Embed Size (px)

Citation preview

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 1/79

Foreign exchange risk

INDEX

1Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 2/79

Foreign exchange risk

2Guru nanak college of arts, science and commerce

S.NO TOPIC PAGE

NO.1. CHAPTER 1

• Introduction• History

3-5

6-122. CHAPTER 2

• Meaning and

definition• Types of foreign

exchange risk • Advantages and

disadvantages

13

14-15

16-17

3. CHAPTER 3• Foreign exchange rate• Quotations• Types of exchange

rate systems• Determinants of FX

rates

18-19

20-22

23-27

28-32

4. CHAPTER4• Foreign exchange

market• Market participants• Financial instruments• Structure of forex

market

33-37

38-43

44-46

47-49

5. CHAPTER 5

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 3/79

Foreign exchange risk

3Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 4/79

Foreign exchange risk

Introduction

Foreign exchange business has become very important these days not

only for companies and banks but also from the country's point of view.

The foreign exchange markets, in recent times, have turned highly

volatile and turbulent and 2008 taught business to rethink about risk.

Many business enterprises basking in the glory of a booming market

suddenly realized what it means to tackle a volatile foreign exchange

market or meet risk head on.

When companies conduct business across borders, they must deal in

foreign currencies. Companies must exchange foreign currencies for

home currencies when dealing with receivables, and vice versa for

payables. This is done at the current exchange rate between the two

countries. Foreign exchange risk is the risk that the exchange rate will

change unfavorably before the currency is exchanged.

This risk usually affects businesses that export and/or import, but it can

also affect investors making international investments. For example, if money must be converted to another currency to make a certain

investment, then any changes in the currency exchange rate will cause

4Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 5/79

Foreign exchange risk

that investment's value to either decrease or increase when the

investment is sold and converted back into the original currency.

The risk that the exchange rate on a foreign currency will move against

the position held by an investor such that the value of the investment is

reduced. For example, if an investor residing in the United States

purchases a bond denominated in Japanese yen, deterioration in the rate

at which the yen exchanges for dollars will reduce the investor's rate of return, since he or she must eventually exchange the yen for dollars.

Also called exchange rate risk.

The risk that the return on an investment may be reduced or eliminated

because of a change in the exchange rate of two currencies. For

example, if an American has a CD in the United Kingdom worth 1

million British pounds and the exchange rate is 2 USD: 1 GBP, then the

American effectively has $2 million in the CD. However, if the

exchange rate changes significantly to, say, 1 USD: 1 GBP, then the

American only has $1 million in the CD, even though he/she still has 1

million pounds. Foreign exchange risk is also called exchange rate risk.

Foreign exchange risk is the exposure of an institution to the potential

impact of movements in foreign exchange rates.5

Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 6/79

Foreign exchange risk

Foreign exchange risk arises from two factors: currency mismatches in

an institution’s assets and liabilities (both on- and off-balance sheet) that

are not subject to a fixed exchange rate. Such risk continues until the

foreign exchange position is covered. This risk may arise from a variety

of sources such as foreign currency retail accounts and retail cash

transactions and services, foreign exchange trading, investments

denominated in foreign currencies and investments in foreign

companies. The amount at risk is a function of the magnitude of potential exchange rate changes and the size and duration of the foreign

currency exposure.

6Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 7/79

Foreign exchange risk

History

The foreign exchange market (fx or forex) as we know In a typical

foreign exchange transaction, a party purchases a quantity of one

currency by paying a quantity of another currency. The modern foreign

exchange market began forming during the 1970s when countries

gradually switched to floating exchange rates from the previous exchange rate regime , which remained fixed as per the Bretton

Woods system .

w it today originated in 1973. However, money has been around in one

form or another since the time of Pharaohs. The Babylonians are

credited with the first use of paper bills and receipts, but Middle Eastern

moneychangers were the first currency traders who exchanged coins

from one culture to another. During the middle ages, the need for

another form of currency besides coins emerged as the method of

choice. These paper bills represented transferable third-party payments

of funds, making foreign currency exchange trading much easier for

merchants and traders and causing these regional economies to flourish.

7Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 8/79

Foreign exchange risk

From the infantile stages of forex during the Middle Ages to WWI, the

forex markets were relatively stable and without much speculative

activity. After WWI, the forex markets became very volatile and

speculative activity increased tenfold. Speculation in the forex market

was not looked on as favorable by most institutions and the public in

general. The Great Depression and the removal of the gold standard in

1931 created a serious lull in forex market activity. From 1931 until

1973, the forex market went through a series of changes. These changesgreatly affected the global economies at the time and speculation in the

forex markets during these times was little, if any.

The Bretton Woods Accord

The first major transformation, the Bretton Woods Accord, occurred toward the

end of World War II. The United States, Great Britain and France met at the

United Nations Monetary and Financial Conference in Bretton Woods, N.H. to

design a new global economic order. The location was chosen because, at the time,

the U.S. was the only country unscathed by war. Most of the major European

countries were in shambles. Up until WWII, Great Britain's currency, the Great

British Pound, was the major currency by which most currencies were compared.

This changed when the Nazi campaign against Britain included a major counterfeiting effort against its currency. In fact, WWII vaulted the U.S. dollar

from a failed currency after the stock market crash of 1929 to benchmark currency

8Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 9/79

Foreign exchange risk

by which most other international currencies were compared. The Bretton Woods

Accord was established to create a stable environment by which global economies

could restore themselves. The Bretton Woods Accord established the pegging of

currencies and the International Monetary Fund (IMF) in hope of stabilizing the

global economic situation.

Now, major currencies were pegged to the U.S. dollar. These currencies wereallowed to fluctuate by one percent on either side of the set standard. When a

currency's exchange rate would approach the limit on either side of this standard

the respective central bank would intervene to bring the exchange rate back into

the accepted range. At the same time, the US dollar was pegged to gold at a price

of $35 per ounce further bringing stability to other currencies and world forex

situation.

The Bretton Woods Accord lasted until 1971. Ultimately, it failed, but did

accomplish what its charter set out to do, which was to re-establish economic

stability in Europe and Japan.

The Beginning of the free-floating system

After the Bretton Woods Accord came the Smithsonian Agreement in December of

1971. This agreement was similar to the Bretton Woods Accord, but allowed for agreater fluctuation band for the currencies. In 1972, the European community tried

to move away from its dependency on the dollar. The European Joint Float was

9Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 10/79

Foreign exchange risk

established by West Germany, France, Italy, the Netherlands, Belgium and

Luxemburg. The agreement was similar to the Bretton Woods Accord, but allowed

a greater range of fluctuation in the currency values.

Both agreements made mistakes similar to the Bretton Woods Accord and in 1973

collapsed. The collapse of the Smithsonian agreement and the European Joint Float

in 1973 signified the official switch to the free-floating system. This occurred by

default as there were no new agreements to take their place. Governments were

now free to peg their currencies, semi-peg or allow them to freely float. In 1978,the free-floating system was officially mandated.

In a final effort to gain independence from the dollar, Europe created the European

Monetary System in July of 1978. Like all of the previous agreements, it failed in

1993.

The major currencies today move independently from other currencies. The

currencies are traded by anyone who wishes. This has caused a recent influx of

speculation by banks, hedge funds, brokerage houses and individuals. Central

banks intervene on occasion to move or attempt to move currencies to their desired

levels. The underlying factor that drives today's forex markets, however, is supply

and demand. The free-floating system is ideal for today's forex markets. It will be

interesting to see if in the future our planet endures another war similar to those of the early 20th century.

TIMELINE OF FOREIGN EXCHANGE

10Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 11/79

Foreign exchange risk

• 1944 Bretton Woods Accord is established to help stabilize the global

economy after World War II.• 1971 Smithsonian Agreement established to allow for greater fluctuation

band for currencies.• 1972 European Joint Float established as the European community tried to

move away from its dependency on the U.S. dollar.• 1973 Smithsonian Agreement and European Joint Float failed and signified

the official switch to a free-floating system.•

1978 The European Monetary System was introduced so other countriescould try to gain independence from the U.S. dollar.

• 1978 Free-floating system officially mandated by the IMF.• 1993 European Monetary System fails making way for a world-wide free-

floating system.

Barter

Before paper money became a medium of exchange the barter exchange allowed

people to exchange both goods and services. For example a farmer might exchange

grain for firewood or a cow for food. Even today international barter systems

remain in use throughout the world. Sometimes in a quite sophisticated fashion.

Nevertheless it was the introduction of paper money that allowed the development

of sophisticated international commerce by establishing a set of common

characteristics for the money for all countries.

The Gold Standard System

11Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 12/79

Foreign exchange risk

Precious metals in the form of gold or silver coins were a perfect example of early

types of money. An important concept of early paper money was that it was

backed by gold or silver. The holder could request convertibility to gold at any

time. Ultimately people’s faith in the value of paper money was linked to the

underlying value of hard assets in each country. In fact the gold standard ensured

the soundness of everybody’s money and controlled inflation as well.

When a holder of paper money in the U.S. found the value of his dollar holdings

falling in terms of gold he could exchange dollars for gold. This had the effect of reducing the amount of dollars in circulation. As the supply of dollars fell its value

stabilized and then rose. Thus the exchange of dollars for gold reserves was

reversed. As long as the discipline of linking each countries currency to reserves of

gold the simple economics of supply and demand would dictate both currency

valuation and the economics of each country. Money supply was linked to the

success of the economy and the ability of the country to retain reserves of gold.

The gold standard system of exchange sounds ideal. Currency values linked to a

universally recognised store of value, with low interest rates and virtually no

inflation, yet the gold standard ended in the early 1930’s. Why did the world’s

monetary authorities move away from the gold standard?

The answer lies in one word ‘leverage’. The conservative monetary policies of theworld in the first half of the 20th century could not accommodate the growing

needs of the world’s economy. People could not afford to by such luxury items as

12Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 13/79

Foreign exchange risk

cars, fridges and houses with the cash balances they had. A cash balance would

only buy you a part of a car, or a fridge and an even smaller piece of a house.

Today we casually use our credit cards to buy things we need, or we obtain a loan

to buy a house or a car to leverage our current and future income streams. Imagine

how unsatisfying it would be not be able to buy items which would enhance our

life styles. We think nothing of obtaining a loan and making monthly payments out

of our cash reserves.

Let’s look at an example of finance leverage. If you bought a house for $200,000

with a down payment of 10% and an annual price increase of 10%, what do you

think would be your return on capital? It would be 100% because you only spent

$20,000 in cash for your down payment and the increase in price over one year is

also $20,000 so your return on your capital investment of $20,000 is 100%.

From then on the amount of money in circulation equalled the amount of the gold

reserves plus the amount of credit in the market. Increased credit also increases the

money supply.

13Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 14/79

Foreign exchange risk

Definition

This risk usually affects businesses that export and/or import, but it can also affect

investors making international investments. For example, if money must be

converted to another currency to make a certain investment, then any changes inthe currency exchange rate will cause that investment's value to either decrease or

14Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 15/79

Foreign exchange risk

increase when the investment is sold and converted back into the original

currency.

Meaning

Foreign exchange is essential to coordinate international business transactions.

Foreign exchange describes the process of trading different currencies to make and

receive payments. Additionally, investors look to foreign exchange markets to

trade currencies for a profit. These foreign exchange transactions do carry distinct

risks. In order to minimize risks, you should understand the factors related tocurrency fluctuations, before coordinating business strategy.

Types of foreign exchange risk

• Credit risk : The risk that a counterparty will not settle an obligation for

full value, either when due or at any time thereafter.

15Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 16/79

Foreign exchange risk

• Replacement risk : The risk that counterparty to an outstanding

transaction for completion at a future date will fail to perform on the

settlement date.This failure may leave the solvent party with an unhedged or

open market position or deny the solvent party unrealised gains on the

position. The resulting exposure is the cost of replacing, at current market

prices, the original transaction.

• Systemic risk : The risk that the failure of one participant in a transfer

system, or in financial markets generally, to meet its required obligations

when due will cause other participants or financial institutions to be unable

to meet their obligations (including settlement obligations in a transfer

system) when due. Such a failure may cause significant liquidity or credit

problems and, as a result, might threaten the stability of financial markets

and confidence in the market.

• Legal risk : The risk that a counterparty will incur damage because laws or

regulations are inconsistent with the rules of the settlement system,

settlement arrangements or other interests entrusted to the settlement system.

Legal risk is also created by unclear or unsystematic application of laws and

regulations.

• Liquidity risk : The risk that a counterparty (or participant in a settlement

system) will not settle an obligation for full value when due. Liquidity risk

16Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 17/79

Foreign exchange risk

does not imply that a counterparty or participant is insolvent since it may be

able to settle the required debit obligations at some time thereafter.

• Market risk : The risk that an institution or other trader will experience a

loss on a trade owing to an unfavourable exchange rate movement .

• Operational risk : The risk of incurring interest charges or other penalties

for misdirecting or otherwise failing to make settlement payments on time

owing to an error or technical failure.

17Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 18/79

Foreign exchange risk

Advantages

Leverage - Huge leverage is available in Forex trading, often up to 100:1

meaning that large profits can be generated from small margin deposits.

Liquidity - The enormous size and global trading of the forex markets means that

the markets in the major currency pairs are very liquid making trade executions

almost instant with little slippage.

Ability to go short - Since currency trading always involves buying one

currency and selling another, there is no structural bias to the market. This means a

trader has equal potential to profit in a rising or falling market.

Trends - Fundamentally, the value of a country's currency is determined by

interest rates and the strength of the economy in relation to other countries.

Currencies, therefore, have a greater tendency to trend until the fundamentals

change.

18Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 19/79

Foreign exchange risk

Disadvantages

Leverage - With huge leverage available to forex traders the danger is that

positions which carry too much risk for the account size can be taken on, leading to

margin calls. Effective money management rules must be adhered to.

Brokers - Retail traders must use a broker rather than dealing directly in the

interbank market. The broker will be the counterparty in all transactions and is,

effectively, making the market. They can, therefore, widen spreads or even refuse

to trade during volatile trading conditions. To avoid dealing with brokers an

alternative to forex is to use futures. See online futures trading for more details.

Spreads - As the retail trader must use a broker to trade, they cannot deal at the

interbank rates. A broker will generally quote a fixed spread of 3-20 pips

depending on the currency pair. The underlying interbank rate might be as little as

1 pip.

19Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 20/79

Foreign exchange risk

Foreign exchange rate

Rate at which one currency may be converted into another. also called rate of

exchange or exchange rate or currency exchange rate.

A foreign exchange rate is the price of one currency in terms of another. For

example, suppose the foreign exchange rate for the Japanese yen vis-à-vis the U.S.

dollar is ¥100 = $1. If the foreign exchange rate changes to, say, ¥110 = $1, theyen is now weaker and the dollar stronger, since it now costs 10 yen more to buy a

single dollar. But if the foreign exchange rate changed to ¥90 = $1, the yen is now

worth more, since it only costs 90 yen to buy a dollar. The foreign exchange rate

for the yen could also strengthen against the dollar while its foreign exchange rate

against other currencies weakens. A currency's foreign exchange rate is determined

by many factors, including the macroeconomic, monetary, and trade policies of its

own country and those of other nations. The foreign exchange rate is key for

investors when buying stocks quoted in currencies other than their own, because

the foreign exchange rate will determine the amount they receive in their own

currency upon sale.

20Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 21/79

Foreign exchange risk

Terms related to Exchange Rates:

• Short Rate

The short rate is an abbreviation for 'short term interest rate'; that is, the interestrate charged (usually in some particular market) for short term loans.

• Bill of Exchange

A bill of exchange is from the late Middle Ages. A bill of exchange is a contract

entitling an exporter to receive immediate payment in the local currency for goods

that would be shipped elsewhere. Time would elapse between payment in onecurrency and repayment in another, so the interest rate would also be brought into

the transaction

• Purchasing Power Parity

PPP stands for purchasing power parity, a criterion for an appropriate exchange

rate between currencies. It is a rate such that a representative basket of goods incountry A costs the same as in country B if the currencies are exchanged at that

rate.

21Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 22/79

Foreign exchange risk

Actual exchange rates vary from the PPP levels for various reasons, such as the

demand for imports or investments between countries.

Quotations

An exchange system quotation is given by stating the number of units of "quotecurrency" (price currency, payment currency) that can be exchanged for one unit of

"base currency" (unit currency, transaction currency). For example, in a quotation

that says the EUR/USD exchange rate is 1.2290 (1.2290 USD per EUR, also

known as EUR/USD; see foreign exchange market), the quote currency is USD

and the base currency is EUR.

There is a market convention that determines which is the base currency and which

is the term currency. In most parts of the world, the order is: EUR – GBP – AUD –

NZD – USD – others. Thus if you are doing a conversion from EUR into AUD,

EUR is the base currency, AUD is the term currency and the exchange rate tells

you how many Australian dollars you would pay or receive for 1 euro. Cyprus and

Malta which were quoted as the base to the USD and others were recently removed

from this list when they joined the euro. In some areas of Europe and in the non- professional market in the UK, EUR and GBP are reversed so that GBP is quoted

as the base currency to the euro. In order to determine which is the base currency

22Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 23/79

Foreign exchange risk

where both currencies are not listed (i.e. both are "other"), market convention is to

use the base currency which gives an exchange rate greater than 1.000. This avoids

rounding issues and exchange rates being quoted to more than 4 decimal places.

There are some exceptions to this rule e.g. the Japanese often quote their currency

as the base to other currencies.

Quotes using a country's home currency as the price currency (e.g., EUR 0.735342

= USD 1.00 in the euro zone) are known as direct quotation or price quotation

(from that country's perspective) and are used by most countries.

Quotes using a country's home currency as the unit currency (e.g., EUR 1.00 =

USD 1.35991 in the euro zone) are known as indirect quotation or quantity

quotation and are used in British newspapers and are also common in Australia,

New Zealand and the eurozone.• Direct quotation: 1 foreign currency unit = x home currency units• Indirect quotation: 1 home currency unit = x foreign currency units

Note that, using direct quotation, if the home currency is strengthening (i.e.,appreciating, or becoming more valuable) then the exchange rate number

decreases. Conversely if the foreign currency is strengthening, the exchange rate

number increases and the home currency is depreciating.

23Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 24/79

Foreign exchange risk

Market convention from the early 1980s to 2006 was that most currency pairs were

quoted to 4 decimal places for spot transactions and up to 6 decimal places for

forward outrights or swaps. (The fourth decimal place is usually referred to as a

"pip"). An exception to this was exchange rates with a value of less than 1.000

which were usually quoted to 5 or 6 decimal places. Although there is no fixed

rule, exchange rates with a value greater than around 20 were usually quoted to 3

decimal places and currencies with a value greater than 80 were quoted to 2

decimal places. Currencies over 5000 were usually quoted with no decimal places

(e.g. the former Turkish Lira). e.g. (GBPOMR : 0.765432 - EURUSD : 1.5877 –

GBPBEF : 58.234 - EURJPY : 165.29). In other words, quotes are given with 5

digits. Where rates are below 1, quotes frequently include 5 decimal places.

In 2005 Barclays Capital broke with convention by offering spot exchange rates

with 5 or 6 decimal places on their electronic dealing platform. The contraction of

spreads (the difference between the bid and offer rates) arguably necessitated finer

pricing and gave the banks the ability to try and win transaction on multibank

trading platforms where all banks may otherwise have been quoting the same

price. A number of other banks have now followed this.

While official quotations are given with the full number, for example 1.4320,many investors and analysts drop the integer for convenience and use only the

fractional part, such as 4320. These are used frequently where a move in price is

being described, for example 4320 to 4290 as opposed to 1.4320 to 1.4290.

24Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 25/79

Foreign exchange risk

25Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 26/79

Foreign exchange risk

TYPES OF EXCHANGE RATE SYSTEMS.

We can roughly categorize countries as falling into three main categories of

exchange rate regimes.

1. Flexible exchange rate systems (also known as floating exchange rate systems.)

2. Managed floating rate systems.

3. Fixed exchange rate systems (also known as pegged exchange rate systems).

Flexible Exchange Rate Systems

• In a flexible exchange rate system, the value of the currency is determined by the

market, i.e. by the interactions of thousands of banks, firms and other institutions

seeking to buy and sell currency for purposes of transactions clearing, hedging,

arbitrage and speculation.

• So higher demand for a currency, all else equal, would lead to an appreciation of

the currency. Lower demand, all else equal, would lead to a depreciation of the

currency. An increase in the supply of a currency, all else equal, will lead to a

depreciation of that currency while a decrease in supply, all else equal, will lead to

an appreciation.

• Essentially, we can characterize the equilibrium exchange rate under a flexible

exchange rate system as the value that is consistent with covered and uncovered

26Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 27/79

Foreign exchange risk

interest rate parity given values for the expected future spot rate and the forward

exchange rate.

• Since 1971, economies have been moving towards flexible exchange rate systems

although only relatively few currencies are classifiable as truly floating exchange

rates.

• Most OECD countries have flexible exchange rate systems: the U.S., Canada,

Australia, Britain, and the European Monetary Union.

Managed Floating Rate Systems

• A managed floating rate systems is a hybrid of a fixed exchange rate and a

flexible exchange rate system. In a country with a managed floating exchange rate

system, the central bank becomes a key participant in the foreign exchange market.

• Unlike in a fixed exchange rate regime, the central bank does not have an explicit

set value for the currency; however, unlike in a flexible exchange rate regime, it

doesn’t allow the market to freely determine the value of the currency.

• Instead, the central bank has either an implicit target value or an explicit range of

target values for their currency: it intervenes in the foreign exchange market by

buying and selling domestic and foreign currency to keep the exchange rate close

to this desired implicit value or within the desired target values.

27Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 28/79

Foreign exchange risk

• Example: Suppose that Thailand had a managed floating rate system and that the

Thai central bank wants to keep the value of the Baht close to 25 Baht/$. In a

managed floating regime, the Thai central bank is willing to tolerate small

fluctuations in the exchange rate (say from 24.75 to 25.25) without getting

involved in the market.

• If, however, there is excess demand for Baht in the rest of the market causing

appreciation below the 24.75 level the Central Bank increases the supply of Baht by selling Baht for dollars and acquiring holdings of U.S dollars. Similarly if there

is excess supply of Baht causing depreciation above the 25.25 level, the Central

Bank increases the demand for Baht by exchanging dollars for Baht and running

down its holdings of U.S dollars.

• So under a managed floating regime, the central bank holds stocks of foreign

currency: these holdings are known as foreign exchange reserves. It is important to

realize that a managed float can only work when the implicit target is close to the

equilibrium rate that would prevail in the absence of central bank intervention.

Otherwise, the central bank will deplete its foreign exchange reserves and the

country will be in a flexible exchange rate system because they can no longer

intervene.

Fixed (Pegged) Exchange Rate Systems

28Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 29/79

Foreign exchange risk

• Prior to the 1970’s most countries operated under a fixed exchange rate system

known as the Bretton-Woods system. We will discuss Bretton-Woods in more

detail later, for now think of it as a system whereby the exchange rates of the

member countries were fixed against the U.S. dollar, with the dollar in turn worth a

fixed amount of gold.

• Even though this system broke down, many countries still have an exchange rate

system where the central bank announces a fixed exchange rate for the currency

and then agrees to buy and sell the domestic currency at this value.

• The basic motivation for keeping exchange rates fixed is the belief that a stable

exchange rate will help facilitate trade and investment flows between countries by

reducing fluctuations in relative prices and by reducing uncertainty.

• However, it is important to note that financial markets have developed

sophisticated derivatives that allow firms to hedge future exchange rate fluctuation

risks. Regardless, fixed exchange rates are still fairly common.

• It is important to realize that demand and supply for currency still exist as in the

case of floating exchange rates. However, changes in demand and supply

theoretically no longer affect the price of the currency, which is fixed. However, as

we will soon see, the price of the currency may only remain fixed in the short run;there may be substantial long run changes in the exchange rate.

29Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 30/79

Foreign exchange risk

• One could almost argue that the key distinction between fixed and floating rates

is a tradeoff of continuous, small changes in the exchange rate for discrete, larger

changes.

• In a fixed exchange rate system, the Central Bank stands ready to exchange local

currency and foreign currency at a pre-announced rate.

• One important concept to keep in mind is the market equilibrium exchange rate,the rate at which supply and demand will be equal, i.e. markets will clear. In a

flexible exchange rate system, this is the spot rate. In a fixed exchange rate system,

the pre-announced rate may not coincide with the market equilibrium exchange

rate.

• In any market, there will be situations of excess demand and excess supply.

Under a flexible exchange rate system, these changes cause appreciation or

depreciation of the currency respectively. Under a fixed exchange rate system the

Central Bank remains prepared to absorb the excess demand or supply.

• In order to do this exchange the Central Bank must hold stocks of both foreign

and domestic currency. Since the central bank prints domestic currency, holding

stocks of domestic currency poses no problems. The difficulty comes in holding anadequate stock of foreign currency known as foreign exchange reserves.

30Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 31/79

Foreign exchange risk

Determinants of FX rates

The following theories explain the fluctuations in FX rates in a floating exchange

rate regime (In a fixed exchange rate regime, FX rates are decided by its

government):

• International parity conditions: Relative Purchasing Power Parity, interest

rate parity, Domestic Fisher effect, International Fisher effect. Though to

some extent the above theories provide logical explanation for the

fluctuations in exchange rates, yet these theories falter as they are based on

challengeable assumptions [e.g., free flow of goods, services and capital]

which seldom hold true in the real world.

31Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 32/79

Foreign exchange risk

• Balance of payments model : This model, however, focuses largely on

tradable goods and services, ignoring the increasing role of global capital

flows. It failed to provide any explanation for continuous appreciation of

dollar during 1980s and most part of 1990s in face of soaring US current

account deficit.

• Asset market model : views currencies as an important asset class for

constructing investment portfolios. Assets prices are influenced mostly by

people’s willingness to hold the existing quantities of assets, which in turndepends on their expectations on the future worth of these assets. The asset

market model of exchange rate determination states that “the exchange rate

between two currencies represents the price that just balances the relative

supplies of, and demand for, assets denominated in those currencies.”

None of the models developed so far succeed to explain FX rates levels and

volatility in the longer time frames. For shorter time frames (less than a few days)

algorithm can be devised to predict prices. Large and small institutions and

professional individual traders have made consistent profits from it. It is

understood from above models that many macroeconomic factors affect the

exchange rates and in the end currency prices are a result of dual forces of demand

and supply. The world's currency markets can be viewed as a huge melting pot: in

a large and ever-changing mix of current events, supply and demand factors areconstantly shifting, and the price of one currency in relation to another shifts

accordingly. No other market encompasses (and distills) as much of what is going

on in the world at any given time as foreign exchange.

32Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 33/79

Foreign exchange risk

These elements generally fall into three categories:• Economic factors• Political conditions• Market psychology.

Economic factors

These include:

• economic policy, disseminated by government agencies and central banks• economic conditions, generally revealed through economic reports, and

other economic indicators.

Economic policy comprises government fiscal policy (budget/spending practices)and monetary policy (the means by which a government's central bank influences

the supply and "cost" of money, which is reflected by the level of interest rates).

Government budget deficits or surpluses: The market usually reacts negatively to

widening government budget deficits, and positively to narrowing budget deficits.

The impact is reflected in the value of a country's currency.

Balance of trade levels and trends: The trade flow between countries illustrates the

demand for goods and services, which in turn indicates demand for a country's

33Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 34/79

Foreign exchange risk

currency to conduct trade. Surpluses and deficits in trade of goods and services

reflect the competitiveness of a nation's economy. For example, trade deficits may

have a negative impact on a nation's currency.

Inflation levels and trends: Typically a currency will lose value if there is a high

level of inflation in the country or if inflation levels are perceived to be rising. This

is because inflation erodes purchasing power, thus demand, for that particular

currency. However, a currency may sometimes strengthen when inflation rises

because of expectations that the central bank will raise short-term interest rates tocombat rising inflation.

Economic growth and health: Reports such as GDP, employment levels, retail

sales, capacity utilization and others, detail the levels of a country's economic

growth and health. Generally, the more healthy and robust a country's economy,

the better its currency will perform, and the more demand for it there will be.

Productivity of an economy: Increasing productivity in an economy should

positively influence the value of its currency. Its effects are more prominent if the

increase is in the traded sector .

Political conditions

Internal, regional, and international political conditions and events can have a

profound effect on currency markets.

34Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 35/79

Foreign exchange risk

All exchange rates are susceptible to political instability and anticipations about

the new ruling party. Political upheaval and instability can have a negative impact

on a nation's economy. For example, destabilization of coalition governments in

Pakistan and Thailand can negatively affect the value of their currencies. Similarly,

in a country experiencing financial difficulties, the rise of a political faction that is

perceived to be fiscally responsible can have the opposite effect. Also, events in

one country in a region may spur positive/negative interest in a neighboring

country and, in the process, affect its currency.

Market psychology

Market psychology and trader perceptions influence the foreign exchange market

in a variety of ways:

Flights to quality: Unsettling international events can lead to a "flight to quality,"

with investors seeking a "safe haven." There will be a greater demand, thus a

higher price, for currencies perceived as stronger over their relatively weaker

counterparts. The U.S. dollar, Swiss franc and gold have been traditional safe

havens during times of political or economic uncertainty.[14]

Long-term trends: Currency markets often move in visible long-term trends.

Although currencies do not have an annual growing season like physical

commodities, business cycles do make themselves felt. Cycle analysis looks atlonger-term price trends that may rise from economic or political trends.[15]

35Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 36/79

Foreign exchange risk

"Buy the rumor, sell the fact": This market truism can apply to many currency

situations. It is the tendency for the price of a currency to reflect the impact of a

particular action before it occurs and, when the anticipated event comes to pass,

react in exactly the opposite direction. This may also be referred to as a market

being "oversold" or "overbought".[16] To buy the rumor or sell the fact can also be

an example of the cognitive bias known as anchoring, when investors focus too

much on the relevance of outside events to currency prices.

Economic numbers: While economic numbers can certainly reflect economic

policy, some reports and numbers take on a talisman-like effect: the number itself becomes important to market psychology and may have an immediate impact on

short-term market moves. "What to watch" can change over time. In recent years,

for example, money supply, employment, trade balance figures and inflation

numbers have all taken turns in the spotlight.

Technical trading considerations: As in other markets, the accumulated price

movements in a currency pair such as EUR/USD can form apparent patterns that

traders may attempt to use. Many traders study price charts in order to identify

such patterns.

36Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 37/79

Foreign exchange risk

Foreign exchange market

The foreign exchange market (forex, FX, or currency market) is a worldwide

decentralized over-the-counter financial market for the trading of currencies.

Financial centers around the world function as anchors of trading between a wide

range of different types of buyers and sellers around the clock, with the exception

of weekends. The foreign exchange market determines the relative values of

different currencies.

The primary purpose of the foreign exchange market is to assist international trade

and investment, by allowing businesses to convert one currency to another

currency. For example, it permits a US business to import British goods and pay

Pound Sterling, even though the business's income is in US dollars. It also supports

speculation, and facilitates the carry trade, in which investors borrow low-yielding

currencies and lend (invest in) high-yielding currencies, and which (it has been

claimed) may lead to loss of competitiveness in some countries.

In a typical foreign exchange transaction, a party purchases a quantity of one

currency by paying a quantity of another currency. The modern foreign exchange

market began forming during the 1970s when countries gradually switched to

floating exchange rates from the previous exchange rate regime, which remainedfixed as per the Bretton Woods system.

The foreign exchange market is unique because of

37Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 38/79

Foreign exchange risk

• its huge trading volume, leading to high liquidity;• its geographical dispersion;• its continuous operation: 24 hours a day except weekends, i.e. trading from

20:15 GMT on Sunday until 22:00 GMT Friday;• the variety of factors that affect exchange rates;• the low margins of relative profit compared with other markets of fixed

income; and• the use of leverage to enhance profit margins with respect to account size.

The foreign exchange market is the largest and most liquid financial market in the

world. Traders include large banks, central banks, currency speculators,

corporations, governments, and other financial institutions. The average daily

volume in the global foreign exchange and related markets is continuously

growing. Daily turnover was reported to be over US$3.98 trillion in April 2010 by

the Bank for International Settlements.

The foreign exchange market in India started in earnest less than three decades ago

when in 1978 the government allowed banks to trade foreign exchange with one

another. Today over 70% of the trading in foreign exchange continues to take place

in the inter-bank market. The market consists of over 90 Authorized Dealers

(mostly banks) who transact currency among themselves and come out “square” or without exposure at the end of the trading day. Trading is regulated by the Foreign

Exchange Dealers Association of India (FEDAI), a self regulatory association of

dealers. Since 2001, clearing and settlement functions in the foreign exchange

38Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 39/79

Foreign exchange risk

market are largely carried out by the Clearing Corporation of India Limited (CCIL)

that handles transactions of approximately 3.5 billion US dollars a day, about 80%

of the total transactions.The liberalization process has significantly boosted the

foreign exchange market in the country by allowing both banks and corporations

greater flexibility in holding and trading foreign currencies. The Sodhani

Committee set up in 1994 recommended greater freedom to participating banks,

allowing them to fix their own trading limits, interest rates on FCNR deposits and

the use of derivative products.

The features of the FOREX market which contributes to its growth are:

• Liquidity – Higher the liquidity, the more powerful will be from the investor side

as it gives them the choice to open or close a position of any size.

• Promptness and Availability-The FOREX market need not has to wait to give any

certain respond to any given occasion due to its 24 hour work schedule and

likelihood to trade round the clock.

• Value- Except for the natural bid market spread between the supply and demand

price the FOREX market has usually incurred no service charge.

• Market trend-Each currency reveals its own typical temporary modificationswhich represents investments managers with the chances to manipulate in the

FOREX market.

39Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 40/79

Foreign exchange risk

• Margin- Widespread credit leverages or margins in conjunction with highly

variable currency quotations makes this market a highly gainful but also very

chancy.

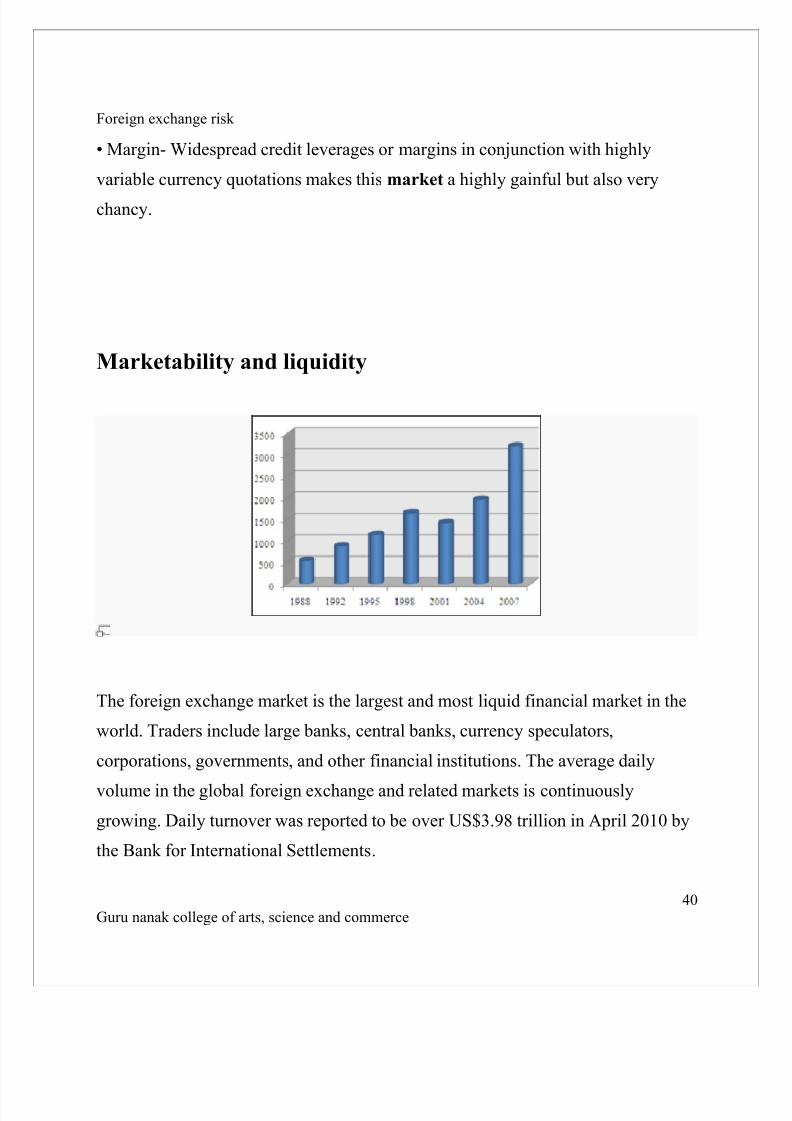

Marketability and liquidity

The foreign exchange market is the largest and most liquid financial market in the

world. Traders include large banks, central banks , currency speculators ,

corporations, governments , and other financial institutions . The average daily

volume in the global foreign exchange and related markets is continuously

growing. Daily turnover was reported to be over US$3.98 trillion in April 2010 by

the Bank for International Settlements .

40Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 41/79

Foreign exchange risk

Of the $3.98 trillion daily global turnover, trading in London accounted for around

$1.85 trillion, or 36.7% of the total, making London by far the global center for

foreign exchange. In second and third places respectively, trading in New York

City accounted for 17.9%, and Tokyo accounted for 6.2%. [4] In addition to

"traditional" turnover, $2.1 trillion was traded in derivatives .

Exchange-traded FX futures contracts were introduced in 1972 at the Chicago

Mercantile Exchange and are actively traded relative to most other futures

contracts.

Several other developed countries also permit the trading of FX derivative

products (like currency futures and options on currency futures) on their

exchanges. All these developed countries already have fully convertible capital

accounts. Most emerging countries do not permit FX derivative products on their

exchanges in view of prevalent controls on the capital accounts. However, a few

select emerging countries (e.g., Korea, South Africa, India) have already

successfully experimented with the currency futures exchanges, despite havingsome controls on the capital account.

41Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 42/79

Foreign exchange risk

Market participants

Unlike a stock market, the foreign exchange market is divided into levels of

access. At the top is the inter-bank market, which is made up of the largest

commercial banks and securities dealers. Within the inter-bank market, spreads,

which are the difference between the bid and ask prices, are razor sharp and

usually unavailable, and not known to players outside the inner circle.

The difference between the bid and ask prices widens (from 0-1 pip to 1-2 pips for

some currencies such as the EUR). This is due to volume. If a trader can guarantee

large numbers of transactions for large amounts, they can demand a smaller

difference between the bid and ask price, which is referred to as a better spread.

The levels of access that make up the foreign exchange market are determined bythe size of the "line" (the amount of money with which they are trading). The top-

tier inter-bank market accounts for 53% of all transactions.

42Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 43/79

Foreign exchange risk

After that there are usually smaller banks, followed by large multi-national

corporations (which need to hedge risk and pay employees in different countries),

large hedge funds, and even some of the retail FX-metal market makers. According

to Galati and Melvin, “Pension funds, insurance companies, mutual funds, and

other institutional investors have played an increasingly important role in financial

markets in general, and in FX markets in particular, since the early 2000s.” (2004)

In addition, he notes, “Hedge funds have grown markedly over the 2001–2004

period in terms of both number and overall size” Central banks also participate in

the foreign exchange market to align currencies to their economic needs.

• Banks

The interbank market caters for both the majority of commercial turnover and large

amounts of speculative trading every day. A large bank may trade billions of

dollars daily. Some of this trading is undertaken on behalf of customers, but much

is conducted by proprietary desks, trading for the bank's own account. Until

recently, foreign exchange brokers did large amounts of business, facilitating

interbank trading and matching anonymous counterparts for large fees. Today,

however, much of this business has moved on to more efficient electronic systems.

The broker squawk box lets traders listen in on ongoing interbank trading and isheard in most trading rooms, but turnover is noticeably smaller than just a few

years ago.

43Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 44/79

Foreign exchange risk

• Commercial companies

An important part of this market comes from the financial activities of companies

seeking foreign exchange to pay for goods or services. Commercial companies

often trade fairly small amounts compared to those of banks or speculators, and

their trades often have little short term impact on market rates. Nevertheless, trade

flows are an important factor in the long-term direction of a currency's exchange

rate. Some multinational companies can have an unpredictable impact when very

large positions are covered due to exposures that are not widely known by other

market participants.

• Central banks

National central banks play an important role in the foreign exchange markets.

They try to control the money supply, inflation, and/or interest rates and often have

official or unofficial target rates for their currencies. They can use their often

substantial foreign exchange reserves to stabilize the market. Nevertheless, the

effectiveness of central bank "stabilizing speculation" is doubtful because central

banks do not go bankrupt if they make large losses, like other traders would, and

there is no convincing evidence that they do make a profit trading.

• Forex Fixing

Forex fixing is the daily monetary exchange rate fixed by the national bank of each

country. The idea is that central bank use the fixing time and exchange rate to

44Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 45/79

Foreign exchange risk

evaluate behavior of their currency. Fixing exchange rates reflects the real value of

equilibrium in the forex market. Banks, dealers and online foreign exchange

traders use fixing rates as a trend indicator.

The mere expectation or rumor of central bank intervention might be enough to

stabilize a currency, but aggressive intervention might be used several times each

year in countries with a dirty float currency regime. Central banks do not always

achieve their objectives. The combined resources of the market can easily

overwhelm any central bank. Several scenarios of this nature were seen in the

1992–93 ERM collapse, and in more recent times in Southeast Asia.

• Hedge funds as speculators

About 70% to 90% of the foreign exchange transactions are speculative. In other

words, the person or institution that bought or sold the currency has no plan to

actually take delivery of the currency in the end; rather, they were solely

speculating on the movement of that particular currency. Hedge funds have gained

a reputation for aggressive currency speculation since 1996. They control billions

of dollars of equity and may borrow billions more, and thus may overwhelm

intervention by central banks to support almost any currency, if the economic

fundamentals are in the hedge funds' favor.

• Investment management firms

45Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 46/79

Foreign exchange risk

Investment management firms (who typically manage large accounts on behalf of

customers such as pension funds and endowments) use the foreign exchange

market to facilitate transactions in foreign securities. For example, an investment

manager bearing an international equity portfolio needs to purchase and sell

several pairs of foreign currencies to pay for foreign securities purchases.

Some investment management firms also have more speculative specialist

currency overlay operations, which manage clients' currency exposures with the

aim of generating profits as well as limiting risk. Whilst the number of this type of

specialist firms is quite small, many have a large value of assets under management (AUM), and hence can generate large trades.

• Retail foreign exchange brokers

Retail traders (individuals) constitute a growing segment of this market, both in

size and importance. Currently, they participate indirectly through brokers or

banks. Retail brokers, while largely controlled and regulated in the USA by the

CFTC and NFA have in the past been subjected to periodic foreign exchange

scams.To deal with the issue, the NFA and CFTC began (as of 2009) imposing

stricter requirements, particularly in relation to the amount of Net Capitalization

required of its members. As a result many of the smaller, and perhaps questionable

brokers are now gone.

There are two main types of retail FX brokers offering the opportunity for

speculative currency trading:

46Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 47/79

Foreign exchange risk

• Brokers serve as an agent of the customer in the broader FX market, by seeking

the best price in the market for a retail order and dealing on behalf of the retail

customer. They charge a commission or mark-up in addition to the price

obtained in the market.

• Dealers or market makers, by contrast, typically act as principal in the

transaction versus the retail customer, and quote a price they are willing to deal

at—the customer has the choice whether or not to trade at that price.

In assessing the suitability of an FX trading service, the customer should consider

the ramifications of whether the service provider is acting as principal or agent.

When the service provider acts as agent, the customer is generally assured of a

known cost above the best inter-dealer FX rate. When the service provider acts as

principal, no commission is paid, but the price offered may not be the best

available in the market—since the service provider is taking the other side of the

transaction, a conflict of interest may occur.

• Non-bank foreign exchange companies

47Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 48/79

Foreign exchange risk

Non-bank foreign exchange companies offer currency exchange and international

payments to private individuals and companies. These are also known as foreign

exchange brokers but are distinct in that they do not offer speculative trading but

currency exchange with payments. I.e., there is usually a physical delivery of

currency to a bank account. Send Money Home offers an in-depth comparison into

the services offered by all the major non-bank foreign exchange companies.

It is estimated that in the UK, 14% of currency transfers/payments are made via

Foreign Exchange Companies. These companies' selling point is usually that they

will offer better exchange rates or cheaper payments than the customer's bank.These companies differ from Money Transfer/Remittance Companies in that they

generally offer higher-value services.

• Money transfer/remittance companies

Money transfer companies/remittance companies perform high-volume low-value

transfers generally by economic migrants back to their home country. In 2007, the

Aite Group estimated that there were $369 billion of remittances (an increase of

8% on the previous year). The four largest markets (India, China, Mexico and the

Philippines) receive $95 billion. The largest and best known provider is Western

Union with 345,000 agents globally followed by UAE Exchange & Financial

Services Ltd.

FINANCIAL INSTRUMENTS

48Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 49/79

Foreign exchange risk

•

SpotA spot transaction is a two-day deliverytransaction (except in the case of trades

between the US Dollar, Canadian Dollar, Turkish Lira, EURO and Russian Ruble,

which settle the next business day), as opposed to the futures contracts , which are

usually three months. This trade represents a “direct exchange” between two

currencies, has the shortest time frame, involves cash rather than a contract; and

interest is not included in the agreed-upon transaction.

• Forward

One way to deal with the foreign exchange risk is to engage in

a forward transaction. In this transaction, money does not actually change hands

until some agreed upon future date. A buyer and seller agree on an exchange rate

for any date in the future, and the transaction occurs on that date, regardless of

what the market rates are then. The duration of the trade can be one day, a few

days, months or years. Usually the date is decided by both parties. and forward

contract is a negotiated and agreement between two parties

• Swap

The most common type of forward transaction is the currency swap . In a swap, two

parties exchange currencies for a certain length of time and agree to reverse the

transaction at a later date. These are not standardized contracts and are not traded

through an exchange.

49Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 50/79

Foreign exchange risk

•

FutureForeign currency futures are exchange traded forward transactions with standard

contract sizes and maturity dates — for example, $1000 for next November at an

agreed rate. Futures are standardized and are usually traded on an exchange created

for this purpose. The average contract length is roughly 3 months. Futures

contracts are usually inclusive of any interest amounts.

• Option

A foreign exchange option (commonly shortened to just FX option) is a derivative

where the owner has the right but not the obligation to exchange money

denominated in one currency into another currency at a pre-agreed exchange rate

on a specified date. The FX options market is the deepest, largest and most liquid

market for options of any kind in the world.

• Speculation

Controversy about currency speculators and their effect on currency devaluations

and national economies recurs regularly. Nevertheless, economists

including Milton Friedman have argued that speculators ultimately are a stabilizing

influence on the market and perform the important function of providing a marketfor hedgers and transferring risk from those people who don't wish to bear it, to

50Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 51/79

Foreign exchange risk

those who do. [18] Other economists such as Joseph Stiglitz consider this argument

to be based more on politics and a free market philosophy than on economics.

Large hedge funds and other well capitalized "position traders" are the main

professional speculators. According to some economists, individual traders could

act as "noise traders" and have a more destabilizing role than larger and better

informed actors.

Currency speculation is considered a highly suspect activity in many

countries.While investment in traditional financial instruments like bonds or stocks

often is considered to contribute positively to economic growth by providing

capital, currency speculation does not; according to this view, it is

simply gambling that often interferes with economic policy. For example, in 1992,

currency speculation forced the Central Bank of Sweden to raise interest rates for a

few days to 500% per annum, and later to devalue the krona. Former Malaysian

Prime Minister Mahathir Mohamad is one well known proponent of this view. He

blamed the devaluation of the Malaysian ringgit in 1997 on George Soros andother speculators.

Gregory J. Millman reports on an opposing view, comparing speculators to

"vigilantes" who simply help "enforce" international agreements and anticipate the

effects of basic economic "laws" in order to profit.

In this view, countries may develop unsustainable financial bubbles or otherwise

mishandle their national economies, and foreign exchange speculators made theinevitable collapse happen sooner. A relatively quick collapse might even be

preferable to continued economic mishandling, followed by an eventual, larger,

collapse. Mahathir Mohamad and other critics of speculation are viewed as trying

51Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 52/79

Foreign exchange risk

to deflect the blame from themselves for having caused the unsustainable

economic conditions.

The Structure of Foreign Exchange Markets

The forex is unique among financial markets in a number of ways. One of these is

that it was not traditionally used as an investment vehicle. It had, and still

maintains to some extent, a somewhat more utilitarian purpose. In today’s

globalized economy, most businesses have some international exposure, creating

the need to exchange one currency for another in order to complete transactions.

For example, Honda builds its cars in Japan and exports them to the United States,where an eager American buyer exchanges his dollars for a brand new Honda.

Some of this money has to make its way back to Japan to pay the factory workers

that built the car, but first those dollars have to be exchanged for Japanese yen,

since that is the currency the Japanese factory workers are paid in. Transactions

such as this are facilitated by international banks and are done through a

mechanism known as the foreign exchange market, or forex. Since banks are used

to facilitate these cross-border transactions, they naturally want to be paid for their

services. This payment comes in the form of a bid/ask spread – offering to buy the

desired currency at a slightly lower price than they are willing to sell it at, and

52Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 53/79

Foreign exchange risk

pocketing the difference. Considering the fact that more than $3bn moves through

the forex market daily, these seemingly small fees can add up to a significant sum.

The 2nd tier of the market is made up of smaller bits of larger multinational

institutions. This is when, for example, a bank branch in the US deals with another

branch of the same bank in, say, Japan. So when you walk into your local branch

and want to exchange currency, they will give you a quote which is not exactly

representative of the interbank exchange rate. You are free to shop around for a

better quote, and you would often be wise to do so, as rates can vary significantlyfrom one bank to another.

The purpose of the foreign exchange market is to facilitate the trading of various

currencies around the world. Although many different types of currency are

exchanged, the majority of trades involve only a small number of them, including

the U.S. Dollar, Yen, Euro, Swiss Franc, Pound Sterling, Australian Dollar, and

Canadian Dollar. The U.S. Dollar is involved in over 90% of all exchanges on the

forex markets. Contrary to popular belief, there is no one centralized market in

which all currency trading occurs; rather, the foreign exchange is a loose

conglomerate of several different markets, each of which has its own rules and

regulations. Major markets are located in the U.S., London, and Tokyo, and each is

open during different hours according to their time zones. Naturally, trading is

heaviest when the market hours overlap, and almost two thirds of the tradingactivity at the New York market takes place during the morning while the

European markets are still open.

53Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 54/79

Foreign exchange risk

Because there is no centralized market, a single exchange rate for a given currency

does not exist. Because of the over-the-counter (OTC) nature of the markets, the

bid and ask rates for a currency can vary among different geographic markets and

market makers, although they are usually fairly close to each other. Since the price

of a currency must be given in relation to another currency, it is expressed in the

form XXX/YYY, where each trio of letters represents the international currency

code. For example, the price of Euros in U.S. Dollars is written as EUR/USD.

Traditionally, the first currency in the pair, called the base currency, is always the

one that was strongest when the pair was created, and the other currency is knownas the counter currency. The actual prices themselves are in decimal form,

typically rounded to the nearest ten-thousandth of a unit.

The forex markets make up the largest marketplace in the world, with the

equivalent of $1.9 trillion changing hands every 24 hours. It is largely a short term,

speculative market, with more than 40% of positions closed out before two days,

and nearly 4 out of 5 lasting less than a week. It is an extremely liquid market,

much more so than equities, due to the many participants throughout the world and

the very high daily turnover. The top ten most active traders, however, account for

nearly 73% of total trading volume. Made up of international banks, these huge

players provide the market with bid and ask prices that are far tighter than retail

customers can expect, and trading activity that occurs between them is known as

the “interbank market”.

Introduced in 1972 at the Chicago Mercantile Exchange, forex futures contracts are

derivative instruments that are actively traded as well, as they account for around

seven percent of total foreign exchange volume. In addition, foreign exchange

54Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 55/79

Foreign exchange risk

options have taken hold as a popular hedging strategy. They represent contracts to

buy currency at a certain price on a set day in the future, and investors often

purchase these derivatives to offset any potential losses they may suffer due to the

decline in price of a currency. Another way traders are able to mitigate risk is

through a swap, in which both parties agree to exchange one currency for another

for a set period of time, and will then reverse the transaction after the period

expires.

55Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 56/79

Foreign exchange risk

Foreign exchange exposure

The foreign exchange rate exposure of a firm is a measure of the sensitivity of its

cash flows to changes in exchange rates. Since cash flows are difficult to measure,

most researchers have examined exposure by studying how the firm.s market

value, the present value of its expected cash flows, responds to changes in

exchange rates.When a company has cash flows that are denominated in a foreign currency, it

becomes exposed to foreign exchange risk, or in other words, has foreign exchange

exposure. Foreign exchange exposure can also arise when a firm has assets

denominated in a foreign currency, because the value of those assets will fluctuate

with the exchange rate.

The more cash flows a company has denominated in a foreign currency, the greater

its foreign exchange exposure is, especially if the exchange rates of the currencies

in question are not correlated--that is, if they do not move together (such as the

euro and the Swiss frank).

To calculate its foreign exchange exposure, a company needs to measure how

much money it would lose if foreign exchange rates that it has cash flows or assetsdenominated in moved unfavorably.

56Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 57/79

Foreign exchange risk

Foreign exchange risk is related to the variability of the domestic currency values

of assets, liabilities or operating income due to unanticipated changes in exchange

rates, whereas foreign exchange exposure is what is at risk. Foreign currency

exposures and the attendant risk arise whenever a company has an income or

expenditure or an asset or liability in a currency other than that of the balance-sheet

currency. Indeed exposures can arise even for companies with no income,

expenditure, asset or liability in a currency different from the balance-sheet

currency. When there is a condition prevalent where the exchange rates become

extremely volatile the exchange rate movements destabilize the cash flows of a business significantly. Such destabilization of cash flows that affects the

profitability of the business is the risk from foreign currency exposures.

57Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 58/79

Foreign exchange risk

Classification of Exposures

Financial economists distinguish between three types of currency exposures –

transaction exposures, translation exposures, and economic exposures. All three

affect the bottom- line of the business.

• Transaction Exposure

Transaction exposure can be defined as “the sensitivity of realized domesticcurrency values of the firm’s contractual cash flows denominated in foreign

currencies to unexpected exchange rate changes. Transaction exposure is

sometimes regarded as a short-term economic exposure. Transaction exposure

arises from fixed-price contracting in a world where exchange rates are changing

randomly.

Suppose that a company is exporting deutsche mark and while costing the

transaction had reckoned on getting say Rs.24 per mark. By the time the exchange

transaction materializes i.e. the export is affected and the mark sold for rupees, the

exchange rate moved to say Rs.20 per mark.

58Guru nanak college of arts, science and commerce

8/6/2019 frx mkt (1)

http://slidepdf.com/reader/full/frx-mkt-1 59/79

Foreign exchange risk

The profitability of the export transaction can be completely wiped out by the

movement in the exchange rate. Such transaction exposures arise whenever a