Embed Size (px)

Citation preview

7/17/2019 frsbog_mim_v06_3014.pdf

http://slidepdf.com/reader/full/frsbogmimv063014pdf 1/23

FEDERAL

RESERVE BOARD

WASHINGTON

X-5515

Decerr ber 3, 1917.

\Jhen

the United St· ttes joined

in

the war <J.gainst Germany

in Apri1 of th i s ye·1r, tha C1.sh reserves '1gainst ccmbinod note

and

deposit

l i ab i l i t i e s of

the

Fede::-'11 ReserYe System were. 83fo.

At the end

f

Hove:. l,er they were about 63.21" (see memo. No. 1).

This me'lns tha t

the

financial operat ions of the

Government,

c o v e r i n ~

lof'.ns to

the aggreg,.ite

ofmbout

t6,500,000,000

during

the per iod fr'>m A

pr i l

to Ncvomber 30,

have

brought about a re

duction in reserves of

about

21/L \le must ben.r

in

mind, how-·

ever,

the.t

ful l payment

for

the second Liberty

Loan

has

not

ywi,

been

c M p l t ~ t e d ( tbe l as t instfll lment not being due unt i l January

15th

anC.:

about

$1,400,000,000

beinr s t i l l paid

by

credi t and

about 650:COO;OOC being s t i l l on deposi t a g ~ i n s t cer t i f icqtes

of indebtedneos sold an0 ir1cluded in

the

above

$6,500,000,000},

I t i s qui'tt:l possible, the:.·efvre, tha t

our

reserves

have

not yc't

reached

the i r

lowest point in connection with the

payment

of

th i s loan, thoug 'l the paying off

of

the Cert i f ica tes of indebtnc: •

ne s s

wil l

l

iq·v.idut e some of the

loans

of

the Federal

Reserve D n ~ k :

and

thus counteract

to a cer ta in

extent

demands

for

further l o i r n ~

from

them.

I f between A p r i l 6th and November 30th, 1917, there hu.c. nu ;

been an

increase

of Cl49,0CO,OOO in the free gold holdings

of

'the

Federal Reserve

System (see

Memo No. 2) the

reserve

p e r c e n t a r : ~ >

would have dropped

b;r a furtheX" 5.6fo to 57.61 .

7/17/2019 frsbog_mim_v06_3014.pdf

http://slidepdf.com/reader/full/frsbogmimv063014pdf 2/23

2.

X-556

t

i s to be

hoped, and i t must be our

ser ious

concern,

that between

now and

the

next Liberty Loan campaign the reserve

percentage

wil l

again.be

increased. During the previous campaign

in June

i t

dropped

down

from

81.0fo

to

71.4fo/and

then recovered

to 82% in

A -ugust

(see memo

No.;. 3). t

is too ear ly

to

attempt

to

prognosticate how

fqst ::md how far the

reserve

strength wil l

recover th is time,

but

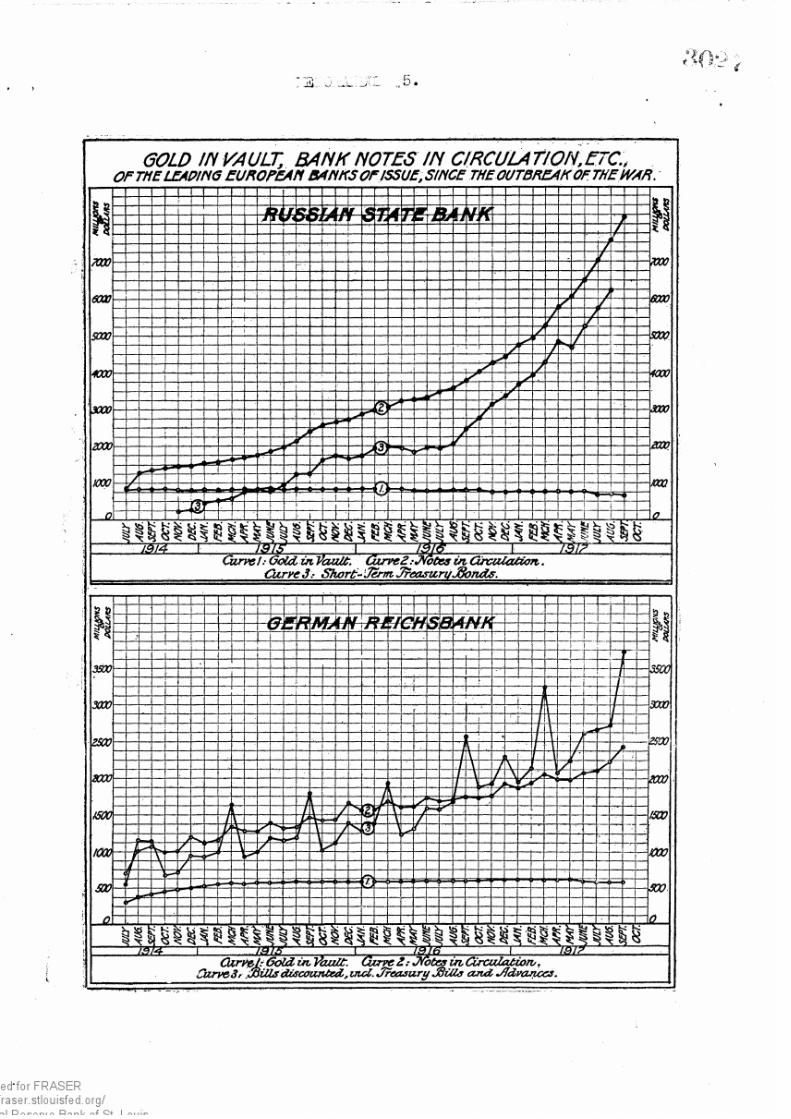

i we consult the charts (Nos.

4

and 5)

showing similar developments in the

Bank

of England, the Banque

de France, the Reichsbank

and

the Bank of

Russia, we

find that

we

must be

prepared

for

a

continuous

r ise

in

the

l i ab i l i t i e s

and

a

cor1tinuous fa l l in reserves of our Federal Reserve B a n r ~ s .

Indeed, we wil l

perceive

tha t in European central banks in mo&t

cases

r i se and

f a l l

show a

fatal accelera t ion

with each s u c c a s s : ~ : \ J e

year.

The German

Reichobank s chart

shows

most ~ l e a r l y

the l ines on which

the

Federal Reserve System s chart is l ikely

to

develop;

i t

sh0ws

a t

the

same

time

the

dangers

tha t

are

f ~ H : -

ing

us

i f we do not move

cautiously.

f

we look a t

the Reichsbank chart

we

find in l ine 3 ( oUJ. ,,

discounted, including ireR.sury b i l l s and advances) seven

p0ak•i

indicatir.g

the large increases in

loans and

discounts ace

or:if·,:ir,,.

ing

the

payments

for each

successive loan.

Within one mcn·C.L

af ter reaching

the

peak

of the

loarl

~ a e r e follows

l iquida-

t ion bringing the

curve down

to

about

the previous level ; b 1 1 ~

we

find that th is

level r i ses between

loans

so

that

each s1. c.,.: _;

-

ive

s tar t ing point

i s higher than the

previous

one, and

bet;;G

c

:

the f i r s t

and

the las t

tltar-ting

points the:re i s a. d i f f o r e ~ c e :n

7/17/2019 frsbog_mim_v06_3014.pdf

http://slidepdf.com/reader/full/frsbogmimv063014pdf 3/23

s. X-556

over

$2,000,000,000, and

the

reserve has gone down from 36.7fo

to 15.efo.

In

France trom

59.Sfo

to 14.1%;

Russia

.from 60.2%

to

7

41o.

The Bank

of

:2ngle.nd

's

chon"t

does

not ehow

the

real

picture because

about

$910,000,000 of small treasury

circulating

notes

c:ire

not

included (Greenbacks

to

all

intents and purposes,

secured by only l4.9fo

of

gold -

memo.

Ho

6)

Uld

the

deposits

of the Bank of E n g l ~ n d , which p l ~ y a large p ~ r t in England's

resei·ve position must be

considered.

The

Bank

of England's

reserve

p e r c e n t ~ g e

dropped from 39.4fo to

27.1% ( i f

we include

the 9 3 ~ , o o o , o o o

l ~ e a s u r y

notes i t

d r ~ ~ p e d

to about 2 0 . s ~ since

the begir.nir.g of

the

war. But we must

bear

in mind that Engl.find,

from the beginning of the war, drew on the United States f irst

for

gold

and later on

or

crerlit. ~ i t h o u t t h ~ a p p r o x i m ~ t e l y

$4,000,000,000 ($1,?00,000,000

securities sold artd

$2,500,000,000

in djrect loans) which Engl'tnd thus

secured

from the United Stat&s,

Sterling

e x c h ~ n ~ G

l o n ~

since would have collqpsed like

Russian

and

ltaliQ.n ~ x c h a n ; ; : e

'.l.nd Er.gland,

l ike

those countries, wou.ld

be practic -lly or a paper basis today, Fr"l.nce would be

in

the

same condition h ~ d i t

r.ot been

for

o u ~ assistance unless, indeed;

these two

countries

should hava been

able to continue

the war

without i m p o r t a . ~ i o n s from us. (In spite

of

our

assistance,

France's

eondition

a p p e ~ r s

to be a cri t ical one - see

memo.

No. )

I mention the experiences

of

France and England only because

I am

seriou$ly

alarmed by

the thought of

what will be

our

condi•

t ion when

our gold reserve should reach the danger .Point, when out

currency bhould

become

seriously

depreciated

- with

consequent

7/17/2019 frsbog_mim_v06_3014.pdf

http://slidepdf.com/reader/full/frsbogmimv063014pdf 4/23

4.

X.-55G

extreme increases :;.n prices

-

and

when

our

power

of expansion

on

any

re11.scn lbly

safe

·;A.sis

should

have

come

to

e.n

end.

When

we ri:iach

that

µrin+ t wil l mean

a

cntastrophe

because, unlike

England ri.nd Frri.nce,

we

hR.ve

nobody irho

wil l st•rnd

behind us flncl

bols ter up our

credi t .

How so:on

wil l

we

reach

that

point?

I t i s

too

early to venture

any

g u ~ J s as to our abil i ty. to

l iquidate

the

investments of

our

Federal

Reserve Banks,

thereby

regaining our

strength

befcre the issue o.f the next Liberty

Lo<i.n.

I t is

not

too ~ a r l y , however, to sound a word cf w lrning and to

ascertaiu what means we h'lve

to

arrest a development which,

i f

shown

to exist might

prove

disastrous.

J f

E1xperience

shculd

shew

that

our

reserve

pcwer

i s

~ v d n d l i n g

from

one

loan

'-l.nother

y

~ n y t h i n e

l i ke

151.,

the

second

or

third

followLw

lor.i.• l

would bt•ing us fnce to f ~ c e with a c r i t i c ~ l s i tua-

t ion .

v:hat

men.no

of

protection

are

there n.vailflble to the Fed-

e r ~ l Reserve

3anks?

And wh<it else c tn there e done to Wl \rd

o f

a

tco r ~ p i J

decline of our ~ n k i n f

s t r e n ~ t h

(1)

The Federl'll Heserve Banks, by raising

the i r ra tes

wil l

have

to

t r y

to

l i o u i d ~ t e

3

s<Jbst l.ntial

portion

of

the i r

investments.

The

di f f icul ty in

the

wqy of

carrying

such policy into

effect

is the

<hnger

c.f cre<tting

a

f in lncial

disturbance which

might

make

things worse ~ n d ~ f f e c t unfavor<ibly the large

l o ~ n

o p e r ~ t i o n s

of

the

Government.

We must, therefore,

move

cautiously

and ci:i.nnot

forcA

matters beyond

certain l imi ts .

7/17/2019 frsbog_mim_v06_3014.pdf

http://slidepdf.com/reader/full/frsbogmimv063014pdf 5/23

X 556

-5-

(2)

The

Fel0ral

Reserve Banks must t ry to

increase their

goll ho1lings b: : continuing to wi thlraw golJ cert if icates from

circulat ion

anl

substi tute Feleral

reserve

notes.

This

process will

bocorce more

anl

more

J. ifficult

as

the

amount

of outstan..ling

cer t i f i

cates b e c o ~ e s s ~ l l e r

anl

smaller.

(3)

Foleral Reserve Banks mu.st continue the i r effor ts to

secure

goll anl goll cert if icates

from the

vaults

of the

banks.

But

we have

lrawn

heavily

on that source of

s u ~ p l y

anl i t will

be

more

~ i f f icul t in

the

future than n

the past to

gain goll from that

quarter.

(4)

We

r r ~ h t t r ;

to

bet

goll from abroal.

Can

we

get i t?

t

woull be very interesting to

f inl

out what bap[;ened to the

Russian

anl French gol l

n

Lonlon. Is i t im possi ble to get Englanl to reloasi.; .

soma portion

of

that golJ, proviJ.eJ i t is available anl necessar1?

(5)

The

Feleral

Reserve

Banks

must

t ry to

reduce

their

f loat

(the

amount

invested

in

checks

anl

t ransfers) by

raising

the

rate of intorest upon which

these

transactions are

based

anl by trying,

if a t a l l possible, further to reluce the

.:ouble

circle that n.oney

lescribes when

paid in

by the

banks for account

of

the

Government

ani

pail out again y the Government.

(6)

e

n:ust

bend

every

effort

to

prnv0nt

prn:anent

cor; ;ora:te

financing, camouflaged as co.rmiercial paper, from creeping in to the

Faieral

Res0n0

Banks. The s0curitfos n:arket

being

in a

most un-

sat isf

actor: ; conli t i on, corpori:\.tions w l l

tr:, to

cnlat0 so cur i t ies

7/17/2019 frsbog_mim_v06_3014.pdf

http://slidepdf.com/reader/full/frsbogmimv063014pdf 6/23

X-556

- 6 -

in

form

available

for

investment

y

Federal Reserve Banks; or

amenJ;:r.ents

wil l

be rccorrn.er.dec:

wHh

the

object

of

permitting

l-

eral

Reserve Banks

to

lenJ on corporate

securi t ies .

t i s most

impor·tant that some machinery be created (a Government corporation

such

as

we have

i iscussed) to relieve the FeJeral

Reserve Banks

from

a l l i ional pressuro from the so directions.

(7)

The

Feleral

Reserve Banks have

about

100,000,000 in-

vostei

in

Government

securi t ies .

Tbe

Federal

Reserve

Banks are per-

mi

t t eJ to convert the i r one year

notes

anl other

hol..lings

of Govern-

ment bonls into tho 3

conversion

bonJs)

only.

These bonis sel l a t

present at about 86 n ~

the

arr:.ounts

investel can not therefore

be

l iqui ia teJ a t

th is time. If Fcleral

Reserve .Bo.nks were

permitted

(with

the

approval

of

the

Secretary of

the Treasury) to

convert their

hollings

into

whatever

bonU.s the

Treasury

issues from

time

to

tio:e,

they coull

free

themselves

of these

investments.

These are

pal l ia t ive

measures,

necessar:/ anj important)

in-

jeei)

but they wil l not alequately remedy the si tuat ion i i t should.

be shown that

we

are placing Governrr.ent

securi t ies

faster

than

the

country is able

to alzlsorb them, either because

the country

J.oes not

yet save

enough

or because we are rr.oving

too

fast

-

or both.

I

need not

go

into the question

of

savings,

exce;t

to

say

that i

a Governrr;ent corportation (mentioned

under

6) shoulJ be

established and Congress

should

erripoNer

the Presidnet to l icense

7/17/2019 frsbog_mim_v06_3014.pdf

http://slidepdf.com/reader/full/frsbogmimv063014pdf 7/23

X-556

- 7 ·

al l public

sales

of cocpr' 'ate foCt .nties -

the

PresiJent

vestin3

this

P'IWVer

in

the

boar:t u:: saiu r.orporation -

waste

by

States anJ.

rr:unicipalitiGs coulJ

be

chocked an:t expansion by sale of securities

c o u l ~ be controllaJ..

Our rrain concern

1

however

1

n:ust be as

to

the

speeJ

with

which we are m o v i n ~ We rrust

be certain

that Ne have not

started

u ~ o a three mile run at a thousanJ yarJ pace.

sure to get •

1

winJ.ed and

to get

knockeJ.

out.

Otherwise,

we are

In

this connection the

question is a burning one, whether

i t

is possible, without enJangering

our chances of

victory, to

bring

the

rr.ili ta r

an.:..

naval J.)rosram of

the

UniteJ

States

anJ her

all ies

into a scope

that

will

0nable us to

be

ttuite certain

that financially we

can hold out even

i

the war should

continue for

several

years.

People

talk

about

tho

rrarvellously

increasel

savin;;

power

of

the

country.

But this impr3ssive increase

is causei y increased

prices

and

increased

wages (moving in a

vicious circle).

Anl

as th0se

increase the

amount

that tho

Governn:ent nust borrow

increases

and

the

value

of

the

dollar

decreases.

Issuing billions for perishable gools (and, worse than that,

perishable

goods

that

destroy

things

of

pernanent

value)

creates

inflation;

i t

creates

increased l e ~ o s i t s a n ~ circulation anl increased

loans

based upon

inflated values (except stocks

and bonds Nhich

go dOW n)

n ~

thereby

creates a

~ e w n l for

increasel reserves.

Increased resarves in turn aro cr0ated by

increased borroWing

7/17/2019 frsbog_mim_v06_3014.pdf

http://slidepdf.com/reader/full/frsbogmimv063014pdf 8/23

X·-556

8,

from

Federal

Reserve

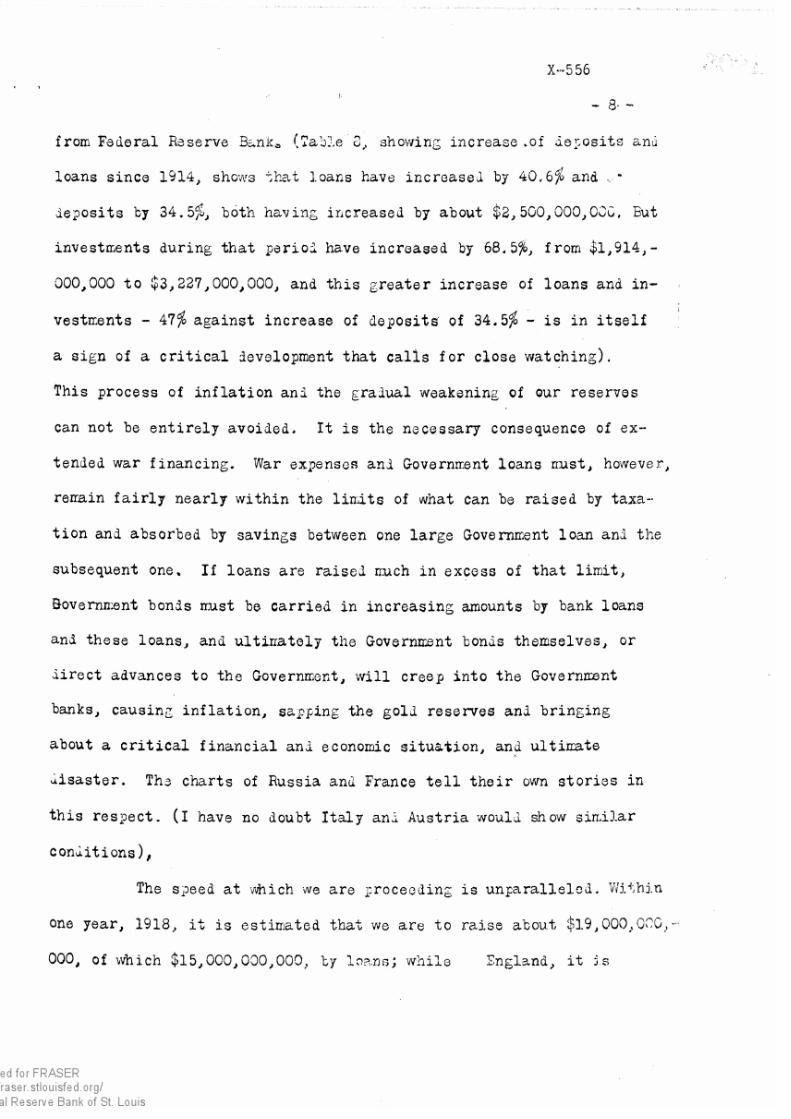

Bc..nk. ~ a b J . e

showing

increase

.of d.ei:osits

anu

loans since 1914,

shows

~ J : i . a t loans

have increaseJ

by 40,6%

and

·

•

aeposits

by

34.5%,

both

having

iDcreased

by

about

2,500,000,00C.

But

investments

during that perioi

have

increased by 68.5%

1

from

1,914,-

000,000 to

3,227,000,000, and

this greater

increase of

loans

and in

vestrr.ents

47

against

increase

of deposits· of

34.5 is

in

i tself

a

sign

of a crit ical ievelopment that

calls

for close

watching).

This

process

of

inflation

ani

the graiual

weakening

of

our

reserves

can

not

be entirely

avoided.

t is the necessary

consequence of

ex

tended war

financing.

War expensca and Governrrent loans n:ust, h ~ n e v e t

rerrain

fairly nearly within the

lirr,i

ts of

what can

be raised by

taxa-·

tion

and absorbed

by savings

between

one

large Government

loan anJ. the

subsequent one.

If

loans

are

raised

n:uch in excess

of

that limit,

Governrr.ent bonds n:ust be carried in increasing amounts by bank loans

and

these

loans, and ultinately

the

Governzwnt bonds themselves, or

i irect advances to the Government, will

creep

into the Governn:.ent

banks,

causing inflation,

sapping

the

gold reserves and

bringing

about a

cri t ical

financial and economic

situation,

a n ~ ultin:ate

~ i s a s t e r . Tha charts of

Russia

anu France

tel l their own stories

in

this respect.

(I

have no doubt Italy an.i Austria woulJ. show sin.Har

conJ.itions)

The s:peed at

v.hich

we are

proceoding

is

unparalleled.

W i ~ ~ h i n

one year,

1918, i t

is estimated

that we

are

to raj.se

about

19,000>000_,··

n g l a n d ~ i t

js

.; .

e

7/17/2019 frsbog_mim_v06_3014.pdf

http://slidepdf.com/reader/full/frsbogmimv063014pdf 9/23

- 9 -

estirrated has rais:id ·1: 7

::_· ::i.ri.s

a fl a':crage of 6.725,000,000 11cr

year,

France

4,

37

0 000,

000,

Ge

r:rPLrq

S;

469,

000, 000,

nussia 5, 000, 000, 000,

(See

m n i o s ~

9 to 12).'. 2.n.: as

rJta: .:.eCl

bi;)fore, these

countries

couL

resort to ether financi&.l rrarkets

in or.J.er to

strangth0n the i r

l)ositjcn,

while we

not only

can not oorrow abroal

1

or sel l our secur i t ies abroai

1

but n:ust finance by

our

loans our

a l l ies

as

well

as

ourselves

an ,

in

addition,

have the proceeds of credits openeJ. b; us

used

quite ex

tensively for our a l l i e s

purchases

of gooJ.s in foreign countries .

This l a t t e r ciroumstanco,

and

the

scopc

ani speed with which our

departments

anl our a l l i e s cal l upon the Treasury for funls an

credits are }he danger points which rr.ust comrrana our closest

a t t0nt

0

.6r.,

The

next

month wil l

bring us ief in i te figures upon which

to base rel iable conclusions. e are

lea l ing

with

a

new rr:achifoJry

anl

new

conl i t ions an have

no

p ~ o e t l e n t s

tha t

wouli enable us

to

io

n:.ore

a t th i s

tirr.e than to

point

to certain poss ibi l i t ies , which,

i they shouLi beconce

raal i

t i c s , nay prove

a serious menace

to the

successful prosecution

of the war.

P M. W.

12/7

/17

7/17/2019 frsbog_mim_v06_3014.pdf

http://slidepdf.com/reader/full/frsbogmimv063014pdf 10/23

December

6

l917

•

lvJ MORANDUM l

RATIO. ·:>F

TIE

FEDERAL RESERVE BANKS

TOTAL

RESEFNES

TO

NET DEPOSIT

AND

FEDERAL

.RESERVE NOTE LIABILITIES

COMBINED ON NOVEMBER 30,

1917.

Total Reserve 1,

576

211 000

Total net J.eposits • • 1,594,647,000

Total F. R. notes

in

circulation

Total

net

leposit

and F.

R.

n o ~ e

l iabi l i t ies Corr.bined 2

1

651,630,000

:Ratio

of to ta l

re3erve

to

net deposit ani

F.

R.

note

l iabi l i t ies o m b i n o ~

-

63.2 per

cent

,·

\. · \. -

X-556.

7/17/2019 frsbog_mim_v06_3014.pdf

http://slidepdf.com/reader/full/frsbogmimv063014pdf 11/23

FREE GOLD ON APRIL § AND NOVEMl: .;;R 30,

191

7.

Not ioposit

l i ab i l i ty

Reserve requirel

3 5 ~ o )

F.

R.

notas

in

circulat ion

Reson.re requirei (40 )

Total

nat

ieposi t

&

note Liab

1

1

1

s

Total

rosorves required

Total

reserves he l l

o l ~ hol l ings in excess of

r0serve requirements

Gain

in

free ;ol:i between

April

6 aal Nov. 30, 1917

Apri l

6,

1917.

376,510,000

.

150,6J4,JOO

1 3 6 7 9 ~ o o o

416,703,000

9

62

662 1 000

54

5)

9 59

000

Percentages of

reserve to

coi:1binel

net

:le,posit an.i note

l iabi l i t ies

April

6 - (962,662,000 1,136,792,000)

84.7 per

cant.

Nov. 30 -

(1,676,211,000

+

2,652,554,000)

63.2

h

«

X-556.

November

30,

1917.

1, 59

5,

571, 000

558,450, 000

2,652,554,000

981,243,000

1,676,211,000

694, 968,000

If i t

hal

not

been for

the increase

of 149,009,000 in free goll batween April 6 anl N o v e r r ~ e r

30,

1917,

the

reserve

percentage woul.i

have

iroppel to

57.6

(1,676,211,000 - 149,009,000 + 2,652,554,000)

7/17/2019 frsbog_mim_v06_3014.pdf

http://slidepdf.com/reader/full/frsbogmimv063014pdf 12/23

X-·53E

MEl\. lOP.ANDUM 3 •

RATIO OF TOTAL RESERVE

OF THE

F' iDERAL RESERVE

D l i l U ~ S TO COMBINED NET

DEPOSIT

AND

FEDERAL

RESERVE NOTE

LI.ABILITIES.

April

5-6

.May 11

June

15

June 22

June

29

July 6

July

13

July

20,

July 27

Aug. 3

Aug.

10

Aug.

17

Aug. 24

.Aug.

31

Sept.

7

Sapt .

14

Sept. 21

Sept.

28

Oct.

5

Oct.11-12

Oct. 19

Oct.

26

Nov.

2

lfov. 9

Nov.

16

Nov.

23

Nov. 30

1917

II

II

II

II

II

II

II

II

I

I

II

II

II

I

II

II

. . . .

.

..

............... .

.

.

.

. .

........

......... .

········ ...

.

. .

.

.

.

.

. .

.

........ .

I • • • • t •

e

t • • • \ • • • t

.

.

.

. .

.

.

. ..

.......... .

.

.

. .

.

. . . . . . .

.

.

..... .

.

.

.

.

. . .

, ...... -

.....

.............................

....

83.0

81 l

71.4

71.6

75.4

79.6

79.9

79.1

80.l

81. 9

82. 7

82.0

82.6

81.

7

79.6

80.0

7 ~ 6

77.1

74.4

74.5

75.6

71. 7

69.0

69 .4

65.8

64.7

63.2

par

cent

II

II

II II

II II

II II

tr

II

II

II

II

II II

II

II II

II II

II

II

II II

II II

II

II

II II

II II

II II

I ti

II II

II II

II

II

II II

n

7/17/2019 frsbog_mim_v06_3014.pdf

http://slidepdf.com/reader/full/frsbogmimv063014pdf 13/23

-

-·--

- --- ---

- . .

-

-· ___._ _

. . .

CiOLD IN VAULT:BAIVK NOTeSll'f.CIRCULAT/ON,'eTC..:

01:'

r e J.J:AP/f((j eLJROPEAN / JANK$ OFISSfJE,S/l{CE THe OfJ 81U AK OF H ~ W A R ;

H

H

-

I

••

·--

-

-

.

-

I

\

...

-

I

KXQ

'

m;i

J -

I

IXJ

,

'

1

'

I

'

I

.

BrXJ

1 ~

I

I\.

.......

I

,

.

J

'

:

7(XJ

I

,_

'

·--

\

I I

,,

tW

r

I \. I

--

'

I

--

:

>:

-

;w

«»

I

---

...._

J(XJ

I/

-...·

I ~

/

--

'

-...

~ l

;av

.

'

1 ~

z

'

,,

w

' (p

..

I I

n

- ~ ~ -

~ ' C

. ~ i) ~ ~ ~ ~ k: ~ ~ ~ ~ · a ~

~ ~ ~ ~ ~ ~ ~ ~ - ~ ~ ~

" '-. ~ Q ~

~ i . : ~ ~ ~ : ) ~ ~ I

~ ~ L : ~ ~ ~ ~ ~ ~

~ l t < ~ I S ~

~ ~ ... ·•·

,_

I

/, . 'wf/ '

I

r_w n

I

7

·

Curw::I: 6oldandSiiierm.Issuean . _ .: ..:

- _

--

a t n Z : ~ t u m i / l c t ; u a t ~ n .

C u r 1 1 e 3 : S ~

ui,' 'I>"

• .7

:tJeJUUtl tbtC.

ti

,,

; ...

....

_

,..,

-

l

.

.

·-

...

·-

-

....

._.

~ ~

....

--

...

--

-

,

-

....

I

--

-

lW

_,, -

,

...

._

... ___.

:w

-

-

-

~

-

i.7

.....

---

r- -

---

...

' '--

.....

\-

w

..

-

--'

I/

-

\

I

.m,1

-

/CW

,-

I

-

Jl(p soo

-

:-;·,

~ ~

~ - ~

~ - ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ I ~ ~ ~ ~ ~ '

~ i

~ ~ ~ ~ ~ ~

~

;;:: -:

... . .....

i

s i i ; ~ ~

._.,..,

Curve/,

(}old in.Tlaa/,t; CUrvet .-.JfiJtt:.t

zii

Q;rcalaaon .

Ov11eJ; l/dvances

t fW lJoP6r1J 1neM

since

tlle-1Yar:

.

·---

7/17/2019 frsbog_mim_v06_3014.pdf

http://slidepdf.com/reader/full/frsbogmimv063014pdf 14/23

_ .. ::....

..

_,,

..

..

GOLD IN YAULT,

BANK NOT.ES

IN CIRCUlATION,eTC.,

OF 77f£ LEA/JING cl/lfO/i# Alf Mff l (S }/&'/SS<Je; S/NCe TH£0(JT JR£AKOF.

THEWA f

.

I I

H

'

I

...

'

_.._

.

....

•• r

, ...

-

.•

-1 .1

....

-

.

.

...

..

,

; tW

v

,

· ~

i .

I

/

r

v

'

17

I / 17

'

-,

v

LI

sew

' /

--...

-,

'

I /

J

.

I

fJ

.J

/

·- ·-

I

."'

'

r

-

..,

-

.? .

...

J

-- -

i

-

I /

)

LI

.a:tt? .

,_

-

_

3

/

f J ) J

/

/

.av

I.

'

-

T

:-_

- - -

...

I

I I

'

I

I

n

r I I

I

·1

I

'

Q ti Ii: ki ; ;:: S l

~ ~ ~ ~ q ~ H : l i ; " { '

~ ~ ~

@

~ ~ ~ § ~ ~ ~ ~ ~ ~

/CA IL<.

I

1.ql.'>

I

'.'"1/l"J'

I

7.-0.T'::J

Curn:t.-

6(){,d,Ur. Paul&. uvve2.-. Yotes

m

a:rcataao,,,.

atr e

J.-

Short; .. .ler11t

.7rea.ruru1lottds.

' ' -

I

i ~ 1 1

I

I

I I

~ ·

I

_ _

•: P

ii·

'

•

....

-·

.,.,_

6 .

•

T

T

~ ~

I

"

-

,

.,,,.

111 1

t

a u L 11

~

....

-R

'

I

. I

' -

I

---r----·

- -

I I .1

I

I I

'

I

-

I

I T

,-

-

1 --

3S(J()

....

I

I

f- .

--

I

I

.I

l

I I

I

TT

3'W

11

xw

·

I

T

'

.1

I

I

I

-:::;

--

J

iz5W

\

I/ '

J

I

,

\

;

"'

I

·-'

,

....

I I

/

I?

If

I

-

1 1)

··--·

I

··-

-

,

J

- -

I

'

·"

-

. I

,_

I

'

I/

-

LI

I v

.av

·--

I

I

--

....

II

I

-

-

DJ

---

I

-

..

-

l 'l

.

i

glg

'" ' . hl

~ ~ ._.

;::

~

,.

1-.:. ~ :i ~

~ Q

lg

~ ~ ~ ~ - ~ - ~ ~ ~ ; ~ ~ ~ ~ ~ ~

~ ' I ;

~ ~ ~ q ' ~ - · ~ ' 1 ; ~ 8 ~ ~ ~ ~

~ ~ · ~ ~

i

,

_ ,,

,,.

I . Q I ?

C k r ~ Vold in, YaaLt: Z .·./Vote m

Ctrca/ation,.

Cunf6a, · Ul4 . r c o ~ , ma

T r ~ u r g

JJU/8 a n d

./ldval'fc,a.

-

-

-- . (

-

·

---·

. -

7/17/2019 frsbog_mim_v06_3014.pdf

http://slidepdf.com/reader/full/frsbogmimv063014pdf 15/23

Total Metal l ic

. Reserve

Government

Deposits

Other lDeposi

ts

1 3 2 . ~ 1 1 : : .:lotes in

Ci rel.I.la

t

on

Totc.l

Rai:io .of Reserve

t 0 C C:t1ii.1EHi

Deposit

and

Note

Liabis

Treasury

notes

outs tanJ ing

Coin ni bull ion

Cover

Per cent

RATIO OF i O IJ .T.i

HESEHVE

·ro (;()}ffiilWL FE?0S.:T J .NP ~ W I E L I . 1 ' . : : ? : L : : ~ ' E ~ L

FOR THE

PRINCIPAL

ElffiOPE..AN J3ANK2 SSUE.

(In thousands of lo1J

an3)

Bank of

England Bank

of France

Russian State Bank

:July

29,,

:Nov.

14, :July

30, :Nov.

15,

:July. 16,

:Sept.

16,

Jul;,

31)

:1914

:1917

:1914

:1917

.

o

29,

: to

29,

1914

:1914 :1917

:$185,567 : $270, 603

:$919

J 968

i$683,825:$683,371 :$742,249

:$363)670

.

61,869 205,486

73,834

6, 37

5:

264,937

: 109 J 421

d

: )

299,

515

264, 830

586,468

182,

881

533,213:

327 J 585 :1, 710, 221

:

471)265

998JJ92

l,5-16,570

:4,842,337:1,433)696

:10,001,423

991,957

39.4

27.l

138,695

14.9

59.5

14.1:

60.2

7.4

36.

7

Oct.

23,

1917

: l ,365,J26

:3)778JJ36

15.8

7/17/2019 frsbog_mim_v06_3014.pdf

http://slidepdf.com/reader/full/frsbogmimv063014pdf 16/23

X-555

Tho following

i s

a

quotatior .

from a l e t t e r of a Dutch G0ntlowan.

According to

the

off ic ia l mGmorandum regarding

Fronch

f inances, Franco had borro

:1ed in

Englo.nd

som3what over Fcs.

8,000,000,000, and close to Fcs. 6 000 000 000 in

thG

United

Sta tes .

Further advances

which

w0 U.S . ) have

made

in H10

mean timo may

have brought

Fr:?.nc,3's d::bt ir,

th i s

country up to

about

Fcs.

8,000,000,000, making a

tot .al

cf Fcs .

16,000

0C'J,C01).

Tho off ic ia l estimate

of

crops of Franca indicatrn

tha t there wil l be

a shortage

of

wheat,

rye, barley, and oacs

of

about

45i

against

tho average yiold of these crops for tho

years 1905

to

1914.

What i s more

serious

i s

tna t

the

short·-

age

;i s greatest

in

wh0at, \'ihere i t amounts to more than

551o

The T0mps

of

Septo:-uber

28th estimates t ha t France L1ay

have

to import between thr00 and fcur b i l l i on Francs o ~

cereals

to

make up tho shortage

cf

th i s

y ~ a r

I t seems impossible to

soe

how France wilL be

able tc

keep up

her

ra te of exchange, eveL

i f

peace

should

c o ~ e

Unlike

England,

France

does not

dispose

of

any foreign invest

went s which can

be eas i ly

made

avai lable .

For

pol i t ica l

reasons, the French

markets were

closed to jus t

foreign

secur i t i es

which would have helped the country most

now, and

the

Government

and

the banks co-operated in put t ing

7/17/2019 frsbog_mim_v06_3014.pdf

http://slidepdf.com/reader/full/frsbogmimv063014pdf 17/23

-2-

X-555

the

savir gs

of

th

nat ion which

ware

ava i lab le fd r

i iwestment

abroad -

chiefly

in Russia, South America and llfoxico - just

the countries where investors have rsceivod the heaviest

blows.

I t

was

exac t ly

on

acc0urlt

f t h i s

s i tuat ion tha t

France

fou:?: lci

herse l f actual ly the miust

of a

f inancia l cr is is

at

the cut -

break

of

the war. T ~ e necessitL1s

of

the

war long

a,;o

~ o r s w : e d

whatever foreign

assets of

a more l iquid kind

France

may

have

been holding and

t

is

a ' Jellhr.:own

fac t

tha t

the country

has

ever, gene

so fa r as to

pract ical ly pledge

tha credi t

of

i t s

c i t i e s

and i t s bigbest private enterprises f inancia l ly to

back

up tho

G o v e r n ~ o n t

If

we tu rn

to the

conditions

of the Bank of France, we

do not f ind any more reassuring fac t s .

"On

Octcber

l l t h

the note c ircula t ion

was Fcs.

21,500-

000,000, which were covered

by

cnly Fcs. 3,300,000,000 actual

gold, bein

only about 1 5 ~ Most

of

tha assets held against

t h e note i ssues are absolute ly unco l lec tab le fo r the t ime

being.

They cons is t up to :

Fcs. 12,100,000,000

of

advances

to

the

Sta te

1,150,000,000 Bil ls of Exchange net col lect ible

under

the moratorium.

and 3,500,000,000

cf advances to foreign governwents

which notoriously are ~ d v a n e e a to the

Russian Government

t r tha p ~ y o e n t

of

i n t ~ r e s t

on i t s pre-war debt hold

in France.

7/17/2019 frsbog_mim_v06_3014.pdf

http://slidepdf.com/reader/full/frsbogmimv063014pdf 18/23

This makes a

t o t a l

of

un

col lect

i ble

3

X 555.

assets of Fcs. 16,750,000,000,

or

about 771.

of the

t o t a l

amount of notes outstanding.

11

Perhaps

one

of the greatest d iU ic ult

ies

which

is

in

store for the

French ~ o n y

market and which

may

well give

the f ina l

blow

to

the

whole

structure•

l i e s in

the fact tha t

the

day

wust

come when

the

French

Government

wil l

cease

to

p y

out

to

the

French

holders

of the Russia pre-war

debt

the

in teres t

which i t can never hope to

col lect i t s e l f .

When tha t

day comes

I fear a very s r i o ~ s si tuat ion.

P. JL W

7/17/2019 frsbog_mim_v06_3014.pdf

http://slidepdf.com/reader/full/frsbogmimv063014pdf 19/23

Il\CBEASES EETVlEEN JLTIE 30, 1914 AND SEPTEMBER

l l ,

1917

OF

LO.A.i. 1S

.AJ:TD

DISCOUN1I

1

S .AND

NET

D.fil'OSITS

OF NATIONAL BAJ.'JKS, .AS

SHO';IN .BY

COMPTROLLER'S

.A.BSTBACTS.

J u ~ e

30, 1914 Sept. 11,

1917

Increases.

. .

--------------------------------------------------------------------------------

(In

thousands of

dollars) .

.

.

Loans and discoi.mts

:

:

inoludiI1£

O'Tard.ra.fts

6,445,555 9,064,855

$2,619,300=

4o.6%

.

Other loans ~ n d invest-

.

:

m ~ n t s excluding p r

:

.

mane11t in Q'est. '.l1ents

l ~ 1 4 2 8 8 8

3 ~

227'

124

1 ~ 3 1 2 2

236=

68.5%

Total

loans

and

investments,

8,360,

443

12,291,979

:

3,931,536=

47&0

liet

deposits, on

which

.

reserve s

conri:.u.ted:

7,495,149

10,082,779

2,5s7:630= 34.5%

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - ~ - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

7/17/2019 frsbog_mim_v06_3014.pdf

http://slidepdf.com/reader/full/frsbogmimv063014pdf 20/23

X-556

:M EMORANOU 9

BRinSH

WAR

I.CANS

On

September 30,

c c o r ~ i n g

to of

i ~ i l

announcement of the Chan

cellor of the Exchequer, tha

total

funiei debt of the United Kingdom

stood at :C2 518,

300

000 equivalent to

$12, 255,

307, 000.

In

ail i t ion

there

were outstandin; on November 3 about t,991,000,000 equivalent to

$4,820,000,000, of . Treasury

Bills about

$1,475,000,000 loans from the

United States Government anl seve-ra.l hun..ired millions of credits raise.i

in Holland, Scandanavia, Japan anl other foreign countries, rrakin6 a

total of about

18.

7

billions

oi dollars

(see

London Economist, Nov. 17,

1917).

The Lonion

Ei::ono;:r;ist gives tl1e to ta l

net borrowings of tho Brit ish

Governn.ent for

tho

p e r i o ~ August l 1914

to November

10, 1917 as

L4,491,-

514,000 equivalent

to

$ 2 1 , 8 5 7 , 9 5 3 ~ 0 ' . J O ,

'Jf

which

tl,260,0JO,OOO

e q u i v ~

a.lent

to

$ 6 ) : l . 3 ~ ; · o o o ,

000

:rep.resents a..ivanres to Dominj.ons and .Allies

Unler

date of November 14 the

Bank

of EnglanJ reports

among i ts

assets Government

Securi

t ics amou.nting

to

t58, 721,,

320,

equivalent to

$285,768JOOO.

Taking

the larger

e s t i r r a ~ e of total war ..iebt of $21,857,-

953,000 given by

the Lon ..lon

Economist as our

basis

for calculation, we

obtain

a 7early

average

of war

loans

raised between August 1914 and

November

1917 of

about

6,725 million dollars.

7/17/2019 frsbog_mim_v06_3014.pdf

http://slidepdf.com/reader/full/frsbogmimv063014pdf 21/23

X-556

MEMOR NDUM

10

FRENCH

WAR

LOAN§

I

The

Economiste Europeen

quotes

an

of

ficia.l

bu.J.get

r e ~ : J o r t ,

i n ~ i c a t i n ~ the

follcrfling increases in the French National lebt

ce-

~ w e e n August l 1914 a n ~ S e p t e r r ~ e r 30 1 ~ 1 7 :

National

Defense short-tenr. tonJs,

~ d o n s

de

la Defense Nationale )

National Defense Obligations ,

5 fundel loans

oi

1915

anl

1916

Tote.l

Millions

of

Francs.

21,

700

840

21. 920

44,460

This total is exclusive of 12,350 rr,illions of

francs, equivalent

to ~ 2 3 8 3 . 5

r r ~ l l i o n s of

lollars (at the

nominal

rate of 19.3¢

per

franc)

of war aJ.vances 1. :, the Bank of F 1 ~ a n c e shown an:;ong i t s assets

on :foverr.ber 15, 1917 - The Bank also carries ar i t s assets an

iteffi of 3.145 millions of francs, or about 607

million

Jollars

dis-

counteC.

Treasurr

l3ills,

ti1e proceei.i.s of which were

alvanced

to

the

Allies.

I t

is not clear whether this arr.ount is included in

the

above total of 44,460 millions of fra;.1cs To the

total

given should

be aJled also the

following

amounts

largely taken

from M.

Klotz

s

Treasury

Sta

err.ent as at Juli 31 1917:

Bills s o l ~ in England

Millions

of

francs.

7,952

.Amounts

borrowed

in

the

UniteJ

States:

Bank creli ts ,

Industrial credit

Afril

1917 creli t operations,

Anblo-French loan,

Alvances

by United States

Gov•t.

Amount

borrovveJ. in Japan,

.AO.vances ·by the

Bank

of Algeria,

Total

518

239

498

. l 243

(Nov.l,1917) 4,248.7

129.0

65.0

14,892.7

Total

long-term

anl

short-term

lorr2stic

outstanJ.ing

Sept. 30 1917

Advances

of the

Ba.nk

of France,

loans

44,460

.J..h35Q.

71,702,7

or rrillion

$13,838.8

Assurring this amount to

represent

total

ex;·enditures between August

7/17/2019 frsbog_mim_v06_3014.pdf

http://slidepdf.com/reader/full/frsbogmimv063014pdf 22/23

•

•

·x556

MDviOR NDtlM

RUSSIAN

W R UWis •

.According to an

off

icia.l anno'\lncement of the Russian Finance

Minister (re:produced

in the Economiste E u r o p ~ e n

of

October 12,

l9i7)

the

Russian

State

expenditures between

August 1, 1914

and

Se:ptember

l 1917,

aggregated

41,393,000,000 Rubles, or 21,317,000,000 nominal,

W h i l e ~ Q o v a r n m e n t : . . r e v e n t w J £ 9 r the

same ;period was

only

about

9, 701.,000,000

Rubles, or 4,996,000,000

nominal..

This

leav.:is a

tota.l of 16,321,000,000

which had to ·oe covered by loans. .Aggregate domestic long-term a.nd short

tenn loans <ire t;iven in the statement as 12,758,000,000

Rubles

or

6

1

570,000

000 non1inal, the remainder of 9,'{49,000,000 non1ina.l thus

being

covered by

foreign loans,

largely

a.dvanc'3d y Great :Brita.in.

On September 29,

1917 tl1e Russian

State Bank reports

among i t s

assets

13 ,394,

795:

000 Rubles

of

snort-term

Treasury bonds

(Eons cl.u lrenor)

besides

828,994,000 R u h i ~ s of advances

for p r o v i s i o n i n ~

operations of ~ h e

Government, or

a total

of l4,223,7s9,ooo Rubles eY.uivalent to abou·t 7,325

mill ion

dollars

a,t the noni:i.nal rc:ite of 51.,5 cents per R u b l ~ Per contra

the

:Bank

re:ports a to tal of 15,886,953,000 Rubles or 8,181,781,000

nOiilina.l of notes in

actUz1.l

circula. t i on •

.Assuming

a

to tal war

debt to September 1917 of 16,319,000,000

the yearly increase

of

the

debt

would average sl ight ly over 5 bi l l ion

dollars.

7/17/2019 frsbog_mim_v06_3014.pdf

http://slidepdf.com/reader/full/frsbogmimv063014pdf 23/23

x556

MEMOR NDUM 12

GD1AN

W R

LOANS.

In mil l ions

of

Marks @ Dollars

(In

millions)

1st • 4 480.8

2i l.d• • • • • • • • • • • • • • •

9 106.3

3rd• • • · · · · · · · · l 2 l 6 2 . 6

4th 10

767 6

5th• • • • 10 699.o

Gth• ••• ••••• ••••• ••• •••• 13 120.0

1,066 4

2,167.J

2,894.7

2,562.7

2,546.4

3,122.6

7th

•.•.....••.•••.•.....••..• · ~ · ~ · · ~ 1 ~ 2 ~ · 4 ~ 3 _ 0 _ . o __ ~ _ . ; ; ; 2 ~ 9 ~ 5 - s ~ · - 3 _

Total ••••••••

72,766.3

@ •.Marks converted at 2 3 . e ~ per Mark.

i7,31s.4

Note: The above totals a r ~

exclusive of Treasury

Bil ls

Treasury Notes, Government War Loan bank notes and other unfuncled

obligations of the Imperial Goveimient.

Ille

above increase

in the

public

debt

averages

about ~ ; 5 4 6 9 0 0 0 0 0 0 per

year, to

which sho-ild

be

added a

certain

amount

of floatine; indebtedness chief ly in the

fol tl of Treasury b i l l s

and War Loan bank notes.