Embed Size (px)

Citation preview

FUNDAMENTALS VALUATION

SANWARIA AGRO OILS

LIMITED

29th

June 2011

ANALYTICAL CONTACT

Ms. Revati Kasture +91-22-6754 3465 [email protected]

BUSINESS DEVELOPMENT CONTACTS

MUMBAI

Mr. P. N. Satheeskumar +91-22-6754 3555 [email protected]

KOLKATA

Mr. Sukanta Nag +91-33- 2283 1800 [email protected]

CHENNAI

Mr. V Pradeep Kumar +91-44-2849 7812 [email protected]

AHMEDABAD

Mr. Mehul Pandya +91-79-40265656 [email protected]

NEW DELHI

Ms. Swati Agrawal +91- 11- 2331 8701 [email protected]

BANGALORE

Mr. G. Sundara Vathanan +91-80-2211 7140 [email protected]

HYDERABAD

Mr. Ashwini Kumar Jani +91-40-40102030 [email protected]

CARE EQUITY RESEARCH OFFERS

Independent Research of equities on fundamentals or valuations or both

IPO Grading

White Label Research

Valuation of companies for Institutional Investors, Asset Managers and Corporates

Sector Write-ups for Offer Documents of securities

SANWARIA AGRO OILS LTD

1 www.careratings.com

EQUIGRADE

EQUIGRADE – Analytical Power for Investment Decisions

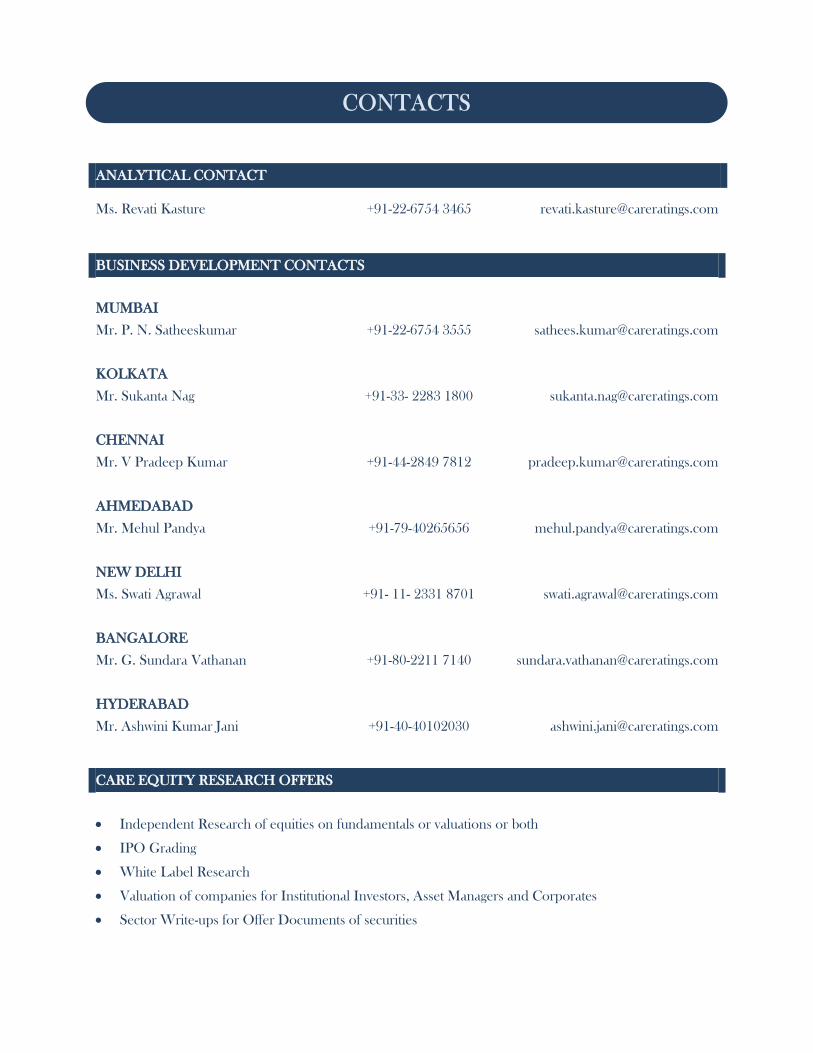

Sanwaria Agro Oils Limited Solvent Extraction Industry

Good Fundamentals; Fairly Priced CMP: Rs. 34.3 / CIV: Rs. 32 Sensex: 18694

CARE Research assigns 3 /5 on fundamental grade to Sanwaria

Agro Oils Limited [SAOL]

CARE Research assigns a fundamental grade of 3/5 to SAOL. This

indicates ‘Good Fundamentals’. The grade draws strength from the

uptrend in the soya oil and soya food products industry coupled

with the expansion in capacity. The soya oil consumption in India

has been increasing over last many years due to the perceived

health benefits of soya oils over other regularly consumed edible

oils. SAOL is a well established player in the soya oil extraction

industry, with efficient procurement channel, warehousing

capabilities and fairly good distribution network. The company also

boasts of higher profit margins in the industry.

CARE Equity Research believes the increased revenue share of

branded refined oil, higher operating rates coupled with SOAL’s

venture into the value added soya products such as textured

vegetable protein (TVP), diversification into other vegetable oils

and vanaspati would help SOAL earn higher margins in the future.

Valuations

CARE Equity Research assigns valuation grade of 3/5 to SOAL

based on the current Intrinsic Value (CIV) of Rs. 32 as against

Current Market Price (CMP) of 34.3, indicating ‘Fairly Priced’ at

CMP. The valuation is arrived using justified P/BV multiple and

verified by the P/S multiple.

29th

June 2011

Financial Information Snapshot

(Rs. Million) FY10 FY11 E FY12 P FY13 P

Operating Income 11,168 15,718 20,518 25,222

EBITDA 677 727 1,908 2,201

PAT 388 534 1,146 1,121

Fully Diluted EPS* (Rs.) 2.2 1.5 2.8 2.7

Dividend Per Share (Rs.) 0.2 0.1 0.2 0.2

P/E (times)

22.3 12.3 12.5

EV/EBITDA (times)

21.1 8.1 7.0

* Calculated on Current Face Value of Rs. 1/- per share

SANWARIA AGRO OILS LTD

www.careratings.com 2

EQUIGRADE

Revenues and profitability affected by agricultural commodity cycles; however uptrend in edible oil

consumption to augur well

Since SOAL’s revenue primarily comprises of sales of de-oiled cakes and soya oil (crude and refined), the

company’s revenues are heavily dependent on the soya production and prices which are in turn linked to the

agricultural commodities cycle both domestic and international.

Soya oil is currently in an uptrend; soya oil prices surged in FY11, with refined soya oil prices in March 2011 at

Rs. 63,000/ tonne - around 50% higher y-o-y and crude soya oil prices at Rs 58,300/ tonne - around 45% higher

y-o-y. Although, there may be a slight correction in prices, CARE Equity Research believes the prices are

expected to be on the higher side for the next two years; above the average prices in FY11.

Given, the current demand supply gap of around 9 million tonnes, and a relatively lower per capita

consumption of edible oil at around 14.5 kgs per annum in India, as compared with the world average of 23.9

kgs per annum, demand for edible oil is expected to rise. After considering the capacity additions of around

15,700 TPD expected in the industry by 2013, there will still to be a substantial demand supply gap. The same

is expected to augur well for SOAL’s business.

Comfortably placed on the soya procurement front; dedicated network of agents; also adequate warehousing

capacity

SAOL is based in the highest soybean growing state and the proximity of the plant to the mandis results in

lower procurement costs. SOAL owns sourcing licenses at over 70 mandis in MP. The company also has

dedicated agents at Mandis for the procurement of soya and other agricultural produce. The company has over

the years built strong relationship with the farmers by making timely payment and also procuring other crops

such as wheat and other food grains during the non-soya season, ensuring income round the year for the farmer

and thereby ensuring purchase of soybean seeds at competitive prices. The company also has adequate

warehousing capacity at its plants, which allows it to store the excess soybean and allows optimum utilization of

processing capacity.

FUNDAMENTAL GRADE Good Fundamentals 3 /5

SANWARIA AGRO OILS LTD

3 www.careratings.com

EQUIGRADE

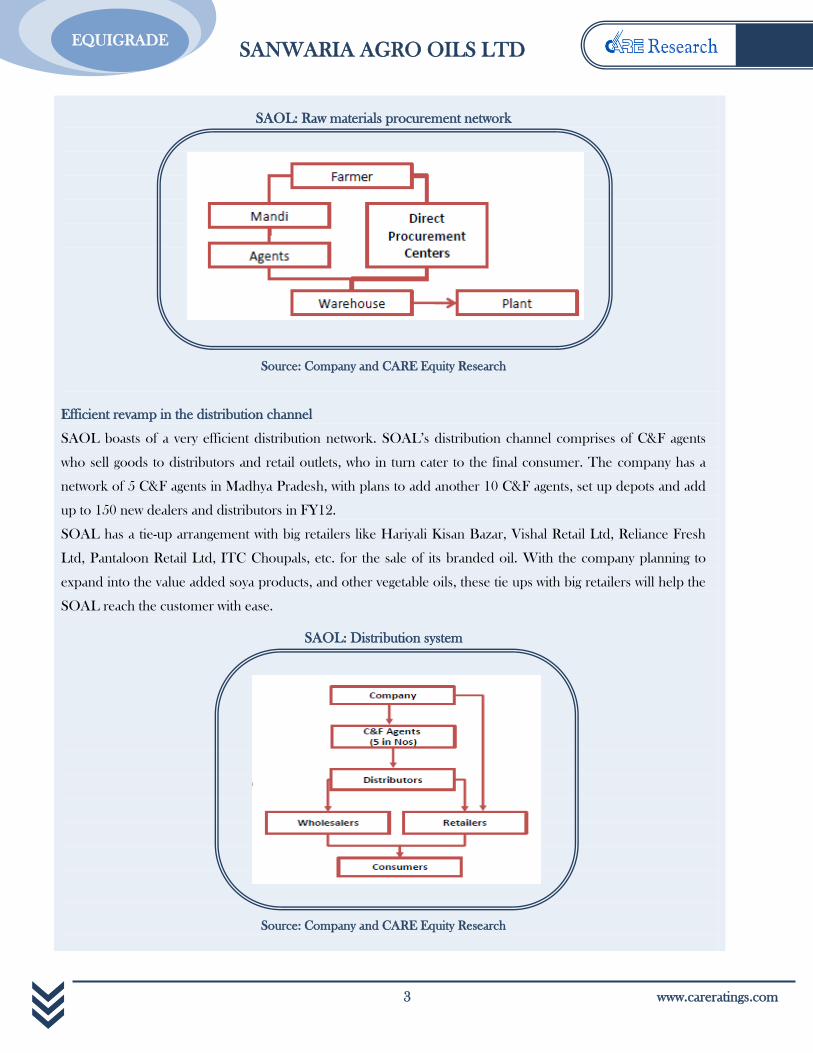

SAOL: Raw materials procurement network

Source: Company and CARE Equity Research

Source: Company and CARE Equity Research

Efficient revamp in the distribution channel

SAOL boasts of a very efficient distribution network. SOAL’s distribution channel comprises of C&F agents

who sell goods to distributors and retail outlets, who in turn cater to the final consumer. The company has a

network of 5 C&F agents in Madhya Pradesh, with plans to add another 10 C&F agents, set up depots and add

up to 150 new dealers and distributors in FY12.

SOAL has a tie-up arrangement with big retailers like Hariyali Kisan Bazar, Vishal Retail Ltd, Reliance Fresh

Ltd, Pantaloon Retail Ltd, ITC Choupals, etc. for the sale of its branded oil. With the company planning to

expand into the value added soya products, and other vegetable oils, these tie ups with big retailers will help the

SOAL reach the customer with ease.

SAOL: Distribution system

Source: Company and CARE Equity Research

SANWARIA AGRO OILS LTD

www.careratings.com 4

EQUIGRADE

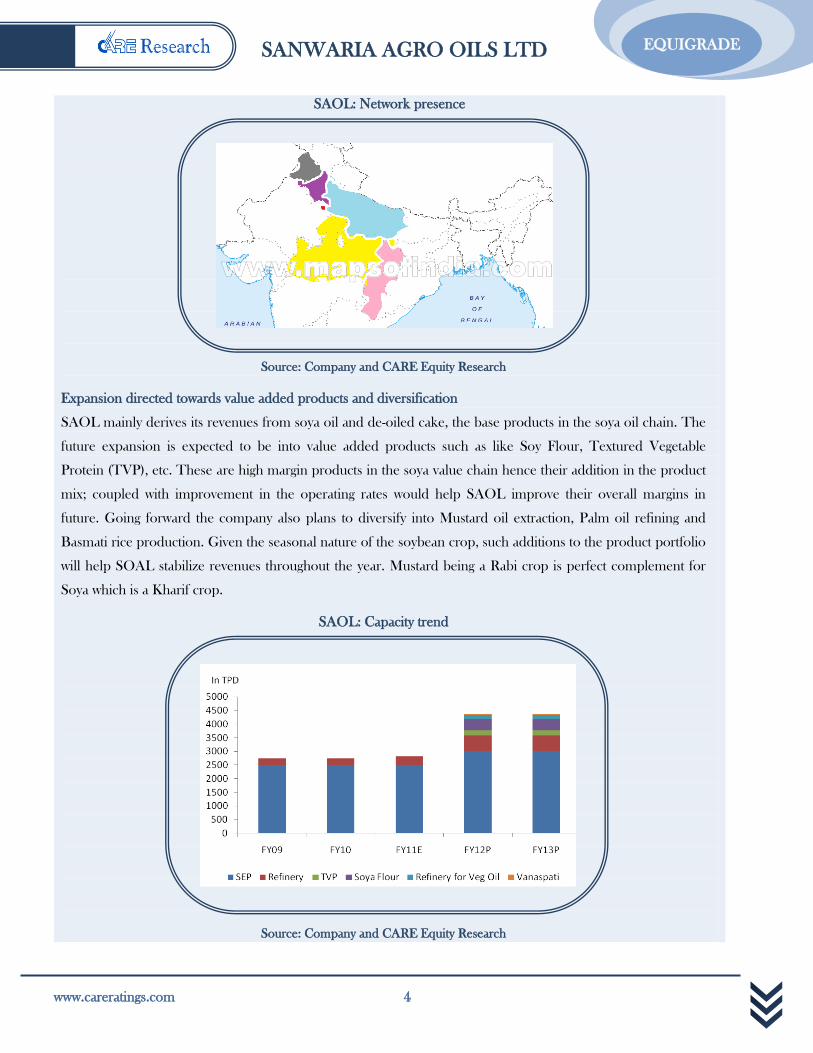

SAOL: Network presence

Source: Company and CARE Equity Research

Expansion directed towards value added products and diversification

SAOL mainly derives its revenues from soya oil and de-oiled cake, the base products in the soya oil chain. The

future expansion is expected to be into value added products such as like Soy Flour, Textured Vegetable

Protein (TVP), etc. These are high margin products in the soya value chain hence their addition in the product

mix; coupled with improvement in the operating rates would help SAOL improve their overall margins in

future. Going forward the company also plans to diversify into Mustard oil extraction, Palm oil refining and

Basmati rice production. Given the seasonal nature of the soybean crop, such additions to the product portfolio

will help SOAL stabilize revenues throughout the year. Mustard being a Rabi crop is perfect complement for

Soya which is a Kharif crop.

SAOL: Capacity trend

Source: Company and CARE Equity Research

SANWARIA AGRO OILS LTD

5 www.careratings.com

EQUIGRADE

New capacity would however be subject to successful placement of fresh equity

SOAL’s expansion plans would require a capital expenditure of around Rs. 240 crores (around Rs 160 crores

for plant & machinery). The company plans to finance the same through a mix of internal accruals, promoter

capital and fresh equity issue. The internal accruals are expected to be around Rs. 40 crores. The balance of Rs

200 crores is expected to be through a fresh equity issue. Although, as per the discussion with the management

the capital through the fresh issue should be raised in couple of months, CARE Equity Research feels any delay

in the same would affect the expansion and thereby the growth in revenue and profitability. Also, per share

valuation of the fresh issue is yet to be determined, and hence the true impact of dilution cannot be ascertained

completely.

SAOL: Capital Expenditure

Source: Company and CARE Equity Research

Management succession not an issue

SAOL’s management is well experienced in the solvent extraction industry. SAOL’s present chairman and

promoter, Mr Ram Narayan Agarwal, has more than 45 years of experience in the solvent extraction industry.

Though a non-executive director, he still guides the management of the company and oversees all the major

decisions of the company. He is assisted by his four sons, who looks after day to day workings of the company

and ensures smooth running of SAOL under the guidance of Mr. Ram Narayan Agarwal. CARE Equity

Research believes that management succession is not a cause of concern with SAOL owing to the personal

involvement of the four sons of Mr. Ram Narayan Agarwal.

Capacity In TPD Rs. Mn

SEP 1000 201.4

Refinery (Soya Oil) 325 99.5

TVP 200 535.0

Soya Flour 400 485.0

Refinery (Other Veg Oil) 150 249.6

Vanaspati 50 95.5

SANWARIA AGRO OILS LTD

www.careratings.com 6

EQUIGRADE

In compliance with the listing agreement 49

The company has 12 Board of Directors, with 4 of them being Executive, 2 Non-Executive and 6 Non Executive

and Independent Directors. The board has formed 3 sub committees for audit, remuneration and investor

grievances. The audit board has 3 members, all Independent and Non-Executive, headed by Mr. Santosh Kumari

Tiwari. The remuneration and investor grievances committee too has 3 members each and is again formed of

Independent and Non–Executive directors. As per the annual report the same is in compliance with the listing

agreement of the stock exchanges.

SANWARIA AGRO OILS LTD

7 www.careratings.com

EQUIGRADE

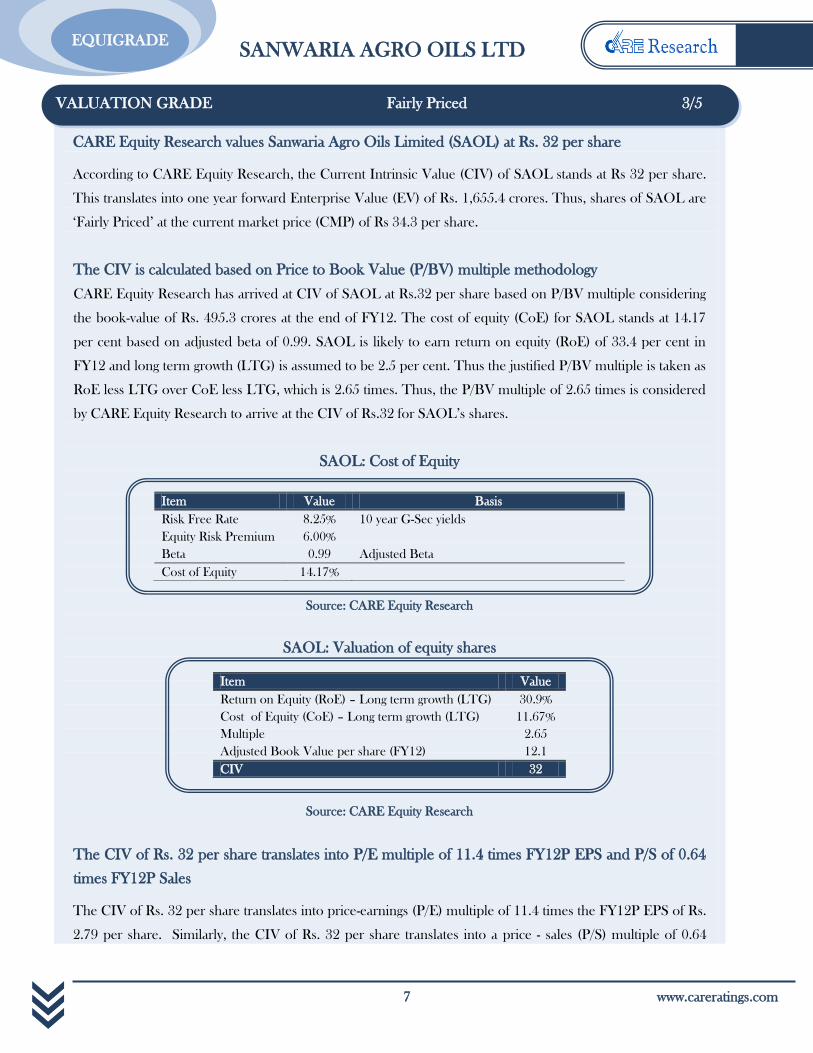

CARE Equity Research values Sanwaria Agro Oils Limited (SAOL) at Rs. 32 per share

According to CARE Equity Research, the Current Intrinsic Value (CIV) of SAOL stands at Rs 32 per share.

This translates into one year forward Enterprise Value (EV) of Rs. 1,655.4 crores. Thus, shares of SAOL are

‘Fairly Priced’ at the current market price (CMP) of Rs 34.3 per share.

The CIV is calculated based on Price to Book Value (P/BV) multiple methodology

CARE Equity Research has arrived at CIV of SAOL at Rs.32 per share based on P/BV multiple considering

the book-value of Rs. 495.3 crores at the end of FY12. The cost of equity (CoE) for SAOL stands at 14.17

per cent based on adjusted beta of 0.99. SAOL is likely to earn return on equity (RoE) of 33.4 per cent in

FY12 and long term growth (LTG) is assumed to be 2.5 per cent. Thus the justified P/BV multiple is taken as

RoE less LTG over CoE less LTG, which is 2.65 times. Thus, the P/BV multiple of 2.65 times is considered

by CARE Equity Research to arrive at the CIV of Rs.32 for SAOL’s shares.

SAOL: Cost of Equity

Source: CARE Equity Research

SAOL: Valuation of equity shares

Source: CARE Equity Research

The CIV of Rs. 32 per share translates into P/E multiple of 11.4 times FY12P EPS and P/S of 0.64

times FY12P Sales

The CIV of Rs. 32 per share translates into price-earnings (P/E) multiple of 11.4 times the FY12P EPS of Rs.

2.79 per share. Similarly, the CIV of Rs. 32 per share translates into a price - sales (P/S) multiple of 0.64

VALUATION GRADE Fairly Priced 3/5

Item Value Basis

Risk Free Rate 8.25% 10 year G-Sec yields

Equity Risk Premium 6.00%

Beta 0.99 Adjusted Beta

Cost of Equity 14.17%

Item Value

Return on Equity (RoE) – Long term growth (LTG) 30.9%

Cost of Equity (CoE) – Long term growth (LTG) 11.67%

Multiple 2.65

Adjusted Book Value per share (FY12) 12.1

CIV 32

SANWARIA AGRO OILS LTD

www.careratings.com 8

EQUIGRADE

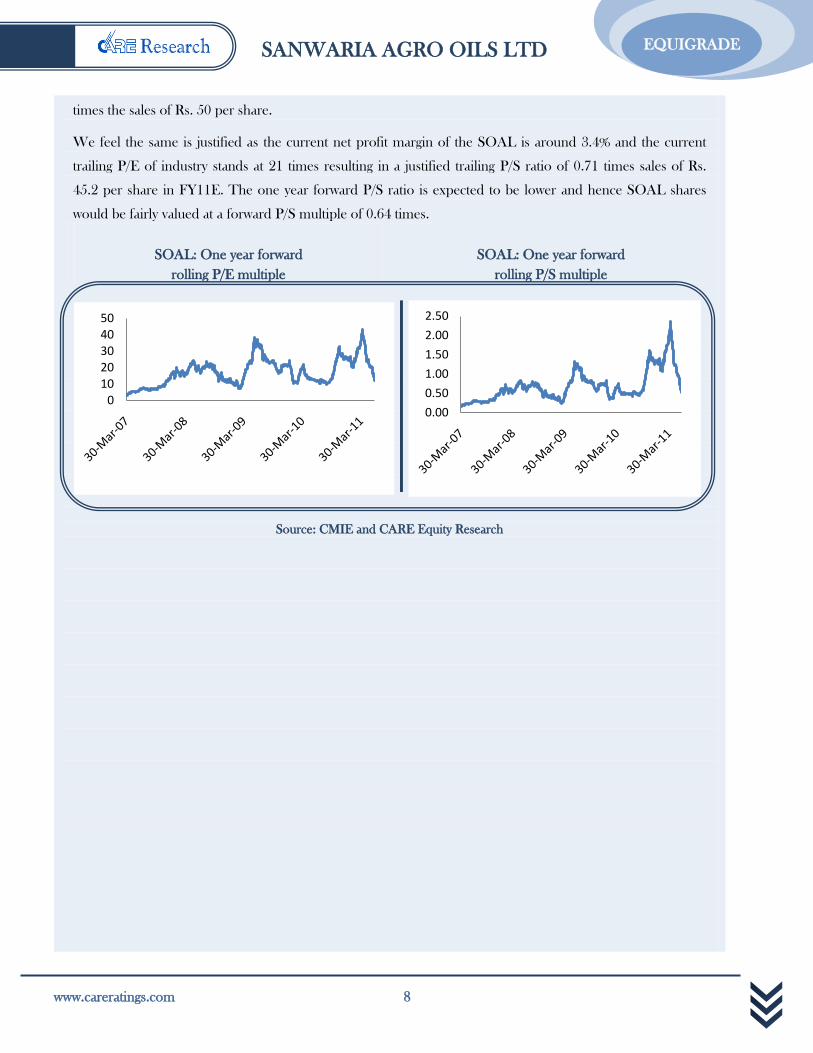

times the sales of Rs. 50 per share.

We feel the same is justified as the current net profit margin of the SOAL is around 3.4% and the current

trailing P/E of industry stands at 21 times resulting in a justified trailing P/S ratio of 0.71 times sales of Rs.

45.2 per share in FY11E. The one year forward P/S ratio is expected to be lower and hence SOAL shares

would be fairly valued at a forward P/S multiple of 0.64 times.

SOAL: One year forward

rolling P/E multiple

SOAL: One year forward

rolling P/S multiple

Source: CMIE and CARE Equity Research

01020304050

0.00

0.50

1.00

1.50

2.00

2.50

SANWARIA AGRO OILS LTD

9 www.careratings.com

EQUIGRADE

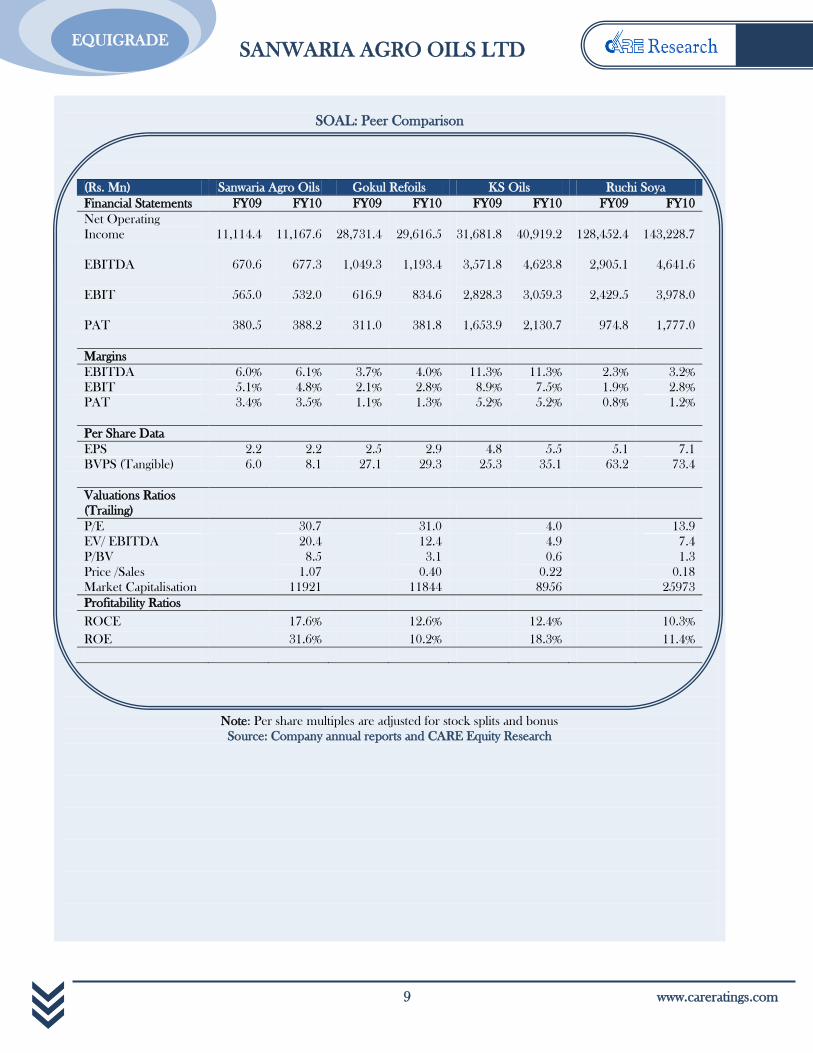

SOAL: Peer Comparison

(Rs. Mn) Sanwaria Agro Oils Gokul Refoils KS Oils Ruchi Soya

Financial Statements FY09 FY10 FY09 FY10 FY09 FY10 FY09 FY10

Net Operating

Income

11,114.4

11,167.6

28,731.4

29,616.5

31,681.8

40,919.2

128,452.4

143,228.7

EBITDA

670.6

677.3

1,049.3

1,193.4

3,571.8

4,623.8

2,905.1

4,641.6

EBIT

565.0

532.0

616.9

834.6

2,828.3

3,059.3

2,429.5

3,978.0

PAT

380.5

388.2

311.0

381.8

1,653.9

2,130.7

974.8

1,777.0

Margins

EBITDA 6.0% 6.1% 3.7% 4.0% 11.3% 11.3% 2.3% 3.2%

EBIT 5.1% 4.8% 2.1% 2.8% 8.9% 7.5% 1.9% 2.8%

PAT 3.4% 3.5% 1.1% 1.3% 5.2% 5.2% 0.8% 1.2%

Per Share Data

EPS 2.2 2.2 2.5 2.9 4.8 5.5 5.1 7.1

BVPS (Tangible) 6.0 8.1 27.1 29.3 25.3 35.1 63.2 73.4

Valuations Ratios

(Trailing)

P/E

30.7

31.0

4.0

13.9

EV/ EBITDA

20.4

12.4

4.9

7.4

P/BV

8.5

3.1

0.6

1.3

Price /Sales

1.07

0.40

0.22

0.18

Market Capitalisation

11921

11844

8956

25973

Profitability Ratios

ROCE 17.6% 12.6% 12.4% 10.3%

ROE 31.6% 10.2% 18.3% 11.4%

Note: Per share multiples are adjusted for stock splits and bonus

Source: Company annual reports and CARE Equity Research

SANWARIA AGRO OILS LTD

www.careratings.com 10

EQUIGRADE

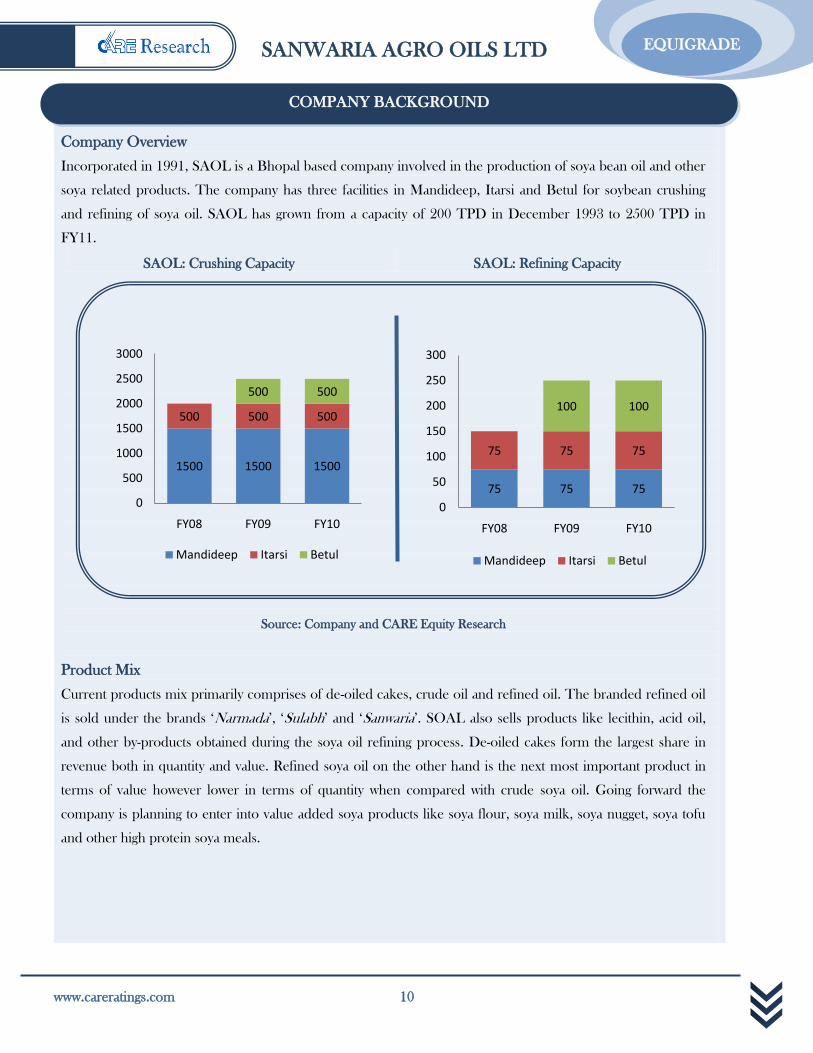

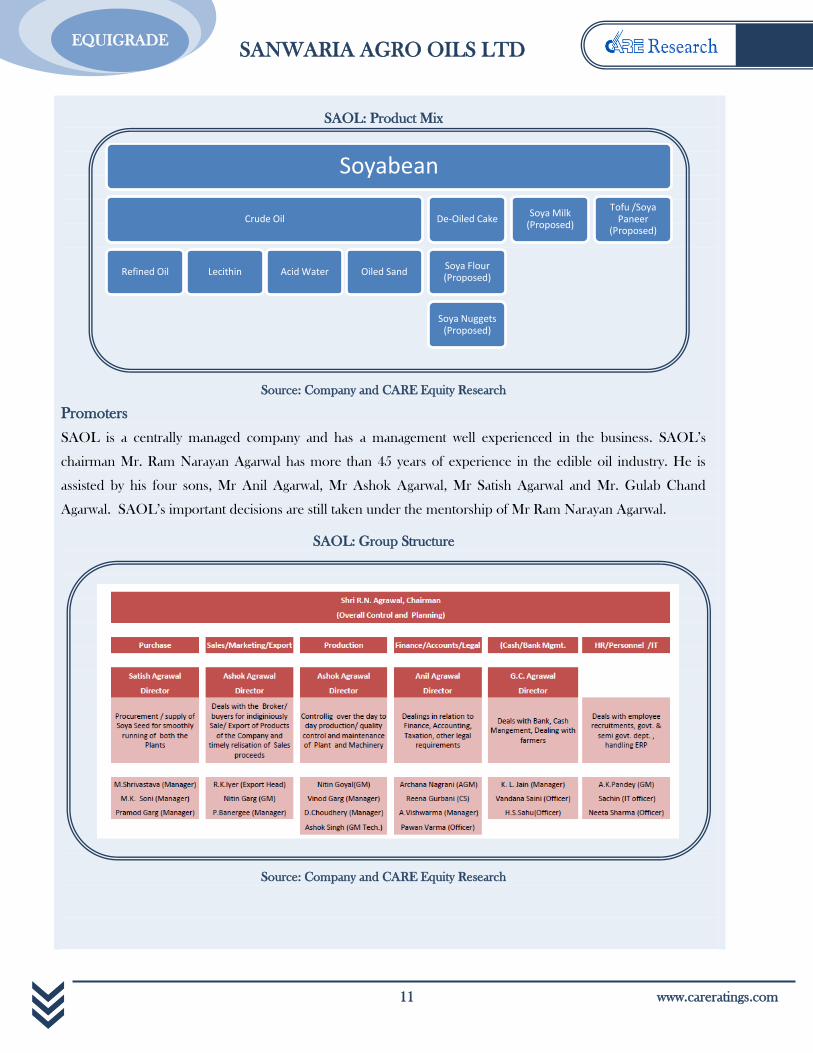

Company Overview

Incorporated in 1991, SAOL is a Bhopal based company involved in the production of soya bean oil and other

soya related products. The company has three facilities in Mandideep, Itarsi and Betul for soybean crushing

and refining of soya oil. SAOL has grown from a capacity of 200 TPD in December 1993 to 2500 TPD in

FY11.

SAOL: Crushing Capacity SAOL: Refining Capacity

Source: Company and CARE Equity Research

Product Mix

Current products mix primarily comprises of de-oiled cakes, crude oil and refined oil. The branded refined oil

is sold under the brands ‘Narmada’, ‘Sulabh’ and ‘Sanwaria’. SOAL also sells products like lecithin, acid oil,

and other by-products obtained during the soya oil refining process. De-oiled cakes form the largest share in

revenue both in quantity and value. Refined soya oil on the other hand is the next most important product in

terms of value however lower in terms of quantity when compared with crude soya oil. Going forward the

company is planning to enter into value added soya products like soya flour, soya milk, soya nugget, soya tofu

and other high protein soya meals.

COMPANY BACKGROUND

1500 1500 1500

500 500 500

500 500

0

500

1000

1500

2000

2500

3000

FY08 FY09 FY10

Mandideep Itarsi Betul

75 75 75

75 75 75

100 100

0

50

100

150

200

250

300

FY08 FY09 FY10

Mandideep Itarsi Betul

SANWARIA AGRO OILS LTD

11 www.careratings.com

EQUIGRADE

SAOL: Product Mix

Source: Company and CARE Equity Research

Promoters

SAOL is a centrally managed company and has a management well experienced in the business. SAOL’s

chairman Mr. Ram Narayan Agarwal has more than 45 years of experience in the edible oil industry. He is

assisted by his four sons, Mr Anil Agarwal, Mr Ashok Agarwal, Mr Satish Agarwal and Mr. Gulab Chand

Agarwal. SAOL’s important decisions are still taken under the mentorship of Mr Ram Narayan Agarwal.

SAOL: Group Structure

Source: Company and CARE Equity Research

Soyabean

Crude Oil

Refined Oil Lecithin Acid Water Oiled Sand

De-Oiled Cake

Soya Flour (Proposed)

Soya Nuggets (Proposed)

Soya Milk (Proposed)

Tofu /Soya Paneer

(Proposed)

SANWARIA AGRO OILS LTD

www.careratings.com 12

EQUIGRADE

Edible oil consumption in India is expected to continue to grow

The domestic consumption of edible oils is expected to rise with rise in the disposable incomes and changing

food habits of Indian consumers. The per capita edible oil consumption in India is around 14.5 kgs per annum,

much lower when compared with the world average of 23.9 kgs per annum. The total edible oil consumption in

India is around 17 million tonnes, with around 9 million tonnes of the demand currently being met by imports.

Although a total of around 15,700 TPD of capacity expansion is expected in the edible oil industry by the end

of 2013, the same would not be sufficient to meet the demand supply gap, which will continue to persist.

Edible Oils: Capacity Expansion Projects

Note: TPD – Tonnes Per Day, MTA – Million Tonnes per Annum, LTA – Lakh Tonnes per Annum

Source: CMIE and CARE Research

Shifting focus to Soya bean oil

Groundnut, mustard and soya are the three preferred oils used in India. While, mustard oil continues to be the

widest consumed edible oil in India with a share of around 41 per cent, soya is the next most used source of

edible oil – around 27 per cent share, and there has been an increase the consumption of soya oil over the

years.

SNAPSHOT OF THE INDUSTRY

Company Location Product Capacity Units

Emami Biotech Ltd Krishnapatnam Palm Oil 1000 TPD

Krishnapatnam Sunflower Oil 200 TPD

Pipapav Palm Oil 1000 TPD

Pipapav Sunflower Oil 300 TPD

Jaiprakash Associates Ltd Rewa Mustard Oil 1.0 LTA

Rewa Soya Oil 1.0 LTA

Adani Wilmar Ltd Mundra Edible Oil 4000 TPD

Liberty Oil Mills Ltd Bhuj Refined Oil 1200 TPD

Nellore Refined Oil 1200 TPD

Dakshina Refined Oil 1200 TPD

Gokul Refoils & Solvents Ltd. MAH Edible Oil 1000 TPD

AP Edible Oil 1000 TPD

Ruchi Soya Industries Ltd Haldia, Kandla,

Mumbai Palm Oil 1.1 MTA

Sanwaria Agro Oils Ltd Mandideep,

Itarsi

Soya Oil

Refined Oil

1000

150

TPD

TPD

SANWARIA AGRO OILS LTD

13 www.careratings.com

EQUIGRADE

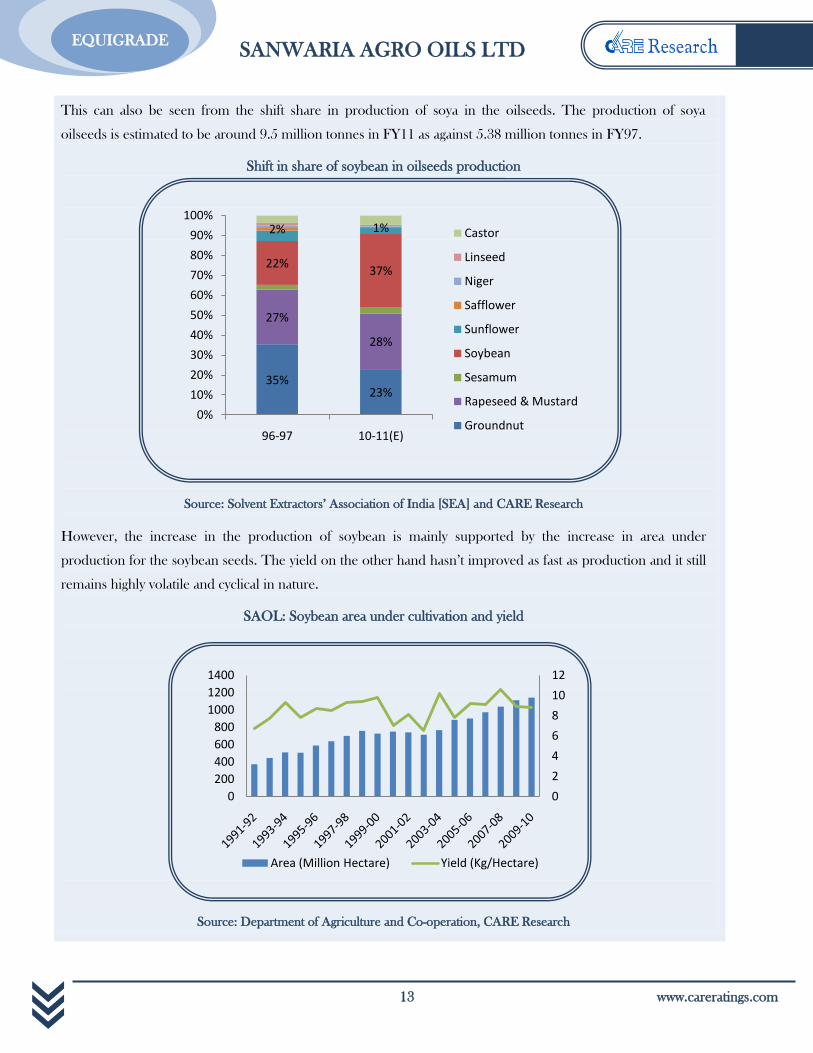

This can also be seen from the shift share in production of soya in the oilseeds. The production of soya

oilseeds is estimated to be around 9.5 million tonnes in FY11 as against 5.38 million tonnes in FY97.

Shift in share of soybean in oilseeds production

Source: Solvent Extractors’ Association of India [SEA] and CARE Research

However, the increase in the production of soybean is mainly supported by the increase in area under

production for the soybean seeds. The yield on the other hand hasn’t improved as fast as production and it still

remains highly volatile and cyclical in nature.

SAOL: Soybean area under cultivation and yield

Source: Department of Agriculture and Co-operation, CARE Research

0

2

4

6

8

10

12

0

200

400

600

800

1000

1200

1400

Area (Million Hectare) Yield (Kg/Hectare)

35%23%

27%

28%

22%37%

2% 1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

96-97 10-11(E)

Castor

Linseed

Niger

Safflower

Sunflower

Soybean

Sesamum

Rapeseed & Mustard

Groundnut

SANWARIA AGRO OILS LTD

www.careratings.com 14

EQUIGRADE

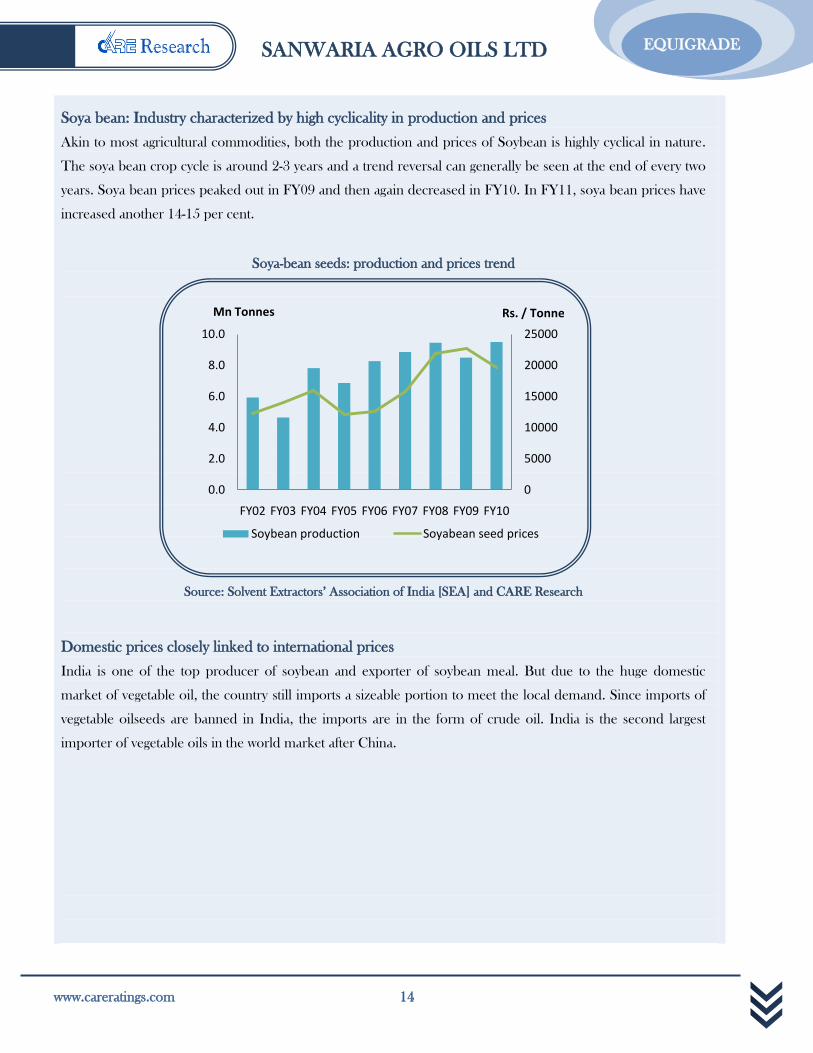

Soya bean: Industry characterized by high cyclicality in production and prices

Akin to most agricultural commodities, both the production and prices of Soybean is highly cyclical in nature.

The soya bean crop cycle is around 2-3 years and a trend reversal can generally be seen at the end of every two

years. Soya bean prices peaked out in FY09 and then again decreased in FY10. In FY11, soya bean prices have

increased another 14-15 per cent.

Soya-bean seeds: production and prices trend

Source: Solvent Extractors’ Association of India [SEA] and CARE Research

Domestic prices closely linked to international prices

India is one of the top producer of soybean and exporter of soybean meal. But due to the huge domestic

market of vegetable oil, the country still imports a sizeable portion to meet the local demand. Since imports of

vegetable oilseeds are banned in India, the imports are in the form of crude oil. India is the second largest

importer of vegetable oils in the world market after China.

0

5000

10000

15000

20000

25000

0.0

2.0

4.0

6.0

8.0

10.0

FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10

Rs. / TonneMn Tonnes

Soybean production Soyabean seed prices

SANWARIA AGRO OILS LTD

15 www.careratings.com

EQUIGRADE

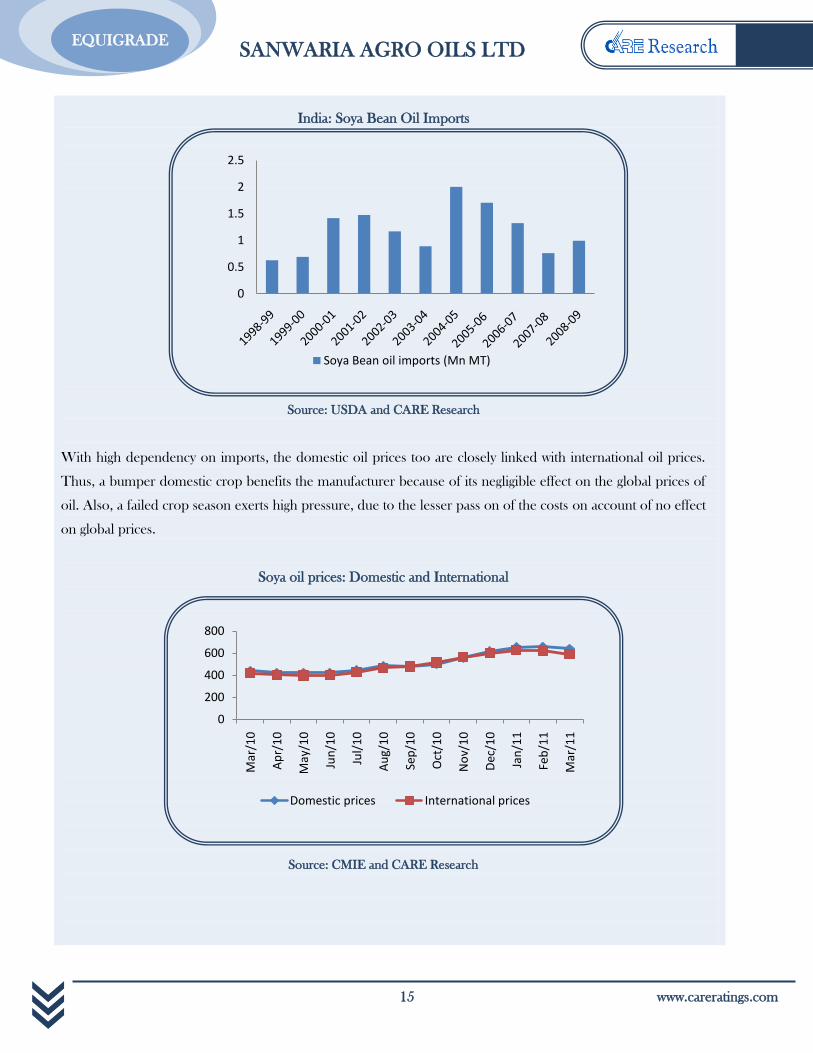

India: Soya Bean Oil Imports

Source: USDA and CARE Research

With high dependency on imports, the domestic oil prices too are closely linked with international oil prices.

Thus, a bumper domestic crop benefits the manufacturer because of its negligible effect on the global prices of

oil. Also, a failed crop season exerts high pressure, due to the lesser pass on of the costs on account of no effect

on global prices.

Soya oil prices: Domestic and International

Source: CMIE and CARE Research

0

0.5

1

1.5

2

2.5

Soya Bean oil imports (Mn MT)

0

200

400

600

800

Mar

/10

Ap

r/1

0

May

/10

Jun

/10

Jul/

10

Au

g/1

0

Sep

/10

Oct

/10

No

v/1

0

Dec

/10

Jan

/11

Feb

/11

Mar

/11

Domestic prices International prices

SANWARIA AGRO OILS LTD

www.careratings.com 16

EQUIGRADE

TVP: the road ahead

Textured Vegetable Protein or TVP as a product is fast picking up in India. TVP is made from the de-oiled

cake which is a left over after the oil is extracted from the soya seeds. The TVP trades around Rs 35,000 /tonne

making it almost one half of the price of the Soya Refined oil. In soya bean oil extraction process, around 18

per cent of the weight of the seeds is extracted as oil and remaining 82 per cent is processed for de-oiled cake.

Thus, the revenues from de-oiled cake and TVP are generally around 60 per cent of the total revenues of a

soya bean oil manufacturer. TVP is also a very high margin and profitable business for a soya bean oil

manufacturer. Most of the soya oil manufacturers are now foraying into TVP segment due to the high

profitability and its increasing consumption trend in India.

SANWARIA AGRO OILS LTD

17 www.careratings.com

EQUIGRADE

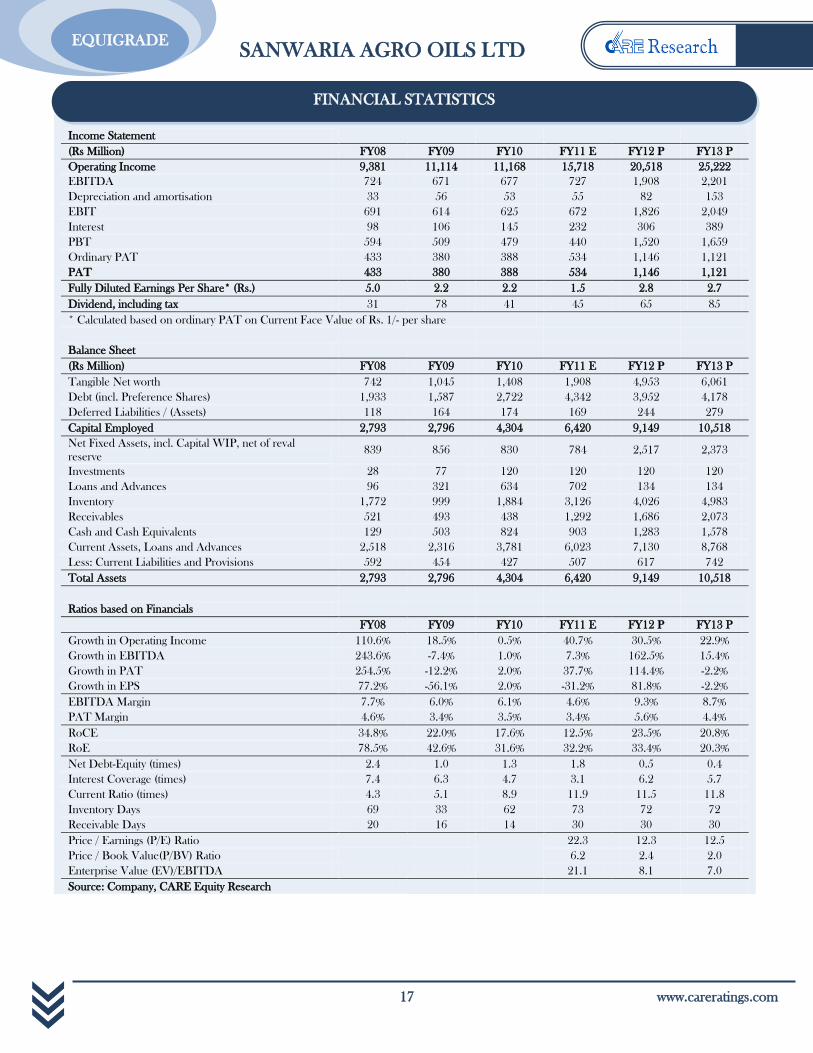

Income Statement

(Rs Million) FY08 FY09 FY10 FY11 E FY12 P FY13 P

Operating Income 9,381 11,114 11,168 15,718 20,518 25,222

EBITDA 724 671 677 727 1,908 2,201

Depreciation and amortisation 33 56 53 55 82 153

EBIT 691 614 625 672 1,826 2,049

Interest 98 106 145 232 306 389

PBT 594 509 479 440 1,520 1,659

Ordinary PAT 433 380 388 534 1,146 1,121

PAT 433 380 388 534 1,146 1,121

Fully Diluted Earnings Per Share* (Rs.) 5.0 2.2 2.2 1.5 2.8 2.7

Dividend, including tax 31 78 41 45 65 85

* Calculated based on ordinary PAT on Current Face Value of Rs. 1/- per share

Balance Sheet

(Rs Million) FY08 FY09 FY10 FY11 E FY12 P FY13 P

Tangible Net worth 742 1,045 1,408 1,908 4,953 6,061

Debt (incl. Preference Shares) 1,933 1,587 2,722 4,342 3,952 4,178

Deferred Liabilities / (Assets) 118 164 174 169 244 279

Capital Employed 2,793 2,796 4,304 6,420 9,149 10,518

Net Fixed Assets, incl. Capital WIP, net of reval

reserve 839 856 830 784 2,517 2,373

Investments 28 77 120 120 120 120

Loans and Advances 96 321 634 702 134 134

Inventory 1,772 999 1,884 3,126 4,026 4,983

Receivables 521 493 438 1,292 1,686 2,073

Cash and Cash Equivalents 129 503 824 903 1,283 1,578

Current Assets, Loans and Advances 2,518 2,316 3,781 6,023 7,130 8,768

Less: Current Liabilities and Provisions 592 454 427 507 617 742

Total Assets 2,793 2,796 4,304 6,420 9,149 10,518

Ratios based on Financials

FY08 FY09 FY10 FY11 E FY12 P FY13 P

Growth in Operating Income 110.6% 18.5% 0.5% 40.7% 30.5% 22.9%

Growth in EBITDA 243.6% -7.4% 1.0% 7.3% 162.5% 15.4%

Growth in PAT 254.5% -12.2% 2.0% 37.7% 114.4% -2.2%

Growth in EPS 77.2% -56.1% 2.0% -31.2% 81.8% -2.2%

EBITDA Margin 7.7% 6.0% 6.1% 4.6% 9.3% 8.7%

PAT Margin 4.6% 3.4% 3.5% 3.4% 5.6% 4.4%

RoCE 34.8% 22.0% 17.6% 12.5% 23.5% 20.8%

RoE 78.5% 42.6% 31.6% 32.2% 33.4% 20.3%

Net Debt-Equity (times) 2.4 1.0 1.3 1.8 0.5 0.4

Interest Coverage (times) 7.4 6.3 4.7 3.1 6.2 5.7

Current Ratio (times) 4.3 5.1 8.9 11.9 11.5 11.8

Inventory Days 69 33 62 73 72 72

Receivable Days 20 16 14 30 30 30

Price / Earnings (P/E) Ratio

22.3 12.3 12.5

Price / Book Value(P/BV) Ratio

6.2 2.4 2.0

Enterprise Value (EV)/EBITDA

21.1 8.1 7.0

Source: Company, CARE Equity Research

FINANCIAL STATISTICS

SANWARIA AGRO OILS LTD

www.careratings.com 18

EQUIGRADE

CARE Equigrade Grid (CEG)

Through CEG, CARE Equity Research addresses two critical factors considered by an investor while investing in a

particular company’s equity shares:

1. Fundamentals: Whether the company is fundamentally sound with respect to its business, its financial position, its

management and its prospects.

2. Valuation: What is the Current Intrinsic Value (CIV) of the stock and how it compares vis-a-vis its Current

Market Price (CMP)

These factors are answered assigning quantitative grades to both these parameters. CEG is the snapshot of

‘Fundamental Grade’ and ‘Valuation Grade’ assigned by CARE Equity Research.

Fundamental Grade

This grade represents how sound the company is fundamentally, vis-à-vis other listed companies in India. This grade

captures:

1. Business Fundamentals and Prospects

2. Financial Soundness

3. Management Quality

4. Corporate Governance Practices

The grade is assigned on a five-point scale as under:

CARE Fundamental Grade Evaluation

5/5 Strong Fundamentals

4/5 Very Good Fundamentals

3/5 Good Fundamentals

2/5 Modest Fundamentals

1/5 Weak Fundamentals

Valuation Grade

This grade represents the potential value in the company’s equity share for the investor over a 1 year period. The

Current Intrinsic Value (CIV) or the price arrived by CARE Equity Research on fundamental basis is compared with

the current market price (CMP) of the stock and the grade is assigned based on the gap between CIV and CMP of the

stock.

EXPLANATION OF GRADES

SANWARIA AGRO OILS LTD

19 www.careratings.com

EQUIGRADE

The grade is assigned on a five-point scale as under:

CARE Valuation Grade Evaluation

5/5 Considerable Upside Potential

(>25% upside from CMP)

4/5 Moderate Upside Potential

(10-25% upside from CMP)

3/5 Fairly Priced

(+/- 10% from CMP)

2/5 Moderate Downside Potential

(10-25% downside from CMP)

1/5 Considerable Downside Potential

(>25% downside from CMP)

Grading determination is a matter of experienced and holistic judgment, based on relevant quantitative and qualitative factors of

the company in relation to other listed companies.

DISCLOSURES

Each member of the team involved in the preparation of this grading report, hereby affirms that there exists no conflict of

interest that can bias the grading recommendation of the company.

This report has been sponsored by the company.

DISLCLAIMER

This report is prepared by CARE Research, a division of Credit Analysis & REsearch Limited [CARE]. CARE Research has taken

utmost care to ensure accuracy and objectivity while developing this report based on information available in public domain or from

sources considered reliable. However, neither the accuracy nor completeness of information contained in this report is guaranteed.

CARE Research operates independently of ratings division and this report does not contain any confidential information obtained by

ratings division, which they may have obtained in the regular course of operations. Opinions expressed herein are our current

opinions as on the date of this report.

CARE’s valuation of the security is mainly based on company specific fundamental factors. Equity prices are affected by both

fundamental factors as well as market factors such as – liquidity, sentiment, broad market direction etc. The impact of market factors

can distort the price of the security thereby deviating from the intrinsic value for extended period of time. This report should not be

construed as recommendation to buy, sell or hold a security or any advice or any solicitation, whatsoever. It is also not a comment on

the suitability of the investment to the reader. The subscriber / user assumes the entire risk of any use made of this report or data

herein. CARE specifically states that it or any of its divisions or employees have no financial liabilities whatsoever to the subscribers /

users of this report. This report is for personal information only of the authorised recipient in India only. This report or part of it

should not be reproduced or redistributed or communicated directly or indirectly in any form to any other person, especially outside

India or published or copied for any purpose.

Published by Credit Analysis & REsearch Ltd., 4th Floor Godrej Coliseum, Off Eastern Express Highway, Somaiya

Hospital Road, Sion East, Mumbai – 400 022.

CARE Research is not responsible for any errors or omissions in analysis/inferences/views or for results obtained from the use of

information contained in this report and especially states that CARE (including all divisions) has no financial liability whatsoever to

the user of this product. This report is for the information of the intended recipients only and no part of this report may be published

or reproduced in any form or manner without prior written permission of CARE Research.

SANWARIA AGRO OILS LTD

www.careratings.com 20

EQUIGRADE

Credit Analysis & REsearch Ltd. (CARE) is a full service rating company that offers a wide range of rating and grading services

across sectors. CARE has an unparallel depth of expertise. CARE Ratings methodologies are in line with the best international

practices.

CARE Research

CARE Research is an independent research division of CARE Ratings, a full service rating company. CARE Research is

involved in preparing detailed industry research reports with 5 year demand and 2 year profitability outlook on the industry

besides providing comprehensive trend analysis and the current state of the industry. CARE Research also offers research that

is customised to client requirements. CARE Research currently offers reports on more than 21 industries that include Cement,

Steel, Aluminium, Construction, Shipping, Ship-building, Commercial Vehicles, Two-Wheelers, Tyres, Auto Components,

Pipes, Natural Gas, Retail, Sugar, etc. CARE Research offers independent research of equities through its product

‘EQUIGRADE’. CARE Research now offers city specific grading of real estate projects through its product 'CARE Real Estate

Project Star Ratings’

CREDIT ANALYSIS & RESEARCH LTD

HEAD OFFICE |Mr. P. N. Satheeskumar | Cell: +91-9820416004 | Tel: +91-22-6754 3555 | E-mail:

4th Floor, Godrej Coliseum, Somaiya Hospital Road, Off Eastern Express Highway, Sion (East), Mumbai - 400 022 |

Tel: +91-022- 6754 3456 | E-mail: [email protected] | Fax: +91-022- 6754 3457

KOLKATA | Mr. Sukanta Nag | Cell: +91-98311 70075 | Tel: +91-33- 2283 1800/ 1803, 2280 8472 |

E- mail: [email protected] | 3rd Flr., Prasad Chambers (Shagun Mall Bldg), 10A, Shakespeare Sarani, Kolkata -700 071

CHENNAI | Mr. V Pradeep Kumar | Cell: +91 9840754521 | Tel: +91-44-2849 7812/2849 0811 | Fax: +91-44-2849 0876 |

Email: [email protected] | Unit No. O-509/C, Spencer Plaza, 5th Floor, No. 769, Anna Salai, Chennai - 600 002

AHMEDABAD | Mr. Mehul Pandya | Cell: +91-98242 56265 | Tel: +91-79-40265656 | Fax: +91-79-40265657 |

E-mail:[email protected] | 32, Titanium, Prahaladnagar Corporate Road, Satellite, Ahmedabad - 380 015.

NEW DELHI | Ms. Swati Agrawal | Cell: +91-98117 45677 | Tel: +91- 11- 2331 8701/ 2371 6199 |

E-mail: [email protected] | 3rd Floor, B -47, Inner Circle, Near Plaza Cinema, Connaught Place, New Delhi - 110 001.

BANGALORE | Mr. G. Sundara Vathanan | Cell: +91 98860 24430 | Tel:+91-80-2211 7140 |

E-mail: [email protected] | Unit No. 8, I floor, Commander's Place, No. 6, Raja Ram Mohan Roy Road,

(Opp. P F Office), Richmond Circle, Bangalore - 560 025.

HYDERABAD | Mr. Ashwini Kumar Jani | Cell: +91-91766 47599 | Tel: +91-40-40102030 |

E-mail: [email protected] | 401, Ashoka Scintilla | 3-6-520, Himayat Nagar | Hyderabad - 500 029

ABOUT CARE

![Supply Chain Management and Store Operation in Pantaloon Retail India Pvt[1]. Ltd Pantaloon](https://img.pdfslide.us/doc/110x75/55721004497959fc0b8ca3ea/supply-chain-management-and-store-operation-in-pantaloon-retail-india-pvt1-ltd-pantaloon.jpg)