Embed Size (px)

Citation preview

Fund Balance with Treasury

RECONCILIATION PROCEDURES

A Supplement to the Treasury Financial ManualI TFM 2-5100

November 1999

Financial Management ServiceDepartment of theTreasury

2-5100 SUPPLEMENT TO VOL I TREASURY FINANCIAL MANUAL

i

TABLE OF CONTENTS

I. Date of Standard Operating Procedures ........................................................................................................................1

II. Purpose...............................................................................................................................................................................1

III. Acronyms and Forms .......................................................................................................................................................1

IV. Background........................................................................................................................................................................2

V. Policy...................................................................................................................................................................................3

A. Periodic Review and Evaluation......................................................................................................................3B. Differences .........................................................................................................................................................3C. Adjustments.......................................................................................................................................................3D. Financial Management System Responsibilities ..........................................................................................3E. Internal Controls ................................................................................................................................................4

VI. Fund Account Symbols ...................................................................................................................................................4

VII. Agency Location Code ....................................................................................................................................................5

VIII. Fund Balance Reconciliation...........................................................................................................................................5

A. Documentation Used for Reconciliation........................................................................................................51. Agency Source Documents.............................................................................................................52. Treasury Reports...............................................................................................................................6

a. SF 224: Statement of Transactions .................................................................................6b. SF 1218/1221: Statement of Accountability/Transactions..........................................6c. SF 1219/1220: Statement of Accountability/Transactions..........................................6d. Reconciliation of Checks Issued.....................................................................................7e. FMS 6652: Statement of Differences ..............................................................................7f. FMS 6653: Undisbursed Appropriation Account Ledger...........................................8g. FMS 6654: Undisbursed Appropriation Account Trial Balance................................8h. FMS 6655: Unappropriated Receipt Account Ledger..................................................8i. FMS 6655: Receipt Account Trial Balance....................................................................8j. FMS 6655: Report of Unavailable Receipt Transactions.............................................9k. FMS 2108: Yearend Closing Statement..........................................................................9

B. Step-By-Step Reconciliation Process.............................................................................................................91. Comparing FMS 6653 and General Ledger Totals .....................................................................11

• Exhibit 1A—How to Compare FMS 6653 and General Ledger Totals .............................11• Exhibit 1B—How to Identify Differences in FMS 6653 and .................................................

General Ledger Entries Reported by the Agency...............................................................12• Exhibit 1C—How to Identify Differences in FMS 6653

and General Ledger Entries Reported by Another Agency..............................................13• Exhibit 1D—How to Determine the Month-End Unreconciled Balance .........................15

2. Identifying Prior Month Differences............................................................................................16• Exhibit 2A—How to Identify Prior Month Differences ....................................................16

3. Reconciling the Statements of Differences ................................................................................17• Exhibit 3A—How to Reconcile the Statement of Differences for Disbursements ........17

SUPPLEMENT TO VOL I 2-5100TREASURY FINANCIAL MANUAL

ii

• Exhibit 3B—How to Use Worksheet 1B for the Statement of Differences forDisbursements .........................................................................................................................19

• Exhibit 3C—How to Reconcile the Statement of Differences for Deposits ....................20• Exhibit 3D—How to Use Worksheet 1C for the Statement of Differences for Deposits 22• Exhibit 3E—How to Reconcile Check Issue Audits Using FMS 5206 ............................23

4. Researching Uncleared Differences .................................................................................................24• Exhibit 4A—How to Research Uncleared Differences ......................................................24

IX. General Information.........................................................................................................................................................25

A. Most Commonly Made Errors .......................................................................................................................25B. Frequently Asked Questions/Answers .......................................................................................................26C. Helpful Hints ....................................................................................................................................................27

APPENDICES

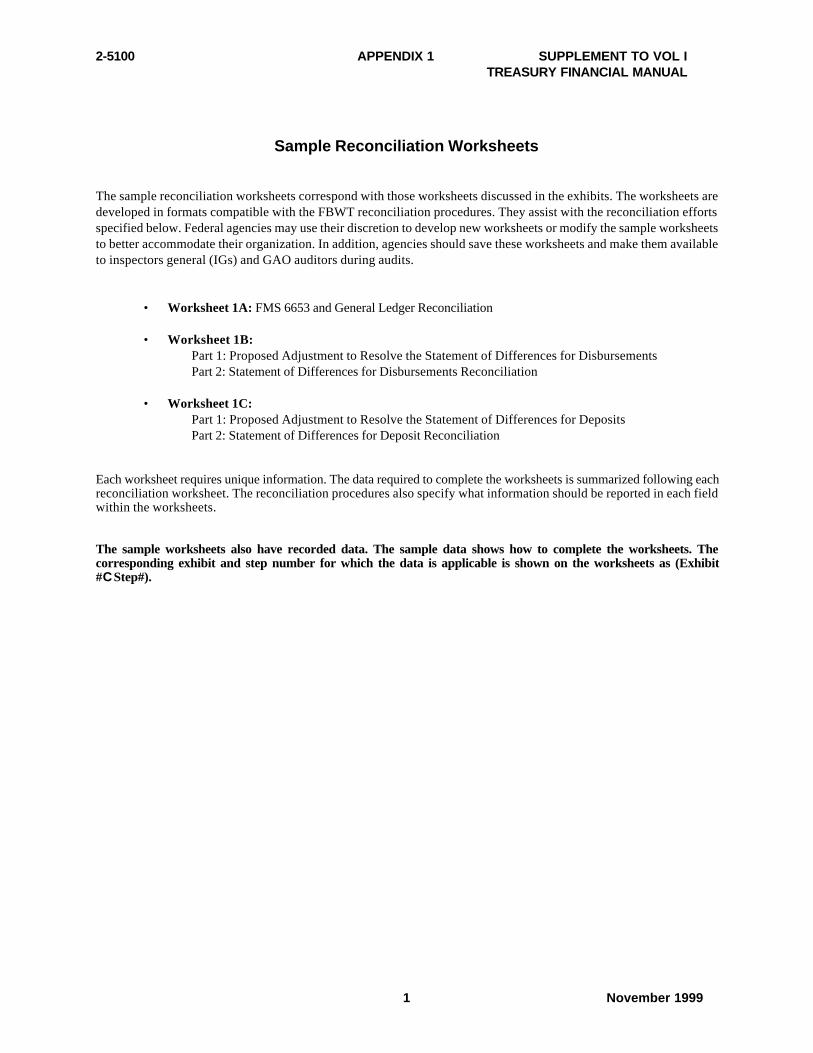

Appendix 1: Sample Reconciliation Worksheets

Worksheet 1A: FMS 6653 and General Ledger Reconciliation

Worksheet 1B:Part 1: Proposed Adjustments to Resolve the Statement of Differences for DisbursementsPart 2: Statement of Differences for Disbursements Reconciliation

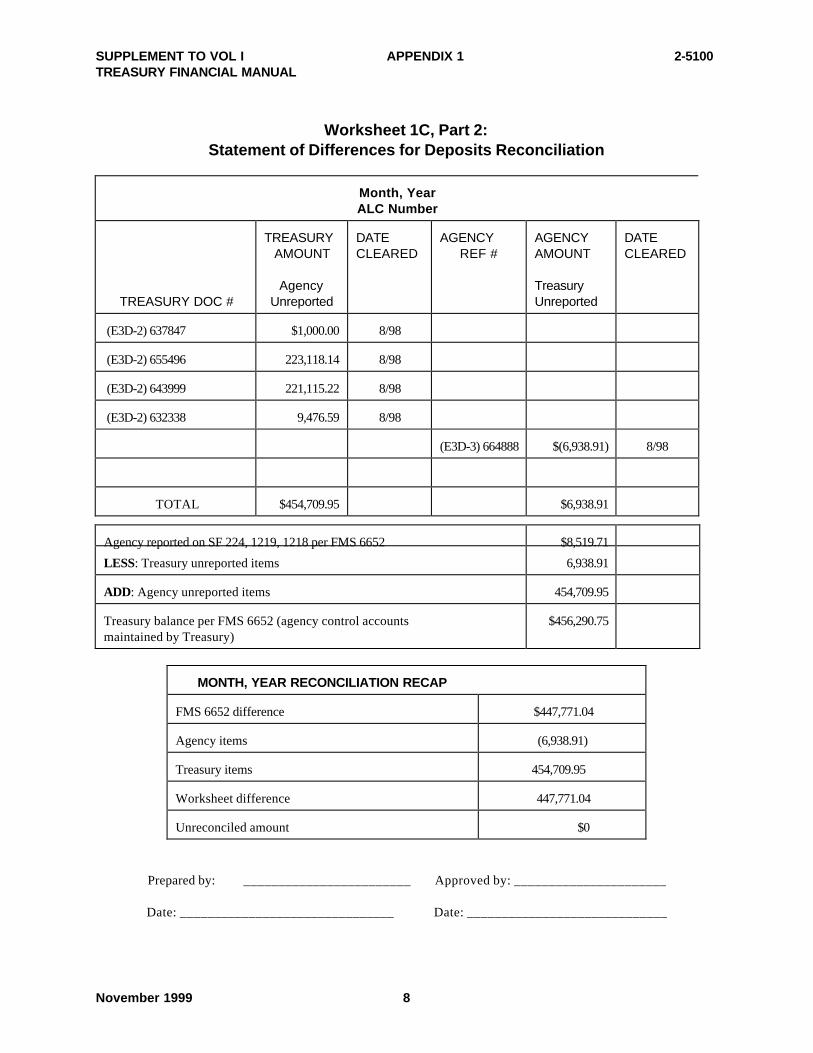

Worksheet 1C:Part 1: Proposed Adjustments to Resolvethe Statement of Differences for DepositsPart 2: Statement of Differences for Deposits Reconciliation

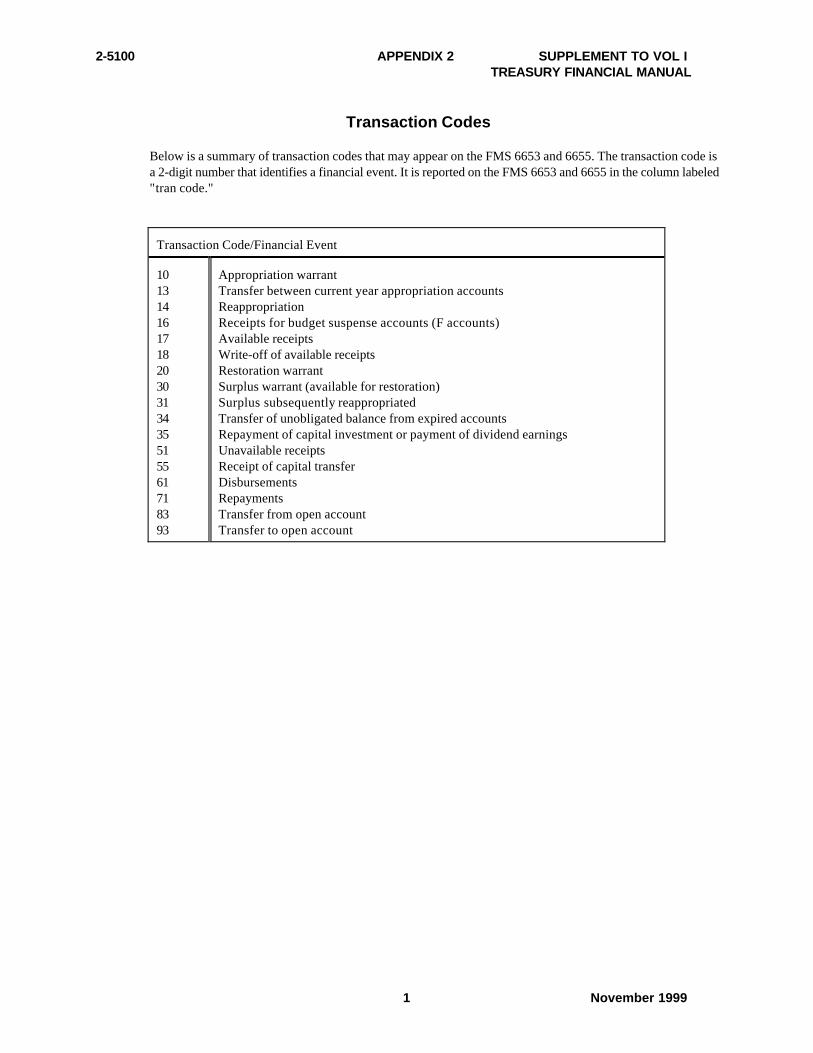

Appendix 2: Transaction Codes

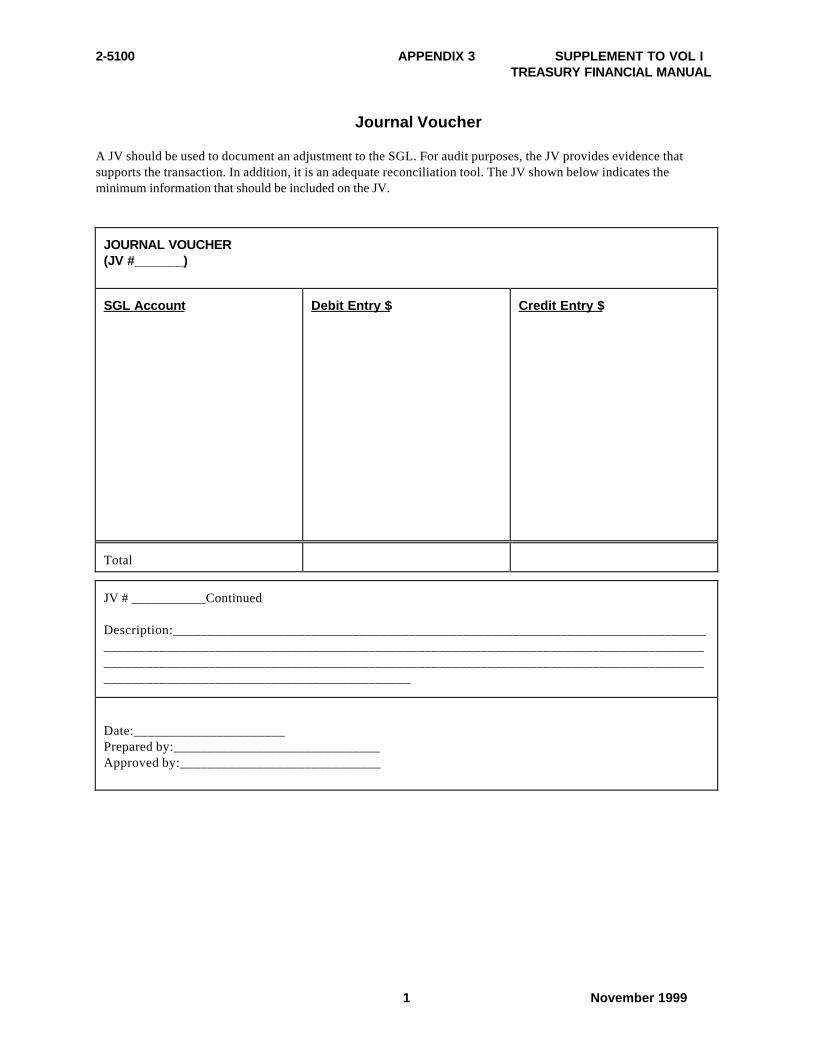

Appendix 3: Journal Voucher

Appendix 4: Sample Reconciliation Correspondence

Sample Memo1. FMS 6653: Monthly Fund Balance Reconciliation Sample

Sample Letter1. Discrepancy with Amount Reported 2. Request for Documentation

Appendix 5: Fund Balance Process and Reconciliation Flowchart

Appendix 6: References

Appendix 7: Contacts

Appendix 8: Glossary of Terms

2-5100 SUPPLEMENT TO VOL ITREASURY FINANCIAL MANUAL

November 19991

FUND BALANCE WITH TREASURY RECONCILIATION PROCEDURES

A Supplement to the TFM

I. Date of Standard Operating Procedures (SOPs):

These SOPs were established May 31, 1999, but are subject to change as deemed necessary. The month and date ofany change will be appropriately documented. The Financial Analysis Branch (FAB) maintains this document. FABwill provide revised procedures electronically via Internet, transmittal letter updates and in the Treasury FinancialManual (TFM).

II. Purpose:

The procedures defined in this document provide step-by-step instructions on reconciling the Fund Balance withTreasury (FBWT). Also included is guidance on reconciling warrant and nonexpenditure transactions. Theseprocedures pertain to Federal agencies that must report receipt and disbursement activity to Treasury.

III. Acronyms and Forms:

The acronyms used throughout this document are summarized below.

A. AcronymsACR Agency Confirmation ReportALC Agency Location CodeCFO Chief Financial OfficerCP&R Check Payment and Reconciliation SystemEFT Electronic Funds TransferDO Disbursing OfficerFAB Financial Analysis BranchFBWT Fund Balance with TreasuryFI Financial InstitutionFMS Financial Management ServiceFRB Federal Reserve BankFY Fiscal yearG/L General LedgerGOALS Government On-line Accounting Link SystemJV Journal VoucherOMB Office of Management and BudgetOPAC On-line Payment and Collection SystemNTDO Non-Treasury Disbursing OfficeRFC Regional Financial CenterSGL Standard General LedgerSIBAC Simplified Interagency Billing and CollectionSOD Statements of DifferencesSTAR FMS's integrated accounting systemUSDO U.S. Disbursing Officer

SUPPLEMENT TO VOL I 2-5100TREASURY FINANCIAL MANUAL

November 1999 2

B. FormsSF 215: Deposit TicketSF 224: Statement of TransactionsSF 1081: Voucher and Schedule of Withdrawals and CreditsSF 1098: Schedule of Canceled or Undelivered ChecksSF 1151: Nonexpenditure TransferSF 1166: Voucher and Schedule of PaymentsSF 1218: Statement of AccountabilitySF 1219: Statement of AccountabilitySF 1220: Statement of TransactionsSF 1221: Statement of TransactionsSF 5515: Debit VoucherFMS 145: Schedule of Canceled EFT ItemsFMS 1185: Schedule of Unavailable Checks/Cancellations/CreditsFMS 2108: Yearend Closing StatementFMS 5206: Advice of Check Issue DiscrepancyFMS 6200: WarrantsFMS 6652: Statement of DifferencesFMS 6653: Undisbursed Appropriation LedgerFMS 6654: Undisbursed Appropriation Account Trial BalanceFMS 6655: Receipt Account LedgerFMS 6655: Receipt Account Trial BalanceFMS 6655: Report of Unavailable Receipt Transactions

IV. Background:

The FBWT account is an asset account representing the future economic benefit of monies that can be spent forauthorized transactions. The SGL defines the FBWT as consisting of all funds on deposit with Treasury, excludingseized cash deposited, reported on the Statement of Transactions, Statement of Accountability and the Yearend ClosingStatement. Federal agencies use the FBWT account to record appropriation, receipt, transfer and disbursement activity.Typical fund balance transactions involve: (1) appropriations; (2) accounts receivable; (3) disbursements/deposits intransit; (4) accrued payroll/benefits; (5) accounts payable; (6) miscellaneous receipts; and (7) advances on customerorders. Agencies record this activity in the U.S. Standard General Ledger (SGL) Account 1010 and any relatedsubaccounts. The fund balance is increased by a debit general ledger (G/L) entry. Credit G/L entries decrease the fundbalance. Federal agencies must use the FBWT account to reconcile with the Department of the Treasury, FinancialManagement Service (FMS) records. This reconciliation is essential to enhancing internal controls, improving theintegrity of various U.S. Government financial reports and providing a more accurate measurement of budget results.

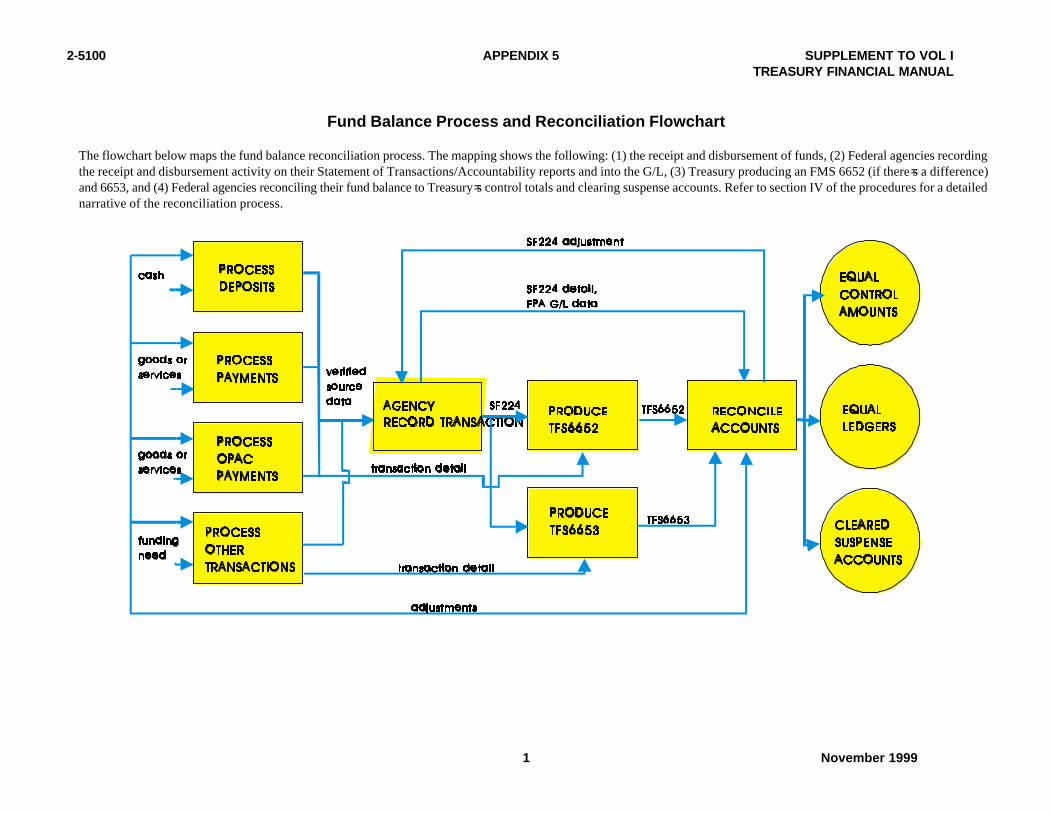

Federal agencies derive fund balances from different sources. At the agency level, agencies accumulate the fundbalance from the numerous receipt and disbursement transactions they record in the SGL 1010 account during anaccounting month. Agencies also report this activity on their Statement of Transactions and Statement ofAccountability. FMS uses STAR, an accounting and reporting system that integrates data from financial institutions(FIs) via CA$HLINK, the On-line Payment and Collection System (OPAC) and the Regional Finance Centers (RFCs).FMS uses the information consolidated into STAR to compare agencies reported receipts and disbursements toamounts reported by depositories using form FMS 6652. Therefore, any discrepancies between agency reports and datafrom banks, RFCs and the OPAC system are reported on FMS 6652. FMS also uses STAR information to generate andpresent accounting results for the month by fund to Federal agencies. FMS presents those accounting results on theFMS 6653: Undisbursed Appropriation Account Ledger, FMS 6654: Undisbursed Appropriation Account Trial Balance,FMS 6655: Receipt Account Ledger/Trial Balance, and FMS 6652: Statement of Differences (SOD). FMS 6653 and 6654give agencies their closing fund balances. The FMS 6655 discloses agencies = receipt account totals. Agencies mayaccess those reports, FMS 6652, 6653, 6654 and 6655, using either the Government On-line Accounting Link System(GOALS) or microfiche. See Appendix 5 of this document for a map of reconciliation process procedures.

2-5100 SUPPLEMENT TO VOL ITREASURY FINANCIAL MANUAL

November 19993

V. Policy:

A. Periodic Review and Evaluation

Federal agencies must reconcile their SGL 1010 account and any related subaccounts with the FMS 6652, 6653,6654 and 6655 on a monthly basis (at minimum). They must review those accounts each month to maintain theaccuracy and reliability of their fund balance records for both prior year and current year appropriations.Agencies must reconcile no-year, revolving, deposit and trust fund accounts. They also must reconcileclearing and receipt accounts. This detailed reconciliation assures that agency data accumulated in the fundbalance account is accurate. It also allows the agency to resolve differences in a timely manner. Whenresolving differences, agencies should maintain detailed reconciliation worksheets (see Appendix 1) that, ifneeded, can be reviewed by the agency=s auditors or Treasury.

B. Differences

Federal agencies must research and resolve differences reported on the monthly FMS 6652. They also mustresolve all differences between the balances reported on their G/L FBWT accounts and balances reported onthe FMS 6653, 6654 and 6655. FMS notifies agencies of their deposit and disbursement differences on FMS6652. FAB also sends periodic reminder letters of deposit and disbursement differences to each agency.

C. Adjustments

An agency may not arbitrarily adjust its FBWT account. Only after clearly establishing the causes of errorsand properly documenting those errors, should an agency adjust its FBWT account balance. If an agencymust make material adjustments, the agency must maintain supporting documentation. This will allow correctinterpretation of the error and its corresponding adjustment.

D. Financial Management System Responsibilities

Reconciliation and related verifications ensure and demonstrate the integrity of the accounting system. Thesefunctions are necessary for a well-regulated system. To increase the efficiency of reconciling the fund balance,each agency=s system should perform the following:

• Each financial system=s policies and documented procedures should provide for: (1) regular androutine reconciliation of G/L accounts, (2) thorough investigation of differences, (3)determination of specific causes of differences and (4) initiation of corrective action. Thisincludes having the ability to schedule coordinated cutoffs and systematically produce a trialbalance of the G/L. These activities must be scheduled and conducted to facilitate rather thanimpede the reconciliation process.

• Also, the accounting system should be capable of producing subsidiary reports that providea detailed history of receipt and disbursement activity recorded during the month, by fund. Thesubsidiary report balances should agree with the G/L.

• Processing controls and error checks should be programmed into the automated system, to theextent feasible. This will provide the maximum assurance that data recorded in the fund balanceaccount is accurate.

• Federal agencies = financial management systems should satisfy the directives promulgated bythe Joint Financial Management Improvement Program, Core Financial System Requirements;the Chief Financial Officers Act of 1990; Government Management Reform Act of 1994; theOffice of Management and Budget (OMB) Circular A-127, Financial Management Systems;OMB Circular A-123, Management Accountability and Control; the Federal Managers= FinancialIntegrity Act; and the Treasury Financial Manual. These regulations provide guidance on the

SUPPLEMENT TO VOL I 2-5100TREASURY FINANCIAL MANUAL

November 1999 4

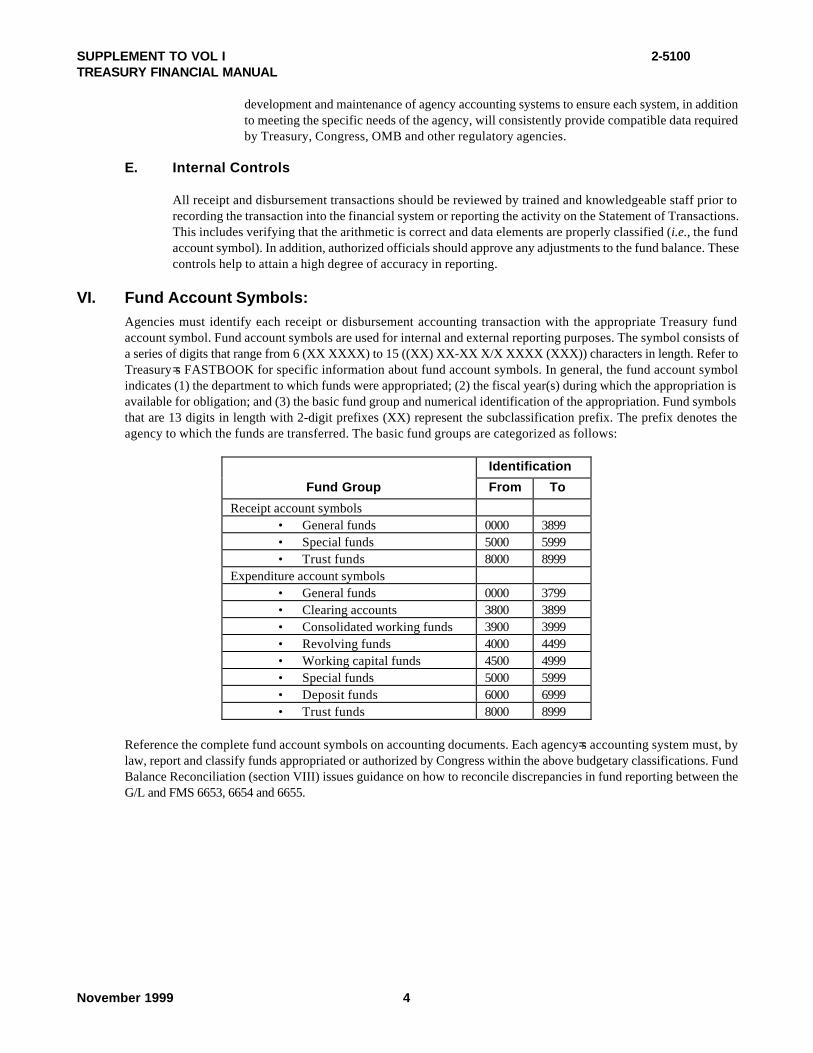

development and maintenance of agency accounting systems to ensure each system, in additionto meeting the specific needs of the agency, will consistently provide compatible data requiredby Treasury, Congress, OMB and other regulatory agencies.

E. Internal Controls

All receipt and disbursement transactions should be reviewed by trained and knowledgeable staff prior torecording the transaction into the financial system or reporting the activity on the Statement of Transactions.This includes verifying that the arithmetic is correct and data elements are properly classified (i.e., the fundaccount symbol). In addition, authorized officials should approve any adjustments to the fund balance. Thesecontrols help to attain a high degree of accuracy in reporting.

VI. Fund Account Symbols:Agencies must identify each receipt or disbursement accounting transaction with the appropriate Treasury fundaccount symbol. Fund account symbols are used for internal and external reporting purposes. The symbol consists ofa series of digits that range from 6 (XX XXXX) to 15 ((XX) XX-XX X/X XXXX (XXX)) characters in length. Refer toTreasury =s FASTBOOK for specific information about fund account symbols. In general, the fund account symbolindicates (1) the department to which funds were appropriated; (2) the fiscal year(s) during which the appropriation isavailable for obligation; and (3) the basic fund group and numerical identification of the appropriation. Fund symbolsthat are 13 digits in length with 2-digit prefixes (XX) represent the subclassification prefix. The prefix denotes theagency to which the funds are transferred. The basic fund groups are categorized as follows:

Identification

Fund Group From To

Receipt account symbols• General funds 0000 3899• Special funds 5000 5999• Trust funds 8000 8999

Expenditure account symbols• General funds 0000 3799• Clearing accounts 3800 3899• Consolidated working funds 3900 3999• Revolving funds 4000 4499• Working capital funds 4500 4999• Special funds 5000 5999• Deposit funds 6000 6999• Trust funds 8000 8999

Reference the complete fund account symbols on accounting documents. Each agency=s accounting system must, bylaw, report and classify funds appropriated or authorized by Congress within the above budgetary classifications. FundBalance Reconciliation (section VIII) issues guidance on how to reconcile discrepancies in fund reporting between theG/L and FMS 6653, 6654 and 6655.

2-5100 SUPPLEMENT TO VOL ITREASURY FINANCIAL MANUAL

November 19995

VII. Agency Location Code (ALC):

The ALC is a unique numeric symbol used as an identifier in financial reports and documents prepared by or foragencies and disbursing offices. The ALC contains eight, four or three digits. An 8-digit ALC, XX-XX-XXXX, identifiesthe reporting and accounting sources. The first two characters of the 8-digit code identify the department or agency.The third and fourth digits represent the bureau within the department or agency. The remaining four digits identifythe accounting station within the bureau. The 4-digit ALC, 00-00-XXXX, is the non-Treasury disbursing office symbol.Treasury establishes and approves each ALC.

VIII. Fund Balance Reconciliation:

Agencies must perform fund balance reconciliation for each Treasury fund account symbol. Any reports or documentsused to reconcile must reflect an identical accounting month and fund account symbol. If an agency=s G/L Chart ofAccounts includes subaccounts for the SGL 1010 account, agencies must include subaccount balances in the summarySGL account total.

A. Documentation Used for Reconciliation

The basic records used to report collection and disbursement activity are derived from source documents thatevidence a transaction. These documents serve as the official means of reference to reconcile the FBWTaccount. Federal agencies may use the source documents identified below in part 1, “Agency SourceDocuments.” The documents FMS uses to compare fund balance activity are identified in the following listing,under part 2 “Treasury Reports.”

1. Agency Source Documents

Federal agencies may internally develop and use various documents to track, record and reportfinancial events. They should record only those documents that comply with statutory requirements.Agencies should use the following sources, currently used throughout the Federal Government, toreport on the status of receipts or disbursements:

• Letters of credit.• SF 1166.• SF 1081.• SF 1098.• SF 1151.• SF 215.• SF 5515.• FMS 145.• FMS 1185.• FMS 6200.• OPAC (in lieu of SF 1081).

Agencies generally use the trial balance to obtain the SGL 1010 account balances. The trial balanceshould reveal, at a minimum, the following information by fund account symbol for easierreconciliation:

• Balance forwarded from previous month.• Current month debits/credits (based on increases and decreases to the account).• Ending fund balance (the difference between the balance forwarded and net current month

activity).

2. Treasury Reports

SUPPLEMENT TO VOL I 2-5100TREASURY FINANCIAL MANUAL

November 1999 6

FMS provides FMS 6652, 6653, 6654 and 6655 reports to Federal agencies monthly. These reportscapture data recorded on agencies = Statements of Transactions and Accountability reports and dataentered into the FMS central accounting and reporting system. Agencies should use these reportsto reconcile their FBWT account. The reconciliation helps to (1) validate that reliable data is reported,(2) identify and correct errors with agencies = records and (3) determine any discrepancies reportedby FMS. Agencies should notify FMS of any discrepancies.

a. SF 224: Statement of Transactions

The SF 224 is the central accounting document used only by 8-digit ALCs to report theirmonthly accounting activity to Treasury. The SF 224 provides Treasury with informationon agency deposits and disbursements. The report captures data by appropriation, fundand receipt accounts.

Agencies for which Treasury disburses must prepare and submit the SF 224 via GOALS bythe 5th workday of the current month. A separate SF 224 must be furnished for each 8-digitALC. The SF 224 may contain adjustments for prior month=s accounting activity or reflectno activity for the month, if applicable. Agencies must submit a supplemental SF 224 by the8th workday of the current month. FMS uses the supplemental SF 224 to capture financialactivity not reported on the original SF 224 or to adjust information reported on the originalSF 224.

FMS relies on the totals reported on the SF 224 to identify differences between Federalagencies = records and Treasury control totals reported by financial institutions. The totalin section II, line 1, identifies the net disbursements recorded by an agency. It is separatedinto current and prior month amounts. The amount on this line is compared to Treasurydisbursement control totals. The total in section III, line 3, identifies the collection anddeposit activity. It includes total collections for the current and prior months. Informationon this line is compared to Treasury deposit control totals.

b. SF 1218/1221: Statement of Accountability/Transactions

The SF 1218 is the means by which Treasury determines the accountability of foreigndisbursing officers (USDOs) for funds held outside Treasury. SF 1218 reflectsaccountability transactions reported under the 4-digit ALC. An SF 1218 must be providedwhenever an SF 1221 is submitted.

The SF 1221 is prepared by USDOs who collect and/or disburse foreign currency. In thisreport, the information is classified by appropriation, fund and receipt accounts. The SF1221 supports the SF 1218 and provides Treasury with a monthly statement of paymentsand collections made by USDOs. The SF 1218 and 1221 reports are due to Treasury by the7th workday following the close of an accounting month.

c. SF 1219/1220: Statement of Accountability/Transactions

Domestic DOs and other agencies with disbursing authority submit a monthly SF 1219 and1220 to Treasury. Treasury uses the reports to summarize collection and disbursementactivity for the month. This includes all Electronic Fund Transfer payments, preparedchecks or other disbursements. SF 1219 provides detailed information about disbursingoffice collections and disbursements. Section I of the SF 1219 discloses changes to thedisbursing officer=s accountability. These changes are based on increases and decreasesto fund balances. Section II provides details of disbursement and deposit activity as wellas prior period adjustments. SF 1220: Statement of Transactions is similar to the SF 224. Italso provides Treasury with information related to an agency=s disbursement and collection

2-5100 SUPPLEMENT TO VOL ITREASURY FINANCIAL MANUAL

November 19997

activity. Agencies report the disbursement and collection data by appropriation, fund andreceipt accounts. The SF 1219 and 1220 statements must be submitted to Treasury by the7th workday following the close of the accounting month.

d. Reconciliation of Checks Issued

FMS performs a two-step reconciliation of checks issued by RFCs and NTDOs. First, FMScompares item for item each check issued to the amount paid by the Federal Reserve Banks(FRBs) as presented through financial institutions. Second, FMS compares Statements ofAccountability, SF 1219 or 1218 (line 2.10), to the detail of checks issued to assure allchecks issued have been recorded as charges against appropriation or fund accountsymbols.

At the close of each week and month, disbursing officers submit to FMS a Level 8 magnetictape (or electronic file transmission) that details by check symbol, serial number and amountall checks issued during the period (refer to I TFM 4-6500 for specific reportingrequirements). Daily, FRB check processing offices submit to FMS an electronic file thatdetails by check symbol, serial number and amount all checks paid that business day. TheLevel 8 check data and the FRB paid data are entered into the FMS Check Payment andReconciliation (CP&R) system. Items that match exactly are reconciled and placed inarchive. For items that do not match exactly, FMS reviews an image of the check todetermine if a forgery has been paid or if the issue data was erroneous. Where forgery hasoccurred, FMS reclaims the payment amount from the financial institution. When the issuerecord is at fault, FMS issues the DO an FMS Form 5206. The DO must review each FMS5206, determine the reason for the error, record an appropriate adjustment and report suchadjustments on their next SF 1219 or 1218.

Monthly, each DO prepares and submits to FMS their SF 1219 or 1218. Line 2.10 summarizesthe Level 8 detail check data submitted net of FMS 5206 adjustments processed and otherDO identified adjustments. FMS compares SF 1219/1218 reporting to check issue data, FMS5206 adjustments and DO requested adjustments entered into the FMS CP&R system. Fordiscrepancies detected in this comparison, FMS sends the DO notification by letter. TheDO must review the letter and determine the appropriate action needed to bring the CP&Rsystem and the SF 1219/1218 reporting into agreement (see section VIII, part 3, exhibit 3E).

e. FMS 6652: Statement of Differences

FMS provides FMS 6652 to Federal agencies for both disbursements and deposits. A FMS6652 is generated for each ALC by accounting and accomplished month if there is adiscrepancy. The accounting month is the month the report is generated. The accomplishedmonth is the month the difference occurred. Differences resulting from deposits indicatethere is a discrepancy between the monthly totals submitted through the banking systemvia SF 215/5515s and the totals provided by the agency on the SF 224 (section III, line 3)or 1219 (section I, line 4.2). Treasury removes deposit differences of less than $50 and morethan 6 months old to a small difference account. The SOD for Disbursement transactionsreveal discrepancies between monthly totals reported by the RFCs and/or through OPACtransactions between agencies and totals in agency reports on the SF 224 (section II, line1) or 1219 (line 2.80). As stated in section V, agencies must research and resolve alldifferences. Differences that are not cleared during the next accounting month are carriedforward to subsequent months until cleared. Agencies should report clearly supportedcorrective entries on the subsequent month=s Statement of Transactions/ Accountability.

Federal agencies should compare the items reported on their internal deposit listing orcollection schedules to the monthly deposit ticket/debit voucher support listing received

SUPPLEMENT TO VOL I 2-5100TREASURY FINANCIAL MANUAL

November 1999 8

via GOALS or CA$HLINK to reconcile deposit differences. An agency can reconciledisbursement differences by comparing the transactions reported on the support listingsfor disbursement transactions to the agency=s internal subsidiary report or control ledgerof disbursement activity and/or individual disbursement source documents. Thedisbursement support listings generated from GOALS include the RFC Agency Link(agency confirmation report) and OPAC transactions.

f. FMS 6653: Undisbursed Appropriation Account Ledger

FMS provides Federal agencies with a monthly FMS 6653 for expenditure accounts thathave monthly activity. FMS 6653 provides information about the appropriation warrantsissued, nonexpenditure transfers, transactions reported by agencies on the Statement ofTransactions and those reported by other agencies as well as certain centrally processedFMS documents. Transactions commonly reported by other agencies and FMS are thenonexpenditure transfer, payroll disbursements, warrant and GOALS charges.

FMS 6653 is arranged to report the opening fund balance for the month, current monthtransactions, net disbursements and the closing balance at the end of the accountingmonth. Federal agencies must reconcile the FBWT account to the closing balancepresented on FMS 6653 and FACTS II.

The transaction codes reported on FMS 6653 indicate the type of activity reported. Themost commonly used transaction codes are 10: appropriation warrant, 61: disbursementsand 71: repayments. A detailed listing of transaction codes that may appear on FMS 6653is shown in Appendix 2.

g. FMS 6654: Undisbursed Appropriation Account Trial Balance

FMS 6654 provides agencies with summary data about their expenditure accounts. Thisdata is summarized for each appropriation and fund account at the department level and atthe bureau level for certain executive departments. The data reveals the balance forwardedat the beginning of the fiscal year, cumulative warrants, nonexpenditure transactions, netdisbursements to date and closing balances at month end. Federal agencies must reconciletheir FBWT accounts to the closing balances shown in this report.

h. FMS 6655: Unappropriated Receipt Account Ledger

FMS 6655 contains detailed receipt transactions and balances reported by an agencyduring an accounting month. These balances are unavailable for expenditure until Congresspasses specific appropriation legislation. It discloses information related to the balanceforwarded, current month receipt transactions and the month-end closing account total.This information is reported for each special and trust fund receipt account. Federalagencies must reconcile their receipt activity to the closing balance shown on FMS 6655.The transaction codes that may appear on the FMS 6655 are disclosed in Appendix 2.

i. FMS 6655: Receipt Account Trial Balance

FMS 6655 shows receipt balances by fund account symbol and department. This includesyear-to-date and current month receipt totals. Federal agencies must reconcile their currentmonth and year-to-date receipt activity to the balances disclosed in this report.

j. FMS 6655: Report of Unavailable Receipt Transactions

2-5100 SUPPLEMENT TO VOL ITREASURY FINANCIAL MANUAL

November 19999

FMS 6655 shows collections or deposits of funds in accounts that are not immediatelyavailable for expenditure. The unavailable receipt balances are provided for each receiptaccount symbol.

k. FMS 2108: Yearend Closing Statement

FMS 2108 reports the fund balance for each expenditure account symbol that has a balanceand/or activity for the fiscal year. The FMS 2108 also reports the amount of receivables,unfilled customer orders, unobligated balances and unpaid obligations. Beginning fiscal1999, Federal agencies will submit the FMS 2108 data to FMS using the Federal Agencies =Centralized Trial Balance System (FACTS II).

B. Step-By-Step Reconciliation Process

The steps used to perform fund balance reconciliation are presented in exhibits 1A through 4A. Each exhibituses three column headings: “step,” “action” and “required documents.” The “step” column numbers theactions that must be accomplished to complete the reconciliation. The “action” column describes each stepin terms of the specific processes that need to be performed to accomplish the reconciliation. The “action”column also gives examples of common discrepancies and details corrections that must be made to theagency’s Statement of Transactions/Accountability and/or the G/L. “Action” also describes commonreconciliation worksheet annotations. The final column titled “required documents” lists the reports an agencywill use to perform the actions/reconciliations.

This section provides step-by-step procedures for reconciling the agency FBWT accounts to the FMS 6653.The following procedures also apply to reconciling FMS 6654 (when there is no monthly activity for anexpenditure account symbol), FMS 6655 as well as the SF 224, 1218/1221 and 1219/1220 reports. Theprocedures are in how-to exhibit formats. As a quick reference, the exhibits provide step-by-step directionsfor the following:

1. Comparing FMS 6653 and General Ledger Totals

• Exhibit 1A—How to Compare FMS 6653 and General Ledger Totals.

• Exhibit 1B—How to Identify Differences in FMS 6653 and General Ledger Entries Reported bythe Agency.

• Exhibit 1C—How to Identify Differences in FMS 6653 and General Ledger Entries Reported byAnother Agency.

• Exhibit 1D—How to Determine the Month-End Unreconciled Balance.

2. Identifying Prior Month Differences

• Exhibit 2A—How to Identify Prior Month Differences.

3. Reconciling Statements of Differences

• Exhibit 3A—How to Reconcile Statement of Differences for Disbursements.

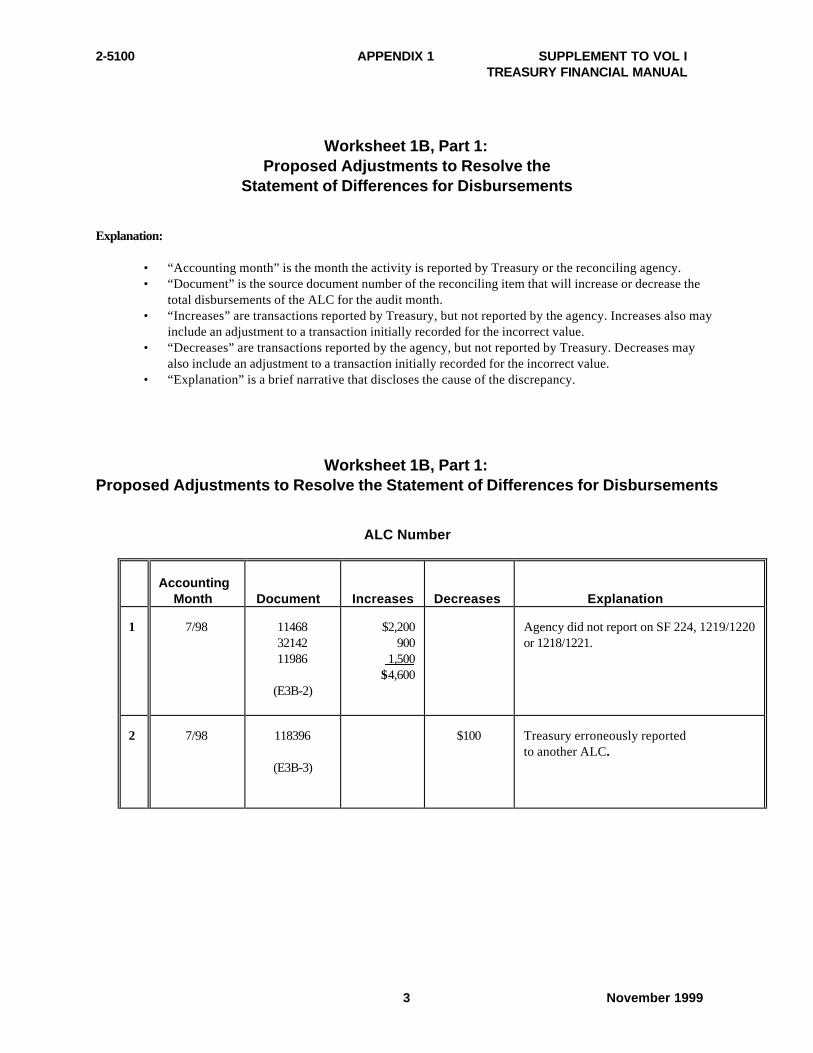

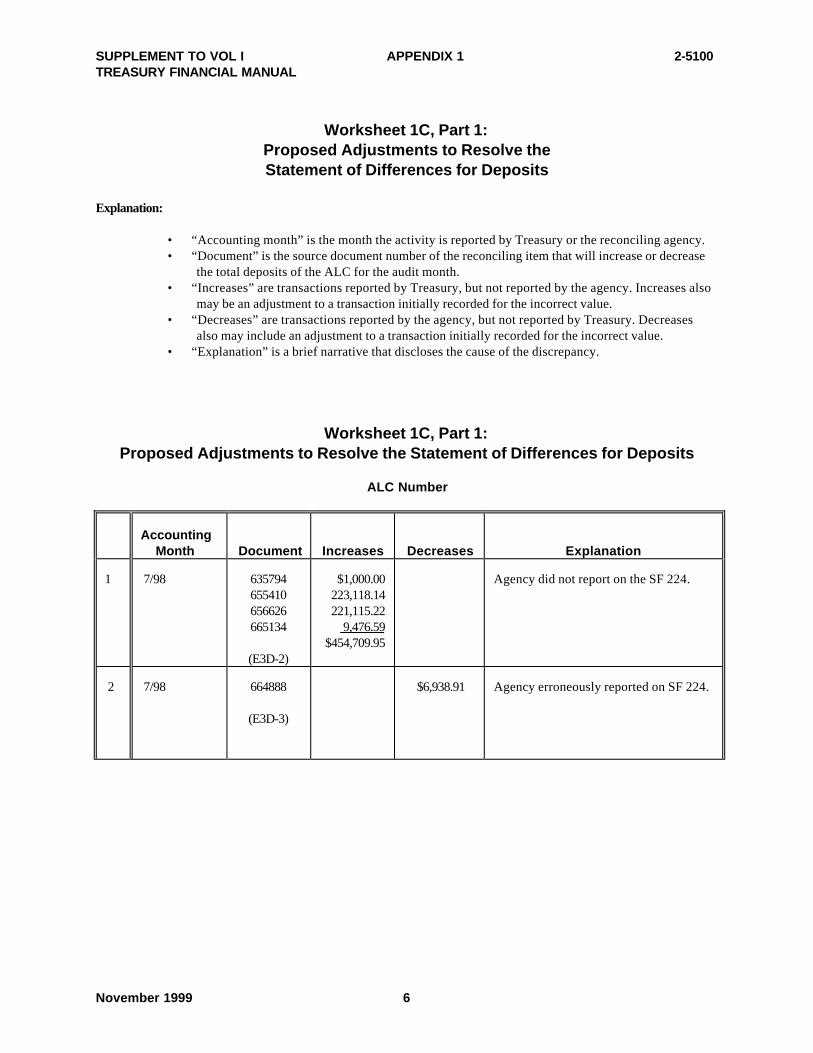

• Exhibit 3B—How to Use Worksheet 1B: Statement of Differences for Disbursements.

• Exhibit 3C—How to Reconcile Statement of Differences for Deposits.

• Exhibit 3D—How to Use Worksheet 1C: the Statement of Differences for Deposits.

SUPPLEMENT TO VOL I 2-5100TREASURY FINANCIAL MANUAL

November 1999 10

• Exhibit 3E—How to Reconcile Check Issue Audits Using FMS 5206.

4. Researching Uncleared Differences

• Exhibit 4A—How to Research Uncleared Differences.

2-5100 SUPPLEMENT TO VOL ITREASURY FINANCIAL MANUAL

November 199911

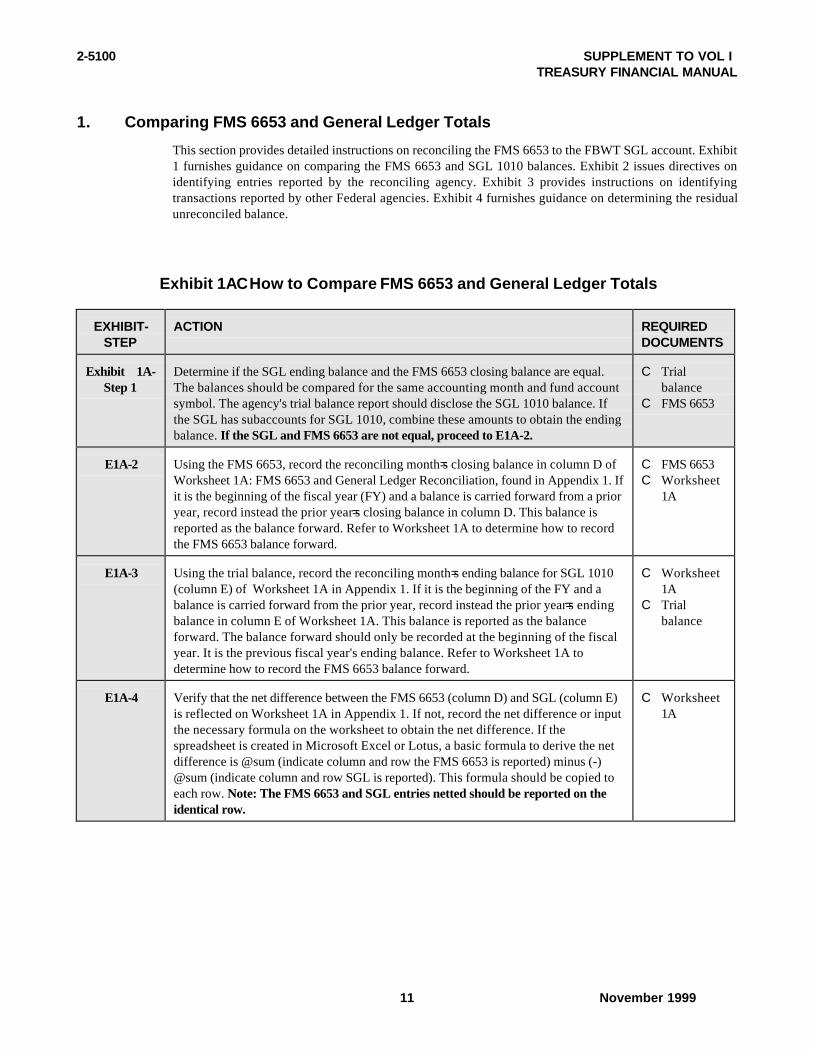

1. Comparing FMS 6653 and General Ledger Totals

This section provides detailed instructions on reconciling the FMS 6653 to the FBWT SGL account. Exhibit1 furnishes guidance on comparing the FMS 6653 and SGL 1010 balances. Exhibit 2 issues directives onidentifying entries reported by the reconciling agency. Exhibit 3 provides instructions on identifyingtransactions reported by other Federal agencies. Exhibit 4 furnishes guidance on determining the residualunreconciled balance.

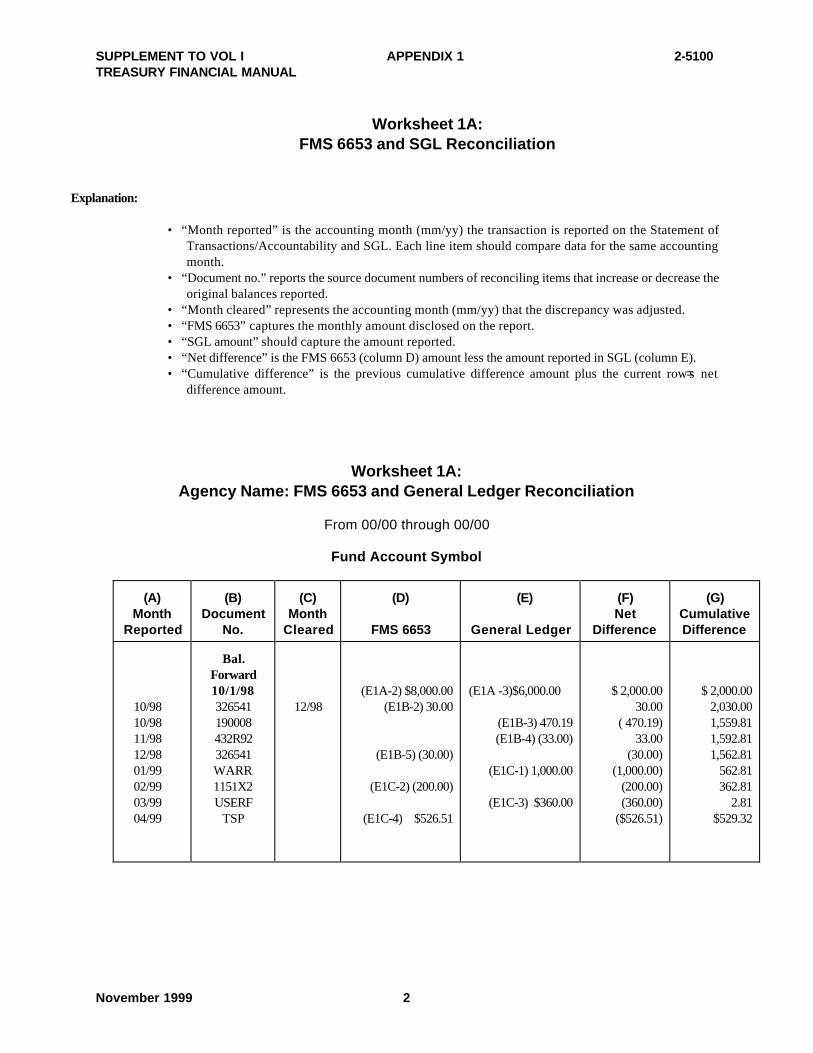

Exhibit 1ACHow to Compare FMS 6653 and General Ledger Totals

EXHIBIT-STEP

ACTION REQUIREDDOCUMENTS

Exhibit 1A-Step 1

Determine if the SGL ending balance and the FMS 6653 closing balance are equal.The balances should be compared for the same accounting month and fund accountsymbol. The agency's trial balance report should disclose the SGL 1010 balance. Ifthe SGL has subaccounts for SGL 1010, combine these amounts to obtain the endingbalance. If the SGL and FMS 6653 are not equal, proceed to E1A-2.

C Trialbalance

C FMS 6653

E1A-2 Using the FMS 6653, record the reconciling month=s closing balance in column D ofWorksheet 1A: FMS 6653 and General Ledger Reconciliation, found in Appendix 1. Ifit is the beginning of the fiscal year (FY) and a balance is carried forward from a prioryear, record instead the prior year=s closing balance in column D. This balance isreported as the balance forward. Refer to Worksheet 1A to determine how to recordthe FMS 6653 balance forward.

C FMS 6653C Worksheet

1A

E1A-3 Using the trial balance, record the reconciling month=s ending balance for SGL 1010(column E) of Worksheet 1A in Appendix 1. If it is the beginning of the FY and abalance is carried forward from the prior year, record instead the prior year=s endingbalance in column E of Worksheet 1A. This balance is reported as the balanceforward. The balance forward should only be recorded at the beginning of the fiscalyear. It is the previous fiscal year's ending balance. Refer to Worksheet 1A todetermine how to record the FMS 6653 balance forward.

C Worksheet1A

C Trialbalance

E1A-4 Verify that the net difference between the FMS 6653 (column D) and SGL (column E)is reflected on Worksheet 1A in Appendix 1. If not, record the net difference or inputthe necessary formula on the worksheet to obtain the net difference. If thespreadsheet is created in Microsoft Excel or Lotus, a basic formula to derive the netdifference is @sum (indicate column and row the FMS 6653 is reported) minus (-)@sum (indicate column and row SGL is reported). This formula should be copied toeach row. Note: The FMS 6653 and SGL entries netted should be reported on theidentical row.

C Worksheet1A

SUPPLEMENT TO VOL I 2-5100TREASURY FINANCIAL MANUAL

November 1999 12

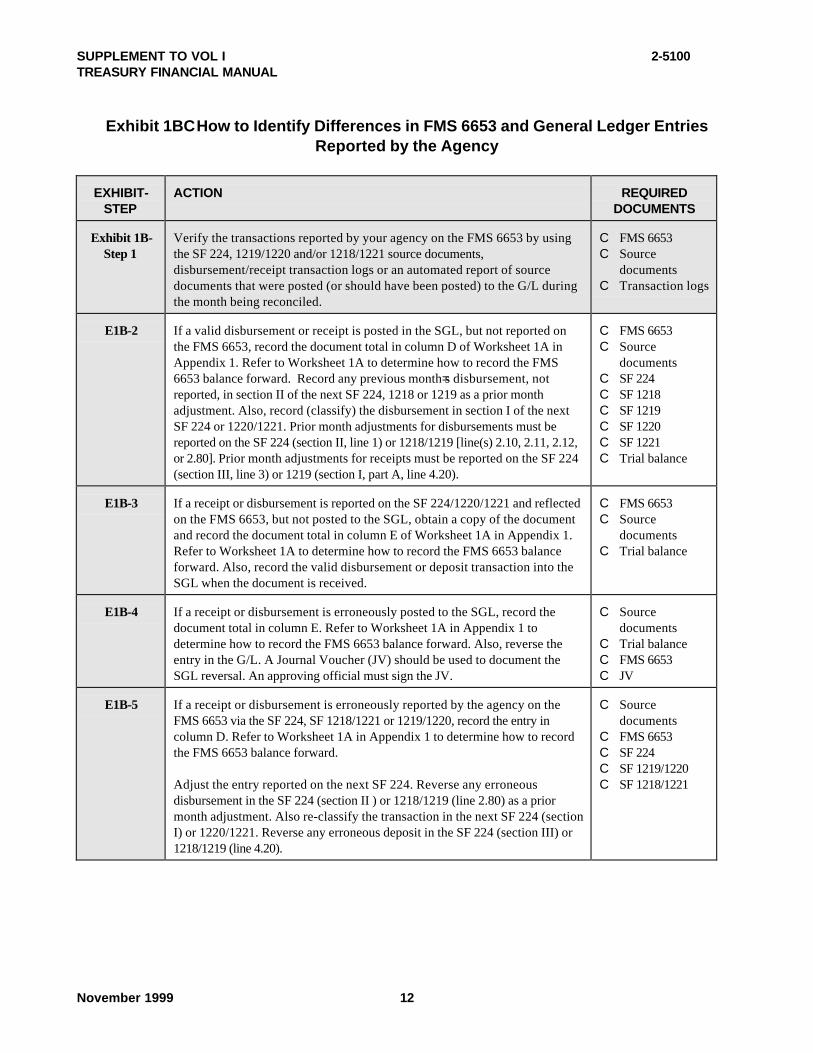

Exhibit 1BCHow to Identify Differences in FMS 6653 and General Ledger EntriesReported by the Agency

EXHIBIT-STEP

ACTION REQUIREDDOCUMENTS

Exhibit 1B-Step 1

Verify the transactions reported by your agency on the FMS 6653 by usingthe SF 224, 1219/1220 and/or 1218/1221 source documents,disbursement/receipt transaction logs or an automated report of sourcedocuments that were posted (or should have been posted) to the G/L duringthe month being reconciled.

C FMS 6653C Source

documentsC Transaction logs

E1B-2 If a valid disbursement or receipt is posted in the SGL, but not reported onthe FMS 6653, record the document total in column D of Worksheet 1A inAppendix 1. Refer to Worksheet 1A to determine how to record the FMS6653 balance forward. Record any previous month=s disbursement, notreported, in section II of the next SF 224, 1218 or 1219 as a prior monthadjustment. Also, record (classify) the disbursement in section I of the nextSF 224 or 1220/1221. Prior month adjustments for disbursements must bereported on the SF 224 (section II, line 1) or 1218/1219 [line(s) 2.10, 2.11, 2.12,or 2.80]. Prior month adjustments for receipts must be reported on the SF 224(section III, line 3) or 1219 (section I, part A, line 4.20).

C FMS 6653C Source

documentsC SF 224C SF 1218C SF 1219C SF 1220C SF 1221C Trial balance

E1B-3 If a receipt or disbursement is reported on the SF 224/1220/1221 and reflectedon the FMS 6653, but not posted to the SGL, obtain a copy of the documentand record the document total in column E of Worksheet 1A in Appendix 1.Refer to Worksheet 1A to determine how to record the FMS 6653 balanceforward. Also, record the valid disbursement or deposit transaction into theSGL when the document is received.

C FMS 6653C Source

documentsC Trial balance

E1B-4 If a receipt or disbursement is erroneously posted to the SGL, record thedocument total in column E. Refer to Worksheet 1A in Appendix 1 todetermine how to record the FMS 6653 balance forward. Also, reverse theentry in the G/L. A Journal Voucher (JV) should be used to document theSGL reversal. An approving official must sign the JV.

C Sourcedocuments

C Trial balanceC FMS 6653C JV

E1B-5 If a receipt or disbursement is erroneously reported by the agency on theFMS 6653 via the SF 224, SF 1218/1221 or 1219/1220, record the entry incolumn D. Refer to Worksheet 1A in Appendix 1 to determine how to recordthe FMS 6653 balance forward.

Adjust the entry reported on the next SF 224. Reverse any erroneousdisbursement in the SF 224 (section II ) or 1218/1219 (line 2.80) as a priormonth adjustment. Also re-classify the transaction in the next SF 224 (sectionI) or 1220/1221. Reverse any erroneous deposit in the SF 224 (section III) or1218/1219 (line 4.20).

C Sourcedocuments

C FMS 6653C SF 224C SF 1219/1220C SF 1218/1221

2-5100 SUPPLEMENT TO VOL ITREASURY FINANCIAL MANUAL

November 199913

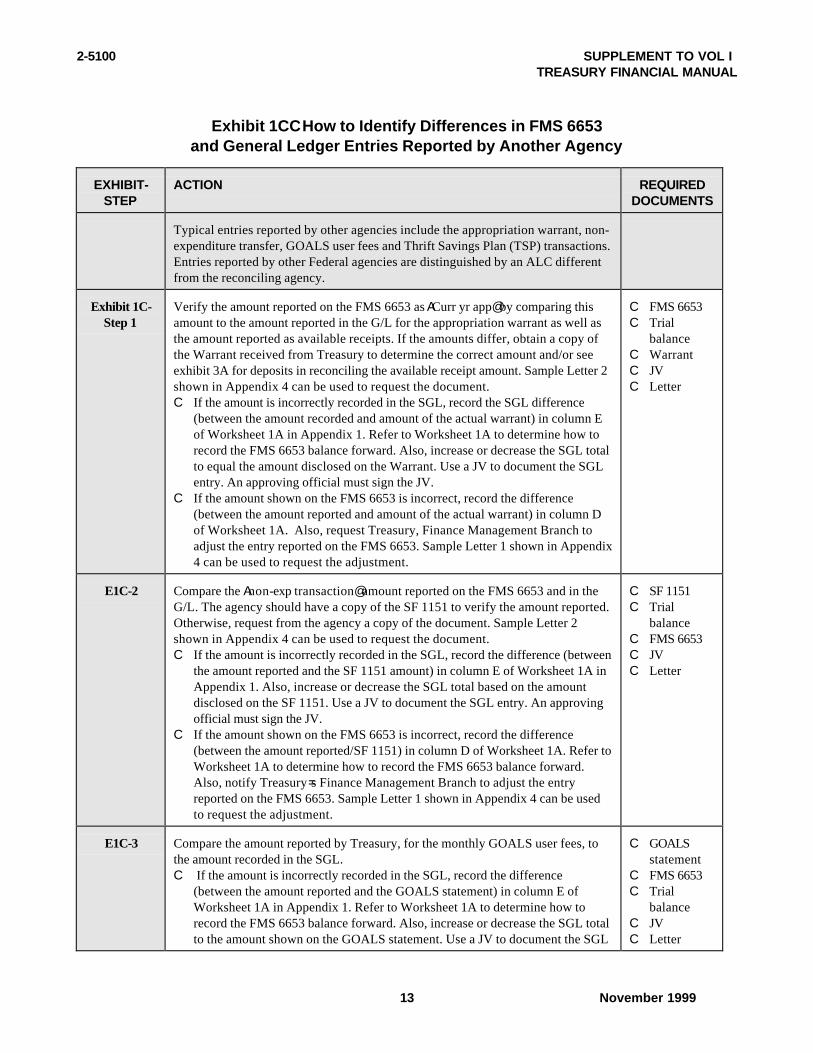

Exhibit 1CCHow to Identify Differences in FMS 6653and General Ledger Entries Reported by Another Agency

EXHIBIT-STEP

ACTION REQUIREDDOCUMENTS

Typical entries reported by other agencies include the appropriation warrant, non-expenditure transfer, GOALS user fees and Thrift Savings Plan (TSP) transactions.Entries reported by other Federal agencies are distinguished by an ALC differentfrom the reconciling agency.

Exhibit 1C-Step 1

Verify the amount reported on the FMS 6653 as ACurr yr app@ by comparing thisamount to the amount reported in the G/L for the appropriation warrant as well asthe amount reported as available receipts. If the amounts differ, obtain a copy ofthe Warrant received from Treasury to determine the correct amount and/or seeexhibit 3A for deposits in reconciling the available receipt amount. Sample Letter 2shown in Appendix 4 can be used to request the document.C If the amount is incorrectly recorded in the SGL, record the SGL difference

(between the amount recorded and amount of the actual warrant) in column Eof Worksheet 1A in Appendix 1. Refer to Worksheet 1A to determine how torecord the FMS 6653 balance forward. Also, increase or decrease the SGL totalto equal the amount disclosed on the Warrant. Use a JV to document the SGLentry. An approving official must sign the JV.

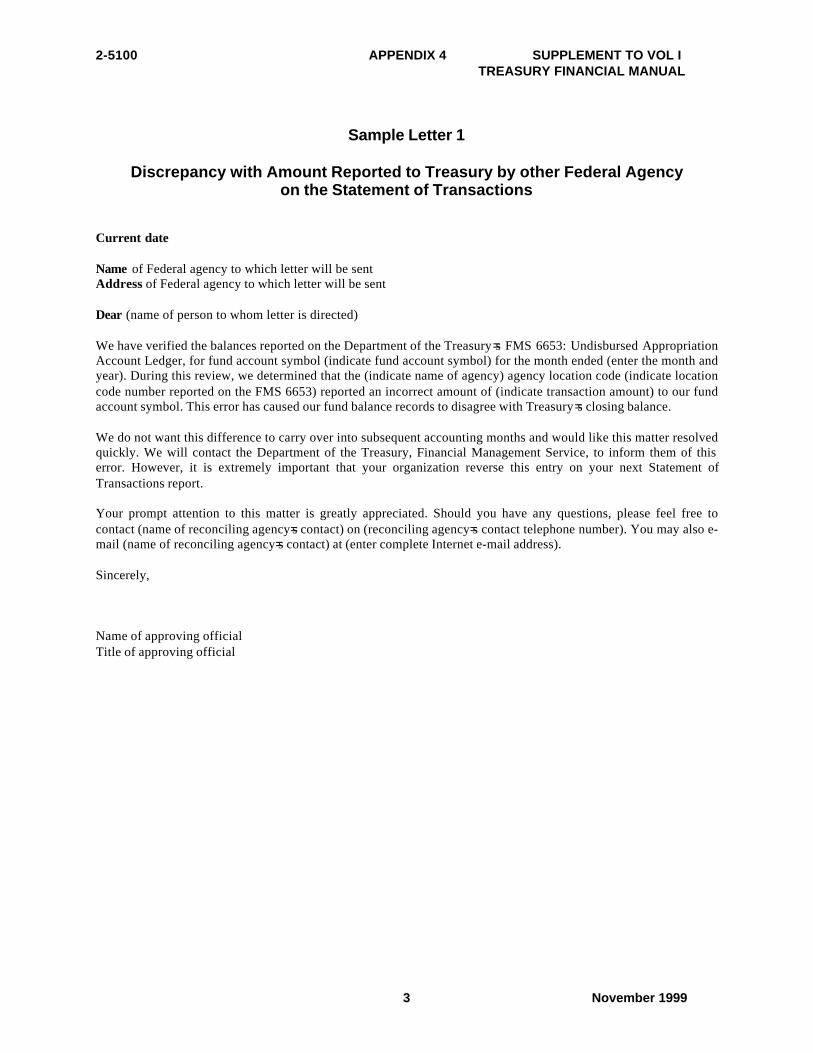

C If the amount shown on the FMS 6653 is incorrect, record the difference(between the amount reported and amount of the actual warrant) in column Dof Worksheet 1A. Also, request Treasury, Finance Management Branch toadjust the entry reported on the FMS 6653. Sample Letter 1 shown in Appendix4 can be used to request the adjustment.

C FMS 6653C Trial

balanceC WarrantC JVC Letter

E1C-2 Compare the Anon-exp transaction@ amount reported on the FMS 6653 and in theG/L. The agency should have a copy of the SF 1151 to verify the amount reported.Otherwise, request from the agency a copy of the document. Sample Letter 2shown in Appendix 4 can be used to request the document.C If the amount is incorrectly recorded in the SGL, record the difference (between

the amount reported and the SF 1151 amount) in column E of Worksheet 1A inAppendix 1. Also, increase or decrease the SGL total based on the amountdisclosed on the SF 1151. Use a JV to document the SGL entry. An approvingofficial must sign the JV.

C If the amount shown on the FMS 6653 is incorrect, record the difference(between the amount reported/SF 1151) in column D of Worksheet 1A. Refer toWorksheet 1A to determine how to record the FMS 6653 balance forward.Also, notify Treasury =s Finance Management Branch to adjust the entryreported on the FMS 6653. Sample Letter 1 shown in Appendix 4 can be usedto request the adjustment.

C SF 1151C Trial

balanceC FMS 6653C JVC Letter

E1C-3 Compare the amount reported by Treasury, for the monthly GOALS user fees, tothe amount recorded in the SGL.C If the amount is incorrectly recorded in the SGL, record the difference

(between the amount reported and the GOALS statement) in column E ofWorksheet 1A in Appendix 1. Refer to Worksheet 1A to determine how torecord the FMS 6653 balance forward. Also, increase or decrease the SGL totalto the amount shown on the GOALS statement. Use a JV to document the SGL

C GOALSstatement

C FMS 6653C Trial

balanceC JVC Letter

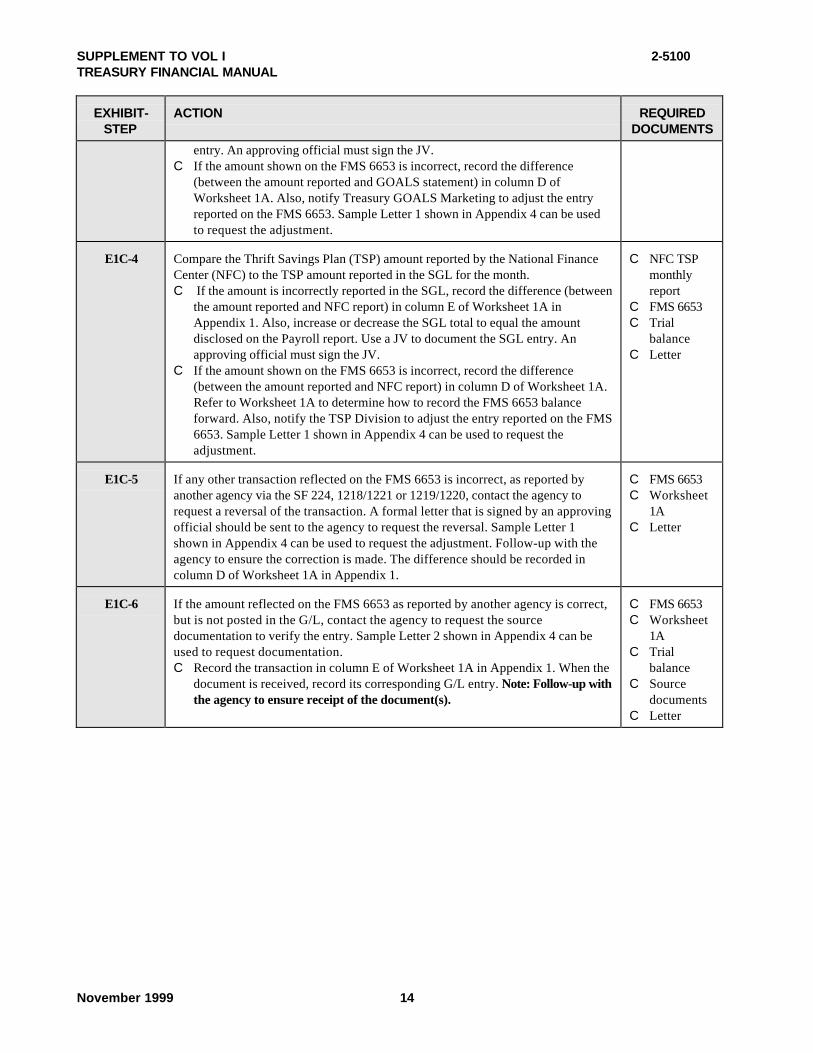

SUPPLEMENT TO VOL I 2-5100TREASURY FINANCIAL MANUAL

November 1999 14

EXHIBIT-STEP

ACTION REQUIREDDOCUMENTS

entry. An approving official must sign the JV.C If the amount shown on the FMS 6653 is incorrect, record the difference

(between the amount reported and GOALS statement) in column D ofWorksheet 1A. Also, notify Treasury GOALS Marketing to adjust the entryreported on the FMS 6653. Sample Letter 1 shown in Appendix 4 can be usedto request the adjustment.

E1C-4 Compare the Thrift Savings Plan (TSP) amount reported by the National FinanceCenter (NFC) to the TSP amount reported in the SGL for the month.C If the amount is incorrectly reported in the SGL, record the difference (between

the amount reported and NFC report) in column E of Worksheet 1A inAppendix 1. Also, increase or decrease the SGL total to equal the amountdisclosed on the Payroll report. Use a JV to document the SGL entry. Anapproving official must sign the JV.

C If the amount shown on the FMS 6653 is incorrect, record the difference(between the amount reported and NFC report) in column D of Worksheet 1A.Refer to Worksheet 1A to determine how to record the FMS 6653 balanceforward. Also, notify the TSP Division to adjust the entry reported on the FMS6653. Sample Letter 1 shown in Appendix 4 can be used to request theadjustment.

C NFC TSPmonthlyreport

C FMS 6653C Trial

balanceC Letter

E1C-5 If any other transaction reflected on the FMS 6653 is incorrect, as reported byanother agency via the SF 224, 1218/1221 or 1219/1220, contact the agency torequest a reversal of the transaction. A formal letter that is signed by an approvingofficial should be sent to the agency to request the reversal. Sample Letter 1shown in Appendix 4 can be used to request the adjustment. Follow-up with theagency to ensure the correction is made. The difference should be recorded incolumn D of Worksheet 1A in Appendix 1.

C FMS 6653C Worksheet

1AC Letter

E1C-6 If the amount reflected on the FMS 6653 as reported by another agency is correct,but is not posted in the G/L, contact the agency to request the sourcedocumentation to verify the entry. Sample Letter 2 shown in Appendix 4 can beused to request documentation.C Record the transaction in column E of Worksheet 1A in Appendix 1. When the

document is received, record its corresponding G/L entry. Note: Follow-up withthe agency to ensure receipt of the document(s).

C FMS 6653C Worksheet

1AC Trial

balanceC Source

documentsC Letter

2-5100 SUPPLEMENT TO VOL ITREASURY FINANCIAL MANUAL

November 199915

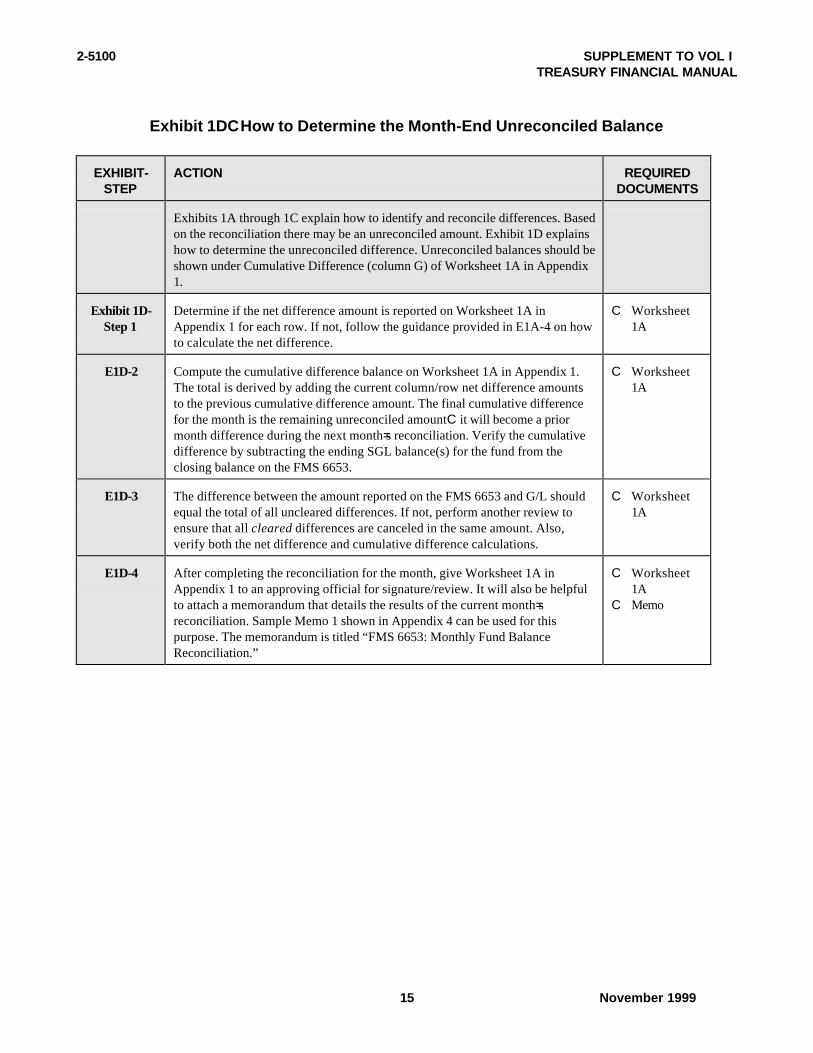

Exhibit 1DCHow to Determine the Month-End Unreconciled Balance

EXHIBIT-STEP

ACTION REQUIREDDOCUMENTS

Exhibits 1A through 1C explain how to identify and reconcile differences. Basedon the reconciliation there may be an unreconciled amount. Exhibit 1D explainshow to determine the unreconciled difference. Unreconciled balances should beshown under Cumulative Difference (column G) of Worksheet 1A in Appendix1.

Exhibit 1D-Step 1

Determine if the net difference amount is reported on Worksheet 1A inAppendix 1 for each row. If not, follow the guidance provided in E1A-4 on howto calculate the net difference.

C Worksheet1A

E1D-2 Compute the cumulative difference balance on Worksheet 1A in Appendix 1.The total is derived by adding the current column/row net difference amountsto the previous cumulative difference amount. The final cumulative differencefor the month is the remaining unreconciled amountC it will become a priormonth difference during the next month=s reconciliation. Verify the cumulativedifference by subtracting the ending SGL balance(s) for the fund from theclosing balance on the FMS 6653.

C Worksheet1A

E1D-3 The difference between the amount reported on the FMS 6653 and G/L shouldequal the total of all uncleared differences. If not, perform another review toensure that all cleared differences are canceled in the same amount. Also,verify both the net difference and cumulative difference calculations.

C Worksheet1A

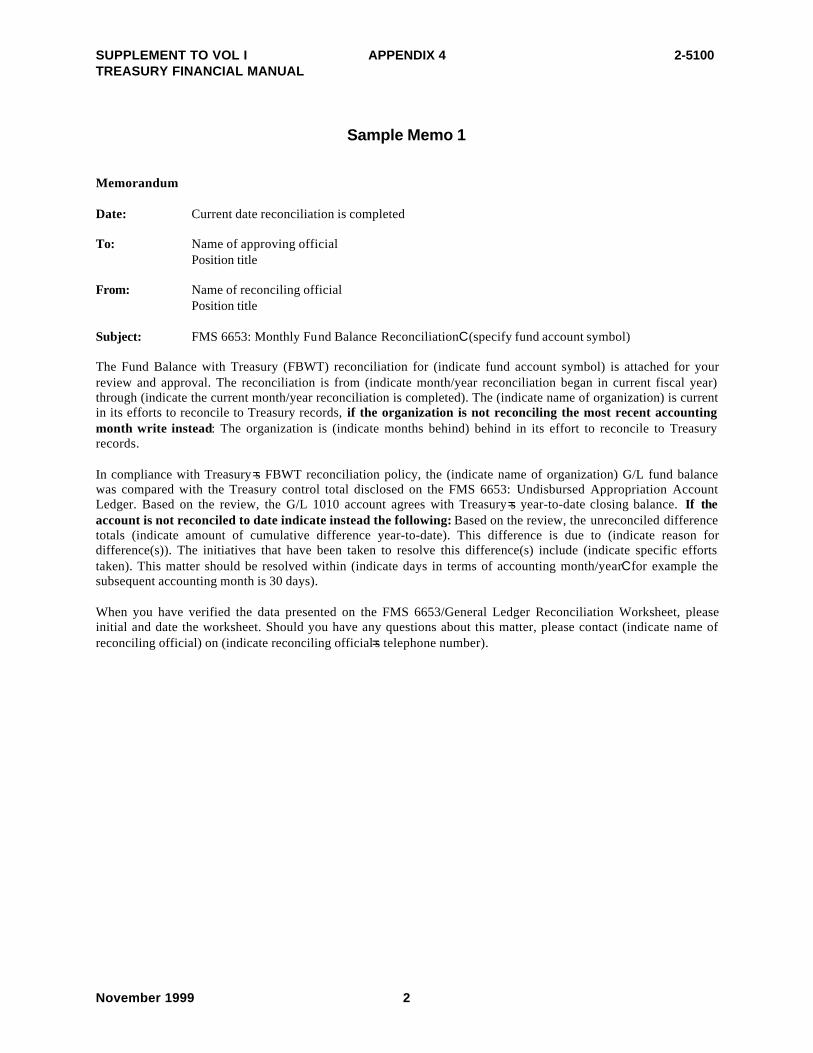

E1D-4 After completing the reconciliation for the month, give Worksheet 1A inAppendix 1 to an approving official for signature/review. It will also be helpfulto attach a memorandum that details the results of the current month=sreconciliation. Sample Memo 1 shown in Appendix 4 can be used for thispurpose. The memorandum is titled “FMS 6653: Monthly Fund BalanceReconciliation.”

C Worksheet1A

C Memo

SUPPLEMENT TO VOL I 2-5100TREASURY FINANCIAL MANUAL

November 1999 16

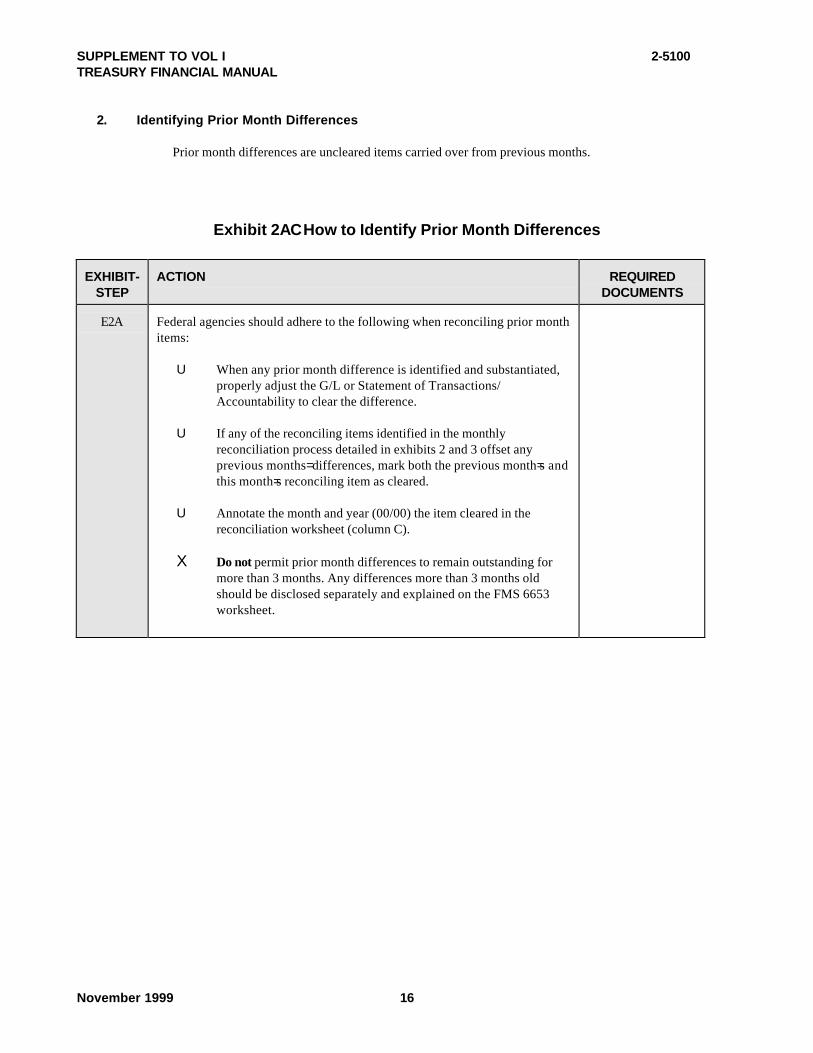

2. Identifying Prior Month Differences

Prior month differences are uncleared items carried over from previous months.

Exhibit 2ACHow to Identify Prior Month Differences

EXHIBIT-STEP

ACTION REQUIREDDOCUMENTS

E2A Federal agencies should adhere to the following when reconciling prior monthitems:

U When any prior month difference is identified and substantiated, properly adjust the G/L or Statement of Transactions/Accountability to clear the difference.

U If any of the reconciling items identified in the monthlyreconciliation process detailed in exhibits 2 and 3 offset anyprevious months= differences, mark both the previous month=s andthis month=s reconciling item as cleared.

U Annotate the month and year (00/00) the item cleared in thereconciliation worksheet (column C).

X Do not permit prior month differences to remain outstanding formore than 3 months. Any differences more than 3 months oldshould be disclosed separately and explained on the FMS 6653worksheet.

2-5100 SUPPLEMENT TO VOL ITREASURY FINANCIAL MANUAL

November 199917

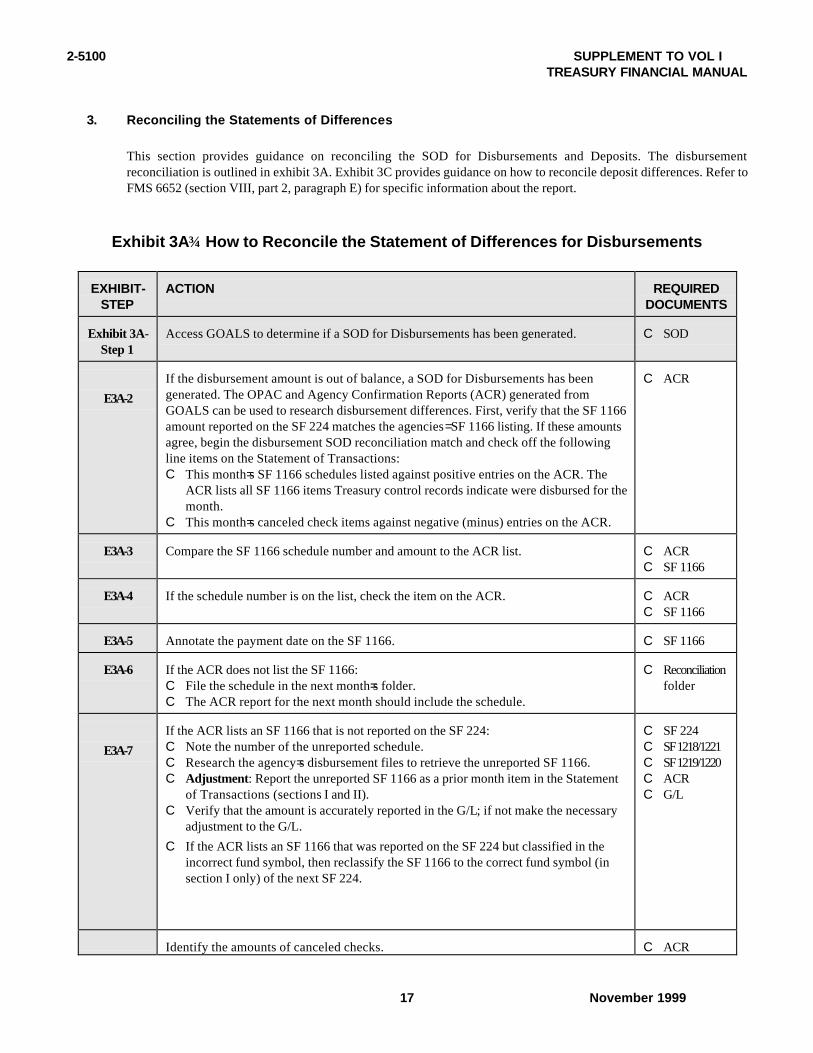

3. Reconciling the Statements of Differences

This section provides guidance on reconciling the SOD for Disbursements and Deposits. The disbursementreconciliation is outlined in exhibit 3A. Exhibit 3C provides guidance on how to reconcile deposit differences. Refer toFMS 6652 (section VIII, part 2, paragraph E) for specific information about the report.

Exhibit 3AHow to Reconcile the Statement of Differences for Disbursements

EXHIBIT-STEP

ACTION REQUIREDDOCUMENTS

Exhibit 3A-Step 1

Access GOALS to determine if a SOD for Disbursements has been generated. C SOD

E3A-2

If the disbursement amount is out of balance, a SOD for Disbursements has beengenerated. The OPAC and Agency Confirmation Reports (ACR) generated fromGOALS can be used to research disbursement differences. First, verify that the SF 1166amount reported on the SF 224 matches the agencies = SF 1166 listing. If these amountsagree, begin the disbursement SOD reconciliation match and check off the followingline items on the Statement of Transactions:C This month=s SF 1166 schedules listed against positive entries on the ACR. The

ACR lists all SF 1166 items Treasury control records indicate were disbursed for themonth.

C This month=s canceled check items against negative (minus) entries on the ACR.

C ACR

E3A-3 Compare the SF 1166 schedule number and amount to the ACR list. C ACRC SF 1166

E3A-4 If the schedule number is on the list, check the item on the ACR. C ACRC SF 1166

E3A-5 Annotate the payment date on the SF 1166. C SF 1166

E3A-6 If the ACR does not list the SF 1166:C File the schedule in the next month=s folder.C The ACR report for the next month should include the schedule.

C Reconciliationfolder

E3A-7

If the ACR lists an SF 1166 that is not reported on the SF 224:C Note the number of the unreported schedule.C Research the agency=s disbursement files to retrieve the unreported SF 1166.C Adjustment: Report the unreported SF 1166 as a prior month item in the Statement

of Transactions (sections I and II).C Verify that the amount is accurately reported in the G/L; if not make the necessary

adjustment to the G/L.

C If the ACR lists an SF 1166 that was reported on the SF 224 but classified in theincorrect fund symbol, then reclassify the SF 1166 to the correct fund symbol (insection I only) of the next SF 224.

C SF 224C SF 1218/1221C SF 1219/1220C ACRC G/L

Identify the amounts of canceled checks. C ACR

SUPPLEMENT TO VOL I 2-5100TREASURY FINANCIAL MANUAL

November 1999 18

EXHIBIT-STEP

ACTION REQUIREDDOCUMENTS

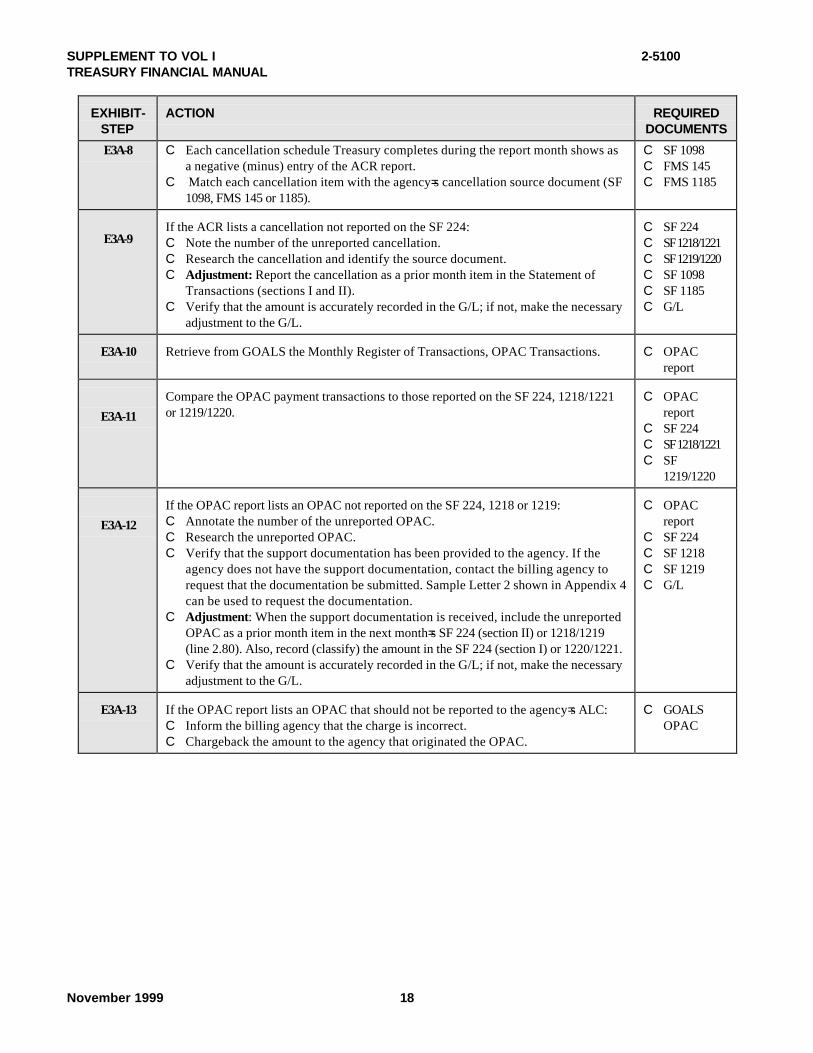

E3A-8 C Each cancellation schedule Treasury completes during the report month shows asa negative (minus) entry of the ACR report.

C Match each cancellation item with the agency=s cancellation source document (SF1098, FMS 145 or 1185).

C SF 1098C FMS 145C FMS 1185

E3A-9If the ACR lists a cancellation not reported on the SF 224:C Note the number of the unreported cancellation.C Research the cancellation and identify the source document.C Adjustment: Report the cancellation as a prior month item in the Statement of

Transactions (sections I and II).C Verify that the amount is accurately recorded in the G/L; if not, make the necessary

adjustment to the G/L.

C SF 224C SF 1218/1221C SF 1219/1220C SF 1098C SF 1185C G/L

E3A-10 Retrieve from GOALS the Monthly Register of Transactions, OPAC Transactions. C OPACreport

E3A-11

Compare the OPAC payment transactions to those reported on the SF 224, 1218/1221or 1219/1220.

C OPACreport

C SF 224C SF 1218/1221C SF

1219/1220

E3A-12

If the OPAC report lists an OPAC not reported on the SF 224, 1218 or 1219:C Annotate the number of the unreported OPAC.C Research the unreported OPAC.C Verify that the support documentation has been provided to the agency. If the

agency does not have the support documentation, contact the billing agency torequest that the documentation be submitted. Sample Letter 2 shown in Appendix 4can be used to request the documentation.

C Adjustment: When the support documentation is received, include the unreportedOPAC as a prior month item in the next month=s SF 224 (section II) or 1218/1219(line 2.80). Also, record (classify) the amount in the SF 224 (section I) or 1220/1221.

C Verify that the amount is accurately recorded in the G/L; if not, make the necessaryadjustment to the G/L.

C OPACreport

C SF 224C SF 1218C SF 1219C G/L

E3A-13 If the OPAC report lists an OPAC that should not be reported to the agency=s ALC:C Inform the billing agency that the charge is incorrect.C Chargeback the amount to the agency that originated the OPAC.

C GOALSOPAC

2-5100 SUPPLEMENT TO VOL ITREASURY FINANCIAL MANUAL

November 199919

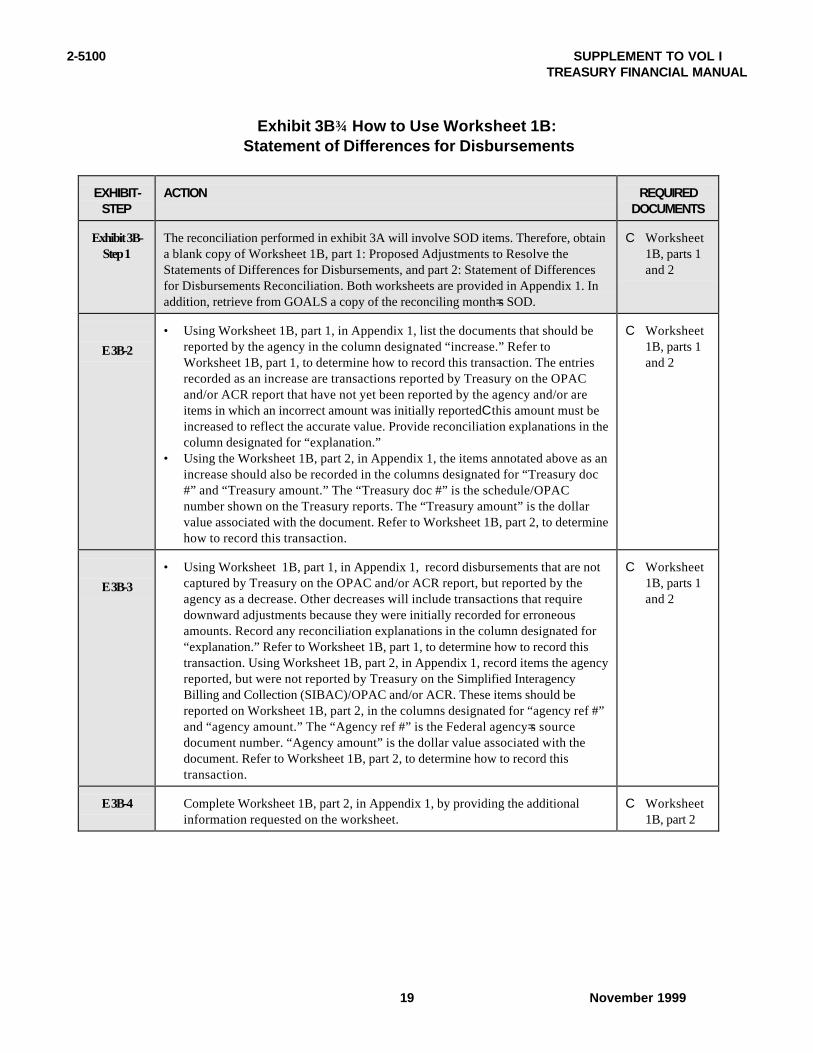

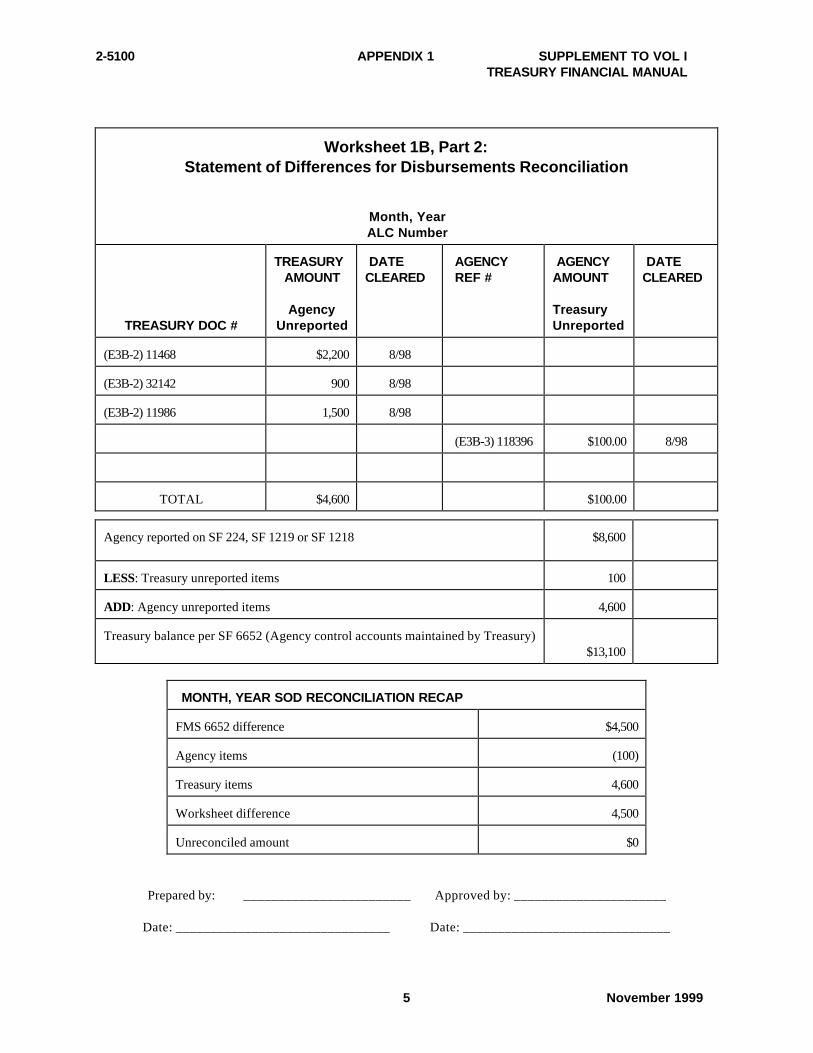

Exhibit 3BHow to Use Worksheet 1B: Statement of Differences for Disbursements

EXHIBIT-STEP

ACTION REQUIREDDOCUMENTS

Exhibit 3B-Step 1

The reconciliation performed in exhibit 3A will involve SOD items. Therefore, obtaina blank copy of Worksheet 1B, part 1: Proposed Adjustments to Resolve theStatements of Differences for Disbursements, and part 2: Statement of Differencesfor Disbursements Reconciliation. Both worksheets are provided in Appendix 1. Inaddition, retrieve from GOALS a copy of the reconciling month=s SOD.

C Worksheet1B, parts 1and 2

E 3B-2

• Using Worksheet 1B, part 1, in Appendix 1, list the documents that should bereported by the agency in the column designated “increase.” Refer toWorksheet 1B, part 1, to determine how to record this transaction. The entriesrecorded as an increase are transactions reported by Treasury on the OPACand/or ACR report that have not yet been reported by the agency and/or areitems in which an incorrect amount was initially reportedCthis amount must beincreased to reflect the accurate value. Provide reconciliation explanations in thecolumn designated for “explanation.”

• Using the Worksheet 1B, part 2, in Appendix 1, the items annotated above as anincrease should also be recorded in the columns designated for “Treasury doc#” and “Treasury amount.” The “Treasury doc #” is the schedule/OPACnumber shown on the Treasury reports. The “Treasury amount” is the dollarvalue associated with the document. Refer to Worksheet 1B, part 2, to determinehow to record this transaction.

C Worksheet1B, parts 1and 2

E 3B-3

• Using Worksheet 1B, part 1, in Appendix 1, record disbursements that are notcaptured by Treasury on the OPAC and/or ACR report, but reported by theagency as a decrease. Other decreases will include transactions that requiredownward adjustments because they were initially recorded for erroneousamounts. Record any reconciliation explanations in the column designated for“explanation.” Refer to Worksheet 1B, part 1, to determine how to record thistransaction. Using Worksheet 1B, part 2, in Appendix 1, record items the agencyreported, but were not reported by Treasury on the Simplified InteragencyBilling and Collection (SIBAC)/OPAC and/or ACR. These items should bereported on Worksheet 1B, part 2, in the columns designated for “agency ref #”and “agency amount.” The “Agency ref #” is the Federal agency=s sourcedocument number. “Agency amount” is the dollar value associated with thedocument. Refer to Worksheet 1B, part 2, to determine how to record thistransaction.

C Worksheet1B, parts 1and 2

E 3B-4 Complete Worksheet 1B, part 2, in Appendix 1, by providing the additionalinformation requested on the worksheet.

C Worksheet1B, part 2

SUPPLEMENT TO VOL I 2-5100TREASURY FINANCIAL MANUAL

November 1999 20

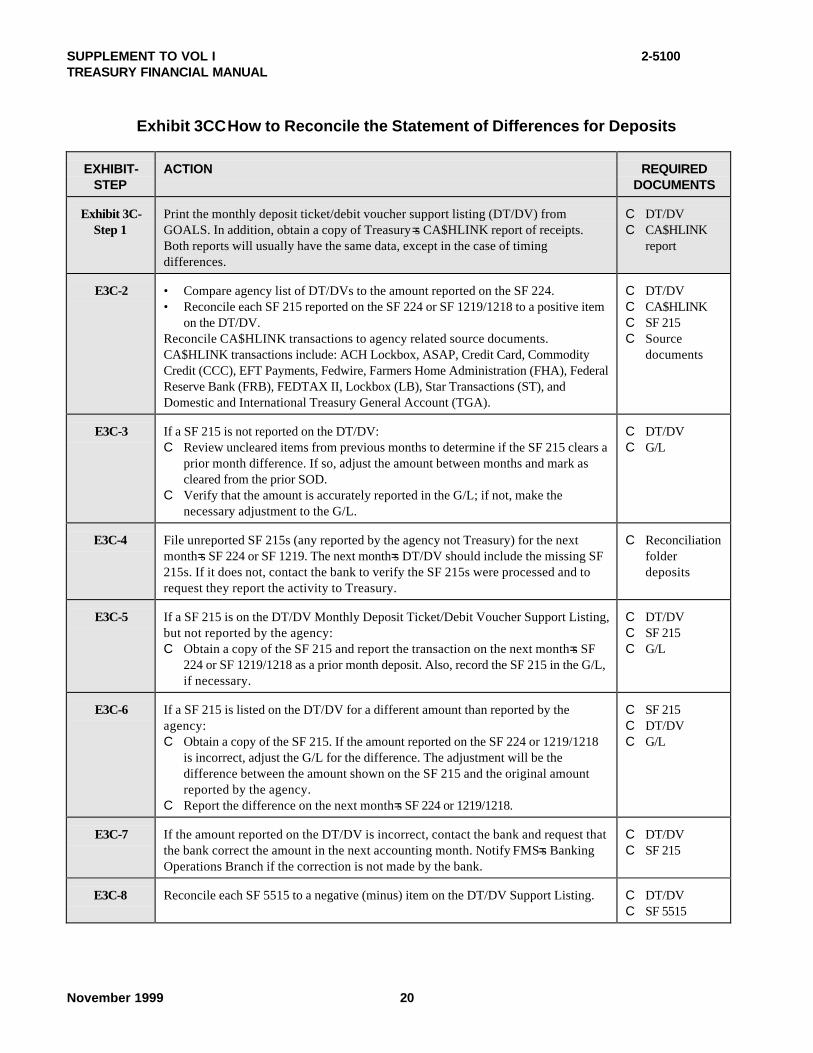

Exhibit 3CCHow to Reconcile the Statement of Differences for Deposits

EXHIBIT-STEP

ACTION REQUIREDDOCUMENTS

Exhibit 3C-Step 1

Print the monthly deposit ticket/debit voucher support listing (DT/DV) fromGOALS. In addition, obtain a copy of Treasury =s CA$HLINK report of receipts.Both reports will usually have the same data, except in the case of timingdifferences.

C DT/DVC CA$HLINK

report

E3C-2 • Compare agency list of DT/DVs to the amount reported on the SF 224.• Reconcile each SF 215 reported on the SF 224 or SF 1219/1218 to a positive item

on the DT/DV.Reconcile CA$HLINK transactions to agency related source documents.CA$HLINK transactions include: ACH Lockbox, ASAP, Credit Card, CommodityCredit (CCC), EFT Payments, Fedwire, Farmers Home Administration (FHA), FederalReserve Bank (FRB), FEDTAX II, Lockbox (LB), Star Transactions (ST), andDomestic and International Treasury General Account (TGA).

C DT/DVC CA$HLINKC SF 215C Source

documents

E3C-3 If a SF 215 is not reported on the DT/DV:C Review uncleared items from previous months to determine if the SF 215 clears a

prior month difference. If so, adjust the amount between months and mark ascleared from the prior SOD.

C Verify that the amount is accurately reported in the G/L; if not, make thenecessary adjustment to the G/L.

C DT/DVC G/L

E3C-4 File unreported SF 215s (any reported by the agency not Treasury) for the nextmonth=s SF 224 or SF 1219. The next month=s DT/DV should include the missing SF215s. If it does not, contact the bank to verify the SF 215s were processed and torequest they report the activity to Treasury.

C Reconciliationfolderdeposits

E3C-5 If a SF 215 is on the DT/DV Monthly Deposit Ticket/Debit Voucher Support Listing,but not reported by the agency:C Obtain a copy of the SF 215 and report the transaction on the next month=s SF

224 or SF 1219/1218 as a prior month deposit. Also, record the SF 215 in the G/L,if necessary.

C DT/DVC SF 215C G/L

E3C-6 If a SF 215 is listed on the DT/DV for a different amount than reported by theagency:C Obtain a copy of the SF 215. If the amount reported on the SF 224 or 1219/1218

is incorrect, adjust the G/L for the difference. The adjustment will be thedifference between the amount shown on the SF 215 and the original amountreported by the agency.

C Report the difference on the next month=s SF 224 or 1219/1218.

C SF 215C DT/DVC G/L

E3C-7 If the amount reported on the DT/DV is incorrect, contact the bank and request thatthe bank correct the amount in the next accounting month. Notify FMS=s BankingOperations Branch if the correction is not made by the bank.

C DT/DVC SF 215

E3C-8 Reconcile each SF 5515 to a negative (minus) item on the DT/DV Support Listing. C DT/DVC SF 5515

2-5100 SUPPLEMENT TO VOL ITREASURY FINANCIAL MANUAL

November 199921

EXHIBIT-STEP

ACTION REQUIREDDOCUMENTS

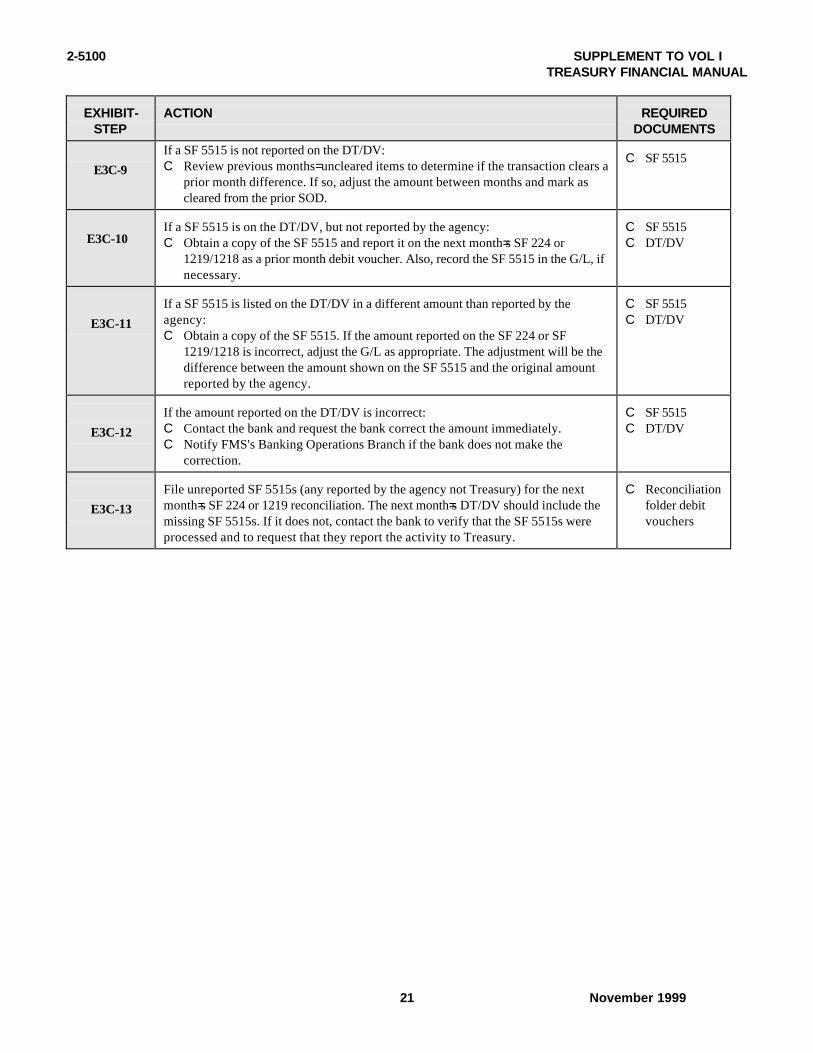

E3C-9

If a SF 5515 is not reported on the DT/DV:C Review previous months= uncleared items to determine if the transaction clears a

prior month difference. If so, adjust the amount between months and mark ascleared from the prior SOD.

C SF 5515

E3C-10If a SF 5515 is on the DT/DV, but not reported by the agency:C Obtain a copy of the SF 5515 and report it on the next month=s SF 224 or

1219/1218 as a prior month debit voucher. Also, record the SF 5515 in the G/L, ifnecessary.

C SF 5515C DT/DV

E3C-11

If a SF 5515 is listed on the DT/DV in a different amount than reported by theagency:C Obtain a copy of the SF 5515. If the amount reported on the SF 224 or SF

1219/1218 is incorrect, adjust the G/L as appropriate. The adjustment will be thedifference between the amount shown on the SF 5515 and the original amountreported by the agency.

C SF 5515C DT/DV

E3C-12

If the amount reported on the DT/DV is incorrect:C Contact the bank and request the bank correct the amount immediately.C Notify FMS's Banking Operations Branch if the bank does not make the

correction.

C SF 5515C DT/DV

E3C-13

File unreported SF 5515s (any reported by the agency not Treasury) for the nextmonth=s SF 224 or 1219 reconciliation. The next month=s DT/DV should include themissing SF 5515s. If it does not, contact the bank to verify that the SF 5515s wereprocessed and to request that they report the activity to Treasury.

C Reconciliationfolder debitvouchers

SUPPLEMENT TO VOL I 2-5100TREASURY FINANCIAL MANUAL

November 1999 22

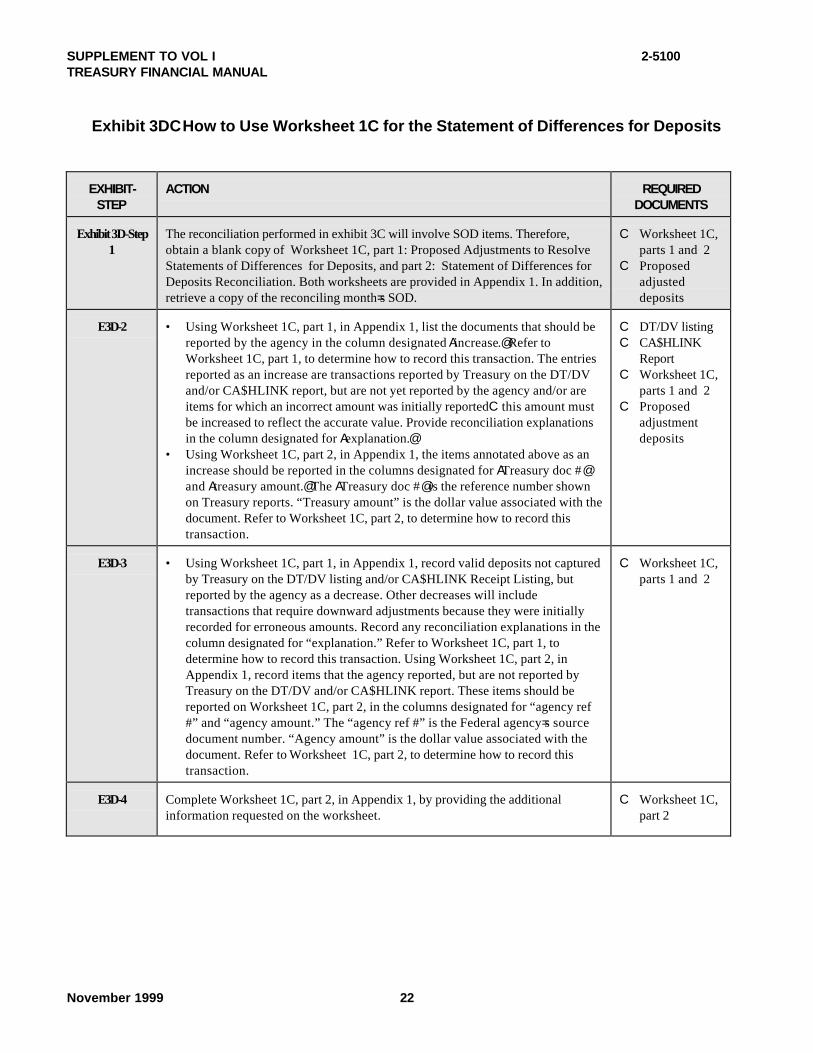

Exhibit 3DCHow to Use Worksheet 1C for the Statement of Differences for Deposits

EXHIBIT-STEP

ACTION REQUIREDDOCUMENTS

Exhibit 3D-Step1

The reconciliation performed in exhibit 3C will involve SOD items. Therefore,obtain a blank copy of Worksheet 1C, part 1: Proposed Adjustments to ResolveStatements of Differences for Deposits, and part 2: Statement of Differences forDeposits Reconciliation. Both worksheets are provided in Appendix 1. In addition,retrieve a copy of the reconciling month=s SOD.

C Worksheet 1C,parts 1 and 2

C Proposedadjusteddeposits

E3D-2 • Using Worksheet 1C, part 1, in Appendix 1, list the documents that should bereported by the agency in the column designated Aincrease.@ Refer toWorksheet 1C, part 1, to determine how to record this transaction. The entriesreported as an increase are transactions reported by Treasury on the DT/DVand/or CA$HLINK report, but are not yet reported by the agency and/or areitems for which an incorrect amount was initially reportedC this amount mustbe increased to reflect the accurate value. Provide reconciliation explanationsin the column designated for Aexplanation.@

• Using Worksheet 1C, part 2, in Appendix 1, the items annotated above as anincrease should be reported in the columns designated for ATreasury doc #@and Atreasury amount.@ The ATreasury doc #@ is the reference number shownon Treasury reports. “Treasury amount” is the dollar value associated with thedocument. Refer to Worksheet 1C, part 2, to determine how to record thistransaction.

C DT/DV listingC CA$HLINK

ReportC Worksheet 1C,

parts 1 and 2C Proposed

adjustmentdeposits

E3D-3 • Using Worksheet 1C, part 1, in Appendix 1, record valid deposits not capturedby Treasury on the DT/DV listing and/or CA$HLINK Receipt Listing, butreported by the agency as a decrease. Other decreases will includetransactions that require downward adjustments because they were initiallyrecorded for erroneous amounts. Record any reconciliation explanations in thecolumn designated for “explanation.” Refer to Worksheet 1C, part 1, todetermine how to record this transaction. Using Worksheet 1C, part 2, inAppendix 1, record items that the agency reported, but are not reported byTreasury on the DT/DV and/or CA$HLINK report. These items should bereported on Worksheet 1C, part 2, in the columns designated for “agency ref#” and “agency amount.” The “agency ref #” is the Federal agency=s sourcedocument number. “Agency amount” is the dollar value associated with thedocument. Refer to Worksheet 1C, part 2, to determine how to record thistransaction.

C Worksheet 1C,parts 1 and 2

E3D-4 Complete Worksheet 1C, part 2, in Appendix 1, by providing the additionalinformation requested on the worksheet.

C Worksheet 1C,part 2

2-5100 SUPPLEMENT TO VOL ITREASURY FINANCIAL MANUAL

November 199923

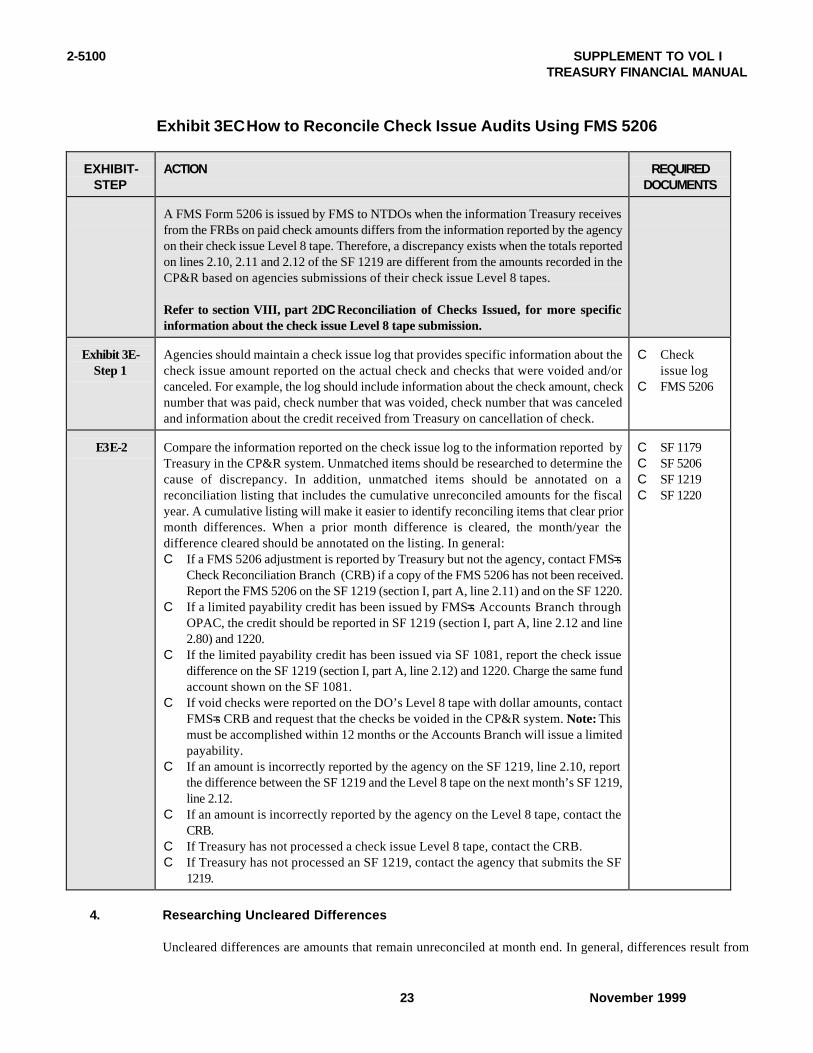

Exhibit 3ECHow to Reconcile Check Issue Audits Using FMS 5206

EXHIBIT-STEP

ACTION REQUIREDDOCUMENTS

A FMS Form 5206 is issued by FMS to NTDOs when the information Treasury receivesfrom the FRBs on paid check amounts differs from the information reported by the agencyon their check issue Level 8 tape. Therefore, a discrepancy exists when the totals reportedon lines 2.10, 2.11 and 2.12 of the SF 1219 are different from the amounts recorded in theCP&R based on agencies submissions of their check issue Level 8 tapes.

Refer to section VIII, part 2DCReconciliation of Checks Issued, for more specificinformation about the check issue Level 8 tape submission.

Exhibit 3E-Step 1

Agencies should maintain a check issue log that provides specific information about thecheck issue amount reported on the actual check and checks that were voided and/orcanceled. For example, the log should include information about the check amount, checknumber that was paid, check number that was voided, check number that was canceledand information about the credit received from Treasury on cancellation of check.

C Checkissue log

C FMS 5206

E3E-2 Compare the information reported on the check issue log to the information reported byTreasury in the CP&R system. Unmatched items should be researched to determine thecause of discrepancy. In addition, unmatched items should be annotated on areconciliation listing that includes the cumulative unreconciled amounts for the fiscalyear. A cumulative listing will make it easier to identify reconciling items that clear priormonth differences. When a prior month difference is cleared, the month/year thedifference cleared should be annotated on the listing. In general:C If a FMS 5206 adjustment is reported by Treasury but not the agency, contact FMS=s

Check Reconciliation Branch (CRB) if a copy of the FMS 5206 has not been received.Report the FMS 5206 on the SF 1219 (section I, part A, line 2.11) and on the SF 1220.

C If a limited payability credit has been issued by FMS=s Accounts Branch throughOPAC, the credit should be reported in SF 1219 (section I, part A, line 2.12 and line2.80) and 1220.

C If the limited payability credit has been issued via SF 1081, report the check issuedifference on the SF 1219 (section I, part A, line 2.12) and 1220. Charge the same fundaccount shown on the SF 1081.

C If void checks were reported on the DO’s Level 8 tape with dollar amounts, contactFMS=s CRB and request that the checks be voided in the CP&R system. Note: Thismust be accomplished within 12 months or the Accounts Branch will issue a limitedpayability.

C If an amount is incorrectly reported by the agency on the SF 1219, line 2.10, reportthe difference between the SF 1219 and the Level 8 tape on the next month’s SF 1219,line 2.12.

C If an amount is incorrectly reported by the agency on the Level 8 tape, contact theCRB.

C If Treasury has not processed a check issue Level 8 tape, contact the CRB.C If Treasury has not processed an SF 1219, contact the agency that submits the SF

1219.

C SF 1179C SF 5206C SF 1219C SF 1220

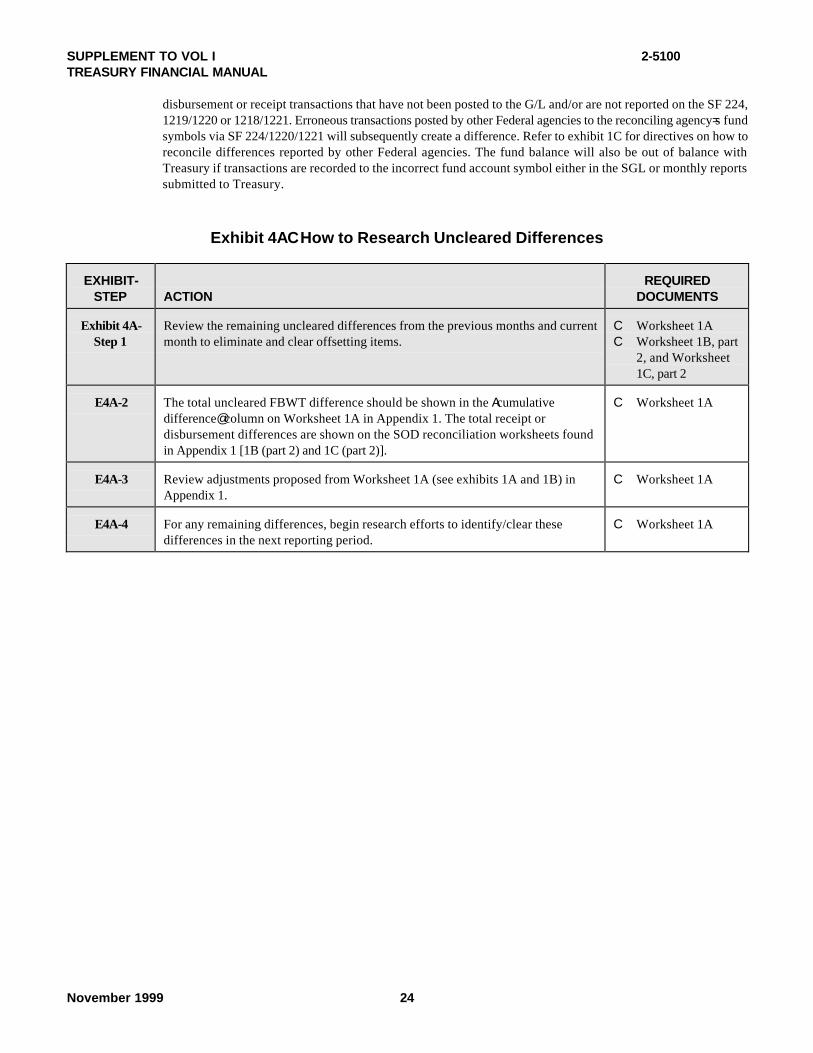

4. Researching Uncleared Differences

Uncleared differences are amounts that remain unreconciled at month end. In general, differences result from

SUPPLEMENT TO VOL I 2-5100TREASURY FINANCIAL MANUAL

November 1999 24

disbursement or receipt transactions that have not been posted to the G/L and/or are not reported on the SF 224,1219/1220 or 1218/1221. Erroneous transactions posted by other Federal agencies to the reconciling agency=s fundsymbols via SF 224/1220/1221 will subsequently create a difference. Refer to exhibit 1C for directives on how toreconcile differences reported by other Federal agencies. The fund balance will also be out of balance withTreasury if transactions are recorded to the incorrect fund account symbol either in the SGL or monthly reportssubmitted to Treasury.

Exhibit 4ACHow to Research Uncleared Differences

EXHIBIT-STEP ACTION

REQUIREDDOCUMENTS

Exhibit 4A-Step 1

Review the remaining uncleared differences from the previous months and currentmonth to eliminate and clear offsetting items.

C Worksheet 1AC Worksheet 1B, part

2, and Worksheet1C, part 2

E4A-2 The total uncleared FBWT difference should be shown in the Acumulativedifference@ column on Worksheet 1A in Appendix 1. The total receipt ordisbursement differences are shown on the SOD reconciliation worksheets foundin Appendix 1 [1B (part 2) and 1C (part 2)].

C Worksheet 1A

E4A-3 Review adjustments proposed from Worksheet 1A (see exhibits 1A and 1B) inAppendix 1.

C Worksheet 1A

E4A-4 For any remaining differences, begin research efforts to identify/clear thesedifferences in the next reporting period.

C Worksheet 1A

2-5100 SUPPLEMENT TO VOL ITREASURY FINANCIAL MANUAL

November 199925

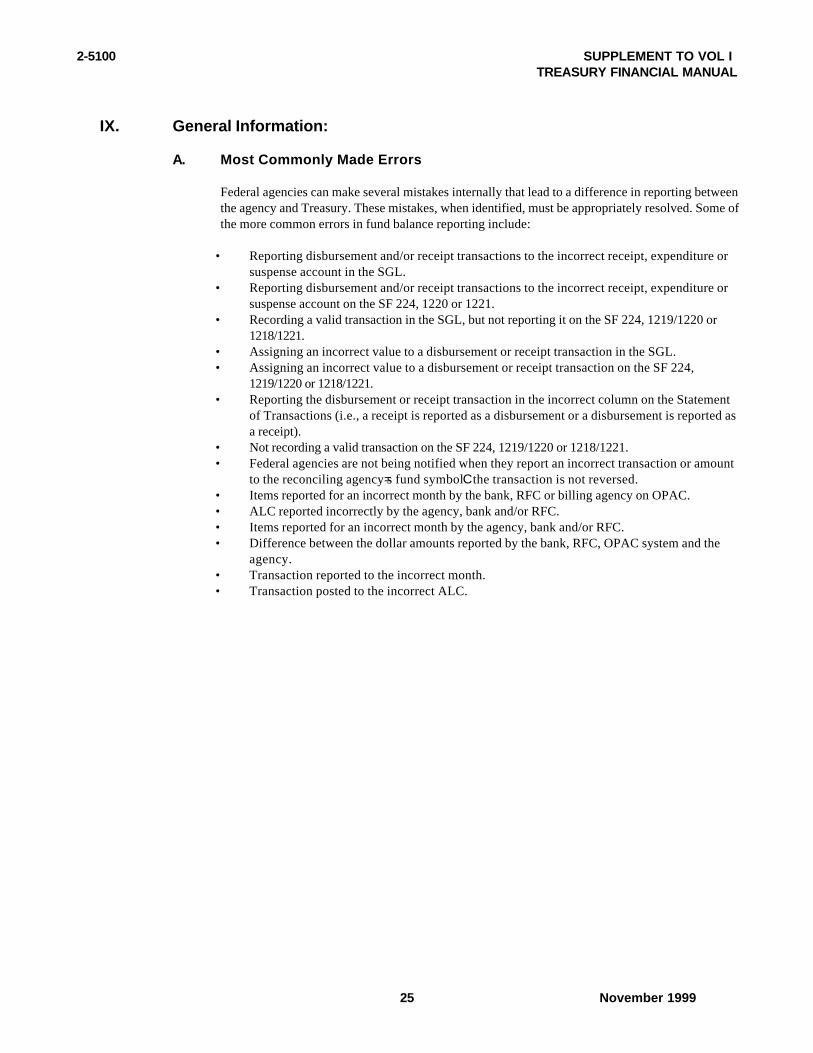

IX. General Information:

A. Most Commonly Made Errors

Federal agencies can make several mistakes internally that lead to a difference in reporting betweenthe agency and Treasury. These mistakes, when identified, must be appropriately resolved. Some ofthe more common errors in fund balance reporting include:

• Reporting disbursement and/or receipt transactions to the incorrect receipt, expenditure orsuspense account in the SGL.

• Reporting disbursement and/or receipt transactions to the incorrect receipt, expenditure orsuspense account on the SF 224, 1220 or 1221.

• Recording a valid transaction in the SGL, but not reporting it on the SF 224, 1219/1220 or1218/1221.

• Assigning an incorrect value to a disbursement or receipt transaction in the SGL.• Assigning an incorrect value to a disbursement or receipt transaction on the SF 224,

1219/1220 or 1218/1221.• Reporting the disbursement or receipt transaction in the incorrect column on the Statement

of Transactions (i.e., a receipt is reported as a disbursement or a disbursement is reported asa receipt).

• Not recording a valid transaction on the SF 224, 1219/1220 or 1218/1221.• Federal agencies are not being notified when they report an incorrect transaction or amount

to the reconciling agency=s fund symbolCthe transaction is not reversed.• Items reported for an incorrect month by the bank, RFC or billing agency on OPAC.• ALC reported incorrectly by the agency, bank and/or RFC.• Items reported for an incorrect month by the agency, bank and/or RFC.• Difference between the dollar amounts reported by the bank, RFC, OPAC system and the

agency.• Transaction reported to the incorrect month.• Transaction posted to the incorrect ALC.

SUPPLEMENT TO VOL I 2-5100TREASURY FINANCIAL MANUAL

November 1999 26

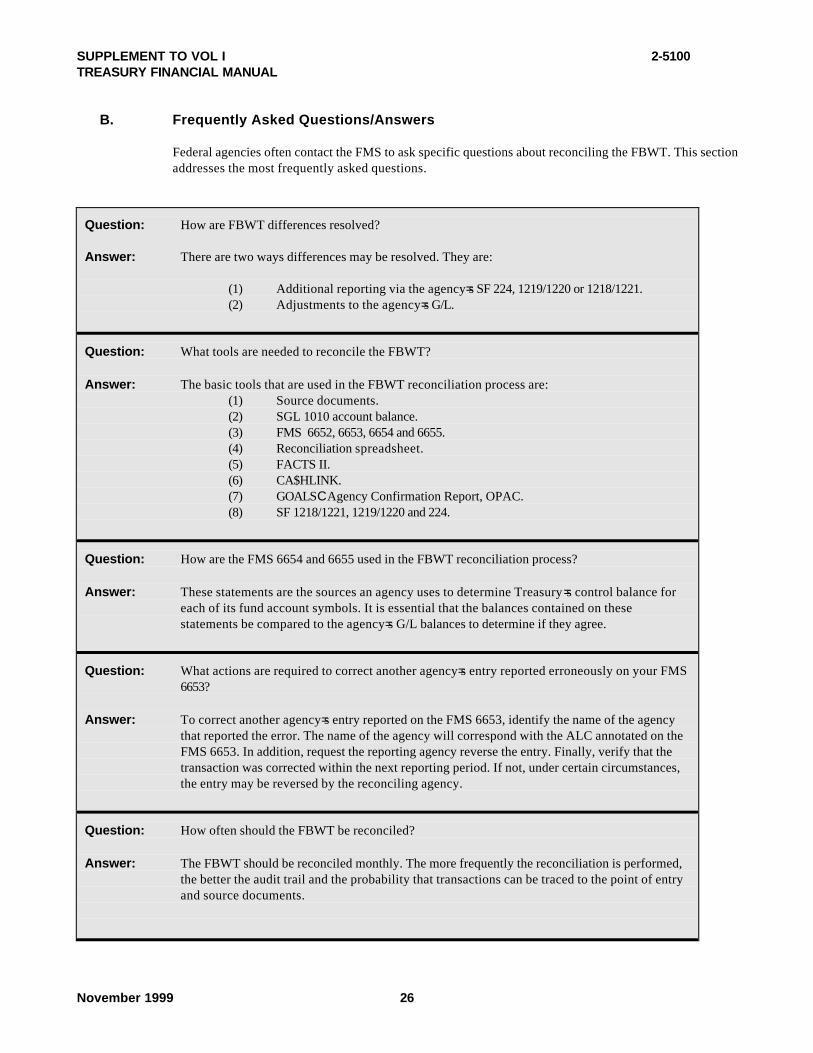

B. Frequently Asked Questions/Answers

Federal agencies often contact the FMS to ask specific questions about reconciling the FBWT. This sectionaddresses the most frequently asked questions.

Question: How are FBWT differences resolved?

Answer: There are two ways differences may be resolved. They are:

(1) Additional reporting via the agency=s SF 224, 1219/1220 or 1218/1221.(2) Adjustments to the agency=s G/L.

Question: What tools are needed to reconcile the FBWT?

Answer: The basic tools that are used in the FBWT reconciliation process are:(1) Source documents.(2) SGL 1010 account balance.(3) FMS 6652, 6653, 6654 and 6655.(4) Reconciliation spreadsheet.(5) FACTS II.(6) CA$HLINK.(7) GOALSCAgency Confirmation Report, OPAC.(8) SF 1218/1221, 1219/1220 and 224.

Question: How are the FMS 6654 and 6655 used in the FBWT reconciliation process?

Answer: These statements are the sources an agency uses to determine Treasury =s control balance foreach of its fund account symbols. It is essential that the balances contained on thesestatements be compared to the agency=s G/L balances to determine if they agree.

Question: What actions are required to correct another agency=s entry reported erroneously on your FMS6653?

Answer: To correct another agency=s entry reported on the FMS 6653, identify the name of the agencythat reported the error. The name of the agency will correspond with the ALC annotated on theFMS 6653. In addition, request the reporting agency reverse the entry. Finally, verify that thetransaction was corrected within the next reporting period. If not, under certain circumstances,the entry may be reversed by the reconciling agency.

Question: How often should the FBWT be reconciled?

Answer: The FBWT should be reconciled monthly. The more frequently the reconciliation is performed,the better the audit trail and the probability that transactions can be traced to the point of entryand source documents.

2-5100 SUPPLEMENT TO VOL ITREASURY FINANCIAL MANUAL

November 199927

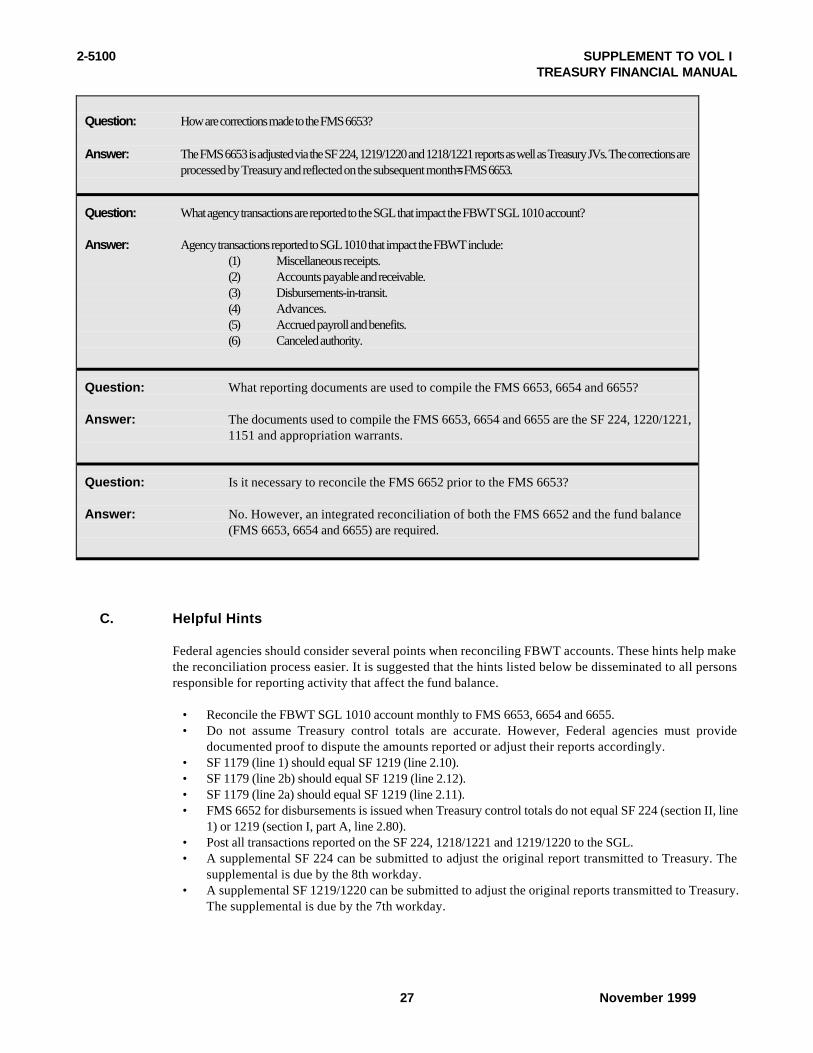

Question: How are corrections made to the FMS 6653?

Answer: The FMS 6653 is adjusted via the SF 224, 1219/1220 and 1218/1221 reports as well as Treasury JVs. The corrections areprocessed by Treasury and reflected on the subsequent month=s FMS 6653.

Question: What agency transactions are reported to the SGL that impact the FBWT SGL 1010 account?

Answer: Agency transactions reported to SGL 1010 that impact the FBWT include:(1) Miscellaneous receipts.(2) Accounts payable and receivable.(3) Disbursements-in-transit.(4) Advances.(5) Accrued payroll and benefits.(6) Canceled authority.

Question: What reporting documents are used to compile the FMS 6653, 6654 and 6655?

Answer: The documents used to compile the FMS 6653, 6654 and 6655 are the SF 224, 1220/1221,1151 and appropriation warrants.

Question: Is it necessary to reconcile the FMS 6652 prior to the FMS 6653?

Answer: No. However, an integrated reconciliation of both the FMS 6652 and the fund balance(FMS 6653, 6654 and 6655) are required.

C. Helpful Hints

Federal agencies should consider several points when reconciling FBWT accounts. These hints help makethe reconciliation process easier. It is suggested that the hints listed below be disseminated to all personsresponsible for reporting activity that affect the fund balance.

• Reconcile the FBWT SGL 1010 account monthly to FMS 6653, 6654 and 6655.• Do not assume Treasury control totals are accurate. However, Federal agencies must provide

documented proof to dispute the amounts reported or adjust their reports accordingly.• SF 1179 (line 1) should equal SF 1219 (line 2.10).• SF 1179 (line 2b) should equal SF 1219 (line 2.12).• SF 1179 (line 2a) should equal SF 1219 (line 2.11).• FMS 6652 for disbursements is issued when Treasury control totals do not equal SF 224 (section II, line

1) or 1219 (section I, part A, line 2.80).• Post all transactions reported on the SF 224, 1218/1221 and 1219/1220 to the SGL.• A supplemental SF 224 can be submitted to adjust the original report transmitted to Treasury. The

supplemental is due by the 8th workday.• A supplemental SF 1219/1220 can be submitted to adjust the original reports transmitted to Treasury.

The supplemental is due by the 7th workday.

SUPPLEMENT TO VOL I 2-5100TREASURY FINANCIAL MANUAL

November 1999 28

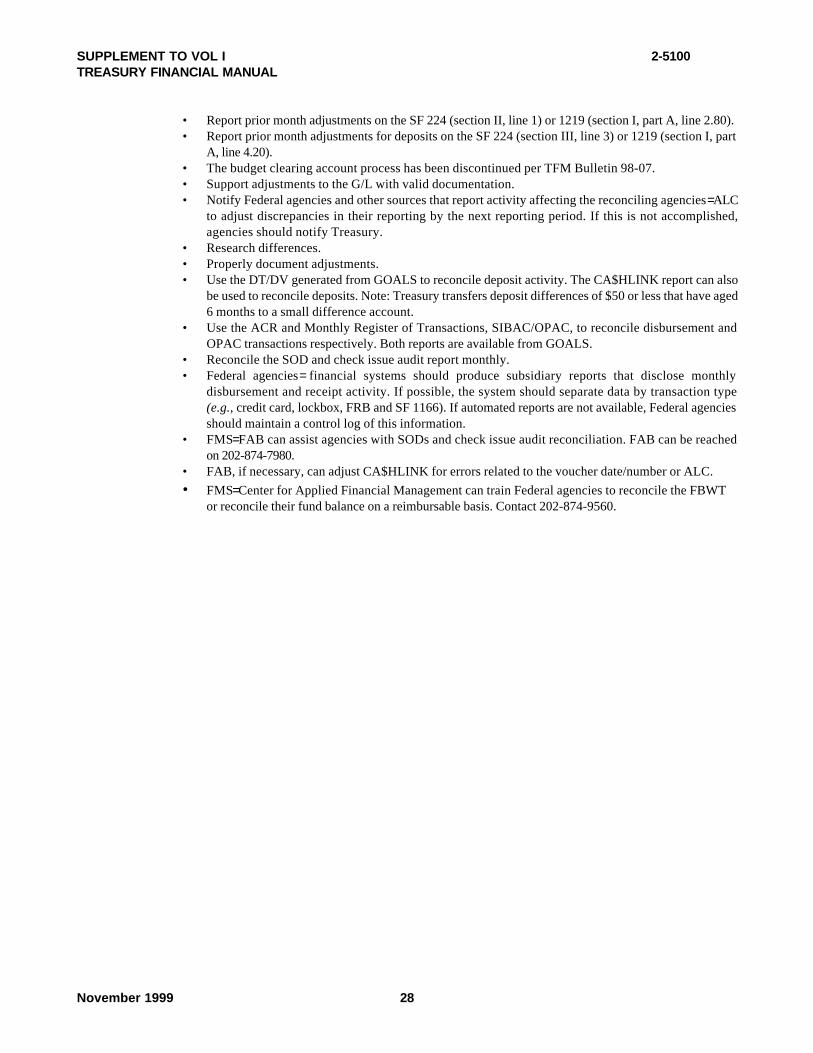

• Report prior month adjustments on the SF 224 (section II, line 1) or 1219 (section I, part A, line 2.80).• Report prior month adjustments for deposits on the SF 224 (section III, line 3) or 1219 (section I, part

A, line 4.20).• The budget clearing account process has been discontinued per TFM Bulletin 98-07.• Support adjustments to the G/L with valid documentation.• Notify Federal agencies and other sources that report activity affecting the reconciling agencies = ALC

to adjust discrepancies in their reporting by the next reporting period. If this is not accomplished,agencies should notify Treasury.

• Research differences.• Properly document adjustments.• Use the DT/DV generated from GOALS to reconcile deposit activity. The CA$HLINK report can also

be used to reconcile deposits. Note: Treasury transfers deposit differences of $50 or less that have aged6 months to a small difference account.

• Use the ACR and Monthly Register of Transactions, SIBAC/OPAC, to reconcile disbursement andOPAC transactions respectively. Both reports are available from GOALS.

• Reconcile the SOD and check issue audit report monthly.• Federal agencies = financial systems should produce subsidiary reports that disclose monthly

disbursement and receipt activity. If possible, the system should separate data by transaction type(e.g., credit card, lockbox, FRB and SF 1166). If automated reports are not available, Federal agenciesshould maintain a control log of this information.

• FMS= FAB can assist agencies with SODs and check issue audit reconciliation. FAB can be reachedon 202-874-7980.

• FAB, if necessary, can adjust CA$HLINK for errors related to the voucher date/number or ALC.• FMS= Center for Applied Financial Management can train Federal agencies to reconcile the FBWT