Embed Size (px)

Citation preview

Discussion Paper

Fuel Tax Credit Reform

Fuel Tax Credit Reform Discussion Paper

May 2005 First released 27 May 2005 Updated 2 June 2005

© Commonwealth of Australia 2005

ISBN 0 642 74276 6

This work is copyright. Apart from any use as permitted under the Copyright Act 1968, no part may be reproduced by any process without prior written permission from the Commonwealth. Requests and inquiries concerning reproduction and rights should be addressed to the:

Commonwealth Copyright Administration Attorney General�s Department Robert Garran Offices National Circuit Canberra ACT 2600

Or posted at: http://www.ag.gov.au/cca

Page iii

CONTENTS

OVERVIEW ........................................................................................................v Fuel tax credit reform.................................................................................................................. v Purpose of this paper .................................................................................................................. v

CHAPTER 1: THE FUEL TAX CREDIT SYSTEM .......................................................... 1 Fuel tax relief for businesses and households ..........................................................................1 Timetable for implementation of fuel tax reform ....................................................................5 How will blends of fuel be treated?...........................................................................................6 Environmental measures.............................................................................................................6 Claiming arrangements for fuel tax credits ..............................................................................7 Claims for fuel purchased or imported under the Energy Grants (Credits) Scheme .........8

CHAPTER 2: LEGISLATIVE DESIGN OF THE FUEL TAX CREDIT SYSTEM .......................... 9 The Fuel Tax Act...........................................................................................................................9 Administration and compliance regime ...................................................................................9 What are coherent principles? ..................................................................................................10

CHAPTER 3: ENTITLEMENT TO A FUEL TAX CREDIT .......................................................13 Coherent Principle 1: Scope of the measure � incidence of fuel taxation ........................13 Coherent Principle 2: Business use of taxable fuels..............................................................13 Coherent Principle 3: Private use of taxable fuels ................................................................18 Coherent Principle 4: Working out how much fuel tax credit is payable on the fuel......19 Coherent Principle 5: Change in purpose for which the fuel is acquired or imported ...22 Coherent Principle 6: Where there is no prospect of the fuel being used .........................22 Coherent Principle 7: The Greenhouse Challenge Plus Programme .................................23 Coherent Principle 8: Schemes ................................................................................................25

CHAPTER 4: ACCOUNTING FOR AND CLAIMING A FUEL TAX CREDIT ...............................27 Coherent Principle 9: Fuel tax credit to be claimed in the same way as an input tax credit ......................................................................................................................................27 Coherent Principle 10: Application of GST tax periods .......................................................28 Coherent Principle 11: Application of GST attribution rules ..............................................28 Coherent Principle 12: The GST rules that apply to the way a business is organised will also apply to fuel tax credits .............................................................................................29

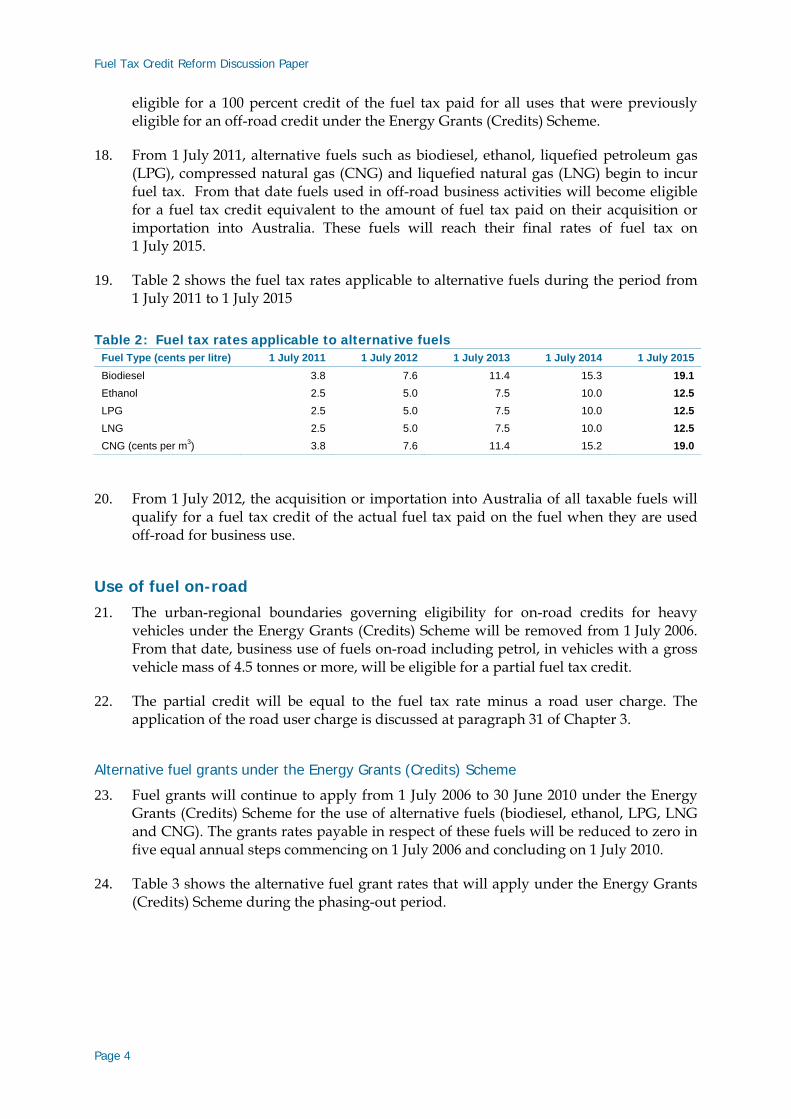

Page v

OVERVIEW

Fuel tax credit reform

1. In the policy document Securing Australia�s Energy Future (the energy white paper) the Government announced a major programme of reform to modernise and simplify the fuel tax system. The changes will lower compliance costs, reduce tax on business and remove fuel tax for thousands of businesses and households.

2. As part of the reform, the current complex system of grants and rebates will be replaced by a single fuel tax credit system. This system will allow businesses to claim their fuel tax credits through the Business Activity Statement in the same way that they claim goods and services tax (GST) input tax credits. The system will also allow householders to claim a fuel tax credit for fuel used in the generation of electricity.

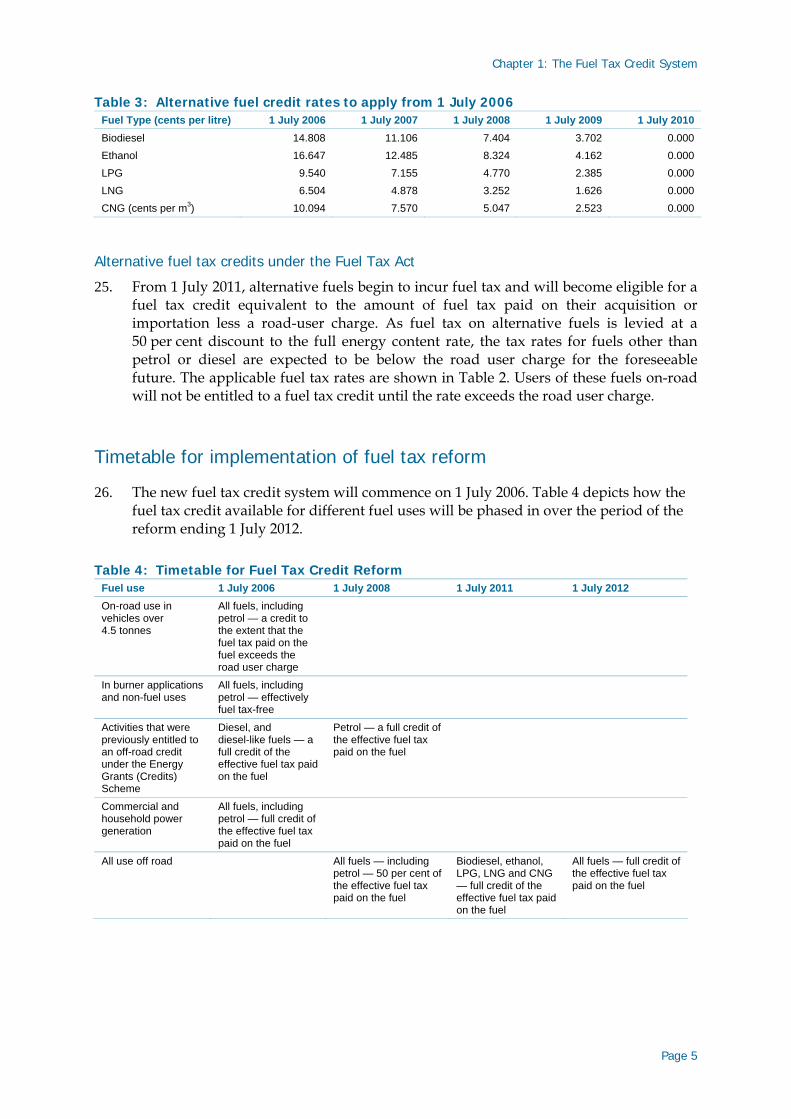

3. Under the fuel tax credit system, all fuels, including petrol consumed off-road for business purposes, will become tax-free over time. This will provide fuel tax relief for the first time to businesses involved in a range of activities. For example, businesses involved in manufacturing, quarrying and construction will become entitled to fuel tax relief for the first time. Other major beneficiaries will include primary production, mining and commercial power generation.

4. The fuel tax credit system reform also expands fuel tax relief for fuel consumed in road transport by allowing partial fuel tax credits for all taxable fuels, including petrol, consumed on road for all business purposes in registered vehicles with a gross vehicle mass of 4.5 tonnes or more.

Purpose of this paper

5. The purpose of this paper is to:

! ensure that the proposed legislative framework that will govern fuel tax credits is practical, minimises compliance costs for business and effectively delivers the Government�s policy, and

! allow industry to identify possible issues with implementing the policy and with the design of the legislation.

Overview

Page vi

6. The paper outlines the legislative model for the delivery of fuel tax credits and discusses the principles of eligibility, accounting and reporting under the new system. It also discusses the measures for providing fuel tax relief to householders for fuel consumed in heating and the generation of electricity.

7. The paper does not necessarily represent the concluded view of either Treasury or the Government.

Page 1

CHAPTER 1: THE FUEL TAX CREDIT SYSTEM

This chapter provides an overview of the key elements of the fuel tax credit system for providing fuel tax relief to businesses and households. The chapter also provides a brief overview of the claiming arrangements for fuel tax credits and outlines the environmental measures for the fuel tax credit system that will support effective management of energy and compliance with diesel emissions.

Fuel tax relief for businesses and households

1. The fuel tax credit system will substantially lower the fuel tax burden on business and households. The changes will refocus the fuel tax system away from specific fuels, and towards types of fuel uses. They also reflect the Government�s aim to lower compliance costs and reduce the burden of fuel tax on business.

2. The Government�s objective in reforming fuel taxation and credit arrangements is that when the reforms are fully implemented, fuel tax will only be effectively collected from fuel consumed:

! in the private use of motor vehicles

! for any other private purpose (except for the generation of electricity and use in burner applications)

! in the business use of vehicles with a gross vehicle mass of less than 4.5 tonnes

! in the business use of vehicles with a gross vehicle mass of 4.5 tonnes or more but only to the extent of the applicable road user charge.

3. Fuel tax will continue to be collected on aviation fuels1 for cost recovery reasons, and a levy will also continue to be collected on certain lubricant oils under the Product Stewardship (Oil) Programme.2

4. The reforms to broaden fuel tax relief will be phased in, commencing 1 July 2006, with the final changes taking effect on 1 July 2012.

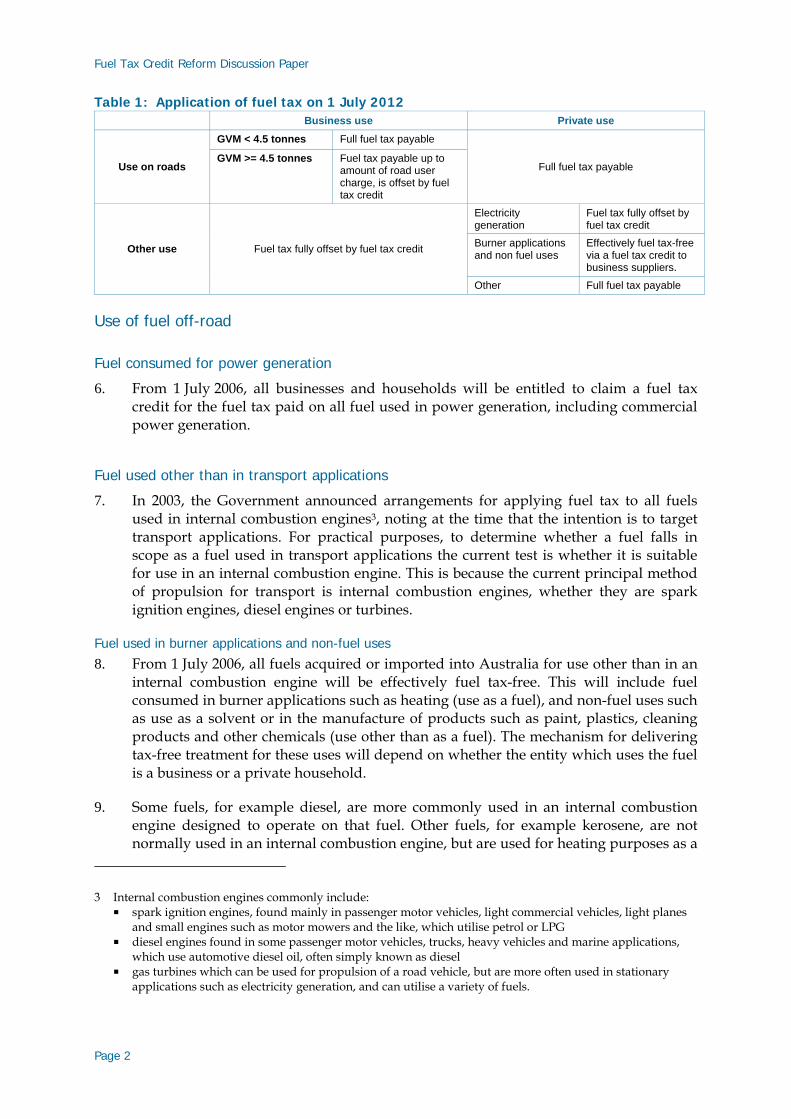

5. Table 1 provides an overview of how fuel tax will apply when the reforms are fully implemented.

1 Products classified in the schedules to the Customs and Excise Tariff Acts as kerosene for use as fuel in an aircraft or gasoline for use as fuel in an aircraft.

2 The product stewardship for oil programme (PSO) began on 1 January 2001. It is designed to support and encourage environmentally sustainable management of recycling waste oil. Under the programme, the Government collects a levy on all petroleum-based oil or synthetic equivalents produced in or imported to Australia. This levy funds benefits paid to waste oil recyclers and for eligible uses of specific oils.

Fuel Tax Credit Reform Discussion Paper

Page 2

Table 1: Application of fuel tax on 1 July 2012 Business use Private use

GVM < 4.5 tonnes Full fuel tax payable

Use on roads GVM >= 4.5 tonnes Fuel tax payable up to

amount of road user charge, is offset by fuel tax credit

Full fuel tax payable

Electricity generation

Fuel tax fully offset by fuel tax credit

Burner applications and non fuel uses

Effectively fuel tax-free via a fuel tax credit to business suppliers.

Other use Fuel tax fully offset by fuel tax credit

Other Full fuel tax payable

Use of fuel off-road

Fuel consumed for power generation

6. From 1 July 2006, all businesses and households will be entitled to claim a fuel tax credit for the fuel tax paid on all fuel used in power generation, including commercial power generation.

Fuel used other than in transport applications

7. In 2003, the Government announced arrangements for applying fuel tax to all fuels used in internal combustion engines3, noting at the time that the intention is to target transport applications. For practical purposes, to determine whether a fuel falls in scope as a fuel used in transport applications the current test is whether it is suitable for use in an internal combustion engine. This is because the current principal method of propulsion for transport is internal combustion engines, whether they are spark ignition engines, diesel engines or turbines.

Fuel used in burner applications and non-fuel uses

8. From 1 July 2006, all fuels acquired or imported into Australia for use other than in an internal combustion engine will be effectively fuel tax-free. This will include fuel consumed in burner applications such as heating (use as a fuel), and non-fuel uses such as use as a solvent or in the manufacture of products such as paint, plastics, cleaning products and other chemicals (use other than as a fuel). The mechanism for delivering tax-free treatment for these uses will depend on whether the entity which uses the fuel is a business or a private household.

9. Some fuels, for example diesel, are more commonly used in an internal combustion engine designed to operate on that fuel. Other fuels, for example kerosene, are not normally used in an internal combustion engine, but are used for heating purposes as a

3 Internal combustion engines commonly include: ! spark ignition engines, found mainly in passenger motor vehicles, light commercial vehicles, light planes

and small engines such as motor mowers and the like, which utilise petrol or LPG ! diesel engines found in some passenger motor vehicles, trucks, heavy vehicles and marine applications,

which use automotive diesel oil, often simply known as diesel ! gas turbines which can be used for propulsion of a road vehicle, but are more often used in stationary

applications such as electricity generation, and can utilise a variety of fuels.

Chapter 1: The Fuel Tax Credit System

Page 3

burner fuel or in uses other than as a fuel. Kerosene can, however, also be used for powering an internal combustion engine. For this reason the equivalent rate to the diesel rate is included in the excise tariff for fuels that are suitable for use in an internal combustion engine, as a revenue protection measure.

10. The Government currently provides fuel tax-free treatment for certain non-fuel uses of petroleum products, such as those mentioned above. Depending on the type of petroleum product, the fuel tax-free treatment is currently delivered by either a grant under the Energy Grants (Credits) Scheme, a free rate under the Excise tariff or by the remission and refund provisions of the Excise and Customs legislation.

11. Under fuel tax reform, all of the current mechanisms for delivering fuel tax-free treatment for petroleum products will be removed, and from 1 July 2006 fuel tax will apply to all petroleum products, including blends of petroleum products suitable for use as a fuel in an internal combustion engine. Effective fuel tax-free treatment for these products where used other than as a fuel in an internal combustion engine will be delivered by a fuel tax credit to either the user of the fuel, or at another point in the supply chain, depending on whether the use is business or private.

12. For the business use of petroleum products such as burner fuels or in non-fuel uses, the effective fuel tax-free treatment will be delivered through a fuel tax credit to the business as the end user of the product.

13. Where a petroleum product is used as an ingredient in the manufacture of another product (for example, paint, cleaning agents, plastics) and where that final product is not suitable for use as a fuel in an internal combustion engine, the manufacturer (for example, a paint manufacturer) will be entitled to a fuel credit on the petroleum component.

14. In order that private users of these products will not have to enter the fuel tax credit system, a fuel tax credit will apply further up the supply chain with the benefit passed on in the price of the product, ensuring that the product is effectively fuel tax-free for these users. For products used as burner fuels, such as kerosene and heating oil, the distributor will be entitled to claim a fuel tax credit for fuel sold to a private household. For products used in non-fuel applications, such as kerosene used as a solvent, a fuel credit would be given to the packager of such products, packaged in small containers for resale in retail outlets.

15. The tax and credit treatment of fuels used in burner and non-fuel applications is discussed in the Treasury paper, Review of the Schedule to the Excise Tariff that will be released shortly.

Other use of fuel off-road

16. From 1 July 2006, a fuel tax credit will apply to the acquisition or importation of diesel and diesel-like fuels in activities that currently qualify for an off-road credit under the Energy Grants (Credits) Scheme.

17. From 1 July 2008 all other off-road business use of all taxable fuels will become eligible for a 50 per cent credit of the fuel tax paid for the acquisition or importation of the fuel into Australia. At the same time the acquisition or importation of petrol will become

Fuel Tax Credit Reform Discussion Paper

Page 4

eligible for a 100 percent credit of the fuel tax paid for all uses that were previously eligible for an off-road credit under the Energy Grants (Credits) Scheme.

18. From 1 July 2011, alternative fuels such as biodiesel, ethanol, liquefied petroleum gas (LPG), compressed natural gas (CNG) and liquefied natural gas (LNG) begin to incur fuel tax. From that date fuels used in off-road business activities will become eligible for a fuel tax credit equivalent to the amount of fuel tax paid on their acquisition or importation into Australia. These fuels will reach their final rates of fuel tax on 1 July 2015.

19. Table 2 shows the fuel tax rates applicable to alternative fuels during the period from 1 July 2011 to 1 July 2015

Table 2: Fuel tax rates applicable to alternative fuels Fuel Type (cents per litre) 1 July 2011 1 July 2012 1 July 2013 1 July 2014 1 July 2015 Biodiesel 3.8 7.6 11.4 15.3 19.1 Ethanol 2.5 5.0 7.5 10.0 12.5 LPG 2.5 5.0 7.5 10.0 12.5 LNG 2.5 5.0 7.5 10.0 12.5 CNG (cents per m3) 3.8 7.6 11.4 15.2 19.0

20. From 1 July 2012, the acquisition or importation into Australia of all taxable fuels will qualify for a fuel tax credit of the actual fuel tax paid on the fuel when they are used off-road for business use.

Use of fuel on-road 21. The urban-regional boundaries governing eligibility for on-road credits for heavy

vehicles under the Energy Grants (Credits) Scheme will be removed from 1 July 2006. From that date, business use of fuels on-road including petrol, in vehicles with a gross vehicle mass of 4.5 tonnes or more, will be eligible for a partial fuel tax credit.

22. The partial credit will be equal to the fuel tax rate minus a road user charge. The application of the road user charge is discussed at paragraph 31 of Chapter 3.

Alternative fuel grants under the Energy Grants (Credits) Scheme

23. Fuel grants will continue to apply from 1 July 2006 to 30 June 2010 under the Energy Grants (Credits) Scheme for the use of alternative fuels (biodiesel, ethanol, LPG, LNG and CNG). The grants rates payable in respect of these fuels will be reduced to zero in five equal annual steps commencing on 1 July 2006 and concluding on 1 July 2010.

24. Table 3 shows the alternative fuel grant rates that will apply under the Energy Grants (Credits) Scheme during the phasing-out period.

Chapter 1: The Fuel Tax Credit System

Page 5

Table 3: Alternative fuel credit rates to apply from 1 July 2006 Fuel Type (cents per litre) 1 July 2006 1 July 2007 1 July 2008 1 July 2009 1 July 2010 Biodiesel 14.808 11.106 7.404 3.702 0.000 Ethanol 16.647 12.485 8.324 4.162 0.000 LPG 9.540 7.155 4.770 2.385 0.000 LNG 6.504 4.878 3.252 1.626 0.000 CNG (cents per m3) 10.094 7.570 5.047 2.523 0.000

Alternative fuel tax credits under the Fuel Tax Act

25. From 1 July 2011, alternative fuels begin to incur fuel tax and will become eligible for a fuel tax credit equivalent to the amount of fuel tax paid on their acquisition or importation less a road-user charge. As fuel tax on alternative fuels is levied at a 50 per cent discount to the full energy content rate, the tax rates for fuels other than petrol or diesel are expected to be below the road user charge for the foreseeable future. The applicable fuel tax rates are shown in Table 2. Users of these fuels on-road will not be entitled to a fuel tax credit until the rate exceeds the road user charge.

Timetable for implementation of fuel tax reform

26. The new fuel tax credit system will commence on 1 July 2006. Table 4 depicts how the fuel tax credit available for different fuel uses will be phased in over the period of the reform ending 1 July 2012.

Table 4: Timetable for Fuel Tax Credit Reform Fuel use 1 July 2006 1 July 2008 1 July 2011 1 July 2012 On-road use in vehicles over 4.5 tonnes

All fuels, including petrol — a credit to the extent that the fuel tax paid on the fuel exceeds the road user charge

In burner applications and non-fuel uses

All fuels, including petrol — effectively fuel tax-free

Activities that were previously entitled to an off-road credit under the Energy Grants (Credits) Scheme

Diesel, and diesel-like fuels — a full credit of the effective fuel tax paid on the fuel

Petrol — a full credit of the effective fuel tax paid on the fuel

Commercial and household power generation

All fuels, including petrol — full credit of the effective fuel tax paid on the fuel

All use off road All fuels — including petrol — 50 per cent of the effective fuel tax paid on the fuel

Biodiesel, ethanol, LPG, LNG and CNG — full credit of the effective fuel tax paid on the fuel

All fuels — full credit of the effective fuel tax paid on the fuel

Fuel Tax Credit Reform Discussion Paper

Page 6

How will blends of fuel be treated?

27. The treatment of fuel blends, and the entity able to claim a fuel tax credit relating to a fuel blend, will depend on whether or not the blend is suitable for use in an internal combustion engine.

Fuel blends suitable for use in an internal combustion engine 28. The end user will be the entity entitled to claim a fuel tax credit for the use of fuel

blends of a type suitable for use in an internal combustion engine. Where a fuel blend meets a particular fuel standard, for instance petrol or diesel, it will be treated as having paid fuel tax at the rate applicable to the unblended fuel covered by the standard. For fuel blends where one of the constituents attracts fuel tax at a discounted rate, such as a blend of diesel and biodiesel, the result of this treatment would actually be a fuel tax credit in excess of the fuel tax actually incurred. Where a fuel blend does not meet a fuel standard, the amount of fuel tax credit will not be more than the actual fuel tax paid on the fuels that make up the blend.

29. Where a fuel blend considered suitable for use in an internal combustion engine is packaged into small containers for retail sale for use in non-fuel applications, as a solvent or a cleaning product for example, the packager of the blend will be entitled to claim a fuel tax credit. This will avoid the need for private users of such products to enter the fuel tax credit system to receive effective fuel tax-free treatment.

Fuel blends not suitable for use in an internal combustion engine 30. Where a fuel blend is not suitable for use in an internal combustion engine, the

manufacturer of the blend will be entitled to claim a credit for any fuel tax paid on the constituents of the blend. Some examples of these types of blends are cleaning solvents, paints and mould release agents.

Increase in fuel tax on petrol and diesel in 2006 and 2007 31. From 1 January 2006 the fuel tax on petrol, and from 1 January 2007 the fuel tax on

diesel, will increase for a period of two years to fund grants under the Energy Grants (Cleaner Fuels) Scheme Act 2003 to encourage the production of low-sulphur petrol and diesel. As this fuel tax differential is hypothecated for the purpose of funding the cleaner fuel grants, the rate of fuel tax credit available for petrol and diesel during these years will be exclusive of the amount of fuel tax imposed to fund the production grants.

Environmental measures

32. As a supplement to measures already in place for addressing the environmental impact of fuel use, the Government will introduce two new measures to ensure that those businesses receiving fuel tax credits meet appropriate environmental standards.

Chapter 1: The Fuel Tax Credit System

Page 7

33. These environmental measures are the Greenhouse Challenge Plus Programme and compliance with one of five emissions performance criteria by vehicles using diesel fuel on-road.

Membership of the Greenhouse Challenge Plus Programme 34. Businesses claiming over $3 million each year in fuel tax credits will need to be

members of the Government�s Greenhouse Challenge Plus Programme. Under this programme member businesses must measure their greenhouse gas emissions, develop action plans for greenhouse gas abatement and report to the Government on their actions.

Compliance with performance criteria 35. Operators of diesel vehicles with a gross vehicle mass of 4.5 tonnes or more will need

to meet one of five performance criteria to be entitled to a fuel tax credit. The claimant�s vehicle must either:

! have been manufactured after 1 January 1996

! be part of an accredited audited maintenance programme

! meet the Australian Transport Council�s in-service emission standard (referred to in the Diesel National Environment Protection (Diesel Vehicle Emissions) Measure)

! comply with a Government-endorsed maintenance schedule which includes an emissions component, or

! be a �dedicated farm vehicle�.

36. The first four criteria are designed to ensure that the operators of diesel vehicles have an incentive to make sure their vehicle meets the emissions standard set under the Diesel National Environment Protection (Diesel Vehicles Emissions) Measure. The fifth is designed to exempt farm vehicles, as these vehicles do not generally contribute to urban air quality problems.

Claiming arrangements for fuel tax credits

37. Businesses will claim fuel tax credits on the Business Activity Statement in line with their reporting and claiming arrangements for the GST.

38. Administering fuel tax credits under the Business Activity Statement will streamline the payment of credits. It will also simplify and reduce business interactions with the ATO as businesses will have a single point of contact with the ATO.

39. When the fuel tax credit system is fully implemented, business entities will no longer need to estimate fuel use in various uses at various times according to complex and inconsistent criteria. This will lead to a significant reduction in record-keeping required to substantiate entitlements.

Fuel Tax Credit Reform Discussion Paper

Page 8

40. The extension of eligibility under the new arrangements will also reduce the need for businesses to clarify eligibility guidelines through costly negotiation and litigation.

41. Householders using fuel to generate electricity, and volunteer organisations not required to be registered for the GST using fuel in emergency vehicles, will claim fuel tax credits via a separate mechanism to the Business Activity Statement. Treasury and the ATO are currently exploring options for delivery of credits to these fuel users.

Claims for fuel purchased or imported under the Energy Grants (Credits) Scheme

42. Although the Energy Grants (Credits) Scheme will no longer provide a credit for diesel purchased or imported after 30 June 2006, certain claims under that scheme will be allowed until 30 June 2007. The claims must be for diesel that was eligible to receive a grant and purchased or imported prior to 1 July 2006 for use by an entity that was entitled to make a claim under the scheme.

43. Diesel purchased or imported for use in the period from 1 July 2003 until 30 June 2006 may alternatively be claimed as a fuel tax credit under the proposed Fuel Tax Act from 1 July 2006. The claim must be for diesel that was eligible to receive a grant and was purchased for use by an entity that was entitled to make a claim under the Energy Grants (Credits) Scheme.

44. A claim in respect of a particular purchase, importation or use of diesel may be made only once under either the Energy Grants (Credits) Scheme or the Fuel Tax Act.

45. A grant will continue to be paid under the Energy Grants (Credits) Scheme for the purchase for use of alternative fuels on-road until 30 June 2010. The amount of grant payments will be progressively reduced to zero in five steps commencing 1 July 2006 and ending on 1 July 2010.

Page 9

CHAPTER 2: LEGISLATIVE DESIGN OF THE FUEL TAX CREDIT SYSTEM

This chapter outlines the legislative model for the delivery of fuel tax credits and provides some commentary on �coherent principles� based drafting. The chapter explains what is meant by �coherent principles� and why Treasury is adopting this approach for drafting the Fuel Tax Act.

The Fuel Tax Act

1. Fuel tax credits will be delivered within a taxation framework, rather than as a grant as is presently the case under the Energy Grants (Credits) Scheme.

2. The Fuel Tax Act will be the means of providing fuel tax credits to business from 1 July 2006 and, in the future, will establish a uniform system for the taxation of fuels, both locally produced and imported, commencing with the taxation of gaseous fuels1 from 2011.

3. Under the Act, fuel tax relief will be provided in the form of a fuel tax credit for the fuel tax embedded in the price of the fuel. This fuel tax credit will be claimed on the Business Activity Statement and will be offset against an entity�s other tax liabilities.

Administration and compliance regime

4. The Fuel Tax Act will operate under the general compliance and administrative umbrella of the Taxation Administration Act 1953. Matters such as the operation of running balance accounts, the public and private rulings system, taxation objections, reviews and appeals and the collection and recovery of tax-related liabilities are administered under this Act.

5. The administration of the Fuel Tax Act will align with the administration of the other indirect taxes (GST, luxury car tax and the wine equalisation tax) under a new part in the Schedule to the Taxation Administration Act 1953. This part will be modelled on the current indirect tax provisions in Part VI of the Taxation Administration Act 1953. This means that entities will have the same rights and obligations in relation to the Fuel Tax Act as they have for the other indirect taxes. This administrative regime will:

! establish that the Commissioner of Taxation will administer all indirect taxes

! support the payment and recovery of indirect taxes

! oblige entities to keep records to substantiate all indirect tax transactions

! provide penalties for breaching obligations under the various indirect tax acts

! permit entities to rely on the Commissioner of Taxation�s interpretation of the law

1 LPG, CNG and LNG.

Fuel Tax Credit Reform Discussion Paper

Page 10

! set time limits on credit and refund entitlements

! allow the review of assessment and other indirect tax decisions

! confer power on the Commissioner of Taxation to gather information

! protect confidentiality of information.

6. The administrative arrangements for fuel tax credits, to be included in the Taxation Administration Act 1953, will apply to the Fuel Tax Act in its entirety. That is, they will also apply to the taxation of fuels as they are brought under the Fuel Tax Act, starting with gaseous fuels in 2011.

Self-assessment

7. Under the fuel tax credit system, entities will self-assess their entitlement to a fuel tax credit as they do for the other indirect taxes.

What are coherent principles?

8. The Fuel Tax Act will be drafted using the coherent principles approach to tax design.

9. The coherent principles approach to tax design delivers on the Government�s commitment, as part of its A New Tax System proposal in 1998, to design the tax laws using general principles in preference to long and detailed provisions.

10. Under coherent principles, the operative legislative provisions that implement the policy are expressed as principles. They will prescribe the legislative outcome rather than the mechanism that produces it, and typically avoid the detail that appears in more traditional legislative design approaches.

Why is the approach called ‘coherent’?

11. �Coherent� means that the reader should find the principles cogent. They may be abstract, but they should convey an idea that is meaningful to a reader who is familiar with the subject, even if the principle�s full scope is not immediately evident. This approach aims to:

! help the reader make sense and order out of the law

! capture the essence of the intent of the law, so that it is clear on first approach

! write the law in a non-technical style, avoiding the use of expressions that can only be understood by referring to definitions or other lower level rules

! make the law intuitive or obvious to someone who understands its intent and context.

Chapter 2: Legislative design of the Fuel Tax Credit System

Page 11

12. The advantages offered by principles-based tax law are that it:

! is conceptually clearer and usually shorter

! promotes long-term certainty, by providing a framework for working out how the law applies to developments that were not contemplated at the time the law was written

! makes the law more stable, with less need for modifications and changes.

Carve-outs and add-ons

13. At times, a coherent principle may be wider in its application than the policy intent, for example it may encompass more situations than desired. Rather than modifying the principle in a way that results in a loss of coherence, carve-outs from the operation of the principle should be used.

14. Alternatively, a principle may not cover a situation that needs to be treated in a similar way. An add-on to the principle is therefore identified, unless there is a coherent way of reforming the principle at a higher level.

15. The aim is for the principles to be consistent with the �benchmark� tax principles and that deviations from the benchmark be made explicitly. This results in more coherent outcomes in the law.

Is it possible that the coherent principles approach will make the application of the law less certain?

16. There is an argument that the traditional �black letter� law approach to tax design provides greater certainty for taxpayers because it sets out how the law will apply in their particular circumstances.

17. But the end product is long and complex and, no matter how much care is taken to address all known circumstances, new circumstances will emerge as business practices change over time.

18. In that event, the black letter approach is actually less certain, because the reader often can�t work out how, in principle, the law should apply to those new and emerging circumstances.

19. Principled law, on the other hand, while not usually providing specific details about the cases it covers, will provide a framework for working out how it applies to each of those cases, including the newly emerging ones. Hence principled law will be more stable, with fewer amendments needed to address particular circumstances that were not contemplated when the law was drafted.

How will the detail be provided?

20. The coherent principles approach can accommodate detailed or specific rules when they are needed. However, such rules will not be provided as a matter of course. The

Fuel Tax Credit Reform Discussion Paper

Page 12

approach requires a plan for unfolding the principles and for providing detail about how the principles will apply to a particular case (usually the most common cases). This unfolding can take place in the law itself, or in the regulations, but will mostly be undertaken in the Explanatory Memorandum.

21. After enactment, the law will continue to be unfolded, where necessary, through practical application of the law, including, as now, by rulings made by the Commissioner of Taxation.

Page 13

CHAPTER 3: ENTITLEMENT TO A FUEL TAX CREDIT

This chapter examines the principles that define an entity�s entitlement to a fuel tax credit. Each principle describes the legislative outcome intended to be achieved. Carve-outs are used to narrow the intent of the principle where it is too wide in its application. Where a principle does not cover a situation that will be treated similarly, an add-on is used to modify the principle. Commentary is provided on each principle to explain how it operates.

Coherent Principle 1: Scope of the measure — incidence of fuel taxation

Principle

Fuel tax will apply to all fuels capable of being used in transport applications.

Commentary

1. As part of the 2003-04 Budget, the Government announced the commencement of a process to implement important long-term reforms to the taxation of all fuels. As part of this process all currently untaxed fuels used in internal combustion engines will be brought into the fuel tax system. At the time of the announcement the Government noted that the intention is to target transport applications.

2. The introduction of fuel tax for currently untaxed fuels will be gradually phased in from 1 July 2011 over a transitional period, with final rates being in place on 1 July 2015. Fuels that will become taxable from 1 July 2011 will include LPG, LNG and CNG.

3. Fuel tax is currently levied on fuels under the Excise Act 1901 and Customs Act 1901 and associated legislation (that is, the respective tariff Acts). The Fuel Tax Act will establish a uniform system for taxation of fuels, both locally produced and imported. The Act will facilitate the taxing of gaseous fuels from 1 July 2011, when fuel tax is first levied on LPG, LNG and CNG. In the longer term, the Act may also accommodate the taxation of those fuels currently taxed through the Excise and Customs legislation, such as petrol, diesel and other petroleum products.

Coherent Principle 2: Business use of taxable fuels

Principle

You are entitled to a fuel tax credit for taxable fuel that you acquire, or import into Australia, to be consumed in carrying on your enterprise.

Add-on: Fuel sold for private use other than in an internal combustion engine

4. You are entitled to a fuel tax credit if you sell fuel to a private household for use as a burner fuel in heating applications, or if you package fuel for non-fuel uses in containers of a defined capacity for resale in a retail outlet. The Treasury discussion

Fuel Tax Credit Reform Discussion Paper

Page 14

paper, Review of the Schedule to the Excise Tariff Act seeks industry views on the appropriate container level under which use of fuel for non-fuel purposes is essentially private use. That paper will be available shortly.

5. The use of fuel in private applications such as heating and non-fuel uses will be effectively fuel tax-free. A fuel tax credit will be provided to the sellers and packagers of the fuels rather than requiring the private users to register to claim the fuel tax credit. It is expected that the fuel tax-free status of these fuels will be reflected in the price of the fuel to the private end user.

Carve-out 2.1: Requirement to be registered for GST

6. You are not entitled to a fuel tax credit unless you are registered for the GST.

7. If you are a volunteer organisation you will not be required to be registered for the GST to claim a fuel tax credit for fuel used in operating an emergency vehicle.

8. If you are a non-resident who acts through an Australian resident agent, that agent will be able to register for GST and claim the fuel tax credit on your behalf.

Commentary

9. An entity must be registered for the GST to be entitled to claim a fuel tax credit. This means that it will need to be carrying on an enterprise or intending to carry on an enterprise from a particular date, according to the meaning of �enterprise� in the GST legislation.

Entities currently entitled to a grant under the Energy Grants (Credits) Scheme

10. An entity that is an existing claimant under the Energy Grants (Credits) Scheme and is also registered for the GST will not be required to undertake any additional procedures in order to claim a fuel tax credit. Current claimants who are not registered for the GST will need to meet the requirements for registration under the GST legislation and become registered before they will be entitled to claim a fuel tax credit.

Entities with a low annual turnover

11. Under the GST legislation, entities with a low annual turnover ($50,000 or less for business or $100,000 or less for a non-profit body) may choose whether or not to register for GST. However, a fuel tax credit will not be available to entities not registered for the GST, regardless of turnover. The exception to this will be volunteer organisations that operate emergency vehicles. Under the GST legislation, entities not registered for the GST cannot claim input tax credits for the GST that they pay on business inputs, including fuel. Under the fuel tax credits system they will also forfeit their entitlement to claim a fuel tax credit should they choose to remain unregistered.

Volunteer organisations that use fuel in emergency vehicles

12. Volunteer organisations not registered for the GST that currently receive credits under the Energy Grants (Credits) Scheme for the use of fuel in emergency vehicles will not be required to register for the GST to claim a fuel tax credit. Similarly, volunteer organisations operating emergency vehicles that become entitled to claim a fuel tax

Chapter 3: Entitlement to a fuel tax credit

Page 15

credit for the first time after 1 July 2006 will not be required to register for the GST but may choose to do so.

Non-residents

13. Non-residents can register for the GST if they are carrying on an enterprise or intend to carry on an enterprise from a particular date. They will need to be registered for GST to claim a fuel tax credit unless they act through an Australian resident agent.

14. Where a non-resident acts through a resident agent, the agent is responsible for the GST consequences of those actions. The effect of this is that:

! if a non-resident is registered, the agent must also be registered

! GST payable on sales or importations made through the agent is payable by the agent, not the non-resident

! input tax credits for purchases or importations made through the agent are claimed by the agent, not the non-resident.

Branches, groups and joint ventures

15. Special rules apply under the GST legislation to provide flexibility in the way certain businesses deal with their GST liabilities and input tax credit entitlements. These rules cover the treatment of GST branches, GST groups and GST joint ventures. These rules are discussed at paragraphs 16 to 19 of Chapter 4.

16. Under the fuel tax credit system, businesses will align their arrangements for claiming fuel tax credits with the way they report for the GST. This means that fuel tax credits will be dealt with in the same way as the input tax credit allowed under the GST law for the purchase of the fuel.

Carve-out 2.2: Use of fuel in a vehicle with a gross vehicle mass of less than 4.5 tonnes in travelling on a public road

17. You are not entitled to a fuel tax credit for fuel you acquire or import into Australia to be consumed in a vehicle with a gross vehicle mass of less than 4.5 tonnes, in travelling on a public road.

Commentary

18. The 4.5 tonne gross vehicle mass cut-off was chosen because:

! it is more difficult to distinguish between private and business use of fuel in vehicles with a smaller gross vehicle mass

! additional licensing conditions must be met in all Australian jurisdictions to drive a vehicle of this mass or greater

! providing a fuel tax credit for all on-road business uses of fuel would have a prohibitive revenue cost.

Fuel Tax Credit Reform Discussion Paper

Page 16

Meaning of ‘gross vehicle mass’

19. A vehicle�s �gross vehicle mass� means: the gross vehicle mass or if the vehicle is a prime mover, the gross combination mass as accepted by the authority that registered the vehicle, whether that is a state authority or the vehicle is registered under the Federal Interstate Registration Scheme.

Meaning of ‘Australia’

20. �Australia� does not include any external Territory, but does include an installation which is deemed by section 5 of the Customs Act 1901 to be part of Australia.

Meaning of ‘public road’

21. A road is a public road if it is:

! opened, declared or dedicated as a public road under a statute

! vested in a government authority having statutory responsibility for the control and management of public road infrastructure

! dedicated as a public road at common law.

22. A road is not a public road if it is a:

! road constructed or maintained under a statutory regime by a public authority that is not an authority responsible for the provision of road transport infrastructure, in circumstances where the statutory regime provides that public use of, or access to, the road is subordinate to the primary objects of the statutory regime

! forestry road

! private access road for use in a mining operation, or

! road, that has not been dedicated as a public road, over privately owned land.

Meaning of ‘forestry road’

23. A forestry road is a road within a forest or plantation which is constructed and maintained primarily and principally for the purposes of providing access to an area to facilitate forestry activities (for example, to facilitate trees to be planted or tended in the area, or timber felled in the area to be removed) and for related forestry management activities.

Meaning of ‘private access road for use in a mining operation’

24. A private access road for use in a mining operation is a private road which is constructed and maintained by a person who carries on a mining operation for the purposes of providing access to a mining operation, or a private road which connects a mining site and a place at which beneficiation of minerals or mineral ores occurs.

Incidental use of fuel

25. Incidental use of fuel may occur when a vehicle or piece of equipment that is used almost exclusively off-road, is moved a short distance from one off-road location to another via a public road or operating incidentally on a public road, for example, when

Chapter 3: Entitlement to a fuel tax credit

Page 17

a combine harvester that is harvesting grain on one part of a property is moved to another part of the property via a public road.

26. Similarly fuel may be used in a vehicle in an on-road application when it is stationary or when it is being moved off a public road. This is also considered to be incidental use of the fuel. Some other examples of incidental use of fuel are where:

! a vehicle is loading or unloading goods or passengers

! the agitator on a cement truck is turning while the vehicle is stationary

! the refrigeration compartment of a vehicle is cooling while the vehicle is stationary, or

! the vehicle is travelling on a private road on private property.

27. Use of fuel in a vehicle or piece of equipment otherwise giving rise to a fuel tax credit will not be denied a credit because it is incidental to the off-road operations of the vehicle or piece of equipment.

28. Use of fuel that is unrelated to the operation of the vehicle is not incidental use.

Carve-out 2.4: Requirement that a vehicle meets certain criteria

29. You are not entitled to a fuel tax credit for fuel used on-road in a diesel vehicle with a gross vehicle mass of 4.5 tonnes or more unless the vehicle meets one of the following criteria:

! it is manufactured after 1 January 1996

! it is part of an accredited audited maintenance programme

! it meets the Australian Transport Council�s in-service emission standard (referred to in the National Environment Protection (Diesel Vehicle Emissions) Measure

! it complies with a Government-endorsed maintenance schedule which includes an emissions component

! it is a dedicated farm vehicle.

Commentary

30. From 1 July 2006, in order to qualify for a fuel tax credit for diesel fuel used on-road, diesel heavy vehicle operators will need to demonstrate their vehicles meet an environmental performance benchmark. The Department of Transport and Regional Services has recently put out a tender to develop standards and documentation that will be used to ensure compliance with the benchmark.

31. The Secretary to the Department of Transport and Regional Services will have the power to determine appropriate maintenance schedules that allow vehicle operators to

Fuel Tax Credit Reform Discussion Paper

Page 18

demonstrate their vehicle is not likely to be a high polluter and to accredit an audited maintenance programme.

32. The term �dedicated farm vehicle� means:

! a vehicle used in carrying on a primary production business

! predominantly on an agricultural property

! by or on behalf of an entity that carries on a primary production business.

33. Entities claiming fuel tax credits for fuel used on-road will self-assess their compliance status with the emissions requirements. However, written records must be kept to prove the validity of a claim.

Carve-out 2.5: Aviation fuels

34. You are not entitled to a fuel tax credit for the acquisition or importation into Australia of fuel to be used in aviation.

Commentary

35. Fuel tax imposed on aviation fuels has been historically levied for the specific purpose of funding aviation regulatory bodies. Fuel tax on aviation fuels is not within the scope of the fuel tax reforms.

Coherent Principle 3: Private use of taxable fuels

Principle

You are not entitled to relief from fuel tax on fuel that you acquire or import into Australia for uses other than in carrying on your enterprise.

Carve-out: Fuel tax credit for fuel use in power generation

36. You are entitled to a fuel tax credit for taxable fuel that you acquire, or import into Australia, to be consumed in generating power at your premises.

Commentary

37. From 1 July 2006, all private use of all fuels for household electricity generation will be effectively fuel tax-free. Separate administrative arrangements from the Business Activity Statement will apply for claiming of fuel tax credits by householders for fuel consumed in electricity generation at their premises. Treasury and the ATO are currently examining options to allow private users of fuel to claim fuel tax credits.

38. Note: Business entities that claim for both private and commercial power generation may claim all their fuel tax credits on the Business Activity Statement.

Chapter 3: Entitlement to a fuel tax credit

Page 19

Coherent Principle 4: Working out how much fuel tax credit is payable on the fuel

Principle

The amount of your fuel tax credit is the amount of effective fuel tax that was payable on the fuel.

Unfolding

39. For a business, the effective fuel tax payable is worked out by assuming that the fuel tax has been calculated on the fuel at the rate in force at the start of the tax period in which you acquire or import the fuel.

40. For private users of fuel, the effective fuel tax payable is worked out by assuming that the fuel tax has been calculated on the fuel at the rate in force at the beginning of the financial year in which the claim is received by the ATO.

Commentary

41. The fuel tax rates are itemised in the Excise and Customs Tariff Acts.

42. Where a fuel blend meets a particular fuel standard, for instance petrol or diesel, it will be treated as having the same fuel tax rate as the rate applicable to the standard. Where a fuel blend does not meet a fuel standard, the amount of fuel tax credit will be based on the effective fuel tax paid on the fuels that make up the blend.

43. Where a fuel is a blend of fuels (other than a blend that meets a particular fuel standard), the amount of fuel tax credit will not be more than the effective fuel tax paid on the fuels that make up the blend.

44. If entities acquire or import fuel for eligible and ineligible use they will need to apportion the use of the fuel between eligible and ineligible uses to determine the amount of the fuel that is eligible for a fuel tax credit. The deductive or constructive methods of calculation may be used to establish the amount of the fuel eligible for a fuel tax credit.

45. An entity may choose the type of calculation method that is most appropriate to its circumstances and pattern of fuel usage.

46. Under the constructive method, claimants calculate the quantity of fuel eligible for a fuel tax credit in a tax period by adding the amounts of fuel acquired or imported that were used or are intended to be used in each eligible activity.

47. Under the deductive method, claimants deduct from the fuel acquired or imported, the quantity of fuel that was used or is intended to be used in each ineligible activity to arrive at the quantity of fuel that is eligible for a fuel tax credit.

Fuel Tax Credit Reform Discussion Paper

Page 20

Carve-out 4.1: Fuel tax imposed to fund a cleaner fuel grant

48. You must reduce the amount of your fuel tax credit by any fuel tax that is imposed to fund a cleaner fuel grant.

Commentary

49. The Government announced in the 2003-04 Budget that from 1 January 2006, the fuel tax on petrol will increase for a period of two years to fund a cleaner fuel grant for the production or importation of premium unleaded petrol with less than 50 parts per million sulphur. Similarly, the fuel tax on diesel will increase for a period of two years from 1 January 2007 to fund a cleaner fuel grant for diesel with less than 10 parts per million sulphur. The initiative, including the additional fuel tax rates required to fund the proposal, will be reviewed in the period prior to implementation to ensure that it aligns with the timing of the new fuels standards and market conditions. The indicative fuel tax increase would be 0.7 cents per litre on all diesel and 0.06 cents per litre on all petrol, to fund subsidies for the increased production costs of 1.0 cent per litre for 10 parts per million sulphur diesel and 1.1 cents per litre for 50 parts per million sulphur premium unleaded petrol.

50. The fuel tax credit allowed for these fuels during the years when the grant is available will be net of the amount of the additional fuel tax imposed.

Carve-out 4.2: Fuel tax offset by a cleaner fuel grant or production subsidy

51. You must reduce the amount of your fuel tax credit by any cleaner fuel grant or production subsidy that reduces the effective fuel tax paid on the fuel that has been paid or is payable for the fuel.

52. Note: This reduction reflects the fact that the subsidy is a partial return of the fuel tax embedded in the fuel, reducing the amount of fuel tax effectively paid on the fuel.

Commentary

53. Certain fuels are eligible for the payment of a production subsidy for the importation or domestic manufacture of the fuel. A production subsidy is currently available to offset the fuel tax payable on biodiesel. This subsidy will maintain the effective fuel tax rate of zero for 100 per cent biodiesel until 30 June 2011. The subsidy is also payable on fuel blends containing biodiesel, extending the effective fuel tax rate of zero to the biodiesel component of fuel blends for the same period. Similar arrangements apply to domestically produced ethanol under an arrangement administered by the Department of Industry, Tourism and Resources.

54. The subsidies payable for biodiesel and ethanol will be progressively reduced in five even annual instalments, beginning 1 July 2011 and ending 1 July 2015, to arrive at a final fuel tax rate for these fuels.

55. If a fuel receives a subsidy, the available fuel tax credit will be reduced by the amount of the grant or subsidy that has been paid on the fuel. Biodiesel and ethanol are

Chapter 3: Entitlement to a fuel tax credit

Page 21

currently taxed at 38.143 cents per litre. Producers receive a subsidy equivalent to the tax on the fuel, making the effective fuel tax on the fuel zero. As no effective fuel tax has been paid there will not be any entitlement to a fuel tax credit for the use of the fuels before 1 July 2011, other than where they are contained in a fuel blend that meets a particular fuel standard (see paragraph 42 above).

Carve-out 4.3: Entitlement to a drawback of duty

56. The amount of fuel tax credit you are entitled to will be reduced by the amount of any drawback of duty that you receive.

Commentary

57. In certain circumstances, an entity may be entitled to a drawback of duty under the Customs Regulations 1926 or the Excise Regulations 1925 on diesel fuel for which they also qualify for a fuel tax credit. Where this is the case, the amount of the fuel tax credit payable will be reduced by the amount of the drawback paid to the entity.

Carve-out 4.4: Road-user charge

58. The amount of fuel tax credit that you are entitled to for fuel used in a registered vehicle travelling on a public road is the fuel tax paid on the fuel minus the applicable road-user charge.

Commentary

59. You are not entitled to a fuel tax credit for fuel you acquire or import into Australia for use in a registered vehicle with a gross vehicle mass of 4.5 tonnes or more, in travelling on a road, except to the extent that the fuel tax paid on the fuel exceeds the applicable road-user charge.

Application of the road-user charge

60. The net fuel tax (fuel tax minus the fuel tax credit) collected from on-road vehicle operators will represent an official non-hypothecated road-user charge. This charge will be set in accordance with the National Transport Commission�s heavy vehicle charging determination process. The fuel tax-based charge will be adjusted annually in a similar fashion to the way that the States and Territories adjust registration fees for heavy vehicles. Changes to the charge will be made by varying the level of fuel tax credit paid for fuel used in heavy vehicles.

61. The road-user charge for petrol and alternative fuels will be the same as for diesel.

Meaning of ‘registered vehicle’

62. Registered vehicle means a vehicle that is registered for use on public roads.

Fuel Tax Credit Reform Discussion Paper

Page 22

Coherent Principle 5: Change in purpose for which the fuel is acquired or imported

Principle

If you use the fuel for a purpose for which it was not acquired or imported, you must make an adjustment to the fuel tax credit (including a zero credit) that you have claimed for the fuel.

You should make that adjustment in the tax period in which the fuel was used for the purpose other than for which it was acquired or imported.

Commentary

63. An entity need only acquire or import fuel before claiming a fuel tax credit�it will not need to have actually used the fuel. However, if the entity does not in fact use the fuel for the purpose for which it acquired or imported it, an adjustment must be made to reflect that. It may be that the activity in which the fuel is actually consumed is different from that which was intended, for example a proportion of the fuel is consumed for a private purpose or the consumption of the fuel results in a different fuel tax credit rate being applicable to the actual use.

64. A fuel tax credit adjustment will increase or decrease an entity�s tax liability for a tax period.

Coherent Principle 6: Where there is no prospect of the fuel being used

Principle

If you have no real prospect of being able to use the fuel, you must make an adjustment to the fuel tax credit that you have claimed in respect of the fuel.

You should make that adjustment in the tax period in which there stops being any reasonable prospect of the fuel being used.

Commentary

65. An adjustment to the amount of fuel tax credit will need to be made where it turns out that the fuel is not used for a creditable purpose, for example, a supply of fuel that an entity has paid for or been invoiced for, is cancelled or not delivered or the fuel is lost, stolen or otherwise disposed of.

Chapter 3: Entitlement to a fuel tax credit

Page 23

Coherent Principle 7: The Greenhouse Challenge Plus Programme

Principle

Entities claiming more than $3 million in fuel tax credits in a financial year under the Fuel Tax Act will not be entitled to payment of any fuel tax credit unless they are members of the Greenhouse Challenge Plus Programme.

Add-on

66. An entity who is a member of the Greenhouse Challenge Plus Programme is entitled to payment of fuel tax credits for fuel acquired or imported into Australia prior to it becoming a member of the Greenhouse Challenge Plus Programme.

Unfolding

67. From 1 July 2006, the receipt of fuel tax credits by entities claiming more than $3 million a year will be conditional on those entities participating in the Greenhouse Challenge Plus Programme.

68. A series of rules will apply to entities claiming more than $3 million in fuel tax credits:

! Entities claiming credits totalling more than $3 million in a financial year will not be entitled to receive payment of any credits they may otherwise be entitled to, unless at the time they make a claim they are members of the Greenhouse Challenge Plus Programme.

! Entities who are entitled to more than $3 million in credits in a financial year will be subject to the Greenhouse Challenge Plus Programme membership requirements.

! The Greenhouse Challenge Plus Programme membership requirements will be applied to an entity consistent with the way in which the entity reports for GST purposes.

! The membership requirements for the Greenhouse Challenge Plus Programme are set out in the Greenhouse Challenge Plus Programme Framework 2005, as amended from time to time.

! The Secretary to the Department of the Environment and Heritage will be responsible for deciding whether an entity is a member of the Greenhouse Challenge Plus Programme.

! The Secretary to the Department of the Environment and Heritage and the Commissioner of Taxation may exchange information on taxpayers who are likely to claim more than $3 million in credits, for the purposes of determining whether they are Greenhouse Challenge Plus Programme members and therefore able to receive those credits.

Fuel Tax Credit Reform Discussion Paper

Page 24

Commentary

69. Where an entity becomes a member of the Greenhouse Challenge Plus Programme it will be entitled to the payment of any fuel tax credits for fuel that they acquired or imported into Australia before it joined the programme.

70. Membership of the Greenhouse Challenge Plus Programme is intended to encourage the prudent management of energy use by significant energy users, such as large mining and transport companies. As members of the programme, fuel tax credit recipients will measure their greenhouse emissions, develop action plans for abatement and report annually on progress.

71. An entity will need to self-assess its entitlements to fuel tax credits under the Energy Grants (Credits) Scheme and the Fuel Tax Act in a financial year to determine whether it will need to become a member of the Greenhouse Challenge Plus Programme.

72. As with other aspects of fuel tax credits, the Greenhouse Challenge Plus Programme criterion will apply on a self-assessment basis.

Application to branches, groups and joint ventures

73. Entities operating through branches, GST groups, or GST joint ventures will operate under the fuel tax credit system in the same way that they do for GST purposes under the Business Activity Statement. In respect of the application of the Greenhouse Challenge Plus Programme that means:

! the $3 million threshold for entities operating through branches will be calculated as the sum of fuel tax credits received by the parent and all of its branches

– If the criterion applies, then the entity (parent and branches) will be required to join the Greenhouse Challenge Plus Programme to be entitled to payment of fuel tax credits.

! the $3 million threshold for entities operating within a GST group will be calculated as the sum of fuel tax credits received by the group as a whole

– If the criterion applies, then the group member claiming fuel tax credits on behalf of the group will be required to join the Greenhouse Challenge Plus Programme and enter into a Greenhouse Challenge Plus Programme agreement on behalf of all entities within the group to be entitled to payment of fuel tax credits.

! the $3 million threshold for a GST joint venture will be calculated as the sum of fuel tax credits received by the joint venture operator on behalf of the joint venture

– If the criterion applies, then the joint venture operator will be required to join the Greenhouse Challenge Plus Programme on behalf of the GST joint venture.

– Where a joint venture operator consolidates its claims in relation to a number of GST joint ventures, the $3 million threshold will apply separately to the individual GST joint ventures within the claim, rather than to the consolidated group.

Chapter 3: Entitlement to a fuel tax credit

Page 25

– The joint venture operator will need to ensure that all the GST joint ventures that exceed the $3 million threshold are included in their Greenhouse Challenge Plus Programme agreements.

Coherent Principle 8: Schemes

Principle

The Commissioner of Taxation may disregard schemes entered into for the sole or dominant purpose of deriving a benefit (either directly or indirectly) under the Fuel Tax Act that is not expressly provided for.

Commentary

74. This principle is based on the current anti�avoidance provisions in the GST Act. It is intended to deter schemes that give an entity a benefit under the Act that is not expressly provided for. For example, if the dominant purpose or principal effect of a scheme is to give an entity a benefit by increasing its entitlement to a fuel tax credit, the Commissioner will have the power to negate the benefit obtained by declaring how much fuel tax credit the entity would have been entitled to, apart from the scheme.

Page 27

CHAPTER 4: ACCOUNTING FOR AND CLAIMING A FUEL TAX CREDIT

This chapter explains the accounting and reporting arrangements for fuel tax credits. For business entities, these arrangements will align as far as possible with the existing arrangements for the GST. Householders using fuel to generate electricity and volunteer organisations using fuel in emergency vehicles will report and claim fuel tax credits via a different arrangement to business. Treasury and the ATO are currently examining options for providing a fuel tax credit to these fuel users.

Coherent Principle 9: Fuel tax credit to be claimed in the same way as an input tax credit

Principle

Business entities will claim a fuel tax credit in the same way that they claim a GST input tax credit.

Unfolding

1. Businesses will claim their fuel tax credits on the Business Activity Statement, thus aligning the mechanism for claiming fuel tax credits with the mechanism for claiming GST input tax credits.

Commentary

Third party claiming arrangements

2. The ATO currently administers arrangements under the Energy Grants (Credits) Scheme where claimants give permission to a third party to make and/or receive grant claims on their behalf.

3. For example, one of these arrangements allows fishing cooperatives and fuel suppliers to enter into a commercial arrangement with fishers where the fuel supplier can claim a fuel grant on behalf of the fisher and sell fuel to the fisher at a price that is reduced by the amount of the eligible grant.

4. Another arrangement � e-grant � allows for fuel claims to be made through a fuel supplier or fuel card provider. Almost all e-grant claims are for fuel used in road transport.

5. These arrangements will be discontinued under the fuel tax credit system as they are contrary to the intent of the reform that all business claims for fuel tax credits will be made on the Business Activity Statement according to fixed monthly, quarterly or yearly reporting periods. In addition, third party arrangements do not fit with the wider tax implications that are intended to be met under fuel tax credit reform, such as accounting for other tax liabilities.

Fuel Tax Credit Reform Discussion Paper

Page 28

Coherent Principle 10: Application of GST tax periods

Principle

The tax periods that apply to a business for the GST will also apply for fuel tax credits.

Unfolding

6. Business entities will claim fuel tax credits in accordance with the cycle in which they lodge their Business Activity Statement, which may be monthly, quarterly or yearly. An entity will not be able, for example, to report on GST liabilities on a yearly basis but claim its fuel tax credits on a quarterly basis.

Commentary

GST instalment payers

7. The GST legislation allows certain entities with annual turnovers of less than $2 million to remit their GST by instalments. This arrangement will not be affected by the fuel tax credit system and entities who are entitled to remit GST as instalment payers may continue to do so and to claim fuel tax credits as part of their instalment return process. A fuel tax credit will not be incorporated into an entity�s instalment amount.

Coherent Principle 11: Application of GST attribution rules

Principle

Fuel tax credits will be attributed to the same tax period as the GST input tax credit for the acquisition or importation of the fuel.

Unfolding

8. The point at which a business entity becomes entitled to a fuel tax credit will depend on whether it accounts for GST on a cash basis or an accruals basis.

9. If a business entity accounts on a cash basis, the accounting of amounts paid or received is attributed only when those amounts are actually paid or received. For GST, this means that input tax credits are attributed to the periods in which consideration is paid. For fuel tax credits, a business entity will therefore attribute fuel tax credits to the period in which it pays for a supply of fuel.

10. If a business entity accounts on an accruals basis, the accounting of amounts paid or received is attributed to the period when the obligation to pay or the entitlement to be paid arises. This will normally be when a GST tax invoice has been issued or received.

11. For GST, this means that input tax credits are attributed to the period in which the acquirer:

! provided any consideration for the acquisition, or

! was issued with an invoice for the acquisition

Chapter 4: Accounting for and claiming a fuel tax credit

Page 29

whichever is the earlier.

12. For fuel tax credits a business entity will attribute its credits to the same period in which:

! it provided consideration for the supply of fuel, or

! it was issued an invoice for the supply of fuel

whichever is the earlier.

Commentary

Non-residents

13. Where an Australian resident agent acts for a non-resident, the same rules will apply to fuel tax credits as apply to the GST. The effect of this is that:

! GST input tax credits for purchases or importations of fuel made through the agent will be claimed by the agent and not the non-resident

! fuel tax credits on the purchase or importation of fuel will be claimed by the agent, not the non-resident.

Delaying a claim for a fuel tax credit

14. There may be situations where an entity does not become aware that it holds a tax invoice in respect of a creditable acquisition until after it has lodged its Business Activity Statement for the period. The GST Act allows an entity to postpone the attribution of the GST input tax credit to any tax period after it holds a tax invoice. The same rule will apply to the attribution of a fuel tax credit where an entity is unaware that it holds a tax invoice until after its BAS is lodged. Subject to the time limit on claims outlined in paragraph 15 below, an entity will be able to claim for the fuel tax credit in any tax period after it holds a tax invoice.

Time limit on claims for fuel tax credits

15. Entitlement to a fuel tax credit will expire four years after the end of the tax period to which it relates unless a claim for the credit is notified to the Commissioner before that time.

Coherent Principle 12: The GST rules that apply to the way a business is organised will also apply to fuel tax credits

Principle

If a special GST rule applies to the way an entity�s business is organised, the same rule will apply to the entity for fuel tax credits.

Fuel Tax Credit Reform Discussion Paper

Page 30

Commentary

GST branches

16. Some business entities operate through a divisional or branch structure. Their normal accounting practice may be to account on a branch or divisional basis and amalgamate their accounts once a year. As these entities are able to register branches separately for GST, the branch accounts for the GST input tax credits on the creditable acquisitions and importations that it makes. Similarly, under the fuel tax credits system each branch will claim fuel tax credits for the acquisitions or importation of fuel, separately to their parent entity.

GST groups

17. Entities may form a GST group subject to the approval of the Commissioner of Taxation. Supplies and acquisitions made wholly within a GST group are taken out of the GST system. GST on taxable supplies made to entities outside of the group is payable by one entity (the representative member). Further, the representative member is entitled to any GST input tax credits that arise from acquisitions made from entities outside of the group. Similarly, under fuel tax credits the representative member of the group will be entitled to claim fuel tax credits that relate to acquisitions or importations of fuel for the group.

GST joint ventures

18. Participants in a GST joint venture may supply goods and services to each other within the joint venture. Under the special GST rules, supplies and acquisitions made between participants of the joint venture are taken out of the GST system.

19. One participant in the GST joint venture or another entity (known as the joint venture operator) pays the GST and is entitled to the GST input tax credits that relate to supplies, acquisitions and importations that it makes for the purposes of the joint venture on behalf of the other participants in the joint venture. Similarly, under fuel tax credits the operator of a joint venture will be entitled to any fuel tax credits in respect of acquisitions or importations of fuel it makes on behalf of the other joint venturers for the purpose of the joint venture.