Embed Size (px)

Citation preview

1

Full Year 2013 Financial Results

23 January 2014

2

Scope of Briefing

Address by Chief Executive Officer

Group Financial Highlights

Business Review & Outlook

3

Address by

Chief Executive Officer

4

Clarity of Focus

Staying on multi-business strategy

Building on strong foundations:

Commitment to quality execution

Raising productivity & efficiencies

Investing in people & technology innovation

Ensuring financial discipline

Maintaining a strong balance sheet

5

Gradual Global Recovery

Broad-based recovery in the US

Patchy recovery in Europe

China expected to grow at a modest pace

6

Performance Highlights

FY 2013 net profit was S$1.4b

ROE was 14.9%

FY 2013 EVA was S$939m

Total distribution of 49.5 cts per share

The financials exclude revaluation, major impairment and divestments.

7

Offshore & Marine

FY2013

Delivered a record number of

22 rigs worldwide

Reinforced Near Market,

Near Customer strategy with

presence in Mexico

Total new orders won:

About S$7b

Net orderbook at 31 Dec:

S$14.2b, with visibility into 2019

Keppel FELS, Singapore

8

Offshore & Marine

Focusing on execution &

delivery

Keppel FELS completed 21 out

of the 22 rigs delivered in 2013

Fortifying integrated regional

network

Growing technology expertise

Expanding current suite of

30 proprietary solutions

Developing innovative solutions

for new frontiers

Leading solution - Keppel’s proven

KFELS B Class jackup rig

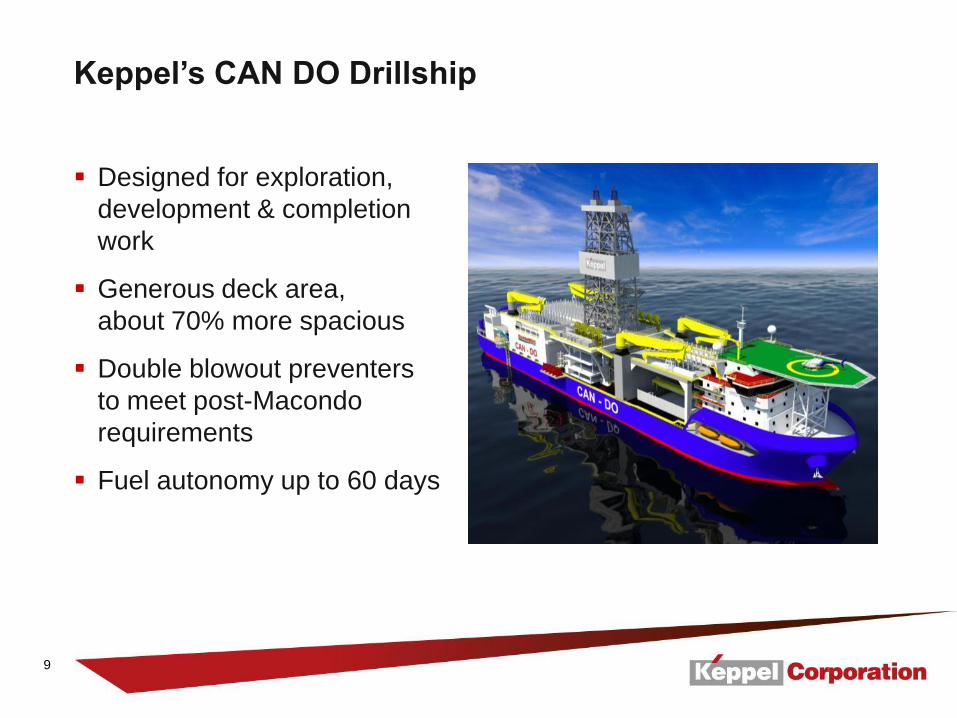

9

Designed for exploration,

development & completion

work

Generous deck area,

about 70% more spacious

Double blowout preventers

to meet post-Macondo

requirements

Fuel autonomy up to 60 days

Keppel’s CAN DO Drillship

10

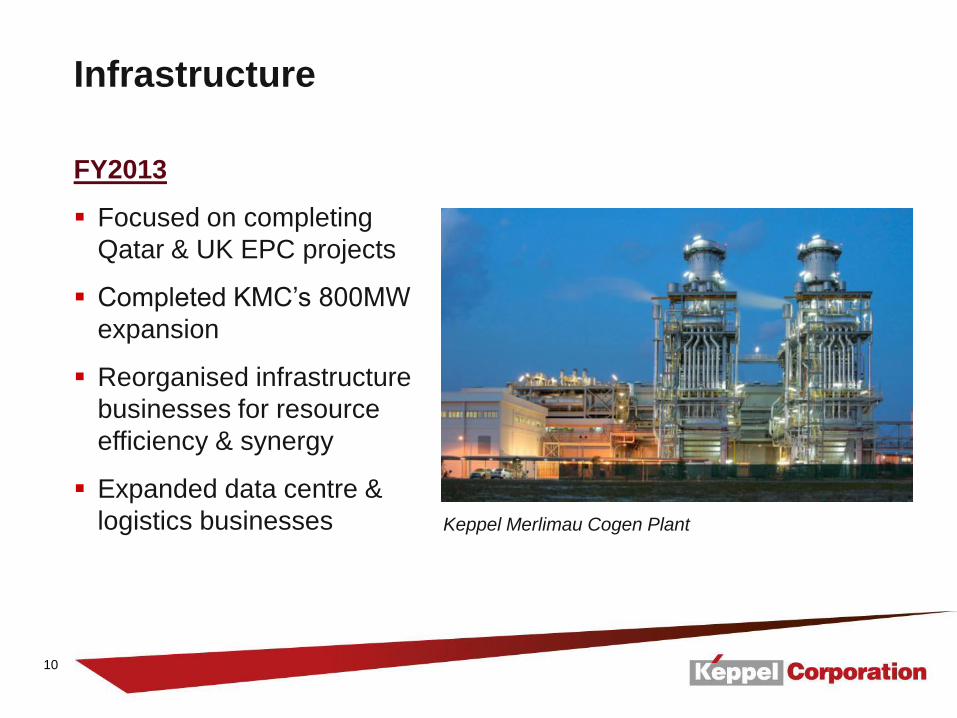

Infrastructure

FY2013

Focused on completing

Qatar & UK EPC projects

Completed KMC’s 800MW

expansion

Reorganised infrastructure

businesses for resource

efficiency & synergy

Expanded data centre &

logistics businesses

Keppel Merlimau Cogen Plant

11

Infrastructure

Scaling up the

data centre business

Expanding portfolio

in Singapore,

Ireland & the

Netherlands

Exploring a

data centre REIT

Citadel 100 data centre, Ireland

12

Infrastructure

Expanding logistics network in China

Acquired an integrated port logistics facility in Sanshui, Foshan

Logistics hubs in Anhui, Jilin and Tianjin to be operational in 2015

Sino-Singapore Jilin Food Zone

International Logistics Park

Tianjin Eco-City Integrated Distribution Hub

Sanshui Port, Foshan

Wuhu Sanshan Port, Wuhu

Keppel Wanjiang International Coldchain

Logistics Park, Anhui

Lanshi Port, Foshan

Under construction:

Operational:

Nanhai Distribution Centre, Foshan

13

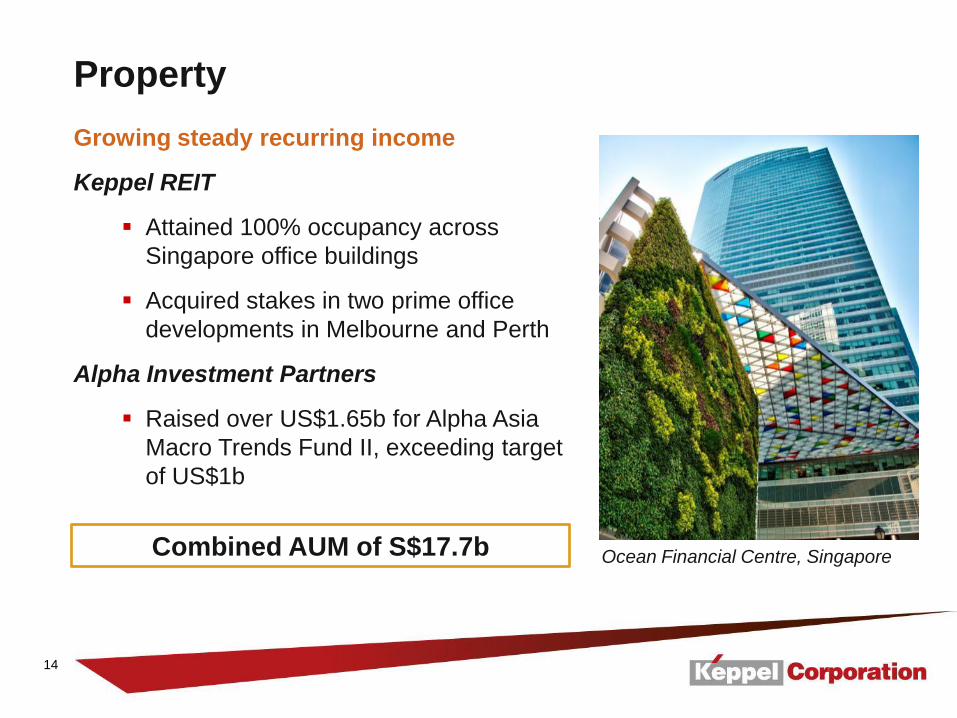

Property

FY2013

Trading properties:

Over 4,400 homes sold

across Asia

3 residential sites acquired in

Singapore & China

Commercial portfolio:

Total GFA of about 650,000 sq m

(under development & recently

acquired in the region)

Unlocked value for re-investment

Park Avenue Heights, Chengdu

14

Property

Combined AUM of S$17.7b

Growing steady recurring income

Keppel REIT

Attained 100% occupancy across

Singapore office buildings

Acquired stakes in two prime office

developments in Melbourne and Perth

Alpha Investment Partners

Raised over US$1.65b for Alpha Asia

Macro Trends Fund II, exceeding target

of US$1b

Ocean Financial Centre, Singapore

15

Configured for growth and

value creation through

innovation and discipline.

16

Group Financial

Highlights

17

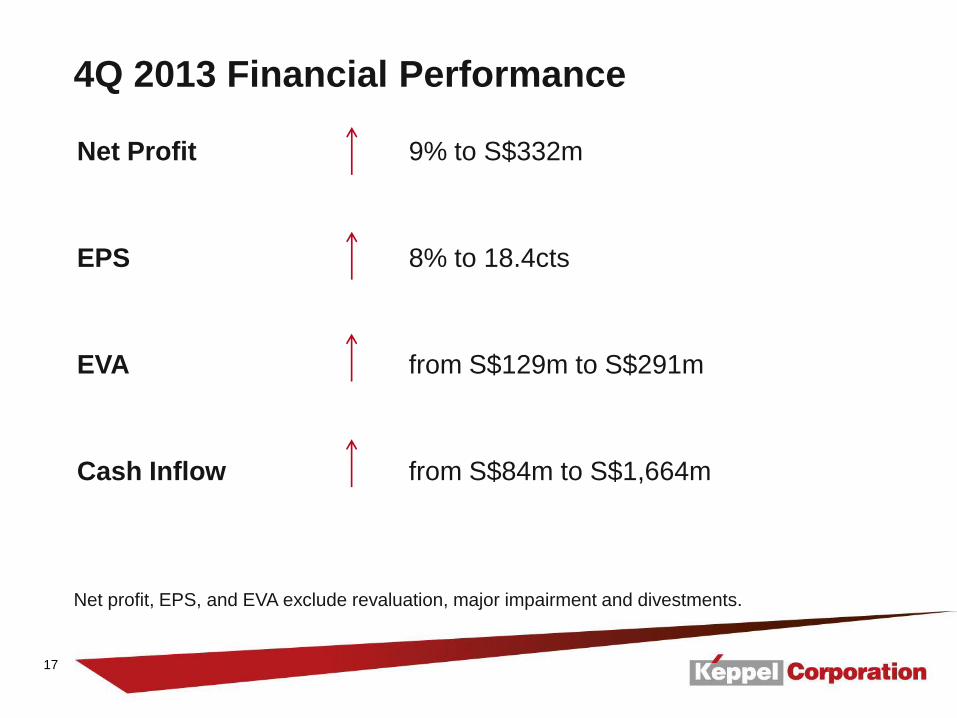

4Q 2013 Financial Performance

Net profit, EPS, and EVA exclude revaluation, major impairment and divestments.

Net Profit 9% to S$332m

EPS 8% to 18.4cts

EVA from S$129m to S$291m

Cash Inflow from S$84m to S$1,664m

18

4Q 2013 Financial Highlights

S$m

4Q 2013

4Q 2012

% Change

Revenue 3,598 2,999 20

EBITDA 538 482 12

Operating Profit 474 425 12

Profit Before Tax 566 539 5

Net Profit 332 305 9

EPS (cents) 18.4 17.0 8

The financials exclude revaluation, major impairment and divestments.

19

4Q 2013 Revenue by Segments

S$m

4Q 2013

%

4Q 2012

%

% Change

Offshore & Marine 2,071 58 1,712 57 21

Infrastructure 975 27 715 24 36

Property 538 15 559 19 (4)

Investments 14 - 13 - 8

Total 3,598 100 2,999 100 20

20

4Q 2013 Pre-tax Profit by Segments

The financials exclude revaluation, major impairment and divestments.

S$m

4Q 2013

%

4Q 2012

%

% Change

Offshore & Marine 333 59 241 45 38

Infrastructure (99) (18) (61) (12) 62

Property 311 55 327 61 (5)

Investments 21 4 32 6 (34)

Total 566 100 539 100 5

21

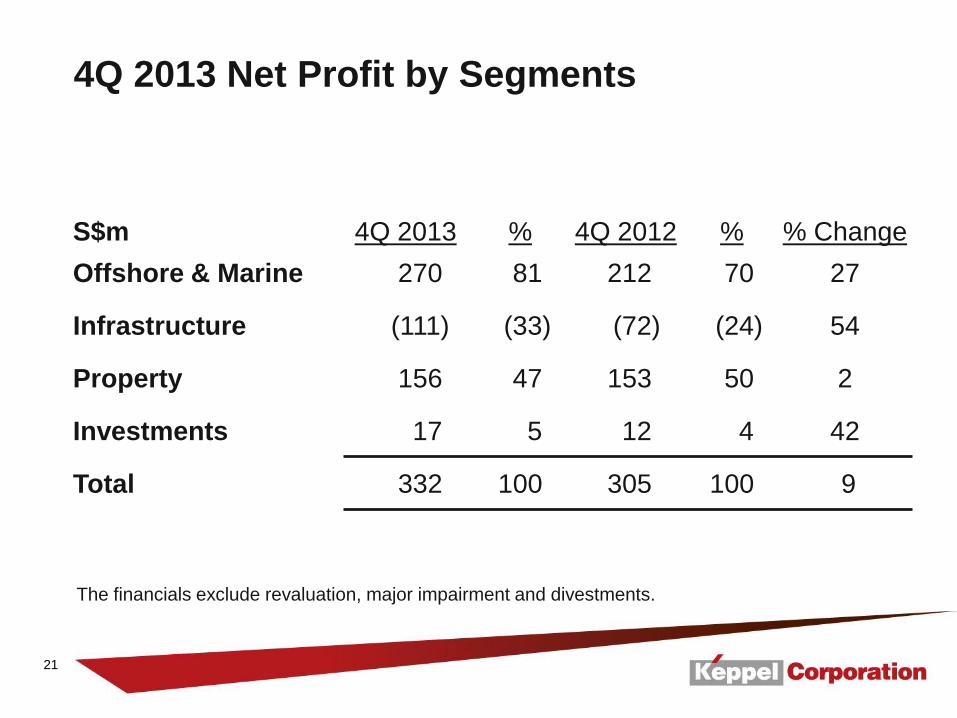

4Q 2013 Net Profit by Segments

The financials exclude revaluation, major impairment and divestments.

S$m

4Q 2013

%

4Q 2012

%

% Change

Offshore & Marine 270 81 212 70 27

Infrastructure (111) (33) (72) (24) 54

Property 156 47 153 50 2

Investments 17 5 12 4 42

Total 332 100 305 100 9

22

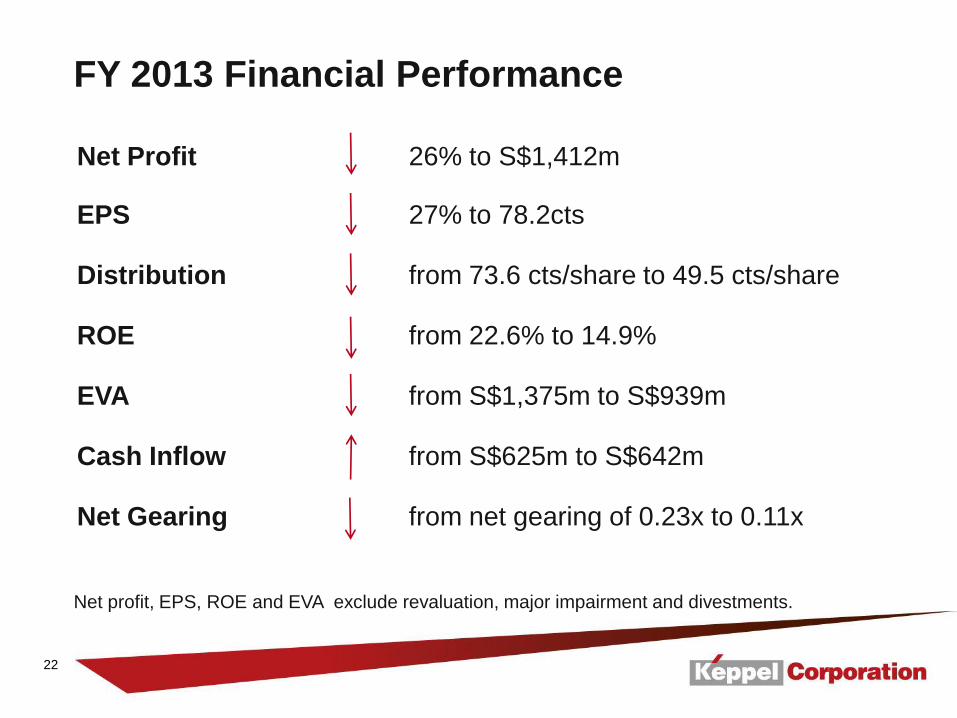

FY 2013 Financial Performance

Net profit, EPS, ROE and EVA exclude revaluation, major impairment and divestments.

Net Profit 26% to S$1,412m

EPS 27% to 78.2cts

Distribution from 73.6 cts/share to 49.5 cts/share

ROE from 22.6% to 14.9%

EVA from S$1,375m to S$939m

Cash Inflow from S$625m to S$642m

Net Gearing from net gearing of 0.23x to 0.11x

23

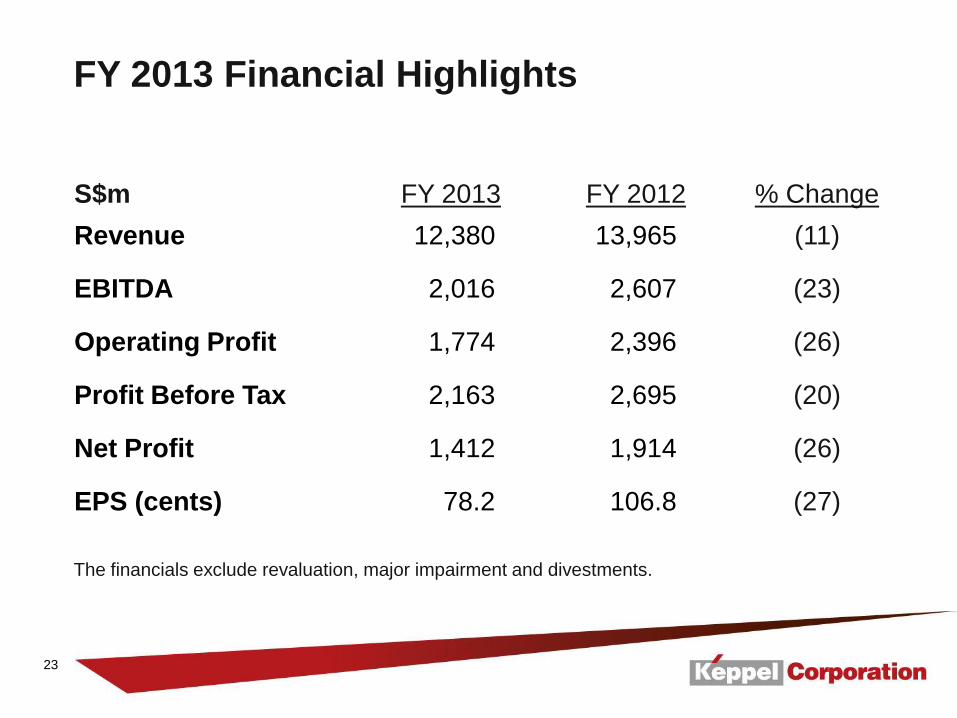

FY 2013 Financial Highlights

S$m

FY 2013

FY 2012

% Change

Revenue 12,380 13,965 (11)

EBITDA 2,016 2,607 (23)

Operating Profit 1,774 2,396 (26)

Profit Before Tax 2,163 2,695 (20)

Net Profit 1,412 1,914 (26)

EPS (cents) 78.2 106.8 (27)

The financials exclude revaluation, major impairment and divestments.

24

FY 2013 Revenue by Segments

S$m

FY 2013

%

FY 2012

%

% Change

Offshore & Marine 7,126 58 7,963 57 (11)

Infrastructure 3,459 28 2,832 20 22

Property 1,768 14 3,018 22 (41)

Investments 27 - 152 1 (82)

Total 12,380 100 13,965 100 (11)

25

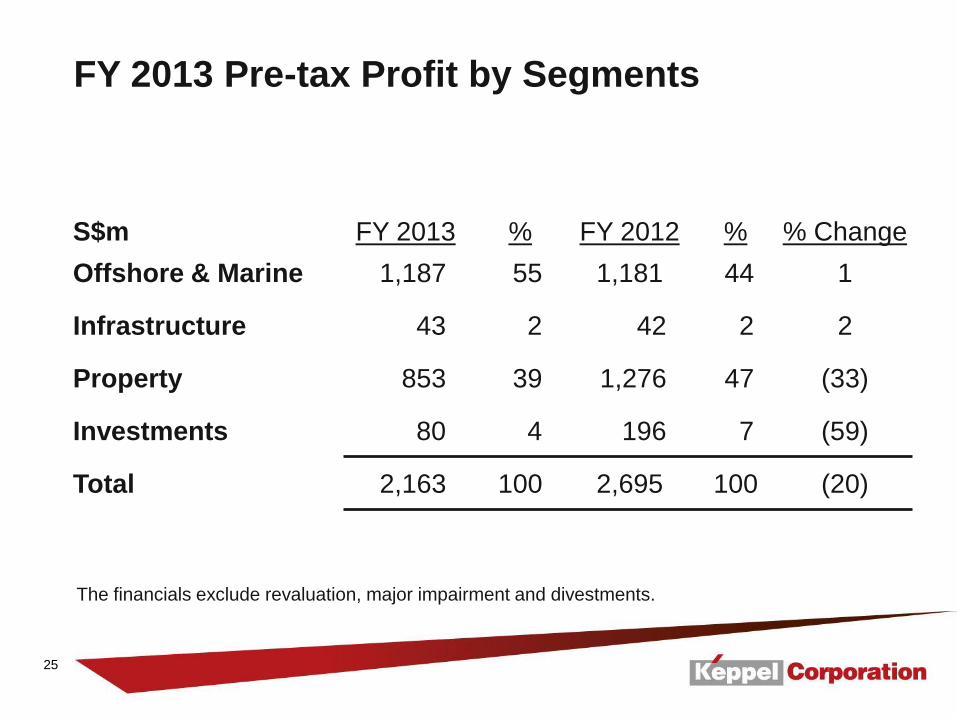

FY 2013 Pre-tax Profit by Segments

The financials exclude revaluation, major impairment and divestments.

S$m

FY 2013

%

FY 2012

%

% Change

Offshore & Marine 1,187 55 1,181 44 1

Infrastructure 43 2 42 2 2

Property 853 39 1,276 47 (33)

Investments 80 4 196 7 (59)

Total 2,163 100 2,695 100 (20)

26

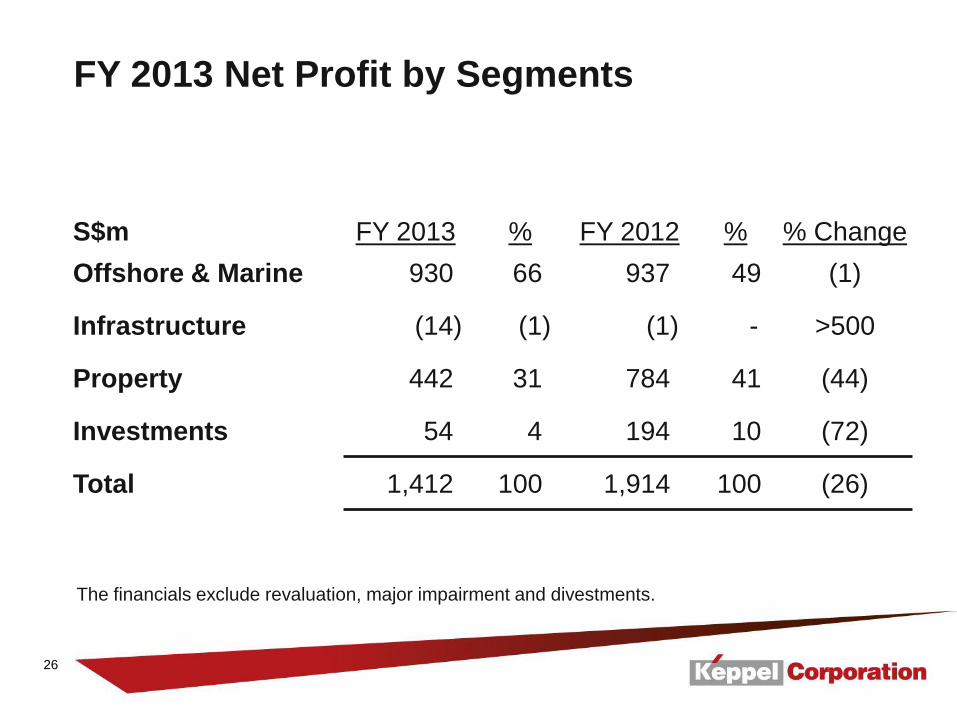

FY 2013 Net Profit by Segments

The financials exclude revaluation, major impairment and divestments.

S$m

FY 2013

%

FY 2012

%

% Change

Offshore & Marine 930 66 937 49 (1)

Infrastructure (14) (1) (1) - >500

Property 442 31 784 41 (44)

Investments 54 4 194 10 (72)

Total 1,412 100 1,914 100 (26)

27

14.5 15.5 17.0 17.6

41.9

18.4

16.6 17.4 20.0 21.6

29.1

19.1

15.6 16.9 17.3

22.8

18.8

22.3

15.0 18.1

20.0

21.8

17.0

18.4

EPS (Cents)

Net Profit & EPS (Excluding Revaluation, Major Impairment and Divestments)

61.7

67.9

74.3

83.8

106.8

253 272 298 312

751

331

291 304 352 384

521

346

272 296 305

406

337

403 263

318 352

389

305

332

Net Profit (S$m)

1Q:

1,079 1,190

1,307

1,491

1,914 4Q:

3Q:

2Q:

1Q:

4Q:

3Q:

2Q:

1Q:

1Q:

2Q:

1,412

2Q:

78.2

3Q: 3Q:

4Q: 4Q:

28

253 272 298 312

751

357

291

726

352 384

521

347

272

296

305 406

346

457 266

246

636

844

619

685

Net Profit (S$m)

Net Profit & EPS (Including Revaluation, Major Impairment and Divestments)

14.5 15.5 17.0 17.6

41.9

19.8

16.6

41.5

20.0 21.6

29.1

19.2

15.6

16.9

17.3 22.8

19.3

25.3 15.2

14.0

36.1

47.4

34.5

38.0

EPS (Cents)

3Q:

4Q:

61.9

87.9 90.4

109.4

124.8

1,082

1,540 1,591

1,946

2,237

4Q:

3Q:

2Q:

1Q:

1Q:

4Q:

3Q:

2Q:

1Q:

1Q:

2Q: 2Q:

1,846 102.3

3Q:

4Q:

29

21.8% 22.5% 20.8% 20.8%

22.6%

14.9%

2008 2009 2010 2011 2012 2013

ROE & Dividend

12.7 13.6 14.5 17.0 18.0

10.0

31.8

34.6 38.2

43.0 45.0 40.0

Interim Dividend Full-Year Dividend ROE

Plus

Dividend in specie ~20.9cts/share

Plus

Dividend in specie ~28.6cts/share

ROE excludes revaluation, major impairment and divestments.

Dividend in specie ~9.5cts/share

Plus

30

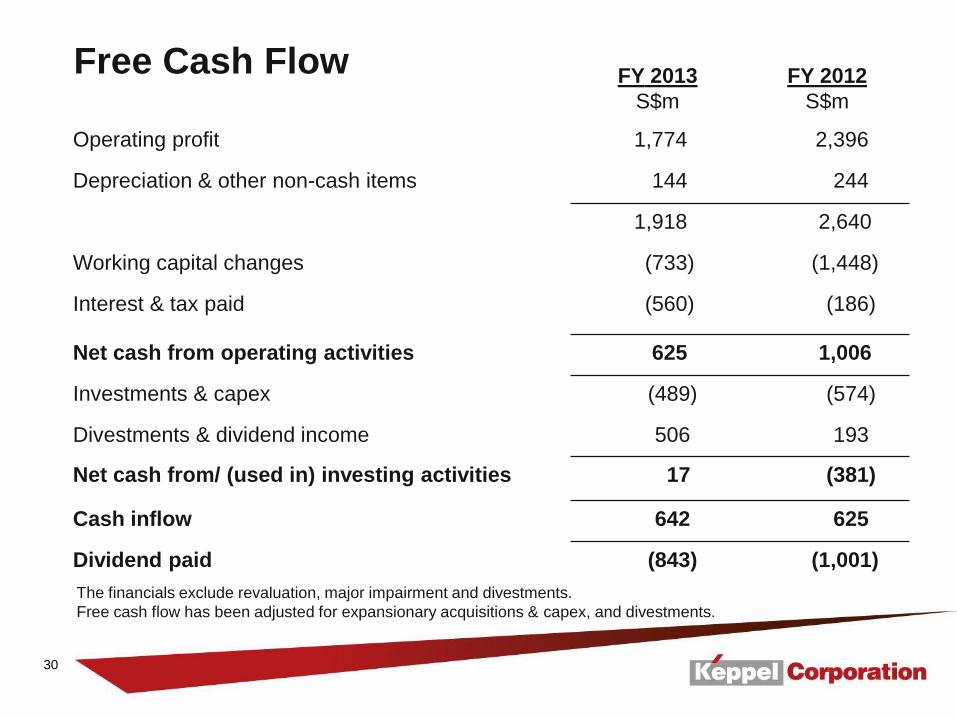

FY 2013

S$m

FY 2012

S$m

Operating profit 1,774 2,396

Depreciation & other non-cash items 144 244

1,918 2,640

Working capital changes (733) (1,448)

Interest & tax paid (560) (186)

Net cash from operating activities 625 1,006

Investments & capex (489) (574)

Divestments & dividend income 506 193

Net cash from/ (used in) investing activities 17 (381)

Cash inflow 642 625

Dividend paid (843) (1,001)

The financials exclude revaluation, major impairment and divestments.

Free cash flow has been adjusted for expansionary acquisitions & capex, and divestments.

Free Cash Flow

31

Business Review &

Outlook

32

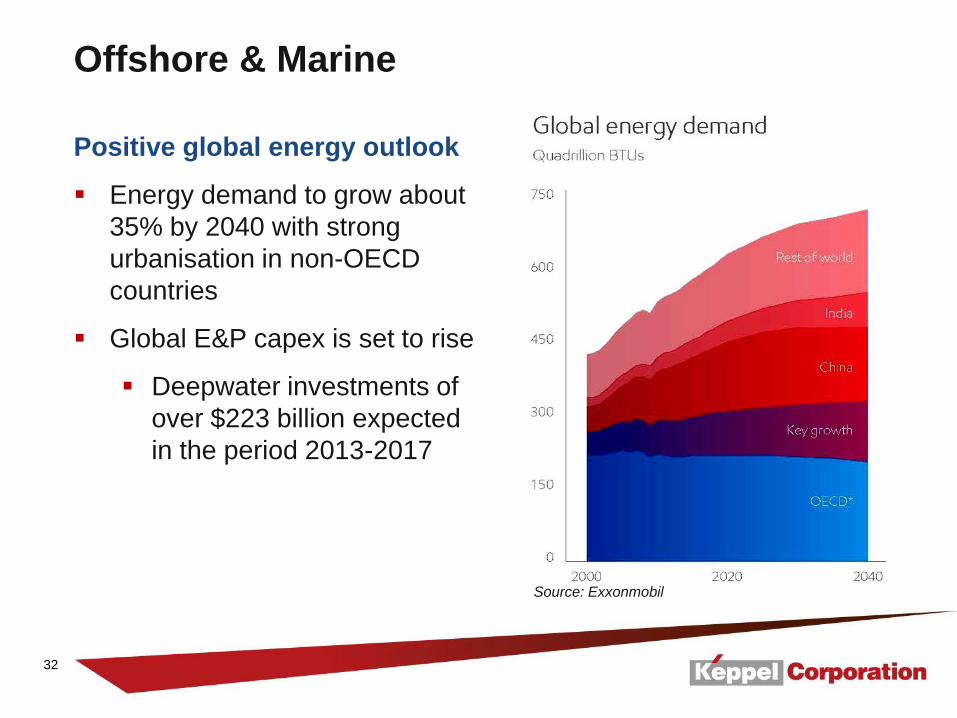

Offshore & Marine

Source: Exxonmobil

Positive global energy outlook

Energy demand to grow about

35% by 2040 with strong

urbanisation in non-OECD

countries

Global E&P capex is set to rise

Deepwater investments of

over $223 billion expected

in the period 2013-2017

33

Offshore & Marine

4Q

2013

Secured S$2.1b of new orders including 7 jackups

and 3 FPSOs conversion/upgrades

Completed 4 jackups, 1 accommodation semi,

2 semi upgrades and 3 specialised vessels

Signed MOU with PEMEX to develop a yard in Mexico

Keppel Shipyard, Singapore

34

Infrastructure

4Q

2013

Runcorn EPC project to be substantially completed in 2014;

Doha North ready for final commissioning before targeted

handover in end-2014

Keppel Seghers wins WTE technology package contract in

Yangzhou, China, from repeat customer

Yangzhou WTE Plant, China

35

Property

4Q

2013

Sold over 900 homes in Asia

Improved office occupancy: MBFC Tower 3 is 95% full

Acquired a 10.4-ha residential site in Tianjin Eco-City

Corals at Keppel Bay, Singapore

36

Q&A FY 2013 Results

37

Additional Information The financials exclude revaluation, major impairment and divestments.

38

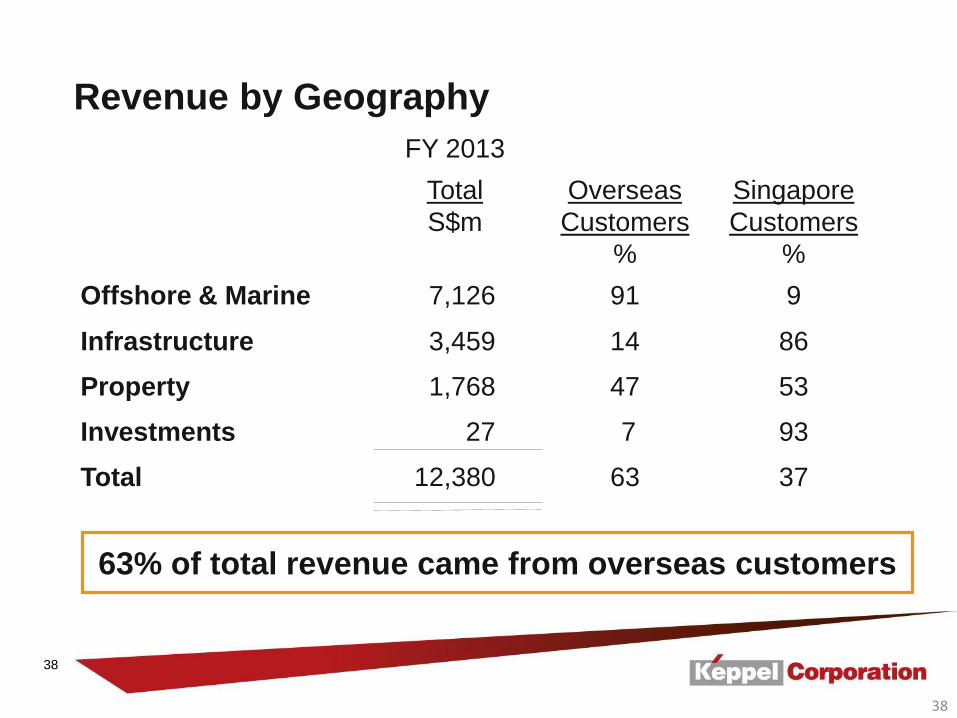

38

FY 2013

Total

S$m

Overseas

Customers

%

Singapore

Customers

%

Offshore & Marine 7,126 91 9

Infrastructure 3,459 14 86

Property 1,768 47 53

Investments 27 7 93

Total 12,380 63 37

Revenue by Geography

63% of total revenue came from overseas customers

39

39

S$m

FY 2013

%

FY 2012

%

% Change

Offshore & Marine 1,181 59 1,211 47 (3)

Infrastructure 120 6 84 3 43

Property 690 34 1,178 45 (41)

Investments 25 1 134 5 (81)

Total 2,016 100 2,607 100 (23)

EBITDA by Segments

40

40

S$m

31 Dec 2013

31 Dec 2012

Shareholders’ Funds 9,701 9,246

Capital Employed 13,689 13,578

Net Debt 1,535 3,153

Net Gearing Ratio 0.11x 0.23x

ROE 14.9% 22.6%

Capital/Gearing/ROE

41

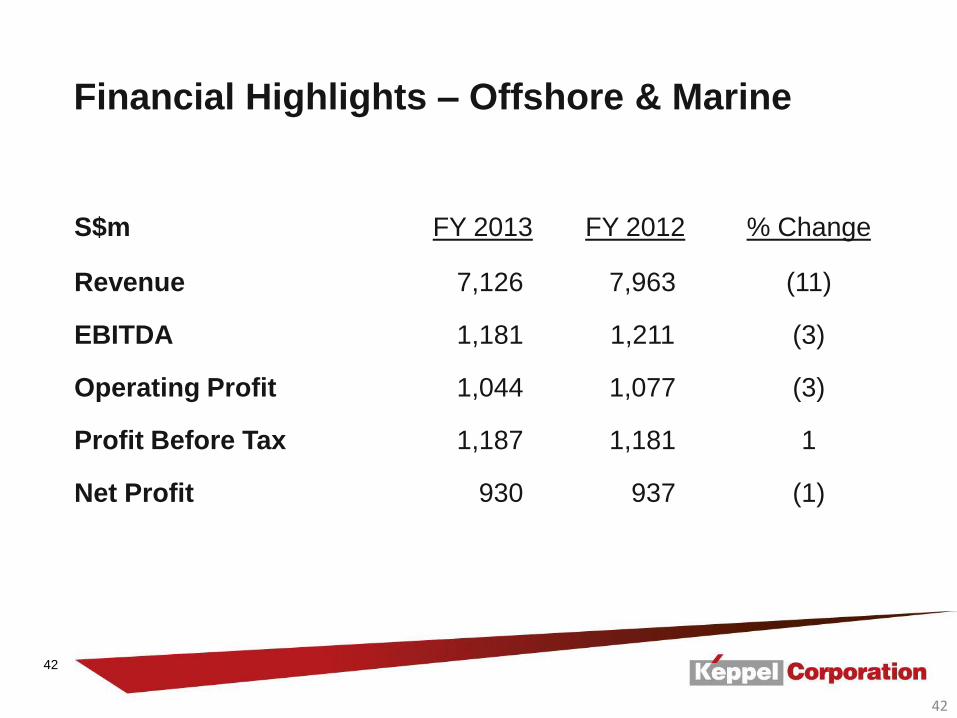

OFFSHORE & MARINE

42

42

S$m FY 2013 FY 2012 % Change

Revenue 7,126 7,963 (11)

EBITDA 1,181 1,211 (3)

Operating Profit 1,044 1,077 (3)

Profit Before Tax 1,187 1,181 1

Net Profit 930 937 (1)

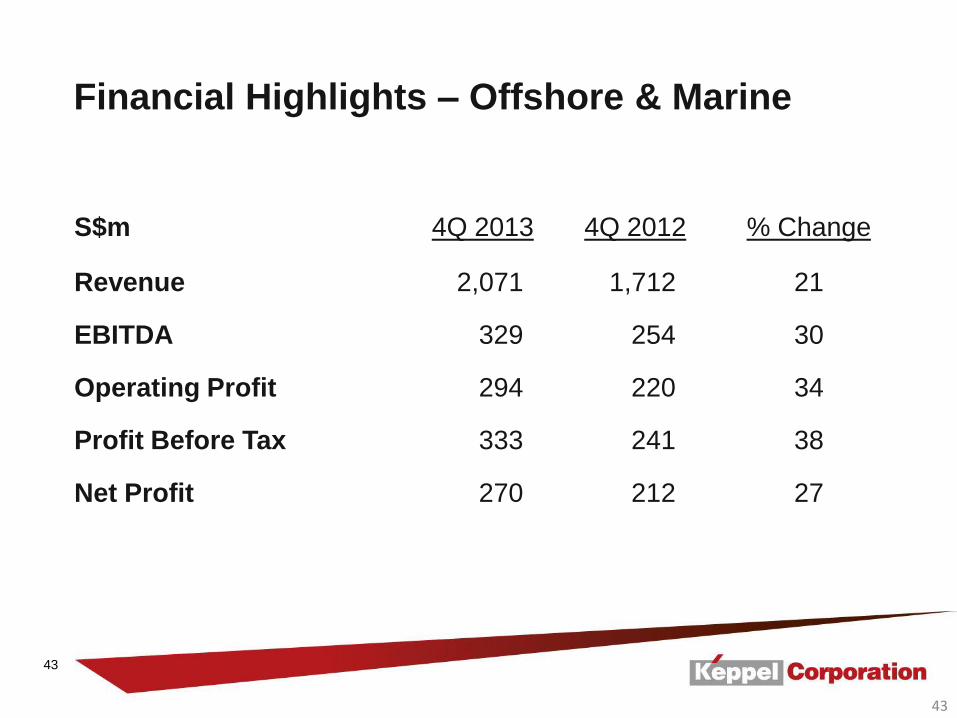

Financial Highlights – Offshore & Marine

43

43

S$m 4Q 2013 4Q 2012 % Change

Revenue 2,071 1,712 21

EBITDA 329 254 30

Operating Profit 294 220 34

Profit Before Tax 333 241 38

Net Profit 270 212 27

Financial Highlights – Offshore & Marine

44

S$2.1 billion contracts secured in 4Q 2013:

7 Jackups, 3 FPSO Conversion/Upgrades, 1 FSO Turret Fabrication,

1 Accommodation Semi Repair, 2 Submersible Barges and

1 Crane Vessel Repair

Major contract completions in 4Q 2013:

4 Jackups, 1 Accommodation Semi, 2 Semi Upgrades,

1 Diving Support Vessel, 1 Bulk Carrier and 1 Tug

44

Offshore & Marine Review

45

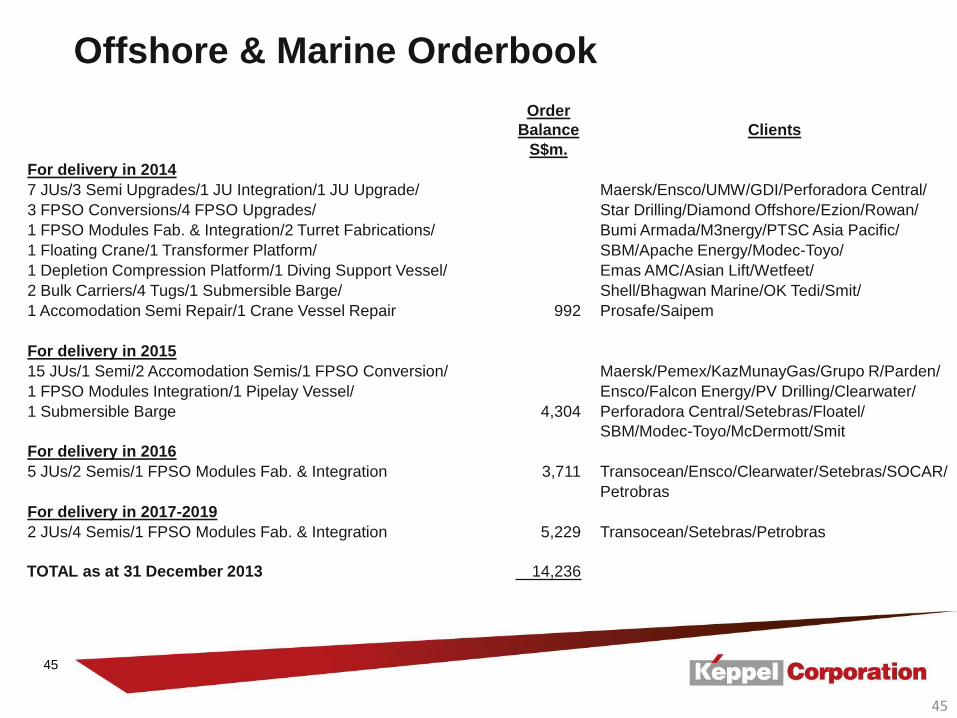

45

Offshore & Marine Orderbook

Order

Balance Clients

S$m.

For delivery in 2014

7 JUs/3 Semi Upgrades/1 JU Integration/1 JU Upgrade/ Maersk/Ensco/UMW/GDI/Perforadora Central/

3 FPSO Conversions/4 FPSO Upgrades/ Star Drilling/Diamond Offshore/Ezion/Rowan/

1 FPSO Modules Fab. & Integration/2 Turret Fabrications/ Bumi Armada/M3nergy/PTSC Asia Pacific/

1 Floating Crane/1 Transformer Platform/ SBM/Apache Energy/Modec-Toyo/

1 Depletion Compression Platform/1 Diving Support Vessel/ Emas AMC/Asian Lift/Wetfeet/

2 Bulk Carriers/4 Tugs/1 Submersible Barge/ Shell/Bhagwan Marine/OK Tedi/Smit/

1 Accomodation Semi Repair/1 Crane Vessel Repair 992 Prosafe/Saipem

For delivery in 2015

15 JUs/1 Semi/2 Accomodation Semis/1 FPSO Conversion/ Maersk/Pemex/KazMunayGas/Grupo R/Parden/

1 FPSO Modules Integration/1 Pipelay Vessel/ Ensco/Falcon Energy/PV Drilling/Clearwater/

1 Submersible Barge 4,304 Perforadora Central/Setebras/Floatel/

SBM/Modec-Toyo/McDermott/Smit

For delivery in 2016

5 JUs/2 Semis/1 FPSO Modules Fab. & Integration 3,711 Transocean/Ensco/Clearwater/Setebras/SOCAR/

Petrobras

For delivery in 2017-2019

2 JUs/4 Semis/1 FPSO Modules Fab. & Integration 5,229 Transocean/Setebras/Petrobras

TOTAL as at 31 December 2013 14,236

46

INFRASTRUCTURE

47

47

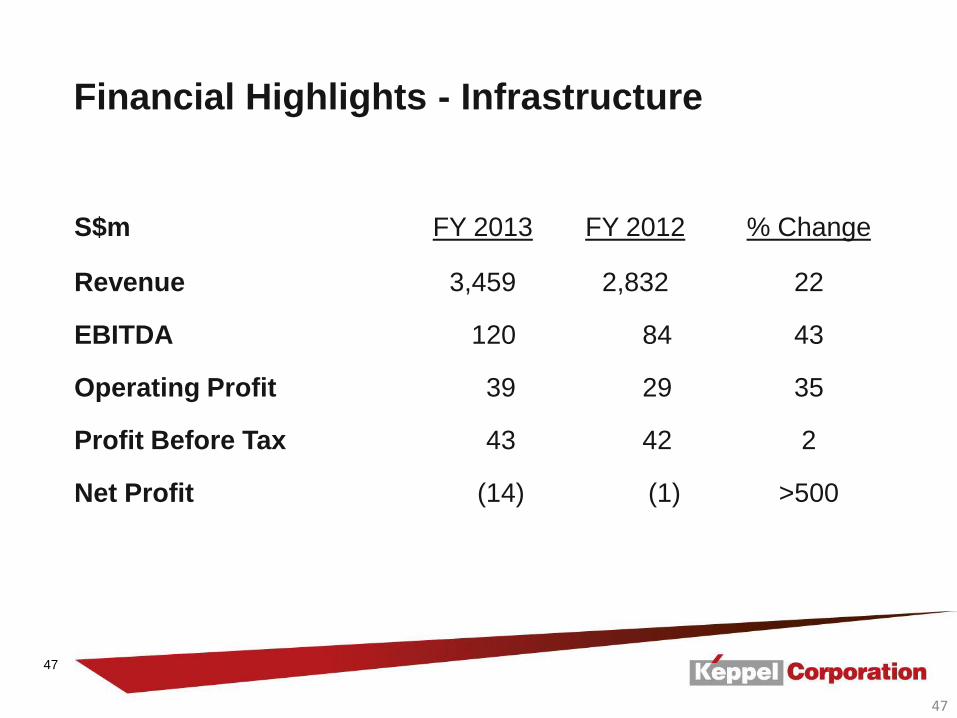

Financial Highlights - Infrastructure

S$m FY 2013 FY 2012 % Change

Revenue 3,459 2,832 22

EBITDA 120 84 43

Operating Profit 39 29 35

Profit Before Tax 43 42 2

Net Profit (14) (1) >500

48

48

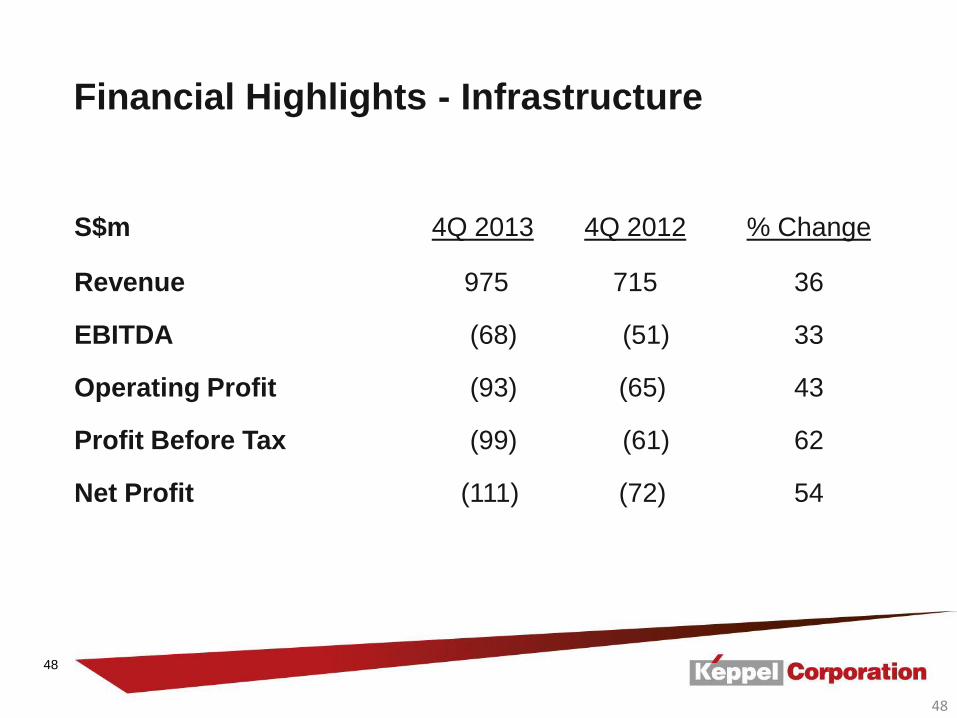

Financial Highlights - Infrastructure

S$m 4Q 2013 4Q 2012 % Change

Revenue 975 715 36

EBITDA (68) (51) 33

Operating Profit (93) (65) 43

Profit Before Tax (99) (61) 62

Net Profit (111) (72) 54

49

PROPERTY

50

50

Financial Highlights - Property

S$m FY 2013 FY 2012 % Change

Revenue 1,768 3,018 (41)

EBITDA 690 1,178 (41)

Operating Profit 666 1,157 (42)

Profit Before Tax 853 1,276 (33)

Net Profit 442 784 (44)

51

51

Financial Highlights - Property

S$m 4Q 2013 4Q 2012 % Change

Revenue 538 559 (4)

EBITDA 274 267 3

Operating Profit 270 259 4

Profit Before Tax 311 327 (5)

Net Profit 156 153 2

52

INVESTMENTS

53

53

S$m FY 2013 FY 2012 % Change

Revenue 27 152 (82)

EBITDA 25 134 (81)

Operating Profit 25 133 (81)

Profit Before Tax 80 196 (59)

Net Profit 54 194 (72)

Financial Highlights - Investments

54

54

S$m 4Q 2013 4Q 2012 % Change

Revenue 14 13 8

EBITDA 3 12 (75)

Operating Profit 3 11 (73)

Profit Before Tax 21 32 (34)

Net Profit 17 12 42

Financial Highlights - Investments

55

This release may contain forward-looking statements which are subject

to risks and uncertainties that could cause actual results to differ

materially from such statements. Such risks and uncertainties include

industry and economic conditions, competition, and legal, governmental

and regulatory changes. The forward-looking statements reflect the

current views of Management on future trends and developments.

1

ADDRESS BY KEPPEL CORPORATION LIMITED’S ACTING CHIEF FINANCIAL OFFICER, PAUL TAN

AT THE FULL YEAR 2013 RESULTS PRESENTATION

THURSDAY, 23 JANUARY 2014

1. Group Financial Highlights (Slide 16) 1.1 4Q 2013 Financial Performance (Slide 17)

Thank you, Chin Hua. A very good evening to all of you. The Group had a good quarter. Net profit for the fourth quarter of 2013 was $332 million, an improvement of 9% compared to the same period last year. Earnings per share for the quarter rose by 8% to 18.4 cents while EVA was at $291 million.

Cash inflow for the quarter was a robust $1.6 billion due to higher cash flow generated from operations mainly from our Offshore & Marine division.

1.2 4Q 2013 Financial Highlights (Slide 18)

For the fourth quarter, all key line items registered improvement from the same period last year, driven largely by higher revenue and margins at the Offshore & Marine division, despite higher losses in the Infrastructure division.

1.3 4Q 2013 Revenue by Segments (Slide 19)

Overall revenue rose by 20% in the fourth quarter, led mainly by the revenue growth in the Offshore & Marine and Infrastructure divisions.

Offshore & Marine’s increase in revenue was largely attributed to new jobs in the year and deliveries in the fourth quarter. Infrastructure registered a 36% improvement in fourth quarter’s revenue, driven largely by the higher contracted load for the expanded Keppel Merlimau Cogen plant.

2

1.4 4Q 2013 Pre-tax Profit by Segments (Slide 20)

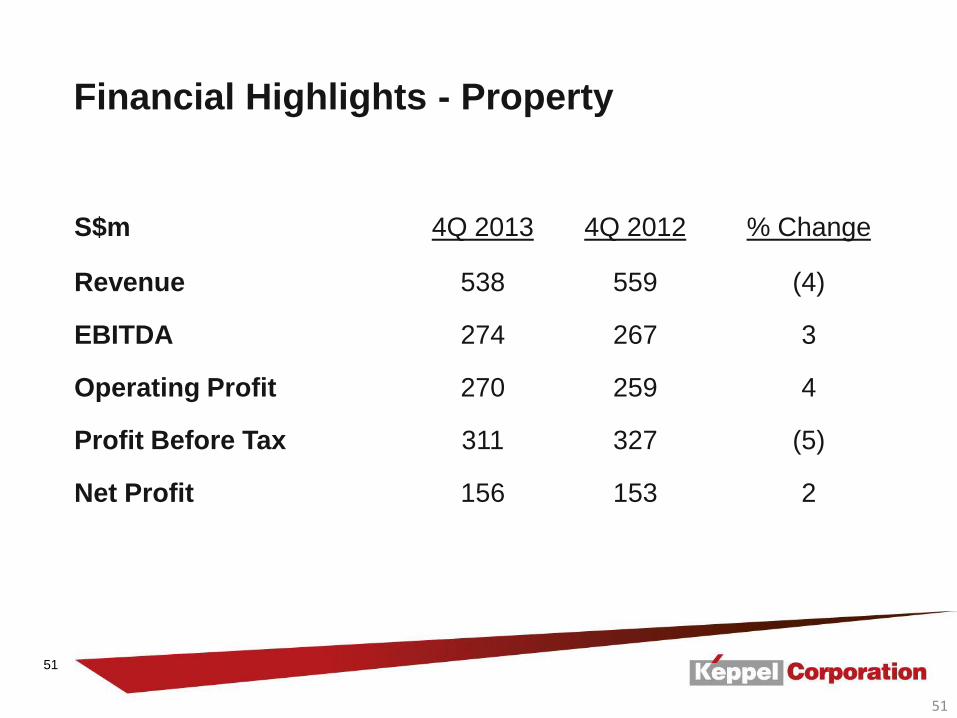

Increase in Offshore & Marine’s pre-tax earnings for the fourth quarter was due to higher revenue and margins.

Infrastructure’s losses were a result of cost overrun and prolongation cost at the Greater Manchester Energy-from-Waste Plant and the Doha North Sewage Treatment Works. These projects have continued to be very challenging. We have made appropriate claims for variation, prolongation and extension of time for the two Qatar projects. These are still being negotiated with our customers. Property recorded a 5% dip in pre-tax profit compared to the same period last year.

1.5 4Q 2013 Net Profit by Segments (Slide 21)

Group net profit in the fourth quarter was 9% higher. All divisions posted higher net profits, except for Infrastructure because of cost overrun resulting in the higher losses.

1.6 FY 2013 Financial Performance (Slide 22)

For the full year, the Group posted net earnings of $1.4 billion, representing a 26% decrease from the previous year. As we have highlighted in the earlier quarters, this year’s net profit is lower in the absence of one-time gains from the sale of apartments at Reflections at Keppel Bay in 2012. Earnings per share saw a similar decrease to 78 cents. We are pleased to propose a final dividend of 30 cents per share for this year. Together with the interim cash dividend of 10 cents and dividend in specie of Keppel REIT units equivalent to 9.5 cents per share, total distribution for 2013 will amount to 49.5 cents per share.

ROE declined to 14.9% while EVA was $939 million.

Our net gearing decreased from 23% in 2012 to 11% at the end of 2013, largely due to the deconsolidation of Keppel REIT from the Group with effect from the third quarter. As we have pointed out in the previous quarter, our stake in Keppel REIT has been reduced to a non-controlling interest following the dividend in specie distributions and private placements of Keppel REIT units.

3

1.7 FY 2013 Financial Highlights (Slide 23)

All key line items for the full year decreased compared to 2012, mainly because of lower revenue from the Offshore & Marine and Property divisions. The decline in profit is mainly due to lower earnings from the Property Division. The previous year also benefitted from a substantial gain on sale of equity investments.

1.8 FY 2013 Revenue by Segments (Slide 24)

Full year revenue at $12.4 billion was 11% lower than 2012. At Offshore & Marine, 22 rigs were completed and delivered. Many new jobs were also started during the year. These new jobs have not reached the stage of revenue recognition, resulting in revenue of Offshore & Marine falling by 11% in the year to $7.1 billion. Infrastructure’s higher revenue was attributed mainly to the expanded capacity of our power plant. Full year revenue for Property division decreased as a result of lower revenue from Reflections at Keppel Bay.

1.9 FY 2013 Pre-tax Profit by Segments (Slide 25)

Despite lower revenue, Offshore & Marine reported marginally higher pre-tax profit for the year because of improved operating margins. Higher earnings from the power and gas business were offset by the losses arising from our EPC projects in Qatar and UK. Pre-tax earnings of our Property division declined due to lower revenue.

1.10 FY 2013 Net Profit by Segments (Slide 26)

Net profit of Offshore & Marine was at the same level as 2012. It remains the top contributor to net profit, accounting for 66% of the Group’s full year earnings. Lower profits from Keppel Bay were partially offset by the higher earnings at Keppel Land and Keppel REIT.

Previous year’s earnings from Investments were higher due to one-time gains from sale of equities.

4

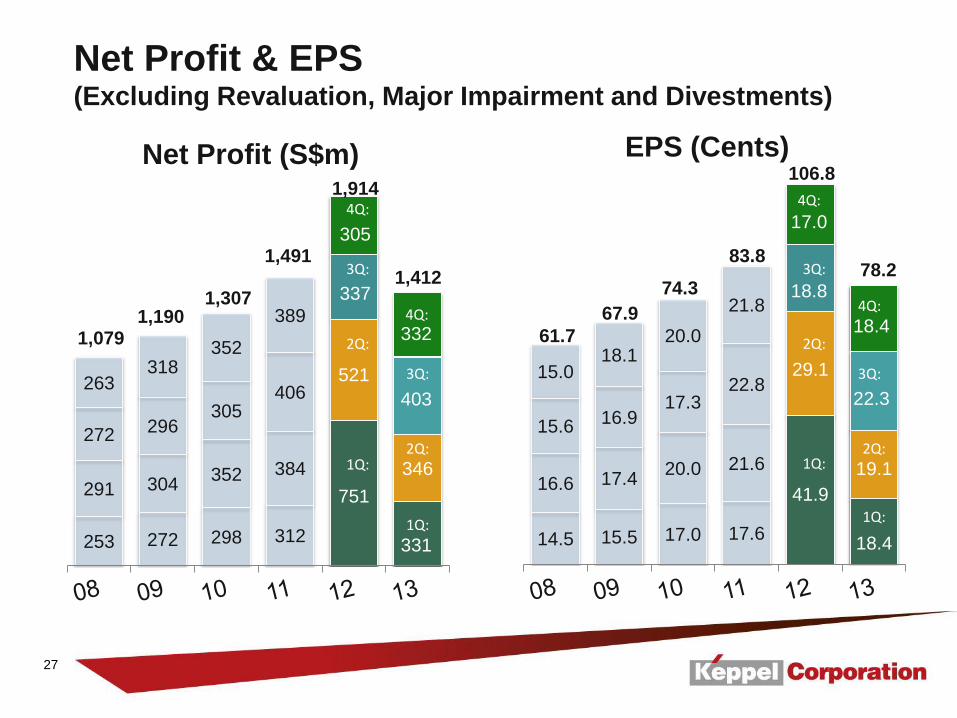

1.11 Net Profit and EPS – Excluding Revaluation, Major Impairment and Divestments (Slide 27) Net profit for the year of $1.4 billion is $502 million below 2012. Considering the huge exceptional gains from Reflections at Keppel Bay and sales of some equity investments in 2012 plus current year's cost overruns of the EPC projects in Doha and Manchester, our operating performance in 2013 continues to be strong. Despite the challenges in the year, our net profit for the second half of 2013 is 14% higher than the corresponding period in 2012.

1.12 Net Profit and EPS – Including Revaluation, Major Impairment and Divestments (Slide 28)

Gains from revaluation of investment properties and divestments for the year amounted to $434 million. This brings our overall net profit to $1.85 billion, 18% below 2012.

1.13 ROE & Dividend (Slide 29)

ROE decreased to 14.9% in 2013, reflecting the lower profit.

A final dividend of 30 cents per share has been proposed. Together with the interim cash dividend and distribution in specie of Keppel REIT units, the total distribution to our shareholders for 2013 will be 49.5 cents per share. This represents a payout ratio of 63% of our recurring profit.

1.14 Free Cash Flow (Slide 30)

We have redefined our free cash flow by excluding expansionary acquisitions (e.g. investment properties), capital expenditure (e.g. expansion of our co-gen plant) and major divestments. This better reflects our operational free cash flow excluding cash outflow for long term growth for the Group. Cash flow of $1.9 billion was generated from operations, about $700 million below the previous year. With higher cash receipts at Offshore & Marine from the deliveries of rigs and new orders secured in 2013, the resultant net cash from operating activities amounted to $625 million. In 2013, the Group spent $489 million on investments and operational capital expenditure mainly for Offshore & Marine division.

5

After taking into account dividend income and divestment proceeds of $506 million, net cash from investing activities was $17 million. The resultant cash inflow was $642 million for the year, which is at the same level as 2012.

2. Business Review & Outlook (Slide 31) 2.1 Positive Global Energy Outlook (Slide 32)

Global energy demand is projected to continue to rise with increased urbanisation and economic growth in developing countries. E&P spending is expected to increase to meet this trend and boost depleting oil and gas reserves. This positive development will benefit the Offshore and Marine industry.

2.2 Offshore & Marine (Slide 33)

The Offshore & Marine division ended the year well with strong order wins of $2.1 billion in the fourth quarter bringing our net order book to a record $14.2 billion.

On time deliveries made by the division in this quarter bear testament to our strong project execution capabilities.

The MOU signed with PEMEX to develop a new yard in Mexico reinforces our Near Market Near Customer strategy and will enable Keppel to strengthen its foothold in the growing Offshore & Marine market in Mexico.

2.3 Infrastructure (Slide 34)

Our EPC projects in Doha and Runcorn are expected to be substantially completed by the end of 2014, providing us with more visibility in completing the contracts. Building on its proven track record in WTE technologies, Keppel Seghers has recently secured a WTE technology package contract from a repeat customer in Yangzhou, China.

6

2.4 Property (Slide 35)

We have sold more than 900 homes in our key markets in Asia this quarter, primarily from our developments in China. On the commercial front, MBFC Tower 3 is 95% committed while Ocean Financial Centre has achieved full occupancy. We have also completed the divestment of our share in Jakarta Garden City realising a net gain of approximately $149 million. We continue to build up our portfolio of quality developments in China with the addition of a prime residential site in Tianjin Eco-City this quarter. About 350 landed homes are expected to be built on this site, which will be launched progressively from the second half of 2014. As we look ahead to a new year, we are mindful of the challenges. In Offshore & Marine, we will have to fend off the competition, execute well and innovate to stay ahead. In Infrastructure, we remained focused on completing the EPC contracts within the costs to complete and projected timeline, and returning the division to profitability. In Property, we have to seek out opportunities and capture value despite market cooling measures.

We are committed to achieving all these and more to sustain growth for the Group.

Thank you.