Embed Size (px)

Citation preview

From Technology to Knowledge Development in UAE

Dr. Eesa Mohammed BastakiChairman, Emirates Science Club

13 December 2012

2nd International Platform on Integrating Arab e-InfrastructureIn a Global Environment, eAGE2012

December 12-13, 2012, Zayed University, Dubai, UAE

Contents

Introduction…

What is Venture Capital?

Patents Registered in the Arab World

ICT Economy Driving Forces

ICT Incubation Center.. A VC Requirement

Research & Business Development (R&BD)

An Initiative to Create an Eco-System through Funding ICT value chain

Appendix

INTRODUCTION…

4

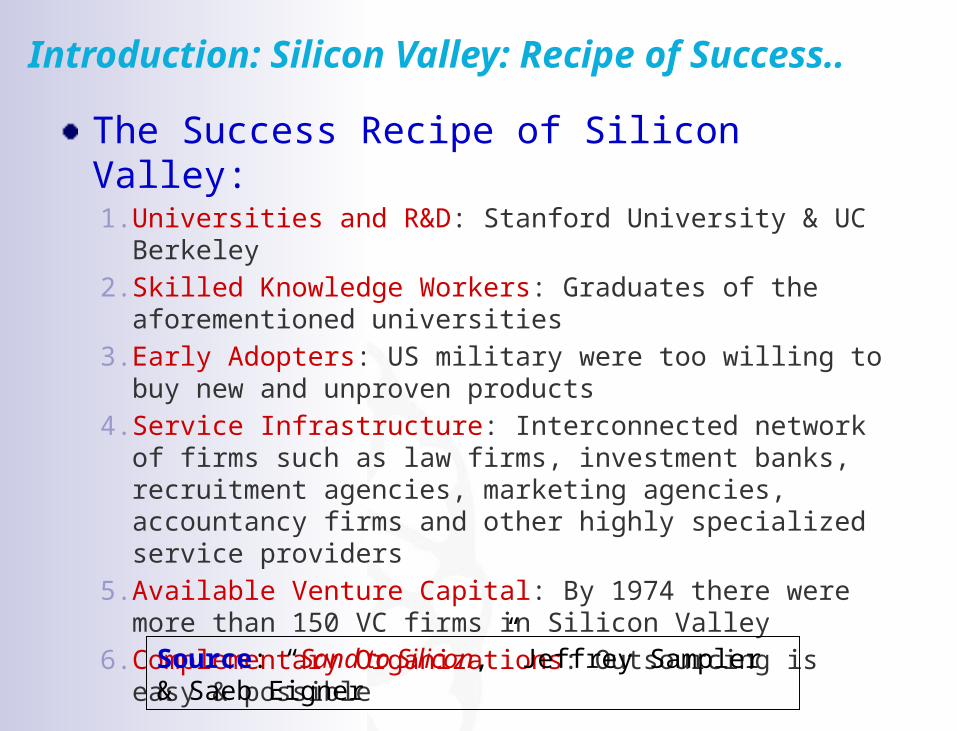

Introduction: Silicon Valley: Recipe of Success..

The Success Recipe of Silicon Valley:1. Universities and R&D: Stanford University & UC Berkeley

2. Skilled Knowledge Workers: Graduates of the aforementioned universities

3. Early Adopters: US military were too willing to buy new and unproven products

4. Service Infrastructure: Interconnected network of firms such as law firms, investment banks, recruitment agencies, marketing agencies, accountancy firms and other highly specialized service providers

5. Available Venture Capital: By 1974 there were more than 150 VC firms in Silicon Valley

6. Complementary Organizations: Outsourcing is easy & possible

Source: “Sand to Silicon,” Jeffrey Sampler & Saeb Eigner

© Copyright ICT Fund 2011

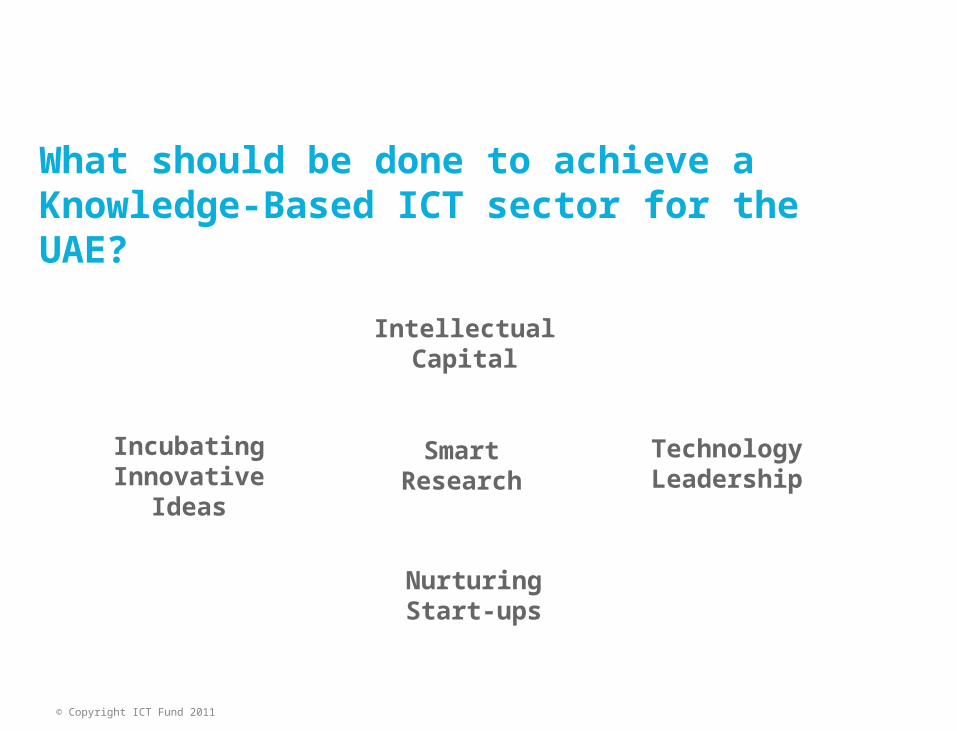

Intellectual Capital

Incubating Innovative

Ideas

Smart Research

Nurturing Start-ups

Technology Leadership

What should be done to achieve a Knowledge-Based ICT sector for the UAE?

7

Strategic Vision: After Oil

Strategic Vision

“Achieve a long-term sustainable, prosperous & productive lifestyle after oil for UAE’s next generations through ICT innovation and creativity”

PATENTS REGISTERED IN THE ARAB WORLD

9

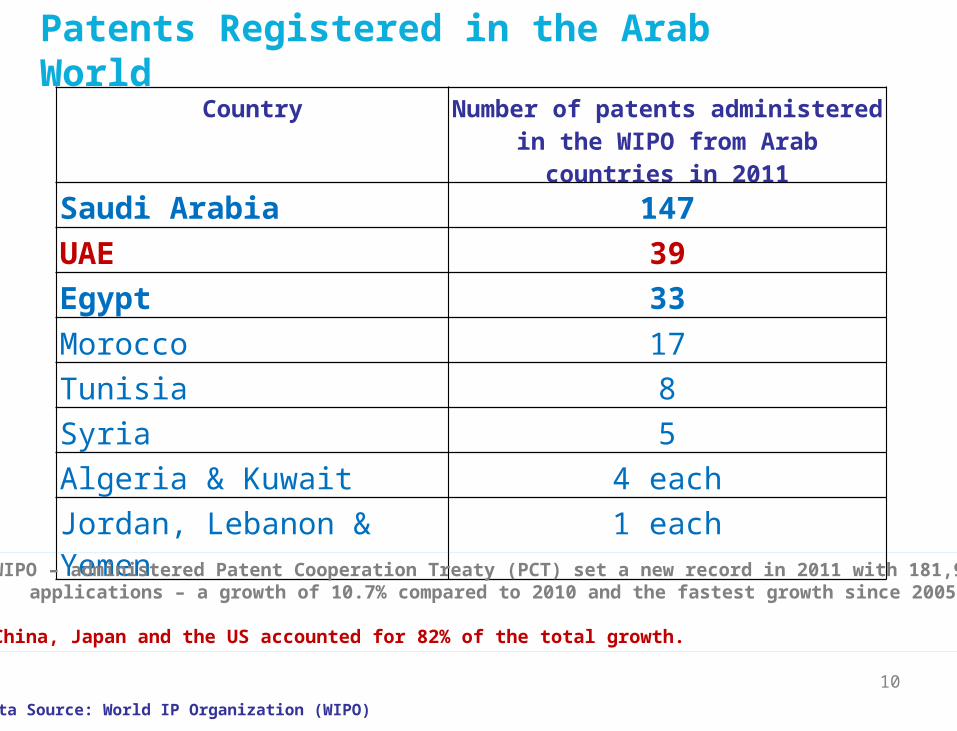

Patents Registered in the Arab World

Data Source: Arab Human Development Reports

Number of patents registered in the United States from Arab countries during the period 1980-2000

Country Number of patents registered in the United States from Arab countries during the period 1980-2000

Bahrain 6

Egypt 77

Jordan 15

Kuwait 52

Oman 5

Saudi Arabia 171

Syria 10

UAE 32

Yemen 2

10

Patents Registered in the Arab World

Data Source: World IP Organization (WIPO)

Country Number of patents administered in the WIPO from Arab countries in 2011

Saudi Arabia 147

UAE 39

Egypt 33

Morocco 17

Tunisia 8

Syria 5

Algeria & Kuwait 4 each

Jordan, Lebanon & Yemen 1 each

• WIPO – administered Patent Cooperation Treaty (PCT) set a new record in 2011 with 181,900 applications – a growth of 10.7% compared to 2010 and the fastest growth since 2005.

• China, Japan and the US accounted for 82% of the total growth.

ICT ECONOMY DRIVING FORCES

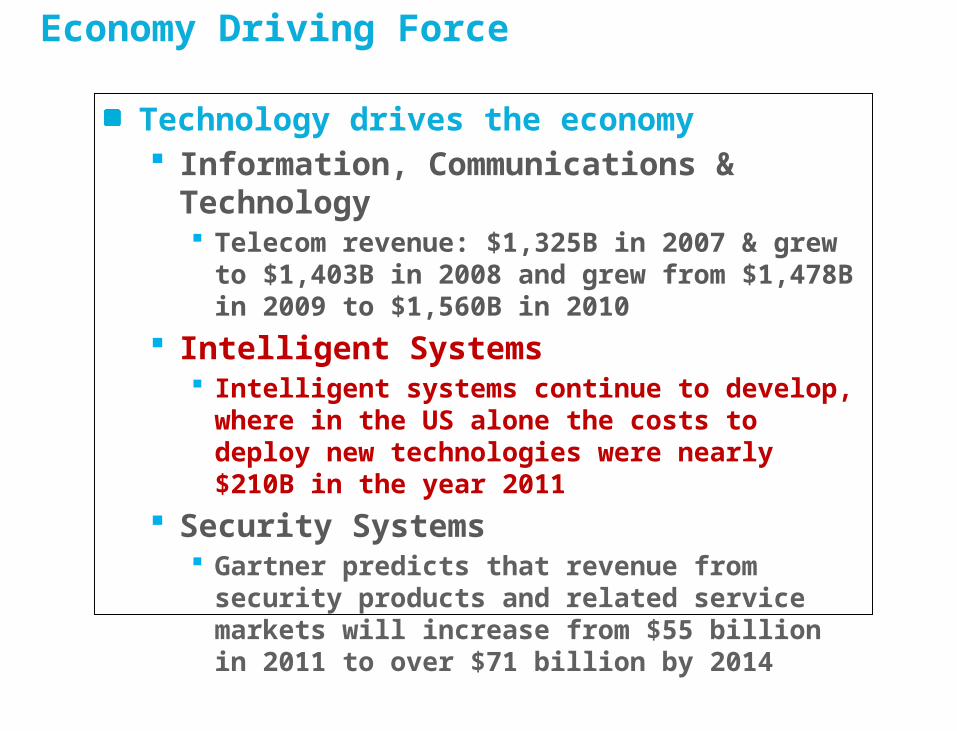

Economy Driving Force

Technology drives the economy Information, Communications & Technology

Telecom revenue: $1,325B in 2007 & grew to $1,403B in 2008 and grew from $1,478B in 2009 to $1,560B in 2010

Intelligent Systems Intelligent systems continue to develop, where in

the US alone the costs to deploy new technologies were nearly $210B in the year 2011

Security Systems Gartner predicts that revenue from security

products and related service markets will increase from $55 billion in 2011 to over $71 billion by 2014

Economy Driving Force

RegionalIDI

Rank

Europe

Global IDI Ran

k

Asia & Pacific

Global IDI Ran

k

Americas

Global IDI Ran

k

Arab State

s

Global IDI Ran

k

CIS

Global IDI Ran

k

Africa

Global IDI Ran

k

1Swede

n1

Korea (Rep)

2

United

States

17 UAE 32 Russia 50Seychelles

57

2Denma

rk3

Hong Kong, China

11Canad

a19

Bahrain

42Ukrain

e51

Mauritius

62

3Netherl

ands4 Japan 12

Argentina

47Qata

r44 Belarus 54

South Africa

87

4 Iceland 5Austra

lia14 Chile 48

Saudi

Arabia

55Moldov

a68

Cape Verde

105

5 Norway 6Singap

ore15

Uruguay

49Kuwa

it57

Kazakhstan

69 Gabon 107

ITU’s Ranks in ICT Development Index (IDI)

Top Worldwide Smartphone Operating System Markey Share

Worldwide smartphone operating system (OS) market share in 2009-2015, according to Gartner

Smartphone OS market share and compound annual growth rate 2011-2015, according to IDC

OS(listed

alphabetically)

2009market share

2010market share

2011market share

2015market Share

2011market share

2015market Share

2011-2015CAGR

Android 3.9% 22.7% 38.5% 48.8% 39.5% 45.4% 23.8%

BlackBerry 19.9% 16.0% 13.4% 11.1% 14.9% 13.7% 17.1%

iOS 14.4% 15.7% 19.4% 17.2% 15.7% 15.3% 18.8%Symbian 46.9% 37.6% 19.2% 0.1% 20.9% 0.2% -65.0%Windows

Phone/Mobile 8.7% 4.2% 5.6% 19.5% 5.5% 20.9% 67.1%

Others 6.1% 3.8% 3.9% 3.3% 3.5% 4.6% 28.0%Total

smartphones sold

172 million

297 million

468 million

631 million 450 million N/A 19.6%

Source: Gartner (April 2011)Source: IDC (March 2011)

via: mobiThinking

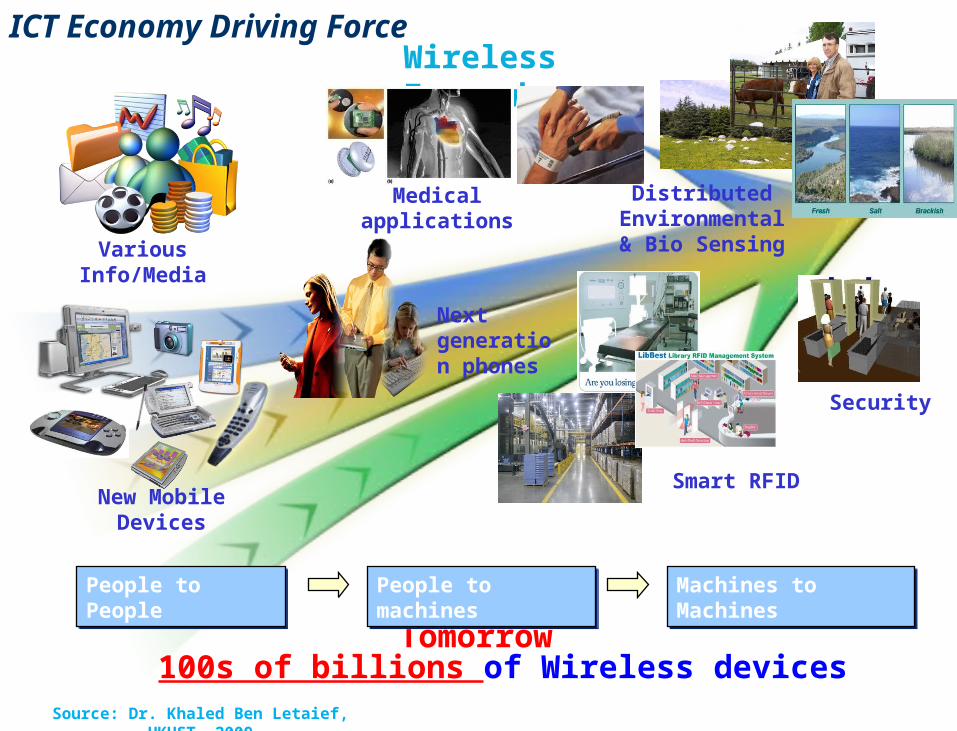

Wireless Revolution

Voice

Yesterday- 1999

Millions of wireless devices

SMS

Last Year- 2011

Billions of wireless devices

Mobile TV

Video

Internet

WiFi

ICT Economy Driving Force

Source: Dr. Khaled Ben Letaief, HKUST, 2009

Wireless Everywhere

Tomorrow100s of billions of Wireless devices

VariousInfo/Media

New MobileDevices

Distributed Environmental& Bio Sensing

Smart RFID

People to PeoplePeople to People People to machinesPeople to machines Machines to MachinesMachines to Machines

Next generation phones

Medical applications

Security

ICT Economy Driving Force

Source: Dr. Khaled Ben Letaief, HKUST, 2009

Economy Driving Force

Country KEI (Knowledge Economy Index) [2009]

Algeria 3.22

Bahrain 6.04

Djibouti 1.47

Egypt 4.08

Jordan 5.54

Kuwait 5.85

Lebanon 4.81

Mauritania 2.36

Morocco 3.54

Oman 5.36

Qatar 6.73

Saudi Arabia 5.31

Sudan 1.78

Syria 3.09

Tunisia 4.42

UAE 6.73

Yemen 2.2

Data Source: World Bank

KEI (Knowledge Economy Index) [2009]

KEI (Knowledge Economy Index): The knowledge Economy Index takes into account whether the environment is conducive for knowledge to be used effectively for economic development. The KEI is calculated based on the average of the normalized scores of a country or region on all four pillars related to knowledge economy - economic incentive and institutional regime, education, innovation and ICT. (0 is the lowest score and 10 is the maximum score).

Four pillars related to knowledge economy:1. Economic incentive and institutional regime2. Education3. Innovation4. ICT

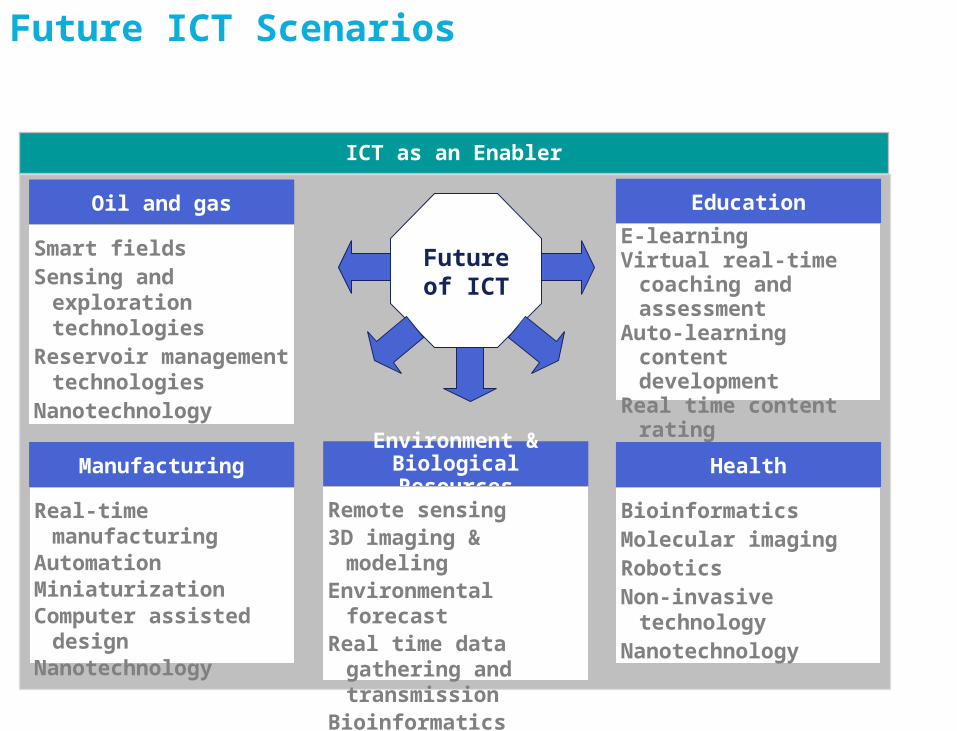

ICT as an Enabler

Future of ICT

Oil and gas

Smart fieldsSensing and exploration

technologiesReservoir management

technologiesNanotechnology

Manufacturing

Real-time manufacturingAutomation MiniaturizationComputer assisted

design Nanotechnology

Education

E-learningVirtual real-time

coaching and assessment

Auto-learning content development

Real time content rating

Environment & Biological Resources

Remote sensing3D imaging & modeling Environmental forecastReal time data gathering

and transmissionBioinformatics

Health

BioinformaticsMolecular imagingRoboticsNon-invasive technologyNanotechnology

Future ICT Scenarios

ICT INCUBATION CENTER..A VC REQUIREMENT…

© Copyright ICT Fund 2012

Why Incubation in UAE?

An ICT Incubation Center for UAE Creating an R&BD culture is one of the three

paths to: Diversifying UAE economy Creating advanced technology Enabling knowledge-based economy

Enabling knowledge transfer requires incentives due to the fact that All VCs are multinationals They are willing to relocate to areas that offer either

innovative or financial advantage Success stories open doors to Emirati VCs who are

interested in entering into the ICT area of innovation

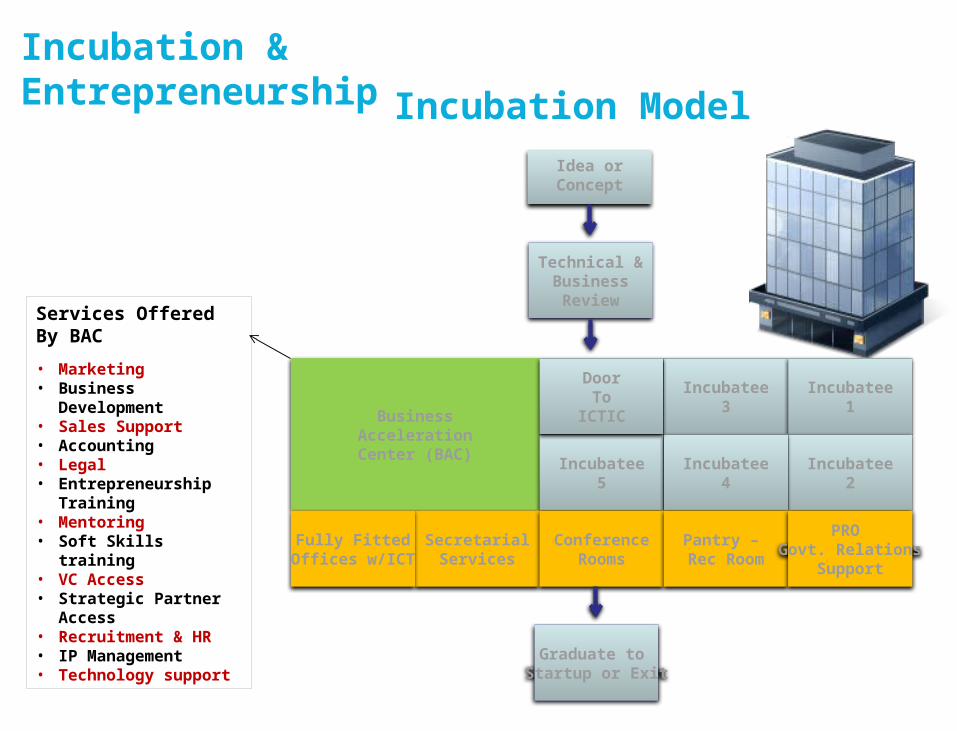

Incubation & Entrepreneurship

Idea orConcept

Technical &BusinessReview

Services Offered By BAC

• Marketing• Business Development• Sales Support• Accounting• Legal• Entrepreneurship

Training• Mentoring• Soft Skills training• VC Access• Strategic Partner

Access• Recruitment & HR• IP Management• Technology support

Incubatee3

Incubatee1

BusinessAccelerationCenter (BAC)

Incubatee2

Incubatee5

Incubatee4

SecretarialServices

ConferenceRooms

Pantry – Rec Room

PRO Govt. Relations

Support

Fully FittedOffices w/ICT

DoorTo

ICTIC

Graduate to Startup or Exit

Incubation Model

RESEARCH & BUSINESS DEVELOPMENT (R&BD)

R&BD: A Value-Added Concept

Element One Element Two Element Three

AcademiaCulture Industry

• Identify the constituents

• Plan for ac-tivities and events to adapt the R&D culture

• Find research ar-eas applicable to all the con-stituents

• Collaborate with local & interna-tional institutes for technical cre-ation

• Set mechanisms for knowledge transfer initia-tives (e.g labs, R&D, TIC, etc)

• Identify in-dustrial needs & re-quirements

• Link them with the academia

• Create the R&BD Culture: Through well prepared Strategic plans & actions

• Create the R&BD Culture: Through well prepared Strategic plans & actions

R&BD Constituents

Private

Element Four

• Government is a very es-sential con-stituent to initiate funds and create the culture

Government

Element Five• The pri-vate sector should play the role of what is known in the indus-try as: VC or CSR (Corporate Social Re-sponsibil-ity)

© Copyright ICT Fund 2007

AN INITIATIVE TO CREATE AN ECO-SYSTEM THROUGH FUNDING ICT VALUE CHAIN

ICT Fund Eco-System – Business Model

25

Scholarships

© Copyright ICT Fund 2007

www.bastaki.aewww.bastaki.comwww.bastaki.netwww.bastaki.org

IF YOUR AMBITION MATCHES OUR INTEREST…COME TALK TO ME!

© Copyright ICT Fund 2007

APPENDIX

Some ICT Incubation Statistics

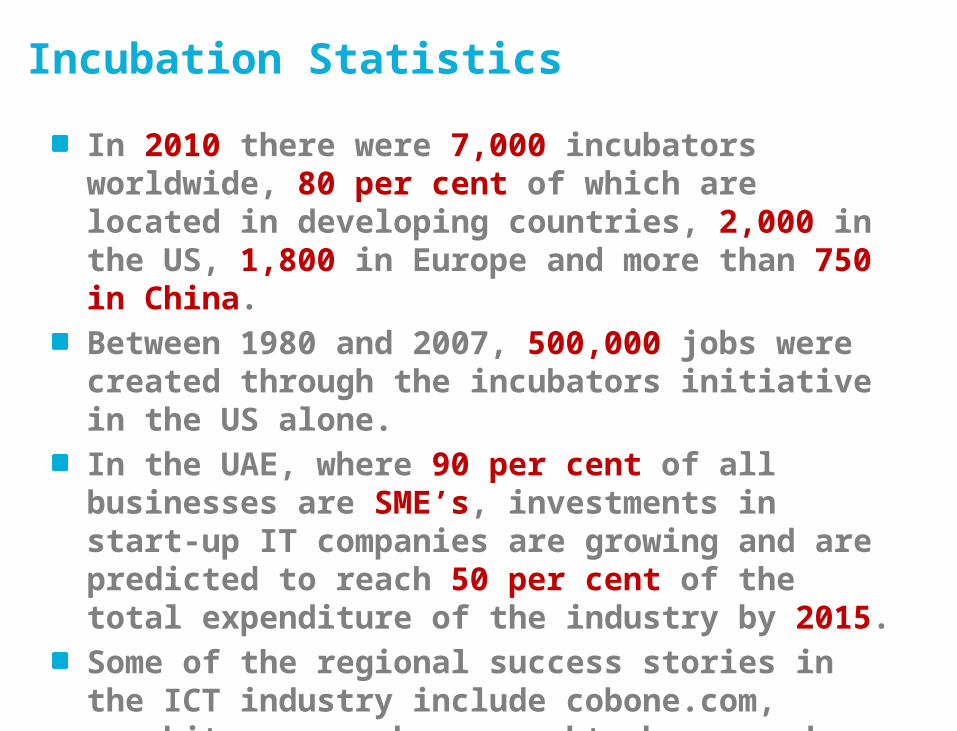

Incubation Statistics

In 2010 there were 7,000 incubators worldwide, 80 per cent of which are located in developing countries, 2,000 in the US, 1,800 in Europe and more than 750 in China.

Between 1980 and 2007, 500,000 jobs were created through the incubators initiative in the US alone.

In the UAE, where 90 per cent of all businesses are SME’s, investments in start-up IT companies are growing and are predicted to reach 50 per cent of the total expenditure of the industry by 2015.

Some of the regional success stories in the ICT industry include cobone.com, gonabit.com, souk.com. maktoob.com and bayt.com.

Green ICT…Smarter technology use could reduce global emissions by 15 per cent and save global industry US$800 billion in annual energy costs by 2020

ICT sector’s carbon footprint is about 2% of global emissions and will grow about 6%per year (CAGR)

PC ownership will quadruple between 2007 and 2020 to four billion devices; emissions will double over the same period, with laptops overtaking desktops as the main source of global ICT emissions (22 per cent)

Carbon footprint of Internet is around 300m tons of CO2 per year

Sources: Climate Group, Global e-Sustainability Initiative (GeSI) & Gartner

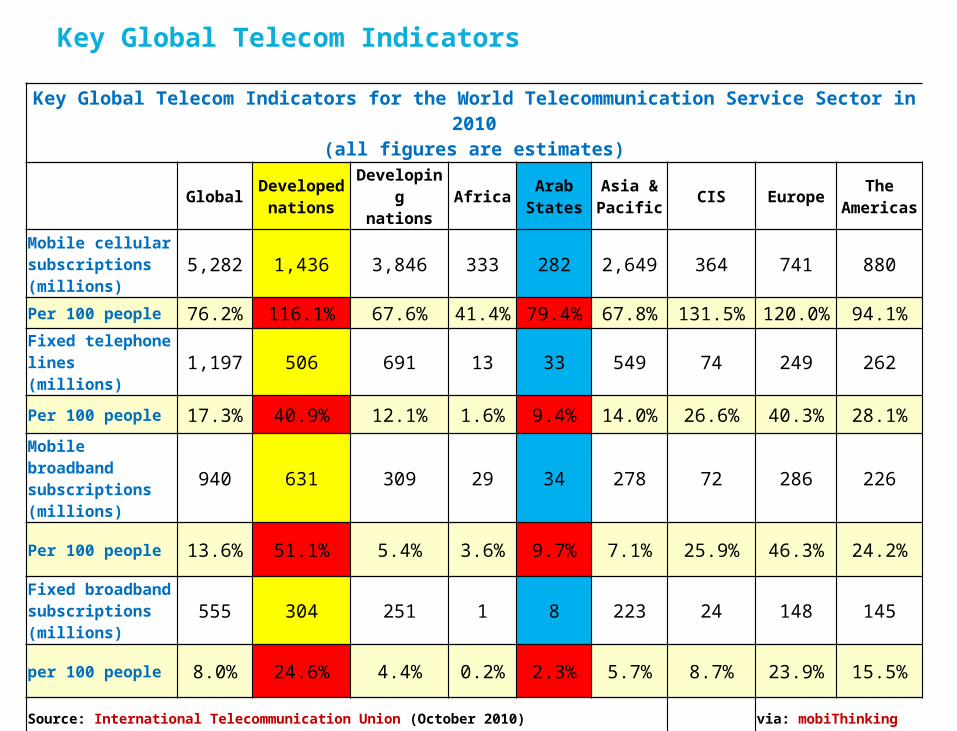

Key Global Telecom Indicators

Key Global Telecom Indicators for the World Telecommunication Service Sector in 2010

(all figures are estimates)

GlobalDevelope

dnations

Developing

nationsAfrica

ArabStates

Asia & Pacific

CIS EuropeThe

Americas

Mobile cellular subscriptions(millions)

5,282 1,436 3,846 333 282 2,649 364 741 880

Per 100 people 76.2% 116.1% 67.6% 41.4% 79.4% 67.8% 131.5% 120.0% 94.1%Fixed telephone lines(millions)

1,197 506 691 13 33 549 74 249 262

Per 100 people 17.3% 40.9% 12.1% 1.6% 9.4% 14.0% 26.6% 40.3% 28.1%

Mobile broadband subscriptions(millions)

940 631 309 29 34 278 72 286 226

Per 100 people 13.6% 51.1% 5.4% 3.6% 9.7% 7.1% 25.9% 46.3% 24.2%

Fixed broadband subscriptions(millions)

555 304 251 1 8 223 24 148 145

per 100 people 8.0% 24.6% 4.4% 0.2% 2.3% 5.7% 8.7% 23.9% 15.5%

Source: International Telecommunication Union (October 2010) via: mobiThinking