Embed Size (px)

Citation preview

SIBERIAN COAL ENERGY COMPANY

Investor presentationJanuary 2017

Fuelling industryPowering the world

Disclaimer

This presentation has been prepared by SUEK Group (the “Company”). The information in this presentation is provided in a summary form and does not purport to be complete.

This presentation contains certain “forward-looking statements”. All statements, other than statements of historical fact, are forward-looking statements that involve risks and uncertainties. There can be no assurances that such statements will prove accurate and actual results and future events could differ materially from those anticipated in such statements. Such information contained herein represents management’s best judgement as of the date hereof based on information currently available. The Company does not assume the obligation to update any forward-looking statement.

This presentation does not constitute or form part of, and should not be construed as, an offer, invitation or recommendation with respect to any of the facilities of the Company, or an offer, invitation or recommendation to sell or issue, or the solicitation of an offer to buy or acquire, the facilities or any of the securities of the Company in any jurisdiction or an inducement to enter into any investment activity. No part of this presentation, nor the fact of its distribution, should form the basis of, or be relied upon in connection with, any contract or commitment or investment decision whatsoever.

The information and opinions contained in this presentation are provided as at the date of this presentation and are subject to change. This presentation contains information derived from public sources that have not been independently verified.

1

Content

2

CompanyOverview

OurStrategy

Key PerformanceHighlights

ProductionAssets

Logistics

KeyOperational Figures

CoalMarket Overview andOutlook

GlobalCash Cost Curve

SUEK Sales

KeyFinancial Figures

DebtSnapshot

CorporateGovernance

3

4

5

6

7

8

9

10

11-12

13

14

15

Contacts 16

29.2

30.1

37.5

38.7

40.4

44.4

46.9

55.0

71.7

110.3

51.9

Kideco

Rio Tinto

Banpu

Peabody

Adaro

Bumi

SUEK

Anglo American

BHP Billiton

Glencore

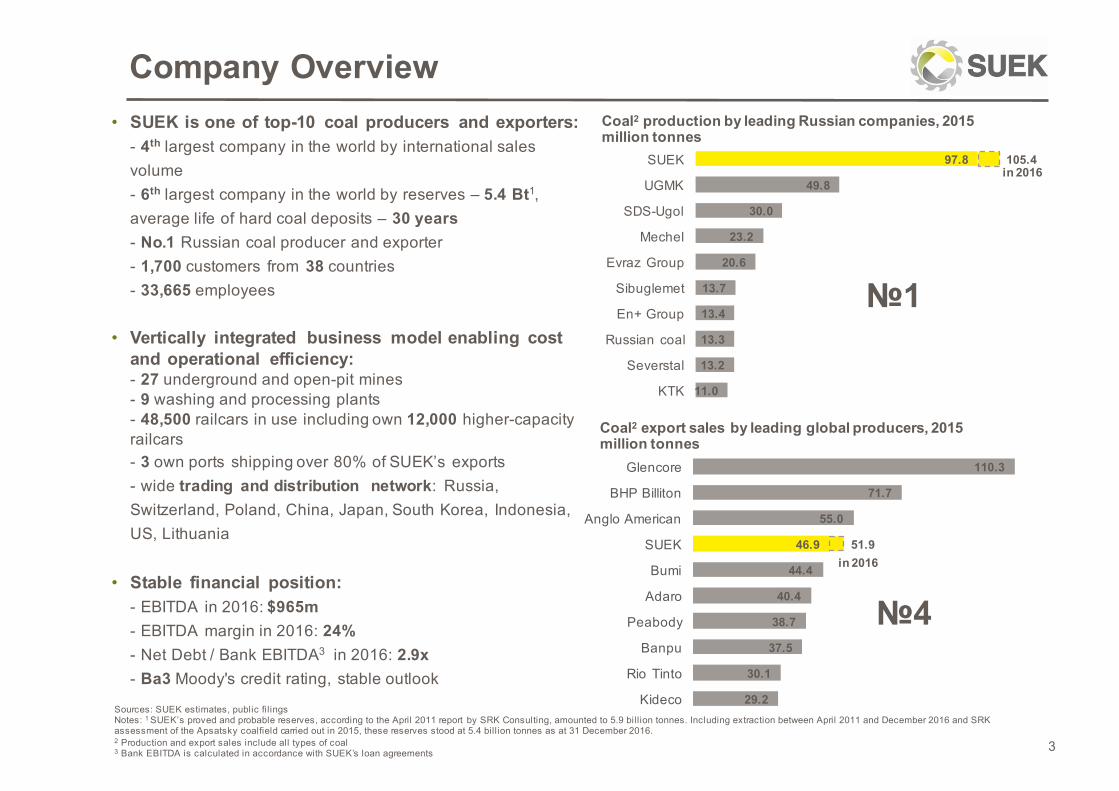

Company Overview

3

№1

№4

• SUEK is one of top-10 coal producers and exporters:- 4th largest company in the world by international sales volume- 6th largest company in the world by reserves – 5.4 Bt1, average life of hard coal deposits – 30 years - No.1 Russian coal producer and exporter- 1,700 customers from 38 countries- 33,665 employees

• Vertically integrated business model enabling cost and operational efficiency:- 27 underground and open-pit mines- 9 washing and processing plants- 48,500 railcars in use including own 12,000 higher-capacity railcars- 3 own ports shipping over 80% of SUEK’s exports- wide trading and distribution network: Russia, Switzerland, Poland, China, Japan, South Korea, Indonesia, US, Lithuania

• Stable financial position:- EBITDA in 2016: $965m- EBITDA margin in 2016: 24%- Net Debt / Bank EBITDA3 in 2016: 2.9x- Ba3 Moody's credit rating, stable outlook

Сoal2 production by leading Russian companies, 2015million tonnes

Coal2 export sales by leading global producers, 2015million tonnes

11.0

13.2

13.3

13.4

13.7

20.6

23.2

30.0

49.8

97.8 105.4

KTK

Severstal

Russian coal

En+ Group

Sibuglemet

Evraz Group

Mechel

SDS-Ugol

UGMK

SUEKin 2016

in 2016

Sources: SUEK estimates, public filingsNotes: 1 SUEK’s proved and probable reserves, according to the April 2011 report by SRK Consulting, amounted to 5.9 billion tonnes. Including extraction between April 2011 and December 2016 and SRK assessment of the Apsatsky coalfield carried out in 2015, these reserves stood at 5.4 billion tonnes as at 31 December 2016.2 Production and export sales include all types of coal3 Bank EBITDA is calculated in accordance with SUEK’s loan agreements

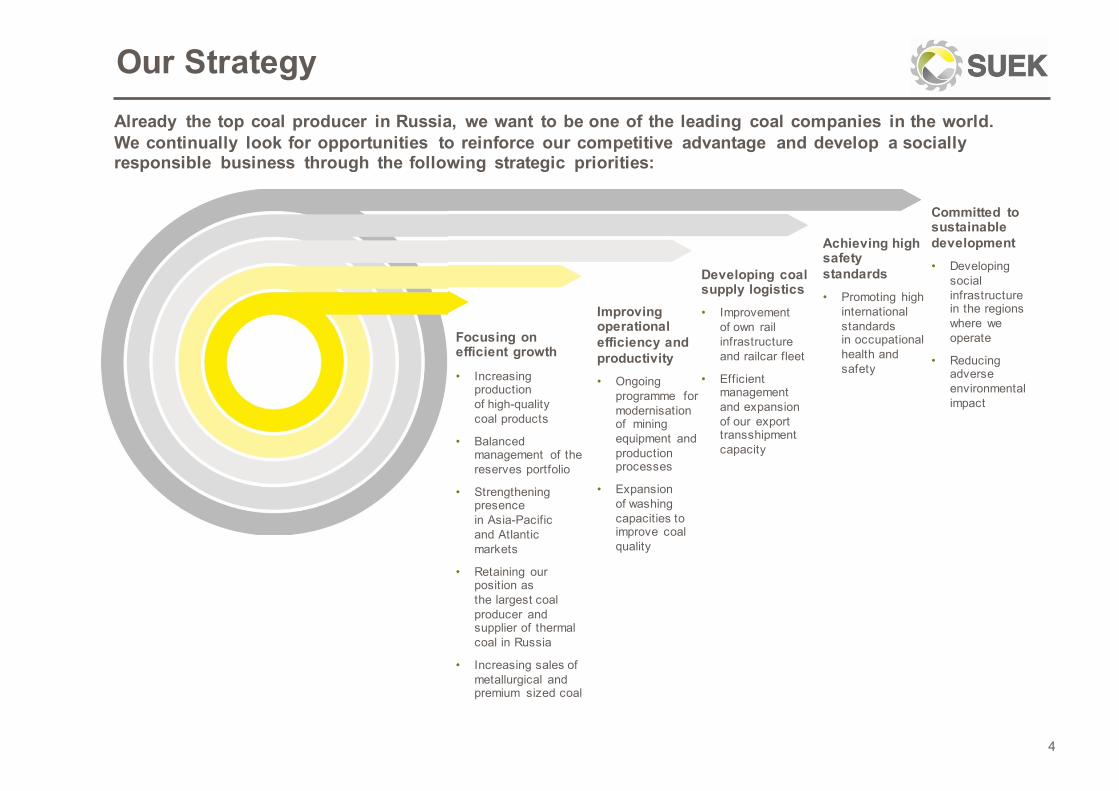

Our StrategyAlready the top coal producer in Russia, we want to be one of the leading coal companies in the world. We continually look for opportunities to reinforce our competitive advantage and develop a socially responsible business through the following strategic priorities:

4

Focusing on efficient growth

• Increasing production of high-quality coal products

• Balanced management of the reserves portfolio

• Strengthening presencein Asia-Pacificand Atlantic markets

• Retaining our position as the largest coal producer and supplier of thermal coal in Russia

• Increasing sales of metallurgical and premium sized coal

Committed to sustainable development • Developing

social infrastructure in the regions where we operate

• Reducing adverse environmental impact

Improving operational efficiency and productivity • Ongoing

programme for modernisationof mining equipment and production processes

• Expansion of washing capacities to improve coal quality

Developing coal supply logistics • Improvement

of own rail infrastructure and railcar fleet

• Efficient management and expansion of our export transshipment capacity

Achieving high safety standards • Promoting high

international standards in occupational health and safety

5

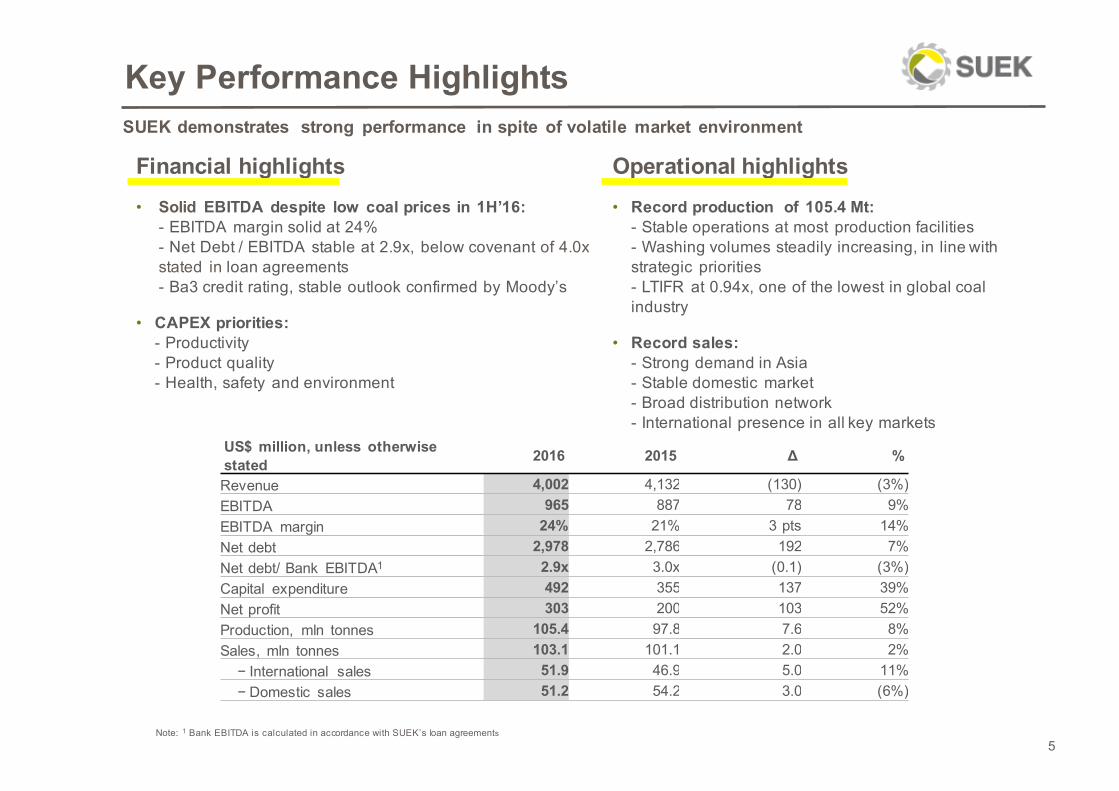

Financial highlights• Solid EBITDA despite low coal prices in 1H’16:

- EBITDA margin solid at 24%- Net Debt / EBITDA stable at 2.9x, below covenant of 4.0x stated in loan agreements- Ba3 credit rating, stable outlook confirmed by Moody’s

• CAPEX priorities:- Productivity- Product quality- Health, safety and environment

Key Performance Highlights

US$ million, unless otherwise stated 2016 2015 Δ %

Revenue 4,002 4,132 (130) (3%)EBITDA 965 887 78 9%EBITDA margin 24% 21% 3 pts 14%Net debt 2,978 2,786 192 7%Net debt/ Bank EBITDA1 2.9x 3.0x (0.1) (3%)Capital expenditure 492 355 137 39%Net profit 303 200 103 52%Production, mln tonnes 105.4 97.8 7.6 8%Sales, mln tonnes 103.1 101.1 2.0 2%

− International sales 51.9 46.9 5.0 11%− Domestic sales 51.2 54.2 3.0 (6%)

Operational highlights• Record production of 105.4 Mt:

- Stable operations at most production facilities- Washing volumes steadily increasing, in line with strategic priorities- LTIFR at 0.94x, one of the lowest in global coal industry

• Record sales:- Strong demand in Asia - Stable domestic market - Broad distribution network- International presence in all key markets

SUEK demonstrates strong performance in spite of volatile market environment

Note: 1 Bank EBITDA is calculated in accordance with SUEK’s loan agreements

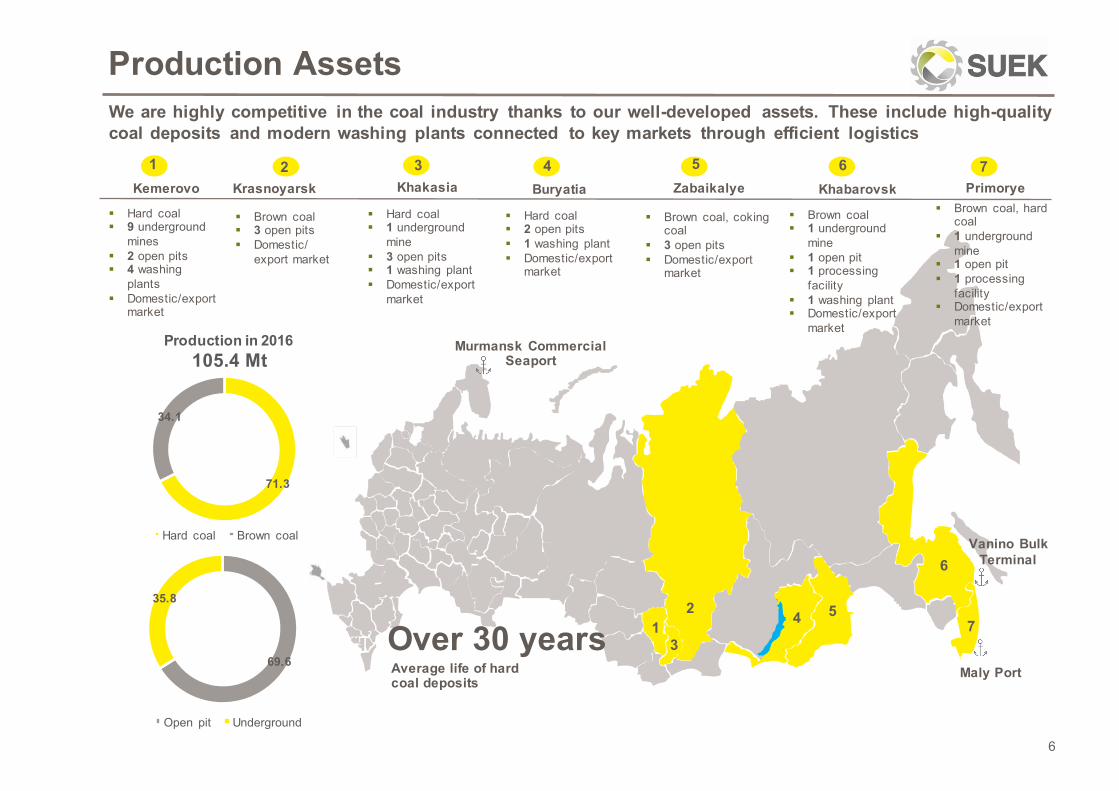

§ Brown coal§ 1 underground

mine§ 1 open pit§ 1 processing

facility§ 1 washing plant§ Domestic/export

market

1

Production Assets

6

§ Hard coal§ 9 underground

mines§ 2 open pits§ 4 washing

plants§ Domestic/export

market

Kemerovo

§ Brown coal§ 3 open pits§ Domestic/

export market

PrimoryeKhabarovskZabaikalyeKhakasiaKrasnoyarsk Buryatia

§ Hard coal§ 1 underground

mine§ 3 open pits§ 1 washing plant§ Domestic/export

market

§ Hard coal§ 2 open pits§ 1 washing plant§ Domestic/export

market

§ Brown coal, coking coal

§ 3 open pits § Domestic/export

market

Murmansk Commercial Seaport

Vanino BulkTerminal

Maly Port

Production in 2016105.4 Mt

We are highly competitive in the coal industry thanks to our well-developed assets. These include high-quality coal deposits and modern washing plants connected to key markets through efficient logistics

21

2

§ Brown coal, hard coal

§ 1 underground mine

§ 1 open pit§ 1 processing

facility§ Domestic/export

market

76543

3

4 5

6

7

Average life of hard coal deposits

Over 30 years

71.3

34.1

Hard coal Brown coal

69.6

35.8

Open pit Underground

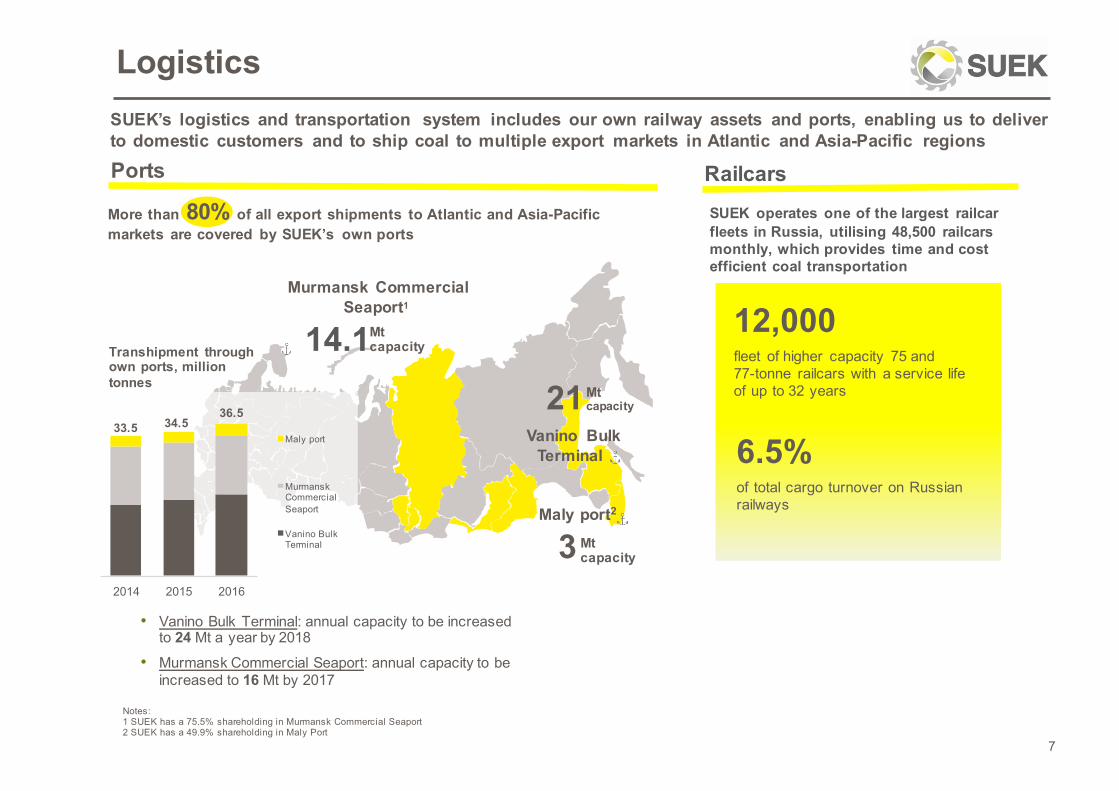

More than 80% of all export shipments to Atlantic and Asia-Pacific markets are covered by SUEK’s own ports

LogisticsSUEK’s logistics and transportation system includes our own railway assets and ports, enabling us to deliver to domestic customers and to ship coal to multiple export markets in Atlantic and Asia-Pacific regions

7

RailcarsPorts

Murmansk Commercial Seaport1

3 Mtcapacity

Notes:1 SUEK has a 75.5% shareholding in Murmansk Commercial Seaport2 SUEK has a 49.9% shareholding in Maly Port

12,000fleet of higher capacity 75 and 77-tonne railcars with a service life of up to 32 years

SUEK operates one of the largest railcar fleets in Russia, utilising 48,500 railcars monthly, which provides time and cost efficient coal transportation

6.5%of total cargo turnover on Russian railways

Vanino BulkTerminal

Maly port2

21Mtcapacity

• Vanino Bulk Terminal: annual capacity to be increased to 24 Mt a year by 2018

• Murmansk Commercial Seaport: annual capacity to be increased to 16 Mt by 2017

Transhipment through own ports, million tonnes

Mtcapacity

2014 2015 2016

Maly port

Murmansk Commercial Seaport

Vanino Bulk Terminal

33.5 34.536.5

14.1

2012

2013

2014

2015

2016

Own coal Purchased coal

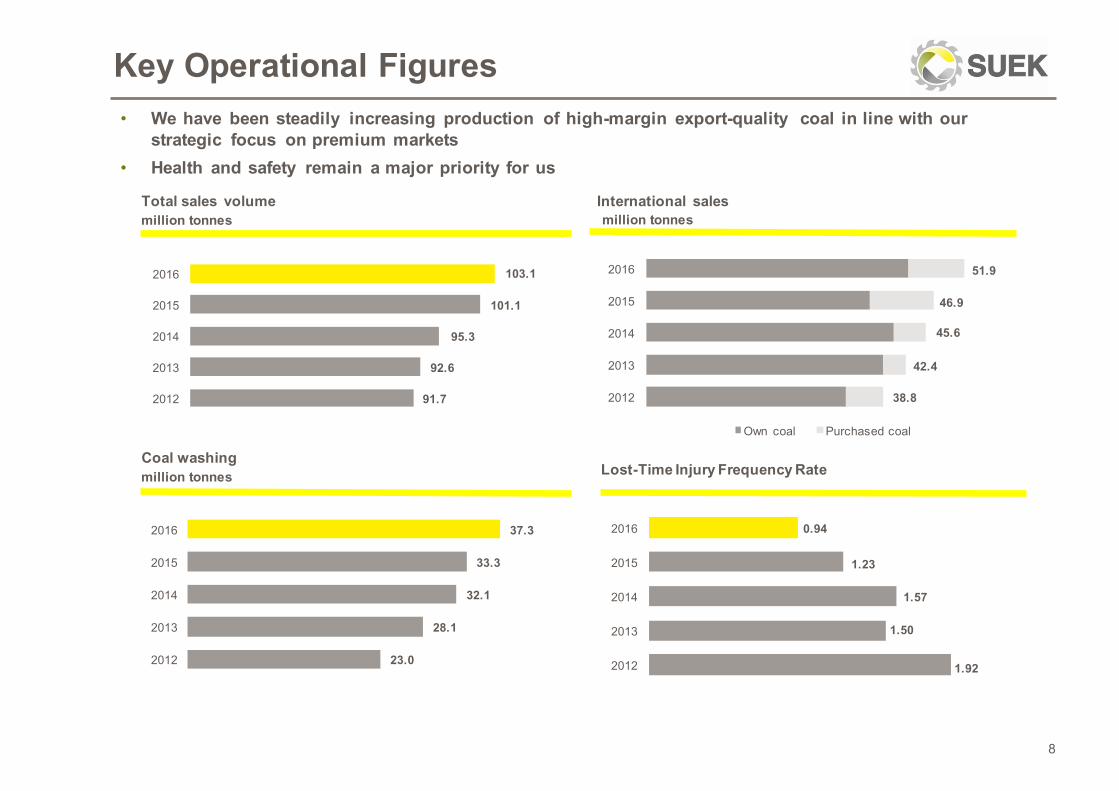

Key Operational Figures

Total sales volume International salesmillion tonnes million tonnes

Coal washingLost-Time Injury Frequency Ratemillion tonnes

8

51.9

38.8

42.4

45.6

46.9

• We have been steadily increasing production of high-margin export-quality coal in line with our strategic focus on premium markets

• Health and safety remain a major priority for us

23.0

28.1

32.1

33.3

37.3

2012

2013

2014

2015

2016

1.92

1.50

1.57

1.23

0.94

2012

2013

2014

2015

2016

91.7

92.6

95.3

101.1

103.1

2012

2013

2014

2015

2016

0,00%

5,00%

10,00%

15,00%

20,00%

25,00%

30,00%

-

200,0

400,0

600,0

800,0

1 000,0

1 200,0

1 400,0

1 600,0

1 800,0

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

mill

ion

tonn

es

China India

JKT (Japan/Korea/Taiwan) SEA (Malaysia/Phil/Thai/Viet)

ROW % China

% India

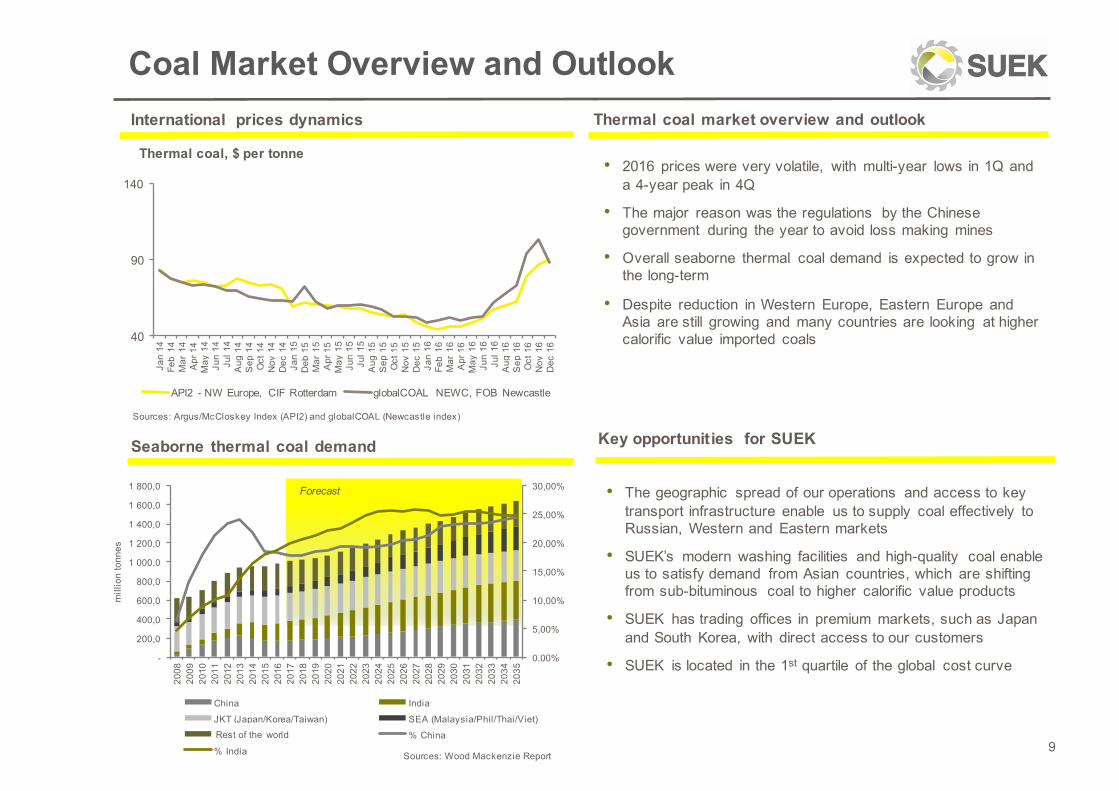

Coal Market Overview and Outlook

9Sources: Wood Mackenzie Report

Forecast

Thermal coal market overview and outlook

• 2016 prices were very volatile, with multi-year lows in 1Q anda 4-year peak in 4Q

• The major reason was the regulations by the Chinese government during the year to avoid loss making mines

• Overall seaborne thermal coal demand is expected to grow in the long-term

• Despite reduction in Western Europe, Eastern Europe and Asia are still growing and many countries are looking at higher calorific value imported coals

Seaborne thermal coal demand Key opportunities for SUEK

• The geographic spread of our operations and access to key transport infrastructure enable us to supply coal effectively to Russian, Western and Eastern markets

• SUEK’s modern washing facilities and high-quality coal enable us to satisfy demand from Asian countries, which are shifting from sub-bituminous coal to higher calorific value products

• SUEK has trading offices in premium markets, such as Japan and South Korea, with direct access to our customers

• SUEK is located in the 1st quartile of the global cost curve

Sources: Argus/McCloskey Index (API2) and globalCOAL (Newcastle index)

International prices dynamics

Thermal coal, $ per tonne

40

90

140

Jan

14Fe

b 14

Mar

14

Apr

14

May

14

Jun

14Ju

l 14

Aug

14

Sep

14

Oct

14

Nov

14

Dec

14

Jan

15D

eb 1

5M

ar 1

5A

pr 1

5M

ay 1

5Ju

n 15

Jul 1

5A

ug 1

5S

ep 1

5O

ct 1

5N

ov 1

5D

ec 1

5Ja

n 16

Feb

16M

ar 1

6A

pr 1

6M

ay 1

6Ju

n 16

Jul 1

6A

ug 1

6S

ep 1

6O

ct 1

6N

ov 1

6D

ec 1

6

API2 - NW Europe, CIF Rotterdam globalCOAL NEWC, FOB Newcastle

Rest of the world

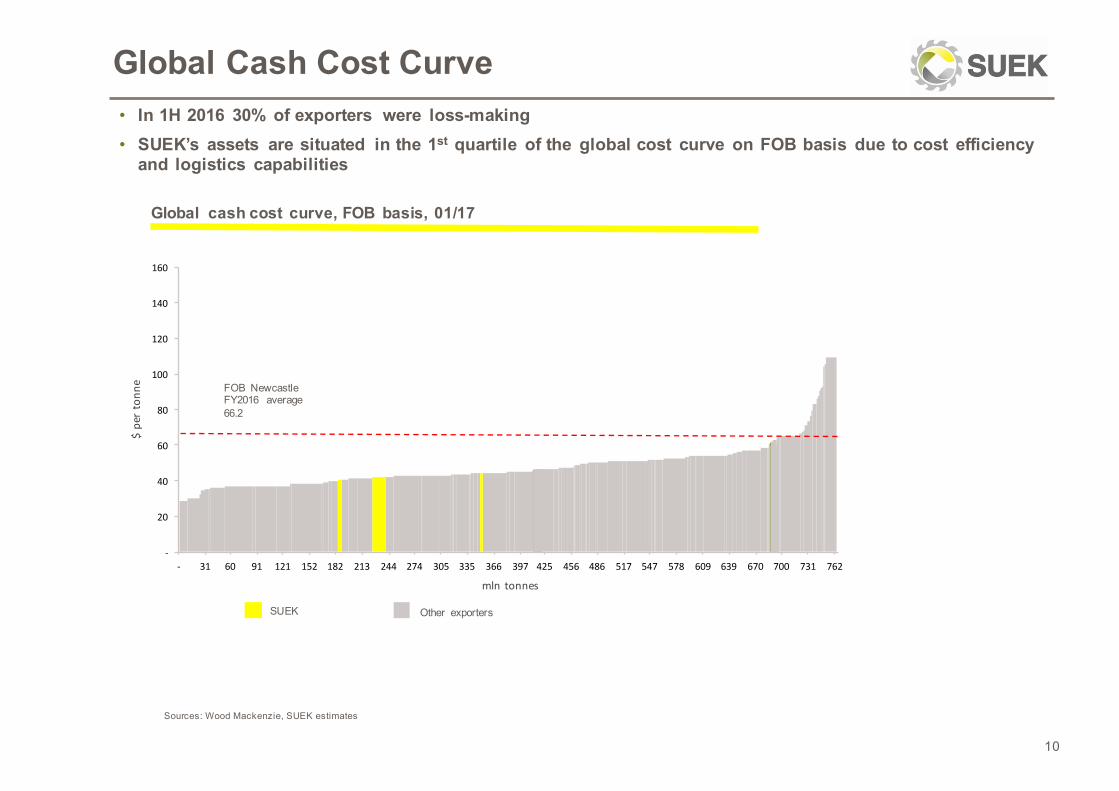

Global Cash Cost Curve

Sources: Wood Mackenzie, SUEK estimates

10

Global cash cost curve, FOB basis, 01/17

• In 1H 2016 30% of exporters were loss-making• SUEK’s assets are situated in the 1st quartile of the global cost curve on FOB basis due to cost efficiency

and logistics capabilities

-

20

40

60

80

100

120

140

160

- 31 60 91 121 152 182 213 244 274 305 335 366 397 425 456 486 517 547 578 609 639 670 700 731 762

$pertonn

e

mln tonnes

SUEK Other exporters

FOB Newcastle FY2016 average 66.2

Ust-Luga Port

MurmanskCommercialSeaport

Vanino Bulk Terminal

Maly PortAzov Port

Vostochny Port

Railways

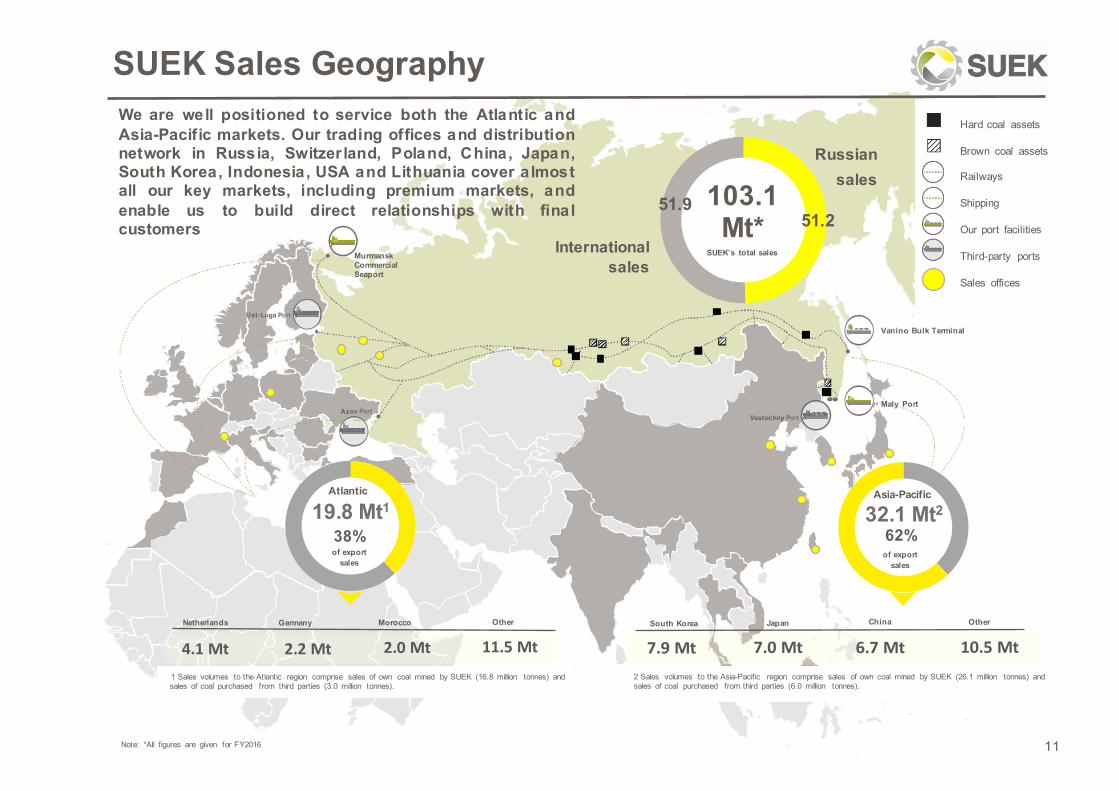

Shipping103.1 Mt*

11

We are well positioned to service both the Atlantic andAsia-Pacific markets. Our trading offices and distributionnetwork in Russia, Switzer land, Poland, China, Japan,South Korea, Indonesia, USA and Lithuania cover almostall our key markets, including premium markets, andenable us to build direct relationships with finalcustomers

19.8 Mt1

38%of export

sales

Atlantic

32.1 Mt2

62%of export

sales

Asia-Pacific

Netherlands MoroccoGermany Other South Korea Japan China Other

Hard coal assets

Brown coal assets

Railways

Shipping

Our port facilities

Third-party ports

Sales offices

SUEK Sales Geography

Note: *All figures are given for FY2016

Russian sales

International sales

SUEK’s total sales

51.251.9

1 1 Sales volumes to the Atlantic region comprise sales of own coal mined by SUEK (16.8 million tonnes) andsales of coal purchased from third parties (3.0 million tonnes).

2 Sales volumes to the Asia-Pacific region comprise sales of own coal mined by SUEK (26.1 million tonnes) and sales of coal purchased from third parties (6.0 million tonnes).

4.1Mt 2.2 Mt 2.0Mt 11.5 Mt 7.9Mt 7.0Mt 6.7Mt 10.5Mt

915

2 965

Russia

Export

46%

31%

18%

5%

SGK

Other power plants

Public utilities

Other

50%

50%

Russian market International market

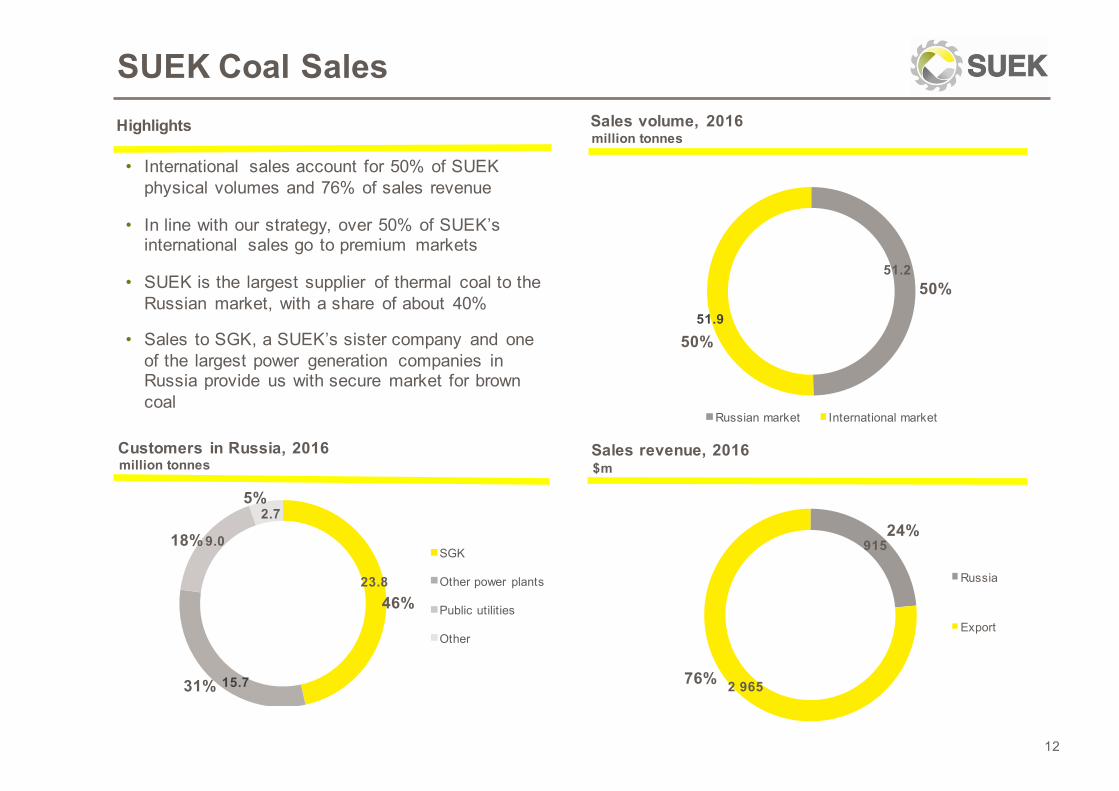

SUEK Coal SalesSales volume, 2016

• International sales account for 50% of SUEK physical volumes and 76% of sales revenue

• In line with our strategy, over 50% of SUEK’s international sales go to premium markets

• SUEK is the largest supplier of thermal coal to the Russian market, with a share of about 40%

• Sales to SGK, a SUEK’s sister company and one of the largest power generation companies in Russia provide us with secure market for brown coal

Sales revenue, 2016

12

million tonnes

Customers in Russia, 2016

Highlights

$m

51.9

51.2

76%

million tonnes

23.8

2.7

9.0

15.7

24%

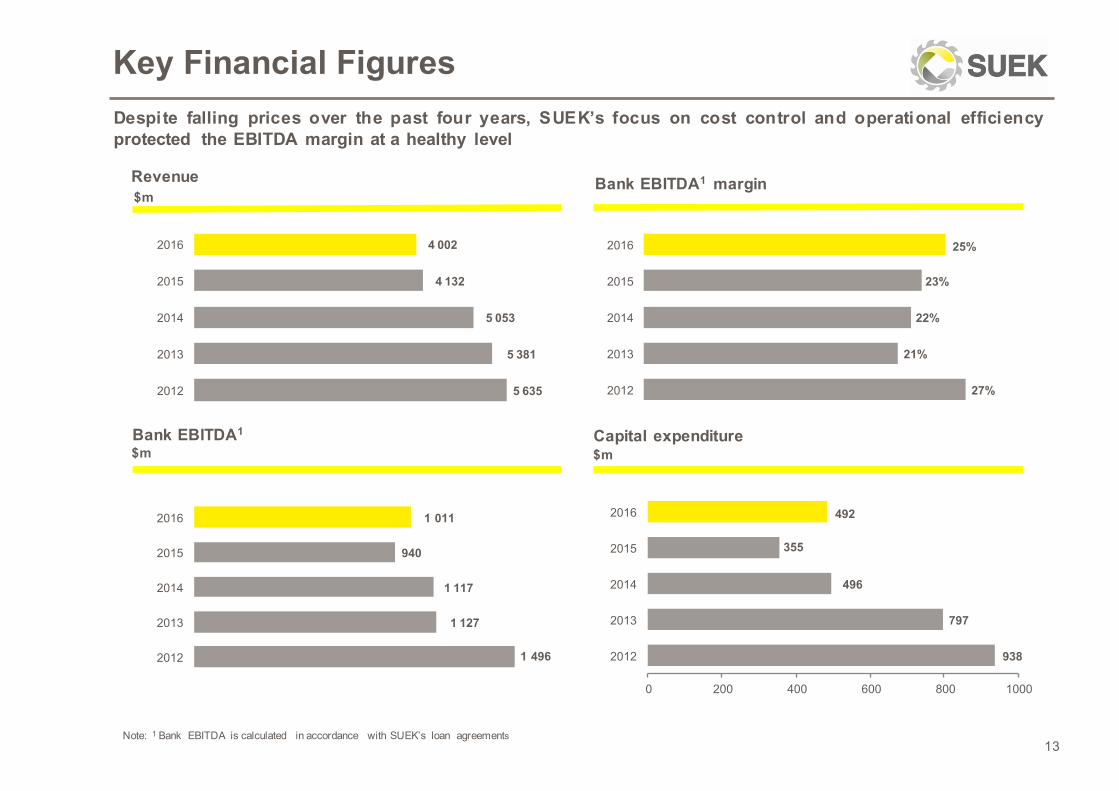

1 496

1 127

1 117

940

1 011

2012

2013

2014

2015

2016

Key Financial Figures

$m

13

Revenue Bank EBITDA1 margin

Bank EBITDA1 Capital expenditure$m $m

Note: 1 Bank EBITDA is calculated in accordance with SUEK’s loan agreements

Despite falling prices over the past four years, SUEK’s focus on cost control and operational efficiencyprotected the EBITDA margin at a healthy level

938

797

496

355

492

0 200 400 600 800 1000

2012

2013

2014

2015

2016

27%

21%

22%

23%

25%

2012

2013

2014

2015

2016

5 635

5 381

5 053

4 132

4 002

2012

2013

2014

2015

2016

3 001

3 444 3 373 3 3423 425

2 786 2 791

2 978

2.43.1 3.3 2.99 3.3 2.96 3.23 2.94

10.9

8.9 9.2 9.3

7.8 7.57.3

7.9

0

2

4

6

8

10

12

2000

2500

3000

3500

30'Jun 2013

31'Dec 2013

30'Jun 2014

31'Dec 2014

30'Jun 2015

31'Dec 2015

30'Jun 2016

31 Dec'16

Net Debt Net Debt/EBITDA EBITDA/Interest Expense

Debt Snapshot as of 31 December 2016

14

Net debt and covenant ratios

Debt structure as of 31 December 2016

Note: 1Bank EBITDA is calculated in accordance with SUEK’s loan agreements

$m Debt repayment profile

• Net debt/ Bank EBITDA1 ratio: 2.94x, below covenant of 4.0x

• Moody’s: Ba3 Stable confirmed in October 2016

• February 2016: $1,252m PXF • October 2016: issue of 3-year RUB 8bn

bonds

$m

85%

7%8%

USD RUR EUR

75%

5%

5%1%

8%6%

PXF ECA LoanBonds SwapBilateral Short term loans

1020

698890

432 391

69 43

36

38

40

38 28

364

24491

152 229

29 31

1 419

980 1 021

623 648

120 105

2016 2017 2018 2019 2020 2021 2022

Other Debt

ECA Loan

PXF

TOTAL

RUB

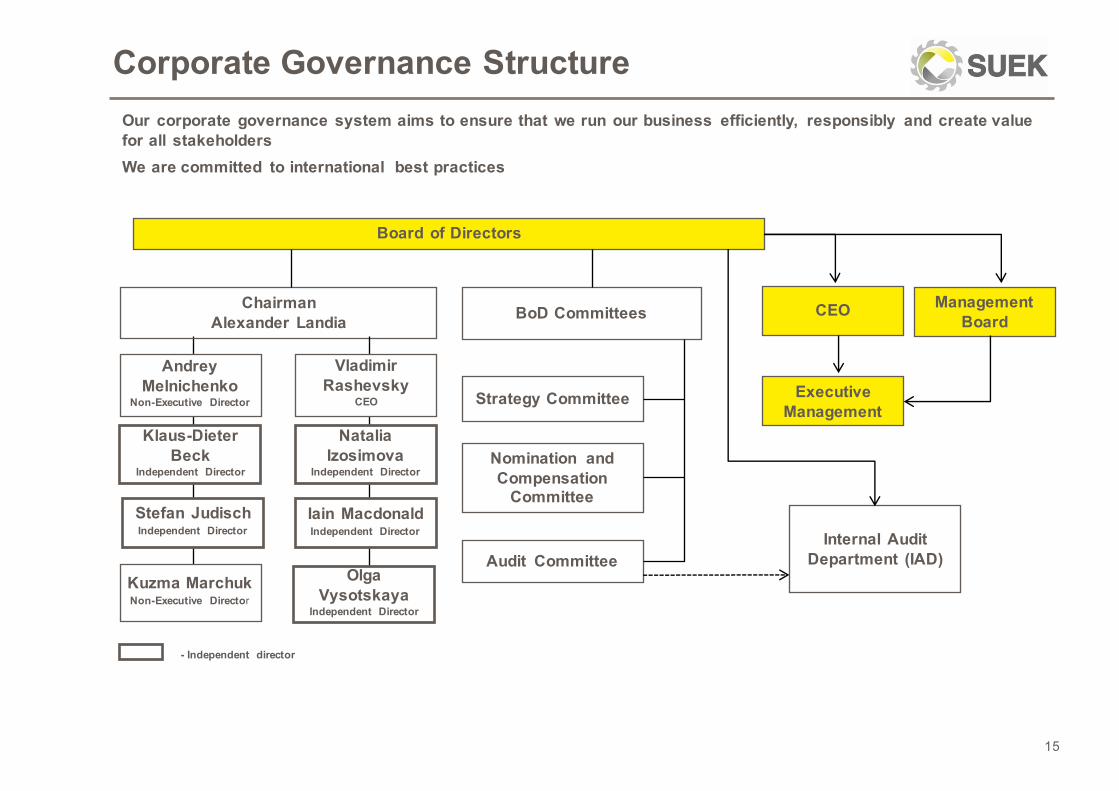

Corporate Governance Structure

15

Board of Directors

Management Board

CEOChairmanAlexander Landia

Executive Management

BoD Committees

Klaus-Dieter Beck

Independent Director

Stefan JudischIndependent Director

Kuzma MarchukNon-Executive Director

Natalia Izosimova

Independent Director

Iain MacdonaldIndependent Director

Olga Vysotskaya

Independent Director

Andrey Melnichenko

Non-Executive Director Strategy Committee

Nomination and Compensation

Committee

Audit CommitteeInternal Audit

Department (IAD)

Our corporate governance system aims to ensure that we run our business efficiently, responsibly and create value for all stakeholdersWe are committed to international best practices

Vladimir Rashevsky

CEO

- Independent director

For more information please visit www.suek.com

or contact our Investor Relations [email protected]

Contacts