Embed Size (px)

Citation preview

From PLI’s Online Program GAAP "Codification": What Attorneys Need to Know about the New Accounting Rule System #24855

GAAP “Codification”: What Attorneys Need to know about the New Accountingabout the New Accounting

Rule Systemy

Joseph J. Floyd of Floyd Advisory LLC Steven R. Paradise of Vinson & Elkins LLP

Charles R. Hacker, Jr. of PricewaterhouseCoopers , p

Agenda

• Accounting Rule Making and the Motivation for the

CodificationCodification

• Overview of the Codification

• Impact on Financial Reporting

• Researching an Accounting Topic

• Impact on Accounting and Auditing Litigation

Alignment ith IFRS• Alignment with IFRS

• Q and A – Panel discussion and Participants

Pre‐Codification Assemblage of Rules and Guidance The “Alphabet Soup” of AccountingThe Alphabet Soup of Accounting

1936 1959 CAP issued 51 ARBs1936‐1959 CAP issued 51 ARBsPlus

1959‐1973 APB issued 31 OpinionspPlus

1973‐Present FASB issued 168 Statements1984 EITF i f d1984 EITF is formed

PlusAICPA GuidanceAICPA Guidance

EqualsJuly 1, 2009 FASB’s GAAP Codificationy

Source of slide content www.aicpa.org

The “OLD” GAAP HIERARCHYA. FASB Statements of Financial Accounting Standards and

Interpretations, FASB Statement 133 Implementation Issues, FASB Staff Positions, and AICPA Accounting Research Bulletins and APB Opinions that are not superseded by actions of the FASBthat are not superseded by actions of the FASB

B. FASB Technical Bulletins, if cleared by FASB, AICPA Industry Audit and Accounting Guides and Statements of PositionAccounting Guides and Statements of Position

C. AICPA Accounting Standards Executive Committee Practice Bulletins that FASB cleared consensus positions of the FASB Emerging Issuesthat FASB cleared, consensus positions of the FASB Emerging Issues Task Force and the Topics discussed in Appendix D of EITF Abstracts

D. Implementation guides (Q&As) published by the FASB staff, AICPAD. Implementation guides (Q&As) published by the FASB staff, AICPA Accounting Interpretations, AICPA Industry Audit and Accounting Guides and Statements of Position not cleared by the FASB, and practices widely recognized and prevalent either generally or in the i d tindustry

Source of content www.fasb.org

Motivation for the CodificationMotivation for the Codification

• All authoritative literature in one spot

• Simplify user access to all authoritative GAAP

• Reduce the amount of time and effort required to solve an• Reduce the amount of time and effort required to solve an accounting research issue

• Mitigate the risk of noncompliance with standards through i d bili f h li

g p gimproved usability of the literature

• Provide readily available information with real‐time updates as new standards are releasednew standards are released

• Context inclusion for a more complete understanding of the literature

The Process

Fi d FASB i 2001 b b f FASAC • First suggested to FASB in 2001 by members of FASAC • In 2004 FASB surveyed 1400 users of GAAP, over 95% supported pursuing the Codification

• FAF approves funding for the FASB’s Codification and retrieval project

• Top financial reporting professionals were recruited for two • Top financial reporting professionals were recruited for two to six month assignments

• Project was estimated to take three to five years to complete• Thousands of pronouncements organized into 90 topics• On June 30, 2009 FASB issued “The FASB Accounting Standards Codification”Standards Codification

• The Codification is effective for financial statements issued for interim and annual periods ending after September 15, 20092009

Source used for content www.fasb.org

Overview of the Codification

♦Areas: Grouping of approximately 90 topics

♦Topics: Broadest categorization of related content

♦Subtopics: Generally distinguished by type or scope

♦Sections: Correlate with IFRS/IAS sections

♦Subsections: All f th ti d i ti f t t♦Subsections: Allow further segregation and navigation of content

Source of slide content www.aicpa.org

Updates to the Codification

• Existing guidance will be updated and new guidance will be incorporated into the Codification in real time, providing users with access to most recent FASB deliberations

• As the FASB amends existing Codification paragraphs, both the current paragraph and the new paragraph, “Pending Text”, will reside in the Codification es de t e Cod cat o

• Once the new guidance is effective, the outdated guidance will be removed

• All guidance in the Codification will be updated through "Codification Update Instructions" ("CUIs") and the FASB will no l i ff i i ( )longer issue FASB Statements, FASB Staff Positions (FSPs), FASB Interpretations (FINs), or Emerging Issues Task Force (EITF) Abstracts

Source of slide content www.pwc.com

Impact On Financial Reporting

• Financial statements issued for interim or annual periods ending after September 15, 2009, will make all references to the Codification or simply explain the accounting concepts

• FASB has publicly encouraged the use of plain English in financial statement disclosures

• The SEC encourages companies to draft financial statement disclosures to avoid specific GAAP references and to more clearly explain accounting conceptsexplain accounting concepts

• “Old” GAAP references should not be used

• SEC has stated they will not require a preferability letter if an accounting change is in response to a newly issued update of FASB ASC.

Source of content www.aicpa.org and www.fasb.org

Researching an Accounting TopicWhat Tools Are Available?

FASB website (www.asc.fasb.org)• Basic view

What Tools Are Available?

• Basic view

– No charge

– Limited functionality, only content

• Professional view

– Requires a paid subscription

– Provides full functionality (including joining sections and viewing– Provides full functionality (including joining sections and viewing original source documents via the print screen feature)

Comperio – PwC’s tool (www.pwccomperio.com)U d t d t i l d C difi ti• Updated to include Codification

• Includes much of the same functionality as professional view on FASB’s website

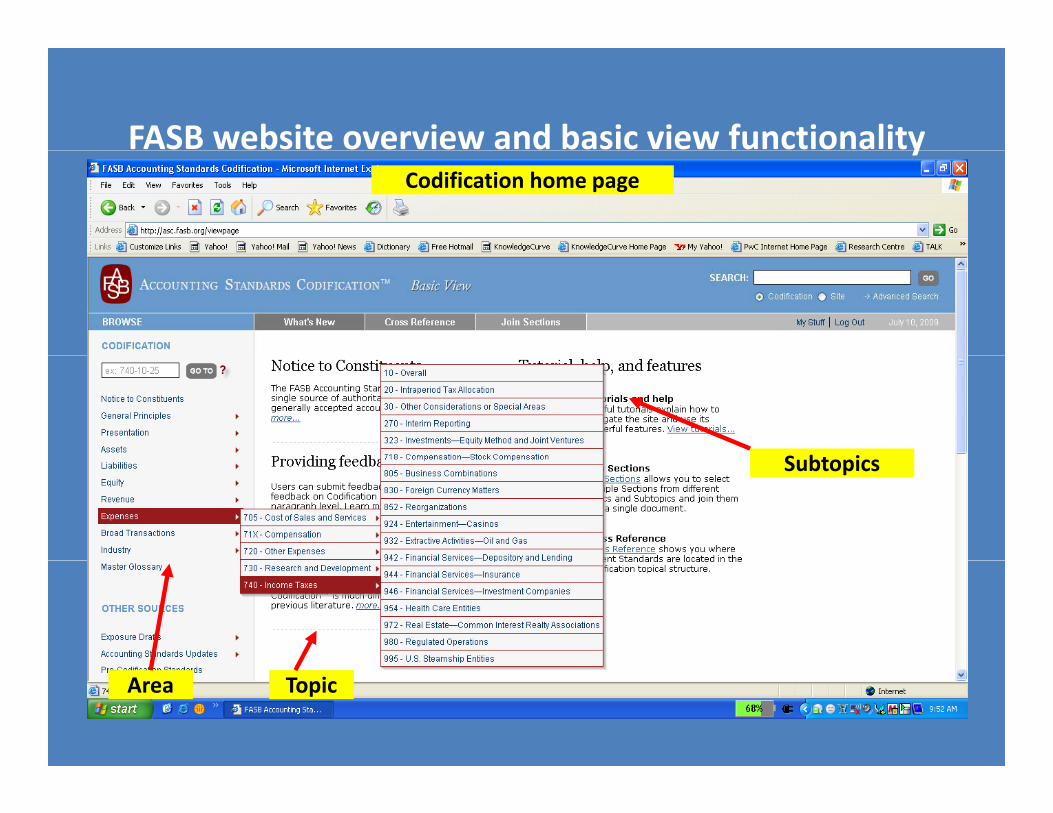

FASB website overview and basic view functionalityyCodification home page

S bt iSubtopics

Area Topic

FASB website overview and basic view functionalityy

Sections within

ASC 740‐10

FASB website overview and basic view functionalityy

Paragraphs 6 th h 9 ithithrough 9 within

ASC 740‐10‐30

FASB website overview and basic view functionalityy

Cross Reference feature

FASB website overview and basic view functionality

Cross Reference featuregenerated report

y

Prior standard New ASCPrior standard reference (e.g., FIN 48, par. 8)

New ASC reference: 740‐10‐30‐7

FASB website overview and basic view functionalityy

Industry‐specific guidanceguidance

FASB website overview and basic view functionalityy

Master Glossary

FASB website overview and basic view functionalityy

New content

FASB website overview and basic view functionalityR f K i i htRecap of Key insights

• Cross Reference featureCross Reference feature

– Allows users to cross reference historical references and new ASC references

• Master Glossary

– Provides a listing of all defined terms in the Codification

F t C difi ti d t• Future Codification updates

– Will contain a new standard along with instructions for how the standard will be incorporated into the Codification

Note – Users can still attain access to pre‐Codification standards

on the FASB’s website.

FASB Website Overview and Other Functionalityy

Defined term

Slide 24

FASB Website Overview and Other Functionalityy

SEC Material

Slide 25

FASB Website Overview and Other Functionalityy

To view source document

Slide 28

FASB Website Overview and Other Functionalityy

Source document

Slide 29

FASB Website Overview and Other Functionality

Impact on Accounting and AuditingImpact on Accounting and Auditing Litigation

• Benefits realized through Codification:• Benefits realized through Codification:

‐“One‐Stop Shopping”p pp g

‐Increased access for attorneys and other non‐accounting professionalsaccounting professionals

‐Minimize Risk

‐Assure complete and thorough research

‐Minimize potential for surprise

• Potential uncertainty:

– Unintentional changes to GAAPSubstantive GAAP not intended to change‐Substantive GAAP not intended to change

‐Changes to structure and presentation may cause rules to be applied differently

‐Codification may use different phraseology

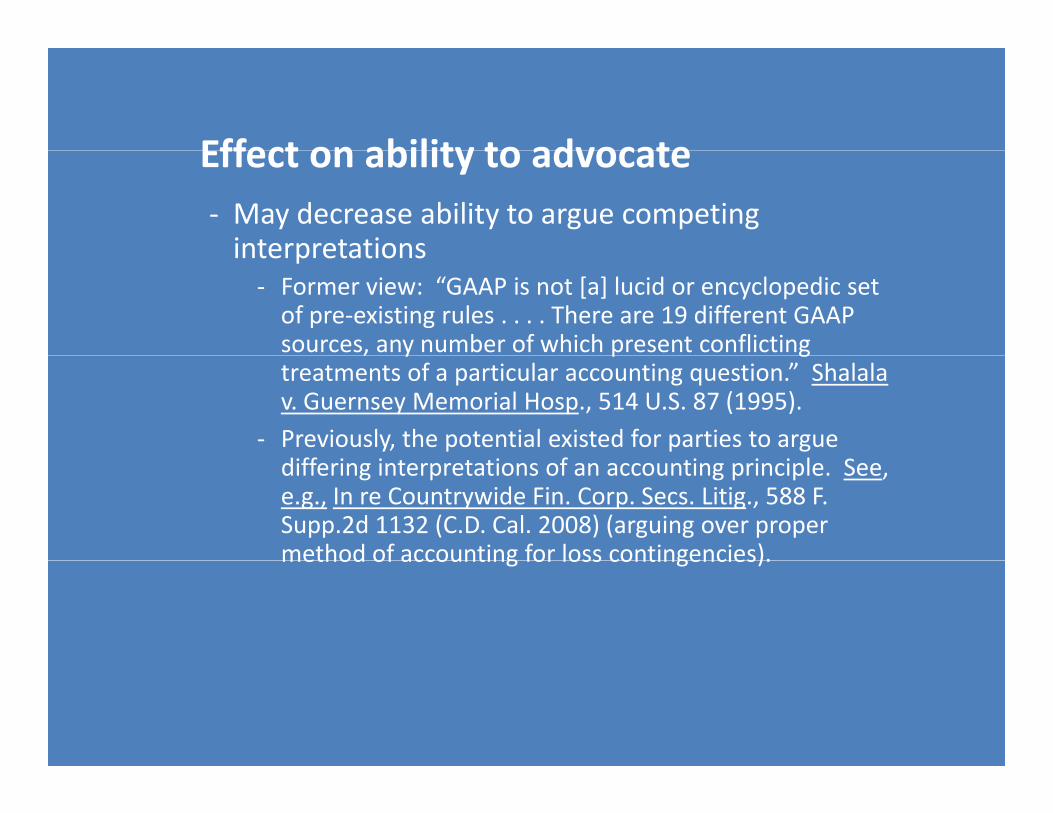

Effect on ability to advocateEffect on ability to advocate‐ May decrease ability to argue competing interpretationsinterpretations‐ Former view: “GAAP is not [a] lucid or encyclopedic set of pre‐existing rules . . . . There are 19 different GAAP sources, any number of which present conflicting , y p gtreatments of a particular accounting question.” Shalala v. Guernsey Memorial Hosp., 514 U.S. 87 (1995).

‐ Previously, the potential existed for parties to argue d ff f ldiffering interpretations of an accounting principle. See, e.g., In re Countrywide Fin. Corp. Secs. Litig., 588 F. Supp.2d 1132 (C.D. Cal. 2008) (arguing over proper method of accounting for loss contingencies).method of accounting for loss contingencies).

Experts

• Codification applies prospectively

• When did the dispute arise? Is there a governing agreement?g

Advising Clients

‐Ensure Compliance ‐Obscure or ambiguous provisions may have been changed by the Codification

‐New/Existing Agreements‐Include explicit references to Codification?

‐Financial Statements‐Cite in “plain English” or to Codification

‐SEC‐Releases clarify that all references in SEC rules/guidance refer to GAAP principals as set forth in the Codification

Q and Al dPanel Discussion and Participants