Embed Size (px)

Citation preview

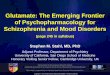

MSCI EM REBOUND +55% IN 33 WKS – MID 34-74% RANGE

1

• 55% rally from the lows in 33 weeks is in line with the 52% average of the 4 previous rebounds (ranging fom34-74%)

• EM has already regained its previous highs; this took 6½y post-1997, 3¼y post-2000, 1½y post-2016, while the 2007 high is yet to be regained, over a decade since the peak

• EM is now 3% above its dollar 1Q peak (EM ex-China is still 8% below; FM 12% below, DM 1% above, US 4% above)

100

120

140

160

180

200

220

240

260

280

300

-60

0

-50

0

-40

0

-30

0

-20

0

-10

0 0

+10

0

+20

0

+30

0

+40

0

+50

0

+60

0

+70

0

+80

0

1998 2001 2008 2016 2020

MSCI EM in $ rebased to 0 at market low, 5 major EM crashes of 33%+

US, EM, DM HAVE ALL REGAINED 1Q $ HIGHS

2

-40

-30

-20

-10

0

10

20

US

(3.6

%)

EM (

2.6

%)

DM

(1

.4%

)

EM e

x-C

hin

a (-

8.0

%)

Fro

nti

er (

-11

.8%

)

EM A

sia

(12

.2%

)

EMEA

(-2

0.3

%)

LatA

m (

-32

.7%

)

EM G

row

th (

17

.9%

)

EM V

alu

e (-

12

.2%

)

MSCI indices, % change vs 1Q 2020 high in $

DRIVEN BY CHINA, TAIWAN AND KOREA IN EM

3

-50

-40

-30

-20

-10

0

10

20

30

Ch

ina

(21

.5%

)

Taiw

an (

15

.1%

)

Ko

rea

(8.0

%)

EM (

2.6

%)

Arg

enti

na

(2.3

%)

Ind

ia (

-3.6

%)

Mal

aysi

a (-

7.6

%)

EM e

x-C

hin

a (-

8.0

%)

Sau

di A

rab

ia (

-8.9

%)

Qat

ar (

-10

.3%

)

Ph

ilip

pin

es (

-10

.8%

)

S A

fric

a (-

12

.0%

)

UA

E (-

17

.4%

)

Ind

on

esia

(-2

2.4

%)

Mex

ico

(-2

3.7

%)

Ch

ile (

-24

.3%

)

Cze

ch (

-25

.3%

)

Egyp

t (-

26

.9%

)

Po

lan

d (

-27

.2%

)

Hu

nga

ry (

-27

.5%

)

Thai

lan

d (

-27

.5%

)

Per

u (

-28

.7%

)

Pak

ista

n (

-31

.2%

)

Ru

ssia

(-3

4.7

%)

Bra

zil (

-37

.8%

)

Turk

ey (

-40

.7%

)

Gre

ece

(-4

3.2

%)

Co

lom

bia

(-4

6.1

%)

MSCI EM country indices, % change vs 1Q 2020 high in $

FRONTIER

4

-60

-50

-40

-30

-20

-10

0

10

20

30

40

Leb

ano

n (

35

.3%

)

Tun

isia

(3

.6%

)

Ban

glad

esh

(1

.8%

)

Vie

tnam

(-1

.3%

)

Lith

uan

ia (

-3.2

%)

Nig

eria

(-5

.4%

)

Slo

ven

ia (

-8.1

%)

Cro

atia

(-1

0.8

%)

Fro

nti

er (

-11

.8%

)

Mo

rocc

o (

-14

.4%

)

Ku

wai

t (-

15

.8%

)

Om

an (

-16

.0%

)

Ro

man

ia (

-16

.0%

)

Serb

ia (

-16

.2%

)

Bah

rain

(-1

7.4

%)

Sri L

anka

(-2

0.2

%)

Ken

ya (

-22

.1%

)

Jord

an (

-22

.7%

)

WA

EMU

(-2

5.3

%)

Kaz

akh

stan

(-2

6.8

%)

Esto

nia

(-2

8.8

%)

Mau

riti

us

(-4

7.4

%)

MSCI FM country indices, % change vs 1Q 2020 high in $

EM SECTORS – FINANCIALS THE BIG LAGGARD

5

-40

-30

-20

-10

0

10

20

30

40

Co

ns

Dis

cr (

34

.8%

)

Hea

lth

care

(2

8.1

%)

IT (

20

.1%

)

Co

mm

un

icat

ion

s (1

9.4

%)

EM (

2.6

%)

Mat

eria

ls (

-0.2

%)

Co

ns

Stap

les

(-6

.4%

)

Ind

ust

rial

s (-

9.5

%)

Uti

litie

s (-

20

.3%

)

Rea

l Est

ate

(-2

1.9

%)

Fin

anci

als

(-2

2.8

%)

Ener

gy (

-31

.3%

)

Roundtrip

MSCI EM sector indices, % change vs 1Q 2020 high in $

COVID - EAST ASIA SUCCESSWATCHING 2ND WAVE

6

0

50

100

150

200

250

300

350

400

Cze

chia

(1

,06

5)

Po

lan

d (

57

7)

Hu

nga

ry (

43

8)

Arg

en

tin

a (2

26

)

Gre

ece

(20

6)

Co

lom

bia

(1

81

)

Ru

ssia

(1

31

)

UA

E (1

21

)

Per

u (

75

)

Ch

ile (

73

)

Qat

ar (

73

)

Bra

zil (

49

)

Mex

ico

(4

0)

Ind

ia (

34

)

Mal

aysi

a (3

2)

Turk

ey (

27

)

S A

fric

a (2

5)

Ph

ilip

pin

es

(17

)

S A

rab

ia (

12

)

Ind

on

esia

(1

2)

Pak

ista

n (

5.7

)

Ko

rea

(2.2

)

Egyp

t (1

.9)

Taiw

an (

0.1

)

Thai

lan

d (

0.1

)

Ch

ina

(0.0

)

latest rolling 7-day cases per million -1m -3m

FISCAL CAPACITY HAS BEEN KEY

7

Bahrain

Croatia

Kazakhstan

Kenya

Kuwait

LithuaniaMorocco

Serbia

Vietnam

Brazil

Chile

China

Colombia

Czech Republic

Egypt

Greece

Hungary

India

Indonesia

Korea

Malaysia

Mexico

Pakistan

Peru

Philippines

Poland

Russia

South AfricaTaiwanThailand

Turkey

UAE

Saudi Arabia

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

-2 0 2 4 6 8 10 12 14 16

YtD

ch

g in

10

yea

r lo

cal y

ield

(p

pts

)

10 year local yield (%)

Easier

Harder

Top right - bond yields are high and have risen - fisal stimulus is challenging.

Bottom left - bond yields are low and in some cases falling, fiscal stimulus

easier.

8

Source: MSCI, Bloomberg, Renaissance Capital

BOND FLOWS TURNED +VE IN JUNE; EQUITY IN MID-AUG

• Hard currency debt funds have been seeing inflows since April (9% of AUM), local currency has net inflows since July (4% of AUM) and equity since mid-August (1% of AUM)

• Equity funds have seen a long run outflows, but not in huge size (4.4% of AUM YtD)

• Frontier funds have been seeing outflows all year (18% of AUM from peak)

-20.0

-15.0

-10.0

-5.0

0.0

5.0

Jan

Feb

Mar

Ap

r

May Jun

Jul

Au

g

Sep

Oct

No

v

Dec

EM equity Frontier equity Bond total Bond hard Bond lc

CUMULATIVE FLOWS YtD 2020 (% of AUM)

9

Source: MSCI, Bloomberg, Renaissance Capital

EM EQUITIES HAVE SEEN OUTFLOWS FOR 7 YEARS

• EM Equities have seen net outflows over the last seven years – EM equities is an under-owned asset class vs DM equities and vs EM bonds and DM equities

• Major outflows from Frontier funds as investors question the asset class

100

120

140

160

180

200

220

240

EM Equity

Frontier Equity

EM Bond - hard ccy

EM Bond - local ccy

CUMULATIVE FLOWS 2010-2020 (% of AUM)

EM underperformingDollar weakness

45 YRS OF EM EQUITIES VS $

10

60

70

80

90

100

110

120

130

140

150

30

50

70

90

110

130

150

170

190

210

Jan

-76

Jan

-77

Jan

-78

Jan

-79

Jan

-80

Jan

-81

Jan

-82

Jan

-83

Jan

-84

Jan

-85

Jan

-86

Jan

-87

Jan

-88

Jan

-89

Jan

-90

Jan

-91

Jan

-92

Jan

-93

Jan

-94

Jan

-95

Jan

-96

Jan

-97

Jan

-98

Jan

-99

Jan

-00

Jan

-01

Jan

-02

Jan

-03

Jan

-04

Jan

-05

Jan

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

Jan

-16

Jan

-17

Jan

-18

Jan

-19

Jan

-20

EM - IFC Composite/MSCI EM (from 1987) relative to DM, TR Dollar Index (RHS)

1. Credit bubble 1973-1980 (7y)

2. Debt crisis 1980-1987 (7y)

3. Rediscovery 1987-1994 (7y)

Dollar strengthEM outperforming

4. Rolling crises 1994-2002 (7y)

5. Boom time 2002-2011 (8y)

6. Disillusionment 2011-2020? (9y)

Source Bloomberg, Renaissance Capital

EM & FM WEAKER DOLLAR BENEFICIARIES

11

HU

PL

CZ

LatAm

EMEA

ZA

BR

KR

CO

EM

PE

MY

CLMX

BRIC

TR

EM AsiaTWTH

ID

GR

RU

PH

INCN

AR

AE

PK

EGQASA

MA

Frontier

KZ

BG

UA

RO

LTSI

VN

MU

RSKE

EELKNG

OMJOLBBD

KWBH

HRTN

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

-0.1 0.0 0.1 0.2 0.3 0.4 0.5 0.6

BETA (y-axis) and CORRELATION (x-axis) vs weakening dollar, 10 yrs of weekly returns

EM SECTOR WEAKER DOLLAR BENEFICIARIES

12

EM

Real Estate

Materials

Utilities

Financials

Cons Staples

Industrials

Telecoms

Energy

Cons Discr

Healthcare

IT

0.4

0.6

0.8

1.0

1.2

1.4

1.6

0.25 0.30 0.35 0.40 0.45 0.50

BETA (y-axis) and CORRELATION (x-axis) vs weakening dollar, 10 yrs of weekly returns

PER VS HISTORY

13

0

5

10

15

20

25

US

(+

42

%)

Wo

rld

(+

37%

)

Ja

pa

n (

+2

7%

)

EA

FE

(+

26%

)

Eu

rop

e (

+25

%)

Ch

ina

(+

46%

)

EM

Asia

(+

33%

)

EM

(+

30%

)

EM

ex-C

hin

a (

+1

4%

)

La

tAm

(+

5%

)

FM

(+

24%

)

EM

EA

(+

18

%)

12M FWD PER 12M FWD PER 10yr avg

12M FWD PER vs 10 yr average – Latam, EM ex-China and EMEA have had the smallest re-ratings

MSCI EM 27% DISCOUNT TO DM

14

-35

-30

-25

-20

-15

-10

-5

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

EM vs DM EM v DM avg +/- 1SD▪ MSCI EM trading at a 27%

12M FWD PER discount to

MSCI World

▪ Vs a 10 yr average of 23%

▪ 0.6 Standard Deviations

cheap

MSCI EM 12M FWD PER premium (discount) to DM (%) and 10yr avg, +/- 1SD

MSCI FM 12% DISCOUNT TO DM

15

▪ MSCI FM trading at a 12%

12M FWD PER discount to

MSCI EM

▪ Vs a 10 yr average of 7%

▪ 0.6 Standard Deviations

cheap

▪ But when Kuwait exits MSCI

FM at end-November,

valuation resets from 13.0x

to 10.9x

▪ And discount reaches 26%, a

decade high

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

FM vs EM FM v EM avg +/- 1SD AdjustedMSCI FM 12M FWD PER premium (discount) to EM (%) and 10yr avg, +/- 1SD

EM PER VS HISTORY

16

0

2

4

6

8

10

12

14

16

18

20

22

Arg

enti

na

(+5

07

%)

Ind

ia (

+3

3%

)

Sau

di A

rab

ia (

+43

%)

Ph

ilip

pin

es (

+9%

)

Thai

lan

d (

+31

%)

Taiw

an (

+20

%)

Ch

ile (

+2%

)

Ch

ina

(+4

6%

)

EM A

sia

(+3

3%

)

Mal

aysi

a (-

1%

)

BR

IC (

+44

%)

Per

u (

+17

%)

Ind

on

esia

(+3

%)

EM (

+3

0%

)

Mex

ico

(-1

3%

)

Qat

ar (

+17

%)

LatA

m (

+5

%)

Bra

zil (

+1

1%

)

Po

lan

d (

+6%

)

Ko

rea

(+2

6%

)

Cze

ch (

-4%

)

S A

fric

a (-

17

%)

EMEA

(+1

8%

)

Gre

ece

(-3

0%

)

UA

E (+

22

%)

Co

lom

bia

(-3

1%

)

Hu

nga

ry (

-3%

)

Ru

ssia

(+3

2%

)

Egyp

t (-

24

%)

Pak

ista

n (

-20

%)

Turk

ey (

-30

%)

12M FWD PER 12M FWD PER 10yr avg

12M FWD PER vs 10 yr average (green – cheap vs 10 yr avg, red – expensive vs 10 yr avg)

EM SECTOR PER VS HISTORY

17

0

5

10

15

20

25

30

35

He

alth

care

(+

41

%)

Co

ns D

iscr

(+1

03%

)

Te

leco

ms (

+5

7%

)

Co

ns S

tap

les (

+9

%)

IT (

+2

7%

)

EM

(+

30%

)

Ind

ustr

ials

(+

1%

)

En

erg

y (

+3

9%

)

Ma

teria

ls (

-7%

)

Utilit

ies (

-5%

)

Fin

an

cia

ls (

-8%

)

Re

al E

sta

te (

-32

%)

12M FWD PER 12M FWD PER 10yr avg

12M FWD PER vs 10 yr average (green – cheap vs 10 yr avg, red – expensive vs 10 yr avg)

EM DIVIDEND YIELDS DRIVING FLOWS IN TO EQUITIES

18

Dividend yields are higher than bond yields in 14 EM countries, vs 7 in

2015 and 3 in 2010. 17 EM countries have dividend yield > 1yr deposit

rate

0

2

4

6

8

10

12

14

16

*Pak

ista

n

*Cze

ch R

epu

blic

*Gre

ece

*Ru

ssia

So

uth

Afr

ica

*UA

E

Tu

rkey

Egy

pt

*Po

lan

d

*Qat

ar

*Mal

aysi

a

Bra

zil

Mex

ico

*Tai

wan

*Co

lom

bia

*Hu

nga

ry

*Ch

ile

*Sau

di A

rab

ia

*Th

aila

nd

Ind

on

esia

Per

u

*Ko

rea

*Ch

ina

*Ph

ilip

pin

es

Ind

ia

2021E dividend yield, % 10yr local currency bond yield (%) 1yr retail deposit rate (%)

DIVIDEND YIELDS VS BOND YIELDS

19

10 yr returns better for countries with higher relative div yld.

EM GDP REBOUNDS RANKED

20

IMF WEO October 2020: 2021 GDP growth rebound vs 2020

-2

-

2

4

6

8

10

12

14

16

18

20

22

24

Per

u (

+21

.2)

Ind

ia (

+1

9.1

)

Arg

enti

na

(+1

6.7

)

Ph

ilip

pin

es (

+15

.7)

Mal

aysi

a (+

13

.8)

Gre

ece

(+1

3.6

)

Mex

ico

(+1

2.5

)

Co

lom

bia

(+1

2.2

)

Cze

chia

(+

11

.6)

Thai

lan

d (

+11

.1)

S A

fric

a (+

11

.0)

Ch

ile (

+10

.5)

Hu

nga

ry (

+10

.0)

Turk

ey (

+1

0.0

)

Bra

zil (

+8

.6)

S A

rab

ia (

+8.5

)

Po

lan

d (

+8.2

)

UA

E (+

7.9

)

Ind

on

esia

(+7

.6)

Qat

ar (

+7.0

)

Ru

ssia

(+6

.9)

Ch

ina

(+6

.4)

Ko

rea

(+4

.7)

Taiw

an (

+3.2

)

Pak

ista

n (

+1.4

)

Egyp

t (-

0.8

)

2021 rebound (ppts) 2021 GDP growth (%)

21

-2

0

2

4

6

8

10

12

14

16

18

20

22

24

Mau

riti

us

(+2

4.1

)

Cro

atia

(+1

5.0

)

Slo

ven

ia (

+1

1.9

)

Mo

rocc

o (

+1

1.9

)

Tun

isia

(+1

1.0

)

Sri L

anka

(+9

.8)

Esto

nia

(+9

.7)

Om

an (

+9

.5)

Ro

man

ia (

+9.4

)

Ku

wai

t (+

8.7

)

Jord

an (

+8.4

)

Serb

ia (

+7.9

)

Bah

rain

(+7

.2)

Nig

eria

(+6

.0)

Sen

egal

(+5

.9)

Lith

uan

ia (

+5.9

)

Kaz

akh

stan

(+

5.7

)

Vie

tnam

(+5

.1)

Ivo

ry C

oas

t (+

4.4

)

Ken

ya (

+3

.6)

Ban

glad

esh

(+0

.6)

2021 rebound (ppts) 2021 GDP growth (%)

FM GDP REBOUNDS RANKEDIMF WEO October 2020: 2021 GDP growth rebound vs 2020

COMMODITY DEMAND

22

US$ GDP growth for key EM Asia back well above 2007-12 levels

-500

0

500

1,000

1,500

2,000

2,500

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

Bangladesh

Malaysia

Vietnam

Thailand

Korea

Indonesia

India

China

TOTAL

CONCLUSION

23

1. Dollar weakness and EM equity strength go hand-in-hand (historically on a 7-10yr

cycle). A split Senate could be good for EM as it implies more emphasis on monetary

stimulus (weak dollar, search for yield).

2. Dividend yields exceed local bond yields in over half of EM now, and term deposits in

two-thirds of EM.

3. Lacklustre flows to EM equity over the last decade suggest potential for significant

re-allocation to EM equities from international investors on the back of a normalization of

trade rhetoric and weaker dollar.

4. Weaker dollar suggests investors may move up the risk curve rotating out of Asia

towards cheaper currencies in Latin America and EMEA – financials could also perform

better

5. A stronger CNY suggests dollar GDP creation by China back to record levels,

supporting commodities

6. Frontier equities look particularly cheap once Kuwait transitions at the end of

November

DISCLAIMER

This Communication is for information purposes only. The Communication does not form a fiduciary relationship or constitute advice and is not and should not be construed

as a recommendation or an offer or a solicitation of an offer of securities or related financial instruments, or an invitation or inducement to engage in investment activity, and

cannot be relied upon as a representation that any particular transaction necessarily could have been or can be effected at the stated price. The Communication is not an

advertisement of securities nor independent investment research, and has not been prepared in accordance with legal requirements designed to promote the independence

of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. Opinions expressed therein may differ or be

contrary to opinions expressed by other business areas or groups of Renaissance Capital as a result of using different assumptions and criteria. All such information is

subject to change without notice, and neither Renaissance Capital nor any of its subsidiaries or affiliates is under any obligation to update or keep current the information

contained in the Communication or in any other medium.

Descriptions of any company or issuer or their securities or the markets or developments mentioned in the Communication are not intended to be complete. The

Communication should not be regarded by recipients as a substitute for the exercise of their own judgment as the Communication has no regard to the specific investment

objectives, financial situation or particular needs of any specific recipient. The material (whether or not it states any opinions) is for general information purposes only and

does not take into account your personal circumstances or objectives and nothing in this material is or should be considered to be financial, investment or other advice on

which reliance should be placed. Any reliance you place on such information is therefore strictly at your own risk. The application of taxation laws depends on an investor’s

individual circumstances and, accordingly, each investor should seek independent professional advice on taxation implications before making any investment decision. The

Communication has been compiled or arrived at based on information obtained from sources believed to be reliable and in good faith. Such information has not been

independently verified, is provided on an ‘as is’ basis and no representation or warranty, either expressed or implied, is provided in relation to the accuracy, completeness,

reliability, merchantability or fitness for a particular purpose of such information, except with respect to information concerning Renaissance Capital, its subsidiaries and

affiliates. All statements of opinion and all projections, forecasts, or statements relating to expectations regarding future events or the possible future performance of

investments represent Renaissance Capital’s own assessment and interpretation of information available to them currently. Any information relating to past performance of

an investment does not necessarily guarantee future performance.

The Communication is not intended for distribution to the public and may be confidential. It may not be reproduced, redistributed or published, in whole or in part, for any

purpose without the written permission of Renaissance Capital, and neither Renaissance Capital nor any of its affiliates accepts any liability whatsoever for the actions of

third parties in this respect. The information may not be used to create any financial instruments or products or any indices. Neither Renaissance Capital and its affiliates, nor

their directors, representatives, or employees accept any liability for any direct or consequential loss or damage arising out of the use of all or any part of the

Communication.

© 2020 Renaissance Securities (Cyprus) Limited. All rights reserved. Regulated by the Cyprus Securities and Exchange Commission

24