1,110 barrels per day at its peak.

Niobrara PotentialThe Niobrara has taken longer to be well understood by

drillers and producers, because its geology is more variablethan that of some other major shale plays. But recent reportsfrom the major producers active in the formation indicatethat many of the drilling and completion challenges arebeing resolved. Indeed, many counties are setting records forproduction, and there is a strong sense that a breakout is athand.

Many industry analysts concur. In a comprehensive in-vestment review released in February, Morgan Stanley Re-search published an exploration and production evaluationof the Niobrara and concluded that “the Niobrara is on thecusp of broad delineation, which we expect in 2013. As hasbeen clear in earnings so far [in the first] quarter, results areoutperforming expectations and productive areas continueto expand. We believe this will be the ‘must own’ play thisyear.”

Oil and gas producers in the play say that several factorsare coming together, beginning this year. One is the increas-ing length of lateral legs of horizontal drilling. In the com-plex geology of the Niobrara, drilling laterally is not assimple as “landing” the bore from vertical to horizontal andthen racing along. Players report well design and completiontechniques are starting to mature from experimentation tostandardization.

Noble Energy Inc., one of the biggest operators in theNiobrara, plans to drill 60 long laterals in 2013, a manifoldincrease from its 2012 program of only about a dozen long-lateral wells. Noble has reported at least three wells with atleast four months of production history that are outperform-ing their projected performance, known as the “type curve.”

Notably, the curve for each field and type of well is con-stantly revised, so consistent production over many monthsand across several wells can mean a change in the typecurve. That is relevant to investors, because the value of awell or a field or a play is determined by independent audi-tors using many data points, including type curves. And, ofcourse, more production means more royalties.

The increases in production date back to last year.Anadarko Production Corp. reported it increased Niobrara

production to 103,000 barrels of oil equivalent a day in thefourth quarter of 2012, a 13% rise compared to the fourthquarter of 2011. For wells that produce primarily crude oilbut also lighter liquids, as well as some natural gas, all of theoutput is reported as barrels of oil equivalent.

Noble hiked its production to 86,000 barrels of oil equiv-alent per day, a 15% improvement in the fourth quarter of2012 as compared to the fourth quarter of 2011. Bill BarrettCorp. reported gains of 2,570 barrels, a 70% gain quarter-over-quarter, indicating that producers of all sizes are realiz-ing step-change increases in production.

Prudent investors triangulate on any sector or asset class,seeking independent confirmation of trends. For the Nio-brara, one outside perspective comes from how prominentlythat play figures in the analysis of companies that are activein many producing areas across the country and around theworld.

For example, in late January and early February, Baird Eq-uity Research issued reports on Noble Energy and Anadarko,the two top Niobrara players in terms of acreage, and also onWhiting Petroleum Corp., a shale producer best known forits position in the Bakken shale in North Dakota. As mightbe expected, the Niobrara figured large for Noble Energy,but also Anadarko, which has development all over theworld. The Niobrara also came to the fore for Whiting.

“Noble’s D-J Basin acreage remains the focal point of theportfolio as resource potential continues to rise (multipletimes over at this point),” wrote Baird, “with successful ex-tended lateral and density tests supportive of increased re-covery. The productive footprint is also expanding withnorthern Colorado adding another layer of liquids drilling,80% oil, to the region. There is more to come on all frontsin 2013 as Noble further refines its optimal developmentplan; drilling 60 extended laterals including 8/80-acre units,testing a 15-well horizontal pilot, and further delineating.”

Even with activities in half a dozen international plays,“Anadarko has quickly become quite the shale machine,”Baird noted. “Anadarko has done an impressive job of build-ing a deep inventory of shale and other unconventional pro-jects in the Lower 48, including key positions in theNiobrara, Eagle Ford, Permian and Marcellus.”

Specific to the Wattenberg Field section of the Niobrara,Baird reported that Anadarko is currently running 11 rigs inthe play. Optimal spacing and lateral length tests by thecompany continue, though bias is towards 12 wells per sec-tion and longer laterals, as it has successfully tested lateralsout to 10,000 feet.

With plenty of activity in North Dakota, Whiting is “ac-celerating activities in the Niobrara,” according to Baird.“The Niobrara will be a key contributor to future productiongrowth. Whiting is acquiring seismic data and plans addi-tional tests in the Niobrara “A” zone. Well costs are esti-mated at $4.3 million to $5.3 million and estimated ultimaterecovery is in the range of 300,000 to 400,000 barrels of oilequivalent. For full development, Whiting plans to build an-other gas processing plant by the end of 2013 which couldaccommodate up to a six-rig development program in theplay.

“Management remains excited about Niobrara develop-ment, which will be a key contributor to the company’s fu-ture production growth,” wrote Baird, noting that Whitingcompleted the Wildhorse 04-0414H well targeting the Nio-brara “B” zone, with an impressive initial production rate of1,170 barrels of oil equivalent per day. !

PH

OTO

BY B

RIA

N P

AYN

E

14901 Quorum DriveSuite 800

Dallas, TX 75254

Tel: 972-770-0500Fax: 972-770-0565

FuturaRoyalties.com