Embed Size (px)

DESCRIPTION

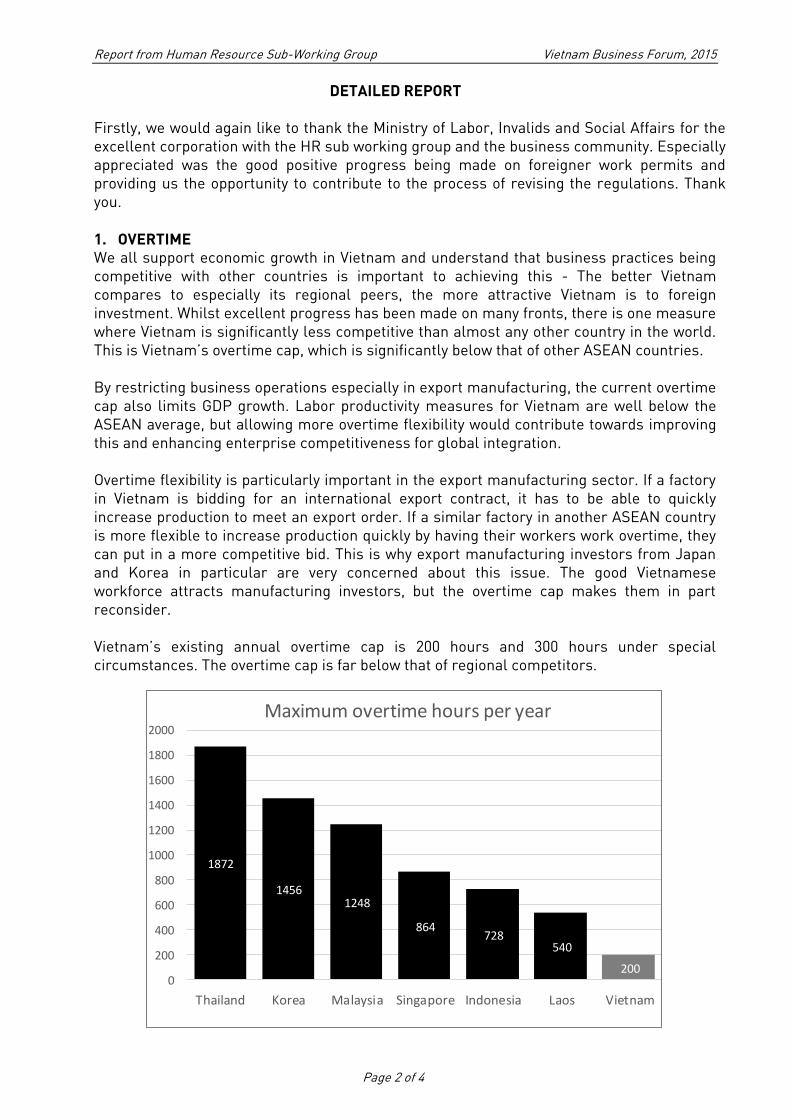

Full Annual Vbf Report 2015 Final, Full Annual Vbf Report 2015 Final, , Full Annual Vbf Report 2015 Final, , Full Annual Vbf Report 2015 Final, , Full Annual Vbf Report 2015 Final, , Full Annual Vbf Report 2015 Final, , Full Annual Vbf Report 2015 Final, , Full Annual Vbf Report 2015 Final, , Full Annual Vbf Report 2015 Final,

Citation preview

ANNUAL VIETNAM BUSINESSFORUM 2015

Hanoi, December 1, 2015

Annual Vietnam Business Forum 2015

ENHANCING ENTERPRISE COMPETITIVENESS FOR GLOBAL

INTEGRATION

Hanoi, December 1, 2015

DISCLAIMER The Vietnam Business Forum (“VBF”) is a structured and ongoing policy dialogue between the Vietnamese Government and the local and the foreign business community for a favorable business environment that attracts private sector investment and stimulates sustainable economic growth in Vietnam. This publication was created for the Annual Vietnam Business Forum on December 1, 2015 in Hanoi. The conclusions and judgments contained in this publication, as well as presentations made by businesses’ representatives at the Forum, should not be attributed to, and do not necessarily represent the views of, the VBF Consortium Board, or the VBF Secretariat, or its co-chairing institutions including Vietnam’s Ministry of Planning and Investment, the World Bank Group, and IFC - a member of the World Bank Group. These parties do not guarantee the accuracy of the data in this publication and the aforesaid presentations, and accept no responsibility for any consequences of their use. This publication is distributed subject to the condition that it shall not, by way of trade or otherwise, be lent, re-sold, hired out, or otherwise circulated on a commercial basis.

Page 1 of 2

TABLE OF CONTENTS TENTATIVE AGENDA Section I: REVIEW OF BUSINESS CLIMATE 1.1. Vietnam Chamber of Commerce and Industry - VCCI 1.2. American Chamber of Commerce - AMCHAM 1.3. European Chamber of Commerce - EUROCHAM 1.4. Korea Chamber of Commerce - KOCHAM 1.5. Japanese Business Associations in Vietnam - JBAV 1.6. Australian Chamber of Commerce - AUSCHAM 1.7. Nordic Chamber of Commerce - NORDCHAM Section II: INVESTMENT & TRADE, BANKING AND CAPITAL MARKETS 2.1. INVESTMENT AND TRADE 2.1.1. Position Paper of VBF Investment & Trade Working Group 2.1.1.a. Attachment 1 to the Position Paper – Foreign Arbitral Awards 2.1.1.b. Attachment 2 to the Position Paper – Petition from the Association of Vietnamese

Insurers on Decision 35/2015/QD-TTg 2.1.2. Report of Investment & Trade Working Group on Investment & Enterprise Laws 2.1.3. Investment & Trade Progress Report 2.2. BANKING 2.2.1. Position Paper of VBF Banking Working Group 2.2.2. Banking Progress Report 2.3 CAPITAL MARKETS 2.3.1. Position Paper of VBF Capital Markets Working Group 2.3.2. Talking points with the State Securities Commission on Capital Markets Issues 2.3.3. Meeting Notes with the State Securities Commission on October 27, 2015 Section III: AGRICULTURE, EDUCATION & TRAINING, HR AND GOVERNANCE & INTEGRITY 3.1. AGRIBUSINESS 3.1.1. Position Paper of VBF AgriBusiness Working Group 3.2. EDUCATION & TRAINING 3.2.1. Position Paper of VBF Education & Training Working Group 3.2.2. Education & Training Progress Report 3.2.3. Meeting Notes with Ministry of Education and Training on Decree 73 on Nov 13,

2015 3.3. HUMAN RESOURCE 3.3.1. Position Paper of VBF Human Resource Working Sub-Group

Page 2 of 2

3.3.2. Human Resource Progress Report 3.3.3. Meeting Notes with Ministry of Labor, Invalids and Social Affairs on Draft Decree

amending Decree 102/2013/ND-CP on August 6, 2015 3.4. GOVERNANCE & INTEGRITY 3.4.1. Position Paper of VBF Governance & Integrity Working Group Section IV: INFRASTRUCTURE, AUTOMOTIVE AND MINING 4.1. INFRASTRUCTE 4.1.1. Position Paper of VBF Infrastructure Working Group 4.1.2. Infrastructure Progress Report 4.2. AUTOMOTIVE 4.2.1. Position Paper of VBF Automotive Working Group 4.2.2. Automotive Progress Report 4.3. MINING 4.3.1. Position Paper of VBF Mining Working Group 4.3.2. Mining Progress Report Section V: REPORTS FROM OTHER WORKING GROUPS 5.1. TAX 5.1.1. Position Paper of VBF Tax Sub- Working Group 5.1.2. Tax Progress Report 5.1.3. Talking points with Ministry of Finance on Some Tax Related Issues 5.1.4. Meeting Notes with Ministry of Finance on Double Taxation Agreement on August

25, 2015 5.2. LAND 5.2.1. Position Paper of VBF Land Sub-Working Group 5.2.2. Land Progress Report 5.3. POWER AND ENERGY 5.3.1. Position Paper of VBF Power & Energy Sub-Working Group 5.3.2. Meeting Notes with Ministry of Industry & Trade and Ministry of Planning &

Investment on Power & Energy Related Issues 5.4. PORT AND SHIPPING 5.4.1. Position Paper of VBF Port & Shipping Sub-Working Group 5.5. TOURISM 5.5.1. Position Paper of VBF Tourism Working Group 5.5.2. Meeting Notes with Vietnam National Administration of Tourism on Related Issues

on October 8, 2015 Section VI: APPENDIXES 6.1. Summary Notes of Mid-term Vietnam Business Forum – June 2015 6.2. Prime Minister’s Speech in Mid-term Vietnam Business Forum – June 2015

Page 1 of 2

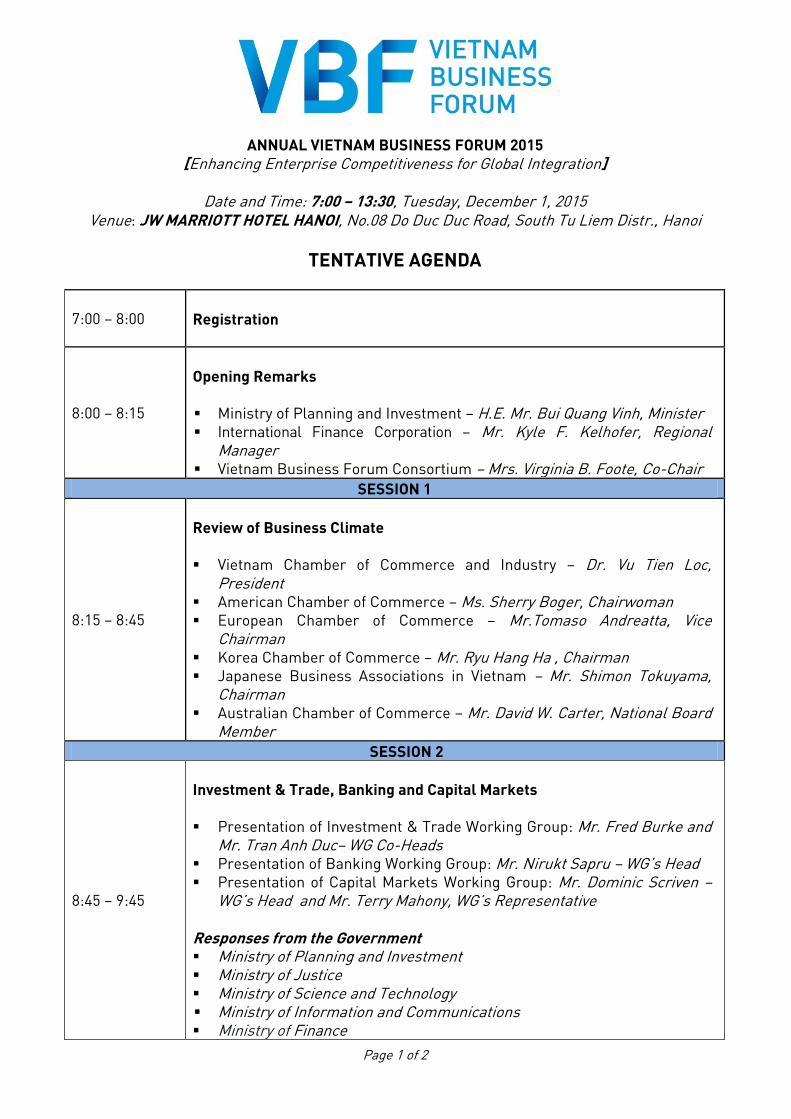

ANNUAL VIETNAM BUSINESS FORUM 2015 [Enhancing Enterprise Competitiveness for Global Integration]

Date and Time: 7:00 – 13:30, Tuesday, December 1, 2015

Venue: JW MARRIOTT HOTEL HANOI, No.08 Do Duc Duc Road, South Tu Liem Distr., Hanoi

TENTATIVE AGENDA 7:00 – 8:00

Registration

8:00 – 8:15

Opening Remarks Ministry of Planning and Investment – H.E. Mr. Bui Quang Vinh, Minister International Finance Corporation – Mr. Kyle F. Kelhofer, Regional

Manager Vietnam Business Forum Consortium – Mrs. Virginia B. Foote, Co-Chair

SESSION 1

8:15 – 8:45

Review of Business Climate Vietnam Chamber of Commerce and Industry – Dr. Vu Tien Loc,

President American Chamber of Commerce – Ms. Sherry Boger, Chairwoman European Chamber of Commerce – Mr.Tomaso Andreatta, Vice

Chairman Korea Chamber of Commerce – Mr. Ryu Hang Ha , Chairman Japanese Business Associations in Vietnam – Mr. Shimon Tokuyama,

Chairman Australian Chamber of Commerce – Mr. David W. Carter, National Board

Member SESSION 2

8:45 – 9:45

Investment & Trade, Banking and Capital Markets Presentation of Investment & Trade Working Group: Mr. Fred Burke and

Mr. Tran Anh Duc– WG Co-Heads Presentation of Banking Working Group: Mr. Nirukt Sapru – WG’s Head Presentation of Capital Markets Working Group: Mr. Dominic Scriven –

WG’s Head and Mr. Terry Mahony, WG’s Representative Responses from the Government Ministry of Planning and Investment Ministry of Justice Ministry of Science and Technology Ministry of Information and Communications Ministry of Finance

Page 2 of 2

Ministry of Public Security Ministry of Transport State Bank of Vietnam State Securities Commission of Vietnam

9:45 – 10:00 Keynote Address by DEPUTY PRIME MINISTER H.E. Mr. VU VAN NINH

10:00 – 10:15 COFFEE BREAK

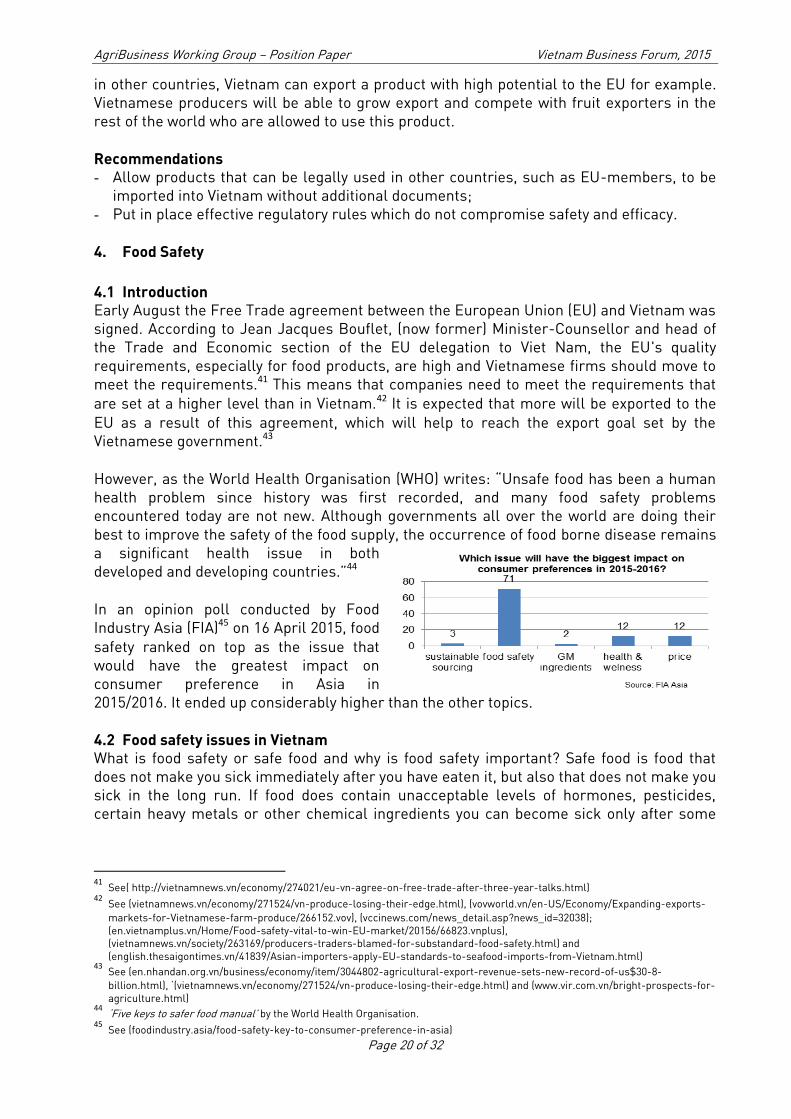

SESSION 3

10:15 – 11:15

Agriculture, Education & Training, HR, and Governance & Integrity Presentation of Agri-Business Working Group: Mr. David Whitehead,

WG’s Head Presentation of Education and Training Working Group: Mr. Brian

O'Reilly, WG’s Head Presentation of HR SubGroup: Mr. Colin Blackwell, Sub-WG’s Head Presentation of Governance & Integrity Working Group: Mr. Phil

Newman, WG’s Representative Responses from the Government (40’) Ministry of Agriculture and Rural Development Ministry of Education and Training Ministry of Labor, Invalids and Social Affairs

SESSION 4

11:15 – 12:00

Infrastructure, Automotive and Mining Presentation of Infrastructure Working Group: Mr. Tony Foster, WG’s

Head Presentation of Automotive Working Group: Mr. Wail A Farghaly, WG’s

Head Presentation of Mining Working Group: Mr. Bill Howell, WG’s Head

Responses from the Government (30’) Ministry of Industry and Trade Ministry of Finance Ministry of Natural Resources and Environment

SESSION 5

12:00– 12:15

Closing Remarks World Bank in Vietnam – Mrs. Victoria Kwakwa, Country Director Vietnam Business Forum Consortium – Dr. Vu Tien Loc, Co-Chair Ministry of Planning and Investment – H.E. Mr. Bui Quang Vinh, Minister

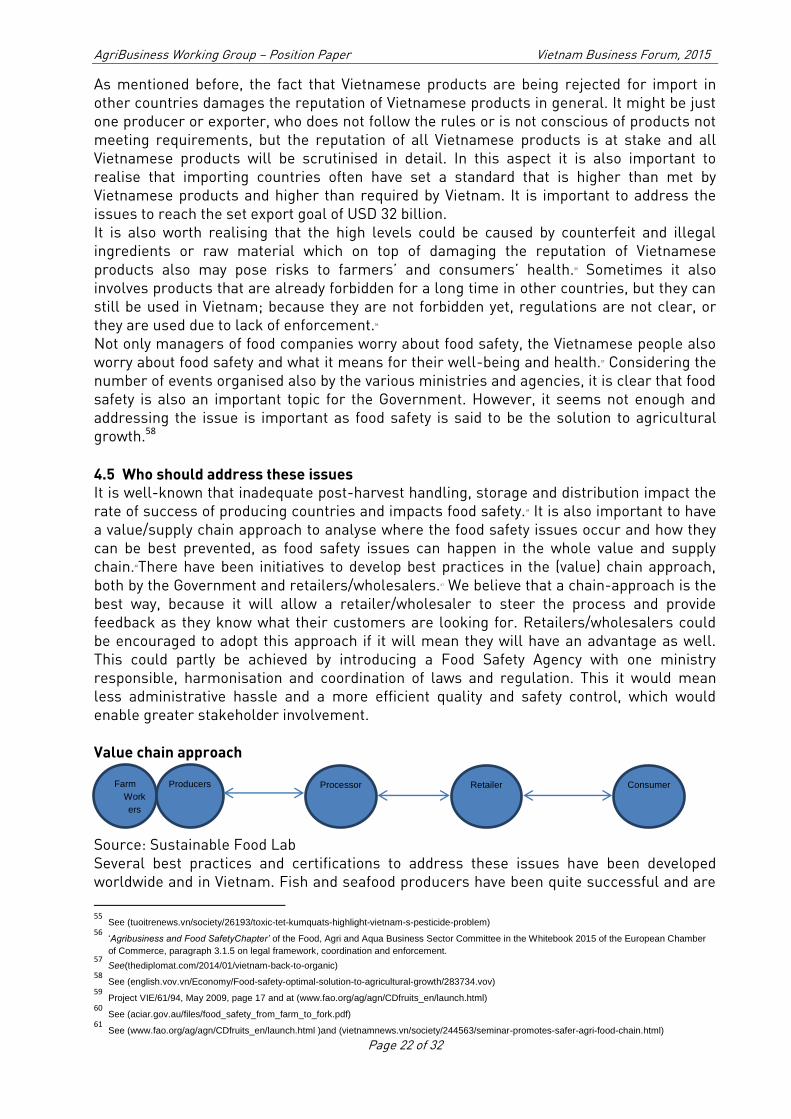

12:15 – 13:30 LUNCHEON

VIP Lunch – By Invitation Only Event Room 3 – JW MARRIOTT Hanoi Hotel Networking Lunch JW Café Restaurant Area & Fountain Area

Section I

REVIEW OF BUSINESS CLIMATE

Page 1 of 12

THE VIETNAM CHAMBER OF COMMERCE AND INDUSTRY (“VCCI”)

RECOMMENDATIONS

Vietnam Business Forum 2015 Ha Noi, December 1,2015

Prepared by

The Vietnam Chamber of Commerce and Industry

I. RECOMMENDATIONS FOR CUSTOMS ADMINISTRATIVE REFORM The 2015 Survey of Business Satisfaction with the Customs Administrative Procedures is a collaborative effort of the Vietnam Chamber of Commerce and Industry (VCCI), the General Department of Vietnam Customs (GDVC), and the Vietnam Governance for Inclusive Growth project (USAID GIG). The survey received 3,123 responses from businesses engaging in regular import – export activities. This paper documents a summary of recommendations by businesses as a result of the mentioned above survey. Summary: In 2015, the Customs Service has continued its reform efforts towards facilitating businesses. Remarkable progress has been recognized by the business community concerning the improvement of the customs legislation system, transparency of access to legal information and customs procedures as well as prompt and effective support of customs authorities. Businesses are expecting stronger and more drastic reforms of the Customs Service in many areas such as improving quality of customs legal normative documents, further simplifying and making public and transparent of administrative procedures, improving tax related processes and procedures, focusing more on specialized inspection, enhancing the effectiveness of cooperation between customs authorities and other agencies involved in the implementation of customs procedures for businesses. In 2015, the Vietnam Customs has made continued efforts for reform and modernization in support of compliance with the international standards, practices and commitments. Many synchronized measures have been actively undertaken by the Sector in term of completing the customs legal system in the direction of simplifying the administrative procedures, implementing the automated customs clearance system VNACCS/VCIS nationwide, strengthening the employment of information technology (IT) through the application of electronic signatures, electronic paymentand receipt of cargo electronic manifestsat seaports; expanding the application of barcodes in port monitoring... and implementing the Declaration of Customer Service revised in 2015, undertaking proactive measures to prevent negative affairs and corruption. These are the specific measures being adopted by the Customs Service to realize the reform goals in the Customs Development Strategy until 2020, the Plan for reform, development and modernization of the Customs Service for the 2011-2015 period, especially at Resolution No. 19/2014/NQ-CP and Resolution No.19/2015/NQ-CP of the Government to reduce Vietnam‟s customs clearance time to the level of the ASEAN-6 countries

Page 2 of 12

by 2015 and of the ASEAN-4 countries in 2016 and at Directive No.24/CT-TTg dated 08/05/2014 of the Prime Minister on strengthening the tax and customs administrative reform and managementto further promote the customs modernization.

These measures have achieved remarkable results, helping lower the costs and time ofcustoms clearance of goods for export and import businesses. However, the survey also noted the fact that the business community still has high hopes for more drastic and stronger reforms of the customs service acrossvarious aspects. Below is a summary of specific recommendations by businesses for the Customs in the time to come: 1. Improving quality of customs legal normative documents The quick revision and finalization of the provisions of Customs legislation in recent years has created favorable conditions for businesses engaging in import and export activities. However, the issuance of amendments, supplements and replacements takes place so quickly, causing the risk that no sooner had many enterprises got the hang of old circulars, new circulars were already issued, (e.g Circular 22/2014/TT-BTC took place in a very short time was already replaced by Circular 38/2015/TT-BTC). Besides, there exists the fact that those documents are too long and their provisions are unclear and vague, making it easier to be differently interpreted and applied by customs authorities and businesses. Given quality of such documents, it also caused inconsistent implementation of customs procedures by different customs units and officers. Some amongst them stick to such rigid regulations, for example concerningquality check of leatheretete on the seat of mobility disablity chairs. Some do not fully comply with regulations of dossiers & documents as prescribed but require businesses to present additional documents, causing difficulties for businesses. Recommendations: It is necessary to improve the quality of customs legal normative documents which should have explicit contents, creating a unified understanding between customs authorities, other relevant agencies and businesses.

2. Further simplifying some customs procedures Regulations on customs procedures: Some regulations on customs procedures are unclear and unreasonable, say, procedure of cancelling customs declaration, procedure of on spot import and export; the analysis and classification of goods take too long and require too many samples; the regulation on time for temporary import for re-export of vehicles is too cumbersome; the regulation on deadline to submit quality check results is not suitable with the goods of heavy machinery, large shipments; as well as the regulation that does not allow revision of location codes is not reasonable. Actual inspection of goods and customs supervision: The procedure of implementing actual inspection and customs supervision at many local customs agencies remains unclear. It is suggested by businesses that this procedurebe revised in order to avoid inadequacy for businesses Post-clearance checks: This procedure is assessed by businesses as inadequate as this is required even for the declaration that already went through actual inspection. The settlement of difference in terms of inventory data by customs authorities and businesses for the type of

Page 3 of 12

processing and export production is not reasonable. That the customs authorities collect tax arrears on this difference is not consistent with reality, causing businesses„ dissatisfaction. Reporting on liquidation for processing and export production: This procedure is not provided with specific guidelines. Many businesses said they do not know how to make reports and it takes them lots of time to do it and so they prefer the old liquidation procedure better. Regulations on customs procedures implemented by amongst customs authorities and by other management agencies are not consistent, for instance: it isn„t required by customs authorities to have certification on declaration form while it is required by tax agencies to do so. 3. Improving tax related processes and procedures Tax-related policies have some irrational points: many businesses reported on irrationalities in regulations concerning the tax on goods temporarily imported for re-export and or goods imported via express courier and sold through contract with processing enterprises. The tax reduction and exemption procedure that is stipulated by the Ministry of Planning and Investment in Circular No.04/2012/TT-BKHĐT remains unclear, even for the category of goods that can be locally produced. The regulation of tax payment prior to customs clearance for good compliants is not reasonable either, which is not encouraging for businesses. It is suggested to reconsider the time for tax payment for the input materials for export in the case of production duration over 275 days; the procedures of tax exemption are cumbersome & time consuming for businesses that have to make many trips back & forth to revise and provide additional documents. Circulation of tax payment documents between bank, treasury and customs is not good, causing inconvenience to businesses in proving that they already paid tax for the opened declaration form. The working time of the bank and customs agency regarding the implementation of this procedure is not well coordinated: The declaration is already made but tax can‟t be paid for clearance as the banks close early on weekdays and are not open on weekends, public holidays, or Tet holidays. Identification of HS code and tariff. There still exists the fact that a same goods item is subject to different HS codes at different customs branches, causing troubles for many businesses. Vietnam participates in many trade agreements and there are corresponding import - export tariff that should be timely and comprehensively disseminated to enterprises so that they know and benefit from the signed agreements. Prices for tax and fee calculation. Despite new regulations, price consultations have been done correctly. There remains the cases where price consultation is required for every importation even when the enterprise import the same goods with stable price determination factors. The price Database is not transparent and open to for enterprises to check on their own. Customs fee is not significant but businesses have to take time for such payment procedures. Certificate of origin for imports. Many businesses report that the signatures on preferential C/Os are not timely updated, unlike the sample signature, and take time to verify; Form D C/O is received after the goods ... In such cases, the customs authorities often require businesses to pay taxes at high rates and receive refund later upon having verification results, the procedure for which is very complicated. The procedures for checking the C/O are not

Page 4 of 12

consistently implemented across different units. For instance, one C/O is accepted as valid at the dossier receiving section, but is not accepted by the sections of reexamination or post-clearance checks and businesses are required to pay tax arrears.

4. Improving the effficiency of methods and means of customs management, professional

skills, attitudes of customs officers VNACCS system has some shortcomings yet: This system is evaluated by businesses to have many advantages, but some shortcomings remain, say, wrong notification of pending customs declaration, tax & fee payment; failure to declare re-export of temporarily imported equipment under the category of G23, S0218-SS1-0000 error (failure to browse/select export license); overlapping of code contents; liquidation errors (data is inaccurate & ineffectively used, which is very time consuming for businesses); import tax and VAT are unclear & duplicated; entry for 3 digits of the declared weight is not allowed & places of figures in USD is not suitable with international standards; declaration only allowed after 24 hours of adjustment of tax enforcement is unreasonable. The declaration form is difficult to see & its layout looks confusing, which makes it very easy to do wrong; the section of code of reference legal documents & digital signatures is complicated for the shipments that have many goods items. There are many problems in using the customs declaration software: When declaration errors happened, businesses asked for help from customs agency that forwarded the question to the Thai Son software company. But when the businesses reached Thai Son, this company said they only provided terminal softwares, not customs management softwares. Businesses were very unhappy with this problem. Customs information technology infrastructure has some limitations yet: The infrastructure of information technology is not synchronized with slow traffic and constantly jammed network and errors; which results in slow updates on tax payment of businesses, sometimes for 2 – 3 days; the 3G internet is not available at remote border gates, which is very difficult for businesses to open or revise declarations...The lookup of tax debt on the Portal of General Department of Customs may cause the risk of disclosing information of businesses. It is recommended to provide a single user and password (not log in using indentity card and tax code). In case of forgetting password, re-registration is required and password will be sent to the email that is registered before. Spirit of service, professional competence of customs officers: Some customs officials still harass and cause troubles for businesses in the process of implementing customs administrative procedures; some customs officers are assessed as “weak at professional competence” and “limited legal knowledge about using HS code of goods in specialized technical areas”,“inconsistent in implementation”,“low technical capability”, “limited knowledge of regulations and documents”, “different explanation by different customs officers”, “provide verbal guidance only”, “refuse to sign on professional form to avoidhaving to take responsibility”; some customs officers are “not polite”,“not enthusiastic or cooperative” in their support for businesses, or sometimes“indifferent, insensitive” to the difficulties and loss of businesses, “undemocratic” and “harrassing” businesses. 5. Problems concerning specialized management of imports and exports Currently, there are too many documents issued by ministries and agencies concerning specialized management of export and import goods. Many provisions are unclear with constant changes; the validity of newly issued documents is too short which makes it difficult for businesses

Page 5 of 12

to fully update. The contents of some regulations are incomplete and confusing to businesses (e.g. Decision No. 11 039/QD-BCT of the Ministry of Industry and Trade stipulates that the import of relays is subject to examination and energy stamping but does not specify which agencies or organizations are in charge of this, the businesses therefore don‟t know where to go to for following this procedure....).The contents of regulations on categories of goods subject to specialized examination is fragmented, unclear and difficult to find, resulting in different understanding and explainations between customs authorities and businesses, or amongst different State management agencies, for instance the regulation concerning the weight of container trucks, tractors, etc. Regulations of specialized management and examination are overlapping: One item is subject to both product certification and examination of each individual import shipment. The same product item is, all the time, subject to application for permits, quality check. Too many licenses/permits are required and repeated for many times. Scope of specialized examination is too wide and unncessary in many cases: For instance, it is required to do specialized examination for the products imported, packed with other products and exported (e.g. the sauce bags are imported, and then packed with locally produced prozen potato products and later exported); examination, performance and energy stamping are required for specialized equipment and materials of mineral & coal industry which have special high technical and safety requirements and are under management by specialized agencies; quality check is required for materials, equipment....imported in service of processing contract of ship building for export); the same thing happens to the export of fertilizers; forest service procedures are required for the export of cinnamon oil and quality check is even required for the goods that already go through international inspection... Specialized inspection time is too long, for example, quality check of steel as defined in Circular 44 / TTLT BCT-BKHCN dated 31/12/2013 lasts 2-4 weeks; time for quality check of seed corn is 7 – 10 days long; time for examination and certification of food safety by health agencies is too long, which results in failure to ensure the deadline of submission to the customs within 30 days. It takes about 15 days to get the permit from the Telecom Bureau for electronic equipment...Specialized inspection results amongst different agencies and units are not consistent. This agency says yes while another says no to the same results. Documents are not conforming to reality, for example, the list of machinery, equipment, raw materials that can be domestically produced stipulated in Circular 04/2012 /TT-BKH dated 08/13/2012: The list is not concrete, too general and contains many items which either can not be produced domestically or can be produced but o do not meet the quality requirements for high-tech manufacturing sectors (eg in the oil and gas field). Lack of coordination and information sharing amongst agencies: This results in the fact that businesses, for many times, have to provide the same information and documents to many agencies. For instance, many paper works have been reduced and cut thanks to the electronic customs system but this is not synchronized and recognized by other relevant agencies, like banks and tax authorities. Some papers are, therefore, not provided by the customs service but still required by banks or tax authorities.

Page 6 of 12

Recommendation: The customs authorities should share information and data via the network with specialized management and inspection agencies to reduce the burden of paperwork, time and costs for businesses. It is recommended to remove the requirement of state quality check for those goods that already go through international registration inspection. Before the issuance of any regulations, reality check should be done; application of any new regulations should be announced on the media at least 3 – 6 months before their effective date to avoid damages and losses to businesses. The quarantine certification of imports – exports is currently causing troubles for businesses. For the exports since 1/1/2015, it is required by the phytosanitary agency that the exports including agricultural products, forest products such as cashew nuts, cassava, wood chips, coffee ... must be subject to phytosanitary certification before being exported, even where it is not required by the foreign side. This results in increase in customs clearance time and costs (including quarantine cost, storage cost, cost of ship missing, labor cost,..) for businesses. Time of quarantine check is too long (it was reported by some businesses as 15 days); quarantine check cost is unreasonable (phytosanitary control additionally charged for businesses is 14,000vnd/ton for export starch); duplication check are done by agencies, causing difficulties for businesses; colostrum powder milkis subject to both animal quarantine (implemented by animal health agency) and food safety control (health agency). Many requirements by state agencies are impossible for businesses to comply with, for instance: pressed wood pallets are not subject to quarantine control and fumigation under the international convention (ISPM15), so businssess can not acquire the deed from suppliers but businsses are still required to submit this document to the quarantine agency under the Circular Circular 30/2014/TT-BNN; the quarantine agency also require certification of plant origin for the goods that are stuffed or packed with wooden materials.... Recommendation: It is recommended by many businesses to remove the requirement of export quarantine in the case where it is not required by foreign buyers in the exporting countries. In considering this deregulation, it is proposed to allow businesses to submit the quarantine certificate after the goods have been cleared/ or after the ship has departed in order to avoid ship missing ( especially onSaturdays, Sundays and holidays) Declaration of chemical substances: it was reported by many businesses that many products that are regular exports have to be subject to declaration all the time. One cheminal substance having many different colors is required by the customs agencies to acquire separate certification for each individual color. Currently, only Bureau of Cheminal Substance is allowed to grant certification, which is not convenient to businesses. It takes too long time to receive results (5- 10 days, or even 3 – 4 weeks in case of errors); the requirement of having to acquire certification before customs clearance is troublesome to businesses, especially for import shipments from near markets (E.g import from Thailand, shipment takes 3 days only and businesses, therefore, can‟t acquire certification before customs clearance); certification often has mistakes regarding product name or invoice number...); Recommendation: it is recommended by businesses to annul the procedure of declaration of chemical substances, arguing that the objectives of this procedure is unclear and increases costs (official fees, storage costs, informal charges)for businesses; allow submission of

Page 7 of 12

certification within 15 days after clearance of goods; apply electronic declarationand certificationto better facilitate the compliance with this procedure. In summary, the survey result of business perception in 2015 revealed that the Customs Service has worked out many solutions to reform administrative procedures in order to facilitate import-export operations - contributing to the economic development. Electronic customs procedures are implemented but because its effectiveness is related to the management responsibility of many ministries and agencies, the declaration system remains complex and unsynchronized. The ministries and the Customs Service should improve coordination efficiency, creating more favorable conditions for businesses in import and export activities. At the same time, the Customs Service also need to strengthen professional training, improve behaving culture for public servants so as for the system to operate more efficiently.

II. RECOMMENDATIONS FOR TAX REFORM The Vietnam Chamber of Commerce and Industry (VCCI) in coordination with the Prime Minister‟s Advisory Council of Administrative Procedures Reform, the World Bank‟s International Finance Corporation and the General Department of Taxation have conducted the survey on “Evaluation of tax administration reform: Businesses‟ satisfaction levels in 2014”. There were 2,542 responses received from businesses for the survey carried out on national scale for the first time on this tax field. This paper documents a summary of recommendations by businesses as a result of the mentioned above survey. Dramatic changes can be seen in tax policy and legislation as to implement the Government‟s Resolution No.19 on improving business environment and enhancing national competitiveness since mid-2014. This has been demonstrated by the issuance of a series of documents including Circular No. 119/2014 / TT-BTC dated 08/25/2014 of the Ministry of Finance amending and supplementing 07 circulars on taxes; Decree No. 91/2014 / ND-CP dated 01 / 10/2014 amending and supplementing 04 decrees on taxes, Circular No. 151/2014 / TT-BTC dated 10/10/2014 guiding the implementation of Decree No. 91/2014 / ND-CP, Law No. 71 / 2014 / QH13 amending and supplementing a number of articles of the Laws on taxes (05 Laws), Decree No. 12/2015 / ND-CP dated 12/02/2015 of the Government detailing the implementation of the Law amending and supplementing some articles of the Laws on tax and amending and supplementing some articles of the decrees on taxes..Etc. These tax reform efforts have promoted the positive impacts to the business community. A series of important changes including the deregulation of control for the cost of advertising and promotion ... of businesses, the deregulation of having to submit a list of invoices of goods and services sold or purchased when filing dossiers of corporate income tax, the extension of subjects eligible for quarterly declaration of VAT, the deregulation of the businesses having to adjust input VAT when they cannot acquire payment documents from bank on the due date, the revision of regulations to allow businesses to pay tax by quarter, and settle by year-end ... are working well in practice and contributing to dealing with difficulties, promoting investment, production and business for businesses. The application of electronic tax declaration and payment has helped reduce time and costs for businesses. However, businesses still have expected the tax service to continue its efforts for further reform. The tax policy and legislation should be developed in a transparent, clear, and easy to

Page 8 of 12

implement fashion. It is needed to enhance the effectiveness of information dissemination to support businesses to timely update on new tax policies. The tax refund for businesses is to be conducted more quickly. The tax sector should enhance IT applications, but need to ensure stability in the use of declaration software by businesses. Besides, it is necessary to create the interconnection between the tax authority and other state agencies concerned, and enhance transparency in the work of inspection and examination of businesses and improve the quality of tax cadres and civil servants. 1. Developing tax policies and legislation in a transparent, clear and easy for

implementation Many businesses reported on the situation of many tax laws being unlikely to be directly applied in practice. Very often, it requires the issuance of too many circulars, dispatches, guidelines for the tax laws to be implemented. This makes the tax legislation system way too complex, easy to be interpreted in different ways, making it difficult for businesses to comply with as a result. It was said by many businesses that some tax laws are currently unclear, difficult to apply, lacking of consistency between businesses and tax authorities, and between tax authorities and other agencies concerned, or even within the tax service department itself. For example, a number of provisions relating to the determination of the reasonable expenses to be deducted when calculating corporate income tax are not clear, and not suitable with the businesses‟ requirements of being vibrant and competitive. Similarly, provisions concerning the time of issuing invoices is not consistent with the business practices. The regulation on the abbreviated names and addresses on the bill has not yet been clearly defined. This might causes lots of troubles because many businesses or consumers have very long names and addresses, even there is insufficient room to print the bills with the smallest font size words, and the handwriting if used often has errors. It is needed to have a specific list of words to be abbreviated, even truncated and if a tax code or an industry code is available, these codes should be used while other information doesn‟t matter much. Regulations related to the personal income tax are yet less favorable. Personal income tax should only be settled for cases where arising payable tax, there is no need to declare or settle for the cases where no taxes are payable. Recommendation: The tax policies and legislation need to be developed in a transparent, clear and easy to implement fashion as well as to be highly stable and predictable. The guidelines need to be concrete, with examples being provided and easy for businesses to grasp. After a new document is issued to amend, revise, supplement or repeal the old regulations, it should be codified into a system so that businesses just need to simply refer to the final text to comply with and don‟t have to go through a series of previously issued versions. 2. Strengthening communication, information support for businesses concerning new tax

policies and legislation Relatively quick changes in tax policies and procedures are making it difficult for businesses to effectively grasp information and comply with those regulations. Although many changes are needed which tend to facilitate the businesses, but these amendments, if codified and timely updated to businesses, will help businesses to capture new documents and comply with in an easier way.

Page 9 of 12

Many reported that the tax information was slow and difficult to access. Some modes of information dissemination were yet less effective, for instance, dispatches and documents sent by some tax departments by post to the businesses are often delayed, or not in time. Training courses are still organized by the tax service concerning the new issuance of tax circulars, decrees, and policies new, but some businesses do not receive any notifications and information about those courses. Many businesses update themselves through the sites and notifications from consulting firms, saying that they rarely get updated by the tax authorities.

Recommendation: The tax authorities at all levels need to innovate in their activities of communicating, propagating and updating on new tax policies for businesses. Tax agencies should schedule training sessions to make it convenient for businesses to fully participate without affecting their production and business activities. The local tax departments should be more positive, more proactive to timely update businesses on changes in tax policies and legislation. It is suggested to notify businesses via email on the issuance of new tax policies and legal documents. Before the tax policies and legislation take effect, it is necessary to timely notify tax payers so that they are aware of and find it easier to comply with. 3. Speeding up the tax refund to businesses Many businesses reported on slow receipt of tax refund. The settlement of tax documents can be fast but businesses have to wait for many months before they can actually receive the refund money. According to regulations, the tax refund period is within 12 months and even under the new regulations, the refund can be even made on monthly or quarterly basis for the export businesses whose to be deducted VAT is of up to 300 million dong, the enforcement in fact remains troublesome for businesses due to long waiting time. This does not correspond with the fact that businesses are to be immediately fined if they make late payment of taxes. Recommendation: The tax refund to businesses should be made quickly, to solve problems and create the favorable conditions for businesses. 4. Implementing inter-connection between the tax authorities and relevant state agencies As it was reflected by many businesses, business related administrative procedures implemented by the relevant government agencies are not connected effectively. Data between tax departments, tax branches and department of planning and investment remain unsynchronized and businesses, therefore, have to prepare many declaration forms and provide a same kind of information for many different state agencies while these agencies may share the same database with each other. The relevant authorities (such as investors, State Treasuries at all levels ...) are responsible for issuing payment receipts to the taxpayers and notify directly the tax authorities. The amount paid by businesses at the treasuries are not fully updated to tax authorities but the businesses must provide documents to prove them having paid. There are some cases where businesses already paid taxes but it is still reported on the system of tax authorities as tax debts, affecting the interests and reputation of the businesses. Recommendation: It needs to be inter-connected and timely shared the information amongst tax authorities, and between tax authorities and other relevant agencies in the process of settling procedures for businesses.

Page 10 of 12

5. Simplifying the tax declaration forms Many businesses rated tax declaration forms as complicated and cumbersome with some duplicate information and unnecessary indicators. The forms use many jargons which are difficult to understand for businesses, while they do not receive timely instructions from the tax authorities. Some forms are constantly changed along with the changes of circulars despite negligible changes in the contents of these forms, which is unnecessary and causes troubles for businesses, making them to spend more time on studying and updating on these changes while more mistakes may occur also. Recommendation: It is recommended that tax authorities develop simpler, easier to understand forms and remove unnecessary indicators, especially should limit constant changes in the forms. It is not necessary to issue a new form if the old form is still usable under the new regulations. Illustration examples and attached forms should be provided available on the website of tax authorities concerning each individual problem. A tax officer with good professional competence should be assigned to work as a telephonist to provide necessary guidance to businesses. Workshops should frequently be organized to update businesses on new tax policies and answer their questions and complaints concerning tax related issues. Additionally, online tax declaration should be employed as a measure to minimize errors and misunderstanding about the forms. The form templates should be provided with consistent guidance for businesses to avoid unnecessary confusion 6. Implementing consistently tax procedures There currently exists inconsistency regarding the sequences and procedures of handling work amongst departments in some local tax authorities, as well as between the tax authorities and other relevant agencies. This is the main reason leading to different guidance provided to businesses, causing difficulties in the process of implementing corporate tax obligations. For example, there is no consistency between the customs authorities and the tax authorities in dealing with the amount of tax payable for the imports or inconsistency between the tax authorities and the banks concerning electronic tax payment, etc. Recommendation: It is necessary to better define the sequences and procedures of handling work between higher and subordinate tax authorities, and between tax authorities and relevant authorities. Also, it is needed to anticipate possible conflicts once applicable and provide redress mechanism. 7. Performing inspection activities in a transparent manner Tax inspections remain a burden for many businesses. According to some businesses, prolonged tax examinations and inspections are troublesome and costly for them. It was reported that before tax inspections were conducted once every two years on average but now tend to be done once a year. It was also said that tax related inspections are carried out so frequently but repeated, which is time consuming for businesses. Currently, too many different state agencies are authorized to carry out tax related inspections. Tax authorities do not timely notify and provide adequate guidance to businesses while they impose rigid administrative sanctions when inspecting businesses. Many businesses said that their objectives are to do business, create jobs and make profit which later is contributed to state budget. Therefore, the State management agencies that perform inspections/examinations should focus on supervising and reminding and creating favorable conditions for businesses.

Page 11 of 12

Recommendation: It is recommended by businesses to develop a clearer and more transparent inspection process. The selection of sample for inspection should be done scientifically to avoid that some same businesses are inspected for too many times. Also, time for inspection visits should be shortened to avoid affecting business activities

8. Applying a stable tax declaration software The tax declaration software is assessed to have many advantages but the support for using this software have not met the needs of businesses. Despite continuous upgrades, the software still fails to facilitate the data export from the accounting software of businesses to the tax declaration support software (for example, the data of revenue can be well exported from the accounting software to VAT declaration software, but as for the declaration of special consumption tax, the data fail to be exported or it takes lots of time and has to go through many steps as the software does not support automatic export to the declaration form but requires manual inputting…) Many businesses also said that the tax declaration software still incurred errors, the old data is often lost when new version is updated. Barcodes for submitting a tax declaration can‟t be scanned from time to time. In addition, the software has not been updated as much as to keep up with the changes of forms issued along with the guiding circulars of the Ministry of Finance, many forms are yet missing and paper versions are listed instead . This leads to incorrect declarations, and often it is late after it is revised. Some businesses said they were even fined because of this situation. The declaration support program yet lacks many items, so online declaration is impossible, for example, there are items for financial statement, documents for personal income tax withholding, or fee forms... Therefore, besides online declaration, businesses still have to directly submit some reports. It can be said that despite changes, nothing much is done to actually help save time and cost for businesses and tax authorities. There is no delivery confirmation on the software, so businesses are easily prone to violation of time limit whether they submit on time or not. Recommendation: The tax service is recommended to first focus on accounting operations to be really complete and stable before any application of information technology to facilitate businesses. Many businesses suggested that it is needed to improve the software to better support businesses to declare more easily and add to the software the forms that are to be filled regularly by businesses. Whenever one new regulation is issued, relevant support should be updated on the software. And when the software is upgraded, it is necessary to notify businesses so that they know how to declare correctly and avoid having to declare again and again. It is also proposed by most businesses to upgrade transmission lines to ensure quick and smooth declaration. The declaration software should supplement and upgrade forms and mode of online submission of reports instead of businesses having to make submissions directly at the tax offices. In the meanwhile, submission of report should be allowed via email with registered addresses and digital signature. The software also needs to be upgraded to be compatible with different browser types to better enable the declaration. In addition, the deadline for declaration should be extended and fine on late submission can be imposed later accordingly.

Page 12 of 12

9. Regarding civil servants The quality of tax officers is assessed as the critical factor determining the quality of tax administrative procedures. Therefore, the tax service should prioritize recruitment of competent and virtuous employees. It is necessary to regularly provide training for capacity building for tax officers in order to have a strong and competent staff. This service is easily prone to the abuse of power, strict sanctions against acts of harassment of taxpayers should, therefore, be imposed.

Page 1 of 2

American Chamber of Commerce in Vietnam

AMCHAM STATEMENT

Annual Vietnam Business Forum Hanoi, December 1, 2015

Presented by

Ms. Sherry Boger Chairwoman, AmCham Vietnam

Prime Minister and Ministers, Business leaders Distinguished Delegates Ladies and Gentlemen 1. This is a key moment for Vietnam, the beginning of a new era with the XII Party

Congress early next year and leaders for 2016-2020. 2. Vietnam has succeeded at attracting FDI and increasing trade. U.S. - Vietnam trade in

2015 will likely reach over $45 billion, another annual increase of over 20%. 3. The TPP is a promise, not yet a reality. It covers many issues we have discussed for

years at VBF. It offers a framework and focus for efforts in 2016. Regulatory Coherence, Transparency and Meaningful Public Comment (TPP Chapter 25) is an essential first step to implement Vietnam’s commitments for public comment on proposed administrative regulations from citizens and businesses that would be affected.1 Education, a key development driver (TPP Chapter 23). We need work-ready graduates, science and technology, research, and innovation. AmCham companies are involved in a number of education projects. We encourage the government to lead a large-scale transformation to scale HEEAP 3.0 nation-wide, supported by both Vietnamese and FDI business associations and companies. Very few Vietnam enterprises are part of global supply chains. Although Vietnam has attracted FDIwith significant export growth,more than two-thirds of Vietnam’s exports are from FDI factories; and imported materials and components account for 90% of the export value. AmCham companies, together with VCCI and other business associations, are cooperating in supplier development so that Vietnam companies will qualify to join global supply chains. Efficient Customs Administration and Trade Facilitation (TPP Chapter 5) is essential for

1This was a key point in the Prime Minister’s New Year Message on Jan 1, 2014"… interaction

between State agencies, between the State apparatus and socio-political organizations … .Dialogues with the people and businesses …to promote closer relationships between the State, cadres, civil servants and the people and better match policy and legislation with reality." From the Prime Minister’s New Year Message, January 1, 2014.

Page 2 of 2

Vietnam enterprises to join global supply chains. We have established a “Vietnam Trade Facilitation Alliance,” (VTFA), in cooperation with VCCI and leading export industry associations, to provide technical assistance to build capacity for Vietnam Customs to implement TFA commitments. 4. We highlight two “concrete targets” from the many issues covered in our written

statement. Technical Barriers to Trade – a specific example – Vietnam’s restrictions on imports of Used Machinery and Equipment (TPP Chapter 7) Circular 23/2015, issued on Nov 13, 2015, with entry into effect on July 1, 2016(to replace Circular 20/2014) is universally opposed by FDI and domestic business associations. It would cause delays in customs processing, have a negative impact on modernization and industrialization, especially of supplier industries, discriminates against domestic industries, and is not in accordance with Article 2.2 of the WTO Technical Barriers to Trade Agreement or the TPP Chapter on TBT.

We raised this issue in many consultations and at the June VBF. We againrequest that restrictions on imports of machinery and equipment based on any arbitrary time standard be removed, administrative procedures to ensure compliance with international standards of safety, energy savings and environmental requirements be simplified and incorporated into the National Single Window project, and any quality standards be based on international standards. Visas: Temporary Entry for Business Persons (TPP Chapter 12) Vietnam’s revised Immigration Law became effective on January 1, 2015. According to some provisions, U.S. citizens will receive Vietnam visas that have a three-month validity, and a single entry, while Vietnamese citizens receive U.S. visas with multiple-entry, one year validity.

We raised this issue at the June 2015 VBF and heard in July that U.S. citizens would receive one-year validity, multiple-entry visas, but we have not yet seen any. We hope that this issue will be resolved soon. 5. Conclusion We appreciate the guidance in the Prime Minister’s 2014 New Year’s Message, in Resolutions 19/2014 and 19/2015 and this opportunity for "… interaction between State agencies, between the State apparatus and socio-political organizations … .Dialogues with the people and businesses … to promote closer relationships between the State, cadres, civil servants and the people and better match policy and legislation with reality." I wish participants good health, happiness and success. Thank you.

Page 1 of 10

American Chamber of Commerce in Vietnam (“AmCham”)

AMCHAM STATEMENT

Annual Vietnam Business Forum Hanoi, December 1, 2015

Presented by Ms. Sherry Boger

Chairwoman

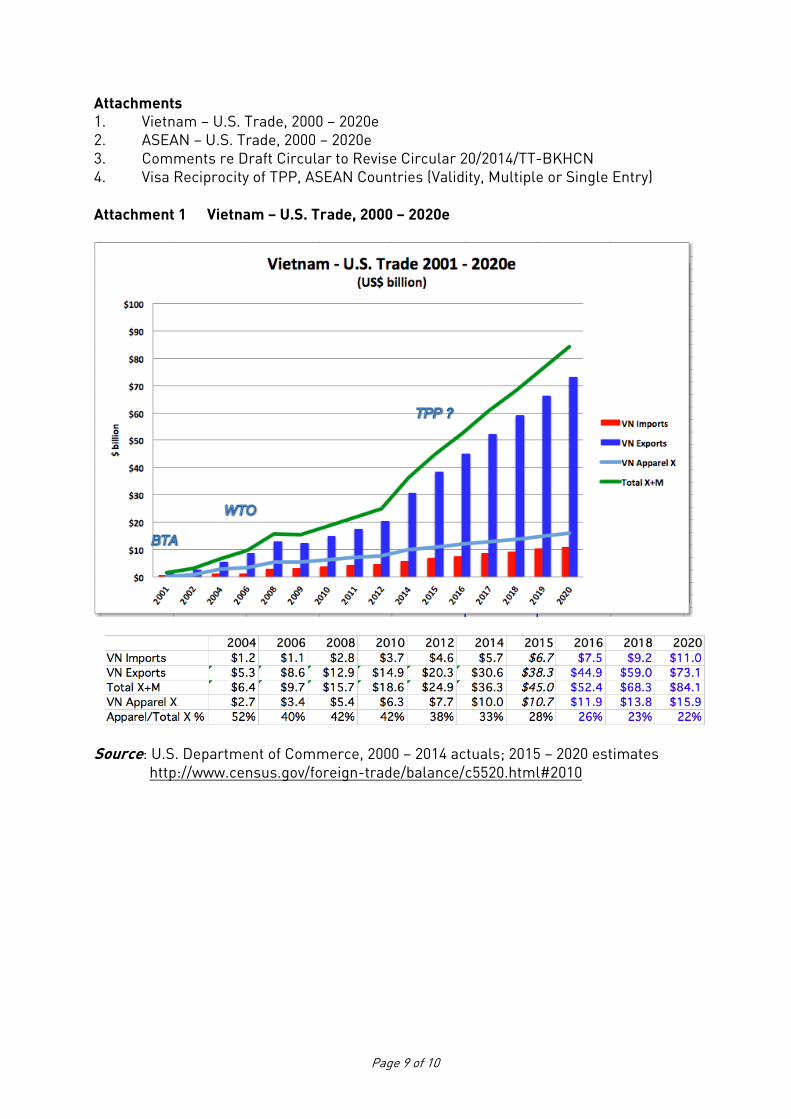

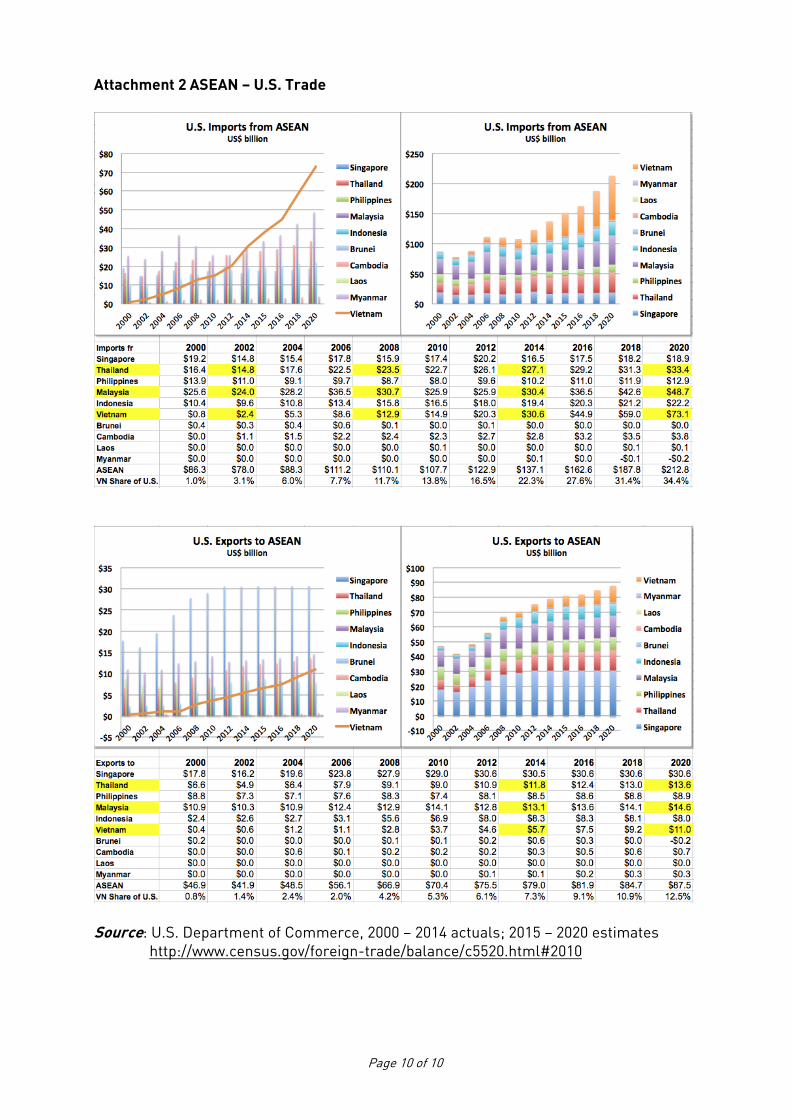

Prime Minister and Ministers, Business leaders Distinguished Delegates Ladies and Gentlemen I am pleased to participate in this important VBF Meeting. 2015-2016: A WATERSHED MOMENT IN TIME We are now at the end of a very meaningful year, and the beginning of a new moment for Vietnam. In April this year, Vietnam celebrated the 40th Anniversary of peace. In August, we celebrated the 70th Anniversary of Vietnam’s National Foundation Day. This year also marked the 20th Anniversary of the normalization of relations between Vietnam and the United States, and the 15th Anniversary of the Vietnam-U.S. Bilateral Trade Agreement. We are half way through the Social Economic Development Strategy 2011-2020, where the objective was to move from a low-income, agricultural country to a middle-income, industrialized country by 2020, based on modernization, industrialization, and integration into the international economy. In October, Vietnam joined other TPP countries in reaching agreement on a 21st Century agreement that will help achieve that objective. And early next year, Vietnam will convene its XII Party Congress to elect leadership for the coming five years, and to plan specific programs and activities to achieve the 2020 objective of becoming a middle-income, industrialized country. We share Vietnam’s vision for 2020: a middle-income, industrialized country, a thriving commercial environment with efficient trade and robust local and foreign investment, a coherent regulatory environment that is efficient, transparent, logical, predictable, and consistent; where investors, business persons and tourists can enter Vietnam with minimum cost or inconvenience; where legitimate businesses local and foreign, can quickly establish a business; hire and develop talented staff at a fair and competitive wage; quickly, easily and confidently determine customs and tax liabilities; and where supply chains are speedy, reliable, and cost effective. VIETNAM HAS SUCCEEDED AT INTEGRATION INTO THE INTERNATIONAL ECONOMY First, Vietnam has been extremely successful in international economic integration in general and with the United States in particular. This year, total trade between our two countries is likely to increase again by more than 20% and reach $45 billion, and could exceed $80 billion by 2020 if present trends continue, and even more with TPP. Moreover,

Page 2 of 10

Vietnam has increased its standing as the leading ASEAN country supplier to the United States: Vietnam’s share was 22%, and could exceed 30% by 2020, if present trends continue. On the other hand, Vietnam is the lowest-ranked of the ASEAN - 6 countries for imports from the U.S., at about $6.7 billion in 2015. This figure could certainly be increased by improving Vietnam’s business environment for exporters from the U.S. and other countries, and importers in Vietnam and their distributors. At the same time, revenues of AmCham companies and their partners in Vietnam’s domestic market continued to grow, and a number of AmCham companies have increased their FDI in Vietnam. Business and Government leaders are increasingly aware of the growing importance of the Asia Pacific Region and the associated benefits of TPP. Global middle-class spending is projected to increase from $21.3 trillion in 2009 to $55.7 trillion in 2030. Asia’s share should increase from 23% in 2009 to 59% in 2030. TRANSPACIFIC PARTNERSHIP A PROMISE, NOT YET A REALITY Vietnam could be the largest beneficiary from the TPP in relative terms. Some experts predict that Vietnam’s exports will increase by 28.4% with TPP. The expected export “baseline” in 2025 without TPP of $239.0 billion could grow to $307 billion. In addition, the expected GDP growth benefits are substantial. Vietnam’s GDP in 2025 could be 10.5% higher than the baseline estimate. After five years of negotiations, and nearly ten days of marathon negotiations in Atlanta, the TPP negotiations were concluded successfully on October 5, 2015. However, the TPP is still a promise, not yet a reality. Each TPP country has its own procedures for ratification, implementing legislation, and administrative actions, which will be difficult. The TPP covers many of the issues that we have discussed for years in the Vietnam Business Forum. It is a framework for action, and should be a focus in 2016. TRANSPARENCY AND MEANINGFUL PUBLIC COMMENT (TPP CHAPTER 25) Local and national Government agencies must improve their competitiveness and robustly implement streamlined procedures as Government service providers to businesses and citizens to help prepare for international economic integration. An essential first step is to implement Vietnam’s domestic and international commitments for public comment on proposed administrative regulations from citizens and businesses that would be affected. This is required by the Law on Promulgation of Legal Documents and Vietnam’s international commitments in the Bilateral Trade Agreement, the WTO Accession Agreement, etc. Laws and regulations must be reviewed by VCCI, the Fatherland Front, and several ministries, including Justice, Internal Affairs, Finance, and Foreign Affairs, which will assess whether the drafts are in accordance with prevailing regulations and international commitments. However, this requirement seems to be followed in very few cases.

Page 3 of 10

EDUCATION: (TPP CHAPTER 23) Education of work-ready graduates for industry is essential if Vietnam is to become a middle-income industrial country by 2020. And AmCham companies are pleased to be involved in a number of projects either leading or contributing to vocational, practical and curriculum modernization. Notably, the Higher Engineering Education Alliance Program (HEEAP) 2.0 is a public-private partnership over the period 2012-2016 with an estimated target investment from current and future industry, Government, and education partners of $40 million. Vietnamese engineering programs are being brought into compliance with requirements set by leading higher education accrediting organizations, specifically ABET (the Accreditation Board for Engineering Technology) and the CDIO™ INITIATIVE (Conceive, Design Implement, Operate), an innovative educational framework for producing the next generation of engineers. USAID will soon announce a new five-year program to support a strategic collaborative dialogue with industry and Vietnamese Government, by supporting an alliance of U.S. universities and businesses to develop a dynamic innovation ecosystem of students, faculty, industry and Government. The alliance will implement institutional policy change, student learning platforms, maker innovation spaces, faculty instructional innovation, and applied curricula in the areas of science, technology, engineering and math (STEM), providing students the work-ready competencies to invent-build-launch solutions and value for Vietnam’s social and economic viability. We encourage the Government to lead a large scale transformation to scale HEEAP in the period 2017-2021 with HEEAP 3.0 across the country, with support from Vietnam’s business associations and companies as well as FDI companies, to achieve internationally recognized accreditations, support basic and applied research, and develop a foundation for innovation and entrepreneurship. SUPPLY CHAIN AND INTERNATIONAL ECONOMIC INTEGRATION (TPP CHAPTER 22) Vietnam has been extremely successful in attracting FDI and benefitting from significant export growth from FDI factories, but Vietnam’s enterprises have had limited results in participating directly in that success. More than two-thirds of Vietnam’s exports are from FDI factories; and Vietnam’s main contribution to the FDI production/supply chains is low-skilled labor. The cost of imported materials and components is estimated to equal 90% of the value of Vietnam’s exports of manufactured goods. Last November, our Manufacturing Committee organized a supplier development day with the participation of a number of Vietnam companies. This year, our Manufacturing Committee and member companies will organize two days of supplier training and development. In addition, AmCham and VCCI will cooperate in orientation programs for Vietnamese enterprises in the food, apparel, footwear and furniture sectors to prepare them for a “Women Owned Business Supplier Development Conference” on behalf of a major U.S. retailer in HCM City in January. We would like to extend this program, in cooperation with the Ministry of Planning & Investment, VCCI, and other Vietnam business associations. CUSTOMS ADMINISTRATION AND TRADE FACILITATION (TPP CHAPTER 5) Complementing their WTO efforts to facilitate trade, the TPP Parties have agreed on rules to enhance trade facilitation, improve transparency in customs procedures, and ensure integrity in customs administration. We have established a “Vietnam Trade Facilitation Alliance” (“VTFA”) led by VCCI and

Page 4 of 10

AmCham, with the participation of leading export industry associations to facilitate regular Government-business consultations and help achieve the customs KPI in Resolutions 19/2014 and /2015. Supported by a grant from the USAID Governance for Inclusive Growth Program and contributions from business associations, part of the World Bank Trade Facilitation Support Program of technical assistance provided by the developed countries to the developing countries under Section II of the WTO Trade Facilitation Agreement, the VTFA is working to establish formal consultative relationships between the General Department of Vietnam Customs (“GDVC”), and other Government agencies involved in international trade, and business associations, as provided for by the WTO Trade Facilitation Agreement and by the WCO Revised Kyoto Convention, as well as the TPP and other Free Trade Agreements. The VTFA is intended to serve as a national coalition for business and trade stakeholders to provide regular consultations with GDVC and other ministries or agencies regulating international trade, through regularly scheduled formal monthly and quarterly public meetings. We look forward to close cooperation between business associations and customs agencies, to achieve the efficiencies and benefits expected from robust implementation of the Trade Facilitation Agreement commitments. FOOD SAFETY - SANITARY AND PHYTOSANITARY (SPS) MEASURES (TPP CHAPTER 6) In developing SPS rules, the TPP Parties have advanced their shared interest in ensuring transparent, non-discriminatory rules based on science, and reaffirmed their right to protect human, animal or plant life or health in their countries. The TPP builds on WTO SPS rules for identifying and managing risks in a manner that is no more trade restrictive than necessary. TPP Parties agree to allow the public to comment on proposed SPS measures to inform their decision-making, and to ensure traders understand the rules they will need to follow. In addition, TPP Parties commit to improve information exchange related to equivalency or regionalization requests and to promote systems-based audits to assess the effectiveness of regulatory controls of the exporting Party. In an effort to rapidly resolve SPS matters that emerge between them, they have agreed to establish a mechanism for consultations between Governments. We look forward to developing a public-private partnership to provide technical assistance to build capacity in this chapter, as well. TECHNICAL BARRIERS TO TRADE (“TBT”) (TPP CHAPTER 7) In developing TBT rules, the TPP Parties have agreed on transparent, non-discriminatory rules for developing technical regulations, standards and conformity assessment procedures, while preserving TPP Parties’ ability to fulfill legitimate objectives. They agree to cooperate to ensure that technical regulations and standards do not create unnecessary barriers to trade. TBT Specific Case: Imports of Used Equipment (proposed revised Circular 20) At meetings in both HCMC and Hanoi, businesses universally opposed the revised circular, which was intended to promote development of manufacturing industries by “encouraging imports of new machinery, equipment and production lines that are manufactured with the latest technology”. The draft is now in its ninth revision, as of August 18, 2015, but the comments and recommendations of businesses have not been taken into account

Page 5 of 10

sufficiently. The restrictions in the draft Circular are likely to have the opposite effect, and discourage manufacturing industries, because of coverage of long-term capital equipment, parts and accessories due to the broad scope of the Harmonized System customs classification codes involved. An extensive global trade in used manufacturing equipment has developed, particularly in capital-intensive industries, because it is often preferable for an investor to obtain high-quality used or remanufactured equipment, often moving equipment from one of their own existing factories in another country to Vietnam, rather than order new equipment with long delivery lead times and much higher cost. The Japanese Business Association of Vietnam has stated that “Japanese used machineries function properly even after having been used for half a century, and it is common to use them in Japan as well. As the used machinery import regulations could prevent the development of upstream/midstream industries, we would like the Government to ease the used machinery import regulations”.1 In addition to its negative impact on Vietnam’s modernization and industrialization, the proposed regulation is not in accordance with Article 2.2 of the WTO Agreement on Technical Barriers to Trade. The prohibition of imports of equipment and machinery older than 10 year-old involves application of a single arbitrary time standard to numerous classes and categories of machinery and production equipment. This time standard is not based upon available scientific and technical information with respect to the many different kinds of machinery and equipment, whose useful production lives and uses vary widely. We respectfully request that the restrictions on imports of machinery and equipment based on an arbitrary time standard be removed, administrative procedures to ensure compliance with international standards of safety, energy savings and environmental requirements be simplified and incorporated into the National Single Window project, and any quality standards be based on international standards. (See attachment 3 for details).

STATE OWNED ENTERPRISES (TPP CHAPTER 17) TPP Parties recognize the benefit of agreeing on a framework of rules on SOEs, where private sector and the state sector compete on a “level playing field” Vietnam’s 1992 Constitution was revised in 2013 and included change in the role of the State Sector. AmCham, along with many others, submitted a viewpoint with recommendations regarding the State Sector. In the revised constitution as approved by the National Assembly, Article 51, paragraph 2 stated, “All components/varieties of the economy are important parts of the nation’s economy. All owners of all components/varieties of the economy are equal, [and] cooperate and compete according to the law.” This is roughly congruent with AmCham’s recommendation to the National Assembly that “The final version of the Constitution would be improved through a provision that clearly states that private enterprises are entitled to treatment no less favorable than that accorded to SOEs under the law”. We hope for the rapid implementation of this principle.

1 International Conference Proceedings: Vietnam to be a New Processing and Manufacturing Center of the World after 2015, Oct 24, 2015.

Organized by the World Bank, the State Bank of Vietnam, and the Central Committee of the Fatherland Front of Vietnam, p 126.

Page 6 of 10

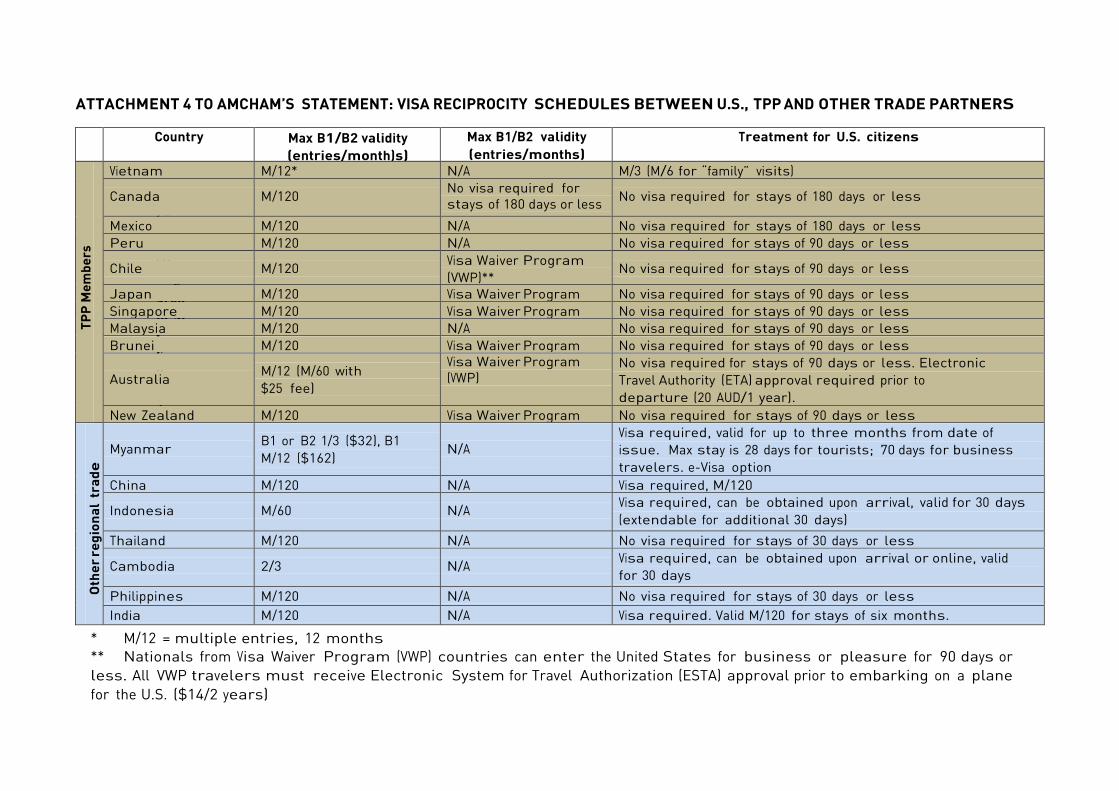

LABOUR (TPP CHAPTER 19) All TPP Parties are International Labour Organization (ILO) members and recognize the importance of promoting internationally recognized labour rights. TPP Parties have agreed to adopt and maintain in their laws and practices the fundamental labour rights as recognized in the ILO 1998 Declaration. Each of the 12 TPP Parties commits to ensure access to fair, equitable and transparent administrative and judicial proceedings and to provide effective remedies for violations of its labour laws. They also agree to public participation in implementation of the Labour chapter, including establishing mechanisms to obtain public input. The commitments in the chapter are subject to the dispute settlement procedures laid out in the Dispute Settlement chapter. The Labour chapter establishes a mechanism for cooperation on labour issues, including opportunities for stakeholder input in identifying areas of cooperation and participation, as appropriate and jointly agreed, in cooperative activities. AmCham cooperated closely with MOLISA, VCCI, and VGCL, supported by the ILO, in the Tri-partite Partnership to consult on revisions of the Labour Code during the years 2008 – 2012. We look forward to renewing our cooperation and developing a public-private partnership to provide technical assistance to meet the commitments in the TPP Labour Chapter, as well. TECHNICAL ASSISTANCE FOR DEVELOPMENT AND CAPACITY BUILDING (TPP CHAPTER 21) The TPP includes specific commitments on development and trade capacity building to ensure that all Parties are able to meet the commitments in the Agreement and take full advantage of its benefits. AmCham is already cooperating with VCCI and other leading Vietnamese business associations in the Vietnam Trade Facilitation Alliance to provide technical assistance to Vietnam Customs for capacity building under Section II, paragraph 9, to implement the commitments of the WTO Trade Facilitation Agreement, and we are ready to cooperate on TPP commitments as well, including food safety and labour. VISAS: TEMPORARY ENTRY FOR BUSINESS PERSONS (TPP CHAPTER 12) Almost all TPP Parties have made commitments on access for each other’s business persons, which are in country-specific annexes. However, Vietnam’s Immigration Law was revised in June 2014 and became effective on January 1, 2015, without reference to the TPP. We think this change was a major step backwards. According to some provisions of the law, U.S. citizens that plan to visit Vietnam under the equivalent of a U.S. B-1 or B-2 visa will receive visas that have, at most, a three-month period of validity, and a single entry only. This development has already resulted in significant impediments to business and pleasure travel both ways between Vietnam and the U.S., and could reduce the large revenues that tourism generates, not to mention the negative impact on the planned development of tourism as one of the five priority industry clusters in Vietnam. We raised this same issue at the June 2015 Vietnam Business Forum and heard in July that U.S. citizens would receive one-year validity, multiple-entry visas, but we have not yet seen any. If the Government of Vietnam does not align its process with the multiple entry 12-month temporary business/tourism visa provided by the U.S. to Vietnamese citizens, then in the near future, based on reciprocity, U.S. visas for Vietnamese citizens that are temporary visitors could be reduced to match the one entry, 3-month visas currently provided to U.S.

Page 7 of 10

citizens. The U.S. Mission to Vietnam reports that the issue is currently in active discussion within the Government of Vietnam, and if recent Vietnam media reports are an indication, the hope is this issue will be resolved within the next few months. (See attachment 4). TAX We have raised with both the Ministry of Finance and the Ho Chi Minh City People’s Committee a particular situation where U.S. importers and their distributors are being disadvantaged by a requirement to pay Value Added Tax on imported goods twice. The tax authorities froze distributors’ bank accounts while the case was under appeal. This case has now been resolved satisfactorily, after more than two years of effort. There are a number of other cases involving tax issues that we will raise. INEFFICIENT CURRENCY CONTROLS, NOT IN ACCORDANCE WITH IMF ARTICLE VIII “The Government of Vietnam notified the International Monetary Fund (IMF) that it accepted the obligations of Article VIII, Sections 2, 3 and 4 of the IMF's Articles of Agreement, with effect from November 8, 2005”. “Under Article VIII, Sections 2, 3 and 4, IMF members undertake not to impose restrictions on the making of payments and transfers for current international transactions, and not to engage in, or permit any of their fiscal agencies to engage in, any discriminatory currency arrangement or multiple currency practice, except with IMF approval”. “By accepting the obligations of Article VIII, Sections 2 (Avoidance of restrictions on current payments), 3 (Avoidance of discriminatory currency practices) and 4 (Convertibility of foreign-held balances), Vietnam signals to the international community that it will pursue economic policies which will make restrictions on the making of payments and transfers for current international transactions unnecessary, and will contribute to a multilateral payments system free of restrictions”.2 However, Vietnam does not seem to follow the commitments. We realize there may be concerns about the stability of the financial system, but we do not hear of IMF approval when there are restrictions on making payments and transfers for current international transactions. When the market price of dollars exceeds the “band” of the official rate, there are simply no dollars to be purchased. Also, all fees and charges incurred on a foreign currency denominated transaction need to be detailed in a contract between the parties in order for the Vietnamese based party to secure the foreign currency to settle the transaction, even where these are global standard fees charged against a transaction of this nature.

In addition to the difficulties that importers and exporters face in acquiring dollars because of Vietnam’s inefficient foreign exchange controls, we note that the first factor to consider In making an Non-Market Economy - country determination under section 771(18)(A) of the U.S. Tariff Act of 1930, as amended, Section 771(18)(B) requires that the U.S. Department of Commerce “take into account the extent to which the currency of the foreign country is convertible into the currency of other countries”. INEFFICIENT FINANCIAL REGULATORY CONTROLS Accounting standards for business entities provide a framework for transparency, accountability, and efficiency of financial markets.

2 https://www.imf.org/external/np/sec/pr/2006/pr0602.htm and https://www.imf.org/external/pubs/ft/aa/#art8 Section 2. Avoidance of

restrictions on current payment no member shall, without the approval of the Fund, impose restrictions on the making of payments and transfers for current international transactions.

Page 8 of 10

In Vietnam, accounting standards are issued by the Ministry of Finance of Vietnam and are known as “Vietnam Accounting Standards” The Department of Accounting and Auditing Policy of the Ministry of Finance has formed the Vietnamese Accounting Standards Board (“VASB“) to develop and approve the standards. To date the Ministry of Finance has issued a number of VAS, plus additional mandatory implementation guidance known as “circulars”. The Ministry of Finance states that it takes International Financial Reporting Standards (“IFRS“) into account in developing VAS. However, the IASB web site states clearly that Vietnam has not yet adopted the IFRS or the IFRS for SMEs (Small and Medium Entities): “Some Vietnamese companies prepare IFRS financial statements for the purpose of reporting to foreign investors. However, those IFRS financial statements are supplementary financial statements published in addition to – not instead of – financial statements prepared using Vietnamese Accounting Standards (“VAS“). The VAS financial statements are the statutory and primary financial statements”.3 As a result, both foreign and domestic businesses are subject to additional record keeping requirements that add complexity, time and cost to their statutory reporting commitments. In addition, domestic Vietnamese businesses may be restricted in their access to foreign capital to support their growth and development. CORRUPTION We know the Government shares with us the concern that corruption has become corrosive and widespread in Vietnam and is dangerous to the economy and society as a whole. While there have been some actions from the Government, it is time to address corruption in a wider fashion by implementing systems well known to reduce the opportunities for illegal payments as well as incorporating a code similar to the U.S. Foreign Corrupt Practices Act (FCPA) or the UK’s Bribery Act. A significant step forward would be to take actions that greatly limit the use of cash payments and face-to-face transactions, and to increase the use of e-Commerce in Vietnam. CONCLUSION Once again, we express our appreciation for the guidance in the Prime Minister’s 2014 New Year’s Message, in Resolutions 19/2014 and /2015 and this opportunity for interaction between State agencies, between the State apparatus and socio-political organizations. Dialogues with the people and businesses to promote closer relationships between the State, cadres, civil servants and the people and better match policy and legislation with reality.4

We look forward to close cooperation and support through regular and meaningful Government - Business consultations at all levels of Government, with concrete targets to be achieved. We remain active in support for the TPP and the preparations in Vietnam needed to bring further success.

On behalf of all AmCham members,

I wish distinguished participants good health, happiness and success.

Thank you very much. 3 http://www.ifrs.org/Use-around-the-world/Documents/Jurisdiction-profiles/Vietnam-IFRS-Profile.pdf

4 “Strengthen interaction between the authorities in the state apparatus, and between the state apparatus and political - social organizations.

Expand the dialogue with citizens and businesses in various forms to help the State, officials and civil servants are more close, which makes guidelines, policies and legislation be more closely with reality”.

Page 9 of 10

Attachments 1. Vietnam – U.S. Trade, 2000 – 2020e 2. ASEAN – U.S. Trade, 2000 – 2020e 3. Comments re Draft Circular to Revise Circular 20/2014/TT-BKHCN 4. Visa Reciprocity of TPP, ASEAN Countries (Validity, Multiple or Single Entry) Attachment 1 Vietnam – U.S. Trade, 2000 – 2020e

Source: U.S. Department of Commerce, 2000 – 2014 actuals; 2015 – 2020 estimates http://www.census.gov/foreign-trade/balance/c5520.html#2010