Embed Size (px)

Citation preview

Full CostingUniversity of Vienna

Content

• Introduction• Aims of Full Costing • Implementation of Full Costing• Full costing model• Conclusion and Challenges

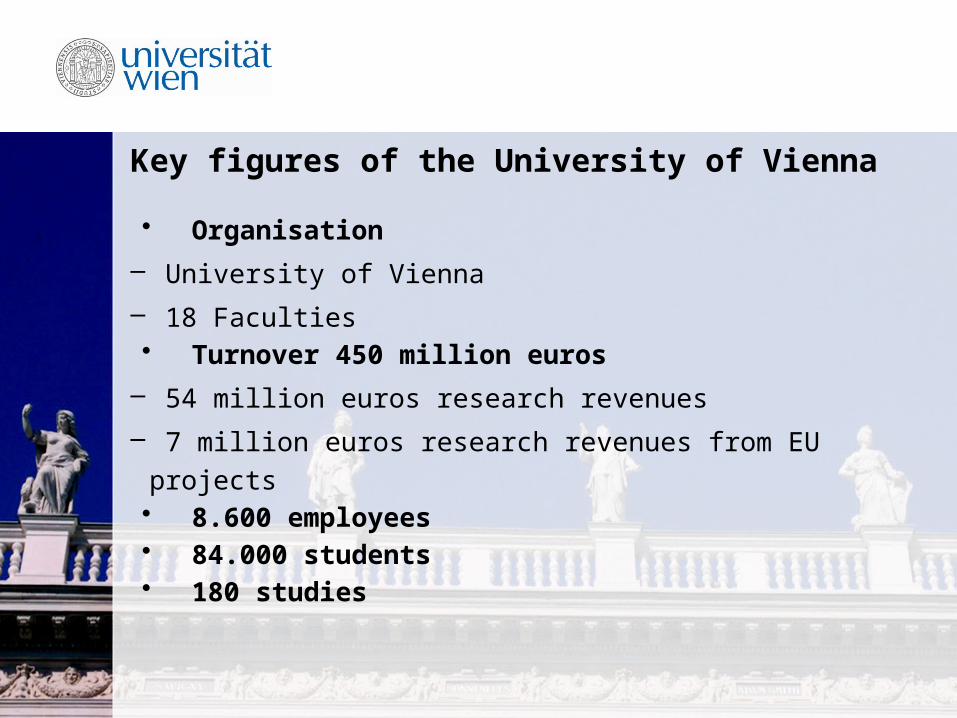

Key figures of the University of Vienna

• Organisation

– University of Vienna

– 18 Faculties • Turnover 450 million euros

– 54 million euros research revenues

– 7 million euros research revenues from EU projects• 8.600 employees• 84.000 students• 180 studies

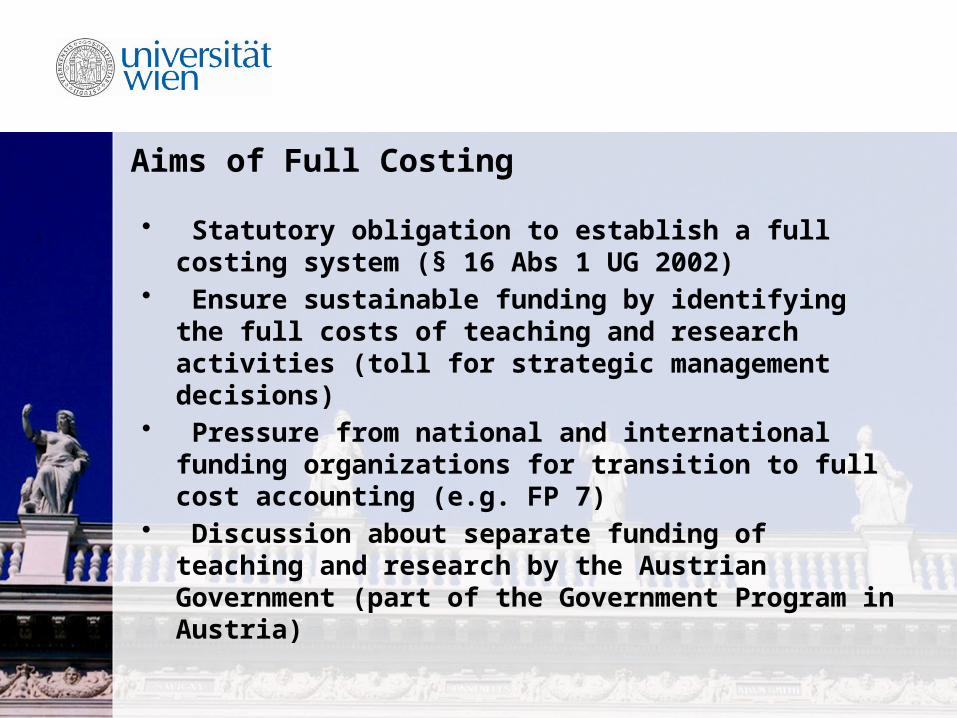

Aims of Full Costing

• Statutory obligation to establish a full costing system (§ 16 Abs 1 UG 2002)

• Ensure sustainable funding by identifying the full costs of teaching and research activities (toll for strategic management decisions)

• Pressure from national and international funding organizations for transition to full cost accounting (e.g. FP 7)

• Discussion about separate funding of teaching and research by the Austrian Government (part of the Government Program in Austria)

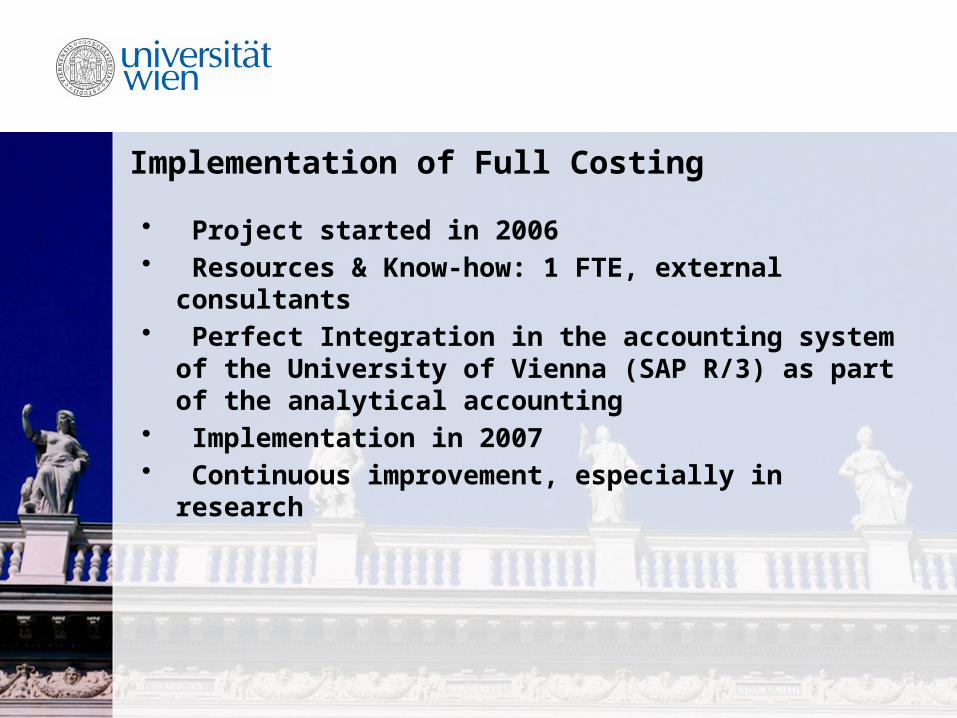

Implementation of Full Costing

• Project started in 2006• Resources & Know-how: 1 FTE, external consultants• Perfect Integration in the accounting system of the

University of Vienna (SAP R/3) as part of the analytical accounting

• Implementation in 2007• Continuous improvement, especially in research

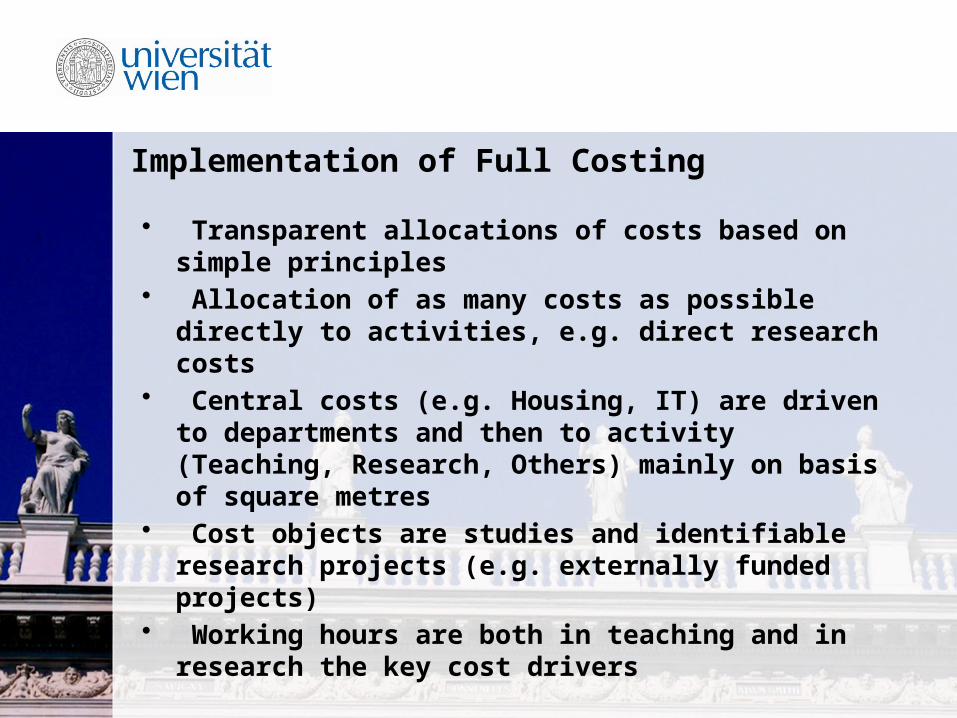

Implementation of Full Costing

• Transparent allocations of costs based on simple principles

• Allocation of as many costs as possible directly to activities, e.g. direct research costs

• Central costs (e.g. Housing, IT) are driven to departments and then to activity (Teaching, Research, Others) mainly on basis of square metres

• Cost objects are studies and identifiable research projects (e.g. externally funded projects)

• Working hours are both in teaching and in research the key cost drivers

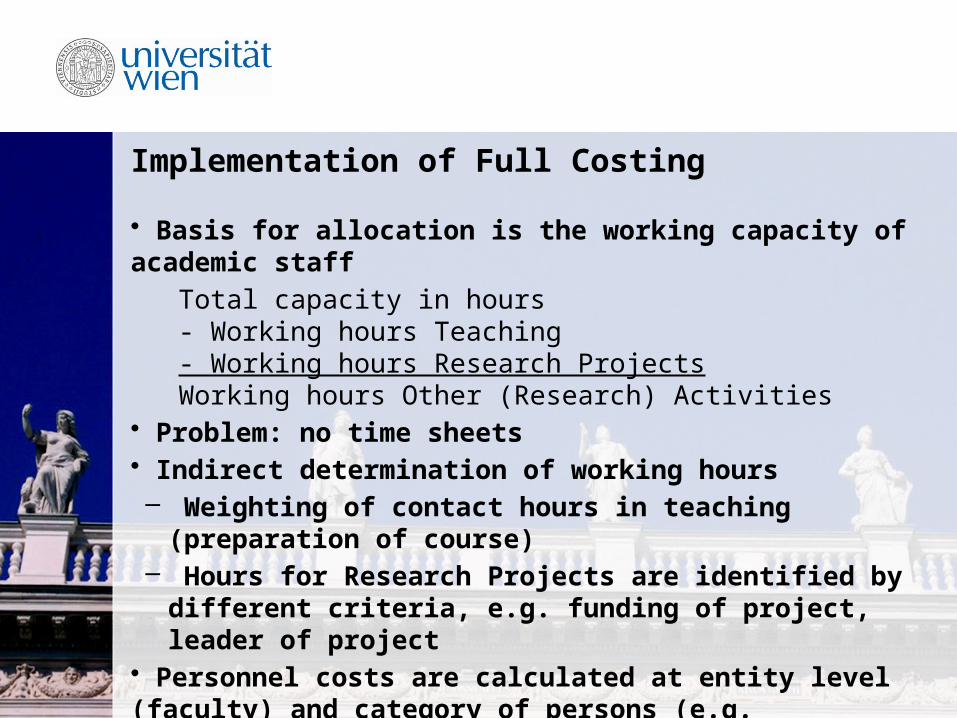

Implementation of Full Costing

• Basis for allocation is the working capacity of academic staff

Total capacity in hours- Working hours Teaching- Working hours Research Projects

Working hours Other (Research) Activities• Problem: no time sheets• Indirect determination of working hours– Weighting of contact hours in teaching (preparation of

course)– Hours for Research Projects are identified by different

criteria, e.g. funding of project, leader of project• Personnel costs are calculated at entity level (faculty) and category of persons (e.g. professor, assistant, lecturer)

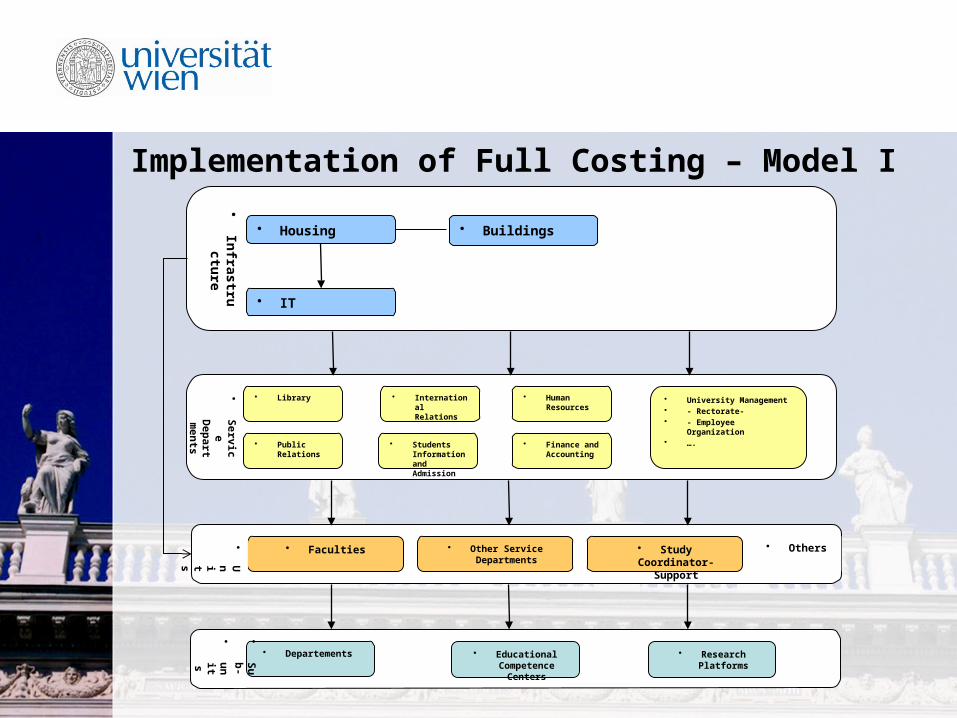

Implementation of Full Costing – Model I

•S

erv

ice

Dep

ar

tmen

ts

• Library • University Management

• - Rectorate-• - Employee

Organization• ….

• Human Resources

• International Relations

• Students Information and Admission

• Public Relations

• Finance and Accounting

• Faculties • Other Service Departments

•Units

• Study Coordinator-

Support

• Others

• Housing • Buildings

• IT

•In

frastru

ctu

re

• Departements

•Sub-

•uni

ts

• Research Platforms

• Educational Competence

Centers

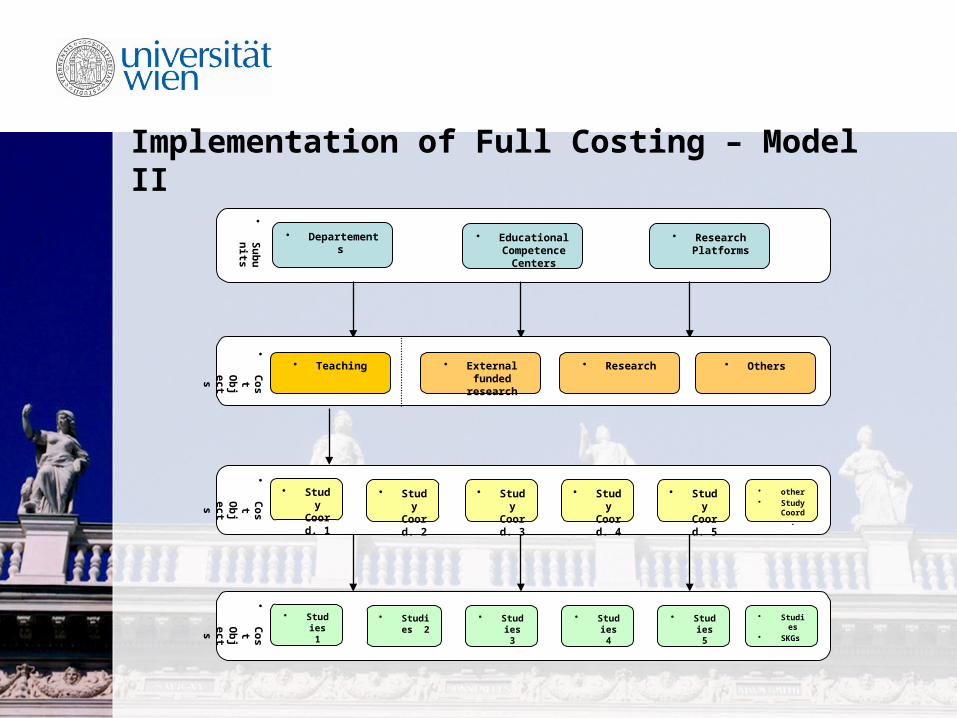

Implementation of Full Costing – Model II

• Departements

•S

ub

un

its

• Research Platforms

• Educational Competence Centers

• Study

Coord. 1

• Study

Coord. 2

•C

os

t O

bj

ect

s

• Study

Coord. 3

• Study

Coord. 4

• Study

Coord. 5

• other• Study

Coord.

• Studies 1

• Studies 2

•C

os

t O

bj

ect

s

• Studies 3

• Studies 4

• Studies 5

• Studies

• SKGs

• Teaching • External funded

research

•C

os

t O

bj

ect

s

• Research • Others

Conclusion and Challenges - Teaching

• Full costs of teaching are well identified

• The outcome are actual costs per student (great range

between humanities and natural sciences)

• Use for standard costing calculations of studies

Conclusion and Challenges – Research

• Full costing methodology is focused on the control and

decision needs of the management of the University of

Vienna

• Separatly adjustments necessary, to fulfil the EC cost

reporting requirments (elimination of ineligible costs from

indirect costs -> indirect taxes, duties, exchange rate

losses, interest payable, provision)

• University of Vienna uses flat rate of 60 % in FP7

• Ongoing preparation for declaring actual indirect costs

(Simplified Method) in the next FP

• Main problem: no time sheets

Thank you for your attention!

• Contact details

Dr. Manuela Raith

Vice Head of Accounting and Finance

Dr.-Karl-Lueger-Ring 1

1010 Vienna

Tel.: +43 1 4277 12503

Email.: [email protected]